Embed Size (px)

Citation preview

KARNATAKA ELECTRICITY REGULATORY COMMISSION

TARIFF ORDER 2016

OF

HESCOM

ANNUAL PERFORMANCE REVIEW FOR FY15

&

ANNUAL REVENUE REQUIREMENT FOR FY17-19

&

REVISION OF RETAIL SUPPLY

TARIFF FOR FY17

30th

March 2016

6th and 7th Floor, Mahalaxmi Chambers

9/2, M.G. Road, Bengaluru-560 001

Phone: 080-25320213 / 25320214

Fax : 080-25320338

Website: www.karnataka.gov.in/kerc - E-mail: [email protected]

ii

C O N T E N T S

CHAPTER

Page No.

1 Introduction 3

1.0 Hubli Electricity Supply Company Ltd., 3

1.1 HESCOM at a Glance 5

1.2 Number of Consumers, Sales in MU and Revenue

detail of HESCOM

6

2 Summary of Filing and Tariff Determination

Process

7

2.0 Background for Current Filing 7

2.1 Preliminary Observations of the Commission 7

2.2 Public Hearing Process 8

2.3 Consultation with the Advisory Committee of the

Commission

9

3 Public Consultation – Suggestions / Objections

and Replies

10

3.1 List of Persons who filed written objections 10

3.2 List of persons who made oral submission in

public hearing

11

4 Annual Performance Review for FY15 12

4.0 HESCOM’s Application for APR for FY15 12

4.1 HESCOM’s Submission 12

4.2 HESCOM’s Financial Performance as per

Audited Accounts for FY15

13

4.2.1 Sales for FY15 15

4.2.2 Distribution Losses for FY15 20

4.2.3 Power Purchase 22

4.2.4 RPO Compliance by HESCOM for FY15 24

4.2.5 Operation and Maintenance Expenses 25

4.2.6 Depreciation 29

4.2.7 Capital Expenditure for FY15 29

4.2.8 Prudence Check of FY15 33

4.2.9 Interest and Finance Charges 38

4.2.10 Interest on Working Capital 39

4.2.11 Interest on Consumer Deposits 40

4.2.12 Other Interest and Finance Charges 40

4.2.13 Other Debits 41

4.2.14 Net Prior Period Credits / Charges 42

4.2.15 Return on Equity 42

4.2.16 Income Tax 43

4.2.17 Other Income 43

4.2.18 Fund Towards Consumer Relations / Consumer

Education

44

4.3 Abstract of Approved Revised ARR for FY15 44

4.4 Gap In Revenue for FY15 45

5.0 Annual Revenue Requirement for FY17-19 – 46

iii

HESCOM’s Filing

5.1 Annual Performance Review for FY15 & FY16 47

5.2 Annual Revenue Requirement for FY17-19 47

5.2.1 Capital Investments for FY17-19 47

5.2.2 Sales Forecast for FY17-19 53

5.2.3 Distribution Losses for FY17-19 66

5.2.4 Power Purchase for FY17-19 67

5.2.5 Sources of Power 69

5.2.6 HESCOM’s Power Purchase Cost and

Transmission Charges

73

5.2.7 RPO Target for FY17 77

5.2.8 O & M Expenses for FY17-19 78

5.2.9 Depreciation 82

5.2.10 Interest on Capital Loans 84

5.2.11 Interest on Working Capital 87

5.2.12 Interest on Consumer Security Deposit 88

5.2.13 Interest on belated payment of power purchase

cost

89

5.2.14 Other Debits 90

5.2.15 Return on Equity 90

5.2.16 Other Income 92

5.2.17 Fund towards Consumer Relations / Consumer

Education

93

5.3 Treatment of Regulatory Asset 93

5.4 Abstract of ARR for FY16 94

5.5 Segregation of ARR into ARR for Distribution

Business and ARR for Retail Supply Business

95

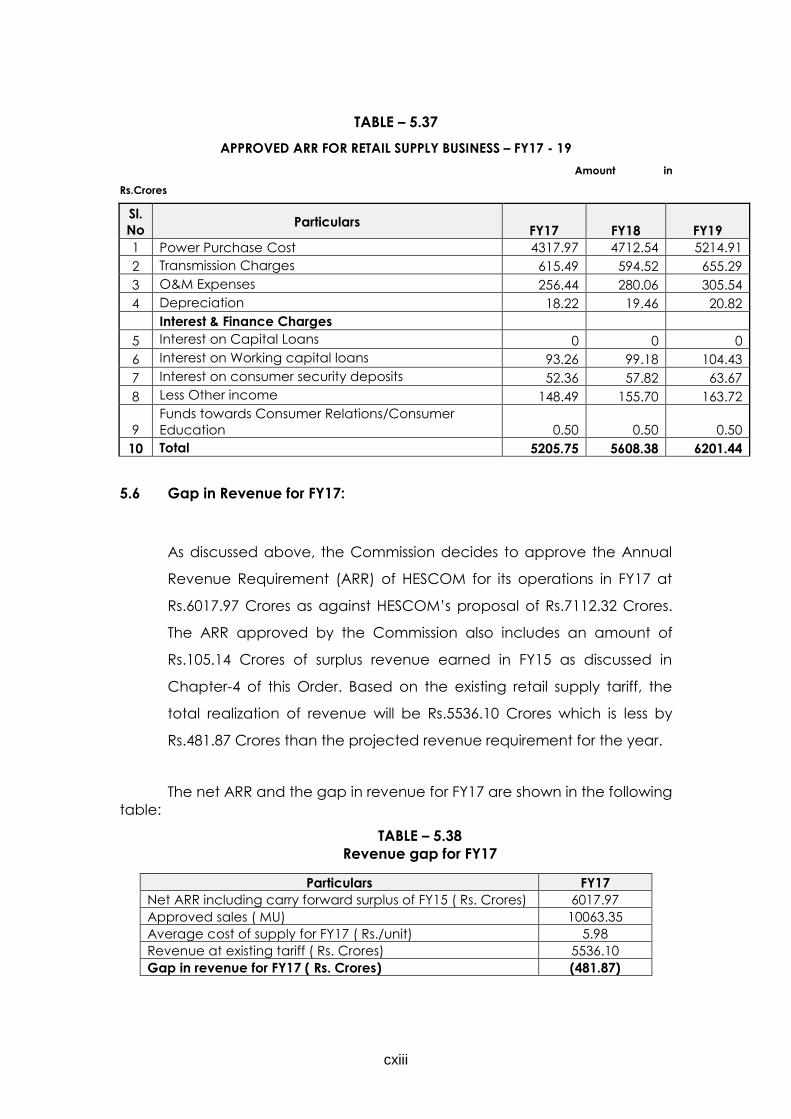

5.6 Gap in Revenue for FY17 97

5.7 Application for Additional Revenue Requirement

for FY17

98

6 Determination of Tariff for FY17 100

6.0 HESCOM’s Proposal and Commission Analysis for

FY17

100

6.1 Tariff Application 100

6.2 Statutory Provisions Guiding Determination of

Tariff

100

6.3 Consideration for Tariff setting 101

6.4 New Tariff Proposals by HESCOM 102

6.5 Revenue of Existing Tariff and Deficit for FY17 104

6.6 Other Issues 136

6.6.1 Tariff for Green Power 136

6.6.2 Determination of Wheeling Charges 136

6.6.3 Wheeling within HESCOM area 137

6.6.4 Wheeling of Energy using Transmission Network

or network of more than one licensee

139

6.6.5 Charges for Wheeling of energy by RE sources

(non REC route) to Consumers in the State

