Embed Size (px)

Citation preview

j

No.

®^

^

In the Supreme Court of Ohio

.13 - 050HSBC BANK USA, NATIONAL ASSOCL4 TION, AS TR USTEE UNDER POOLINGAND SERVICING AGREEMENT DATED AS OF NO VEMBER 1, 2006, FREMONT

HOME LOAN TR UST 2006-D

Plaintiff-AppelleeV.

MICHELLE SCACCHIAND

RICHARD SCACCI, et al.

Defendants-Appellants.♦

On Discretionary Appeal From the---- - Court of Appeals; Ele-vcnth ApPellate-Dis_trct

Geauga County, OhioCase No. 2012-G-3062

♦

MEMORANDUM IN SUPPORT OF JURISDICTION♦

James R. Douglass (0022085)4600 Prospect AvenueCleveland, Ohio 44103Tel: 216 991 7640Fax: 216 373-0536E-Mail: [email protected] for Defendant-AppellantsMichelle and Richard Scacchi

Dean Kanellis (0064069)75 Public Square, 4th FloorCleveland, Ohio 44113Tel: 216 771 6500Fax: 216 771 6540

Counsel for Plaintiff-AppelleesHSBC Bank USA, National Assn. et al.

^^^^ ^^^^^^

CLF,HYt OF COURTSUPREME COURT OF OHI_0

TABLE OF CONTENTS

EXPLANATION OF WHY THE ISSUES RAISED IN THIS CASE ARE OFPUBLIC OR GREAT GENERAL INTEREST . . . . . . . . . . . . . . . . . . . . . . . . . . .

P.age:

STATEMENT OF THE CASE AND FACTS . . . . . . . . . .. . . . . . . . . . . . . . . . . . . . 3

ARGUMENT IN SUPPORT OF PROPOSITIONS OF LAW . . . . . . . . . . . . . . . . 5

Proposition of Law No. 1: Where a promissory note is securedby mortgage, the note, not the mortgage represents the debt. The Mortgageis, therefore, a mere incident, and an assignment of such incident will not,in law, carry with it transfer of the debt; on the other hand a transfer of thenote by the owner so as to vest legal title in the indorsee will carrywith it equitable ownership of the mortgage ............... ............... ............ ......5

Proposition of Law No. 2: Mortgage foreclosure is a two stepProcess and a Plaintiffs right to enforce the Note is a threshold issue that aCourt must decide before considering the equitable claim of foreclosure ... ............7

CONCLUSION . ................................................................................8

CERTIFICATE OF SERVICE . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9

APPENDIX Pam

Opinion of the Eleventh Appellate District dated Feb. 11, 2013 . . . . . . . . . . . . . .......1

Opinion of the Eleventh AppellateDistrict dated Nov. 26, 2012 ...........................6

EXPLANATION OF WHY THE ISSUES RAISED IN THIS ARE OFPUBLIC OR GREAT GENERAL INTEREST

The decision of the Eleventh District in HSBC Bank USA, National Association,

etc. v. Scacchi disturbs the carefully crafted statutory scheme that governs the

enforcement of negotiable instruments in Ohio.

"For nearly a century, Ohio courts have held that whenever a promissory note is

secured by a mortgage, the note constitutes evidence of the debt and the mortgage is a

mere incident to the obligation." Edgar v. Haines (1923) 109 Ohio St. 159, 164. An

assignment of such mortgage did not, in law, carry with it a transfer of the debt; whereas,

on the other hand a transfer of the note by the owner so as to vest legal title in the

indorsee carried with it equitable ownership of the mortgage. Kernohan v. Manss (1895)

53 Ohio St. 118.

The decision in HSBC Bank National Association, etc. v. Scacchi runs afoul of

Ohio's logical and long standing policy that a negotiable instrument must "tell its own

story". National City Bank, Dayton v. The Ohio National Life Assurance Corporation

(Hamilton Co. 1996) 111 Ohio App. 3d 387 ¶ 3, and directly contradicts the

unambiguous language of R.C. 1303.31 governing who may enforce a negotiable

instrument in Ohio. The Eleventh District has created the anomaly that two separate and

distinct persons may enforce a negotiable instrument in Ohio. The party entitled to

enforce defined by the Legislature in R.C. 1303.31, and the party who took assignment of

the mortgage. This outcome places Ohio homeowners at risk of multiple and inconsistent

claims on the same obligation. Leaving the law as defined by the Eleventh District in

1

I

Scacchi creates a paradigm of risk, confusion and uncertainty for any obligor on a

negotiable instrument in Ohio.

The instant case is also of special importance because of the nature of the

purported "assignor" of the mortgage to Plaintiff. The Assignment of Mortgage was

executed by Mortgage Electronic Registrations Systems, Inc. (MERS), as Nominee for

Fremont Investment and Loan. MERS was never party to, nor a holder of, the note.

Accordingly, if permitted to stand, this case will stand for the proposition that a non-party

to a negotiable instrument is vested with the authority to transfer the authority to enforce

the instrument by assignment of the mortgage. The result is that for any given loan, there

could be two persons seeking enforcement of the same negotiable instrument; the party

entitled to enforce the instrument under RC 1303.31 and the party who took assignment

of the mortgage. A result that is in direct conflict with both the statutory scheme

governing enforcement of negotiable instruments and established case law dating back to

the Civil War.

The Eleventh District's apparent confusion, is also evident from its decisions in

Federal Home Loan Mortgage v. Rufo 11th Dist. No. 2012-A-0011, 2012 Ohio 5930,

2012 Ohio App LEXIS 5118 and BAC Home Loans Servicing, etc. v. Meister l lth Dist.

No. 2012-L-042, 2013 Ohio 873, 2013 Ohio App LEXIS 765, that latter case purportedly

overruling the instant case "to the extent it is inconsistent with Schawrtzwald on the issue

of standing" Id ¶9. This apparent confusion appears to be shared by the Eighth District in

its decision in CitiMortgaQe v. Patterson 8th Dist. No. 98360, 2012 Ohio 5894, 2012 Ohio

App. LEXIS 5084, Memorandum in Support of Jurisdiction pending Ohio Sup Court

Case No. 2013-0128.

