Embed Size (px)

Citation preview

IFRS for SMEs - does one size fit all?

CPA PNG Lae conference

August 2017

Presented by Stephen Beach

Partner, PwC

• www.pwc.com/pg

PwC

CPA PNG

2005 Lae Conference

• IFRS: Does one size fit all?

PwC

Stephen Beach

Partner

PricewaterhouseCoopers, Lae

*connectedthinking

PwC

Contents

• Current PNG financial reporting regime for SMEs

• Recent ASB activity

• Overview of IFRS for SMEs

• Main differences from full IFRS

• International experience on differential reporting for micro-enterprises

• The way forward for PNG

Current PNG financial reporting regime for SMEs

PwC

• All PNG companies required to prepare general purpose finance statements

• General purpose v special purpose

• Reporting company v exempt company

• An exempt company is one that is: Not a subsidiary of an overseas company Not an issuer or subsidiary of an issuer Not a subsidiary of a company that is not exempt Meets the size criteria A subsidiary of an exempt company

Current PNG financial reporting regime for SMEs

PwC

• Can be an exempt company if: • Total assets do not exceed K5m • No more than 25 shareholders • No more than 100 employees

• If only 1 or 2 criteria met, can still be exempt if ALL shareholders

agree

• Criteria are a mix of size and ownership

• No changes in asset limit since 1997

• The majority of companies in PNG are exempt companies

Current PNG financial reporting regime for SMEs

PwC

• Exempt companies – no audit requirement and do not file their accounts with IPA

• Must still produce general purpose accounts for shareholders that comply with PNG GAAP - PNG GAAP comprises full IFRS

• Therefore full IFRS is applicable to all companies in PNG

• IFRS exemptions for unlisted companies, for example EPS and segmental reporting

• ASB provided exempt companies with exemption from complying with IAS 7, 12, 27, 32 and 39 - no change in exemptions since 1997

Current PNG financial reporting regime for SMEs

PwC

The issues for SME’s in PNG • Size criteria for exempt companies not revised since 1997

• Even with the limited exemptions, full IFRS is far too

complicated for most large enterprises, let alone SMEs

• IFRS for SMEs not approved for use in PNG

• Most SMEs do not have users who need or would benefit from general purpose financial statements

Recent ASB activity

PwC

• ASBPNG met for the first time in 10 years in May 2017

• Re-affirmed PNGGAAP comprises IFRS

• Approved all new IFRS issued since 2007

• Approved IFRS for SMEs for use in PNG - effective date 1 January 2018

• Agreed to consider further changes to the differential reporting regime

PwC

Overview of the IFRS for SMEs

• Full IFRS was largely designed for the consolidated statements of listed companies

• Some parts of full IFRS are unnecessary, too complex or too expensive for other sorts of reporting: e.g. unconsolidated statements or most unlisted companies

• IFRS for SMEs, published in July 2009, is designed for this other reporting

• Size doesn’t matter - applicability is based on publicly accountable

PwC

Entities

Listed Unlisted

Publicly accountable

Not publicly accountable

PwC

Public accountability

“An entity has public accountability if its debt or equity instruments are traded in a public market, or if it is in the process of issuing such instruments for trading in a public market, or if it holds assets in a fiduciary capacity for a broad group of outsiders as one of its primary businesses.”

• Includes all listed entities, banks, insurance companies, superannuation funds, investment funds, unit trusts, securities brokers and other financial institutions

• No size criteria applied by ASB

• Over 90% of companies in PNG eligible to adopt IFRS for SMEs

PwC

Overview of IFRS for SMEs

• IFRS for SMEs is 230 pages long (156 pages in A4)

• Full IFRS over 4,000 pages, with currently 41 separate standards plus interpretations

• There are 35 sections on various accounting topics, plus a preface and a glossary

• Amendments were expected every 3 years, but since 2009 only amended once in 2015

PwC

High-level comparison with full IFRS

• Shorter

• Less frequent amendment

• Simplifications:

- deleted topics

- simpler recognition and measurement

- deleted options

- inserted options

- fewer disclosures (down from 3,000 to 450 in the PwC checklist)

