Embed Size (px)

Citation preview

HOUSING REPORTSOUTHEAST MICHIGAN | OCTOBER 2020

OCTOBER 2020HOUSING REPORT

Southeast Michigan

Strong Housing SignalsThe housing market continues to be a bright spot for the economy with increased interest from buyers for single family housing. If homes continue to sell at the current pace, we may remain in a seller’s market all winter. In Michigan, there are many factors that lead to the slowing of sales in the colder months but due to the shutdown in spring, we currently see a carryover of demand from buyers who are still interested in the limited inventory available.

Delayed Cooldown

2019 was a strong year and, in the midst of the global pandemic, the summer months provided a record number of sales in 2020. Even better, recent new pending contracts are still hitting highs, which will ensure strong closed sales through the fourth quarter as we head into winter.

While it may seem like the market is slowing, it may take an extra month or two to really cool off. The third quarter set new records for both closed sales and home values. Monthly price per square foot for a typical year peaks in July, but this year it looks to have been pushed back to September. Furthermore, days on market have also been on the decline through September indicating that homes are still selling quickly.

Out of Supply

Inventory is down 48% from 2019, while pending sales are up 35% from last year. Tight supply has created heavy competition among buyers for homes in our market. Months supply of inventory increased just slightly from last month up 4%. In 2019, months’ supply of inventory was at 2.9 months in September, in comparison right now we only have 1.2 months of supply which is not typical this time of year. Months’ supply refers to the number of months it would take for the current inventory of homes on the market to sell given the current sales pace. Historically, six months of supply is associated with moderate price appreciation, so lower levels of supply tend to push prices up more rapidly. Sellers who haven’t gotten a quick hit should remain patient and give buyers time to take a second look and make a deal.

Month July '19 Aug '19 Sep '19 Q3 '19Sales 4976 5111 4453 14,540

MoM 6% 3% -13%$/SF 143.83$ 142.91$ 140.02$

MoM 1% -1% -2%DOM 35 38 42

MoM -5% 8% 12%Month Jul '20 Aug '20 Sep '20 Q3 '20

Sales 5866 5634 5266 16,766 MoM 39% -4% -7% 19 vs 20

$/SF 153.16$ 152.32$ 153.50$ 15%MoM 4% -1% 1%

DOM 42 39 36MoM -7% -9% -7%

Copyright 2020, Real Estate One

OCTOBER 2020HOUSING REPORT

Southeast Michigan

Buyer Pipeline

Mortgage applications are up 30% from a year ago and there are plenty of active buyers lined up in the pipeline. This is great news for sellers as the strong demand has been driving up prices faster in the past few months than at any time in recent years. While this is fantastic for a homeowner’s equity, the limited inventory, rapid price increase and growing competition may choke off some of the buyers that are trying to move through the market. When first-time homeowners are unable to complete the purchase process, the rate of homeownership declines.

Working from home for good?

Most teleworkers expect to continue at home even after a Covid Vaccine. While not all industries and positions have this luxury, many may not be going back to the office. Currently about 3 out of every 10 adults are working from home either full or part time. Sixty-one percent of those working from home believe they will continue to work from home even after a vaccine is distributed. How will this impact home buying priorities and decisions? If around 20% of the working population goes home full time, they may be putting more of an emphasis on home expenditures.

Noteworthy News

• Builder confidence reaches record high.

• Coronavirus-related evictions delayed until 2021.

• Single-family housing starts reaches highest levels since 2007.

• Coronavirus second surge beginning to show signs across the country. Michigan numbers are on the rise.

• Mortgage rates fall to a record low for the 11th time this year.

• Second stimulus negotiations have been delayed, most likely to come after the election.

Copyright 2020, Real Estate One

OCTOBER 2020HOUSING REPORT

$100

$110

$120

$130

$140

$150

$160

$170

0

1,000

2,000

3,000

4,000

5,000

6,000

Dec '18 Mar '19 Jun '19 Sep '19 Dec '19 Mar '20 Jun '20 Sep '20

Closed Single-Family Home Sales

5-County Summary

34,673YTD CLOSED SALES

-7% from last year

$257KYTD AVG SALE PRICE

+8% from last year

6,593AVAILABLE LISTINGS-10% from last month

5,548NEW PENDINGS

-13% from last month

$146YTD PRICE PER SQ FT

+6% from last year YTD Closed Volume: $8.9B (0%)

