Embed Size (px)

Citation preview

Housing Treasury – Financing Risk

B5: Key developments in the bank lending and private placement markets

Speaker: Phil JenkinsPartner

Centrus Advisors

Chair: Paul JacksonTreasury Independent

Housing Treasury – Financing Risk

B5: Key developments in the bank lending & private placements markets

23 October 2013

T R E A S U R Y & D E R I VAT I V E S D E B T A D V I S O R Y P R O J E C T F I N A N C E C O R P O R AT E F I N A N C E ⎢ ⎢ ⎢

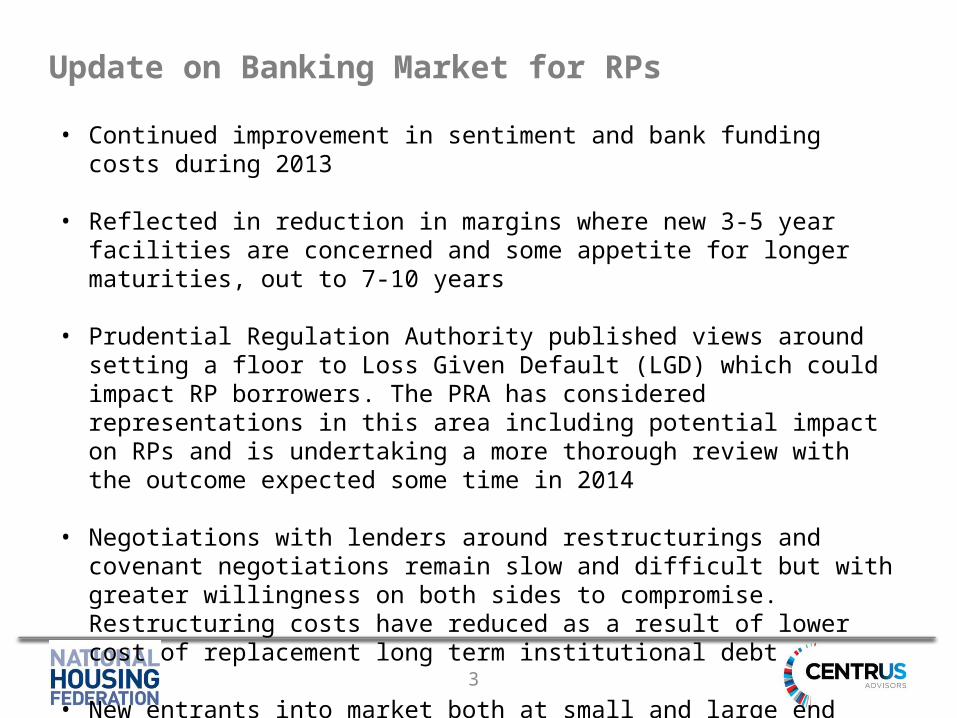

Update on Banking Market for RPs

3

• Continued improvement in sentiment and bank funding costs during 2013

• Reflected in reduction in margins where new 3-5 year facilities are concerned and some appetite for longer maturities, out to 7-10 years

• Prudential Regulation Authority published views around setting a floor to Loss Given Default (LGD) which could impact RP borrowers. The PRA has considered representations in this area including potential impact on RPs and is undertaking a more thorough review with the outcome expected some time in 2014

• Negotiations with lenders around restructurings and covenant negotiations remain slow and difficult but with greater willingness on both sides to compromise. Restructuring costs have reduced as a result of lower cost of replacement long term institutional debt

• New entrants into market both at small and large end

4

Desired Outcomes: A Divergence of Views

Divergence

remains but the ‘gap’ has

reduced over the past 6 – 12 months

Engagement with Lender(s) requires careful planning &

implementation beforehand

Borrower Objective

How can we protect the embedded value

in existing loan arrangements and

any other advantageous

commercial terms ?

Lender Objective

How can we use this to renegotiate the existing loan(s) ?

MarginTerm

PrepaymentHedging

FeesAsset CoverCovenantsRestrictions

Bond Mandates

Factors Driving Economics of Restructure

5

Factor Restructure Parameters

Starting point – has loan already been re-priced or not?

Dynamic of margin increases vs prepayments (cost of replacement debt?)

Degree of covenant headroom sought – will lenders see a 2nd bite of the cherry?

“Expected life” i.e. how much value do you ascribe to latter years?

Strength of existing lender relationships How to deal with syndicated arrangements?

