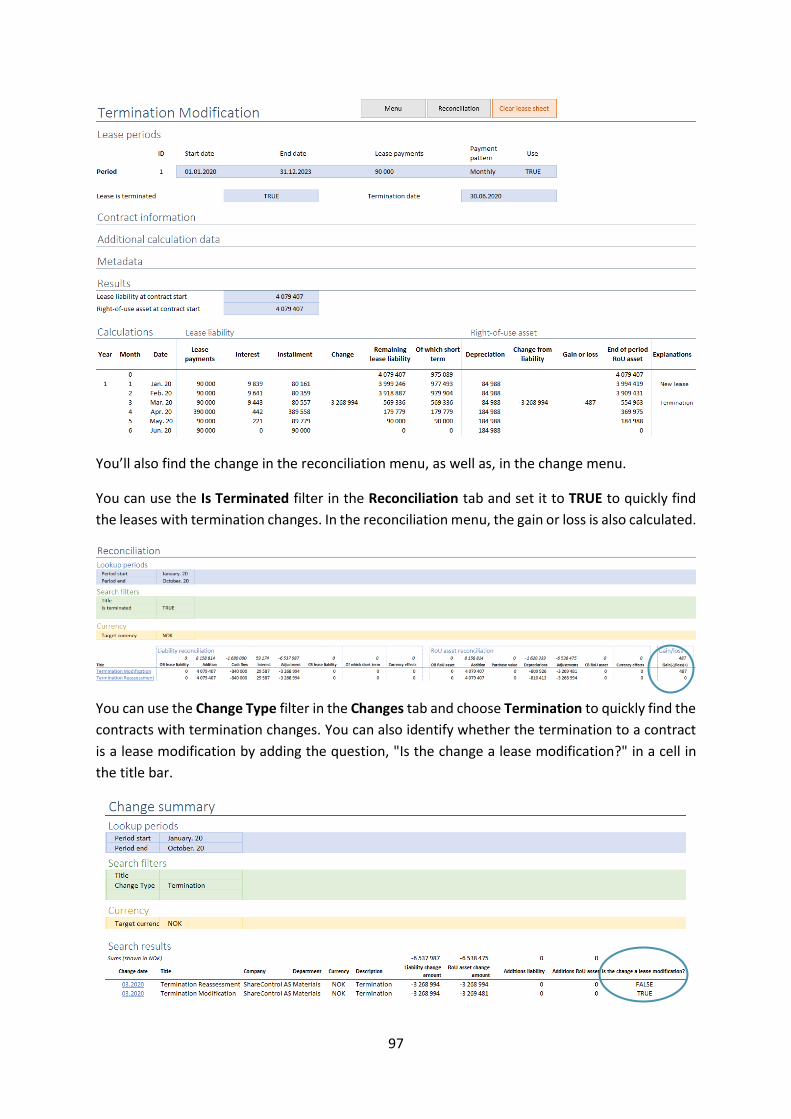

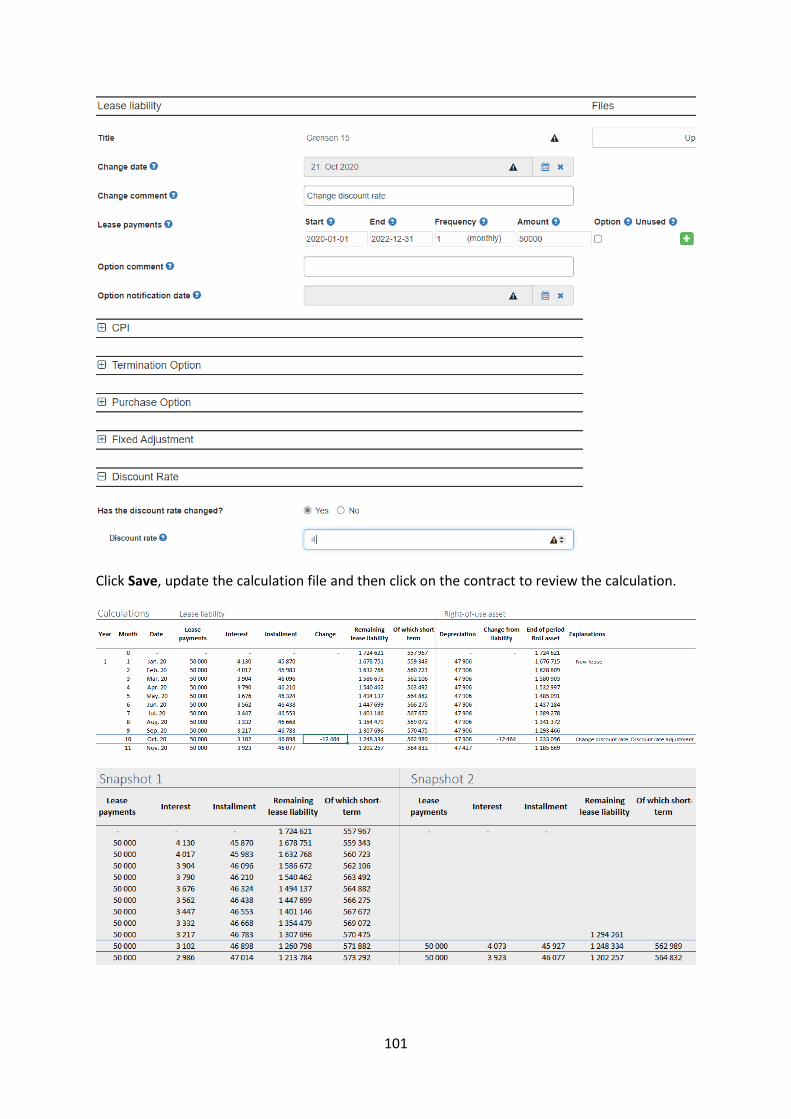

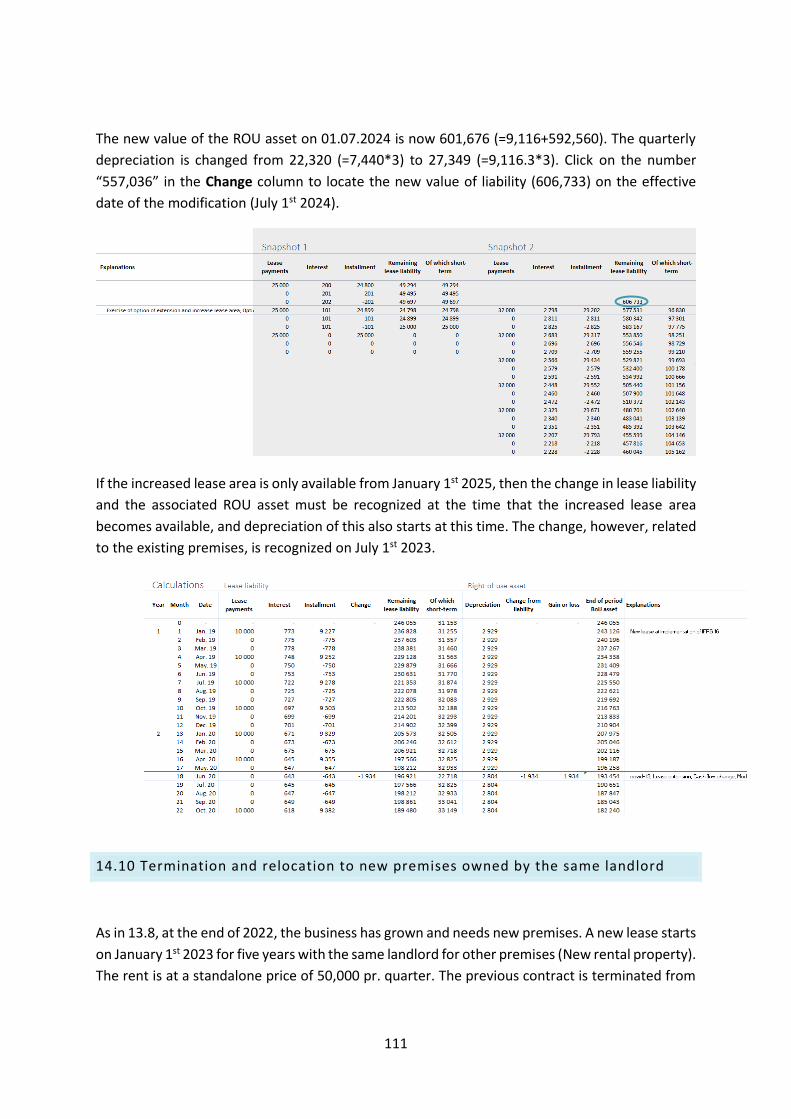

Embed Size (px)

Citation preview

IFRS 16 User Guide Updated 22. December 2021

Share Control AS

© 2021

Chapters

Chapters ........................................................................................................................................... 2

1. Introduction ................................................................................................................................. 1

2. Before you start ........................................................................................................................... 1

3. Frontpage ShareControl IFRS 16 .................................................................................................. 1

4. Introduction to ShareControl IFRS16’s functions ........................................................................ 3

4.1 Lookup .................................................................................................................................... 3

4.2 Search ..................................................................................................................................... 4

4.3 Deleting folders and files ........................................................................................................ 5

4.4 Settings ................................................................................................................................... 6

4.4.1 Landing page .................................................................................................................... 7

4.4.2 Library .............................................................................................................................. 7

4.4.3 Metadata ........................................................................................................................ 10

4.4.4 Field descriptions ........................................................................................................... 11

4.4.5 Guidelines ...................................................................................................................... 12

4.4.6 Hide fields ...................................................................................................................... 14

4.4.8 Lock reporting period ..................................................................................................... 17

4.4.9 Properties and Support .................................................................................................. 17

4.4.7 Synchronization .............................................................................................................. 18

4.4.8 IFRS 16 ............................................................................................................................ 19

4.5 Libraries, folders and files ..................................................................................................... 20

4.5.1 Creating contracts (Folders): from draft to publish ....................................................... 21

4.5.2 Using the funnel (filtering and sorting by metadata/columns) ..................................... 24

4.5.3 Folders options (Cogwheel) ........................................................................................... 26

4.5.4 Files options (Cogwheel) ................................................................................................ 32

4.5.5 Uploading documents .................................................................................................... 33

4.5.6 Locking folders and documents ..................................................................................... 34

4.5.7 Sharing specific documents ........................................................................................... 35

4.5.8 SharePoint and file menus in Word, Excel and PowerPoint .......................................... 35

4.5.9 Mobile access ................................................................................................................. 35

4.6 Processing tasks .................................................................................................................... 35

4.6.1 Task details on the frontpage ........................................................................................ 36

4.6.2 Assigning tasks ............................................................................................................... 37

4.6.3 Task status on folders .................................................................................................... 38

5. Upload contracts using SharePoint ............................................................................................ 39

5.1 Tips for creating folders ........................................................................................................ 40

6. Upload contracts using the excel template ............................................................................... 41

6.1 Register start date and end date of lease payment correctly .............................................. 45

6.1.1 Actual lease payment pattern ........................................................................................ 45

6.1.2 Registers cash flow based on a date .............................................................................. 46

6.1.3 Check calculation warnings ............................................................................................ 46

7. Rent free periods/ periods with different lease payments/ other non-lease payments .......... 46

7.1 Rent free periods/ periods with different lease payments .................................................. 46

7.2 Other non-lease payments ................................................................................................... 48

7.3 Index regulation of other non-lease payments .................................................................... 49

8. Foreign currency exchange ........................................................................................................ 50

8.1 Foreign entities ..................................................................................................................... 51

8.2 Contract currencies different from the entity’s functional currency ................ 54

9. Business combination (IFRS 3. 28 A and B) ................................................................................ 57

10. Sub lease and use of the solution as a lessor (Pro version) ..................................................... 58

10.1 Offset ROU asset against lease receivable ............................................................. 61

11. Metadata (Contract data) for IFRS 16 ...................................................................................... 61

12. Consistency in data and summary of calculation rules............................................................ 69

13. Adjust index or rate and log other change .............................................................................. 69

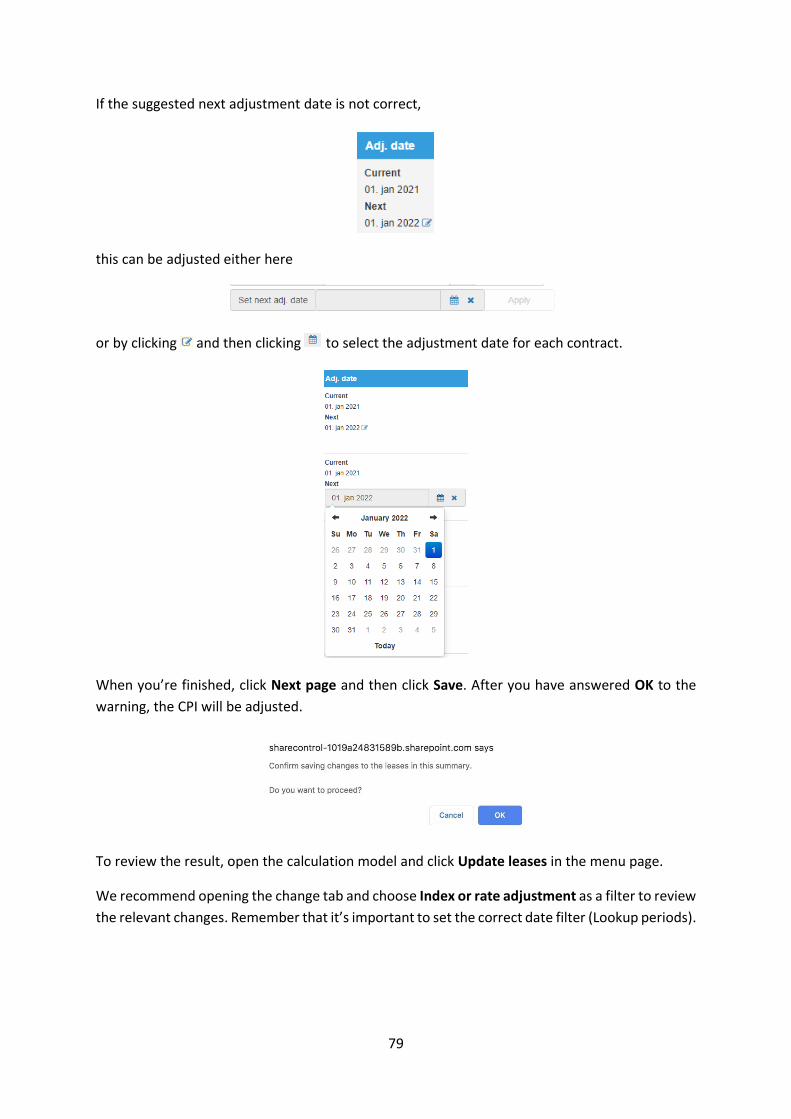

13.1 Adjust index or rate ............................................................................................................ 70

13.2 Update index or rate for several contracts simultaneously (Mass update) ....................... 74

13.3 Roll back mass adjustments ............................................................................................... 83

14. Lease modification and reassessment ..................................................................................... 84

14.1 Change date ........................................................................................................................ 86

14.2 Modify a contract ............................................................................................................... 88

14.3 Exercise an extension option that previously has not been exercised .............................. 91

14.4 Terminate a lease contract (In the lease period) ............................................................... 94

14.4.1 Situation A: Reassessment ........................................................................................... 94

