Embed Size (px)

Citation preview

How do East African cities

deliver sustainable

economic development

through infrastructure

delivery?

September 2014

CONTENTS

Section 1: East Africa country profiles

Section 2: What are the real problems?

Section 3: A model for economic development

Section 4: Our approach to economic development

5

23

30

34

3

4

Quite rightly, the talk of an “African economic Renaissance” continues to grow. The reality is that a wide range of African countries have now experienced consistent and robust growth for over a decade. In the period since 2002, the size of the overall African economy has more than trebled. What makes this economic performance all the more remarkable is that half of the decade has been marked by a deeply troubled global economy. A diverse group of African economies (including Ethiopia and Tanzania in East Africa)are among the fastest growing in the world, with growth at 7%+ over a sustained period. The signs for Africa and East Africa in particular are good - investor interest is driven by strong economic growth, rising foreign exchange reserves, quality and cost competitiveness and encouraging Government policy-making. These strong levels of economic growth have led to an expansion of industry, commerce and per capita income which in turn has fuelled demand for infrastructure services including energy, transportation, ICT, water supply, growing agriculture and urban infrastructure. East Africa has a history that demonstrates the positive relationship between infrastructure growth and country buoyancy (measured by GDP). In the period between 1995-2005, improvements in communication technologies and Power infrastructure boosted growth by approximately one percentage point per year. Indeed in terms of access to improved sources of water and sanitation and internet density, it is at least comparable with the subcontinent’s leader, Southern Africa. However, even with this investment, East Africa’s infrastructure ranks behind that of its neighbours South and West Africa across a range of other indicators and by contrast, density of fixed-line telephones, power generation capacity, and access to electricity remain extremely low (though utility performance is improving through regional power trades). The road network requires improvement and all forms of surface transport are challenged by border crossings, port delays, slow travel, limited railways, and trade logistics. Air transport benefits from a strong hub-and-spoke structure but has made little progress toward a free and competitive market. Of the seven countries in the region, four are landlocked, two have populations of fewer than 10 million people, and two have an annual gross domestic product of less than $10 billion. The difficult economic geography of East Africa makes a regional approach to infrastructure development necessary to achieve further improvement. We are delighted that this, our first East Africa economic development specific publication, creates an opportunity through our current thought leadership and capabilities, to consider both the unique strengths of each country in the cluster whilst also enabling a genuine discussion on regional infrastructure development, cognizant of a complex set of problem statements. We hope that you are as excited as us at the opportunities for sustainable economic development to galvanize community development and prosperity and set a course for an integrated and connected (East) Africa! We look forward to meeting with you and discussing every matter of interest. Warmest regards,

Joe Cosma

FOREWORD

Joe Cosma

Advisory Sector Leader

Government & Infrastructure

Tel: +27 (0)11 772 5416 Email: [email protected]

Celestine Munda

East Region Advisory Leader

Tel: +27 (0)11 772 3315 Email: [email protected]

5

East Africacountry profiles

6

South Sudan

Tanzania

KenyaUganda

Ethiopia

Country overview

Opportunity indicators Risk indicators

GDP (current) US$43.13bn Ease of doing business overall rank out of 184 countries (16th in Africa)

127

Population growth (annual) 2.09%Transparency International Corruption Perceptions Index (0=highly corrupt, 100=very clean; ranked 26th in Africa)

33

Population (m) 88.38Strength of investor protection index (0 =unfavourable, 10=favourable; ranked 25th in Africa) 4.3

Mobile penetration (% of population with mobile access) 16.67% Logistics Performance Index: overall rank out of 155

countries (34th in Africa) 141

Urban population (% of total) 17.02% Democracy score (0=lowest, 10=highest) 1

Real GDP growth (compound average growth rate): 5-year forecast (2018)

6.38%Mo Ibrahim Index of African Governance (rank out of 52 countries)

33

Real GDP growth (compound average growth rate): 10-year historical (2003) 9.76%

Perceptions of governance – rule of law: percentile rank (0=lowest, 100=highest) 29.11

GDP per capita (US$): 5-year forecast (2018) US$677Perceptions of governance – regulatory quality: percentile rank (0=lowest, 100=highest) 18

Country wealth (1=low income, 2=lower middle, 3=upper middle, 4=high income (non-OECD), 5=high income (OECD))

1Quality of overall infrastructure (1=extremely underdeveloped, 7=extensive and efficient by international standards)

3.6

Literacy rate (total population %) 42.7% Corporate maximum tax rate (%) 30%

Source: The World Bank; OECD National Accounts; United Nations Population Division & World Urbanization Prospects; Oxford Economics; ITU International; Transparency International; International Bank for Reconstruction and Development; Polity IV Project; Mo Ibrahim Index of African Governance; Worldwide Governance Indicators; WEF Global Competitiveness Report; Worldwide Corporate Tax Guide

Ethiopia

Zemedeneh Negatu

EY Country Leader

Tel: + 251 11 550 4933 Email: [email protected]

7

Ethiopia’s top 10 project investors since 2007Countries are ranked by most new projects (2007–12).The top investors show a diverse investment focus toward manufacturing-led activity, while the US’s capital flowed toward resource extraction and the UAE’s toward real estate construction.

Source: All diagrams on this page have been sourced from fDi Markets and EY analysis.

Top sectors

Ethiopia’s investment into top sectors (2007–12) by most projects

(Total = 69)

Food and tobacco, professional services, textiles and automotives accounted for 54% of project activity.

Ethiopia’s investment into top sectors (2007–12) by most capital invested

(Total = US$4,833m)

FDI trends in Ethiopia

Capital invested FDI (US$m) Jobs created by FDI

2003 2004 2005 2006 2008 2009 2010 2011 20122007

77

995

33

200

20

1,350

9671

1,123 1,310

321 290630

2,630

6,656

441

1,3601,507

8

762

2,390

21

3

1

10 10

8 8

20

13

New projects Capital invested Jobs created5.4% -28.7% -32.5%% CAGR (2007–12)

New projects FDI

Ethiopia’s inflow of investment of FDI since 2003Ethiopia received 1.6% of Africa’s total FDI for new projects and 0.8% of capital invested since 2007.Nearly 43% of capital invested into Ethiopia went into manufacturing activities. Food and tobacco, textiles, ICT and automotives are the major sector beneficiaries of FDI projects.

Jobs created by FDICapital invested FDI (US$m)

India USA China UAE UK Turkey Egypt Kenya NigeriaGermany

609

4,657

774

1,165

368

4,182

3,362

1,240

667

5,094

112117 45 19252 182 165

443458

2,013

16

13

10

6

4

2 222

3

New projects FDI

Ethiopia’s top 5 investors for FDI new project since 2007 (total = 69)

India 23%

Other investors 29%

Germany 6%

UAE 9%United States 19%

China 14%

Ethiopia’s top 5 investors for FDI capital invested since 2007 (total = US$4,833m)

India 12%

Germany 9%

China 8%

Other investors 13%

UAE 42%

United States 16%

Real estate30%

Food and tobacco 16%

Coal, oil and natural gas 12%

Communications8%

Textiles8%

Other sectors28%

Food and tobacco18%

Automotive OEM7%Metals

6%

Other sectors 46%

Financial services 13%

Textiles 10%

8

Ethiopia’s top investors by their top sector FDI investments since 2007Investor countries are ranked by most new projects 2007–12.These top investors contribute to 71% of all project activity and 87% of capital invested into Ethiopia since 2007.

Ethiopia’s FDI outlook

FDI outlook

2000 2013 2018 Comments

Natural resourcesGold reserves and the potential for commercial development in natural gas, iron ore and oil

reserves provide growing interest for investors.

LabourWorking population is growing rapidly and cost of labour remains low. Education and literacy rates are relatively poor but are improving.

Market sizeStill a small economy in absolute terms, but sustained and rapid growth, coupled with a large population, makes this a market with significant potential.

Infrastructure Infrastructure levels are rapidly improving, with substantial investments being made.

BureaucracyBureaucracy is a challenge to business, although improvements are being made (Ethiopia ranks in the 3rd quartile in the World Bank's Doing Business Index, ahead of Brazil and

India).

Political environment

The handover of power following the passing of Meles Zenawi has been smooth, and the

political environment remains stable. Ethiopia is a nominal democracy, although power has generally been concentrated in a dominant ruling party.

Overall outlook for FDINatural resources, a large population and a rapidly growing economy, with particular emphasis on manufacturing capacity and agribusiness opportunities, will attract increasing

levels of FDI.

Source: Oxford Economics; EY analysis

Very unattractive Unattractive Average Attractive Very attractive for FDI

Jobs created by FDICapital invested FDI (US$m)

Text

iles

Food

and

toba

cco

Fina

ncia

l ser

vice

s

Alte

rnat

ive

/ re

new

able

ene

rgy

Aut

omot

ive

OEM

Food

and

toba

cco

Soft

war

e an

d IT

ser

vice

s

Busi

ness

ser

vice

s

Coal

, oil

and

natu

ral g

as

Beve

rage

s

Aut

omot

ive

OEM

Non

-aut

omot

ive

tran

spor

t OEM

Text

iles

Cera

mic

s an

d gl

ass

Met

als

Real

est

ate

Com

mun

icat

ions

Tran

spor

tatio

n

Chem

ical

s

1,98

9

317

1,51

7

19 34

80 66 72

993

115

577

15 30 14 26

557

221

37

189

169

2,11

6

67

404

67

1,26

7

15 37 14

103

1,47

0

3,00

0

351

97

168

112 22

8

131 22

1

1,09

2

India China UAE GermanyUnited States

6% projects/ 9.5% capital

Food

and

toba

cco

100

9% projects/42% capital14.5% projects/8% capital19% projects/16% capital23% projects/13% capital

4 4

2

1 1

3

2 2

1 1

4

1 1 1

2

1 1 1

2

1

New projects FDI

Source: fDi Markets; EY analysis.