140

6.6.6 Charges for Wheeling Energy by RE sources

Wheeling energy from the State to a consumer /

other outside the State and for those opting for

140

iv

renewable energy certificate

6.7 Other Tariff Related issues 140

6.8 Cross Subsidy Levels for FY17 145

6.9 Effect of Revised Tariff 145

6.10 Summary of the Tariff Order 146

6.11 Commission’s Order 147

APPENDIX 148

APPENDIX – I 185

v

LIST OF TABLES

Table

No.

Content Page

No.

4.1 Revised ARR for FY15 – HESCOM’s Submission 12

4.2 Financial Performance of HESCOM for FY15 14

4.3 HESCOM’s Accumulated Profit / Losses 14

4.4 Approved and Actual Sales - FY15 20

4.5 Incentive for loss reduction for FY15 21

4.6 HESCOM’s Power Purchase for FY15 22

4.7 RPO Compliance as submitted by HESCOM for FY15 24

4.8 O & M Expenses for FY15 – HESCOM’s Submission 25

4.9 Approved O & M Expenses as per Tariff Order dated

12.05.2014

26

4.10 O & M Expenses of HESCOM as per Annual Audited

Accounts for FY15

26

4.11 Allowable O & M expenses for FY15 28

4.12 Capital Expenditure for FY15 30

4.13 Approved Vs Actual Capital Investment 33

4.14 Gist of Prudence check findings for FY15 34

4.15 Summary of Works having cost overrun 35

4.16 Summary of Works having Time overrun 35

4.17 Details of Amounts disallowed in APR FY15 36

4.18 Allowable Interest on Loans – FY15 38

4.19 Allowable Interest on Working Capital for FY15 40

4.20 Allowable Interest on Finance Charges 41

4.21 Allowable Other Debits 41

4.22 Allowable Return on Equity 43

4.23 Approved Revised ARR for FY15 as per APR 44

5.1 Proposed ARR for FY17-19 46

5.2 Proposed Capex for the control period 49

5.3 Category wise Approved number of Installations 64

5.4 Category wise approved energy sales 65

5.5 Projected Distribution Losses – FY17-19 – HESCOM’s

Submission

66

5.6 Approved & Actual Distribution Losses – FY10 to FY16 66

5.7 Approved Distribution Losses for FY17-19 67

5.8 Requirement of Electricity as filed by Licensees 68

5.9 Energy Requirement as filed by HESCOM 68

5.10 Power Purchase requirement approved for the

Control Period FY17 to FY19

69

5.11 Consolidated Power Purchases requirement for FY17 70

5.12 Consolidated Power Purchases requirement for FY18 70

5.13 Consolidated Power Purchases requirement for FY19 71

5.14 Abstract of Power Purchase allowed for ESCOMs for

the control period FY17 to FY19

73

5.15 Power Purchase Cost of HESCOM for FY17 75

vi

5.16 Power Purchase Cost of HESCOM for FY18 76

5.17 Power Purchase Cost of HESCOM for FY19 76

5.18 O & M Expenses for FY17-19 – HESCOM’s Proposal 79

5.19 Computation of Inflation Index for FY17 81

5.20 Approved O & M expenses for FY17-19 82

5.21 Depreciation – FY17-19 – HESCOM’s Proposal 83

5.22 Approved Depreciation for FY17-19 84

5.23 Interest on Capital Loans – HESCOM’s Proposal 85

5.24 Approved Interest on Capital Loans for FY17-19 86

5.25 Interest on Working Capital – HESCOM’s Submission 87

5.26 Approved Interest on Working Capital Loans for FY17-

19

88

5.27 Interest on Consumer Security Deposits for FY17-19 –

HESCOM’s Proposal

88

5.28 Approved Interest on Consumer Security Deposit for

FY17-19

89

5.29 Approved Interest and finance charges for FY17-19 90

5.30 Status of Debt Equity Ratio for FY17-19 91

5.31 Approved Return on Equity for FY17-19 92

5.32 Other Income for FY17-19 – HESCOM’s Proposal 92

5.33 Approved Other Income for FY17-19 93

5.34 Approved ARR for FY17-19 95

5.35 Approved Segregation of ARR – FY17-19 96

5.36 Approved Revised ARR for Distribution Business – FY17-

19

96

5.37 Approved ARR for Retail Supply Business – FY17-19 97

5.38 Revenue Gap for FY17 97

6.1 Revenue Deficit for FY17 105

6.2 Wheeling Charges 137

vii

LIST OF ANNEXURES

SL.NO. DETAILS OF ANNEXURES Page

No.

