Embed Size (px)

Citation preview

HMDA Data

Robert B. Avery

Association of Public Data Users Annual Conference 2008

September 24, 2008

This presentation reflects the joint work of Robert B. Avery, Kenneth P. Brevoort and Glenn B. Canner. The views expressed here are those of the author and do not necessarily represent those of the Board of Governors of the Federal Reserve System or members of the staff.

HMDA Background

The Home Mortgage Disclosure Act (HMDA) of 1975 enacted to address concerns about redlining practices Requires most lenders in metropolitan areas to disclose information

about their mortgage lending activity each year by census tract and type of loan.

HMDA amended by Congress in 1989 to add application-by-application disclosure of:

1. Race, ethnicity and sex of applicants2. Borrower income3. Disposition of applications (approval, denial, etc.) and

reasons for denial4. Loan size, type of loan, and census tract5. Information on the sale of the loan in the secondary market

HMDA Price Disclosures Federal Reserve amended Regulation C in 2002

to require disclosure of information about loans with prices above designated thresholds; such loans are referred to as “higher-priced loans” but are not equivalent necessarily to “subprime.”

What is disclosed?1. Rate spread in percentage points2. Spread is difference between APR on loan and yield on Treasury security

of comparable maturity 3. Spread reported for first lien loans if above 3 percentage points4. Spread reported for subordinate lien loans if above 5 percentage points 5. Lien status (first, subordinate, no lien)

The 2007 HMDA Data

For 2007: 8,610 lenders reported on roughly 21 million loan applications down about 25 percent from 2006Reporters include 6,858 banking institutions

and 1,752 mortgage companies -- including 1,124 independent mortgage companies

Number of reporters fell about 3 percent; virtually all the decline due to independent mortgage companies that ceased operations

FHA and Nonowner-Occupant Lending FHA-lending:

FHA share of market fell from 16 percent as recently as 2000 to only 3 percent in 2006. FHA share rebounded to 5 percent in 2007 and indications are it is growing rapidly in 2008

Growth of nonowner-occupied lending: In mid-1990s share was 5 percent, reached peak in 2006 at

17 percent; share fell to 15 percent in 2007 Important in current market because investors are quick to

walk away from property when values fall

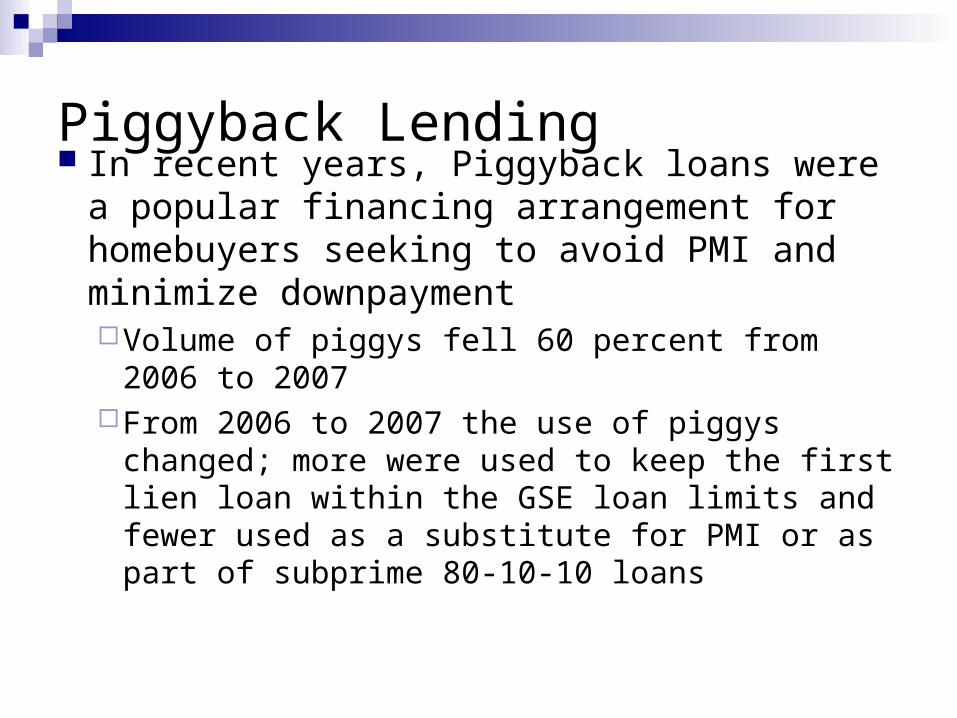

Piggyback Lending In recent years, Piggyback loans were a

popular financing arrangement for homebuyers seeking to avoid PMI and minimize downpaymentVolume of piggys fell 60 percent from 2006 to 2007From 2006 to 2007 the use of piggys changed;