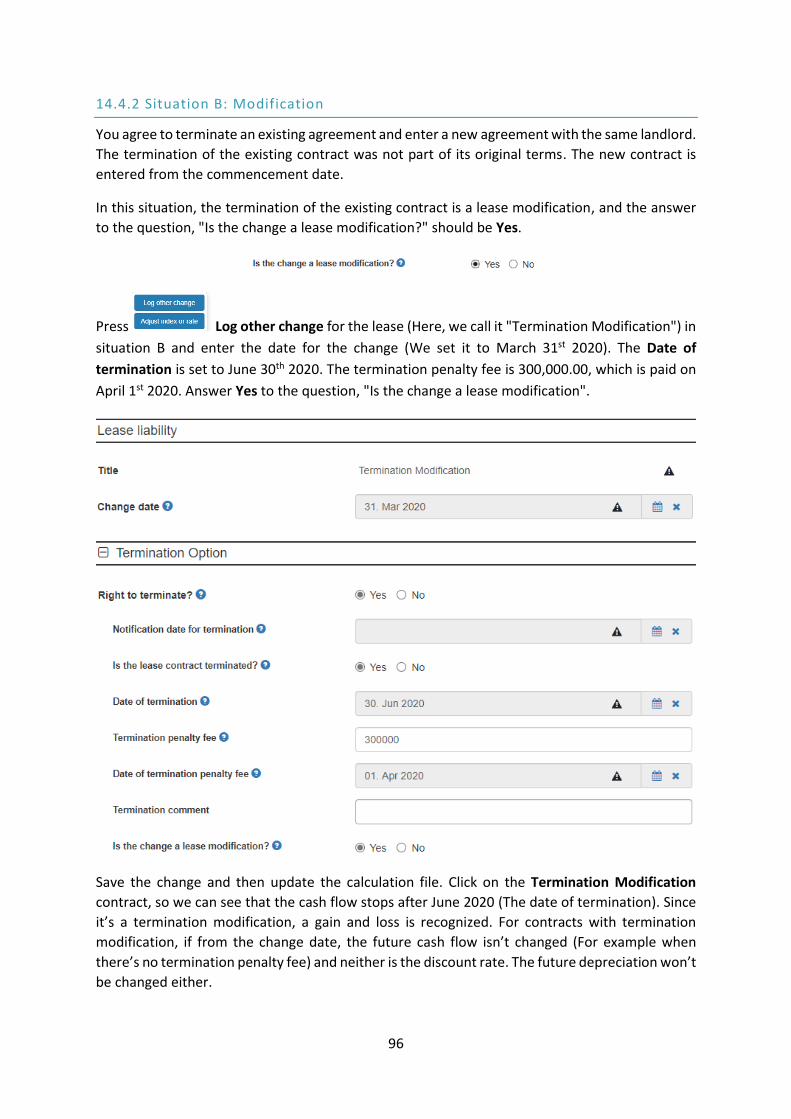

14.4.2 Situation B: Modification ............................................................................................. 96

14.4.3 Situation C: Immediate termination ............................................................................ 98

14.5 Purchase option .................................................................................................................. 99

14.6 Change in the discount rate ............................................................................................. 100

14.7 Residual value guarantee ................................................................................................. 102

14.8 Reduction in scope - modification versus reassessment ................................................. 102

14.9 Reassessment of option and increase in scope ................................................................ 108

14.10 Termination and relocation to new premises owned by the same landlord ................. 111

14.11 Impairment of the ROU asset ......................................................................................... 114

14.12 Covid-19-Related Rent Concessions ............................................................................... 115

14.12.1 Release of payments ................................................................................................ 116

14.12.2 No rent is payable in Q3 2020, rent in Q3 2021 is increased by 11’. ....................... 118

14.12.3 No rent is payable in Q3 2020 and one quarter is added to the end of the lease at a

rent of 10’ for that quarter. .................................................................................................. 119

14.13 Log multiple changes in the same date or the same month .......................... 120

14.14 How to test the accounting of changes .......................................................................... 121

15. Errors ...................................................................................................................................... 121

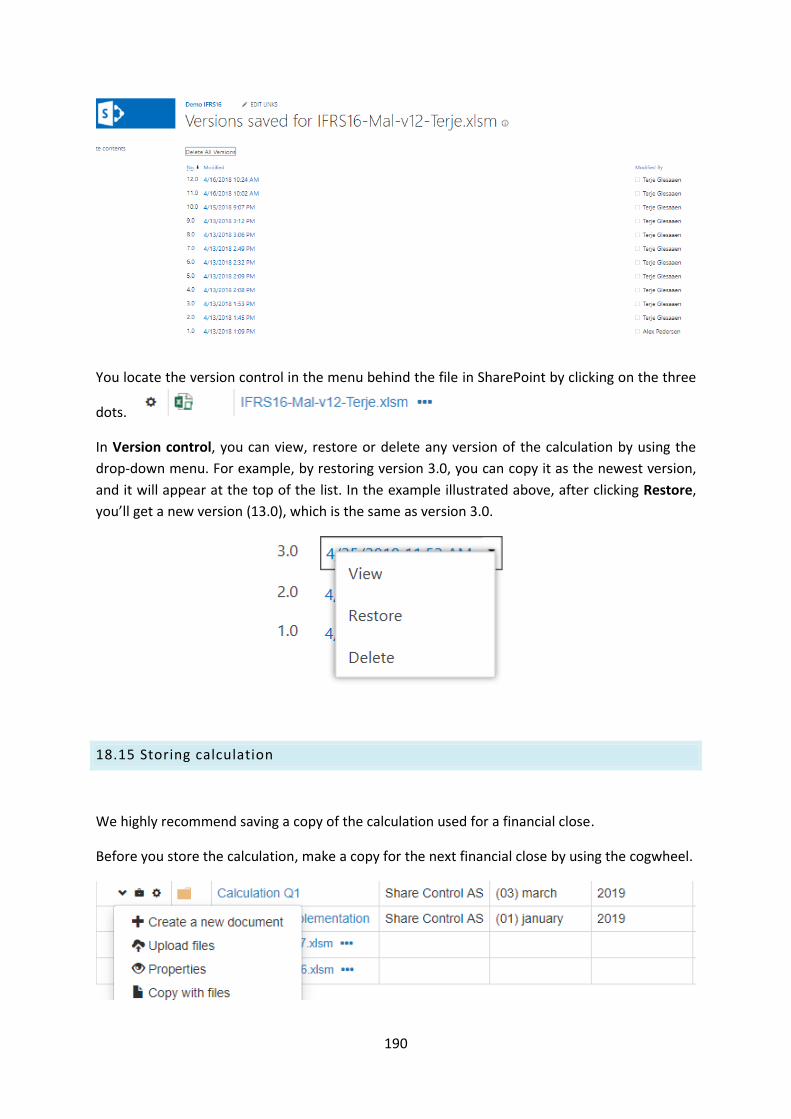

15.1 Roll back to previous version ............................................................................................ 121

15.2 Accounting date ................................................................................................................ 125

15.2.1 A lease contract has not been registered when it was entered ................................ 127

15.2.2 Forgot to register index regulation ............................................................................ 129

15.2.3 A contract was entered with incorrect lease payments ............................................ 130

15.2.4 Discount rate is not correct ....................................................................................... 131

15.2.5 Exercise of an extension option was not registered in the correct period ................ 133

15.2.6 Forgot to change the discount rate when exercising an extension option ............... 135

15.2.7 Change the start date of a contract to an earlier or a later date .............................. 135

15.2.8 Change in the asset removal obligation..................................................................... 137

15.2.9 Change post-paid to prepaid ..................................................................................... 138

15.2.10 Forgot to register the termination of a contract ..................................................... 140

15.2.11 The termination of a contract is incorrect ............................................................... 143

15.2.12 Remove a lease that has incorrectly been registered as an IFRS lease ................... 145

16. Deleting a lease contract ....................................................................................................... 147

17. Implementing IFRS 16 – the implementation options ........................................................... 148

17.1 The full retrospective implementation ............................................................................ 148

17.2 ROU asset = lease liability ................................................................................................. 148

17.3 Measure ROU asset retrospectively ................................................................................. 149

17.4 Transition relief for leases ending within 12 months and low value assets lease ........... 149

18. Calculation.............................................................................................................................. 150

18.1 Access to the calculation spreadsheet ............................................................................ 151

18.2 Establish link between SharePoint and Excel ................................................................... 151

18.2.1 Warning about disconnected workbooks (Warning ID 605) ..................................... 154

18.3 The main calculation spreadsheet (Menu) ....................................................................... 154

18.3.1 The Menu spreadsheet .............................................................................................. 155

18.3.2 Update data from SharePoint .................................................................................... 155

18.3.3 Settings ....................................................................................................................... 156

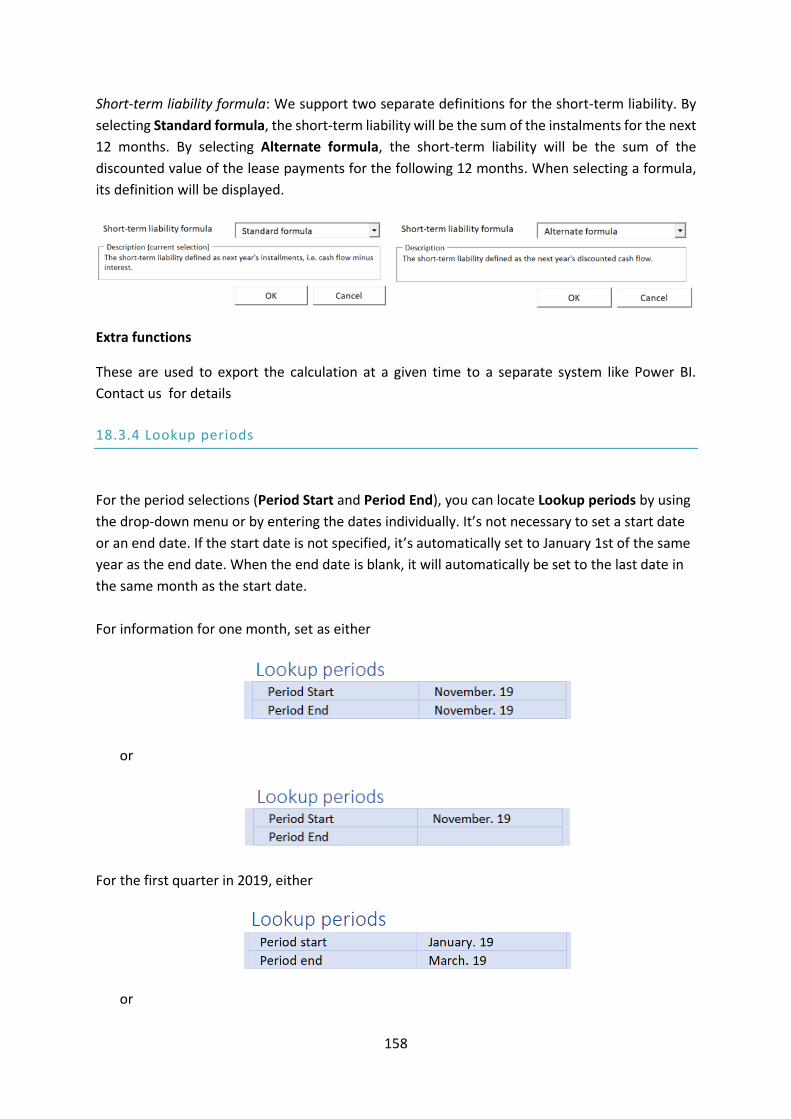

18.3.4 Lookup periods ........................................................................................................... 158

18.3.5 Currency ..................................................................................................................... 159

18.3.6 Go directly from the calculation file to the contract in SharePoint ........................... 161

18.3.7 Search filters .............................................................................................................. 162

18.3.8 Modify columns in the view ....................................................................................... 164

18.3.9 Archive calculation and serve links between SharePoint and calculation file ........... 165

18.4 The calculation of individual contracts ............................................................................. 168

