Embed Size (px)

Citation preview

Financial stress Markov-switching Better ?

How to predict financial stress? An assessment ofMarkov switching models

Thibaut Duprey (Bank of Canada)

Benjamin Klaus (European Central Bank)

The views expressed in this paper are those of the authors and do not necessarily reflect thoseof the Bank of Canada, the European Central Bank, the Banque de France or the Eurosystem.

IWFSAS 2017

Financial stress Markov-switching Better ?

Focus of the paper

Continuous metric (Markov switch, eg for business cycle)

vs. binary models (Logit, eg for banking crises)

Financial stress Markov-switching Better ?

Focus of the paper

1 Can we use Markov switching to predict the financial cycle ?

2 Which variables predict the entry into / exit from high financialstress ?

I What are the vulnerabilities associated with subsequent realisedfinancial stress ?

3 Were those predictors useful even before the 2008 crisis ?

4 Do we gain additional predictive power by looking at the wholefinancial cycle instead of using standard binary crisis indicators ?

Financial stress Markov-switching Better ?

Related literature

• Dating business cycle turning points : Hamilton (1989),Filardo (1994), Diebold et al (1994), Chauvet and Piger (2008),Gadea and Perez-Quiros (2012)

• Measuring financial market stress : Hollo et al (2012),Hartmann et al (2013), Duprey et al (2017)

• Comparing early warning models : Abiad (2003) evaluates thesignalling ability of MS models for Asian currency crises

Financial stress Markov-switching Better ?

Section 1

Preliminary : Measuring financial stress

end of 2006

end of 2007

end of 2008

Financial stress Markov-switching Better ?

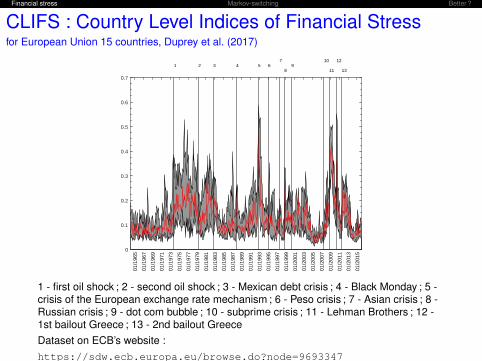

CLIFS : Country Level Indices of Financial Stressfor European Union 15 countries, Duprey et al. (2017)

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

1 2 3 4 5 67

89

10

11

12

13

01/1

965

01/1

967

01/1

969

01/1

971

01/1

973

01/1

975

01/1

977

01/1

979

01/1

981

01/1

983

01/1

985

01/1

987

01/1

989

01/1

991

01/1

993

01/1

995

01/1

997

01/1

999

01/2

001

01/2

003

01/2

005

01/2

007

01/2

009

01/2

011

01/2

013

01/2

015

Fin

anci

al S

tres

s In

dex

(FS

I)

1 - first oil shock ; 2 - second oil shock ; 3 - Mexican debt crisis ; 4 - Black Monday ; 5 -crisis of the European exchange rate mechanism ; 6 - Peso crisis ; 7 - Asian crisis ; 8 -Russian crisis ; 9 - dot com bubble ; 10 - subprime crisis ; 11 - Lehman Brothers ; 12 -1st bailout Greece ; 13 - 2nd bailout GreeceDataset on ECB’s website :https://sdw.ecb.europa.eu/browse.do?node=9693347

Financial stress Markov-switching Better ?

Real GDP growth per quantiles of CLIFSfor European Union 15 countries

y-o-

yre

alG

DP

grow

th

-3

-2

-1

0

1

2

0-10 10-20 20-30 30-40 40-50 50-60 60-70 70-80 80-90 90-100

Quantile of CLIFS

Financial stress Markov-switching Better ?

Section 2

Markov-switching models for early-warning

Financial stress Markov-switching Better ?

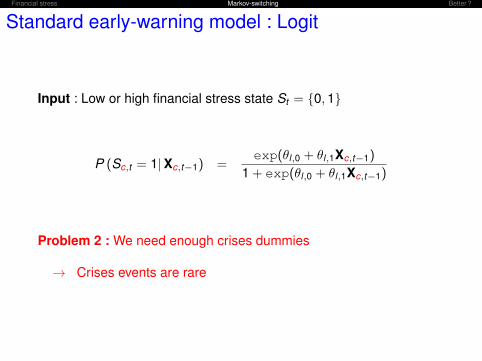

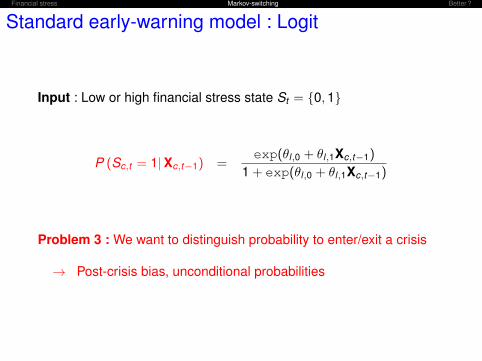

Standard early-warning model : Logit

Input : Low or high financial stress state St = {0,1}

P (Sc,t = 1|Xc,t−1) =exp(θl,0 + θl,1Xc,t−1)

1 + exp(θl,0 + θl,1Xc,t−1)

dd

dd

Financial stress Markov-switching Better ?

