Embed Size (px)

Citation preview

Chronicle Of The Neville Wadia Institute Of Management Studies And Research ISSN 2230-9667

Feb., 2012

272

Financial management

IFRS Vs Indian Gaap - Some Key Differences

Mr. Santosh V. Rode Faculty of Management

Parikrama Group of Institution, AhmednagarResearch student of M.PHIL program at Brihan Maharashtra Collage of Commerce, Deccan, and Pune.

Introduction:

India has set a roadmap for convergence with International Financial Reporting Standards (IFRS) com-mencing from 1 April, 2011. The convergence with IFRS standards is set to change the landscape for financial reporting in India. IFRS represents the most commonly accepted global accounting framework as it has been adopted by more than 100 countries. With the growth of Indian Economy and increasing integration with the global economies, Indian corporate are raising capital globally. Under the circum-stances, it would be imperative for Indian corporate to adopt IFRS for their financial reporting.

While the Core Group of Ministry of Corporate Affairs (MCA) has recommended convergence to IFRS in a phased manner from 1st April, 2011 Indian corporate having global aspirations should consider earlier voluntary adoption. While there are several similarities between Indian GAAP and IFRS, still there are differences which can have significant impact on the financial statements. This paper is aim to bring out such aspects and a comparative analysis on Indian Generally Accepted Accounting Principles (Indian GAAP) vis-à-vis IFRS.

Objective of the Study:

The primary objective of study is explain the deference between the International Financial Regulation Standard (IFRS) and Indian Generally Accepted Accounting principles (GAAP). This study also aims to find out the contribution of IFRS and Indian GAAP. in setting accounting standard .

Scope and Limitations:

I am preparing this paper “IFRS Vs INDIAN GAAP - SOME KEY DIFFERENCES” to provide a broad understanding of IFRS requirements in India, some key differences between IFRS and Indian Account-ing Standards and IFRS requirements at the time of first time adoption. The preparation of financial statements complying with IFRS is the responsibility of the management and accordingly this paper does not replace the need for professional judgment having regard to relevant standards and other re-quirements.

Chronicle Of The Neville Wadia Institute Of Management Studies And ResearchISSN 2230-9667

Feb., 2012

273

Financial management

Source of Data:

This study mainly base on secondary data. This study explains the difference between IFRS and Indian GAAP. For this study, International Accounting Standard and Indian Chartered Accounting Institute Discloser reports has been used for explaining the deference between the IFRS and Indian GAAP and the data pertinent to IFRS and Indian GAAP has been collected from journals & magazines as well as the internet.

Ifrs Vs Indian Gaap: Some Key Differences

In this study try to cover the maximum accounting standards has been disclosed in accounting conven-tions like IAS 1, IAS 2, IAS 7, IAS 10, IAS 16, IAS 18, IAS 21, IAS 32, IAS 39 and IAS 40. Some key deference’s are explained as follows:

Topic Category Requirements as perIFRS

Requirements as per Indian GAAP

Compliance withGAAP

General Disclosure

Entities should make an explicit and unreserved statement in the notes that the financial Statements comply with IFRS.

There is a presumption that financial statements should be prepared in compliance with accounting standard to give a true and fair view.

True and fairview

The override does not apply where there is a conflict between local company law and IFRS; in such a situation, the IFRS must be applied.

True and fair override is generallynot permitted under Indian GAAP. Further in terms of hierarchy local legislations are more superior

Preparation andpresentation

Presentationanddisclosure

An entity has to present financial statements on a consolidated basis unless it meets the exemption criteria prescribed under IAS 27 para. 10

An entity has been to present financial statement on a stand alone basis. Accounting standard does not required entity to prepare or present consolidated financial statement

First timeadoption

IFRS 1 IFRS 1 specifically deals with how to apply IFRS for the first time.

Indian Accounting Standards does not give specific guidance on first time adoption of the standards by an entity.

Chronicle Of The Neville Wadia Institute Of Management Studies And Research ISSN 2230-9667

