Embed Size (px)

Citation preview

A PROJECT REPORT ON

IMPACT OF FII ON STOCK MARKET

A PROJECT REPORT

Submitted by

ASHOK AMIPARA (09003)

VIMAL BODA (09018)

BATCH – 2009-2011

To

Director (PGDM)

In partial fulfillment of the requirements of

Tolani Institute of Management Studies, Adipur

For the award of the degree of

Post Graduate Diploma in Management

Tolani Institute of Management StudiesAdipur – 370 205

FEBRUARY 2011

Tolani Institute of Management Studies Page 1

DECLARATION

We hereby declare that the project work entitled “IMPACT OF FII ON STOCK

MARKET” Submitted to Tolani Institute of Management Studies, Adipur is a record of an

original work done by me under the guidance of Prof. Hitendra Lachhwani and this project work

is not submitted for the award of any other degree/diploma/associate ship/fellowship or seminar

award.

Ashok Amipara

Vimal boda

14-02-2011

ADIPUR

Tolani Institute of Management Studies Page 2

Executive Summery

Title : “IMPACT OF FII ON STOCK MARKET”

Objectives :

Primary Objective:

To study the impact of FII on Indian stock market.

To understand the concept of BSE sensitive index.

Secondary Objective:

To understand the concept of FIIs.

To understand the relationship between the Sensex and FII.

To know the sector which get affected more by activities of FIIs.

Research Methodology:

• Research problem

• Research design

• Sampling design

• Data collection method

ResearchProblem:

The project deals with the “Impact of Foreign Institutional Investors on Indian Stock Market”.

This research project studies the relationship between FIIs investment and stock indices. For this

purpose India’s two major indices i.e. Sensex and S&P CNX Nifty are selected. These two

indices, in a way, represent the picture of India’s stock markets. Five indices of BSE i.e. BSE

Auto, BSE Bankex, BSE IT, BSE FMCG, BSE Oil and Gas are also selected so as to further

observe the effect of FII in particular industry . So this project reveals the impact of FII on the

Indian capital market.

Tolani Institute of Management Studies Page 3

There may be many other factors on which a stock index may depend i.e. Government policies,

budgets, bullion market, inflation, economic and political condition of the country, FDI,

Re./Dollar exchange rate etc. But for this study I have selected only one independent variable i.e.

FII. This study uses the concept of correlation, regression and hypothesis to study the

relationship between FII and stock index. The FII started investing in Indian capital market from

September 1992when the Indian economy was opened up in the same year. Their investments

include equity only. The sample data of FIIs investments consists of daily basis from January

2001 to February 2011.

RESEARCHDESIGN:

Null Hypothesis (Ho): The various BSE indices and S&P CNX Nifty index does not rise with the

increase in FIIs investment.

Alternate Hypothesis (Ha): The various BSE indices and S&P CNX Nifty index rises with the

increase in FIIs investment.

Tolani Institute of Management Studies Page 4

Exploratory Research:

As an exploratory study is conducted with an objective to gain familiarity with the phenomenon or to achieve new insight into it, this study aims to find the new insights in terms of finding the relationship between FII’S and Indian Stock Indices.

SAMPLING DESIGN:

• Universe

In this study the universe is finite and will take into the consideration related news and events

that have happened in last few year.

• Sampling Unit:

As this study revolves around the foreign institutional investment and Indian stock market. So

for the sampling unit is confined to only the Indian stock market.

Data collection Method:

Secondary data: For the secondary data various literatures, books, journals, magazines, web links

are used. As there are not possibilities of collecting data personally so no questionnaire is made.

Tolani Institute of Management Studies Page 5

RESEARCH ANALYSIS TOOLS:

Regression analysis and Correlation analysis:

Regression Analysis: We can analyze how a single dependent variable is affected by the values

of one or more independent variables — for example, how an athlete's performance is affected

by such factors as age, height, and weight.

Correlation:

This analysis tool and its formulas measure the relationship between two data sets

that are scaled to be independent of the unit of measurement. We can use the Correlation tool to

determine whether two ranges of data move together — that is, whether large values of one set

are associated with large values of the other (positive correlation), whether small values of one

set are associated with large values of the other (negative correlation), or whether values in both

sets are unrelated (correlation near zero).

Finding & Analysis:

According to findings and results, we can conclude that FII have positive correlation

with NIFTY & SENSEX as well as other sectorial indices but did not have any

significant impact on the Indian capital market.

Recommendations:

After the analysis of the project study, following recommendations can be made:

1) Simplifying procedures and relaxing entry barriers for business activities and providing investor friendly laws and tax system for foreign investors. 2) Allowing foreign investment in more areas. In different industries indices the FIIs should be encouraged through different patterns.3) Somewhere, a restriction related to the track record of Sub- Accounts is also to be made on the investors who withdraw money out of the Indian stock market who have invested with the help of participatory notes.

Tolani Institute of Management Studies Page 6

4) We have to modernize and also have to save our culture. Similarly the laws should be such that it protect domestic investors and also promote trade in country through FIIs.

5) Encourage industries to grow to make FIIs an attractive junction to invest.

Tolani Institute of Management Studies Page 7

Tolani Institute of Management Studies Page 8

Tolani Institute of Management Studies Page 9

Tolani Institute of Management Studies Page 10

Tolani Institute of Management Studies Page 11

Tolani Institute of Management Studies Page 12

1. INTRODUCTION:

Financial markets are the catalysts and engines of growth for any nation. India’s financial market

began its transformation path in the early 1990s. The banking sector witnessed sweeping

changes, including the elimination of interest rate controls, reductions in reserve and liquidity

requirements and an overhaul in priority sector lending. Persistent efforts by the Reserve Bank of

India (RBI) to put in place effective supervision and prudential norms since then have lifted the

country closer to global standards. Around the same time, India’s capital markets also began to

stage extensive changes. The Securities and Exchange Board of India (SEBI) was established in

1992 with a mandate to protect investors and usher improvements into the microstructure of

capital markets, while the repeal of the Controller of Capital Issues (CCI) in the same year

removed the administrative controls over the pricing of new equity issues. India’s financial

markets also began to embrace technology. Competition in the markets increased with the

establishment of the National Stock Exchange (NSE) in 1994, leading to a significant rise in the

volume of transactions and to the emergence of new important instruments in financial

intermediation.

Indian investors have been able to invest through mutual funds since 1964, when UTI was

established. Indian mutual funds have been organized through the Indian Trust Acts, under

which they have enjoyed certain tax benefits. Between 1987 and 1992, public sector banks and

insurance companies set up mutual funds. Since 1993, private sector mutual funds have been

allowed, which brought competition to the mutual fund industry. This has resulted in the

introduction of new products and improvement of services. The notification of the SEBI (Mutual

Fund) Regulations of 1993 brought about a restructuring of the mutual fund industry. An arm’s

length relationship is required between the fund sponsor, trustees, custodian, and asset

Management Company. This is in contrast to the previous practice where all three functions,

namely trusteeship, custodianship, and asset management, were often performed by one body,

Usually the fund sponsor or its subsidiary. The regulations prescribed disclosure and

advertisement norms for mutual funds, and, for the first time, permitted the entry of private

sector mutual funds. FIIs registered with SEBI may invest in domestic mutual funds, whether

listed or unlisted. The 1993 Regulations have been revised on the basis of the recommendations

Tolani Institute of Management Studies Page 13

of the Mutual Funds 2000 Report prepared by SEBI. The revised regulations strongly emphasize

the governance of mutual funds and increase the responsibility of the trustees in overseeing the

functions of the asset management company. Mutual funds are now required to obtain the

consent of investors for any change in the “fundamental attributes” of a scheme, on the basis of

which unit holders have invested. The revised regulations require disclosures in terms of

portfolio composition, transactions by schemes of mutual funds with sponsors or affiliates of

sponsors, with the asset Management Company and trustees, and also with respect to personal

transactions of key personnel of asset management companies and of trustees.

India opened its stock markets to foreign investors in September 1992 and has, since 1993,

received considerable amount of portfolio investment from foreigners in the form of Foreign

Institutional Investor’s (FII) investment in equities. This has become one of the main channels of

portfolio investment in India for foreigners. In order to trade in Indian equity markets, foreign

corporations need to register with the SEBI as Foreign Institutional Investor (FII). SEBI’s

definition of FIIs presently includes foreign pension funds, mutual funds,

charitable/endowment/university fund’s etc. as well as asset management companies and other

money managers operating on their behalf

The sources of these FII flows are varied .The FIIs registered with SEBI come from as many as

28 countries(including money management companies operating in India on behalf of foreign

investors).US based institutions accounted for slightly over 41% those from the U.K constitute

about 20% with other Western European countries hosting another 17% of the FIIs. Portfolio

investment flows from industrial countries have become increasingly important for developing

countries in recent years. The Indian situation has been no different. A significant part of these

portfolio flows to India comes in the form of FII’s investments, mostly in equities. Ever since the

opening of the Indian equity markets to foreigners, FII investments have steadily grow from

about Rs.2600 crores in 1993 to over Rs.272165 crores till the end of Feb 2008. While it is

generally held that portfolio flows benefit the economies of recipient countries, policy makers

worldwide have been more than a little uneasy about such investments. Portfolio flows often

referred as “hot money”-are notoriously volatile compared to other types of capital inflows.