I Total Approved Power Purchase Quantum and Cost

of all ESCOMs for FY17

206

II Approved Power Purchase quantum and cost of

HESCOM for FY17

212

III Proposed and approved Revenue for FY17 218

IV Electricity Tariff – 2017 219

viii

ABBREVIATIONS

AAD Advance Against Depreciation

AEH All Electric Home

ABT Availability Based Tariff

A & G Administrative & General Expenses

ARR Annual Revenue Requirement

ATE Appellate Tribunal for Electricity

BBMP Bruhut Bangalore Mahanagara Palike

BDA Bangalore Development Authority

BESCOM Bangalore Electricity Supply Company

BMP Bangalore Mahanagara Palike

BST Bulk Supply Tariff

BWSSB Bangalore Water Supply & Sewerage Board

CAPEX Capital Expenditure

CCS Consumer Care Society

CERC Central Electricity Regulatory Commission

CEA Central Electricity Authority

CESC Chamundeshwari Electricity Supply Corporation

CPI Consumer Price Index

CWIP Capital Work in Progress

DA Dearness Allowance

DCB Demand Collection & Balance

DPR Detailed Project Report

EA Electricity Act

EC Energy Charges

ERC Expected Revenue From Charges

ESAAR Electricity Supply Annual Accounting Rules

ESCOMs Electricity Supply Companies

FA Financial Adviser

FKCCI Federation of Karnataka Chamber of Commerce & Industry

FR Feasibility Report

FoR Forum of Regulators

FY Financial Year

GESCOM Gulbarga Electricity Supply Company

GFA Gross Fixed Assets

GoI Government Of India

GoK Government Of Karnataka

GRIDCO Grid Corporation

HESCOM Hubli Electricity Supply Company

HP Horse Power

HRIS Human Resource Information System

ICAI Institute of Chartered Accountants of India

IFC Interest and Finance Charges

IW Industrial Worker

ix

IP SETS Irrigation Pump Sets

KASSIA Karnataka Small Scale Industries Association

KEB Karnataka Electricity Board

KER Act Karnataka Electricity Reform Act

KERC Karnataka Electricity Regulatory Commission

KM/Km Kilometre

KPCL Karnataka Power Corporation Limited

KPTCL Karnataka Power Transmission Corporation Limited

KV Kilo Volts

KVA Kilo Volt Ampere

KW Kilo Watt

KWH Kilo Watt Hour

LDC Load Despatch Centre

MAT Minimum Alternate Tax

MD Managing Director

MESCOM Mangalore Electricity Supply Company

MFA Miscellaneous First Appeal

MIS Management Information System

MoP Ministry of Power

MU Million Units

MVA Mega Volt Ampere

MW Mega Watt

MYT Multi Year Tariff

NFA Net Fixed Assets

NLC Neyveli Lignite Corporation

NCP Non Coincident Peak

NTP National Tariff Policy

O&M Operation & Maintenance

P & L Profit & Loss Account

PLR Prime Lending Rate

PPA Power Purchase Agreement

PRDC Power Research & Development Consultants

REL Reliance Energy Limited

R & M Repairs and Maintenance

ROE Return on Equity

ROR Rate of Return

ROW Right of Way

RPO Renewable Purchase Obligation

SBI State Bank of India

SCADA Supervisory Control and Data Acquisition System

SERCs State Electricity Regulatory Commissions

SLDC State Load Despatch Centre

SRLDC Southern Regional Load Dispatch Centre

STU State Transmission Utility

TAC Technical Advisory Committee

TCC Total Contracted Capacity

x

T&D Transmission & Distribution

TCs Transformer Centres

TR Transmission Rate

VVNL Visvesvaraya Vidyuth Nigama Limited

WPI Wholesale Price Index

WC Working Capital

xi

KARNATAKA ELECTRICITY REGULATORY COMMISSION,

BENGALURU - 560 001

Dated this 30th day of March, 2016

Order on HESCOM’s Annual Performance Review for FY15 & Annual

Revenue

Requirement for FY17-19 & Revision of

Retail Supply Tariff for FY17

In the matter of:

Application of HESCOM in respect of the Annual Performance Review for FY15,

Annual Revenue Requirement for FY17-19 and Revision of Retail Supply Tariff

for FY17, under Multi Year Tariff framework.

Present: Shri M.K.Shankaralinge Gowda Chairman

Shri H.D.Arun Kumar Member

Shri D.B.Manival Raju Member

O R D E R

The Hubli Electricity Supply Company Ltd., (hereinafter referred to

as HESCOM) is a Distribution Licensee under the provisions of the

Electricity Act 2003, and has, on 05.12.2015, filed the following

applications for consideration and orders:

a) Review of Annual Performance for FY15 and approval of

revised ARR thereon.

b) Approval of ARR for FY17-19

xii

c) Approval for revision of Retail Supply Tariff, for the financial

year 2016-17 (FY17)

In exercise of the powers conferred under Sections 62, 64 and other

provisions of the Electricity Act, 2003, read with KERC (Terms and

conditions for Determination of Tariff for Distribution and Retail Sale of

Electricity) Regulations 2006, and other enabling Regulations, the

Commission has considered the applications and the views and

objections submitted by the consumers and other stakeholders. The

Commission’s decisions are given in this order, Chapter wise.

xiii

CHAPTER – 1

INTRODUCTION

1.0 Hubli Electricity Supply Company Ltd.,:

Hubli Electricity Supply Company Ltd., (HESCOM) is a Distribution

Licensee under Section 14 of the Electricity Act, 2003 (hereinafter

referred to as the Act). HESCOM is responsible for purchase of power,

distribution and retail supply of electricity to its consumers and also

providing infrastructure for open access, Wheeling and Banking in its

area of operation which includes seven Districts of the State as

indicated below:

HESCOM is a registered company under the Companies Act, 1956,

incorporated on 30th April, 2002. HESCOM commenced its operations

on 1st June, 2002.

1. Bagalkot

2. Belgaum

3. Bijapur

4. Dharwad

5. Gadag

6. Haveri

7. Uttara Kannada

xiv

O&M Zones O&M Circles O&M Divisions

Hubli Zone

Hubli Circle

Hubli Urban

Hubli Rural

Dharwad Urban

Dharwad Rural

Gadag

Haveri Circle

Haveri

Ranebennur

Sirsi Circle

Sirsi

Karwar

BelgaumZone

Belgaum Circle

Belgaum Urban

Belgaum Rural

Bailahongal

Ghataprabha

Chikkodi Circle

Chikkodi

Athani

Raibagh

Bijapur Circle

Bijapur

Indi

Jamakandi

Bagalkot Circle

Bagalkot

Basavana Bagewadi

Mudhol

xv

The O & M divisions of HESCOM are further divided into seventy eight

sub-divisions. These sub-divisions are further divided into 255 O & M

section offices.

Section offices are the base level offices looking into the operation

and maintenance of the distribution system in order to provide reliable

and quality power supply to HESCOM’s consumers.

1.1 HESCOM at a glance:

The profile of the HESCOM is as indicated below:

Source: HESCOM Website/ Tariff Application / Audited Accounts for FY15

Sl.

No. Particulars Statistics

1. Area Sq. km. 54513

2. Districts Nos. 7

3. Taluks Nos. 49

4. Population Lakhs 166

5. Consumers as on

31.01.2016

Lakhs 42.16

6. Energy Sales for FY15 MU 9208.39

7. Zone Nos. 2

8. DTCs as on 31.01.2016 Nos. 144482

9. Assets as on 31.03.2015 Rs. in Crores 6431.24

10. HT lines as on 31.01.2016 Ckt. kms 65383

11. LT lines as on 31.01.2016 Ckt. kms 114051

12. Total employees strength:

A Sanctioned Nos. 15938

B Working Nos. 7868

13. Revenue Demand Rs. in Crores 4851.58

14. Revenue Collection Rs. in Crores 4179.27

xvi

1.2 Number of Consumers, Sales in MU and Revenue details of HESCOM in

FY15 is as follows:

CATEGORY

HESCOM

No. of

Installation

Sales in

MU

Revenue in

Rs.Crs.

Domestic 2993380 1407.28 606.86

Commercial 303582 485.66 391.11

Industrial 97442 1241.88 786.26

Agriculture 603172 5422.17 2567.51

Others 92476 651.4 553.51

Total 4090052 9208.39 4905.25

HRECS is one of the distribution licensees purchasing power from HESCOM as

per the bulk supply tariff determined by the Commission. HRECS has filed

separate application for approval of ARR and retail supply tariff for its

distribution and supply area for the control period FY17 - 19.

HESCOM has filed its application for approval of Annual Performance Review

for FY15, Annual Revenue Requirement (ARR) for FY17-19 and revision of

Retail Supply Tariff for FY17.