MONTHLY SALES $/SF

Southeast Michigan

15% 23%

-34%

-99%

4%31% 34% 34% 34%

-120%

-100%

-80%-60%

-40%

-20%

0%

20%

40%

60%

-

50,000

100,000

150,000

200,000

Jan Feb Mar Apr May Jun Jul Aug Sep

Monthly Showings2019 v 2020

2019 2020 +/-

50

100

150

200

250

300

7/1/207/8/20

7/15/20

7/22/20

7/29/208/5/20

8/12/20

8/19/20

8/26/209/2/20

9/9/20

9/16/20

9/23/20

9/30/20

10/7/20

SEMI Daily New PendingsCombined SF and Condos

'19 Pendings '20 Pendings

Jul 1 — Oct 137-day Avg

New PendingsRunning 28% higher

-9% -13% -13% -13%-21% -27% -35%

-41%-47%

-51%-6 0%

-5 0%

-4 0%

-3 0%

-2 0%

-1 0%

0%

0

5000

10000

15000

20000

Jan Feb Mar Apr May Jun Jul Aug Sept Oct

Inventory2019 v 2020

2019 2020 +/-

First Day of Month

Market activity continues to be strong despite having half as many available listings as this time last year. September new pendings dropped off slightly compared to the prior month but were up 35% compared to last year. As seen above, daily new pendings continue to run nearly 30% higher than a year ago. YTD closed sales are down 7%, but that gap is narrowing (it was 12% last month) and closed sales should be even by the end of the year. Values continue to rise with YTD average sale price up 8% and price per square foot up 7%. The market continues to be strong as it’s started into the fourth quarter. It’s not too late for sellers to jump in and take advantage of the great market opportunities.

Copyright 2020, Real Estate One

OCTOBER 2020HOUSING REPORT

Southeast Michigan

-

50,000

100,000

150,000

200,000

Jan Feb Mar Apr May Jun Jul Aug Sep

Monthly Showings2019 v 2020

2019 2020

+34%

-

10,000

20,000

30,000

40,000

50,000

60,000

Jan Feb Mar Apr May Jun Jul Aug Sep

<$150k Showings2019 v 2020

2019 2020

+18%

-

20,000

40,000

60,000

80,000

Jan Feb Mar Apr May Jun Jul Aug Sep

$150k-$300k Showings2019 v 2020

2019 2020

+39%

-

20,000

40,000

60,000

80,000

Jan Feb Mar Apr May Jun Jul Aug Sep

$150k-$300k Showings2019 v 2020

2019 2020

+39%

Showing Activity

-

5,000

10,000

15,000

20,000

Jan Feb Mar Apr May Jun Jul Aug Sep

>450k Monthly Showings2019 v 2020

2019 2020

+55%

Copyright 2020, Real Estate One

OCTOBER 2020HOUSING REPORT

Oakland CountySingle-Family Homes

11,589YTD CLOSED SALES

-6% from last year

$339KYTD AVG SALE PRICE

+6% from last year

2,356AVAILABLE HOMES-6% from last month

1,806NEW PENDINGS

-10% from last month

$170YTD PRICE PER SQ FT

+5% from last year

Closed Sales

$120

$130

$140

$150

$160

$170

$180

0

400

800

1,200

1,600

2,000

Dec '18 Mar '19 Jun '19 Sep '19 Dec '19 Mar '20 Jun '20 Sep '20

MONTHLY SALES $/SFYTD Closed Volume: $3.9B (0%)

13% 19%

-35%

-99%

2%

26% 27% 29% 28%

-120%

-100%

-80%

-60%

-40%

-20%

0%

20%

40%

-

10,000

20,000

30,000

40,000

50,000

60,000

70,000

Jan Feb Mar Apr May Jun Jul Aug Sep

Monthly Showings2019 v 2020

2019 2020 +/-

0

10

20

30

40

50

60

70

80

7/1/207/8/20

7/15/20

7/22/20

7/29/208/5/20

8/12/20

8/19/20

8/26/209/2/20

9/9/20

9/16/20

9/23/20

9/30/20

10/7/20

Daily New PendingsSingle Family

'19 Pendings '20 Pendings

Jul 1 — Oct 137-day Avg

New PendingsRunning 28% higher

-12%-19% -21% -21%

-30% -31% -39% -39%-45%

-49%-6 0%

-5 0%

-4 0%

-3 0%

-2 0%

-1 0%

0%

0

1000

2000

3000

4000

5000

6000

Jan Feb Mar Apr May Jun Jul Aug Sept Oct

Inventory2019 v 2020

2019 2020 +/-

First Day of Month

New pending sales activity continues to outpace last year, despite buyers having half as many available listings to choose from. Fierce competition continues to have buyers bidding prices up for move-in-ready homes in the entry and middle price ranges. With closer-to-normal inventory in the upper price ranges, sales are brisk, but values are flat. YTD closed sales are down 6% but that gap shrinks each month and should be gone before the end of the year. YTD closed volume is already even. It’s not too late for potential sellers who were distracted by one of 2020’s curveballs to take advantage of its strong real estate market. The shortage of entry and mid-value listings will continue to provide seller opportunities through the balance of the year.

