Embed Size (px)

Citation preview

How to Enter PMI/MIP in Encompass

You must enter PMI in two locations in Encompass. In the MIP/PMI/Guarantee Fee Calculation screen and in the Aggregate Escrow Account setup form.

The MIP/PMI/Guarantee Fee Calculation screen can be accessed on many different screens depending on what forms you have access to.

Some of these forms include: 1003 Page 2, Borrower PreQual, Processor summary, RegZ-LE, and RegZ-CD forms.

Click the Edit Field Value icon for Mortgage Insurance on the 1003 Page 2 or Borrower PreQual to enter PMI/MIP:

The following screen shots provide examples of PMI/MIP entries for conventional and FHA loans.

For conventional loans; the first Monthly Mortgage Insurance Factor should be entered from the MI cert found in the eFolder. The renewal and Cancel At should be automatically populated by the system.

BPMI Monthly SPLIT MI Upfront paid at closing: This is an example of a 1 point upfront and 50 Bps monthly

factor scenario for split MI.

SPLIT MI Upfront Financed: This is an example of a 1 point upfront and 50 Bps monthly factor scenario

for split MI.

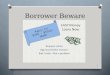

LPMI MI

Borrower Paid Single Premium Borrower Financed Single Premium

FHA Loans

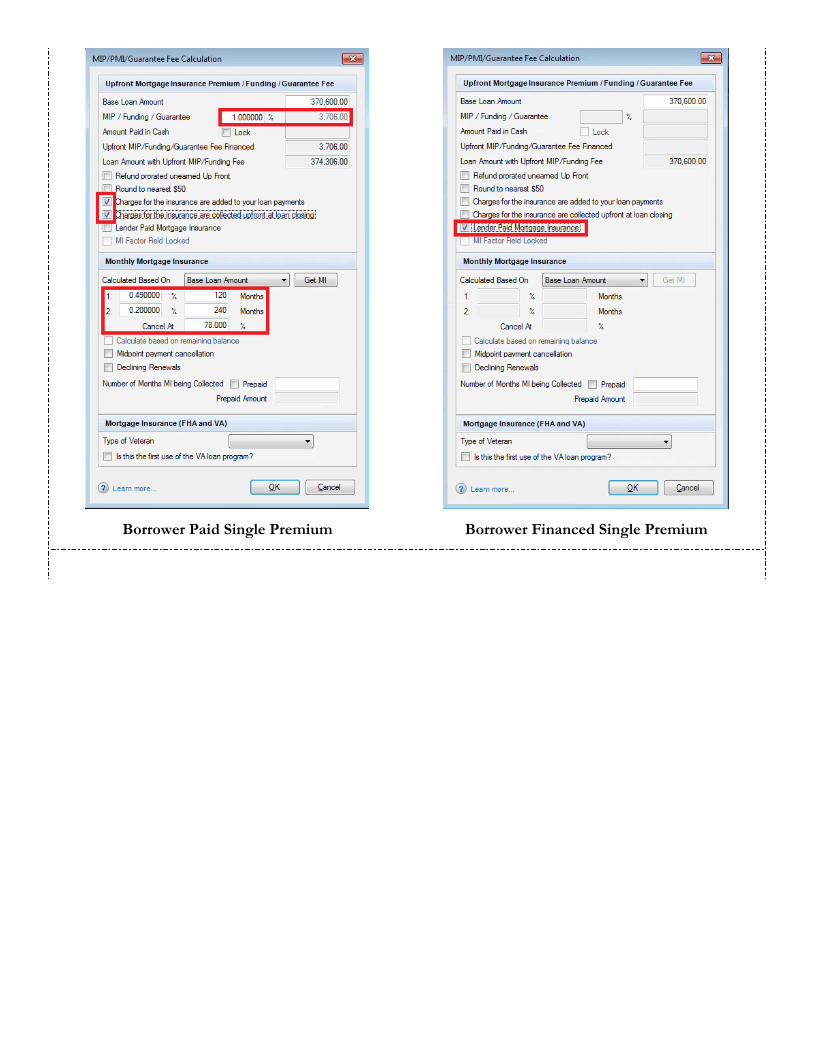

Note: Please check the “Cancel At” for HPA Compliance:

“Cancel At” should be automated but users. However, it is important to double check this.

