Embed Size (px)

Citation preview

IASFAA Conference Fast Currents and Flash Floods

A discussion on AR Collections, Skip Tracing & Institutional Delinquency

Presenters

Ms. Randi Hudson, Briar Cliff University

Dr. John G. Schwarm, General Revenue Corporation

Agenda • Institutional Loans

– Loan design and documentation

– Loan Size / ABI

– Workout strategies

• Skip Tracing Strategies

– Situational Analysis Cause and Solutions

– Government Regulations

– 21st Century tools

• A/R Collections

– Situational Analysis Cause and Solutions

– Critical Business Importance

– Metrics and Benchmarks

– Internal and Agency Relations

– Scorecards

– Collection Fees

A/R Collections

Situational Analysis

• Cost of education vs. income

– Parents income reductions / job loss / layoffs

– Graduates not finding employment

• Credit history and Poor credit history socially acceptable

– Financial tools designed to manipulate this group

– College doesn’t care about small balances

A/R Collections

Situational Analysis

• Social perceptions and blended families

– Graduates boomerang back home

– Sandwich generation caring for older parents and returning college graduates

– Delay of marriage and home ownership

– Generation without critical skills and financial capacity to be independent.

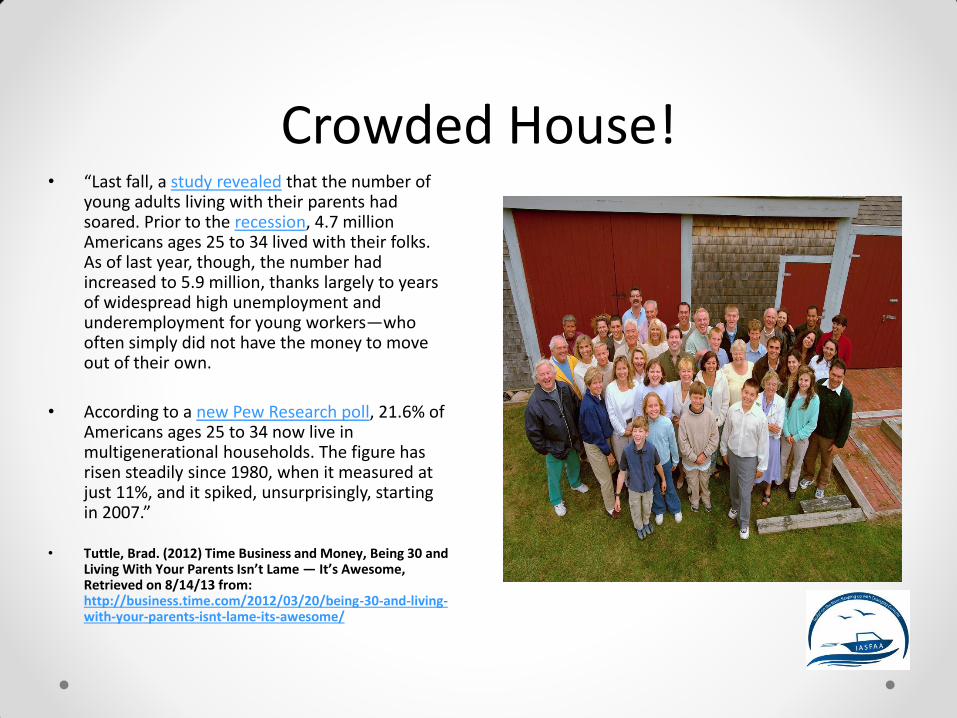

Crowded House!

• “Last fall, a study revealed that the number of young adults living with their parents had soared. Prior to the recession, 4.7 million Americans ages 25 to 34 lived with their folks. As of last year, though, the number had increased to 5.9 million, thanks largely to years of widespread high unemployment and underemployment for young workers—who often simply did not have the money to move out of their own.

• According to a new Pew Research poll, 21.6% of Americans ages 25 to 34 now live in multigenerational households. The figure has risen steadily since 1980, when it measured at just 11%, and it spiked, unsurprisingly, starting in 2007.”

• Tuttle, Brad. (2012) Time Business and Money, Being 30 and Living With Your Parents Isn’t Lame — It’s Awesome, Retrieved on 8/14/13 from: http://business.time.com/2012/03/20/being-30-and-living-with-your-parents-isnt-lame-its-awesome/

“Move Out Already!”

• “Nearly 25 million adults live at home with their parents because they’re unemployed or underemployed, they’re trying to pay off student loans or save money to buy a place, or for any number of other reasons. While calling mom and dad your “roommates” may be a smart financial move, it’s the kiss of death for a healthy dating life. Trulia’s survey found that only 5% of unmarried adults would be open to dating someone who lived with their parents.”