Standard early-warning model : Logit

Input : Low or high financial stress state St = {0,1}

P (Sc,t = 1|Xc,t−1) =exp(θl,0 + θl,1Xc,t−1)

1 + exp(θl,0 + θl,1Xc,t−1)

Problem 1 : We need an exogenous sequence of events to predict

→ Subjectivity bias

Financial stress Markov-switching Better ?

Standard early-warning model : Logit

Input : Low or high financial stress state St = {0,1}

P (Sc,t = 1|Xc,t−1) =exp(θl,0 + θl,1Xc,t−1)

1 + exp(θl,0 + θl,1Xc,t−1)

Problem 2 : We need enough crises dummies

→ Crises events are rare

Financial stress Markov-switching Better ?

Standard early-warning model : Logit

Input : Low or high financial stress state St = {0,1}

P (Sc,t = 1|Xc,t−1) =exp(θl,0 + θl,1Xc,t−1)

1 + exp(θl,0 + θl,1Xc,t−1)

Problem 3 : We want to distinguish probability to enter/exit a crisis

→ Post-crisis bias, unconditional probabilities

Financial stress Markov-switching Better ?

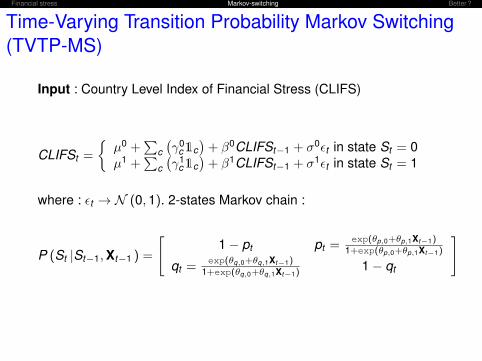

Time-Varying Transition Probability Markov Switching(TVTP-MS)

Input : Country Level Index of Financial Stress (CLIFS)

CLIFSt =

{µ0 +

∑c

(γ0

c1c)+ β0CLIFSt−1 + σ0εt in state St = 0

µ1 +∑

c

(γ1

c1c)+ β1CLIFSt−1 + σ1εt in state St = 1

where : εt → N (0,1). 2-states Markov chain :

P (St |St−1,Xt−1 ) =

[1− pt pt =

exp(θp,0+θp,1Xt−1)1+exp(θp,0+θp,1Xt−1)

qt =exp(θq,0+θq,1Xt−1)

1+exp(θq,0+θq,1Xt−1)1− qt

]

Solves 1 and 2 : subjectivity bias + crises events are rare

Financial stress Markov-switching Better ?

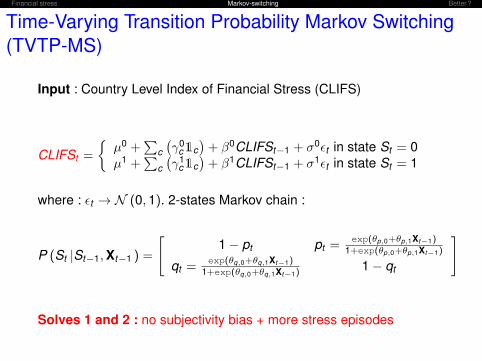

Time-Varying Transition Probability Markov Switching(TVTP-MS)

Input : Country Level Index of Financial Stress (CLIFS)

CLIFSt =

{µ0 +

∑c

(γ0

c1c)+ β0CLIFSt−1 + σ0εt in state St = 0

µ1 +∑

c

(γ1

c1c)+ β1CLIFSt−1 + σ1εt in state St = 1

where : εt → N (0,1). 2-states Markov chain :

P (St |St−1,Xt−1 ) =

[1− pt pt =

exp(θp,0+θp,1Xt−1)1+exp(θp,0+θp,1Xt−1)

qt =exp(θq,0+θq,1Xt−1)

1+exp(θq,0+θq,1Xt−1)1− qt

]

Solves 1 and 2 : no subjectivity bias + more stress episodes

Financial stress Markov-switching Better ?