more were used to keep the first lien loan within the GSE loan limits and fewer used as a substitute for PMI or as part of subprime 80-10-10 loans

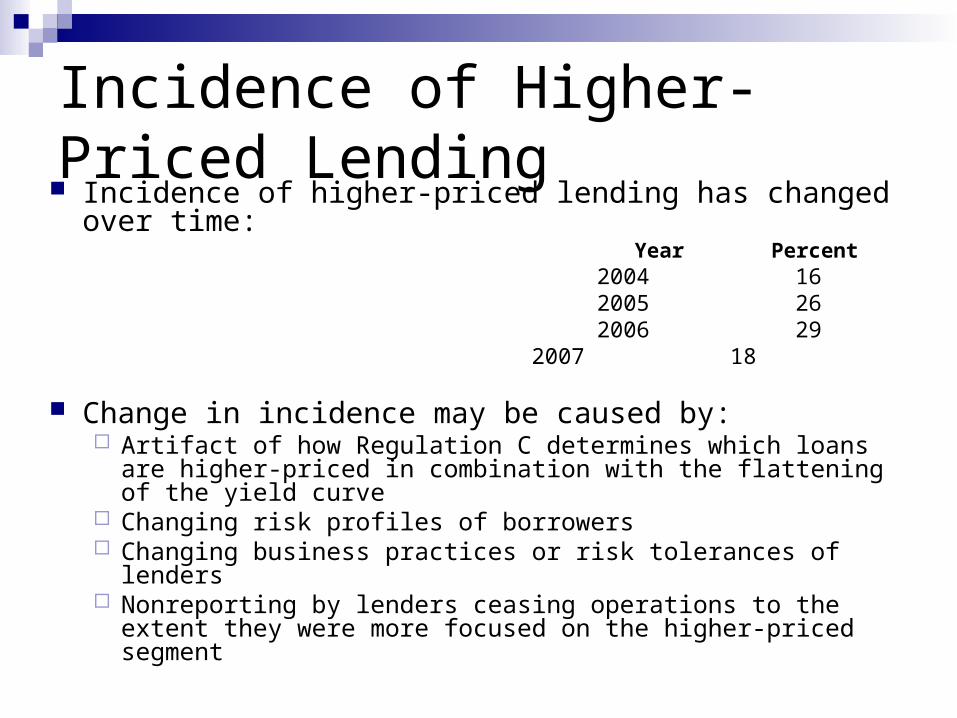

Incidence of Higher-Priced Lending Incidence of higher-priced lending has changed over

time: Year Percent

2004 16 2005 26 2006 29

2007 18

Change in incidence may be caused by: Artifact of how Regulation C determines which loans are higher-

priced in combination with the flattening of the yield curve Changing risk profiles of borrowers Changing business practices or risk tolerances of lenders Nonreporting by lenders ceasing operations to the extent they