18.4.1 Calculation spreadsheet for individual contracts ...................................................... 168

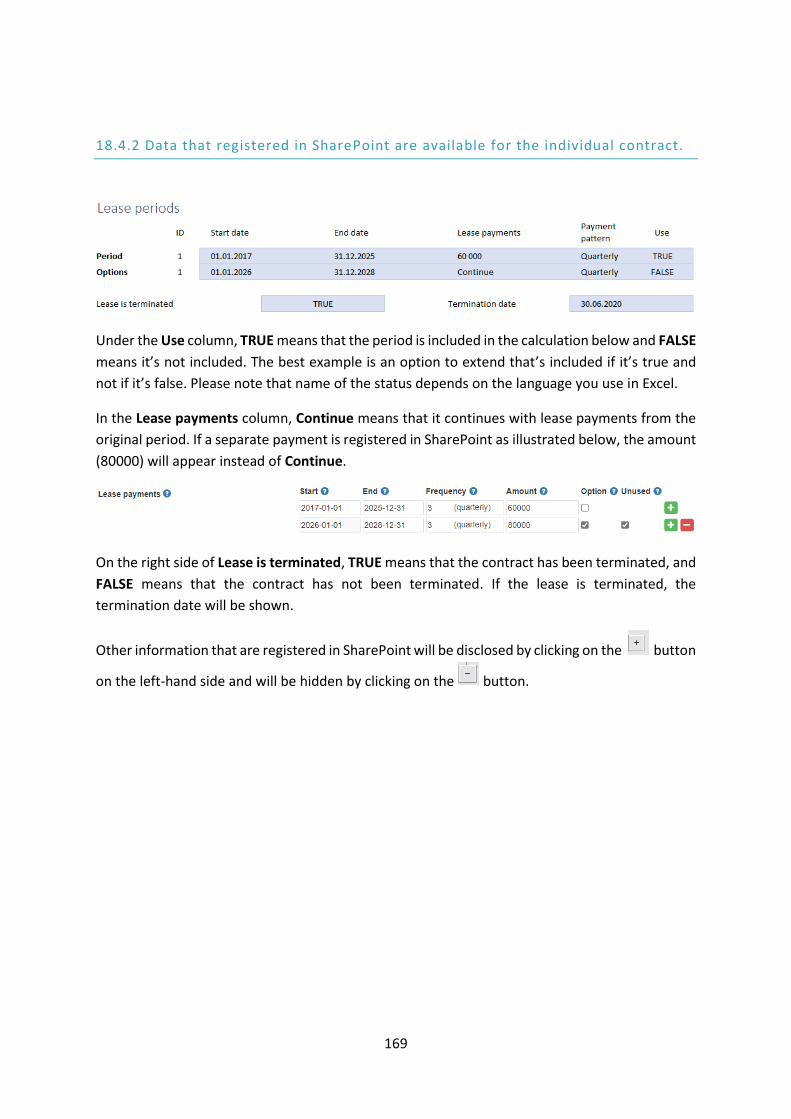

18.4.2 Data that registered in SharePoint are available for the individual contract. ........... 169

18.4.3 Lease payments that occur in the previous month ................................................... 171

18.4.4 Go directly from the calculation file to the contract in SharePoint ........................... 172

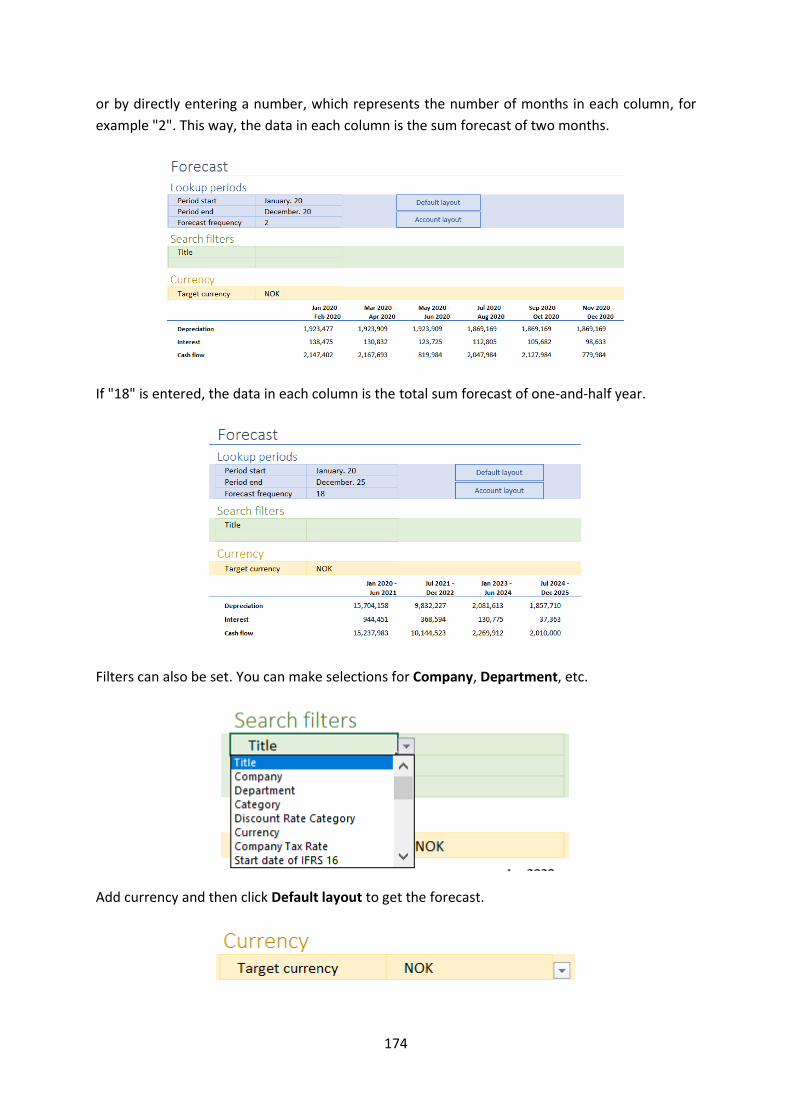

18.5 Forecast and Budget (Pro version) ................................................................................... 172

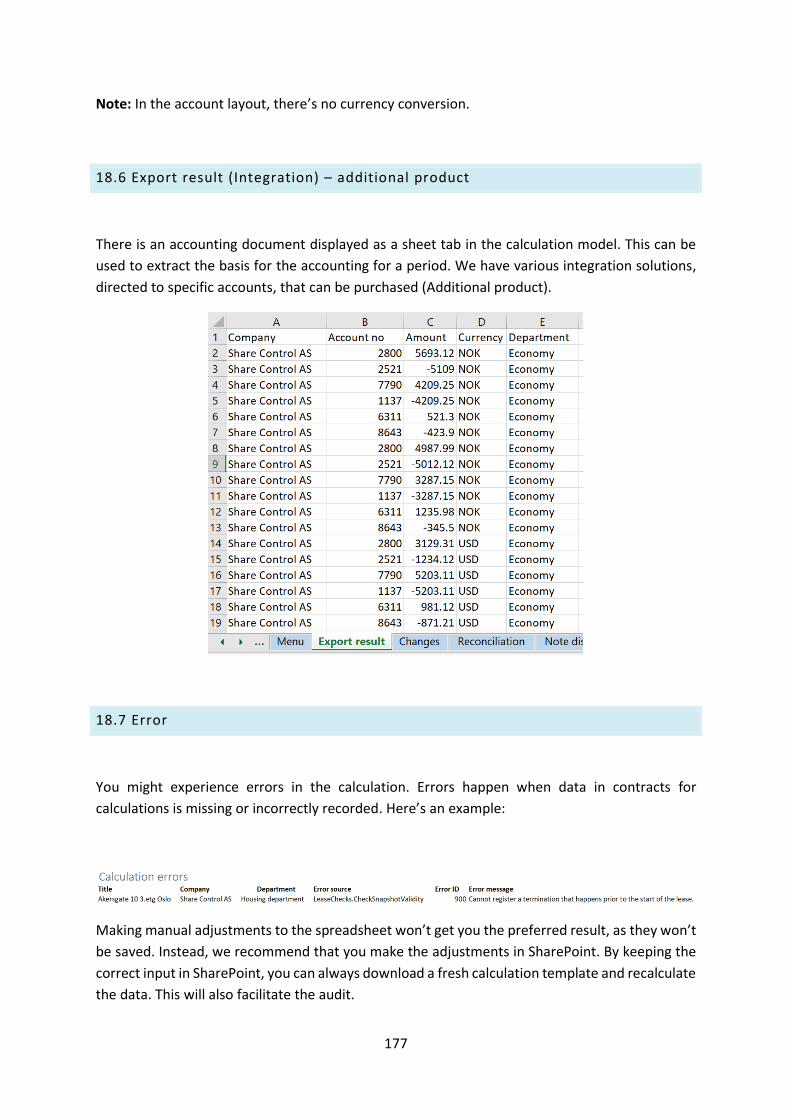

18.6 Export result (Integration) – additional product ................................................ 177

18.7 Error .................................................................................................................................. 177

18.8 Warnings ........................................................................................................................... 178

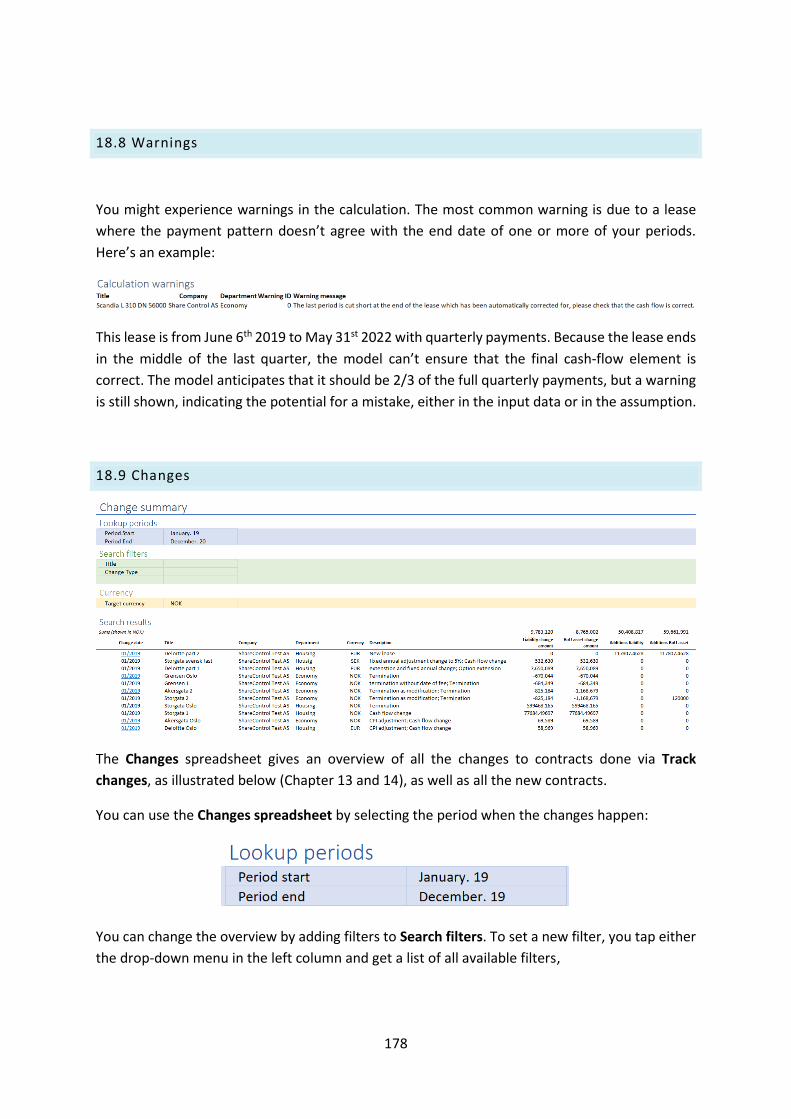

18.9 Changes ............................................................................................................................ 178

18.10 Reconciliation ................................................................................................................. 180

18.11 Note disclosures ............................................................................................................. 181

18.11.1 Critical judgment and accounting estimates ........................................................... 183

18.13 Fixed assets footnote (Pro version) ................................................................................ 186

18.14 Other information about Calculation ............................................................................. 187

18.14.1 The DCF model ......................................................................................................... 187

18.14.2 Depreciations ........................................................................................................... 188

18.14.3 Fixed adjustments .................................................................................................... 188

18.14.4 Daily rates ................................................................................................................ 189

18.14.5 Go back to an old calculation ................................................................................... 189

18.15 Storing calculation .......................................................................................................... 190

18.16 Include other non IFRS 16 contracts in the calculation file ............................................ 192

19. Review and audit .................................................................................................................... 193

20. FAQs (Frequently asked questions) ....................................................................................... 193

20.1 I have established a new library with contracts in SharePoint, but they’re not included in

the calculation, even if I press Update leases. ......................................................................... 194

20.2 When a new contract should be registered in Share Control .......................................... 194

1

1. Introduction

This user guide helps you to start using ShareControl Contract and IFRS 16. It demonstrates the

functionality of the ShareControl add-in for SharePoint IFRS 16, as well as the use of the

ShareControl IFRS 16 excel VBA calculation.

The installation process of the ShareControl add-in and organization of sites are fully described in

the installation manual.

2. Before you start

It’s important that you consider how you want to organize your contracts in the IFRS 16 libraries

before you start, since it can be quite complicated to change the structure after you have

uploaded a significant number of contracts.

Here are some questions that we recommend considering before you start.

1) Consider your legal structure and how your financial processes are today.

a. Will the IFRS 16 contracts and calculation be entered and maintained by individual

entities, by the group or by segments?

b. How does the review and audit process work today (Is it by legal entities, by

segments, etc.)?

c. How are the IFRS figures reported today? By reporting entities, by the group, etc.

(Group IFRS entries).

d. Do I need an overview of all IFRS 16 contracts in the group or do I prefer reporting

by different reporting entities?

e. Will I have dedicated employees to review IFRS 16 contracts for the consistency

of input data? Would I engage with an external consultant to do this work?

f. Is access/ limited access critical for me?

g. How do I foresee the maintenance of the IFRS contract management, going

forward? Do I foresee the accounting data included in my accounting system or

kept separate and adjusted in the IFRS reporting?

2) ShareControl and its suppliers will help you evaluate how sites, access and systems

should be set up. We’ll also provide you with templates to facilitate the set up.

3. Frontpage ShareControl IFRS 16

2

The front page provides you with the following information:

• The status of your tasks (See the Task section).

• Contracts that need to be reviewed, due to an upcoming index regulation or a contract

option (Extension option, termination option and purchase option) or expiration.

The information can be accessed directly from the front page by clicking on the task or the

reminder. You can also include the reminder in the calendar or send an email directly to the

responsible person by clicking

Expand the Date filter by clicking the menu below.

3

Please note that we introduced an integration with Power Automate for notifications in 2021. See

a separate guide for set up and use.

4. Introduction to ShareControl IFRS16’s functions

Microsoft 365’s standard menu is on top and will be available for you when you work in the add-

in.

Please note that the language in the menu will follow the language in your Microsoft 365’s general

setup. If you use a different language than English in your set up, this menu and some of the

property choices will appear in your chosen language.

ShareControl’s main menu includes Up One Level (Only for administrators), Recycle Bin, Settings

(Only for administrators), Tasks, Mass Adjustments and Recent Documents. The Share button

and the Search field are on the right side. The libraries are shown to the left below the logo, where

you can alternate between the front page and different libraries.

4.1 Lookup

You find the Lookup function in the right corner.

4

In the Lookup function you’ll access downloadable IFRS calculation templates, along with

guidance and IFRS standards. Accessing the relevant IFRS requires a subscription to eIFRS. See link

for subscription.

https://shop.ifrs.org/ProductCatalog/Product.aspx?ID=1595

(Link for online subscription, - recommended if you don't need the printed standards.)

You’ll find the Installation manual under User Guide.

There are also links to relevant articles, etc. And you can add internal guidelines by clicking

Calendar and Guidelines in the submenu of Settings.

4.2 Search

You can search through all the documents in a site, or all documents you have access to, through

the Search function in SharePoint.

The Search function, located in the upper right corner, is available in SharePoint and ShareControl.

The search results are shown separately and look like this:

5

4.3 Deleting folders and files

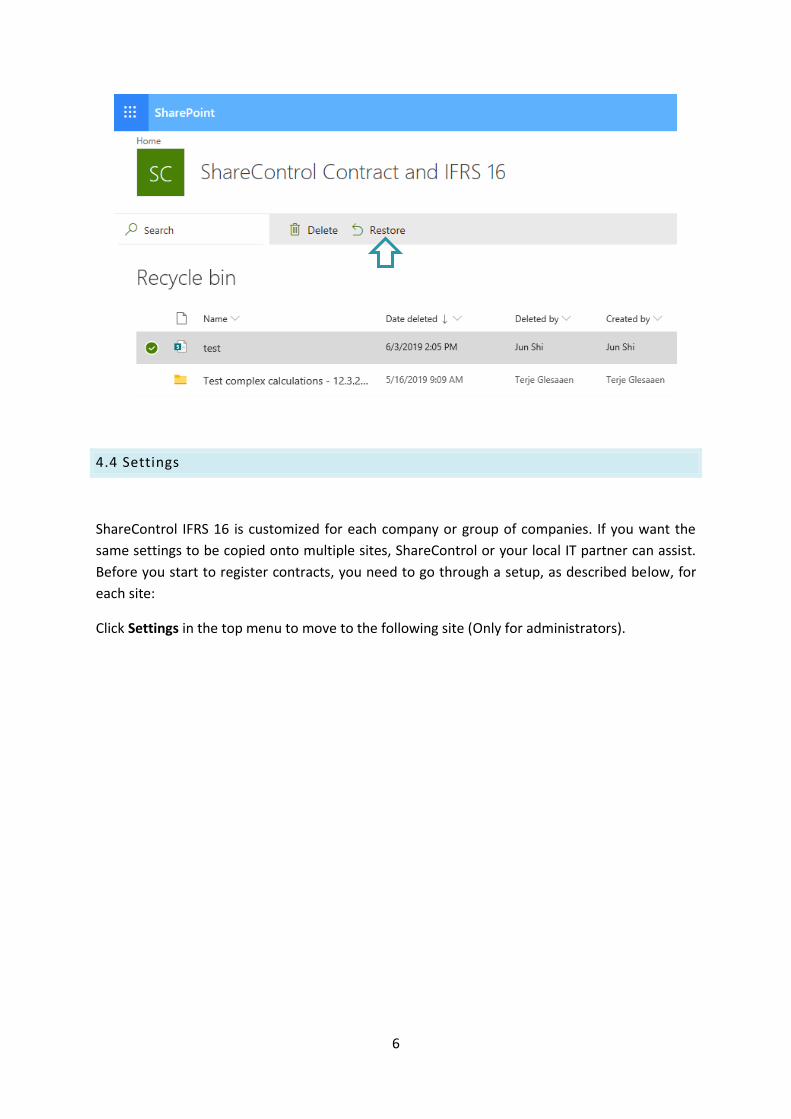

Everything deleted in SharePoint and ShareControl goes to the Recycle Bin on the site.