2

In our view, Schwartzwald extends the limitations of our holding in

Jordan and stands for the proposition that a party may establish its interestin the suit, and therefore have standing to invoke the jurisdiction of theCourt when, at the time it files its complaint of foreclosure, it either (1)has had a mortgage assigned or (2) is the holder of the note.

Id at ¶21 (emphasis supplied)

These decisions by both the Eleventh and Eighth Districts evidence an apparent

lack of understanding that foreclosure is a two (2) step process requiring judgment be had

on the note before execution through the equitable remedy of foreclosure. First Knox

National Bank v. v. Peterson 5ffi Dist. No. 08CA28, 2009 Ohio 5096, ¶18; National City

Bank v. Skipper 9th Dist No. C.A. 24772, 2009 Ohio 5940.

The apparent confusion, amongst Courts of Appeals, that has led to the disregard

of established case law dating back to the Civil War, is apparently occasioned by

language found in dicta in Federal Home Loan Corporation v. Schwartzwald (2012) 134

Ohio St. 3d. 13, 2012 Ohio 5017 that the holder of either the note or the mortgage may

enforce the note regardless of whether the mortgagee by way of assignment is entitled to

enforce the note. Inasmuch as the subject dicta followed a thorough review of law from

jurisdictions outside Ohio standing for the proposition that negotiation of the note to the

plaintiff prior to filing of the suit was a jurisdictional prerequisite to vest the court with

subject matter jurisdiction, such dicta cannot be confused with the holding of this court.

STATEMENT OF THE CASE AND FACTS

On or about September 7, 2006, Defendants-Appellants Michelle and Richard

Scacchi executed an adjustable rate note in the amount of $179,100.00 payable to

Fremont Investment & Loan. The promissory note based upon which Plaintiff sought

judgment was attached to the Complaint of Plaintiff as Exhibit A. As appears from the

four corners of the note, it is and remains payable to Fremont Investment & Loan and not

3

A :a

to Plaintiff HSBC Bank USA National Association. The Note bears no endorsement to

HSSBC Bank or to blank. The loan was secured by a mortgage in favor of MERS, as

nominee for Fremont Investment and Loan.

On August 6, 2010, Plaintiff HSBC Bank USA National Association, as Trustee

under the Pooling and Servicing Agreement dated as of November 1, 2006, Fremont

Home Loan Trust 2006-D filed a Complaint for Money, Foreclosure and Other Equitable

Relief against Defendants-Appellants Michelle and Richard Scacchi, The United States

of America and the Treasurer of Geauga County. Attached to Plaintiff's Complaint was a

note payable to Fremont Investment and Loan, a Home Affordable Modification

Agreement entered into by and between Michelle Scacchi and Richard Scacchi as buyers

and Litton Loans Servicing as the servicer. (T.d. 2). The note attached to Plaintiff's

Complaint is not endorsed and remains payable to Fremont Investment & Loan and not

Plaintiff HSBC Bank USA National Association. Therefore the Plaintiff in this case, just

as was the case with the Plaintiff in Schwartzwald, lacked the legal authority to enforce

the note pursuant to RC 1303.31. However, the Eleventh District found that HSBC Bank

USA National Association could enforce the note as the record indicated that the

mortgage was assigned to HSBC Bank by MERS prior to the filing of suit. The court

further found that "[t]he assignment of the mortgage, though not containing an express

transfer of the note, was sufficient to transfer, both the mortgage and the note." Denial of

Application for Reconsideration. P. 4.

On November 7, 2011, Defendants-Appellants Michelle and Richard Scacchi

filed a Motion for Relief from Judgment (T.d. 44) and on February 8, 2012, the Motion

for Relief from Judgment was denied (T.d. 46) despite the fact that the Plaintiff did not

4

oppose the Motion. On March 9, 2012, a timely Appeal was taken by Defendants-

Appellants Michelle and Richard Scacchi (T.d. 50). On November 26, 2012 the Court of

Appeals journalized a Judgment Entry affirming the decision of the trial court. In its

decision, this court relied upon it own decisional authority that standing is not a

jurisdictional prerequisite and that a lack of standing may be cured by substituting the

real party in interest for an original party pursuant to Civ.R. 17(A). The reliance upon its

own decisional authority was notwithstanding the decision of the Ohio Supreme Court in

Federal Home Loan Mortgage v. Schwartzwald Id that specifically rejected that view and

held that: "The lack of standing at the commencement of a foreclosure action requires

dismissal of the complaint; however that dismissal is not adjudication on the merits and is

therefore without prejudice." Id. at ¶ 40 The Appellants filed an Application for

Reconsideration that was denied.

ARGUMENT IN SUPPORT OF PROPOSITION OF LAW

Proposition of Law No. I:

Where a promissory note is secured by mortgage, the note, not the mortgagerepresents the debt. The mortgage is, therefore, a mere incident, and an assignmentof such incident will not, in law, carry with it a transfer of the debt; on the otherhand a transfer of the note by the owner so as to vest legal title in the indorsee will

carry with it equitable ownership of the mortgage.

The foregoing proposition of law is taken verbatim from the decision of this Court

in Kernohan v. Manss (1895) 53 Ohio St. 118; 1895 LEXIS 129 and remains as true and

well reasoned today as it was in 1895.

The law and policy relative to negotiable instruments remains unchanged and

remains simple and straight forward. That policy requires that the note tell its own story.

11 Am Jur 2d (1963) 83, Bills and Notes, Section 57.

5

Parol or other extrinsic evidence is not admissible to add a party to the instrument

who does not appear upon its face. Whoever takes negotiable paper enters into a contract

with the parties who appear on the face of the instrument, and can look to no other

persons for payment. National City Bank, Dayton v The Ohio National Life Assurance

Corporation (Hamilton Co. 1996) 111 Ohio App 3d 387; 676 NE2d 536; 1996 Ohio App

LEXIS 2205; 32 UCC Rep. Serv. 2d (Callaghan) 871.

The UCC was created to simplify, clarify, and modernize the law governing

commercial transactions and to permit continued expansion of commercial practice

through custom, usage, and agreement of the parties. The payee on a note must be able to

determine the identity of the payor without reference to extrinsic evidence. Otherwise the

payee could well be required to pay the same obligation on multiple occasions.

