Embed Size (px)

Citation preview

3Q’15 MARKET SUMMARYHOUSTON, TX METRO AREA

Cresa Houston5599 San Felipe, Suite 500Houston, Texas 77056713.402.5800

cresa.com/houston

Connect with us and get up-to-date information:

Cresa : The Tenant’s Advantage

Facebook.com/cresa

Follow us!@cresahouston

TABLE OF CONTENTS01

02

04

05

06

MARKET AT-A-GLANCE

RENTAL RATES

LEASING ACTIVITY

SUBLEASE SPACE

CONSTRUCTION & DELIVERIES

Information contained herein is provided, in part, from third party sources including: CoStar

Group, Greater Houston Partnership, Bureau of Economic Analysis, Bauer College of

Business, University of Houston - Institute for Regional Forecasting, U.S. Census Bureau,

Perryman Group, Institute for Supply Management – Houston, Houston Association of

Realtors, National Association of Realtors, C2ER Cost of Living Index 3Q’2015, Baker

Hughes U.S. Rig Count Reports.

Even though obtained from sources deemed reliable, no warranty or representation,

expressed or implied, is made as to the accuracy of the information herein.

09

07

08

SUBMARKET SNAPSHOTS

NET ABSORPTION

SALES ACTIVITY

03 VACANCY RATES

11

10

MARKET OUTLOOK

HOUSTON ECONOMY

1.7%

0.3%

1.3%

$45.12 CBD: Class A 8.4%

$28.02 CBD: Class B 15.6%

$41.73 CBD: Class A + B 10.8%

0.1%

0.1%

0.1%

$35.37 Houston: Class A 10.2%

$21.73 Houston: Class B 12.6%

$29.06 Houston: Class A + B 11.4%

0.1%

0.2%

0.1%

$32.90 Suburban: Class A 10.8%

$21.73 Suburban: Class B 12.6%

$27.08 Suburban: Class A + B 11.6%

WesternGeco 554,385 Westchase Renewal

Texas Children's Health Plan 139,244 Bellaire Lease

EMAS 93,600 Westchase Sublease

WD Vonn Gonten 73,000 Katy Fwy Lease

Pannell Kerr Forster of Texas 65,416 San Felipe/Voss Lease

Jones and Carter 55,676 Bellaire Sublease

MRC Global 50,237 CBD Sublease

Quantlab Financial 46,098 Greenway Plaza Lease

Brock Holdings III 38,240 Gulf Fwy/Pasadena Lease

PMC Sierra 33,370 FM 1960/Hwy 249 Lease

HOUSTON MARKETAT-A-GLANCE

With West Texas crude prices slipping below $45/bbl in 3Q’15, the

downturn that has characterized Houston’s economic landscape

this year, is expected to last longer than originally anticipated – at

least through 2016.

There is good news for tenants, however, as the Houston office

market remains tenant favorable, especially in terms of increased

tenant concessions such as longer periods of free rent, free parking,

and larger tenant improvement allowances. Sublease space and

large blocks saw some high figures in the third quarter, even though

rental rates continue to climb slowly.

Given the cyclical nature of the economy, over the long term, the

Houston office market will return to a balanced supply and demand,

but in the interim, prolonged job cuts continue to have an impact.

TENANT’S PERSPECTIVE

MARKET TRENDS

Even though asking rates are increasing, rates at which deals were done decreased, coupled with attractive concession packages.

Houston today is a tenant-favorable market. Many, however, are delaying making large commitments on space or opting for shorter-term leases.

Landlord concessions remain in the tenant’s favor, in order to stay competitive and retain tenants, especially in the suburban submarkets.

More layoffs, bankruptcies, and M&A activity are expected in the oil industry as budgets are slashed, rig counts and drilling permits decline, and exports reduced (due to an appreciating dollar)..

Total non-farm employment increased 1.3% year-over-year in August 2015 – sectors that experienced decreases in employment include manufacturing, construction, and mining and logging.

Regardless of rates increasing slightly, other fundamentals have weakened – including higher vacancy rates, less absorption, construction, and leasing activity, and increased sublease space.

RECENT TRANSACTIONS RENTAL & VACANCY RATES

Tenant Size (SF) Submarket Type Avg. Rate Vacancy Rate Margin from Q2

01

01 HOUSTON MARKET AT-A-GLANCE

MAJOR SUBMARKET STATS | CLASS A + B OFFICE

SUBMARKET MAP | CLASS A + B OFFICE

GALLERIA

$34.839.6%

G

REENWAY

$32.398.1%

M

ED CENTER

$27.2210.2%

CBD

$41.6510.8%

KATY FWY

$32.2310.0%

W

ESTCHASE

$30.269.0%

E. F

ORT BEND CO

$25.239.0%

N

ORTH BELT

$23.6325.0%

N

ORTHWEST

$20.0816.4%

FM 1960

$19.3012.4%

MIDTOWN

$32.0011.0%

TH

E

WOODLAND

S

$30.475.5%

$

%

Rental Rate

Vacancy Rate

AREA OVERVIEW

WEST BELT

$27.9411.3%

Gross Rental Rate Vacant Available Total Net Absorption Leasing ActivitySF

DeliveredUnder

ConstructionSubmarket Inventory (SF) Direct Sub. Direct Sub. Total Quarter YTD 2015 Deals SF

CBD 47,458,584 $41.65 $27.36 10.8% 1.7% 12.4% (98,306) (1,744,510) 22 145,963 0 1,578,258

Suburban 215,815,534 $27.08 $24.95 11.6% 1.0% 12.6% 833,114 3,981,704 449 2,770,088 1,188,757 10,532,914

E. Fort Bend Co. 8,860,889 $25.23 $21.26 9.0% 0.6% 9.6% 183,926 372,743 30 158,384 137,800 5,824

FM 1960 11,495,518 $19.30 $18.97 12.4% 0.3% 12.7% 76,634 605,208 33 98,708 0 0

Galleria/W. Loop 22,997,133 $34.38 $27.74 9.6% 1.1% 10.6% 66,773 (326,830) 50 243,462 92,021 1,145,000

Greenway Plaza 10,638,618 $32.39 $24.03 8.1% 0.2% 8.3% (12,652) (236,710) 26 166,063 0 858,275

Katy Freeway 34,295,789 $32.23 $23.72 10.0% 2.4% 12.4% 244,731 360,150 68 314,537 305,807 2,365,694

Midtown 6,754,545 $32.00 $25.80 11.0% 0.1% 11.1% 47,737 163,267 22 67,224 167,562 0

North Belt 12,190,983 $23.63 $17.25 25.0% 3.3% 28.2% (300,493) (1,190,631) 9 16,713 0 68,950

Northwest 9,167,626 $20.08 $17.08 16.4% 0.7% 17.0% (17,727) (180,321) 19 81,418 0 15,000

Medical Center 9,413,199 $27.22 $16.93 10.2% 0.0% 10.2% 10,719 (159,931) 14 76,537 0 0

West Belt 6,211,786 $27.94 $21.80 11.3% 1.3% 12.6% 12,252 1,039,999 12 75,056 0 200,000

Westchase 16,159,401 $30.26 $32.50 9.0% 1.7% 10.7% 106,891 (118,349) 34 691,981 0 1,545,000

Woodlands 17,148,948 $30.47 $33.19 5.5% 0.4% 5.9% 146,988 2,192,085 29 120,320 38,350 1,589,652

Other Suburban 50,481,099 $22.37 $25.55 13.7% 0.2% 13.9% 271,206 1,468,674 102 658,795 447,217 2,739,519

TOTAL 263,274,118 $29.07 $25.35 11.4% 1.1% 12.6% 734,808 2,237,194 471 2,916,051 1,188,757 12,111,172

02

RENTAL RATES

Overall, rental rates for Class A and B citywide are holding

steady but starting to see small decreases in some key

submarkets. Even though asking rates are still increasing,

rates at which deals were actually done decreased, coupled

with attractive concession packages.

RENTAL RATES

• Rental rates are the highest they have been in Houston’s history.

• Over the past year, rental rates have seen a 3.2% increase

(nearly $1), from $28.15 PSF gross in 3Q’14 to $29.06 in 3Q’15.

• Year-over-year Class B rates showed the largest increase of

3.3% to $21.73 PSF gross; Class A rates increased by 2.3% to

$35.37 PSF gross.

• In 3Q’15, the highest rates were found in the central submarkets

(the CBD, Greenway Plaza, Galleria/West Loop) and out west

(Katy Freeway).