9

Project numberCapital value (US$m)

1200

2400

3600

4800

Power plantsand transmission

grids

Commercialconstruction

Airports Industrialconstruction

Roads andbridges

Rail

4,368

3,827

5

147

4

6

2

133

2

751

2

194

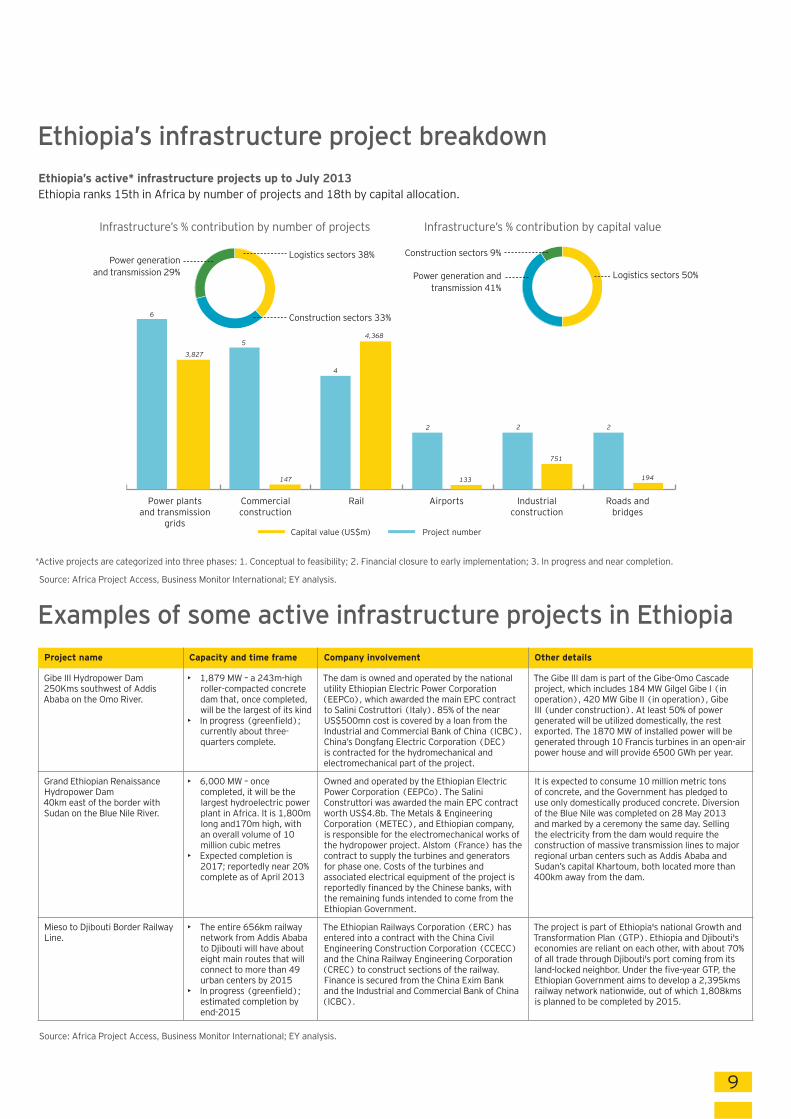

Ethiopia’s active* infrastructure projects up to July 2013Ethiopia ranks 15th in Africa by number of projects and 18th by capital allocation.

Ethiopia’s infrastructure project breakdown

Examples of some active infrastructure projects in Ethiopia

Project name Capacity and time frame Company involvement Other details

Gibe III Hydropower Dam250Kms southwest of Addis Ababa on the Omo River.

• 1,879 MW – a 243m-high roller-compacted concrete dam that, once completed, will be the largest of its kind

• In progress (greenfield); currently about three-quarters complete.

The dam is owned and operated by the national utility Ethiopian Electric Power Corporation (EEPCo), which awarded the main EPC contract to Salini Costruttori (Italy). 85% of the near US$500mn cost is covered by a loan from the Industrial and Commercial Bank of China (ICBC). China’s Dongfang Electric Corporation (DEC) is contracted for the hydromechanical and electromechanical part of the project.

The Gibe III dam is part of the Gibe-Omo Cascade project, which includes 184 MW Gilgel Gibe I (in operation), 420 MW Gibe II (in operation), Gibe III (under construction). At least 50% of power generated will be utilized domestically, the rest exported. The 1870 MW of installed power will be generated through 10 Francis turbines in an open-air power house and will provide 6500 GWh per year.

Grand Ethiopian Renaissance Hydropower Dam40km east of the border with Sudan on the Blue Nile River.

• 6,000 MW – once completed, it will be the largest hydroelectric power plant in Africa. It is 1,800m long and170m high, with an overall volume of 10 million cubic metres

• Expected completion is 2017; reportedly near 20% complete as of April 2013

Owned and operated by the Ethiopian Electric Power Corporation (EEPCo). The Salini Construttori was awarded the main EPC contract worth US$4.8b. The Metals & Engineering Corporation (METEC), and Ethiopian company, is responsible for the electromechanical works of the hydropower project. Alstom (France) has the contract to supply the turbines and generators for phase one. Costs of the turbines and associated electrical equipment of the project is reportedly financed by the Chinese banks, with the remaining funds intended to come from the Ethiopian Government.

It is expected to consume 10 million metric tons of concrete, and the Government has pledged to use only domestically produced concrete. Diversion of the Blue Nile was completed on 28 May 2013 and marked by a ceremony the same day. Selling the electricity from the dam would require the construction of massive transmission lines to major regional urban centers such as Addis Ababa and Sudan’s capital Khartoum, both located more than 400km away from the dam.

Mieso to Djibouti Border Railway Line.

• The entire 656km railway network from Addis Ababa to Djibouti will have about eight main routes that will connect to more than 49 urban centers by 2015

• In progress (greenfield); estimated completion by end-2015

The Ethiopian Railways Corporation (ERC) has entered into a contract with the China Civil Engineering Construction Corporation (CCECC) and the China Railway Engineering Corporation (CREC) to construct sections of the railway. Finance is secured from the China Exim Bank and the Industrial and Commercial Bank of China (ICBC).

The project is part of Ethiopia's national Growth and Transformation Plan (GTP). Ethiopia and Djibouti's economies are reliant on each other, with about 70% of all trade through Djibouti's port coming from its land-locked neighbor. Under the five-year GTP, the Ethiopian Government aims to develop a 2,395kms railway network nationwide, out of which 1,808kms is planned to be completed by 2015.

Infrastructure’s % contribution by capital value

Construction sectors 9%

Power generation andtransmission 41%

Logistics sectors 50%

Infrastructure’s % contribution by number of projects

Construction sectors 33%

Logistics sectors 38%Power generation

and transmission 29%

*Active projects are categorized into three phases: 1. Conceptual to feasibility; 2. Financial closure to early implementation; 3. In progress and near completion.

Source: Africa Project Access, Business Monitor International; EY analysis.

Source: Africa Project Access, Business Monitor International; EY analysis.

10

South Sudan

Tanzania

KenyaUganda

Ethiopia

Country overview

Kenya

Gitahi Gachahi

EY East Africa Regional Leader

Tel: + 254 20 271 5300 Email: [email protected]

Opportunity indicators Risk indicators

GDP (current) US$37.34bn Ease of doing business overall rank out of 184 countries (13th in Africa)

121

Population growth (annual) 2.72%Transparency International Corruption Perceptions Index (0=highly corrupt, 100=very clean; ranked 37th in Africa)

27

Population (m) 44Strength of investor protection index (0 =unfavourable, 10=favourable; ranked 19th in Africa)

5

Mobile penetration (% of population with mobile access) 67.49%

Logistics Performance Index: overall rank out of 155 countries (26th in Africa) 122

Urban population (% of total) 23.98% Democracy score (0=lowest, 10=highest) 8

Real GDP growth (compound average growth rate): 5-year forecast (2018)

5.72% Mo Ibrahim Index of African Governance (rank out of 52 countries)

25

Real GDP growth (compound average growth rate): 10-year historical (2003) 4.91%

Perceptions of governance – rule of law: percentile rank (0=lowest, 100=highest)

16.43

GDP per capita (US$): 5-year forecast (2018) US$1,209Perceptions of governance – regulatory quality: percentile rank (0=lowest, 100=highest) 47

Country wealth (1=low income, 2=lower middle, 3=upper middle, 4=high income (non-OECD), 5=high income (OECD))

1Quality of overall infrastructure (1=extremely underdeveloped, 7=extensive and efficient by international standards)

4

Literacy rate (total population %) 87.4% Corporate maximum tax rate (%) 30%

Source: The World Bank; OECD National Accounts; United Nations Population Division & World Urbanization Prospects; Oxford Economics; ITU International; Transparency International; International Bank for Reconstruction and Development; Polity IV Project; Mo Ibrahim Index of African Governance; Worldwide Governance Indicators; WEF Global Competitiveness Report; Worldwide Corporate Tax Guide

11

Kenya’s top 10 project investors since 2007Countries are ranked by most new projects (2007–12).Most of India and the US’s capital is directed toward manufacturing and electricity activity, while all the top investors have the majority of their project investments focused into marketing, support, financial and other professional services.

Source: All diagrams on this page have been sourced from fDi Markets and EY analysis.

Kenya’s top 5 investors for FDI new projects since 2007 (total = 207)

Kenya’s top 5 investors for FDI capital invested since 2007 (total = US$9,822m)Top sectors

Kenya’s investments into sectors (2007–12) by most projects

(Total = 207)

ICT, professional services, automotives and transport logistics remain key, attracting a third of all projects and nearly two-thirds of capital invested.

