Embed Size (px)

Citation preview

IMPACT OF EUROPEAN UNION SUGAR SUBSIDIES ON THE

MANUFACTURING & AGRICULTURE SECTOR OF PAKISTAN

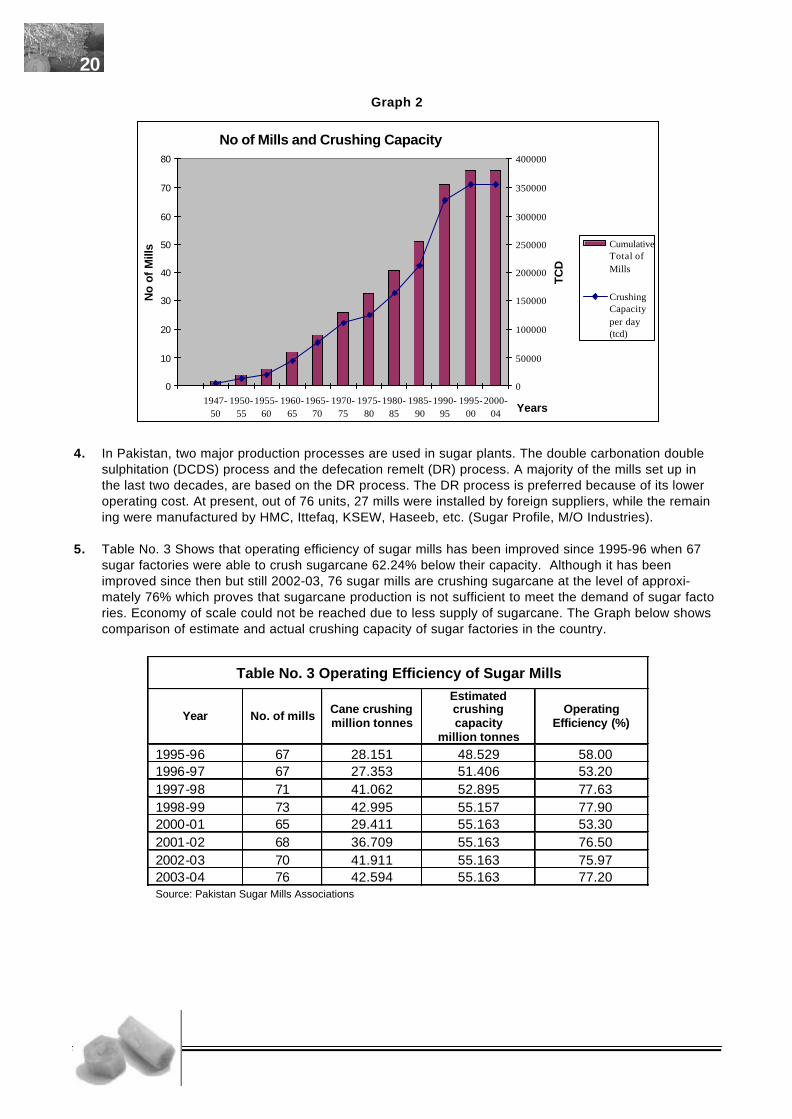

Many WWF projects in Pakistan focus on freshwater and toxics and require funding.For up-to-date information on funding requirements and for details onWWF’s Freshwater and Toxics Programme (FTP), please contact:

Hammad Naqi Khan: Director Freshwater and Toxics Programme, WWF - Pakistan

Coordinated & Reviewed: Dr. Nasir Mahmood Nasir, Freshwater and Toxics Programme, WWF - Pakistan

Conducted: Centre for Policy & Development Alternatives, Lahore - Pakistan

Cover Page Design: Communications Division WWF - Pakistan

Published April, 2005 by WWF - Pakistan, Ferozepure Road, Lahore - 54600, Pakistan

Opinions expressed in this publication do not necessarily reflect the views of WWF and its members.All written material in this report may be reprinted, provided the source is credited to WWF - Pakistan

IMPACT OF EUROPEAN UNION SUGARSUBSIDIES ON THE MANUFACTURING

AND AGRICULTURE SECTOR OF PAKISTAN

WWF - PAKISTAN

TABLE OF CONTENTS

Contents Page No.List of tables 3List of graphs 5List of annexes 7Acronyms 9Executive summary 11

Chapter No. 1: Introduction and Methodology 1. Introduction 151.2 Methodology 16

Chapter No. 2: Development of Sugar Sector 2.1 The Sugar Industry 182.2 Installed Capacity 192.3 Raw Material 222.4 Marketing of Sugarcane 252.5 By-Products of Sugar 26

Chapter No. 3: Domestic and World Balance Sheet of Sugar3.1 Domestic Demand and Supply Position 283.2 Recovery Level 283.3 Consumption of Sugar 303.4 Domestic Price Situation 323.5 Cost of Sugar Production 333.6 Excise and Other Taxes 353.7 Import Duties and Restrictions 353.8 World Supply, Demand, Stocks and Trade Positions 363.9 International Prices 37

Chapter No. 4: The International Sugar Policies4.1 EU's Sugar Policies 38 4.1.1 Export Subsidies 394.1.2 Market Access 404.1.3 Domestic Support 404.1.4 Special Safeguard Measures 404.1.5 Tariff Rate Quotas 414.1.6 Case Against EU Sugar Dumping 414.1.7 The DSB Decision 424.1.8 Possible EU Policy Reforms 434.1.9 Proposed Reforms of EU Sugar Sector (3 Scenarios) 434.2 USA Sugar Policies 444.3 Japanese Sugar Policies 454.4 Developing Countries' Sugar Policies 46

1

Chapter No. 5: EU Sugar Policies' Impact on Pakistan's Sugar Sector5.1 Impact of EU Reforms on Pakistan's Sugar Imports 475.2 Impact of EU Imported Sugar 565.3 Impact of EU on Export of Sugar 575.4 Impact of the DSB Decision on Pakistan's Sugar Export 57

Chapter No. 6: Sugar Sector's Impact on Environment6.1 Impact of Water Scarcity on Sugarcane and Environment 596.2 Soil Erosion, Agricultural Chemicals, Silt Run-off from Sugarcane Farms 606.3 Silt Run-off 616.4 Use of Pesticides 616.5 Use of Chemical Fertilisers 616.6 Suffocation 616.7 Burning of Sugarcane Fields 626.8 Mechanization in Sugarcane Cultivation 626.9 Impact of Sugarcane Processing Plants on Environment 62

Chapter 7: Recommendations for Sustainable Sugar Production in thePresent and Future Scenario 64

Bibliography 69

2

List of Tables

Title of Table Page No.

Table No. 1: Province-wise No. of Sugar Mills 18

Table No. 2: Crushing Capacity of Pakistan Sugar Mills 19

Table No. 3: Operating Efficiency of Sugar Mills 20

Table No. 4: Utilisation of Sugarcane and Production of Sugar 21

Table No. 5: Area, Production and Yield of Sugarcane 1990-91 to 2002-03 24

Table No. 6: Provincial Shares in Area and Production of Sugarcane Average of 2000-01 to 2002-03 25

Table No. 7: Domestic Balance Sheet of Sugar 28

Table No. 8: Sugar Production and Recovery Level 29

Table No. 9: Per Capita Consumption of Sugar 31

Table No. 10: Support Price of Sugarcane and Retail Price of Sugar 32

Table No. 11: Cost of Sugar Production Analysis 33

Table No. 12: Excise and Other Taxes on Sugar Industry 35

Table No. 13: Sugar Imports Duty Structure 36

Table No. 14: World Balance Sheet 36

Table No. 15: International Prices of Sugar 37

Table No. 16: Pakistan's Imports from the EU and the World 48

Table No. 17: Comparison of CIF of EU Imported Sugar and Domestic Market Prices 49

Table No. 18: Price Differential of Imported Sugar fromOther than EU Countries and Domestic Market Price. 50

Table No. 19: Ratio of Imports to Local Production and Consumption 51

Table No. 20: Revenue Loss to Sugar Sector in Pakistan 52

Table No. 21: Sugar Export to the World 52

Table No. 22: Ratio of Pakistan's Total Export to Local Production 53

Table No. 23: Comparison of Cost of Production with fob Prices 54

Table No. 24: Production, Consumption and Exportable Surplus 54

3

List of Graphs

Title of graph Page No.

Graph No. 1: Number of Sugar Mills in Pakistan 19

Graph No. 2: Number of Mills and Crushing Capacity 20

Graph No. 3: Comparison of Estimated and Actual Crushing of Sugar Mills 21

Graph No. 4: Sugarcane Production, Crushing and Sugar Production 22

Graph No. 5: Area of Sugarcane in Pakistan 22

Graph No. 6: Yield of Sugarcane in Pakistan 23

Graph No. 7: Production of Sugarcane in Pakistan 24

Graph No. 8: Provincial shares of Area under Sugarcane Cultivation 25

Graph No. 9: Sugarcane Production and Sucrose Recovery Level 29

Graph No. 10: Per Capita Consumption of Sugar 31

Graph No. 11: Support Prices of Sugarcane and Retail Prices of Sugar 32

Graph No. 12: International Prices of Sugar 37

Graph No. 13: Comparison of EU and World Cif Prices of Imported Sugar to Pakistan 48

Graph No. 14: Comparison of EU Cif Prices of Imported Sugar toPakistan Domestic Market Prices 49

Graph No. 15: Comparison of Other than EU Cif Prices andDomestic Market Prices of Sugar 50

Graph No. 16: Share of Imported Sugar in Domestic Production and Consumption 51

Graph No. 17: Difference between Cost of Production andFob Prices of Pakistan's Exported Sugar 54

Graph No. 18: Production, Consumption and Deficit/Surplus of Sugar 55

5

List of Annexes

Title of Annex Page No.