Copyright 2020, Real Estate One

OCTOBER 2020HOUSING REPORT

BirminghamSingle-Family Homes

327YTD CLOSED SALES

+2% from last year

$766KYTD AVG SALE PRICE

+2% from last year

140AVAILABLE HOMES

-14% from last month

65NEW PENDINGS

+14% from last month

$300YTD PRICE PER SQ FT

+4% from last year

Closed Sales

$220

$240

$260

$280

$300

$320

$340

0

10

20

30

40

50

60

Dec '18 Mar '19 Jun '19 Sep '19 Dec '19 Mar '20 Jun '20 Sep '20

MONTHLY SALES $/SFYTD Closed Volume: $250M (+3%)

14% 15%-50%

-100%-29%

-7% -1%27% 18%

60%

-120%-100%-80%-60%-40%-20%0%20%40%60%80%

-

500

1,000

1,500

2,000

Jan Feb Mar Apr May Jun Jul Aug Sep Oct21st

Monthly Showings2019 v 2020

2019 2020 +/-

0

1

2

3

7/1/207/8/20

7/15/20

7/22/20

7/29/208/5/20

8/12/20

8/19/20

8/26/209/2/20

9/9/20

9/16/20

9/23/20

9/30/20

10/7/20

Daily New PendingsSingle Family

'19 Pendings '20 Pendings

Jul 1 — Oct 137-day Avg

-13% -17%-22%

-26%

-44%

-32%-31% -30% -29%

-37%

-5 0%-4 5%-4 0%-3 5%-3 0%-2 5%-2 0%-1 5%-1 0%-5 %0%

0

50

100

150

200

250

300

Jan Feb Mar Apr May Jun Jul Aug Sept Oct

Inventory2019 v 2020

2019 2020 +/-

First Day of Month

Although inventory continues to drop and is down 37% compared to a year ago, sales activity has been strong. Upper-end sales activity was slow to restart in May but continues to gain momentum. September showings were up 60% compared to last year and YTD closed sales caught and surpassed 2019 numbers. As shown by the price per square foot ($/SF) line in the top chart. Values, which were down earlier this year, have been climbing rapidly since July. With the inventory shortage and buyers competing for well-appointed homes, it’s not too late for sellers to take advantage of the strong market.

