Embed Size (px)

Citation preview

Role of Bond Counsel • History • Opinion • Validity • Tax-Exemption

Tax Rules for Private Activity

Multi-Family Bonds (Residential Rental Property)

• Official Action — Provide Housing - Not for refinancing or working capital

• 95/5 - 95% of the net bond proceeds must be used for capital costs of the exempt facility (i.e. the Project). 5% is so-called “bad money.” Includes costs of issuance (not more than 2%) — Tax Questionnaire - expectations. At completion measured again

• Residential Rental Property - a building or structure, together with any functionally related and subordinate facilities, containing one or more similarly constructed units which (i) are to be used on other than a transient basis, (ii) are available to the general public and (iii) satisfy the continuous rental and low or moderate income occupancy requirements

• complete units - living, sleeping, eating, cooking and sanitation

• functionally related and subordinate facilities • not used on transient basis — no hotels, motels, rooming

houses etc. Single Room Occupancy is OK • available to the general public (some exceptions e.g. - elderly) • low income set aside (20% at 50%; 40% (or in NYC - 25%) at

60% of AMI for Qualified Project Period — later of (A) occ. of 10% of units or (B) date of iss. until later of (I) 15 yrs after 50% occ. (II) no bonds outstanding or (III) §8 assistance terminates

• Deep Rent Skewed – of low income units – 15% at 40% of AMI

• limits on land acquisition (25% of net bond proceeds)

• acquisition of existing Project – not from “related” person – 15% rehabilitation requirement

• bond maturity (120% of average economic life of assets financed)

• TEFRA

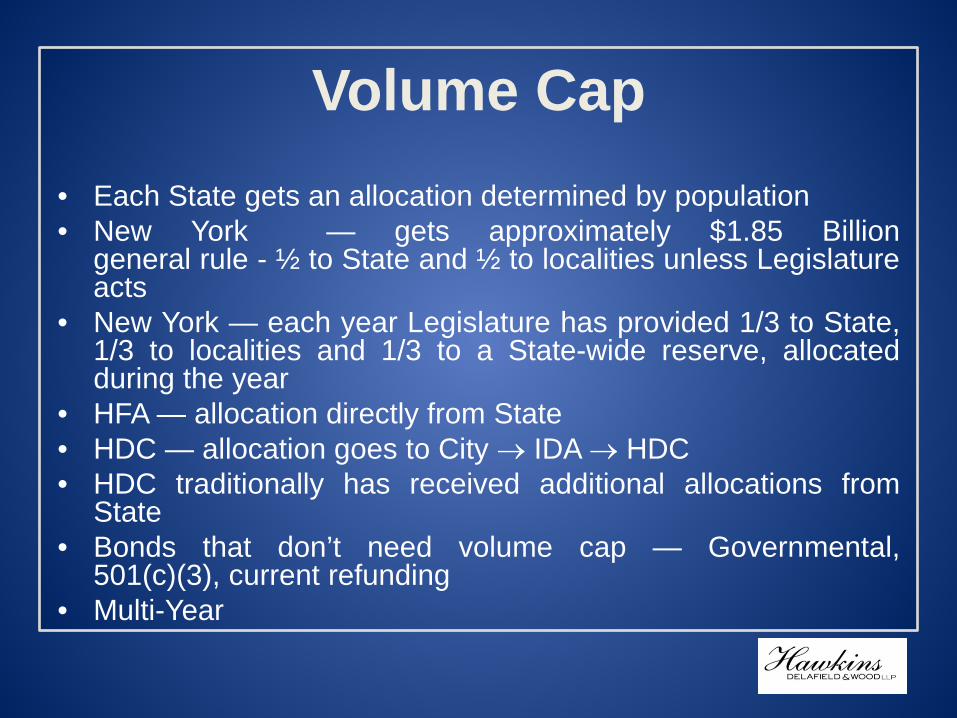

Volume Cap

• Each State gets an allocation determined by population • New York — gets approximately $1.85 Billion

general rule - ½ to State and ½ to localities unless Legislature acts

• New York — each year Legislature has provided 1/3 to State, 1/3 to localities and 1/3 to a State-wide reserve, allocated during the year

• HFA — allocation directly from State • HDC — allocation goes to City → IDA → HDC • HDC traditionally has received additional allocations from

State • Bonds that don’t need volume cap — Governmental,

501(c)(3), current refunding • Multi-Year

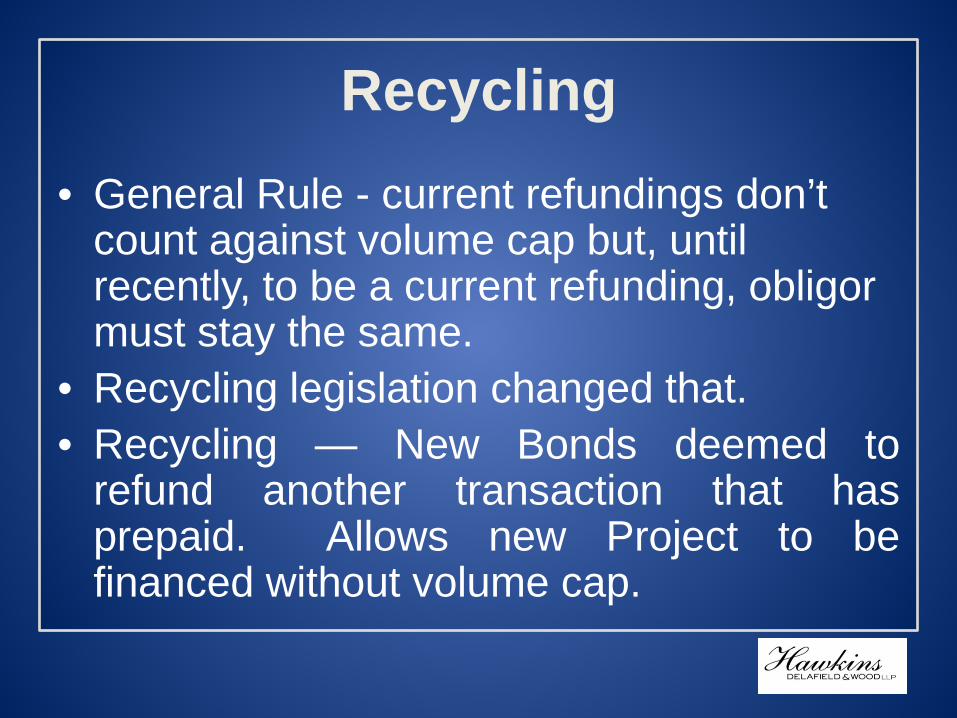

Recycling

• General Rule - current refundings don’t count against volume cap but, until recently, to be a current refunding, obligor must stay the same.

• Recycling legislation changed that. • Recycling — New Bonds deemed to

refund another transaction that has prepaid. Allows new Project to be financed without volume cap.

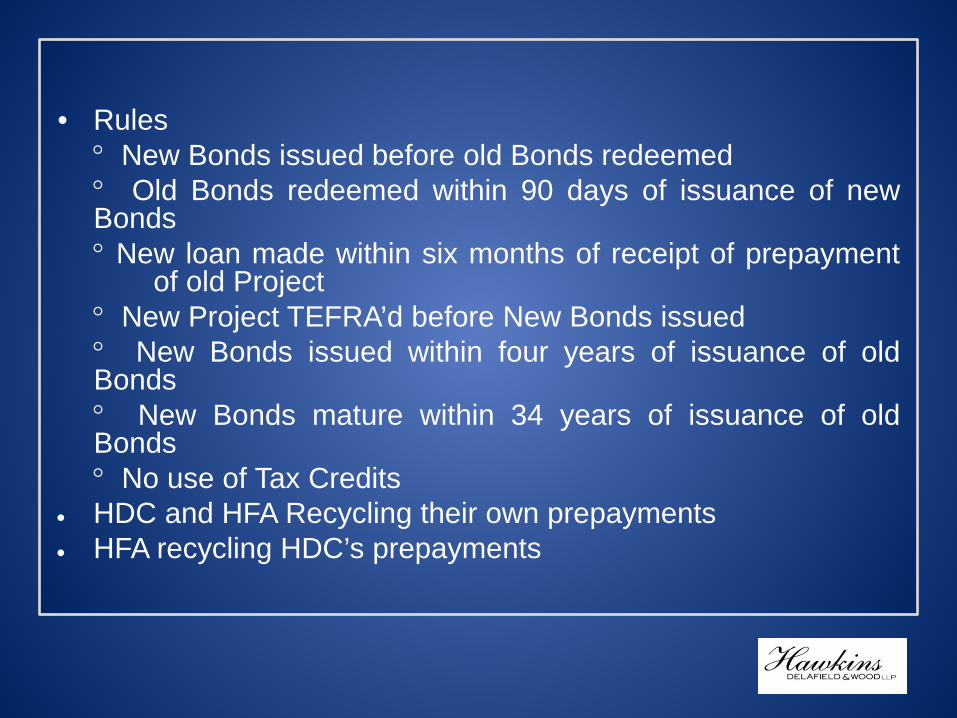

• Rules ° New Bonds issued before old Bonds redeemed ° Old Bonds redeemed within 90 days of issuance of new

Bonds ° New loan made within six months of receipt of prepayment

of old Project ° New Project TEFRA’d before New Bonds issued ° New Bonds issued within four years of issuance of old

Bonds ° New Bonds mature within 34 years of issuance of old

Bonds ° No use of Tax Credits • HDC and HFA Recycling their own prepayments • HFA recycling HDC’s prepayments

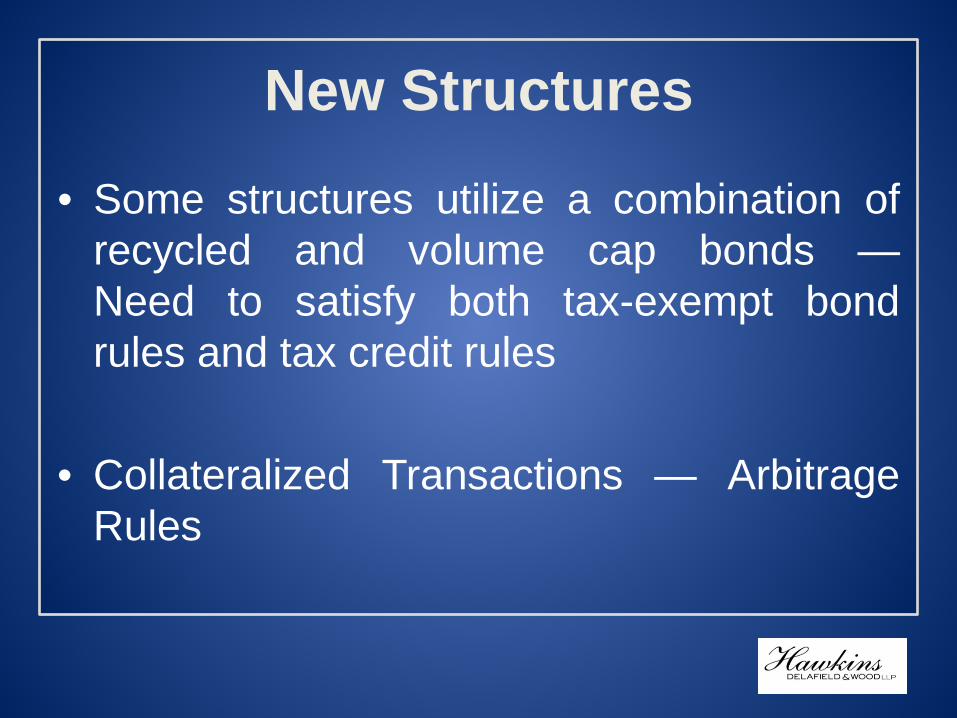

New Structures

• Some structures utilize a combination of recycled and volume cap bonds — Need to satisfy both tax-exempt bond rules and tax credit rules

• Collateralized Transactions — Arbitrage

Rules

N Y S A F A H C o n f e r e n c e

A d v a n c e d B o n d s

95/5 Test and 50% Test

May 7, 2013

9 5 / 5 Te s t

• Sometimes referred to as the Good Cost Bad Cost Test – a tax-exempt bond test and not a LIHTC Test.