"Parol evidence is not admissible to add a party to the instrument whodoes not appear upon its face. * * * Whoever takes negotiable paper entersinto a contract with the parties who appear on the face of the instrument,and can look to no other persons for payment." Bank v. Cook (1882), 38

Ohio St. 442. If one could not depend on the face of the negotiableinstrument to determine its nature and effect, those dealing in commercialmatters would have "to refer to extrinsic matters to understand andappreciate 'the unique legal liabilities associated with [the] instrument []and conduct their affairs accordingly[,]"' in violation of the purpose of theUniform Commercial Code. Aetna Casualty & Sur. Co. v. Fennessey

(1994) 37 Mass. App . Ct. 668 642 N.E.2d 1050, 1052, review denied(1995), 419 Mass. 1102, 646 N.E.2d 409, quoting White & Summers,Uniform Commercial Code (1988) 623, Section 13-1

National City Bank id.

The purpose behind the rule that parol or other extrinsic evidence is not admissible to add

a party to an instrument that does not appear on its face is simple and straightforward. If

the rule were otherwise, a defendant would be unable to defend himself or herself from a

suit brought by the party entitled to enforce the note as defined in RC 1303.31.

6

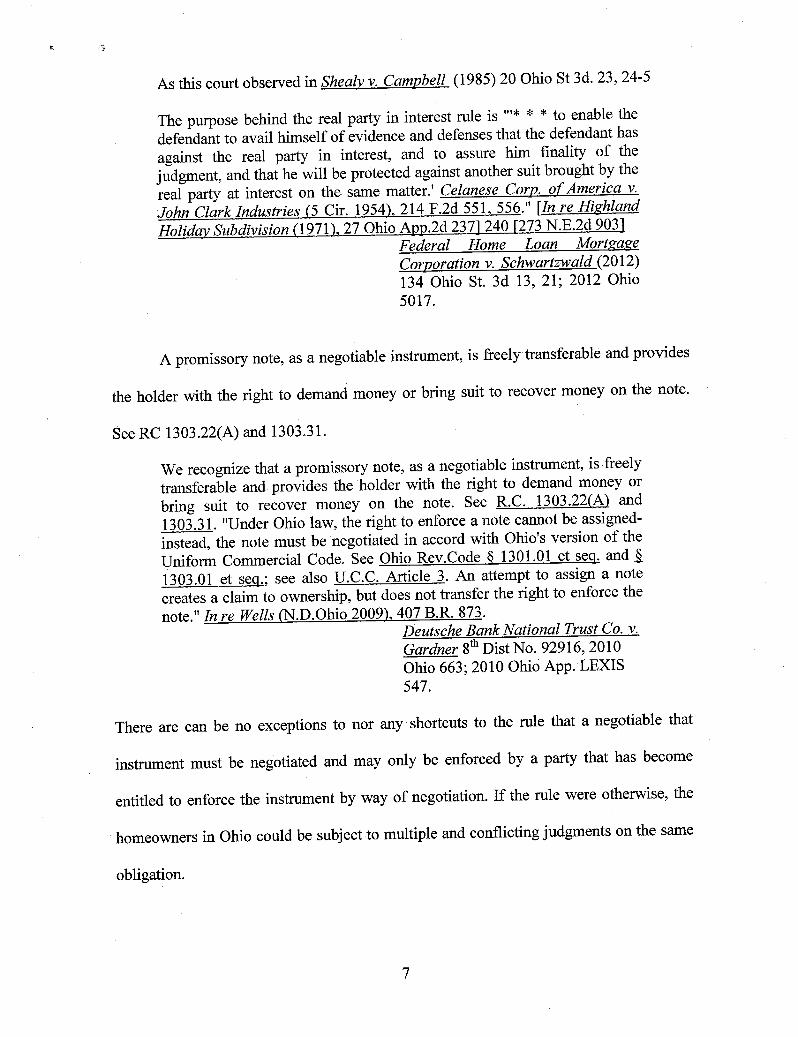

As this court observed in Shealy v. Campbell (1985) 20 Ohio St 3d. 23, 24-5

The purpose behind the real party in interest rule is "'* * * to enable thedefendant to avail himself of evidence and defenses that the defendant hasagainst the real party in interest, and to assure him finality of thejudgment, and that he will be protected against another suit brought by thereal party at interest on the same matter.' Celanese CoLp. of America v.

John Clark Industries (5 Cir. 1954) 214 F.2d 551 556." [In re Hi h^ land

Holiday Subdivision(1971) 27 Ohio App 2d 2371240 f273 N.E.2d 9031Federal Home Loan MortgaZeCorporation v. Schwartzwald (2012)134 Ohio St. 3d 13, 21; 2012 Ohio5017.

A promissory note, as a negotiable instrument, is freely transferable and provides

the holder with the right to demand money or bring suit to recover money on the note.

See RC 1303.22(A) and 1303.31.

We recognize that a promissory note, as a negotiable instrument, is freelytransferable and provides the holder with the right to demand money orbring suit to recover money on the note. See R.C. 1303.22(A) and1303.31. "Under Ohio law, the right to enforce a note cannot be assigned-instead, the note must be negotiated in accord with Ohio's version of theUniform Commercial Code. See Ohio Rev.Code $ 1301.01 et seg. and ^1303.01 et seg.; see also U.C.C. Article 3. An attempt to assign a notecreates a claim to ownership, but does not transfer the right to enforce the

note." In re Wells (N D Ohio 2009) 407 B.R. 873.Deutsche Bank National Trust Co. v.Gardner 8h Dist No. 92916, 2010Ohio 663; 2010 Ohio App. LEXIS547.

There are can be no exceptions to nor any shortcuts to the rule that a negotiable that

instrument must be negotiated and may only be enforced by a party that has become

entitled to enforce the instrument by way of negotiation. If the rule were otherwise, the

homeowners in Ohio could be subject to multiple and conflicting judgments on the same

obligation.

7

Proposition of Law No. II:

Mortgage foreclosure is a two step process and a Plaintiff's right to enforce

the Note is a threshold issue that a Court must decide before considering the

equitable claim of foreclosure.