Kenya’s investments into sectors (2007–12) by most capital invested

(Total = US$9,822m)

FDI trends in Kenya

Capital invested FDI (US$m) Jobs created by FDI New project FDI

2003 2004 2005 2006 2008 2009 2010 2011 20122007

650

13 151213

9

23

29

34

5854

929579

275 174 332549

3,716

1,382

2,855

988

1,865 1,761

391

908

2,297

3,744

3,127

7,391

2,906

% CAGR (2007–12)New projects Capital invested Jobs created43.1 % 24.3% 26.2%

Kenya’s inflow of investment of FDI since 2003Kenya received 5% of Africa’s total FDI for new projects and 1.5% of capital invested since 2007.As the hub of East Africa, Kenya has seen robust investment growth, especially into manufacturing-led and consumer-facing activity. Kenya also has as one of the fastest growth rates of all investors of outward investments into Africa. Active exploration and successful finds have seen the resource sector attracting an increasing share of capital; 35% of the total since 2007.

Jobs created by FDICapital invested FDI (US$m) New project FDI

United States India UK South Africa Japan Togo France UAE South KoreaChina

762

29

24

22

14

11

98

7 7 7

2,175

3,702

6,617

725

3,497

106 217 167

1,250

162

742

75 135447 346 249 266

42

576

China 5%

Other investors 52%

India 38%

Other investors 30%

Mauritius 6%

United States 8%Israel 11%

UK 7%

United States 14%

India 11%

UK 11%

South Africa 7%

Coal, oil and natural gas 32%

Communications19%

Alternative/renewable energy

16%

Transportation4%

Financial services 4%

Other sectors25%

Communications17%

Business services10%Software and

IT services 9%

Transportation5%

Other sectors 42%

Financial services 17%

12

Kenya’s top investors by their top sector FDI investments since 2007Investor countries are ranked by most new projects 2007–12.These top investors contribute to 47% of all project activity and 56% of capital invested into Kenya since 2007.

Kenya’s FDI outlook

FDI outlook

2000 2013 2018 Comments

Natural resourcesKenya has historically lacked the natural resources that makes many other African economies attractive. However, the recent discovery of oil in the northwestern Turkana

region by Tullow may change that.

LabourA rapidly growing working population, a good-quality system of education and a relatively

efficient labour market makes Kenya attractive from a labour perspective.

Market sizeThe absolute size of the economy is relatively small, but a large population and rising GDP

per capita levels offer growth potential.

InfrastructureLack of investment funds has limited spending on infrastructure to date, but investment levels should rise over the next decade.

BureaucracySignificant levels still remain, which hinders business. Although Kenya is well positioned compared with many other African countries, only modest improvements in recent years

may be cause for concern.

Political environmentProgress has been made in embedding democratic institutions and processes. The

successful and peaceful presidential election provides cause for optimism.

Overall outlook for FDI

Kenya is already established as a gateway to the East Africa region, and this status will

be reinforced as the region continues to grow and as levels of infrastructure and the

institutional environment continue to improve. Oil discoveries in Kenya and the region as a whole will provide an accelerator for growth.

Source: Oxford Economics; EY analysis

Very unattractive Unattractive Average Attractive Very attractive for FDI

Jobs created by FDICapital invested FDI (US$m) New project FDI

83

393

24 48 38104 150

900

63133

300

41

461

1,292

19

323

155

24

235 279 246

104 79

520

23 47 25139 101

443

68131

272

1,543

38 6818 38 15 31 19 34

99

527

8 15 39

2,025

2,618

7

4 4 4

3

1

5

3 3

2 2

1

5

3 3 3

2

1

4

3

2 2

5

1 1

Soft

war

e an

d IT

ser

vice

s

Busi

ness

ser

vice

s

Com

mun

icat

ions

Beve

rage

s

Fina

ncia

l ser

vice

s

Alte

rnat

ive

/ re

new

able

ene

rgy

Com

mun

icat

ions

Busi

ness

ser

vice

s

Aut

omot

ive

OEM

Soft

war

e an

d IT

ser

vice

s

Coal

, oil

and

natu

ral g

as

Chem

ical

s

Fina

ncia

l ser

vice

s

Soft

war

e an

d IT

ser

vice

s

Busi

ness

ser

vice

s

Hea

lth c

are

Tran

spor

tatio

n

Met

als

Fina

ncia

l ser

vice

s

Busi

ness

ser

vice

s

Soft

war

e an

d IT

ser

vice

s

Com

mun

icat

ions

Aut

omot

ive

OEM

Cons

umer

ele

ctro

nics

Non

-aut

omot

ive

tran

spor

t OEM

United States South Africa JapanIndia

14% projects/8% capital 12% projects/38% capital 11% projects/7% capital

UK

7% projects/1% capital 4% projects/ 2% capital

161

Source: fDi Markets; EY analysis.

13

Project numberCapital value (US$m)

Power plants and

transmissiongrids

Roads andbridges

WaterRailAirports Health careCommercialconstruction

Industrialconstruction

Ports

5,431

17,590

2,714

4,991

1,303341 440 745

100

31

12

8

6

43

2 21

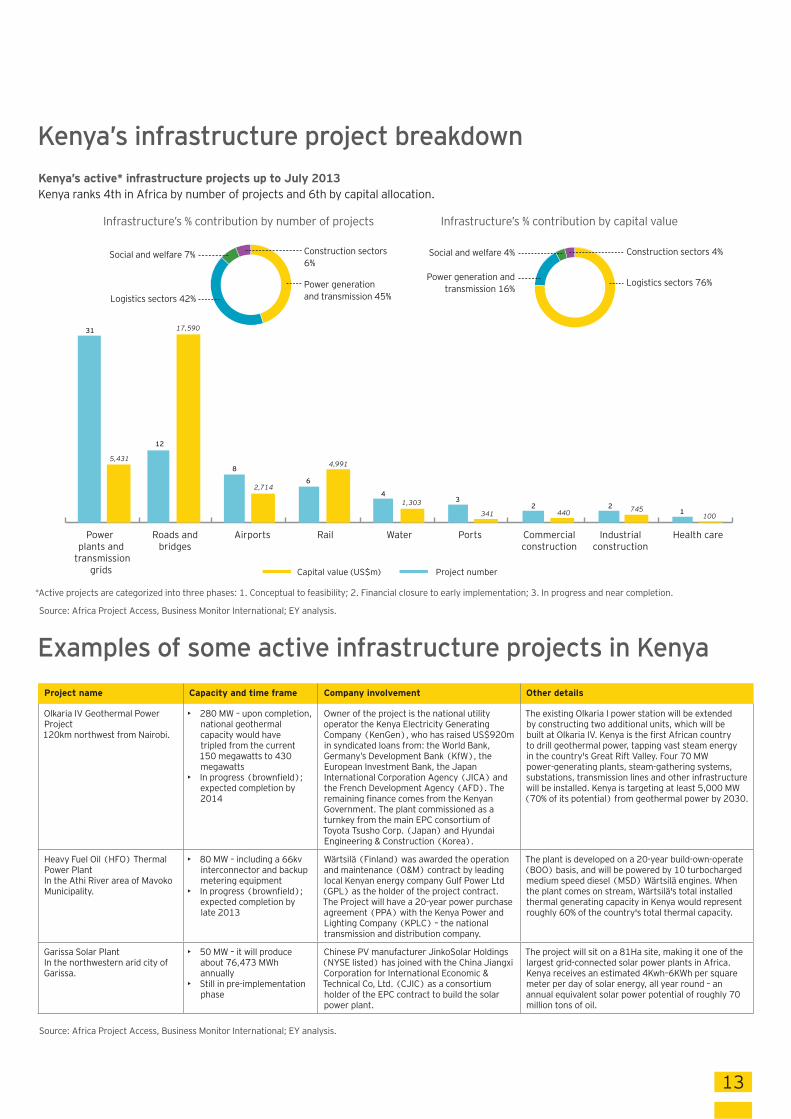

Kenya’s active* infrastructure projects up to July 2013Kenya ranks 4th in Africa by number of projects and 6th by capital allocation.

Kenya’s infrastructure project breakdown

Examples of some active infrastructure projects in Kenya

Project name Capacity and time frame Company involvement Other details

Olkaria IV Geothermal Power Project120km northwest from Nairobi.

• 280 MW – upon completion, national geothermal capacity would have tripled from the current 150 megawatts to 430 megawatts

• In progress (brownfield); expected completion by 2014

Owner of the project is the national utility operator the Kenya Electricity Generating Company (KenGen), who has raised US$920m in syndicated loans from: the World Bank, Germany’s Development Bank (KfW), the European Investment Bank, the Japan International Corporation Agency (JICA) and the French Development Agency (AFD). The remaining finance comes from the Kenyan Government. The plant commissioned as a turnkey from the main EPC consortium of Toyota Tsusho Corp. (Japan) and Hyundai Engineering & Construction (Korea).

The existing Olkaria I power station will be extended by constructing two additional units, which will be built at Olkaria IV. Kenya is the first African country to drill geothermal power, tapping vast steam energy in the country's Great Rift Valley. Four 70 MW power-generating plants, steam-gathering systems, substations, transmission lines and other infrastructure will be installed. Kenya is targeting at least 5,000 MW (70% of its potential) from geothermal power by 2030.

Heavy Fuel Oil (HFO) Thermal Power PlantIn the Athi River area of Mavoko Municipality.

• 80 MW – including a 66kv interconnector and backup metering equipment

• In progress (brownfield); expected completion by late 2013

Wärtsilä (Finland) was awarded the operation and maintenance (O&M) contract by leading local Kenyan energy company Gulf Power Ltd (GPL) as the holder of the project contract. The Project will have a 20-year power purchase agreement (PPA) with the Kenya Power and Lighting Company (KPLC) – the national transmission and distribution company.