Copyright 2020, Real Estate One

OCTOBER 2020HOUSING REPORT

Macomb CountySingle-Family Homes

7,392YTD CLOSED SALES

-10% from last year

$227KYTD AVG SALE PRICE

+8% from last year

1,075AVAILABLE HOMES-3% from last month

1,222NEW PENDINGS

-8% from last month

$136YTD PRICE PER SQ FT

+6% from last year

Closed Sales

$90

$100

$110

$120

$130

$140

$150

$160

0

400

800

1,200

Dec '18 Mar '19 Jun '19 Sep '19 Dec '19 Mar '20 Jun '20 Sep '20

$/SFYTD Closed Volume: $1.6B (-2%)MONTHLY SALES

15%33%

-36%

-99%

6%

41% 40% 42% 48%

-120%

-100%

-80%-60%

-40%

-20%

0%

20%

40%

60%

-

5,000

10,000

15,000

20,000

25,000

30,000

Jan Feb Mar Apr May Jun Jul Aug Sep

Monthly Showings2019 v 2020

2019 2020 +/-

0

5

10

15

20

25

30

35

40

45

50

7/1/207/8/20

7/15/20

7/22/20

7/29/208/5/20

8/12/20

8/19/20

8/26/209/2/20

9/9/20

9/16/20

9/23/20

9/30/20

10/7/20

Daily New PendingsSingle Family

'19 Pendings '20 Pendings

Jul 1 — Oct 137-day Avg

Roughly 30% Higher

-12% -13% -11%-13%-18%

-28% -35%-42%

-49%-53%

-6 0%

-5 0%

-4 0%

-3 0%

-2 0%

-1 0%

0%

0

500

1000

1500

20002500

3000

3500

Jan Feb Mar Apr May Jun Jul Aug Sept Oct

Inventory2019 v 2020

2019 2020 +/-

First Day of Month

Inventory continues to decline—down 53% compared to last year. Despite the lower inventory, both showings and new pendings are up compared to the same time last year. The additional activity is narrowing the YTD closed sales gap. A month ago it was 15%. This month it’s 10%. The additional new pendings will continue to cause that gap to narrow over the next few months. Low interest rates and high demand continue to drive up values. YTD average sale price and price per square foot are both up—8% and 6% respectively. Looking at the price per square foot ($/SF) line in the top chart, values which dipped during the shutdown have been rapidly rising in recent months. It’s a great time to sell.

Copyright 2020, Real Estate One

OCTOBER 2020HOUSING REPORT

St. Clair ShoresSingle-Family Homes

768YTD CLOSED SALES

-9% from last year

$185KYTD AVG SALE PRICE

+8% from last year

73AVAILABLE HOMES

no change from last month

128NEW PENDINGS

-3% from last month

$144YTD PRICE PER SQ FT

+7% from last year

Closed Sales

$90

$100

$110

$120

$130

$140

$150

$160

0

20

40

60

80

100

120

140

Dec '18 Mar '19 Jun '19 Sep '19 Dec '19 Mar '20 Jun '20 Sep '20

$/SFYTD Closed Volume: $142M (-1%)MONTHLY SALES

-12%

19%

-26%

-98%

9%

38%

11%24%

42%

-120%

-100%

-80%

-60%

-40%

-20%

0%

20%

40%

60%

-

500

1,000

1,500

2,000

2,500

Jan Feb Mar Apr May Jun Jul Aug Sep

Monthly Showings2019 v 2020

2019 2020 +/-

0

1

2

3

4

5

6

7

7/1/207/8/20

7/15/20

7/22/20

7/29/208/5/20

8/12/20

8/19/20

8/26/209/2/20

9/9/20

9/16/20

9/23/20

9/30/20

10/7/20

Daily New PendingsSingle Family

'19 Pendings '20 Pendings

Jul 1 — Oct 137-day Avg

-9% -9%

9%

-4% -9%-24%

-38% -40%-49%

-48%-6 0%

-5 0%

-4 0%

-3 0%

-2 0%-1 0%

0%

10%

20%

0

50

100

150

200

250

Jan Feb Mar Apr May Jun Jul Aug Sept Oct

Inventory2019 v 2020

2019 2020 +/-

First Day of Month

Inventory is down 48% from last year and existing listings are selling faster than new ones arrive on the market. Despite the lack of inventory, intense buyer demand had September showings up 42% and new pendings 49% higher than last year. September closed sales were up from August and it was the second highest closed sales month in the past two years. Values continue to rise—average sale price is up 8% and price per square foot is up 7% compared to last year. Looking at the price per square foot ($/SF) line in the top chart, prices have been rising rapidly in recent months. For sellers who are thinking about making their move, it’s not too late to cash in on a great seller’s market.