Investors are known to pull back portfolio investments at the slightest hint of trouble in the host

Tolani Institute of Management Studies Page 14

country often leading to disastrous consequences to its economy. They have been blamed for

exacerbating small economic problems in a country by making large and concerted withdrawals

at the first sign of economic weakness. They have also been responsible for spreading financial

crisis –causing contagion in international financial markets.

International capital flows and capital controls have emerged as an important policy issues in the

Indian context as well. The danger of “abrupt and sudden outflows” inherent with FII flows and

their destabilizing effect on equity and foreign exchange markets have been stressed. The

financial market in India have expanded and deepened rapidly over the last ten years. The Indian

capital markets have witnessed a dramatic increase in institutional activity and more specifically

that of FII’s. This change in market environment has made the market more innovative and

competitive enabling the issuers of securities and intermediaries to grow. In India the

institutionalization of the capital markets has increased with FII’s becoming the dominant owner

of the free float of most blue chip Indian stocks. Institutions often trade large blocks of shares

and institutional order’s can have a major impact on market volatility. In smaller markets,

institutional trades can potentially destabilize the markets. Moreover, institutions also have to

design and time their trading strategies carefully so that their trades have maximum possible

returns and minimum possible impact costs.

Tolani Institute of Management Studies Page 15

LITERATURE REVIEW:

Purendra Verma (2002) has investigated the impact of FII on Capital Market to find the relation

between FII and Stock indices. For this he has taken seven indices into consideration, out of

them five are Consumer Durables, Capital Goods, Fast Moving Consumer Goods, Health Care,

Information Technology and the other two are Sensex and Nifty. He observed these indices

during January 1993 to September 2001. If BSE & Nifty increase with rise in FII investment, He

has taken hypothesis for this study. To find out the results he used least square method. Finally,

after completing his study he concluded that except IT sector on all other indices the impact is

very low during January 1993 to September 2001 as the correlation is negative in Consumer

Durables, Capital Goods, Fast Moving Consumer Goods, Health Care, Sensex and Nifty.

Paramita Mukherjee, Suchismita Bose and Dipankar Coondoo (2002) carried out research on the

topic Foreign Institutional Investment in The Indian Equity Market an Analysis of daily flows

during Jan 1999 - May 2002. The paper was conducted to understand the relationship of foreign

institutional investment (FII) flows to the Indian equity market. FII flows to and from the Indian

market tend to be caused by return in the domestic equity market and not the other way round.

Returns in the equity market are very important to influence the flows of FIIs in the country.

They concluded that in India the prime focus should be on regaining investor’s confidence in the

equity market so as to strengthen the domestic investor’s base of the market.

S.S.S. Kumar (2005) of IIM-Kozhikode carried out research on the Role of Institutional

Investors in Indian Stock Market during 1992 - 2005. The paper was conducted to examining

whether the institutional investors, with their war chests of money, set the direction to the

market. He concluded with the use of Regression analysis that the combined force of the FIIs and

MF are a powerful force and in fact their direction can forecast market direction. It gives it

constantly rise in Indian context since all their trades are delivery based and Market become

more efficient with the growing presence of institutional investors who primarily go by

fundamentals.

Tolani Institute of Management Studies Page 16

Anand Bansal and J.S. Pasricha (2009) in the paper titled Foreign Institutional Investor’s Impact

on Stock Prices in India for the purpose of analyzing Impact of FIIs entry and the stock market

behavior. Average return before and after the event day has been calculated for different sub

sample days, the change of volatility in the Indian stock prices has been examined by comparing

the variance of the returns of sub sample days before and after the event day. They concluded

that return declined reasonably after the entry of FIIs, the correlation between FIIs investments

and market volatility and market return has been comparatively low. It means volatility in Indian

market is not the function of FIIs investment flows.

TIMS Batch 2008-10, Leena Kanjani, Sulabh Mehta, Anita Pariyani, Amin Pattani, Mehul

Rakholiya & Krishna Vyas conducted a research study on FII in India, they analyzed the

monthly movement of stock market from 2006 to 2009. The paper was conducted to understand

influence of FII on movement of Indian Stock market and to understand the FII policy in India.

They used Correlation and Hypothesis test methodology and concluded that FII did have

significant impact on Sensex but there is less co-relation with Benkex and IT.

Sandhya Ananthanarayanan from CRISIL, Chandrasekhar Krishnamurti from Department of

Finance and Nilanjan Sen from Nanyang Technological University conducted this research of

Foreign Institutional Investors and Security Returns: Evidence from Indian Stock Exchanges for

understanding the impact of trading of Foreign Institutional Investors on the major stock indices

of India. Their contribution to this growing literature pertaining to globalization is twofold. First,

they separate the flows into expected and unexpected and found that unexpected flows have a

greater impact than expected flows. Second, they identify the specific flows of foreign

institutional investors flowing into (or out of) each exchange and examine the impact on the

specific stock market indices. Their principal conclusions are as follows. They found strong

evidence consistent with the base-broadening hypothesis consistent with prior work. They do not

found compelling confirmation regarding momentum or contrarian strategies being employed by

foreign institutional investors. Their findings supported the price pressure hypothesis. They do

not found any substantiation to the claim that foreigners’ destabilize the market.

Tolani Institute of Management Studies Page 17

FII AND GOVERNMENT POLICIES:

Investment by FII was jointly regulated by Securities and Exchange Board of India (SEBI)

through the SEBI (Foreign Institutional Investors) Regulations, 1995 and by the Reserve Bank of

India through Regulation 5(2) of the Foreign Exchange Management Act (FEMA), 1999. The

promulgation of legislation pertaining to foreign investment by SEBI in 1995 market a watershed

for FII flows to India; this led to a significant increase in the level of FII equity inflows in the

pre-Asian crisis period. The SEBI FII Regulations and RBI policies are amended and modified

from time to time in response to the gradual maturing of the Indian financial market and changes

taking place in the global economic scenario.

In order to trade in India equity market, foreign corporation need to register with SEBI as

Foreign Institutional Investors. Without registration they can invest, but cases require the

approval from RBI. They are generally concentrated in secondary market. FII are allowed to

invest in

a) Securities in primary and secondary market including shares, debentures and warrant of

companies, unlisted, listed or to be the listed in India.

b) Units of mutual funds

c) Dated government securities

d) Derivative traded in a recognized stock market and

e) Commercial papers

FII can invest their own funds as well as invest on behalf of their overseas clients registered as

such with SEBI. These client accounts that the FII manages are known as ’sub accounts’. FII sub

accounts include those foreign corporate, foreign individual, institution funds or portfolio

established or incorporated outside India.

Tolani Institute of Management Studies Page 18

FII may issue deal in or hold off share derivative instrument such as participatory notes (PN).

The entities that can subscribe to the PN are

a) Any entity incorporated in a jurisdiction that requires filing of constitutional or other

documents with a registrar of companies or comparable regulatory agency or body under the

applicable companies legislation in that jurisdiction

b) Any entity that is regulated authorized or supervised by a central bank, such as the Bank of

England, or any other similar body provided that the entity must not only be authorized but also

be regulated by the aforesaid regulatory bodies

c) Any entity that is regulated, authorized or supervised by a securities or futures commission,

such as the Financial Services Authority or other securities or futures authority or commission in

any country, state or territory

d) Any entity that is a member of securities or futures exchanges such as the New York Stock

Exchange or other self-regulatory securities or futures authority or commission within any

country, state or territory provided that the aforesaid mentioned organizations which are in the

nature of self- regulatory organizations are ultimately accountable to the respective securities

financial market regulators.

Tolani Institute of Management Studies Page 19

Investment limit for FIIs:

As per the September 1992 policy permitted foreign institutional investment registered FII could

individually invest in a maximum of 5% of a company’s issued capital and all FIIs together up to

a maximum of 24%. From November 1996 are allowed to make 10 percentage investment in

debt securities subject to the specific approval from SEBI as a separate category of FIIs or sub

accounts as 100% debt fund investment such investment were of occurs subjected to the fund

specific ceiling prescribed by SEBI and had to be within overall ceiling US 1.5 $. The

investment was however, restricted to the debt instrument of companies listed or to be listed on

the stock exchanges. In 1997, the aggregate limit on investment by FIIs was allowed to be raised

from 24% to 30% by then board of directors of individual companies by passing a resolution in

their meeting and by special resolution to that effect in the company’s Board meeting. In June

1998 the 5% individual limit was raised to 10%.In March 2000, the ceiling on aggregate FII

portfolio investment increased to 49%.This was subsequently raised to 49%, on March 8 2001,

Finance minister announced February 28 2002 that foreign institutional investors can invest in

accompany under the portfolio investment rout beyond 24% of the paid up capital of the

company with the approval of the general body of the share holders by a special resolution.

Tolani Institute of Management Studies Page 20

New registration criteria for FIIs in India:

With a view to make the P-Note holders eligible for FII registration thereby obviating the need

for ODIs, SEBI has made the following relaxations in the FII registration criteria: Broad Based

Criteria – Registration criteria for “broad based funds” has been modified to include entities

having at least 20 investors with no single investor holding more than 49% of the shares or units

of the fund as against the earlier 10% limit. Track Record of the Applicant – Track record of

individual fund managers will be considered for the purpose of ascertaining the track record of a

newly set up fund, subject to such fund manager providing its disciplinary track record details.

