Embed Size (px)

Citation preview

8/3/2019 Historical Perspective of Rate Cuts

http://slidepdf.com/reader/full/historical-perspective-of-rate-cuts 1/5

Comment MORGAN STANLEY DEAN WITTER

Please refer to important disclosures at the end of this report.

Page 1

Strategy

Equity Research

North America

Market Commentary/Strategy January 11, 2001Anand S. Iyer, CFA+1 (1)212 761 [email protected]

Historical Perspective of Rate Cuts

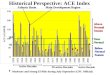

• Historical Perspective of Fed Rate Cuts

The history of rate cuts has consistently led to a rise in the convertible

market

• Since 1985, There Have Been 7 Rate Cuts

Cuts occurred in 1998, ’96 ’92 ’91, ’89, ’86 and ’85 - during whichtime the convertible market rose an average of 21%.

• In 1991, When Rates Were Cut from 7.00% to 4.00%, The Convertib le market

Rose by 32.9%, and in 1992, When Rates Were cut by 100 bps, The

Convertible Market Rose by 18.3%

Although 2001 may not exactly replicate 1991-1992, we think areduction in rates of a 200 basis point magnitude could result in a 15-20% convertible market return in 2001.

U.S. Convertible Research

8/3/2019 Historical Perspective of Rate Cuts

http://slidepdf.com/reader/full/historical-perspective-of-rate-cuts 2/5

MORGAN STANLEY DEAN WITTER

U.S. Convertible Research – January 11, 2001

Please refer to important disclosures at the end of this report.

Page 2

Historical Perspective of Rate Cuts

Over the Past Month We Have Made Several Changes inthe MSDW Convertible Recommended Portfolio.

As we expect overall earnings to be slower, and short rates

to continue to decline, our strategy is to select those

convertibles which offer:

1. High yield-to-maturity, where earnings growth

prospects should occur later in 2001

2. Those interest rate sensitive sector convertibles which

would benefit from a decline in interest rates.

3.

Some value convertibles from telecom sector whichsuffered greatly in the year 2000.

Therefore, our recommendations are:

High Yield Convertibles:

• NVIDIA (NVDA) 4.75% Convertible SubordinatedNotes due 2007

• International Rectifier (IRF) 4.25% ConvertibleSubordinated Notes due 2007

• Excite@Home (ATHM) 0.525% (OID) ConvertibleSubordinated Debentures due 2018

• Aether Systems (AETH) 6.00% Convertible

Subordinated Notes due 2005

Rate Cut Beneficiaries:

• Fifth Third Bancorp (FITB) $1.50 Trust ConvertiblePreferred Stock due 2028

• ACE Limited (ACL) $4.125 PEPS due 2003

• Providian Financial (PVN) 3.25% ConvertibleSubordinated Notes due 2005

Telecom:

• TCI Pacific/TCOMA (T) $5.00 ConvertiblePreferred due 2006

• Global Crossing (GX) $16.875 (6.75%) ConvertiblePreferred Stock due 2012

Exhibit 1

Interest Rate Changes and Convertible Market Performance, 1985 - 2000 (Rate Cut Years in Bold)

Total ReturnConvertible NASDAQ

Fed’s Rate Action Commentary Market Composite

Current 6.00% Federal Reserve is expected to continue to cut rates.

2000 5.50% 6.50% Rate increases on 2/2 & 3/21 followed by 50 bps hike on 5/16 -18.01% -40.09%

1999 4.75% 5.50% Three rate hikes are mitigated by Y2K liquidity 41.47% 84.83%

1998 5.50% 4.75% 18 months of rate stability followed by three late-year cuts 6.67% 39.21%

1997 5.25% 5.50% One rate hike followed by a long period of stable rates 18.40% 23.14%

1996 5.50% 5.25% One early rate cut on 1/31 followed by a stable rate trend 15.06% 21.95%

1995 5.5% 6.0% 5.5% Rate rises 50 bps to 6.00% on 2/1 followed by 2 rate cuts 24.74% 42.58%1994 3.00% 5.50% Series of six rate hikes from 2/4 through 11/15 -4.71% -2.43%

1993 Stable @ 3.00% Rate is constant for 17 months 19.47% 15.63%

1992 4.00% 3.00% Three rate cuts totaling 100 bps occur in 2-3 mo. intervals 18.34% 15.43%

1991 7.00% 4.00% Ten rapid rate cuts totaling 300 bps occur by year-end 32.85% 57.54%

1990 8.25% 7.00% Four late-year rate cuts total 125 basis points -6.40% -18.61%

1989 9.00% 8.25% Five early-year rate hikes are followed by six rate cuts 13.80% 20.14%

8/3/2019 Historical Perspective of Rate Cuts

http://slidepdf.com/reader/full/historical-perspective-of-rate-cuts 3/5

MORGAN STANLEY DEAN WITTER

U.S. Convertible Research – January 11, 2001

Please refer to important disclosures at the end of this report.

