Embed Size (px)

Citation preview

Impact of Changing the Maximum Out-of-Pocket Amounts for

Qualified Health Plans and Stand Alone Dental Plans

REPORT

PREPARED FOR

NORC AND THE CENTER FOR CONSUMER

INFORMATION AND INSURANCE OVERSIGHT (CCIIO)

BY

JULIE PEPER, FSA, MAAA KARAN RUSTAGI, ASA, MAAA STEVE WESSLING, ASA, MAAA

JOHN EBELING

AUGUST 26, 2013

Impact of Changing the Maximum Out-of-Pocket Amounts

August 26, 2013 Page 2

I. Background

The Affordable Care Act (ACA) restricts the maximum out-of-pocket (MOOP) payment for Essential

Health Benefits (EHB) to $6,350 for an individual in 2014. Essential Health Benefits cover pediatric dental

services, which can be offered as a stand-alone dental product (SADP) or as part of a qualified health

plan (QHP) benefit package. When offered as part of a QHP, the consumer will have a total MOOP of

$6,350. When offered as a SADP, the SADP is permitted to have a MOOP of up to $700, resulting in a

total MOOP for the consumer in excess of the $6,350 level in the QHP, up to $7,050. The Center for

Consumer Information and Insurance Oversight (CCIIO) is exploring policies to coordinate MOOPs

between the QHPs and SADPs to remove the discrepancy in total MOOP experienced or perceived by

the consumer. One method of removing this discrepancy is to lower the MOOP on QHPs and/or SADPs

such that the total MOOP for QHPs and SADPs is $6,350.

Wakely Consulting Group, in partnership with NORC at the University of Chicago, was retained by CCIIO

to report on the plan design impacts needed to keep the actuarial value (AV) constant as the MOOP is

varied. MOOP changes were modeled on both the QHPs and the SADPs. One method of removing the

discrepancy is to lower the MOOP on QHPs or SADPs such that the total MOOP for QHPs and SADPs is

$6,350. Wakely determined the change in cost if it is not possible to keep the actuarial value the same

with reasonable plan design changes. Throughout this report, reasonable plan design changes are those

that we would expect a typical consumer to find acceptable. The primary approach to determining

consumer acceptability was based on the plan designs currently available in the dental insurance

market.

II. Executive Summary

To address questions about the interplay of MOOPs for QHPs and SADPs, Wakely has analyzed the

impact of changes in MOOPs on QHPs with SADPs. Individual and Small Group products must meet

certain AVC requirements, essentially being within two percentage points of the requirements at each

metal tier level (60%, 70%, 80% or 90%). Further, any net changes in AV cause the premiums to change

since changes in AV affect the expected cost of a plan. Therefore, any changes in MOOP would need to

be offset by changing other cost sharing features to continue to meet the required AV levels and not

cause premiums to change. Wakely tested several sample starting plan designs to inform the decision of

how much the MOOP can be varied and the corresponding cost sharing changes required.

For SADPs, Wakely tested four plans, two with an actuarial value around 85% and two with an actuarial

value around 70%. Each plan design started with a MOOP of $700. The analysis modeled decreasing

MOOPs down to $100 in $100 increments and increasing MOOPs up to $1,000 in $100 increments.

For QHPS, Wakely used four plans, two with an actuarial value around 70% (silver metal level) and two

with an actuarial value around 60% (bronze metal level). At each actuarial value level, the two plans

Impact of Changing the Maximum Out-of-Pocket Amounts

August 26, 2013 Page 3

included a deductible plan and a High Deductible Health Plan (HDHP)1. Each plan design started with a

MOOP of $6,350. The analysis modeled decreasing MOOPs down to $5,350 in $100 increments.

For both SADPs and QHPs, Wakely identified the simplest offsetting changes in other cost sharing

elements that kept the actuarial value the same at each MOOP level. The most important conclusion

from our analysis is that MOOPs on both the medical QHPs and SADPs can mostly be varied with

reasonable and offsetting cost sharing changes. Reasonability of cost sharing is determined based on

the levels currently available in the market. For example, cost sharing that exceeds 50% of the cost of

the service was considered unreasonable. Throughout this document, we use the term ‘unreasonable

cost sharing’ if the level of cost sharing is rarely seen in the market.

For a SADP with a 70% actuarial value, we found that the MOOP can be increased from the standard

$700 up to $1,000. To offset the reduction in actuarial value, the deductible needs to be reduced from

$150 to $110 without any other changes to the plan designs. There is limited room to decrease the

MOOP without increasing cost sharing to unreasonable or nearly unreasonable levels. Unreasonable

cost sharing includes cost sharing that is more than 50% of the average cost of the service. The SADP

MOOP can be decreased from $700 to $400 with a corresponding increase in deductible from $150 to

$300. Any additional reductions in MOOP cannot be absorbed by reasonable changes to plan designs.

For the QHPs, the MOOP can be reduced from the highest 2014 allowable limit of $6,350 down to

$5,350 without requiring unreasonable plan design changes, which means that premium increases are

not necessary. This observation was true for all four sample plans we tested. Further reductions in

MOOP could be made for Silver plans without requiring unreasonable plan design changes. However,

MOOP could not be reduced to much less than $5,350 without requiring unreasonable plan design

changes for Bronze plans.

Wakely also looked at whether the cost sharing changes would impact premiums due to induced

demand. That is, we estimated whether members would be likely to use more services given the

resulting cost sharing at each MOOP level. For QHPs, the change in MOOP resulted in a modest AV

change. It is not expected that QHPs would see a significant increase in induced demand based on the

resulting cost sharing changes. For SADPs, there is a significant change in AV, particularly at the lower

MOOP levels. Significant induced demand is possible at these lower levels, increasing premiums.

We would expect lower MOOPs and higher copays, deductibles or coinsurance to generally be more

appealing to sicker individuals. Therefore, we believe it is reasonable to assume that lowering the

MOOP would increase average morbidity and therefore average cost. However, the effect may not be

material depending on how significant the plan design changes are.

Our analysis was based on the Federal Actuarial Value Calculator (AVC), the Wakely pricing model,

information and guidance provided by CCIIO, the Towers Watson Dental pricing model, and actuarial

judgment. Actual results will likely vary from our estimates. Our analysis was limited because we used

1 Deductible plans are more common and popular in the market than HDHPs, but deductible plans are also more

difficult to model for our analysis.

Impact of Changing the Maximum Out-of-Pocket Amounts

August 26, 2013 Page 4

pricing models that employ distributions for average members (or average adults), rather than actual

detailed claims.2 Our analysis was designed for purposes of assisting CCIIO with making general

decisions. If CCIIO decides to move forward with changes in maximum allowable MOOPs and

integration between medical and SADP MOOPs, we recommend further analysis and refinement of our

estimates.

III. Task 1a: Impact of MOOP on Stand-Alone Dental Plans

Wakely created four stand-alone dental plan designs to estimate the impact on plan designs of changing

the MOOP at various levels. All the MOOP and deductible levels shown in this analysis are at the

member level as opposed to the family level. The analysis shows the actuarial value impact of changing

the MOOP and then outlines the required cost sharing changes for the actuarial value (AV) to remain in

line with the original plan. Four plan designs were created; two at the 70% AV level and two at the 85%

AV level.

The coinsurance and deductible levels in the plans are similar in design to plans that are currently in the

marketplace. One relatively minor simplification in the design is that the deductible in these sample

plans applies to all services, whereas many plans in the marketplace do not apply the deductible to

preventive services, particularly at the 85% AV level. Table 1 displays the high level plan design features

and resulting AV of each of the four plans. The ‘Deductible’ and ‘MOOP’ rows show the deductible and

maximum out-of-pocket applicable to dental benefits only. The next four rows show the applicable

coinsurance to various broad service categories. The ‘Effective Coinsurance’ rows shows a weighted

average coinsurance across all four service categories for a nationwide average pediatric population.

The ‘Target AV’ row shows the actuarial value that we were targeting when selecting the benefit design.

The ‘Actual AV’ shows the actuarial value of the plan design we selected. The difference in target and

actual AV is a result of not selecting accurate but odd cost sharing features such as a deductible of

$148.50 on the ‘70% Plan 1’. These two rows show that our plan designs were actuarially equivalent to

the targeted plan actuarial values.

2 Detailed claims for a representative population under similar programs and circumstances were not available.

High quality and representative data will likely only become available when 2014 experience under the ACA

reforms becomes available.

