Embed Size (px)

Citation preview

IIP

art T

wo

Cost Measurement SystemsThe previous part discussed how

cost management information

supports decisions about setting

strategy and using scarce, con-

strained resources. Cost manage-

ment helps define strategy by

predicting and estimating the

costs and benefits of alternatives.

The key to using scarce capacity

wisely is to measure the profit or

value contributed by alternative

products and services, and of

course, part of profit is the costs

used to generate revenues.

Part Two builds cost management

tools to promote understanding of

productive processes. Chapters 4

through 7 develop three key di-

mensions of costing systems, that

cost managers evaluate when de-

signing cost systems. Chapter 4

identifies resources by value chain

operation or function (functional

costing) and distinguishes be-

tween unit-level and higher-level

costs and among three product

costing methods. Chapter 5 de-

scribes five major types or levels

of activities that drive costs.

Chapter 6 uses cost categories

and job costing to trace costs to

products, jobs, and projects using

unit-level and full ABC costing

methods. Chapter 7 applies costs

to continuously produced output

by the methods of process cost-

ing. Chapter 8 describes decision

making and allocation of costs to

jointly produced products. Chap-

ter 9 explains decision making us-

ing several common methods of

allocating service department

costs.

Part Three uses understanding of

costs and activities to help im-

prove the effectiveness and effi-

ciency of productive processes.

Look ahead➤

Look back Look at this part

➤➤

44Measuring Costs ofOperationsAfter completing this chapter, you should be able to:

1. Measure product costs, contributions to profit, and operating expenses usingthroughput, variable, and absorption costing.

2. Compare alternative product costs and their effects on profits.

3. Understand how different methods for measuring product costs create differentincentives for managing scarce productive resources.

Cost Management

Challenges1. How can cost managers

measure the financialresults of operations in away that reinforces properuse of resources?

2. How can alternativemethods of calculatingproduct costs createdifferent incentives?

3. How should costmanagers measure costsfor internal decisionmaking?

Memorandum

To: Glenn PenskiDirector of Cost Management Systems

From: Robert TraversVice President of Marketing and Sales

CC: Anne HechmanVice President of Manufacturing

Subject: Congratulations on a job well done

Glenn: I think your analyses and recomendations were exactly on target. We

have all but eliminated our backlog of late customer orders. And our customers

could not be happier. I also will be announcing at our next Executive Committee

meeting that we have added two major customers in Europe because we are

able to meet their on-time delivery requirements. Without our recent changes,

we would not have been able to meet their needs without upsetting our current

customers. Good work, Glenn.

Memorandum

To: Glenn PenskiDirector of Cost Management Systems

From: Anne HechmanVice President of Manufacturing

CC: Robert TraversVice President of Marketing and Sales

Subject: Re: Congratulations on a job well done, but...

Glenn (and Robert): I agree that we understand how to schedule our productive

resources much better and that we are much more responsive to customer

orders. Manufacturing operations are much smoother and there is much less

tension in the department now that we rarely have to expedite orders.

However, I do not think that we have completely solved our problems. We

are having limited success in reducing inventories and keeping non-bottleneck

processes idle when their output is not needed. We are still getting reports from

your office, Glenn, that idle capacity is hurting us by creating higher unit costs

and by not converting idle capacity into value-added products. I interpret these

reports to mean that we should keep all of our processes busy all the time. I am

concerned that either the concept of keeping some capacity idle is flawed or you

are measuring costs incorrectly.

I hope you realize that I am grateful for the improvements you have helped

make, but I also think that we can take another step to create cost reports that

reinforce what we should do to use our manufacturing capacity wisely. I hope

that you can sort out what is going on and make some improvements on the

reporting side.

IntroductionOrganizations like Contaminant Measuring Devices (CMD) are formed to manage pro-ductive processes efficiently and to generate customer value and profit.1 As discussedin Chapter 3, any organization’s capacity to do these things is constrained. If an orga-nization provided only one product or service, managing processes would be relativelyeasy, though not trivial. Management of resources would entail forecasting total sales,estimating total costs, and subtracting costs from revenue to get expected profits. If ex-pected profits are too low, managers could either change businesses or find ways to in-crease sales and/or reduce costs.2 This principle is deceptively simple, however,because most organizations provide many different products and services, and eachmay place different but competing demands on the organization’s resources. In this sit-uation, it can be difficult to know how to use scarce or constrained resources to gener-ate the most value or profit. In order to choose among competing products andservices, managers need to know what resources are needed and how much of the con-strained resources each product or service consumes and the profit each can generate.The purpose of this chapter is to analyze how to measure the costs of resources andprofitability of products and services in ways that reinforce good decision-making.

What Are The Resources Of An Organization?If you could view CMD from an aerial vantage point, you could observe resourcesflowing into the company and finished products flowing out. If the roof were transpar-ent or detachable, you also could see that CMD’s business and production processesneed many resources. These resources include physical resources such as money, parts,materials, buildings, machinery, and computers. In addition to physical resources,CMD needs human resources such as the talent, effort, and knowledge of its employ-ees. These resources are not free, and because the resources are not free, they must bemanaged wisely.

It is common for organizations to identify resources by at least three dimensions:3

1. The type of resource acquired.2. How the resource is used.3. How traceable a resource is to a particular decision.

Distinctions by type, use, and traceability have been used by accountants and financialanalysts for many years because they provide information that is useful for decision-making and that communicates how the organization has converted money and humancapital into products and services.

Types of Resources

We will use three general resource types that organizations obtain: materials, conver-sion, and operating resources. Note that organizations that outsource portions of theirvalue chains also treat those purchased products or services as material, conversion, oroperating resources, depending on their nature.

Material resources. Material resources are physical objects that may be incorpo-rated into products or used to maintain or enhance the organization’s productive and

108 Part II Cost Measurement Systems

Introduction

1See the introduction to Chapter 3 for a description of CMD and its products.2Note that accountants refer to the costs of items sold and the costs of using other resources to make

sales possible as expenses. Therefore, accountants and financial managers define profits as sales lessexpenses.

3Chapter 5 introduces a fourth dimension, the level or type of cost driver, in order to measure resourceuse more accurately.

What Are the Resources of an Organization?

Material resources arephysical objects thatmay be incorporatedinto products or usedto maintain or enhancethe organization’sproductive andsupport facilities

Chapter 4 Measuring Costs of Operations 109

support facilities. Materials include raw materials and purchased parts, components,and assemblies, such as the laser instruments that CMD manufactures and assemblesinto the devices it sells. Materials also include the maintenance and office supplies thatCMD uses to support production and the general organization.

Conversion resources. Providing products and services usually requires labor,equipment, and productive facilities; together, these are called conversion resourcesbecause they have the capability to convert other resources into products and services.CMD’s conversion resources include its manufacturing, technical, and supervisory la-bor and its manufacturing equipment and buildings.

Operating resources. Other types of physical and human resources are necessary tocreate and sustain the organization itself and to enable transactions with parties exter-nal to the organization. At CMD, these other operating resources include the corporateoffice and the marketing, sales, and customer service departments. Without these ele-ments of the value chain, CMD would not be able to function efficiently or effectively.

How Resources Are Used

Historically, manufacturing organizations developed accounting systems to supporttheir primary objective of efficient manufacturing. In many cases, most of these com-panies’ resources were dedicated to and used in manufacturing processes. Other oper-ating resources were much less important. Since manufacturing efficiency has beena key element in competing successfully, accountants have distinguished betweenproduction resources used to manufacture products and nonproduction resourcesused to support manufacturing processes. Supply, administration, marketing, and dis-tribution resources always have been necessary, but as support for the primary objec-tive of manufacturing. Thus, these other elements of the value chain have not receivedas much attention from accountants or accounting systems.

The world of business has changed in many ways since the days when manufac-turing was the primary industrial activity. The private and public service sectors aremuch larger than the manufacturing sector in many advanced economies includingCanada. Even in most manufacturing companies, support and service resources aremuch more extensive and important than they were. However, most accounting sys-tems still separate production resources from nonproduction resources, especially forfinancial and tax reporting. Though cost managers now correctly focus on all elementsof the value chain, it is important that they also understand the origins and limitationsof most formal accounting systems that support financial and tax reporting. Analyzingnonproduction resources, which can be the majority of resources, may require use ofinformation not normally supplied by the formal accounting system.

