Embed Size (px)

Citation preview

Hevkn 1994, Vbt 9. Na 4. 63&4SS2.

Formulating Vertical Integration Strategies^KATHRYN RUDIE HARRIGAN

Columbia University

A framework is proposed that develops the dimensions of vertical integra-tion strated and proposes key factors that might augment their uses withinvarious scenarios. These represent new hypotheses and conjectures aboutmake-or-buy decisions that require empirical testing. If the framework isvalid, strategists could formulate better hybrid vertical integration strategiesby recogniang the hypothesized effects of these forces on the industriesthat might be linked.

Managers need a ready supply of raw matoials andservices, as wdl as a ready market for their firms'outputs. The business arratigements tbat are used tocontrol tbese risks are forms of vertical integration.Tbey tnay include vertical acquisitions, or intemaldevdo{«ient of supplying or distributing units, orotber means of extending firms' control over out-siders.

The Phenomenon of Vertical Integration

Vertical integration is a corporate strategy tbat hasbeen misunderstood. It has lotig been a key force intbe development of bigb productivity and managerialscqibistication in U.S. business (Cbandler, 1977). Ver-tically integrated corporations bave been key enginesof cbange in tbe past and bave enbanced sbarebolderwealtb (Lubatkin, 1982). Yet earUer findings tbat"dominant verticals" (Rumelt, 1974) and verticalmergers were least successful as diversifications(Baker, Miller, & Ramsperger, 1981) may bavesoured mana^rs and academic researcbers on tbeusefulness of tbis strategy unnecessarily. Oftentimesresearcbas did not recognize tbat votical integrationcould be an effective strategy, provided it was usedpnutently, because tbey often took an overly aggre-gated view of it. Because critics bave not discemedbow tbe impOTtant dimensions of vertical integraticm

be adapted over time (as industries cbange).

'The research was st^iported by tbe Strategy Researcb Center,Cdurabia University. Comments and oitidsm from William H.Newman, Ian MacMillan, and Donald C. Hambrick are alsograulaHy acknowledged. The author is indebted to Donald C.I&iabrick for suggesting the graphic configuration in Fipire 1.

tbey have not recognized how to make this a moredurable and keen competitive weapon. Because suc-cessful vertical integration strategies require thecooperation of several strategic business units(SBUs), the formulation of such strategies is in theprovince of the chief executive officer (CEO). Insome cases, effective vertical integration may evenrequire temporary subsidization of one business unitat the expense of another. Decisions regarding sucbSBU coordination (and resource allocations amongthem) must be made by the chief strategists. Tbuseffective vertical integration strategies need to refiectbotb business unit and corporate level strategyrequirements.

Tbis paper proposes a framework for developingeffective vertical integration strategies. It wasdeveloped by syntbesizing tbe tbeoretical foundationsestablisbed by tbe industrial economics and strategicmanagement literatures witb firms' observed behav-iors. Thus it suggests a new way to look at verticalintegration and the forces that affect firms' cboicesconcerning vertical linkages. It develops normativepropositions conceming wbicb generic verticalstrategies migbt be more appropriate under differentcompetitive circumstances, and it uses examples offirms' successes or failures in using vertical integra-tion to suggest bow traditional concepts of thisstrategy mi^t be amended to refiect effective in-dustry practices. These suggestions are new hypo-theses, which will require empirical testing. Verticalintegration is one of tbe first diversification strategiestbat firms embrace. Unfortunatdy, some firms seemto use it in a manner that seems inappropriate fortbdr circumstances. Tbe issue of vertical inte^ation

638

deserves additional analysis because it bas beenmisunderstood in tbe past, and because tbe develop-ment of a more rigorous means of analyzitig thisstrategy (and the performance it promises) cotildresult in the formulation of more effective industrylinkages, more rapid technological improvements,stronger global strategies, and better use of verticalintegration. Table 1 summarizes many ofthe advan-tages and risks associated with vertical integration.

The narrow case in which a firm's major diversi-fication strategy has been only vertical is not the focusof this inquiry. Instead, it considers the largeruniverse of firms that have linked two or more SBUsthrough vertical relationsbips and bave diversified inotber ways as well. Rumeh (1974) would bave foundtbat many of tbe more diversified firms in his For-tune 500 sample also bad vertical transfers of goodsor services in-bouse, bad tbat been tbe focus of bisinquiry. Tbus Rumelt reported tbat 22 percent of tbefirms in bis sample embraced a dominant verticalstrategy in 1969 (up from 20 percent in 1949), butvertical linkages also existed witbin tbe bighly diver-

Table 1Some Advantages and Disadvantages

of Vertical Integration

Advantages Disadvantages

Internal benefitsIntegration econoniies reduce

costs by eliminating steps, re-ducing duplicate overbead,and cutting costs (tecbnologydependent)

Iniproved coorditiation of activ-ities reduces inventorying andother costs

Avoid time-consuming tasks,such as price shopping, com-municating design details, ornegotiating contracts

Cortipetitive benefitsAvoid forecbsure to inputs, ser-

vices, or marketsImproved marketitig or techno-

logical intelligenceOpportunity to create product

differentiation (increasedvalue added)

Superior control of firm's eco-nomic environment (marketpower)

Create credibility for new prod-ucts

Synergies could be created bycoordinatbig vertical activitiesskillfully

Internat costsNeed for overbead to coordinate

vertical integration increasedcosts

Burden of excess capacity fromunevenly balanced tninimumefficient scale plants (technol-ogy dependent)

Poorly organized vertically in-tegrated firms do not enjoysipergies tbat compensate forbigber costs

Competitive dangersObsolete processes may be per-

petuatedCreates mobility (or exit) bar-

rierslinks firm to sick adjacent busi-

Lose access to itiformation fromsuppliers or distributors

Synergies created through ver-' tical im^ration may be over-

ratedManagers integrated before

tbinking tbrough the most ap-propriate way to do so

sified firms he bad classified in otber ways. Ifprevious studies of votical inte^ation used dassifica-tion rules simiiar to Rumelt's, tbey also may baveunderstated its tme activity level. For example.Federal Trade Commission data for 1948 to 1972conceming large acquisitions (assets larger tban $10million) indicate tbat less than 15 percent of thesewere vertical mergers; and Salter and Wdnhold's(1979) list of $100 million or more acquisitions madeduring 1975-1978 indicated that only 4 percent werevertical. Thus an illusion was perpetuated that ver-tical integrations were rare, except in the ral, mbber,basic metals, and forest products industries. But, infact, acquisitions that are classified as bdng other-wise "related" to tbe firm's core businesses may alsobave provided new distribution cbannds or otherassets that are vertically related to them.

Acquired firms are bundles of assets rather thansingle business units, as Ocddental Petroleumdiscovered when courting Cities Service (and as DuPont learned while absorbing Conoco). Acquisitionscan offer vertical linkages as wdl as nonvertical diver-sifications. Corporate strategists must dedde whetherto retain the business units acqtiired inddentally inthis fashion; and if tbey are vertically rdated,strategists must dedde wbetber to encourage intra-firm commerce (subsidy) or demand arms-lengthtransactions between vertical sister units. Thus, moreseemingly unrelated mergers bave vertical elementsto tbem tban is generally recognized, but oftentimesstrategists see no advantage to encouraging verticalrelationsbips between in-bouse units. Tbis may oc-cur because tbe opportunities for vertical competitiveadvantage bave passed in some industries. In otbercases, bowever, tbis occurs because managers did notrecognize bow to exploit tbe advantages of verticalintegration effectively.