• Corbett, Michael, February 2012, Romance & Real Estate: How Your Housing Situation Affects Your Love Life. Retrieved on 8/14/13 from: http://business.time.com/2012/02/14/romance-real-estate-how-your-housing-situation-affects-your-love-life

Critical Business Importance

• Business Officers

– Not the “bad guys” but enforce institution policies

– Collecting on accounts equals institutional profitability

– Negotiate with students and families continuously

– Design repayment strategies for win / win relationship

– Decide on when to move accounts to collection agencies

Metrics and Benchmarks

• Schwarm’s 90/10 Postulate: “90% of students pay on time with the remainder of 5% will pay with some encouragement and the other 5% will attempt to avoid the debt.”

• Internal collections: Work the account for 90 days, then to external collections

• External collections: Work the account for 365 days, then returned to college

Metrics and Benchmarks • Agencies provide

recovery performance

• Institutions develop analysis tools – Recovery performance

– Type of account

– Cost to institution

– Customer Service

– Complaints and violations

– Law suits

• 40% Recovery rate for internal collections

• 30% Recovery rate for external collections

• 2nd and 3rd placement accounts recover 15%.

Internal and Agency Relations External Collections

• Fluid and frequent communication

• Realistic results

• Expert in all collection regulations

• Reasonable costs

Internal Collections

• Collaborative with all departments

• Consistency in treatment of accounts

• Respect for student / situation

• Negotiations with head and heart

It’s Greek to Me!

Collectors have to use all three strategies when negotiation:

• Logos: Appeal to the logic of the student.

• Pathos: An emotional appeal to student.

• Ethos: Appeal to student as you are the authority on issue and have great character and respect.

Agency and Internal Scorecards • Separated by debt type

– Federal loans – A/R accounts – Institutional loans – Parking – Tuition Accounts – Misc. debt types

• Measure net placements – Net out adjustments – Net of closed accounts

• Updatable report – Adjust totals monthly – Customers pay monthly

• Separate payment – Cash – Consolidation

• Fair and non-biased

• Outcome based

• Quantitative

• Time frame 1 year min

• Shared with agencies

• Comparison of “like” portfolios

• Encourages competition

• Compare against internal collection efforts

• Qualitative issues – Agency customer service

– Complaints by staff

– Complaints by students

– Agency communication

– Value proposition

Collection fees • Fees based on:

– Age of debt

– ABI (Average borrower Indebtedness)

– 1st, 2nd, or 3rd placement

– Type of school / program

– Type of debt i.e. parking, tuition, loan,

– RFI / RFQ / RFP

• Can you charge collection fees?

• Disclosures to students

• Can you report to credit bureau?

• When to report to credit bureau?

• Pre-collection periods

Institutional Loans

• Loan Purpose and Design – Designed for an emergency or

other financial tool

– Promissory note, Loan terms and repayment options, collection fees, and credit bureau reporting

– Consider cosigners

– Total Available resources in portfolio budget

– Number of loans per year and minimum balance

– Renewable loan each year

– Consider satisfactory academic progress

Institutional Loan Documentation • Student loan application

– Demographics, address, e-mail, phone

– References

• Promissory Note – Wet vs. Electronic signature

– Cosigners?

– Include all loan terms, fixed rates, variable rates, late charges, credit bureau reporting, and collection fees

Institutional Loan Size & Servicing • Cost of servicing a loan is the same regardless

of size

• Smaller loans are harder to collect, student indifferent to amount

• Many small loans increase workload on business office / collection office

• ABI = Average Borrower Indebtebness – Amounts > $3,000.00 have lower success rate

than those from $1,000.00 - $3,000.00

Institutional Loans

Work Out Strategies • Consider max term of repayment of 10 years

• Waiving of fees, late charges, past due interest

• After 30 days, contact cosigner directly

• Minimum monthly payment, any delinquency, no new loans

• Gather financial history and review budget with individual

• Design comfortable and realistic payment plans

• Schedule payment dates according to payroll

Skip Tracing Strategies

Using 21st Century Tools

Sea Hunt or Skip Tracing • We live in a world where virtually all our students are

in constant connection with their respective social networks. However, they are largely disconnected from their financial life and even harder to reach when you are looking for a payment. In this portion of the session, you will listen to a discussion of new strategies, tips, and tricks from the professionals on how they track down these missing persons.

Skips: definition and goals.

• Account holders that do not have current contact information with the creditor.

– Strategic search involving numerous leads

• Goal: Locating and validating

– Contacting 1st and 2nd degree relatives

– Validate residence and place of employment

– Obtain personal information to enable collection

– Once contacted, good chance of recovery

Why do people skip?

