Embed Size (px)

Citation preview

Iceland – Economic Outlook

28 January 2021

Successful Bond Issuance Eurobond issuance in the amount of 750 million with 0% coupon

Maturity in April 2028 – fits well into maturity profile of outstanding debt

Bonds were issued at a yield of 0,117% - 48 bps over Midswaps

Terms improved by 12 bps from the initial price guidance in book building process

Well received by investors with demand totaling 3.5 bn. EUR – more than 4x issued amount

The buyer group included over 150 investors mainly from Northern-Europe

Investor group: banks, insurance companies and other institutional investors

Joint lead managers were Citibank, Barclays, and Deutsche Bank

COVID-19: Successful health responseAs of January, Iceland has the lowest number of new COVID-19 cases per capita in Europe. Testing, contact tracing and quarantines have been pivotal.

Source: Macrobond.

0

100

200

300

400

500

600

700

800

13-Jan-20 13-Feb-20 13-Mar-20 13-Apr-20 13-May-20 13-Jun-20 13-Jul-20 13-Aug-20 13-Sep-20 13-Oct-20 13-Nov-20 13-Dec-20

New COVID-19 cases now among the lowest in OECDNew diagnosed COVID-19 cases per 100,000 population, 14 day cumulative

OECD interquartile range Iceland OECD median

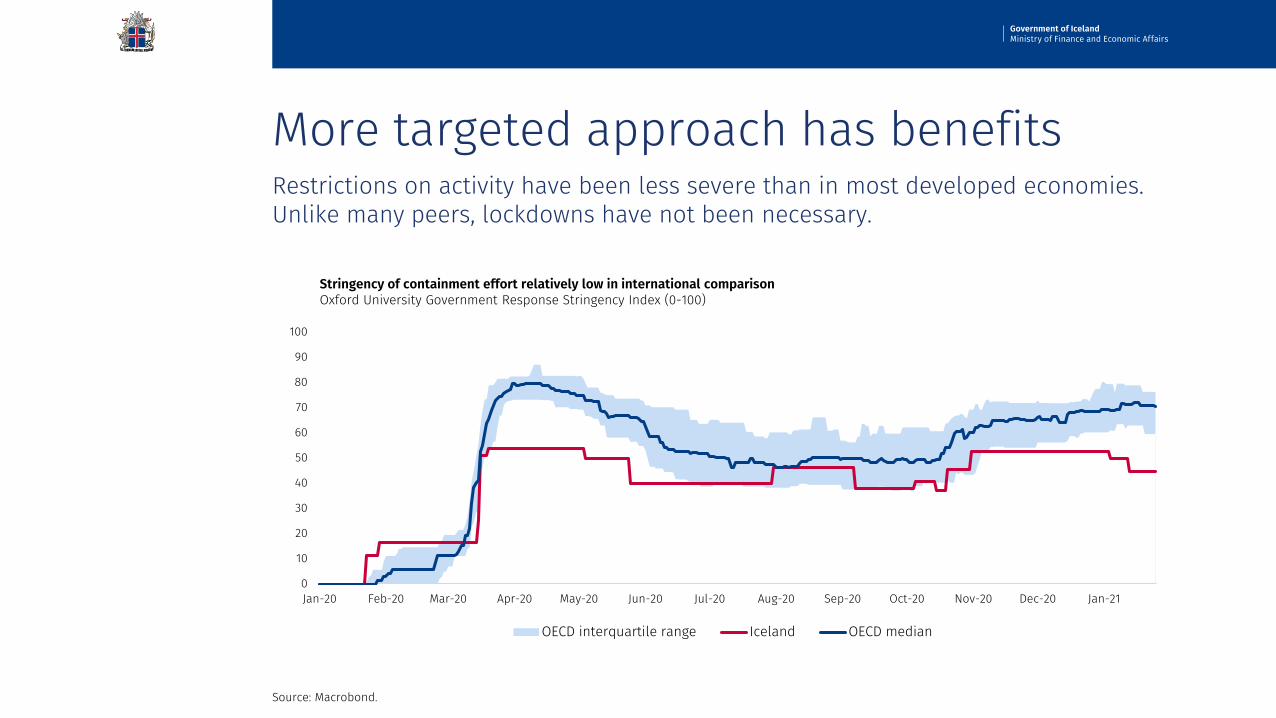

More targeted approach has benefitsRestrictions on activity have been less severe than in most developed economies. Unlike many peers, lockdowns have not been necessary.

Source: Macrobond.

0

10

20

30

40

50

60

70

80

90

100

Jan-20 Feb-20 Mar-20 Apr-20 May-20 Jun-20 Jul-20 Aug-20 Sep-20 Oct-20 Nov-20 Dec-20 Jan-21

Stringency of containment effort relatively low in international comparisonOxford University Government Response Stringency Index (0-100)

OECD interquartile range Iceland OECD median

Iceland entered the downturn from a favorable starting positionIceland’s track record of high and sustainable growth, underpinned by a strong resource base, sound policies, favorable demographics and strong human capital, is a cause for optimism.

Germany

France

Italy

UK

DenmarkSweden

Iceland

80

90

100

110

120

130

140

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

Iceland had experienced strong growth in recent years in comparison with peersGDP, 2010 = 100

Forecast

Source: Statistics Iceland (2010-2019 historical figures for Iceland), IMF WEO October 2020 (2020-2021 forecasts, 2010-2019 historical figures for other countries).