Page 3

Exhibit 2

Interest Rate Changes and Convertible Market Performance, 1985 - 2000 (Rate Cut Years in Bold)Column Headings

1988 6.83% 8.69% Ten incremental rate hikes negate easing early in the year. 13.30% 12.67%

1987 6.00% 6.83% Rates increase via five rate hikes despite two inter-year cuts -5.90% -6.45%

1986 7.75% 5.875% Four rate cuts result in 187.5 bps easing 14.53% 7.34%.

1985 8.125% 7.75% Moderate 37.5 bps easing resulting from 13 rate decisions 26.26% 32.25%

Notes: The years indicated in Bold are those years in which Federal Reserve interest rate cuts relate to positive equity and convertible market performance

Sources: Federal Reserve Data and Morgan Stanley Dean Witter

NVIDIA (NVDA) 4.75% Convertible SubordinatedNotes due 2007 - (Convertible Price: 75%, stock price:$44.3125). With a 6.3% current yield and a 9.9% yieldto its 2007 maturity, the NVDA 4.75% convertible notes

suggest a solid degree of defensiveness relative to thecommon stock, in our view. Using a volatility of 55%,which is about 66% of the company’s long term calloption volatility, and a 700 basis point spread, producesa theoretical valuation of 80%, suggesting the security is13% undervalued based on its current price. In addition,Mark Edelstone believes Strong Buy rated NVDA isenjoying strong market share gains in the desktop PCmarket, combined with the opportunity to enjoyadditional revenue streams from new products in thenext 6 to 9 months.

International Rectifier (IRF) 4.25% ConvertibleSubordinated Notes due 2007 - (Convertible Price:75.125%, stock price: $36.8125). At current levels, wefavor the convertible for yield-oriented investors as thesecurity offers a 5.7% current yield and a 9.6% yield toits July 15, 2007 maturity. Its 53% conversion premiumand 50% delta suggest moderate participation in theunderlying common, while its 2.4% premium overinvestment value points to a solid level of defensivenessas long as credit spreads remain at recent levels. Mark Edelstone believes IRF will meet operating expectationsfor the December quarter and that continued solidexecution should enable growth in the March quarter.Currently trading at C2001 PEG of 0.3x and 10xearnings, IRF looks to be undervalued.

Excite@Home (ATHM) 0.525% (OID) ConvertibleSubordinated Debentures due 2018 - (ConvertiblePrice: 37.00%, stock price: $7.00). We view the ATHM0.525% (OID) convertible bond as a credit sensitivechoice. The convertible offers a 1.4% current yield but a19.0% yield-to-put in less than three years. The issue istrading at an implied credit spread of 1,828 basis pointswhich implies a 10% premium to investment value.

Aether Systems (AETH) 6.00% ConvertibleSubordinated Notes due 2005 - (Convertible Price:59.50%, stock price: $37.4375). We continue view theAETH convertible as a defensive means of stayinginvolved in the enterprise wireless systems space and as

appropriate for credit sensitive investors. The issuecurrently offers an 10.9% current yield and an equity-like 21.2% yield to its 3/05 maturity, a relatively soundthesis, considering the company’s cushion of over $1billion of cash. The company’s $27 per share of cashnow represents over 75% of AETH’s common stock price.

Given our expectation of continued rate cuts, we havealso modified the MSDW Recommended Convertible

Portfolio by adding interest sensitive securities,specifically those from the financials group, as it couldaugur a more favorable investment climate for thesector. Our three recent additions to the MSDW

Convertible Recommended Portfolio in the financialsector includes:

Fifth Third Bancorp (FITB) $1.50 Trust ConvertiblePreferred Stock due 2028 - (Convertible Price:$37.6875, stock price: $59.9375). We view the FITB asattractive as it offers a reasonable 3.97% current yieldand high 94% delta with which to participate in thecommon and offers an opportunity for conservativeinvestors due to its Aa3/A investment grade rating. Wenote that Diane Merdian raised her investment rating onFITB common stock to Outperform from Neutral lastNovember on the heels of the company’s announced

$4.9 billion acquisition of Old Kent Financial.