CMD’s value chain is shown again in Exhibit 4–1. Recall that physical and humanresources are supplied to and used in all elements of the value chain to deliver the mostcustomer value at lowest cost.At CMD, production pro-cesses (the middle, shaded ele-ment in Exhibit 4–1) usematerials and conversion re-sources to make its measure-ment devices. CMD’s othervalue chain processes use non-production resources to pro-vide support services, researchand development, design, sup-ply, marketing, distribution,and customer service.

Conversion resourcesinclude labor,equipment, andproductive facilities

Production resourcesare used to manufactureproducts

Nonproductionresources are used tosupport manufacturingprocesses

In some processes, there isno substitute for highlyskilled human resources.

A cross-classification by resource type and productive use is displayed with typi-cal examples in Exhibit 4–2. This exhibit shows that classifying operating resources, inparticular, into production or nonproduction uses can be difficult.

Traceability of Resources

A third useful dimension of resources is how easy it is to trace the cost of a resource toa decision or set of decisions. Cost managers ask, “If we make this particular decision,what resources must we obtain or use, and what will they cost?” Acquisition and use ofall resources is caused by management decisions, but ease of tracing resource costs tospecific decisions is important to cost managers who are analyzing or planning the costeffects to the organization of those decisions.

Direct resources. Sometimes, it is easy to see how specific decisions have causedthe acquisition of specific resources. These decisions are directly responsible for thoseresources, and the resources are called direct resources of those decisions. For exam-ple, a decision to produce laser instruments would cause the acquisition of the materi-als necessary to make the instruments. Making more instruments obviously causes theacquisition of more materials. Likewise, the decision to open a sales office in BuenosAires obviously causes the acquisition of specific physical and human resourcesnecessary for the office, and the decision to open and operate that office is directly

110 Part II Cost Measurement Systems

Exhibit 4–1

CMD’s Value Chain—Production andNonproduction Resources

Physicalresources

Humanresources

Support services• Accounting• Human resources• Legal services• Information systems• Telecommunications

DistributionProductionDesign

Research and

develop-ment

Supply MarketingCustomer

service

Measuringdevices

and services

Exhibit 4–2

Categories and Examplesof Resources

Used inUses Used to Produce Nonproduction Value

Resources Products and Services Chain Elements

Material resources Parts, assemblies, protective Cleaning supplies, officecoverings, connectors, supplies, repair itemssupplies

Conversion resources (convert Labor, supervision, maintenance, Labor, equipment, andmaterials into products, utilities, buildings, equipment facilities in administration,services, and sales) marketing, sales, distribution,

customer service

Operating resources (provide Internal business processes Internal business processesoperating support) (management, accounting, (management, accounting,

information systems, human information systems, humanresources, etc.), engineering resources, etc.), research and

development

Direct resources areobtained as the directresult of certaindecisions; decisions aredirectly responsible forthose resources

Chapter 4 Measuring Costs of Operations 111

responsible for acquiring and paying for those resources. Often, however, it is not easyto trace all resources to all decisions.

Indirect resources. Resources that are difficult to trace to specific management de-cisions are called indirect resources of those decisions. Other common names for in-direct resources are overhead, common costs, and burden, though these sometimesconvey a derogatory image (e.g., unproductive or unnecessary). For example, CMDhired and retained Robert Travers as vice president of marketing and sales; that hiringdecision is directly responsible for recruiting and paying for this human resource.Though Mr. Travers manages all of CMD’s sales operations, it is not easy to trace anyof his cost to the decision to open the Buenos Aires sales office. Thus, Mr. Traverscould be classified as an indirect resource of the Buenos Aires office. As another ex-ample, Anne Hechman, vice president of manufacturing is paid by CMD to manage itsmanufacturing processes, but she does not actually manufacture a single instrumentherself. Thus, though she is necessary to support production, CMD acquired and paysfor this human resource to indirectly support manufacturing of specific instruments.Thus, Anne Hechman is an indirect manufacturing resource.

The distinction between direct and indirect resources is not restricted to human re-sources. For example, at its primary location CMD manages the company and manu-factures its products in the same large building, using the same computer network.How much of the building and computer network resources were obtained for admin-istration? How much for manufacturing each instrument? It may not be easy to tracethese resources directly to decisions about either administration or manufacturing, letalone to manufacturing specific instruments. Thus, the building and computer networkresource would be considered to be an indirect resource for both administration andmanufacturing.

Supply versus use of resources. Organizations may acquire some resources to pro-vide the capacity to produce a certain level of products or services. The capacity the or-ganization makes available for use is the resources supplied. For example, CMD hasacquired the human and physical capacity to make more products than they currentlycan sell. The supply of skilled technicians who build the instruments, for example, is adirect cost of the capacity decision, not of specific decisions to use the capacity tomake products, services, or sales. However, the amount of their labor that is used is po-tentially traceable to products, for example, by maintaining records of who worked onwhich products. If we asked, “What resources are used for the Buenos Aires office?”we would identify the human and physical resources in place in Buenos Aires as wellas a portion, perhaps, of the management resource provided by Mr. Travers. Spendingfor Mr. Travers himself, ignoring travel costs, does not depend on how much theBuenos Aires office uses him. However, knowing how much of his capability is usedby the Buenos Aires office is informative when analyzing how much other work Mr.Travers is capable of performing. Thus, the capacity used for productive purposes isthe resources used. Confusing the distinction between supply and use of a resource ispotentially misleading because of the different impacts of decisions on spending anduse of resources. As we shall see, organizations use different costing systems depend-ing on their distinctions between supply and use of resources.

Three Dimensions of Resources

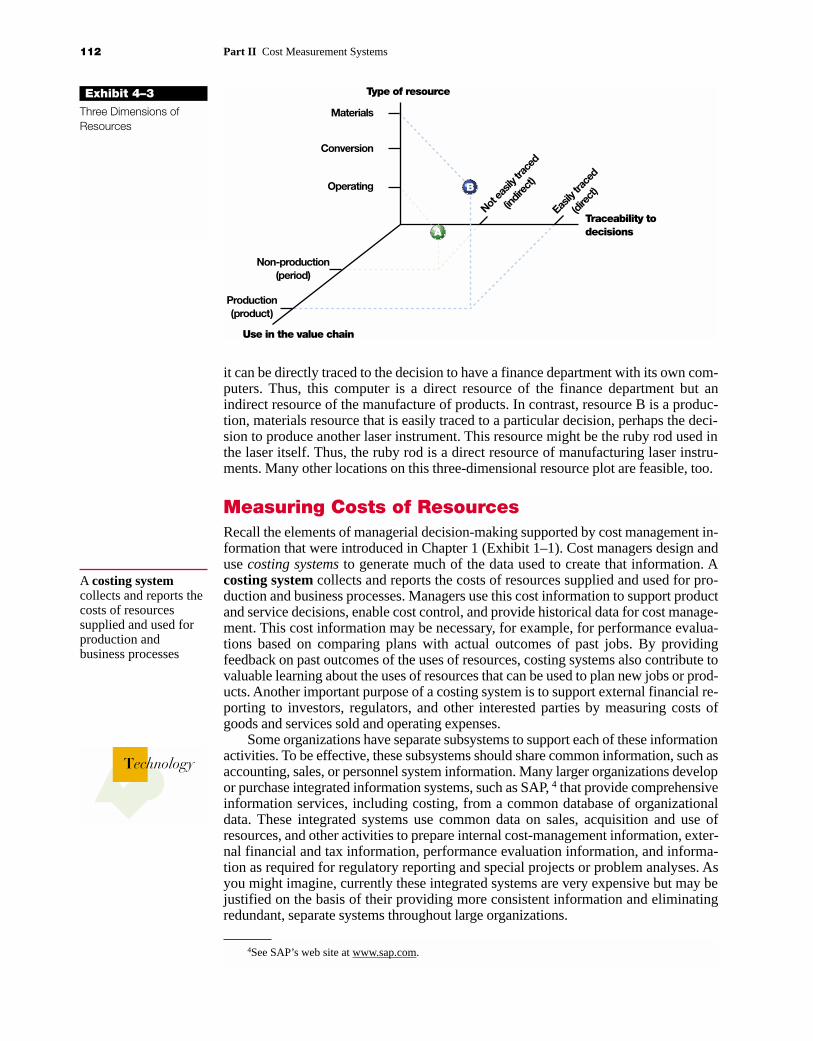

In summary, every resource fits into the qualitative dimensions of type of resource, usein the value chain, and traceability to decisions to supply or use resources. These qual-itative dimensions and two example resources are shown in Exhibit 4–3.

