Embed Size (px)

Citation preview

Vietnam Economic Outlook 2012 - 2013October 2012

Lam Phi Yen

Head of Corporate Sales HCM – Global Markets, Vietnam

+84-8-3520 4113

Agenda

• Vietnam Economic Update

• Reform

• Doing business in Vietnam

• Q & A

Vietnam Economic Update

Macro-economic performance

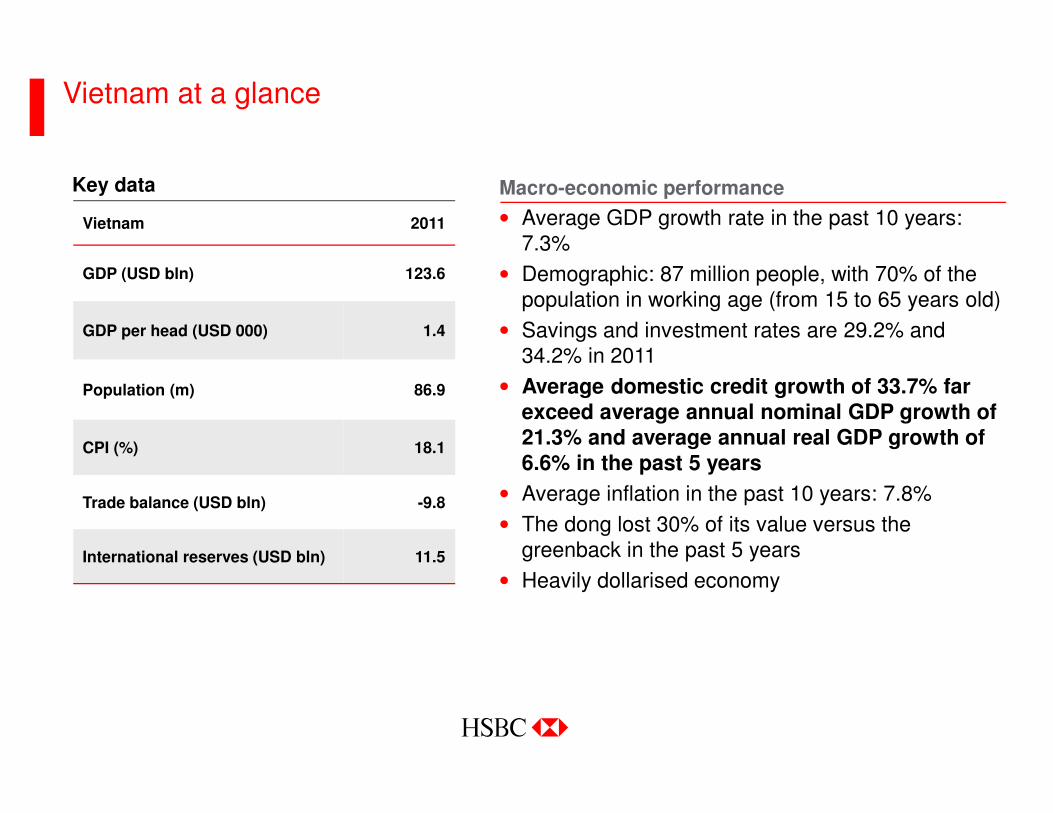

• Average GDP growth rate in the past 10 years: 7.3%

• Demographic: 87 million people, with 70% of the population in working age (from 15 to 65 years old)

• Savings and investment rates are 29.2% and 34.2% in 2011

• Average domestic credit growth of 33.7% far exceed average annual nominal GDP growth of 21.3% and average annual real GDP growth of 6.6% in the past 5 years

• Average inflation in the past 10 years: 7.8%

• The dong lost 30% of its value versus the greenback in the past 5 years

• Heavily dollarised economy

Vietnam 2011

GDP (USD bln) 123.6

GDP per head (USD 000) 1.4

Population (m) 86.9

CPI (%) 18.1

Trade balance (USD bln) -9.8

International reserves (USD bln) 11.5

Key data

Vietnam at a glance

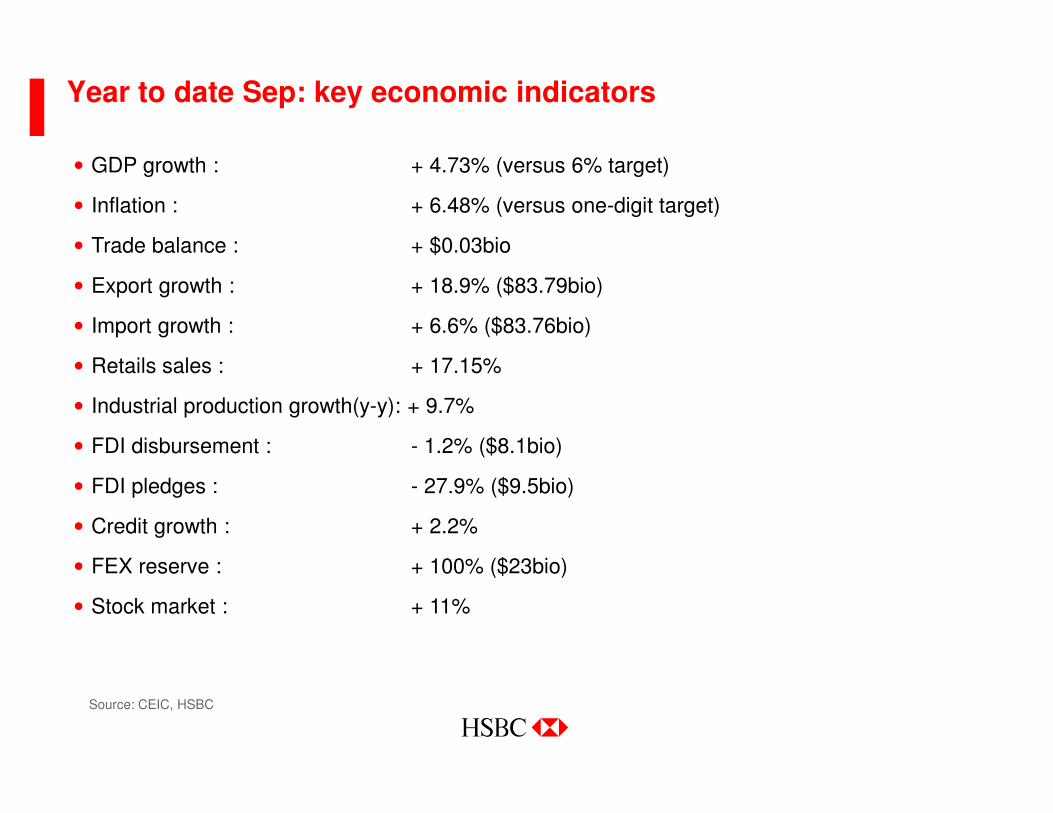

Year to date Sep: key economic indicators

• GDP growth : + 4.73% (versus 6% target)

• Inflation : + 6.48% (versus one-digit target)

• Trade balance : + $0.03bio

• Export growth : + 18.9% ($83.79bio)

• Import growth : + 6.6% ($83.76bio)

• Retails sales : + 17.15%

• Industrial production growth(y-y): + 9.7%

• FDI disbursement : - 1.2% ($8.1bio)

• FDI pledges : - 27.9% ($9.5bio)

• Credit growth : + 2.2%

• FEX reserve : + 100% ($23bio)

• Stock market : + 11%

Source: CEIC, HSBC

What’s Behind Vietnam’s Growth?