• The Northwest, North Belt, Westchase, and Greenway Plaza

submarkets saw a decline in rental rates.

SUBMARKET RENTAL RATES 3Q’15

Westchase

The Woodlands

Midtown

Katy Freeway

Greenway Plaza

Galleria/W. Loop

CBD

Houston

West Belt

$0

Rental Rate Houston Avg Rate

Medical Center

Sugar Land

North Belt

Northwest

$10 $20 $30 $40 $50

HISTORICAL DIRECT AVERAGE RATES

3Q ‘08 3Q ‘09 3Q ‘10 3Q ‘11 3Q ‘12 3Q ‘13 3Q ‘14

$40.00

$35.00

$30.00

$25.00

$20.00

$15.00

$10.00

$5.00

$0.00

Class A Class B Houston Average Rate

3Q ‘15

FM 1960

03

HISTORICAL TOTAL VACANT AVAILABLE SUBMARKET VACANCY RATES 3Q’15

CBD

Midtown

West Belt

Houston

FM 1960

Northwest

North Belt

Medical Center

Katy Freeway

0%

Vacancy Rate Houston Avg Rate

Galleria/W. Loop

Westchase

Sugar Land

Greenway Plaza

5% 10% 15% 20%

Class A Class B Houston Average Rate

14%

13%

12%

11%

10%

9%

8%

7%

3Q ‘08 3Q ‘09 3Q ‘10 3Q ‘11 3Q ‘12 3Q ‘13 3Q ‘14 3Q ‘15

NOTES

• Citywide, in Class A and B buildings, vacancy rates increased

by 0.1% (10 basis points) quarter-over-quarter to 11.4%; year-

over-year vacancy rates increased by 1.7% (170 basis points).

• Larger increases have been felt in Class A properties - vacancy

has jumped from 7.6% to 10.2% in just a year.

• In 3Q’15, the lowest vacancy rates (below 10.0%) were in

Woodlands (5.5%), Greenway Plaza (8.1%), Sugar Land (9.0%),

Westchase (9.0%), and Galleria/West Loop (9.6%).

• The highest vacancy rates were in FM 1960 (12.4%), Northwest

(16.4%), and North Belt (25.0%).

Demand for space has slowed considerably and citywide

vacancy increased by 1.7% (170 basis points) year-over-

year to 11.4%. Coupled with the delivery of nearly 1.2 million

square feet of office space and 12.9 million square feet

due to be delivered in the coming years, vacancy is sure to

continue it’s upward trend.

VACANCY RATES

The Woodlands

04

LEASING ACTIVITY

Lease transaction volume continued to decline in 3Q’15

to approximately 2.9 MSF, nearly half of the activity when

compared year-over-year. The slowdown in leasing activity is

mainly due to the uncertainty of oil prices, coupled with the

delivery of product that is not yet leased.

NOTES

• Leasing activity in the first three quarters of 2015 (9.2 MSF) was

about half when compared to the first three quarters of 2014

(16.7 MSF).

• The total number of deals in 3Q’15 was also down to 469 –

lower than the previous 39 quarters and much lower than a year

earlier (1,036 deals in 3Q’14).

• Lease transaction volume fell below the 15-year quarterly

average of 4.3 MSF.

• 3Q’15 was the slowest quarter in terms of leasing activity since

the great recession.

• The submarkets with the most activity include Galleria/West

Loop, Westchase, and Katy Freeway.

• Medical Center, Midtown, and FM 1960 were among the lowest.

TOP 10 TRANSACTIONS HISTORICAL LEASING ACTIVITY

‘01 ‘02 ‘03 ‘04 ‘05 ‘06 ‘07 ‘08 ‘09 ‘10 ‘11 ‘12 ‘13 ‘14

25

20

15

10

5

5,000

4,000

3,000

2,000

1,000

Milli

ons

Total SF Leased Total Deals

WesternGeco 554,385 10001 Richmond Westchase

Texas Children's Health Plan

139,244 6330 W. Loop South Bellaire

EMAS 93,600 10500 Richmond Westchase

WD Vonn Gonten 73,000 10496 Old Katy Rd. Katy Fwy

Pannell Kerr Forster of Texas

65,416 5847 San Felipe San Felipe/Voss

Jones and Carter 55,676 6330 W. Loop South Bellaire

MRC Global 50,237 1301 McKinney CBD

Quantlab Financial 46,098 3 Greenway Plaza Greenway Plaza

Brock Holdings III 38,240 4440 SH 225 Gulf Fwy/Pasadena

PMC Sierra 33,370 11450 Compaq Ctr. W. FM 1960/Hwy 249

Tenant SF Building Submarket

YTD‘15

0 0

Q2’15 Q3’15

1 20

West Belt

CBD

Greenway Plaza

Galleria/W. Loop

Westchase

Katy Freeway

Sugar Land

North Belt

Northwest

The Woodlands

FM 1960

Midtown

SUBMARKET COMPARISON

Leasing activity dwindled starting in 4Q’14. Katy Freeway, The Galleria, and Westchase submarkets saw the most activity during the second quarter of 2015.

Medical Center

Q4’14 Q1’15

05

SUBLEASE SPACE

There is currently 7.8 MSF of space on the sublease market.

Sublease space is continuing to hit the market as the amount

of space available has more than doubled year-over-year.

NOTES

• This space has an average gross rental rate of $25.30. Sublease

rental rates have decreased over the past several quarters.

• This space has an average time on the market of 14.4 months.

• The submarkets with the most sublease space are Katy Freeway

(2.3 MSF), CBD (1.5 MSF), and Westchase (924 KSF).

LARGE BLOCKS OF SUBLEASE SPACE

• There are 87 buildings in the Houston market that have large

blocks of sublease space (20,000 SF+)

• Available space of this size has more than tripled year-over-year.

• This equates to 6.2 MSF (~79%) of total sublease space and has

an average gross rental rate of $25.87.

• Average time on the market for this dataset is 11.0 months

HISTORICAL SUBLEASE SPACE

$33

$29

$25

$21

$17

10%

8%

6%

4%

2%

Gross Rent Total Available

$13 0%

SUBLEASE SPACE BY SUBMARKET

‘07 ‘08 ‘09 ‘10 ‘11 ‘12 ‘13 ‘14 ‘15

Other

The Woodlands

Galleria

Greenspoint

Westchase

CBD

Katy Freeway

FM 1960

0

SF Available

1 MSF 2 MSF0.5 MSF 1.5 MSF 2.5 MSF

Greenway

Northwest

Sugar Land

06

CONSTRUCTION &DELIVERIES

Nearly 1.2 MSF was delivered across Houston during 3Q’15.

This was preceded by a year of record deliveries equating

to nearly 13 MSF. There was an additional 12.9 MSF under

construction across the Houston area at the end of the third

quarter.

DELIVERIES (BLDGS. OVER 100.000 SF)

• There were five building completions totaling 853,000 square feet

in the third quarter (buildings with more than 100,000 SF).

• Of the 853,000 SF delivered in 3Q’15, roughly 36% was leased at

the time of completion.

• The tenancy profile of two of the buildings delivered in 3Q’15 was

single tenant, corporate users, taking 27% of the space delivered

and equating to 233,000 SF.

• 1Q’15 saw the most SF delivered in a single quarter over the past

15 years.

• Completions were dispersed across Houston with one building

each in the E. Fort Bend Co./Sugar Land, Southwest Far, Katy

Freeway, Midtown, and Katy/Grand Parkway submarkets.

PROPOSED DEVELOPMENT

• There is an additional 29.5 MSF proposed in 240

properties, most of which, given current economic

conditions, will not come out of the ground until at least

the end of 2016.

• The submarkets that have the most proposed

development include: CBD (5.6 MSF), Katy Freeway (5.1

MSF), and The Woodlands (4.9 MSF).