Perpetual Registration – FII and sub-account registrations will be perpetual, subject to payment

of fees. Under the earlier regime, FIIs and their sub-accounts were registered for a period of three

years after which the renewal application was subject to a re-examination by SEBI. Relaxation of

the “regulated” requirement –Pension Funds, Foundations, Endowments, University Funds and

Charitable trusts or societies have been exempted from the requirement of being “regulated” for

registration as FIIs.

Tolani Institute of Management Studies Page 21

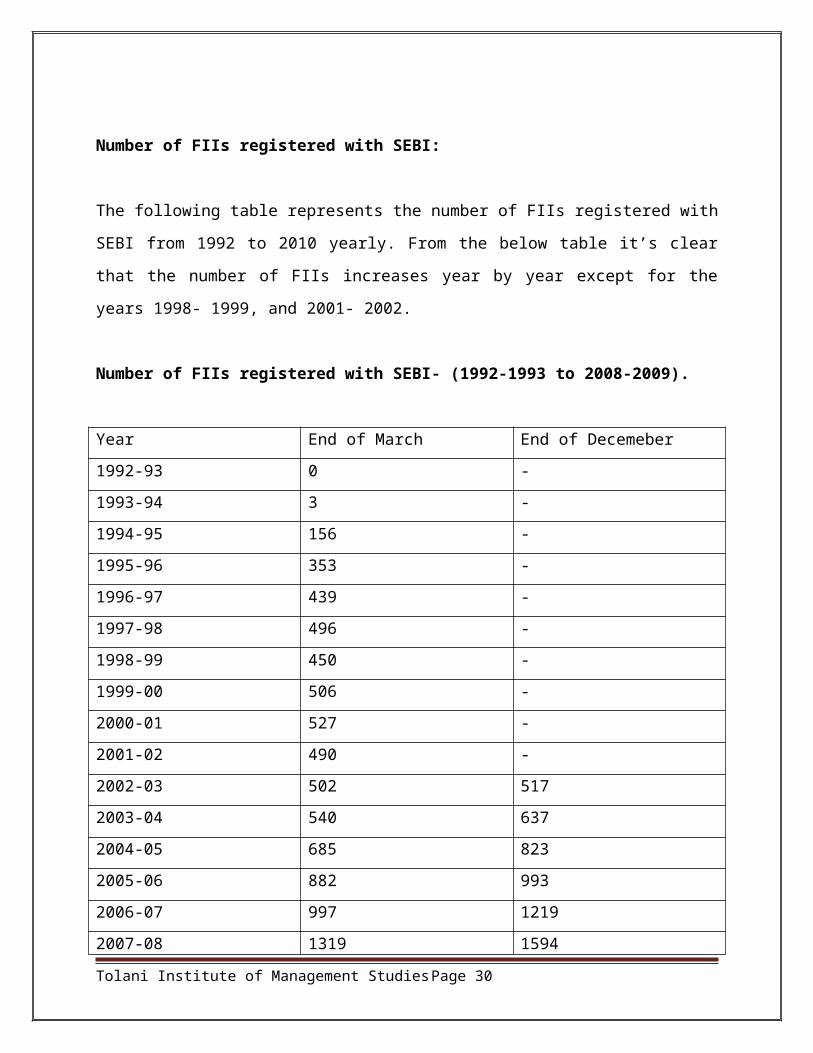

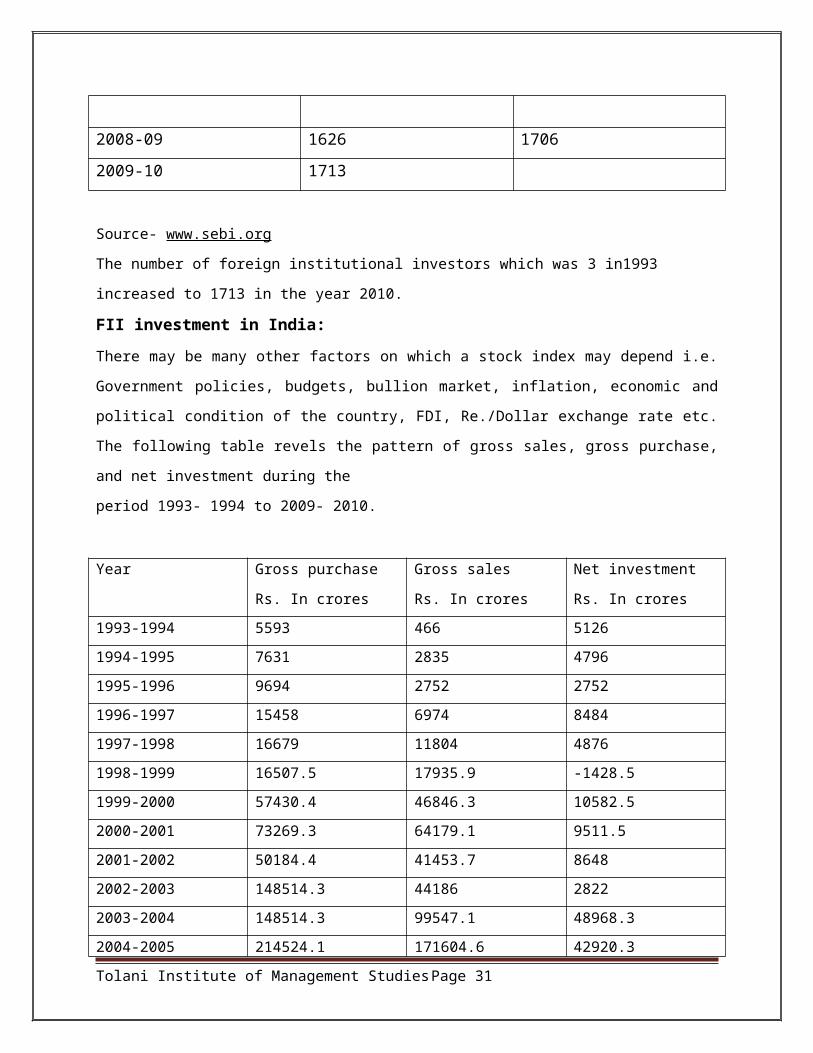

Number of FIIs registered with SEBI:

The following table represents the number of FIIs registered with SEBI from 1992 to 2010

yearly. From the below table it’s clear that the number of FIIs increases year by year except for

the years 1998- 1999, and 2001- 2002.

Number of FIIs registered with SEBI- (1992-1993 to 2008-2009).

Year End of March End of Decemeber

1992-93 0 -

1993-94 3 -

1994-95 156 -

1995-96 353 -

1996-97 439 -

1997-98 496 -

1998-99 450 -

1999-00 506 -

2000-01 527 -

2001-02 490 -

2002-03 502 517

2003-04 540 637

2004-05 685 823

2005-06 882 993

2006-07 997 1219

2007-08 1319 1594

2008-09 1626 1706

2009-10 1713

Source- www.sebi.org

The number of foreign institutional investors which was 3 in1993 increased to 1713 in the year 2010.

Tolani Institute of Management Studies Page 22

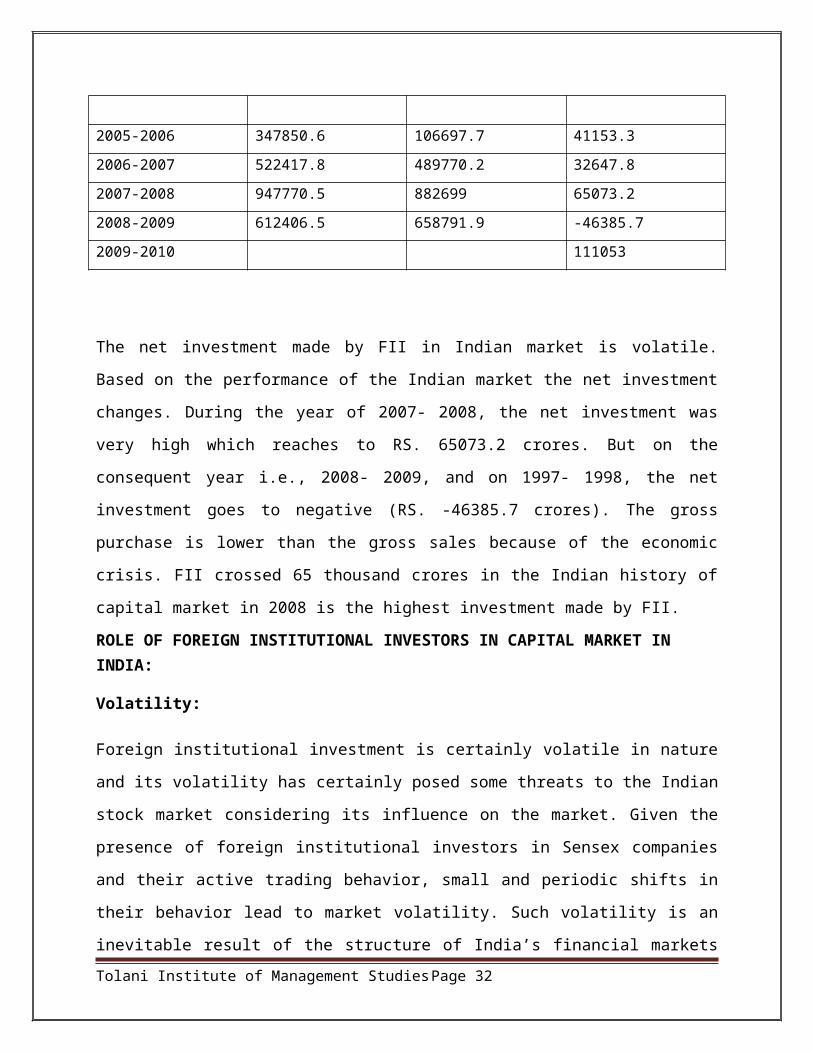

FII investment in India:

There may be many other factors on which a stock index may depend i.e. Government policies, budgets,

bullion market, inflation, economic and political condition of the country, FDI, Re./Dollar exchange rate

etc. The following table revels the pattern of gross sales, gross purchase, and net investment during the

period 1993- 1994 to 2009- 2010.