• Private consumption makes up about 68% of GDP in Vietnam

• Government consumption usually constitutes around 7% of GDP

• Investment represents about 39% of GDP

• Exports make up around 70% of GDP (in 2010 it was 77.5% of GDP)

• Credit expansion

• Labor force

Source: CEIC, HSBC

Contribution to GDP has changed

15.00

20.00

25.00

30.00

35.00

40.00

45.00

1985 1990 1995 2000 2005 2010 Year

%

Agriculture Industry Service

Industry, 42%

Service, 42%

Agriculture,

16%

7

Average growth rate in working age population (% y-o-y)

-1.00

-0.50

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

AU CH HK IN ID JP SK MY NZ PH SG SL TW TH VN

1990s 2000s 2010s 2020s

Source: UNPD, HSBC

8

The economy is reliant on credit growth

10

15

20

25

30

35

40

45

50

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012f 2013f

5

5.5

6

6.5

7

7.5

8

8.5

9

Credit grow th GDP grow th

Source: CEIC, HSBC

9

Growth is affected by low demand, both internal and external

• Though contracted, the pace of contraction of both new orders and new export orders has been much slower than previous month

• Externally, growth is affected by

Euro zone crisis, sluggish US

recovery process and slowing

China growth. The prospect for

exports in coming months is not

really positive

40

45

50

55

60

Mar-11 Jun-11 Sep-11 Dec-11 Mar-12 Jun-12 Sep-12

New Orders New Ex port Orders

HSBC PMI

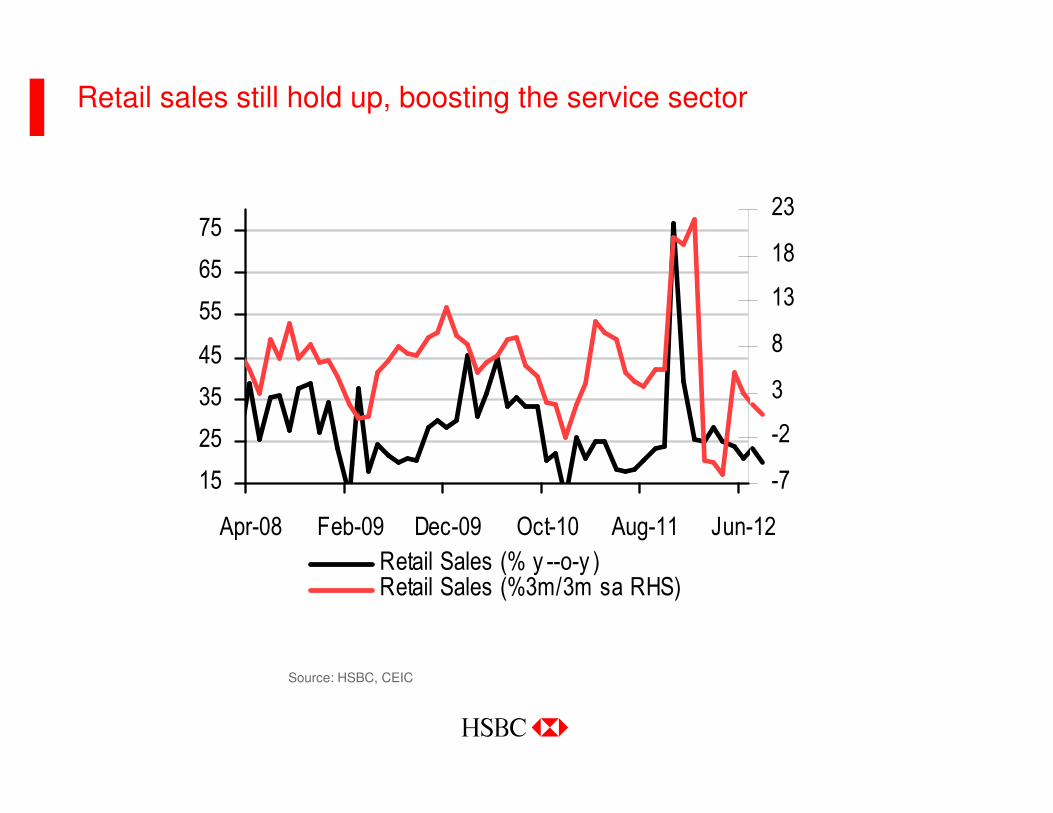

Retail sales still hold up, boosting the service sector

15

25

35

45

55

65

75

Apr-08 Feb-09 Dec-09 Oct-10 Aug-11 Jun-12

-7

-2

3

8

13

18

23

Retail Sales (% y --o-y )Retail Sales (%3m/3m sa RHS)

Source: HSBC, CEIC

Investment by sector

15

25

35

45

55

1995 1997 1999 2001 2003 2005 2007 2009 2011

State Non State Foreign Inv ested Sector

• State makes up 51% of total

investment (average figure of

the last 10 years)