The Recycle Bin is emptied either manually or automatically after 93 days. The content is then

moved to the administrator’s recycle bin. The administrator can access deleted content from this

recycle bin.

Select the folders/ files you want to restore and select Restore.

6

4.4 Settings

ShareControl IFRS 16 is customized for each company or group of companies. If you want the

same settings to be copied onto multiple sites, ShareControl or your local IT partner can assist.

Before you start to register contracts, you need to go through a setup, as described below, for

each site:

Click Settings in the top menu to move to the following site (Only for administrators).

7

4.4.1 Landing page

The Menu let you choose which page appears first when you open the add-in. You will normally

have the standard setting here.

4.4.2 Library

8

To configure, go to the Library menu. It’s important that you select the relevant category for

creating a library, as the metadata will vary from one category to another.

By clicking on a single category, you can see which libraries you have created in the different

categories. You can also hide, create new, and remove libraries from the category. Note that if

you have ShareControl Contract, it's only one type of libraries that are available. If you have the

full versions of ShareControl Contract and IFRS 16, you’ll have different kinds of libraries available

for different kinds of contracts (Land and properties, other IFRS 16 contracts and contracts outside

the scope of IFRS 16).

9

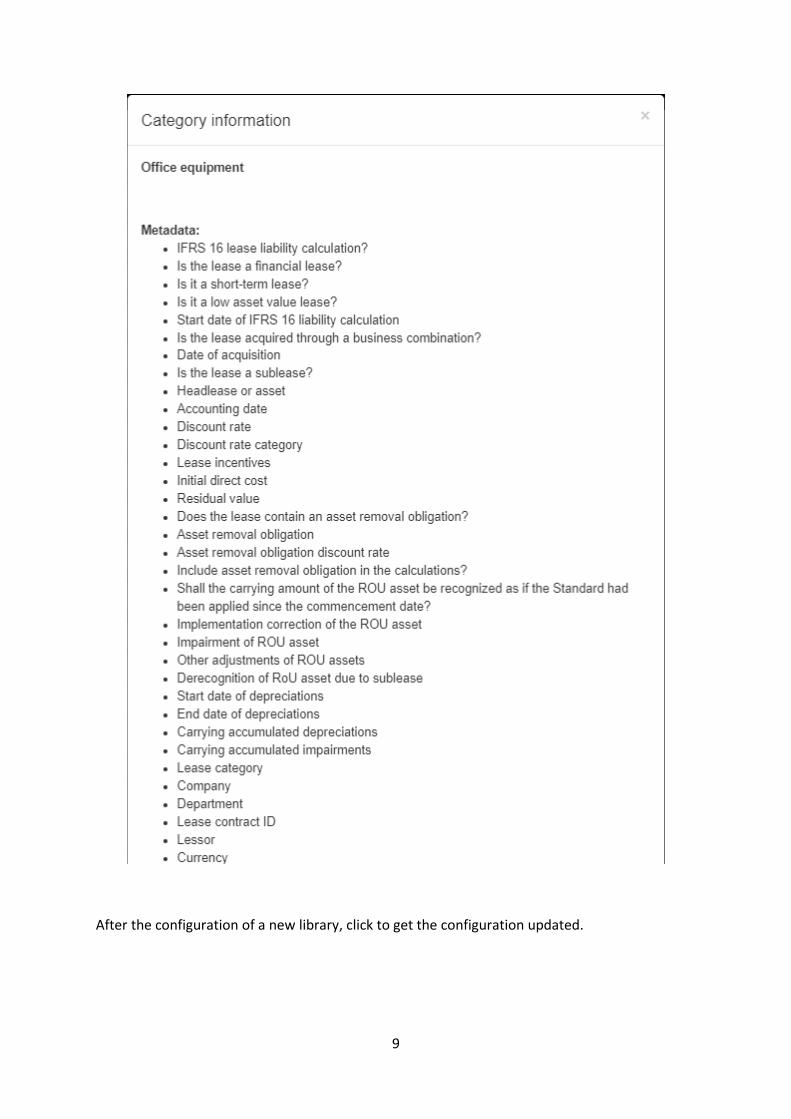

After the configuration of a new library, click to get the configuration updated.

10

Click on the right to change the name of a library, and when finished, click to save. Click

to hide the library. You can create new libraries by typing in the text and clicking . You

can find all hidden libraries by clicking the drop-down menu called, Choose existing, and you can

unhide them by selecting them individually.

4.4.3 Metadata

Metadata (Or Index data) is used in all libraries to organize files and prepare calculations under

IFRS 16. Metadata is shown as a dropdown menu when you’re creating or editing folders. The use

of metadata creates a uniform document structure. The metadata in IFRS 16 will be consistent for

all folders. If metadata is not selected, the sorting functionality will be less effective.

The following metadata should be set (Included in the drop-down menu) before you start to

register a contract:

Lease category (The standard IAS 16 classification) - Use to classify ROU Assets for footnotes, etc.

Company – Legal entity that has entered the contract.

Department – Should be consistent with your accounting system to facilitate reconciliation and

transfer of files.

Discount rate category – Is used to set discount rates in the calculation of present value of the

lease liability for new or modified/ reassessed lease contracts. Categories of discount rates can

be based on geography (Countries), rental period and underlying assets.

Currency – Includes all relevant currencies that the group operates. Please use the same

abbreviation as used by the bank/ accounting system of updated currency rates.

Type of lease adjustment – CPI, interest, market adjustments or any other adjustment.

Under the Account vouchers, you also need to set the year and period (Normally the month) as

metadata. This is set by default but can be modified.

To edit the metadata, move to the relevant category and click the title you want to edit. Click

on the right to edit the value, and when finished, click to save. Select to delete. You can

11

create new values by typing in the text and clicking at the end of the metadata list.

Note: Deleting or changing values in Settings will affect all folders where these values

have been used. The metadata will also be changed in locked folders.

If the app is set up several times, the metadata cannot be changed for all installations

at the same time. Metadata changes need to be made per installed app.

When you’re creating a new folder in a library and are missing a value in the metadata,

you can’t move directly from the folder to Settings to create a new value. The folder needs

to be saved first, and then you can change the settings for the metadata by going back,

editing the folder, and adding the new value.

If a category of metadata can’t be used, these can be removed. We can assist you in

doing this. It’s not recommended that you try to do this by yourself.

4.4.4 Field descriptions

Field description is used for describing and explaining common metadata. You can choose

metadata from the dropdown menu and create new values by typing or editing the description in

the text and clicking . Click on the right to edit the value and when finished, click

to save. Select to delete.

12

By clicking on the question mark by the side of a metadata category for IFRS 16, the description

of the metadata will be shown on the screen.

4.4.5 Guidelines

13

The administrator can add internal guidelines, relevant articles, links, etc. under guidelines.

Combine the company’s guidelines with the IFRS standards to have all the information in one

place. This way, you’ll save time for emails, version conflicts, etc. You can also add forms,

templates and links to other websites, such as IFRS 16 articles, Auditors website, etc.

We recommend separating guidelines from other documents, as these are used to understand

company processes and principles and therefore shall not be edited by the users (As opposed to

folders and documents in the library). Internal guidelines can be uploaded to the relevant library

and will not be shown in other libraries.

Start by saving the file in SharePoint. Click Up one level in the top menu. Move to Site Contents

and use the Documents library to upload your guidelines, etc.

If you’re unable to find the Site Contents, click the cogwheel to the

upper right and select Site Contents from the menu.

Go back to the Settings app, and select the Calendar and guidelines tab.

14

To add guidelines, enter the title, type or copy a URL, upload a file, etc. Or use to find the

document that you wish to add. (You can now browse Document and select the file uploaded to

the Document library as described above).

When you click , you will see the window below. You can also select the library where you

want to place the file. Select Choose libraries and select the libraries where the link should be

placed. Click to save.

To make the change, click the , and when finished, click to save. To delete, click .

4.4.6 Hide fields

The IFRS 16 solution contains all fields and metadata that might be relevant for companies using

the solution. Different companies have different situations and might not need to use all the

fields. The 2021 version makes it possible to hide fields that are not relevant.

Go to Settings and IFRS 16.

15

Click on Show additional options.

You can hide fields that might not be relevant. We can assist you in this process.

16

You can also enable or disable the Cash Flow function. If it’s enabled, the system will automatically

split the lease payments according to the change date to more effectively show the change in the

lease payments before and after the specified change date.

As illustrated below, if the Cash flow function is enabled, you can view the historical data marked

in yellow before the change date under the lease payment.

You can display or hide links to relevant public websites where the CPI rate can be read.

You can choose between linking to ssb.no (Norway) or scb.se (Sweden) or you can choose both.

The link will appear under Index regulation for individual contracts

or under the Mass adjustment function:

17

4.4.8 Lock reporting period

In order to avoid changes or new contract to be entered in periods that are closed, you can set a

start date for a reporting period. This is to ensure that already reported figures are affected. For

errors in previous periods, see the new accounting date functionality (Section 15).

Go to Settings and choose IFRS 16, set the date and press Save.

4.4.9 Properties and Support

Information about your license key. You need your license key to get new versions.

Register the company or group that will appear on the front page.

Hide or show the Tasks function.

18

Hide or show the contracts that need to be reviewed on the frontpage.

A choice as to whether to open files directly on the PC instead of on the web. The default behavior

of Macro documents is to open documents in Client Applications. The default behavior of other

type of documents is to open documents in Office Web Apps.

Upgrade the structure of the libraries after you’ve upgraded the app to a newer version with a

different library structure.

Information about support.

4.4.7 Synchronization

You can get a synchronized copy of the content in your libraries by using OneDrive combined with

SharePoint.

This function is useful if you need to copy files to a new site, download files for security storage

or due to requirements for local storage of files (Please see Microsoft security

https://products.office.com/nb-no/business/office-365-trust-center-welcome?omkt=en-US).

19

4.4.8 IFRS 16

You can have better control of registration by adding a cut-off date to the ShareControl Settings

menu. By setting this date the administrator will be able to restrict its users from making changes

that will affect results in accounting periods that have been closed. This includes both entering

new contracts and making changes to existing contracts.

You can choose reporting periods and set the first date the change can be registered. For example,

you can set reporting period date to June 30th 2020 to prevent any changes or leases being

registered before this date, so that the data in the calculation file for half-year report 2020 won’t

be changed.

A choice as to whether or not Mass update CPI or Rate and Log change should be included in the

menu

20

Scan buttons for upgrading the app to new version.

Download IQY files with all IFRS 16 data.

4.5 Libraries, folders and files

This chapter describes the library functionality, including folders and files.

21

Libraries are found on the left side of the menu and the name can be modified under Settings.

Click to get access.

Like Excel, you can use the funnel ( ) to sort and filter the content. This function is explained

further in chapter 4.5.2. This functionality is helpful when sorting and finding documents.

By clicking , the definition of each metadata appears based on the definition in IFRS 16 and

guidance about how data should be filled in to get correct values in the calculation will also

appear. You can modify and customize definitions under Settings Field descriptions.

Expired contracts are marked in pink. This is checked against the actual date.

4.5.1 Creating contracts (Folders): from draft to publish

Each unique contract needs a separate folder to be able to perform calculations.

Click New item to enter the metadata (Properties) for this folder. Follow the instructions and

register the contract details as required, you can always get help by clicking the question marks.

22

After you finish entering the metadata (Properties) for the folder, you have two choices: Save

draft and Save and publish.

If you’re confident that the data that you entered is correct, which means there won't be any

correction of data that will affect the result of calculation (Data, such as number of payments per

year, Start date or End date of lease payments, Discount rate, etc.), you can click the Save and

publish button.

After the folder is published, you can change data that won't affect the calculation for any

published folder via Edit (Data, such as Title, General information, Property details, Company,

Department, etc.). You can’t correct any data that affects the calculation via Edit. Correction of

error of a published contract's original data that is used in an IFRS 16 calculation in the initial

registration can only be done by rolling back to the previous versions. Please read chapter 15 for

guidance. Changes of data that will affect the calculation to the published folder, such as CPI

adjustment, execution of options, etc. can be done through Log other change.

Click a published folder and then click the Edit or the Log change button to edit or log changes to

an existing published folder. Please read Chapter 5 to get tips for creating folders and chapter 13

and 14 for more information about log changes.

23

If you’re not confident that the data that you entered is correct, which means you might make

some corrections to data later that will affect the result of calculation, you can click the Save draft

button.

As a published folder, changes of parameters that affect the IFRS 16 calculation can only be done

through the change log, so that the net present value of the changes is recorded at the date of

the change. However, all elements of the draft contract can be changed. You can change all the

existing data and add new data to an existing draft folder by clicking the folder and then clicking

Edit.

You can make changes to the data as many times as you want by editing the folder and saving it

as draft. When you’re confident that there’ll be no changes to the original data that will affect the

calculation, you can publish it, either by clicking the folder and then clicking Publish or by clicking

Save and publish (In the submenu of Save) after you click Edit to make changes.

When a contract is saved as a draft, it will appear as a draft in SharePoint with a draft icon " ".

24

You don’t have to publish a contract to include it in the calculation. A draft contract is included in

the calculation file (Marked in grey color and with a draft icon ), so you can check its calculation

result before you publish the contract.

We recommend that all the new IFRS 16 contracts are stored as drafts. Since all the drafts are

included in the calculation and you can't change any contracts that have been audited/ reported

without using Log change, it means that if the drafts are audited/ reported, you must publish

them and any changes you will make to them must be done via Log change.

4.5.2 Using the funnel (filtering and sorting by metadata/columns )

Click on to see the following choices:

25

The choices vary, depending on the type of metadata/ column. The text-field allows you to type

optional text and, if there is a dropdown menu, you’ll see the following picture:

You can select the options you want, and use the Select all or the Remove all choices button to

quickly select or unselect your choices.

The Show button applies your selections. Remove removes the filtering for that column. Remove

all removes all filtering for all columns. The filter functionality will be inactive when you leave a

library. An active filter will be shown by a yellow funnel.