Resource A in Exhibit 4–3 is a nonproduction, operating resource that is not easilytraced to some particular decision, say the decision to produce one more laser instru-ment at CMD. This resource might be a computer in the finance department or a hu-man resources specialist in the personnel department. Note that though the computer inthe finance department may not be traceable to a decision to make a laser instrument,

Indirect resources areresources that areacquired but aredifficult to trace tosome managementdecisions

Resources suppliedcomprise the capacitythe organization makesavailable for use

Resources usedcomprise the capacityused for productivepurposes

it can be directly traced to the decision to have a finance department with its own com-puters. Thus, this computer is a direct resource of the finance department but anindirect resource of the manufacture of products. In contrast, resource B is a produc-tion, materials resource that is easily traced to a particular decision, perhaps the deci-sion to produce another laser instrument. This resource might be the ruby rod used inthe laser itself. Thus, the ruby rod is a direct resource of manufacturing laser instru-ments. Many other locations on this three-dimensional resource plot are feasible, too.

How Do Organizations of Resources?Recall the elements of managerial decision-making supported by cost management in-formation that were introduced in Chapter 1 (Exhibit 1–1). Cost managers design anduse costing systems to generate much of the data used to create that information. Acosting system collects and reports the costs of resources supplied and used for pro-duction and business processes. Managers use this cost information to support productand service decisions, enable cost control, and provide historical data for cost manage-ment. This cost information may be necessary, for example, for performance evalua-tions based on comparing plans with actual outcomes of past jobs. By providingfeedback on past outcomes of the uses of resources, costing systems also contribute tovaluable learning about the uses of resources that can be used to plan new jobs or prod-ucts. Another important purpose of a costing system is to support external financial re-porting to investors, regulators, and other interested parties by measuring costs ofgoods and services sold and operating expenses.

Some organizations have separate subsystems to support each of these informationactivities. To be effective, these subsystems should share common information, such asaccounting, sales, or personnel system information. Many larger organizations developor purchase integrated information systems, such as SAP, 4 that provide comprehensiveinformation services, including costing, from a common database of organizationaldata. These integrated systems use common data on sales, acquisition and use ofresources, and other activities to prepare internal cost-management information, exter-nal financial and tax information, performance evaluation information, and informa-tion as required for regulatory reporting and special projects or problem analyses. Asyou might imagine, currently these integrated systems are very expensive but may bejustified on the basis of their providing more consistent information and eliminatingredundant, separate systems throughout large organizations.

112 Part II Cost Measurement Systems

Exhibit 4–3

Three Dimensions ofResources

Type of resource

Materials

Conversion

Operating

Non-production(period)

Production(product)

Not ea

sily t

race

d

(indir

ect)

Easily

trac

ed

(dire

ct)

Traceability todecisions

Use in the value chain

B

A

Measuring Costs of Resources

A costing systemcollects and reports thecosts of resourcessupplied and used forproduction andbusiness processes

4See SAP’s web site at www.sap.com.

Technology

Chapter 4 Measuring Costs of Operations 113

Design Issues

In designing costing systems, cost managers seek answers to many questions related tothe information they need to present about the acquisition and use of resources for theirorganizations’ most important management decisions. They may ask decision-makersand other members of the cost management team variations of the following questionsabout the decision-making of their organization. We consider these types of questionsin this and subsequent chapters.

Importance of resource supply versus resource use (Chapter 4):� Do we need to make a distinction between costs of supplying versus using

resources?� Do we need to isolate and report the costs of supplying and using different

resources, or will average costs across types of resources be adequate?� Do we need expected supply or use, historical supply or use, opportunity costs,

or all of the above?� Do we need resource costs classified by where the work is performed?

Importance of nature of work versus location of work (Chapter 5):� Is it important to know how the work of the organization is done?� Do we need costs to provide incentives for improvements, or are other incentives

more appropriate?

Uniqueness of outputs (Chapters 6 and 7):� Do we need specific costs of each product and service, or will average costs across

products and services be adequate?� Do we need periodic costs and/or costs for the entire life of projects, products and

services?

Common to all considerations:� Do we need rapid reporting of costs, or can we tolerate delays in reporting? How

long can the delays be?� Do we need complex reporting of costs, or is simple, uncomplicated reporting

more useful?� Do we need flexible data that can be reorganized into unique information by each

decision-maker, or is it better to provide information in a format common to alldecision-makers?

� Do decision-making and financial reporting needs conflict, or can the same infor-mation meet both needs?

� Do we have an unlimited budget to develop and maintain the costing system, ormore realistically, do we have a budget limit? Given the budget limit, what trade-offs of information for the cost of information must we make?

As Exhibit 4–4 shows, the three discriminating categories of questions (concernwith resource supply or use, nature of work, and uniqueness of output) are associatedin practice with different cost-system designs. Chapter 4 investigates the implicationsof resource supply or use for cost-system design and introduces functional costing.Chapter 5 describes activity-based costing as a system solution to concerns about ac-tivities and the nature of work. Chapters 6 and 7 describe cost systems for outputs thatare either unique or undifferentiated, respectively.

Beyond asking and answering these types of questions, there are almost no formu-las or recipes that prescribe what a costing system should be. Actually, this is goodnews for cost managers. Thoroughly understanding how to match costing informationto decision-making needs is a major way that cost managers use their judgment to addvalue to their organizations. This section of the text is devoted to investigating alterna-tive costing systems and how they may be configured to best serve organizations and

decision-makers. Before diving into this topic, we need to develop a common, funda-mental understanding of the concept and measurement of “cost.”

What Do We Really Mean by “Cost”?The measurement of cost is fundamental to managing organizations’ resources becausecosts are important measures of resource availability and use. Cost is a measure of thesupply or use of a scarce or constrained resource to achieve a specific outcome.5 Anorganization gives up (or “sacrifices”) scarce resources in order to obtain otherresources. The value given up is a measure of the purchase cost of resources. These

114 Part II Cost Measurement Systems

Exhibit 4–4

Three Dimensions ofCosting System Designsin Practice

Job costing

Operation costing

Process costing

Functionalcosting

(introducedin Chapter 4)

Activity-based

costing

Throughputcosting

Variablecosting Absorption

costing

Supplyor use ofresources

Nature orlocation of

work

Uniquenessof products

Cha

pte

rs 6

and

7

Chapte

r 5Chapter 4

Progressive cost managers at Borg-Warner Automotive Diversified Transmission Products Corpora-tion anticipated recent trends toward designing costing systems that serve decision-makers by pro-viding the information they need to improve their products’ competitiveness and value. Costmanagers first learned what decisions had to be made by their internal customers, corporate man-agers and plant managers, whose needs were very different. They learned, for example, that plantmanagers need specialized information about how processes use resources and how that use canbe improved, but not the great amount of detail on past departures from standards that had beenprovided. Corporate managers, who had received the same cost reports as plant managers, wereoverwhelmed by the accumulated detail of all the plant-level reports and could not find the informa-tion they needed to improve their strategic choices. By working closely with decision-makers at bothlevels, cost managers were able to design effective costing systems and reports.

Source: G. Hanks, M. Freid, and J. Huber, “Shifting Gears at Borg-Warner.” Also see, P. Drucker, “TheInformation Executives Truly Need.” Full citations are in the bibliography.Visit www.borg-warner.com.

Cost Management in

Practice 4.1

What Do We Really Mean by “Cost”?

5Usually, costs are expressed in monetary terms, though that is not always necessary or even desirable.As an alternative, some public and nonprofit organizations use nonmonetary measures of cost, as in measur-ing the “cost” of a public policy in terms of the incidence of poverty, crime, or disease. Likewise, benefitsmay be expressed in nonmonetary terms. Some would argue that the primary justification for politicalprocesses is to make tradeoffs of nonmonetary social costs and benefits that cannot be made easily in tradi-tional markets for products and services.

LO1 Measure productcosts, contributions toprofit, and operatingexpenses usingthroughput, variables, andabsorption costing.

Cost is a measure ofthe acquisition orconsumption of ascarce or constrainedresource to achieve aspecific outcome

Chapter 4 Measuring Costs of Operations 115

acquired resources are subsequently supplied to production and nonproductionprocesses and used to produce and sell products and services or to support productionand sales. The value of the resources made available is the cost of resources supplied.Cost of resources supplied may or may not be the same as cost of resources used be-cause an organization may choose to make available more resources than it uses at anytime, perhaps to take advantage of currently low prices or to accommodate unexpectedneeds or shortages. The value of the resources not actually used is the cost of reserve orexcess capacity, as discussed in Chapter 3. The value of resources consumed for pro-ductive purposes is the cost of resources used.