The Legacy of Vertical Integration

Vertical integration bas been an important mana-gerial innovation and a necessary technological stepin developing certain industries, but it may not beappropriate in tbe same form under all circum-stances. For example, ownership of ore mines, ships,foundries, rolling mills, and fabricating plants wasnecessary for steel companies to lower costs and im-prove productivity in the 1890s. In its early years.Ford Motor Company owned and operated everystage of processing from iron ore to Hnisb-and-trimoperations (except tires and glass). In these early

639

years, suppliers may not have berai as willing to shareFord's gamble in persua^ng consumers to purcbase"horsdess carriages," so Ford bad to devdop com-ponraits to its spedfications for itsdf. Tliere weresubstantial economies assodated with vertical in-tegration once FOTd bad overcome the public'sresistance to ptu'ehasing this tiovel product, and thesecost advantage rewarded Ford's gamble. Ford's in-tegrated strate^ and logi^ical system enabled largenumbers of consumers to afford low priced andreliable automobiles in 1910 (CbamSa, 1977) becauseit lowered FcH-d's costs of (^-ocurement, standardizedits components, and fadlitated an end-to-end pro-duction process. Tbis is tbe type of vertical integra-tion bebavior one tnigbt expect witbin emerging in-dustries wbere firms must provide tbdr own infra-stmctures and otber supplies.

By 1983, bowever, tbe automobile industry badmatured sucb tbat uncertainties regarding genericproduct demand were reduced. Ford's outside sup-l^iers were willing to invest in tooling and otber assetsto supply tbe autotnakers, and bigb degrees of inter-nal transfers were no longer necessary if unecono-mic. (And tbe throughput of U.S. automakers wasnot large enough for vertical integration to remainas economic as it once was.) The challenge fromJapanese automakers was difficult to meet whenfirms sucb as Ford were so strategically infiexible.Moreover, vertical integration bad lost some of itsattraction because managers (wbo often resented bav-ing to buy from sister units) did not understand tberole tbat vertical integration played in tbdr firm'scorporate scbeme. Often finns did not have the sup-porting mechatiisms needed to reap the maximumsynergies that migbt be available from vertically in-tegrated linkages, or tbey tnisapidied tbem in otberways (Williamson, 1975). In brief, in tbeory, manyfirms favor making ratber tban buying key resourcesand se^ces, but their inabilities to matiage integra-tion taint thdr appredation of this strategy. More-over, the use of vertical int^ratim must change withtime. The competitive damage created by excessiveintegration can be substantial, as in the examples ofthe U.S. automobile and sted industries in 1983.

Antitrust dedsions also have created a tarnishedimage of vertictd int^'ation. Economists, wbo didnot consider tbe particular requisities of diversefirm's corporate strategies, bave rdnforced aunidimensicmal view of vertical integraticHi based

on tbeories of market power and tbe ideal of perfectlycompetitive industries (Addman, 1979; Blair &Kaserman, 1978; Comanor, 1967; Dennison, 1939;Frank, 1925; Jewkes, 1930; and Lavington, 1925).Tbese scholars largely have not recognized that dif-ferent motives for vertical integration—such astechnological leadersbip, to secure access to rawmaterials, or competitive preemption—migbt existwitbin tbe same industry; nor bave tbey consideredtbe diversity of ways in wbicb vertical integrationstrategies migbt be formed (Adams & Dirlam, 1964;Qevenger & Campbell, 1977; Greenbut & Obta,1979; Larson, 1978; Mancke, 1972; Perry, 1980). Forexample, firms vary in bow many tasks tbey performin-house, in the number of buyer-seller linkagesdownward in a vertical chain they forge, and in theform of control employed. Few economic scholars,except perhaps Bork (1954), McCSee and Bassett(1976), anti Porter (1980), have recognized the waysin which vertical integration could make industriesmore competitive (rather tban less so). Most econo-mic scbolars bave beld one view of vertical integra-tion, a view based beavily on tbe convenient assump-tion of a monopolist, instead of considering bowfirms migbt use tbis strategy differently.

Because industry structures differ, it is not surpris-ing tbat many approacbes to vertical control couldsatisfy managers' needs for a ready supply of rawmaterials or a ready market for tbeir factories' out-put. Tbe successes some firms bad witb strategies offull integration, long vertical cbains, and otber varia-tions is surprising, bowever. Some firms, such asRobert Hall or Botany Industries, have sufferednotable failures from vertical integration of thewrong type and/or its use at the wrong time (Harri-gan, 1983a). But if managers better understood themany dimensions of vertical integration and the keyforces that affect their abilities to execute verticalstrategies well, they could better avoid fundamentalerrors assodated with vertical integration and maxi-mize the benefits available in joining dissimilar butrdated businesses. Briefiy, managers would not at-tempt to create synergies in cases where externalforces made integration too risky or thdr intemalsystems made communicatiotis inadequate.

A New Look at Vertical Integration

The dd concept of vertical integration as being 100percent owned operations that are physically inter-connected to supply 1(X) percent of a firm's needs is

640

outinoded. Under !^q>r(9riate drcumstances, qualitycontrol and access to stable supplies can be obtain-ed through quasi-int^ration arrangements. Firmscould contract for R&D services, for example, toutilize the technology of genetic engineering in prod-uct devdopment, or they could form joint venturesto obtain this capability. Finns could bave com-ponents engineered to tbdr tigbt and bigbly spedficinstmctions by outsiders, as do Japanese automobilemanufacturers, for example. And if tbeir bargain-ing power is sufficient, firms can use a kanban or"just in time" system of inventory control tbat sbiftstbe burden of bolding costs to tbeir suppliers(Obmae, 1982).

If firms prefer not to use outsiders as extensionsof tbdr corporate entity, a variety of otber verticalarrangements are possible. Some firms may concludethat they need not undertake certain activities at all.Eli Lilly, for example, uses outsiders exclusively withsuccess to merchandise its ethical Pharmaceuticals.Tandy/Radio Shack, by contract, uses primarily itsown retail outiets to distribute personal computers,but it has been increasing its use of outsiders. In othersituations, firms may find that tbey can enjoy tbe in-tegration economies, uncertainty reduction, compe-titive intdligence, and otber benefits tbat intemal ver-tical linkages may provide tbrotigb outsiders. The keyin using vertical integration is recognizing which ac-tivities to perform in-house, how to relate these ac-tivities to each other, how much of its needs the firmsbould satisfy in-bouse, bow mucb ownersbip equityneeds to be risked in doing so, and wben tbese dimen-sions sbould be adjusted to accommodate new com-petitive conditions. Briefiy, tbe concept of verticalintegration sbould be expanded to encompass a vari-ety of arrangements by wbicb tbe firm cim use out-siders (as well as its own business units) to forge anoptimal vertical system for supplying goods, services,and capabilities.

The Dimensions of Vertical Strategy

In any vertical integration strategy, consdous (orunconsdous) dedsions are made regarding: (1) tbebreadtb of integrated activities undertaken; (2) tbenumber of stages of integrated activities; (3) tbedegree of intemal transfers for eacb vertical linkage;and (4) tbe form of ownersbip used to control tbevertical rdationsbip.

Breadth of Integrated Activittes

Tbe breadtb of integrated activities is tbe numbsof tasks tbat firms perform in-bouse. Firms perform-ing many upstream or downstream tasks in-bouse arebroadly integrated; firms performing few verticallyrelated tasks are tiarrowly integrated.