• Procrastination

• Fear / Panic

• Path of least resistance

• Confusion

• Don’t know who to talk to on campus

• Problem too deep to find a way out

• Learned behavior from parents / peers

How can you disappear? • Don’t use credit – cash only

• Don’t own property – no bank accounts

• Couch surf / roommate responsible

• Spouse responsible for everything

• Parents hiding adult children

• Straw purchase (Parents buying car for child)

• Living in shelter / foreign assignment

Competencies of a skip tracer Detail-oriented

Assertiveness

Persuasiveness

Helpfulness

Creativity

Competitiveness

Goal Oriented

Intelligence

Common Sense

Patience

Self-control

Friendly Personality

Persistence

Typical Account Scrub –

Placement process

High Performance Collection Agency

Methodology

Accounts Distributed Skip Trace or Contact to

Federal Unit

Skip Trace Division and Front Line Collection Division

Management Review

Weekly Inventory Spins

Calling Strategies

Telephone contact is attempted via Time

Management and dialer campaigns launched

Skip-tracing

Skip-trace waterfall initiated coupled with manual skip-

tracing

Skip Trace Waterfall Tools

Accurint • A LexisNexis brand skip-tracing tool designed to locate more debtors, increase

amounts collected, increase efficiency and shorten the collection cycle

Acxiom Insight Collect • Interfaces with FACS™ to effect a waterfall scrub and locate process

Banko • Processing to determine if a debtor has filed bankruptcy

CBC Innovis • Provides unique address and telephone numbers in order to maximize ability to

contact debtors

Equifax • Provides CBR reports and other location tools

Experian • Provides CBR reports and other location tools

DeathMaster • Verification of deceased debtors by SSN, including date and place of death

Electronic Directory Assistance

• Integrated into FACS™ to find telephone numbers for homes and businesses

Teletrack • Credit bureau for sub-prime lenders not reporting to the major credit bureaus

TALX The Work Number • Automated employment and income verifications

TransUnion • A debtor locating tool with the following features: Individual Monitoring SSN

Search ID Search Contact Locator Comprehensive Locator Report

Verifacts • A tool used to located a debtor’s telephone number and place of employment

Social Networks & Skip Tracing • Use social network to find subject, do not use

this medium to communicate or collect.

• Business officers rarely use any social media to locate debtors

– Use alternative products such as Trans Union, Equifax, and Experian

– Address, employment, and Social Security Number searches through credit bureaus