High-level comparison with full IFRS

PwC

• The IFRS for SMEs contains five types of simplifications compared with full IFRS • Substantially fewer disclosures (down from 3,000 to 450 in the

PwC checklist) • Simplified redrafting • Some topics are omitted because they are not relevant to typical

entities within scope of the standard • Earnings per share • Interim financial reporting • Segment reporting • Accounting for assets Held for Sale

• Some accounting policy options in full IFRS are not allowed because a more simplified method is available

• Simplification of many of the recognition and measurement principles that are in full IFRS

Undue cost or effort exemptions

• Various exemptions in IFRS for SMEs in relation to certain requirements on the basis of ‘undue cost or effort’ or because they are ‘impracticable’.

• ‘Impracticable’ - applying a requirement is impracticable when the entity cannot apply it after making every reasonable effort to do so.

• Undue cost or effort’ depends on the specific circumstances and on management’s professional judgement in assessing the costs involved (eg valuation fees, employee time and effort) and the benefits to users from being provided the information.

• Not intended to be a low hurdle

PwC

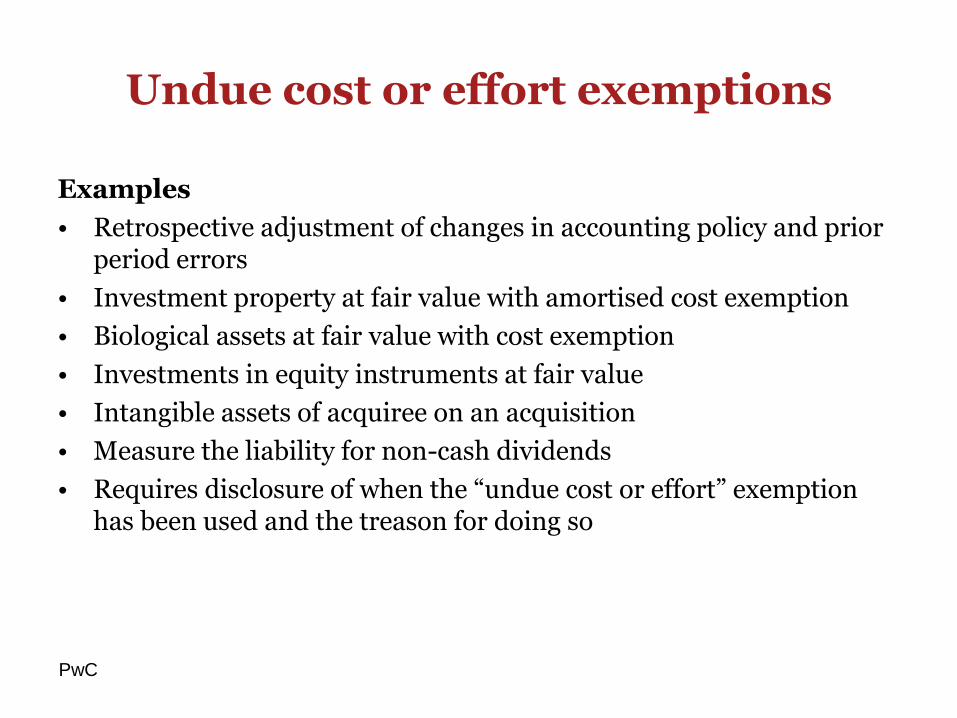

Undue cost or effort exemptions

Examples

• Retrospective adjustment of changes in accounting policy and prior period errors

• Investment property at fair value with amortised cost exemption

• Biological assets at fair value with cost exemption

• Investments in equity instruments at fair value

• Intangible assets of acquiree on an acquisition

• Measure the liability for non-cash dividends

• Requires disclosure of when the “undue cost or effort” exemption has been used and the treason for doing so

PwC

Key differences - Financial statements

PwC

Full IFRS: A statement of changes in equity is required, presenting a reconciliation of equity items between the beginning and end of the period.