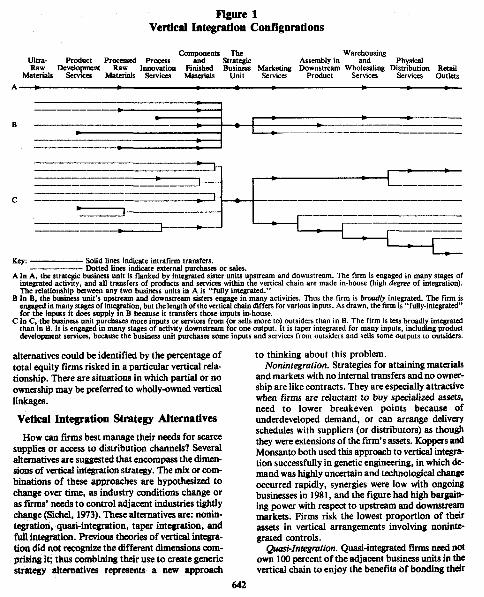

Traditional concepts of vertical int^ration did notaddress tbe number of integrated activities tbat firmsmigbt undertake. Figure 1 contrasts tbe old view,represented by firm A, witb examples of tbe ex-panded concept of vertical integration proposed bere.In Figure 1, firm A is not as broadly ititegrated asare firms B and C. Circumstances in wbicb firmsmigbt cboose tbe broadest integrations successfullyare suggested elsewbere.

Stages of Integrated Aetivities

Tbe number of stages undertaken in tbe dimensionof vertical integration tbat many traditional viewshave embraced. Figure 1 shows that firm A has morestages than firms B or C, because its activities extendfrom ultra-raw materials to retiiil ouUds, but firmC is engaged in a greater number of steps in the va-tical chain. Although Rgure 1 depicts the transfor-mation process as an extension of adjacent stages ac-tivities, it is possible for firms to skip a stage in thechain (by using outsiders for an intermediate process-ing step) in order to monitor costs better, to save onasset investments for fadlities that would be under-utilized if brought in-house, or for otber reasons.

Degree of Internal Transfers

Tbe degree of integration is tbe proportion of aresource transferred intemally, and fully integratedfirms transfer almost 100 percent of a particular ser-vice or material in-bouse. In Figure 1 only firm Cis "taper integrated" with respect to services andmaterials upstream and downstream. Firms A andB are "fully integrated."

Form of Ownersbip Arraagement

The form of integrated ownersbip indicates theproportion of a firm's equity invested in a verticallylinked venture, and in some environments carefullyspecified contracts, franchises, jinnt vmtures, orother forms of quasi-integration can be good alter-natives to wholly-owned ventures. Figiu-e 1 does mxillustrate different f<Hms of ownra'siap, but these

641

Fignre 1Vertical Integration Confignrations

Components The WarehousingUltra- Product Processed Process and Strategic Assembly in and PbysicalRaw Develoianent Raw Innovation Finisbed Business Marketing Downstream Wbolesating Distribution Retail

Materials Services Materials Services Materials Unit Services Product Services Services Outlets

^

Key:- - Solid lines indicate intrafirm transfers.— Dotted lines indicate external purcbases or sales.

A In A, tbe strategic business unit is flanked by integrated sister tmits upstreani and downstream. Tbe firm is engaged in tnany stages ofintegrated activity, and all transfers of products and services witbin the vertical chain are made in-house (high degree of integration).The relationship between any two business units in A is "fully integrated."

B in B, the business unit's upstream atid downstream sisters engage in many activities. Tbus the firm is broadty integrated. Tbe firm isengaged in many stages of integration, but tbe tengtb of tbe vertical chain differs for various inputs. As drawn, tbe firm is "fully-integrated**for the inputs it does supply in B because it transfers those inputs in-bouse.

C In C, the business unit purcbases more inputs or services from (or sells more to) outsiders than in B. Tbe firm is less broadly integratedtban in B. It is engaged in many stages of activity downstream for one output. It is taper integrated for many inputs, induditig productdevelopment services, because the business unit purchases some inputs and services from outsiders and sells some outputs to outsiders.

alternatives could be identified by the percentage oftotal eqtiity firms risked in a particular vertical rda-tionship. There are situations in which partial or noownership may be preferred to wholly-owned verticallinkages.

Vetical Integration Strategy Alternatives

How can firms best manage thdr needs for scarcesupplies or access to distribution channels? Severalaltematives are suggested that encompass the dimen-sicms of vertical integraticm strategy. The mix or com-binations of tbese approacbes are bypotbesized tocbange over time, as industry conditions cbange oras firms' needs to control adjacent industries tightiychange (Sichel, 1973). Tbese altematives are: nonin-tegration, quasi-integration, taper integration, andfuU integratim. Previous tbeories of vertical int^ra-don did not recognize tbe different dimensions com-prising it; tbtis combinitig tbdr use to create genericstrategy dtematives represents a new

to tbinking about this problem.Nonintegration. Strategies for attaining materials

and markets with no internal transfers and no owner-ship are like contracts. They are espedally attractivewhen firms are reluctant to buy spedalized assets,need to lower breakeven points because ofunderdeveloped demand, or can arratige deliveryschedules with suppliers (or distributors) as thoughthey were extensions of the firm's assets. Koppers andMotisanto both used this approach to vertical int^ra-tion successfully in genetic engineering, in which de-mand was highly uncertain and technological cbangeoccurred rapidly, synergies were low witb ongoingbusinesses in 1981, and tbe figure bstd bigb bargain-ing power with respect to upstream and downstreammarkets. Firms risk the lowest proportion of thdrassets in vertical arrangements involving noninte-grated controls.

Quasi-integration. Quasi-integrated firms need notown 100 percent of the adjacent business units in tbevertical cbain to enjoy tbe benefits of bonding tbdr

642

interests to other firms' interests. The bond betweenrirms could take the form of cooperative ventures,minority equity agreements, loans or loan guarantees,prepurchase credits, spedalized logistical facilities or"understandings" concerning customary arrange-ments (Blms, 1972; Porter, 1980). Downstream quasi-integration arrangements enable firms to retain a net-work of qualified distributors to maintain quality im-ages. Upstream "take-or-pay contratts" andkanbanarrangements enable firms to enjoy the advantagesof vertical integration without assuming the risks ofit. Whiskey distillers used quasi-integration suc-cessfully to penetrate diverse geographical markets,and microcomputer producers used it to obtain soft-ware and distribution of their products. The com-petitive scanning advantages of quasi-integration canbe especially effective if firms using it devise in-telligence gathering mechanisms to use the informa-tion that adjacent firms and competitors mightprovide.

Quasi-integrated arrangements place greater pro-portions of ownership equity at risk, but they alsoprovide greater fiexibility in responding to changingconditions than a contract may provide. Tbe tbirdownersbip alternative, full ownersbip, is most fre-qently observed. It assumes tbat tbe firm exerts com-plete control over tbe activities of tbe vertically linkedbusinesses. Full ownersbip risks tbe greatest propor-tion of equity, but many firms believe it is easier tomanage tban contractual or quasi-integrated rdation-sbips and prefer it over tbem (Harrigan, fortb-coming).

Taper Integration. Wben firms are backward orforward integrated but rely on outsiders for a por-tion of tbdr supplies or distribution, tbey are' 'taperintegrated." Sucb firms can monitor tbe R&D de-velopments of outsiders, reduce vulnerability tostrikes and shortages witbin their systems, and ex-amine the products of competitors while enjoying tbelower costs and greater advantages (and profit mar-gins) or vertical integration. Under certain drcum-stances taper integration is not necessary and firmscan add substantial value tbrougb upstream or down-stream activities, taper integration can be used effec-tively, as American Cyanamid did in etbical pbar-maceuticals by supplying basic and finisbed cbemicalsto its Lederle Laboratories subsidiary wben it wasconvenient to do so but relying on outsiders to sut^lychemicals in otber cases. Similarly Amoco (StandardOil of Indiana) and many otber petroleum refinersfound tbat upstream taper int^ration arrangemoits

provided them with access to enough crude oil tokeep thdr plants running economically, and that sdl-ing a portion of thdr primary petrocbonicals to othrafirms allowed them to gain scale economies throughspedalization in processing downstream. Taper inte-gration represents a useful compromise between de-sires to control adjacent businesses and needs to re-tain strategic fiexibility.

