Embed Size (px)

Citation preview

How Will AgriculturalE-Markets Evolve?

Royce Nicolaisen, CEO

AgEx.com

February 22, 2001

“I’m all for progress. It’s change Ican’t stand.”

Mark Twain

“Our e-commerce strategy is to avoidit as long as possible.” --Anonymous U.S. Ag company

AgEx.com provides e-procurement solutions to top U.S.food and beverage manufacturing companies. Our goalis to enable our clients to leverage a more efficientpurchasing process so that they ultimately increase theirbottom line and maximize shareholder value.

E-commerce In Perspective

•E-commerce is not new

–UPC codes

–Electronic Data Interchange (EDI)

–Vendor Managed Inventories (VMI)

•Has already dramatically changed the fooddistribution landscape

•UPC codes alone altered the power balance

–Retailers now control market information

•Wal-Mart's exceptional growth can be traced toaggressive use of technology

–Pioneered vendor managed inventory concept

E-commerce In Perspective

•Food retailers’ fear of Wal-Mart has triggered the mostimportant trend in the food distribution business today –rapid consolidation of retailers and manufacturers

•This consolidation is already having a severe impact onprimary food producers

E-commerce In Perspective

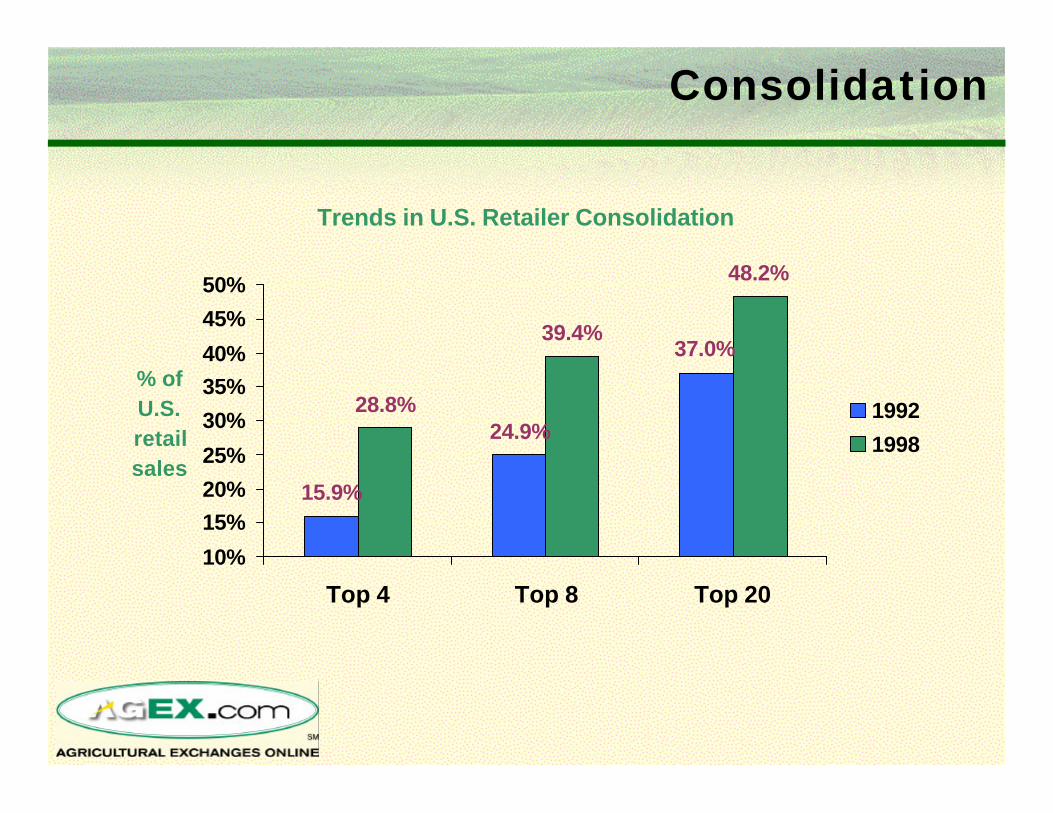

Consolidation

“Since 1996, large retailers have purchased almost 3,500supermarkets, representing annual grocery store salesof more than $67 billion.” --Agricultural Outlook, Aug 2000