26

4.5.3 Folders options (Cogwheel)

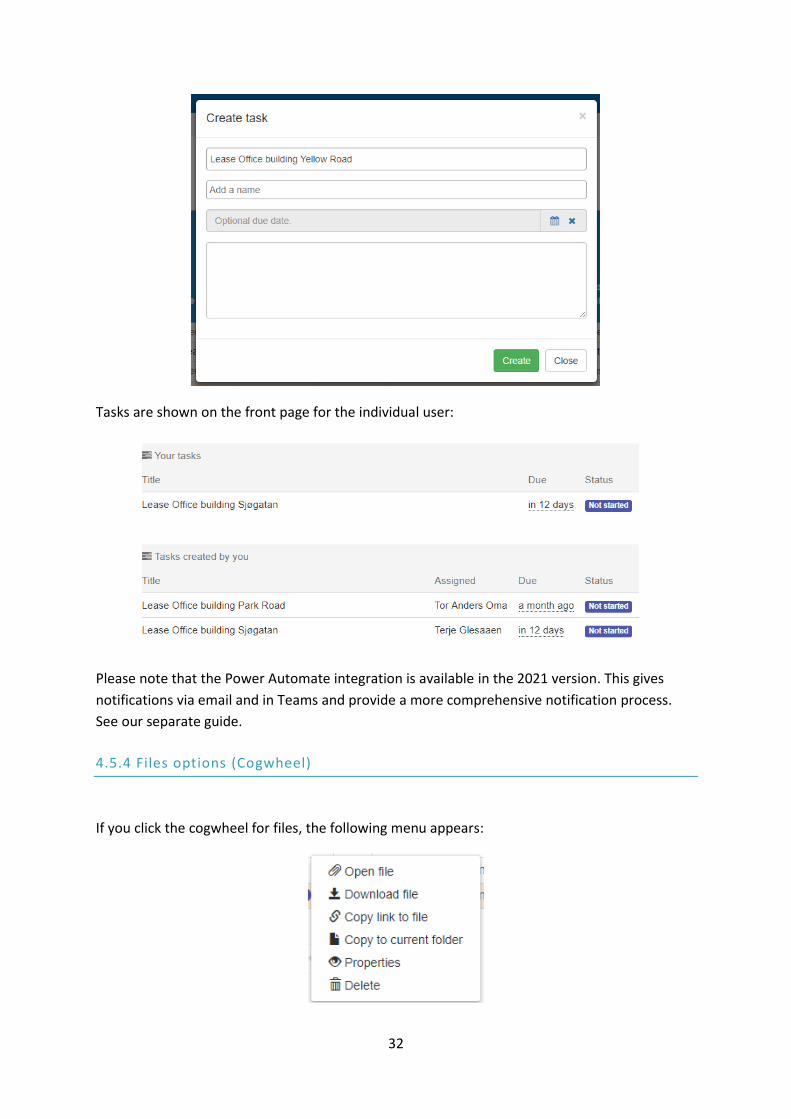

If you click the cogwheel for folders, the following menu appears:

● You can create a new file in Word, Excel, PowerPoint, or OneNote by clicking Create a new

document. It requires that you write the name of the file and select the type of file you want to

create. The file is immediately shown in the folder.

● You can upload files from your computer/ server by clicking Upload files. You can use File

Selection or drag and drop the files from your computer or emails to this window. See more

information here:

27

● Properties shows the properties of a folder and its metadata. When selecting Properties, a

window opens. Click Edit if you want to change the name or metadata. You’ll get the same window

by clicking on the folder name. The data for IFRS 16 is described below.

● You can copy a folder with metadata, including files in the folder, by clicking Copy with files.

This is useful for a more efficient registration. In the next menu you can choose the files to copy

and edit the file name before copying by clicking .

● Copy without files can be used for copying folders and metadata, but not the files attached to

the folder. Data that is unique to an IFRS 16 contract or hidden under Settings is not copied to a

new contract. This is to avoid copying irrelevant data.

Examples of data that’s not copied:

• Business combination date

• Fixed regulation

• One-time payments

• Residual value guarantee

• Other information about the right of use asset

• Termination

28

● Move folder allows you to move a folder with files to a different library. Please note that if the

library has different metadata, this will leave the field blank or make it invisible.

Choose the library you want to move the file to in this menu.

The Move function is found under the cogwheel and is useful when you want to clean up your

library by moving expired contracts to a separate library or by reorganizing your libraries.

Moving a contract from one library to another involves a check of the metadata. This is to ensure

that you don’t transfer a contract from one library with a specific metadata set to another library

with a different metadata set, which will result in data loss. Below is an overview of the different

messages that can appear when you move a contract.

If this green message appears, the destination library is ok.

29

If the metadata is significantly different, you’ll get the following yellow message (See illustration

below). In this case, you’re not allowed to move the contract to the selected library. This is to

prevent data loss.

You need to either select a library with similar metadata or establish a new library with similar

metadata. Under the Library settings you can see the category for the library you want to move

from and establish a library with the same metadata.

30

If there’s information in the contract that needs to be modified or deleted before you move the

contract, the message will look as illustrated below. The folder can’t be moved before the Data

field is deleted. In the example below, the folder you suggested moving to didn’t have the General

information or Property details.

31

● Lock allows you to prevent folders from being edited. Read access will still apply for users. This

option is changed to Unlock if the folder is already locked. Only administrators and site owners

can access the Lock and Unlock functionality.

● Create task (or task status) allows you to create a task related to a specific folder, set an optional

due date and assign it to another user of ShareControl.

32

Tasks are shown on the front page for the individual user:

Please note that the Power Automate integration is available in the 2021 version. This gives

notifications via email and in Teams and provide a more comprehensive notification process.

See our separate guide.

4.5.4 Files options (Cogwheel)

If you click the cogwheel for files, the following menu appears:

33

● Open file opens the file

● Download file downloads the file to your computer or server.

● Copy link to file gives you access to the URL address of the file.

● Copy to current folder provides you with a copy of the file to the same folder. You change the

filename in this submenu:

● Properties accesses the file name and you can change the file name here.

● Delete deletes the document (You can restore it by clicking the recycle bin).

Quick view of documents: Behind each folder and file, you’ll find three dots. Click to quickly share

the folder and see the file simultaneously. You can also open the Version log to access earlier

versions of the documents.

4.5.5 Uploading documents

Upload files allows you to upload one or several documents.

If you receive documents as attachments in emails and want to upload them to a folder, you can

drag the files directly from an e-mail to a SharePoint folder.

If you want to use the drag-and-drop method when uploading, open Upload files and drag the

files you want to upload to this window.

We recommend having a descriptive filename to understand the content of the file and to be able

to search for the document.

34

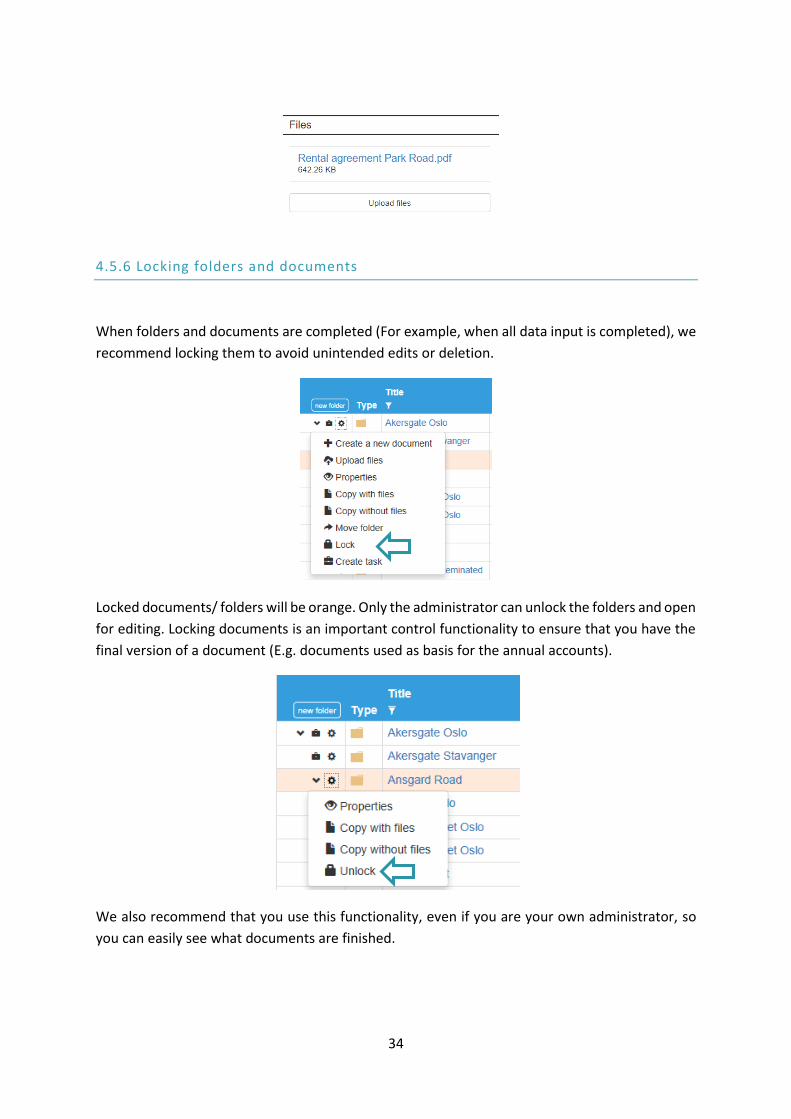

4.5.6 Locking folders and documents

When folders and documents are completed (For example, when all data input is completed), we

recommend locking them to avoid unintended edits or deletion.

Locked documents/ folders will be orange. Only the administrator can unlock the folders and open

for editing. Locking documents is an important control functionality to ensure that you have the

final version of a document (E.g. documents used as basis for the annual accounts).

We also recommend that you use this functionality, even if you are your own administrator, so

you can easily see what documents are finished.

35

4.5.7 Sharing specific documents

SharePoint allows you to share documents with others, including external users and those who

don’t normally have access to the Site. (See Installation manual chapter 6 for more information

about site sharing.)

Sharing documents can be done directly in the Office menu for Word, Excel, PowerPoint, etc.

Share documents by using options under File. This sharing functionality is SharePoint’s ability to

share Sites with others.

All users will work on the same document. It’s not necessary to send the document by e-mail, as

the receiver will get a link to the document. You can also send the document directly by e-mail.

4.5.8 SharePoint and file menus in Word, Excel and PowerPoint

You can access the files directly from Word, Excel and PowerPoint in the Last documents menu.

You don’t need to open the ShareControl add-in to get access.

4.5.9 Mobile access

SharePoint has launched an app to mobile phones (See the App Store). Your contracts can be

accessed through your mobile device based on a search of file names. We therefore encourage

you to use descriptive file names for contracts that you upload.

4.6 Processing tasks

Use the task function to assign tasks to others and process tasks that others have assigned to you.

Task processing can be viewed on the front page of the ShareControl add-in.

36

Your tasks contains an overview of all tasks assigned to you.

Tasks created by you gives an overview of all tasks you have assigned to others.

Other tasks shows the ones you’re not involved with, and where you can find them.

When you have selected a task, you’ll see its details to the right.

4.6.1 Task details on the frontpage

37

Documents displays the task folder(s) and its related documents.

Task shows all tasks processed in that folder. The most recent task will be on the top, with older

and completed tasks below.

The task status is shown beside the name of the person responsible. The initial message is shown

immediately, and no feedback is given. Click the speech bubble to add feedback, then select

Approve, Prepared, Decline or Not started to set the task status.

Click Show additional options to get Task administration. Then change the assigner, the assigned,

the title of the task, the deadline, and delete the task. When you Approve or Decline the most

recent task, you can create a New task.

4.6.2 Assigning tasks

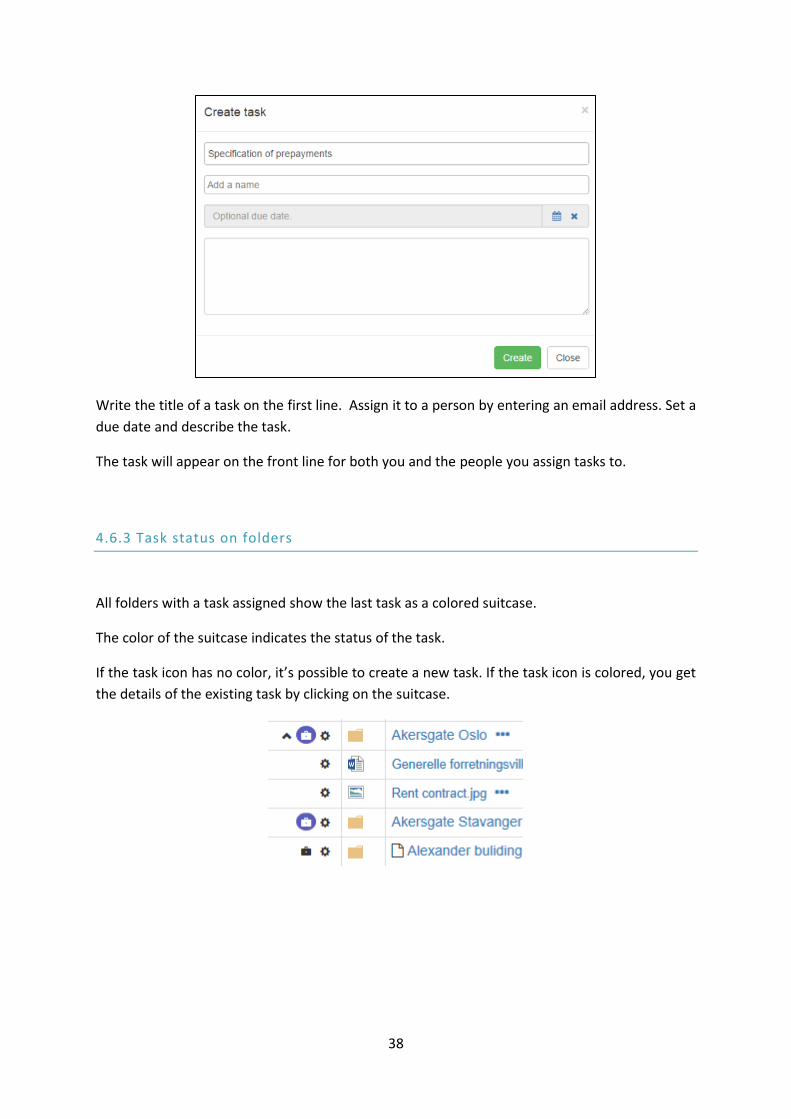

Click the task icon to start a new task.

38

Write the title of a task on the first line. Assign it to a person by entering an email address. Set a

due date and describe the task.

The task will appear on the front line for both you and the people you assign tasks to.

4.6.3 Task status on folders

All folders with a task assigned show the last task as a colored suitcase.

The color of the suitcase indicates the status of the task.

If the task icon has no color, it’s possible to create a new task. If the task icon is colored, you get

the details of the existing task by clicking on the suitcase.

39

5. Upload contracts using SharePoint

Please see the section below for guidance on how to complete information. In the SharePoint

registration, contracts are uploaded directly in SharePoint and not by using the excel spreadsheet.

But the information is the same. The excel upload will register all the data in SharePoint after the

excel spreadsheet are uploaded.

Click on the preferred library on the left side, then click on new item to get a blank schedule:

Each unique contract needs a separate folder to be able to perform calculations.

40

One unique lease needs one folder to do a separate calculation, but leases can of course be

combined to follow the portfolio application in IFRS 16 B1 or be combined as described in B2 (We

also offer separate solutions for car leases, based on input from a lessor).

By clicking on the different sections, you will get further guidance. You can also click on the

question mark. An explanation of information to be included in each field is described in the

attachment.

We recommend using the copy function to copy information from an existing folder, for

consistency in the registration of metadata.

5.1 Tips for creating folders

Once you have established the libraries you need and entered metadata, you can create folders

and upload documents. Consider the following when creating folders:

• One unique contract requires one folder; a subcontract will normally also require a

separate folder to include separate data for the DCF (Discounted cash flow) calculation. It

can be combined with the original contract, but the metadata needs to cover both

contracts in that case.