Full Integration. Physically interconnectedtechnologies usually involve high degrees of internaltransfers, but full int^ration also can be used effec-tively if price competition is not fierce, disecononmiesfrom temporary imbalances are not significant, andlittle hardship occurs from bdng cut off from out-side market or tecbnological intelligence. Transfer-ring all of tbe firm's needs for a particular good orservice in-bouse exposes it to increased risks of ex-cess capadty, competitive infiexibility, and loss ofinfomiation concerning customer or competitivecbanges. Firms also face bigber capital costs andbigber exit barriers with this strategy (Harrigan, 1981,1983b). Nevertheless, Brooks Brothers sells its owntailored suits with success, Courtaulds used its ownrayon fiber in textiles, and PPG Industries used itsown synthetic soda ash to make glass. These firmswere fully integrated with respect to the materialsnamed above without encountering the problemsotber firms bave faced witb tbis strategy altemative.In general, it would seem tbat full integration worksbest witbin stable environments, but for corporatestrategy reasons it may be necessary if outside sup-pliers or distributors are inadequate. Altbougb itseems generally wise to bave competitive antennaecollecting intelligence upstream and downstream byenga^ng in some commerce witb outsiders, taper in-tegration may not be necessary in some settings inwbicb full integration is tbe more profitable strategy.

Breadth and Stages of Integration. Firms tbat per-form many activities involved in making a particularproduct (sucb as Pfizer in pbarmaceuticals and Ten-neco in coal gasification) may enjoy synergies witbtbdr other businesses. Being broadly integrated alsooffers tbem opportunities to capture large profitmargins by adding more vaiue themsdves. Firms thatengage in several vertical stages for each integratedactivity tbey undertake (such as Texas Instmmentsin miaocomputers and MOIHI in p^rcrieum refining)can enjoy these synergies at sevoal diverse levdswithin thdr organizations. They also can controlcmdid aspects of tbdr produds' quality by par-

643

tidpatii% at several stages in tbe ebain of process-ing. Ahbough it serans evident tbat integrating broadand long rangii% operaticms could be complex andcostly, it is bypotbesized tbat in some cases it couldbe bigbly rewarding because sucb strategies lever:^firms' abilities to enter new markets, exploit newtecbtiolo^es, and evaluate tbe impact of evolutionarychanges faster.

Particular cinnbitiations of the breadth of activitiesintegrated, number of stages undertaken, degree ofintemal transfers, and form of ownership control aremore likdy to be successful for certain firms thanothers, depending on: (1) the uncertainty surround-ing sales growth, industry infrastmcture, and othermarket traits; (2) tbe likelibood tbat tbe industry inquestion will undergo radical tecbnological cbange,severe price warfare, or otber stmctural cbanges caus-ing competition to be volatile; (3) tbe power of firmsto bargain, cajole, or pressure suppliers (or distribu-tors) into performing value adding tasks for tbem;and (4) firms' strategy needs. (For example, more in-tegration migbt be used if tbe firm's CEO concludedthat it needed greater control over adjacent partiesto attain tedmological leadership or other objectives.)It is important to nctfe tbat tbe most appropriate ver-tical integration strate^es will cbange over time asindustry conditions cbange, as corporate strategyneeds cbange, and as firms' capabUities evolve. TbeCEO must assess tbe rdative wortb of tbe strategyaltematives sketcbed above in ligbt of tbe forces tbatkey factors exert on tbe dimensions of verticalintegration.

Factors Affecting Vertical Strategies

Four key factors are bypotbesized to affect tbe ver-tical integration strategies tbat firms embrace:(1) forces propelling industry evolution and exacer-bating demand uncertainty; (2) tbe nature of com-petition in the linked industries; (3.) the bargainingpower of suppliers or distributors (and customers);and (4) corporate strategy requirements. Table 2details the effects of these factors on the dimensionscomprising vertical strategy altematives. From this[ffesentation and the discussion bdow, certain com-binations of these dimensions are shown to be moreapptopnate tban otbers wben tbe key factors occurtogetber in certain ways.

Fwces Propeili^ bdnsbr Evolutioii

Induaries evdve in Aructure as firms make diverse

investments in tbem and ovQ-come customers' reluc-tance to adopt new products (or new generations ofproducts). Tecbnologic^ iimovation is a major causeof accderated industry evolution and of increased de-tnand uncertainty. Different vertical integrationstrategies will be more appropriate if tecbnologycbanges rapidly (or slowly), depending on wbetberfirms would be tecbnological leaders or followers.Pioneering firms would be more likely to integratetban would tecbnological followers. Witb tbis excep-tion, bowever, less vertical integration is expectedearly (and late) in an industry's evolution in contrastwitb tbe scenario Stigler (1951) envisioned, becauseof (1) tbe risks of demand uncertainty and (2) dif-fering needs to prove a new product's wortb. Tbere-fore, tbe most likely pattern of integration bebaviorone migbt expect to see overtime (bolding otber fac-tors constant) is an inverted U-sbape.

Demand Uncertainty. Wben demand conditionsbecome stable, bigber degrees of intemal integrationmigbt be undertaken witb ease because one firm'ssales volumes can become large (and regular) enoughto absorb the output of adjacent plants without in-curring costly excess capadty penalties. Because itwould take time for the experience spurring salesgrowth to occur, one would not expect firms withinmany embryonic industries (as well as declining in-dustries) to be broadly integrated or engaged in manystages of integrated opo^ons. Demand for productsin embryonic and declining settings may be highlyuncertain. The chief strategist may elect for tbe firmto undertake more activities or more integrated stagesin settings in wbicb pioneering investments are nec-essary to acbieve otber corporate objectives, sucb astbe creation of infrastmdures, particularly if existingdistribution cbannds are blocked or inappropriate fortbe firm's needs.

Creating Credibility for New Industries. Verticalintegration bebaviors in new industries would be ex-pected to differ from those in established industriesand to differ from behaviors within raibryonic indus-tries that began in the previous century. There weresignificant differences in the need for infrastmc-tures—cbamiels of distribution, standard means ofassessing quality, and so on—supporting tbe devdop-ment of tbe embryonic steel, automobile, and tobac-co industries of tbe last century compared witb tbosesurrounding tbe embryotiic industries of tbe 1980s.In newly devdoping countries and earlier in tbedevelopment of U.S. business, it frequently was

644

Table 2An niustration of the Strategic Framework

Strategy Dining Characteristics When Appropriate Advantages Risks

Degree of integrationFull All of a particular in-

integration put (or output) is trans-ferred in-bouse to a sisterbusiness unit. Often ad-jacent, integrated stagesare in balance in theirthroughput volumes.

Tapered Some portion (but notintegration all) of Hrm's require-

ments fcM- an input is sup-plied in-house or someportion of outputs is sdd(consumed) in-house.