"The note and mortgage are inseparable; the former as essential, the latter as an

incident. An assignment of the note carries the mortgage with it, while an assignment of

the latter alone is a nullity." Carpenter v. Longan, (1873) 83 U.S. 271, 274, 21 L.Ed. 313.

"Being but an incident of the debt, the mortgage remains, until foreclosure or possession

taken, in the nature of a chose in action. Where given to secure notes, it has no

determinate value apart from the notes, and, as distinct from them, is not a fit subject of

assignment." Kernohan v. Manss, Id.. In other words, a person may not bring suit on a

mortgage alone. Enforcement of the mortgage may only be had once entitlement to relief

on the note it secures has been established.

Foreclosure is a two step process. First Knox National Bank v. Peterson, Id. Only

after the Court determines liability on the underlying obligation can it move to the

foreclosure of the mortgage. Id. See also, National City Bank v. Skipper, Id. This is

because the mortgage is but an incident to the debt. Kernohan v. Manss, Id. It does not

have a life of its own, and until foreclosed, it remains but a chose in action. Id. at p. 133.

Therefore, Plaintiffs entitlement to enforce the Note is a threshold issue that the Court

must decide before considering the foreclosure claim.

CONCLUSION

VV-HEIZEFOIZE, Appellants, Richard and Michelle Scacchi, respectfully requests

and moves the Supreme Court of Ohio to accept jurisdiction over this appeal because the

issues presented in this case are of public or great general interest.

8

4EESSS

Respectf ully submitted,

R. DOU ASS220 85)AR. DO GLAS O. LPA

4600 Prospect Ave.Cleveland, Ohio 44103(216) 991-7640 Office(216) 373-0536 Facsimilefire dco achgaol. com

CERTIFICATE OF SERVICE

A copy of the foregoing has been served by ordinary U. S. Mail on this^ day

of March, 2013 upon the following:

Dean Kanellis75 Public Square4"` FloorCleveland, Ohio 44113

Marlon Primes400 US Courthouse801 W. Superior AvenueCleveland, Ohio 44113Attorney for United States

Bridey MatheneyAssistant Prosecuting Atty.231 Main Street, Suite 3AChardon, Ohio 44024Attorney for Treasurer

9

HLED^^^ COLEFc`r OF APMALS

FEB 112013STATE OF OHIO DENISE M)^P ;NsKc

CLERK Of^BRTSCOUNTY OF GEAUGX-3EAUGAPouNn'

HSBC BANK USA, NATIONALASSOCIATION, AS TRUSTEE UNDERPOOLING AND SERVICINGAGREEMENT DATED AS OFNOVEMBER 1, 2006, FREMONT HOMELOAN TRUST 2006-D,

Plaintiff-Appellee,

- vs -

MICHELLE SCACCHI, et al.,

Defendants-Appellants,

THE UNITED STATES OF AMERICA,et al.,

Defendants-Appellees.

IN THE COURT OF APPEALS

ELEVENTH DISTRICT

JUDGMENT ENTRY

CASE NO. 2012-G-3062

This cause. comes before this court upon consideration of appellants'

application for reconsideration and motion for en banc consideration;

On December 4, 2012, appellants, Michelle and Richard Scacchi, filed a

motion requesting this court reconsider our decision in HSBC Bank v. Scacchi,

11th Dist. No. 2012-G-3062, 2012-Ohio-5441, pursuant to App.R 26(A).

Appellee, HSBC Bank USA ("HSBC"), successfully sought leave to file a delayed

response and filed its answer in opposition on December 21, 2012.

As the basis for their application, appellants highlight the recent Ohio

Supreme Court case Fed. Home Loan Mtge. Corp. v. Schwartzwald, 134 Ohio

St.3d 13, 2012-Ohio-5017

;/// ^^f 7/

App.R. 26 does not provide specific guidelines to be used by an appellate

11 court when determining whether a prior decision should be reconsidered or

modified. State v. Black, 78 Ohio App.3d 130, 132 (1991). However, the

standard that has been generally accepted for addressing an App.R. 26(A)

motion was stated in Matthews v. Matthews, 5 Ohio App.3d 140 (1981). In

Matthews, the court observed: "The test generally applied *** is whether the

motion calls to the attention of the court an obvious error in its decision or raises

an issue for consideration that was either not considered at all or was not fully

considered by the court when it should have been." Id. at paragraph two of the

syllabus. An application for reconsideration is not designed to be used in

situations wherein a party simply disagrees with the logic employed or the

conclusions reached by an appellate court. State v. Owens, 112 Ohio App.3d

334, 336 (1997). App.R. 26(A) is meant to provide a mechanism by which a

party may prevent a miscarriage of justice that could arise when an appellate

court makes an obvious error or renders a decision that is not supported by the

law. Id.

The issue of standing in the context of a mortgage foreclosure action has

developed significantly since this appeal was heard. Previously, the Ohio

Supreme Court, in, State ex re1. Jones v. Suster, 84 Ohio St.3d 70 (1998),

indicated that standing is not jurisdictional, explaining that, pursuant to Civ.R. 17,

"lack of standing may be cured by substituting the proper party so that a court

otherwise having subject matter jurisdiction may proceed to adjudicate the

matter." Id. at 77. Relying on this proposition, this court held standing to not be