The plant is developed on a 20-year build-own-operate (BOO) basis, and will be powered by 10 turbocharged medium speed diesel (MSD) Wärtsilä engines. When the plant comes on stream, Wärtsilä's total installed thermal generating capacity in Kenya would represent roughly 60% of the country's total thermal capacity.

Garissa Solar PlantIn the northwestern arid city of Garissa.

• 50 MW – it will produce about 76,473 MWh annually

• Still in pre-implementation phase

Chinese PV manufacturer JinkoSolar Holdings (NYSE listed) has joined with the China Jiangxi Corporation for International Economic & Technical Co, Ltd. (CJIC) as a consortium holder of the EPC contract to build the solar power plant.

The project will sit on a 81Ha site, making it one of the largest grid-connected solar power plants in Africa. Kenya receives an estimated 4Kwh–6KWh per square meter per day of solar energy, all year round – an annual equivalent solar power potential of roughly 70 million tons of oil.

Infrastructure’s % contribution by capital value

Construction sectors 4%Social and welfare 4%

Power generation andtransmission 16%

Logistics sectors 76%

Infrastructure’s % contribution by number of projects

Power generation and transmission 45%

Construction sectors 6%

Logistics sectors 42%

Social and welfare 7%

*Active projects are categorized into three phases: 1. Conceptual to feasibility; 2. Financial closure to early implementation; 3. In progress and near completion.

Source: Africa Project Access, Business Monitor International; EY analysis.

Source: Africa Project Access, Business Monitor International; EY analysis.

14

South Sudan

Tanzania

KenyaUganda

Ethiopia

Country overview

South Sudan

Key factors1. South Sudan control 75% of daily oil production (Sudan has been the 3rd largest sub-Saharan Africa oil producer)

2. Until January 2012, oil production accounted for 98 percent of the government’s revenues

3. The U.S. government’s long-standing sanctions against the Sudan were officially removed from applicability to South Sudan in December 2011

4. Strong reserves of copper, gold and tin

5. South Sudan has received more than US$4bn foreign aid since 2005 and Government revenues are remain largely dependent on foreign aid. Government is burdened with large levels of debt

6. Insecure property rights and weak price signal given markets are not organised

7. Factors inhibiting investment in South Sudan include limited physical infrastructure, a lack of both skilled and unskilled labour (has fewer than 400 kilometers of paved roads, despite the existence of three power plants, none of which are working at full capacity, the country is almost completely reliant on diesel-run generators for electricity) and Foreign exchange market rules and regulations are highly restrictive

Opportunity indicators NOTE

GDP (current) US$13.8bn

Population growth (annual) 4.1%

Population (m) 11

Mobile penetration (% of population with mobile access) 20%

Urban population (% of total) 33.2%

Real GDP growth (compound average growth rate): forecast 5 year (2018) 2.75%

Real GDP growth (compound average growth rate): historical 10 year (2003) -11.35% A, B

GDP per capita (US$): forecast 5 year (2018) US$4,336

Country wealth (1=low income, 2=lower middle, 3=upper middle, 4=high income (non-OECD), 5=high income (OECD)) n/a

Literacy rate (total population %) 27%

NOTE:A. Independence on 9 July 2011;B. Gross Domestic Product (GDP) in South Sudan contracted by 55.80% in 2012 from the previous year given an oil transit fee conflict

with Sudan

Gitahi Gachahi

EY East Africa Regional Leader

Tel: + 254 20 271 5300 Email: [email protected]

15

South Sudan

Tanzania

KenyaUganda

Ethiopia

TanzaniaCountry overview

Joseph Sheffu

Country Leader

Tel: +255 22 2667227 Email: [email protected]

Opportunity indicators Risk indicators

GDP (current) US$28.25bnEase of doing business overall rank out of 184 countries (18th in Africa) 134

Population growth (annual) 3.12%Transparency International Corruption Perceptions Index (0=highly corrupt, 100=very clean; ranked 22nd in Africa)

35

Population (m) 49.3 Strength of investor protection index (0 =unfavourable, 10=favourable; ranked 22nd in Africa)

5

Mobile penetration (% of population with mobile access) 55.53%

Logistics Performance Index: overall rank out of 155 countries (12th in Africa) 88

Urban population (% of total) 26.74% Democracy score (0=lowest, 10=highest) 2

Real GDP growth (compound average growth rate): forecast 5 year (2018)

6.47% Mo Ibrahim Index of African Governance: (rank out of 52 countries)

10

Real GDP growth (compound average growth rate): historical 10 year (2003)

6.95% Perceptions of governance – rule of law: percentile rank (0=lowest, 100=highest) 48.83

GDP per capita (US$): forecast 5 year (2018) US$934Perceptions of governance – regulatory quality: percen-tile rank (0=lowest, 100=highest) 56

Country wealth (1=low income, 2=lower middle, 3=upper middle, 4=high income (non-OECD), 5=high income (OECD))

1Quality of overall infrastructure (1=extremely under-developed, 7=extensive and efficient by international standards)

3.1

Literacy rate (total population %) 69.4% Corporate maximum tax rate (%) 30%

Source: The World Bank; OECD National Accounts; United Nations Population Division & World Urbanization Prospects; Oxford Economics; ITU International; Transparency International; International Bank for Reconstruction and Development; Polity IV Project; Mo Ibrahim Index of African Governance; Worldwide Governance Indicators; WEF Global Competitiveness Report; Worldwide Corporate Tax Guide

16

Tanzania’s top 10 project investors since 2007Countries are ranked by most new projects (2007–12).Nearly half of the UK’s capital investments and 20% of their project interests goes towards resources. Manufacturing of beverages and alternative energy too attracts a third of their project focus. The rest of the interest is similarly diverse as those from Kenya, India and South Africa’s – with a particular focus on professional services.

Source: All diagrams on this page have been sourced from fDi Markets and EY analysis.

Tanzania’s top 5 investors for FDI new projects since 2007 (total = 128)

Tanzania’s top 5 investors for FDI capital invested since 2007 (total = US$9,452m)Top sectors

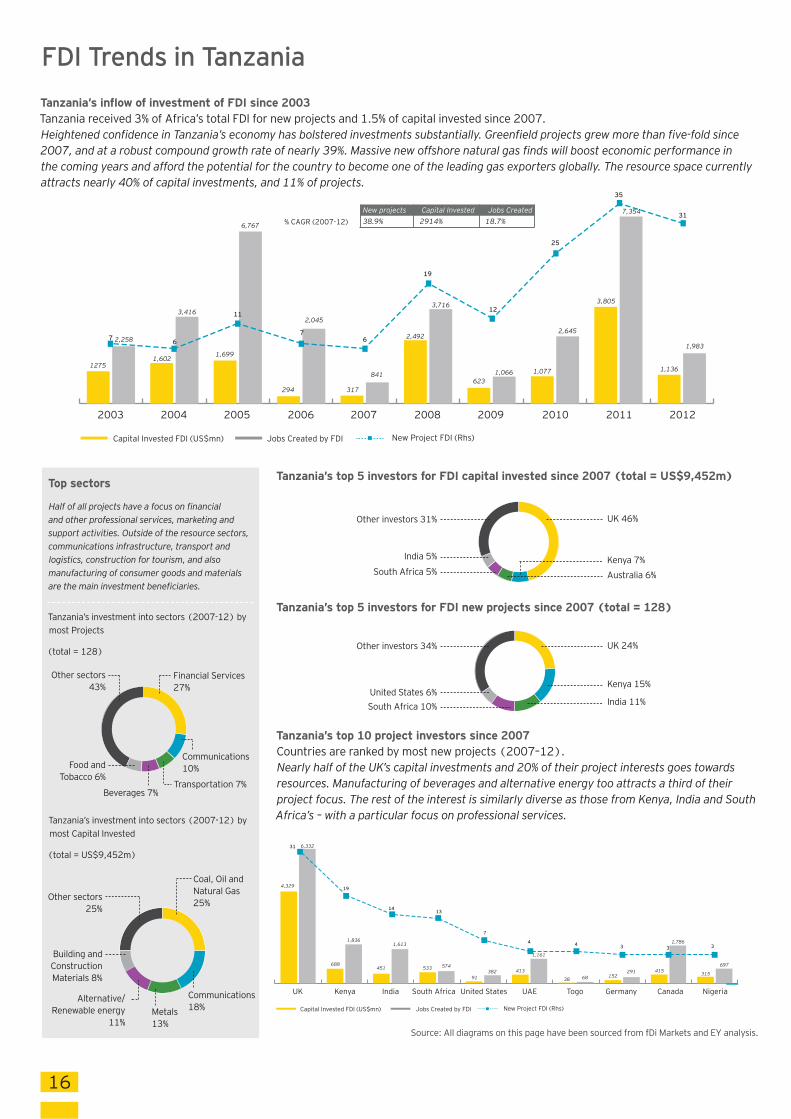

Tanzania’s investment into sectors (2007-12) by most Projects

(total = 128)

Half of all projects have a focus on financial and other professional services, marketing and support activities. Outside of the resource sectors, communications infrastructure, transport and logistics, construction for tourism, and also manufacturing of consumer goods and materials are the main investment beneficiaries.