In mature aiut stable envirtm-ments protect proprietary pro-cesses from es[Honage

Maintain tight quality controlat all stages

If Hrm seeks technological orquality leader^ship position

Diseconomies from imbal-ance are not significant

Technological changes occurslowly

Physical interconnection un-necessary

Diseconomies in minimumefficient scale [dant that are un-derutilized are substantial

If firm seeks technological,quality, or market share leader-ship in volatile competitive set-tings

New products needing expla-nations or infrastructure no out-siders provide

If firm desires to prod in-house units

Nonintegra- No internal transfers Better quaiity/prices avaii-tion of inputs (or outputs) to able from outsiders

in-house sister units Costs of investitig to makecomponents is too formidableor volume consumed is too iow(and selling to outsiders wouldbe difficult or a serious diversi-fication from core business offirm)

If technology is changingrapidly

If price competition (andother competitive tactics) causesmarket shares to fluctuate wild-ly

I f demand is highly uncertain

Superior ctmtrol of ecwiomicenvironment

Avoid foreclosure to inputsor markets

Guarantee quality is consis-tent with corporate image

Capture integration econo-mies (espedally advantageous ifmarket share leader)

Enables firm to moiutor out-side R&D and mark^ing prac-tices. Could incorporate out-siders' innovations while gain-ing capability in-house, as well

Enables firrn to understandsuppliers' (or distributors') coststructures and profit margins

Increases bargaining power(implied threat of full integra-tion)

Same as full integration withless risk

No penalties from underuti-lized plants

Avoids purchasing highlyspecific assets (av(nds inflexibil-ity)

Avoids purchasing large ca-pacity when firm's needs aresmall

Lowers overhead and break-even points

Allows preplanned deliveryschedules to reduce inventory-ing costs (kanban)

Breaith of integrationBroadly Many activities (in-

integrated puts, services, or chiui-nels of distributiOT orconsumption) related tothe needs of a particularbusiness tmit are en^ig^in. (Broadly integratedstrategies need not in-volve many verticalstages of processing.)

Narrowly Few activities (inputs,integrUed sorices, or channds) are

engaged in.

Product differentiability ishigh

No outsiders yet producegoods or services needed

Industry structures beccnningestablished and economies be-c<Hning apparent

Decrease market powerTechnolc^ does not provitfe

many integration eccmcHniesAsset inflexibilityPrice renegotiati(His difficultMinimum efficient scale

plants are rarely the same up-stream and downsueam. tlutsscnne portion of linkage is like-ly to be out of balance

Subcontractors will not beavailable to abso-b fluctuatiraisin production and demand

Access to best suppliers (ordistributors) will be cut off(competitive ftHcdosure)

Pay prnniums ftxc access tooutsiders* goods and services

Lower pri(»ity as a cust(nn«(or vendor), because outsido-sare overflow outlets primarily

Same as full inte^iuion butmore advantagMus

Quality contrtri may ncH be ashigh and market power of firmmay be unable to exert controlover adjacent Hrms throu^contract

Subcontractor will not beavEulable to pn-form neededtasks

Firm loses cost advantages ofintegration economies (wherethese exist)

Maintains intelligence con- No scale Mon(»nies availablecerning component costs and at the small volumes needed forways to streamline product de- in-house (and market) COT-sign (experience curve) sumption

Maintains product quality Cwtly setup costs associatedand design secrecy with short production runs for

disparate compcments

When industry structure is No penalties from frequentembryonic, demand is highiy setups or other production costsuncertain, or industry is declin- Access to the innovations ofine outside supphers or distributors

When firm's requirements Lower mobility (or exit bar-fora particular good or service riers)are low

Loss of access to sui^riies orother scarce resources

Less contrcd over producSspecifications and quality (un-less ccmtnuAs can be used toconu^ supi^iers or d ^ bsatisfactorily)

645

Table 2 (continued)

Strategy Defining Characteristics When Appropriate Advantages Risks

Stages of integrated activityMany sU^es Firm is eng^ed in When product (or compo-

many vertically related nents) are state of the art andactivities—from ultra- firm seeks technological leader-raw materials to distribu- hititMi to final ccHisumers—in which the buyer-sellerrelationships couldoccur.

shipW

Few stages Firm is engaged in fewvertKaliy relatKl activi-ties in the chain fromultra-raw materials todistribution

Form of ownershipWholly- Businesses are wholly-

owned owned by firm.

iu^i- Less than full owner-integration ship and control. Couid

include joint ventures,franchises, minorityequity investments, loanguarantees, or an "un-derstanding" regardingcustomer relationships

hen life of product is ex-pected to be eight years orlonger

V/hen firm is foreclosed bycompetitors

When firm seeks quality lead-ership

When technological or cus-tomer scanning is less important

When product lives are ex-pected to be short or the newobsolescing technology will bevery unlike past processes

When product is very youngor industry structure is embry-onic

When demand is decliningWhen physical interconnec-

tions are few or not necessary

When contracts or otherquasi-integrated forms of con-trol are inadequate

When firm desires to protecttechnology or trade secrets fromoutsiders

When demand is declining(except as a "phase-out" tactic)

If risk of failure and invest-ment costs are high

If economies of integrationare insignificant but need forcontrol is strong

Technology changes rapidlyIndustry structures are still

embryonicTo transfer ownership of an

undesirable business unit to out-siders

If corporate mission does notrequire tight control over qual-ity

If competition is vt^atile

Captures more of value add-ed in veitical chain of process-ing

Firm can create substantialimprovements in supplyingtechnology or distribution prac-tices

Could create highly differen-tiated and high quality products

Preanpt nonintegrated com-petitors by forcing industrystructures to evolve to firm's ad-vantage

Control proprietary advan-tages

Reach ultimate consumersmore effectively

Outsiders' itinovations can beharnessed to improve productquality or design

Firm can piggyback on themarketing or brand image ex~penditures of outsiders

Proceeds from irivestmentneed not be shared with others

Greater strategic flexibilitybecause business units are fullyowned and controUed

Reduces asset investmentsAllows firm to create

"spider's web" of quasi-inte-grations to sam^de several firms'approaches to a technological ornuu'keting problem

Creates bargaining powerover adjacent business units

ln^)roves access to new mate-rials or processes

Scanning advantages of taperintegration with less asset risk

Integration economies oflapw integratiori (provided firmmanages quasi-integrated rela-tionship effectively)

Lowers fixed costs while pro-viding access to adjacent firms'intelligence and skills

Synergies foregone if com-munications systems do not ex-ploit these linkages welt

Creates exit barriers due toobsolescence

Risks of throughput imbal-ance magnified for each s t^eadded to vertical chain

Subcontractors needed to al-leviate imbalances in through-put (due to technology orchanging demand) will not beavailable

Costly and inefficient if firmsdo not manage complexity well

Involves firms in very diverseactivities that may be far fromits core strengths

Firm's product perceived asa "me-too" entry

Integrated competitors willenjoy superior cost structuresand intelligence

Same risks as being too inte-grated on other strategy dimen-sions above; risk exposure ismaximum

Could create mobility or exitbarriers if partnws are impor-tant to other businesses of thefirm

Costs of managing quasi-in-tegrated rela,tionship exceedbenefits of this control system

Contractual problems couldstymie strategic flexibility andrun up administration costs

net^^sary for firms to undertake many stages of in-tcgx&ted activities (and to provide the necessary in-frastructures) in order to help an industry to develop.But ROW nmny new industries can use the same in-frastructures devdoped in an earlier era by firms that

646

once integrated vertically to build them. The majorreason for pioneering firms within embryonic indus-tries to undertake many stages of integrated actiwtiynow would be to create credibility for a radical newindustry. This was once the case in persuading textile

firms to use rayon as well as cotton and wool on theirlooms; and Celanese forward integrated from rayonto yarn, textiles, and garment manufacture to proveto consumers, as well as textile firms, that its newfiber (rayon acetate) was viable. Similarly ALCOAonce forward integrated beyond its current numberof integrated stages to fabricate aluminum productsto sell to consumers when other metals fabricatorswould not use its new metal. In the 1980s, however,there seem to be few new industries (except, perhaps,genetic engineering) for which this need to create newmarket conduits is as high as it was in earlier eras.