IFRS for SMEs: Same requirement. However, if the only changes to the equity during the period are a result of profit or loss, payment of dividends, correction of prior-period errors or changes in accounting policy, a combined statement of income and retained earnings can be presented instead of both a statement of comprehensive income and a statement of changes in equity.

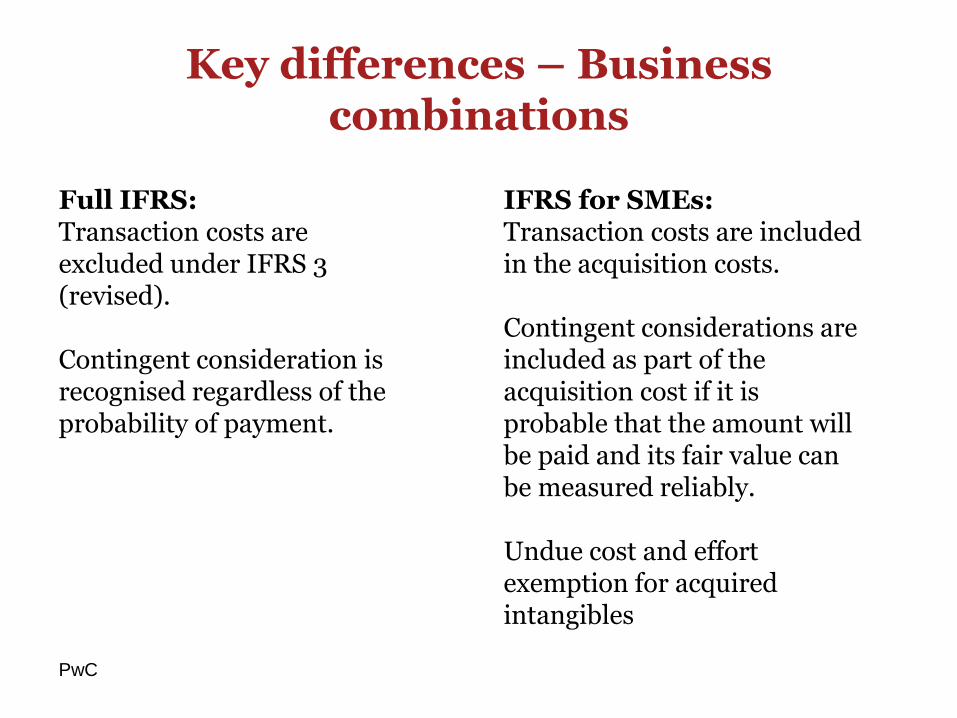

Key differences – Business combinations

PwC

Full IFRS: Transaction costs are excluded under IFRS 3 (revised). Contingent consideration is recognised regardless of the probability of payment.

IFRS for SMEs: Transaction costs are included in the acquisition costs. Contingent considerations are included as part of the acquisition cost if it is probable that the amount will be paid and its fair value can be measured reliably. Undue cost and effort exemption for acquired intangibles

Key differences – investments in associates and joint ventures

PwC

Full IFRS: Investments in associates and joint ventures are accounted for using the equity method. The cost and fair value model are not permitted except in separate financial statements. Joint operations are accounted for under the proportionate consolidation method. The cost model is not permitted.

IFRS for SMEs: An entity may account of its

investments in associates or jointly controlled entities using one of the following:

• The cost model (cost less any accumulated impairment losses).

• The equity method. • The fair value through

profit or loss model.

Key differences – borrowing costs

PwC

Full IFRS: Borrowing costs that are directly attributable to the acquisition, construction or production of a qualifying asset as part of the cost of that asset are capitalised. All other borrowing costs are expensed.

IFRS for SMEs: All borrowing costs are expensed.

Key differences – Financial assets and liabilities

PwC

Full IFRS: IAS 39 distinguishes four measurement categories of financial instruments: • Financial assets or financial liabilities at fair value through profit or loss. • Held-to-maturity investments. • Loans and receivables. • Available-for-sale financial assets. (Changes coming from IFRS 9)

IFRS for SMEs: IFRS for SMEs distinguishes between basic and complex financial instruments. Section 11 establishes measurement and reporting requirements for basic financial instruments; Section 12 deals with additional financial instruments, such as derivatives. Most basic financial instruments are measured at amortised cost. All others are measured at fair value through profit or loss.