• Don’t upload your complete contract archive before you test the calculation. If fields are

erroneously entered, they need to be manually edited.

• We recommend uploading some contracts and testing the calculation before deciding

what structure fits your company best.

41

• Folders can be copied and documents and metadata can be reused, such as different

contracts from the same lessee. By using the copy function, you’ll make the registration

process more efficient. It also helps you to understand the data that is to be included in

each cell and to do the work consistently.

• The metadata that must be entered for each contract to be able to perform calculations

are marked in color. These need to be complete before the metadata is saved.

Company and Department must be entered in order to sort by companies and department. This

can be important for integration with your accounting system. If other data fields are required,

we can add those.

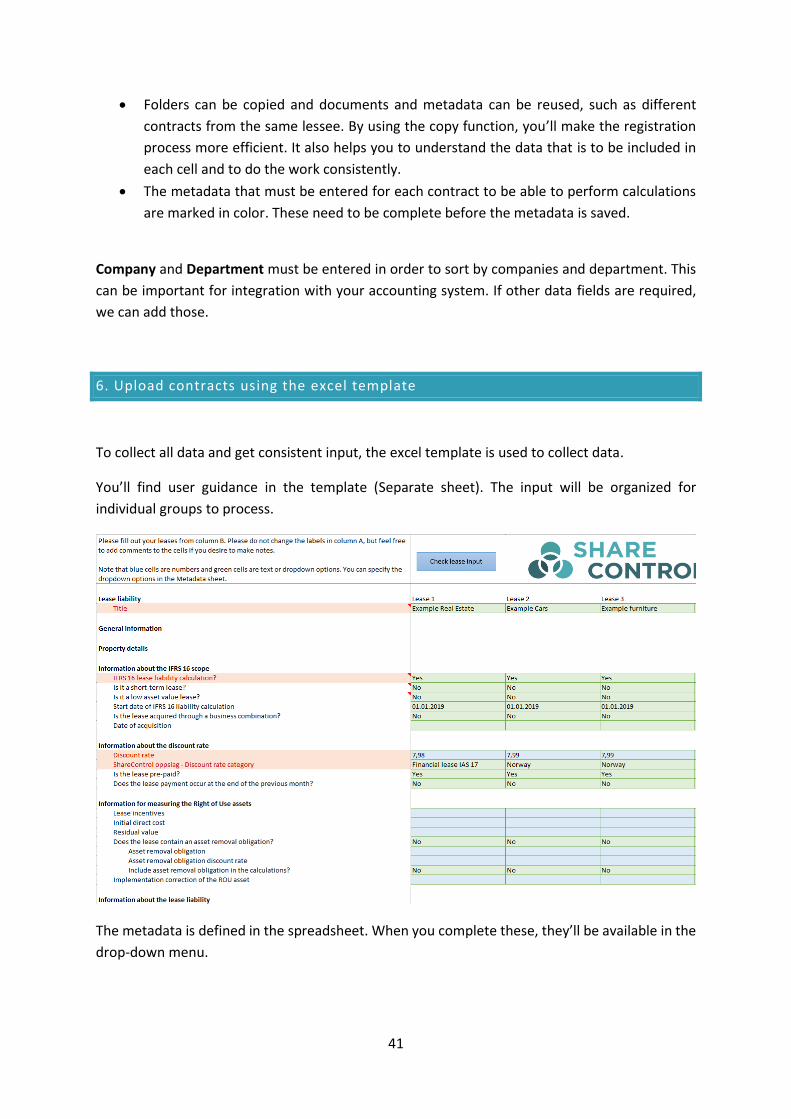

6. Upload contracts using the excel template

To collect all data and get consistent input, the excel template is used to collect data.

You’ll find user guidance in the template (Separate sheet). The input will be organized for

individual groups to process.

The metadata is defined in the spreadsheet. When you complete these, they’ll be available in the

drop-down menu.

42

The rows marked in red are mandatory. There’s a user guidance in a separate sheet described

below:

Title

In the calculation model, this is the name that identifies the contract and can only be about 20

characters long. If the name is longer, the last characters are deleted. For example, avoid writing

a "rent", "lease" at the beginning, but write instead, “Storgata 20, Parkveien 3”, etc. It’s

unnecessary to write the department- or the company name as they are registered separately.

Discount rate

The Discount rate category can be entered by selecting among the categories that you’ve defined

under the Metadata sheet. Categories of discount rates can be based on geography, rental period

and underlying asset. Please note that the Discount rate are normally not changed during the

lease term unless there is a change in the lease.

Pre-paid or post-paid lease payments

This will follow the payment pattern. Pre-paid payments are used for contracts (Most contracts)

where payments are made in advance, and post-paid payments are used for contracts where the

payments are at the end of the period. For pre-payments leases, interest will be calculated at the

beginning of each period. The last period will therefore have no interest.

Does the lease payment occur at the end of the previous month?

Answer Yes if the payment is actually made during the month before the lease period. The same

way the payment for the first quarter is made in December the year before. This will shift the

interest and depreciations to the following month, but reduces the lease liability in the month the

payment is made. The lease period is set to the period that the lease payment covers. For

example, the lease payment for a new lease from January to March is paid in December. The start

date of the lease period should be January 1, and by answering Yes to the question, the instalment

is made in December.

Use daily rates?

This function is used for payments that is based on daily rates and the periodic payments depend

on the number of days in the month.

Information measuring the right-of-use asset

43

These fields are used to enter a correction of the value of the ROU asset. This will normally not be

relevant in connection to the implementation of IFRS 16, as this results in a capitalization with

subsequent expense of previously recognized costs. For contracts entered after January 1st 2019,

these costs described in IFRS 16.24 are required to be capitalized.

Asset removal obligation: Entering values here is added to the value of the right of use asset and

should be the discounted value. The costs of dismantling and removing the item and restoring the

site on which it’s located must therefore be adjusted for inflation until this time. Be aware that

this is not a new provision under IFRS 16, but a coordination with the provisions of IAS 16.16 (c).

Impairment of ROU asset and Other adjustments of ROU assets

These options are also available under log lease changes and will affect the value of the ROU asset

the date of the change. An example is, an impairment of the ROU assets during the lease period

that needs to be registered here or other changes, like a partial reduction of the ROU asset, due

to modifications of the lease term.

Lease Payments

There are several elements that need to be considered:

What is the payment for the rental elements? It’s not necessarily the amount stated in the lease

contract or what’s paid on the last invoice. Payment to the lessor may also include more than the

actual rental element, such as property tax, lessor administration costs and insurance. In these

cases, the payment will be divided between rent and non-rent elements.

What is variable and fixed rent? It’s only the fixed rent that shall be included in the lease

obligation. For example, revenue -based rent is not included, but a guaranteed minimum rent will

be a fixed rent.

Is there an identified asset? A lease can be part of a service agreement. See guidance in IFRS 16

B9-B39 identify a lease.

The length of the lease. Understanding the length of the lease may have a significant impact on

the liability and the ROU asset in the balance sheet. Examples are options for renewal or a right

to termination before expiration of the agreement. In these cases, the lessee must assess the

period to be included in the calculation.

Non-lease components. The lessee may choose to include non-rental non-lease in measuring the

lease liability. Our experience, however, is that for property rentals, non-lease elements and

coverage of landlord activities and expenses will often be variable. This is why they’re not included

in the minimum lease payment.

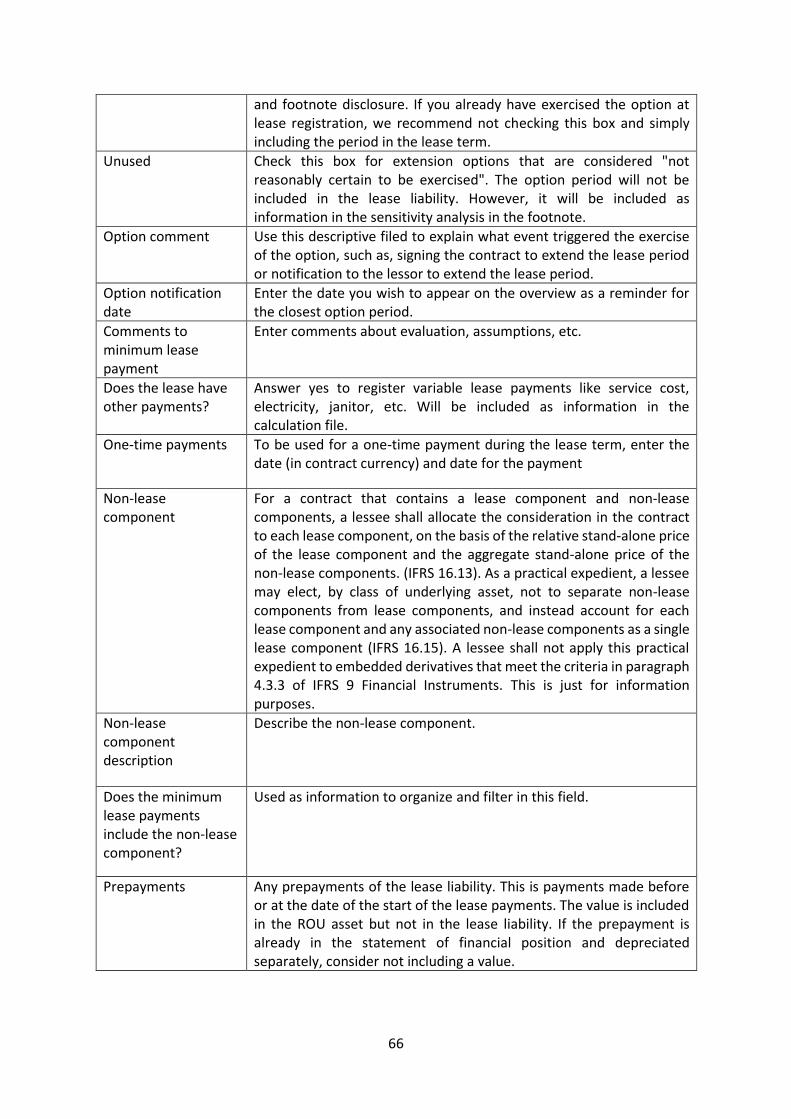

Option to extend lease period?

We recommend that all options to extend is included for overview. It also allows for the option

to be included at a later time, if currently it’s not reasonably certain that the option will be

44

exercised. To exercise an option previously not included, the log lease change functions need to

be used. (There’s no benefit to include options for extension. This only increases the lease liability

and the ROU asset without affecting depreciation significantly).

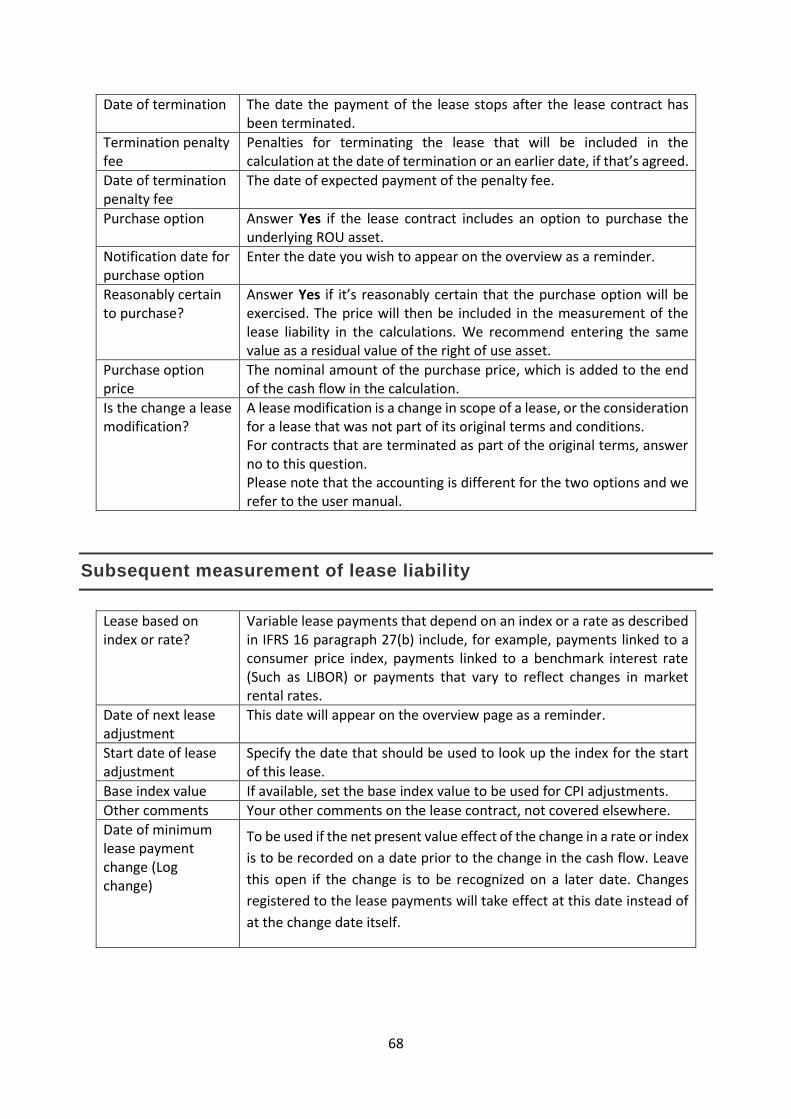

Date of termination

This field is not required for implementation. Leases that are terminated will not normally be

included (If the remaining rental period is less than 12 months). If a terminated lease shall be

included in the calculation, the End date of lease payment define the period for the lease. A lease

that’s terminated after implementation of the standard, use the termination function under Log

other change.

Notification Dates

There are several notification dates in the solution that we recommend using as a reminder, when

an option for extension or purchase of underlying asset is to be exercised or when a termination

right may be reversed. The date to be used is usually before the date of exercise of the option.

The notification will appear on the front page.

45

The first index regulation that should be noted is regulation after January 1st 2019. Remember

that the index regulation on January 1st 2019 will be included in the minimum lease payment.

After the contracts have been uploaded in SharePoint, based on the template, the contract and

the last invoice is recommended to be uploaded, for access, review and audit.

Please note that we have an integration with Power Automate in the 2021 version and refer to

the separate Power Automate guidance. You will still have notification on the front page.

6.1 Register start date and end date of lease payment correctly

The start date and the end date of lease payments are some of the factors that determine your

lease’s cash flow, which is one of the main contributors to the lease’s liability. Therefore, it’s

important to register the start date of lease payment and the end date of lease payment correctly

in our solution, to reflect the real cash flow of the lease contract payments.

6.1.1 Actual lease payment pattern

To register the start- and end date of lease payments correctly, you need find out the actual cash

flow pattern for the lease contract. We recommend that you check the lease contract or your

recent invoices of the lease payments to find out when and for which period the leases are to be

paid. After you have established the payment pattern for a lease, you can register the start- and

end date of lease payments accordingly. The payment pattern needs to be correct for

reconciliation to invoices and accruals in your accounting records.