Embedded hedging which may limit scope of prepayment

Clear understanding of the costs associated with hedging restructures

Clarity around legal position where consents etc. concerned

Ability to consistently compare proposals involving materially different terms

Availability of a robust “Plan B” and a willingness to follow through with it

What can borrowers “put on the table” e.g. ancillary business

Illustrations of Recent LSVT Restructures

6

LSVT 1 LSVT 2 LSVT 3*

Deal type Full LSVT covenant removal

Full LSVT covenant removal

Full LSVT covenant removal

Prepayment (as % of original facility)

35% 25% 0%

Original margin c.30bps c.90bps c.35bps

Renegotiated margin

c.100bps c.140bps c.200bps

Cost as % of original debt

11% 8% 19%

*LSVT 3 – Centrus has subsequently been appointed to seek improvement to terms since receipt of original offer

Summary Around Bank Negotiations

7

• Key issues from borrower perspective• Clarity around legal position• Development of credit story (e.g. around mergers)• Development of a clear lender engagement strategy (specific to each lender)

• Do you have a credible Plan B?• Is it aligned with corporate strategy• Are you prepared to follow through with it if necessary?

• Quantification• Are you able to quantify complex restructures often involving hedging?• Do you have sufficient access to market information in order to benchmark

proposals?

• Mergers • Some thoughts around the “path of least resistance”

Private Placements: An Evolving Arena

UK investor market continues

to adapt to the post-bank dominated

funding environment

Public bond issuance now well established with investors looking

through credit ratings in terms of

pricing differentiation

Rapidly evolving market for listed and bilateral PPs as well as other formats such as retail bonds and

sale and leaseback

Increasing range of formats and options for borrowers

• RPs need to understand full range of options & where these are best applied

• RPs are increasingly moving away from a standardised funding model

• Widening investor base caters for most current forms of requirement

8

Market Developments During 2013*

9

Issuer Key Features Other Comments

£100m shelf facility with Pricoa Capital offering uncommitted but highly certain facility with drawdown flexibility

Pricing highly competitive to public bond market where investor has appetite for the credit in question

Pricing @ +112bps represented narrowing of previous differential between larger deals/issuers and smaller ones

Bought by a single new investor to the sector, unclear at this stage whether one-off or more sustained pattern

Heavily deferred structure, £1m drawn up front with £49m drawn at agreed rate in 2017

Unusual structure requiring co-incidence of needs between borrower and investor. Cost of carry savings offset by higher coupon/margin

£50m retained bonds issued through innovative auction process at differential spreads

Allowed Moat to tap into different levels of demand and pricing appetite as opposed to a classic “clearing price” via book building

Unsecured structure with funding SPV guaranteed by non asset owning parent company. Rated AA- by Fitch

More expensive on a spread to gilts basis than conventional funding but offers flexibility and a robust “Plan B”

*based upon available information

Private Placement & Other Non-bank Options

10

•Question•Consideration

Public Bond

Agented PP

Bilateral PP

S&L

Retail Bond

Listed PP

• All options have their place

• Highly dependent on borrowers’ objectives which are increasingly diverging

• Important to understand and align with investor appetite & objectives

• Large investors may operate across many formats

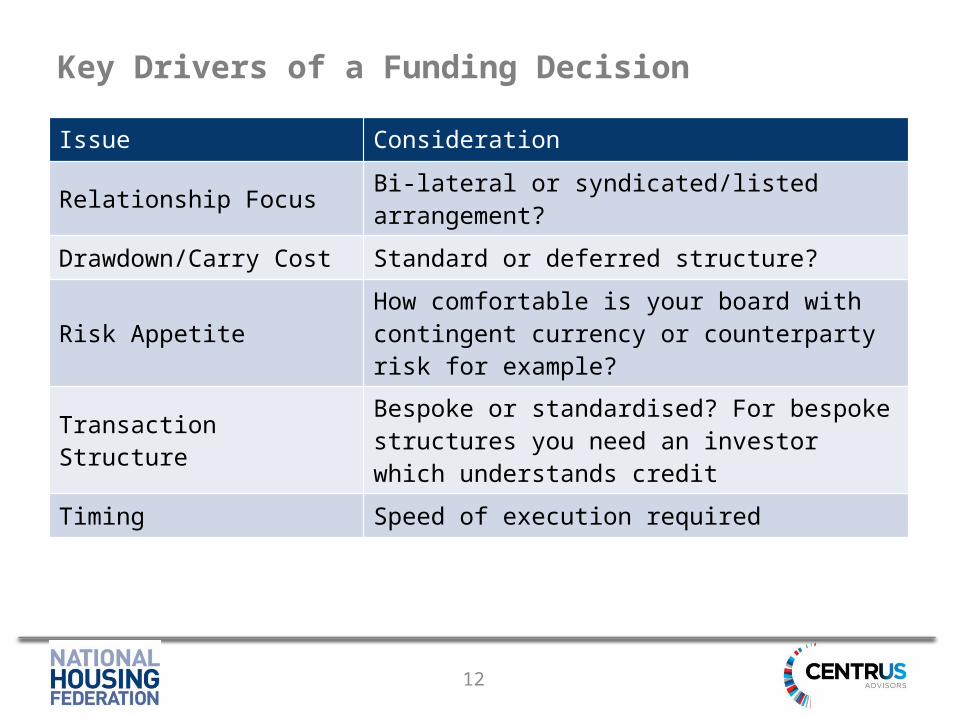

Key Drivers of a Funding Decision

11

•Question•Consideration

Issue Consideration

Size Of organisation and funding requirement

Borrowing FrequencyHow often are you planning to return to the market?