• Contributes about 40% GDP

• Inefficient but requires

continued support to exist

Investment by value

12

Service sector recovers and leads the growth, followed by the industry

13

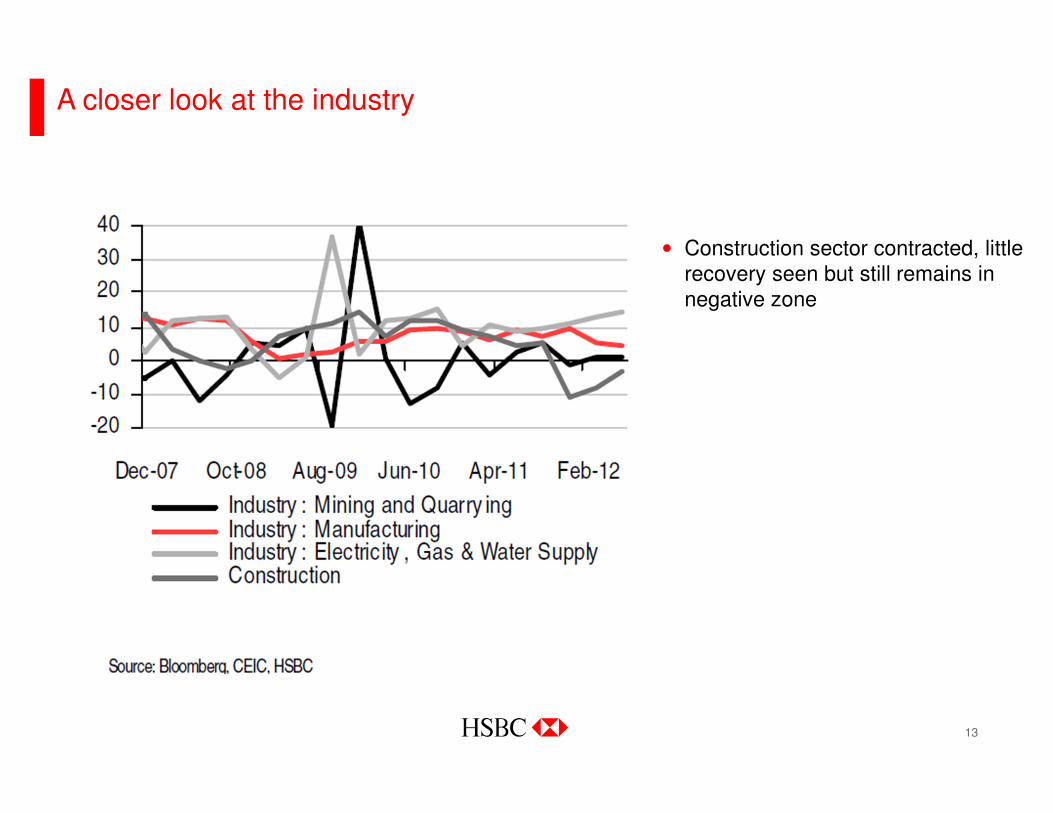

A closer look at the industry

• Construction sector contracted, little recovery seen but still remains in negative zone

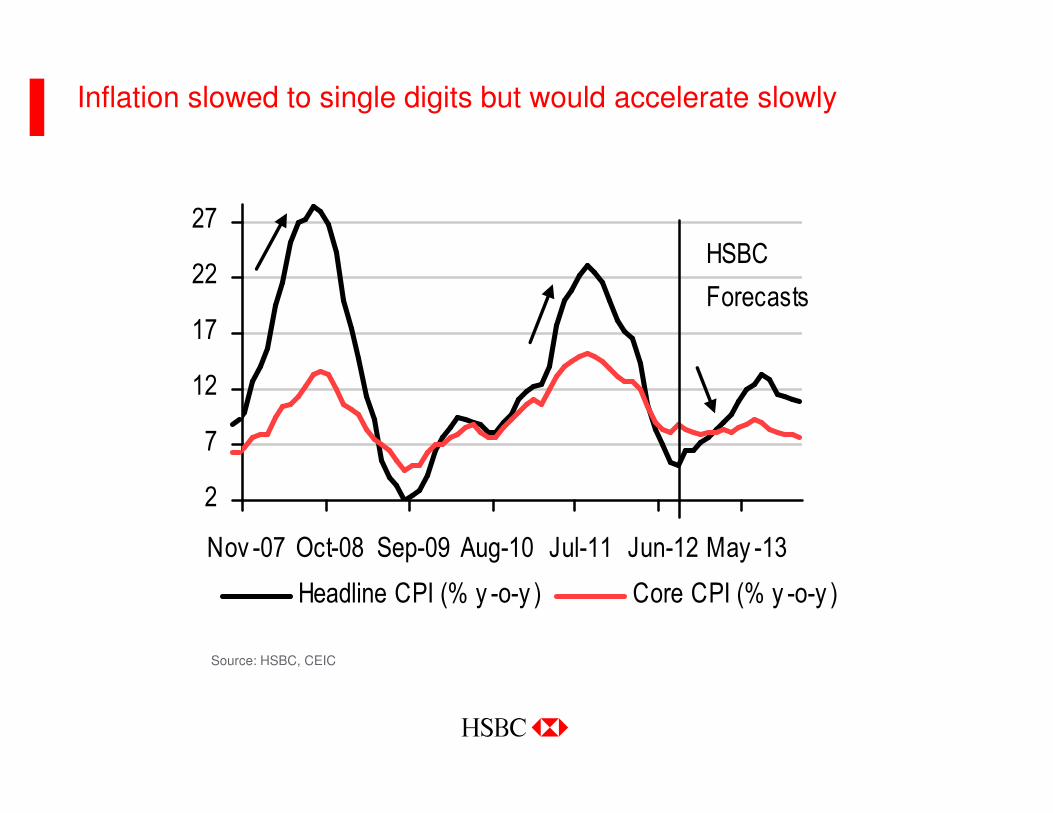

Inflation slowed to single digits but would accelerate slowly

Source: HSBC, CEIC

2

7

12

17

22

27

Nov -07 Oct-08 Sep-09 Aug-10 Jul-11 Jun-12 May -13

Headline CPI (% y -o-y ) Core CPI (% y -o-y )