were more focused on the higher-priced segment

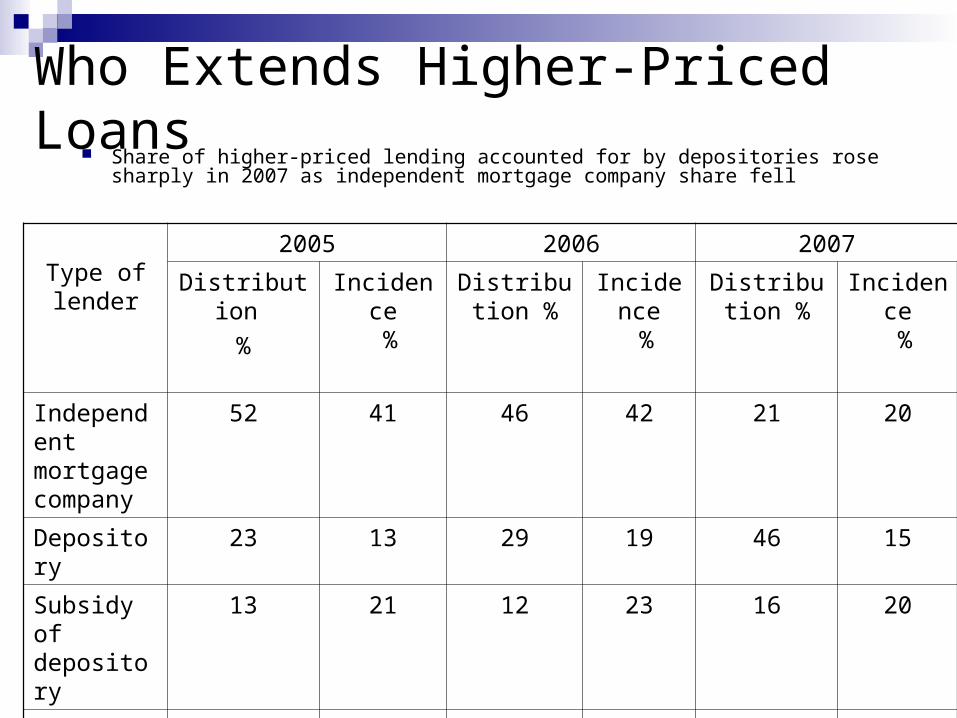

Who Extends Higher-Priced Loans Share of higher-priced lending accounted for by depositories rose

sharply in 2007 as independent mortgage company share fell

Type of lender

2005 2006 2007

Distribution

%

Incidence %

Distribution %

Incidence %

Distribution %

Incidence %

Independent mortgage company

52 41 46 42 21 20

Depository 23 13 29 19 46 15

Subsidy of depository

13 21 12 23 16 20

Affiliate of depository

12 31 13 38 18 41

Total 100 25 100 28 100 19

Effects of Closed LendersLoan Counts by Month, 2006 and 2007

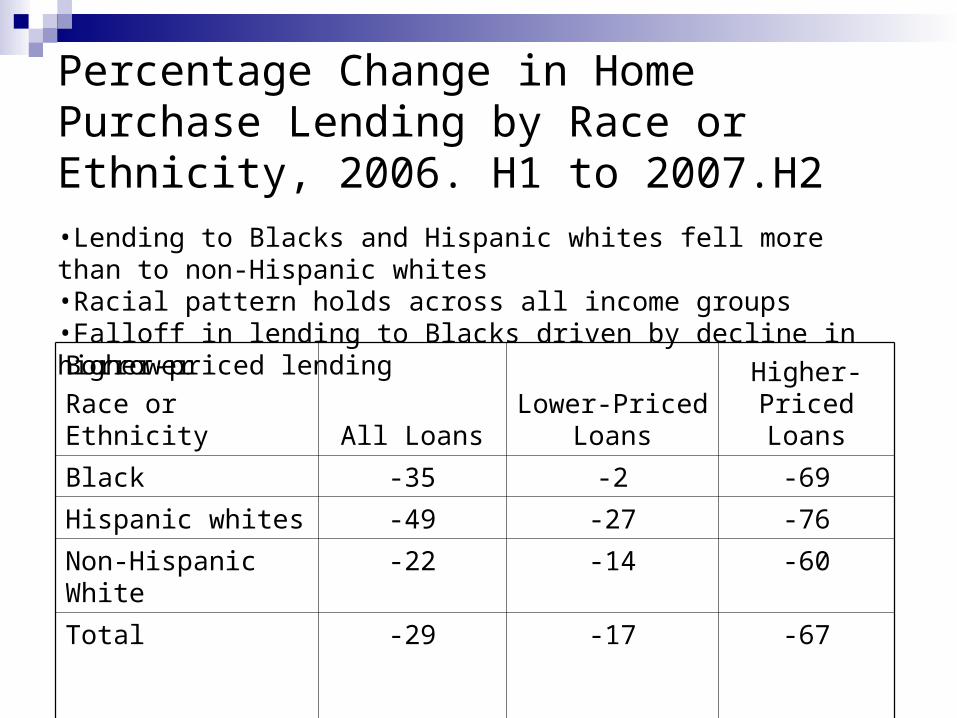

Percentage Change in Home Purchase Lending by Race or Ethnicity, 2006. H1 to 2007.H2