Sugar Land 1 133,000 100.0%

Southwest 1 100,000 100.0%

Katy Freeway 1 300,907 0.0%

Midtown 1 167,562 28.7%

Katy/Grand Parkway 1 151,187 16.4%

Total 5 852,656 35.9%

Submarket Bldgs SF % Leased

FM 1960 2 770,000 100.0%

Katy Freeway 9 2,543,657 73.3%

Southwest 5 1,381,977 70.8%

West Belt 1 206,754 15.0%

Woodlands 2 2,000,000 100.0%

Total 19 6,902,388 81.8%

Submarket Bldgs SF % Leased

7705 Highway 90AE. Fort Bend Co./Sugar Land

133,000 SF100% Leased

Nalco Champion

270 Abner Jackson ParkwaySouthwest Far

100,000 SF100% Leased

Dow

1414 EnclaveKaty Freeway West

300,907 SF0.0% LeasedMulti-Tenant

2299 San FelipeMidtown

167,562 SF28.7% LeasedMulti-Tenant

24275 Katy FreewayKaty/Grand Parkway

151,187 SF16.4% LeasedMulti-Tenant

DELIVERIES BY SUBMARKET 1H’15 DELIVERIES BY SUBMARKET 3Q’15

3Q’15 MAJOR DELIVERIES

06 CONSTRUCTION & DELIVERIES

06

2015 1 600,000 11.6% 100.0%

2016 6 4,583,440 88.4% 100.0%

2017 0 NA NA NA

Single Tenant Bldgs. SF % of Devs. % Leased

ST Total 7 5,183,440 47.4% 100.0%

2015 6 1,848,523 32.1% 37.8%

2016 10 3,344,287 58.1% 17.4%

2017 2 566,813 9.8% 49.7%

Multi-Tenant Bldgs. SF % of Devs. % Leased

MT Total 18 5,759,623 52.6% 27.1%

TOTAL 28 10,943,063 100.0% 61.7%

Greenway Plaza

Galleria/W. Loop

The Woodlands

Westchase

CBD

Northeast

West Belt

0

SF Leased SF Unleased

1 MSF 2 MSF

Delivered Projected

0

2 MSF

4 MSF

6 MSF

8 MSF

10 MSF

‘00 ‘01 ‘02 ‘03 ‘04 ‘05 ‘06 ‘07 ‘08 ‘09 ‘10 ‘11 ‘12 ‘13 ‘14 ‘16 ‘17‘15‘990.5 MSF 1.5 MSF 2.5 MSF

10.9 MSF

4Q’15 02/2017

CONSTRUCTION AT-A-GLANCE

SLATED OFFICE DELIVERY

PRE-LEASEDPERCENTAGE

Combined both multi-tenant and single tenant (for just multi-tenant projects, the pre-leased percentage is 27.1%)

62%

SINGLE TENANTCONSTRUCTION

There is 5.2 MSF of single-tenant space under construction compared to 5.8 MSF of multi-tenant space

47%

• At the end of the 3Q’15, Houston had approximate 12.9 MSF of

office space under construction in 60 buildings. Of these, 25 are

at least 100,000 SF and encompass over 10.9 MSF.

• The tenancy profile of 47.4% of the buildings (100,000 SF+)

currently under construction is single tenant, corporate users

totaling over 5.1 MSF in seven buildings.

• Multi-tenant buildings over 100,000 SF, which account for 52.6%

of inventory under construction (5.8 MSF), are 27.1% pre-leased

with a weighted average rent of $44.66 PSF gross with average

operating expenses between $13.00 and $14.00/SF.

UNDER CONSTRUCTION

12 MSF

14 MSF

Katy Freeway

CONSTRUCTION BY SUBMARKET HISTORICAL CONSTRUCTION

CONSTRUCTION & DELIVERIES

06 CONSTRUCTION & DELIVERIES

3Q’15 UNDER CONSTRUCTION

915 Eldridge PkwyKaty Fwy West

526,637 SF0.0% LeasedMulti-Tenant

Delivers 4/2016

925 Eldridge PkwyKaty Fwy West

600,000 SF100% LeasedConocoPhillips

Delivers 10/2015

1500 Post Oak BlvdGalleria

600,000 SF100% LeasedBHP Billiton

Delivers 10/2016

10353 RichmondWestchase445,000 SF

100% LeasedMulti-Tenant

Delivers 2/2016

9811 Katy FwyKaty Fwy East

526,637 SF58.5%

Multi-TenantDelivers 11/2015

Subsea Ln @ W Lake HoustonNortheast Near1,700,000 SF100% Leased

FMC TechnologiesDelivers 1/2016

3773 RichmondGreenway Plaza

210,000 SF37.4% LeasedMulti-Tenant

Delivers 4/2016

2101 Citywest BlvdWestchase

1,100,000 SF100% Leased

Phillips 66Delivers 6/2016

609 Main StCBD

1,057,668 SF0.0% LeasedMulti-Tenant

Delivers 12/2016

825 Town & CountryKaty Fwy East

227,063 SF62.3% LeasedMulti-Tenant

Delivers 11/2015

3737 Buffalo SpeedwayGreenway Plaza

400,000 SF22.9% LeasedMulti-Tenant

Delivers 10/2015

1110 Main StCBD

406,600 SF100% LeasedHilcorp EnergyDelivers 1/2016

07

HISTORICAL NET ABSORPTION SUBMARKET COMPARISON

NET ABSORPTION

The second quarter saw total net absorption of 735 KSF,

which was not balanced with deliveries (excess of 1.2 MSF).

Suburban submarkets such as The Woodlands, Sugar Land

and Katy Freeway experienced the most positive absorption

in the third quarter.

• Absorption in 2014 at 9.3 MSF was historically the highest it’s

been in the past 15 years.

• The Woodlands far outweighs all submarkets in terms of net

absorption over the past year with over 3.9 MSF. The closest

submarket was Katy Freeway with 1.2 MSF..

• The submarkets with the most negative net absorption in 3Q’15

and over the past year were CBD and North Belt.

NOTES

0 MSF

(2) MSF

2 MSF

4 MSF

6 MSF

8 MSF

10 MSF

‘99 ‘00 ‘01 ‘02 ‘03 ‘04 ‘05 ‘06 ‘07 ‘08 ‘09 ‘10 ‘11 ‘12 ‘13 ‘14 ‘15

Class A Class B Houston Total Absorption

5 MSF

Q3’15

Westchase

Midtown

Sugar Land

FM 1960

Katy Freeway

The Woodlands

West Belt

Northwest

Medical Center

Greenway Plaza

Galleria/W. Loop

North Belt

CBD

Q4’14 Q1’15 Q2’15

3 MSF1 MSF(1) MSF(3) MSF

08

TRANSACTION SUMMARY

Sales of significant office properties (75,000 SF+) were strong

in the third quarter with over 2.1 million square feet in 12

buildings trading hands. A majority of the properties coming

to market are single-tenant or deals with major tenancy with

a great deal of term remaining.

Below is a summary of significant transactions (75,000 SF+)

that have closed year-to-date by quarter.

SALES ACTIVITY

1Q’15 6 2,552,269 96% $871,338,775 $341

2Q’15 7 1,171,338 76% $174,400,000 $149

3Q’15 12 2,149,464 75% $294,550,000 $137

Quarter No. SF Occ. Price $/SF

YTD 25 5,873,071 84% $1,340,288,775 $228

LARGEST 3Q’15 TRANSACTIONS

Building Galleria Place I & II One Commerce Green 400 N Sam Houston Pky E Academy HQ

Address 5251 & 5333 Westheimer 515 W Greens Rd 400 North Belt 1540 North Mason Road

Date August 15 September 15 July 15 August 15

Submarket Galleria/Uptown Greenspoint Greenspoint Energy Corridor

Class A B B A

Year Built 1976 1983 1981 2015

SqFt 401,271 340,956 234,147 217,782

Occ. 52% 100% 64% 100%

$/SF $226 $139 $43 $266

Buyer Lincoln Prop. JV Illinois (State) Nabors Industries Hartman Moody National Companies

Seller Songy JV Carlyle Parkway Properties Parkway Properties Academy Sports + Outdoors

CBDSUBMARKET UPDATE

The CBD Submarket is the city’s largest submarket with

nearly 36.5 million square feet of Class A and B space. The

long-term viability of the CBD as the city’s premier submarket

has been ensured as a result of the massive $5 billion public/

private investment in downtown since early 2000.

MARKET TRENDS

MARKET DRIVERS

TENANT’S PERSPECTIVE

• The average rental rate rate experienced an increase between

2Q and 3Q’2015. This rate is at historically its highest level in

this submarket at $41.73 gross PSF.

• At 3Q’15 the vacancy rate of 10.8% was the highest it has

been since 2006.

• Sublease space is at an all-time high at nearly 1.5 million SF.

• Unstable price of oil expected to continue to have an impact

on office rents and vacancy for the remainder of 2015.

• Face rates will remain high, as landlords don’t correct down

as quickly as they correct up.

• Developers are bringing some space to the market to help

meet the increases in demand – one large multi-tenant build-

ing will deliver in January 2016 adding inventory to the CBD.

• Increases in concessions will continue given the instability of

oil prices.