HSBC

Forecasts

15

But the outlook may be less optimistic

Source: CEIC, HSBC

Input price is rising The trend is turning on inflation

Source: CEIC, HSBC, GSO

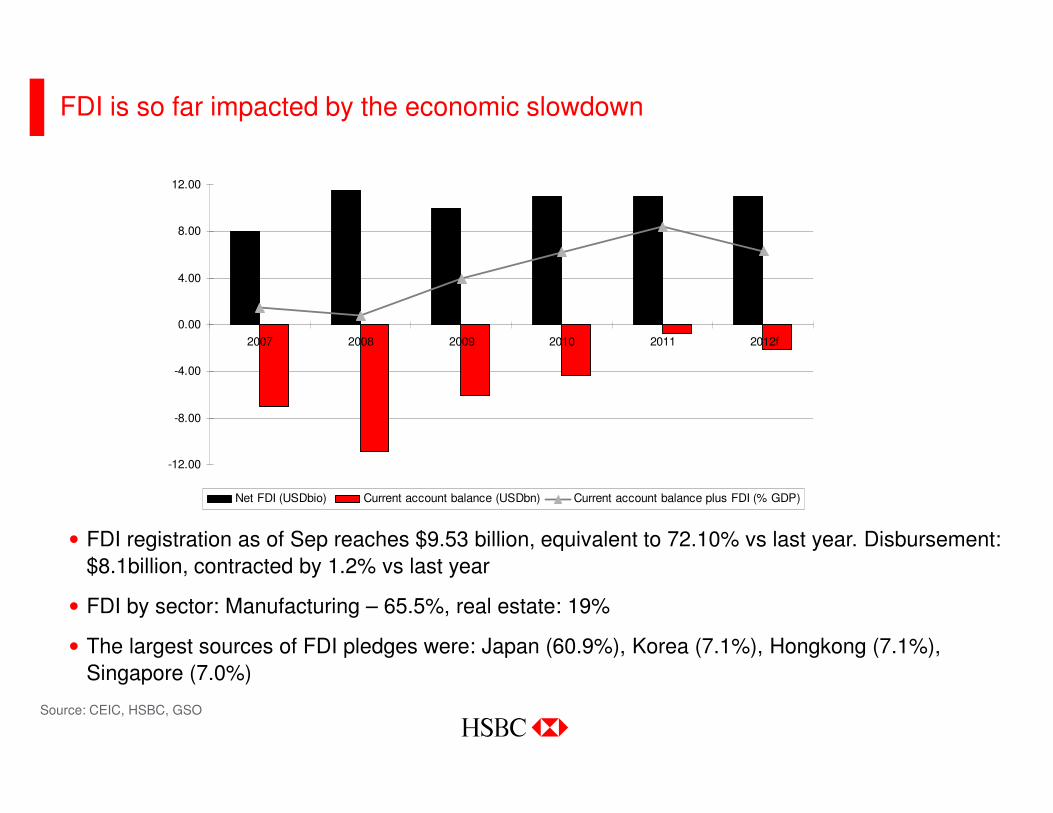

FDI is so far impacted by the economic slowdown

• FDI registration as of Sep reaches $9.53 billion, equivalent to 72.10% vs last year. Disbursement:

$8.1billion, contracted by 1.2% vs last year

• FDI by sector: Manufacturing – 65.5%, real estate: 19%

• The largest sources of FDI pledges were: Japan (60.9%), Korea (7.1%), Hongkong (7.1%),

Singapore (7.0%)

-12.00

-8.00

-4.00

0.00

4.00

8.00

12.00

2007 2008 2009 2010 2011 2012f

Net FDI (USDbio) Current account balance (USDbn) Current account balance plus FDI (% GDP)

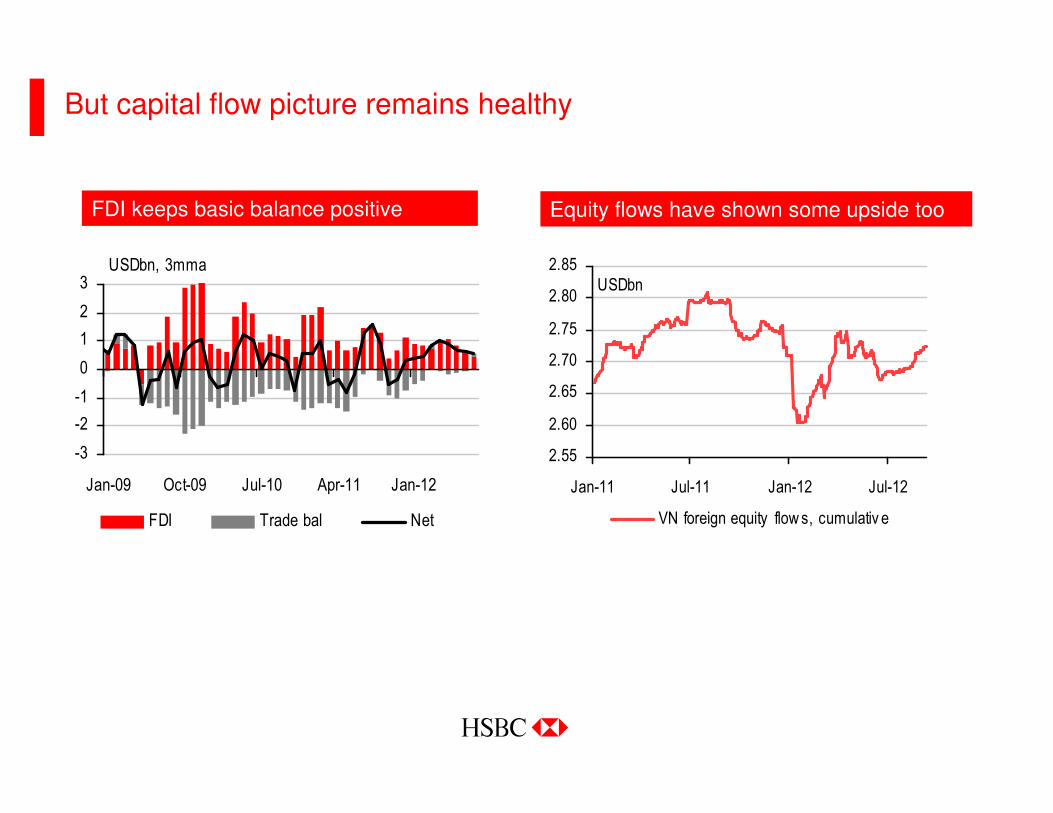

But capital flow picture remains healthy

-3

-2

-1

0

1

2

3

Jan-09 Oct-09 Jul-10 Apr-11 Jan-12

FDI Trade bal Net

USDbn, 3mma

2.55

2.60

2.65

2.70

2.75

2.80

2.85

Jan-11 Jul-11 Jan-12 Jul-12

VN foreign equity flows, cumulativ e

USDbn

FDI keeps basic balance positive Equity flows have shown some upside too

18

Trade deficit turns surplus

Source: CEIC, HSBC

• YTD Sep trade balance is USD 30m

surplus

• Robust export performance

• Import number is steady

Trade deficit

0

2

4

6

8

10

12

14

16

18

20

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

(e)

Year

bio

US

D

Trade deficit (bio USD)