Impact of Changing the Maximum Out-of-Pocket Amounts

August 26, 2013 Page 5

Table 1: Plan Designs

Plan 70% Plan 1 70% Plan 2 85% Plan 1 85% Plan 2

Deductible $150 $100 $0 $25

MOOP $700 $700 $700 $700

Class 1 Preventive and Diagnostic 0% 0% 0% 0%

Class 2 Basic 40% 50% 15% 10%

Class 3 Major 50% 60% 40% 40%

Medically Necessary Ortho 50% 70% 50% 40%

Effective Coinsurance 28% 36% 19% 15%

Target AV 70.0% 70.0% 85.0% 85.0%

Actual AV 70.5% 70.5% 84.9% 85.5%

For each plan, a $700 MOOP was used as the starting point. Wakely estimated the effect on the

actuarial value from changing the MOOP in $100 increments from $100 to $1,000. The deductible or

coinsurance was then adjusted to offset the impact of the MOOP change and to create a plan with an

actuarial value equal to the starting plan.

Table 2 below shows the changes in MOOP for the 70% Plan 1, the resulting actuarial value after the

MOOP changes, the change in cost sharing necessary to offset the actuarial value from the MOOP

change, and the final actuarial value after all cost sharing changes. The table shows every other MOOP

change (every $100) and the effective coinsurance over all service categories. In each table below, the

first row shows how the MOOP changes compared to the Original plan (MOOP of $700), the second row

lists out the revised MOOP (Original plus change shown in first row). The Actuarial Value with MOOP

changes shows what the actuarial value of the plan would be without any changes to other cost sharing

elements. The ‘Cost Impact with MOOP changes’ row shows the estimated change in plan cost due to

the change in MOOP compared to the original plan. The next row shows what changes to other cost

sharing elements were made (deductible and coinsurance). The effective coinsurance is the weighted

average cost sharing. The cost impact estimates what the net effect of the MOOP and cost sharing

changes are (targeting 0% but not always possible). The Additional Costs for Induced Demand estimates

the effect of the cost sharing changes on overall costs due to changes in utilization.

The full details are included in Appendix A.

Table 2: Impact of MOOP Changes for 70% Plan 1

MOOP MOOP MOOP Original MOOP MOOP MOOP MOOP MOOP MOOP

↑ 300 ↑ 200 ↑ 100 70% Plan ↓ 100 ↓ 200 ↓ 300 ↓ 400 ↓ 500 ↓ 600

Revised MOOP $1,000 $900 $800 $700 $600 $500 $400 $300 $200 $100

Actuarial Value with MOOP changes 68% 69% 70% 71% 72% 73% 75% 77% 81% 90%

Cost Impact with MOOP changes -4% -3% -1% 0% 2% 3% 6% 9% 16% 28%

Offsetting Benefit Change

Deductible $110 $120 $135 $150 $170 $195 $240 $300 $200 $100

Effective Coinsurance 28% 28% 28% 28% 28% 28% 28% 0% 0% 0%

Actuarial Value with Offsetting Changes 70% 71% 70% 71% 70% 71% 70% 73% 81% 90%

Cost Impact 0% 0% 0% 0% 0% 0% 0% 4% 15% 28%

Additional Costs for Induced Demand -1% -1% 0% 0% 0% 1% 2% 19% 22% 29%

Impact of Changing the Maximum Out-of-Pocket Amounts

August 26, 2013 Page 6

The table above shows that for each $100 increase in MOOP (starting at $700) the deductible needs to

be lowered by $10-15 to offset the increase in actuarial value. For every $100 reduction in MOOP, the

deductible has to be increased by $20-60 to keep the actuarial value constant. In the lower MOOP

values (such as MOOPs of $100-300), the deductible could not be raised high enough to achieve an

actuarial value similar to the original plan. In fact, for MOOPs below $400, the deductible had to be

reduced to match the MOOP. It does not make sense to have a MOOP greater than the deductible. Also,

the coinsurance level becomes irrelevant when deductible matches out-of-pocket maximum and so we

set it to 0% at lower MOOPs. Having a MOOP of $300 or less on dental will result in a significant increase

in cost for the SADP since the resulting AV is higher than the original. For example, a MOOP of $100 will

increase plan cost by 28% since the resulting AV of 90% is 28% higher than the original AV of 70%.

In addition to the cost impact due to higher AVs, induced demand is expected to increase costs further

at the lower MOOP levels, with costs increasing up to an additional 29% at the lowest MOOP level. For

example, in the scenario above where the MOOP and the deductible are both equal to $100, we expect

members to hit that MOOP during their first routine visit to the dentist. Beyond the first visit, the

members would not be required to pay anything out of pocket for dental services. From the plan’s

perspective, the only remaining checks and balances to reduce superfluous care would be any limits on

services such as a maximum of two annual routine dental checkups. Since these service limits do not

exist on all types of dental services, we believe a low cost sharing would induce additional demand for

dental services to increase plan costs by as much as 29% when the MOOP is $100 compared to a MOOP

of $700.

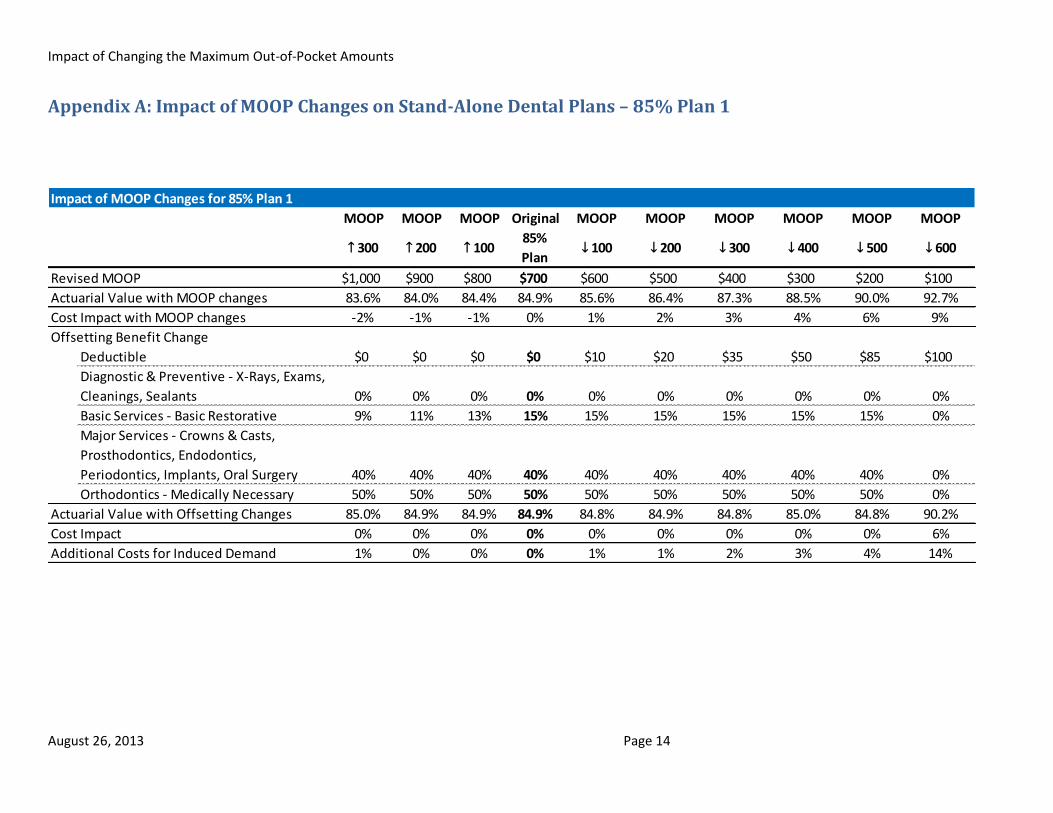

Table 3 below shows similar details as Table 2, but for the 85% Plan 1. The full details of all cost sharing

and changes are shown in Appendix A.

The first 85% actuarial value plan started with no deductible so the only cost sharing that could be

reduced to offset the rise in MOOP was coinsurance. The table above shows the changes in effective

coinsurance that were required to offset the MOOP increases3. When the MOOP was lowered, the

deductible was increased to keep the actuarial value constant. When the MOOP was lowered to $100,

even with the deductible at $100, the actuarial value was still 90%, which means that plan cost would

increase at that low of a MOOP level. Our calculations show that the cost impact would be 6% increase

3 At the higher MOOP levels, increases in MOOP do not change the actuarial value materially because the

continuance curves indicate very few people have costs in excess of the associated levels.