HESCOM’s application, the objections / views of stakeholders thereon and the

Commission’s decisions on the approval of Annual Performance Review for

FY15, ARR for FY17-19 and revision of Retail Supply Tariff for FY17 are

discussed in detail in the subsequent Chapters of this Order.

xvii

CHAPTER – 2

SUMMARY OF FILING & TARIFF DETERMINATION PROCESS

2.0 Background for Current Filing:

The Commission in its Tariff Order dated 6th May, 2013 had approved

the ERC for FY14 to FY16 and the Retail Supply Tariff of HESCOM for

FY14 under MYT principles for the control period of FY14 to FY16.

HESCOM in its present application filed on 15th December, 2015 has

sought approval for the Annual Performance Review (APR) for FY15

based on the audited accounts, ARR for the fourth control period i.e.

FY17-19 and revision of Retail Supply Tariff for FY17.

2.1 Preliminary Observations of the Commission

After a preliminary scrutiny of applications the Commission had

communicated its observations to HESCOM on 1st January, 2016. The

preliminary observations were mainly on the following points:

Capital Expenditure

Sales Forecast

Assessment of IP set consumption

Power Purchase

Issues pertaining to items of revenue and expenditure

Other new proposals

Compliance to Directives

In response HESCOM has furnished its replies on 11th January, 2016. The

replies furnished by HESCOM are considered in the respective Chapters of

this Order. Further, the Commission also held a validation meeting to discuss

the proposals of HESCOM on 10th February, 2016.

xviii

2.2 Public Hearing Process:

As per the Karnataka Electricity Regulatory Commission (Terms and

Conditions for Determination of Tariff for Distribution and Retail Sale of

Electricity) Regulations, 2006, read with the KERC Tariff Regulations,

2000, and KERC (General and Conduct of Proceedings) Regulations

2000, the Commission vide its letter dated 1st January, 2016 treated the

application of HESCOM as petition and directed HESCOM to publish

the summary of its ARR and Tariff proposals in the newspapers calling

for objections, if any, from interested persons.

Accordingly, HESCOM has published the same in the following

newspapers:

Name of the News Paper Language Date of Publication

INDIAN EXPRESS English 17/1/2016

&

18/1/2016

TIMES OF INDIA

PRAJAVANI Kannada

VIJAYAVANI

HESCOM’s application on APR of FY15, ARR for FY17-19 and revision of

retail supply tariff for FY17 were also hosted on the web sites of HESCOM

and the Commission for the ready reference and information of the general

public.

In response to the application of HESCOM, the Commission has received ten

statements / letters of objections. HESCOM has furnished its replies to all

these objections. The Commission has held a Public Hearing on 3rd March,

2016 at Dharwad. The details of the written / oral submissions made by

various stake holders and the responses from HESCOM thereon and

Commissions’ views have been discussed in Chapter - 3 / Appendix to this

Order.

2.3 Consultation with the Advisory Committee of the Commission:

xix

The Commission has also discussed the proposals of KPTCL and all

ESCOMs in the State Advisory Committee meeting held on 10th March, 2016.

During the meeting the following important issues were also discussed:

Performance of KPTCL / ESCOMs during FY15

Major items of expenditure of KPTCL / ESCOMs for FY17-19

Members of the Committee have offered valuable suggestions on the

proposals. The Commission has taken note of these suggestions while

passing the order.

xx

CHAPTER – 3

PUBLIC CONSULTATION

SUGGESTIONS / OBJECTIONS & REPLIES

3.1 In pursuance of the provisions of section 64 of the Electricity Act, 2003,

the Commission undertook the process of public consultation in order

to obtain suggestions/views/objections from the interested stake-

holders on the application for APR for FY15 and ERC, ARR and Retail

supply Tariff for FY 17, FY18 and FY19 under the MYT Principles filed by

HESCOM. In the written submissions as well as during the public

hearing some Stake-holders and public have raised several objections

to the Tariff Applications filed by HESCOM. The names of the persons

who have filed written objections and made oral submissions are given

below:

List of persons who filed written objections:-

Sl.

No

Applicatio

n No. Name & Address of Objectors

1 HB-01 Sri Yagnanarayana M.N, General Secretary, Laghu

Udyog Bharati – Karnataka, Bengaluru.

2 HB-02 Sri G.G. Hedge, President Balakedarara

Hitharakshaka Sangha, Sirsi.

3 HA-01 Sri S.K Hedge, Kumta Taluk Vidhyuth Balakedarara

Hitharakshana Samithi, Kumta

4 HA-02 Sri Siddheshwar G Kammar, Hon. Gen. Secretary,

Karnataka Chamber of Commerce & Industry,

Hubballi.

5 HA-03 Shri R.K. Rangrej, Ex-President, Chairman, Electricity

Sub- Committee, Gadag District Chamber of

Commerce & Industry, Gadag.

6 HA-04 Shri. Shantilal Mostawal, Hon. Secretary, Karnataka

Cotton Association, Hubballi

7 HA-05 Sri G.G. Hegde Kadekodi, President, Uttara

Kannada District Chamber of Commerce and

Agriculture, Sirsi.

8 HA-06 Sri Aravind K Pai, Kumta.

9 HA-07 Sri K.B. Arasappa, Hon. Gen. Secretary, KASSIA,

Bengaluru.

10 HA-08 Sri Lokaraj, Secretary, Federation of Karnataka

Chambers of Commerce and Industry, Bengaluru

11 AE-01 Sri P.N. Karanth, Kundapura.

xxi

12 AE-02 Sri Praveen Sood, IPS, Additional Director General of

Police, Administration, Bengaluru

3.2 List of the persons, who made oral submissions during the Public

Hearing, held on 03.03.2016.

SL.No. Names & Addresses of Objectors

1 Sri G.G. Hedge Kadekodi for FKCCI, North Kanara District

Chamber Sirsi, Consumer Protection Society, Sirsi & Karnataka

Electricity Governance Network

2 Sri R.G. Joshi, Kumta

3 Sri Prabhakar Nagarmunchi, KASSIA, Bangalore.

4 Sri Aravind K Pai, Kumta

5 Sri S. K. Hedge, Kumta

6 Sri Siddeshwar Kammar & Sri A.S. Kulkarni, Karnataka Chamber

of Commerce, Hubballi.

7 Sri Pramod Shanbhag, Shreyas Papers, Dandeli

8 Sri Basavaraj Ingalagi, Belagavu (Hosur Village).

9 Sri R.K. Rangrej, Gadag District Chamber of Commerce.

10 Sri Chethan Jain, I Ex.

11 Sri A.A. Thargar, Dharwad.

3.3 The gist of the objections, Replies by HESCOM and the Commission’s

Views is appended to this order in Appendix-1

xxii

CHAPTER – 4

ANNUAL PERFORMANCE REVIEW FOR FY15

4.0 HESCOM’s Application for APR for FY15:

The HESCOM, in its application dated 15th December, 2015, has sought

approval of revised ARR in the Annual Performance Review (APR) for

FY15, based on the Audited Accounts.

The Commission in its letter dated 1st January, 2016 had communicated

its preliminary observations. The HESCOM, in its letter dated

11thJanuary, 2016 has furnished its repliesto the preliminary observations

of the Commission.