Annex No. 1: Area, Yield and Production of Sugarcane 1992-93 to 2002-03 71

Annex No. 2: Highly Protected Tariff Structure of Sugar Exporting Countries 72

Annex No. 3: Imports of Sugar in Pakistan 73

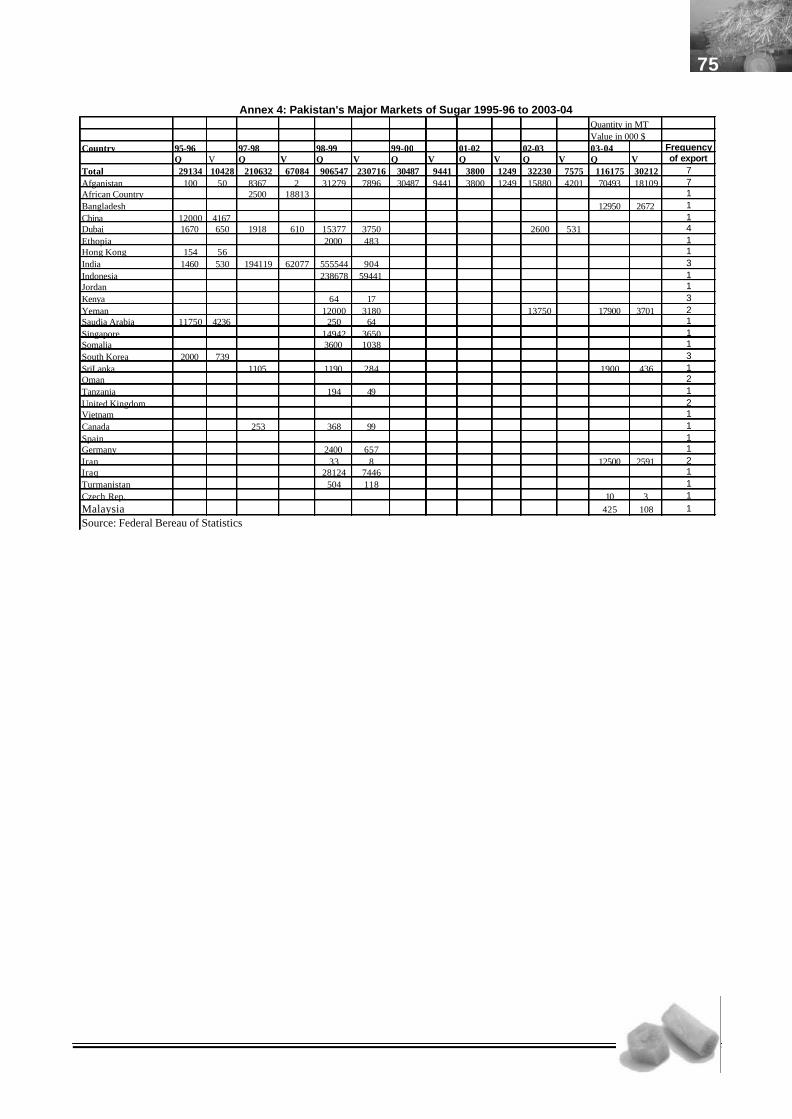

Annex No. 4: Pakistan's Major Markets of Sugar Export 1995-96 to 2003-04 75

Annex No. 5: Export of Sugar from Pakistan (fob price for different destination) 76

Annex No. 6: Leading Sugar Exporting Countries of the World 77

Annex No. 7: Questionnaires and agenda of consultative meeting 78

7

ACRONYM

ACP African Caribbean Pacific Countries AFTA Asian Free Trade AgreementAoA Agreement on AgricultureASEAN Association of South East Asian NationsCAP Common Agriculture PolicyCCC Commodity Cash CreditCMO Common Market OrganizationCPR Cash Price ReceiptDCDS Double Carbonation Double SulphitationDR Defecation RemeltDSB Dispute Settlement BodyEIA Environment Impact Assessment EU European Union FAOSTAT Food, Agriculture Organization StatisticsFBS Federal Bureau of Statistics GDP Gross Domestic ProductionHMC Heavy Mechanical Complex TexilaIMF International Monetary FundKSEW Karachi Shipyard Engineering WorksMFN Most Favored Nation TreatmentMT Metric Tonmt Million TonMINFAL Ministry of Food, Agriculture and LivestockNAFTA North America Free Trade AgreementNFA National Food, Authority of Philippines NWFP North West Frontier ProvincePSMA-SZ Pakistan Sugar Mills Association - Sindh ZonePSSI Pakistan Sustainable Sugar InitiativesSCM Subsidy and Countervailing MeasuresSRI Sugarcane Research InstitutesSTRV Short Term Raw ValueTCD Tonnes Crushed Per DayTCP Trading Corporation of PakistanTRQ Tariff Rate QuotasUSDA United States Department of AgricultureWTO World Trade OrganizationWWF World Wide Fund for Nature

9

EXECUTIVE SUMMARY

The study is divided into seven chapters including introduction and recommendations. In the first chapter,introduction and objectives of the study have been explained. Chapter 2 explains the details of developmentand progress of sugar sector in Pakistan. Sugar sector means establishment of sugar factories, supply andmarketing of raw material and production of by-products. Chapter 3 is about domestic and world balancesheet of sugar, cost of sugar production in Pakistan and analysis of domestic and international sugar prices.The objective of writing this chapter is to give a full picture of Pakistan's domestic sugar scenario so that itcould be understood that Pakistan's sugar industry is meeting the domestic sugar requirements and deficit orsurplus situations of sugar. Cost of production has been explained in view of checking feasibility of export ofsugar from Pakistan. In Chapter 4, sugar trade policies of developed and developing countries have beenexplained in detail. Recent decision of WTO's Dispute Settlement Body (DSB) has been explained. PossibleEU reforms have also been mentioned thoroughly. In Chapter 5, keeping in view one of the objectives of thestudy, impact of EU policy, DSB decision and possible EU reforms have been discussed. It has been ana-lyzed that Pakistan's sugar industry would be competitive in international sugar market and what would bethe impact of domestic sugar production and import in the country. It has been checked that production ofsugar in Pakistan viable or not. Chapter 6 explains the most important objective of the study in which impactof Pakistan's sugar sector performance on socio-economic and environmental issues have been analyzed.To realize the actual impact of sugar sector on these issues, a survey has been conducted and a consulta-tion meeting was held of all stake holders of sugar sector. Based on the findings of survey and consultationmeeting, the impact on socio-economic environmental issues of sugar sector has been assessed. In Chapter7, comprehensive recommendations have been made to overcome deficiencies of the sugar sector inPakistan. In the following paragraphs short summary of each chapter is stated.

Chapter One: Introduction and methodology

This study was conducted to understand and appraise the impact of European Union sugar policies onPakistan's sugar sector and to offer a differentiated overview as a basis for decisions affecting the develop-ment of sugar market-liberalization strategies in Pakistan.

As a result of WTO Dispute Settlement Body (DSB) decision and future restructuring of the EU sugarmarket, gradual liberalization in the world sugar market may take place and sugar producing and exportingcountries would likely to adjust their policies of domestic sugar production and international trade regime.This policy shift may have an impact on every country's economic, social and environmental sectors.

One of the objectives of the study was to assess not only the economic impacts but, above all, ramifica-tions in terms of human rights as well as social and ecological implications. A key aspect of this approachwas the involvement of the actors concerned, with a special emphasis on particularly vulnerable groups(landless, farm workers and other marginalised population groups).

WWF started Pakistan Sustainable Sugar Initiative (PSSI), with the ultimate aim of influencing sugarcanecultivation and processing practices at the appropriate levels (i.e. in the field, through influencing businessdecisions, via government policies). WWF also aims to encourage the sugar sector to reduce other adverseenvironmental impacts and to deliver more benefits to people.

Multiple methods were used to understand the environmental and economic impact of European Unionpolicies on the sugar sector of Pakistan. In order to incorporate manufacturers and sugarcane growers' pointof view on the said issues, a country wide survey was conducted. A meeting was also held at Lahore whereall the stakeholders of sugar sector were assembled. The purpose of that meeting was to get the final feedback of the growers, manufacturers and traders on various aspects of the research. Findings of the surveyresearch and consultation meeting are incorporated into different chapters of study.

Chapter Two: Development of Sugar Sector

This chapter contains the information about sugar mills such as, the number of mills, their crushing capacity and their location. In Pakistan, two major production processes are used in sugar plants. The double carbonation double sulphitation (DCDS) process and the defecation remelt (DR) process. The DR process is preferred because of its lower operating cost.

Among 105 sugarcane growing countries, Pakistan is the 5th largest country in the

11

world in terms of area under sugarcane cultivation, 11th by production and 60th in yield. Sugarcane is grownon about one million hectares. Sugarcane is a high delta crop and requires 80 to 90 acre inches of water inSindh and about 64 acre inches water in the Punjab. Water is too crucial to production and productivity ofsugarcane crop but is a scarce resource.

It is quite visible that there is an upward trend in area, production and yield apart from a rare decline infew years. In Pakistan yield is perhaps the lowest among all major sugarcane growing countries in the worldhowever, Pakistan has all the essential ingredients to produce high yield sugarcane.

Farmers normally sell their sugarcane directly to sugar mills but some contractor and middlemen havealso been involved in this business. Sugarcane is not a profitable crop, it hardly covers input cost but all thetime there is no other option.

Chapter Three: Domestic and World Balance Sheet of Sugar

In Pakistan, almost 99% sugar is extracted from sugarcane. Sugar production of the last three years onaverage gives an operational efficiency of about 80%, leaving 20% idle capacity. The sugar productioncapacity of these mills is above five million tons of sugar. The mills require about 65 million tons of sugar-cane to run on full capacity. Pakistan was a sugar importing country as demand outstripped supply for mostof the part of 1962 to 2000. However, situation has since changed. Country produced surplus sugar, whichhas created huge closing stocks from year 2000 to 2003. Sucrose recovery level in Pakistan is very lowbecause sugarcane takes about 4-5 days after harvesting to the point of mill gate. This leads not only toreduction in weight by about 2 percent but also affects recovery of sugar by 0.1 percent for each day in tran-sit. Mill inefficiency in juice extraction is another reason. Cane is also mixed with trash that affects the millefficiency.

International Sugar Organisation has forecast global production of sugar in 2003-04 at 146.99 milliontons, and consumption at 145.62 million tonnes. End year stocks are projected at 64.51 million tonnes.

The support price of sugarcane is the amount which farmer gets on delivery of the crop to the factorygates; higher support price encourages farmers to increase production. Support prices have increased in thepast three decades except for a decrease in 2003. The retail price of sugar has also increased in the pastthree decades. After 1985 world international prices remained between US$ 200 to 397 US$ / ton. The risingcost of production which was contrasted by plummeting prices of sugar proved awful, disastrous of sugarindustry.