19

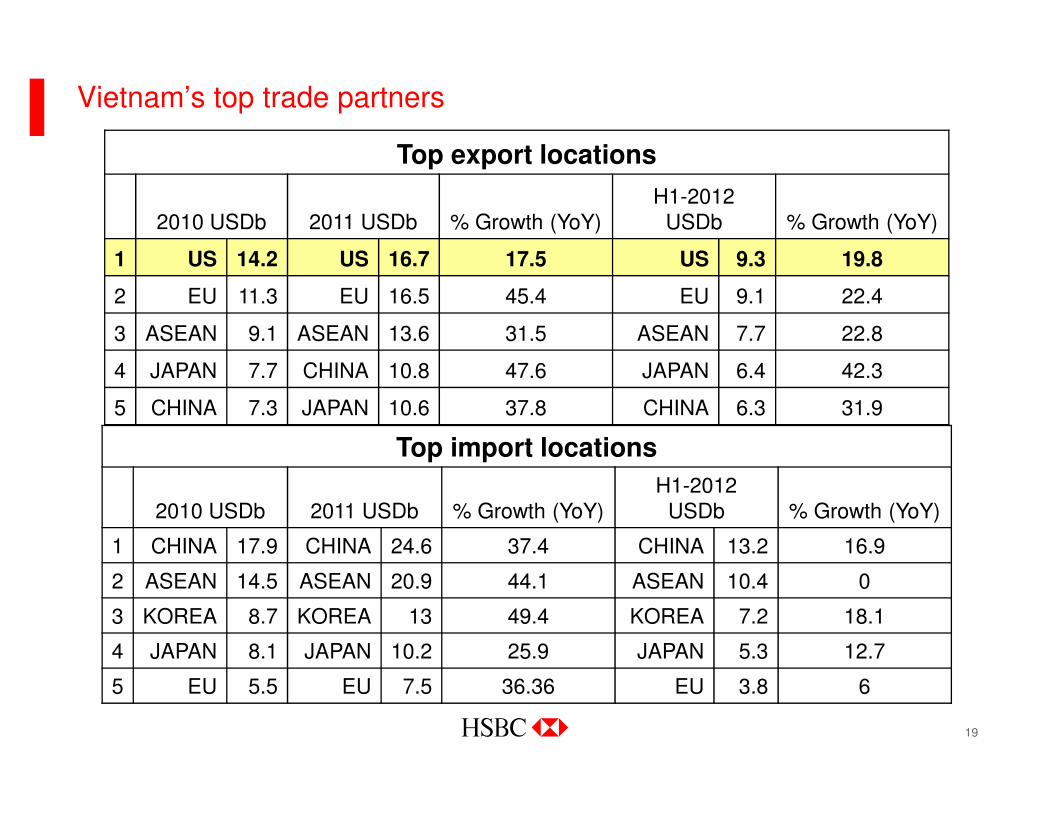

Vietnam’s top trade partners

Top export locations

2010 USDb 2011 USDb % Growth (YoY)H1-2012

USDb % Growth (YoY)

1 US 14.2 US 16.7 17.5 US 9.3 19.8

2 EU 11.3 EU 16.5 45.4 EU 9.1 22.4

3 ASEAN 9.1 ASEAN 13.6 31.5 ASEAN 7.7 22.8

4 JAPAN 7.7 CHINA 10.8 47.6 JAPAN 6.4 42.3

5 CHINA 7.3 JAPAN 10.6 37.8 CHINA 6.3 31.9

Top import locations

2010 USDb 2011 USDb % Growth (YoY)H1-2012

USDb % Growth (YoY)

1 CHINA 17.9 CHINA 24.6 37.4 CHINA 13.2 16.9

2 ASEAN 14.5 ASEAN 20.9 44.1 ASEAN 10.4 0

3 KOREA 8.7 KOREA 13 49.4 KOREA 7.2 18.1

4 JAPAN 8.1 JAPAN 10.2 25.9 JAPAN 5.3 12.7

5 EU 5.5 EU 7.5 36.36 EU 3.8 6

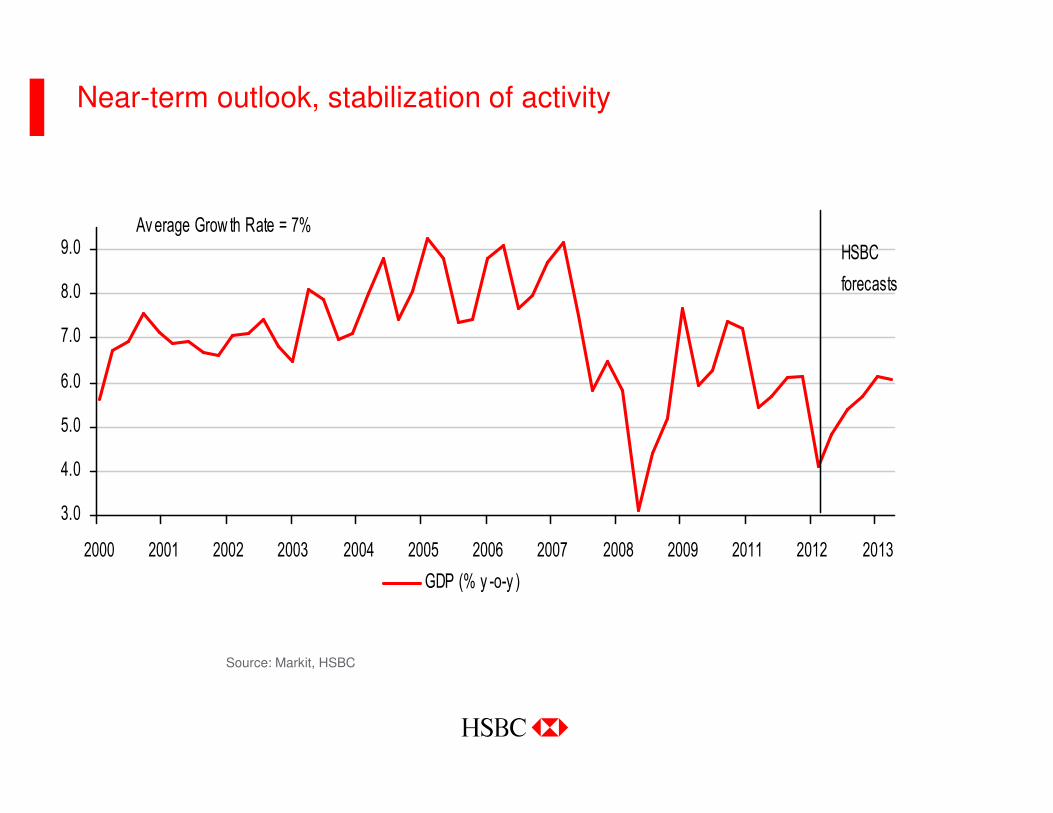

Near-term outlook, stabilization of activity

Source: Markit, HSBC

3.0

4.0

5.0

6.0

7.0

8.0

9.0

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2011 2012 2013

GDP (% y -o-y )