Consolidation

Trends in U.S. Retailer Consolidation

15.9%

24.9%

37.0%

28.8%

39.4%

48.2%

10%

15%20%

25%

30%

35%40%

45%

50%

Top 4 Top 8 Top 20

% of U.S. retail sales

1992

1998

Retail Consolidation

Acquiring Co. (Sales) Co. Acquired (Sales) Total Sales

Kroger ($28.2 billion) Fred Meyer ($14.9 billion) $43.1 billion

Albertson's ($16.0) American Stores ($19.7) $36.3 billionButtrey ($0.4)Sessells ($0.2)

Safeway ($23.7) Carr Gottstein ($0.5) $24.2 billion

Top 5 Grocery Consolidations in 1998

Food Industry Consolidation

Recent Mergers & Acquisitions in Food Industry(1998-2000)

ACQUIRING COMPANY ($ Sales) COMPANY ACQUIRED ($ Sales) TOTAL SALES

Unilever ($43.6 billion) Bestfoods ($8.6 billion) $52.2 billion

Philip Morris ($27.5) Nabisco ($8.3) $35.8

General Mills ($6.7) Pillsbury ($5.9) $12.6

Kellogg ($7.0) Keebler ($2.67) $9.7

•While retailers and grocery manufacturers consolidate,the supply side remains fragmented