46

6.1.2 Registers cash flow based on a date

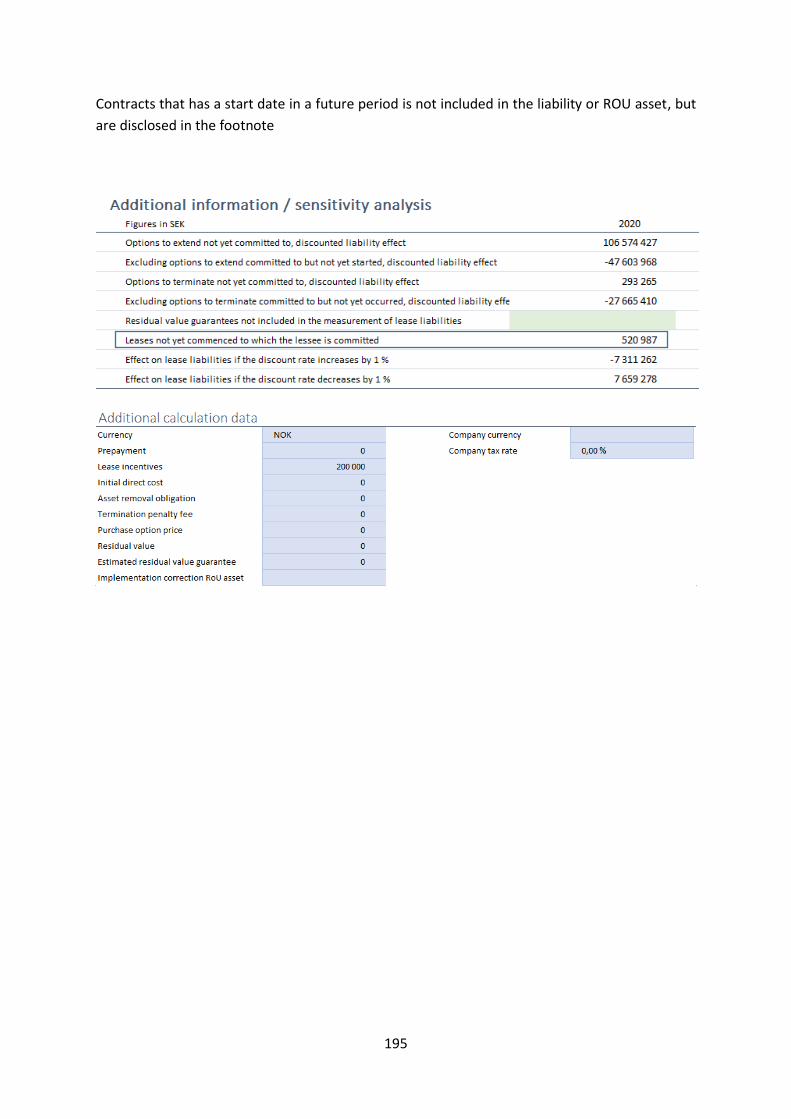

The calculation model registers cash flow based on date, frequency and amount, as opposed to direct cash flow registration (i.e. a list of dates and amounts). This makes registering simple and regular cash flows easier. There are, however, certain caveats you must pay attention to when it comes to irregular payments or date choices. The most common of these is that the end date is always inclusive, meaning that if a lease starts on January 1st 2020 and ends on January 1st 2021, the calculation considers this a 1 year and 1 day long lease, not a 1 year lease. The number of payments that occur are based on the number of months in a given payment period, rounded up, and will for a monthly paid lease with these dates result in 13 payments and not 12, as one might expect. If the lease is in fact a 1 year and 1 day lease with 12 payments, one can either register a second payment period to include the final day with a payment of 0, or one can set the depreciation end date to be 1 day later than the end of the lease payments.

6.1.3 Check calculation warnings

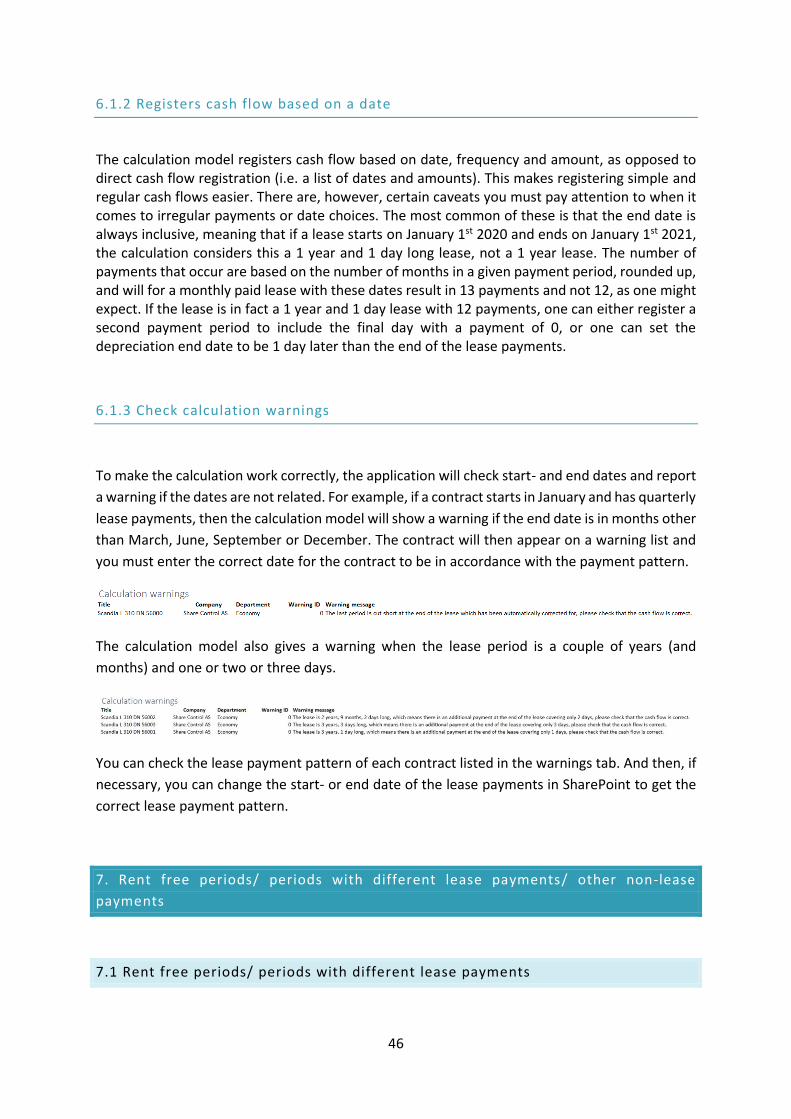

To make the calculation work correctly, the application will check start- and end dates and report

a warning if the dates are not related. For example, if a contract starts in January and has quarterly

lease payments, then the calculation model will show a warning if the end date is in months other

than March, June, September or December. The contract will then appear on a warning list and

you must enter the correct date for the contract to be in accordance with the payment pattern.

The calculation model also gives a warning when the lease period is a couple of years (and

months) and one or two or three days.

You can check the lease payment pattern of each contract listed in the warnings tab. And then, if

necessary, you can change the start- or end date of the lease payments in SharePoint to get the

correct lease payment pattern.

7. Rent free periods/ periods with different lease payments/ other non-lease

payments

7.1 Rent free periods/ periods with different lease payments

47

A contract where rent is unpaid, or paid in a lower amount, in a period after ROU asset are

available for use by a lessee, a rent free period or a period with low rent is registered as follows

(Please remember that you shall ONLY register periods after January 1st 2019):

In this example, the contract started from January 1st 2019. It has a rent-free period until June

30th 2019 and then continue with lease payment 170,000 each quarter until December 31st 2025,

which is the end date of the contract. This can also be done by using the field for the start date

for depreciation.

In this calculation, interest will be calculated and added to the lease liability in the rent-free

period. Please note that the lease liability will increase in the rent-free period.

48

Please note that the rent free period is only relevant after the ROU asset is available. If a contract

is entered for a future period and the ROU asset is not available, the lease liability should not be

recognized before the underlying asset is available. See IFRS 16.22.

7.2 Other non-lease payments

In the 2021 version, you can now register other lease payments, such as variable payments that

are not fixed lease payments of the underlying asset. Examples are; service cost in a contract for

the rent of a building (Electricity, water, cleaning, janitor services, etc.) or service cost for

machinery, and variable rent, such as cost for a crew on a ship, fuel, service, etc.

To use this function, you need to turn on this feature under Settings, go to the IFRS 16 tab and

click on Show additional options.

Select Show for Other non-lease payments.

The question, "Does the lease have other payments?” will then turn up. Click Yes and fill in the

amount. We recommend that you use the same period for the lease payment, so that the

amounts can be index regulated, going forward.

In the calculation file, the amounts will be disclosed under the Other lease payments headline for

the individual contracts.

49

In the Menu sheet, the figures will turn up if you choose Other non-lease payments as a column.

7.3 Index regulation of other non-lease payments

Other non-lease payments can be index regulated together with the lease payments in the Index

regulation function.

50

You can also use the Mass index regulation function where other non-lease payments will turn

up as a separate column.

8. Foreign currency exchange

At the date of implementation, the exchange rate at that date should be used to measure lease

liability and ROU asset.

IFRS 16 doesn’t provide specifics for foreign exchange effect. Foreign currency exchange

differences follow IAS 21 consistently with other financial liabilities. A lessee’s lease liability is a

monetary item and consequently, if denominated in a foreign currency, is required to be

remeasured by using closing exchange rates at the end of each reporting period. (BC 196 Foreign

currency exchange) (The Basis of Conclusion from IFRS 16)

51

The exchange differences, relating to lease liabilities denominated in a foreign currency, should

be recognized in profit or loss.

The value of the ROU asset doesn’t have any effect on the change in foreign currency and should

be recognized to the exchange rate at the date of the transaction (IAS 21.23) or at the rate of the

initial implementation. In ShareControl, all contracts are kept in the currency they are registered.

8.1 Foreign entities

We recommend using the foreign currency translation function in your consolidation system to

handle different currencies. This means that the input for Share Control should be recorded in the

reporting entities, based on their functional currencies. This can be handled by the accounting

integration function (Additional product).

In the recently released 2020 version, you can choose between calculating contracts in foreign

currency at the closing exchange rate or to the average exchange rate. This can be found in the

Currency Settings section of Application settings, which is found on the menu page. If Use closing

currency rates only is unchecked, as shown below, then the calculation will use average exchange

rates for income statement captions.

You can choose between exchange rates from Norges Bank or Sveriges Riksbank.

The calculation will now automatically convert income statement captions (Interest and

depreciation) to the average rate for the actual month and balance sheet captions to the closing

rate for the chosen period. The opening balance will be converted in accordance with the closing

exchange rate for the prior period. All future payments, as in footnotes or future payments in

forecast, is translated in accordance with the closing exchange rate. The exchange rates follow

the date selector, meaning that if the end date is set to March, it uses the exchange rate at the

end March as the closing rate, if available. Forecasting and budget uses the same currency table

52

as the other summary sheets. Thus, if you set the main lookup to be 2020 and do a forecast for

2022, then it will be converted in accordance with the closing exchange rate for 2020. It’s

therefore important to set the appropriate Menu lookup period before generating the forecast.

The exchange rate difference will be automatically calculated, in the reconciliation spreadsheet,

as well as, in the footnote disclosure, for the liability, as well as, the right of use asset. This is

useful for currency translation for foreign operation. For individual contracts, please see below.

The currency effects are shown as illustrated below in the footnote.

They are also shown in the complete fixed asset footnote (Pro-version).

53

To review the exchange rates used, click the Edit currency table button on the menu page, which

shows the table of exchange rates used (In this example the exchange rates are retrieved from

Norges Bank).

54

You can also review all or some of the foreign exchange rate formulas in the spreadsheet, by using

the setting below. Show some means that only changes and balance sheet captions will have the

conversion shown as an Excel formula, while all other results will be pre-calculated.

Finally, the amount in other comprehensive income (Net of currency effects on Lease liability

and Right of use asset) is shown under other comprehensive income in the tab note disclosure.

8.2 Contract currencies different from the entity’s functional currency

If a lease contract is entered in a foreign currency other than the entities functional currency, the

ROU asset is required to be recorded, applied to the foreign currency amount, the spot exchange

rate between the functional currency and the foreign currency, at the date of the transaction (IAS

21.21). In subsequent periods, non-monetary items that are measured in terms of historical cost

in a foreign currency shall be translated using the exchange rate at the date of the transaction

(IAS 21.23). Subsequent changes in the ROU asset, such as index regulation, extend of lease

periods, etc. shall be measured according to the spot exchange rate between the functional

currency and the foreign currency at the date of the transaction.

In the 2020/21 version of ShareControl, this functionality is available if you use this option under

Information about the lease liability, by answering Yes to this question. Please note that this

option needs to be turned on under Settings to be disclosed. See below.

If the lease currency is in USD and the functional currencies of the company that held the lease

set EUR in this field. This will be shown as below (The exchange rate on January 1st 2019 is set to

0.9 in the example below)

55

Please don’t use this field if you want to translate a foreign operation. See section 8.1. if that’s

the case.

Set the exchange rate at the commencement of the lease (Or set it to January 1st 2019 if the lease

was there at the implementation of IFRS 16). If you want to use the exact same exchange rate as

in the calculation sheet, look up the exchange rate from the exchange rate table. Please note that

the calculation uses monthly average exchange rates and not spot rates when converting monthly

changes of lease liability and right-of-use asset. So if you want the same exchange rate, you have

to use the average rate for the month of the transaction.

The right of use asset is now kept at the exchange rate, registered, and you will see that for the

individual contracts in the calculation file.

Subsequent changes in the lease need to be registered at the exchange rate at the date of change.

You need to register the exchange rate for each change in the contract, like rate adjustment,

exercise of an option, etc. In the illustration below, we have made the index adjustment with an

exchange rate USD to EUR at 0.89 on January 1st 2020.

56

In the calculation, this can be viewed as follows:

The change in ROU asset in EUR is the USD change of USD 52.073 * 0,89 = 46.355 and the ROU is

kept in the EUR functional currency.

The currency effects of the translation of the lease liability from the functional currency to the

reporting currency is shown in note disclosure under Amounts recognized in profit and loss as

foreign currency effects. This amount should be part of the profit and loss statement and not in

other comprehensive income.

57

In the case where the reporting (Lookup) currency is the same as the functional currency of the

lease, the Foreign currency effect will show the exchange effects on the lease liability only, as

there are none for the right-of-use asset. In the case where someone at the group level has a

foreign company that has a lease in a third currency, there will be a split between the foreign

currency effects and the transaction differences on net investments in foreign operations. This

split is calculated using the average of the average exchange rates for the period. This is easiest

shown through an example:

Assume a group in Norway (Reporting in NOK) owns a company in Germany (Reporting in EUR)

that has a lease in USD. In this case, the liability is in USD, while the right-of-use asset is in EUR,

using the historic exchange rates. If the group in Norway generates the note disclosures in NOK,

the two posts are calculated in the following way:

Foreign currency effects (NOK)

= −Liability currency effect (USD → EUR) × Average rate (EUR → NOK),

Transaction differences (NOK)

= RoU-asset currency effect (EUR → NOK)

− Liability currency effect (USD → NOK) − Foreign currency effects (NOK).

9. Business combination (IFRS 3. 28 A and B)

In a business combination, the acquirer shall measure the lease liability at the present value of

the remaining lease payments (As defined in IFRS 16), as if the acquired lease were a new lease

at the acquisition date. The acquirer shall measure the right-of-use asset in the same amount as

the lease liability, adjusted to reflect favorable or unfavorable terms of the lease, compared to

market terms.