Ideally, the value given up to supply or use a resource is measured as an opportu-nity cost, which is the current value of the forgone, next-best alternative use of what-ever is supplied or used. Because opportunity costs can be difficult to measure reliably,most cost management systems measure actual or expected out-of-pocket costs,which are the payments (usually cash or obligations to pay cash) made for resources.Out-of-pocket costs can be the same as opportunity costs, but may not be the same be-cause of imperfect markets and changes in the decision-making environment betweenwhen a resource was acquired and when it is used.6

Actual costs usually are measured as the past payments for currently owned re-sources, whereas expected costs are the predicted or forecasted payments for futureresources. For example, the actual cost of CMD’s equipment is the money that waspaid to obtain it. As another example, the expected cost of one of CMD’s new productsis the monetary value of the resources that CMD expects to acquire and consume tocomplete it.

Traditionally, the costs of resources used to produce products are called productcosts, and these become cost of inventory and cost of goods sold expense when theproducts are sold. The costs of resources used in nonproduction value-chain elementsare called period costs and become other income-statement expenses of the period.Traditionally they have been considered support costs of doing business during the pe-riod. Since they are expensed when used, period costs do not become part of the valueof inventories for financial or tax reporting.

Total Cost

CMD’s total cost includes the costs of all resources supplied to the company during aspecified time period. Total cost would include the costs of all production and nonpro-duction resources, or all material, conversion, and operating resources, or all direct andindirect resources. It is possible, of course, to create many different subtotals of costs,such as total production costs, total conversion costs, total direct costs, or total directmaterial costs. Organizations would create these subtotals to reflect decision-makingand reporting needs. For example, CMD’s executives receive a report each week fromGlenn Penski that totals weekly costs by type of resource used for the seven types ofCMD’s instruments. Exhibit 4–5 shows an excerpt from a recent week’s report. AnneHechman uses this report to monitor how her department is using the company’s scarceresources. (Note that blank columns B–E will be filled with more detailed cost infor-mation about products in subsequent exhibits.)

Exhibit 4–5 shows that during the week CMD completed 380 measuring instru-ments of all models (cell G2) at a total cost of $5,104,500 (F12). Note that only theamount of labor traced to production of products is counted as a direct labor cost (F6).Unused labor is part of indirect production cost (F9). Subtotals of types of resourcecosts for all products manufactured also are in column F.

Cost of resourcessupplied is the valueof the resources madeavailable

Cost of resourcesused is the value ofresources consumed forproductive purposes

Out-of-pocket costsare the payments(usually cash orobligations to pay cash)made for resources

Actual costs usuallyare measured as thepast payments forcurrently ownedresources

Expected costs are thepredicted or forecastedpayments for futureresources

Product costs are costsof resources used toproduce products

Period costs are costsof resources used innonproduction value-chain elements

Total cost includes thecosts of all resourcesacquired or used duringa specified time period

6An imperfect market does not have reliable prices for all resources. Furthermore, alternative opportu-nities change because of technology, preferences, and information.

Average Cost

One could compute the average cost per unit of product by dividing total costs of a pe-riod (F12) by the number of units of product made that period (G2). Exhibit 4–5 com-putes this figure as $13,433 per unit (G12 � $5,104,500 � 380 units and also equalsG7 � G11, or the sum of average direct and indirect costs). Furthermore, the reportcalculates the average costs per type of resource. For example, during the week, manu-facturing each instrument cost an average of $2,197 in materials (G5) and $924 in con-version (G6). In addition to the easily traced direct costs, each instrument used anaverage of $5,790 of indirect production resources (G9) and $4,522 of indirect operat-ing resources (G10).

Appropriate uses of average costs. Average cost may be useful information; forexample, the vice president of manufacturing may compare average costs with histori-cal trends or expectations for the week. Also, the vice president of marketing may com-pare average costs (which include nonproduction costs) with competitors’ costs andaverage prices obtained for these instruments to assess overall profitability and effec-tiveness of pricing (i.e., average sales prices should exceed average costs).

Dangers of misusing average costs. The average cost usually does not representthe period’s spending for resources to make products because, as in CMD’s case, onlyacquiring material resources can be easily traced to decisions to make more products.

116 Part II Cost Measurement Systems

*Note: Columns B– E will be used in subsequent exhibits

Exhibit 4–5 Weekly Total Cost Information (excerpt)*

A B C D E F G

1 Model All Seven Models

2 Quantity 380

3 Average

Subtotal per Unit

4 Direct costs easily traced to production

5 Material cost (e.g., materials, parts, $ 834,800 $ 2,197assemblies supplied and used for �F5/G2products)

6 Conversion cost (e.g., labor used to make 351,200 924

products) �F6/G2

7 Total direct costs (� F5 � F6) 1,186,000 3,121

8 Indirect costs not easily traced

9 Indirect production cost (e.g., unused 2,200,000 5,790labor, supervision, equipment, � F9/G2maintenance, facilities used to makeproducts)

10 Indirect operating cost (e.g. 1,718,500 4,522management, support services � F10/G2facilities used to operate the business)

11 Total Indirect costs $3,918,500 $10,312

12 Total costs $5,104,500 $13,433

Average cost per unitof product is total costsof a period divided bythe number of units ofproduct made thatperiod

Chapter 4 Measuring Costs of Operations 117

Other resource spending does not change with decisions to make more or fewer unitsof product. Thus, a decision to make more “average” products would not cause CMDto spend $13,433 more for each unit made. If some resources, for example, labor, haveexcess capacity, CMD probably would not spend more on labor unless the excess ca-pacity were to be exhausted.

The average product may not exist except as a mathematical computation of aver-age cost. Therefore, if different products use varying amounts of constrained resources,then some products use more resources than the average, and some use less. In organi-zations with different products and services, average cost usually is not a meaningfulnumber for making decisions about the uses of capacity. If CMD only relied on the av-erage cost for all models, the company could fail to improve its use of scarce resources.For example, though the average price may exceed average cost, which is necessary foroverall profit, some products may be very unprofitable (e.g., cost of resources used ex-ceeds sales revenues) and others may be highly profitable. CMD should stop using itsresources to make the unprofitable products and use the resources to make profitableones, but average cost information alone does not identify which products to drop orexpand.7

Tracing versus Allocating Costs

As discussed in detail in Chapters 5 and 6, organizations usually trace direct costs toproducts and services. Tracing costs means assigning resource costs to products andservices (or organization subunits) through reliable observations and documentation ofresource use. Therefore, organizations rarely use the overall average cost for decision-making because it is cost-effective to trace some costs. That is, the costs of tracing areless than the costs of production errors based on average costs (e.g., producing thewrong products). More details of the week’s output and costs of resources used are inExhibit 4–6. [Put a place marker or paper clip on this exhibit because we will refer toit often. Note that some of the numbers are rounded to the nearest dollar. Note also thatfor simplicity this exhibit gives details for only two of CMD’s seven product models,#700A and #900B.]

When managers use the average cost per unit, they act as if each product modelconsumes $3,121 in traceable, direct cost (G7 � F6 � G2 � G5 � G6). It is apparentfrom rows 5, 6, and 7 of Exhibit 4–6, however, that the different product models usedifferent amounts of direct resources. CMD has traced materials and conversion re-sources to each product model type. At the low end of resource use, Model #700A uses$2,200 (C7) of direct material and conversion cost per unit (C7 � C5 � C6 or B7 �C2). Model #900B, at the high end, uses $4,200 (E7) of direct material and conversioncost per unit, almost twice as much as Model #700A. Most of the difference betweenthese products is the costs of materials (row 5). Although CMD does not do so, otherorganizations may trace use of some marketing and distribution resources directly toproducts and services.

These per-unit measures of direct material and conversion costs themselves appearto be averages. Because CMD has traced these resources to each product line, theseproduct-line averages (cells C5 to C7 and E5 to E7) should be closer to real (but stillunmeasured) per-unit costs than the overall average cost (cells G5 to G7). Some orga-nizations are able to easily trace direct costs to individual units of product or servicewithout averaging. This situation is discussed in Chapter 6.

7Recall that most introductory microeconomic models assume that the firm produces a single product ina perfectly competitive market. In this simplified setting, the most efficient use of productive resources is toproduce the number of units that minimizes that average cost per unit. The production of multiple productsand the real possibility of imperfect markets complicate this simple situation.