–No processing cost advantages to consolidating

–Wide geographic dispersion

–Enterprises are mostly family owned or co-ops

•Sellers continue to lose negotiating leverage

Impact on Supply Side

Price Trends

U.S. Wholesale vs. Retail Refined Sugar Prices

19

24

29

34

39

44

1990,Q1

1990,Q4

1991,Q3

1992,Q2

1993,Q1

1993,Q4

1994,Q3

1995,Q2

1996,Q1

1996,Q4

1997,Q3

1998,Q2

1999,Q1

1999,Q4

cen

ts/lb

U.S. Wholesale

U.S. Retail

Sources: Bureau of Labor Statistics &Milling & Baking News

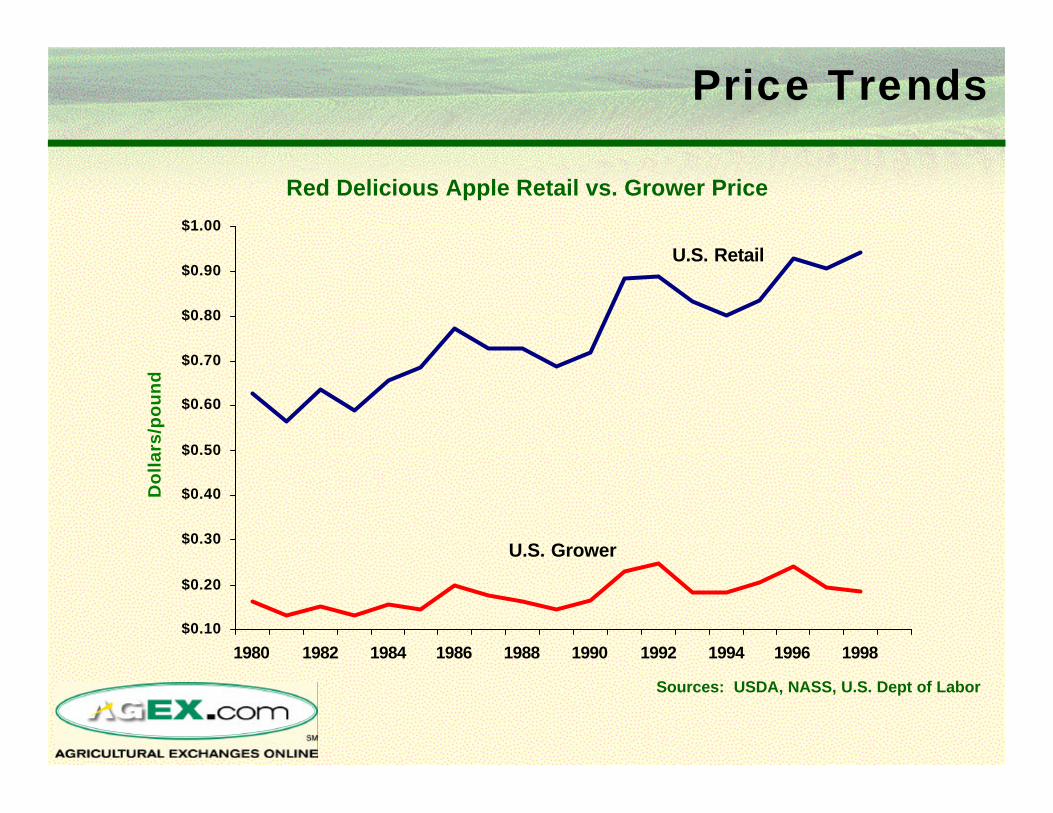

Price Trends

Sources: USDA, NASS, U.S. Dept of Labor

U.S. Retail

$0.10

$0.20

$0.30

$0.40

$0.50

$0.60

$0.70

$0.80

$0.90

$1.00

1980 1982 1984 1986 1988 1990 1992 1994 1996 1998

Do

llar

s/p

ou

nd

U.S. Grower

Red Delicious Apple Retail vs. Grower Price

Price Trends

$0.00

$0.20

$0.40

$0.60

$0.80

$1.00

$1.20

$1.40

$1.60

1960 1963 1966 1969 1972 1975 1978 1981 1984 1987 1990 1993 1996 1999

Do

llars

Per

Po

un

d

Fresh Tomato Retail vs. Grower Price

Sources: USDA, NASS, U.S. Dept of Labor

Share Price – Dole

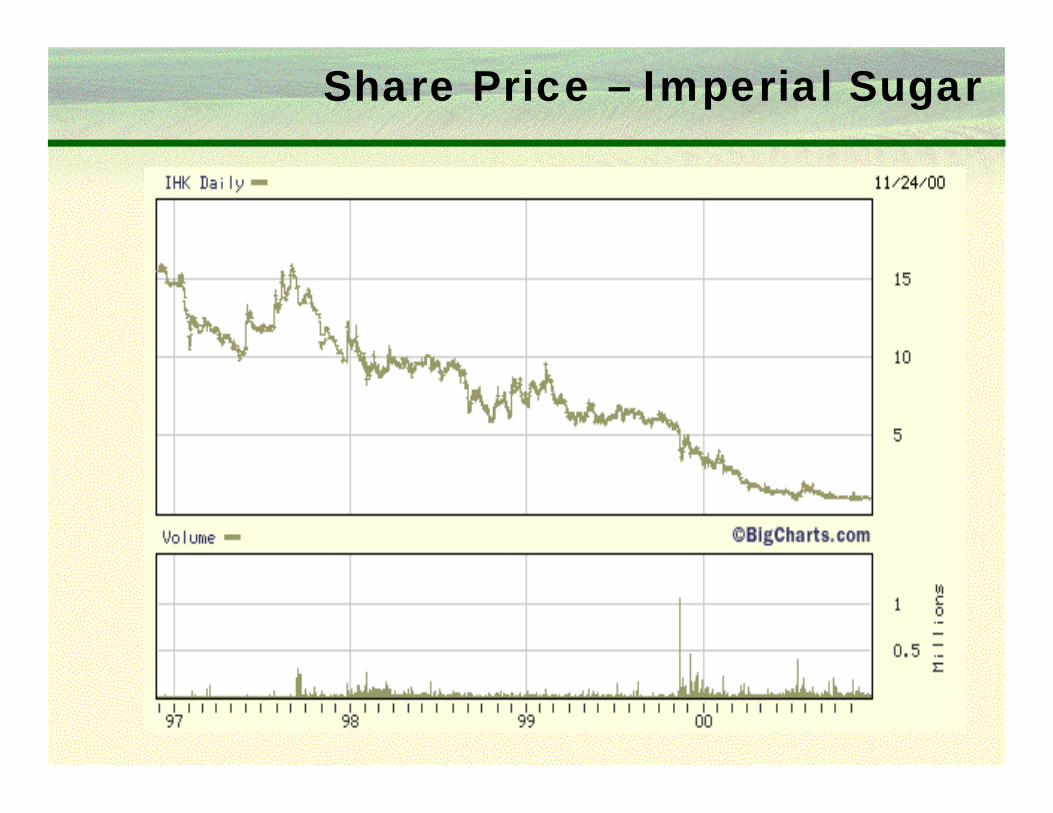

Share Price – Imperial Sugar

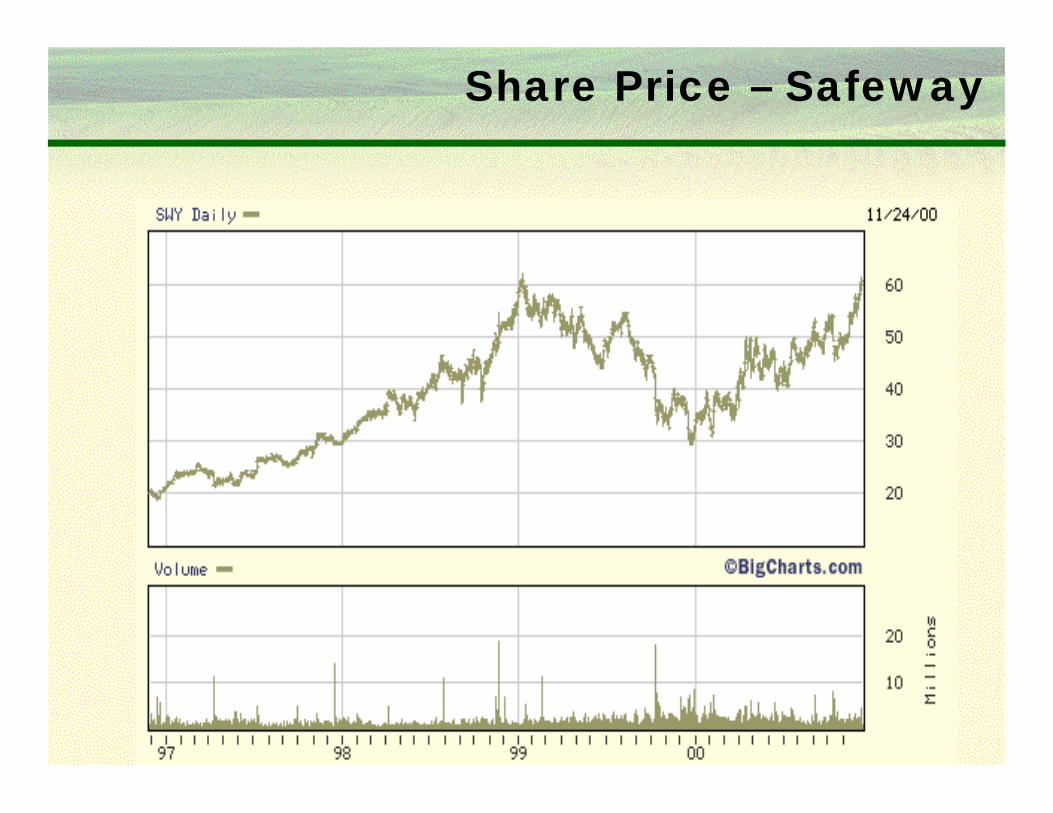

Share Price – Safeway

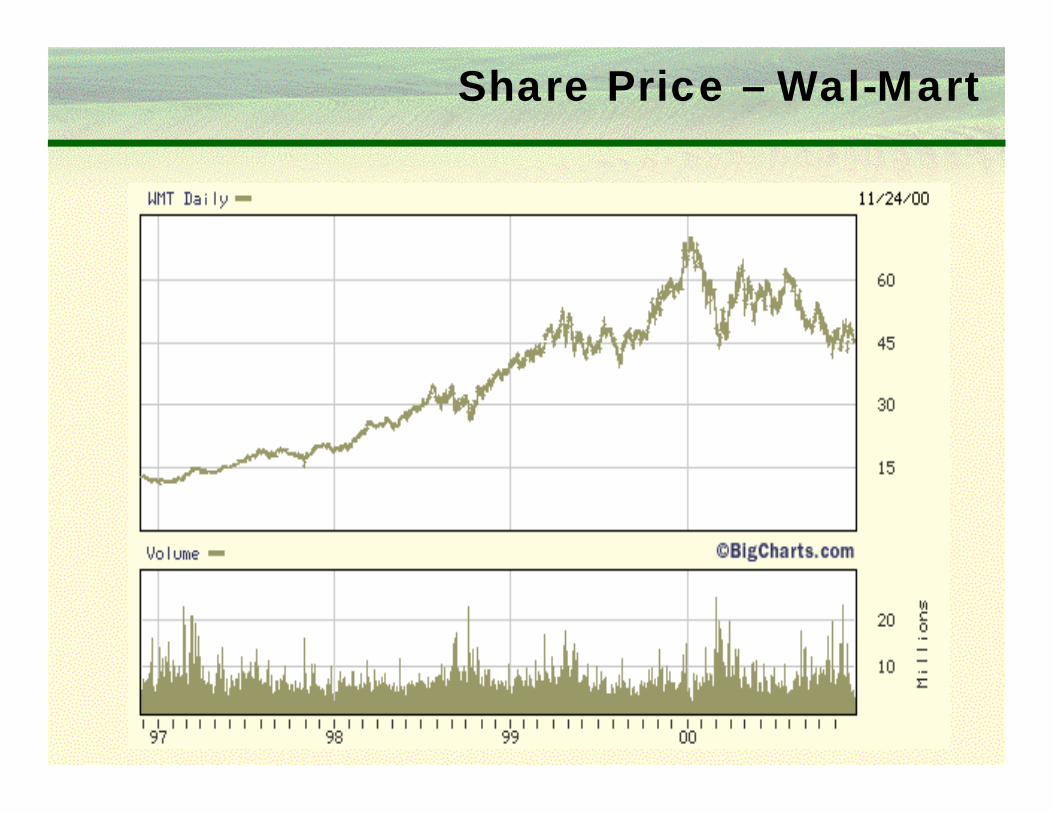

Share Price – Wal-Mart

Major Suppliers Versus S&P 500 For Last 5 Years

Dole Northland DeanFoods

Imperial Sugar

S&P 500

Supplier Trends