HSBC

forecasts

Average Grow th Rate = 7%

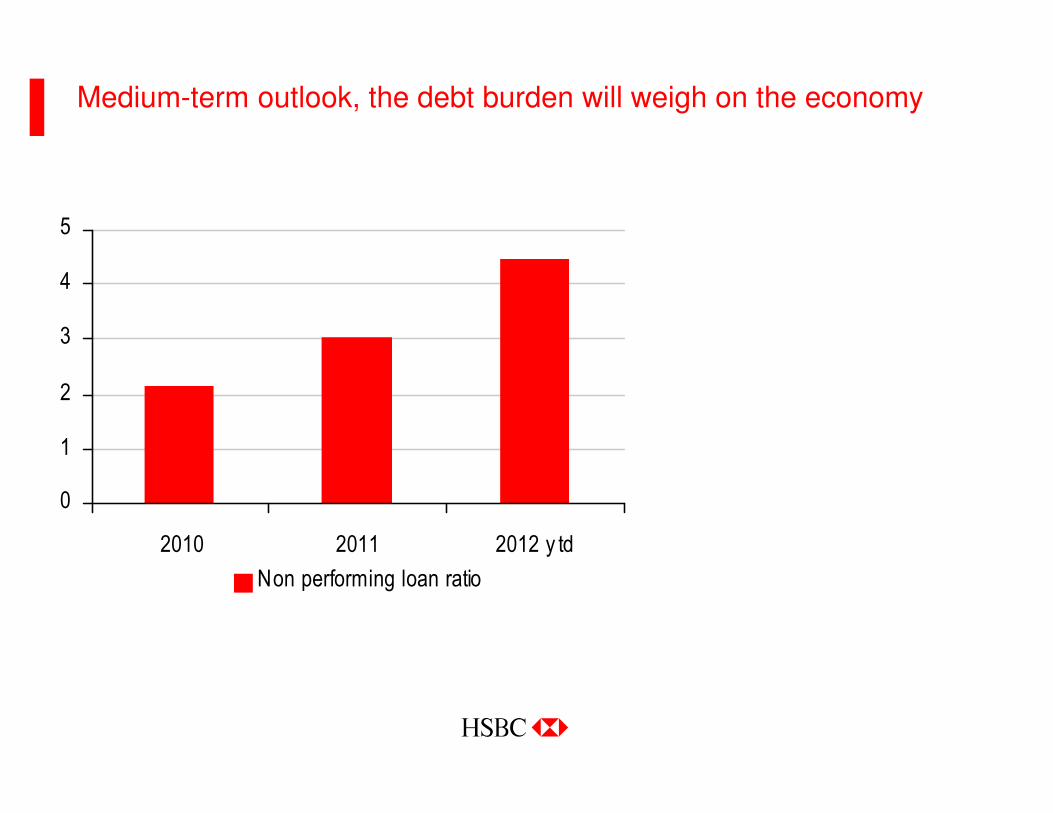

Medium-term outlook, the debt burden will weigh on the economy

0

1

2

3

4

5

2010 2011 2012 y td

Non performing loan ratio

Reform?

• Vietnam has broken the booming period

• Heavily-debted SOEs

• Banking system weakness

• Real estate market is frozen

• Slowing GDP growth with higher inflation has been hurting our workers and farmers

• Last but not least, the whole market is lack of “TRUST”

Hmmmm!!!

Stress…

23

• Banking system and SOE reforms

• “Growth with stability”

• Inflation has been whipped, markets are stable and the currency restores

• Some local banks have been forced to merge; and more to come…

• SOEs are requested to restructure their businesses

• TRUST is being building up slowly; yet a lot of things MUST be done more…

• People are still reluctant to spend

• Companies are still waiting for a clearer picture to expand their business

• Sharply wider budget deficit in the first nine months

What has been going on here…?

24

• Policy discipline is required, and this is a challenge because reform likely needs two phases

• Phase 1: sorting out macro problems…may be the easier part

• Phase 2: solving these problems, especially in banking system and SOEs regime…may be much more difficult

Step by step starting with Phase 1

25

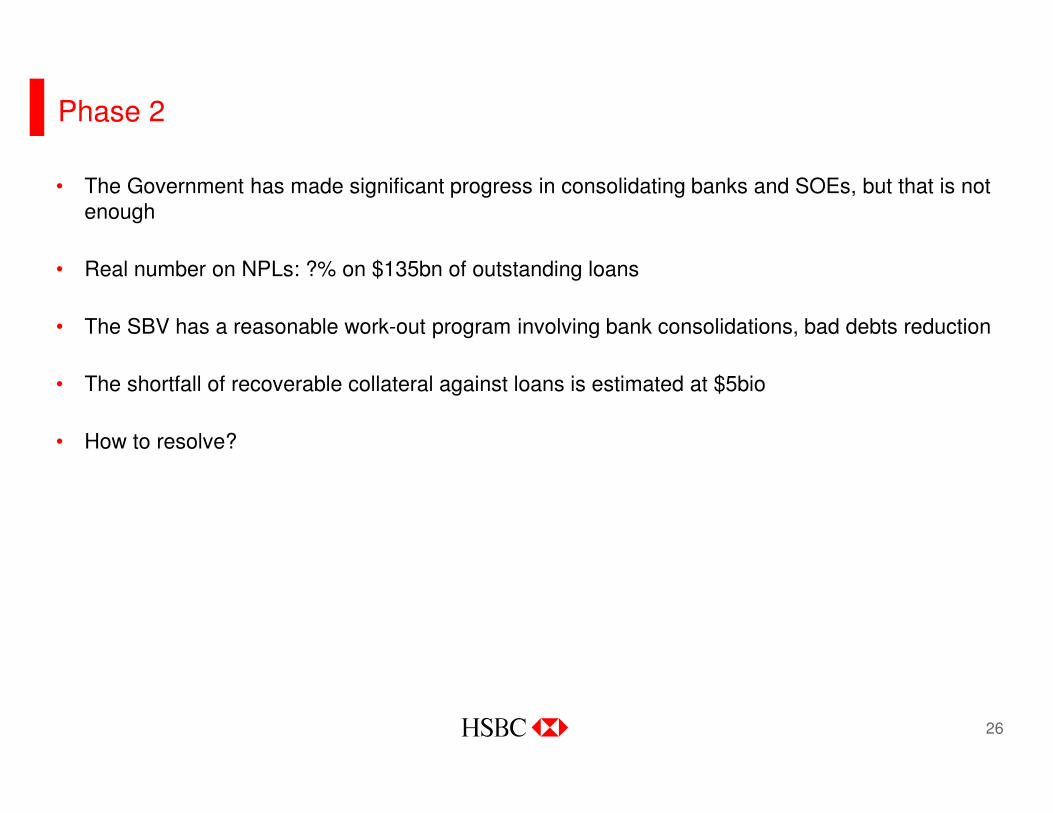

Phase 2

• The Government has made significant progress in consolidating banks and SOEs, but that is not enough

• Real number on NPLs: ?% on $135bn of outstanding loans

• The SBV has a reasonable work-out program involving bank consolidations, bad debts reduction

• The shortfall of recoverable collateral against loans is estimated at $5bio

• How to resolve?