Copyright 2020, Real Estate One

OCTOBER 2020HOUSING REPORT

Wayne CountySingle-Family Homes

12,101YTD CLOSED SALES

-9% from last year

$190KYTD AVG SALE PRICE

+10% from last year

2,538AVAILABLE HOMES-3% from last month

1,978NEW PENDINGS

-8% from last month

$122YTD PRICE PER SQ FT

+7% from last year

Closed Sales

$80

$90

$100

$110

$120

$130

$140

0

400

800

1,200

1,600

2,000

Dec '18 Mar '19 Jun '19 Sep '19 Dec '19 Mar '20 Jun '20 Sep '20

$/SFYTD Closed Volume: $2.3B (0%)MONTHLY SALES

17% 23%

-31%

-98%

2%

33% 40% 36% 36%

-120%

-100%

-80%

-60%

-40%

-20%

0%

20%

40%

60%

-

10,000

20,000

30,000

40,000

50,000

60,000

70,000

Jan Feb Mar Apr May Jun Jul Aug Sep

Monthly Showings2019 v 2020

2019 2020 +/-

0

10

20

30

40

50

60

70

80

7/1/207/8/20

7/15/20

7/22/20

7/29/208/5/20

8/12/20

8/19/20

8/26/209/2/20

9/9/20

9/16/20

9/23/20

9/30/20

10/7/20

Daily New PendingsSingle Family

'19 Pendings '20 Pendings

Jul 1 — Oct 137-day Avg

New PendingsRunning 25 to 35% higher

-6% -8% -10% -9%-17% -23%

-33%

-43%-48%

-51%-6 0%

-5 0%

-4 0%

-3 0%

-2 0%

-1 0%

0%

0

1000

2000

3000

40005000

6000

7000

Jan Feb Mar Apr May Jun Jul Aug Sept Oct

Inventory2019 v 2020

2019 2020 +/-

First Day of Month

Although available inventory is half of what it was a year ago, strong market performance in three consecutive months has been lifting the bar and setting new records for both sales and value. While YTD closed sales are down 9%, the gap is narrowing and with recent new pendings (see chart above) running above last year’s pace, the gap will continue to shrink. Low interest rates and high buyer demand continue to lift values. As seen in the top chart, average price per square foot in the third quarter was the highest it has ever been. Looking ahead, demand and low interest rates will continue to drive the market, but the lack of inventory will limit sales. The market will continue to thrive through the fourth quarter. Potential sellers shouldn’t hesitate to jump in.

Copyright 2020, Real Estate One

OCTOBER 2020HOUSING REPORT

Grosse PointeSingle-Family Homes

616YTD CLOSED SALES

-4% from last year

$407KYTD AVG SALE PRICE

+12% from last year

188AVAILABLE HOMES-6% from last month

94NEW PENDINGS

-3% from last month

$174YTD PRICE PER SQ FT

+5% from last year

Closed Sales

$120

$130

$140

$150

$160

$170

$180

0

25

50

75

100

125

Dec '18 Mar '19 Jun '19 Sep '19 Dec '19 Mar '20 Jun '20 Sep '20

$/SFYTD Closed Volume: $251M (+7%)MONTHLY SALES

-10%

30% -41%-99%

10%-15% 40%

58% 57%

-120%-100%-80%-60%-40%-20%0%20%40%60%80%

- 200 400 600 800

1,000 1,200 1,400 1,600

Jan Feb Mar Apr May Jun Jul Aug Sep

Monthly Showings2019 v 2020

2019 2020 +/-

0

1

2

3

4

5

6

7/1/207/8/20

7/15/20

7/22/20

7/29/208/5/20

8/12/20

8/19/20

8/26/209/2/20

9/9/20

9/16/20

9/23/20

9/30/20

10/7/20

Daily New PendingsSingle Family

'19 Pendings '20 Pendings

Jul 1 — Oct 137-day Avg

-7%-5% -3% -1%

-8%

-1%

-21%-26% -26%

-34%-4 0%

-3 5%

-3 0%

-2 5%

-2 0%-1 5%

-1 0%

-5 %

0%

0

50

100

150

200250

300

350

Jan Feb Mar Apr May Jun Jul Aug Sept Oct

Inventory2019 v 2020

2019 2020 +/-

First Day of Month

Inventory continues to shrink, but despite that, new pendings continue to run above last year’s pace. Third quarter closed sales were up 20% compared to last year. Although September closings were down compared to the prior two months, they were up compared to last year. Despite buyers figuring out how to balance work from home and home-schooling, both September closed sales and new pendings were up by 9% and 40% compared to 2019. YTD closed sales are down 4%, but the gap continues to narrow, and sales will be near even by the end of the year. For those thinking of selling, it’s not too late to jump in. Fourth quarter sales will be about as strong as last year’s third quarter.