0

1

2

3

4

5

6

7

8

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

Foreign exchange reserves are at a comfortable 30% of GDPCentral bank FX reserves, bn. USD

Very strong external position provides policy buffers

Source: Macrobond, Central Bank of Iceland. NIIP excludes depositary institutions in winding-up proceedings.

FX sales in recent months only a

fraction of reserves

-250%

-200%

-150%

-100%

-50%

0%

50%

'02 '04 '06 '08 '10 '12 '14 '16 '18 '20

Large current account surplus has contributed to significant strengthening of NIIPNet international investment position, % of GDP

2020Q3:33% of GDP

Strong bank capital and liquidity buffersCapital adequacy ratios of systematically important banks well above requirements and the banks have ample liquidity to support the economy.

Source: Central Bank of Iceland. In right figure, 2020 value is Q3.

28%

22%25%

0%

5%

10%

15%

20%

25%

30%

Arion Bank hf. Íslandsbanki hf. Landsbankinn hf.

All largest banks comfortably above capital requirementsD-SIB capital requirements and CARs, 2020Q2

Pillar I Pillar II

Capital buffers Management buffers

CAR

0%

5%

10%

15%

20%

25%

30%

2013 2014 2015 2016 2017 2018 2019 2020

Bank capital adequacy ratios high in European comparisonAverage tier 1 capital ratios

Icelandic SIBs Large banks, Nordics

Large banks, Europe

6%

-40%

-30%

-20%

-10%

0%

10%

20%

Domestic consumption of Icelanders has been strongDomestic payment card turnover, real growthy-o-y, 14 day average

Private consumption has reboundedDomestic spending grew once pandemic subsided. Economic policy response and reorientation of spending from tourism abroad to domestic goods and services also help.

Source: Eurostat, Central Bank of Iceland, Ministry of Finance and Economic Affairs.

Thanks to containment of pandemic, consumption recovery has persisted into the new year

-2% -2% -4% -4% -4% -5%

-8%

-14%

-30%

-25%

-20%

-15%

-10%

-5%

0%

Private consumption has been stronger than in peersY-o-y change in quarterly private consumption

2020Q2 2020Q3 Iceland, 2020Q3

Firm recovery expected to begin this yearStrong GDP growth this year expected by IMF (4.1%), Central Bank of Iceland (2.3%) and Statistics Iceland (3.9%), supported by strong fiscal and monetary policy response.