Chapter Four: The International sugar policies

Protection is a major problem in sugar trade. The world sugar market has long been recognized as one ofthe most distorted global commodity markets. It is the disruptive policies of the European Union (EU), theUnited States (US) and Japan that cause most of these distortions. Policies offer very high rates of protec-tion to domestic producers by imposing severe import restrictions and by providing other measures such asexport subsidies or production quotas designed to help raise domestic prices above the world price. And it'son the rise and very damaging to exporters. The level of trade protection has risen in recent years as theworld price of sugar has fallen.

Chapter Five: EU Sugar Policies Reforms Impact on Pakistan's Sugar Sector

Pakistan regularly imports sugar from the world. The European Union is the major supplier of refined sugarto Pakistan, which captured 98% share in quantity and value during 1995-96. In 1996-97 its share declinedto 7.5%, after that it reached 34.4% in term of quantity and 39.5% in terms of value. Pakistan was successfulin finding other cheaper sources of supply. As a result of this shift, EU share in Pakistan's total importdeclined to 10% in term of quantity and 12.8% in term of value in 1999-00 and to the lowest point ever at4.9% in 2000-01. In 2001-02 the share of EU again increased to 7.7% in term of quantity and 8.6% in termof value. In the last 2 years EU dominated Pakistan sugar market and shared 61.8% to 66.8% in term ofquantity and 63.6 to 68.5% in term of value respectively.

Price differential i.e. gap between the cif prices including 10% incidental charges of imported sugar fromthe EU and Pakistan's domestic market prices is too wide which means imported sugar

12

could have been available in the local market at low price compared with domestic price of sugar. This sup-ports an argument that the domestic prices could have been higher in the absence of EU sugar. The EUsugar imports have played an important role in maintaining stability in domestic prices. Similarly price ofimported sugar particularly from other than EU countries were also low and price differential i.e. gap is alsosame as in case of imported sugar from EU. There will be an opportunity for sugar industry to produce sugarin a more efficient way and supply at low price than the border prices in the domestic market.

EU imported sugar is not replacing much of local production. The share of EU imported sugar inPakistan's total imports and domestic production and consumption in 1990s was approximately 30 % ofdomestic consumption. To restrict EU sugar dumping government should increase import duty and giveincentives to local producers so that they could produce at low cost and sell at cheap rates other wise thereis no way to restrict EU dumping.

The impact of EU reforms on Pakistan sugar sector depends on what reforms in the EU policy encom-passes and how the modalities of WTO new framework particularly on agreement on agriculture take shape.

Pakistan is a sporadic exporter of sugar, as it does not have surplus sugar every year. Since 1995-96 to2003-04, Pakistan has exported only a limited quantity of sugar to a few countries. This proves that Pakistanis in no competition with any major sugar exporting country even if there are major policy changes in the EU.Pakistan's fob price does not cover the cost of production and it is difficult to compete in the highly sub-sidised world trade regime. It is evident that fob prices are lower than the cost of production for three years.It is not sensible to export sugar below cost of production to protected market of other countries. Besides,buyers are not likely to import expensive sugar from Pakistan when much cheap sugar is available else-where. Pakistan sugar industry is not much efficient to produce sugar efficiently and to reduce the cost ofproduct through economy of scale by maintaining environmental standards.

Pakistan's sugar industry is not much hopefull with DSB decision. Pakistan's sugar industry would contin-ue to be affected adversely because of high in-put cost compared with other countries as they are producingsugar relatively at a lesser cost of production. Pakistan does not export sugar regularly because no subsidyis provided to exporters. The government is not helping the sugar sector of Pakistan to sort out this problem.

Viability and progress of sugar industry in Pakistan depend on regular supply of raw material at affordableprice. Due to limited supply of sugarcane and under utilization of existing crushing capacity, there is notmuch future for sugar industry. On strictly economic grounds sugar industry is not viable because there isnot enough sugarcane production nor is there any potential for increasing either the area under crop or theproductivity.

Chapter Six: Sugar Sector Impact on Environment

Sugarcane is a high delta crop and uses up to 9% of total fresh water. Practically in Pakistan it requires25/30 irrigation waters in a season. Due to water crises fresh water is not available for rural population, livingcreatures and wildlife. This has an environmental effect.

Due to scarcity of canal water major source of water is tube well. Drastic changes have been observed insoil composition because brackish water of tube well is not good for cultivation/soil. Sugarcane would remainshorter and thin due to the scarcity of water. As with monoculture, sugarcane cultivation is highly susceptibleto soil erosion through wind and water. Sugarcane crop prevents silt run-off. Use of pesticide in sugarcanearea is discouraged. Sugarcane crop almost never requires spray of pesticides hence impact of chemicalpoisoning and silt run-off is never observed but herbicides are used. Excessive water application blocks thesalinity while it may cause of water logging. Scientists reported that suffocation is never found in sugarcanefields. Pesticides spray produce suffocation for few minutes in the sugarcane crop. The fields in sugarcane-growing areas are burned off after harvesting. In mechanical cutting sugarcane is separated from the foliage,which in turn suffocates the sugarcane plants. Waste-water is mostly generated during the washing of sugar-cane contaminated with agrochemicals. Modern plants use closed water-circulation systems and have multi-stage waste-water treatment Plants.

It has been investigated through a survey that shortage of water has negative effect on soil and quality ofsugarcane crop. On the other hand, fresh water is also no more available for consumption of rural popula-tion, forest, wildlife and living creatures.

Chapter Seven: Recommendations

Sugar trade at world market prices below the cost of production is an important issue. The

13

EU dumping has depressed world prices and led to foreign exchange losses to the sugar exporting develop-ing countries. Sugar export market environment at global spectrum holds characteristic of extreme competi-tion in price. As a result, all the sugar-exporting countries invariably arrange subsidy for success in exports.Pakistan's sugar sector is suffering with dumping of EU sugar export and without domestic support subsidiesis unable to compete in the international market at the time of sugar surplus. It is true that government ofPakistan has neither extended similar support in sugar export nor protected sugar industry from dumpedimport from abroad. The dilemma of sugar industry is characterized as: sugar production not on a steadyupturn, cost of sugar production represented a rising trend, sugar industry's plight is attributable to high inci-dence of sugarcane price in cost of sugar production and high incidence of sales tax. Inconsistency domi-nates sugarcane crop cultivation and sugar production and trade. The sugarcane is the basic and only rawmaterial of producing sugar as sugar beet is not cultivated in Pakistan at large scale. The raw materialrequirement of sugar industry comprising 76 sugar mills, with crushing capacity of about 350 thousandtonnes per day can be met through expanding acreage under sugarcane. Monetary gains of sugarcane cropcan be achieved through enhancement in sugarcane yield. Sugarcane yield and sugar recovery of Pakistanhave not been up to mark. Australia obtains 5 tonnes of sugar per acre against 1.7 tonnes of Pakistan.Potential to improve sugar recovery to 10/11% by rich varieties of sugarcane also exists. Higher yield andrecovery on the given 1000 thousand hectares would impressively increase sugarcane and sugar productionvolume. A careful planning preceding each season on sugar production is sine-quo-non for smooth market-ing of sugarcane as well as sugar.

14

CHAPTER ONE: INTRODUCTION AND METHODOLOGY

1.1 Introduction

1. The World trade has been changed after the emergence of World Trade Organisation (WTO). New tradepolicies are profoundly affecting economic as well as political policies of the developed and developing countries. The traditional concept of sovereignty is no more applicable in the new situation. All sugar producing countries are trying to be competitive in the world market and to adjust their production and trade policies according to new WTO trade regime.

2. Pakistan's experience in industrialization is not unique and is consistent with the experience of the developing countries in the region. Public sector played a significant role in the beginning and later on the private sector received all the patronage from the State including high tariffs protection against imports, multiple exchange rates favoring the sugar industry, export bonus scheme and loans on concessional rates. Data on investment in the manufacturing sector during the 1950s is not available though it is assumed to be a small percentage of the GDP. It reached the maximum of 5% in the 1960sbut declined by the 1970s to 3.3%. It was mainly on account of public sector investment in various industries including sugar, Fertiliser and engineering that in man ufacturing appeared strong. The 1980ssaw the lifting of price control from almost all the products including sugar, liberalization of foreign exchange and withdrawal of sub sidies and tariff protection including tax holidays etc.

3. After the emergence of WTO the sugar industry of Pakistan with the process of globalization has to stand on its own feet. WTO rules do not provide the process of protection to an inefficient industry. Comparative advantage will determine the survival of an industry. As a result of WTO Dispute Settlement Body (DSB) decision and future restructuring of the EU sugar market, gradual liberalization in the world sugar market may take place and sugar producing and exporting countries would likely to adjust their policies of domestic sugar production and international trade regime. This policy shift may have an impact on every country's economic, social and environmental sectors.

4. This study has been conducted to understand and appraise the impact of European Union sugar poli-cies on Pakistan's sugar sector and to offer a differentiated overview as a basis for decisions affecting the development of sugar market-liberalization strategies in Pakistan.

5. Concern about externalities is no more confined to the developed world. People of the developing worldequally suffer from environmental hazards due to the development efforts. One of the objectives of this study is to investigate the nature of environmental problems being created by sugar sector and to ana-lyze the economic, social and ecological consequences of liberalized market access for Pakistan's sugar sector.

6. A range of international and bilateral trade policies influence the profitability of the Pakistan sugar indus-try. WTO rules, domestic support for sugar producers as well as export subsidies and overall trade polices of the US, European Union and Japan all influence the world price of sugar and the opportunitiesfor Pakistan to sell its sugar globally. These factors in turn play a role in determining the economic sus-tainability of the Pakistan sugar industry and the environmental impacts of sugar sector in the country. Understanding the impacts of current global sugar policies and likely future reforms on the Pakistan envi-ronment is one component of the approach which World Wildlife Fund is taking to improve the environ-mental performance of the industry.

7. WWF recently started Pakistan Sustainable Sugar Initiative (PSSI), with the ultimate aim of influencing sugarcane cultivation and processing practices at the appropriate levels (i.e. in the field, through influ-encing business decisions, via government poli cies).