Borrower

Race or Ethnicity All LoansLower-Priced

LoansHigher-Priced

Loans

Black -35 -2 -69

Hispanic whites -49 -27 -76

Non-Hispanic White -22 -14 -60

Total -29 -17 -67

•Lending to Blacks and Hispanic whites fell more than to non-Hispanic whites•Racial pattern holds across all income groups•Falloff in lending to Blacks driven by decline in higher-priced lending

Percentage Changes in Lending by Type of Lender

Loan Type All

Depositories in Assessment

Area

Depositories Outside

Assessment Area

Independent Mortgage Company

Home Purchase

Lower Priced -17 -4 -17 -36

Higher Priced -67 -17 -59 -88

Refinance

Lower Priced -16 -11 -7 -38

Higher Priced -57 8 -43 -85

•Independent mortgage companies experienced greater declines than depository institutions regardless of location for all types of lending

House Price Changes and Changes in Lending Falloff in lending activity is related to patterns

of house price changes in preceding yearsMSAs that had larger declines in prices from

2006.Q4 to 2008.Q1 experienced larger declines in lending

Falloff in activity was greater for MSAs that had experienced sharp increases in home prices from 2003.Q1 to 2006.Q4

Lending declined 53 percent in MSAs with sharp declines preceded by sharp increases, compared to a 5 percent decline in MSAs with sharp declines preceded by smaller appreciation

Change in House Price Index from December 2006 to March 2008

Large decrease (greater than 8% decrease)

Small decrease (less than 8% decrease)

Increase (increase greater than 0%)

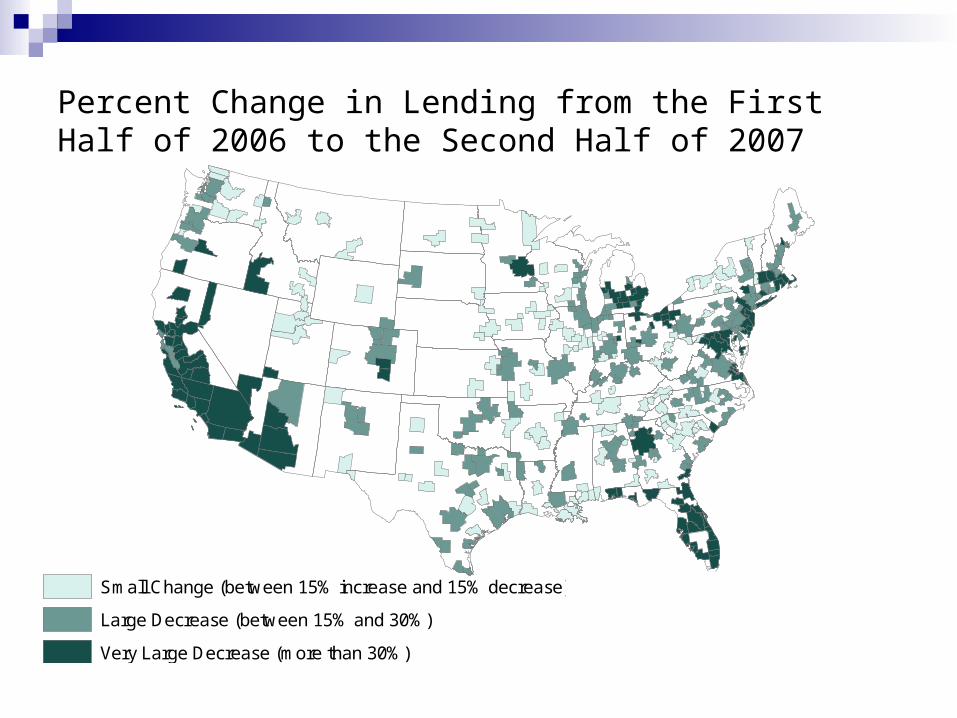

Percent Change in Lending from the First Half of 2006 to the Second Half of 2007

Small Change (between 15% increase and 15% decrease)

Large Decrease (between 15% and 30%)

Very Large Decrease (more than 30%)