When the risks of launching an embryonic industryare quite high, firms can form joint ventures to linksupplies and distribution charmels; and when demandconditions become stable and certain patterns ofcompetition are recognized as being more successfulthan others, more internal integration can be safelyundertaken. When demand is declining, however, thefirst linkage that firms in declining industries mightbe expected to sever are those with owned distribu-tion channels, because making demand dependent onan independent market enables firms to assess moreclearly whether pockets of enduring demand exist forthe product in question (Harrigan, 1980). This is whatCelanese did in acetate, IHamond Shamrock did inacetylene, and Brown Shoe did in leather tanning.In summary, except for the unique situations men-tioned above, specialized suppliers or distributors arebetter suited to provide goods and services to firmsin embryonic industries on a contractual basis untiluncertainties concerning demand and competitiveviability are resolved.

Volatility of Competition

Individual business units would not be expected tofavor vertically integrated strategies in settings inwhich industry structures exacerbate the likelihoodof price warfare and depressed profit margins. Be-cause volatile industry structures increase thelikelihood that competition will degenerate into theuse of tactics that devastate long term profitabilityand sap the irmovative resourcefulness of firms, ver-tical integration generally should be avoided in suchsettings. Other things held constant, the greatestnumber of successful linked stages and the greatestsuccessful breadths of integrated activities would beexpected within settings in which competition isstable. The characteristics of hostile industry struc-

tures have been developed in detail elsewhere (Har-rigan, 1980; Porter, 1980). The elements of industrystructure that affect vertical int^ration include: pro-duct traits, supplier traits, consumer traits, manufac-turing technology traits, and competitor traits.

Product Traits. Because differentiated productscan justify higher prices (Bain, 1968), higher degreesof intemal transfer can be undertaken for such prod-ucts with greater success even when integrationeconomies are not substantial. In choosing whichcomponents or services to produce in-house, how-ever, it is important to understand which attributesof a product create those qualities for which con-sumers are willing to pay a premium. Noncriticalcomponents and services (and those offering pooreconomics) could be purchased from outsiders andsensitive components and services (and those offer-ing the best economics) produced in-house. By free-ing plant space and resources that formerly weredevoted to noncritical and uneconomic componentsand services, firms can undertake a more profitablemix of activities with their resources while tying upthe assets of outsiders for low profit activities.

If trade secrets protect some aspect of a firm'sproducts, higher degrees of integration are necessary,as in the case of Polaroid, which stopped purchas-ing its negative materials from Kodak when its ins-tant photography patent expired. (Too much pro-prietary information was contained there to let com-petitors produce it.) Similarly, Schlumberger ac-quired its own custom logic semiconductor house(Fairchild Camera & Instrument) to protect its pro-prietary knowledge conceming well-logging services,and Dow Chemical often is fully integrated to pre-vent other firms from learning too much about itsprocesses and designs.

Supplier Traits. The principal motives for firms tointegrate backward often include capturing high pro-portions of value added, controlling product quality(and proprietary knowledge), or overcoming compe-titors' advantages if the best suppliers are alreadyunder contract to others. If competition is escalatingon the basis of innovations, however, firms shouldbe wary about embracging high degrees of intemaltransfers because they cut off their access to thebenefits of outsidtfs' innovations in an enviroiunoitin which flexibility is crucial to competitive abiUty.In such settings, it may be desirable to hdp createanother new supplier (through quasi-integration ar-rangements, which allow the new entity to serveothers as well as sponsoring taper integratioa firm)

647

rather that fall into the trap of technological inflexi-bility by fuUy owning such suppliers and buying in-puts only from than.

Consumer Traits. The principal reasons to in-tegrate forward often indude capturing high propor-tions of value added, controlling the quality and im-3^ of one's products, and raising customers' switch-ing cost barriers (Porter, 1980). Compiex productsthat require substantial demonstration or explana-tions and servicing (as microcomputers did in 1978)are strong candidates for downstream linkages. Indoing so, firms must be cautious to ensure: (1) thatthey are not overly dependent on in-house merchan-dise for resale and (2) that they do not stay forwardintegrated after the advantages of being so integratedhave expired. When products become successfulenough to create high customer switching costs, theneed for forward integration is lowered, and firmsshould move away from battlefronts unless they arewell positioned to win price wars.

Manufacturing Technology Traits. The technologyused in manufacturing must offer substantial integra-tion economies in order for vertical integration to beadvantageous (Khandwalla, 1974). Because the mini-mum efficient scale of some technologies is so muchlarger than firms' needs for that component, firmsthat integrate such activities may be forced to entermerchant sales to dispose of their unused outputsfrom the oversized plant (or run the plant at uneco-nomic volumes). Integration should be avoided if thecosts of excess capacity caimot be offset by charg-ing premium prices. Instead, firms should use sub-contractors to perform those tasks that require assetsthat most firms wouid use infrequently at presentoperating scales. Thus, producers of solar collectorpanels send out for chrome plating, and ethicalpharmaceutical firms send out for the brominechemistry step in production.

Firms must keep aware of their distinctive compe-tences in production to ensure that: (1) their criticallyskilled laborers—sdentific researchers and en-gineers—are employed Qest they be hired away byctmpetitors), and (2) they avoid being stuck with ob-solete assets. If firms are constrained by plant space,it may be wise to purchase simple or low volume com-ponoits from outsiders. Critically skilled onployeesthereby can be kept busy on difficult (but challeng-ing} tasks that lev^age firms' future capabilities tocmnpMe, u d the burden of thdr salaries am beqxead ova high vduiae supidying activities. Finally,if technology is changing raindly, using outsiders to

perfonn key intermediate processing steps reduces thelikelihood that firms will be stuck with verticalresources that become high exit barriers. As long asdemand is increasing and firms can avoid price warsin selling thdr output, vertical linkages will not ex-acerbate the tendency for competition to become vo-latile; but unless spedal efforts are made to overcomethese forces, vertical linkages can become high exitbarriers as industries mature (Harrigan, 1983b).

Competitor Traits. Efforts made to diminish thepressures of other structural traits toward price war-fare can be done by competitors who (1) compete onthe basis of price or (2) use vertical integration as ameans of foreclosure. "Dominant verticals," thegroup of narrowly diversified, integrated firms thatRumelt (1974) identified, are most likely to possessthe types of strong commitments to vertical integra-tion strategies that function like exit barriers, caus-ing them to act irrationally, by cutting prices to niain-tain high throughputs in thdr integrated fadlities tothe detriment of other competitors.

Firms that use their vertical linkages as a meansof foreclosing nonintegrated firms from access tomaterials, markets, innovations, and competitive in-telligence also are damaging competitors because theycan escalate the evolution of the industry towardsdefensive vertical integrations. When many firmshave integrated, all face similar pressures to keepthdr vertical chains efficiently utilized, and pricecompetition becomes more likely than if noninte-grated firms were allowed to supply or purchase ex-cess volumes of tnaterials and services to alleviate im-balances in vertically related technologies. Thus itmay be preferable for an industry to have some non-integrated firms to absorb other firms' excess capac-ity, lest industry bloodshed result instead.

In summary, high degrees of internal transfer, longvertical chains, and many integrated activities are ex-pected in settings in which industry structures do notexacerbate price warfare or rapid rates of change inproducts or processes. Because competitors must beable to change tactics rapidly in turbulent industrysettings, a highly integrated posture in such settingscould reduce a firm's maneuverability and damageits profitability. Even the partial reprieve of substan-ti^ integration economies or the ability to chargepremium prices to pay for costly idle capadty maynot offset the long tom corporate damage that beingtoo highly integrated in such settings could create.The tradeoffs that firms will make depend on theiroverall strategies and market power.

648

Firms that possess the bargaining power needed toobtain secure access to suppliers and distributionchannels without damaging thdr strategic flexibilitycould reduce thdr asset exposure and inflexibility byredudng ownership stakes in supplying or distribut-ing business units. Another way is to use the firm'sbargaining power to persuade sequent businesses toassume the duties that a firm wishes to avoid (Mac-Millan, Hambrick, & Pennings, 1982).