8. In a preparatory phase of the PSSI, six sugarcane studies were conducted to identify the issues regard-ing socio-economic and environmental impacts of sugarcane cultivation and processing and themarketing policy issues relating to the sustainable development of sugarcane and sugar in Pakistan. The development of these reports involved all the sugar stakeholders.

15

9. Many of the current sugar growing and processing practices in Pakistan may result in a range of envi-ronmental impacts, including agrochemical runoff, silt runoff, nutrient leaching from the fields, salinity and water logging problems. The effects include damage to ecosystems via chemical poisoning and ecosystem smothering due to the volume of silt running off from the farms. Additional impacts on the environment include habitat loss due to expansion of farm in order to acquire land for sugarcane cultiva-tion, threats to species bio diversity and wider energy-related uses. This study has tried to investigate any of these effects on Pakistan's environment.

10. The world is facing a water crisis and agriculture is by far the biggest user of water; 70% of world's freshwater withdrawals are for agriculture, rising to more than 90% in Pakistan. Land-use changes brought about by farming, whether irrigated or rain fed, influence the quantity, quality and distribution of water that is collected, stored and released into the environment. Without a natural hydrological bal-ance, rivers which flow all year round become seasonal or diverted, lakes and wetland dry up, pollutantsin the water become more concentrated and salt water may seep in to replace abstracted fresh water turning farmland into infertile wastelands. This water crisis may have long lasting effects on environmentof Pakistan.

11. There is a limit to the amount of water available in Pakistan's Indus Basin. Only about 30 per cent of thewater reaches the crop roots. Poor management practices both on sugarcane farms and sugar industry underlie the poor state of affairs. Pakistan's soils have several deficiencies which make it difficult to move from subsistence to high yields of sugarcane. One issue is organic matter deficiency. Inadequate cultural practices, such as poor seed bed preparation in clay soils, broadcast sowing, improper Fertiliserapplication, and watering by turns rather than on crop demand contribute to the low yields. However, themost serious constraints are neither physical nor technical but sociological. Absentee landlordism, iniq-uitous tenancy rights, fragmentation of landholding and poor help from the State have combine to produce an inefficient low yield sugarcane crop. Better Management Practices can reduce the impacts of sugar cane farming and processing on water quantity, water quality, ecosystems, species and ecosys-tem function as well as to provide better access to other water users in the catchments or basins.

12. "WWF aims to enable the sugar sector to use less water and to ensure that water saved from better practices delivers more benefits to people and nature. WWF also aims to encourage the sugar sector toreduce other adverse environmental impacts".

13. One of the objectives of the study is to assess not only the economic impacts but above all, ramifications in terms of human rights as well as social and ecological implications. A key aspect of this approach is the involvement of the actors concerned, with a special emphasis on particularly vulnerable groups (landless, farm workers and other marginalised population groups).

14. The structure in this sector of Pakistan's economy is complex. Sugar production has been one of the most important economic undertakings since independence. Key political measures to provide incentive as political bribe and growing domestic consumer markets, have brought far-reaching changes in sugar sector of Pakistan.

15. The study starts by looking at the way in which sugarcane cultivation, that is to say sugar production, have evolved and how they are structured today. It also includes a survey of the latest economic devel-opments in all key areas of cultivation such as Punjab and Sindh which has been targeted by sugar fac-tories.

1.2 Methodology

16. Multiple methods have been employed to understand the environmental and economic impacts of European Union policies on the sugar sector of Pakistan. In order to incorporate manufacturers and sugarcane growers' point of view on the said issues, a country wide survey was conducted and detailedquestionnaires were designed for all stakeholders of the sugar sector. Another questionnaire was also designed for an envi ronmental specialist to know his position on the issue. Sugar traders were not left

16

designed for an envi ronmental specialist to know his position on the issue. Sugar traders were not left out from this process. At the second stage, as per requirement of the research design, growers and crushers from Punjab, Sindh and NWFP were interviewed in order to collect primary data. From the totalof five growers, two growers were approached in Punjab, two in Sindh and one in NWFP. Similarly, one manufacturer was interviewed from each of the three provinces. Two traders, one from Lahore and one from Karachi were interviewed to apprise the trading side of the matter. It was considered useful to dis-cuss the issue with a scientist to assess the impact of sugar production and cultivation process on environment.

17. In addition to the data collected from surveys, discussions with representatives of companies, trade unions, social movements, non-governmental organisations and research institutes were held. Account must be taken of the fact that the data obtained from different sources does not always tally. Parallel to this field research, theoretical side of the matter was also thrashed out.

18. Finally, a meeting was held at Lahore where all stakeholders of sugar sector were assembled under oneroof to share the finding of theoretical and field research. The purpose of that meeting was to get the final feed back of the growers, manufacturers and traders on various aspects of the research to make it more rigorous and comprehensive. In order to make the research study more accurate and comprehen-sive, findings of the survey research and consultation meeting have been incorporated into different chapters of the study. In chapter seven comprehensive recommendations have been presented to over-come the deficiencies of the sugar sector.

17

CHAPTER TWO: DEVELOPMENT OF SUGAR SECTOR

2.1 The Sugar Industry

1. At the time of Independence in 1947, the country had two sugar mills built in 1936-38, one in NWFP and one in Punjab, each crushing 300-400 tonnes of cane a day. Since then, the sugar industry has emerged as a major processing industry. In the early 50s, three more sugar mills were established. In the meantime, the area under sugarcane increased almost by 100% and reached 397 thousand hectares in 1959-60. The addition of 13 more units in next ten years further expanded the sugarcane cultivation to 620 thousand hectares in 1969-70. Thereafter, 14 more mills were installed up to 1981-82. Simultaneously, the cultivation of sugarcane expanded reaching 947 thousand hectares. Sugar-manufacturing capacity grew rapidly during the 1980s, when liberal sanctioning and credit regimes, coupled with a generally pro-business policy environment, helped to create conditions conducive for private investment in the industry. Major growth in capacities was witnessed in late 80's and early 90's, when industrial sector was fully opened for private investment. During 2003-04, 76 sugar mills were in operation having a crushing capacity of 350,000 tonnes a day. Consequently, about 77 per cent of the total cane produced in the country was crushed for manufacturing white sugar producing 3.9 million tonnes of sugar. Area of sugarcane expanded to more than 1.2 million hectares producing 55 million tonnes of sugarcane. Table below shows the progress of sugar industry in the 1990s.

2. The above table represents the rise in sugar mills since 1990-91 to 2003-04. It indicates that the num-ber of sugar mills increased by 50% over the period. During the period of 1996-97, the number increased to 69. It was at the maximum level that is 73 in the year 1998-99. Then there was a declining trend in the next four years as the number of mills was reduced to 69. After that, there is also an upwardtrend as the number reached 76 in the year 2003-04. Sugar industry is supposed to play an enhanced role of being a catalyst in growth and development of the national economy. By virtue of its being whollyagro-based-cum-rural- in totality, as each sugar mills is designated to remain in the deep rural landmass. Sugar industry is also bound to play a greater role in socioeconomic upswing of the rural sector and contribute further in accelerating development of Pakistan. The Graph below shows progressive growth of sugar factories in the country.

Table 1: Province-wise No. of Sugar Mills

Year Punjab Sindh NWFP Pakistan 1990-91 24 22 5 51 1991-92 25 22 5 52 1992-93 32 24 5 61 1993-94 33 24 6 63 1994-95 36 24 6 66 1995-96 37 24 6 67 1996-97 37 27 5 69 1997-98 39 28 5 72 1998-99 39 29 5 73 1999-00 37 25 5 67 2000-01 35 25 5 65 2001-02 37 27 5 69 2002-03 38 28 5 71 2003-04 39 31 6 76

Source: Annual Report 2003 Pakistan Sugar mills Association Sindh Zone

18

Graph 1

2.2 Installed Capacity

3. Table 2 represents the crushing capacity of Pakistan sugar mills. In 1947, it was 5020 tonnes crushing per day (tcd) for two mills. It rose slowly and reached 18,220 (tcd) from six mills during 1955-60. Then there is a rapid rise. During 1960-65 it was 44,050 (tcd) from twelve mills. In the years 1970-75, it reached the level of 109,350 (tcd). It continued to rise and reached 211,850 (tcd) from 51 mills in 1985-90. During the years 1990 to 2000, it reached its maximum level of 355,150 (tcd) from a total of 76 mills.The total estimated crushing capacity of 76 sugar mills is 5.3 million tonnes per annum. This has been worked out on the basis of 150 operating days. Out of the 76 mills, 39 mills have capacity of 171,000 (tcd) are located in Punjab, 31 with capacity of 154,600 (tcd) in the Sindh and 6 with capacity of 29,500 (tcd) in NWFP. Out of present 76 units, 25 units have the capacity ranging between 6000-9000 tcd, 29 units between 4000-6000 and 22 units have capacities under 4000 tcd (Sugar Profile, M/O Industries). The Graph below also shows progressive growth of crushing capacity sugar factories in the country.

Table 2: Crushing Capacity of Pakistan Sugar Mills

Years No. of Mills Installed

Cumulative Total of Mills

Crushing Capacity per day (tcd)

1947-50 2 2 5,020 1950-55 2 4 12,020

1955-60 2 6 18,220

1960-65 6 12 44,050 1965-70 6 18 76,550

1970-75 8 26 109,350 1975-80 7 33 125,950

1980-85 8 41 164,850 1985-90 10 51 211,850

1990-95 20 71 326,650

1995-00 5 76 355,150 2000-04 0 76 355,150

Source: Sugar Profile, Expert Advisory cell M/O Industries

0

10

20

30

40

50

60

70

80

1990-91

1991-92

1992-93

1993-94

1994-95

1995-96

1996-97

1997-98

1998-99

1999-00

2000-01

2001-02

2002-03

2003-04

Years

No

of M

ills NWFP

Sindh

Punjab

Pakistan

19

Graph 2

4. In Pakistan, two major production processes are used in sugar plants. The double carbonation double sulphitation (DCDS) process and the defecation remelt (DR) process. A majority of the mills set up in the last two decades, are based on the DR process. The DR process is preferred because of its lower operating cost. At present, out of 76 units, 27 mills were installed by foreign suppliers, while the remaining were manufactured by HMC, Ittefaq, KSEW, Haseeb, etc. (Sugar Profile, M/O Industries).