Tanzania’s investment into sectors (2007-12) by most Capital Invested

(total = US$9,452m)

FDI Trends in Tanzania

Capital Invested FDI (US$mn) Jobs Created by FDI New Project FDI (Rhs)

% CAGR (2007-12)

2003 2004 2005 2006 2008 2009 2010 2011 20122007

1275

7 6

11

76

19

12

25

35

31

2,258

1,602

3,416

1,699

6,767

2,045

841

3,716

1,066623

2,492

1,077

3,805

2,645

7,354

1,136

1,983

317294

New projects Capital Invested Jobs Created38.9% 2914% 18.7%

Tanzania’s inflow of investment of FDI since 2003Tanzania received 3% of Africa’s total FDI for new projects and 1.5% of capital invested since 2007.Heightened confidence in Tanzania’s economy has bolstered investments substantially. Greenfield projects grew more than five-fold since 2007, and at a robust compound growth rate of nearly 39%. Massive new offshore natural gas finds will boost economic performance in the coming years and afford the potential for the country to become one of the leading gas exporters globally. The resource space currently attracts nearly 40% of capital investments, and 11% of projects.

Jobs Created by FDICapital Invested FDI (US$mn) New Project FDI (Rhs)

UK Kenya India South Africa UAE Togo Germany Canada NigeriaUnited States

4,329

31

19

1413

7

4 4 3 3 3

6,332

688

1,836

451

1,613

574382

1,161

6838

413152

415291

1,786

315

697

91

533

South Africa 10%

United States 6%

Other investors 34%

UK 46%Other investors 31%

India 5%

South Africa 5% Australia 6%

Kenya 7%

UK 24%

Kenya 15%

India 11%

Financial Services 27%

Transportation 7%Beverages 7%

Food and Tobacco 6%

Other sectors 43%

Communications10%

Coal, Oil and Natural Gas 25%

Communications18%Metals

13%

Alternative/Renewable energy

11%

Building and Construction Materials 8%

Other sectors25%

17

Tanzania’s top investors by their top sector FDI investments since 2007Investor countries are ranked by most new projects 2007–12.These top investors contribute to 66% of all project and 64% of capital invested into Tanzania since 2007.

Tanzania FDI outlook

Source: Oxford Economics and EY analysis

Very unattractive Unattractive Average Attractive Very attractive for FDI

Jobs Created by FDICapital Invested FDI (US$mn) New Project FDI (Rhs)

235

1,326

844 844

440

1774

565

35 90

1,498

79

319

8112

70 67

304

69

205

353

9943

207

35 54 25

200273

532

168112

3868 73

294

146

295

771

7

5

4 4

3

4 4

2 2 2 2 2

11

7

1

2

1

8

Beve

rage

s

Com

mun

icat

ions

Food

& T

obac

co

Coal

, Oil

and

Nat

ural

Gas

Cons

umer

Pro

duct

s

Hot

els

& To

uris

m

Non

Aut

omot

ive

Tran

spor

t OEM

Elec

tron

ic C

ompo

nent

s

Build

ing

& Co

nstr

uctio

n M

ater

ials

Tran

spor

tatio

n

Hea

lthca

re

Fina

ncia

l Ser

vice

s

Fina

ncia

l Ser

vice

s

Fina

ncia

l Ser

vice

s

Fina

ncia

l Ser

vice

s

Alte

rnat

ive/

Rene

wab

le e

nerg

y

Com

mun

icat

ions

Tran

spor

tatio

n

Min

eral

s

UK India South Africa United StatesKenya24% Projects / 46% Capital 15% Projects / 7% Capital 11% Projects / 5% Capital 10% Projects / 5.5% Capital 5.5% Projects / 1% Capital

Source: fDi Markets, and EY analysis.

FDI outlook

2000 2013 2018 Comments

Natural resourcesSome gold reserves and growing levels of optimism about offshore gas fields.

LabourRapidly growing working population and rising literacy levels remain attractive.

Market sizeAmong the fastest growing economies in the world with a sizable population, although GDP per capita levels remain low.

InfrastructureLack of investment funds has limited spending on infrastructure to date, but the new IMF–

backed plan should see improvements over the next five years.

BureaucracySignificant amounts remain, which hinders business.

Political environmentThe political situation is relatively stable and corruption is being actively tackled.

Overall outlook for FDIAn increasingly attractive outlook , with rapid growth, attractive natural resource base, and improving governance.

18

Project numberCapital value (US$mn)

Power plantsand transmission

grids

IndustrialConstruction

PortsOil & Gas Pipelines

Healthcare ResidentialConstruction

AirportsRoads & Bridges

Rail

3,513

6391,100

138

9,200

65

65011 1 11,000

2

6

3 3

12

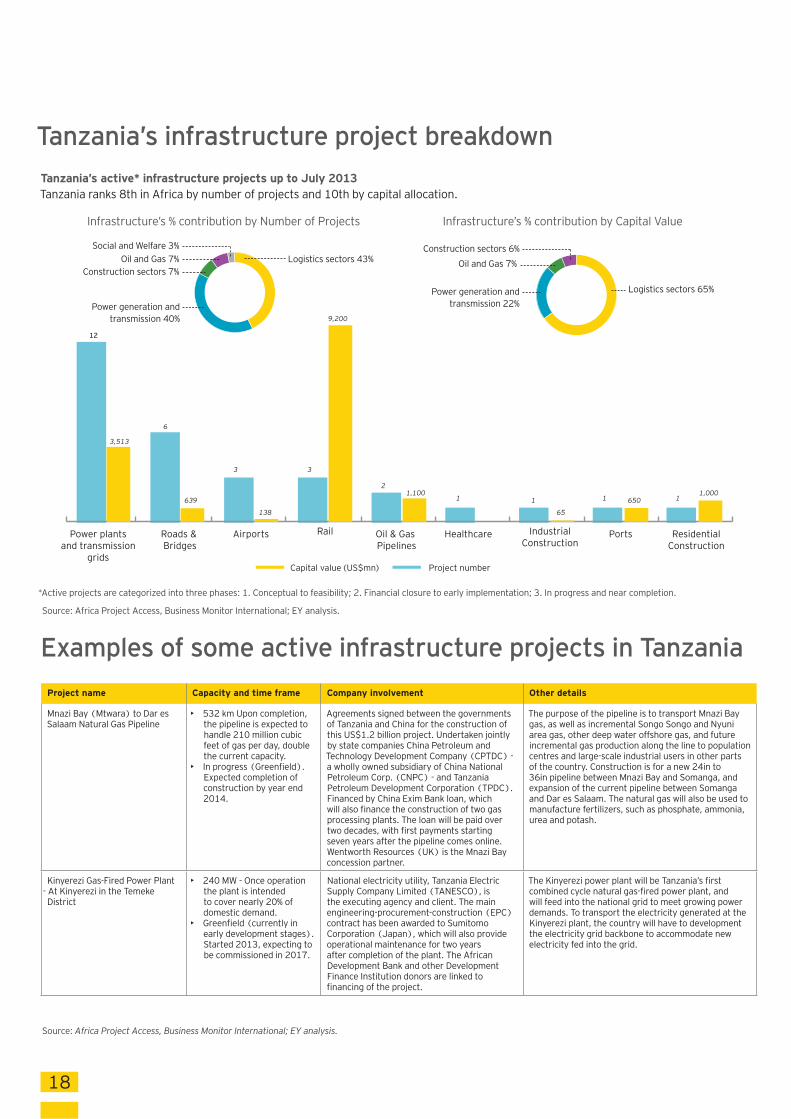

Tanzania’s active* infrastructure projects up to July 2013Tanzania ranks 8th in Africa by number of projects and 10th by capital allocation.

Tanzania’s infrastructure project breakdown

Examples of some active infrastructure projects in Tanzania

Project name Capacity and time frame Company involvement Other details

Mnazi Bay (Mtwara) to Dar es Salaam Natural Gas Pipeline

• 532 km Upon completion, the pipeline is expected to handle 210 million cubic feet of gas per day, double the current capacity.

• In progress (Greenfield). Expected completion of construction by year end 2014.

Agreements signed between the governments of Tanzania and China for the construction of this US$1.2 billion project. Undertaken jointly by state companies China Petroleum and Technology Development Company (CPTDC) - a wholly owned subsidiary of China National Petroleum Corp. (CNPC) - and Tanzania Petroleum Development Corporation (TPDC). Financed by China Exim Bank loan, which will also finance the construction of two gas processing plants. The loan will be paid over two decades, with first payments starting seven years after the pipeline comes online. Wentworth Resources (UK) is the Mnazi Bay concession partner.

The purpose of the pipeline is to transport Mnazi Bay gas, as well as incremental Songo Songo and Nyuni area gas, other deep water offshore gas, and future incremental gas production along the line to population centres and large-scale industrial users in other parts of the country. Construction is for a new 24in to 36in pipeline between Mnazi Bay and Somanga, and expansion of the current pipeline between Somanga and Dar es Salaam. The natural gas will also be used to manufacture fertilizers, such as phosphate, ammonia, urea and potash.

Kinyerezi Gas-Fired Power Plant - At Kinyerezi in the Temeke District

• 240 MW - Once operation the plant is intended to cover nearly 20% of domestic demand.

• Greenfield (currently in early development stages). Started 2013, expecting to be commissioned in 2017.

National electricity utility, Tanzania Electric Supply Company Limited (TANESCO), is the executing agency and client. The main engineering-procurement-construction (EPC) contract has been awarded to Sumitomo Corporation (Japan), which will also provide operational maintenance for two years after completion of the plant. The African Development Bank and other Development Finance Institution donors are linked to financing of the project.

The Kinyerezi power plant will be Tanzania’s first combined cycle natural gas-fired power plant, and will feed into the national grid to meet growing power demands. To transport the electricity generated at the Kinyerezi plant, the country will have to development the electricity grid backbone to accommodate new electricity fed into the grid.

Infrastructure’s % contribution by Number of Projects Infrastructure’s % contribution by Capital Value

Oil and Gas 7%

Logistics sectors 65%

Logistics sectors 43%

Power generation andtransmission 40%

Social and Welfare 3% Construction sectors 6%

Power generation andtransmission 22%

Oil and Gas 7%Construction sectors 7%

*Active projects are categorized into three phases: 1. Conceptual to feasibility; 2. Financial closure to early implementation; 3. In progress and near completion.