• Purpose of 95/5 test is to show that a bond issue qualifies as a tax-exempt bond issue – the interest income earned by the holders of the bonds will be excluded from income for federal income tax purposes.

• The Test is that Qualified Costs of a project must equal or exceed 95% of the Net Bond Proceeds.

May 7, 2013 10

9 5 / 5 Te s t

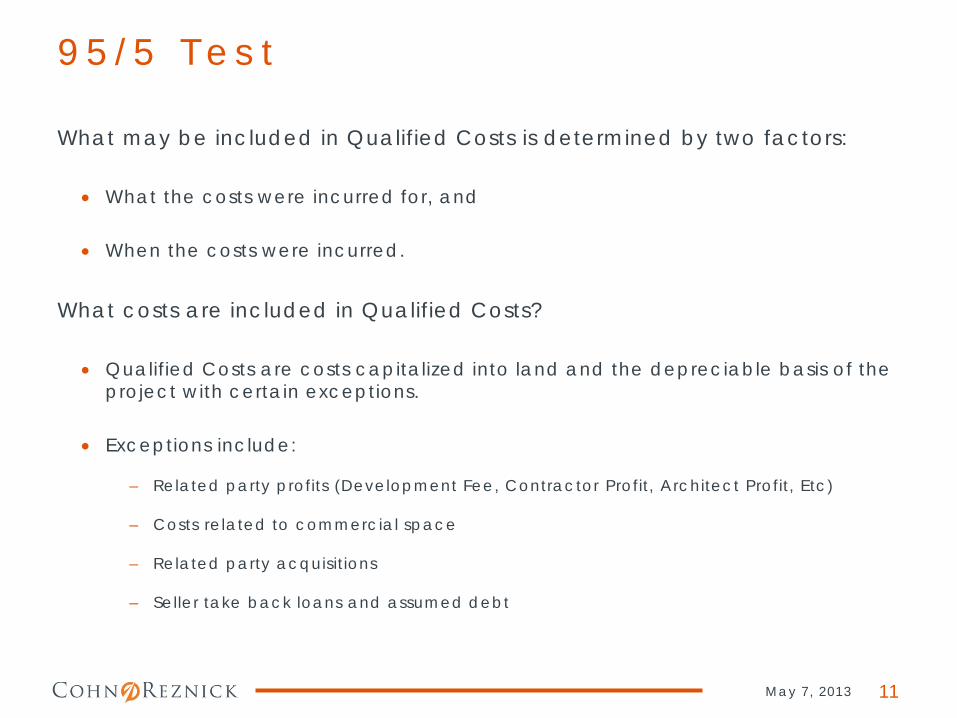

What may be included in Qualified Costs is determined by two factors:

• What the costs were incurred for, and

• When the costs were incurred. What costs are included in Qualified Costs?

• Qualified Costs are costs capitalized into land and the depreciable basis of the project with certain exceptions.

• Exceptions include:

– Related party profits (Development Fee, Contractor Profit, Architect Profit, Etc)

– Costs related to commercial space

– Related party acquisitions

– Seller take back loans and assumed debt

May 7, 2013 11

9 5 / 5 Te s t

When must costs be incurred to be included in Qualified Costs? • Qualified Costs are costs incurred no earlier than 60 days prior to the date of

inducement resolution – again, with certain exceptions.

• Exceptions include:

– Preliminary Expenditure Exception – includes cost for architecture, engineering, survey, soil testing and similar costs incurred prior to commencement of acquisition, construction, or rehabil itation of a project. Does not include land acquisition, site preparation or similar costs incidental to commencement of construction.

– Preliminary Expenditure Exception is l imited to an amount not in excess of 20% of the aggregate issue price of an issue.

– Deminimus Exception – applies only to costs of issuance or to an amount not in excess of the lesser of $100,000 or 5% of the proceeds of an issue.

May 7, 2013 12

9 5 / 5 Te s t

Another Timing Issue to be Aware of: • Reimbursement Allocation – occurs if an expenditure with respect to a project is

paid before the issue date of the bonds for the project. Reimbursement allocations are only allowed if:

– Payment of original expenditure occurred no more than 60 days prior to date of inducement resolution.

– Reimbursement is made not more than 18 months after the later of:

• The date the original expenditure was paid, or

• The date the project is placed in service

– But in no event more than three years after the original expenditure was paid.

May 7, 2013 13

9 5 / 5 Te s t

Current Issues – Things to Pay Attention to:

• Related Party acquisitions of land in new construction deals

• Timing issues with respect to reimbursement allocations. This rule may apply if there is a long lag time between the date of the inducement resolution and the date the bonds are actually issued. Max time between original payment and reimbursement is three years.

• The exclusion of Seller take back loans and assumed debt from qualified acquisition costs could severely limit the amount of tax-exempt bond proceeds a project will qualify for – can you borrow enough to meet the 50% Test?

• Problems where acquisition of existing building occurred prior to inducement resolution – can you borrow enough to meet the 50% Test.

May 7, 2013 14

5 0 % Te s t

A special rule allows tax credits to be obtained for an entire building if 50% or more of the aggregate basis of the building and the land on which the building is located is financed by tax-exempt obligations. More specifically, the 50% test is a fraction: • The numerator of which is the tax-exempt bond proceeds (plus any interest

income earned on unexpended bond proceeds during the construction period) used to finance aggregate basis, and

• The denominator is the aggregate basis in land and building.

May 7, 2013 15

5 0 % Te s t - T h e N u m e r a t o r

• Note that the 50% test does not involve direct tracing of where the tax-exempt bond proceeds were actually spent. Specific guidance related to determining the use of bond proceeds for the 50% test is provided under Treasury Regulation section 1.42-1T(f)(ii).

• Regulation says you respect the allocation of the tax-exempt bond

proceeds included in the bond documents for purposes of the 50% Test. If the bond documents say X amount of the proceeds get used to finance aggregate basis items, you would include X amount of the tax-exempt bond proceeds in your numerator. If the bond documents are inconsistent or silent with respect to the allocation, then you use a pro rata allocation for purposes of determining the portion of the tax-exempt bond proceeds in the numerator of the fraction.

May 7, 2013 16

5 0 % Te s t - T h e N u m e r a t o r

May 7, 2013 17

5 0 % Te s t - T h e D e n o m i n a t o r

• With respect to the denominator, aggregate basis plus land may not equal eligible basis plus land. Aggregate basis includes all depreciable costs including any commercial costs which were excluded from eligible basis.

• Land includes the original purchase price plus any amounts subsequently capitalized to land such as demolition costs or non-depreciable site work.

May 7, 2013 18

5 0 % Te s t -

Current Issues – Things to be Aware of:

• First – if possible, read a draft of the bond indenture document to make sure the maximum amount possible of the tax-exempt bond proceeds will be included in the numerator of the 50% Test Fraction.

• Pay particular attention to how any operating or replacement

reserves are funded. Additionally, be careful with interest reserves funded out of tax-exempt bond proceeds when you have an in-place rehab.

• Scattered site deals – would like to see specific project allocations

within the bond documents for 50% test purposes.

May 7, 2013 19

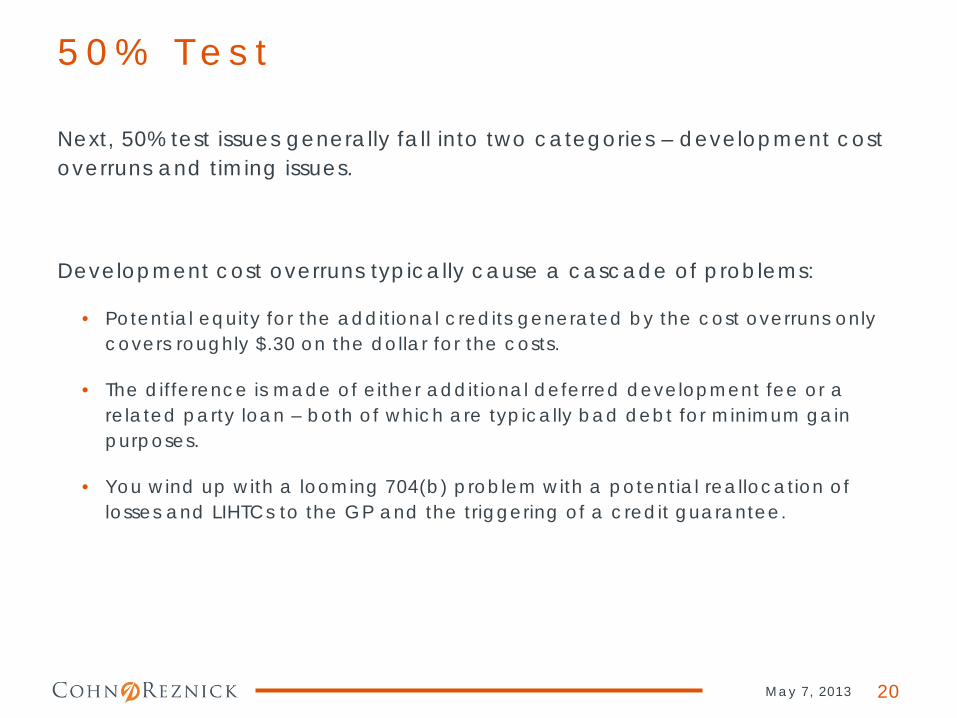

5 0 % Te s t

Next, 50% test issues generally fall into two categories – development cost overruns and timing issues. Development cost overruns typically cause a cascade of problems:

• Potential equity for the additional credits generated by the cost overruns only covers roughly $.30 on the dollar for the costs.

• The difference is made of either additional deferred development fee or a related party loan – both of which are typically bad debt for minimum gain purposes.

• You wind up with a looming 704(b) problem with a potential reallocation of losses and LIHTCs to the GP and the triggering of a credit guarantee.

May 7, 2013 20

5 0 % Te s t

Potential Fixes include: • Early identification of the issue:

‒ Get more tax-exempt bond proceeds ‒ Alter or defer the scope of work to be done (will require multiple approvals –

lender, state housing agency, investor) ‒ Revisit capitalization policy

• These solutions generally only work if the problem is identified early and

all parties are involved

• Late identification of the issue: ‒ Is the fix already in the partnership documents? ‒ Development Deficit Guarantee – whose costs are the additional costs? ‒ Reduction of the Development Fee

May 7, 2013 21

5 0 % Te s t

With respect to timing issues:

• In order to include tax-exempt bond proceeds in the numerator of the 50% test, the funds have to actually have been spent. Bond funds don’t get included in the numerator until they have actually been spent.

• HUD insured deals typically have a several month lag between project completion and the final draw – do you need the final draw to have enough tax-exempt bond proceeds to meet the 50% test?

• Projects that use convention construction financing will not be able to meet the 50% test until after the tax-exempt bonds have been used to repay the construction loan.

• If you have either of the above fact patterns and you anticipate construction completion close to year end, factor the timing issue into when you project credits to begin – may not be the year you originally thought.

• Plan ahead – construction delays may have unanticipated consequences.