2

i^//o a'^ 2

C. Y .

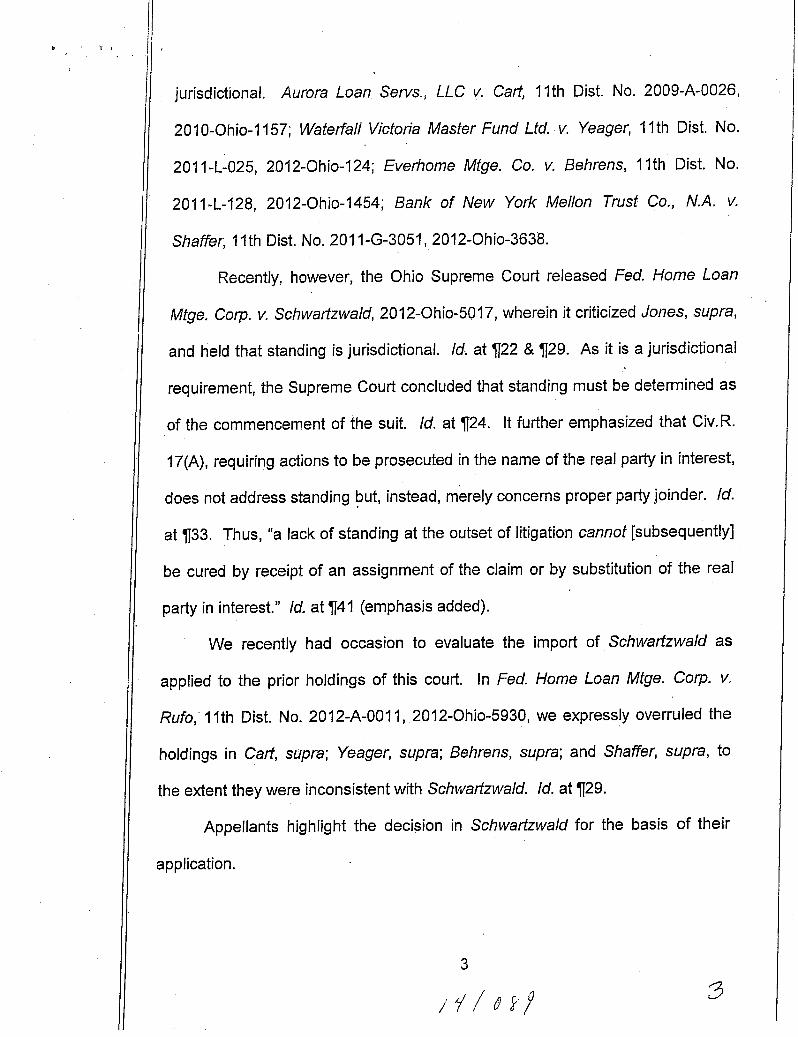

jurisdictional. Aurora Loan Servs., LLC v. Cart, 11th Dist. No. 2009-A-0026,

2010-Ohio-1157; Waterfall Victoria Master Fund Ltd. v. Yeager, 11th Dist. No:

2011-L-025, 2012-Ohio-124; Everhome Mtge. Co. v. Behrens, 11th Dist. No.

2011-L-128, 2012-Ohio-1454; Bank of New York Mellon Trust Co., N.A. v.

Shaffer, 11th Dist. No. 201 1-G-3051, 2012-Ohio-3638.

Recently, however, the Ohio Supreme Court released Fed. Home Loan

Mtge. Corp. v. Schwartzwald, 2012-Ohio-5017, wherein it criticized Jones, supra,

and held that standing is jurisdictional. Id. at ¶22 &¶29. As it is a jurisdictional

requirement, the Supreme Court concluded that standing must be determined as

of the commencement of the suit. Id. at V24. It further emphasized that Civ.R.

17(A), requiring actions to be prosecuted in the name of the real party in interest,

does not address standing but, instead, merely concerns proper party joinder. Id.

at ¶33. Thus, "a lack of standing at the outset of litigation cannot [subsequently]

be cured by receipt of an assignment of the claim or by substitution of the real

party in interest." Id. at ¶41 (emphasis added).

We recently had occasion to evaluate the import of Schwartzwald as

applied to the prior holdings of this court. In Fed. Home Loan Mtge. Corp. v.

Rufo,' 11th Dist. No. 2012-A-0011, 2012-Ohio-5930, we expressly overruled the

holdings in Cart, supra; Yeager, supra; Behrens, supra; and Shaffer, supra, to

the extent they were inconsistent with Schwartzwald. Id. at ¶29.

Appellants highlight the decision in Schwartzwald for the basis of their

application.

3

iy/o^1^ 3

Appellants' application is meritorious to the extent that our decision is,

inconsistent with Schwartzwald on the issue of standing. Upon review, however,

Schwartzwald does not directly influence the holding in this case. In accord with

our decision in Rufo, ¶30, HSBC was "required to have an interest in the note or

mortgage when it filed this action in order to have standing to invoke the

jurisdiction of the trial court." The record indicates the mortgage was assigned

prior to the initiation of the action, a copy of which was attached to the complaint.

The assignment of the mortgage, though not containing an express transfer of

the note, was sufficient to transfer both the mortgage and the note. Rufo, ¶44.

The notarized assignment instrument attached to the complaint states that

Mortgage Electronic Registration Systems, Inc., as nominee for Fremont

Investment and Loan, transferred the mortgage of the subject parcel to HSBC.

The promissory note listing Fremont Investment and Loan as the lender Was also

attached to the complaint. Appellants' application for reconsideration must

therefore be overruled.

We now turn to appellants' request for en banc consideration, filed with

this court on December 19, 2012. App.R. 26(A)(2)(b) provides, in part: "An

application for en banc consideration must explain how the panel's decision

conflicts with a prior panel's decision on a dispositive issue and why

consideration by the court en banc is necessary to secure and maintain

uniformity of the court's decisions."