Source: Africa Project Access, Business Monitor International; EY analysis.

Source: Africa Project Access, Business Monitor International; EY analysis.

19

South Sudan

Tanzania

KenyaUganda

Ethiopia

UgandaCountry overviewCountry overview

Muhammed Ssempijja

Country Leader

Tel: +256 414 343 520 Email: [email protected]

Opportunity indicators Risk indicators

GDP (current) US$19.88bnEase of doing business overall rank out of 184 coun-tries (12th in Africa)

120

Population growth (annual) 3.19 %Transparency International Corruption Perceptions Index (0=highly corrupt, 100=very clean; ranked 35th in Africa)

29

Population (m) 36.84Strength of investor protection index (0 =unfavourable, 10=favourable; ranked 32nd in Africa) 4

Mobile penetration (% of population with mobile access)

48.38% Logistics Performance Index: overall rank out of 155 countries (N/A)

N/A

Urban population (% of total) 15.58% Democracy score (0=lowest, 10=highest) 1

Real GDP growth (compound average growth rate): forecast 5 year (2018) 6.38%

Mo Ibrahim Index of African Governance: (rank out of 52 countries) 19

Real GDP growth (compound average growth rate): historical 10 year (2003) 6.76%

Perceptions of governance – rule of law: percentile rank (0=lowest, 100=highest) 23

GDP per capita (US$): forecast 5 year (2018) US$870 Perceptions of governance – regulatory quality: percen-tile rank (0=lowest, 100=highest) 32

Country wealth (1=low income, 2=lower middle, 3=upper middle, 4=high income (non-OECD), 5=high income (OECD))

1Quality of overall infrastructure (1=extremely under-developed, 7=extensive and efficient by international standards)

3.4

Literacy rate (total population %) 66.8% Corporate maximum tax rate (%) 30%

Source: The World Bank; OECD National Accounts; United Nations Population Division & World Urbanization Prospects; Oxford Economics; ITU International; Transparency International; International Bank for Reconstruction and Development; Polity IV Project; Mo Ibrahim Index of African Governance; Worldwide Governance Indicators; WEF Global Competitiveness Report; Worldwide Corporate Tax Guide

20

Uganda’s top 10 project investors since 2007Countries are ranked by most new projects (2007–12).Neighbouring Kenya is the main investor to Uganda’s landlocked economy, with just over half of its project investment directing into financial services, followed by a quarter share of projects into food manufacturing and retail activity. The UK’s capital is directed into the oil and gas space, split half between extractive means and processing activity.

Source: All diagrams on this page have been sourced from fDi Markets and EY analysis.

Uganda’s top 5 investors for FDI new project since 2007 (total = 120)

Uganda’s top 5 investors for FDI capital invested since 2007 (total = US$17,046m)Top sectors

Uganda’s investment into top sectors, (2007-12) by most Projects

(total = 120)

Financial and other professional services, marketing and support activities account for half of all projects, while manufacturing and retail activity contributes to another third of all project investments.

Uganda’s investment into top sectors, (2007-12)by most Capital Invested

(total = US$17,046m)

FDI Trends in Uganda

Capital Invested FDI (US$mn) Jobs Created by FDI New Project FDI (Rhs)

% CAGR (2007-12)

2003 2004 2005 2006 2008 2009 2010 2011 20122007

422

5 56

15

7

42

17

22

1517

1,179

36 189 69463

1,225

518

4,436

1,374

2,147

3,057

8,505

2,476

2,925

2,134

569

2,030

291374

New projects Capital Invested Jobs Created19,4% 14,3% 31,4%

Uganda’s inflow of investment of FDI since 2003Uganda received 2.7% of Africa’s total FDI new projects and 2.7% of capital invested since 2007.Uganda’s new oil and gas finds has spurred a lot of interests in the resource space, attracting 75% of all capital investments, and 13% of projects. The consumer-facing and consumer goods sectors, as well as the ICT space and manufacturing activity has underpinned growth and investment in the non-resource economy.

Jobs Created by FDICapital Invested FDI (US$mn) New Project FDI (Rhs)

Kenya UK South Africa India UAE France United States Japan ChinaNigeria

2,601

34

18

119

8 7

54

32

2,695

9,317

3,409

902 782 573271

509704778

151 76 28

1,073

166 104128393

1,042

Nigeria 7%India 8%

Other investors 33%

UK 55%

Other investors 13%

South Africa 5%France 5%

Mauritius 7%

Kenya 15%

Kenya 28%

UK 15%

South Africa 9%

Coal, Oil and Natural Gas

9%

Communications13%

Food and Tobacco10%

Transportation5%

Other sectors 30%

Other sectors 30%

Financial Services 33%

Coal, Oil and Natural Gas 73%

Communications12%

Transportation 3%

Financial Services 2%

Other sectors8%

Food and Tobacco2%

21

Uganda’s top investors by their top sector FDI investments since 2007Investor countries are ranked by most new projects 2007–12.These top investors contribute to 68% of all project and 85% of capital invested into Uganda since 2007.

Uganda FDI outlook

Very unattractive Unattractive Average Attractive Very attractive for FDI

Jobs Created by FDICapital Invested FDI (US$mn) New Project FDI (Rhs)

169 306 280

1,786

1,819161 168 112

9,045

2,822

133 29327

839

250 52 219 59 235 60 10 9 26351

97799

118459

12 103 43 207 5128300

28 51 23

18

9

11

7

3

1

7

1 1

3

2 2

6

1 1 1 1

4

Fina

ncia

l Ser

vice

s

Fina

ncia

l Ser

vice

s

Fina

ncia

l Ser

vice

s

Fina

ncia

l Ser

vice

s

Alte

rnat

ive/

Rene

wab

le E

nerg

y

Com

mun

icat

ions

Com

mun

icat

ions

Com

mun

icat

ions

Com

mun

icat

ions

Hea

lthca

re

Food

& T

obac

co

Coal

, Oil

and

Nat

ural

Gas

Coal

, Oil

and

Nat

ural

Gas

Coal

, Oil

and

Nat

ural

Gas

Beve

rage

s

Tran

spor

tatio

n

Tran

spor

tatio

n

Fina

ncia

l Ser

vice

s

Cons

umer

Pro

duct

s

Kenya South Africa India Nigeria MauritiusUK28% Projects / 15% Capital 15% Projects / 55% Capital 9% Projects / 5% Capital 7.5% Projects / 2% Capital 2% Projects / 7% Capital7% Projects / 1% Capital

Source: fDi Markets, and EY analysis.

FDI outlook

2000 2013 2018 Comments

Natural resourcesThere are increasing levels of interest in Uganda’s oil reserves, with production expected to come online in 2016.

LabourA relatively well-educated population with improving levels of education.

Market sizeThe economy is currently small, but high growth rates and a relatively large population offer

much potential and is also acting as a hub for other countries like South Sudan.

InfrastructureContinued improvement over previous decade, with good level of investment, albeit from a

low base.

BureaucracySignificant improvements have taken place and more is expected for years to come based

on focus on liberalization.

Political environmentElective representation and rule of law is strong although change of top leadership through the ballot is still a challenge.

Overall outlook for FDINatural resources which are a strong pull factor for FDI and good macroeconomic management are significant benefits.

22

Project numberCapital value (US$mn)

Power plantsand transmission

grids

WaterRoads andBridges

Rail Oil and GasPipelines

IndustrialConstruction

Ports Airports

7,116

2,532

7,246

618

721462

0

32

1

2,000

4

21

7

29

Uganda’s active* infrastructure projects up to July 2013Uganda ranks 5th in Africa by number of projects and 11th by capital allocation.

Uganda’s infrastructure project breakdown

Examples of some active infrastructure projects in Uganda

Infrastructure’s % contribution by Number of Projects Infrastructure’s % contribution by Capital Value

Oil and Gas pipelines 1%Social and Welfare 3%Construction sectors 10%

Power generation andtransmission 36%

Logistics sectors 50%Logistics sectors 44%

Construction sectors 1%

Power generation andtransmission 42%

Social and Welfare 10%Oil and Gas pipelines 3%

*Active projects are categorized into three phases: 1. Conceptual to feasibility; 2. Financial closure to early implementation; 3. In progress and near completion.

Source: Africa Project Access, Business Monitor International; EY analysis.

Source: Africa Project Access, Business Monitor International; EY analysis.

Project name Capacity and time frame Company involvement Other details

Bujagali Hydropower (Public-Private Partnership) Project

- Ugandan shores of the Victoria Nile (Dumbell Island) near Jinja.

• 250 MW - Full generating capacity achieved in 2012. It aims to produce 50% of the total national electric power demands.

• Financial close achieved in late 2007, and commissioned in 2012.

Bujagali Energy Limited (BEL) is a project-specific privately owned and managed company, which consists of the consortium of Sithe Global Power LLC (US) and Aga Khan for Economic Development (AKFED). The consortium provided US$190 million in funding. A syndicated group of donors provided the balance of US$610 million project finance. The client is the national electricity utility, the Uganda Electricity Transmission Company Limited (UETCL). The main engineering-procurement-construction (EPC) contract was awarded to Salini Costruttori (Italy).

Uganda’s Ministry of Energy and Mineral Development has been nominated for the World Finance Public Private Partnership Awards 2013 because of work on the Bujagali project, for excellence and innovation in the pre-delivery phases. In addition to mobilising private capital, the project promotes private sector ownership and management of the power sector. The project was developed as a turnkey on a build-own-operate-transfer (BOOT) basis with BEL, which included the construction of 100 km of transmission lines.