5. Table No. 3 Shows that operating efficiency of sugar mills has been improved since 1995-96 when 67 sugar factories were able to crush sugarcane 62.24% below their capacity. Although it has been improved since then but still 2002-03, 76 sugar mills are crushing sugarcane at the level of approxi-mately 76% which proves that sugarcane production is not sufficient to meet the demand of sugar factories. Economy of scale could not be reached due to less supply of sugarcane. The Graph below shows comparison of estimate and actual crushing capacity of sugar factories in the country.

No of Mills and Crushing Capacity

0

10

20

30

40

50

60

70

80

1947-50

1950-55

1955-60

1960-65

1965-70

1970-75

1975-80

1980-85

1985-90

1990-95

1995-00

2000-04 Years

No

of M

ills

0

50000

100000

150000

200000

250000

300000

350000

400000

TCD

CumulativeTotal ofMills

CrushingCapacityper day(tcd)

Table No. 3 Operating Efficiency of Sugar Mills

Year No. of mills Cane crushing million tonnes

Estimated crushing capacity

million tonnes

Operating Efficiency (%)

1995-96 67 28.151 48.529 58.00 1996-97 67 27.353 51.406 53.20 1997-98 71 41.062 52.895 77.63 1998-99 73 42.995 55.157 77.90 2000-01 65 29.411 55.163 53.30 2001-02 68 36.709 55.163 76.50 2002-03 70 41.911 55.163 75.97 2003-04 76 42.594 55.163 77.20 Source: Pakistan Sugar Mills Associations

20

Graph 3

6. Table 4 indicates the production and cane crushed by the sugar mills since 1993-94 to 2003-04. According to the table, production of sugarcane increased from 44 millions tonnes to 55 million tonnes till 1998-99 while the cane crushing increased from 34 million tonnes to 43 million tonnes. The increasefrom 76.93% to 77.9% is only marginal during six years from 1993-94 to 1998-99. The quantity of sugar produced increased from 2.901 million tonnes to 3.531 million tonnes in the same six years. However, recovery rate has decreased from 8.48% to 8.21% during the same time period. During the next three years from 1998-99 to 2001-02 production of sugarcane decreased from 55.2 millions tonnes to 48.0 million tonnes while cane crushing has decreased from 43 million tonnes to 36 million tonnes. After that Sugarcane production reached 52.6 million tonnes and cane crushed to 42.6 million tonnes. Sugar production increased to 3.6 million tonnes. The graph interprets the table number 4 and proves that mills have not fully utilized whole production of sugarcane and maximum sugar was produced in 1998-99.

Comparison of Estimated and Actual Crushing of Sugar Mills

0

48.529

51.406

52.895

55.157

55.163

55.163

55.163

28.151

27.353

41.062

42.995

29.411

36.709

41.911

1995-96

1996-97

1997-98

1998-99

2000-01

2001-02

2002-03

Yea

rs

Crushing of Sugarcane

Cane crushing million tons Estimated crushing capacity

Table No. 4 Utilisation of Sugarcane and Production of Sugar

Year No. of mills Production Million Tonnes

Cane crushed Million Tonnes

Percentage crushed

Sugar produced Million Tonnes

Recovery Rate %

1993-94 63 44.427 34.182 76.93 2.901 8.48 1994-95 66 47.168 34.194 75.49 2.983 8.72 1995-96 67 45.230 28.151 62.24 2.450 8.7 1996-97 67 42.000 27.353 64.65 2.379 8.86 1997-98 71 53.104 41.062 77.29 3.549 8.64 1998-99 73 55.191 43.000 77.9 3.542 8.21 1999-00 67 46.697 29.000 62.07 2.429 8.33 2000-01 65 43.608 29.411 66.69 3.016 8.38 2001-02 68 48.042 36.709 76.41 3.249 8.71 2002-03 70 52.050 41.911 80.52 3.677 8.74 2003-04 76 52.585 42.594 81.00 3.944 9.16 Source: Pakistan Sugar Mills Associations,

21

Graph 4

2.3 Raw Material

7. Among 105 sugarcane growing countries, Pakistan is the 5th largest country in the world in terms of area under sugarcane cultivation, 11th by production and 60th in yield. The yield in Pakistan is about 4 tonnes of sugar per hectare against a potential of 10.5 (Farming Outlook 2004). Sugarcane is the main raw material for the production of sugar. Since independence, the area under sugarcane cultivation has increased more rapidly than any other major crop. It is one of the major crops in Pakistan cultivated over an area of around one million hectares. Accounting for 5 per cent of the total cropped area, sugarcane contributes 15 per cent to the value added of major crops. The sugar industry, the second largest agro based industry is dependent on sugarcane farming for the supply of raw material. Sugarcane farm-ing and sugar manufacturing contribute significantly to the national exchequer in the form of various taxes and levies. Sugar manufacturing and by products have contributed handsomely towards the earn-ing of foreign exchange, previously through import substitution and recently through export.

8. Sugarcane is grown on around one million hectares. For the last six years from 1997-98 production has ranged between 46 and 55 million tonnes. Yield, on average is 47.5 tonnes per ha. However, some indi-vidual farmers obtain higher yield up to 100 tonnes per hectare. Cane is also used for non-centrifugal sugar (gur) and seed and the amount of crop harvested for centrifugal sugar each year is around 2/3rd of the total. The contribution of the Punjab in the total cane production is around 60 per cent, Sindh about 30 per cent and NWFP 10 per cent (Farming Outlook). The graph depicts that area of sugarcane did not increase smoothly. There was a cycle of four years. Particularly in 1998-99 it started declining but after that it increased in 2002-03.

Graph 5

Sugarcane Production and crushed and sugar production

0

10

20

30

40

50

60

1993

-94

1994

-95

1995

-96

1996

-97

1997

-98

1998

-99

1999

-00

2000

-01

2001

-02

2002

-03

2003

-04

Years

Can

e p

rod

uce

d a

nd

cr

ush

ed

0

0.5

1

1.5

2

2.5

3

3.5

4

4.5

Su

gar

Pro

du

ctio

n

CaneProducedmilliontonnes

Canecrushedmilliontonnes

Sugarproducedmilliontonnes

Sugarcane Production, crusing and sugar production

Area 000 Hectare

100

300

500

700

900

1100

1990-91

1992-93

1994-95

1996-97

1998-99

2000-01

2002-03

Years

Are

a in

000

Hec

tare

Area000Hectare

22

9. Despite manifold increase in the area under cultivation and production, per hectare yield has not shown any significant improvement. The average yield over ten-year period 1993-2003 shows a comparatively high in the province of Sindh followed by NWFP and the Punjab (Annex I). Sugarcane is a high delta crop and requires 80 to 90 acre inches of water in Sindh and about 64 acre inches water in the Punjab. Water is a scarce resource as Pakistan is an arid country where sustainable availability of water cannot be assured. Water is too crucial to production and productivity of sugarcane crop.

10. In Pakistan yield is perhaps the lowest among all major sugarcane growing countries in the world (Sugar Profile M/O Industries). Sugarcane yield in Pakistan compared with countries of the world in terms of average yield during 2001 was 47.5 tonnes per hectare compare to the world average of 65.2, Asia 65.4, China 77.1, India 70.6, Philippine 92.6, Thailand 57.7 and Australia 75.5 (Farming Outlook 2004). Pakistan has all the essential ingredients to produce high yield sugarcane. Despite manifold increase in the area under cultivation, per hectare, yield has not shown any significant improvement and remained the same. Colombia had the highest yield of 117.9 tonnes/hectare, fol-lowed by Australia (99.2), Egypt (89.0) (Ministry of Industries). Thus, sugarcane production presents a dilemma. As shown in the graph below yield could not increase more than 50 tonnes per hectare.

Graph 6

11. Area under cultivation, production and yield of sugarcane in the country are given in Table-5. it indicatesthat the area, production and yield all registered an increase. It is quite visible that there is an upward trend in all three fields apart from a rare decline in few years. In the year 1990-91, the area was 883.8 hectares, production was 35,988.7 tonnes and the yield was 40.7 tonnes per hectare. It increased in thecoming years but the rate of increase was very slow and that was the reason of Pakistan's lowest yield among all major sugarcane growing countries of the world. The rise continued although there were decline again in few years. There were declining trends from 1991-92 to 1992-3 and from 1999-00 to 2000-01 in all three. As a result of such slow progress, the end result after the year 2003-04 was that the yield could not increase more than 50 tonnes per hectare which was very little. While area under thecrop increased over the period by 19%, production increased by 46% and the yield by 26%. The graph below presents a picture of production of sugarcane growth which also proves that there is a cycle of four year according to fluctuations in the production.

Yield of Sugarcane

20

25

30

35

40

45

50

55

1990-91

1992-93

1994-95

1996-97

1998-99

2000-01

2002-03 Years

Yie

ld to

n / h

a

YieldTons/Hectare

23

Graph 7

12. In consultative meeting manufacturers acknowledged the fact that mill owners have invested money on new automatic machinery but hardly try to help sugarcane farmers. They emphasized that Pakistan is one of the leading manufacturers of sugar in the world but its per acre yield is poorest in the world. Small per acre yield triggers a chain reaction that renders growers and crushers helpless. Growers get meager returns on their investment while sugar mill owners fail to use their crushing capacityadequately and effectively. Only by increasing per acre yield grievances of growers and manufacturers could be redressed (Consultation meeting).

13. Table 6 represents average provincial shares in area and production for 2000-01 to 2002-03. According to this table, Punjab is the leading province in area and production followed by Sindh. NWFP occupies third position.