Copyright 2020, Real Estate One

OCTOBER 2020HOUSING REPORT

DetroitSingle-Family Homes

2,495YTD CLOSED SALES

-14% from last year

$78KYTD AVG SALE PRICE

+15% from last year

1,021AVAILABLE HOMES-8% from last month

468NEW PENDINGS

+2% from last month

$55YTD PRICE PER SQ FT

+9% from last year

Closed Sales

$10

$20

$30

$40

$50

$60

0

50

100

150

200

250

300

350

400

Dec '18 Mar '19 Jun '19 Sep '19 Dec '19 Mar '20 Jun '20 Sep '20

$/SFYTD Closed Volume: $194M (even)MONTHLY SALES

27% 28%-25%

-95%

-5%

39% 42% 48% 50%

-120%

-100%

-80%-60%

-40%

-20%

0%

20%

40%

60%

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

Jan Feb Mar Apr May Jun Jul Aug Sep

Monthly Showings2019 v 2020

2019 2020 +/-

0

2

4

6

8

10

12

14

16

18

20

6/30/207/7/20

7/14/20

7/21/20

7/28/208/4/20

8/11/20

8/18/20

8/25/209/1/20

9/8/20

9/15/20

9/22/20

9/29/20

10/6/20

10/13/20

Daily New PendingsSingle Family

'19 Pendings '20 Pendings

Jul 1 — Oct 137-day Avg

averaging about 30% higher

1% 2% -1% -3%-13%

-22% -28%

-41%-48%

-53%-6 0%

-5 0%

-4 0%

-3 0%

-2 0%

-1 0%

0%

10%

0

500

1000

1500

2000

2500

3000

Jan Feb Mar Apr May Jun Jul Aug Sept Oct

Inventory2019 v 2020

2019 2020 +/-

First Day of Month

Inventory is down 53% from last year and existing listings are selling faster than new ones arrive on the market. Lack of inventory is limiting sales, yet new pendings are running 30% higher than last year. Following the second quarter shutdown, third quarter sales were strong. YTD, closed sales are down 14%, but the gap will continue to narrow as long as this year’s daily new pendings (chart above) exceed last year’s. Values continue to rise—average sale price and price per square foot are both up 15% and 9%. The $/SF line in the top chart shows values have been rising rapidly in recent months. While markets often slow in the fourth quarter, this year’s cycle is lagging, and the fourth quarter will be more like a strong extension of the third.

Copyright 2020, Real Estate One

OCTOBER 2020HOUSING REPORT

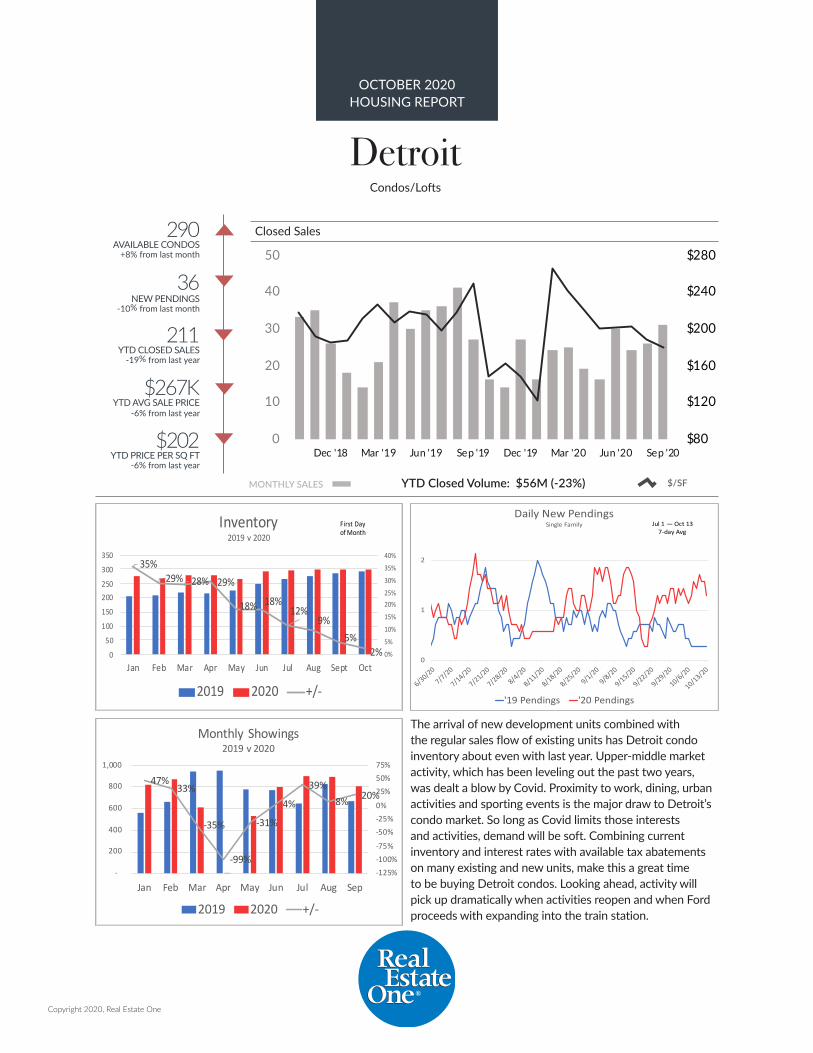

DetroitCondos/Lofts

211YTD CLOSED SALES

-19% from last year

$267KYTD AVG SALE PRICE

-6% from last year

290AVAILABLE CONDOS

+8% from last month

36NEW PENDINGS

-10% from last month

$202YTD PRICE PER SQ FT

-6% from last year

Closed Sales

$/SFYTD Closed Volume: $56M (-23%)