• Due to low vacancies in Class A space, tenants will still

compete for well-located premier office space, however, there

are now more deals to be made.

• Tenants will need to continue to monitor the price of oil due to

its correlation with demand for CBD space.

$ 28.16$0.14 vs

2Q’15

0.2% vs 2Q’15

477K SF vs 2Q’15

Class A Class B

SF00K SF vs

2Q’15

OFFICE SNAPSHOT

Avg. Gross Rental Rate Avg. Gross Rental Rate

Vacancy Vacancy

Net Absorption Net Absorption

Construction Construction

$ 45.29$0.35 vs

2Q’15

%8.40.1% vs

2Q’15

48K SF vs 2Q’15

SF2.3M800K SF vs

2Q’15

SF-19KSF-79K

%15.6

09

4

3

4

1

2

2

3

1

1

3

4

5

1

4

3

5

4

2

1

3

5

1

2

3 4

5

09 CBD SUBMARKET UPDATE

22

UNDER CONSTRUCTION PROPOSED DEVELOPMENT

Hilcorp Energy Tower406,600 SF | 100% Leased

609 Main Street1.1 MSF | 0.0% Leased

700 Avenida De Las Americas115,000 SF | 100% Leased

1600 Louisiana Street1.7 MSF

5 Allen Center1.0 MSF

6 Houston Center633,482 SF

One Market Square750,000 SF

LARGEST EMPLOYERS RECENT LEASES SIGNED

Chevron8,600 Employees

Shell7,000 Employees

JP MorganChase4,892 Employees

CenterPoint Energy3,826 Employees

KBR2,958 Employees

Gardere75,000 SF

MRC Global50,237 SF

VirTis26,198 SF

Plains Marketing24,260 SF

Hughes Watters Askanase24,253 SF

LARGEST SUBLEASE SPACES LARGEST BLOCKS OF SPACE

1415 Louisiana126,262 SF

500 Jefferson97,953 SF

Three Allen Center90,467 SF

BG Group Place81,786 SF

500 Jefferson77,629 SF

800 Bell1,314,350 SF

2 Houston Center234,333 SF

Two Shell Plaza188,695 SF

Two Shell Plaza159,665 SF

Total Plaza145,352 SF

1

2

3

1

2

3

4

5

1

2

3

4

5

1

2

3

4

5

1

2

3

4

5

1

2

3

4

CBD SUBMARKET MAP

09CBD SUBMARKET UPDATE

Capitol Tower750,000 SF | .00% Leased4

The following graph illustrates the

historical rental and vacancy rates for

the submarket in both Class A and

Class B buildings.

RENTAL RATES & VACANCY

09 CBD SUBMARKET UPDATE

Class A Rate Class B Rate Class A Vacancy

3Q ‘08 3Q ‘09 3Q ‘10 3Q ‘11 3Q ‘12 3Q ‘13 3Q ‘14 3Q ‘15

Class B Vacancy

The following graph illustrates the

historical leasing activity for both

Class A and Class B buildings in the

submarket.

LEASING ACTIVITY

The following graph illustrates the

historical net absorption and square

feet delivered for both Class A and

Class B buildings in the submarket.

ABSORPTION & DELIVERIES

SF Leased Total Deals

1MSF

2MSF

3MSF

4MSF

5MSF

0 SF‘00 ‘01 ‘02 ‘03 ‘04 ‘05 ‘06 ‘07 ‘08 ‘09 ‘10 ‘11 ‘12 ‘13 ‘14 ‘15

‘00 ‘01 ‘02 ‘03 ‘04 ‘05 ‘06 ‘07 ‘08 ‘09 ‘10 ‘11 ‘12 ‘13 ‘14 ‘15

SF Delivered YTD Absorption

-2MSF

-1MSF

4%

6%

8%

10%

12%

14%

16%

18%

$15

$20

$25

$30

$35

$40

$45

$50

6MSF

70

140

210

280

350

0

420

6%

8%

10%

12%

14%

4%

16%

18%

$20

$25

$30

$35

$40

$15

$45

$50

2MSF

0 SF

1MSF

0.5MSF

1.5MSF

2.5MSF

-1.5MSF

-.5MSF

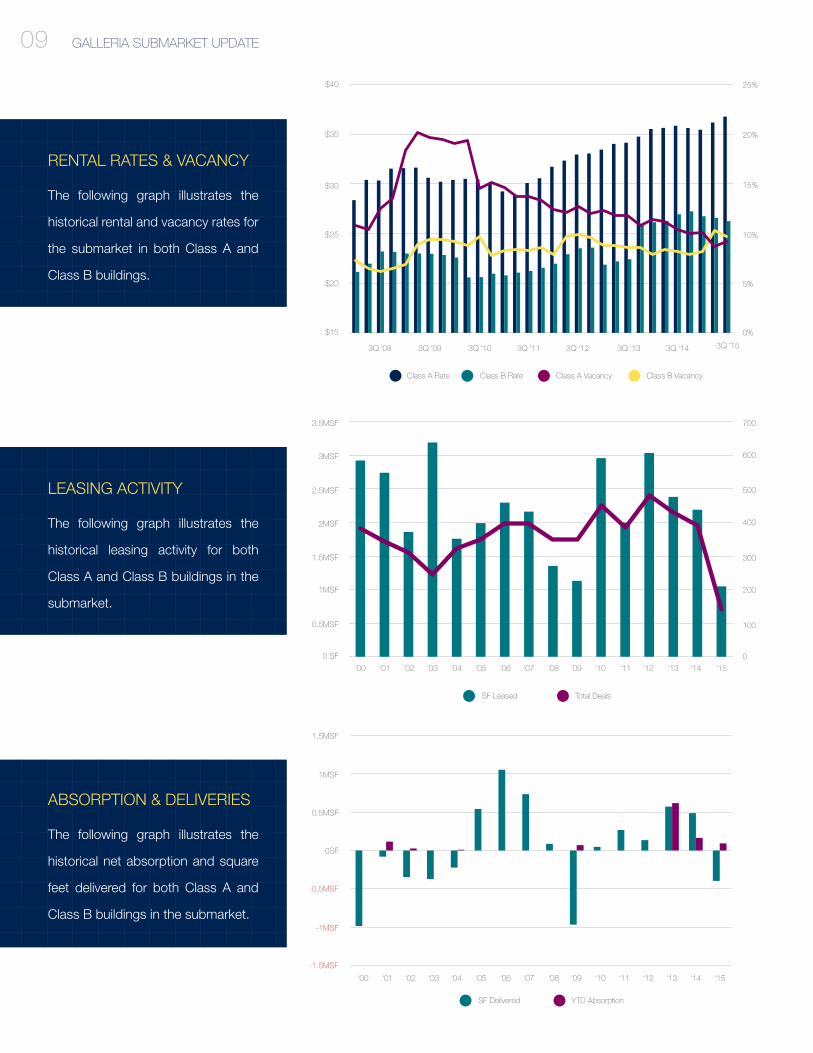

GALLERIASUBMARKET UPDATE

The Galleria area has historically been one of Houston’s

most popular submarkets, providing tenants great access

and amenities. With the metro area’s nation-leading job

growth over the past few years, this submarket has grown

increasingly tight, particularly in Class A buildings.

$ 26.24$0.32 vs

2Q’15

0.5% vs 2Q’15

27K SF vs 2Q’15

Class A Class B

SF0K0K SF vs

2Q’15

OFFICE SNAPSHOT MARKET TRENDS

MARKET DRIVERS

TENANT’S PERSPECTIVE

• In general, the average rental rate (Class A&B) has gradually

continued to increase. This rate is at historically its highest level

in this submarket at $33.60 gross PSF.

• Over the past five years, vacancy rates (Class A&B) have

fluctuated between the 9% - 12% range, and is currently at

10.6%.

• The number of subleases and large blocks being put on the

market has slowed, as has leasing activity - which closed the

quarter with 221,000 SF leased - the smallest amount in the

history of the submarket.

• Unstable price of oil has not had a large impact on office asking

rents, however landlord concessions have greatly increased.

• Face rates will remain high, as landlords don’t correct down as

quickly as they correct up.

• There are a couple of multi-tenant buildings under construction,

which will likely add vacant inventory to the submarket when

they deliver.

• Increases in concessions will continue.

• Tenants will still compete for well-located premier office space,

however, there are now more deals to be made.

• Tenants will need to continue to monitor the price of oil due to

its correlation with demand for space.