Year Gross purchase

Rs. In crores

Gross sales

Rs. In crores

Net investment

Rs. In crores

1993-1994 5593 466 5126

1994-1995 7631 2835 4796

1995-1996 9694 2752 2752

1996-1997 15458 6974 8484

1997-1998 16679 11804 4876

1998-1999 16507.5 17935.9 -1428.5

1999-2000 57430.4 46846.3 10582.5

2000-2001 73269.3 64179.1 9511.5

2001-2002 50184.4 41453.7 8648

2002-2003 148514.3 44186 2822

2003-2004 148514.3 99547.1 48968.3

2004-2005 214524.1 171604.6 42920.3

2005-2006 347850.6 106697.7 41153.3

2006-2007 522417.8 489770.2 32647.8

2007-2008 947770.5 882699 65073.2

2008-2009 612406.5 658791.9 -46385.7

2009-2010 111053

The net investment made by FII in Indian market is volatile. Based on the performance of the

Indian market the net investment changes. During the year of 2007- 2008, the net investment was

very high which reaches to RS. 65073.2 crores. But on the consequent year i.e., 2008- 2009, and

on 1997- 1998, the net investment goes to negative (RS. -46385.7 crores). The gross purchase is

lower than the gross sales because of the economic crisis. FII crossed 65 thousand crores in the

Indian history of capital market in 2008 is the highest investment made by FII.

Tolani Institute of Management Studies Page 23

ROLE OF FOREIGN INSTITUTIONAL INVESTORS IN CAPITAL MARKET IN INDIA:

Volatility:

Foreign institutional investment is certainly volatile in nature and its volatility has certainly

posed some threats to the Indian stock market considering its influence on the market. Given the

presence of foreign institutional investors in Sensex companies and their active trading behavior,

small and periodic shifts in their behavior lead to market volatility. Such volatility is an

inevitable result of the structure of India’s financial markets as well. Markets in developing

countries like India are thin or shallow in at least three senses. First, only stocks of a few

companies are actively traded in the market. Thus, although there are more than 8,000 companies

listed on the stock exchange, the BSE Sensex incorporates just 30 companies, trading in whose

shares is seen as indicative of market activity. Second, of these stocks there is only a small

proportion that is routinely available for trading, with the rest being held by promoters, the

financial institutions and others interested in corporate control or influence. And, third the

number of players trading these stocks is also small.

In such a scenario investment by the foreign institutional investors leads to a sharp price increase

this provides incentives to FII investment and enhances investment and when the correction in

the stock prices begins it would have to be a pull out by the FII and can result in sharp decline in

the prices. The other reason for volatility is that the foreign institutional investors are attracted to

a market by the expectation of price increase that tend to be automatically realized, the inflow of

foreign capital can result in an appreciation of the rupee vis-à-vis the dollar This increases the

return earned in foreign exchange, when rupee assets are sold and the revenue converted into

dollars. As a result, the investments turn even more attractive triggering an investment spiral that

would imply a sharper fall when any correction begins. Apart from that the growing realization

by the FIIs of the power they wield in what are shallow markets, encourages speculative

investment aimed at pushing the market up and choosing an appropriate moment to exit. This

manipulation of the market would certainly enhance the volatility and in volatile markets even

the domestic investors try to manipulate the market when the prices are really high. Overall the

foreign institutional investors have been

Tolani Institute of Management Studies Page 24

Bullish on the Indian stocks but the problem is that this bullish nature might be a result of the

activities outside the Indian market it might be due to the performance of their equity market or

their non equity returns. Therefore they seek out for best returns and diversified geographical

portfolio in order to hedge their risk and when they make some adjustments in their portfolio and

make shifts in favor or against a country it borings about sharp changes.

Price building mechanism:

With the increasing participation of the institutional investors in the capital market, it has also

helped the different companies to raise funds for their use through the capital market in India.

Earlier the companies use to go for debt financing which a cost has attached to it and also in

those days the cost of issuing an IPO was higher as compared to the funds that were being

generated by the companies. With the help of FII the market has become more competitive fair

value of their.

Role of speculation:

The effect of foreign speculative activity in emerging markets can be particularly beneficial if in the emerging market, liquidity is poor first, the potential of market manipulation is acute in small emerging markets and liquidity is often poor. Although there are many policy initiatives that could increase liquidity and reduce the degree of collusion among large traders, there may not be a sufficient mass of domestic speculators to ensure market liquidity and efficiency. Second, opening the market to foreign speculators may increase the valuation of local companies, thereby reducing the cost of equity capital

Tolani Institute of Management Studies Page 25

Tolani Institute of Management Studies Page 26

Tolani Institute of Management Studies Page 27

DETERMINANTS OF FOREIGN INSTITUTIONAL INVESTMENT

After the initiation of economic reforms in the early 1990s, the movement of foreign capital flow

increased very substantially. There are a lot of factors that determine the nature and cause of

foreign institutional investment in a country a few of them being inflation exchange rate equity

returns, government policies, price earring ratio and risk. Now if we try to analyze the relation of

each of these factors with the level of foreign inflow in the country, we might have a better

understanding. let us broadly classify the factors into inflation, risk and stock market returns and

understand the basic principle behind the inflows.

a) Equity returns- An increase in the return in the foreign market will induce investors to

withdraw from the Indian (domestic) stock market to invest in the foreign market. Investors are

believed to follow a higher return, hence when the return in the domestic market increases, FII

flows to the domestic market. While the flows are highly correlated with equity returns in India,

they are more likely to be the effect than the cause of these returns. . It is assumed that the equity

returns have a positive impact on the FII inflow but foreign investors can also get involved in

profit booking. They can buy financial assets when the prices are declining, thereby jacking-up

the asset prices and sell when the asset prices are increasing and hence be the cause of such

returns so making it more of a bi-directional relationship.

b) Risk- Investors are considered to be risk averse, hence when risk in the domestic market

increases they will withdraw from the domestic market, when risk in the foreign market

increases, investors will withdraw from the foreign market and invest in the Indian (domestic)

market. Investments, either domestic or foreign, depend heavily on risk factors. Hence, while

studying the behavior of FII, it is important to consider the risk variable. Risk can be divided into

ex-ante and unexpected risk. While the ex-ante risk certainly has an inverse relation with the

foreign investment nothing can be clearly said about the unexpected risk.

c) Inflation- The inflation no doubt has an inverse relation with the foreign investment inflow as

the investor would keep in mind the purchasing power of the funds invested and as inflation

Tolani Institute of Management Studies Page 28

increase i.e. the purchasing power declines the investor is most likely to withdraw his money.

When inflation in the domestic country increases, the purchasing power of the funds invested

declines, hence investors will withdraw from the domestic market. Similarly, when inflation in

the foreign country increases, the purchasing power of funds invested in the foreign country

declines, causing institutional investors to withdraw from the foreign market and make

investment in the domestic (Indian) market.

d) Exchange rate –When the value of the home currency is stronger the FII investments will

also increase as the percentage of returns the FII get automatically increases and visa versa So it

can be said that the inflation and risk in the domestic country and return in the foreign country

adversely affect the FII flowing to the domestic country, whereas inflation and risk in the foreign

country and return in the domestic country have a favorable effect on the flow of FII.

Tolani Institute of Management Studies Page 29

Portfolio Investment:

Portfolio investment represents passive holdings of securities such as foreign stocks, bonds, or

other financial assets, none of which entails active management or control of the securities’

issuer by the investor; where such control exists, it is known as foreign direct investment.

The liberalization of the policy regime was extended to portfolio investment in September1992.

To begin with, foreign institutional investors such as pension funds or mutual funds were

allowed to invest in the domestic capital market subject simply to registration with the Securities

and Exchange Board of India. Guidelines issued by the Reserve Bank of India permitted such

foreign institutional investors to invest in the secondary market for equity subject to a ceiling of

5per cent (subsequently raised to 10 per cent) for individual foreign institutional investors in a

single Indian firm with an overall limit at 24 per cent of equity (later relaxed to 30 per cent of

equity at the option of the firm) for total foreign institutional investment in a single Indian firm.