Tracing costs isassigning direct costs toproducts and services(or organization sub-units) through reliableobservations anddocumentation ofresource use

Allocating indirect costs. Exhibit 4–6 shows that CMD allocates costs of indirectresources to all products by a rough averaging process because it is too costly to tracethose resources more precisely. Cost allocation means attaching or assigning indirectcosts to products, services, or organizational units by some reasonable but imprecisemethod of averaging. Note that C9 � E9 � G9 and C10 � E10 � G10. These equal,indirect costs per unit for production and operating costs show that CMD did not at-tempt to trace these indirect costs to the product-model level. CMD simply averagedthese costs across all units of product. This can be the least accurate way to allocatecosts, but allocating costs in general is less accurate than tracing costs because allocat-ing costs cannot rely on ready observation or documentation of resource use or spend-ing. In fact, at CMD it appears that allocated indirect costs may be unrelated toresource use.

Cost allocation unrelated to resource use is undesirable if more accurate methodsare cost-effective. There are methods of allocating indirect costs to products and ser-vices that can reflect resource use more accurately, and these are discussed in laterchapters. Chapter 5 presents a method (activity-based costing), for example, that maybe able to trace a large proportion of these indirect resources to products and servicesin a cost-effective manner. In effect, more accurate cost allocation methods seek totransform indirect costs into direct costs. If successful, these methods should providemore accurate measures of resource use.

Unit-Level Costs and Variable Costs

As we have seen, it is relatively easy to observe the costs of direct resources such asparts and materials to make CMD’s devices. Costs of direct resources that are suppliedand used on individual products and services also are called unit-level costs. Unit-level costs to produce and sell products and services usually include costs of parts andmaterials and may include costs of production resources such as labor and energy, and

118 Part II Cost Measurement Systems

Exhibit 4–6 Weekly Cost and Production Information

A B C D E F G

1 Model #700 A #900 B All Seven Models

2 Quantity 48 40 380

3 Average Average Average

Subtotal per Unit Subtotal per Unit Subtotal per Unit

4 Direct costs

5 Material cost $ 67,200 $ 1,400 $124,000 $ 3,100 $ 834,800 $ 2,197

6 Conversion cost 38,400 800 44,000 1,100 351,200 924

7 Total direct costs $105,600 2,200 $168,000 4,200 $1,186,000 3,121

8 Indirect costs

9 Indirect production cost 277,894 5,790 231,579 5,790 $2,200,000 5,790

10 Indirect operating cost 217,074 4,522 180,895 4,522 1,718,500 4,522

11 Total Indirect costs $494,968 10,312 $412,474 10,312 $3,918,500 10,312

12 Total costs $600,568 $12,512 $580,474 $14,512 $5,104,500 $13,433

Unit-level costs arecosts of directresources that areacquired and used onindividual products andservices

Cost allocation isattaching or assigningindirect costs toproducts, services, ororganizational units bysome reasonable butimprecise method ofaveraging

Chapter 4 Measuring Costs of Operations 119

nonproduction resources such as marketing and distribution—if they are acquired tosupport specific products or services. In many cases, however, organizations acquirethese latter resources as indirect resources of production. If costs of using these indirectresources vary with the volume of units of products and services provided, they oftenare called variable costs. This term can be misinterpreted unless it is used very care-fully. Making or selling more or fewer products and services will cause the costs of us-ing these resources to vary up or down. These are variable costs of the use of indirectproduction resources. For example, making more laser instruments will use moreskilled labor at CMD; we know this because the use of skilled labor easily can betraced to the additional laser instruments manufactured.

However, making or selling more or fewer products and services may not causecosts of supplying these resources to vary up or down. To repeat, CMD hires skilledtechnicians to manufacture its laser instrument assemblies, but the company pays themfor at least 40 hours per week, even if they do not have enough demand for laser in-struments to keep them busy for 40 hours per week. Therefore, the costs of usingskilled technicians to make laser instruments may vary with quantities of productsmade, but the costs of supplying (paying the wages and benefits for) skilled technicianswill not vary unless CMD decides to hire or lay off technicians.

Failing to make the distinction between the costs of supplying (e.g., spending for)resources and using resources has caused much confusion and controversy among costmanagers, accountants, financial analysts, and engineers. We need to be clear aboutthis, and we will identify unit-level costs as those incurred for resources that are bothsupplied and used to provide units of products and services. Variable cost refers to thecosts of resource use that vary with the volume of units of product and service pro-vided. As Exhibit 4–7 shows, all unit-level costs are variable costs, but not all variablecosts are unit-level costs.

Fixed Costs, Committed Costs, and Sunk Costs

For many years, accountants have used the term, fixed costs, for production or non-production costs that do not vary with production or sales volumes. These have in-cluded such costs as salaries, rent, depreciation, and property taxes. As we have arguedthroughout this book, however, decisions cause costs—costs do not just happen—andthere are many more decisions made than just production volume. No resource

Exhibit 4–7

Unit-Level andVariable Costs

Costs ofdirect

resourcessupplied and

used toprovide unitsof product or

service

Costs ofindirect

resourcesused to

provide unitsof product or

service

Costs ofdirect and

indirectresources

used toprovide unitsof product or

service

+ = Variablecosts

Unit-levelcosts

Fixed costs are coststhat do not vary withproduction or salesvolumes

Variable costs arecosts of resourceswhose use varies withthe volume of units ofproducts and servicesprovided

decisions are irreversible. All future costs, therefore, are variable with respect to somedecision, so no future cost can be really fixed. It may be costly to change a resourcecost in the future (e.g., renegotiate or nullify a resource contract), but the resource costcan be changed. A better term to use for costs that are not intended to vary with pro-duction or sales volume may be committed cost. This term reflects that the organiza-tion has committed to a certain level and type of resource spending, but theorganization also (at some further cost perhaps) can change the commitment.

In most organizations, labor cost is a committed cost and cannot be changed easilybecause of contractual obligations, policy, or its critical importance. Other committedcosts may include lease obligations, licenses, and various taxes. In contrast, dis-cretionary costs, such as some advertising costs, remodeling, or charitable giving,may be changed quickly and easily. This is a difference of degree; that is, both com-mitted and discretionary costs can be changed, but committed costs are more difficultto change.

When labor is a committed cost, as in many unionized companies or organizationsand countries with strong employment policies, making more or fewer units of productmay not affect the cost to supply labor, positively or negatively. If so, spending for la-bor resources is not different from spending for other physical capacity resources. Inorganizations where this is true of other resources as well, the only unit-level cost ofproducts and services that varies proportionately with the number of units producedmay be the cost of parts and materials. Under these conditions, spending or costs tosupply all other resources would not vary with the number of units.

Furthermore, the organization may or may not use all of the resources to which ithas committed. For example, as discussed in Chapter 3, an organization may committo provide a certain level of production capacity, but may choose to reserve some ofthat capacity for unforeseen needs and may have idle capacity that it cannot use.

Sunk costs. Many organizations have made payments in the past to acquire re-sources that they now control. The amounts of these payments usually are recognizedas the costs of resources that are expected to be used in the future (these resources withfuture benefits are, of course, assets). These resources often include equipment, build-ings, and purchased technology or knowledge. Should you consider the costs of theseresources when making production decisions? That is, should the past payments forthese resources be part of the costs of future products and services? The correct answeris no; past payments for resources are sunk costs—they cannot be undone. Just as withany other resource, only the opportunity costs of these already acquired resourcesshould be counted as part of the cost of future products and services. If these resourceshave no alternative use or value (that is, they cannot even be sold to others), it does notmatter how much you paid for them, their opportunity cost is zero.

As a practical matter, however, many companies count the past payments forresources as part of the cost of current and future products and services. Why? One rea-son is that measuring opportunity costs of all resources is too difficult, so organizationsassume that past purchase prices approximate current opportunity costs. Also, financialand tax reporting rules in most countries, including Canada, require that assets be val-ued at book values, which are their purchase prices, net of accumulated depreciation oramortization. More precisely: at the lower of book or market value. As those resourcesare used, accounting for that use reduces these asset values by the amount of past costsused. Thus, many organizations count the use, depreciation, depletion, and amortiza-tion of existing assets as costs of current and future products and services even thoughthese costs may be sunk costs or allocations of sunk costs. Another, less justifiable rea-son may be that managers are unwilling to admit that payments for resources have beenwasted, so they continue to value resources at their book value unless they are requiredto write down the assets to a lower value.