Popular Social Network Web Sites 10. My Yearbook

11. Meet Up

12. Badoo

13. BeBo

14. My Life

15. Friendster

1. Facebook

2. Twitter

3. Linked In

4. My Space

5. Ning

6. The Google

7. Tagged

8. Orkut

9. Hi 5

Social Networking

Venn Diagram

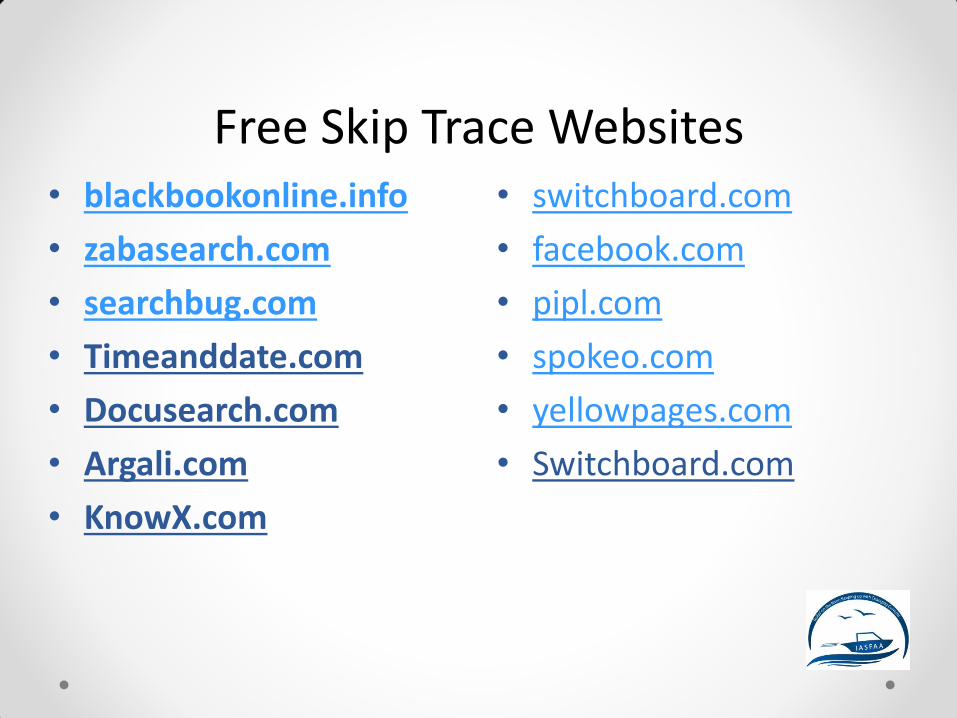

Free Skip Trace Websites • switchboard.com

• facebook.com

• pipl.com

• spokeo.com

• yellowpages.com

• Switchboard.com

• blackbookonline.info

• zabasearch.com

• searchbug.com

• Timeanddate.com

• Docusearch.com

• Argali.com

• KnowX.com

Free Skip Trace Websites • anywho.com

• 411.com

• blackbookonline.info

• yellowbook.com

• manta.com

• hoovers.com

• google.com

• whitepages.com

• people.yahoo.com

• pipl.com

• skipease.com

• addresses.com

• whowhere.com

Fee-Based Skiptrace Services Interactive Data

Master Files

RealEDA

SkipTraceInfo

U.S. TRACERS

Veri Facts

Accurint LexisNexis

Acxiom Insight Collect

Choice Point

Experian

Fletch Data

More Research Tips Charged Internet Search:

• If other attempts have failed to yield information, use a fee-based search engine if one is available.

Tax Assessor:

• Determine if the borrower owns property. Consider calling the landlord for the borrower and leave a message if necessary

Credit Bureaus Credit Bureau Report:

• If other attempts have failed, order a CBR for the borrower. The CBR does not benefit a collector unless the information is used.

Credit Bureaus:

• EQUIFAX www.equifax.com

• TRANSUNION www.transunion.com

• EXPERIAN www.experian.com

What does your SSN reveal? • Social Security "Area Code" Number Chart

The first three digits of a Social Security Number correspond to locations as follows:

• SSN State or Territory SSN State or Territory

• 001-003 New Hampshire 449-467, 627-645 Texas

• 004-007 Maine 468-477 Minnesota

• 008-009 Vermont 478-485 Iowa

• 010-034 Massachusetts 486-500 Missouri

• 035-039 Rhode Island 501-502 North Dakota

• 040-049 Connecticut 503-504 South Dakota

• 050-134 New York 505-508 Nebraska

• 135-158 New Jersey 509-515 Kansas

• 159-211 Pennsylvania 516-517 Montana

• 212-220 Maryland 518-519 Idaho

• 221-222 Delaware 520 Wyoming

• 223-231, 691-699 Virginia 521-524, 650-653 Colorado

What does your SSN reveal? • SSN State or Territory SSN State or Territory

• 232-236 West Virginia 525, 585, 648-649 New Mexico

• 232, 237-246, 681-690 North Carolina 526-527, 600-601, 764-765 Arizona

• 247-251, 654-658 South Carolina 528-529, 646-647 Utah

• 252-260, 667-675 Georgia 530, 680 Nevada

• 261-267, 589-595,766-772 Florida 531-539 Washington

• 268-302 Ohio 540-544 Oregon

• 303-317 Indiana 545-573, 602-626 California

• 318-361 Illinois 574 Alaska

• 362-386 Michigan 575-576, 750-751 Hawaii

• 387-399 Wisconsin 577-579 District of Columbia

• 400-407 Kentucky 580 Virgin Islands

• 408-415, 756-763 Tennessee 580-584, 596-599 Puerto Rico

• 416-424 Alabama 586 Guam 425-428, 587-588, 752-755 Mississippi 586 American Samoa

• 429-432, 676-679 Arkansas 586 Philippine Islands

• 433-439, 659-665 Louisiana 700-728 Railroad Board*

• 440-448 Oklahoma 729-733 Enumeration at Entry

“I’m from the government and I am

here to help”

• Fair Debt Collection Practices Act(FDCPA), 15 U.S.C. §§ 1692-1692p.

• Telephone Consumer Protetion Act (TCPA)

47 U.S.C. § 227

• Consumer Protection Bureau (Dodd / Frank Wall Street Reform and Protection Act)

• Fair Credit Reporting Act (FCRA)

Just call me…Joe…

• Collection agencies can call anyone in an attempt to secure the debtors location. However they must:

– Follow FDCPA

– Disclose who they are if asked

– Just confirming location information on debtor

– Never disclose the information to a third party.

Can I call you during dinner? Generally, the agencies can not call you more than once unless

that person agrees to allow additional contact OR

the debt collector believes the response was erroneous or incomplete and that the person now has the correct information.

Don’t contact the consumer / debtor if they are represented by an attorney known to the debt collector. The collector may not make any additional contacts.

Call me anytime…

• If I have your authorization in writing

• If we have done business together

• If there is a legitimate business need

• To process credit transactions

• To discuss any issues with new purchaser or servicer of existing accounts

Questions John G. Schwarm, MBA, DBA.

General Revenue Corporation

Office: (847) 829-4453

Mobile: (630) 338-3459