Production 000 Tons

200002500030000350004000045000500005500060000

1990-91

1992-93

1994-95

1996-97

1998-99

2000-01

2002-03

Years

Production000 Tons

24

Table 5: Area, Production and Yield of Sugarcane 1990-91 to 2002-03

Years Area 000 Hectare

Production 000 Tonnes Yield Tonnes/Hectare

1990-91 883.8 35988.7 40.7 1991-92 896.1 38864.9 43.4 1992-93 884.6 38058.9 43.0 1993-94 962.8 44427.0 46.1 1994-95 1009.0 47168.4 46.7 1995-96 963.1 45229.7 47.0 1996-97 964.5 41998.4 43.5 1997-98 1056.2 53104.2 50.3 1998-99 1155.1 55191.1 47.8 1999-00 1009.8 46323.6 45.9 2000-01 960.8 43606.3 45.4 2001-02 999.7 48041.6 48.1 2002-03 1099.6 52055.8 47.3 2003-04 1050.8 52584.6 50.0

Source: APCom , Ministry of Food, Agriculture and Livestock, Pakistan

Production000 Tonnes

Production 000 Tonnes

Graph 8

14. Achievement in all the three provinces and in all three operational dimensions sharply surpasses the targets set by the MINFAL. Target fixing is a ritual regularly followed by the Government to set a high bench mark for the growers to reach without any control over the factors of production or without provid-ing conducive environment. The system of estimation is rough and as such, cannot be accepted as reli-able. Area under sugarcane crop in the country was expanded to 1050.8 thousand hectares against tar-get of one thousand hectares. Sugarcane production rose to 52.585 million tonnes while the target was 45.635 million tonnes. Yield was higher at 50.0 tonnes/hectare against the target of 46.02 tonnes/hectare.

15. Over achievement of the targets, underscores the system of estimation as being skewed and weak. Deviations need not be beyond the standard, admitted at five percent. Appropriate comparison in this background would have to be the actual for the previous season. What was achieved in the 2002-2003 compared with the preceding season also gives similar reading.

16. As a consequence, the sugar industry cannot plan its working on sound track. Such an ad hoc system, if not uncertain and un-secure cannot give well measured. Sugar industry has as such fallen prey to uncertainties.

2.4 Marketing of Sugarcane

17. A mini field survey was conducted for this study to know the first hand information of sugarcane market-ing because three years ago farmers faced problem of payments from the sugar mills which are still pending and government has intervened to solve the problem. Unfortunately, farmers are now reluctant to grow sugarcane. Farmers normally sell their sugarcane directly to sugar mills rather than contractor or middleman. However, there are several small farmers, who sells their crop to middleman due to the misbehavior of factory representative/cane clerk because they demand Rs. 100/200 as bribe for accept-ance of sugarcane. Sometime farmers prefer to sell crop to middle man to avoid such kind of corruption even though middleman gives low price but deal in polite manners. Mills start crushing (almost on 15 to 20 November) and mill administration gives out the permits to farmers. In the mean while farmers also start harvesting of sugarcane to supply it on daily basis. So no time period is required

Provincial Shares Area of Sugarcane

Punjab, 1663, 66%

Sindh, 598, 24%

NWFP, 255, 10%

Punjab

Sindh

NWFP

Provincial Shares in Production of Sugarcane

Punjab, 31313, 64%

Sindh, 11616, 24% Punjab

Sindh NWFP

NWFP, 5805, 12%

Table 6 Provincial shares in Area and Production of Sugarcane Average of 2000-01 to 2002-03

Area Production Country/ Province Hectares in

000 Acres in 000 Percent (%) 000 tonnes Percent (%)

Pakistan 1019 2518 100 47769 100 Punjab 673 1663 66 31313 66 Sindh 242 598 24 11616 24 NWFP 103 255 10 5805 10 Source: Agricultural Prices Commission.

25

for marketing. However, if a sugarcane trolley/truck stays outside the mill for one week, it looses 25 to 30 % of its weight. At the same time, mill authorities habitually deceive the farmers through their tricky weigh bridges. In this way, farmers lose another 10 % of sugarcane.

18. Sugarcane is not a profitable crop. Sometime it hardly covers input cost but all the time there is no otheroption. Farmers are not cultivating sugarcane on 100 % land and just growing on 50% or less than50 % area. Cultivation of sugarcane is an arduous activity that takes almost eighteen months for proper growth of the sugarcane crop. The cost of cultivation per acre is Rs19,000 and it is sold at Rs 26,000. The profit of Rs 6000 in sixteen months is not sufficient enough a reason to cultivate sugarcane. On top of it small growers were deceived at various stages, told the growers. Mill owners keep growers waiting for weeks outside the factory before offloading the sugarcane. This tedious and deceitful process that reduces the size of the crop and as a consequence, tells heavily on the growers. Similarly, growers in general and small growers in particular, voiced their reservations about the weighing processes. Growers feel that administration of sugar mills discriminate in this process by using unfair practices (field survey and consultation meeting).

19. The price of sugarcane is fixed by the Government. Mills pay the price according to the flow of supply. There is no payment schedule. In case of excessive production of sugarcane, mill administration cre-ates trouble for small farmers and don't issue permit easily. If one is a big land holder and bit influential, he would get his money within fifteen days otherwise the process of payment takes at least one month. In the days of shortage, they pay immediately to the farmers otherwise they give money within a month or 1 ½ month and release the payments to farmers/growers in the form of Cash Price Receipt (CPR) not cash. Whenever sugarcane production decreases, mill authorities pur-chase sugarcane from middleman at high price but they don't like to purchase it from farmers. The situation may be different in coming years because sugarcane production is already decreased and mill administration is going around and requesting to the farmers for sugarcane supply. If the price remains the same and the administration of mill does not change their behaviors then sugarcane production willreduce up to 40 %, within next two or three years. Growers demanded that if the mills cannot pay the cash price then they should release the payments, at least within a week (field survey 2004)

20. In consultation meeting grievances of small farmers were more evident. Their representatives from NWFP, Sindh and Punjab unanimously castigated manufacturers for paying low prices in comparison to the big landholders. Big farmers, representatives of the sugarcane growers told the participants that they got Rs 70 per mound whereas small farmers were offered Rs 35 in 2002-03. In the year 2003-04 official price was Rs 45 per mound but small growers could hardly fetch Rs 35 (consultation meeting)

21. Mill owners often give the impression that they provide financial help to the growers to cultivate sugar-cane. Delegates from Sindh categorically denied this impression. Sugar mill owners, according to them, charge interest on each penny they provide to the growers for sugarcane crop. Twenty years ago, mills were involved in training but now they don't provide any kind of training/guidance. Fertiliser, seeds and medicines, credit were granted by the mill authorities and later on they got 14 % interest on actual money. Generally farmers are not getting any financial support from the industry. Soft term loans were granted to the farmers and the money was deducted from next year's CPR but now there is nothing except business dealing and exploitation. Sometime mills experts visit farms to provide guidance in sowing, application of Fertilisers and pesticides. Few mills have set up a laboratory to keep the crop friendlyworms. Mill administration opposes the spray of pesticides/insecticides and provides crop friendly worms to control the diseases. Farmers have no knowledge about the WTO trade regime (field survey and consultation meeting).

2.5 By-Products of Sugar

22. Proper utilization of the by-products is necessary for the development of the sugar industry. The cost of sugar production is continuously growing, due to non- utilization of the by-products. If the by-products are properly utilized, the cost of production of sugar may go down by 20% to 25%. The mainby-products of the sugar industry are:

26

27

A. MOLASSESB. BAGASSEC. FILTER CAKE OR PRESS MUD

23. Besides sugar, the industry produces molasses, industrial alcohol which is exported and earns handsome foreign exchange. Sugar industry by its strategic placement in rural heartland is the best suited fordevelopment and growth. Bagasse is used in electricity generation on which sugar plants operate and are in a position to provide power to national grid network in winter season when hydel power genera-tion capacity tends to trim. Bagasse is also used in making of paper and boards, latter having multiple uses as packing material. Medium fibre density wood is also being manufactured by putting into service improved technology of utilizing bagasse. Molasses is uncrystallised syrup extracted from raw sugar during the refining process. Globally, about 75% of molasses is obtained from sugarcane (Saccharum officinarum) and the remainder comes from sugar beet (Beta vulgarise), citrus fruits, corn and sorghum.

24. Availability of molasses in Pakistan has increased from 1.330 million tonnes in 1992-93 to 2.1 million tonnes in 1998-99. It decreased to 1.397 million tonnes in 1999-2000 due to decline in Sugar productionin the country and again increased to 2.004 million tonnes in year 2002-2003. As the commercial utiliza-tion of molasses in the country is very limited, major portion of the commodity is exported. The export ofmolasses has remained between 1.029 million tonnes to 1.835 million tonnes.

CHAPTER THREE: DOMESTIC AND WORLDBALANCE SHEET OF SUGAR

3.1 Domestic Demand and Supply Position

1. In Pakistan, almost 99% sugar is extracted from sugarcane. Sugar production has increased since 1987-88 except for a couple of years to reach the peak of 4.0 million tonnes during 2003-04. Beet and sugarcane production has been 3.226 million tonnes (2001-02), 3.684 million tonnes (2002-03) and 4.02million tonnes (2003-04). Sugar production of the last three years on average at 3.61million tonnes gives an operational efficiency of about 77%, leaving 23% idle capacity (Ministry of Industries). The sugar production capacity of these mills is above five million tonnes of sugar. The mills require about 65 million tonnes of sugarcane to run on full capacity. There exits a mill to-mill competition for acquiring more sugarcane (Farming Outlook).

2. Pakistan was a sugar importing country as demand outstripped supply for almost every year. However, situation has since changed. Country produced surplus sugar, which has created huge closing stocks from year 2000 to 2003 ranging from 600,000 tonnes to 700,000 tonnes. The production, import, export and consumption trends from 1998-99 to date are given in Table-7.

3. During the last season (2003-04), sugar industry rolled out record sugar output at 3994 (3677) thousandtonnes in (2002-03), increased up to 8.70%, showing higher efficiency of sugar production. Opening stocks as of 1st October 2003-04 were 759.3 thousand tonnes, while small quantity of special sugar i.e.7.6 thousand tonnes had also been imported in to the country. Hence total availability of sugar, includingdomestic production, carry over inventory and imports remained at 4761.3 thousand tonnes (Ministry of Industries).

4. The domestic balance sheet proves that Pakistan has never been a regular exporter however, it imported sugar regularly. Size of the industry shows that potential is there but viability of sugar industry depends on several other reasons like availability of sugarcane, cost of sugar production, export opportunities viz a international sugar trade regime.