Appellants cite the conflicting decision requiring en banc consideration as

Rufo, supra. This court's decision in Rufo was released after the present case

4

I //o9G

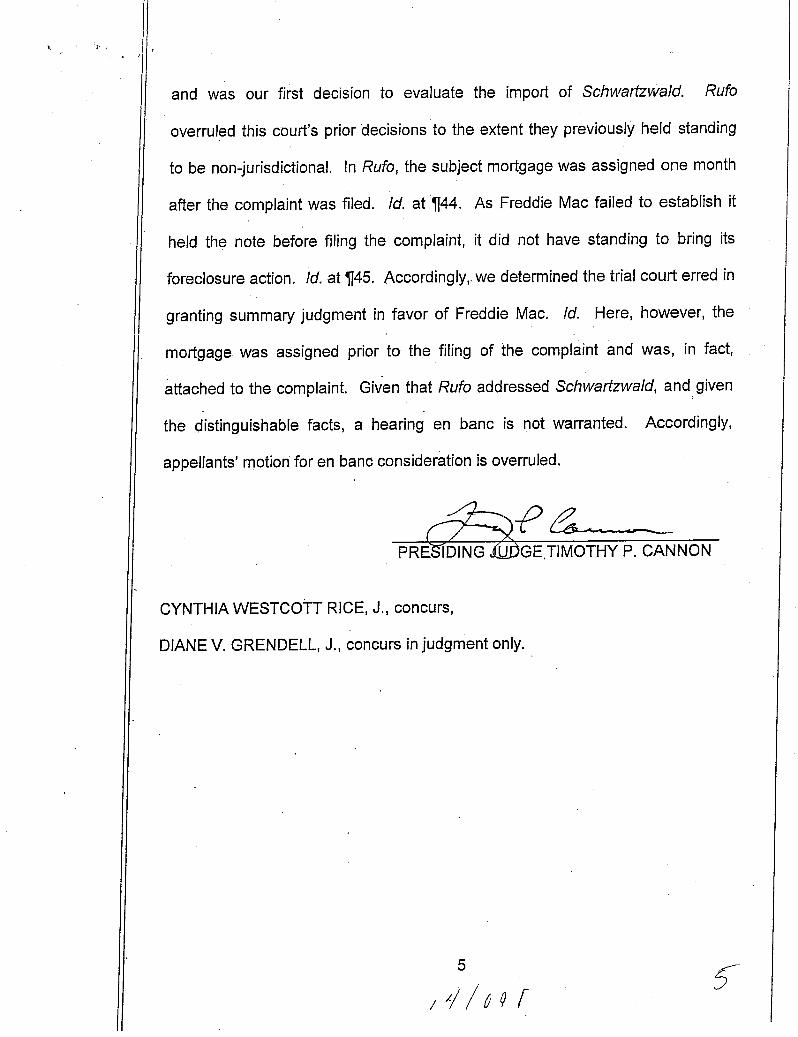

and was our first decision to evaluate the import of Schwartzwald. Rufo

11 overruled this court's prior tlecisions to the extent they previously held standing

to be non-jurisdictional. In Rufo, the subject mortgage was assigned one month

after the complaint was filed. Id. at ¶44. As Freddie Mac failed to establish it

held the note before filing the complaint, it did not have standing to bring its

foreclosure action. Id. at ¶45. Accordingly,. we determined the trial court erred in

granting summary judgment in favor of Freddie Mac. Id. Here, however, the

mortgage was assigned prior to the filing of the complaint and was, in fact,

attached to the complaint. Given that Rufo addressed Schwartzwald, and given

the distinguishable facts, a hearing en banc is not warranted. Accordingly,

appellants' motiori for en banc consideration is overruled.

PRE. IDING U GE,TIMOTHY P. CANNON

CYNTHIA WESTCOTT RICE, J., concurs,

DIANE V. GRENDELL, J., concurs in judgment only.

5

b 1 `d

IN THE COURT OF APPEALS

ELEVENTH APPELLATE DISTRICT

GEAUGA COUNTY, OHIO

HSBC BANK USA, NATIONALASSOCIATION, AS TRUSTEE UNDERPOOLING AND SERVICINGAGREEMENT DATED AS OFNOVEMBER 1, 2006, FREMONT HOMELOAN TRUST 2006-D,

Plaintiff-Appellee,

-vs-

.MICHELLE SCACCHI, et al.,

Defendants-Appel I ants,

THE UNITED STATES OF AMERICA,et al.,

Defendants-Appellees.

^N couRLo^"O'^

^.saF AOV Z6 2012G Rk^ ^M^MSK1FRU^ CO^^S

OPINION

CASE NO. 2012-G-3062

Civil Appeal from the Geauga County Court of Common Pleas, Case No. 10F000938.

Judgment: Affirmed.

Dean Kane(lis, Keith D. Weiner & Associates Co., L.P.A., 75 Public Square, 4th Floor,Cleveland, OH 44113 (For Plaintiff-Appellee).

James R. Douglass,James R. Douglass Co., L.P.A., 20521 Chagrin Boulevard, Suite

D, Shaker Heights, OH 44122-9736 (For Defendants-Appellants).

Marion A. Primes,Office of the U.S. Attorney, 801 W. Superior Avenue, Suite 400,

United States Courthouse, Cleveland, OH 44113 (For Defendants-Appellees, TheUnited States of America and The United States of America U.S. Department of

Justice).

David P. Joyce, Geauga County Prosecutor, and Bridey Matheney, Assistant

Prosecutor, Courthouse Annex, 231 Main Street, Chardon, OH 44024 (For Defendant-

Appellee, Treasurer of Geauga County).

TIMOTHY P. CANNON, P.J.