Tororo-Pakwach Rail Line Rehabilitation - Linking eastern to northern Uganda

• 500 km railway that has been out of operation for the last 18 years. Being fixed in tranches, the first addresses basic clearing and restoring the washed out areas due to flooding, installing new culverts, and re-railing of the track. The next tranche of overhaul work will then commences, which involves new rolling stock.

• Reopened in August 2013.

Rift Valley Railway (RVR), the current operators and concession holder of the Kenyan and Ugandan rail networks. Kato Contractors, a Ugandan engineering company is doing the initial clearing. Overhaul of wagons and locomotives is being funded by the DFI’s, led by the German Development Bank (KfW).

Under the recently launched National Transport Master Plan, the Government is to improve railway infrastructure with a standard gauge railway line. The project is crucial in linking trade routes strategically between Uganda and South Sudan. As political relations are mended between South Sudan and Khartoum, this rail route is expected to boost more trade as far up as Egypt. Upon completion, a 10-wagon train shall operate the route, which should come as a big boost to farmers, whose produce is not selling cheap because of middlemen and poor transport.

23

What are thereal problems?

Rapid population growth and demographic changes The African population has topped the 1bn mark or approximately 15% of the global total (this is set to rise to 30% by 2030). Rapid population growth set against a current lack of and/or age of infrastructure further exacerbates the infrastructure crisis (including spiralling costs of maintenance through use, etc.). A lack of infrastructure investment gives rise to questions of intergenerational parity, where future generations are lumbered with the costs arising from current decision making.

Population mobility Connecting the continent through infrastructure development and removing bottlenecks to greater mobility of people, will allow Africans to work together towards the common goal of developing the continent. There is good progress, Burundi, Kenya, Rwanda, Tanzania, and Uganda - have made some progress on integrating regionally in the East African Community (EAC) since 1999. These advances are critical, as integration would transform the five countries into potentially one coastal, regional economy and reduce transactional business costs.

The impact of changing population demographics on the provision of public services The potential costs of changing demographics are generally acknowledged but often little understood in detail. There are significant challenges to economies (and City budgets) that need to support younger (below the age of 49) population numbers in terms of employment creation, housing and other basic services (access to health, education, etc.). Africa is going through a process of rapid urbanization. The large majority of these new urbanites lives in unplanned, or informal, settlements. These rapid changes signify serious challenges for these communities (individuals) as well as for city authorities, who are faced with the task of providing the expanding populations with adequate infrastructures and services for water, sanitation and solid waste. Empirical evidence shows that a failure to respond to these needs has profound community impacts (social cohesion, urban poverty, etc.).

Responding to changes in population

demographics and social indicators

24

A lack of investment in diversified economic infrastructure creates sustainability risks

An over-reliance on a particular technology (power generation source, etc.) will make that economy vulnerable to the provision of those conditions (e.g. over reliance on Hydro-power makes that economy vulnerable to hydrological conditions).

Low current spending on infrastructure The experience of other developing countries shows that capital investment equivalent to about 25% of GDP is generally needed for a substantial rise in per capita income.

Increased cost of doing business Inadequate levels of existing infrastructure (particularly power and transport) increase the transaction costs of business in most African economies. There are no incentive structures to impact positively on market prices and therefore consumer welfare and transactional business costs.

Inefficient use of existing resources It is often the case that the efficiency of infrastructure programmes can be affected by overstaffing; high procurement costs (coupled with the potential of low quality) and fragmentation over a multitude of small projects.

Inadequate infrastructure frustrates continental integration ambitions To overcome the challenges of continental integration more focus should be given to complimentary cross-border infrastructure, ‘development corridors’ and shared regional standards deliver scale - and economies of scale – beyond the reach of individual country ambition.

Burdensome trade regulations ‘Red tape’ and the costs incurred through complicated border processes and bureaucratic bottlenecks, hinder economic, growth considerably by reducing access to global markets.

Inadequate infrastructure frustrates the promotion of inclusive and sustainable growth

Focussed investment in economic and social infrastructure has played a significant and positive role in the growth performance of fast growing economies (BRICS). Providing infrastructure for the economy and communities is one of the main ways a City will realise inclusive and jobs-rich growth. Affordable infrastructure of a high quality raises economic productivity, permits economic expansion and allows marginalised households and communities to take advantage of new opportunities. It also builds social capital; and raises living standards, as people have access to basic services.

There is currently a pronounced

infrastructure deficit

25

Providing a suitable enabling framework A suitable framework that allows for easy Private Sector entry and exit, or the right incentives for operation (sustaining Private Sector investment requires an active and well-performing Public Sector). The Private Sector conditions would include:

- Attractiveness and ‘bankability’

- Technical feasibility

- Potential economic impact

- Exemplary governance:

i. Quantifiable financial returns

ii. Strong legal and regulatory framework

iii. Funding for project preparation

iv. A positive economic impact

v. Strong stakeholder engagement

vi. Political will

Defining the role of the Public Sector

Delivering innovative approaches to sustainable infrastructure development as well as financing

Environmental awareness and unique country-specific considerations to the built environment are crucial to sustainable development and strong stakeholder engagement. Governments must proactively seek out innovative financing methods (including the use of efficiency gains from performance improvement, development of infrastructure bonds, combining grant and repayable finance methods to benefit from both options and risk diversification, etc.).

Creating adequate maintenance plans

Maintenance plans are crucial for sustainable infrastructure, both corrective and preventative.

26

27

A poor business environment

Inadequate cost recovery

Cost recovery provides the financial foundation for sector development (do tariffs and actual collections cover operational and maintenance costs, what about capital costs for service expansion, do charges encourage local and foreign entrants, where are government subsidies currently and do they need to be re-directed?

The impact of corruption: (including perceived)

Corruption has emerged as a top bottleneck to doing business on the continent.

Insufficient competition

The full benefits of competition are yet to be realised in most infrastructure sectors. In addition, there is a lack of stability due to unpredictable political interference, and insufficient information about future planning.

Low credibility of institutions

The low (including perceived) credibility of regulatory and judicial institutions. Regulatory credibility is undermined in some sectors because of conflicts of interest arising from inadequate separation between policy, regulatory, and operational functions. Effective regulatory decision making can be constrained, by limited regulatory capacity and experience.

1

28

Access to financing and the ability to fund

investment over time

Baseline country and East Africa spending needs

The continent’s infrastructure spending needs are enormously significant, recent studies demonstrate that about 40% of total spending needs are associated with power. Using their meager fiscal resources, African governments simply cannot keep up with spending requirements. A baseline study that determines priority infrastructure needs (responding to local conditions and potential for wider integration) associated to market attractiveness (revenue returning vs. revenue hungry) and its potential economic impact (job creation, economic diversification, regional integration, enhancing innovation, etc.) is crucial.

Understanding the impact of efficient use of current infrastructure to reduce the funding gap

A more efficient use of existing infrastructure can reduce the overall funding gap. In order to achieve this goal, policymakers must focus on reducing inefficiencies through measures such as rehabilitating existing infrastructure, targeting better subsidies and improving budget execution (and health) and physical infrastructure (transportation, power, and information and communication technologies). However, given the potential role of deeper financial markets and more developed capital markets in helping find the necessary resources for such investments, policymakers should also consider improving the infrastructure of the financial system, starting with the payments system.

Identify opportunities to finance and fund the remaining gap and other infrastructure opportunities

In setting up policies to finance the remaining infrastructure gap and other infrastructure opportunities, two areas need consideration:

• Engage, coordinate and leverage different sources of financing and funding - The long-term maturity of infrastructure projects and their large scale require different types of financiers, including Private Sector, bilateral and multilateral partners. Policymakers therefore need to engage and coordinate with many partners. One challenge will be to find ways to leverage aid flows so as to attract the private investment necessary.

• Financial Innovation - African policymakers will also need to create appropriate innovative financing solutions. So far, Private Sector investment has focused on areas such as mobile telephones, power plants and container terminals. In other areas, such as power, water and railways, the Private Sector has preferred the use of concessions and other types of contracts. Innovative financing can play a role in attracting Private Sector funds to these areas. Financing infrastructure projects is challenging because of the large size, long tenures and complexity of projects. In Africa, local banks, which dominate the financial sector, are not able to provide sufficient long-term finance. Untapped sources of funding are also relevant. The use of diaspora bonds (like those issued by Ethiopia) as well as the placement of infrastructure bonds to the diaspora (like those in Kenya). In project finance, solutions to mitigate credit risk could involve multilateral partners. It critical to consider investments in financial infrastructure. Generally, efforts are dedicated to investments in social infrastructure (water supply, sanitation, sewage disposal, education and health) and physical infrastructure (transportation, power, and information and communication technologies). However, given the potential role of deeper financial markets and more developed capital markets in helping find the necessary resources for such investments, policymakers should also consider improving the infrastructure of the financial system, starting with the payments system.

???

Financing is selecting the immediate source of cash that will physically develop the assets, with the repayment of this investment over the life of the asset. Governments have a wide range of financing solutions, both public and private, available to develop infrastructure. Private investors have demonstrated a willingness to participate in a wide range of financing solutions in respect of government infrastructure including.

The difference between funding and financing of infrastructure

Funding is the revenue stream that repays the financing. The funding of infrastructure can be considered as the allocation of ultimate cash flows that support the construction and operation of infrastructure.

Financing

Funding

The adverse impacts of climate change These changes are a major challenge to socio-economic development globally. The African continent, including the East African region, is particularly vulnerable to impacts of climate change affecting key economic drivers such as water resources, agriculture, energy, transport, health, forestry, wildlife, land and infrastructure. The impacts include; water stress and scarcity, food insecurity, diminished hydropower generation potential, loss of biodiversity and ecosystem degradation, increased incidence of disease burden, the crumbling of infrastructure, high costs of disaster management as a result of increased frequency and intensity of droughts, floods and landslides.