Avg. Gross Rental Rate Avg. Gross Rental Rate

Vacancy Vacancy

Net Absorption Net Absorption

Construction Construction

$36.75$0.59 vs

2Q’15

%9.70.6% vs

2Q’15

113K390K SF vs

2Q’15

SF1.1M92K SF vs

2Q’15

%9.2

SF SF-47K

09

1

3

1

1

2

3

5

4

1

2

3

5

2

1

4

3

5

1

2

3

4

5

GALLERIA SUBMARKET UPDATE09

2

2

UNDER CONSTRUCTION PROPOSED DEVELOPMENT

1500 Post Oak Blvd.600,000 SF | 100% Leased

1717 West Loop South380,000 SF | 74.2% Leased

1600 West Loop South120,000 SF | 100% Leased

LARGEST EMPLOYERS RECENT LEASES SIGNED

BHP Billiton2,000 Employees

S&B Infrastructure2,000 Employees

Spectra Energy2,000 Employees

Telecheck2,000 Employees

Bechtel1,700 Employees

Stage Stores168,901 SF

PKF65,416 SF

Capital One Bank58,000 SF

Undisclosed40,703 SF

Alliant39,000 SF

LARGEST SUBLEASE SPACES LARGEST BLOCKS OF SPACE

Galleria Tower II63,829

1800 West Loop South39,626 SF

1775 Saint James Place33,322 SF

5400 Westheimer Court30,481 SF

5555 San Felipe26,407 SF

5251 Westheimer158,084 SF

Five Post Oak Park142,665 SF

2700 Post Oak140,618 SF

1333 West Loop South111,250 SF

1233 West Loop South111,250 SF

1

2

1

2

3

4

5

1

2

3

4

5

1

2

3

4

5

1

2

3

4

5

1

GALLERIA SUBMARKET MAP

09GALLERIA SUBMARKET UPDATE

1885 Saint James Place165,000 SF | 0.0% Leased3

River Oaks District Phase II455,000 SF | 0.0% Leased2

2

The following graph illustrates the

historical rental and vacancy rates for

the submarket in both Class A and

Class B buildings.

RENTAL RATES & VACANCY

Class A Rate Class B Rate Class B Vacancy

3Q ‘08 3Q ‘09 3Q ‘10 3Q ‘11 3Q ‘12 3Q ‘13 3Q ‘14 3Q ‘15

Class A Vacancy

$40

$35

$30

$25

$20

$15

20%

15%

10%

5%

0%

The following graph illustrates the

historical leasing activity for both

Class A and Class B buildings in the

submarket.

LEASING ACTIVITY

The following graph illustrates the

historical net absorption and square

feet delivered for both Class A and

Class B buildings in the submarket.

ABSORPTION & DELIVERIES

SF Leased Total Deals

2MSF

3MSF

300

400

500

600

700

00 SF

‘00 ‘01 ‘02 ‘03 ‘04 ‘05 ‘06 ‘07 ‘08 ‘09 ‘10 ‘11 ‘12 ‘13 ‘14 ‘15

‘00 ‘01 ‘02 ‘03 ‘04 ‘05 ‘06 ‘07 ‘08 ‘09 ‘10 ‘11 ‘12 ‘13 ‘14 ‘15

SF Delivered YTD Absorption

-1MSF

-0.5MSF

0SF

0.5MSF

1MSF

1.5MSF

25%

GALLERIA SUBMARKET UPDATE09

-1.5MSF

0%

5%

10%

15%

20%

25%

$15

$20

$25

$30

$35

$40

1MSF

100

200

0.5MSF

1.5MSF

2.5MSF

3.5MSF

09

$19.93$0.15 vs

2Q’15

0.2% vs 2Q’15

45K SF vs 2Q’15

Class A Class B

SF00 SF vs

2Q’15

OFFICE SNAPSHOT

Avg. Gross Rental Rate Avg. Gross Rental Rate

Vacancy Vacancy

Net Absorption Net Absorption

Construction Construction

$36.70$2.00 vs

2Q’15

%8.80.2% vs

2Q’15

80K SF vs 2Q’15

SF1.5M0K SF vs

2Q’15

SF6KSF101K

%9.2

The Westchase District’s roots trace back to the early 1960s,

evolving from farmland into a 2,460-acre master-planned

community bustling with commercial activity. More than

500,000 people reside within five miles of this submarket,

giving area employers a large, well-educated employee pool.

MARKET TRENDS

MARKET DRIVERS

TENANT’S PERSPECTIVE

• The average rental (Class A&B) rate saw a dip between 3Q’15

and 2Q’15, however, it is still at a near historically high level at

$30.26/SF.

• Overall, the vacancy rate increased by 0.2 percentage points to

9% this quarter.

• Class A sublease space decreased by over 75,000 SF.

• Absorption increased for the second consecutive quarter -

3Q’15 absorption totaled nearly 107 KSF, following a quarter

with 74 KSF.

• Leasing activity continued to slow - the third quarter saw

113,476 SF leased, lower than any quarter in recorded history.

• Price of oil will continue to have an impact on office rents and

vacancy for the remainder of 2015, particularly in submarkets

in west Houston.

• The 1.5 million SF under construction is 100% leased, adding

no vacant space to inventory.

• Due to the low price of oil, tenants are benefitting increases in

concessions.

• The market is currently tenant favorable.

WESTCHASESUBMARKET UPDATE

21

1

2

3

4

5

2

5

1

2

43

5

1

2

3

4

5

09 WESTCHASE SUBMARKET UPDATE

2

4

13

1

UNDER CONSTRUCTION PROPOSED DEVELOPMENT

2101 CityWest1.1 MSF | 0.0% Leased

10353 Richmond445,000 SF | 100% Leased

CityWest 6387,200 SF

CityWest 5306,900 SF

6004 Rogerdale158,607 SF

LARGEST EMPLOYERS RECENT LEASES SIGNED

Jacobs2,344 Employees

Halliburton1,700 Employees

BMC Software1,277 Employees

Phillips 661,100 Employees

CB&I930 Employees

National Oilwell Varco445,000 SF

BMC Software225,000 SF

CB&I100,000 SF

Zachry48,500 SF

USPh40,000 SF

LARGEST SUBLEASE SPACES LARGEST BLOCKS OF SPACE

2103 CityWest Blvd176,193 SF

3010 Briarpark Dr160,356 SF

2107 CityWest Blvd103,018

2050 West Sam Houston Pky89,239 SF

3250 Briarpark Dr41,233 SF

2101 CityWest Blvd314,316 SF

3600 West Sam Houston Pky150,000 SF

2500 CityWest Blvd116,836 SF

2050 West Sam Houston Pky107,088 SF

11490 Westheimer47,363 SF

1

2

1

2

3

4

5

1

2

3

4

5

1

2

3

4

5

1

2

3

4

5

1

2

3

WESTCHASE SUBMARKET MAP

09WESTCHASE SUBMARKET UPDATE

The following graph illustrates the

historical rental and vacancy rates for

the submarket in both Class A and

Class B buildings.

RENTAL RATES & VACANCY

Class A Rate Class B Rate Class A Vacancy

3Q ‘08 3Q ‘09 3Q ‘10 3Q ‘11 3Q ‘12 3Q ‘13 3Q ‘14 3Q ‘15

Class B Vacancy

$40

$35

$30

$25

$20

$15

20%

17%

14%

11%

8%

5%

The following graph illustrates the

historical leasing activity for both

Class A and Class B buildings in the

submarket.

LEASING ACTIVITY

The following graph illustrates the

historical net absorption and square

feet delivered for both Class A and

Class B buildings in the submarket.

ABSORPTION & DELIVERIES

SF Leased Total Deals

1.5MSF

2MSF

2.5MSF

3MSF

3.5MSF

150

200

250

300

350

00 SF

‘00 ‘01 ‘02 ‘03 ‘04 ‘05 ‘06 ‘07 ‘08 ‘09 ‘10 ‘11 ‘12 ‘13 ‘14 ‘15

‘00 ‘01 ‘02 ‘03 ‘04 ‘05 ‘06 ‘07 ‘08 ‘09 ‘10 ‘11 ‘12 ‘13 ‘14 ‘15

SF Delivered YTD Absorption

09 WESTCHASE SUBMARKET UPDATE

1MSF

0.5MSF

100

50

-1MSF

-0.5MSF

0SF

0.5MSF

1MSF

1.5MSF

• The direct average rate (Class A&B) increased slightly between

2Q’15 and 3Q’15 by $0.16 to $31.75 PSF gross.

• Since the previous quarter, the vacancy rate increased by nearly

1.0 percentage points to 10.3%.