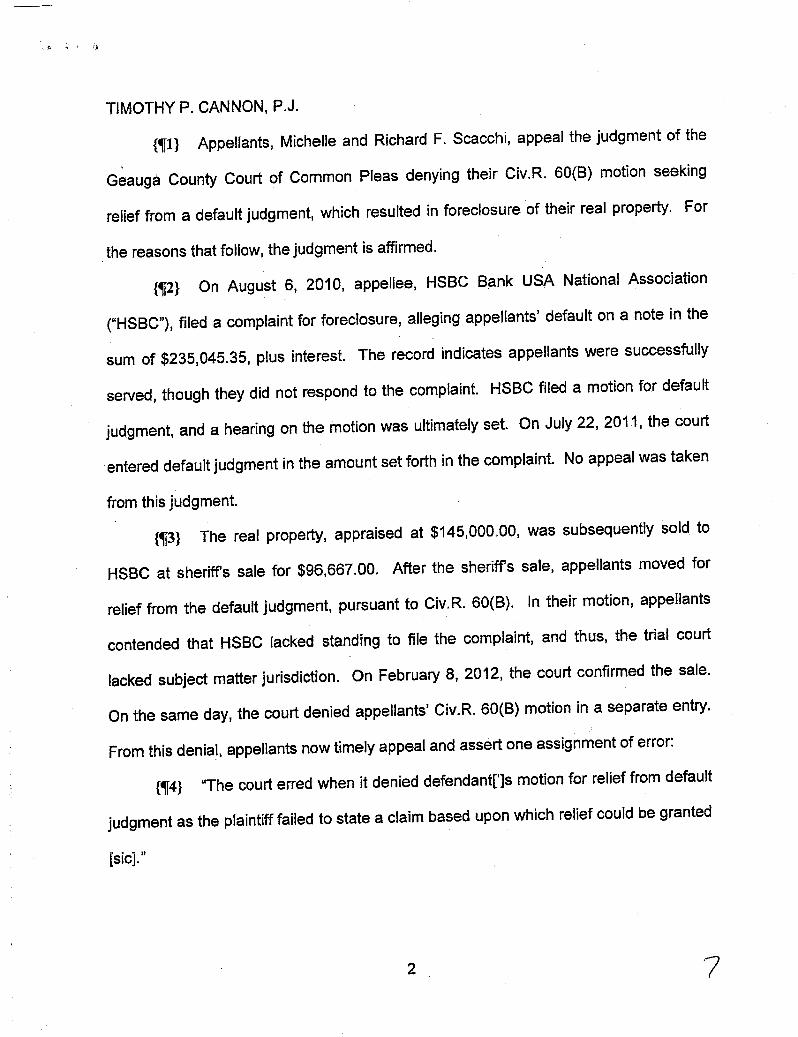

{¶1} Appellants, Michelle and Richard F. Scacchi, appeal the judgment of the

Geauga County Court of Common Pleas denying their Civ.R. 60(B) motion seeking

relief from a default judgment, which resulted in foreclosure of their real property. For

the reasons that follow, the judgment is affirmed.

{¶2} On August 6, 2010, appellee, HSBC Bank USA National Association

("HSBC"), filed a complaint for foreclosure, alleging appellants' default on a note in the

sum of $235,045.35, plus interest. The record indicates appellants were successfully

served, though they did not respond to the complaint. HSBC filed a motion for default

judgment, and a hearing on the motion was ultimately set. On July 22, 2011, the court

entered default judgment in the amount set forth in the complaint. No appeal was taken

from this judgment.

{¶3} The real property, appraised at $145,000.00, was subsequently sold. to

HSBC at sheriffs sale for $96,667.00. After the sheriff's sale, appellants moved for

relief from the default judgment, pursuant to Civ.R. 60(B). In their motion, appellants

contended that HSBC lacked standing to file the complaint, and thus, the trial court

lacked subject matter jurisdiction. On February 8, 2012, the court confirmed the sale.

On the same day, the court denied appellants' Civ.R. 60(B) motion in a separate entry.

From this denial, appellants now timely appeal and assert one assignment of error:

{¶4} "The court erred when it denied defendant[']s motion for relief from default

judgment as the plaintiff failed to state a claim based upon which relief could be granted

[sic]."

2 . ^

{15} In their sole assignment of error, appellants contend the trial court erred in

denying their Civ.R. 60(B) motion, which sought relief from the default judgment on the

grounds the trial court lacked subject matter jurisdiction.

{¶6} Civ.R. 60(B) provides, in pertinent part:

{¶7} On motion and upon such terms as are just, the court may relieve a

party * * * from a final judgment * * * for the following reasons: (1)

mistake, inadvertence, surprise or excusable neglect; (2) newly

discovered evidence which by due diligence could not have been

discovered in time to move for a new trial under Rule 59(B); (3)

fraud * * *; (4) the judgment has been satisfied, released or

discharged '° * *; or (5) any other reason justifying relief from the

judgment. The motion shall be made within a reasonable time, and

for reasons (1), (2) and (3) not more than one year after the

judgment, order or proceeding was entered or taken.

{¶S} Thus, Civ.R. 60(B) provides parties with an equitable remedy requiring a

court to revisit a final judgment and possibly afford relief from that judgment when in the

interest of justice. In re Edge!!, 11th Dist. No. 2009-L-065, 2010-Ohio-6435, ¶52. It is a

curative rule which is to be liberally construed with the focus of reaching a just result.

Hiener v. Moretti, 11th Dist. No. 2009-A-0001, 2009-Ohio-5060, ¶18. "Moreover, Civ.R.

60(B) has been viewed as a mechanism to create a balance between the need for

finality and the need for `fair and equitable decisions based upon full and accurate

information."' Id., quoting In re Whitman, 81 Ohio St.3d 239, 242 (1998). Whether relief

should be granted under a Civ.R. 60(B) motion is a determination entrusted to the

3

{e. @I t

sound discretion of the trial court. In re Whitman, 81 Ohio St.3d 239, 242 (1998), citing

Griffey v. Rajan,33 Ohio St.3d 75, 77 (1987). As such, the standard of review is

whether the trial court abused its discretion. Id.

{¶9} it is well founded that Civ.R. 60(B) relief is not to be used as a substitute

for a direct appeal. Doe v. Trumbull Cty. Children Services Bd., 28 Ohio St.3d 128,

paragraph two of the syllabus (1986). See Am. Express Bank, FSB v. Walfer, 11th Dist.

No. 2011-L-047, 2012-Ohio-3117, ¶14 ("[an appellant] cannot, however, after the

opportunity for direct appellate review has passed, use Civ.R. 60(B) as a means of

indirect entry into appellate review"). Thus, "a Civ.R. 60(B) motion may not be based on

arguments that could have been raised on direct appeal." Wells Fargo Bank, N.A. v.

Smith, 10th Dist. Noa 09AP-559, 2009-Ohio-6576, ¶11 (citation omitted).

{110} In this case, the trial court's July 22, 2011 foreclosure decree was a final,

appealable order, pursuant to R.C. 2505.02, as it affected a substantial right and

determined the action concerning the parties' rights to the subject parcel. Further, it

certified there to be "no just reason for delay" pursuant to Civ.R. 54(B). See Bank of

New York Mellon Trust Co. v. Shaffer, 11th Dist. No. 2011-G-3051, 2012-Ohio-3638,

¶41. Thus, appellant's alleged error concerning standing could have been raised in a

direct appeal of the foreclosure decree. See Deutsche Bank Nati. Trust Co. v.

Richardson, 2d Dist. Nos. 2010-CA-3 & 2010-CA-13, 2011 -Ohio-1 123, ¶32. ("Any error

by the trial court in granting a judgment in foreclosure * * * could have been raised in a

direct appeal of the court's judgment in foreclosure.") In short, appellants "cannot use a

Civ.R. 60(B) motion to raise an issue that should have been raised in a direct appeal."

Id.; see also UBS Real Estate Secs., Inc. v. Teague, 191 Ohio App.3d 189, 2010-Ohio-

4

5634 (2d Dist.), ¶16; GMAC Mtge. LLC v. Herring, 189 Ohio App.3d 200, 2010-Ohio-

3650 (2d Dist.), ¶35.