ACE Limited (ACL) $4.125 PEPS due 2003 -(Convertible Price: $76.4375, stock price: $36.375). Weview the ACL $4.125 PEPS as an equity substitute givenits high delta and low conversion premium. ThisA2/BBB rated issue offers a 5.4% current yield (a 384basis point advantage to the common), and trades with a75% delta and 10% conversion premium. AliceSchroeder upgraded ACE common from Outperform to

8/3/2019 Historical Perspective of Rate Cuts

http://slidepdf.com/reader/full/historical-perspective-of-rate-cuts 4/5

MORGAN STANLEY DEAN WITTER

U.S. Convertible Research – January 11, 2001

Please refer to important disclosures at the end of this report.

Page 4

Strong Buy last week with 34% upside on the commonto her new target of $50.

Providian Financial (PVN) 3.25% Convertible

Subordinated Notes due 2005 - (Convertible Price:99.125%, stock price: $54.4375). The issue offers a3.6% current yield (a 279 basis point advantage over thecommon), a 3.13% yield to the 8/15/05 maturity and has2.61 years of call protection. Using a 400 basis pointcredit spread and a 45% stock volatility, we think thisissue is currently 4% undervalued.

As far as the telecom sector is concerned, we favor thisgroup since we believe that a return of confidence in thetelecom sector and availability of funds to companieswithin the sector could mean that concerns about lack-of-funding - especially among larger, more established

companies - would begin to dissipate.

TCI Pacific/TCOMA (T) $5.00 Convertible Preferreddue 2006 - (Convertible Price: $150.625, stock price:$23.125). We especially favor AT&T and added thissecurity to The Portfolio on 12/26/00, thinking thatAT&T’s announced quarterly reduction on 12/20/2000to $0.15 from $0.88 on an annual basis has sharplyimproved the valuation of the TCI Pacific/TCOMA$5.00 convertible preferred stock (exchangeable intoshares of AT&T) for large cap value investors. We alsoview the security attractive for its upside/downsideparticipation of 83%/40% in the common until its call

date of 8/15/01. We believe both equity-sensitive anddefensive value investors would find this investmentgrade (Baa2/BBB+) convertible preferred stock attractive. We add that Simon Flannery upgraded T

common stock to Strong Buy from Neutral yesterdaynoting that the company’s upcoming four-way break upshould help unlock substantial value for shareholders.

Global Crossing (GX) $16.875 (6.75%) ConvertiblePreferred Stock due 2012 - (Convertible Price:$194.500, stock price: $22.625). We view all three of theGX convertible issues as attractive middle-of-the-roadchoices given their balance of upside potentialparticipation and high current income. However, weprefer the GX $16.875 (6.75%) security as it offers a8.8% current yield, a 10.3% yield to stated maturity, andreasonable equity participation with a 66% delta, and thelongest call protection of the three securities at 4.26years. The security has added takeover protection in thecase of a cash merger.

Finally, we also like Union Pacific as a large cap valueplay:

Union Pacific (UNP) $3.125 Convertible PreferredStock due 2028 - (Convertible Price: $49.00, stock price: $53.188). In our view, the UNP $3.125convertible preferred is appropriate as a way of participating in the favorable energy trends that are acomponent of our investment thesis. The Ba2/'BB+ ratedpreferred offers a 6.4% current yield (a 486 basis pointpick-up over the common) with a 47% delta thatsuggests moderate participation in the common. Webelieve the full valuation of this security, and relatively

high volatility, are due in large part to the practicalconsiderations of the company's investment merits. It isan asset-rich company with a solid credit profile and aclassic "old economy" safe haven.

8/3/2019 Historical Perspective of Rate Cuts

http://slidepdf.com/reader/full/historical-perspective-of-rate-cuts 5/5

MORGAN STANLEY DEAN WITTER

The Americas Europe Japan Asia/Pacific

1585 BroadwayNew York, NY 10036-8293Tel: (1) 212 761-4000

25 Cabot Square, Canary Wharf London E14 4QA, EnglandTel: (44 20) 7513 8000

20-3, Ebisu 4-chome Shibuya-ku,Tokyo 150-6008, JapanTel: (81) 3 5424 5000

Three Exchange SquareHong KongTel: (852) 2848 5200

4th Floor Forbes BuildingCharanjit Rai Marg FortMumbai 400 001, IndiaTel: (91 22) 209 6600