The Commission in its Multi Year Tariff (MYT) Order dated 6th May, 2013

had approved the HESCOM’s Annual Revenue Requirement (ARR) for

FY14 – FY16. Further, in its Tariff Order dated 12th May, 2014, the

Commission had approved the APR for FY13 and had revised the ARR

for FY15 along with Retail Supply Tariff for FY15.

The Annual Performance Review for FY15 based on the HESCOM’s

Audited Accounts is discussed in this Chapter.

4.1 HESCOM’s Submission:

The HESCOM has submitted its proposals for revision of ARR for FY15

based on the Audited Accounts as follows:

TABLE – 4.1

Revised ARR for FY15 – HESCOM’s Submission Amount in Rs. Crores

Sl.

No Particulars As Filed

1 Energy @ Gen Bus in MU 11513.19

2 Energy @ Interface in MU 11059.81

3 Distribution Losses in % 16.74%

Sales in MU

4 Sales to other than IP & BJ/KJ 3849.77

5 Sales to IP & BJ/KJ 5358.62

Total Sales in MU 9208.39

Revenue at existing tariff in Rs Crs

xxiii

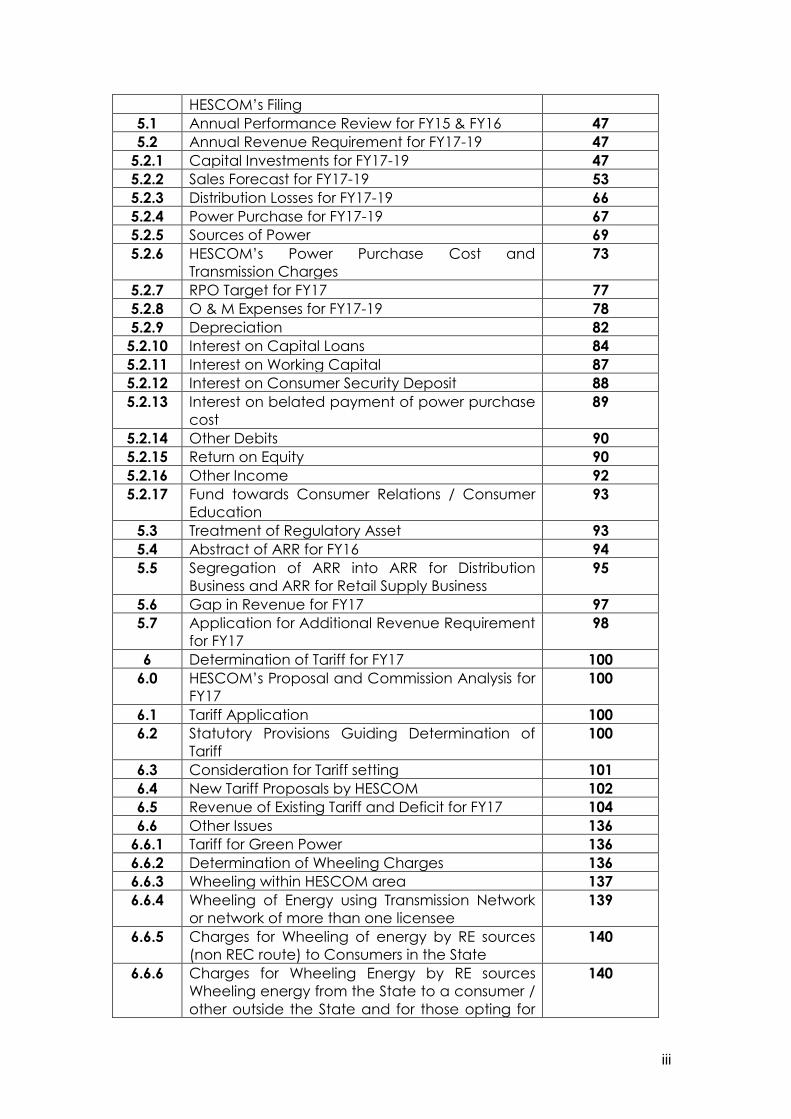

6 Revenue from tariff and Misc. Charges 2292.12

7 RE Subsidy 2559.46

Total Revenue 4851.58

Expenditure in Rs Crs

8 Power Purchase Cost 3330.10

9 Transmission charges of KPTCL 445.54

10 SLDC Charges 9.94

Power Purchase Cost including cost of

transmission 3785.58

11 Employee Cost

12 Repairs & Maintenance

13 Admin. & General Expenses

Total O&M Expenses 580.95

14 Depreciation 99.05

Interest & Finance charges

15 Interest on Loans 180.75

16 Interest on Working capital 18.43

17 Interest on consumer deposits 44.64

18 Other Interest & Finance charges 2.47

19

Less interest & other expenses

capitalised 0.00

Total Interest & Finance charges 246.29

20 Other Debits (0.78)

21 Net Prior Period Debit/Credit 0.00

22 Return on Equity 0.00

23 Provision for taxation 0.00

24 Other Income (8.08)

Net ARR 4719.17

Considering the revenue of Rs.4851.58 Crores against a net ARR of

Rs.4719.17 Crores, the HESCOM has reported surplus in revenue of

Rs.132.41 Crores for FY15.

4.2 HESCOM’s Financial Performance as per Audited Accounts for FY15:

An overview of the financial performance of the HESCOM for FY15 as

per their Audited Accounts is given below:

xxiv

TABLE – 4.2

Financial Performance of HESCOM for FY15

Amount in Rs.Crores

Sl.

No. Particulars FY15

Receipts

1 Revenue from Tariff and misc.charges 2297.20

2 Tariff Subsidy 2554.38

Total Revenue 4851.58

Expenditure

3 Power Purchase Cost 3330.10

4 Transmission charges of KPTCL 445.54

5 SLDC Charges 9.94

Power Purchase Cost including cost of transmission 3785.10

6 O&M Expenses 580.96

7 Depreciation 99.05

Interest & Finance charges

8 Interest on Loans 116.26

9 Interest on Working capital 82.91

10 Interest on consumer deposits 44.64

11 Interest on belated payment of power purchase cost 102.15

12 Other Interest & Finance charges 2.47

Total Interest & Finance charges 348.43

13 Other Debits (0.78)

14 Net Prior Period Debit/Credit 34.66

15 Other income 26.58

Net ARR 4821.32

As per the Audited Accounts, the HESCOM has earned a profit of

Rs.30.26 Crores for FY15. The profits / losses reported by the HESCOM in

its audited accounts in the previous years are as follows:

TABLE – 4.3

HESCOM’s Accumulated Profits / Losses

Particulars

Amount in

Rs. Crs

Accumulated losses as at the end of FY10 (659.08)

Losses incurred in FY11 (64.70)

Profit earned in FY12 39.75

Profit earned in FY13 40.69

xxv

Losses incurred in FY14 (576.25)

Profits earned in FY15 30.26

Accumulated losses as at the end of FY15 (1189.33)

As seen from the above table, the accumulated losses are Rs.1189.33

Crores as at the end of FY15.