Table 3: Impact of MOOP Changes for 85% Plan 1

MOOP MOOP MOOP Original MOOP MOOP MOOP MOOP MOOP MOOP

↑ 300 ↑ 200 ↑ 100 85% Plan ↓ 100 ↓ 200 ↓ 300 ↓ 400 ↓ 500 ↓ 600

Revised MOOP $1,000 $900 $800 $700 $600 $500 $400 $300 $200 $100

Actuarial Value with MOOP changes 84% 84% 84% 85% 86% 86% 87% 88% 90% 93%

Cost Impact with MOOP changes -2% -1% -1% 0% 1% 2% 3% 4% 6% 9%

Offsetting Benefit Change

Deductible $0 $0 $0 $0 $10 $20 $35 $50 $85 $100

Effective Coinsurance 16% 17% 18% 19% 19% 19% 19% 19% 19% 0%

Actuarial Value with Offsetting Changes 85% 85% 85% 85% 85% 85% 85% 85% 85% 90%

Cost Impact 0% 0% 0% 0% 0% 0% 0% 0% 0% 6%

Additional Costs for Induced Demand 1% 0% 0% 0% 1% 1% 2% 3% 4% 14%

Impact of Changing the Maximum Out-of-Pocket Amounts

August 26, 2013 Page 7

in premiums for a MOOP of $100 compared to the original plan. Similar to the 70% Plan 1, induced

demand is expected to increase costs further at the lower MOOP levels, with costs increasing up to an

additional 14% at the lowest MOOP level.

Similar changes were made with the second 70% and 85% actuarial value plans. The summary results for

these plans are shown below in Tables 4 and 5. The full details of all example plans are shown in

Appendix A.

The above analysis shows that for most of the scenarios where MOOP was changed, no cost or premium

increases need to be made to offset these changes. The increases in actuarial value due to lower MOOP

can usually be offset by reducing other cost sharing such as deductibles and coinsurances. However,

there were several cases at the very extreme levels of MOOP where changes in premium would be

needed since it is not possible to keep the same AV as the base plan with reasonable cost sharing

changes. In addition to the higher AVs, many of the plans at lower MOOP levels may also see a

significant increase in cost due to induced demand.

The impact of induced demand is based on a combination of the Federal QHP induced demand factors,

the Towers Watson Dental pricing model, and actuarial judgment. Actual member behavior is difficult

to predict given that these plan designs are not in the market today and studying induced demand is

difficult because of confounding variables. In particular, the current dental products do not include

MOOPs but rather use annual benefit maximums. The induced demand factors should be used as a

general indication of how member behavior may change rather than a reliable prediction based on any

historical data. Wakely does expect that induced demand for dental will be more sensitive to cost

sharing levels than for medical services.

Table 4: Impact of MOOP Changes for 70% Plan 2

MOOP MOOP MOOP Original MOOP MOOP MOOP MOOP MOOP MOOP

↑ 300 ↑ 200 ↑ 100 70% Plan ↓ 100 ↓ 200 ↓ 300 ↓ 400 ↓ 500 ↓ 600

Revised MOOP $1,000 $900 $800 $700 $600 $500 $400 $300 $200 $100

Actuarial Value with MOOP changes 67% 68% 69% 71% 72% 73% 75% 78% 82% 90%

Cost Impact with MOOP changes -4% -3% -2% 0% 2% 4% 7% 11% 17% 28%

Offsetting Benefit Change

Deductible $48 $62 $80 $100 $125 $160 $220 $300 $200 $100

Effective Coinsurance 36% 36% 36% 36% 36% 36% 36% 0% 0% 0%

Actuarial Value with Offsetting Changes 70% 70% 71% 71% 71% 70% 70% 73% 81% 90%

Cost Impact 0% 0% 0% 0% 0% 0% 0% 4% 15% 28%

Additional Costs for Induced Demand -1% -1% 0% 0% 0% 1% 2% 19% 22% 28%

Table 5: Impact of MOOP Changes for 85% Plan 2

MOOP MOOP MOOP Original MOOP MOOP MOOP MOOP MOOP MOOP

↑ 300 ↑ 200 ↑ 100 85% Plan ↓ 100 ↓ 200 ↓ 300 ↓ 400 ↓ 500 ↓ 600

Revised MOOP $1,000 $900 $800 $700 $600 $500 $400 $300 $200 $100

Actuarial Value with MOOP changes 84% 85% 85% 85% 86% 87% 87% 88% 90% 92%

Cost Impact with MOOP changes -1% -1% 0% 0% 1% 1% 2% 3% 5% 8%

Offsetting Benefit Change

Deductible $10 $15 $20 $25 $30 $40 $50 $65 $90 $100

Effective Coinsurance 14% 14% 14% 14% 14% 14% 14% 14% 14% 0%

Actuarial Value with Offsetting Changes 86% 86% 85% 85% 86% 85% 85% 85% 85% 90%

Cost Impact 0% 0% 0% 0% 0% 0% 0% 0% 0% 6%

Additional Costs for Induced Demand -1% -1% 0% 0% 0% 1% 1% 2% 3% 11%

Impact of Changing the Maximum Out-of-Pocket Amounts

August 26, 2013 Page 8

Wakely also explored the potential impact of adverse selection on AVs and resulting plan designs

included in this analysis. Selection may exist in SADPs since it is not a requirement that the benefit must

be purchased for the pediatric population. Therefore it is possible that the SADPs will only be purchased

for children who are expected to incur higher than average dental costs. Adjusting the MOOPs for the

SADP may further impact selection. If there is significant selection, the result is that the AVs for the plan

designs used in this analysis would be higher than currently projected. This would require the starting

plan designs to be adjusted to provide less rich cost sharing. The remainder of the analysis in this

report, particularly the relationship of plan design and cost to MOOP changes, would remain largely the

same.

IV. Task 1b: Impact of MOOP on Qualified Health Plans

Wakely developed four sample plan designs to illustrate the impact of changing MOOP on actuarial

values and the offsetting plan design changes required to return the actuarial value to the original value.

A deductible plan at the Silver level (actuarial value of 70%)

An HDHP at the Silver level

A deductible plan at the Bronze level (actuarial value of 60%)

An HDHP at the Bronze level

The deductible plans are hybrid plans with copays on office visits and generic drugs, and

deductible/coinsurance on all other benefits. These plans are representative of popular plans in the

market place. However, mixing copays on some services and deductibles on others creates some issues

with actuarial value calculations in the Federal Actuarial Value Calculator4 and it is also difficult to

conceptualize the impact of changing the MOOP. Therefore, we included an HDHP plan at each metallic

level which contains a simpler plan design consisting of deductible and coinsurance on all services

(except preventive services as required by the ACA).

Table 6 below shows the plan designs selected for our analysis.

4 The Federal Actuarial Value Calculator does not always produce expected results. For example, an increase in the

deductible would be expected to lower the AV, all else equal. For deductible plans with higher deductible

amounts, the converse occurs.