May 7, 2013 22

Terry Kimm, Partner CohnReznick LLP 7501 Wisconsin Avenue Suite 400E Bethesda, MD 20814 301.652.9100 www.CohnReznick.com

New Business Conduct Standards Impact Swap Transactions Beginning May 1, 2013

New Swap Regulations

New Business Conduct Standards for Swap Dealers and Major Swap Participants

27

Business Conduct Standards for Swap Dealers and Major Swap Participants

• Commodity Futures Trading Commission (“CFTC”) Business Conduct Standards for Swap Dealers and Major Swap Participants Dealing with Counterparties.

• Why are the Business Conduct Standards important? › Impact your ability to enter into new swap transactions

› Impact your ability to amend existing swap transactions

› Impact your ability to terminate existing swap transactions

› Impact your ability to transfer or novate existing swap transactions

• What is important to understand? › The rules and the documentation necessary to complete in order to satisfy

the rules.

› Compliance Date was May 1, 2013 so the rules are now applicable to swap transactions.

28

§ 23.400 Scope

• The Business Conduct Standards apply to (1) swap dealers and, unless otherwise indicated, major swap participants; and (2) in connection with transactions in swaps as well as in connection with swaps that are offered but not entered into.

29

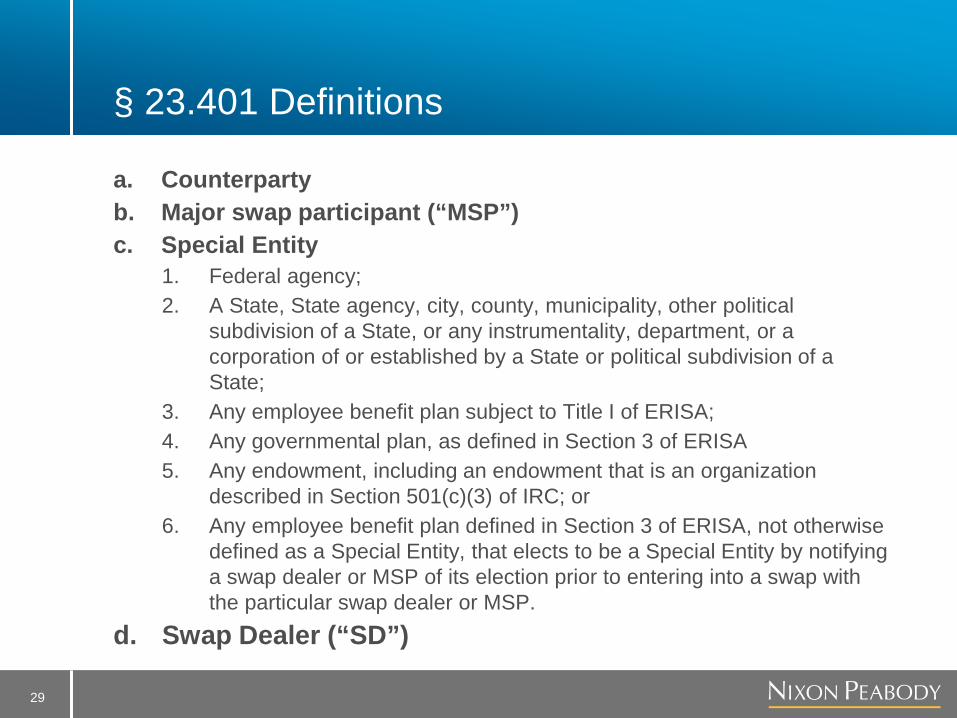

§ 23.401 Definitions

a. Counterparty b. Major swap participant (“MSP”) c. Special Entity

1. Federal agency; 2. A State, State agency, city, county, municipality, other political

subdivision of a State, or any instrumentality, department, or a corporation of or established by a State or political subdivision of a State;

3. Any employee benefit plan subject to Title I of ERISA; 4. Any governmental plan, as defined in Section 3 of ERISA 5. Any endowment, including an endowment that is an organization

described in Section 501(c)(3) of IRC; or 6. Any employee benefit plan defined in Section 3 of ERISA, not otherwise

defined as a Special Entity, that elects to be a Special Entity by notifying a swap dealer or MSP of its election prior to entering into a swap with the particular swap dealer or MSP.

d. Swap Dealer (“SD”)

30

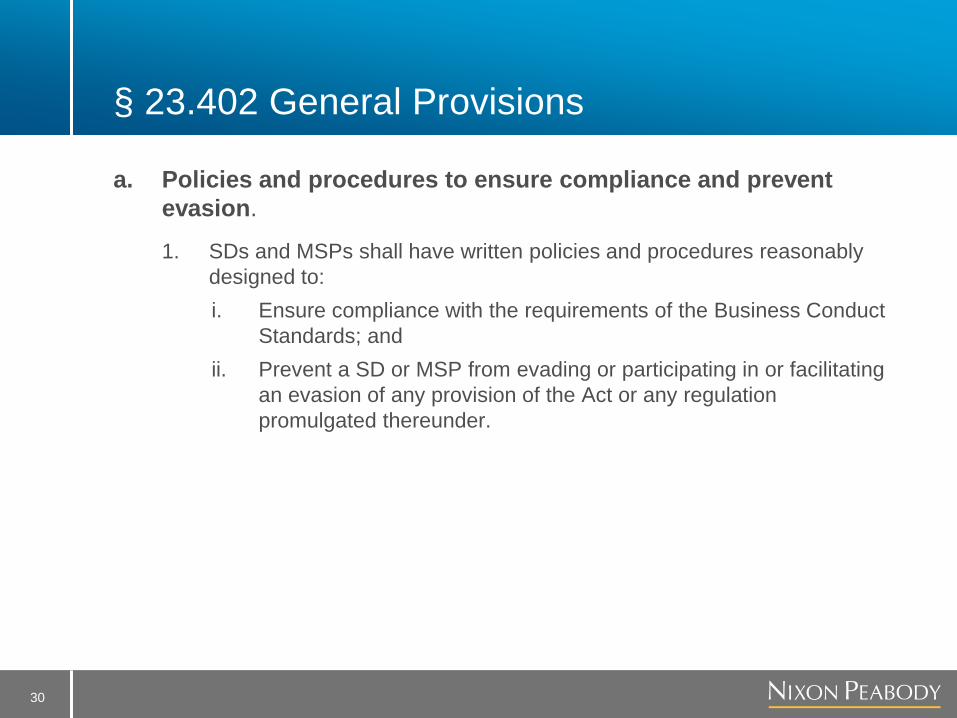

§ 23.402 General Provisions

a. Policies and procedures to ensure compliance and prevent evasion.

1. SDs and MSPs shall have written policies and procedures reasonably designed to: i. Ensure compliance with the requirements of the Business Conduct

Standards; and ii. Prevent a SD or MSP from evading or participating in or facilitating

an evasion of any provision of the Act or any regulation promulgated thereunder.

31

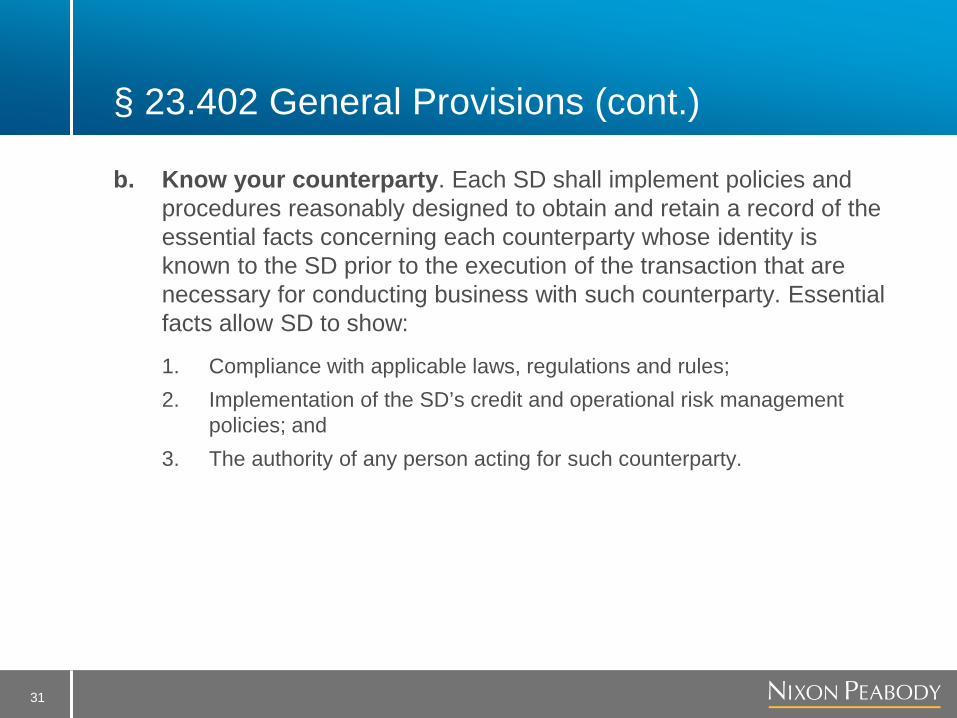

§ 23.402 General Provisions (cont.)

b. Know your counterparty. Each SD shall implement policies and procedures reasonably designed to obtain and retain a record of the essential facts concerning each counterparty whose identity is known to the SD prior to the execution of the transaction that are necessary for conducting business with such counterparty. Essential facts allow SD to show:

1. Compliance with applicable laws, regulations and rules; 2. Implementation of the SD’s credit and operational risk management

policies; and 3. The authority of any person acting for such counterparty.

32

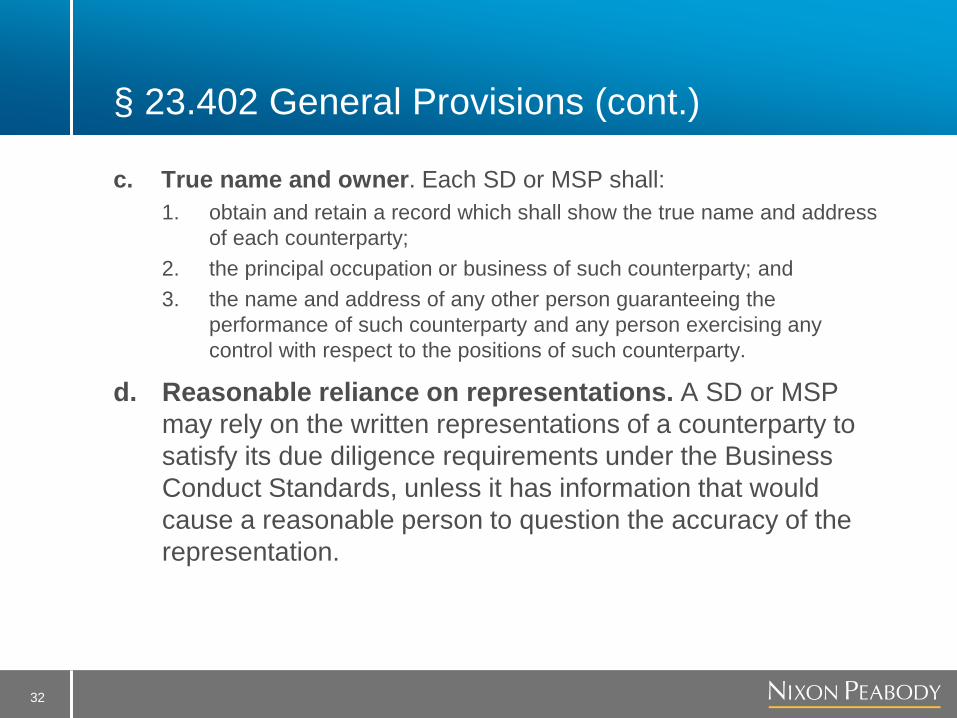

§ 23.402 General Provisions (cont.)

c. True name and owner. Each SD or MSP shall: 1. obtain and retain a record which shall show the true name and address

of each counterparty; 2. the principal occupation or business of such counterparty; and 3. the name and address of any other person guaranteeing the

performance of such counterparty and any person exercising any control with respect to the positions of such counterparty.

d. Reasonable reliance on representations. A SD or MSP may rely on the written representations of a counterparty to satisfy its due diligence requirements under the Business Conduct Standards, unless it has information that would cause a reasonable person to question the accuracy of the representation.