120 Part II Cost Measurement Systems

Sunk costs are pastpayments for resourcesthat cannot be undone

A committed cost is acost that is not intendedto vary with productionor sales volume

Discretionary costsmay be changedquickly and easily

Chapter 4 Measuring Costs of Operations 121

Alternative Costing MethodsIf supplying and using resources result in different measures of costs, which costsshould managers use to solve the problem of how to generate the most profit from con-strained capacity? This cost management issue is: Should managers base productiondecisions on the profitability of products and services using costs of using resources orcosts of supplying resources?

There is considerable, unresolved controversy among managers, consultants, andprofessors about this. Some argue that the answer is always to base production deci-sions on expected supply of unit-level resources since that mirrors the immediate cashflow impacts of decisions. Others argue that costs of resource use, which often requireaveraging of some past, committed, or indirect costs over units produced, are more ef-fective, long-term measures of the profitability of production decisions because, afterthese resources are used, they must be replaced. We will consider implications of botharguments.

Consider Exhibit 4–8, which Glenn Penski prepared to analyze the costs of differ-ent models of CMD’s devices produced during the week. This exhibit uses the basiccost information from Exhibit 4–6 (rows 1 through 12) but combines it in several dif-ferent ways to create different measures of product cost—throughput cost, variablecost, and absorption cost—newly added rows 13 through 15. For simplicity, the exhibitshows details for only two of CMD’s seven models, #700A and #900B, because theyare most different in their use of resources.

Throughput Costing

Those who argue that managers should base production decisions on resource supplyand use also argue that costs of products and services should be based on throughputcosting. Throughput costing measures only unit-level costs as the costs of products orservices. Advocates of throughput costing argue that adding any other indirect, past orcommitted costs to product cost creates improper incentives to drive down the averagecost per unit by making more parts and assemblies on nonbottleneck processes. Sincethese other costs are committed, making more units with the same level of resourcespending arithmetically reduces the average cost per unit and makes the production

Cost Classifications and Decision Making

Refer to Exhibit 4–6 and the preceding discussion. Put yourself in Glenn Penski’s position and re-spond to these comments from co-workers

(Solutions begin on page 135.)

a. “I don’t see the need to develop complex measures of costs of our devices; average cost is fine.We know our products are the best in the industry and we have long backlogs of orders. All weneed to do is make as many devices as we can and charge as much as we can for them.”

b. “You say that you have measured direct costs more accurately by tracing them to differentmodels, but it looks like they are just another average cost at the model level. How is that animprovement over using overall average cost?”

c. Assume that CMD made 25 more of model 900B, increasing total production to 405 units forthe week. Direct material costs per unit remained as before for all models (e.g., C5, E5), as didthe sum of total conversion cost (F6) and indirect cost (F11). In other words, the only total costthat increased was direct materials cost. What do these changes and lack of changes in thevarious costs indicate about Glenn’s classifications of costs? Would allocated costs change?Explain.

d. Are there any possible adverse effects of a decision to make 25 more of model #900B?

You’re the

DecisionMaker 4.1

LO2 Comparealternative product costsand their effects onprofits.

Throughput costingmeasures only the unit-level spending fordirect costs as the costsof products or services

process appear to be more efficient. Throughput costing avoids that incentive becausethe cost per unit depends only on unit-level spending (e.g., costs of materials), not howmany units are made.8

Using throughput costing means that cost managers must distinguish between(1) spending for resources that is caused by the decision to produce different levels of

products and services and (2)use of resources that the orga-nization has committed to sup-ply, regardless of the level ofproducts and services pro-vided. At CMD, Glenn Penskidetermined that only the costsof materials (row 5 of Exhibit4–8) qualify as throughputcosts (row 13) because CMDhas committed, at least for thetime being, to supply all otherresources (manufacturing la-bor, equipment, management,

122 Part II Cost Measurement Systems

8This statement ignores possible effects of gaining or losing quantity discounts on purchases by chang-ing production levels. These effects usually are small, but they would be considered as a benefit or cost ofchanging purchasing levels.

Exhibit 4–8 Weekly Alternative Product Costs

A B C D E

1 Model #700 A #900 B

2 Quantity 48 40

3 Average AverageSubtotal per Unit Subtotal per Unit

4 Direct (variable) costs

5 Unit-level material cost $ 67,200 $ 1,400 $124,000 $ 3,100

6 Variable conversion cost 38,400 800 44,000 1,100

7 Total direct costs 105,600 2,200 168,000 4,200

8 Indirect costs

9 Indirect production cost 277,894 5,790 231,579 5,790

10 Indirect operating cost 217,074 4,522 180,895 4,522

11 Total indirect costs 494,968 10,312 412,474 10,312

12 Total costs $600,568 $12,512 $580,474 $14,512

13 Throughput cost per unit (C5; E5) $ 1,400 $ 3,100

14 Variable cost per unit (C7; E7) $ 2,200 $ 4,200

15 Absorption cost per unit (C7 � E9; E7 � E9) $ 7,990 $ 9,990

Balancing productionprevents built-up of excessinventories of cabinets inprocess at all work stations.

Chapter 4 Measuring Costs of Operations 123

facilities, and so on) regardless of how many measuring devices it makes. Throughputcosting considers all other indirect, discretionary, committed, or past spending for re-sources to be operating costs of the period. Note that some organizations may pay forits labor force or other resources such as energy consumption on an hourly or piece-rate basis depending on how many units of product are made. Because these resourcesare supplied and used on an hourly or piece-rate basis, these would be unit-level costsand product costs for throughput costing.

Variable Costing

Variable costing measures the cost of a product or service according to the resourcesused to provide it. At CMD, Penski measured the variable costs of the company’s prod-ucts in row 14 of Exhibit 4–8. Variable costs at CMD include the unit-level materialcosts (row 5) and the variable conversion costs (row 6) that have been traced to the pro-duction of each product-model line. Thus, CMD’s variable costs are unit-level mater-ial costs plus variable costs of conversion resources used. At other organizations,variable costs may include variable costs of production and sales, distribution, andother used operating resources, the uses of which are traced to products and services.

Note the similarity between variable costing and throughput costing. The only dif-ference is that variable product costs include traced costs of resources used even if ad-ditional spending is not required to supply the resource. As shown, CMD’s variablecosts include the (conversion) costs of its skilled laser-manufacturing technicians usedto make instruments even though CMD pays these technicians a salary.

Absorption Costing

Absorption costing (full costing or full absorption costing9) allocates indirect pro-duction costs to products in addition to unit-level and variable production costs. Notethat because absorption costs conform to financial reporting rules, absorption costs donot include nonproduction costs that may be unit-level or variable costs. Thus, absorp-tion costs are variable production costs plus allocated indirect production costs. Ob-serve that in some organizations absorption costs may not be a simple addition ofvariable costs and allocated indirect costs because absorption costing distinguishes be-tween production and nonproduction resources. Absorption costing counts any variablecosts that are from nonproduction resources as operating expenses. CMD’s situation issimpler because all indirect, nonproduction costs are committed costs.

Bertch Cabinet Manufacturing, Inc., recently adopted synchronous manufacturing, which is a directapplication of the theory of constraints. The company credits this change with reducing cycle times,reducing batch sizes, improving material flow, reducing and better-managing inventory, increasingmorale, and improving customer satisfaction. Bertch’s cost managers had developed a very com-plex costing system but decided to greatly simplify it by converting to throughput costing to be con-sistent with internal decision-making based on TOC. They defined throughput costs as payments toexternal parties for raw materials, components, subcontracted work, sales commissions, trans-portation, and custom duties on international sales. This allows managers to accurately measure theprofit (or throughput) per unit of bottleneck resource for each product in the Bath Cabinet, CulturedMarble Top, Kitchen Cabinet, and Semi-Custom divisions.

Source: J. MacArthur, “From Activity-Based Costing to Throughput Accounting.”

Cost Management in

Practice 4.2

Variable costingmeasures the cost of aproduct or serviceaccording to the unit-level resources used toprovide it

9One cannot observe products consuming indirect resources, but accountants say the products absorbthe costs of indirect resources. Full absorption costing indicates that the full range of production costs is usedto measure the costs of products.

Absorption costing(full costing or fullabsorption costing)allocates indirectproduction costs toproducts in addition tounit-level or variableproduction costs

Operating costs of theperiod are the totalcosts of non-unit-level,past, or committedresources for allproducts

Absorption costing requires judgments or simplifying assumptions about howproducts consume indirect production resources. There are many ways to implementabsorption costing. The simplest way would be to divide total indirect production costsequally across all units of product produced, as CMD did in Exhibit 4–6 and as shownin C9 and E9 of Exhibit 4–8.