3.2 Recovery Level

5. Table-8 depicts the trend of cane production, cane available for sugar industry, sugar production and recovery of sucrose contents. The Graph Given below interprets the table no. 8.

28

Table 7. Domestic Balance Sheet of Sugar (000 tonnes)

Years Opening Stocks

Production Imports

Total Availability

/Supply

Domestic Consumption Exports Carry over

Stocks

1998-99 513.0 3542.0 04.0 4059.0 3040.0 648.0 371.0 1999-00 371.3 2429.0 421.0 3221.3 3171.9 22.2 27.2 2000-01 27.2 3016.0 633.0 3676.2 3054.4 - 621.8 2001-02 620.8 3249.0 27.5 3897.3 3252.1 8.0 637.2 2002-03 637.1 3677.0 9.0 4323.1 3482.8 81.0 759.3 2003-04 759.3 3994.4 7.6 4761.3 3812.8 121.5 827.0

Source: Pakistan Sugar Mills Association Annual Reports. (Figures are rounded off). Agricultural Prices Commission Sugar Policy 2004-05. Ministry of Industry for 2003-04

29

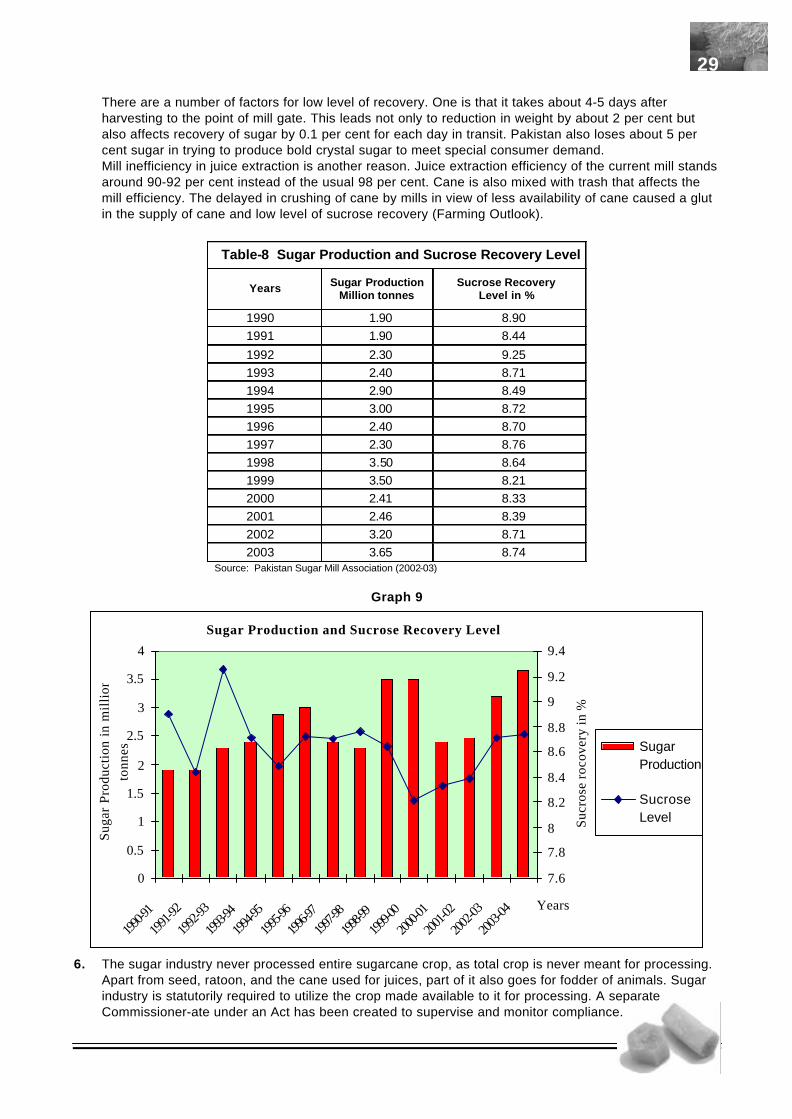

There are a number of factors for low level of recovery. One is that it takes about 4-5 days afterharvesting to the point of mill gate. This leads not only to reduction in weight by about 2 per cent but also affects recovery of sugar by 0.1 per cent for each day in transit. Pakistan also loses about 5 per cent sugar in trying to produce bold crystal sugar to meet special consumer demand.Mill inefficiency in juice extraction is another reason. Juice extraction efficiency of the current mill standsaround 90-92 per cent instead of the usual 98 per cent. Cane is also mixed with trash that affects the mill efficiency. The delayed in crushing of cane by mills in view of less availability of cane caused a glut in the supply of cane and low level of sucrose recovery (Farming Outlook).

Graph 9

6. The sugar industry never processed entire sugarcane crop, as total crop is never meant for processing. Apart from seed, ratoon, and the cane used for juices, part of it also goes for fodder of animals. Sugar industry is statutorily required to utilize the crop made available to it for processing. A separate Commissioner-ate under an Act has been created to supervise and monitor compliance.

Sugar Production and Sucrose Recovery Level

0

0.5

1

1.5

2

2.5

3

3.5

4

1990-9

1

1991-9

2

1992-9

3

1993-9

4

1994-9

5

1995-9

6

1996-9

7

1997-9

8

1998-9

9199

9-00

2000-0

1

2001-0

2

2002-0

3

2003-0

4 Years

Suga

r Pr

oduc

tion

in m

illio

n to

nnes

7.6

7.8

8

8.2

8.4

8.6

8.8

9

9.2

9.4

Sucr

ose

roco

very

in %

SugarProduction

SucroseLevel

Table-8 Sugar Production and Sucrose Recovery Level

Years Sugar Production Million tonnes

Sucrose Recovery Level in %

1990 1.90 8.90 1991 1.90 8.44

1992 2.30 9.25 1993 2.40 8.71 1994 2.90 8.49 1995 3.00 8.72 1996 2.40 8.70 1997 2.30 8.76 1998 3.50 8.64 1999 3.50 8.21 2000 2.41 8.33 2001 2.46 8.39 2002 3.20 8.71 2003 3.65 8.74

Source: Pakistan Sugar Mill Association (2002-03)

Under-utilization of capacity by sugar industry is due to crop size. In order to improve capacity utilizationthere is need to accelerate sugarcane production, so as to attain optimum utilization of the existing capacity (Iskandar M Khan, former Chairman, PSMA). But that is in the realm of wishful thinking.

7. New sugar mills were mushrooming, mostly by the same sponsors. Against only two small units in 1947,as many as 76 today (29 units) were established in the last decade at an exponential rate. The installed capacity of 10,000 metric tonnes at the time of independence has increased by now to 355,150 metric tonnes. Some companies are so fond of making losses that they work hard to increase them every year.There is no known method where any industry, having over 45% excess capacity and not being able to compete in the export market because of much higher cost of production, can be made viable and prof-itable. The patronage and of mushrooming of the sugar industry by very influential and resourceful peo-ple suggests that the poor health of the industry is on account of excess capacity created for political considerations to bribe crony capitalists.

8. There are various reasons for high cost of production in Pakistan. Besides the low recovery and ineffi-ciency of processing, the byproducts such as molasses and cake are not properly utilized. Further, the extra power generated by the mills is not supplied for domestic or commercial use (Dr. Umer Khan).

9. In favorable years, there is more sugar production than the requirements and in adverse years the country falls short of target figures in imports. The government of Pakistan takes care to ensure stable per kg price to the consumer by regulating duty structure while there is no ban on export of sugar. The problems arise in case of surplus or short production of sugar in the country. In case of surplussituation, such as during 2001-02 and 2002-03, the competition in the international market, including India did not allow export because of high cost of production. The ex-mill price of sugar in Pakistan is around Rs 18-19 per kg compared with Rs. 12-14 per kg in the international market. Thus, stocks build up with mills.

3.3 Consumption of Sugar

11. During 1962, the total domestic consumption of sugar was 0.162 million tonnes, which increased to 1.76million tonnes in 1987, and 3.484 million tonnes in the year 2003. Per capita consumption of sugar was 3.4 kg in 1962, which increased to 17.5 kg in 1987 and 23.85 kg in the year 2003. Trend of per capita domestic consumption of sugar as well as GUR is given in Table-9. The graph below indicates that consumption by sweetshops, bakeries and sugar confectionary industry is more than per capitaconsumption of individuals.

12. Up to 1983, per capita consumption of sugar was low mainly due to rationing while consumption of GURwas high. De-rationing of sugar in 1983 resulted in a steep rise in the per capita consumption of sugar. It increased to 17.5 kg. in 1987 from 9.1 kg. in 1980. The consumption of GUR decreased simultane-ously to 11.1 kg. At present, the consumption of sugar is 23.85 kg. and that of GUR 1.39 kg. per capita. On the basis of per capita consumption, the monthly requirement of sugar in the country is around 296.758 thousand tonnes to 300.000 thousand tonnes. Sugar production during last three years exceeded domestic demand. After meeting domestic demand, it was left with a surplus of 637.149 thousand tonnes in 2001, 759.103 thousand tonnes in 2002 and 759.000 thousand tonnes in 2003. However, sugar industry has been unable to export the surplus sugar due to the very high cost of its production. Though the sugar production trend can be termed exciting however, it has not reached the desired level of scale of economies. This is mainly due to under utilization of the installed production capacity (Ministry of Industries).

30

Graph 10

13. Trend forecast per capita sugar consumption comes to 22.08 kgs in 2003-04 accordingly, domestic requirements for 2003-04 for a mid year population of l48 million (as on 1 April 2004) work out to 3.812 million tonnes. In view of the foregoing supply and demand situation, the country would have substantialsurplus stocks of sugar.

14. Sugar availability not simply persisted in excess but bounced to set a new record, due to consistently carryover of surplus for the past three years, its impact in terms of steep fall in sugar prices and increased financial cost of carrying higher inventory for a long period, pushed cost of sales up.