Commission’s analysis and decisions:

The Annual Performance Review for FY15 has been taken up duly

considering the actual expenditure as per the Audited Accounts

against the expenditure approved by the Commission in its Tariff Order

dated 12th May, 2014. The item wise review of expenditure and the

decisions of the Commission thereon are as discussed in the following

paragraphs:

4.2.1 Sales for FY15:

a) Sales- other than IP Sets:

The Commission in its Tariff order dated 12.05.2014, had approved total

sales to various consumer categories at 8855.09 MU as against the

HESCOM’s proposal of 9115.70 MU. The Actual sale of HESCOM as per

the current APR filing [FORMAT D-2] is 9208.39 MU, indicating an

increase in sale to an extent of 353.30 MU, as compared to the

approved sales (as also to its own projected sale). There is an increase

in sales to LT consumers by 543.47 MU and there is a reduction in sale to

an extent of 190.18 MU in HT-categories.

The Commission notes that, as against approved sales of 4073.43 MU to

categories other than BJ/KJ and IP sets [excluding HRECS sales and

supply to the SEZ MU], the actual sales achieved by HESCOM is 3849.77

MU, resulting in the reduction of sales to these categories by 223.66 MU.

Further, the HESCOM has sold 5358.62 MU to BJ/KJ and IP categories

against approved sales of 4781.67 MU, resulting in increased sales to

these categories by 576.95 MU.

xxvi

The actual share of sales to categories other than BJ/KJ and IP sets is

41.81% as against the estimated share of 46.00% resulting in 4.09

percentage point reduction in share to these categories, while the

actual share of sales to BJ/KJ and IP sets has increased by the same

percentage point.

The Commission notes that the major category contributing to the

reduction in sales with respect to the estimates are HT industries (179.53

MU), and LT- 2a (31.14 MU). Further, the sales to IP sets have increased

by 570.24 MU.

In response to the preliminary observations, the HESCOM in its reply has

stated that, HT sales have decreased due to reduction in sales to

categories other than HT-2c as compared to the estimated sales to

these categories. Further, it is stated that the reduction in sale to HT

category is due to HT consumers drawing power under Open Access.

HESCOM has also stated that there is increased sales in LT-1, LT4 (a) &

(c), LT5 and LT6 categories.

The Commission notes that as per the information furnished by the

HESCOM, there is considerable increase in open access sales from

97.37 MU in FY13 to 252.36 MU in FY15.

b) Sales to IP Sets:

In its Tariff Order dated 6th May, 2013, the Commission had approved

specific consumption of IP sets at 8,244 units/installation/annum for the

entire control period of the FY14 to the FY16, whereas, as per the IP sets

consumption reported by the HESCOM in its tariff filing, the specific

consumption works out to 8,996 units /installation/annum for the FY15,

which indicates a huge increase in the specific consumption by 752

units/installation/annum. The total IP sets consumption reported by the

HESCOM for the FY15 was 5,266.70 MU as against 4,696.46 MU sales

quantum approved by the Commission. The difference in IP sets

consumption between the approved and the actual for the FY15 is

570.24 MU.Thus, the specific consumption has increased by 752 units

xxvii

/installation/annum with the corresponding increase in sales also by a

huge quantum of 570.24 MU to that of the approved quantum by the

Commission for the FY15. It is noted that the specific consumption

reported for the FY15 has increased by about 9 per cent which is very

huge compared to the specific consumption achieved by the

HESCOM for the previous years. It is also noted that the specific

consumption should not increase over the years as it remains fairly

constant given that the 11 kV feeders are segregated as rural &

agricultural feeders and power supply to agricultural feeders is

regulated. Further, the consumption of the IP sets can also be

measured accurately on the basis of energy meters’ data of

agricultural feeders at the substations which was not possible earlier.

Moreover, the Commission had approved 5,72,306 as number of

installations, likely to be serviced in the FY15; whereas the actual

number of installations serviced, as reported by the HESCOM, was

6,01,939, an increase by 29,633 numbers. This indicates that, the

increase in number is about 5 per cent of installations serviced during

the FY15, as compared to the approved number of installations by the

Commission. It is noted that the increase in sales can be partly

attributed to increase in number of IP set installations serviced under

regularization scheme as compared to the projected number of

installations for the FY15.

The Commission in its Tariff Order dated 12th May, 2014 had directed

the HESCOM to submit to the Commission every month, the IP sets

consumption based on the feeder energy meters’ data, of agriculture

feeders segregated under NJY, duly deducting the energy losses in the

distribution system. But, the HESCOM has not submitted the metered

consumption data of agricultural feeders every month regularly to the

Commission. The HESCOM in its tariff application has also not submitted

such data of IP sets for the period from April 2014 to March 2015 as

required by the Commission.

xxviii

The Commission in its preliminary observations on the HESCOM’s APR

for the FY15, had directed the HESCOM to justify its claims of IP sets

consumption of 5,266.70 MU considered for the FY15, with necessary

data in support of the same and the methodology adopted to arrive

at the energy loss figures in the 11 kV distribution system for the FY15.

The HESCOM was also directed to furnish whether the total IP sets

consumption for the FY15 has been computed by considering the

specific consumption of agricultural feeders segregated under NJY as

directed or on the basis of readings obtained from the meters fixed to

sample DTCs feeding predominantly IP set loads. However, the

HESCOM, in its reply on the preliminary observations made by the

Commission, has stated that it has analyzed 142 numbers of

agricultural feeders segregated under NJY from April, 2015 onwards

only. It is submitted that, as per the analysis, the IP set consumption in

the river bed areas is ranging from 900 units to 1,667 units, whereas in

other areas the consumption is ranging from 378 units to 1,003 units and

the average consumption is only 603 units per installation per month.

Further, it is also submitted that in some of the feeders, bifurcation of IP

set loads is under progress and wherever exclusive agricultural feeders

are not available, the IP set consumption has been assessed on the

basis of the metered data of sample DTCs feeding predominantly IP

set loads. The HESCOM has requested the Commission to consider the

specific consumption at 727 units per installation per month as filed in

its tariff application.

The Commission notes that, the HESCOM has not submitted the IP sets

consumption details on the basis of meter readings obtained from the

agricultural feeders segregated under NJY, despite achieving

significant progress in commissioning of feeders under NJY, instead, it

has considered the metered data of sample DTCs feeding

predominantly IP set loads as per the methodology approved by the

Commission up to the FY14. It is noted that the HESCOM has not

submitted these details for the FY15. It is also not clear as to how the

HESCOM has computed the total IP set consumption of 5,266.70 MU for

xxix

the FY15 without any basis for arriving at the net IP sets consumption.