BCE Place, 181 Bay Street,Suite 3700Toronto, Ontario M5J 2T3,Canada

Tel: (1) 416 943-8400

Serrano, 5528006 MadridSpainTel: (31 91) 412 11 00

23 Church Street#16-01 Capital SquareSingapore 049481Tel: (65) 834 6888

The Chifley Tower, Level 332 Chifley SquareSydney NSW 2000, AustraliaTel: (61 2) 9770 1111

© 2001 Morgan Stanley Dean Witter

____________________________________________________

The information and opinions in this report were prepared by Morgan Stanley & Co. Incorporated (“Morgan Stanley Dean Witter”). Morgan Stanley Dean Witter doesnot undertake to advise you of changes in its opinion or information. Morgan Stanley Dean Witter and others associated with it may make markets or specialize in,have positions in and effect transactions in securities of companies mentioned and may also perform or seek to perform investment banking services for thosecompanies. This memorandum is based on information available to the public. No representation is made that it is accurate or complete. This memorandum is not anoffer to buy or sell or a solicitation of an offer to buy or sell the securities mentioned.

Within the last three years, Morgan Stanley & Co. Incorporated, Dean Witter Reynolds Inc. and/or their affiliates managed or co-managed a public offering of thesecurities of Aether Systems, Excite@Home, AT&T, Global Crossing Ltd., International Rectifier, NVIDIA Corporation, and Union Pacific.

Morgan Stanley & Co. Incorporated, Dean Witter Reynolds Inc. and/or their affiliates make a market in the securities of Aether Systems, AT&T, Fifth Third Bancorp,NVIDIA Corporation, Excite@Home, and Global Crossing Ltd.

Morgan Stanley & Co. Incorporated, Dean Witter Reynolds Inc. and/or their affiliates or their employees have or may have a long or short position or holding in thesecurities, options on securities, or other related investments of issuers mentioned herein.

An employee or director of Morgan Stanley & Co. Incorporated, Dean Witter Reynolds Inc. and/or their affiliates is a director of Union Pacific.

The investments discussed or recommended in this report may not be suitable for all investors. Investors must make their own investment decisions based on theirspecific investment objectives and financial position and using such independent advisors as they believe necessary. Where an investment is denominated in a currencyother than the investor’s currency, changes in rates of exchange may have an adverse effect on the value, price of, or income derived from the investment. Pastperformance is not necessarily a guide to future performance. Income from investments may fluctuate. The price or value of the investments to which this reportrelates, either directly or indirectly, may fall or rise against the interest of investors.

To our readers in the United Kingdom: This publication has been issued by Morgan Stanley Dean Witter and approved by Morgan Stanley & Co. International Limited,regulated by the Securities and Futures Authority Limited. Morgan Stanley & Co. International Limited and/or its affiliates may be providing or may have providedsignificant advice or investment services, including investment banking services, for any company mentioned in this report. Private investors should obtain the adviceof their Morgan Stanley & Co. International Limited representative about the investments concerned.

This publication is disseminated in Japan by Morgan Stanley Dean Witter Japan Limited and in Singapore by Morgan Stanley Dean Witter Asia (Singapore) Pte.

To our readers in the United States: While Morgan Stanley Dean Witter has prepared this report, Morgan Stanley & Co. Incorporated and Dean Witter Reynolds Inc.are distributing the report in the US and accept responsibility for it contents. Any person receiving this report and wishing to effect transactions in any security

discussed herein should do so only with a representative of Morgan Stanley & Co. Incorporated or Dean Witter Reynolds Inc.

To our readers in Spain: AB Asesores Morgan Stanley Dean Witter, SV, SA, a Morgan Stanley Dean Witter group company, supervised by the Spanish SecuritiesMarkets Commission (CNMV), hereby states that this document has been written and distributed in accordance with the rules of conduct applicable to financialresearch as established under Spanish regulations.

To our readers in Australia: This publication has been issued by Morgan Stanley Dean Witter but is being distributed in Australia by Morgan Stanley Dean WitterAustralia Limited A.B.N. 67 003 734 576, a licensed dealer, which accepts responsibility for its contents. Any person receiving this report and wishing to effecttransactions in any security discussed in it may wish to do so with an authorized representative of Morgan Stanley Dean Witter Australia Limited.

To our readers in Canada: This publication has been prepared by Morgan Stanley Dean Witter and is being made available in certain provinces of Canada by MorganStanley Canada Limited. Morgan Stanley Canada Limited has approved of, and has agreed to take responsibility for, the contents of this information in Canada.

Additional information on recommended securities is available on request.

© Copyright 2000 Morgan Stanley Dean Witter & Co.