$80

$120

$160

$200

$240

$280

0

10

20

30

40

50

Dec '18 Mar '19 Jun '19 Sep '19 Dec '19 Mar '20 Jun '20 Sep '20

MONTHLY SALES

47%33%

-35%

-99%

-31%

4%

39%8% 20%

-125%-100%-75%

-50%-25%0%

25%50%75%

-

200

400

600

800

1,000

Jan Feb Mar Apr May Jun Jul Aug Sep

Monthly Showings2019 v 2020

2019 2020 +/-

0

1

2

6/30/207/7/20

7/14/20

7/21/20

7/28/208/4/20

8/11/20

8/18/20

8/25/209/1/20

9/8/20

9/15/20

9/22/20

9/29/20

10/6/20

10/13/20

Daily New PendingsSingle Family

'19 Pendings '20 Pendings

Jul 1 — Oct 137-day Avg

35%29% 28% 29%

18% 18%12%

9%5%

2% 0%

5%

10%

15%

20%25%

30%

35%

40%

0

50

100

150

200250

300

350

Jan Feb Mar Apr May Jun Jul Aug Sept Oct

Inventory2019 v 2020

2019 2020 +/-

First Day of Month

The arrival of new development units combined with the regular sales flow of existing units has Detroit condo inventory about even with last year. Upper-middle market activity, which has been leveling out the past two years, was dealt a blow by Covid. Proximity to work, dining, urban activities and sporting events is the major draw to Detroit’s condo market. So long as Covid limits those interests and activities, demand will be soft. Combining current inventory and interest rates with available tax abatements on many existing and new units, make this a great time to be buying Detroit condos. Looking ahead, activity will pick up dramatically when activities reopen and when Ford proceeds with expanding into the train station.

Copyright 2020, Real Estate One

OCTOBER 2020HOUSING REPORT

DownriverSingle-Family Homes

2,936YTD CLOSED SALES

-9% from last year

$164KYTD AVG SALE PRICE

+8% from last year

375AVAILABLE HOMES-1% from last month

394NEW PENDINGS

-21% from last month

$117YTD PRICE PER SQ FT

+7% from last year

Closed Sales

$60

$70

$80

$90

$100

$110

$120

$130

0

100

200

300

400

500

Dec '18 Mar '19 Jun '19 Sep '19 Dec '19 Mar '20 Jun '20 Sep '20

$/SFYTD Closed Volume: $480M (-2%)MONTHLY SALES

8% 9%

-34%

-99%

5%28%

39%28%

-10%

-125%

-100%

-75%

-50%

-25%

0%

25%

50%

-

2,000

4,000

6,000

8,000

10,000

12,000

Jan Feb Mar Apr May Jun Jul Aug Sep

Monthly Showings2019 v 2020

2019 2020 +/-

0

5

10

15

20

25

6/30/207/7/20

7/14/20

7/21/20

7/28/208/4/20

8/11/20

8/18/20

8/25/209/1/20

9/8/20

9/15/20

9/22/20

9/29/20

10/6/20

10/13/20

Daily New PendingsSingle Family

'19 Pendings '20 Pendings

Jul 1 — Oct 137-day Avg

up about 30% in recent weeks

-12%-7%

13% 14%

-10% -17%-13%

-27%-34%

-55%-6 0%

-5 0%

-4 0%

-3 0%

-2 0%-1 0%

0%

10%

20%

0

20

40

60

80

100

Jan Feb Mar Apr May Jun Jul Aug Sept Oct

Inventory2019 v 2020

2019 2020 +/-

First Day of Month

Despite the 55% drop in inventory compared to a year ago, buyer demand remains hot. While lack of inventory has been causing a decline in showings, recent daily new pendings continue to run about 30% higher than a year ago but are down compared to prior months. YTD closed sales are down 9%, but average price and price per square foot are both up—8% and 7%. The $/SF line in the top chart also shows a significant value increase in recent months. Inventory will be the key to sales through the balance of the year. For anyone thinking of selling, there’s still time to take advantage of high buyer demand and the low interest rates. Low rates benefit sellers by making their homes affordable to a larger pool of buyers, even at a higher price.