Source: Statistics Iceland actuals and October 2020 forecast.

4,5% 3,9%1,9%

-7,6%

3,9% 3,1% 2,6%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

2017 2018 2019 2020 2021 2022 2023

Statistics Iceland forecast, OctoberContributions to GDP growth

Private consumption Public consumptionCapital formation ExportsImports GDP

0

500

1000

1500

2000

2500

3000

3500

4000

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

2026

2019 GDP level expected to be surpassed in 2023Bn. ISK, 2020 prices

Actuals Forecast

Unemployment has risen as expectedSigns that tide in labor market is shifting, with unemployment rising less in December than anticipated and more companies now intending to hire than lay off staff.

Source: Directorate of Labour, Central Bank of Iceland.

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%Ja

n-18

Mar

-18

May

-18

Jul-

18Se

p-18

Nov-

18Ja

n-19

Mar

-19

May

-19

Jul-

19Se

p-19

Nov-

19Ja

n-20

Mar

-20

May

-20

Jul-

20Se

p-20

Nov-

20

Rise in unemployment is tapering off

of which related to partial employment schemeUnemployment

-60%-50%-40%-30%-20%-10%

0%10%20%

More companies now intend to hire than lay off staff% of firms intending to increase staff minus % of firms intending to decrease staff, next 6 months

September 2020 December 2020

Inflation and unemployment expected to decline in 2021

Source for left figure: Statistics Iceland actuals (2000-2020), Statistics Iceland October forecast (2021-2022).Source for right figure: Statistics Iceland actuals (2019), Statistics Iceland October forecast (2020-2023).

0%

2%

4%

6%

8%

10%

12%

14%

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

Inflation expected to be much lower than in previous downturns and to rapidly approach target this year

Inflation target (2.5%)

3,6%

7,8%

6,8%6,2%

5,4%

2019 2020 2021 2022 2023

Unemployment expected to start to decline this year

Bridge the gap for businesses

Protect vulnerable households

Facilitate a strong rebound

11. Closure subsidies12. Support loans13. Netting of income tax

14. Mental health, remote medicine15. Protection of vulnerable groups16. Special subsidies

17. Boosting innovation18. Summer measures for students19. Effective job-seeking20. Domestic value creation

Phase I (March) Phase II (April)

1. Part-time employment2. Bridge loans to companies3. Deferral of tax payments

4. Wages during quarantine5. Supplemental child benefit6. Private pension withdrawals

7. Subsidy for tourism operators8. VAT refund in construction9. Facilitation of imports10. Investment initiative

21. Income loss grant

22. Extension of Income-relatedunemployment benefits

23. Tax incentive for business investment24. Resilience grant

Phase III (November)

Measures were swiftly introduced to mitigate the economic effects of the crisis

Initiatives in tourism• Marketing campaign abroad once situation

normalizes will highlight Iceland’s strengths as a tourist destination.

Large increase in investment• A government investment boost of 4% of

2020 GDP over the years 2020-2025.

• Emphasis on labor-intensive projects which support long-run productivity.

• Business investment also supported through tax measures.

Boosting innovation• Additional contribution to companies

investing in growth.

• Expediated reimbursements for R&D investments

• In total, a 65% increase in contributions to innovation between 2019 and 2021.

A clear focus on the longer run

Support to R&D has been doubled

Source: Ministry of Finance and Economic Affairs.

0

5.000

10.000

15.000

20.000

25.000

30.000

35.000

2016 2017 2018 2019 2020 2021

Clear focus on innovation with significant strengthening of government supportMillion ISK, 2021 prices

Tax deduction for R&D EU support for education, research and technical development

Icelandic Research Fund Technology Development Fund

Kría, the Icelandic Venture Initiative Tax support for filmmaking

Other

1% of GDPin 2021

Thank you