Impact of Changing the Maximum Out-of-Pocket Amounts

August 26, 2013 Page 9

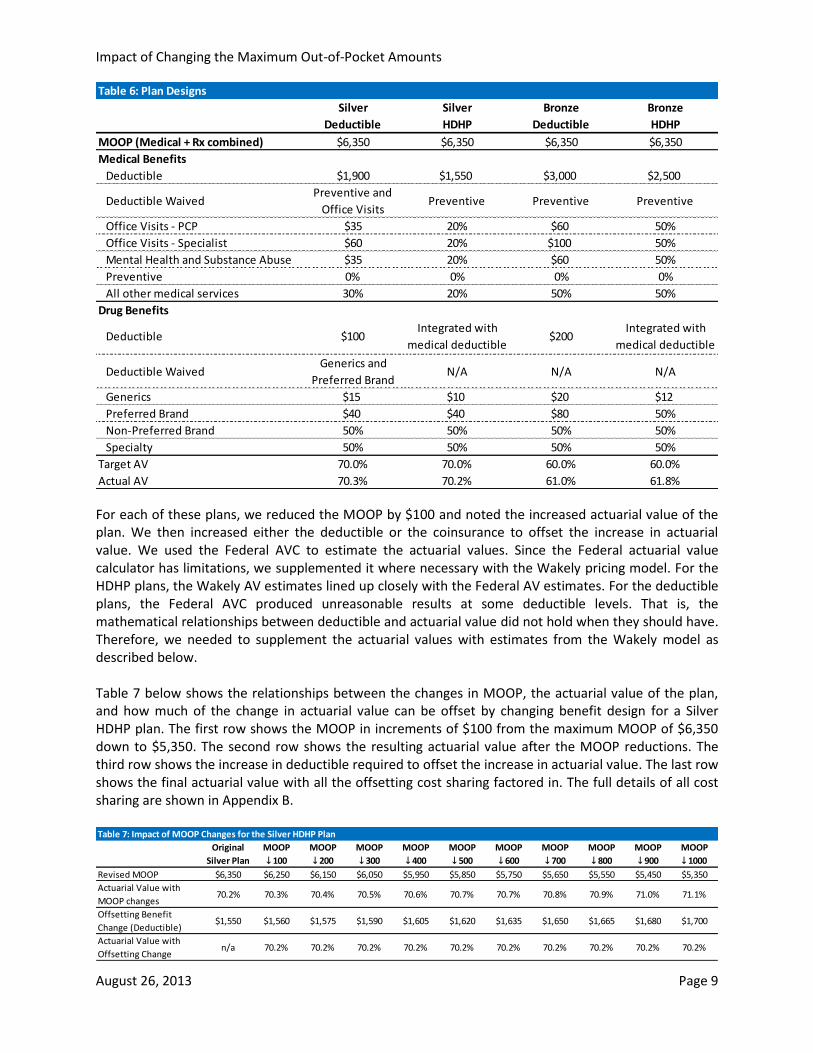

For each of these plans, we reduced the MOOP by $100 and noted the increased actuarial value of the plan. We then increased either the deductible or the coinsurance to offset the increase in actuarial value. We used the Federal AVC to estimate the actuarial values. Since the Federal actuarial value calculator has limitations, we supplemented it where necessary with the Wakely pricing model. For the HDHP plans, the Wakely AV estimates lined up closely with the Federal AV estimates. For the deductible plans, the Federal AVC produced unreasonable results at some deductible levels. That is, the mathematical relationships between deductible and actuarial value did not hold when they should have. Therefore, we needed to supplement the actuarial values with estimates from the Wakely model as described below. Table 7 below shows the relationships between the changes in MOOP, the actuarial value of the plan, and how much of the change in actuarial value can be offset by changing benefit design for a Silver HDHP plan. The first row shows the MOOP in increments of $100 from the maximum MOOP of $6,350 down to $5,350. The second row shows the resulting actuarial value after the MOOP reductions. The third row shows the increase in deductible required to offset the increase in actuarial value. The last row shows the final actuarial value with all the offsetting cost sharing factored in. The full details of all cost sharing are shown in Appendix B.

Table 6: Plan Designs

Silver Silver Bronze Bronze

Deductible HDHP Deductible HDHP

MOOP (Medical + Rx combined) $6,350 $6,350 $6,350 $6,350

Medical Benefits

Deductible $1,900 $1,550 $3,000 $2,500

Deductible WaivedPreventive and

Office VisitsPreventive Preventive Preventive

Office Visits - PCP $35 20% $60 50%

Office Visits - Specialist $60 20% $100 50%

Mental Health and Substance Abuse $35 20% $60 50%

Preventive 0% 0% 0% 0%

All other medical services 30% 20% 50% 50%

Drug Benefits

Deductible $100 Integrated with

medical deductible$200

Integrated with

medical deductible

Deductible WaivedGenerics and

Preferred BrandN/A N/A N/A

Generics $15 $10 $20 $12

Preferred Brand $40 $40 $80 50%

Non-Preferred Brand 50% 50% 50% 50%

Specialty 50% 50% 50% 50%

Target AV 70.0% 70.0% 60.0% 60.0%

Actual AV 70.3% 70.2% 61.0% 61.8%

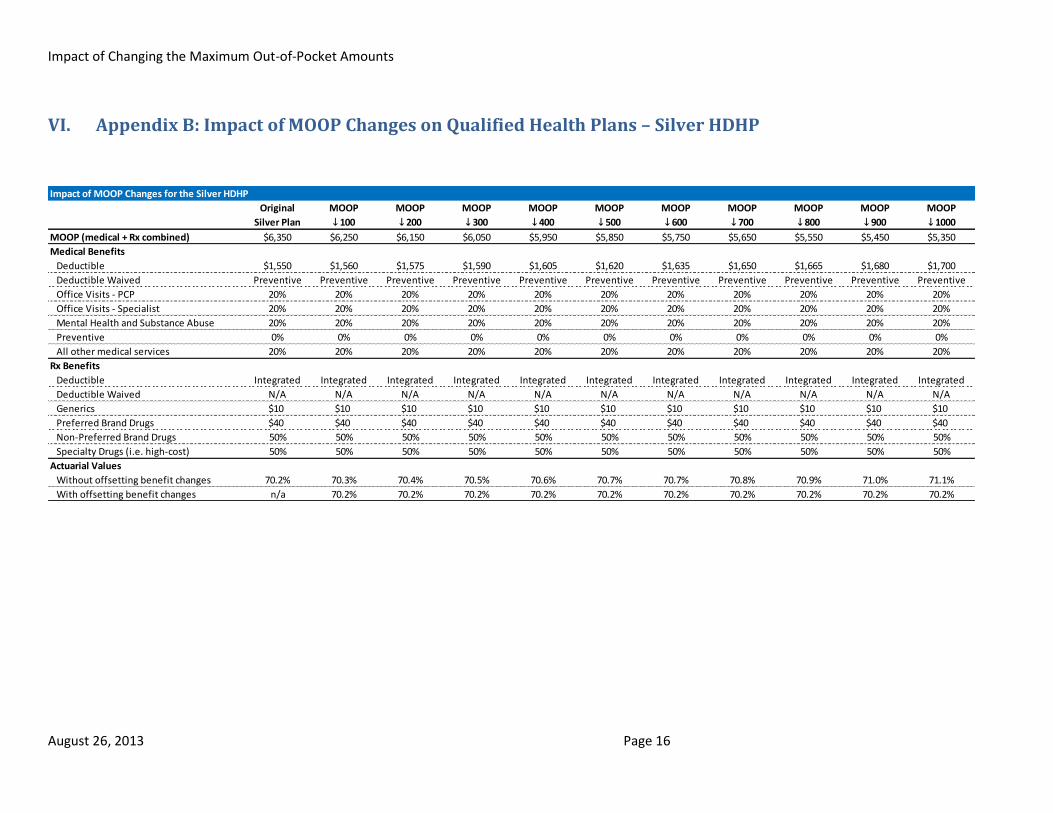

Table 7: Impact of MOOP Changes for the Silver HDHP Plan

Original MOOP MOOP MOOP MOOP MOOP MOOP MOOP MOOP MOOP MOOP

Silver Plan ↓ 100 ↓ 200 ↓ 300 ↓ 400 ↓ 500 ↓ 600 ↓ 700 ↓ 800 ↓ 900 ↓ 1000

Revised MOOP $6,350 $6,250 $6,150 $6,050 $5,950 $5,850 $5,750 $5,650 $5,550 $5,450 $5,350

Actuarial Value with

MOOP changes70.2% 70.3% 70.4% 70.5% 70.6% 70.7% 70.7% 70.8% 70.9% 71.0% 71.1%

Offsetting Benefit

Change (Deductible)$1,550 $1,560 $1,575 $1,590 $1,605 $1,620 $1,635 $1,650 $1,665 $1,680 $1,700

Actuarial Value with

Offsetting Changen/a 70.2% 70.2% 70.2% 70.2% 70.2% 70.2% 70.2% 70.2% 70.2% 70.2%

Impact of Changing the Maximum Out-of-Pocket Amounts

August 26, 2013 Page 10

The table above shows that for every $100 reduction in MOOP, the deductible needed to be increased

by $15-20 to fully offset the increase in actuarial value from reducing the MOOP. Since the MOOP

reductions can be fully offset by increasing the deductible, there is no cost impact for any of the MOOP

levels. Also, since the maximum change in AV is approximately 1%, it is not expected that there would

be a significant impact due to induced demand.