Key differences – PPE

PwC

Full IFRS: Accounting policy choice between the cost model and the revaluation model. The residual value, the depreciation method and the useful life of an asset are reviewed at least at each annual reporting date.

IFRS for SMEs: Prior to 2015, classes of PPE are carried at cost less accumulated depreciation and any impairment losses (cost model). From 2015, revaluation of PPE is now an allowed policy choice. The residual value, the depreciation method and the useful life of an asset are reviewed if there is an indication of change since the last reporting date.

Key differences – Intangible assets

PwC

Full IFRS: Development costs are capitalised when specific criteria are met. Accounting policy choice between the cost model and the revaluation model. Intangible assets with indefinite useful life (including goodwill) are not amortised.

IFRS for SMEs: All research and development costs are recognised as an expense. Intangible assets are carried at cost less any accumulated amortisation and any accumulated impairment losses (cost model). All intangible assets (including goodwill) are considered to have finite lives and amortised (generally maximum period of 10 years).

Key differences – Impairment

PwC

Full IFRS: The following assets are tested for impairment irrespective of whether there is indication of impairment: • Intangible assets with an indefinite useful life or an intangible asset not yet available for use. • Goodwill.

IFRS for SMEs: Assets (including goodwill) are tested for impairment when there is an indication that the asset may be impaired. The existence of impairment indicators is assessed at each reporting date.

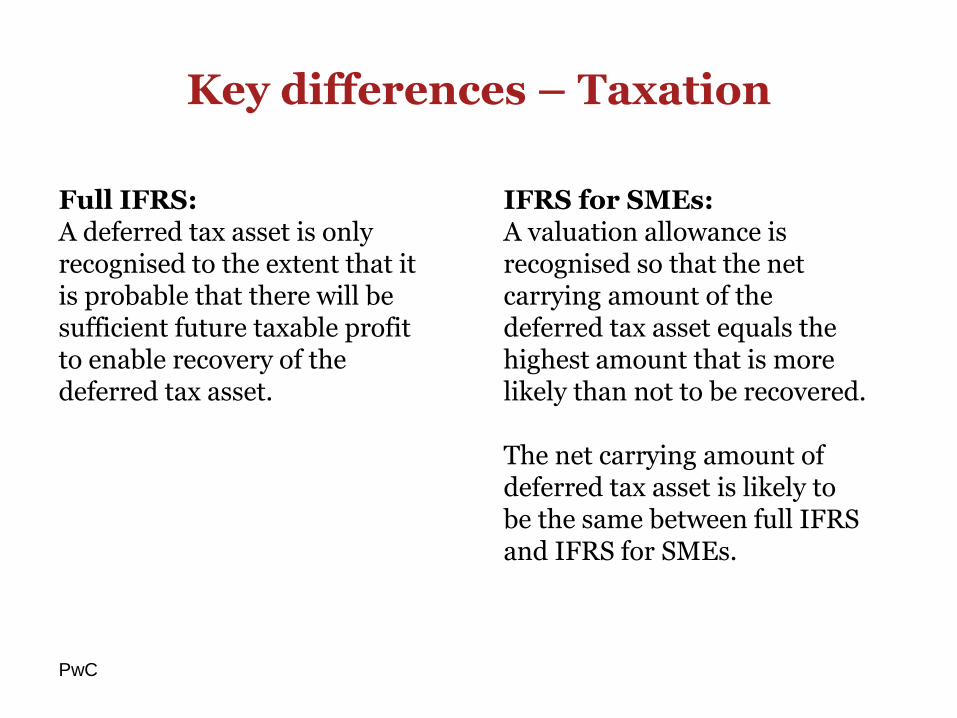

Key differences – Taxation

PwC

Full IFRS: A deferred tax asset is only recognised to the extent that it is probable that there will be sufficient future taxable profit to enable recovery of the deferred tax asset.