Foreign portfolio investment further classified into

1. ADR/GDR,

2. Offshore funds.

Global Depositary Receipt:

A negotiable certificate held in the bank of one country representing a specific number of shares

of a stock traded on an exchange of another country. American Depositary Receipts make it

easier for individuals to invest in foreign companies, due to the widespread availability of price

information, lower transaction costs, and timely dividend distributions. Also called European

Depositary Receipt.

The option of portfolio investment was also made available to domestic corporate entities from

September 1992. Indian firms were allowed access to international capital markets through

global depository receipts or Euro convertible bonds which converted debt into equity after

stipulated period. This access, however, was not automatic. Individual applications, drawn up

Tolani Institute of Management Studies Page 30

inconformity with the general guidelines of the government, were subject to approval. This

process remains unchanged.

Offshore Funds

An offshore fund is a collective investment scheme domiciled in an Offshore Financial Centre,

for example British Virgin Islands, Luxembourg, Cayman Islands or Dublin.

Similar facilities for portfolio investment were subsequently extended to Offshore funds, non-

resident Indians (as individuals) and overseas corporate bodies, only for investment in shares or

debentures through stock exchanges, on the same terms as foreign institutional investors, but

subject to a ceiling of 5 per cent for individual non-resident Indians or overseas corporate bodies

in a single Indian firm.

Tolani Institute of Management Studies Page 31

Tolani Institute of Management Studies Page 32

Foreign Institutional Investors in India:

India opened her doors to foreign institutional investors in September, 1992. This event represents a

landmark event since it resulted in effectively globalizing its financial services industry. Initially,

pension funds, mutual funds, investment trusts, Asset Management Companies, nominee companies

and incorporated/institutional portfolio managers were permitted to invest directly in the Indian stock

markets. Beginning 1996-97, the group was expanded to include registered university funds,

endowment, foundations, charitable trusts and charitable. Since then, FII flows which form a part of

foreign portfolio investments have been steadily growing in importance in India.

In the year 1998, the net flows have been positive. The nuclear tests and East Asian crisis did slow

down the flows but as stated by Gordan and Gupta (2003), their effects were short lived. In

percentage of total net turnover of BSE, the share of average of FII sales and purchases increased

from 2.6 percent in 1998 to 5.5 percent in 2002. The cumulative net FII investment in India as on

August 2003 is approximately $17400 million. As of August 2003 net FII investment was 9 percent

of the BSE market capitalization which is small compared to the size of the market. However, in the

words of Banaji (2002), it is not the market capitalization that matters but what is important is the

level of the free float, that is, the shares that are actually publicly available for trading. With floating

stock in the Indian market being less than 25 percent, about 35 percent of the 3 free float available

has been bagged by FIIs - despite the fact that they invest in just a few highly liquid stocks.

Tolani Institute of Management Studies Page 33

Though India receives hardly 1 percent of the FII investments in emerging markets, the portfolio

flows to India have been less volatile when compared with that of many other emerging markets

(Gordan and Gupta, 2003). FIIs by adopting a bottom-up approach seem to invest in top-quality,

high growth, large cap stocks (Gordan and Gupta, 2003). Sytse et al. (2003) provide empirical

evidence that foreign institutional investors in India, invest in large, liquid companies which

enable them to exit their positions quickly at relatively lower cost and also that the foreign

institutional owners have a larger impact than foreign corporate owners when performance is

measured using stock market valuation criterion.

Given that India is one of the fastest growing economies in South Asia, promising a growth of

over 6 percent, second only to China, it would not be a surprise to see increased FII flows to

India in the future. FIIs are now looking at the economy as a whole, with the macro-economic

factors also playing their role in attracting foreign investors. Factors like a strong currency, key

reforms in the banking, power and telecommunications sector, increased consumer spending and

stable policies are expected to play a major role in attracting FIIs to India. The Securities

Exchange Board of India (SEBI) along with the Institute of Chartered Accountants of India

(ICAI) jointly monitor the markets and announces the regulatory measures thus making the

Indian companies more transparent and more disciplined.

According to the April 2001 report on corporate governance by CLSA Emerging Markets, India

ranks fourth with a score of 55.6 percent. Banaji (2000) emphasizes that the capital market

reforms like improved market transparency, automation, dematerialization and regulations on

reporting and disclosure standards were initiated because of the presence of the FIIs. But FII

flows can be considered both as the cause and the effect of capital market reforms. The market

reforms were initiated because of the presence of FIIs and this in turn has lead to increased

flows.

The Government of India gave preferential treatment to FIIs till 1999-2000 by subjecting their

long term capital gains to lower tax rate of 10 percent while the domestic investors had to pay

higher long-term capital gains tax. The Indo-Mauritius Double Taxation Avoidance Convention

2000 (DTAC), exempts Mauritius-based entities from paying capital gains tax in India -

Tolani Institute of Management Studies Page 34

including tax on income arising from the sale of shares. This gives an incentive for foreign

investors to invest in Indian markets taking the Mauritius route. Consequently, we now see

investments coming from Mauritius while there were none before 2000.

Tolani Institute of Management Studies Page 35

FOREIGN INSTITUTIONAL INVESTMENT: A COST BENEFIT

ANALYSIS

BENEFITS

a) Reduced cost of equity:

FII inflows augment the sources of funds in the Indian capital markets. FII investment reduces

the required rate of return for equity, enhances stock prices, and fosters investment by Indian

firms in the country. The impact of FIIs upon the cost of equity capital may be visualized by

asking what stock prices would be if there were no FIIs operating in India.

b) Stability in the balance of payment:

For promoting growth in a developing country such as India, there is need to augment domestic

investment, over and beyond domestic saving, through capital flows. The excess of domestic

investment over domestic savings result in a current account deficit and this deficit is financed

by capital flows in the balance of payments. Prior to 1991, debt flows and official development

assistance dominated these capital flows. This mechanism of funding the current account deficit

is widely believed to have played a role in the emergence of balance of payments difficulties in

1981 and 1991. Portfolio flows in the equity markets, and FDI, as opposed to debt-creating

flows, are important as safer and more sustainable mechanisms for funding the current account

deficit.

c) Knowledge flows:

The activities of international institutional investors help strengthen Indian finance. FIIs advocate

modern ideas in market design, promote innovation, development of sophisticated products such

as financial derivatives, enhance competition in financial intermediation, and lead to spillovers of

human capital by exposing Indian participants to modern financial techniques, and international

best practices and systems.

Tolani Institute of Management Studies Page 36

d) Strengthening corporate governance:

Domestic institutional and individual investors, used as they are to the ongoing practices of

Indian corporate, often accept such practices, even when these do not measure up to the

international benchmarks of best practices. FIIs, with their vast experience with modern

corporate governance practices, are less tolerant of malpractice by corporate managers and

owners (dominant shareholder). FII participation in domestic capital markets often lead to

vigorous advocacy of sound corporate governance practices, improved efficiency and better

shareholder value.

e) Improving market efficiency:

A significant presence of FIIs in India can improve market efficiency through two channels.

First, when adverse macroeconomic news, such as a bad monsoon, unsettles many domestic

investors, it may be easier for a globally diversified portfolio manager to be more dispassionate

about India's prospects, and engage in stabilizing trades. Second, at the level of individual stocks

and industries, FIIs may act as a channel through which knowledge and ideas about valuation of

a firm or an industry can more rapidly propagate into India. For example, foreign investors were

rapidly able to assess the potential of firms like Infosys, which are primarily export-oriented,

applying valuation principles that prevailed outside India for software services companies.

COSTS

a) Hedging and positive feedback training:

There are concerns that foreign investors are chronically ill informed about India, and this lack of

sound information may generate herding (a large number of FIIs buying or selling together) and

positive feedback (buying after positive returns, selling after negative returns).These Kinds of

behavior can exacerbate volatility ,and push prices away from fair values.

Tolani Institute of Management Studies Page 37

b) Balance of payment vulnerability:

There are concerns that in an extreme event, there can be a massive flight of foreign capital out

of India, triggering difficulties in the balance of payments front. India's experience with FIIs so

far, however, suggests that across episodes like the Pokhran blasts, or the 2001 stock market

scandal, no capital flight has taken place. A billion or more of US dollars of portfolio capital has

never left India within the period of one month. When juxtaposed with India's enormous current

account and capital account flows, this suggests that there is little vulnerability so far.

c) Possibility of takeovers:

While FIIs are normally seen as pure portfolio investors, without interest in control, portfolio

investors can occasionally behave like FDI investors, and seek control of companies that they

have a substantial shareholding in. Such outcomes, however, may not be inconsistent with India's

quest for greater FDI. Furthermore, SEBI's takeover code is in place, and has functioned fairly

well, ensuring that all investors benefit equally in the event of a takeover.

Tolani Institute of Management Studies Page 38

A STUDY OF MAJOR EPISODES OF VOLATILITY

FII investment in equities had little role to play in the crisis.

Fung, Hsieh, and Stsatsaronis (2000) report “At the height of the episode, some Asian

government officials accused speculators and hedge funds of attacking the currencies and

causing their downfall. A public debate ensued, and the International Monetary Fund (IMF)

responded by examining the role of hedge funds in the Asian currency crisis. The resulting study

by Eichengreen, Mathieson, Chadha, Jansen, Kodres, and During the stock market scam which

shook the capital market in India the FII were also one of the major factors which exacerbates

the fall in the Sensex. During the Black Monday episode the FII were also on a heavy selling

spree which ultimately leads to some major fall in the Sensex value.