Absorption costs (C15 and E15 of Exhibit 4–8) may be more accurate measures ofthe consumption of production resources than either throughput or variable costs (rows13 and 14) because absorption costs do recognize and contain indirect productioncosts. However, just as the overall average cost may misstate product costs, by allocat-ing indirect production costs, absorption costs may misstate consumption of indirectproduction resources. It is possible that CMD’s product models use indirect productionresources to a different degree. Absorption costing also ignores products’ use of non-production resources. Thus, absorption costing actually may distort the costs to provideproducts and services if they have greatly different levels of support from indirect re-sources. For example, one product may need much more engineering design supportthan another, but allocations unrelated to resource use or treating the cost as an operat-ing cost obscure this difference. Exhibit 4–9 shows that absorption costs are variableproduction costs plus allocated indirect production costs.

124 Part II Cost Measurement Systems

Exhibit 4–9

Absorption CostsCosts of

direct andindirect

productionresources

used toprovide unitsof product or

service

Allocations ofcosts ofindirect

productionresources not

traced toproducts or

services

Absorptioncosts+ =

VariableProduction

Costs

Approximately 48 percent of Canadian companies use variable costing in their internal accountingsystems. For financial reporting purposes in Canada, the Canadian Institute of Chartered Accoun-tants (CICA) Handbook advocates, but does not require, absorption costing. The Canada Customsand Revenue Agency (CCRA) does not explicitly require absorption costing either. However, it doesrequire that firms be consistent for both financial statements and tax purposes. This results in mostfirms using absorption costing for external reporting purposes.

For example, see S. Inoue, “A Comparative Study of Recent Development of Cost ManagementProblems in U.S.A., U.K., Canada, and Japan,” C. Drury and M. Tayles, “Product Costing in UKManufacturing Organisations,” and E. Shim and E. Sudit, “How Manufacturers Price Products.”

Sources: CICA Handbook, Section 3030 CCRA Interpretation Bulletin No. 473

Research

Insight 4.1

Global

Chapter 4 Measuring Costs of Operations 125

Financial Management of ProcessesWhether one is an advocate of throughput, variable, or absorption costing, there is gen-eral agreement that organizations should manage four financial measures of processes:contribution to profit (per unit, product, and overall), operating expense, inventory, andoperating income.10 If these measures are designed properly (and this is a source of de-bate because of alternative ways of measuring costs), they will reinforce the propermanagement of constrained resources to generate the most profit.

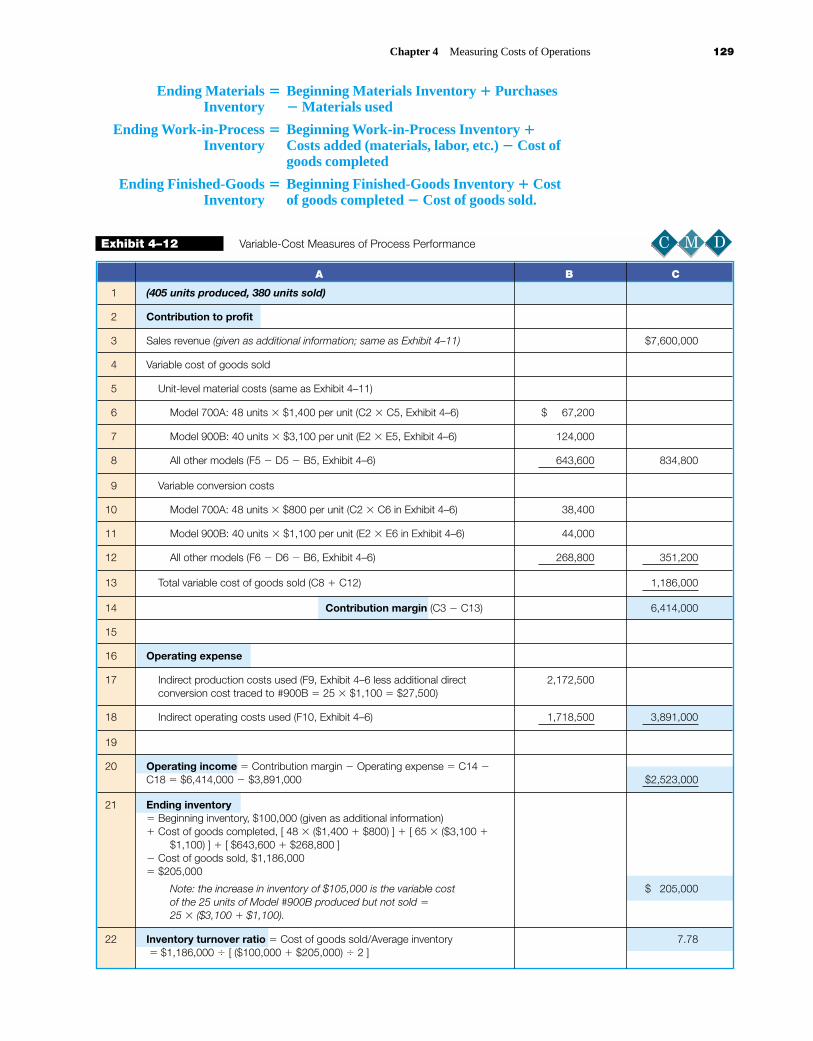

Exhibit 4–10 outlines the three different approaches to product costing and the cor-responding financial measures of process performance. We discuss contribution toprofit, operating expense, and inventory calculations for each costing method sepa-rately. Then, we discuss operating income for the methods together because the con-trasts are most interesting and demonstrate potential conflicts among the methods.

Exhibits 4–11, 4–12, and 4–13 present the financial measures of performance foreach costing method. To show the effects of different costing methods, these exhibitsassume that:

� CMD produced 65 units of Model #900B but sold 40. � Consequently, twenty-five units of Model #900B were added to inventory. � The only spending increase was for direct cost because this increased production.

All other spending as shown in Exhibit 4–6 was unchanged. � All units of other models produced were sold.

Costs of the other models may be found by subtracting costs for #700A and #900Bfrom total costs. (Hint: If you have not worked through You’re the Decision Maker4.1, it would be a good idea to do so now.)

10CMD, like many other companies, uses nonfinancial measures of performance as well as these finan-cial measures. Other chapters discuss this important aspect of measuring performance.

Exhibit 4–10 Measures of Process Performance per Time Period

Costing Approach

Financial Measure Throughput Costing Variable Costing Absorption Costing

Contribution to profit Throughput � Sales � Contribution margin � Gross margin � Sales �Unit-level cost (spent) Sales � Variable Absorption cost ofof goods sold costs (used) of goods sold goods sold

Operating expense Other costs incurred to Other costs incurred to Nonproduction coststransform inventory transform inputs into incurred to transforminto throughput completed products inputs into completed

and goods sold products and goods sold

Inventory All costs used to acquire Variable costs of Full costs of products inobjects for sale products in process or process or completed

completed but not sold but not sold

Inventory (asset) turnover Inventory turnover Inventory turnover

Operating income Throughput � Operating Contribution margin � Gross margin � operatingexpense Operating expense expense

Throughput Costing

Contribution to profit. Throughput costing uses throughput, which is sales revenueless the unit-level cost of goods sold, as the measure of contribution to profit. Rows 2–8 of Exhibit 4–11 show the calculation of throughput for the week. Sales revenue inrow 3 had not been given before in this chapter, but this amount is the total revenueearned from the sale of all products in the week. Information about the costs of prod-ucts other than models #700A and 900B is given in this exhibit as well. Note that onlythe direct material costs of the units that were sold are recognized as throughput cost ofgoods sold. Row 5 counts the unit-level material cost of all 48 units of Model #700Athat were made and sold during the week. However, even though CMD made 65 unitsof Model #900B, only the cost of the 40 units sold is recognized as cost of goods sold(row 6). The cost of the other 25 units that were produced but not sold is added to in-ventory, as shown in subsequent rows of Exhibit 4–11. The unit-level material cost ofthe 292 other model units made and sold also count as throughput cost of goods sold.Subtracting the total cost of goods sold (C7) from sales revenue (C3) yields the week’sthroughput, C8.