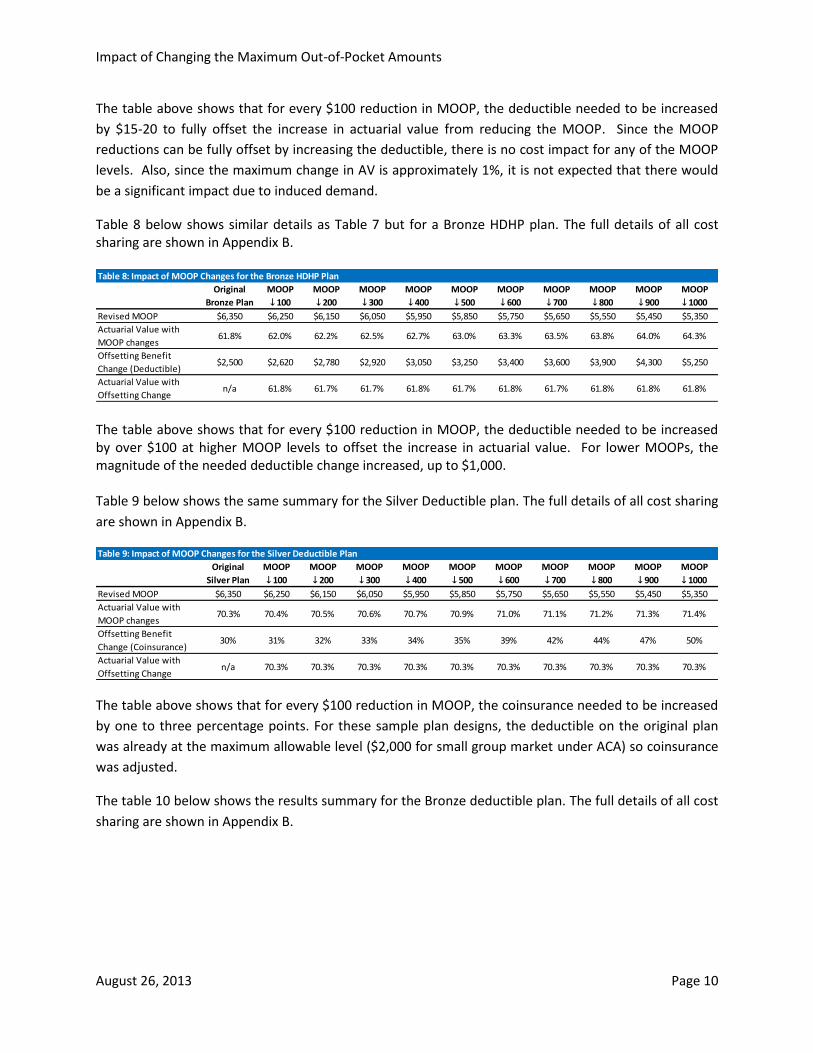

Table 8 below shows similar details as Table 7 but for a Bronze HDHP plan. The full details of all cost sharing are shown in Appendix B.

The table above shows that for every $100 reduction in MOOP, the deductible needed to be increased by over $100 at higher MOOP levels to offset the increase in actuarial value. For lower MOOPs, the magnitude of the needed deductible change increased, up to $1,000. Table 9 below shows the same summary for the Silver Deductible plan. The full details of all cost sharing

are shown in Appendix B.

The table above shows that for every $100 reduction in MOOP, the coinsurance needed to be increased

by one to three percentage points. For these sample plan designs, the deductible on the original plan

was already at the maximum allowable level ($2,000 for small group market under ACA) so coinsurance

was adjusted.

The table 10 below shows the results summary for the Bronze deductible plan. The full details of all cost

sharing are shown in Appendix B.

Table 8: Impact of MOOP Changes for the Bronze HDHP Plan

Original MOOP MOOP MOOP MOOP MOOP MOOP MOOP MOOP MOOP MOOP

Bronze Plan ↓ 100 ↓ 200 ↓ 300 ↓ 400 ↓ 500 ↓ 600 ↓ 700 ↓ 800 ↓ 900 ↓ 1000

Revised MOOP $6,350 $6,250 $6,150 $6,050 $5,950 $5,850 $5,750 $5,650 $5,550 $5,450 $5,350

Actuarial Value with

MOOP changes61.8% 62.0% 62.2% 62.5% 62.7% 63.0% 63.3% 63.5% 63.8% 64.0% 64.3%

Offsetting Benefit

Change (Deductible)$2,500 $2,620 $2,780 $2,920 $3,050 $3,250 $3,400 $3,600 $3,900 $4,300 $5,250

Actuarial Value with

Offsetting Changen/a 61.8% 61.7% 61.7% 61.8% 61.7% 61.8% 61.7% 61.8% 61.8% 61.8%

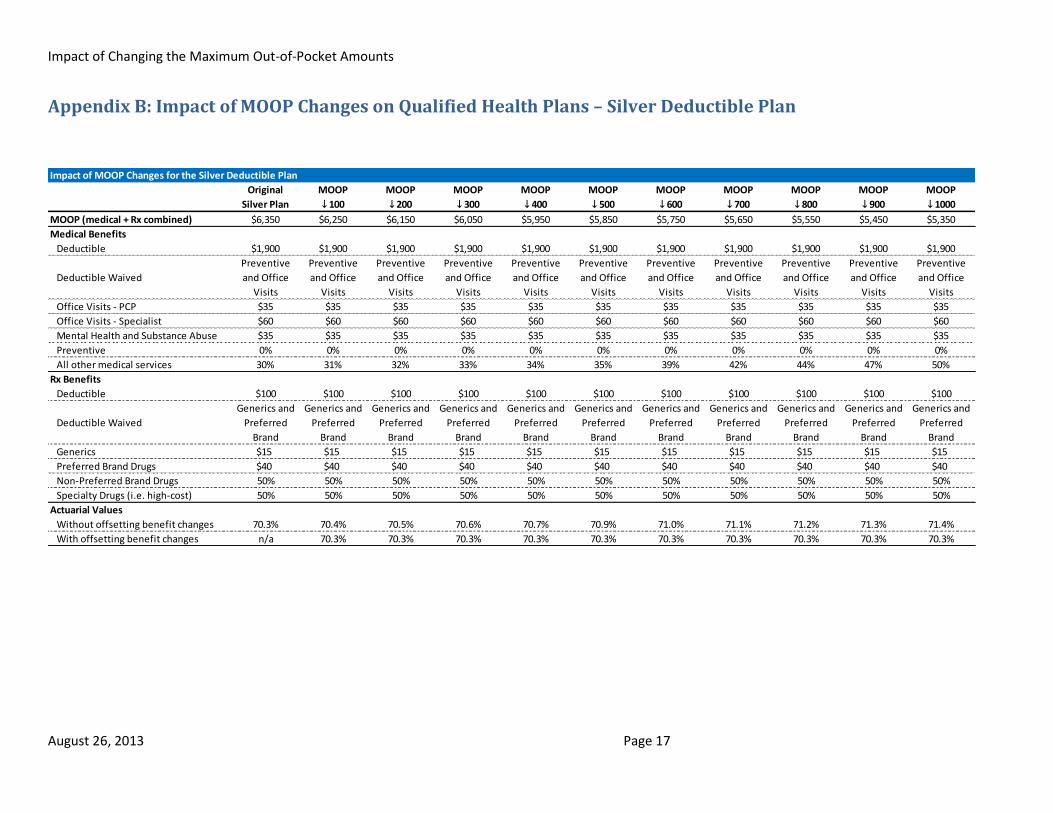

Table 9: Impact of MOOP Changes for the Silver Deductible Plan

Original MOOP MOOP MOOP MOOP MOOP MOOP MOOP MOOP MOOP MOOP

Silver Plan ↓ 100 ↓ 200 ↓ 300 ↓ 400 ↓ 500 ↓ 600 ↓ 700 ↓ 800 ↓ 900 ↓ 1000

Revised MOOP $6,350 $6,250 $6,150 $6,050 $5,950 $5,850 $5,750 $5,650 $5,550 $5,450 $5,350

Actuarial Value with

MOOP changes70.3% 70.4% 70.5% 70.6% 70.7% 70.9% 71.0% 71.1% 71.2% 71.3% 71.4%

Offsetting Benefit

Change (Coinsurance)30% 31% 32% 33% 34% 35% 39% 42% 44% 47% 50%

Actuarial Value with

Offsetting Changen/a 70.3% 70.3% 70.3% 70.3% 70.3% 70.3% 70.3% 70.3% 70.3% 70.3%

Impact of Changing the Maximum Out-of-Pocket Amounts

August 26, 2013 Page 11

The table above shows that for every $100 reduction in MOOP, the medical deductible needed to be

increased by around $200 up to a level of $4,000. After a deductible of $4,000, the Federal models

stopped producing reasonable values. Therefore, we increased the drug deductible using the Wakely

model. Please note that whenever the Federal AVC did not produce reasonable results the Wakely

pricing model was used to estimate the change in AV.