Infrastructure design and development Governments across Africa must consider the impact of infrastructure design and development on:

• The ecology

• The production of increased levels of greenhouse gases and other emissions to air

• Water resources and the overall water environment

• Materials used in the infrastructure build itself

• Land use (current and future)

The environmental impact of service delivery The global requirements, driven through regulation, are becoming more stringent and costly. These indicators are motivated and managed through policies and programmes and should be fundamental to any, and all, infrastructure footprint considerations. A change in population (service users, through urbanisation, etc.) can create an inadequate provision of solid and waste water disposal, increased air pollution, due to transport volumes and emission from processing factories, etc.

Responding to environmental factors

29

30

A model foreconomic development

31

Introducing our model

Economic development

Financial

managementCan you afford it?

6

Human capital

How do you attract the right people?

7Vision

What do you want to achieve?

1

Environment &

social indicators

Why do you need (want)to do it?

2

3Economic &

spatial indicators

Where do you do it and what impact will

it have?

Assess current

infrastructure

Where are you now?

4The role of the

Public Sector

How do you get this done correctly?

5

32

The details

Economic

Development

objectives

Economic

Diversification

Regional

Development

Improving

social

conditions

Job

creation

Enhancing

innovation

Investment

attratcion

Focus on

sectors with

higher value

added

Vision

A model of

economic

reform

EnvirSo

Indic

Ambitionvs Reality

Economicdevelopment

outcomes

Transparentaccountable &org. alignment

Localvs Africa

integration

Assess Current

InfrastructuDeficit

FinancialManagement

HumanCapital

Defining the Public sector

role

RapidUrbanisation

1

3

4

2 I

Local vsregional

integration

Community& stakeholderengagementCreating

effectivemaintenance

plans

Credibility

Innovation

Enabling frameworks

Private

Public

Corruption(perceived)

& politicalinterface

Fiscalin/dependable

FM policy

Treasurymanagement

Roles & responsibilities

Governance,culture & otherorganisational

capabilities

Organisationalcapabilities

Organisationalstructure

Allocation ofresources

Revenuemanagement

Balance sheet

management

Expenditure management

Financingvs funding

21 2024

23

3637

41

22

26

27

28

29

25

35

34

33

iv

iii

ii

i

i

ii iii

iv

3839

40

45

46

42

44

43

31

32

33

ronmentocialcators

Economic& Spatial Modelling

ure

5

6

7

8

9

10

11

mpacts ofclimate changes

Appropriate regulatoryframework

Socialcohesion

Socio-economic& spatial

assessment

Spatialtransportation

Need vs current

practice

Incentivestructures

Existingbarriers

Measuringthe benefits

of publicspending

12

13

14

15

16 17

18

19

1. Population growth2. Population mobility3. Population demographics4. Transport & congestion5. Water resources6. Energy7. Land use8. Monitoring & enforcement9. Labour force & employment profile10. Economic structure & trends11. Income distribution12. Personal income13. GDP14. Business output15. Wealth16. Current spending17. Spend efficiency18. Cost to business19. Burdensome trade regulations20. Development corridors and shared standards21. Diversified development22. Intergovernmental coordination23. Incentives for operations24. Entry/exit market mechanism25. Corrective plans26. Preventative plans27. Sustainability28. Financing & funding solutions29. Judicial system30. Regulatory systems31. Public funds

i. User chargesii. Current & future (borrowing) tax revenuesiii. Grant & donor fundingiv. Funds available through own means

(financial management)32. Private funds

i. Efficiency gainsii. Infrastructure bondsiii. Combined modellingiv. Traditional finance models (PPP, BOOT, etc.)

33. Effective cost recovery

34. Revenue enhancement initiatives and collections35. Asset/liability modelling36. Tariff management37. Tax base forecasting38. Cost control initiatives39. Maximise returns from cash holdings40. Working Capital management41. Government grants vs own means42. Current skills audit43. Forecast future skills

44. Mixed economy model and budget management

45. Organisational design

46. Change management approaches

Key

34

Our approachto economic development

35

Introducing our approach

Economic development

Financial

management

6

Human capital

7

Vision

1

Environment

& social indicators

2

3Economic and

spatial planning

Assess current

infrastructure

4The role of the

Public Sector

5

• Economic impact• Sustainability• Affordability• Deliverability

• Baseline current position• Forecast future demand:

Basic services• Forecast future need: High

value sectors• Establish appropriate

regulatory framework

• Socio-economic and spatial baseline

• Gear appropriate measurement tools

• Framework of key performance areas

• Measure the impact of • Public Sector spending

• Baseline current provision• Determine existing barriers• Consider incentive structures• Assess opportunities of

regional transport corridors

• Revitalise the Public Sector compact

• Develop enabling frameworks• Develop innovation

opportunities • Stakeholder engagement• Customer and service

delivery

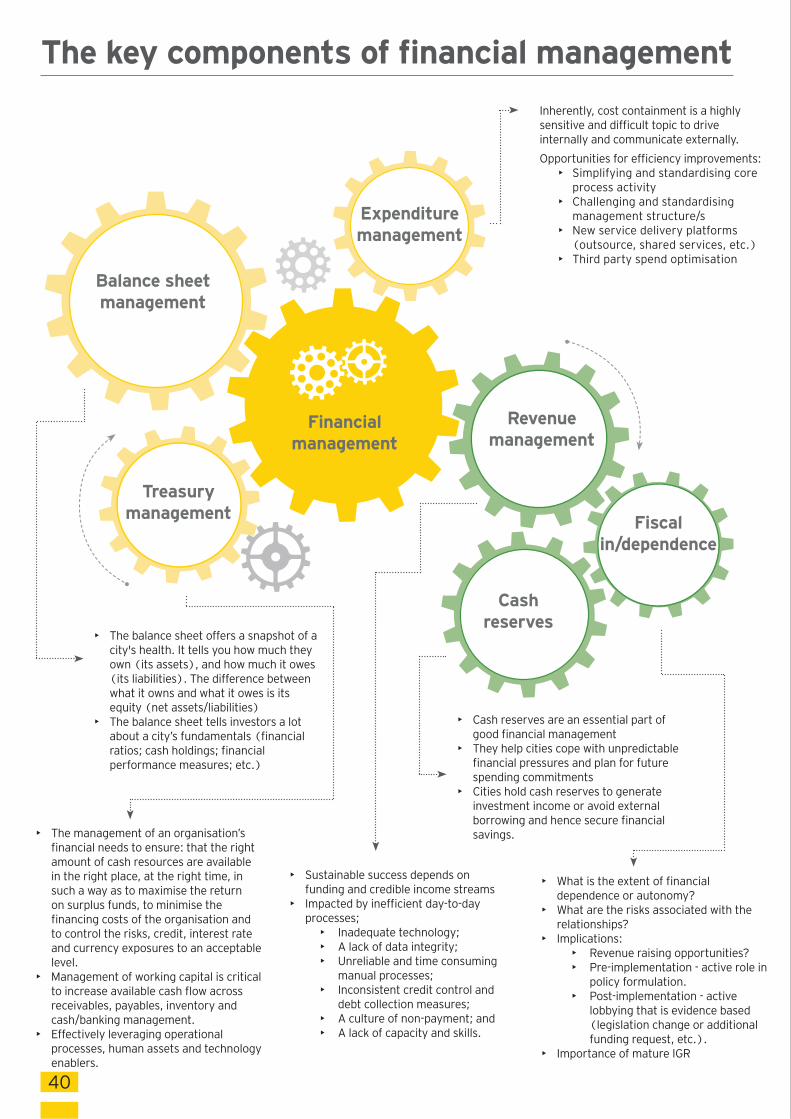

• Financing• Funding• Revenue management• Expenditure management• Treasury management • Balance sheet management• Fiscal in/dependence

• Organisational structure • Roles and responsibilities• Allocation of resources• Organisational capabilities• Governance, culture, talent,

location, systems and process alignment to organisational design

36

The details

v

(eff

fi

)

er

(eff

t)

Lo

(fire

f

t)

ree/fl

of

teerfer

fitw

fi

fror

et

Eff

es

Eff

twv

reov

vsov

s

frC

s

C

te

to

fo

to

S

re

fi

effi

fr

SMAR

/

re

fi

e

OT

to refi

rev

t/

o

rerev

ot

t s

Ceffi

of

fiter te

ver

oof

tov

Est

Are

exte

fi

re

to

or

exte

A

to

or

ofi

C

vsfore

toet

A

fo

e

te

5. D

efi ne the role of the Public Sector

6. F

ina

ncia

l man

agem

ent

7. H

um

an c

apit

al

1. Deliver

Econom

ic im

pact

Su

sta

inab

ilit

y

trad

e c

o

Revit

alise t

he P

ub

lic S

ecto

r co

mp

act

Develo

p e

nabling f

ram

ew

ork

s

Deliv

er

innova

tion

Sta

keho

lder

eng

agem

ent

Cus

tom

er &

ser

vice

del

iver

y

Financin

g Funding

Revenue managementExpenditure managementTreasury management

Acknowledge fi scal in/dependence

Balance sheet management

Organisational structure

Roles & responsibilities

Allocation of resources

Organisational capabilities

Gove

rnance, cu

lture, ta

lent,

loca

tion, syste

ms &

pro

cesse

s

alig

ned to

org

anisa

tional

desig

nLoca

l vs re

gional a

Econo

develop

37

/ter

erfi

re

refir

reEx

to

fire )

Cr

soci

al

o

ofi

envi

ronm

enta

l

te

r

toba

sic se

rvice

s

e(te

owe

tofo

high value sectorsto

v

R

w

ofov

offo

ofi

(S

v

ofSMCA)

of

e

(

s

(w

(s

weA

oto

o

fr

fi

v

exte

of flowof

s

Effv

fits

off

COMES