Time-Varying Transition Probability Markov Switching(TVTP-MS)

Input : Country Level Index of Financial Stress (CLIFS)

CLIFSt =

{µ0 +

∑c

(γ0

c1c)+ β0CLIFSt−1 + σ0εt in state St = 0

µ1 +∑

c

(γ1

c1c)+ β1CLIFSt−1 + σ1εt in state St = 1

where : εt → N (0,1). 2-states Markov chain :

P (St |St−1,Xt−1 ) =

[1− pt pt =

exp(θp,0+θp,1Xt−1)1+exp(θp,0+θp,1Xt−1)

qt =exp(θq,0+θq,1Xt−1)

1+exp(θq,0+θq,1Xt−1)1− qt

]

Solves 3 : no post-crisis bias with conditional probabilities

Financial stress Markov-switching Better ?

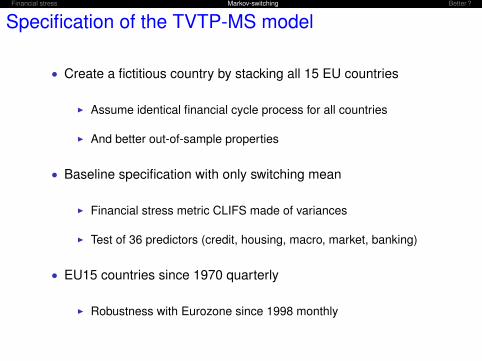

Specification of the TVTP-MS model

• Create a fictitious country by stacking all 15 EU countries

I Assume identical financial cycle process for all countries

I And better out-of-sample properties

• Baseline specification with only switching mean

I Financial stress metric CLIFS made of variances

I Test of 36 predictors (credit, housing, macro, market, banking)

• EU15 countries since 1970 quarterly

I Robustness with Eurozone since 1998 monthly

Financial stress Markov-switching Better ?

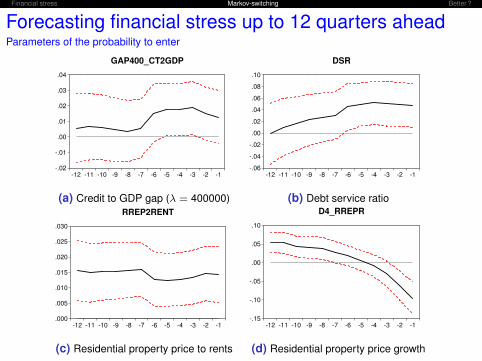

Forecasting financial stress up to 12 quarters aheadParameters of the probability to enter

-.02

-.01

.00

.01

.02

.03

.04

-12 -11 -10 -9 -8 -7 -6 -5 -4 -3 -2 -1

GAP400_CT2GDP

(a) Credit to GDP gap (λ = 400000)

-.06

-.04

-.02

.00

.02

.04

.06

.08

.10

-12 -11 -10 -9 -8 -7 -6 -5 -4 -3 -2 -1

DSR

(b) Debt service ratio

.000

.005

.010

.015

.020

.025

.030

-12 -11 -10 -9 -8 -7 -6 -5 -4 -3 -2 -1

RREP2RENT

(c) Residential property price to rents

-.15

-.10

-.05

.00

.05

.10

-12 -11 -10 -9 -8 -7 -6 -5 -4 -3 -2 -1

D4_RREPR

(d) Residential property price growth

Financial stress Markov-switching Better ?

Stability over time and out-of-sample computationsParameters of the probability to enter

-.05

-.04

-.03

-.02

-.01

.00

.01

.02

.03

20

06

:4

20

07

:2

20

07

:4

20

08

:2

20

08

:4

20

09

:2

20

09

:4

20

10

:2

20

10

:4

20

11

:2

20

11

:4

20

12

:2

20

12

:4

20

13

:2

20

13

:4

20

14

:2

20

14

:4

20

15

:2

GAP400_CT2GDP

(e) Credit to GDP gap (λ = 400000)

-.10

-.05

.00

.05

.10

.15

.20

20

06

:4

20

07

:2

20

07

:4

20

08

:2

20

08

:4

20

09

:2

20

09

:4

20

10

:2

20

10

:4

20

11

:2

20

11

:4

20

12

:2

20

12

:4

20

13

:2

20

13

:4

20

14

:2

20

14

:4

20

15

:2

DSR

(f) Debt service ratio

-.005

.000

.005

.010

.015

.020

.025

.030

.035

20

06

:4

20

07

:2

20

07

:4

20

08

:2

20

08

:4

20

09

:2

20

09

:4

20

10

:2

20

10

:4

20

11

:2

20

11

:4

20

12

:2

20

12

:4

20

13

:2

20

13

:4

20

14

:2

20

14

:4

20

15

:2

RREP2RENT

(g) Residential property price to rents

-.16

-.12

-.08

-.04

.00

.04

200

6:4

200

7:2

200

7:4

200

8:2

200

8:4

200

9:2

200

9:4

201

0:2

201

0:4

201

1:2

201

1:4

201

2:2

201

2:4

201

3:2

201

3:4

201

4:2

201

4:4

201

5:2

D4_RREPR

(h) Residential property price growth

Financial stress Markov-switching Better ?