Further, the HESCOM has also not submitted the necessary data to

justify its claim in respect of IP sets consumption considered for the

FY15. The result of the analysis made by the HESCOM from April, 2015

onwards cannot be a basis for arriving at the total consumption of IP

sets for the previous period, i.e., FY15. It is clear that the HESCOM has

not complied with the Commission’s direction to it to submit the

metered data, despite segregating a large numbers of 11 kV feeders

as rural and agricultural feeders under NJY, wherein it was possible to

compute the total IP set consumption accurately on the basis of

feeder energy meter readings.

Further, the Commission, during the validation meeting held on

10.02.2016, had also directed the HESCOM to submit the IP sets

consumption on the basis of energy meter readings of 11 kV

agricultural feeders which have been segregated under NJY. In

response, the HESCOM has submitted the details of IP sets consumption

based on the meter data in respect of DTCs feeding predominantly IP

loads, in support of its claims in respect of total IP sales to an extent of

5,266.70 MU for the FY15. The HESCOM has stated that the bifurcation

of loads on segregated agricultural feeders was not fully effected in

the field and for that reason, the consumption on the basis of

agricultural feeders for the FY15 could not be furnished to the

Commission and has requested the Commission to approve the sales

of 5,266.70 MU made to IP sets.

The Commission notes that, due to field issues in transferring of loads

from agricultural feeders on to the NJY feeders, the HESCOM has

assessed the IP set consumption for the FY15 based on the readings

from the meters provided to DTCs feeding predominantly IP set loads.

The HESCOM should have addressed these field issues while

commissioning of feeders to ensure that loads on the respective

feeders were transferred to enable taking accurate consumption of IP

sets. Further, the Commission notes that the increase in sales to IP sets

xxx

for the FY15 can only be partly attributed to the fact that the HESCOM

has serviced 29,633 number of IP sets more than it has projected. The

increase in sales could be also due to supplying more number of hours

of power to IP sets on agricultural feeders than stipulated by the

Government. Hence, the HESCOM is directed to regulate henceforth

the hours of power supply to exclusive agricultural feeders as stipulated

by the Government.

For the present accepting the HESCOM’s explanation on this issue, in

the absence of feeder wise energy meter data in respect of

segregated agricultural feeders, based on the meters provided to

DTCs feeding predominantly IP set loads, the Commission decides to

approve 5,266.70 MU sales to IP sets for the FY15 as filed by the

HESCOM, in its tariff application.

The HESCOM is directed to report the total IP set consumption on the

basis of data from energy meters in respect of agricultural feeders

segregated under NJY duly calculating the distribution system losses in

11 KV lines, distribution transformers and LT line, to the Commission

every month regularly. The HESCOM is also directed to calculate the

actual distribution losses prevailing in 11 kV lines, DTCs and LT lines as

per the methodology approved by the Commission for arriving at the

net IP sets consumption.

c) Total Approved Sales:

The category wise sales approved by Commission and the

actuals for FY15 are indicated in the table below:

TABLE – 4.4

Approved & Actual Sales – FY15

Figures in MU

Category Approved

Actuals

considered

for APR

Difference (Actuals

–Approved)

LT-2a* 1346.50 1315.36 -31.14

LT-2b 12.54 13.68 1.14

LT-3 383.71 371.11 -12.60

xxxi

LT-4b 28.57 17.02 -11.55

LT-4c 0.77 1.07 0.30

LT-5 303.44 315.81 12.37

LT-6 199.58 203.28 3.70

LT-6 131.37 133.13 1.76

LT-7 20.07 22.61 2.54

HT-1 200.37 195.96 -4.41

HT-2a 1105.60 926.07 -179.53

HT-2b 121.71 114.55 -7.16

HT-2c 26.00 47.37 21.37

HT-3a & b 148.36 137.38 -10.98

HT-4 18.11 15.70 -2.41

HT-5 26.73 19.67 -7.06

Sub total 4073.43 3849.77 -223.66

BJ/KJ 85.21 91.92 6.71

IP 4696.46 5266.70 570.24

Sub total 4781.67 5358.62 576.95

Grand total** 8855.09 9208.39 353.29 *Including BJ/KJ installations consuming more than 18 units/month

**Excludes sale to HRECS and SEZ.

Thus, the Commission approves sales of 9208.39 MU for FY-15.

4.2.2 Distribution Losses for FY15:

HESCOM’s Submission:

The Commission had approved distribution losses for FY15 as

shown in the table below:

Range FY15

Upper limit 19.50%

Average 19.00%

Lower Limit 18.50%

HESCOM has reported the distribution loss level of 16.74% in its

annual accounts for FY15.

1 Energy at Interface Points in MU 11059.46

2 Total sales in MU 9208.39

3 Distribution losses as a percentage of

input energy at IF points 16.74%

Commission’s analysis and decisions:

The distribution losses of 16.74% reported by the HESCOM is based on

the sales of 9208.39 MU as against the energy of 11059.46 MU at

interface points. Considering the approved range of losses for FY15, the

xxxii

HESCOM has achieved reduction of distribution losses below the lower

limit of allowable losses by 1.76 percentage point. Hence HESCOM is

entitled to incentive for better performance in loss reduction, during

FY15 as follows:

TABLE – 4.5

Incentive for loss reduction for FY15

Particulars FY15

Actual input at IF points as per audited

accounts in MU 11059.46

Retail sales as per audited accounts in

MU 9208.39

Percentage distribution losses 16.74%

Lower limit target for distribution loss 18.50%

Reduction in loss in percentage point 1.76%

Input at target loss for actual sales in MU 11298.64

Decrease in input due to reduction in

distribution losses in MU 239.18

Average cost of power purchase at IF

points in Rs./unit 2.89

Savings in power purchase cost due to

reduction of losses in Rs.Crores 69.18

50% of savings to be included in APR 15

(balance 50% being the share of

consumes) 34.59

Accordingly, the Commission decides to add an amount of Rs.34.59

Crores to the allowable ARR for FY15.

4.2.3 Power Purchase:

The Commission in its Tariff order dated 12th May, 2014 had approved

source wise quantum and cost of power purchase for FY15. The

HESCOM, in its application, has submitted the details of actual power

purchase for FY15 for reviewing its Annual Performance. The details of

power purchase is listed as under:

TABLE – 4.6

HESCOM’s POWER PURCHASE FOR FY 15

Source

Actuals for FY15 Approved for FY15

Difference of Actuals

over the Approved-for

FY15

% increase /decrease over

approved figures

xxxiii

Energy in

MUs

Cost in

Rs Cr

Rate

in Rs

per

Unit

Energy in

MUs

Cost in

Rs Cr

Rate

in Rs

per

Unit

Energy

in MUs

Cost

in Rs

Cr

Rate

in Rs

per

Unit

Energy Cost Rate

KPCL

Hydel

Stations

3474.26 193.09 0.56 3569.02 184.27 0.52 -94.76 8.82 0.04 -2.66 4.79 7.64

KPCL-

Thermal

Stations

2794.25 1123.44 4.02 2908.45 1107.63 3.81 -114.20 15.81 0.21 -3.93 1.43 5.57

Total 6268.51 1316.53 2.10 6477.47 1291.9 1.99 -208.96 24.63 0.11 -3.23 1.91 5.30