There have been four episodes of vulnerability in India, which are negative shocks affecting the

economy, and influencing the behavior of investors. These are: the East-Asian crisis in 1997, the

Pokhran Nuclear explosion (May 1998) and the attendant sanctions, the stock market scam of

early 2001, and the Black Monday of May 17, 2004.10 The investment behavior of the FIIs vis-à-

vis the movements of the stock market indices during these episodes are given in Table.

Tolani Institute of Management Studies Page 39

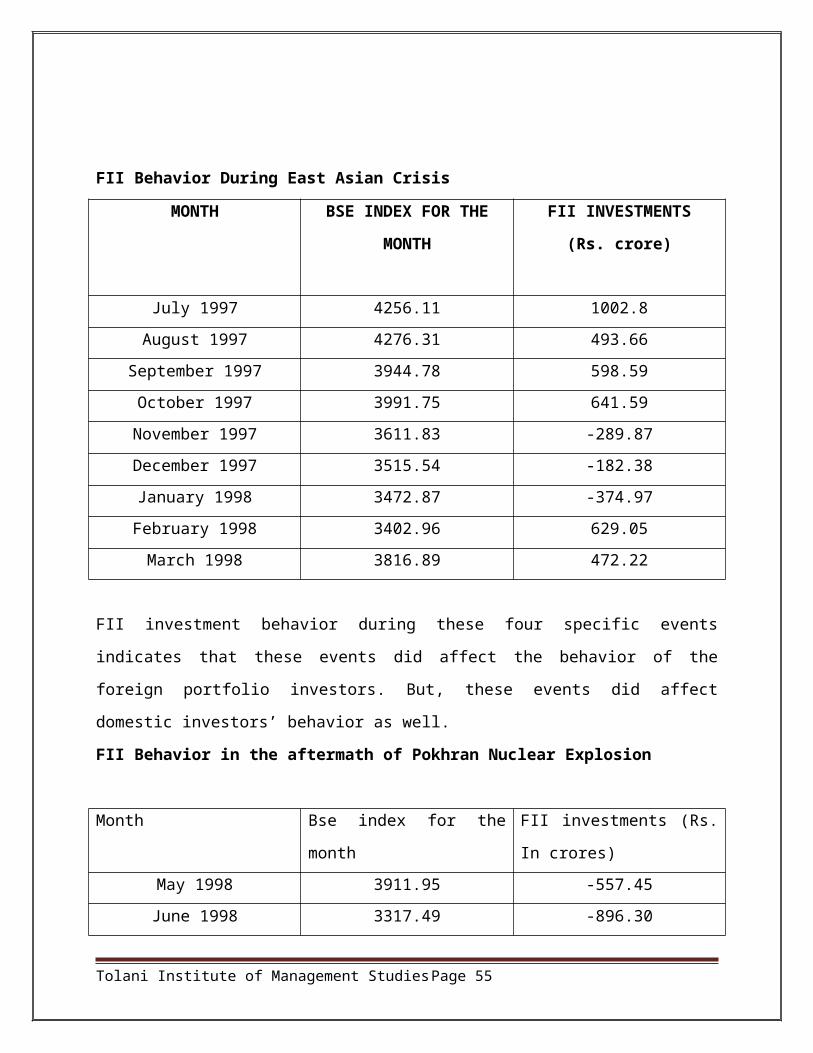

FII Behavior During East Asian Crisis

MONTH BSE INDEX FOR THE

MONTH

FII INVESTMENTS

(Rs. crore)

July 1997 4256.11 1002.8

August 1997 4276.31 493.66

September 1997 3944.78 598.59

October 1997 3991.75 641.59

November 1997 3611.83 -289.87

December 1997 3515.54 -182.38

January 1998 3472.87 -374.97

February 1998 3402.96 629.05

March 1998 3816.89 472.22

FII investment behavior during these four specific events indicates that these events did affect

the behavior of the foreign portfolio investors. But, these events did affect domestic investors’

behavior as well.

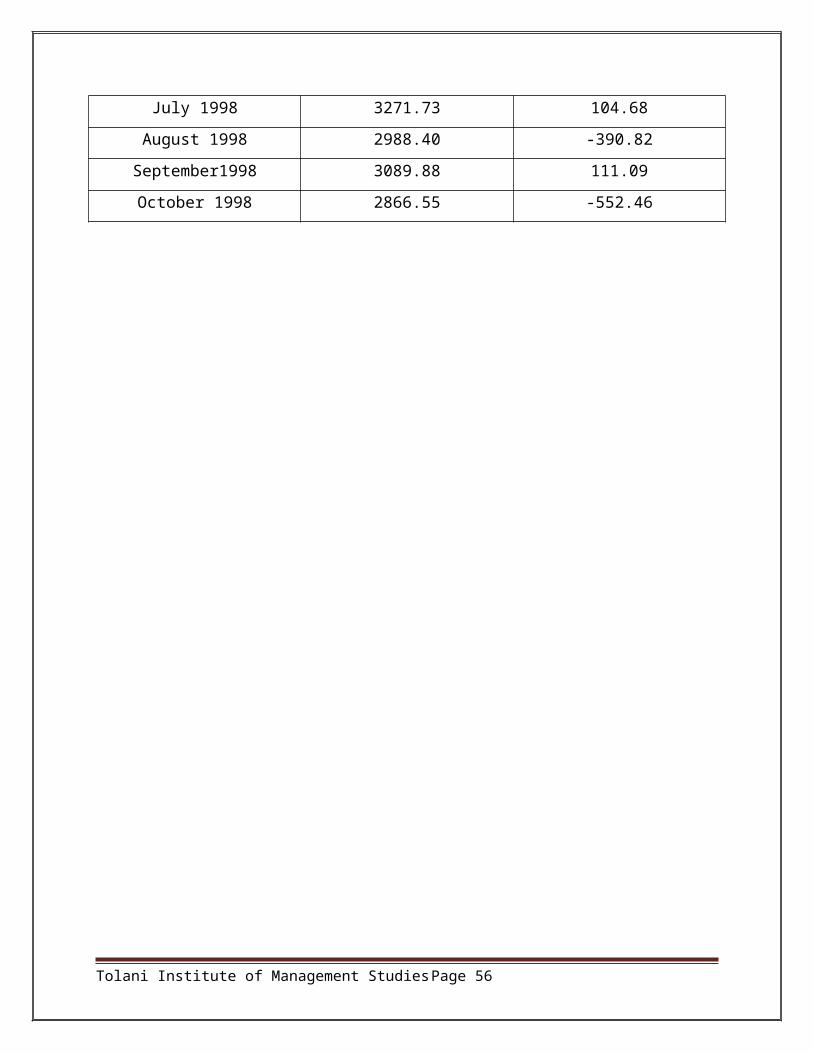

FII Behavior in the aftermath of Pokhran Nuclear Explosion

Month Bse index for the month FII investments (Rs. In crores)

May 1998 3911.95 -557.45

June 1998 3317.49 -896.30

July 1998 3271.73 104.68

August 1998 2988.40 -390.82

September1998 3089.88 111.09

October 1998 2866.55 -552.46

Tolani Institute of Management Studies Page 40

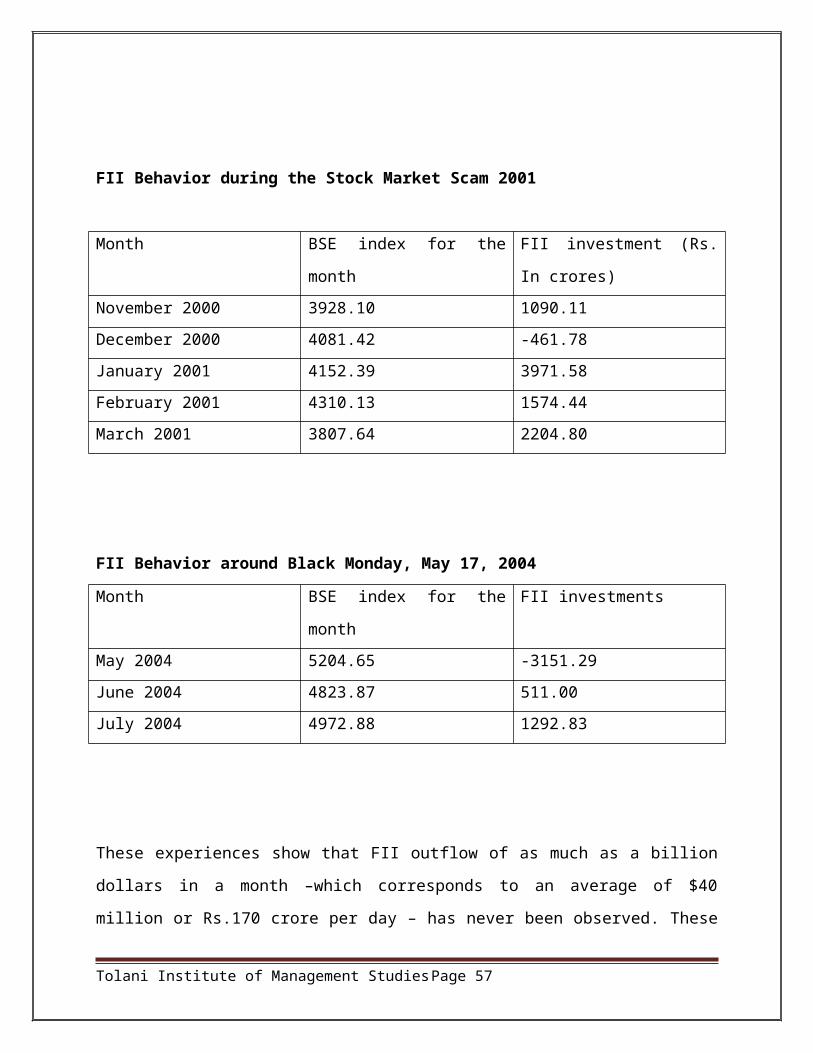

FII Behavior during the Stock Market Scam 2001

Month BSE index for the month FII investment (Rs. In crores)