Feb., 2012

274

Financial management

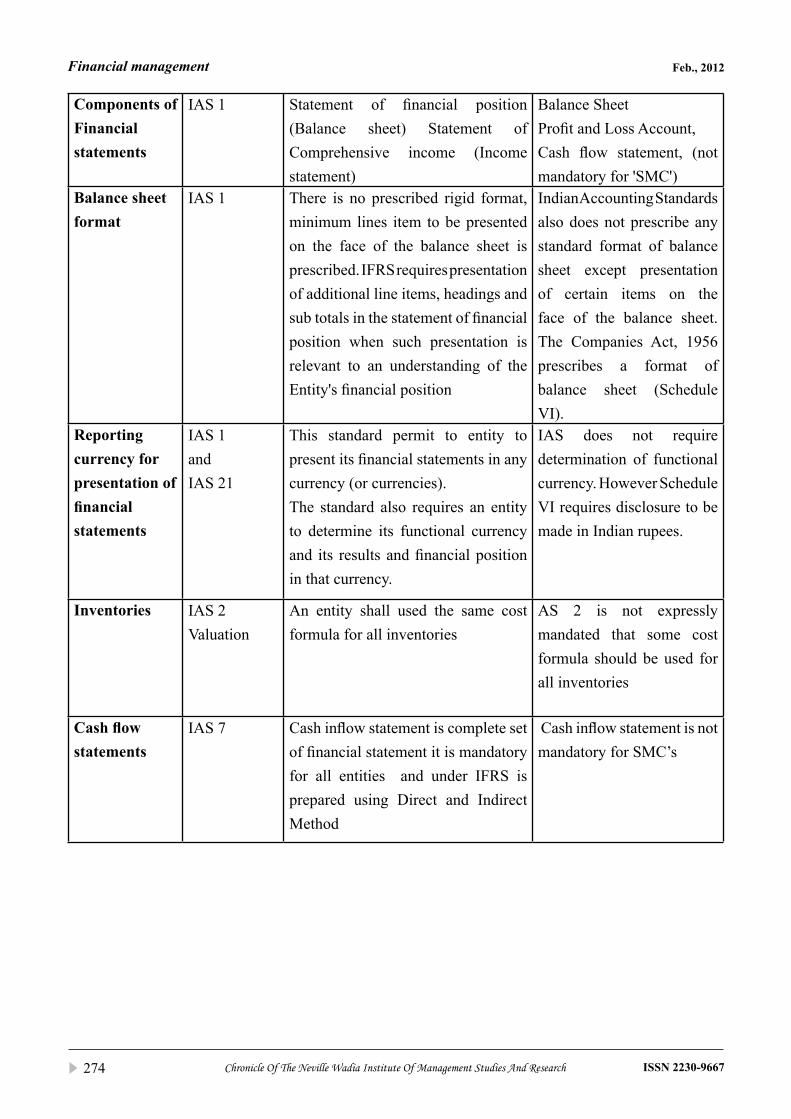

Components ofFinancialstatements

IAS 1 Statement of financial position (Balance sheet) Statement of Comprehensive income (Income statement)

Balance SheetProfit and Loss Account,Cash flow statement, (not mandatory for 'SMC')

Balance sheetformat

IAS 1 There is no prescribed rigid format, minimum lines item to be presented on the face of the balance sheet is prescribed. IFRS requires presentation of additional line items, headings and sub totals in the statement of financial position when such presentation is relevant to an understanding of the Entity's financial position

Indian Accounting Standards also does not prescribe any standard format of balance sheet except presentation of certain items on the face of the balance sheet. The Companies Act, 1956 prescribes a format of balance sheet (Schedule VI).

Reportingcurrency forpresentation offinancialstatements

IAS 1andIAS 21

This standard permit to entity to present its financial statements in any currency (or currencies).The standard also requires an entity to determine its functional currency and its results and financial position in that currency.

IAS does not require determination of functional currency. However Schedule VI requires disclosure to be made in Indian rupees.

Inventories IAS 2 Valuation

An entity shall used the same cost formula for all inventories

AS 2 is not expressly mandated that some cost formula should be used for all inventories

Cash flowstatements

IAS 7 Cash inflow statement is complete set of financial statement it is mandatory for all entities and under IFRS is prepared using Direct and Indirect Method

Cash inflow statement is not mandatory for SMC’s

Chronicle Of The Neville Wadia Institute Of Management Studies And ResearchISSN 2230-9667

Feb., 2012

275

Financial management

Contingenciesand EventsOccurring Afterthe BalanceSheet Date

IAS 10 RecognitionandMeasurement

An entity shall adjust the amounts recognized in the financial statements for events that provide additional evidence of conditions that existed at the balance sheet date and should not be adjusted for events that provide evidence of conditions that did not exist at the balancesheet date.

Under AS 4, non-adjusting eventsare required to be disclosed in the report of the approving authority.

DepreciationAccounting-ComponentApproach

IAS 16 Measurement Valuation

Change in the method of depreciation is treated as change in accounting estimates, reflected in the depreciation charge for the current and prospective years. Depreciation on revalued portion cannot be recouped out of revaluation reserve.

Change in depreciation method is treated as change in accountingpolicies and impact is determinedby retrospectively computing depreciation under new methodand the impact is recorded in theperiod of change. Depreciation on revalued portion is recouped out of revaluation reserve.

RevenueRecognition-Fair value ofconsideration

IAS 18 Revenue should be measured at the fair value of the consideration received or receivable. Where the inflow of the cash or cash equivalent is deferred, discounting to a present value is required to be done.

Revenue is measured by the charges made to the customers or clients for goods supplied or services rendered to them and bythe charges and rewards arising from the use of resources by them. In case of installment sales, discounting would be required.

Chronicle Of The Neville Wadia Institute Of Management Studies And Research ISSN 2230-9667

Feb., 2012

276

Financial management

Accounting for Investment -InvestmentProperty

IAS 40 Scope Investment property is property (land or a building or part of a building or both) held (by the owner or by the lessee under a finance lease) to earn rentals or for capital appreciation or both, rather than for:i) use in the production orsupply of goods or services orfor administrative purposes;ii) sale in the ordinary course of business

An investment property is an investment in land or buildingsthat are not intended to be occupied substantially for use by, or in the operations of, the investing enterprise.

Financial assets

IAS 32,39 Financial assets are classified in four categories:- financial asset at fair value through profit or loss,- held to maturity,- loans and receivables, and` available for sale

AS 13 requires classification of investments into long-term and current investments. AS 30, 31, 32 which are recommendatory up to 31 March, 2011 provide for classification of financial assets which are similar to IFRS.

Conclusion:

From 1st April, 2011 Indian corporate having global aspirations should consider earlier voluntary adop-tion. While there are several similarities between Indian GAAP and IFRS, still there are differences which can have significant impact on the financial statements. Above given explanation is aim to bring out such aspects and a deference on Indian Generally Accepted Accounting Principles (Indian GAAP) vis-à-vis IFRS.

Bibliography:IFRS in India- key aspect. Astute Consulting Group.•International Accounting Standards Board (2007): • International Financial Reporting Standards 2007 (including International Accounting Standards (IAS(tm)) and Interpretations as at 1 January 2007),LexisNexis, ISBN 1-4224-1813-8Wiley Guide to Fair Value Under IFRS [4]•

![17_indian Gaap vs Ifrs[2]](https://img.dokumen.tips/doc/110x75/577d2f631a28ab4e1eb1934d/17indian-gaap-vs-ifrs2.jpg)