Conclusion

The above QHP analysis shows that for up to a $1,000 reduction in MOOP, plan design changes could be

made to maintain the original AV. Therefore, premium increases would not be necessary. For SADPs, a

modest reduction in MOOP can usually be made with reasonable changes to other cost sharing (cost

sharing is commonly found in the market and is less than 50% of the cost of the service). A large

decrease in the MOOP for SADPs will cause a significant increase in dental premium costs, driven by

both a higher AV and projected cost increases due to induced demand.

In the Task 2c analysis we reviewed existing literature on the role of cost sharing and premiums in

consumer purchasing decisions. We concluded that consumers are most sensitive to premiums and

least sensitive to MOOP when making purchasing decisions. Deductibles and copays/coinsurance were

of greater importance than MOOP in most consumers’ purchasing decisions. The fact that reductions in

MOOP on QHPs and some SADPs can be made without impacting premiums but increasing cost sharing

elements such as deductibles and coinsurances may affect consumers’ decision making process. From

the consumer perspective, the least important factor in their purchasing decision (the MOOP) has been

improved while the more important factors (premiums and deductibles/coinsurance) have worsened. It

is difficult to estimate the extent of the impact of MOOP reductions on enrollment given the limited

available research.

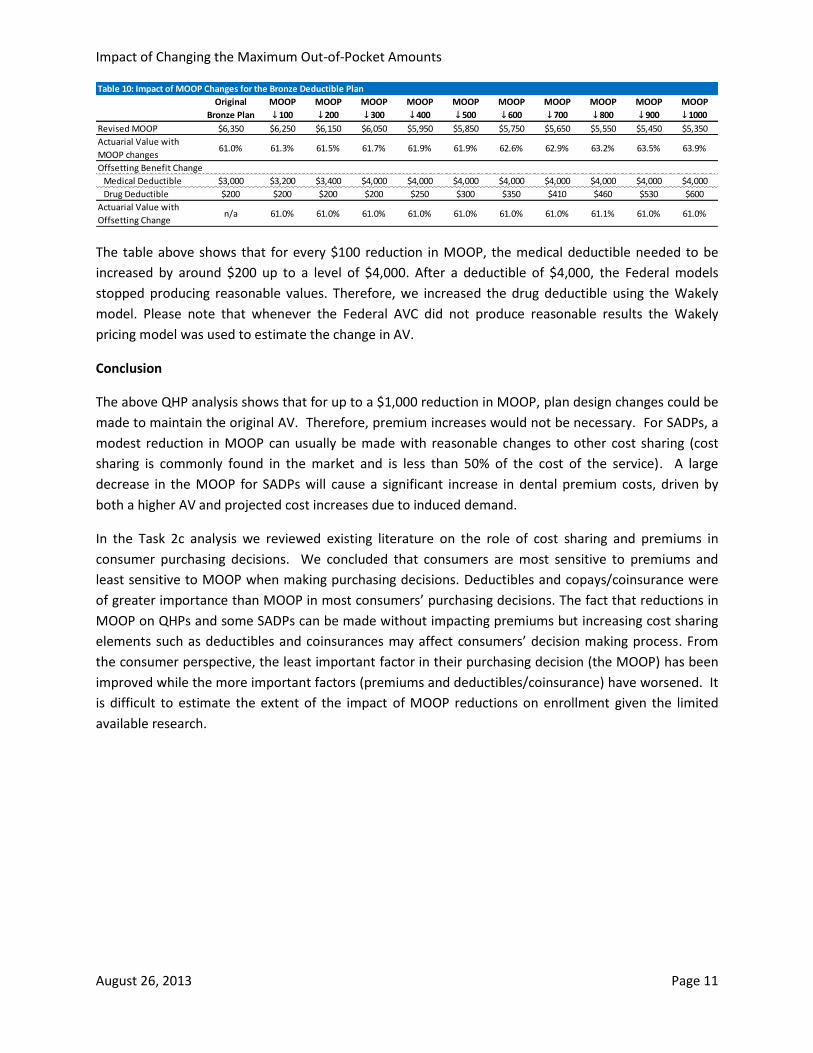

Table 10: Impact of MOOP Changes for the Bronze Deductible Plan

Original MOOP MOOP MOOP MOOP MOOP MOOP MOOP MOOP MOOP MOOP

Bronze Plan ↓ 100 ↓ 200 ↓ 300 ↓ 400 ↓ 500 ↓ 600 ↓ 700 ↓ 800 ↓ 900 ↓ 1000

Revised MOOP $6,350 $6,250 $6,150 $6,050 $5,950 $5,850 $5,750 $5,650 $5,550 $5,450 $5,350

Actuarial Value with

MOOP changes61.0% 61.3% 61.5% 61.7% 61.9% 61.9% 62.6% 62.9% 63.2% 63.5% 63.9%

Offsetting Benefit Change

Medical Deductible $3,000 $3,200 $3,400 $4,000 $4,000 $4,000 $4,000 $4,000 $4,000 $4,000 $4,000

Drug Deductible $200 $200 $200 $200 $250 $300 $350 $410 $460 $530 $600

Actuarial Value with

Offsetting Changen/a 61.0% 61.0% 61.0% 61.0% 61.0% 61.0% 61.0% 61.1% 61.0% 61.0%

Impact of Changing the Maximum Out-of-Pocket Amounts

August 26, 2013 Page 12

V. Appendix A: Impact of MOOP Changes on Stand-Alone Dental Plans – 70% Plan 1

Impact of MOOP Changes for 70% Plan 1

MOOP MOOP MOOP Original MOOP MOOP MOOP MOOP MOOP MOOP

↑ 300 ↑ 200 ↑ 10070%

Plan↓ 100 ↓ 200 ↓ 300 ↓ 400 ↓ 500 ↓ 600

Revised MOOP $1,000 $900 $800 $700 $600 $500 $400 $300 $200 $100

Actuarial Value with MOOP changes 67.9% 68.7% 69.5% 70.5% 71.6% 73.0% 74.6% 77.0% 81.5% 90.0%

Cost Impact with MOOP changes -4% -3% -1% 0% 2% 3% 6% 9% 16% 28%

Offsetting Benefit Change

Deductible $110 $120 $135 $150 $205 $220 $260 $300 $200 $100

Diagnostic & Preventive - X-Rays, Exams,

Cleanings, Sealants 0% 0% 0% 0% 0% 0% 0% 0% 0% 0%

Basic Services - Basic Restorative 40% 40% 40% 40% 40% 40% 40% 0% 0% 0%

Major Services - Crowns & Casts,

Prosthodontics, Endodontics,

Periodontics, Implants, Oral Surgery 50% 50% 50% 50% 50% 50% 50% 0% 0% 0%

Orthodontics - Medically Necessary 50% 50% 50% 50% 50% 50% 50% 0% 0% 0%

Actuarial Value with Offsetting Changes 70.5% 70.6% 70.5% 70.5% 70.5% 70.5% 70.5% 73.3% 80.9% 90.2%

Cost Impact 0% 0% 0% 0% 0% 0% 0% 4% 15% 28%

Additional Costs for Induced Demand -1% -1% 0% 0% 0% 1% 2% 19% 22% 29%

Impact of Changing the Maximum Out-of-Pocket Amounts

August 26, 2013 Page 13

Appendix A: Impact of MOOP Changes on Stand-Alone Dental Plans – 70% Plan 2

Impact of MOOP Changes for 70% Plan 2

MOOP MOOP MOOP Original MOOP MOOP MOOP MOOP MOOP MOOP

↑ 300 ↑ 200 ↑ 10070%

Plan↓ 100 ↓ 200 ↓ 300 ↓ 400 ↓ 500 ↓ 600

Revised MOOP $1,000 $900 $800 $700 $600 $500 $400 $300 $200 $100

Actuarial Value with MOOP changes 67.4% 68.4% 69.4% 70.5% 71.8% 73.4% 75.3% 78.0% 82.3% 90.2%