IFRS for SMEs: A valuation allowance is recognised so that the net carrying amount of the deferred tax asset equals the highest amount that is more likely than not to be recovered. The net carrying amount of deferred tax asset is likely to be the same between full IFRS and IFRS for SMEs.

Key differences – Hedge accounting

PwC

Full IFRS: Strict rules and criteria to qualify for hedge accounting for the effective portion of hedges. Some simplifications under IFRS 9 in relation to effectiveness testing.

IFRS for SMEs: Hedge accounting allowed for specified hedging instruments. No quantitative test for hedge effectiveness – just need an expectation that the hedge will be highly effective.

Transition to IFRS for SMEs

PwC

• Full retrospective application of the IFRS for SMEs effective at the reporting date for an entity's first financial statements prepared in accordance with the IFRS for SMEs

• Comparative information is prepared and presented on the basis of the IFRS for SMEs

• Adjustments arising from the first-time application of the IFRS for SMEs are recognised directly in retained earnings

• To facilitate transition, there are 10 specific optional exemptions, one general exemption and five mandatory exceptions to the requirement for retrospective application.

PwC

International experience on differential reporting for micro-enterprises

• IFRS for SMEs is not the magic bullet solution

• IFRS for SMEs is a simplified version of full IFRS and makes compliance easier for medium and small entities with limited resources

• No significant impact on current practise for most PNG entities – just makes it easier for Directors to confirm compliance with confidence

• IFRS for SMEs is still overly burdensome for micro-enterprises with limited resources

PwC

International experience on differential reporting for micro-enterprises

• Most micro-enterprises do not require general purpose financial

statements as they have limited users who have the ability to demand or access information to meet their own needs

– owner-managers

– Financiers

– tax authorities

• Need for a basic special-purpose financial reporting framework for micro-enterprises that provides basic information that meets the needs of owners, banks and tax authorities.

PwC

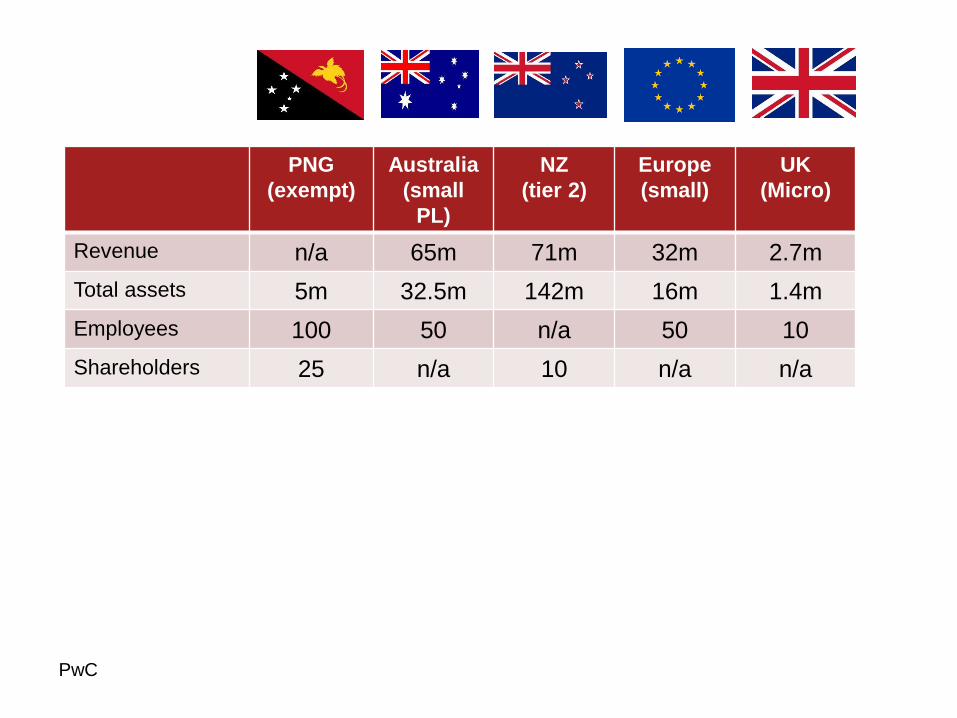

PNG

(exempt)