November 2000 3928.10 1090.11

December 2000 4081.42 -461.78

January 2001 4152.39 3971.58

February 2001 4310.13 1574.44

March 2001 3807.64 2204.80

FII Behavior around Black Monday, May 17, 2004

Month BSE index for the month FII investments

May 2004 5204.65 -3151.29

June 2004 4823.87 511.00

July 2004 4972.88 1292.83

These experiences show that FII outflow of as much as a billion dollars in a month –which

corresponds to an average of $40 million or Rs.170 crore per day – has never been observed.

These values – Rs.170 crore per day – are small when compared with equity turnover in India. In

calendar 2004, gross turnover on the equity market of Rs.88 lakh crore contained Rs.5 lakh crore

of gross turnover by FIIs. This suggests that as yet, FIIs are a small part of the Indian equity

market. Transactions by FIIs of Rs.5 lakh crore in a year might have been large in 1993, but the

success of a radical new market design in the Indian equity market have led to enormous growth

of liquidity and market efficiency on the equity market. Through this, India’s ability to absorb

substantial transactions on the equity market appears to be in place.

Tolani Institute of Management Studies Page 41

The net FII inflows into India have been less volatile compared to other emerging markets this

stability could be attributed to several factors: Strong economic fundamentals and attractive

valuation of companies. Improved regulatory standards, high quality of disclosure and corporate

governance requirement, accounting standards, shortening of settlement cycles, efficiency of

clearing and settlement systems and risk management mechanisms. Product diversification and

introduction of derivatives.

Strengthening of the rupee dollar exchange rate and low interest rates in the US.

Post 2004 Major Volatile Episodes:

As from the month of Jan 2008 the BSE Sensex was already moving down due to the weak

global cues and US recession and similarly the FII investment fell drastically during that period

running panic among the investors and further exacerbating the fall. But in the case of mutual

fund investment went up during the time shows that the domestic institutional investors cash on

the fall of Sensex because of the strong fundamentals of the Indian capital market.

We can very well say that this time around the fall of BSE Sensex was majorly due to the FII

which went on a selling spree which lead to the fall of the market during this Crash.FII acted in

this fashion because of the weak global cues i.e. at that point of time other emerging markets

were also down.

The fall of 769 points by Sensex on Dec 17, 2007 was attributed to the fact mainly due to the

subprime losses and also was exacerbated due to the withdrawal of investments by the FII. As

the subprime losses mainly hit the US economy and the majority of FII participating in the

Indian capital market are from US .To cover their losses in US they started selling in India which

lead to the fall of Sensex on that particular day and subsequent days.

During the month of October 2007 Indian govt. took some strict measure to control the usage of

the Participatory notes. The restrictions proposed by SEBI in regulating participatory notes in a

sudden announcement wrought havoc in the operations of the share market causing a fall of over

1,700 points in the Sensex on Wednesday. SEBI should have used some pragmatic caution by

avoiding the announcement and introducing regulatory steps in a phased manner. The share

Tolani Institute of Management Studies Page 42

market is extremely vulnerable to the sentiments created by the utterances of those in regulatory

authority.

This lead the FII to withdraw from the Indian market as they were not sure of how the measure

taken by the govt. will be implemented .This is clearly viable from the above that this time

around the FII were the main cause of the crash of the Sensex on 18 th Oct. But also there comes

an interesting fact that there was also a heavy selling on 22 nd October but this time the FII

Withdrawal effect was offset by the Huge investment made by domestic institutional investor

specially LIC, which saved the market from a heavy meltdown.

The reasons being given for the crash are the sale of Rs 7300 crore (Rs 73Billion) shares by FII’s

in the past 1 week, an expected increase in interest rates by the US Feds, a crash in the

international commodity prices, and the straw which broke its back seems to be a government

circular which was interpreted that FIIs should be taxed. P Chidambaram, the country’s Finance

Minister, issued an evening press release denying the latter.

Tolani Institute of Management Studies Page 43

Tolani Institute of Management Studies Page 44

Objectives of project

To study the impact of FII on Indian stock market.

To understand the concept of BSE sensitive index.

To understand the concept of FIIs.

To understand the relationship between the Sensex and FII.

To know the sector which get affected more by activities of FIIs.

Tolani Institute of Management Studies Page 45

Methodology

Data Collection Method :

Here, information plays an important role to make research successful. Basically there are two

types of sources to collect data namely they are as under.

Primary data

Secondary data

For this project only secondary data was used.

Secondary data:

For the secondary data various literatures, books, journals, magazines, web links are used. As

there are not possibilities of collecting data personally so no questionnaire is made.

SAMPLING DESIGN:

• Universe

In this study the universe is finite and will take into the consideration related news and events

that have happened in last few year.

• Sampling Unit: -

As this study revolves around the foreign institutional investment and Indian stock market. For

the sampling unit is confined to only the Indian stock market.

Tolani Institute of Management Studies Page 46

Techniques of analysisRegression analysis and Correlation analysis:

Regression Analysis: We can analyze how a single dependent variable is affected by the values

of one or more independent variables — for example, how an athlete's performance is affected

by such factors as age, height, and weight.

Correlation: This analysis tool and its formulas measure the relationship between two data sets

that are scaled to be independent of the unit of measurement. We can use the Correlation tool to

determine whether two ranges of data move together — that is, whether large values of one set

are associated with large values of the other (positive correlation), whether small values of one

set are associated with large values of the other (negative correlation), or whether values in both

sets are unrelated (correlation near zero).

Tolani Institute of Management Studies Page 47

Tolani Institute of Management Studies Page 48

.

Tolani Institute of Management Studies Page 49

TO FIND THE RELATIONSHIP BETWEEN THE FIIS EQUITY INVESTMENT

PATTERN AND INDIAN STOCK INDICES.

The sample data consists of 24 observations for FII, Sensex and S&P CNX Nifty starting from January

2001 to February 2011. Average index of all the indices and daily net investments made by FII is taken

into consideration in the study. FII was taken as independent variable. Stock indices were taken as

dependent variable. The data was taken from various financial sites.

The relationship between the FII’s equity investment pattern and Indian stock indices is studied for the 10

year with the help of correlation and regression analysis. The results and the analysis are shown below:

Tolani Institute of Management Studies Page 50

Correlation

SENSEX NIFTYCORRELATION WITH FII 0.352 0.35

Indices Correlation with FII

Auto 0.32

Bankx 0.33

IT 0.16

FMCG 0.17

Oil and Gas 0.27

From the above table we can say that FII has a positive impact on the indices which means that if

FIIs come in India then they will affect Indian Capital market. FIIs have same co-relation with

Sensex as well as Nifty.

FII ‘s impact on sectorial indices is also positive which shows that bank sector is most affected

sector amongst which we have analyzed and IT sector is the least affected sector but they are

affected positively.

Tolani Institute of Management Studies Page 51

Hypothesis test

Null Hypothesis (H0): Sensex does not rises with the increase in FIIs investment

Hypothesis (Ha): Sensex rises with the increase in FIIs investment.

Correlations

FII INVESTMENT CHANGE IN SENSEX

FII INVESTMENT Pearson Correlation 1 .352**

Sig. (2-tailed) .000

N 2722 2721

CHANGE IN SENSEX Pearson Correlation .352** 1

Sig. (2-tailed) .000

N 2721 2722

**. Correlation is significant at the 0.01 level (2-tailed).

Regression Model

Model R R Square Adjusted R Square

Std. Error of the

Estimate

1 .352a .124 .124 175.463

a. Predictors: (Constant), FII INVESTMENT

Tolani Institute of Management Studies Page 52

The data includes 2722 observations of daily basis of Sensex and FIIs in year from 2000 to 2011. The correlation and regression is calculated.

Here the correlation 0.35 which shows that both have positive relation if FII increase then Sensex will also increase. But if we compare the significance with the degree of freedom then null hypothesis is accepted because (0.00<0.01) so it shows that FIIs will have no significant impact on the Sensex

There is positive effect of FII on Sensex but the correlation coefficient is low. This means that Sensex has a relation with FII but the FII is not influencing the Sensex much. The regression coefficient is 0.124 which reflects 0.124 % variability in Sensex with the independent variable every day due to FII. The standard error comes out to be 175.463 which is high and so it means that the deviation from the mean value is high. This does not mean the relation is false but we can say that the error in linear relation is high.