Credit Quality Comparison with peers

Execution Risk Understanding the risks of different strategies

Credit Rating Do you want to maintain a public rating?

Covenant Capacity & Regulatory Considerations

Recourse or non-recourse solution with the latter taking on greater significance for commercial activity

Security Availability Is security efficiency critical?

Covenant Structure Covenanted or non-covenanted transaction?

Key Drivers of a Funding Decision

12

•Question•Consideration

Issue Consideration

Relationship Focus Bi-lateral or syndicated/listed arrangement?

Drawdown/Carry Cost Standard or deferred structure?

Risk AppetiteHow comfortable is your board with contingent currency or counterparty risk for example?

Transaction StructureBespoke or standardised? For bespoke structures you need an investor which understands credit

Timing Speed of execution required

Features of Alternative Formats

13

Public Bond

Listed PP

Bilateral PP

• Large issuers/issue size

• Standard format & process

• Financial covenants Y/N

• Higher execution risk • Widest investor pool• Listed bond docs• Retained bonds• Rated

• Smaller issuers/issue size

• Standard format• Financial covenants

Y/N• Lower execution risk • Smaller investor pool• Listed bond docs• Deferral options• Usually rated• Price tension/cost

• Smaller issuers/issue size

• Complex or highly bespoke deals

• Financial covenants Lower execution risk

• Smallest investor pool• Loan/NPA docs• Rated or unrated• Deferral options• Speed of execution

Evolving Funding Market for a Rapidly Changing Sector

14

• The financing market for RPs continues to evolve rapidly in response to the changing funding requirements of different RPs

• We expect to see continued divergence away from “standardised” funding as corporate structures change in response to regulation and capacity issues

• Increasing need for highly bespoke funding structures which require investors with real internal credit capability

• Affordable Guarantee Scheme – “The solution looking for a problem”

• Existing legacy bank debt and derivatives will continue a slow but inevitable unwinding and re-structuring with some forced to the negotiating table sooner than others

15

Questions & Discussion

16

Centrus Advisors LLP is an appointed representative of Pegasus Capital LLP which is authorised and regulated by the Financial Conduct Authority, Firm Reference Number 552790. Please visit www.fca.gov.uk/register/home.do for more information. Centrus Advisors LLP is a limited liability partnership incorporated in England and Wales with number OC378028. Registered office at Fleet House, 8-12 New Bridge Street, London EC4V 6AL.

The information contained in this presentation obtained from sources other than Centrus Advisors LLP (“Centrus”) has been compiled by Centrus from sources believed to be reliable, but no representation or warranty, express or implied, is made by Centrus, its affiliates or any other person as to its accuracy, completeness or correctness. This presentation is being provided to you based on our reasonable belief that you are a sophisticated institutional investor that is capable of assessing the merits and risks of the transactions and financial matters discussed herein. All opinions and estimates contained in this presentation constitute Centrus’ judgement as of the date of this presentation, are subject to change without notice and are provided in good faith but without legal responsibility. This presentation is not an offer to sell or a solicitation of an offer to buy any securities. This presentation is not, and under no circumstances should be construed as, a solicitation to act as securities broker or dealer in any jurisdiction by any person or company that is not legally permitted to carry on the business of a securities broker or dealer in that jurisdiction. To the full extent permitted by law neither Centrus nor any of its affiliates, nor any other person, accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or the information contained herein. No matter contained in this document may be reproduced or copied or passed to any other party by any means without the prior consent of Centrus.

All rights reserved.

![Policy B5: Medical - Queen Margaretsqueenmargarets.com/wp-content/uploads/2015/04/Policy-B5-Medical... · [QUEEN MARGARETS, YORK] Policy B5 Policy B5: Medical 1 Policy B5: Medical](https://img.dokumen.tips/doc/110x75/5b8a500b7f8b9a655f8e0e3f/policy-b5-medical-queen-mar-queen-margarets-york-policy-b5-policy-b5.jpg)

![3URWRNROOEHVFKUHLEXQJ /(*,&B5:B - RFID-Webshop 13.56... · 3urwrnrooehvfkuhlexqj /(*,&b5:b (uvwhoogdwxp ˇ˛ 6hlwhˇyrq /(*,&b5:b b5(9 ˘ grf 6dw]duwhq 'dwhqohvhq qlfkwvhjphqwlhuwh/(*,&](https://img.dokumen.tips/doc/110x75/5ab441397f8b9adc638bdd67/3urwrnrooehvfkuhlexqj-b5b-rfid-13563urwrnrooehvfkuhlexqj-b5b-uvwhoogdwxp.jpg)