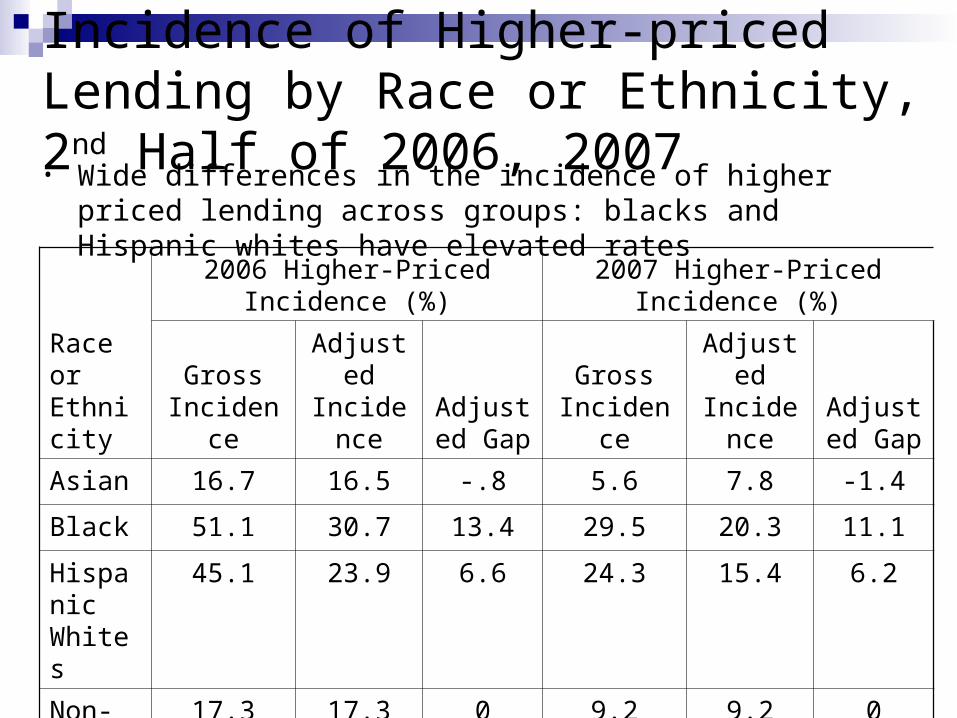

Incidence of Higher-priced Lending by Race or Ethnicity, 2nd Half of 2006, 2007• Wide differences in the incidence of higher priced lending

across groups: blacks and Hispanic whites have elevated rates

Race or Ethnicity

2006 Higher-Priced Incidence (%) 2007 Higher-Priced Incidence (%)

Gross Incidence

Adjusted Incidence

Adjusted Gap

Gross Incidence

Adjusted Incidence

Adjusted Gap

Asian 16.7 16.5 -.8 5.6 7.8 -1.4

Black 51.1 30.7 13.4 29.5 20.3 11.1

Hispanic Whites

45.1 23.9 6.6 24.3 15.4 6.2

Non-Hispanic Whites

17.3 17.3 0 9.2 9.2 0

Denial rates by Race and Ethnicity, 2nd Half of 2006, 2007

Wide differences in denial rates: blacks, Hispanics have elevated rates of loan denial

Race or Ethnicity

2006 Higher-Priced Denial Rate (%)

2007 Higher-Priced Denial Rate (%)

Denial rate

Adjusted denial rate

Adjusted denial

rate gapDenial

rate

Adjusted denial rate

Adjusted denial

rate gap

Asian 16.8 14.8 1.7 17.7 15.1 1.9

Black 32.3 21.5 8.4 34.2 22.9 9.7

Hispanic Whites

26.2 17.6 4.5 30.0 19.7 6.5

Non-Hispanic Whites

13.1 13.1 0 13.2 13.2 0

Modifying HMDA to be Consistent with New HOEPA Rules Definition of higher-priced lending in HOEPA

APR spread for each loan calculated by comparing APR on loan with mortgage rates for lowest risk prime borrowers

Prime rates from weekly Freddie Mac PMMS Loan products not included in PMMS are based on a an

interpolation of the spread differences between PMMS rate on similar products and Treasury yield and adding the interpolated spread to the comparable Treasury yield

Starting date for the new rule