33

§ 23.410 Prohibition on fraud, manipulation, and other abusive practices

a. It is unlawful for a SD or MSP:

1. To employ any device, scheme, or artifice to defraud any Special Entity or prospective customer who is a Special Entity;

2. To engage in any transaction, practice, or course of business that operates as a fraud or deceit on any Special Entity or prospective customer who is a Special Entity; or

3. To engage in any act, practice, or course of business that is fraudulent, deceptive, or manipulative.

34

§ 23.410 Prohibition on fraud, manipulation, and other abusive practices (cont.)

b. Affirmative defense. A SD or MSP may raise an affirmative defense to an alleged violation of paragraph (a)(2) or (3) above if the SD or MSP establishes that it:

1. Did not act intentionally or recklessly in connection with such alleged violation; and

2. Complied in good faith with written policies and procedures reasonably designed to meet the particular requirement that is the basis for the alleged violation.

c. Confidential treatment of counterparty information.

1. It is unlawful for a SD or MSP to: i. Disclose any material confidential information provided by or on

behalf of a counterparty; or ii. Use such material confidential information in any way that would

tend to be materially adverse to the interests of a counterparty

35

§ 23.410 Prohibition on fraud, manipulation, and other abusive practices (cont.)

2. Notwithstanding paragraph (c)(1) above, a SD or MSP may disclose or use material confidential information provided by or on behalf of a counterparty if such disclosure or use is authorized in writing by the counterparty, or is necessary: i. For the effective execution of any swap ii. To hedge or mitigate any exposure created by such swap; or iii. To comply with a request of the CFTC or other legal or regulatory

authorities. Each SD or MSP shall implement written policies and procedures reasonably designed to protect material confidential information provided by or on behalf of a counterparty from disclosure and use in violation of Business Conduct Standards by any person acting for or on behalf of the SD or MSP.

36

§ 23.430 Verification of counterparty eligibility

a. Eligibility. A SD or MSP shall verify that a counterparty meets the eligibility standards for an eligible contract participant, before offering to enter into or entering into a swap with that counterparty.

b. Special Entity. A SD or MSP shall also verify whether the counterparty is a Special Entity.

c. Safe harbor. A SD or MSP may rely on written representations of a counterparty to satisfy the requirements of this section as provided in § 23.402(d). A SD or MSP will have a reasonable basis to rely on such written representations if the counterparty specifies in such representations the specific provision(s) that describe its status as an eligible contract participant and, if applicable, a Special Entity.

37

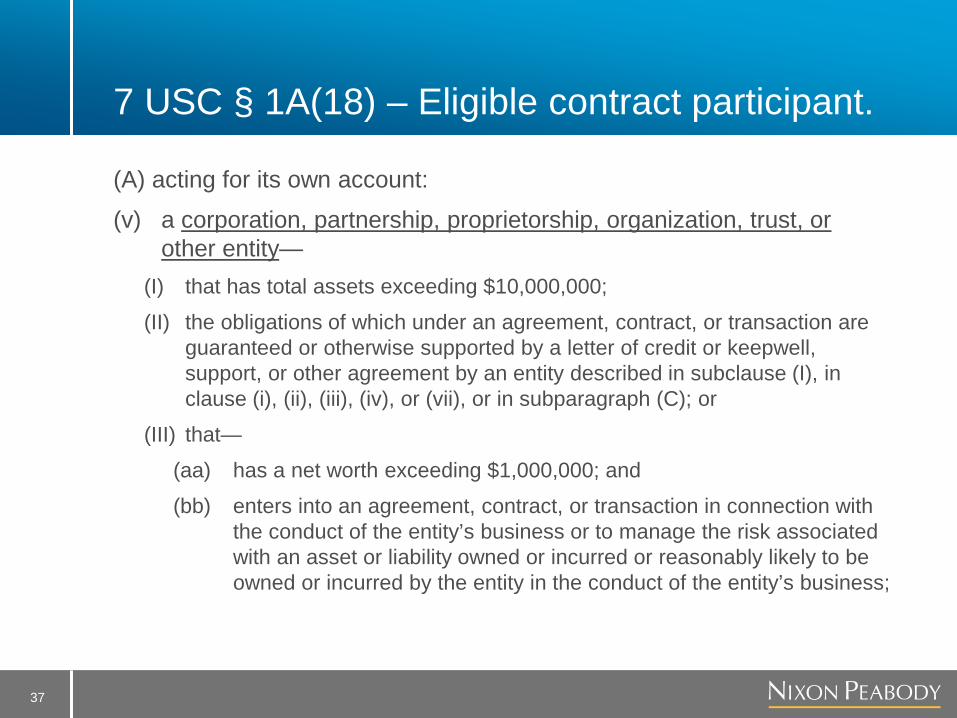

7 USC § 1A(18) – Eligible contract participant.

(A) acting for its own account:

(v) a corporation, partnership, proprietorship, organization, trust, or other entity—

(I) that has total assets exceeding $10,000,000;

(II) the obligations of which under an agreement, contract, or transaction are guaranteed or otherwise supported by a letter of credit or keepwell, support, or other agreement by an entity described in subclause (I), in clause (i), (ii), (iii), (iv), or (vii), or in subparagraph (C); or

(III) that—

(aa) has a net worth exceeding $1,000,000; and

(bb) enters into an agreement, contract, or transaction in connection with the conduct of the entity’s business or to manage the risk associated with an asset or liability owned or incurred or reasonably likely to be owned or incurred by the entity in the conduct of the entity’s business;

38

§ 23.431 Disclosures of material information

a. Prior to entering into a swap, a SD or MSP shall disclose to any counterparty (other than SDs, MSPs, security-based SDs or major security-based swap participants) material information regarding:

1. The material risks of the particular swap, (including, market, credit, liquidity, foreign currency, legal, operational, and any other applicable risks);

2. The material characteristics of the particular swap (including the material economic terms of the swap, the terms relating to the operation of the swap, and the rights and obligations of the parties during the term of the swap); and

3. The material incentives and conflicts of interest that the SD or MSD may have in connection with a particular swap (including, for example, price of the swap, the mid-market mark of the swap, and any compensation to be received from a source other than the counterparty by the SD or MSP in connection with the swap)

39

§ 23.431 Disclosures of material information (cont.)

b. Scenario Analysis. Prior to entering into a swap with a counterparty (other than SDs, MSPs, security-based swap dealers or major security-based swap participants) that is not made available for trading, as provided in Section 2(h)(8) of the Act, on a designated contract market or swap execution facility, a SD shall:

1. Notify the counterparty that it can request and consult on the design of a scenario analysis to allow the counterparty to assess its potential exposure in connection with the swap;

2. Upon request of the counterparty, provide a scenario analysis, which is designed in consultation with the counterparty and done over a range of assumptions, including severe downside stress scenarios that would result in a significant loss;

40

§ 23.431 Disclosures of material information (cont.)

3. Disclose all material assumptions and explain the calculation methodologies used to perform any requested scenario analysis; provided however, that the SD is not required to disclose confidential, proprietary information; and

4. In designing any requested scenario analysis, consider any relevant analyses that the SD undertakes for its own risk management purposes.

c. Daily mark. A SD or MSP shall: 1. For cleared swaps, notify a counterparty of the counterparty’s right to

receive, upon request, the daily mark from the appropriate derivatives clearing organization.

2. For uncleared swaps, provide the counterparty with a daily mid-market mark of the swap (which mark shall not include amounts for profit, credit reserve, hedging, funding, liquidity, or any other costs or adjustments).

41

§ 23.431 Disclosures of material information (cont.)

3. For uncleared swaps, disclose to the counterparty: i. The methodology and assumptions used to prepare the daily mark

and any material changes during the term of the swap; and ii. Additional information concerning the daily mark to ensure a fair

and balanced communication, including A. The daily mark may not necessarily be a price at which either

the counterparty or the SD or MSP would agree to replace or terminate the swap;

B. Depending upon the agreement of the parties, calls for margin may be based on considerations other than the daily mark provided to the counterparty; and

C. The daily mark may not necessarily be the value of the swap that is marked on the books of the SD or MSP.

42

§ 23.432 Clearing disclosures

a. For swaps required to be cleared — right to select derivatives clearing organization. The counterparty has the sole right to select the derivatives clearing organization at which the swap will be cleared.

b. For swaps not required to be cleared — right to clearing. The counterparty:

1. May elect to require clearing of the swap; and 2. Shall have the sole right to select the derivatives clearing organization at

which the swap will be cleared.

43

§23.433 Communications — fair dealing

• With respect to any communication between a SD or MSP and any counterparty, the SD or MSP shall communicate in a fair and balanced manner based on principles of fair dealing and good faith.

44

§ 23.434 Recommendations to counterparties —institutional suitability

a. A SD that recommends a swap or trading strategy involving a swap to a counterparty (other than an SD, MSP, security-based swap dealer or major security-based swap participant) must:

1. Undertake reasonable diligence to understand the potential risks and rewards associated with the recommended swap or trading strategy involving a swap; and

2. Have a reasonable basis to believe that the recommended swap or trading strategy involving a swap is suitable for the counterparty.

45

§ 23.434 Recommendations to counterparties —institutional suitability (cont.)

b. Safe Harbor. A SD may fulfill its obligations under paragraph (a)(2) of this section with respect to a particular counterparty if: 1. The SD reasonably determines that the counterparty, or an agent to

which the counterparty has delegated decision-making authority, is capable of independently evaluating investment risks with regard to the relevant swap or trading strategy involving a swap;

2. The counterparty or its agent represents in writing that it is exercising independent judgment in evaluating the recommendations of the SD with regard to the relevant swap or trading strategy involving a swap;

3. The SD discloses in writing that it is acting in its capacity as a counterparty and is not undertaking to assess the suitability of the swap or trading strategy involving a swap for the counterparty; and

46

§ 23.434 Recommendations to counterparties —institutional suitability (cont.)

4. In the case of a counterparty that is a Special Entity, the SD complies with § 23.440 where the recommendation would cause the SD to act as an advisor to a Special Entity within the meaning of § 23.440(a).

c. A SD will satisfy the requirements of paragraph (b)(1) of this section if it receives written representations, as provided in § 23.402(d), that: 1. In the case of a counterparty that is not a Special Entity, the

counterparty has complied in good faith with written policies and procedures that are reasonably designed to ensure that the persons responsible for evaluating the recommendation and making trading decisions on behalf of the counterparty are capable of doing so; or

2. In the case of a counterparty that is a Special Entity, satisfy the terms of the safe harbor in § 23.450(d).

Amending Swap Documentation to Comply with the Business Conduct Standards

48

Amending Swap Documentation to Comply with the Business Conduct Standards

• Counterparties will need to enter into amendments of their existing ISDA Master Agreements with Swap Dealers or Major Swap Participants so that the parties can each provide the necessary representations and covenants to each other

• The Amendments can be negotiated separately with each Swap Dealer or Major Swap Participant (this approach provides flexibility but may be time consuming and is not preferred by swap dealers)

• The Special Entity, Swap Dealer and Major Swap Participant can make use of the ISDA August 2012 DF Protocol to amend the documentation (this approach can result in the timely amendment of multiple agreements with multiple counterparties, but is not flexible in terms of the provisions of the Protocol documentation)

• Determine if third party consent is needed for amendments to be effective

ISDA August 2012 Dodd-Frank Protocol

50

Purpose of the Protocol

• Facilitate compliance with seven final rules under Title VII of the Dodd-Frank Wall Street Reform and Consumer Protection Act

• Provides for the amendment of existing written swap agreements between two parties as well as for two parties to agree to specified provisions regarding compliance with Dodd-Frank rule requirements while trading without a written swap agreement

51

Key Documents in ISDA Protocol Documentation

1. Adherence Letter

2. ISDA August 2012 DF Protocol Agreement (“Protocol Agreement”)

3. ISDA August 2012 DF Protocol Questionnaire (“Protocol Questionnaire”)

4. ISDA August 2012 DF Supplement (“DF Supplement”)

5. ISDA August 2012 Terms Agreement (“Terms Agreement”)

52

Adherence Letter

• Form of letter is an Exhibit to Protocol Agreement • Purpose is to confirm the agreement of a party

(the “Adhering Party”) to the terms of the Protocol Agreement • Adhering Party

› agrees to pay one-time fee of $500 to ISDA › appoints ISDA as its agent for the limited purposes of the Protocol

Agreement and waives and releases ISDA from any rights, claims, actions, etc. arising out of or relating to the Adherence Letter or the Adhering Party’s adherence to the Protocol Agreement

› provides contact information

53

Adherence Letter (cont.)