26

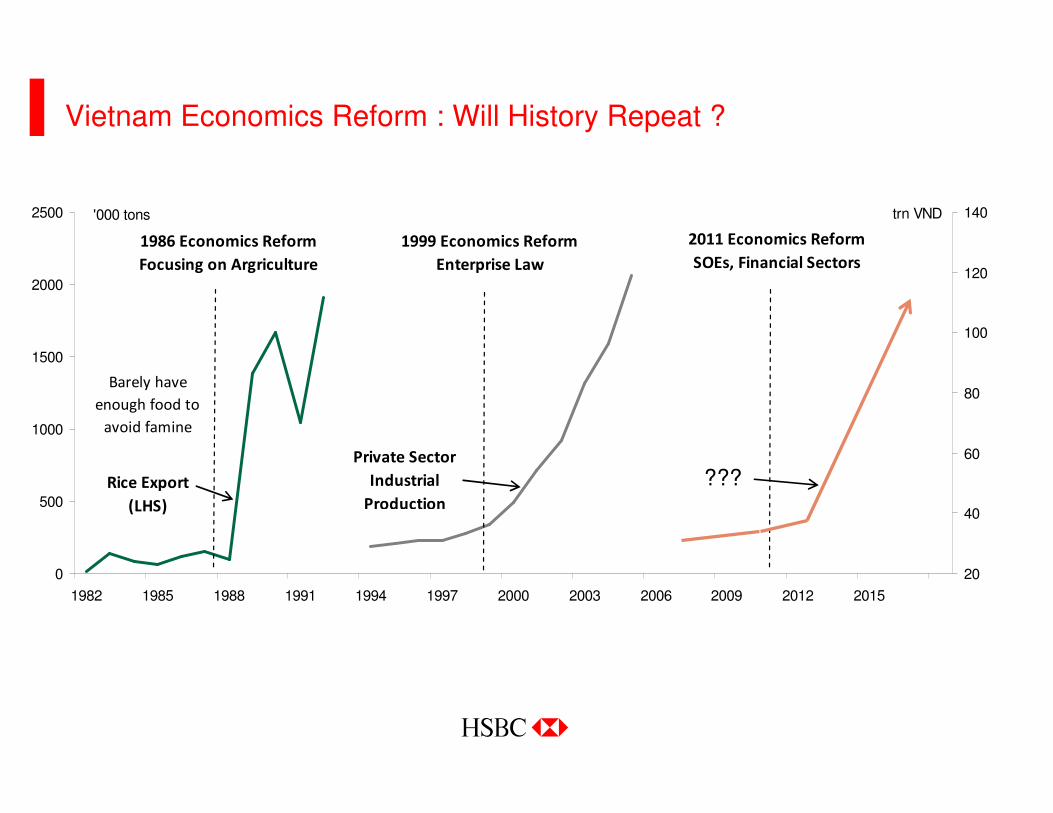

Vietnam Economics Reform : Will History Repeat ?

0

500

1000

1500

2000

2500

1982 1985 1988 1991 1994 1997 2000 2003 2006 2009 2012 2015

'000 tons

20

40

60

80

100

120

140trn VND

1986 Economics Reform

Focusing on Argriculture

1999 Economics Reform

Enterprise Law

2011 Economics Reform

SOEs, Financial Sectors

Barely have

enough food to

avoid famine

Rice Export

(LHS)

Private Sector

Industrial

Production

???

Doing business in Vietnam

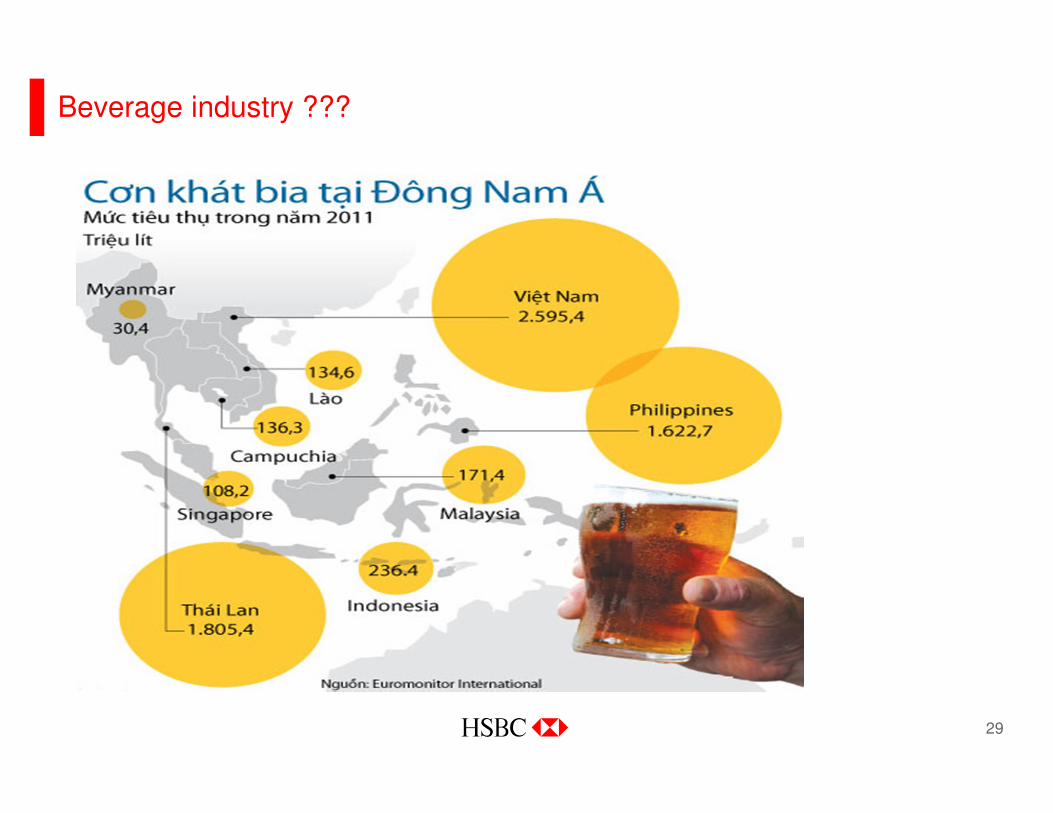

Beverage industry ???

29

• Vietnam ranks the first in consuming beer in ASEAN and the fourth globally

• Vietnam is among top 10 cigarette consumption; around 80 bio cigarettes per annum

• Vietnam ranks No.4 in consuming instant noodle

• Vietnam ranks No.4 in consuming motor bikes in the world

• Vietnamese always love physical GOLD…stay at position No.8 globally

• Vietnamese young generation adore high-tech products

And what will follow these appetites and habits ???