The most important determinants of bargainingpower are: (1) product specifidty to the industry inquestion; (2) existence of alternative outlets orsources of suppliers; (3) ability to self-manufacturethe good/service in question; and (4) dependence ofthe supplier (or distributor) on the business unit(Porter, 1976a). If firms possess the power to leveragethdr market positions, they could use this power tocontrol adjacent firms' assets without owning them.Firms that control brand names or patents, for ex-ample, could hire outsiders to market thdr productsif communications with downstream parties are lessimportant than other advantages that such arrange-ments might provide. But if firms' suppliers or dis-tributors possess bargaining power (and if they can-not be persuaded to perfonn useful services for firms)then those activities may have to be undertaken in-house in order to attain the control that some firmsdesire. If this situation occurs in settings in which de-mand is unstable and competition is volatile, the out-come of doing so could be disastrous.

Corporate Strategy Needs

The foregoing arguments that less integration ispreferable to more must be moderated by considera-tions of corporate strategy needs. Because vertical in-tegration can be costly if used imprudently, corporatestrategists must scrutinize the advantages they hopeto capture by condoning (or denying) the creation ofcertain vertical rdationships. Votical integration maybe part of a larger strategy involving shared resourcesand experience curve economies for some businesses,for example, requiring the firm to sustain relation-ships that the strategy framework otherwise wouldnot recommend.

Some vertical integrations promise to improve longterm synergies for the entire firm, although they ap-pear to penalize a particular business unit. Supplyside economies, for example, could be gained bysharing manufacturing fadlities for components that

could be used in several dissimilar ivoticai iitt^ration strategies that increase or enhaaceinnovations by sharing technological infonnationcommon to separate stages of int^raticm may requremore int^ration than the framework suggests.

The number of stages undertaken, for example,would be expected to be highest if significantsynergies are gained or other corporate needs areserved. The key determinants of whether (or not) afirm should skip a particular stage in its int^ratedchain of activities are the task's importance to its cor-porate mission and the quality of goods or servicesprovided by outsiders. A firm's position within itsindustry also suggests how many integrated stages itwould perform, and firms on the fringes of an in-dustry would be more likdy to purchase (rather thanproduce) materials or services from leader firmswhose upstream plants produce in excess of theirdownstream plants' capadties.

Although firms will vary considerably in whichtasks they choose to do in-house, thdr needs to cap-ture more value added would mean that they per-formed in-house those tasks for which their expen-sive and criticai resources were best suited. Firms alsowill integrate those tasks that woidd enable them toenjoy synergies with other business units, those thatare important to thdr business missions, or that of-fer high profit margins for them. They most likelywould own outright those aspects of thdr businessesthat were most important to them, and they wouldpool the risks (or extend thdr control over adjacentfirms) for less critical activities supplied by outsidersthrough quasi-integration arrangements.

The most scarce resource that firms possess is theirentrepreneurial ability. Rather than sedng thdr mixof businesses as streams of cash fiows, diief execu-tives should consider them as reservoirs of capabili-ties. Thus vertical integration strategies would en-courage activities and rdationships for which person-nel with crudal skills (or other scarce capabilities)might otherwise not be retained.

In previous sections, less vertical integration hasbeen antidpated within turbulent settings, particidar-ly those in which techncdc^cal duutge occurs rapi(By.Firms pursuing techndogical leadersUp strate^es of-fer an important exception to this hypoth^s, how-ever, because they often m:e wiBing to endue the ton-porary imbalances of full integration whm {«oduc-ing sensitive components, and thef are wining to M>-sorb the risks of many int^-ated stages (as detailedin Table 2) in order to be prased <o ejqdcrit the next

649

gennaticm of tedmological innovation. Contrast, foreumide, the different vertical integration strategiesobservfd>le in the electronics industry for creating newgenerations of microprocessors and for produdngsemiconductor memory chips. Firms will purchasecomponents that are not close to thdr technologicalrares if better prices are available from outsiders. Yetthey often continue to make some of these com-ponents in-house, even if they do not have cost ad-vantages, in order to carry over knowledge to the nextgeneration of active components for which theymight sdze preemptive or cost advantages (Mac-MiUan, 1983). In Figure 2, firms seeking technolo-gical, quality, or market share leadership are groupedin the lower rows of the strategy matrix, and thosepursuing a generic "focus" strategy (Porter, 1980)are grouped in the top rows. Briefly, in an emergingindustry, such as semiconductors, leadership objec-tives require a greater degree (and more stages) ofvertical integration than do focused market niche ob-jectives, because leadership is attained through at-tainment of integration economies (cost leadership)or command of proprietary knowledge (technologicalleadership).

Figure 2An Dlustration of

the Strategy Framework forVertical Integration in Emerging Industries

StrategyObjectives

Leadership

Quasi-integration(with few in-temal transfers)

Taper Integration

Taper Integraticm

(Full Integr^icm)

Quasi-integration

Taper Integration

Taper Integration

Full Integratimi

Volatile StableIndustry Traits Affecting Cotnpetitive Conditions

Finally, it is useful to recognize that any corporatescheme to force vertically related business units todeal with each other without the benefit of "openmarket" equivalents (for the purposes of transferpridng and maintaining competitive fiexibility) ispenalizing one party to the transaction for the sakeof the other. Subsidization of uneconomic and non-competitive business units for the sake of ephemeralcorporate advantages is a strategic trap that shouldbe csrefuUy scrutinized, lest the advantages gainedin such subsidization arrangonents be outweighted

by the impairments to competitive fiexibility thatresult. Global competition on several national frontsthrough an integrated, worldwide logistical systemis one example of situations in which the benefits ofencouraging vertical linkages are substantial andcross-subsidization may be necessary. Under such cir-cumstances the linkages should be retained while aworldwide market position is being won.

Applications of theVertical Strategy Framework

Analysis of the forces identified above that makevertical integration more (or less) successful could beapplied in portfolio rationalizations and in the tim-ing of key changes in vertical strategies. In cases inwhich firms gain bundles of assets through acquisi-tions, including businesses that may be verticallyrelated to ongoing businesses, they could apply thisframework to determine how best to use the new sup-plier/distributor relationship potential created byjoining the two firms. In particular, the frameworkcalls attention to situations in which strategists mightdivest vertical units and deploy released resourcesdsewhere, because it asks hard questions about thetrue nature of synergies and the place of vertical in-tegration in corporate strategies.

The generic strategies suggested above and detailedin Table 2 are not intended to be static suggestionsto gain access to resources, capabilities, and knowl-edge. As competitive conditions change, so too mustthe firm's vertical integration strategy. In particular,changes must refiect revisions in the strategic rela-tionships that strategists envision among theirbusiness units. For example, GTE (a telecommunica-tions firm that once had a significant electronics posi-tion but divested its semiconductors around 1969)purchased EMI Semi Inc. in 1979 because it recog-nized its need again for custom integrated circuitdesigns. Similarly, Tandy/Radio Shack adjusted itsdistribution polides to refiect new market realitiesin 1982 by selling some of its microcomputersthrough outsiders. Hoffman-LaRoche reduced itswholesaling activities (switching exclusively to out-siders); and Exxon brought its U.S. crude oil refin-ing and production capacity back into balance witheach other as competitive conditions changed.