• Sublease space continued to increase – up over an additional

408,000 SF in the third quarter alone. Over the past year, each

quarter has seen an increase of at least 250,000 SF.

• Leasing activity remains slow - the third quarter saw 363,268 SF

leased, lower than any quarter since 1Q’2009.

• Vacancy has increased significantly due to several factors,

including over 3.3 million SF delivered in 2015.

• Approximately 2.8 million SF under construction will drive

vacancy up further as space is delivered (half of multi-tenant

new construction is pre-leased); this space was originally

being developed to help meet the rising demand, which has

tapered off this year.

09

The Energy Corridor has long been one of Houston’s most

desirable submarkets and is dominated by large tenants in

the E&P and engineering sectors. This market is driven by

the price of oil and natural gas. Large users like BP, Conoco,

and Shell drive market demand.

MARKET TRENDS

MARKET DRIVERS

TENANT’S PERSPECTIVE

• There are deals to be made in this submarket as space for

lease and sublease continues to climb.

• The majority of space being vacated is obsolete and will need

to be repositioned.

Class A Class B

OFFICE SNAPSHOT

Avg. Gross Rental Rate

Vacancy

Net Absorption

Construction

$ 36.38$0.17 vs

2Q’15

%9.41.4% vs

2Q’15

233K SF vs 2Q’15

SF2.5M200K SF vs

2Q’15

SF262K

KATY FREEWAYSUBMARKET UPDATE

Avg. Gross Rental Rate

Vacancy

Net Absorption

Construction

$ 24.50$0.35 vs

2Q’15

%11.70.1% vs

2Q’15

206K SF vs 2Q’15

SF264K5K SF vs

2Q’15

SF-170K

5

09 KATY FREEWAY SUBMARKET UPDATE

43

1

2

2

1

1

2

45

3

4 5

2

1

4

1

3

12

35

4

UNDER CONSTRUCTION PROPOSED DEVELOPMENT

15377 Memorial Drive389,709 SF | 4.7% Leased

915-925 N. Eldridge Parkway1.5 MSF | 100% Leased

13501 Katy Freeway400,000 SF

Gateway Park Tower514,500 SF

Gateway Park II190,900 SF

Gateway Park III190,900 SF

Gateway Park IV187,500 SF

LARGEST EMPLOYERS RECENT LEASES SIGNED

Wood Group10,960 Employees

BP9,537 Employees

ConocoPhillips3,000 Employees

Shell3,000 Employees

Methodist Hospital2,100 Employees

IHI171,426 SF

Cemex80,000 SF

WD Von Gonten & Co.73,000 SF

Schlumberger51,153 SF

Microsoft40,589 SF

LARGEST SUBLEASE SPACES LARGEST BLOCKS OF SPACE

Three Westlake Park215,861 SF

Two Westlake Park192,975 SF

10777 Clay Rd189,285 SF

16290 Katy Freeway155,050 SF

13111 Broadfield Blvd153,540 SF

13501 Katy Freeway331,707 SF

1414 Enclave300,907 SF

580 WestLake Park Blvd205,304 SF

17000 Katy Freeway174,469 SF

15150 Memorial Dr155,755

1

2

3

1

2

3

4

5

1

2

3

4

5

1

2

3

4

5

1

2

3

4

5

1

2

3

4

5

KATY FREEWAY SUBMARKET MAP

09KATY FREEWAY SUBMARKET UPDATE

2

825 Town & Country227,063 SF | 62.3% Leased

9811 Katy Freeway452,370 SF | 55.2% Leased4

4 5

*26 total buildings are being proposed.

5

3

3

34

The following graph illustrates the

historical rental and vacancy rates for

the submarket in both Class A and

Class B buildings.

RENTAL RATES & VACANCY

Class A Rate Class B Rate Class A Vacancy

3Q ‘08 3Q ‘09 3Q ‘10 3Q ‘11 3Q ‘12 3Q ‘13 3Q ‘14 3Q ‘15

Class B Vacancy

$30

$25

$20

$15

$10

$0

The following graph illustrates the

historical leasing activity for both

Class A and Class B buildings in the

submarket.

LEASING ACTIVITY

The following graph illustrates the

historical net absorption and square

feet delivered for both Class A and

Class B buildings in the submarket.

ABSORPTION & DELIVERIES

SF Leased Total Deals

1MSF

2MSF

3MSF

4MSF

5MSF

100

200

300

400

500

00 SF

‘00 ‘01 ‘02 ‘03 ‘04 ‘05 ‘06 ‘07 ‘08 ‘09 ‘10 ‘11 ‘12 ‘13 ‘14 ‘15

‘00 ‘01 ‘02 ‘03 ‘04 ‘05 ‘06 ‘07 ‘08 ‘09 ‘10 ‘11 ‘12 ‘13 ‘14 ‘15

SF Delivered YTD Absorption

-1MSF

0 SF

1MSF

2MSF

3MSF

4MSF

09 KATY FREEWAY SUBMARKET UPDATE

$5

$40

$35

12%

10%

8%

6%

4%

0%

2%

16%

14%

6MSF 600

$ 26.34$0.44 vs

2Q’15

0.7% vs 2Q’15

155K SF vs 2Q’15

Class A Class B

SF27K23K SF vs

2Q’15

OFFICE SNAPSHOT

Avg. Gross Rental Rate Avg. Gross Rental Rate

Vacancy Vacancy

Net Absorption Net Absorption

Construction Construction

$ 35.34$1.42 vs

2Q’15

%3.70.5% vs

2Q’15

68K382K SF vs

2Q’15

SF1.6M 0 SF vs

2Q’15

%7.7

SF SF79K

THE WOODLANDSSUBMARKET UPDATE

With several construction cranes dotting the horizon and

expanded/new corporate headquarters including Exxon,

Southwest Energy, and Anadarko, small and medium-sized

tenants in The Woodlands are finding themselves squeezed

for space and shocked by increases in rental rates.

MARKET TRENDS

MARKET DRIVERS

TENANT’S PERSPECTIVE

• In general, the average rental rate (Class A&B) has fluctuated,

but has remained in the $28.00 - $30.00 range in the past two

years; currently at $30.47 PSF gross.

• Vacancy has also fluctuated, between the 5% - 6% range over

the past year and half, and is currently at 5.5%.

• Development has slowed significantly.

• Absorption has kept pace with deliveries, and leasing activity

has slowed.

• Demand has come from corporate relocations and expansions

in the energy, medical and chemical sectors.

• Rates for Class B space have held steady due to companies

looking for value space that is near the new corporate

headquarters.

• Recent headquarter moves and expansions have improved

access and drive times, spurring additional development of

other office, retail, hotel, and residential projects.

• Increases in concessions will continue, especially in Class B

product.

• With higher vacancies, more space options are now available.

09

54

31 2

2

3

1

1

2

4

5

32

1

3

4

5

2

1

3

54

4

3

THE WOODLANDS SUBMARKET UPDATE09

UNDER CONSTRUCTION PROPOSED DEVELOPMENT

1725, 1735, 1780 Hughes Land.969,707 SF | 66% Leased

Havenwood Office Park240,470 SF | 0.0% Leased

Wildwood Corporate Centre II1.5 MSF | 100% Leased

10 Waterway Avenue500,000 SF

Superblock East654,119 SF

Superblock West400,000 SF

CityPlace I & II385,900 SF

Energy Crossing North288,000 SF

LARGEST EMPLOYERS RECENT LEASES SIGNED

Anadarko3,481 Employees

Aon Hewitt1,800 Empoloyees

Memorial Hermann1,400 Employees

St. Luke’s Hospital1,348 Employees

Lone Star College System1,178 Employees

HGA26,189 SF

Howard Hughes25,576 SF

Newfield24,910 SF

Undisclosed16,717 SF

Huckabee12,806 SF

LARGEST SUBLEASE SPACES LARGEST BLOCKS OF SPACE

2445 Technology Forest149,988 SF

10101 Woodloch Forest Dr25,879 SF

1450 Lake Robbins Dr24,331 SF

4055 Technology Forest Blvd23,894 SF

9303 New Trails Dr22,196 SF

8800 Technology Forest153,810 SF

1575 Sawdust Rd153,810 SF

2001 Timberloch Place90,539 SF

2445 Technology Forest36,314 SF

2829 Technology Forest36,314 SF

1

2

3

1

2

3

4

5

1

2

3

4

5

1

2

3

4

5

1

2

3

4

5

1

2

3

4

5

THE WOODLANDS SUBMARKET MAP

Springwoods Village150,000 SF | 33.3% Leased4

*13 total buildings are being proposed.