Copyright 2020, Real Estate One

OCTOBER 2020HOUSING REPORT

Livingston CountySingle-Family Homes

2,057YTD CLOSED SALES

-3% from last year

$335KYTD AVG SALE PRICE

+6% from last year

330AVAILABLE HOMES-14% from last month

303NEW PENDINGS

-16% from last month

$164YTD PRICE PER SQ FT

+3% from last year

Closed Sales

$130

$140

$150

$160

$170

$180

0

50

100

150

200

250

300

350

400

Dec '18 Mar '19 Jun '19 Sep '19 Dec '19 Mar '20 Jun '20 Sep '20

$/SFYTD Closed Volume: $689M (+3%)MONTHLY SALES

7% 17%

-37%

-99%

26% 27% 26% 31%26%

-120%

-100%

-80%

-60%

-40%

-20%

0%

20%

40%

- 1,000 2,000 3,000 4,000 5,000 6,000 7,000 8,000

Jan Feb Mar Apr May Jun Jul Aug Sep

Monthly Showings2019 v 2020

2019 2020 +/-

0

2

4

6

8

10

12

14

16

6/30/207/7/20

7/14/20

7/21/20

7/28/208/4/20

8/11/20

8/18/20

8/25/209/1/20

9/8/20

9/15/20

9/22/20

9/29/20

10/6/20

10/13/20

Daily New PendingsSingle Family

'19 Pendings '20 Pendings

Jul 1 — Oct 137-day Avg

0%-9% -8%

-14%-17% -20% -28%-35%

-43%

-50%-6 0%

-5 0%

-4 0%

-3 0%

-2 0%

-1 0%

0%

0

200

400

600

800

1000

Jan Feb Mar Apr May Jun Jul Aug Sept Oct

Inventory2019 v 2020

2019 2020 +/-

First Day of Month

Although inventory is down 50% compared to last year, daily showing activity and new pending sales continue to run at a faster pace than a year ago. Closed sales dropped each of the past two months from July’s record high, but September sales were up 21% compared to a year ago. YTD closed sales are down 3%, but that gap is narrowing and should be closed within the next month or two. Low interest rates and high buyer demand continue to boost values. YTD average sale price is up 6% and price per square foot is up 3%. Declining inventory will increasingly challenge buyers and limit sales despite extreme demand. It’s not too late for sellers who have been holding off to take advantage of what will be a strong fourth quarter.

Copyright 2020, Real Estate One

OCTOBER 2020HOUSING REPORT

St. Clair CountySingle-Family Homes

1,534YTD CLOSED SALES

+1% from last year

$207KYTD AVG SALE PRICE

+9% from last year

294AVAILABLE HOMES-10% from last month

239NEW PENDINGS

-12% from last month

$123YTD PRICE PER SQ FT

+7% from last year

Closed Sales

$80

$90

$100

$110

$120

$130

$140

0

50

100

150

200

250

300

Dec '18 Mar '19 Jun '19 Sep '19 Dec '19 Mar '20 Jun '20 Sep '20

$/SFYTD Closed Volume: $317M (+10%)MONTHLY SALES

8%31%

-30%

-98%

12%

49% 42%19%

36%

-120%

-100%

-80%-60%

-40%

-20%

0%

20%

40%

60%

-

500

1,000

1,500

2,000

2,500

3,000

Jan Feb Mar Apr May Jun Jul Aug Sep

Monthly Showings2019 v 2020

2019 2020 +/-

0

2

4

6

8

10

12

6/30/207/7/20

7/14/20

7/21/20

7/28/208/4/20

8/11/20

8/18/20

8/25/209/1/20

9/8/20

9/15/20

9/22/20

9/29/20

10/6/20

10/13/20

Daily New PendingsSingle Family

'19 Pendings '20 Pendings

Jul 1 — Oct 137-day Avg

-5% -7% -6% 2%-11%

-20% -29%-36%

-45%

-54%-6 0%

-5 0%

-4 0%

-3 0%

-2 0%

-1 0%

0%

10%

0100200300400500600700800

Jan Feb Mar Apr May Jun Jul Aug Sept Oct

Inventory2019 v 2020

2019 2020 +/-

First Day of Month

Despite inventory levels, which have declined every month this year (currently down 54% compared to a year ago), a strong third quarter performance has pushed YTD closed sales slightly ahead of last year. Current showing and new pending activity continue to outperform last year’s pace and, as seen in the top chart above, price per square foot has risen sharply over the past few months. Michigan’s second quarter shutdown appears to have delayed this year’s market cycle. Anyone who has been putting off selling may want to reconsider and act while this strong seller’s market continues to roll. Expect this year’s fourth quarter to have higher third-quarter-like activity.

Copyright 2020, Real Estate One