Tolani Institute of Management Studies Page 53

Hypothesis

Null Hypothesis (H0): Nifty does not rises with the increase in FIIs investment

Hypothesis (Ha): Nifty rises with the increase in FIIs investment.

Tolani Institute of Management Studies Page 54

Correlations

FII INVESTMENT CHANGE IN NIFTY

FII INVESTMENT Pearson Correlation 1 .350**

Sig. (2-tailed) .000

N 2722 2721

CHANGE IN NIFTY Pearson Correlation .350** 1

Sig. (2-tailed) .000

N 2721 2722

**. Correlation is significant at the 0.01 level (2-tailed).

Regression Model Summary

Model R R Square Adjusted R Square

Std. Error of the

Estimate

1 .350a .123 .123 53.109

a. Predictors: (Constant), FII INVESTMENT

Here the correlation 0.35 which shows that both have positive relation if FII increase then Nifty will also increase. But if we compare the significance with the degree of freedom then null hypothesis is accepted because (0.00<0.01) so it shows that FIIs will have no significant impact on the Nifty.

There is positive effect of FII on Nifty but the correlation coefficient is low. This means that Nifty has a relation with FII but the FII is not influencing the Nifty much. The regression coefficient is 0.123 which reflects 0.123 % variability in Nifty with the independent variable every day due to FII. The standard error comes out to be 53.109. Which is low and so it means that the deviation from the mean value is low. This means the relation is there between nifty and FII.

Tolani Institute of Management Studies Page 55

.

Tolani Institute of Management Studies Page 56

Hypothesis

Null Hypothesis (H0): FMCG, IT, Oil & Gas, Auto, Bankx does not rises with the

increase in FIIs investment

Hypothesis (Ha): FMCG, IT, Oil & Gas, Auto, Bankx rises with the increase in FIIs

investment.

Correlations

FII INVESTMENT BANKX CHANGE

FII INVESTMENT Pearson Correlation 1 .333**

Sig. (2-tailed) .000

N 2722 2474

BANKX CHANGE Pearson Correlation .333** 1

Sig. (2-tailed) .000

N 2474 2475

**. Correlation is significant at the 0.01 level (2-tailed).

Model Summary

Model R R Square Adjusted R Square

Std. Error of the

Estimate

1 .333a .111 .111 129.08643

a. Predictors: (Constant), FII INVESTMENT

Tolani Institute of Management Studies Page 57

The correlation coefficient is 0.111 which means there is no significant correlation between banking sector and FIIs on daily basis. It shows the low linear relation between the two variables but not a lack of relationship altogether. Here the standard error is 129.08643 that means error is high. Still It can be seen that BSE banking is affected a lot by FII and with more FIIs index is

also going up.

Correlations

FII INVESTMENT FMCG CHANGE

FII INVESTMENT Pearson Correlation 1 .171**

Sig. (2-tailed) .000

N 2722 2474

FMCG CHANGE Pearson Correlation .171** 1

Sig. (2-tailed) .000

N 2474 2475

**. Correlation is significant at the 0.01 level (2-tailed).

Model Summary

Model R R Square Adjusted R Square

Std. Error of the

Estimate

1 .171a .029 .029 33.227

a. Predictors: (Constant), FII INVESTMENT

Tolani Institute of Management Studies Page 58

In FMCG sector the correlation between FII and index is positive that is .171 which is very low. The co relation co-efficient of regression is .029 that means the only 2.9% volatility comes on daily basis due to FII activity here the standard error is also 33.227 which is very low. So FII is not more affect the FMCG sector on daily basis. Or the flow of FII on this sector is very low.

Tolani Institute of Management Studies Page 59

Correlations

FII INVESTMENT OIL GAS CHANGE

FII INVESTMENT Pearson Correlation 1 .272**

Sig. (2-tailed) .000

N 2722 2474

OIL GAS CHANGE Pearson Correlation .272** 1

Sig. (2-tailed) .000

N 2474 2475

**. Correlation is significant at the 0.01 level (2-tailed).

Model Summary

Model R R Square Adjusted R Square

Std. Error of the

Estimate

1 .272a .074 .074 134.95120

a. Predictors: (Constant), FII INVESTMENT

The data includes 2474 observations of daily basis of Oil and Gas and FIIs in year from 2001 to 2011. Here the correlation is 0.27 which means FII is positively affect the oil and gas sector but the correlation co-efficient is .074 that means the volatility comes due to FII investment in this sector is only 7.4% on daily basis. While considering the std.error which is 134.951 which high so, linearity is not there in the observation.

Tolani Institute of Management Studies Page 60

Correlations

FII INVESTMENT BSE IT CHANGE

FII INVESTMENT Pearson Correlation 1 .165**

Sig. (2-tailed) .000

N 2722 2474

BSE IT CHANGE Pearson Correlation .165** 1

Sig. (2-tailed) .000

N 2474 2475

**. Correlation is significant at the 0.01 level (2-tailed).

Model Summary

Model R R Square Adjusted R Square

Std. Error of the

Estimate

1 .165a .027 .027 83.68679

a. Predictors: (Constant), FII INVESTMENT

There is positive effect of FII on IT sector but the correlation coefficient is also 0.165. This means that IT has a relation with FII but the FII is not influencing the IT much. The regression coefficient is 0.165 which reflects 0.16 % variability in IT with the independent variable every day due to FII. The standard error comes out to be 83.68. Which is low and so it means that the deviation from the mean value is low. This means the relation is there between IT and FII.

Tolani Institute of Management Studies Page 61

Model Summary

Model R R Square Adjusted R Square

Std. Error of the

Estimate

1 .325a .106 .105 65.34498

a. Predictors: (Constant), FII INVESTMENT

Here the FII and auto sector have positively correlated that is 0.32 that means the FII flow comes more in this sector compare to other sector so the volatility of auto sector is more. And the co –efficient of correlation is 0.105 that means the due to FII investment in Auto sector daily volatility is 10.5% in auto index. While the std.error is 65.34 which is very low so the deviation from mean is also low.

Hypothesis of sector indices

Here the correlation of bankx, FMCG, Oil and Gas, IT, and Auto sector are 0.33, 0.17, 0.27, 0.16 , 0.32 which shows that all the five sector have positive relation with FII if FII increase then all five indices will also increase. But if we compare the significance with the degree of freedom then null hypothesis is accepted because (0.00<0.01) so it shows that FIIs will have no significant impact on the indices. There are other factors which also affect the indices.

Tolani Institute of Management Studies Page 62

Correlations

FII INVESTMENT AUTO CHANGE

FII INVESTMENT Pearson Correlation 1 .325**

Sig. (2-tailed) .000

N 2722 2474

AUTO CHANGE Pearson Correlation .325** 1

Sig. (2-tailed) .000

N 2474 2475

**. Correlation is significant at the 0.01 level (2-tailed).

Tolani Institute of Management Studies Page 63

CONCLUSION

According to findings and results, we can conclude that FII have positive correlation with

NIFTY & SENSEX as well as other sectorial indices but did not have any significant impact on

the Indian capital market.

At the significant level 0.01 we found that FII have not any significant effect on SENSEX &

NIFTY and that’s why the null hypothesis is accepted, which says that SENSEX & NIFTY are

not much affected by FII’s investment. but there are other factors like government policies,

budgets, bullion market, inflation, economical and political condition, etc. do also have an

impact on the Indian stock market.

Many research papers says about FII’s have significant impact on Indian Capital Market but it

can be because of their investment, Indian Institutional Investor as well as retail investor may act

on their direction of trading and overall impact will be positive. Through which we cannot

directly say that FII’s have significant impact.

Tolani Institute of Management Studies Page 64

RECOMMENDATIONS

After the analysis of the project study, following recommendations can be made:

1) Simplifying procedures and relaxing entry barriers for business activities and providing investor friendly laws and tax system for foreign investors.

2) Allowing foreign investment in more areas. In different industries indices the FIIs should be encouraged through different patterns .

3) Somewhere, a restriction related to the track record of Sub- Accounts is also to be made on the investors who withdraw money out of the Indian stock market who have invested with the help of participatory notes.

4) We have to modernize and also have to save our culture. Similarly the laws should be such that it protect domestic investors and also promote trade in country through FIIs.

5) Encourage industries to grow to make FIIs an attractive junction to invest.

Tolani Institute of Management Studies Page 65

BIBLIOGRAPHY

www.bseindia.com

www.nseindia.com

http://www.capitalmarket.com/MarketWatch/fii.asp

www.madaan.com/fii.html

http://finance.yahoo.com/q/hp?s=

%5EBSESN&a=00&b=1&c=2000&d=09&e=14&f=2010&g=d

http://www.traderji.com/equities/6939-fii-foreign-institutional-investor.html

www.Sebi.org.in

Books:

Lind, D, Marchal, W, and Wathen, S. (2008). Statistical Techniques in Business and Economics

(13th edition). New Delhi: Tata McGraw-Hill.

Tolani Institute of Management Studies Page 66

![2224. Foreign Institutional Investment [Fii] Impact on Indian Stock Market and Its Investment Behavior [Fin]](https://img.dokumen.tips/doc/110x75/577d20d51a28ab4e1e93dc1d/2224-foreign-institutional-investment-fii-impact-on-indian-stock-market.jpg)