• Adhering Party (cont.) › specifies the acceptable means of receiving delivery of a Protocol

Questionnaire from another Adhering Party (i.e. in person, courier, certified or registered mail, facsimile transmission, e-mail, through ISDA Amend)

54

Protocol Agreement

• Adhering Party can use the terms of the Protocol Agreement to supplement an existing written swap agreement or to enter into a Terms Agreement with another Adhering Party by exchanging Protocol Questionnaires.

55

Protocol Agreement (cont.)

• Protocol Covered Agreement › Terms Agreement or an existing written agreement between two

parties that governs the terms and conditions of one or more transactions in Swaps that each party has or may enter into as principal.

• Adherence to the Protocol Agreement will be evidenced by execution and delivery of the Adherence Letter

• Protocol Questionnaire needs to be executed and submitted by an Adhering Party who has executed and submitted an Adherence Letter.

56

Protocol Agreement (cont.)

• Multiple Protocol Questionnaires can be executed and delivered by an Adhering Party to deliver different Protocol Questionnaires to different counterparties but one (1) Protocol Questionnaire must be delivered to a specific counterparty.

• Adhering Party makes an offer to enter into or supplement a Protocol Covered Agreement by: › executing a completed Protocol Questionnaire; and › delivering the Protocol Questionnaire to another Adhering Party.

• The Adhering Party receiving the Protocol Questionnaire is deemed to have accepted the offer when such Adhering Party delivers a Protocol Questionnaire to the Adhering Party that had delivered its Protocol Questionnaire.

57

Protocol Agreement (cont.)

• Adhering Party may NOT specify additional provisions, conditions or limitations in its Protocol Questionnaire.

• Terms Agreement ─ Every pair of Matched PCA Parties (both PCA Principals to a Protocol Covered Agreement (a “Matched PCA”)) is deemed to have entered into a Terms Agreement if: › BOTH Matched PCA Parties have agreed in their Protocol

Questionnaires (the “Matched Questionnaires”) to enter into the Terms Agreement

58

Protocol Agreement (cont.)

• DF Supplement ─ Every pair of Matched PCA Parties will be deemed to have supplemented each Matched PCA by: › incorporating Schedules 1 and 2 from the DF Supplement; and that › with respect to Schedules 3, 4, 5 and 6 of the DF Supplement, these

Schedules will be deemed incorporated into the Matched PCA if: – BOTH Matched PCA Parties have agreed in the Matched

Questionnaires to incorporate the applicable Schedule into the Matched PCA and each Designated Evaluation Agent, Designated QIR or Designated Fiduciary, as applicable has countersigned the Matched Questionnaire to make the representations and agreements applicable to it

59

Protocol Agreement (cont.)

• Provides that agreement to enter into or supplement a Matched PCA will be effective on the date on which the later of the two Matched PCA Parties delivers its Protocol Questionnaire

• Protocol Agreement is intended for use without negotiation and without specifying additional provisions, conditions or limitations in the Adherence Letter

• Any adherence that ISDA determines is not in compliance with the Protocol Agreement will be void

• Provides basic representations from PCA Principal and PCA Agent and provides basic agreements of the Matched PCA Parties

Things you may need to be doing in anticipation of these rules

61

• How will these rules apply to you? › Do you plan on entering into new swaps or amending, novating or

terminating existing swaps?

• Questions to consider to amend your documents: › Do you have authority to amend your swap documents or do you

need board approval?

› Do you have authority to modify your internal policies and procedures or do you need board approval?

› Do you need Third Party consent for amendments?

Things you may need to be doing in anticipation of these rules

62

• Be prepared to execute ISDA Protocol Documents or some other agreement to comply with business conduct standards › If you are going to execute the ISDA Protocol Documents, you need

to be sure to:

– Execute an adherence letter

– Be prepared to exchange questionnaires

– Have a sense as to what provisions of the ISDA Protocol Documents will apply to you

› If you are going to work outside of the ISDA Protocol Documents, you should contact your swap dealer soon to understand how that process will work.

Things you may need to be doing in anticipation of these rules

The Financial Markets and Latest Financing Structures

New York State Association for Affordable Housing 2013 Pre-Conference Education Forum

May 7, 2013

Matthew Bissonette

Director

Advanced Topics in Tax-Exempt Bonds

1. Market Overview/Rates

2. CRA

3. Latest Structures and Issues

2

Market Overview

Bank Capital Ratios Have Improved / Leverage Reduced

Capital Markets Have Stabilized

Interest Rates Remain at Historically Low Levels

CRA Mandate is as Significant as Ever

Multifamily Sector Fundamentals Solid

LIHTC Pricing at or Close to All-Time Highs in NYC Market and Notably Higher Upstate than Three/Four Years Ago

The Good News

3

Market Overview

Costs of Multifamily Development and Acquisitions are High

Financial Institutions Have Less Risk Appetite Than Pre-Crisis – Still A Lot of Market Volatility

Significant Differences Remain Between Upstate and Downstate

High Unemployment

The Not-As-Good News

4

*Rates are approximate and change frequently

Interest Rates*

5

Today Years Ago

10-Year Treasury 1.80% 1.88%

10-Year MMD 1.73% 1.80%

30-Year MMD 2.87% 3.13%

NYCERS 30-Year 3.08% 3.42%

CRA

CRA continues to be big driver in bank lending and investing

Revision of CRA Rules – CRA Rules open to comment with comments due in next month or so

6

Latest Structures

Cash Collateral (in lieu of LoC)

Short Term Cash Backed Bonds with GNMA Sale

Bridge to FHA

7

Any terms set forth herein are intended for discussion purposes only and are subject to the final terms as set forth in separate definitive written agreements. This presentation is not a commitment to lend, syndicate a financing, underwrite or purchase securities, or commit capital nor does it obligate us to enter into such a commitment, nor are we acting as a fiduciary to you. By accepting this presentation, subject to applicable law or regulation, you agree to keep confidential the existence of and proposed terms for any transaction contemplated hereby (a “Transaction”). Prior to entering into any Transaction, you should determine, without reliance upon us or our affiliates, the economic risks and merits (and independently determine that you are able to assume these risks) as well as the legal, tax and accounting characterizations and consequences of any such Transaction. In this regard, by accepting this presentation, you acknowledge that (a) we are not in the business of providing (and you are not relying on us for) legal, tax or accounting advice, (b) there may be legal, tax or accounting risks associated with any Transaction, (c) you should receive (and rely on) separate and qualified legal, tax and accounting advice and (d) you should apprise senior management in your organization as to such legal, tax and accounting advice (and any risks associated with any Transaction) and our disclaimer as to these matters. By acceptance of these materials, you and we hereby agree that from the commencement of discussions with respect to any Transaction, and notwithstanding any other provision in this presentation, we hereby confirm that no participant in any Transaction shall be limited from disclosing the U.S. tax treatment or U.S. tax structure of such Transaction.

IRS Circular 230 Disclosure: Citigroup, Inc. and its affiliates do not provide tax or legal advice. Any discussion of tax matters in these materials (i) is not intended or written to be used, and cannot be used or relied upon, by you for the purpose of avoiding any tax penalties and (ii) may have been written in connection with the "promotion or marketing" of the Transaction. Accordingly, you should seek advice based on your particular circumstances from an independent tax advisor. We are required to obtain, verify and record certain information that identifies each entity that enters into a formal business relationship with us. We will ask for your complete name, street address, and taxpayer ID number. We may also request corporate formation documents, or other forms of identification, to verify information provided. Any prices or levels contained herein are preliminary and indicative only and do not represent bids or offers. These indications are provided solely for your information and consideration, are subject to change at any time without notice and are not intended as a solicitation with respect to the purchase or sale of any instrument. The information contained in this presentation may include results of analyses from a quantitative model which represent potential future events that may or may not be realized, and is not a complete analysis of every material fact representing any product. Any estimates included herein constitute our judgment as of the date hereof and are subject to change without any notice. We and/or our affiliates may make a market in these instruments for our customers and for our own account. Accordingly, we may have a position in any such instrument at any time. Citi maintains a policy of strict compliance to the anti-tying provisions of the U.S. Bank Holding Company Act of 1956, as amended, and the regulations issued by the Federal Reserve Board implementing the anti-tying rules (collectively, the "Anti-tying Rules"). Moreover, our credit policies provide that credit must be underwritten in a safe and sound manner and be consistent with Section 23B of the Federal Reserve Act and the requirements of federal law. Consistent with these requirements and our Anti-tying Policy: The extension of commercial loans or other products or services to you by Citibank, N.A. (“Citibank”) or any of its subsidiaries will not be conditioned on your taking other products or services offered by Citibank or any of its subsidiaries or affiliates, unless such a condition is permitted under an exception to the Anti-tying Rules. We will not vary the price or other terms of any product or service offered by Citibank or its subsidiaries on the condition that you purchase another product or service from Citibank or any Citi affiliate, unless we are authorized to do so under an exception to the Anti-tying Rules. We will not require you to provide property or services to Citibank or any affiliate of Citibank as a condition to the extension of a commercial loan to you by Citibank or any of its subsidiaries, unless such a requirement is reasonably required to protect the safety and soundness of the loan. We will not require you to refrain from doing business with a competitor of Citi or any of its affiliates as a condition to receiving a commercial loan from Citibank or any of its subsidiaries, unless the requirement is reasonably designed to ensure the soundness of the loan. Although this material may contain publicly available information about Citi corporate bond research or economic and market analysis, Citi policy (i) prohibits employees from offering, directly or indirectly, a favorable or negative research opinion or offering to change an opinion as consideration or inducement for the receipt of business or for compensation; and (ii) prohibits analysts from being compensated for specific recommendations or views contained in research reports. So as to reduce the potential for conflicts of interest, as well as to reduce any appearance of conflicts of interest, Citi has enacted policies and procedures designed to limit communications between its investment banking and research personnel to specifically prescribed circumstances. © 2009 Citigroup Global Markets Inc. Member SIPC. All rights reserved. Citi and Citi and Arc Design are trademarks and service marks of Citigroup Inc. or its affiliates and are used and registered throughout the world.