09THE WOODLANDS SUBMARKET UPDATE

The following graph illustrates the

historical rental and vacancy rates for

the submarket in both Class A and

Class B buildings.

RENTAL RATES & VACANCY

Class A Rate Class B Rate Class A Vacancy

3Q ‘08 3Q ‘09 3Q ‘10 3Q ‘11 3Q ‘12 3Q ‘13 3Q ‘14 3Q ‘15

Class B Vacancy

$40

$35

$30

$15

The following graph illustrates the

historical leasing activity for both

Class A and Class B buildings in the

submarket.

LEASING ACTIVITY

The following graph illustrates the

historical net absorption and square

feet delivered for both Class A and

Class B buildings in the submarket.

ABSORPTION & DELIVERIES

SF Leased Total Deals

0.3MSF

0.6MSF

0.9MSF

1.2MSF

1.5MSF

100

150

200

250

300

500 SF

‘00 ‘01 ‘02 ‘03 ‘04 ‘05 ‘06 ‘07 ‘08 ‘09 ‘10 ‘11 ‘12 ‘13 ‘14 ‘15

‘00 ‘01 ‘02 ‘03 ‘04 ‘05 ‘06 ‘07 ‘08 ‘09 ‘10 ‘11 ‘12 ‘13 ‘14 ‘15

SF Delivered YTD Absorption

0 SF

1MSF

2MSF

3MSF

4MSF

THE WOODLANDS SUBMARKET UPDATE09

$25

$20

12%

9%

6%

0%

3%

15%

HOUSTON ECONOMYFACTS & FIGURES

As anticipated, the third quarter continued to see low oil

prices, job losses and layoffs in the energy sector, M&A

activity, and falling rig counts and drilling permits.

Growth has slowed in foreign markets causing the demand

for Houston’s exports to decrease.

On the bright side, however, the U.S. economy is strong,

and local economists agree that the Houston economy in

resilient and will bounce back.

On the jobs front, although lower than normal, the year

should end with positive employment figures.

The following pages detail the state of the Houston economy

at the end of the third quarter of 2015.

10FORTUNE 500 COMPANIES

Houston ranks third among US metropolitanareas in Fortune 500 headquarters, with 26 companies based in the Houston MSA. More than 88% of these companies are in some way related to the energy industry.

Below is a list of all Fortune 500 companies headquartered in the Houston MSA as of June 2015:

Phillips 66#7

ConocoPhillips #51

Enterprise Products #59

Sysco#61

Plains GP Holdings #67

Halliburton #96

Occidental Petroleum#115

Baker Hughes #119

NOV#127

Anadarko Petroleum #162

EOG Resources #167

Kinder Morgan #193

Waste Management #217

Apache#218

Marathon Oil #227

Cameron Int. #275

Group 1 Automotive#291

CenterPoint Energy #313

Targa Resources #329

Calpine#353

FMC Technologies #357

Quanta Services #361

Buckeye Partners#406

KBR #424

MRC Global #448

Spectra Energy #449

Job growth in the Washington MSA has been

challenged by the contraction of the federal government.

Any improvement in the job growth rate will have to be

fueled by the private sector.

Job growth in the Washington MSA has been

challenged by the contraction of the federal government.

Any improvement in the job growth rate will have to be

fueled by the private sector.

Houston benefited from four years of exceptional

growth and due to this rapid economic expansion, the

city now ranks fourth in the nation in GDP producing

more than $525 billion annually.

If Houston were a country, its economy would be larger

than those of Argentina and Norway, according to the

World Bank, and would rank as the world’s 26th largest

economy. The city of Houston also has a GDP greater

than 42 states.

10 HOUSTON ECONOMY FACTS & FIGURES

New York CIty$1.6 Trillion

Los Angeles$867 Billion

Chicago$611 Billion

Houston$525 Billion

Venezuela$438 Billion

Norway$512 Billion

US GDP RANKING

WORLD GDP RANKING

Job growth in the Washington MSA has been

challenged by the contraction of the federal government.

Any improvement in the job growth rate will have to be

fueled by the private sector.

Houston’s economy grew 1.8% (net of inflation) in 214,

a slowdown from the previous four years. Houston’s

economic growth is projected to double between 2015

and 2040. Houston’s GDP also is projected to top $1.1

trillion by the end of 2027. The adjacent graph shows

the city’s economic makeup.

ECONOMIC GROWTH

Mining

Construction

Manufacturing

Trade

Transportation, Utilities, Warehousing

Information

Finance, Insurance, Real Estate

Services

Government

Agriculture

20.9%

19.3%

18.3%

4.6%

10.5%

1.5%

0.1%

11.9%

5.7%7.2%

Houston’s PMI registered 47.3 at

the end of August, down from 49.1

in July. Houston’s PMI has fallen

below the neutral point of 50 for eight

consecutive months.

Any reading below 50 signifies an

overall contraction in production.

Houston’s PMI had held at or above

the 50 point mark for 64 consecutive

months.

PMI RATING

According to the C2ER Cost of Living

Index for Q2 2015, Houston ranks

third in lowest overall cost of living

among the nation’s 20 most populous

metropolitan areas, with costs 20.5%

below the average for this group.

Houston’s housing costs are 35.9%

below this group’s average.

Houston’s overall after-taxes living

costs are 7.2% lower than the US

average, largely due to affordable

housing prices that are 7.3% below

the national average.

COST OF LIVING

10HOUSTON ECONOMY FACTS & FIGURES

2005 2007 2008 2009 2010 2011 2012 2013

30

40

50

60

70

2014 20152006

50-Point Baseline PMI Reading

PMI Reading

7.2%

10 HOUSTON ECONOMY FACTS & FIGURES

Houston is the “Energy Capital of the World” with almost half

of its economic activity driven by the energy industry. The

city is home to the largest concentration of human capital

and infrastructure for energy research, development, and

production in the nation.

Forty of the nation’s 134 publicly traded oil and gas

exploration and production firms, based in the US are

located in Houston, including 10 of the top 24.

In December 2014, the MSA held one third of the nation’s

jobs in oil and gas extraction and over 16% of jobs in support

activities for mining.

WTI reached a high of $108 in June 2014 before dropping

significantly in the fall. The price continued to drop into the

third quarter, registering in the low-$40s. The quarter ended

at $45.06.

Supply remains high and U.S. production is still going strong.

EIA forecasts have been revised downward stating that WTI

prices will range from $32/bbl to $67/bbl in January 2016

- volatility in oil prices is expected, as economist agree that

there are too many uncertainties.

OIL PRICES

ENERGY & OIL

WHAT EXACTLY CAUSED THE DROP IN OIL PRICES?

The drop in oil prices is due to many factors

but generally because supply is much higher

than demand.

Since 2010, prices hovered in the $100 per

barrel range with production not being able

to keep up with the increased demand.

These high oil prices led to an increase in

drilling, but then demand began to taper off

across Europe, Asia, and the U.S. Unused oil

was just being stockpiled away, causing the

dramatic decrease in prices, and with OPEC

states not agreeing to cut production, the

price of oil continues to fall.

FALLOUT FROM THE SLUMP

• 150,300 - Number of oil and gas extraction, oil

field services and oil field manufacturing jobs in

Houston

• 176,162 - Number of energy jobs cut worldwide

in the past year

• 13% - U.S. oil and gas employment managers

who say they’ve frozen recruitment

• $200,000 - Average wage, including benefits

and other perks, for an energy worker in

Houston

• 50% - Oil and gas contract workers worldwide

who say their pay has been cut in the past year

*Sources: Swift Worldwide Resources, Rigzone.com, Greater Houston Partnership – August 22, 2015

There is a correlation between the

success of the energy industry and

office rental rates, as well as leased

space, in Houston in the submarkets

that have a strong energy tenancy.

As the price of oil increases or de-

creases, Class A rents usually follow

suit, typically with a six-month lag.

With the decrease in the price of oil,

landlord concessions have increased

significantly.

RENT VS THE PRICE OF OIL

The average U.S. rig count for

September 2015 was 848, down

35 from the 883 counted in August

2015, and down 1,082 from the

1,930 counted in September 2014.

The monthly drop in rigs in 2015

reversed for the first time in July.

September’s rig fall takes the rig

count once again into a downtrend,

set earlier in the year.