{¶ii} Assuming the merits of the Civ.R. 60(B) motion could be considered,

appellants' arguments nonetheless fail. The Ohio Supreme Court has set forth a three-

prong test which the movant must meet to prevail on a Civ.R. 60(B) motion. First, the

motion must be timely, i.e., not more than one year after the judgment or order was

entered where the.grounds of relief are Civ.R. 60(B)(1)-(3); otherwise, the motion must

be made within a reasonable time. Second, the party must be entitled to relief under

one of the outlets in Civ.R. 60(B)(1)-(5). Third, the party must have a meritorious

defense or claim to raise if relief is granted. GTE Automatic Elec. v. ARC lndustries, 47

Ohio St.2d 146, paragraph two of the syliabus (1976). A party must satisfy each prong

to be entitled to relief. KMV V Ltd. v. Debolt, 11th Dist. No. 2010-P-0032, 2011-Ohio-

525, ¶24. If one prong is not satisfied, the entire motion must be overruled. ld., quoting

Rose Chevrolet, Inc. v. Adams, 36 Ohio St.3d 17, 20 (1988).

f¶12} In their Civ.R. 60(B) motion before, the trial court, appellants did not

specifically allege which prong of Civ.R. 60(B) should afford them relief. Also, at oral

argument, counsel for appellants did not attempt to explain under which prong of Civ.R.

60(B) relief had been sought. In fact, counsel noted he had no explanation as to why

appellants failed to defend at the trial court level prior to default judgment, essentially

abandoning any contention that the failure constituted "excusable neglect." Instead,

appellants argued the trial court did not have subject matter jurisdiction because HSBC

was not the real party in interest (i.e., that it lacked standing), as it was not the original

5 %0

r,_ ^, "' i

holder of the note and nothing indicated a proper transfer of the note. As such, they

argued the default judgment was void.

{¶13} However, this court has previously held that lack of standing challenges

the capacity of a party to bring an action-it does not challenge the subject matter.

jurisdiction of the trial court. Waterfall Victoria Master Fund Ltd. v. Yeager, 11th Dist.

No. 2011-L-025, 2012-Ohio-124, ¶13;EverHome Mtge. Co. v. Behrens, 11tfi Dist. No.

2011-L-128, 2012-Ohio-1454, ¶12. See also Aurora Loan Servs., LLC v. Cart, 11th

Dist. No. 2009-A-0026, 2010-Ohio-1157, ¶18, citingWashington Mut. Bank v. Novak,

8th Dist. No. 88121, 2007-Ohio-996, ¶16 (noting Civ.R. 17 is not necessary to invoke

the jurisdiction of a common pleas court). Here, as the matter fell squarely within the

class of cases over which the Geauga County Court of Common Pleas has subject

matter jurisdiction, it was properly before the trial court. Thus, the default judgment is

not void.

{¶14} Further, the failure to raise an objection as to standing at the trial court

level constitutes waiver of the claim. See Yeager, supra, ¶13 (failure to raise a standing

or "real party in interest" defense results in waiver of the claim);Behrens, supra, ¶15

("we do not reach the merits of this issue because Mr. Behrens failed to challenge

EverHome's standing prior to the entry of default judgment"). In this case, as the matter

of standing was not timely raised before the trial court, it has been waived.

{¶15} Finally, though not framed as an individual assignment of error, appellants

additionally suggest they were entitied to a hearing on the Civ.R. 60(B) motion. As

appellants correctly point out, "'[i]f the movant files a motion for relief from judgment and

it contains allegations of operative facts which would warrant relief under Civ.R. 60(B),

6 ^^

4ee, tt " a !_4

the trial court should grant a hearing to take evidence and verify these facts before it

rules on the motion."' Kay v. Marc G/assman, Inc., 76 Ohio St.3d 18, 19 (1996), quoting

Coulson v. Coulson,5 Ohio St.3d 12, 16 (1983). As explained above, however,

appellants did not set forth specific allegations of operative facts that would warrant

refief. Therefore, as a hearing is not automatically required, and as no allegations were

set forth which warranted relief, the triai court did not abuse its discretion in failing to

hold a hearing.

ib} Appellants' assignment of error is without merit. The judgment of the{¶

Geauga County Court of Common Pleas is affirmed.

DIANE V. GRENDELL, J.,

CYNTHIA WESTCOTT RICE, J.,

concur.

7 / Zs

IFI ^ El^IN COUR7OF qpPF-ALS

STATE OF OHIO NOV ?6 1012O6NISE ^

COUNTY OF GEAUGAeLERKQk ouRTKI^?EAUGA C flUNTY

HSBC BANK USA, NATIONALASSOCIATION, AS TRUSTEE UNDERPOOLING AND SERVICINGAGREEMENT DATED AS OFNOVEMBER 1, 2006, FREMONT HOMELOAN TRUST 2006-D,

Plaintiff-Appellee,

- vs -

MICHELLE SCACCHI, et al.,

Defendants-Appellants,

THE UNITED STATES OF AMERICA,et al.,

Defendants-Appel lees.

IN THE COURT OF APPEALS

ELEVENTH DISTRICT

JUDGMENT ENTRY

CASE NO. 2012-G-3062

For the reasons stated in the opinion of this court, appellants' assignment

of error is without merit. It is the judgment and order of this court that the

judgment of the Geauga County Court of Common Pleas is affirmed.

Costs to be taxed against appellants.

` ^..__..._._^.PR I G JUD TIMOTHY P. CANNON

FOR THE COURT

fY /6/ 3 ^ ^3

![[Scacchi ITA Libro] - Karpov, Anatoly (Scacchi Primo Amore) (Testo)](https://img.dokumen.tips/doc/110x75/55cf9a31550346d033a0cb1b/scacchi-ita-libro-karpov-anatoly-scacchi-primo-amore-testo.jpg)

![[Scacchi ITA Libro] - Karpov, Anatoly (Scacchi Primo Amore)](https://img.dokumen.tips/doc/110x75/549db557b37959d7618b4593/scacchi-ita-libro-karpov-anatoly-scacchi-primo-amore.jpg)