Major Retailers Versus S&P 500 For Last 5 Years

Costco SafewayS&P 500

Kroger Wal-Mart

Retailer Trends

Going Forward

•The Internet is changing the nature of E-Commerce

•Prior E-Commerce was of the one-to-one type

•The Internet allows for Collaborative E-Commerce

–Electronic marketplaces

–Automated supply chains

Collaborative E-Commerce

Major buyers are already organizing collaborative marketplaces

•Transora

– Formed by 50 major grocery manufacturers, such as P&G,Kraft, and General Mills

–$250 million invested

•Worldwide Retail Exchange

–Includes Safeway, Ahold, Albertson’s

•Global Net Exchange

–Includes Kroger, Sears, Carrefour

Mega Market Implications

•Buyers intend to aggregate demand to conduct evenlarger purchases

•Buyers own the data of transactions flowing through themarketplace and choose not to share with the sellers

•Sellers will need to invest in technology to communicatewith these marketplaces

Supplier Options

•If they do nothing, primary food suppliers will be furthersqueezed on prices and at the same time need to investin IT support

•An option is to form supplier sponsored collaborativemarketplaces that will link to the buyer sponsoredmarketplaces

Supplier Marketplace Benefits

•Participants can own the data flowing through themarket

–Better data will allow for better decision making andhelp “level the playing field”