In January 2007, Citi released a Climate Change Position Statement, the first US financial institution to do so. As a sustainability leader in the financial sector, Citi has taken concrete steps to address this important issue of climate change by: (a) targeting $50 billion over 10 years to address global climate change: includes significant increases in investment and financing of alternative energy, clean technology, and other carbon-emission reduction activities; (b) committing to reduce GHG emissions of all Citi owned and leased properties around the world by 10% by 2011; (c) purchasing more than 52,000 MWh of green (carbon neutral) power for our operations in 2006; (d) creating Sustainable Development Investments (SDI) that makes private equity investments in renewable energy and clean technologies; (e) providing lending and investing services to clients for renewable energy development and projects; (f) producing equity research related to climate issues that helps to inform investors on risks and opportunities associated with the issue; and (g) engaging with a broad range of stakeholders on the issue of climate change to help advance understanding and solutions. Citi works with its clients in greenhouse gas intensive industries to evaluate emerging risks from climate change and, where appropriate, to mitigate those risks.

efficiency, renewable energy & mitigation 8

Using Recycled Bonds and Bifurcated Structures to Finance Affordable Housing

HDC Overview Overview of the Corporation Portfolio performance and financial status HDC Bond Programs: MFHRB (“Open Resolution”), MFSRB (“Mini-Open Resolution”) and

Stand-Alone issuance

Recycling of Multi Family Bonds Overview Challenges Benefits Examples of recycled loans

Bifurcated Structures Overview Structuring advantages

Table of Contents

73

Established in 1971 under laws of the State of New York as a public benefit corporation for the purpose of financing affordable multi-family housing in the City of New York.

Governed by 7-member Board of Directors appointed by Mayor and Governor; chaired by Commissioner of NYC Department of Housing Preservation and Development.

A staff of 168 manages over $12.1 billion of assets, including a multi-family portfolio of over 180,000 units with $8.87 billion in mortgage loans and loan interests as of January 31, 2013.

The #1 issuer in the nation of mortgage revenue bonds for affordable multi-family housing since 2004

- $19.15 billion of mortgage revenue bonds issued since inception; $1.2 billion in CY 2012 - $8.9 billion of bonds outstanding as of March 31, 2013.

General obligation of HDC rated Aa2/AA by Moody’s and Standard & Poor’s, respectively (S&P’s

most recent affirmation report is dated May 30, 2012. Moody’s recently re-affirmed HDC’s ratings in December 2012 in a write-up on NYCHDC MFHRB 2012 Series K/L/M).

Separately capitalized, mortgage insurer (REMIC) rated AA by S&P.

Overview of NYC Housing Development Corporation

74

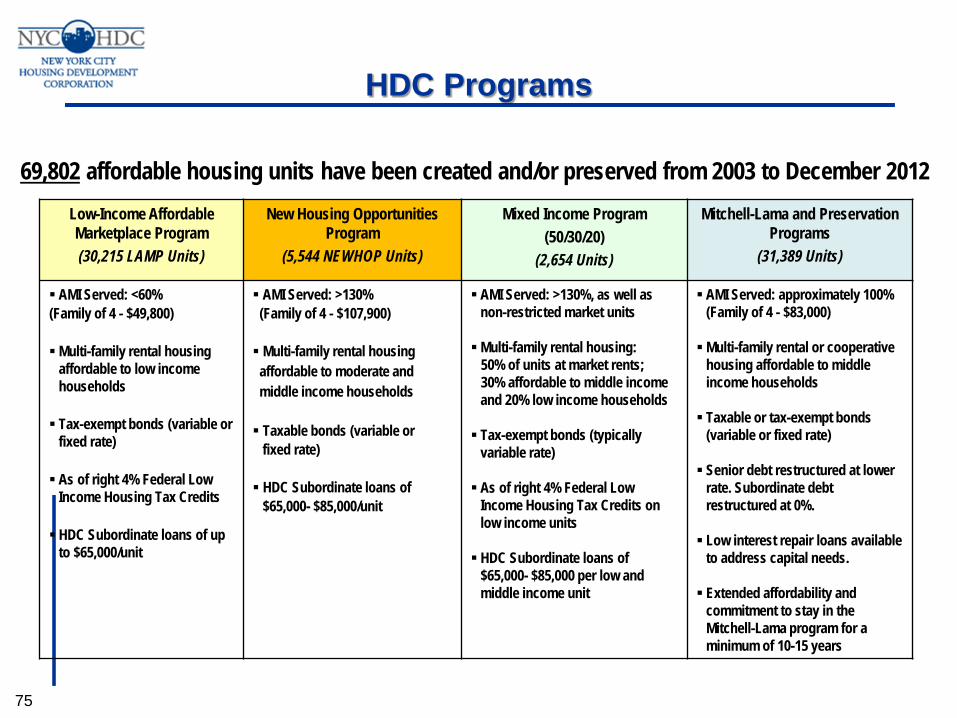

69,802 affordable housing units have been created and/or preserved from 2003 to December 2012

HDC Programs

Low-Income Affordable Marketplace Program (30,215 LAMP Units)

New Housing Opportunities Program

(5,544 NEWHOP Units)

Mixed Income Program (50/30/20)

(2,654 Units)

Mitchell-Lama and Preservation Programs

(31,389 Units)

AMI Served: <60% (Family of 4 - $49,800) Multi-family rental housing

affordable to low income households Tax-exempt bonds (variable or

fixed rate) As of right 4% Federal Low

Income Housing Tax Credits HDC Subordinate loans of up

to $65,000/unit

AMI Served: >130% (Family of 4 - $107,900) Multi-family rental housing affordable to moderate and middle income households Taxable bonds (variable or fixed rate) HDC Subordinate loans of $65,000- $85,000/unit

AMI Served: >130%, as well as non-restricted market units Multi-family rental housing: 50% of units at market rents; 30% affordable to middle income

and 20% low income households Tax-exempt bonds (typically

variable rate) As of right 4% Federal Low

Income Housing Tax Credits on low income units HDC Subordinate loans of

$65,000- $85,000 per low and middle income unit

AMI Served: approximately 100% (Family of 4 - $83,000) Multi-family rental or cooperative

housing affordable to middle income households Taxable or tax-exempt bonds

(variable or fixed rate) Senior debt restructured at lower

rate. Subordinate debt restructured at 0%. Low interest repair loans available

to address capital needs. Extended affordability and

commitment to stay in the Mitchell-Lama program for a minimum of 10-15 years

75

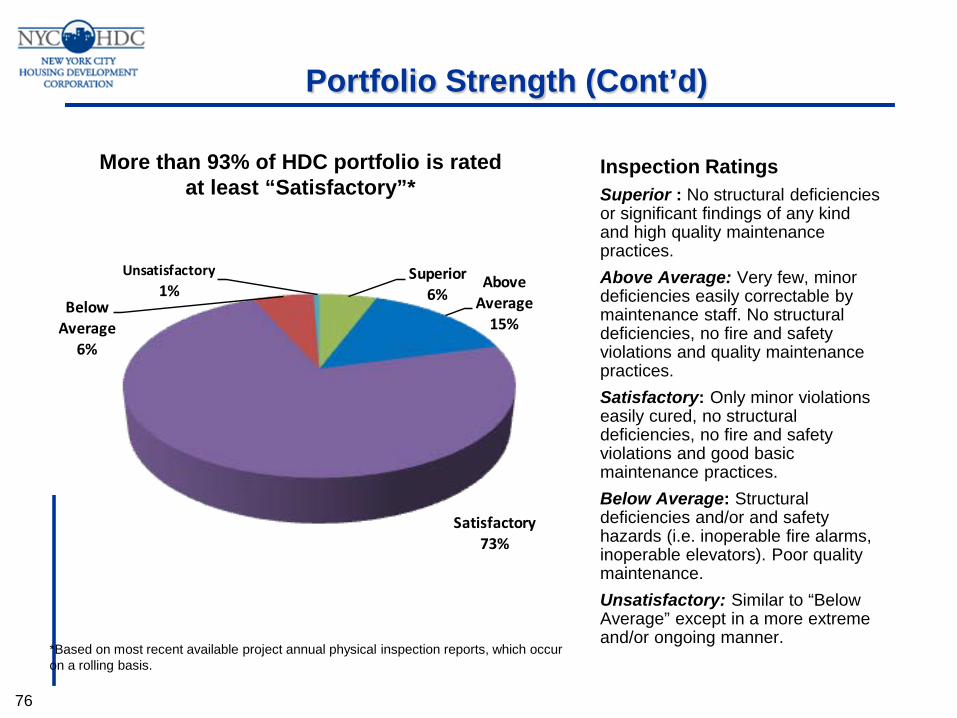

Portfolio Strength (Cont’d)

Superior6%

Above Average

15%

Satisfactory73%

Below Average

6%

Unsatisfactory1%

Inspection Ratings Superior : No structural deficiencies or significant findings of any kind and high quality maintenance practices. Above Average: Very few, minor deficiencies easily correctable by maintenance staff. No structural deficiencies, no fire and safety violations and quality maintenance practices. Satisfactory: Only minor violations easily cured, no structural deficiencies, no fire and safety violations and good basic maintenance practices. Below Average: Structural deficiencies and/or and safety hazards (i.e. inoperable fire alarms, inoperable elevators). Poor quality maintenance. Unsatisfactory: Similar to “Below Average” except in a more extreme and/or ongoing manner.

*Based on most recent available project annual physical inspection reports, which occur on a rolling basis.

76

More than 93% of HDC portfolio is rated at least “Satisfactory”*

77

$0.0 $1.0 $2.0 $3.0 $4.0 $5.0 $6.0 $7.0 $8.0 $9.0

$10.0 $11.0 $12.0 $13.0

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Bil

lio

ns

HDC Fiscal Year

Assets Liabilities Net Position

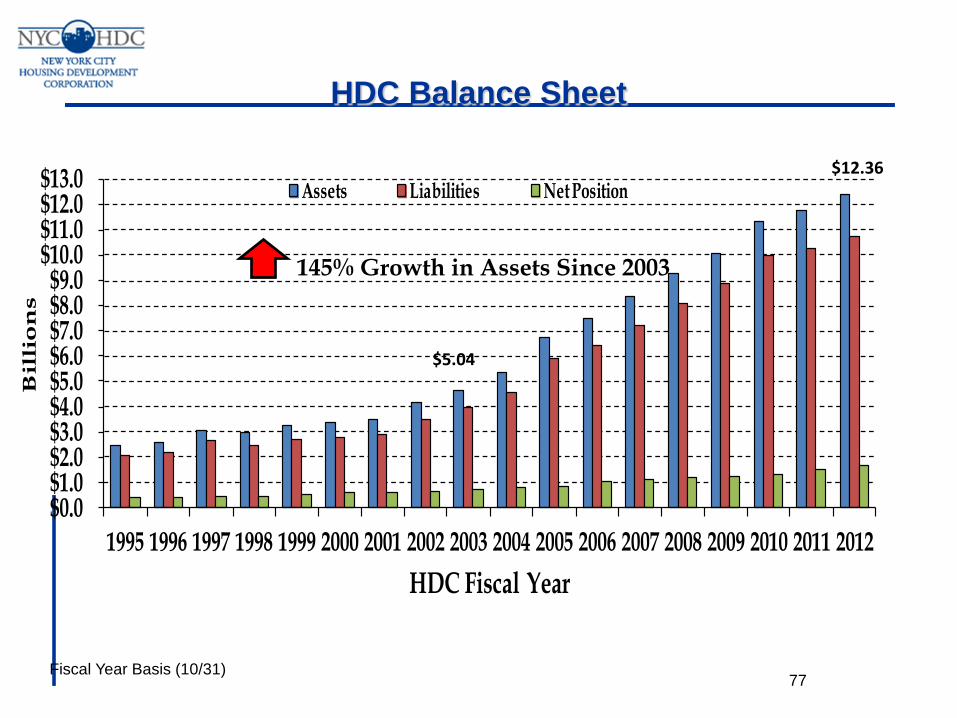

HDC Balance Sheet

145% Growth in Assets Since 2003

$5.04

$12.36

Fiscal Year Basis (10/31)