Australia

(small

PL)

NZ

(tier 2)

Europe

(small)

UK

(Micro)

Revenue n/a 65m 71m 32m 2.7m

Total assets 5m 32.5m 142m 16m 1.4m

Employees 100 50 n/a 50 10

Shareholders 25 n/a 10 n/a n/a

PwC

International experience on differential reporting for micro-enterprises

Australia

• Distinction between reporting and non-reporting entities

• Reporting entities must prepared GPFS but can be either Tier 1 or Tier 2 with reduced disclosures

• Non reporting entities may prepare SPFS that meet certain minimum presentation and disclosure requirements

• The ATO has issued guidelines for accounting principles for SPFS that meet their requirements

• Small proprietary companies are non-reporting entities and are not required to prepare financial reports unless they are foreign controlled or the shareholders direct.

• Small proprietary company (meet 2 out of 3) – Revenue less than $25m (K65m)

– Gross assets less than $12.5m (K32.5m)

– Employees less than 50

PwC

International experience on differential reporting for micro-enterprises

New Zealand

• Relatively complex differential reporting regimes with 2 tiers for “for profit entities” and 4 tiers of reporting for “public benefit entities”

• Tier 2 for-profit entities that are required to prepare general purpose FS can apply NZ IFRS with Reduced Disclosure Requirements. Most tier 2 entities will not have a GPFR requirement

• SMEs that are not required to prepared GPFR can prepare special purpose financial reports for tax purposes using minimum standards set by the tax authorities or follow guidelines issued by the NZICA

• Tier 2 criteria – Not publicly accountable

– Assets less than $60m (K142m)

– Turnover less than $30m (K71m)

– Less than 10 shareholders (with opt out by 95% resolution).

PwC

International experience on differential reporting for micro-enterprises

Europe

• EU single accounting directive 2013/34/EU simplifies reporting for qualifying micro, small and medium sized entities

• Small – Revenue less than Euro 8 million (K32m)

– Total assets less than Euro 4 million (16m)

– Employees less than 50

• GAPSME based on IFRS for SMEs

• No cash flow statement, SOCE and reduced disclosures for small companies

• Small groups exempt from preparing consolidated accounts

PwC

International experience on differential reporting for micro-enterprises

United Kingdom

• FRS 105 “The Financial Reporting Standard applicable to the Micro-entities Regime

• FRS 105 introduced in December 2013 effective from 2015

• Legislative changes contained in the Statutory Instruments 2013/3008 – The Small Companies (Micro-Entities Accounts) Regulations 2013

• Size criteria (meet at least 2 out of 3) – Turnover not more than GBP632,000 (K2.7 million)

– Balance sheet total not more than GBP 316,000 (K1.4 million)

– Average employees not more than 10

• Simplified balance sheet and profit and loss statement

• No cash flow, equity statement or accounting policies

• Limited notes covering – directors benefits, advances, credit and guarantees, and

– guarantees and other commitments

• No revaluations or fair values permitted and no deferred tax accounting

PwC

The way forward for PNG

• IFRS for SMEs available for use from 1 January 2018

• Companies Act amendments required to:

– Change the definition of exempt companies

– Increase the size limits for exempt companies (increase total assets limit from K5m to K10m, but add a turnover limit of K20m)

– Consider a new category of “Small Exempt Company” that can choose to prepare special purpose financial statements under a new micro-enterprise framework (assets <K1m , turnover < K2m)

• CPAPNG and ASB to develop and adopt a micro-enterprise reporting standard

PwC

In summary…..

• One size does not fill all

• IFRS for SMEs is now here and available for use

• No significant impact on the financial statements for the majority of PNG entities

• Benefits for directors, CFO’s and auditors in ensuring compliance

• Education and training requirements

• Not the solution for most SMEs in PNG

• Regulatory changes required to financial reporting requirements

Question time?

PwC