Probability of high financial stress in the next quarter

0.0

0.2

0.4

0.6

0.8

1.0

19

73

Q2

19

75

Q2

19

77

Q2

19

79

Q2

19

81

Q2

19

83

Q2

19

85

Q2

19

87

Q2

19

89

Q2

19

91

Q2

19

93

Q2

19

95

Q2

19

97

Q2

19

99

Q2

20

01

Q2

20

03

Q2

20

05

Q2

20

07

Q2

20

09

Q2

20

11

Q2

20

13

Q2

20

15

Q2

GB

(i) United Kingdom

0.0

0.2

0.4

0.6

0.8

1.0

19

83

Q3

19

85

Q1

19

86

Q3

19

88

Q1

19

89

Q3

19

91

Q1

19

92

Q3

19

94

Q1

19

95

Q3

19

97

Q1

19

98

Q3

20

00

Q1

20

01

Q3

20

03

Q1

20

04

Q3

20

06

Q1

20

07

Q3

20

09

Q1

20

10

Q3

20

12

Q1

20

13

Q3

20

15

Q1

IE

(j) Ireland

0.0

0.2

0.4

0.6

0.8

1.0

19

80

Q2

19

82

Q2

19

84

Q2

19

86

Q2

19

88

Q2

19

90

Q2

19

92

Q2

19

94

Q2

19

96

Q2

19

98

Q2

20

00

Q2

20

02

Q2

20

04

Q2

20

06

Q2

20

08

Q2

20

10

Q2

20

12

Q2

20

14

Q2

ES

(k) Spain

0.0

0.2

0.4

0.6

0.8

1.0

19

98

Q2

19

99

Q2

20

00

Q2

20

01

Q2

20

02

Q2

20

03

Q2

20

04

Q2

20

05

Q2

20

06

Q2

20

07

Q2

20

08

Q2

20

09

Q2

20

10

Q2

20

11

Q2

20

12

Q2

20

13

Q2

20

14

Q2

20

15

Q2

GR

(l) Greece

Financial stress Markov-switching Better ?

Section 3

Better early-warning properties than Logit ?

Financial stress Markov-switching Better ?

Compare the predictive ability of TVTP-MS and LogitUsing signal classification theory (AUROC)

Difficulties :

• Both models are cross-country, but not nested• Either predict a binary indicator or a continuous measure

Solutions :

• Mapping binary and continuous measures of financial stress

St =

{1 if ma(CLIFSt) > p900 if ma(CLIFSt) ≤ p90

What we compare :

• The predicted probabilities of high financial stressP̂Logit (St = 1|Xt−1) and P̂TVTP−MS (St = 1|Xt−1)

• With the episodes of high financial stress St = {0,1}

Financial stress Markov-switching Better ?

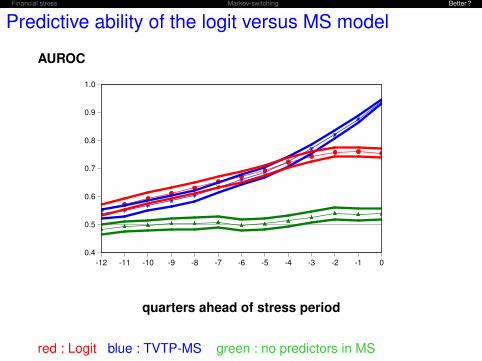

Predictive ability of the logit versus MS model

AUROC

0.4

0.5

0.6

0.7

0.8

0.9

1.0

-12 -11 -10 -9 -8 -7 -6 -5 -4 -3 -2 -1 0

quarters ahead of stress period

red : Logit blue : TVTP-MS green : no predictors in MS

Financial stress Markov-switching Better ?

Wrap-up

Why Markov switching ?• Both event classification and prediction at the same time• Captures the intensity of financial stress• Distinguish the probability to enter/exit financial stress

Which predictors ?• Related to bank credit (debt service ratio) and housing• Harder to find predictor of exiting stress (confidence/market data)• But main predictors not statistically significant before 2007

Good enough ?• In-sample prediction better (a few quarters prior to event)• Out-of-sample estimation of probabilities robust