78

$0.0 $0.1 $0.2 $0.3 $0.4 $0.5 $0.6 $0.7 $0.8 $0.9 $1.0 $1.1 $1.2 $1.3 $1.4 $1.5 $1.6 $1.7

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Bil

lion

s

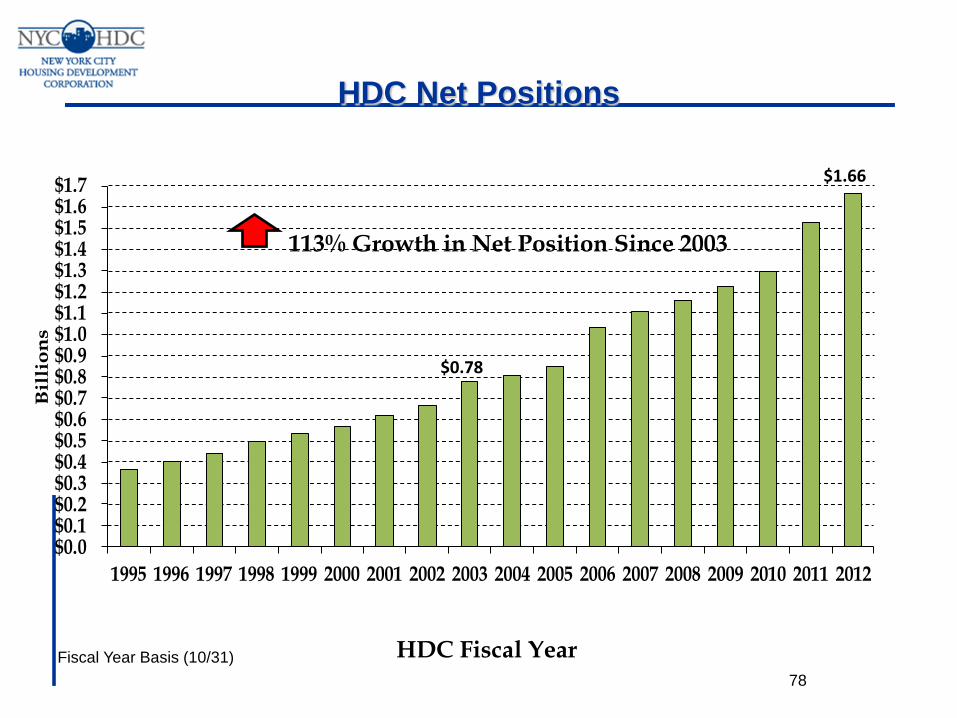

HDC Net Positions

113% Growth in Net Position Since 2003

$0.78

$1.66

Fiscal Year Basis (10/31) HDC Fiscal Year

$0.00$1.00$2.00$3.00$4.00$5.00$6.00$7.00$8.00$9.00

$10.00

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Bil

lio

ns

HDC Fiscal Year

79

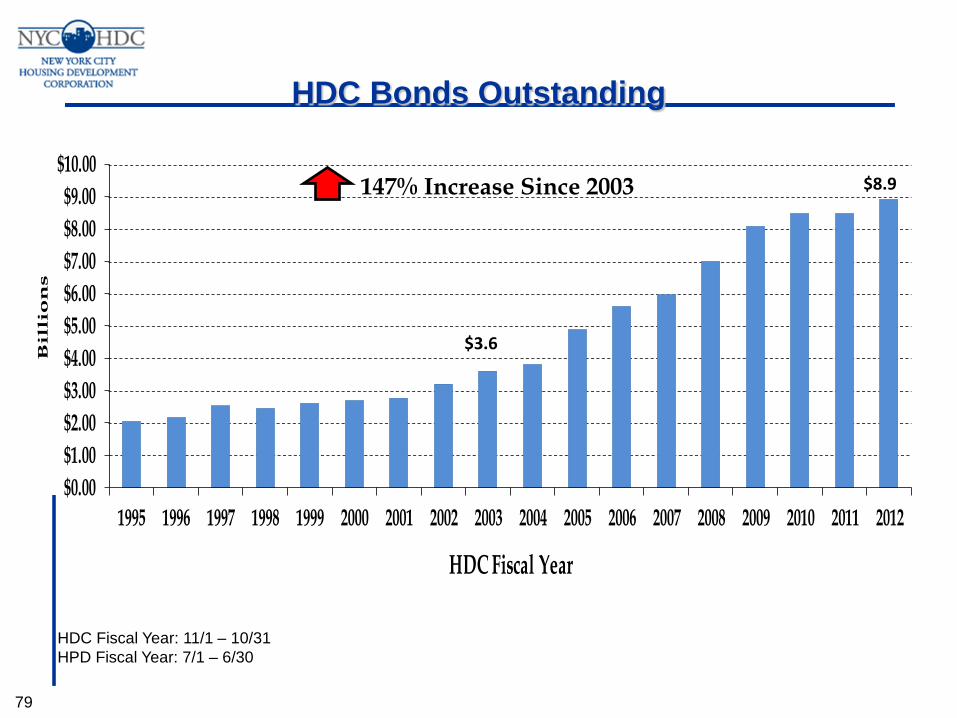

HDC Bonds Outstanding

147% Increase Since 2003

HDC Fiscal Year: 11/1 – 10/31 HPD Fiscal Year: 7/1 – 6/30

$3.6

$8.9

80

HDC has provided over $1.28 billion in 1% subordinate loans funded from its corporate reserves since 2003 in response to Mayor Bloomberg’s New Housing Marketplace Plan

HDC’s Subsidy Contribution

-

200

400

600

800

1,000

1,200

1,400

1,600

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013*

Annual Total Cumulative Total Since 2003

Mill

ion

Fiscal Year Basis (10/31) *Projected HDC Fiscal Year

Multi-Family Housing Revenue Bond Resolution (“MFHRB” or “Open Resolution”)

Established in 1993, the Open Resolution is HDC’s largest single asset, with over $3.75 billion of bonds outstanding in over 130 series and in excess of $5.9 billion of multi-family loans, reserves and other assets(1).

The Open Resolution permits the issuance of an unlimited amount of parity debt. Annual net income for Open Resolution has averaged over $40 million over the past five years. Surplus

revenues can be withdrawn from the Resolution, subject to rating agency cash flow tests. Rated Aa2/AA by Moody’s/S&P; 123% over-collateralization.(2)

Multi-Family Secured Revenue Bond Resolution (“Mini-Open Resolution”) Established in 2005, the Mini-Open Resolution has $64.6mm of bonds outstanding in 4 series with

$100mm of mortgage loans as of January 31, 2013. Permits the issuance of an unlimited amount of parity debt to finance secured mortgage loans. Rated Aa1 by Moody’s.

Stand-Alone Issuance Conduit financing for middle-income, 80/20, and Liberty Bond deals. No credit risk to the Corporation.

81

HDC Bond Programs

(1) As of January 31, 2013; Includes NIBP (Federal New Issue Bond Program) and certain acquired “City Loans” that revert to the City of New York upon retirement of related bonds (2) As of October 31, 2011; Reflects assumed modified cash basis for cash flow projections. Adjusted to exclude subordinate lien assets not assigned a valuation by the rating

agencies

Recycled Bonds recognize the value of preserving

volume cap for affordable housing by re-using bond authority from traditional tax credit transactions that had been previously redeemed and thus no longer available for tax exempt loans. It is similar to recycling authority for single family housing revenue bonds.

Enacted into Federal Law under the Housing and Economic Recovery Act of 2008 (Section 3007).

Recycled Program targets mixed-income or preservation projects that are not heavily relying on tax credit equity because the refunding bonds do not generate new 4% as-of-right tax credits.

82

Recycled Bonds Background

Since this statute was put in place, HDC has developed a program that has successfully recycled over $657mm of tax-exempt bonds either through issuance of COBs (two-thirds) or direct allocations (one-third), financing 52 projects encompassing over 18,000 units.

In addition, since October 2012, HDC provided over $131 million of excess prepayments to NYSHFA that have been recycled into new HFA loans.

83

Recycled Bonds Background

The bond refunding must occur within 4 years of the initial issuance for an eligible rental housing project originally financed with private activity bonds.

Requires new loan to an eligible project within 6 months of the effective date of the prepayment

The maximum maturity for recycled bonds can only be a total of 34 years from the initial bond issuance

The new project is subject to public notice requirements (TEFRA) prior to the issuance of the refunding bonds

Recycled bonds are not eligible for LIHTC. Projects using recycled bonds must follow tax exempt

bonds rules for household affordability. 84

Rules for Recycled Bonds

Six months is not a great deal of time to arrange a new financing for an eligible project. We have requested a legislative change that will increase this to 1 year

The original debt must be refunded before the original bonds are redeemed.

Prepayments need to be coordinated and timed to allow for refunding of the initial debt

HDC has had to use convertible option bonds as a vehicle to refund the original bonds in a manner which allows the original projects to prepay their debt.

85

Challenges of Recycling

Recycled bonds are limited by supply and demand constraints. Supply is limited because only issuers that issue a

great deal of private activity bonds for deals with tax credits will have large prepayments for recycling Demand is limited because most multifamily housing

requires significant subsidies and thus need LIHTC and demand for recycling would go up if volume cap was less available then it is the case generally today.

HDC is unusual because we have such affordable housing needs across income spectrums that we subsidize housing at non tax credit levels and have historically been private activity bond cap constrained.

86

Limitations on Use of Recycled Bonds

In states, particularly NYS, where there is a scarcity of volume cap, recycling creates capacity for tax exempt bonds.

Allows Issuers to prioritize their use of new money volume cap allocated for multifamily housing to be used on projects which will have “as of right” LIHTC.

Recycling is a tool to encourage more affordability in mixed income projects. Such projects need to satisfy the normal tax exempt bond rules of affordability in order to qualify for the tax exempt financing.

Permits more efficient use of volume cap for 80/20 financings, with a portion of the bonds that are in excess of the 50% requirement (for LIHTC) utilizes recycled cap.

87

Benefits of Recycling Bonds

When using recycled bond proceeds, the project does not have to change owners as is the case with a tax credit tax-exempt financing.

This is particularly beneficial when the project being acquired carries a large amount of debt that would generate a large amount of phantom income. When recycled proceeds are used, the acquisition can be

structured as a no tax event, and the acquisition costs will be lower. The interest of the existing owner can be reduced and replaced with a new managing partner.

On projects where there is a higher income limit (eg. 80%), the loan may be able to be underwritten to a higher amount.