•One linkage to the supplier market will allow linkages toall other markets

–Reduced IT costs

•Can collaborate among members

–Trade raw material overages and shortages–Trade plant capacity–Participate in combined offers

•Can better obtain and disseminate crop estimates andmarket demand conditions

–Help reduce over-planting and reckless pricing

•

Supplier Marketplace Benefits

Supplier Marketplace Benefits

•Can conduct aggregated purchases of needed inputssuch as packaging materials, energy, and transportation

•Can utilize marketplace-owned, web hosted businesssoftware applications thereby adding efficiency at lowcost

AgEx.com’s Role

•Organizers of marketplaces designed to assist theprimary food manufacturers

–No other e-commerce company has adopted this approach

–Electronic procurement is about value, rather than cost

–Allows for more participation by suppliers

–Offers price transparency

–Shortens the purchasing cycle

• In regular contact with the major buyinggroups

• Already active in the nut, dried fruit, rice,pulse, sugar, tomato product, and juiceindustries

• Employ latest technology to supportsupplier needs

AgEx.com’s Role

![®f^!ip^ 33080^0 (ooo«ao8)€¦ · i ®f^!ip^ 33080^0 (ooo«ao8) [8oS^£s igooooSoS^S: ioo8aSs^8s ] °S?J"?f^ V JOOO-^SsOoS &g e3^£oj>oo£ (uoooaogoecooSooeo) (^o8oo33Jo^S)](https://img.dokumen.tips/doc/110x75/5fb4c6d5b2536e53d735a761/fip-330800-oooao8-i-fip-330800-oooao8-8oss-igoooososs.jpg)