When the "strategic window" that favored inte-gration has closed (Abell, 1978) and the cost ofemulating competitors' integrated strategies is nolonger justified, prudent firms will uncouple thdr in-

650

tegrated linkages in a timely fashion—before otherfirms reach similar conclusions about the merits ofintegration—-to dispose of thdr assets in a healthymarket. Firms attempting late disintegrations willface greater exit barriers than will early firms and willrealize less value for thdr assets when they finallydo locate a buyer for them (Harrigan, 1980; Porter,1976b). A key review point for dedding whether toreduce integration is when cash outlays would be re-quired to upgrade vertically integrated technologies.Strategists must recognize that business units that areviable only if they have a guaranteed market (orsource of supply) can become cash traps if they arenot cut off at that time.

In summary, firms can form vertical joint venturesto obtain the distribution skills and resources theylack, they can purchase marketing contracts, orotherwise avoid risking too many assets in businesseswhose product demand is highly uncertain (/ theypossess the market power needed to take a positionin businesses they deem too risky to wholly-own.They can use the leverage of their bargaining posi-tions to shift risks to outsiders in a preemptivefashion if they can identify and link up with the bestpartners for joint ventures, contract processing, orsourdng arrangements. Firms could increase ordecrease thdr breadth of integrated activities or theirdegree of intemal transfers in a timely fashion if theyhave accurately diagnosed the forces that make ver-tical integration strategies work well within some set-tings but not well within others. The key to successful

use of vertical integration is recognizing whm andwhere it offers significant competitive advantages andforging the necessary vertical linkages withoutcreating excessive risks.

Vertical integration can offer temporary state-of-the-art advantages that must be wdghed against theadvantages of being fiexible to exploit the next tech-nological innovation. Firms that commit early to ver-tical integration, linking themsleves in a highly in-fiexible fashion to a particular technology, risk be-ing wrong, and the cost could be substantial. But ifthese pioneers are right, vertical integration can bea rationalizing device that forges order in chaotic en-vironments, establishes industry standards, or lowersoperating costs significantly. Then the harm of lateentry can be substantial. Thus, firms should buildpilot plants early to learn about suppliers and dis-tributors before competitors can match these intdli-gence gains with their own experience. (They couldconsider the investment a form of R&D.)

Vertical integration is not a costless strategy. Rec-ogtiizing when outsiders can be entrusted with ac-tivities that firms might otherwise perform intemal-ly is desirable when firms must ration funds, seek di-vestiture (or liquidation) candidates, or otherwiseconsolidate thdr business units' activities, as well aswhen they enter new businesses. The problem is acomplex one, but the framework proposed herdn of-fers one way of analyzing firms' vertical integrationcapabilties and improving thdr strategies.

References

Abell, D. F. Strategic windows. Journat of Marketing, 1978,42(3),21-26.

Adams, W.. & Dirlam, J. Steel imports and the vertical oligopolypower. American Economic Review, 1964, 54, 640-655.

Adelman, M. A. Integration and antitrust policy. Harvard Law

Review, 1979, 63(1), 27-77.

Bain, J. S. Industriat organization. 2nd ed. New York: Wiley, 1968.

Baker, H. K., MiUer, T. O., & Ramsperger, B. J. An inside lookat corporate mergers and acquisition. MSU Business Topics,1981, 29(1), 49-57.

Blair, R., & Kaserman, O. Vertical integration, trying and antitrustpolicy. American Economic Review, 1978, 68, 397-402.

Blois, K. J. Vertical quasi-integration. Journat of IndustriatEconomics, 1972, 20, 253-272.

Bork, R. Vertical integration and the Sherman act: The 1 ^ historyof an economic misconception. University of Chicago LawReview, 1954, 22(1), 158-201.

Chandler, A. D. The visibte hand: The manageriat rvsotution inAmerican business. Cambridge, Mass.: Harvard UnivenityPress. 1977.

Qevenger, T. C , Campbell, G. R. Vertical organization: Aneglected element in market structure-performance models. In-dustriat Organizationat Review, 1977, 5(1), 259-262.

Comanor. W. Vertical mergers, market power, and antitrust laws.American Economic Review, 1967, 57, 259-262.

Dennison, S. R. Vertical integration and the iron and steel industry.Economic Joumat, 1939, 49, 244-258.

Frank, L. K. The significance of industrial integration. Joumatof Political Economy, 1925, 33, 179-195.

Greenhut, M. L., & Ohta, H. Vertical integration of sticcessiveoligopolist. American Economic Review, 1979, 69,137-141.

Harrigan, K. R. Strategy formulation in decKmng industries.Academy of Mangement Review, 1980, 5, 599-604.

Harrigan, K. R. Deterrents to divestiture. Acaderrty of Manage-ment Joumat, 1981, 24, 306-323.

651

Hltrigaa, K. R. Strategies for verticat integration. Lexington,

Man.: Heath, l»83a.

Hkrrigaii, K. R. Exit barriers and vertical integration. Academy

<^ Management Proceedings, 1983b, 32-36.

Hannan, K. R. Strategies for Joint ventures, forthcoming.

Jewkes, J. Factors in industrial integration. Quarterty Joumat of

Economics, 1930, 44, 621-638.

KhandwaUa, P. N. Mass output orientation of operationstectmotogy and organizational structure. Administrative ScienceQtiarterly, 1974, 19, 74-79.

Larson, D. A. An empirical test of the relationship between marketconcentration and vertical integration. Industriat OrganizationReview, 1978, 6(1), 71-74.

Lavington, F. Technical influences on vertical integration.Economica, 1925, 7(19), 27-36.

Lubatkin, M. H. >4 market modet anatysis of diversificationstrategies and administrative experience on the performance ofmerging firms. Unpublished doctoral dissertation. Universityof Tennessee, Knoxville, 1982.

MacMiUan, I. C. Preemptive strategies. Journat of BtjstnessStrategy, 1983, 4(2), 16-26.

MaeMiUan, I. C , Hambrick, D. C,&Pennings, J. H. Backwardvertical integration and interorganizational dependence—AFIMS-based analysis of strategic business units. Working paper,Columbia University Business School, 1982.

Maticke, R. B. Iron ore and steel: A case study of the economiccauses of vertical integration. Journat of Industriat Economics,1972, M, 220-229.

McGee, 3.S.,& Bassett, L. R. Vertical imegration revisited. Joa^nat of Law and Economics, 1976, 19, 17-38.

Ohmae, K. The mind of the strategist. New York: McGraw-Hill,1982.

Perry, M. K. Forward integration by ALCOA: 1888-1930. Jour-nal of Industriat Economics, 1980, 29, 37-53.

Porter, M. E. Intertmmd choice, strategy, and bilateral marketpower. Cambridge, Mass.: Harvard University Press, 1976a.

Porter, M. E. Please note location of nearest exit: Exit barrienand strategic and organizational planning. Catifornia Manage-ment Review, 1976b, 19(2), 21-33.

Porter, M. E. Competitive strategy: Technotogies for analyzingindustries and competitors. New York: Free Press, 1980.

Rumelt, R. P. Strategy, structure and economic performance.Boston: Division of Research, Graduate School of Business Ad-ministration, Harvard University, 1974.

Salter, M. S., & Weinhold, W. A. Diversification through acquisi-tion: Strategies for creating economic value. New York: FreePress, 1979.

Sichel, W. Vertical integration as a dynamic industry coticept. Anti-trust Buttetin, 1973, 18, 463-482.

Stigler, G. J. The division of labor is litnited by the extent of themarket. Joumat of Potiticat Economy, 1951, 59, 185-193.

Williamson, O. F. Markets and hierarchies. New York: Free Press,1975.

Kathryn Rudie Harrigan is Associate Professor of Manage-ment ofOrganizations in the Graduate Schoot of Business,Cotumbia University.

652

![VBT Africa - Development Plan [eng]](https://img.dokumen.tips/doc/110x75/58a07f771a28ab19098b6837/vbt-africa-development-plan-eng.jpg)