88

Benefits of Recycling Bonds

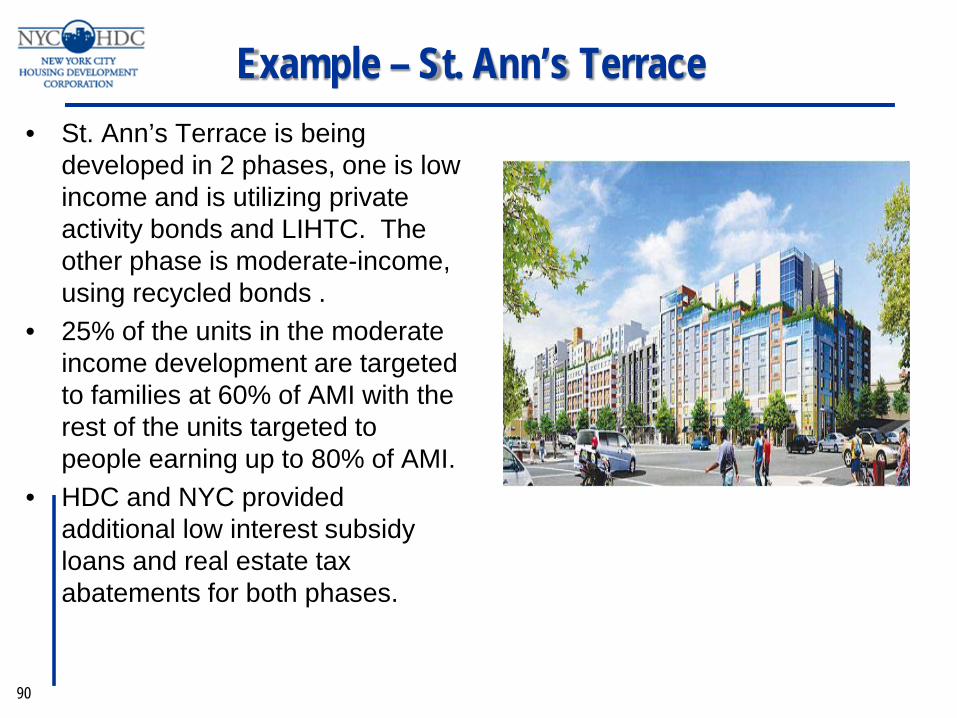

• St. Ann’s Terrace is the nation’s first moderate-income housing complex to use recycled bonds.

• Developed on a 3.5-acre site formerly zoned for industrial use in the Melrose neighborhood of the Bronx.

• St. Ann’s Terrace is a mixed-use development with more than 600 residential units, 45,000-square-feet of ground floor commercial space and underground parking.

• The moderate income component will house 166 households and most of the commercial space.

89

Example – St. Ann’s Terrace

St. Ann’s development has recently converted. Recycled Bonds: $25.8 million 1% Subsidy Loan: $14.1 million

• St. Ann’s Terrace is being developed in 2 phases, one is low income and is utilizing private activity bonds and LIHTC. The other phase is moderate-income, using recycled bonds .

• 25% of the units in the moderate income development are targeted to families at 60% of AMI with the rest of the units targeted to people earning up to 80% of AMI.

• HDC and NYC provided additional low interest subsidy loans and real estate tax abatements for both phases.

90

Example – St. Ann’s Terrace

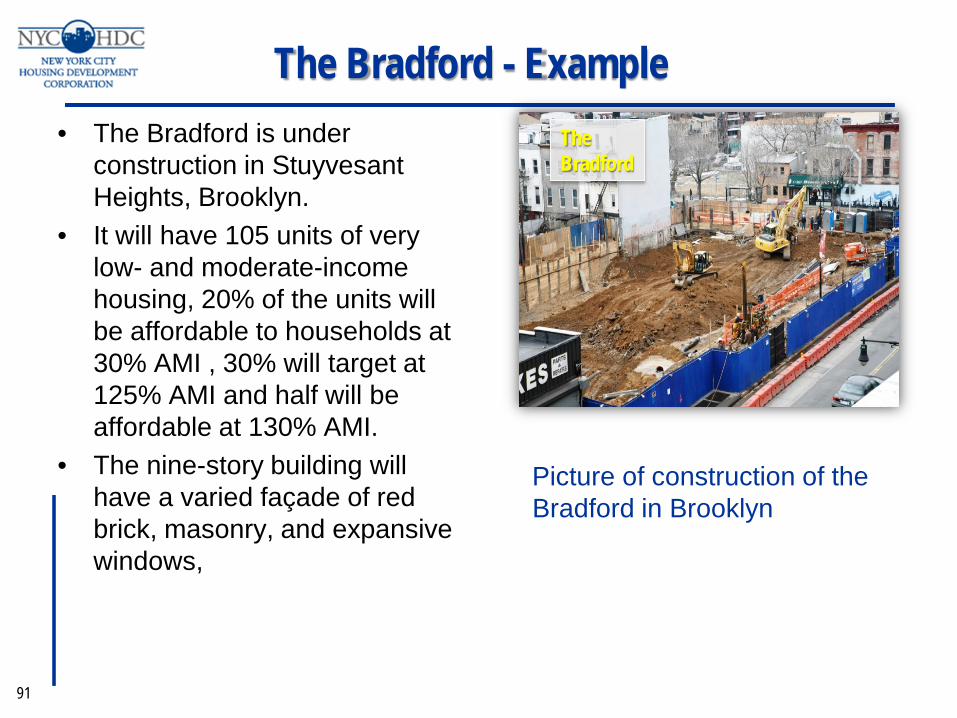

• The Bradford is under construction in Stuyvesant Heights, Brooklyn.

• It will have 105 units of very low- and moderate-income housing, 20% of the units will be affordable to households at 30% AMI , 30% will target at 125% AMI and half will be affordable at 130% AMI.

• The nine-story building will have a varied façade of red brick, masonry, and expansive windows,

Picture of construction of the Bradford in Brooklyn

91

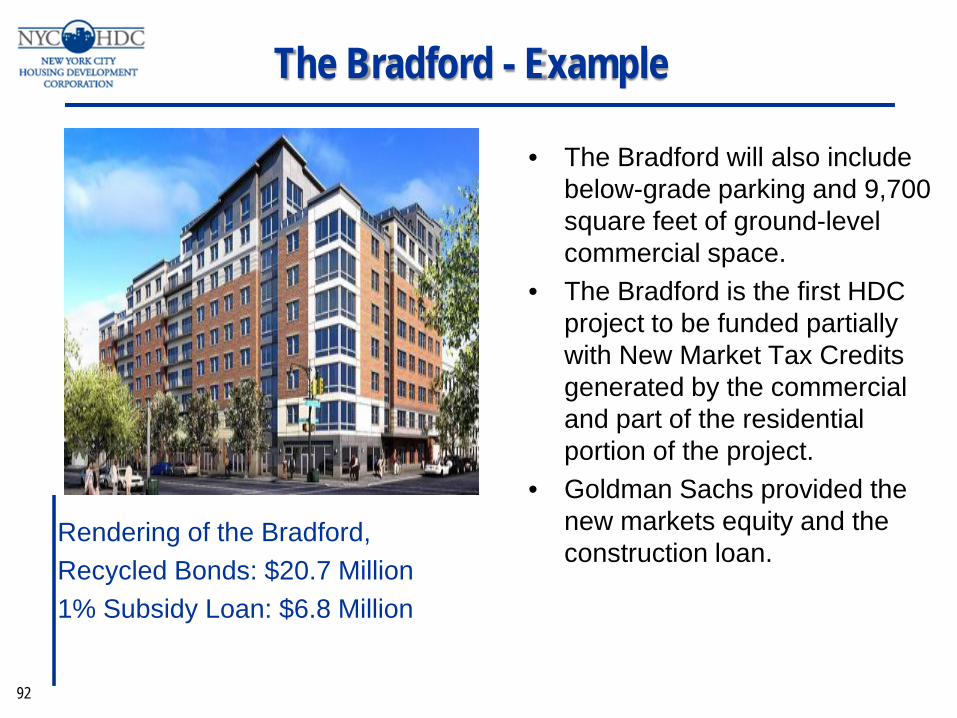

The Bradford - Example The Bradford

Rendering of the Bradford, Recycled Bonds: $20.7 Million 1% Subsidy Loan: $6.8 Million

• The Bradford will also include below-grade parking and 9,700 square feet of ground-level commercial space.

• The Bradford is the first HDC project to be funded partially with New Market Tax Credits generated by the commercial and part of the residential portion of the project.

• Goldman Sachs provided the new markets equity and the construction loan.

92

The Bradford - Example

rd

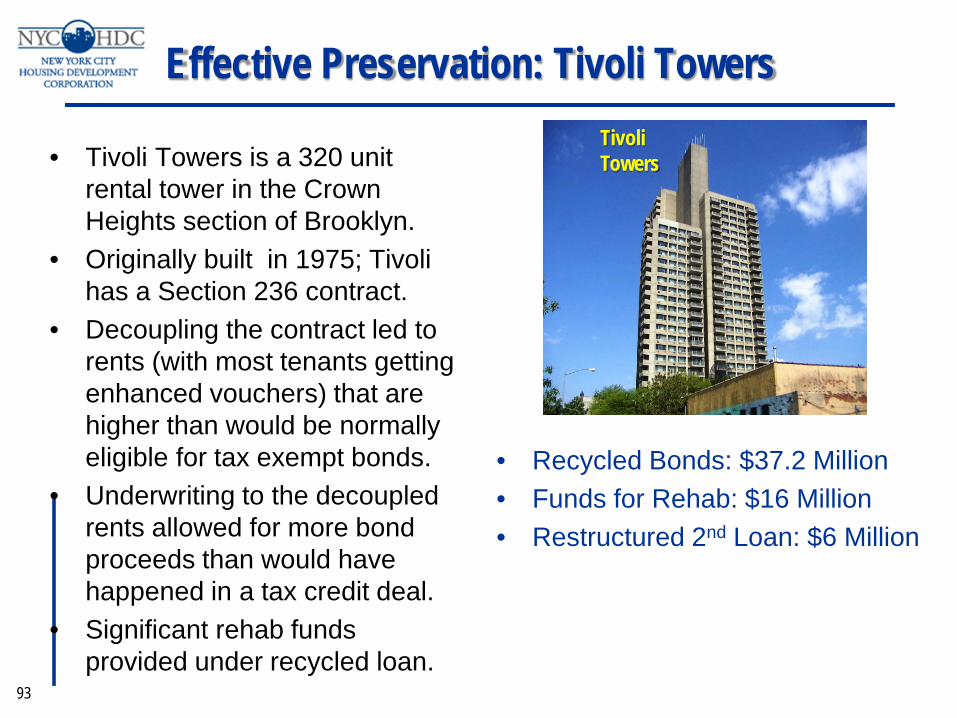

• Tivoli Towers is a 320 unit rental tower in the Crown Heights section of Brooklyn.

• Originally built in 1975; Tivoli has a Section 236 contract.

• Decoupling the contract led to rents (with most tenants getting enhanced vouchers) that are higher than would be normally eligible for tax exempt bonds.

• Underwriting to the decoupled rents allowed for more bond proceeds than would have happened in a tax credit deal.

• Significant rehab funds provided under recycled loan.

• Recycled Bonds: $37.2 Million • Funds for Rehab: $16 Million • Restructured 2nd Loan: $6 Million

93

Effective Preservation: Tivoli Towers Tivoli Towers

Tool for mixed income financings where only the low income units are financed with private activity bonds and LIHTC.

Mixed income developers have the following priorities: Qualify for tax abatements (in NY §421(a)) Finance qualifying units with LIHTC Lower financing costs by utilizing tax-exempt bond

financing By creating separate condos (or sub-leases) for the low

income and market rate units, tax-exempt bonds can be issued to finance construction of the low income units and either taxable bonds or bank loans can be used to finance the market rate units.

94

Bifurcated Structures

By financing only the low income units instead of all of

the units with tax-exempt bonds, the amount of volume cap needed to meet the 50% test is greatly reduced.

There is no need for deep rent skewing and annual income certification since all of the units in the tax-exempt financed condo are low income.

Under federal law, only the low income condo is considered a low income building and the market component is irrelevant, but for New York law, the development is considered to be one unified building and will qualify for the §421(A) tax abatement.

95

Bifurcated Structures

The bifurcated structure allows the developer to sell the

credits for the low income units without allocating the tax credit investor the income from the market rate units.

Tax credit investors may prefer this structure because: They are able to acquire the credits and the losses

generated by the low income units Once construction is completed and the low income units

are placed in service, the tax-exempt debt is retired with the proceeds of the tax credits. There is no permanent tax-exempt debt outstanding for the low income units.

Compliance is easier on an all low-income development.

96

Bifurcated Structures