OIL RIG COUNT

WTI Spot Price CBD

Oil Price Rental Rates

2013 2014

Rig Count

10HOUSTON ECONOMY FACTS & FIGURES

$160

$140

$120

$100

$80

$0

$40

$60

$20

$50

$45

$40

$35

$30

$10

$20

$25

$14

2015

2,100

1,900

1,700

1,500

1,300

500

900

1,100

700

Jan. Feb. March April May June July Aug. Sep. Oct. Nov. Dec.

Katy Fwy. The Woodlands

‘99 ‘00 ‘01 ‘02 ‘03 ‘04 ‘05 ‘06 ‘07 ‘08 ‘09 ‘10 ‘11 ‘12 ‘13 ‘14 ‘15

10 HOUSTON ECONOMY FACTS & FIGURES

POPULATION

Houston is the fourth largest city (2.2 million residents) and

fifth largest MSA in the nation, with approximately 6.5 million

residents. The MSA led the nation in population growth in

2014, adding 156,371 residents.

Houston is anticipated to lead the nation in population

and employment growth between 2015 and 2040, adding

125,000 new residents in 2015. The population is projected

to swell by nearly four million residents by the end of 2040.

POPULATION GROWTH

NEW ARRIVALS

2015 2040

The city of Houston is one of the fastest growing cities in

the U.S. 35,202 residents moved to Houston in 2014. That

is one new resident every 15 minutes. In the MSA, there is

approximately one new resident every 5 minutes.

X

6.5 Million 9.9 Million

10HOUSTON ECONOMY FACTS & FIGURES

Substantial diversification in Houston’s economy in the last

30 years has reduced its vulnerability to downturns in the

upstream energy sector. This is evident in today’s economy.

Drivers powering the rising economic diversification include:

DIVERSIFYING SECTORS

The Texas Medical Center is the

world’s largest medical complex,

with 56 member institutions and 7.2

million annual patient visits (16,000

international). Quality healthcare also

extends citywide, with nearly as many

jobs as the oil and gas field.

Houston is one of the world’s largest

petrochemical producing centers and

the $15 billion petrochemical complex

at the Houston Ship Channel is the

largest in the US and second largest

worldwide.

The region’s geographic location

makes it an easily-accessed portal to

the global marketplace. The Port of

Houston ranks first in the US in total

tonnage (for 22 years straight) and

waterborne cargo value.

Home to the Johnson Space Center,

and a diverse network of 50 research

and education organizations with ties

to aerospace technology, Houston is

a worldwide leader in the aerospace

industry.

Research and development is critical

to NASA’s Johnson Space Center,

the Texas Medical Center, the world’s

largest concentration of energy and

petrochemical companies, and major

universities across the region.

ECONOMIC DIVERSIFICATION

Up from 13% in the mid-1980s, diversifying sectors now contribute to approximately 50% of Houston’s economy.

Oil

Other

Oil

Other

1986

2015

HEALTHCARE PETROCHEMICALS TRADE

AIR & SPACE TECHNOLOGY

10 HOUSTON ECONOMY FACTS & FIGURES

According to the Greater Houston Partnership, Houston

area employment peaked at over 2.9 million in December

2014 and has trended downward ever since. Houston

employment remains 22,200 jobs below its 2014 peak.

EMPLOYMENT

NON-FARM EMPLOYMENT

• Total non-farm employment in the Houston MSA rose slightly

from the previous month to 2.98 million employed.

• From September 2014 to September 2015, local non-farm

employment rose 1.2%, or an increase of 36,200 jobs.

• Accommodation and Food Services, as well as Health Care

and Social Assistance registered the largest job gains since

December 2014, among Houston’s supersectors, adding

12,500 and 11,400 jobs respectively.

• The largest losses came from Trade, Transportation, and

Utilities (-15,000 jobs), and Manufacturing (-14,200 jobs).

• Houston’s September unemployment rate was 4.6%,

unchanged from August and down from 4.9% a year earlier.

JOB RECOVERY

JOB GROWTH

+Houston will account for 25% of all job growth in Texas between 2012 and 2040.

JOBS JOBS JOBS JOBS

Houston Rest of Texas

WORLDWIDE LAYOFFS (OVER 1,000)

EMPLOYMENT VS RENTAL RATE

3,100

2,900

2,700

2,500

2,300

2,100

$40

$35

$30

$25

$20

$5

Houston Rate Class A RateEmployment

‘12 ‘13 ‘14‘09 ‘10 ‘11‘06 ‘07 ‘08‘05

1,900

1,700

$15

$10

Class B Rate

‘15

Houston led the nation in job recovery, adding three new jobs for each lost in the “Great Recession”.

1,500 $0

Oilfield Services

Halliburton 18,000 Employees

Weatherford 14,000 Employees

Baker Hughes 13,000 Employees

Schlumberger 11,000 Employees

Petroleos Mexicanos 10,000 Employees

Schlumberger 9,000 Employees

Nabors Industries 3,480 Employees

Helmerich & Payne 2,130 Employees

FMC Technologies 2,079 Employees

Key Energy Service 2,000 Employees

Archer Ltd. 1,000 Employees

Civeo 1,000 Employees

Husky Oil Sands 1,000 Employees

Precision Drilling 1,000 Employees

E&P

Shell 7,000 Employees

Total 2,000 Employees

Sasol 1,500 Employees

Suncor Energy 1,000 Employees

Manufacturing

US Steel 3,827 Employees

Vallourec 1,400 Employees

“

HOUSING

After a relatively mild August, the Houston housing market

kept pace with 2014’s record sales volumes and prices.

Single-family home sales saw a moderate increase of 3.5%,

and it took 49 days on average to sell the average home.

Houston’s average sales price for a single-family home is

$270,901, a 0.5% increase over the previous year. The

median price for a single-family home also increased to

$208,000, a year-over-year increase of 4.5%.

Houston’s median house price is third lowest among the ten

largest U.S. metropolitan areas, however, the city ranked

fourth in median sales price gain since 2012.

10HOUSTON ECONOMY FACTS & FIGURES

“September showed a bit more vitality than August, and

considering that we are comparing to a record 2014

sales year and remain in a climate of energy-related

layoffs, I’d say that the Houston real estate market is

truly holding its own... Sales inventory has been stable

for the past three months and we expect it to grow in

the last quarter of 2015.”

- HAR Chair, Nancy Furst

FOREIGN TRADE

In 2014, more than $253.3 billion in foreign trade passed through

the Houston-Galveston Customs District, up 0.6% from the

$251.8 billion handled in 2013. Exports accounted for a majority

of the growth.

According to the Greater Houston Partnership, through August

of this year, more than $138.3 billion in foreign trade passed

through the Houston-Galveston Customs District, down 20.2%

from the $173.3 billion in trade handled in the first eight months

of 2014. The decrease in trade value is expected given the drop

in oil prices. Total trade is up when measuring year-to-date

vessel weight, increasing 2.5% to 169.2 billion kilograms.

$40 $47$58

$72$90

$75$95

$119 $127 $129 $132$65

$89

$92$104$113

$151

$117

$149$147

$123 $122

10 HOUSTON ECONOMY FACTS & FIGURESB

illion

s $300

$250

$200

$150

$100

$50

$0

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Exports Imports

11

MARKET OUTLOOK

The outlook for Houston’s economy in the last quarter of

2015 has turned negative. What was a cautiously optimistic

attitude at the beginning of the year has changed midway

through the year, with a recovery not anticipated until at least

the end of 2016.

2015 OUTLOOK

• Worldwide job cuts, reduced capital budgets, reduced

exploration expenditures, and M&A activity continue, adding

to the already large number of subleases and empty blocks of

space.

• Even though rig counts are down, crude oil inventories remain

high and domestic production remains at elevated levels –

showing only small signs of improvement.

• The jobs forecast was revised downward from 62,000

anticipated new jobs in 2015, to 20,000 – 30,000.

• Office development has slowed (if it’s not under construction

already, it likely won’t break ground in 2015). A glut of office

space has been delivered this year. With more product coming

online this year and next, vacancy rates are anticipated to

increase.

• Leasing activity has weakened significantly.

• Due to these market conditions landlord concessions have

increased and rental rates are flattening.

• A return to “normal” is anticipated in 12 - 18 months.

CONTACT US

Cresa © 2015. All rights reserved.

Permission is hereby granted for internal distribution by Cresa business partners. Other

reproduction by any means in whole or part without written permission is prohibited. For

additional information, please contact Elia Quiles, Director of Marketing & Research, at

713.402.5811 or [email protected].

Cresa Houston

5599 San Felipe, Suite 500

Houston, Texas 77056

713.402.5800