• Retails sales industry

• Healthcare service

• …

Other good businesses…

30

31

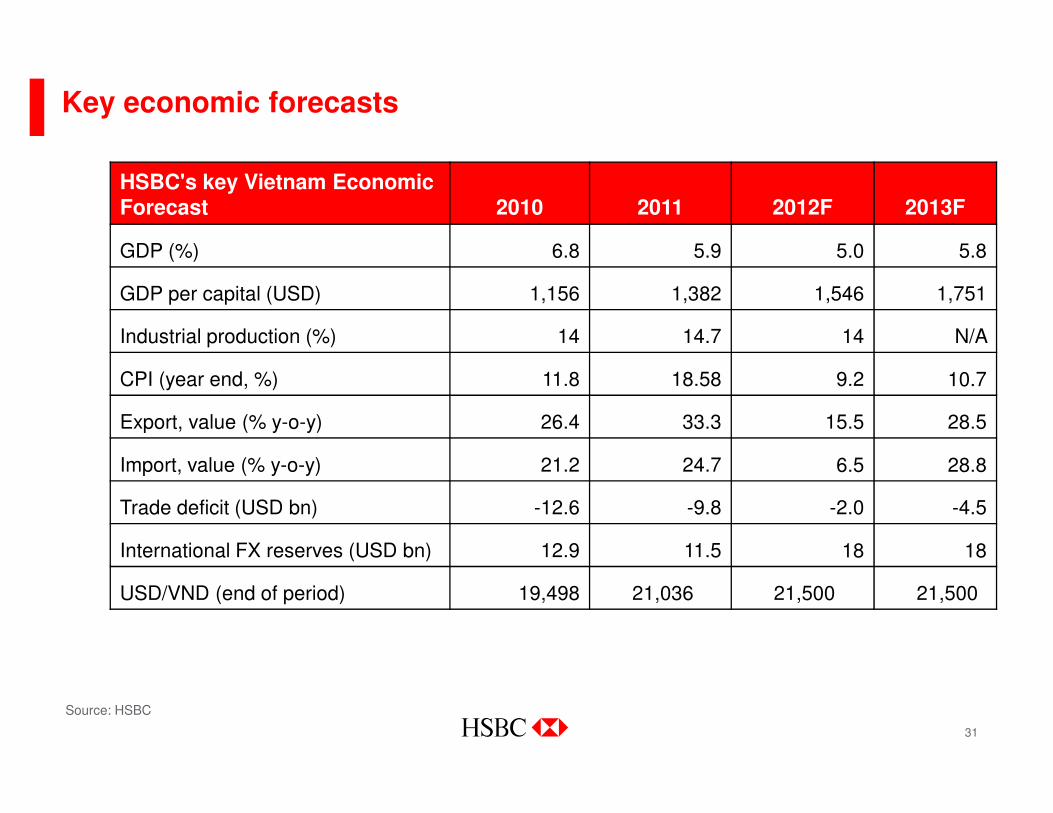

Source: HSBC

HSBC's key Vietnam Economic Forecast 2010 2011 2012F 2013F

GDP (%) 6.8 5.9 5.0 5.8

GDP per capital (USD) 1,156 1,382 1,546 1,751

Industrial production (%) 14 14.7 14 N/A

CPI (year end, %) 11.8 18.58 9.2 10.7

Export, value (% y-o-y) 26.4 33.3 15.5 28.5

Import, value (% y-o-y) 21.2 24.7 6.5 28.8

Trade deficit (USD bn) -12.6 -9.8 -2.0 -4.5

International FX reserves (USD bn) 12.9 11.5 18 18

USD/VND (end of period) 19,498 21,036 21,500 21,500

Key economic forecasts

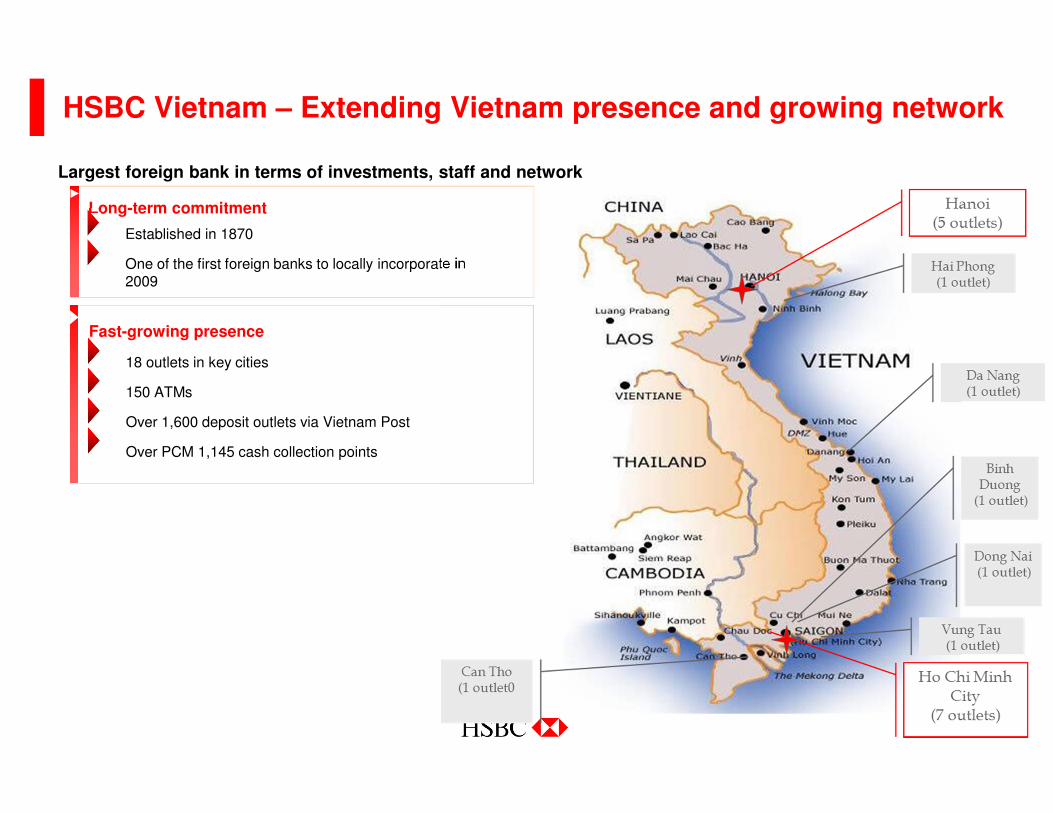

HSBC Vietnam – Extending Vietnam presence and growing network

Fast-growing presence

18 outlets in key cities

150 ATMs

Over 1,600 deposit outlets via Vietnam Post

Over PCM 1,145 cash collection points

Long-term commitment

Established in 1870

One of the first foreign banks to locally incorporate in 2009

Largest foreign bank in terms of investments, staff and network