Cost Impact with MOOP changes -4% -3% -2% 0% 2% 4% 7% 11% 17% 28%

Offsetting Benefit Change

Deductible $48 $62 $80 $100 $125 $160 $220 $300 $200 $100

Diagnostic & Preventive - X-Rays, Exams,

Cleanings, Sealants 0% 0% 0% 0% 0% 0% 0% 0% 0% 0%

Basic Services - Basic Restorative 50% 50% 50% 50% 50% 50% 50% 0% 0% 0%

Major Services - Crowns & Casts,

Prosthodontics, Endodontics,

Periodontics, Implants, Oral Surgery 60% 60% 60% 60% 60% 60% 60% 0% 0% 0%

Orthodontics - Medically Necessary 70% 70% 70% 70% 70% 70% 70% 0% 0% 0%

Actuarial Value with Offsetting Changes 70.4% 70.5% 70.5% 70.5% 70.5% 70.4% 70.3% 73.3% 80.9% 90.2%

Cost Impact 0% 0% 0% 0% 0% 0% 0% 4% 15% 28%

Additional Costs for Induced Demand -1% -1% 0% 0% 0% 1% 2% 19% 22% 28%

Impact of Changing the Maximum Out-of-Pocket Amounts

August 26, 2013 Page 14

Appendix A: Impact of MOOP Changes on Stand-Alone Dental Plans – 85% Plan 1

Impact of MOOP Changes for 85% Plan 1

MOOP MOOP MOOP Original MOOP MOOP MOOP MOOP MOOP MOOP

↑ 300 ↑ 200 ↑ 10085%

Plan↓ 100 ↓ 200 ↓ 300 ↓ 400 ↓ 500 ↓ 600

Revised MOOP $1,000 $900 $800 $700 $600 $500 $400 $300 $200 $100

Actuarial Value with MOOP changes 83.6% 84.0% 84.4% 84.9% 85.6% 86.4% 87.3% 88.5% 90.0% 92.7%

Cost Impact with MOOP changes -2% -1% -1% 0% 1% 2% 3% 4% 6% 9%

Offsetting Benefit Change

Deductible $0 $0 $0 $0 $10 $20 $35 $50 $85 $100

Diagnostic & Preventive - X-Rays, Exams,

Cleanings, Sealants 0% 0% 0% 0% 0% 0% 0% 0% 0% 0%

Basic Services - Basic Restorative 9% 11% 13% 15% 15% 15% 15% 15% 15% 0%

Major Services - Crowns & Casts,

Prosthodontics, Endodontics,

Periodontics, Implants, Oral Surgery 40% 40% 40% 40% 40% 40% 40% 40% 40% 0%

Orthodontics - Medically Necessary 50% 50% 50% 50% 50% 50% 50% 50% 50% 0%

Actuarial Value with Offsetting Changes 85.0% 84.9% 84.9% 84.9% 84.8% 84.9% 84.8% 85.0% 84.8% 90.2%

Cost Impact 0% 0% 0% 0% 0% 0% 0% 0% 0% 6%

Additional Costs for Induced Demand 1% 0% 0% 0% 1% 1% 2% 3% 4% 14%

Impact of Changing the Maximum Out-of-Pocket Amounts

August 26, 2013 Page 15

Appendix A: Impact of MOOP Changes on Stand-Alone Dental Plans – 85% Plan 2

Impact of MOOP Changes for 85% Plan 2

MOOP MOOP MOOP Original MOOP MOOP MOOP MOOP MOOP MOOP

↑ 300 ↑ 200 ↑ 10085%

Plan↓ 100 ↓ 200 ↓ 300 ↓ 400 ↓ 500 ↓ 600

Revised MOOP $1,000 $900 $800 $700 $600 $500 $400 $300 $200 $100

Actuarial Value with MOOP changes 84.3% 84.7% 85.1% 85.5% 85.9% 86.5% 87.3% 88.3% 89.7% 92.1%

Cost Impact with MOOP changes -1% -1% 0% 0% 1% 1% 2% 3% 5% 8%

Offsetting Benefit Change

Deductible $10 $15 $20 $25 $30 $40 $50 $65 $90 $100

Diagnostic & Preventive - X-Rays, Exams,

Cleanings, Sealants 0% 0% 0% 0% 0% 0% 0% 0% 0% 0%

Basic Services - Basic Restorative 10% 10% 10% 10% 10% 10% 10% 10% 10% 0%

Major Services - Crowns & Casts,

Prosthodontics, Endodontics,

Periodontics, Implants, Oral Surgery 40% 40% 40% 40% 40% 40% 40% 40% 40% 0%

Orthodontics - Medically Necessary 40% 40% 40% 40% 40% 40% 40% 40% 40% 0%

Actuarial Value with Offsetting Changes 85.5% 85.5% 85.5% 85.5% 85.5% 85.4% 85.4% 85.4% 85.3% 90.2%

Cost Impact 0% 0% 0% 0% 0% 0% 0% 0% 0% 6%

Additional Costs for Induced Demand -1% -1% 0% 0% 0% 1% 1% 2% 3% 11%

Impact of Changing the Maximum Out-of-Pocket Amounts

August 26, 2013 Page 16

VI. Appendix B: Impact of MOOP Changes on Qualified Health Plans – Silver HDHP

Impact of MOOP Changes for the Silver HDHP

Original MOOP MOOP MOOP MOOP MOOP MOOP MOOP MOOP MOOP MOOP

Silver Plan ↓ 100 ↓ 200 ↓ 300 ↓ 400 ↓ 500 ↓ 600 ↓ 700 ↓ 800 ↓ 900 ↓ 1000

MOOP (medical + Rx combined) $6,350 $6,250 $6,150 $6,050 $5,950 $5,850 $5,750 $5,650 $5,550 $5,450 $5,350

Medical Benefits

Deductible $1,550 $1,560 $1,575 $1,590 $1,605 $1,620 $1,635 $1,650 $1,665 $1,680 $1,700

Deductible Waived Preventive Preventive Preventive Preventive Preventive Preventive Preventive Preventive Preventive Preventive Preventive

Office Visits - PCP 20% 20% 20% 20% 20% 20% 20% 20% 20% 20% 20%

Office Visits - Specialist 20% 20% 20% 20% 20% 20% 20% 20% 20% 20% 20%

Mental Health and Substance Abuse 20% 20% 20% 20% 20% 20% 20% 20% 20% 20% 20%

Preventive 0% 0% 0% 0% 0% 0% 0% 0% 0% 0% 0%

All other medical services 20% 20% 20% 20% 20% 20% 20% 20% 20% 20% 20%

Rx Benefits

Deductible Integrated Integrated Integrated Integrated Integrated Integrated Integrated Integrated Integrated Integrated Integrated

Deductible Waived N/A N/A N/A N/A N/A N/A N/A N/A N/A N/A N/A

Generics $10 $10 $10 $10 $10 $10 $10 $10 $10 $10 $10

Preferred Brand Drugs $40 $40 $40 $40 $40 $40 $40 $40 $40 $40 $40

Non-Preferred Brand Drugs 50% 50% 50% 50% 50% 50% 50% 50% 50% 50% 50%

Specialty Drugs (i.e. high-cost) 50% 50% 50% 50% 50% 50% 50% 50% 50% 50% 50%

Actuarial Values

Without offsetting benefit changes 70.2% 70.3% 70.4% 70.5% 70.6% 70.7% 70.7% 70.8% 70.9% 71.0% 71.1%

With offsetting benefit changes n/a 70.2% 70.2% 70.2% 70.2% 70.2% 70.2% 70.2% 70.2% 70.2% 70.2%

Impact of Changing the Maximum Out-of-Pocket Amounts

August 26, 2013 Page 17

Appendix B: Impact of MOOP Changes on Qualified Health Plans – Silver Deductible Plan

Impact of MOOP Changes for the Silver Deductible Plan

Original MOOP MOOP MOOP MOOP MOOP MOOP MOOP MOOP MOOP MOOP

Silver Plan ↓ 100 ↓ 200 ↓ 300 ↓ 400 ↓ 500 ↓ 600 ↓ 700 ↓ 800 ↓ 900 ↓ 1000

MOOP (medical + Rx combined) $6,350 $6,250 $6,150 $6,050 $5,950 $5,850 $5,750 $5,650 $5,550 $5,450 $5,350