126 Part II Cost Measurement Systems

Throughput is salesrevenue less thethroughput cost ofgoods sold, as thecontribution to profit

Exhibit 4–11 Throughput Measures of Process Performance

A B C

1 (405 units produced, 380 units sold)

2 Contribution to profit

3 Sales revenue (given as additional information) $7,600,000

4 Throughput (unit-level) cost of goods sold

5 Model 700A: 48 units � $1,400 per unit (C2 � C5, Exhibit 4–6) $ 67,200

6 Model 900B: 40 units � $3,100 per unit (E2 � E5, Exhibit 4–6) 124,000

7 All other models (F5 � D5 � B5, Exhibit 4–6) 643,600 834,800

8 Throughput (C3 � C7) 6,765,200

9 Operating expense

10 Conversion costs (F6, Exhibit 4–6) 351,200

11 Indirect production costs (F9, Exhibit 4–6) 2,200,000

12 Indirect operating costs (F10, Exhibit 4–6) 1,718,500 4,269,700

13

14 Operating income � Throughput � Operating expense(C8 � C12 � $6,765,200 � $4,269,700) $2,495,500

15 Ending assets (Throughput inventory)� Beginning assets, $2,700,000 (given as additional information)� Cost of goods completed, (48 � $1,400 � 65 � $3,100 � $643,600)� Cost of goods sold, $834,800� $2,777,500 $2,777,500

Note: The increase of $77,500 in inventory is the unit-level costof the 25 units of Model #900B that were made but not sold� 25�$3,100.

16 Asset (Throughput inventory) turnover ratio � Sales/Averagetotal assets � $7,600,000 � [ ($2,700,000 � $2,777,500) � 2 ] 2.77

Chapter 4 Measuring Costs of Operations 127

Managers would make decisions about best uses of capacity by comparingthroughputs of each alternative product mix, which is the relative proportions or num-bers of products, for example, the number of Model #700A, Model #900B, and othermodels produced. If a different product mix promised a higher total throughput, itwould be preferred to the mix shown in rows 5–7 of Exhibit 4–11. Proponentsof throughput costing say that only this approach is designed to identify the profit-maximizing product mix.

Operating expense. In general, operating expense is all operating costs of theperiod that are not counted in cost of goods sold or inventory. In throughput costing atCMD, operating expense (C12) is all operating costs of the period other than materialscost. Because costs of supplying these resources does not vary with levels of produc-tion, operating costs include conversion costs (B10), indirect production costs (B11),and indirect operating costs (B12). If these are past or committed costs, some argue thatthey can be ignored for the decision of choosing the best use of capacity. The productmix that fully utilizes the bottleneck process and generates the highest expectedthroughput is the best use of capacity.11 In concept, this approach to management ap-pears to be mechanical and almost error-free. However, this approach also can haveshortcomings if it is applied naïvely or to large organizations as a whole.

Even if costs are correctly identified as throughput or operating expense, failing toanalyze operating costs could lead to treating them as fixed costs that cannot change.In fact, the organization can and should analyze whether it can manage throughput andoperating costs more efficiently. In addition, choosing the overall product mix impliescentralized management, where a few managers direct the operations of an entireorganization. This may be feasible at a small company like CMD, but it has proved tobe unwieldy and ineffective in most large organizations. Centralized management usu-ally is too slow and inflexible to meet new challenges. In order to compete more effec-tively, most large organizations have decentralized decision-making authority tosmaller business units or even to individual employees.

Inventory. Inventory, in general, is the cost of materials and products either inprocess or completed but not sold. In throughput costing, all costs (other than operat-ing expense) of unsold resources that an organization had acquired are considered in-ventory (B15). This unusual definition of inventory indicates that all the resources ofthe organization (normally termed assets—including land, buildings, and equipment)are intended to generate goods for sale and are themselves potentially for sale. Notethat throughput costing still only counts unit-level costs as cost of goods sold, however.

The ending assets (throughput inventory in C15) for the week are computed asshown in row 15 by adding changes in assets to the beginning assets. For simplicity, weassume CMD made no net purchases or sales of other assets, so the only change in as-sets is the change in product inventory. That change is the cost of goods completed lessthe cost of goods sold. CMD made 25 more units of Model #900B than it sold, so thethroughput cost of those units is the net increase to inventory.

A throughput measure of the use of inventories is the asset turnover ratio (C16),which is sales revenue divided by average asset level. Since high levels of inventoriestie up scarce monetary and physical resources, low inventory levels are desirable.However, there should be enough inventories on hand to allow for unforeseen varia-tions in needs. Otherwise, bottleneck processes may not have parts and assemblies towork with, and irreplaceable bottleneck time would be lost. These ratios are most use-ful as performance benchmarks. Increasing inventory turnover ratios over time indi-cates improved use of inventories, and vice versa. Comparing inventory turnover ratiosacross organizations that use the same costing method indicates relative efficiencies of

The product mix is therelative proportions ornumbers of productsproduced

11Linear programming is a mathematical technique consistent with throughput costing that can be usedto select the mix of products that maximizes the contribution to profit subject to constrained resources.

Operating expense isall operating costs ofthe period deductedfrom revenues that arenot counted in cost ofgoods sold or inventory

Centralizedmanagement is thedirection of theoperations of an entireorganization by a fewmanagers

Decentralizeddecision-making is thefreedom of managers at various levels of theorganization to makedecisions withoutintervention fromcorporate head office

Inventory is the cost ofmaterials and productseither in process orcompleted but not sold

The asset turnoverratio is sales revenuedivided by averageasset level

the use of inventories. Inven-tory turnover ratios are notcomparable across differentcosting methods since themethods value inventoriesdifferently.

Variable Costing

Exhibit 4–12 presents the vari-able-cost financial measuresof performance, also assumingthat CMD produced 65 unitsof Model #900B but sold 40.As before, only material-cost

spending increased with this increased production. All other spending as shown previ-ously in Exhibit 4–6 was unchanged, and all other model units produced were sold.

Variable costing uses the contribution margin (C14), which is sales revenue (C3)less variable costs of goods sold (C13), as the measure of contribution to profit. Vari-able cost of goods sold is calculated in rows 4 to 13 and includes unit-level materialsand variable conversion costs (and in other organizations any variable support andmarketing/distribution costs). The variable cost of goods sold (C13) is computed byadding the unit-level material costs (C8), which are the same as in Exhibit 4–11, to thevariable conversion costs of Models #700A and #900B from Exhibit 4–6. These calcu-lations appear in rows 10 and 11. To these we also add the variable conversion costs ofthe other 292 units made and sold (B12) to obtain the total variable conversion cost(C12). Note that the variable costs of the additional 25 units of Model #900B made butnot sold are added to inventory, as discussed later.

Using variable costs and the financial criterion of maximizing the contribution toprofit, managers would select the product mix that they expect to generate the highestcontribution margin (C14).

Operating expense. In variable costing, operating expense (C18) is all indirect costsof the period, including both indirect production (B17) and indirect operatingcosts (B18).

Note that the total amount of indirect production cost (B17) is $27,500 less than inExhibit 4–11. All costs must be accounted for. What happened to this amount of cost?It is now part of cost of goods completed but not sold—added to inventory. The addi-tional 25 units used an additional $27,500 of conversion resources (� 25 � $1,100)used and traced to the production of Model #900B. Previously for throughput costingin Exhibit 4–11, the total amount of conversion cost is part of operating expense; noneof it was counted as a product cost. In contrast, for variable costing any variable costused is traced to units produced and counted as product cost, and only the unused por-tion of conversion cost is part of operating expense.

Inventory. In manufacturing organizations like CMD, variable (and absorption) cost-ing methods measure three types of inventory resources or assets: materials, work-in-process, and finished-goods inventories. Materials Inventory is measured at theacquisition price of the materials (including purchase cost, transportation, etc.) avail-able for use. Work-in-Process Inventory is measured as the cost of materials, labor,and other production resources added thus far to products that are not yet completed.Finished-Goods Inventory is measured as the production costs used to make productsthat have been fully completed but not yet sold. All production costs first are accumu-lated in Work-in-Process Inventory. As items are completed, they are then transferredto Finished-Goods Inventory. All beginning and ending inventories are related simi-larly as shown in the following equations:

128 Part II Cost Measurement Systems

Saturn’s “ski-lift” systemenables smooth flow ofautomobiles throughprocesses.

Contribution marginis sales revenue lessvariable costs of goodssold

Work-in-ProcessInventory is measuredas the cost of materials,labor, and otherproduction resourcesadded to products thatare not yet completed

Finished-GoodsInventory is measuredas the production costsused to make productsthat have been fullycompleted but not yetsold

Chapter 4 Measuring Costs of Operations 129