15. In consultation meeting, representatives of the sugar mills were bitter about the inconsistent policies of the government. The government of Pakistan, without taking growers and manufacturers intoconfidence, wastes no time in importing sugar. Similarly, without much consideration, state machinery is eager to control sugar price, which is not an essential food item. Surge in the sugar prices would decrease its consumption, which again was a positive sign for the general health of the people, maintained sugar mill owners. Anxiety about the sugar price hike is baseless, was the chiefargument of the manufacturers. Sugar producers solicited that the government ought

Table-9 Per Capita consumption of Sugar

Total Domestic Consumption of Sugar

Per Capita consumption

of Sugar

Per Capita consumption of Gur

Per Capita* Sweetener

Consumption

Years

(Million tonnes) (kg.) (kg.) (kg.) 1962 0.162 03.40 18.00 21.40 1970 0.455 07.60 24.70 32.30 1980 0.744 09.10 23.90 33.00 1987 1.764 17.50 11.10 28.60 1990 2.200 19.90 08.70 28.60 1995 2.722 21.86 06.64 28.50 2000 3.236 22.69 03.66 26.35 2001 3.050 21.38 04.54 25.92

2002 3.252 22.28 02.42 24.70

2003 3.554 23.85 01.39 25.25

Note:* Per capita sweetener is consumed by sweet shops, sugar confectionaries and bakeries Source: Pakistan Sugar Mills Association Annual Reports

Per Capita Consumtion of Sugar

0

5

10

15

20

25

30

35

1962

1970

1980

1987

1990

1995

2000

2001

2002

2003 Years

Kgs

Per Capita consumption ofSugarPer Capita consumption ofGurPer Capita SweetenerConsumption

31

to change its mindset concerning sugar sector because of its forward and backward linkages (Consultation Meeting).

3.4 Domestic Price Situation

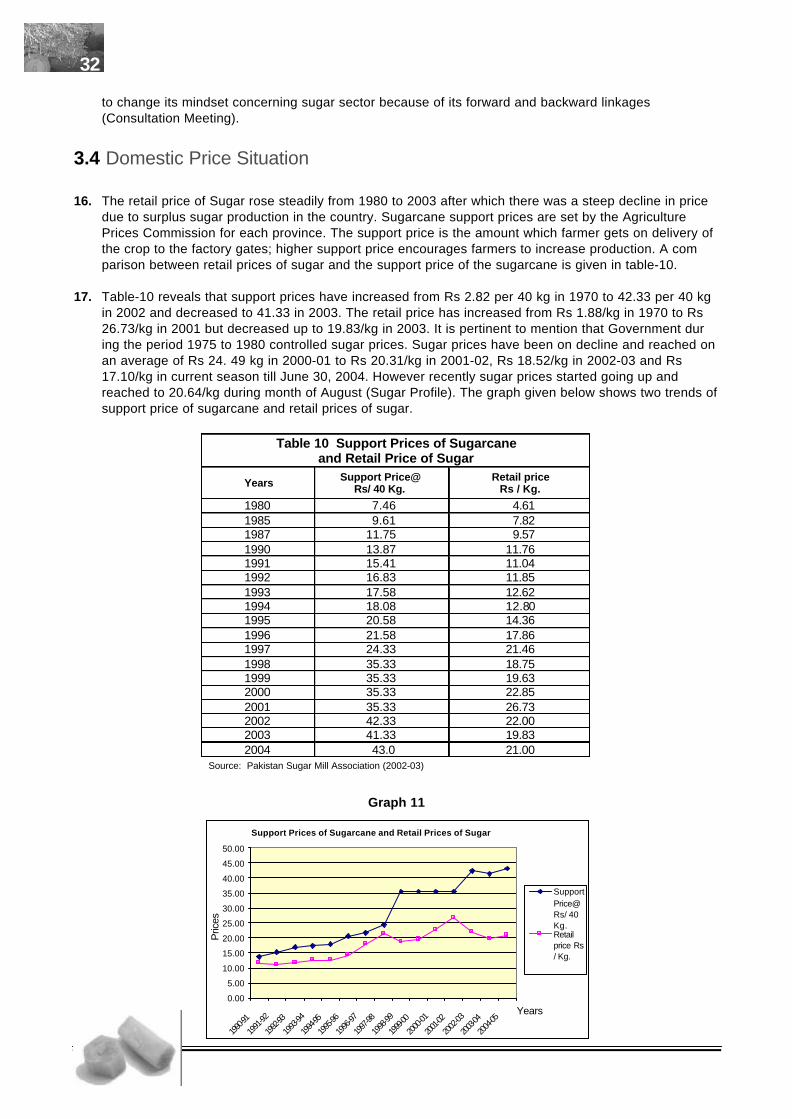

16. The retail price of Sugar rose steadily from 1980 to 2003 after which there was a steep decline in price due to surplus sugar production in the country. Sugarcane support prices are set by the Agriculture Prices Commission for each province. The support price is the amount which farmer gets on delivery of the crop to the factory gates; higher support price encourages farmers to increase production. A comparison between retail prices of sugar and the support price of the sugarcane is given in table-10.

17. Table-10 reveals that support prices have increased from Rs 2.82 per 40 kg in 1970 to 42.33 per 40 kg in 2002 and decreased to 41.33 in 2003. The retail price has increased from Rs 1.88/kg in 1970 to Rs 26.73/kg in 2001 but decreased up to 19.83/kg in 2003. It is pertinent to mention that Government during the period 1975 to 1980 controlled sugar prices. Sugar prices have been on decline and reached onan average of Rs 24. 49 kg in 2000-01 to Rs 20.31/kg in 2001-02, Rs 18.52/kg in 2002-03 and Rs 17.10/kg in current season till June 30, 2004. However recently sugar prices started going up and reached to 20.64/kg during month of August (Sugar Profile). The graph given below shows two trends ofsupport price of sugarcane and retail prices of sugar.

Graph 11

32

Table 10 Support Prices of Sugarcane and Retail Price of Sugar

Years Support Price@ Rs/ 40 Kg.

Retail price Rs / Kg.

1980 7.46 4.61 1985 9.61 7.82 1987 11.75 9.57 1990 13.87 11.76 1991 15.41 11.04 1992 16.83 11.85 1993 17.58 12.62 1994 18.08 12.80 1995 20.58 14.36 1996 21.58 17.86 1997 24.33 21.46 1998 35.33 18.75 1999 35.33 19.63 2000 35.33 22.85 2001 35.33 26.73 2002 42.33 22.00 2003 41.33 19.83 2004 43.0 21.00

Source: Pakistan Sugar Mill Association (2002-03)

Support Prices of Sugarcane and Retail Prices of Sugar

0.00

5.00

10.00

15.00

20.00

25.00

30.00

35.00

40.00

45.00

50.00

1990-9

1

1991

-92

1992-9

3

1993

-94

1994-9

5

1995

-96

1996

-97

1997

-98

1998

-99

1999-0

0

2000

-01

2001-0

2

2002

-03

2003-0

4

2004

-05Years

Pric

es

SupportPrice@Rs/ 40Kg.Retailprice Rs/ Kg.

18. The support price of sugarcane has been on the quantity of cane and not on the quality of cane. This leads to spreading of cane varieties with more weight and low recovery. To offset this, the government introduced a quality premium system in 1994. Under this system if the average recovery of mill stands above bench mark, recovery of 8.5 percent in the Punjab and 8.7 percent in Sindh), the grower waseligible for an additional amount at rate of Rs.0.27 for 1994-96, 0.32 for 1996-97 and 0.50 for in 1997-2002 per 40 kg of cane recovery. 0.1 per cent increase over and above the bench mark recovery. However, this system has not worked. The payment cane on the basis of weight also encouragedplanting of some imported cane varieties like COJ 1148 in the Punjab, which had low recovery. The Government has considered linking of sugarcane price with recovery and to do away with the support price system in sugarcane crop. But this system has yet to be finalized (Farming Outlook).

19. Sugarcane support price is fixed by the government, on average constituting 65 to 77 per cent of the production cost. Similarly, wages, utilities and other costs of production process have been about 16 percent. Variable costs aggregate to 87 per cent and this 'minimum' is determined by the government while the industry has no say in it. Sugar industry claims that price fetched by the industry could not cover costs of production and as a result, sugar industry stands devastated despite its sterlingperformance evinced by production trend. Sugar industry seeks either free market for both cane and sugar, or price support for both. It is absolutely inappropriate to fix price of raw material, leaveend-product free and place them diametrically opposed! Due to this sugar industry has become oppressed, to say the least. Statutorily, sugar industry is required and compelled to process entire cane crop available. The industry's demand for flexibility to process sugarcane volume to the extentproducing sugar adequate for domestic demand is yet to receive consent (PSMA-SZ Report).

20. By applying dynamics research and development in sugarcane crop, yield could have been doubled and that would have given maximum utilization of the capacity and emerging economies of it could haveovercome the problems now being faced. Expansion in sugarcane processing capacity was carried out with reasonably fair projections. Sugarcane crop yield trailing behind candid estimations prevented sugar industrial potentials from a fine flourish.

3.5 Cost of Sugar Production

21. Cost of sugar production represented a rising trend. The major critical component in it has been the price of sugarcane, compounded by effective high at 18% rate of sales tax. On these counts, the sugar industry had no control to contain cost of production. Sugarcane price influence on the cost of sugar production and trend of wholesale price of the sugar vis-à-vis its adverse influence on economic viabilitycan be gauged from the representative data of the past six years. Cost of sugar production per tonduring the past five years, 1997-98 to 2002-2003, ranged from Rs.11,467 to Rs.20,332 i.e. an average increase of 12.88%. In the same period, cost of sugarcane fluctuated from Rs. 9.09 to Rs. 11.68, an average increase by 5.69%. Cost of other components in sugar production could be contained by the sugar industry to a limited extent due to various factors, including inflationary trend in the nationaleconomy (PSMA-SZ Report).

Table –11 Cost of Sugar Production Analysis AVERAGE %

A. VARIABLE COST (RS IN 000) Raw material consumed 879,899 78 Stores consumed 22,890 Total (A) 902,789 80.7

B. FIXED COSTS (RS. IN 000) Manufacturing Expenses 146,793 13.1 Admin and Selling Expenses 42,246 3.7 Financial charges 26,932 2.4 Total (B) 215,971 19.3 Total (A+B) 1,118,760 Molasses sales / transfer 49,992 Total cost 1,068,768

Average production of 8 selected units 67,835 Cost of production/ ton 15,755

Source: Pakistan Sugar mills Associations.

33