Medical Benefits

Deductible $1,900 $1,900 $1,900 $1,900 $1,900 $1,900 $1,900 $1,900 $1,900 $1,900 $1,900

Deductible Waived

Preventive

and Office

Visits

Preventive

and Office

Visits

Preventive

and Office

Visits

Preventive

and Office

Visits

Preventive

and Office

Visits

Preventive

and Office

Visits

Preventive

and Office

Visits

Preventive

and Office

Visits

Preventive

and Office

Visits

Preventive

and Office

Visits

Preventive

and Office

Visits

Office Visits - PCP $35 $35 $35 $35 $35 $35 $35 $35 $35 $35 $35

Office Visits - Specialist $60 $60 $60 $60 $60 $60 $60 $60 $60 $60 $60

Mental Health and Substance Abuse $35 $35 $35 $35 $35 $35 $35 $35 $35 $35 $35

Preventive 0% 0% 0% 0% 0% 0% 0% 0% 0% 0% 0%

All other medical services 30% 31% 32% 33% 34% 35% 39% 42% 44% 47% 50%

Rx Benefits

Deductible $100 $100 $100 $100 $100 $100 $100 $100 $100 $100 $100

Deductible Waived

Generics and

Preferred

Brand

Generics and

Preferred

Brand

Generics and

Preferred

Brand

Generics and

Preferred

Brand

Generics and

Preferred

Brand

Generics and

Preferred

Brand

Generics and

Preferred

Brand

Generics and

Preferred

Brand

Generics and

Preferred

Brand

Generics and

Preferred

Brand

Generics and

Preferred

Brand

Generics $15 $15 $15 $15 $15 $15 $15 $15 $15 $15 $15

Preferred Brand Drugs $40 $40 $40 $40 $40 $40 $40 $40 $40 $40 $40

Non-Preferred Brand Drugs 50% 50% 50% 50% 50% 50% 50% 50% 50% 50% 50%

Specialty Drugs (i.e. high-cost) 50% 50% 50% 50% 50% 50% 50% 50% 50% 50% 50%

Actuarial Values

Without offsetting benefit changes 70.3% 70.4% 70.5% 70.6% 70.7% 70.9% 71.0% 71.1% 71.2% 71.3% 71.4%

With offsetting benefit changes n/a 70.3% 70.3% 70.3% 70.3% 70.3% 70.3% 70.3% 70.3% 70.3% 70.3%

Impact of Changing the Maximum Out-of-Pocket Amounts

August 26, 2013 Page 18

Appendix B: Impact of MOOP Changes on Qualified Health Plans – Bronze HDHP

Impact of MOOP Changes for the Bronze HDHP

Original MOOP MOOP MOOP MOOP MOOP MOOP MOOP MOOP MOOP MOOP

Bronze Plan ↓ 100 ↓ 200 ↓ 300 ↓ 400 ↓ 500 ↓ 600 ↓ 700 ↓ 800 ↓ 900 ↓ 1000

MOOP (Medical + Rx combined) $6,350 $6,250 $6,150 $6,050 $5,950 $5,850 $5,750 $5,650 $5,550 $5,450 $5,350

Medical Benefits

Deductible $2,500 $2,620 $2,780 $2,920 $3,050 $3,250 $3,400 $3,600 $3,900 $4,300 $5,250

Deductible Waived Preventive Preventive Preventive Preventive Preventive Preventive Preventive Preventive Preventive Preventive Preventive

Office Visits - PCP 50% 50% 50% 50% 50% 50% 50% 50% 50% 50% 50%

Office Visits - Specialist 50% 50% 50% 50% 50% 50% 50% 50% 50% 50% 50%

Mental Health and Substance Abuse 50% 50% 50% 50% 50% 50% 50% 50% 50% 50% 50%

Preventive 0% 0% 0% 0% 0% 0% 0% 0% 0% 0% 0%

All other medical services 50% 50% 50% 50% 50% 50% 50% 50% 50% 50% 50%

Rx Benefits

Deductible Integrated Integrated Integrated Integrated Integrated Integrated Integrated Integrated Integrated Integrated Integrated

Deductible Waived N/A N/A N/A N/A N/A N/A N/A N/A N/A N/A N/A

Generics $12 $12 $12 $12 $12 $12 $12 $12 $12 $12 $12

Preferred Brand Drugs 50% 50% 50% 50% 50% 50% 50% 50% 50% 50% 50%

Non-Preferred Brand Drugs 50% 50% 50% 50% 50% 50% 50% 50% 50% 50% 50%

Specialty Drugs (i.e. high-cost) 50% 50% 50% 50% 50% 50% 50% 50% 50% 50% 50%

Actuarial Values

Without offsetting benefit changes 61.8% 62.0% 62.2% 62.5% 62.7% 63.0% 63.3% 63.5% 63.8% 64.0% 64.3%

With offsetting benefit changes n/a 61.8% 61.7% 61.7% 61.8% 61.7% 61.8% 61.7% 61.8% 61.8% 61.8%

Impact of Changing the Maximum Out-of-Pocket Amounts

August 26, 2013 Page 19

Appendix B: Impact of MOOP Changes on Qualified Health Plans – Bronze Deductible Plan

Impact of MOOP Changes for the Bronze Deductible Plan

Original MOOP MOOP MOOP MOOP MOOP MOOP MOOP MOOP MOOP MOOP

Bronze Plan ↓ 100 ↓ 200 ↓ 300 ↓ 400 ↓ 500 ↓ 600 ↓ 700 ↓ 800 ↓ 900 ↓ 1000

MOOP (Medical + Rx combined) $6,350 $6,250 $6,150 $6,050 $5,950 $5,850 $5,750 $5,650 $5,550 $5,450 $5,350

Medical Benefits

Deductible $3,000 $3,200 $3,400 $4,000 $4,000 $4,000 $4,000 $4,000 $4,000 $4,000 $4,000

Deductible Waived Preventive Preventive Preventive Preventive Preventive Preventive Preventive Preventive Preventive Preventive Preventive

Office Visits - PCP $60 $60 $60 $60 $60 $60 $60 $60 $60 $60 $60

Office Visits - Specialist $100 $100 $100 $100 $100 $100 $100 $100 $100 $100 $100

Mental Health and Substance Abuse $60 $60 $60 $60 $60 $60 $60 $60 $60 $60 $60

Preventive 0% 0% 0% 0% 0% 0% 0% 0% 0% 0% 0%

All other medical services 50% 50% 50% 50% 50% 50% 50% 50% 50% 50% 50%

Rx Benefits

Deductible $200 $200 $200 $200 $250 $300 $350 $410 $460 $530 $600

Deductible Waived N/A N/A N/A N/A N/A N/A N/A N/A N/A N/A N/A

Generics $20 $20 $20 $20 $20 $20 $20 $20 $20 $20 $20

Preferred Brand Drugs $80 $80 $80 $80 $80 $80 $80 $80 $80 $80 $80

Non-Preferred Brand Drugs 50% 50% 50% 50% 50% 50% 50% 50% 50% 50% 50%

Specialty Drugs (i.e. high-cost) 50% 50% 50% 50% 50% 50% 50% 50% 50% 50% 50%

Actuarial Values

Without offsetting benefit changes 61.0% 61.3% 61.5% 61.7% 61.9% 61.9% 62.6% 62.9% 63.2% 63.5% 63.9%

With offsetting benefit changes n/a 61.0% 61.0% 61.0% 61.0% 61.0% 61.0% 61.0% 61.1% 61.0% 61.0%

![MOOP - Amazon Web Services · 36. SKOP X 50. Psyche 24. Tip top bus stop 1 55. Tankwa Chess 56. Ephemeropoly Y CLEAR MOOP [MATTER OUT OF PLACE]MAP 68. Step Sequencer 69. Shrine of](https://img.dokumen.tips/doc/110x75/5f7b7e053536e734f8565d4c/moop-amazon-web-services-36-skop-x-50-psyche-24-tip-top-bus-stop-1-55-tankwa.jpg)

![An Empirical Study on the Use and Misuse of Java 8 Streams · programming (MOOP) languages and platforms [5], including Scala [14], Java-Script [44], C# [33], F# [47], Java [39],](https://img.dokumen.tips/doc/110x75/5f09a9987e708231d427e9f7/an-empirical-study-on-the-use-and-misuse-of-java-8-streams-programming-moop-languages.jpg)