In a business combination, the acquisition date for each lease needs to be identified and

registered under the IFRS 16 scope.

58

The start date of the IFRS 16 calculation will in this case be the date of the registered acquisition.

If you need that date for other purposes, you can register the actual start date of the contract

under the section information about the lease liability.

In the calculation file, the information will appear as follows:

10. Sub lease and use of the solution as a lessor (Pro version)

In the Share Control pro version, you can register sub lease contracts, both as financial- and as

operating lease contracts, as a lessor.

Please note that the IASB decided that, when classifying a sublease, an intermediate lessor should

evaluate the lease by reference to the right-of-use asset arising from the head lease and not by

reference to the underlying asset. A classification of a sublease as a financial lease depends on

the sub lease terms, compared with the head lease.

59

To register a contract as a lessor, you always need to register either a lease agreement or an asset

on the balance that you keep as a lessor. You also need to decide if the lease contract qualifies as

a financial lease contract (A requirement for offsetting a lease contract as a lessee) or as an

operating lease contract that’s a registration for a footnote disclosure. See IFRS 16.61.

After you’ve made a decision about the lease being operating or financial, you need to decide on

a head lease or an asset.

The headlease must be registered before you make the identification, and you can now choose

from all leases registered on this site.

Choosing an asset (Not registered in ShareControl), use a description of the asset that’s leased as

shown in the example below.

60

By identifying a head lease or an asset, the contract is registered as a lessor contract and the lease

liability is replaced by a lease receivable. On the menu site, you can see the result as shown below.

In the footnote disclosure, there are separate columns for lease receivables, both financial and

operating.

61

10.1 Offset ROU asset against lease receivable

In case the intermediate lessor recognizes the net investment in the sublease (A receivable) rather

than a right-of-use asset, you can proceed as follows (See IFRS 16 BC 233).

Calculate the amount that should be offset and register the amount here:

The amount will be included in the gain and loss calculation and reduce the book value of the ROU

asset.

11. Metadata (Contract data) for IFRS 16

There are descriptions of different metadata in the IFRS 16 add-in (Click on the question mark).

The metadata required to perform an IFRS 16 calculation is marked in red in the add-in. This needs

to be completed before you can save the registration.

In the template, certain registration rules are implemented to avoid incorrect registration.

Please note the following: Lease payment data should only cover periods from January 1st 2019

and forward. If you consider implementation option IFRS 16, C8 (i) (modified retrospectively

implementation), historical data will be changed in excel, but the date of the start date lease

payments needs to be correct.

Lease liability

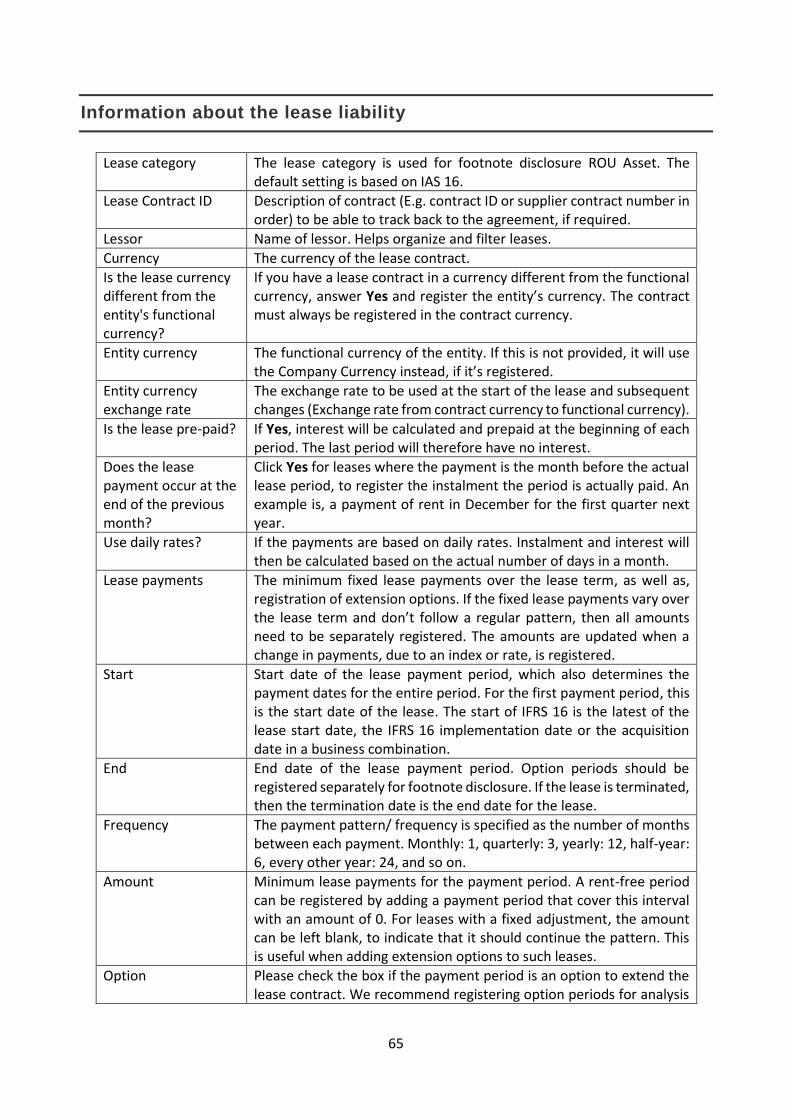

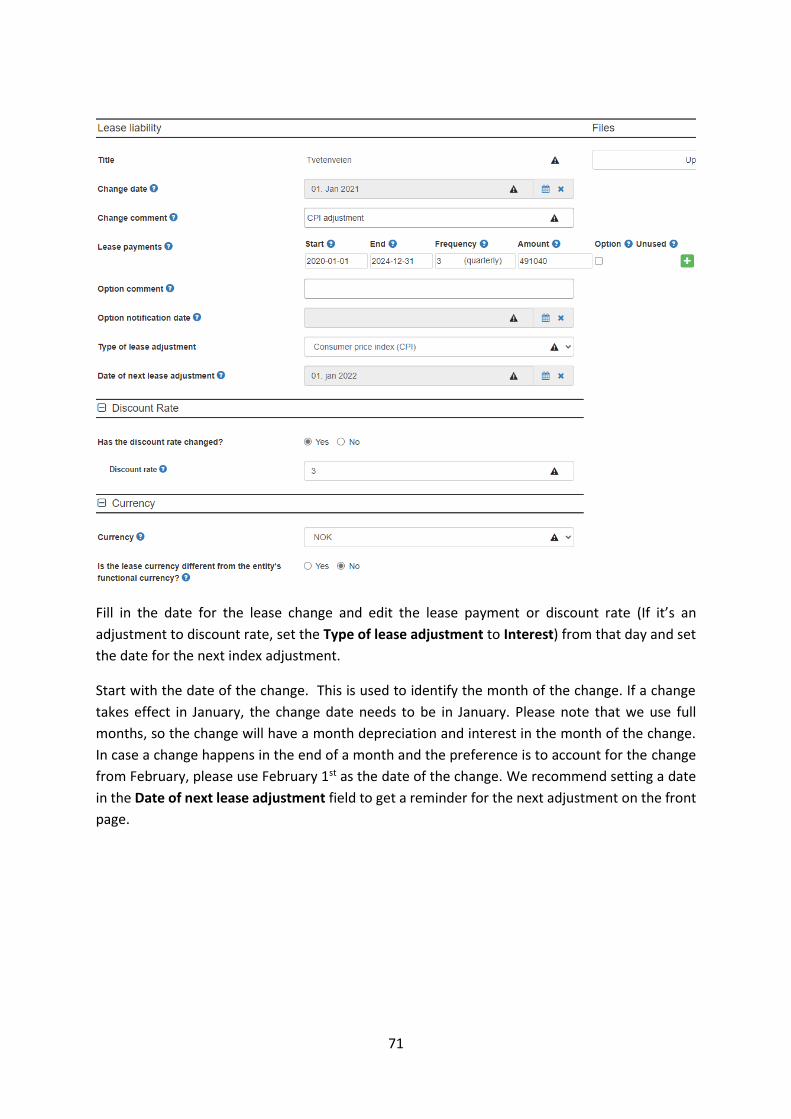

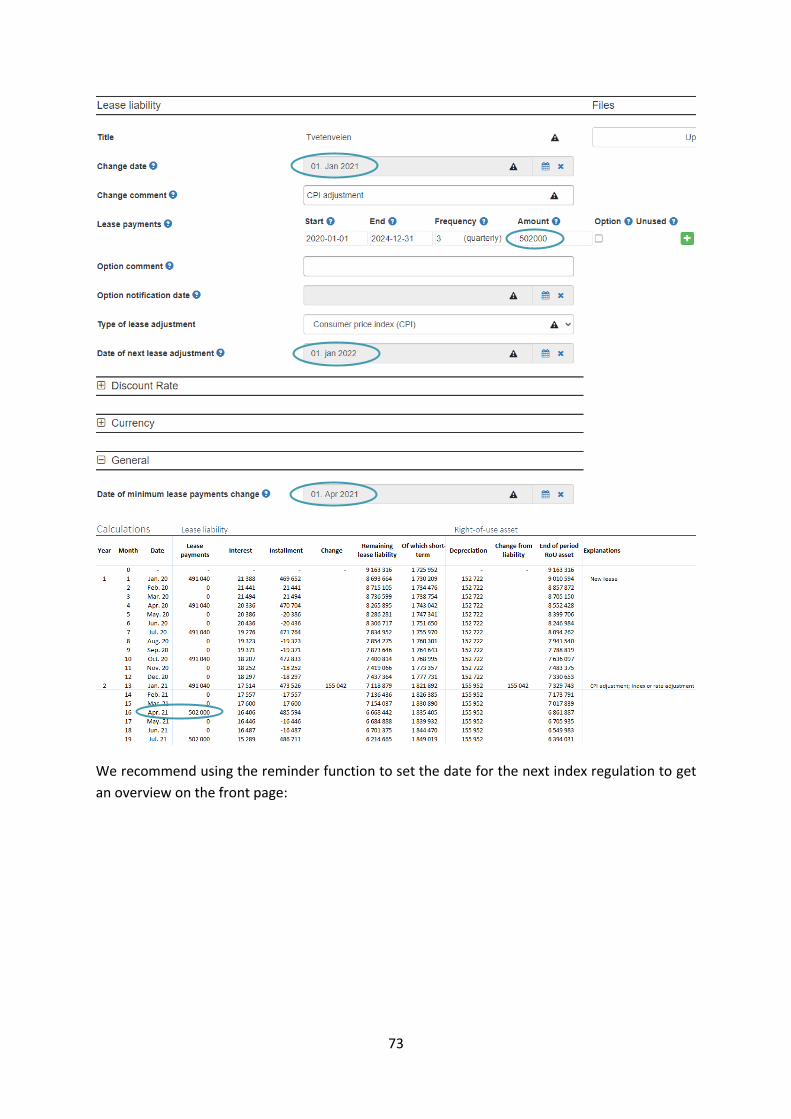

Title We recommend that you use a descriptive title to make it easy to sort and search later. The title is also used in the calculation for identifying individual contracts.

Change date (Log change)

The date the net present value of the change is recorded.

Change comment (Log change)

Comment to the change registered. We recommend making a description for easier overview of changes and roll back to previous versions.

62

General information

Tenant Lease holder’s legal name.

Landlord Legal name.

Property detail

Address Address where the asset is being used.

Postal code Postcode/ ZIP Code

Country Country where the asset is being used.

IFRS 16 scope

IFRS 16 lease liability calculation?

A lessee may elect not to apply the requirements if it's (a) a short-term lease (Less than 12 months), or (b) leases for which the underlying asset is of low value. If the answer is no, please classify the lease as a short-term lease or a low value lease in footnote disclosures. If one of these exceptions is relevant, answer no.

Is it a short-term lease?

A lease that, at the commencement date, has a lease term of 12 months or less. These contracts can be included for information and footnote disclosures. A lease that contains a purchase option is not a short-term lease. Information about payment of short-term lease is required in the footnote disclosures.

Is it a low asset value lease?

If the ROU asset (The right-of-use asset) is of low value. These contracts can be included for information and footnote disclosures. See IFRS 16 B3-B8 for guidance.

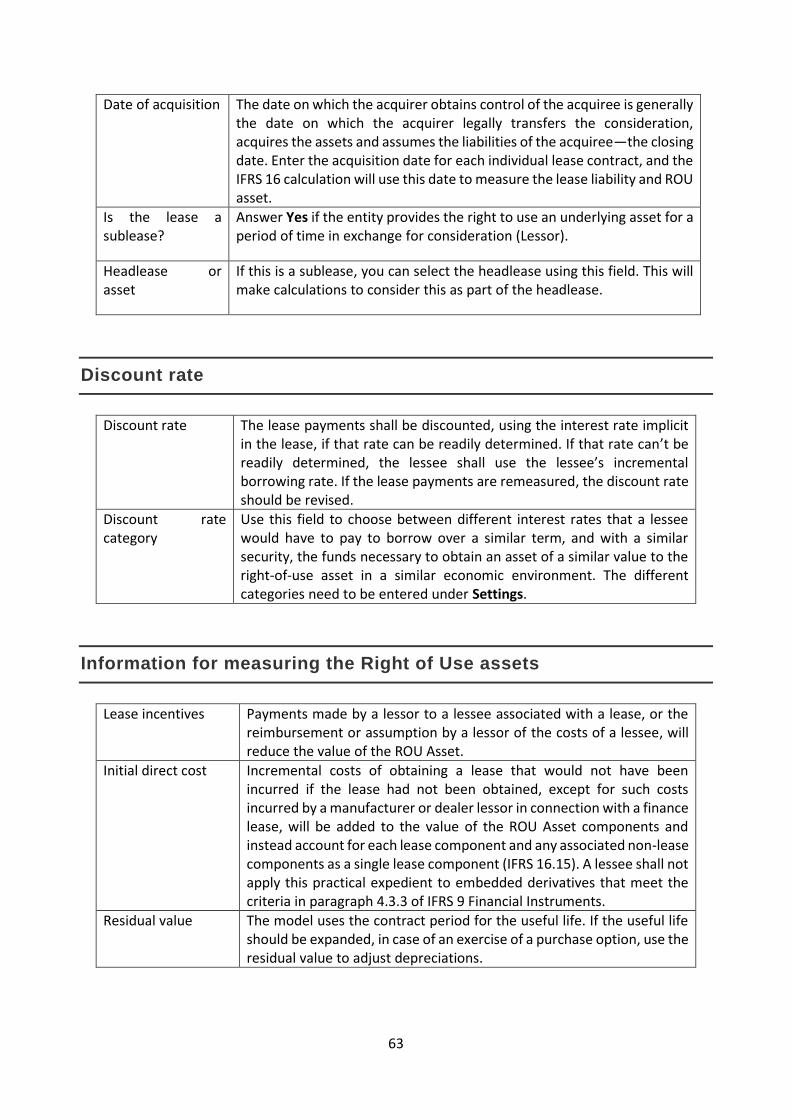

Is the lease a financial lease?

As a lessee, this field is to distinguish between finance leases based on the previous IAS 17, if that’s relevant for your local Gaap accounting. As a lessor, you distinguish between financial leases and operational leases using this question. See IFRS 16.61 for more information.

Is the lease acquired through a business combination?