To comply with the Homeowners Protection Act (HPA), conventional loans with monthly mortgage insurance should be set up to cancel at 78% LTV, if the property is a single-family primary residence.

All multiunit non-primary conventional loans with monthly mortgage insurance will be set up to have monthly mortgage insurance for the life of the loan.

The “Cancel At” LTV % is important because it will affect your calculated APR and finance charges. To ensure the APR and finance charges are accurate and consistent with the calculated APR and finance charge in Mavent, these field triggers have been created.

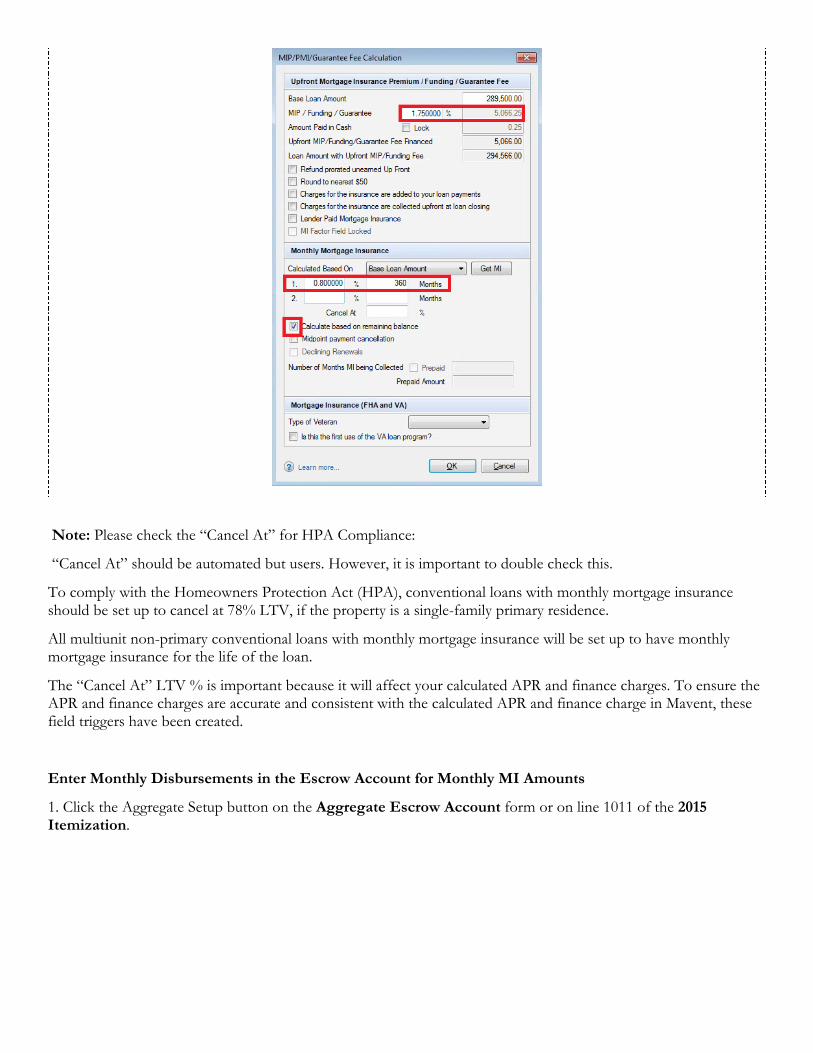

Enter Monthly Disbursements in the Escrow Account for Monthly MI Amounts

1. Click the Aggregate Setup button on the Aggregate Escrow Account form or on line 1011 of the 2015 Itemization.

2. If the PMI is paid monthly, enter 1 in every row for the first 12 months only, as shown in the example below.

![© Encompass Corporation 6 &0 encompass case study ... case study Turpin arker rmstrong encompass case study Turpin arker rmstrong by using encompass uncover, [we] quickly get a feel](https://img.dokumen.tips/doc/110x75/5af0ac5d7f8b9a8c308d7976/encompass-corporation-6-0-encompass-case-study-case-study-turpin-arker-rmstrong.jpg)