CGS 2387.02 735.13 3.08 2592.37 811.6 3.13 -205.35 -76.51 -0.05 -7.92 -9.43 -1.63

Major IPPs 1057.40 496.12 4.69 1208.4 551.7 4.57 -151.00 -55.58 0.13 -12.50 -10.07 2.77

IPPs -Minor

(NCE

Projects)

1017.61 380.64 3.74 1065.3 389.55 3.66 -47.69 -8.91 0.08 -4.48 -2.29 2.29

Other

States

Projects

28.87 9.08 3.15 37.26 11.87 3.19 -8.39 -2.79 -0.04 -22.52 -23.50 -1.27

Short

/Medium

term

including U

I & Sce-11

554.15 277.91 5.02 279.55 145.82 5.22 274.60 132.09 -0.20 98.23 90.58 -3.86

Transmissio

n Charges

(KPTCL &

PGCIL)

- 530.20 - - 515.92 - 0.00 14.28 0.00 - 2.77 -

LDC

Charges

(POSOO &

SLDC)

- 11.19 - - 5.91 - 0.00 5.28 0.00 - 89.34 -

Energy

Balancing

199.6 27.93 1.40 - - - 199.60 27.93 1.40 - - -

Others

Charges

- 0.59 - - - - 0.00 0.59 0.00 - - -

TOTAL 11513.19* 3785.31* 3.29 11660.35 3724.31 3.19 -147.19 61.01 0.09 -1.26 1.64 2.94

*Excluding HRECS

Commission’s analysis and decisions;

1. The actual power purchase for FY15, as filed by the HESCOM, for

approval of ARR in the Annual Performance Review is 11513.16 MU

amounting to Rs.3785.32 Crores as against the approved quantum

of 11660.35 MU amounting to Rs.3724.31 Crores. Thus, there is a

reduction in quantum of power purchase to an extent of 147.19 MU

with an increase in the cost to an extent of Rs. 61.01 Crores.

2. On an analysis of the source-wise approved and actual power

purchases, the following deviations in quantum of energy and its

cost of purchase are found:

As against the approved quantum of 11660.35 MU, the actual

power purchased by HESCOM is 11513.16 MU for FY15, which is

around 1.26% of the approved quantum. Such decrease during

xxxiv

FY14 was 2.67%. The reduction in sales reflected in reduced power

purchase.

i. On verification of the source-wise power purchase, it is found that,

there is lesser energy supply from KPCL thermal, CGS, NCE and

other State projects to an extent of 621.39 MU at a cost of

Rs.119.16 Crores. Consequently, the HESCOM has purchased short

term power to a tune of 554.15 MU at a cost of Rs.277.91 Crores.

The HESCOM has incurred an additional cost Rs.132.09 Crores

towards short term/medium term Power Purchase resulting in an

increase in per unit cost by 9 Paise.

ii. All these factors including the change in the source wise mix of

supply and reconciliation of energy and its cost among ESCOMs

have resulted in higher average power purchase cost of the

HESCOM at Rs.3.29 per KWh as against the approved rate of

Rs.3.19 per KWh leading to an increase by Rs.0.09 per unit. During

FY14, the increase was Rs.0.26 per unit. The increase in per unit

cost is 2.94%, in FY15.

3. The Commission notes that, the SLDC is yet to implement the intra-

state ABT scheme. The Commission therefore directs SLDC to take

appropriate action immediately to expedite the implementation of

intra-state ABT scheme and to host such details on its website.

4. The Commission in its Tariff order dated 2nd March, 2015 had

directed HESCOM to move the Government to effect necessary

adjustments in the tariff subsidy payable to ESCOMs and ensure

that there are no inter- ESCOM payments outstanding in their

accounts. Further, HESCOM was also directed to reconcile the inter-

ESCOM exchanges and its costs duly making necessary

adjustments to ensure proper accounting of energy and its cost.

5. It is observed that, inter-ESCOMs’ balanced energy to an extent of

199.6 MU at a cost of Rs.27.93 Crores has resulted in increased

receivables of HESCOM to an extent of Rs.27.93 Crores in FY15.

xxxv

6. HESCOM is directed to reconcile the inter ESCOM energy

exchanges and its costs every month and the difference amounts

shall be collected/paid out of the tariff subsidy received from the

Government of Karnataka, to ensure proper accounting of energy

and its cost.

In terms of the MYT Regulations, the Commission taking note of the

above facts, decides to consider 11513.19 MU at a cost of Rs. 3785.58

Crores (as per audited accounts) towards power purchases, for

approving the Annual Performance Review of HESCOM for FY15.

4.2.4 Renewable Purchase Obligation (RPO) compliance by the HESCOM for

FY15:

The HESCOM has submitted that its achievement of non-solar RPO and

solar RPO are 10.30% and 0.34%, respectively, as against the targets of

7% and 0.25%, respectively, as indicated below:

TABLE – 4.7

RPO compliance as submitted by the HESCOM for the FY15

Name of

Company

Total Input

Energy incl.

HRECS

(MU)

Non-Solar RPO Solar RPO

Target Achieved Target Achieved

(MU) (%) (MU) (%) (MU) (%) (MU) (%)

HESCOM 11793.59 825.55 7 809.02 6.86 29.48 0.25 39.61 0.34

The Commission has approved total power purchase quantum of

11806.37 MU (including HRECS) for the FY15 in the APR of HESCOM.

Based on the information furnished, the Commission notes that the

HESCOM has purchased non-solar energy of 809.02 MU (6.86%) and

solar energy of 39.61 MU (0.34%). Considering the surplus solar energy

of 10.09 MU, the net short-fall in non-solar RPO is 0.06 percentage point

for the FY15.

The Commission notes that, when the State as a whole is taken for the

purpose of assessment of achievement of non-solar RPO, in aggregate

all the State owned ESCOMs have achieved the total non-solar RPO

xxxvi

target set for the State. The Commission therefore decides not to

recognize the individual achievement of the HESCOM and to treat the

matter as closed.

4.2.5 Operation and Maintenance Expenses:

HESCOM’s Submission:

The HESCOM has sought approval of O&M expenditure of

Rs.580.95 Crores for FY15. HESCOM has claimed the O&M

expenses as follows:

TABLE – 4.8

O & M Expenses for FY15 – HESCOM’s submission

Amount in Rs.Crores

Particulars FY15

Repairs & Maintenance 48.86

Employee Expenses 455.46

A&G expenses 76.63

O&M expenses 580.95

Commission’s analysis and decisions:

The Commission in its Tariff Order dated 12th May, 2014 had approved

O&M expenses for FY15 as detailed below:

xxxvii

TABLE – 4.9

Approved O&M Expenses for FY15 Amount in Rs. Crores.

Particulars FY15

No. of installations as per actuals as per Audited Accts 4289372

Weighted Inflation Index 6.89%

CGI based on 3 Year CAGR 5.17%

Actual O&M expenses for FY13 467.68

Approved O&M Expenses for FY15 565.55

As per the Annual Audited Accounts of HESCOM for FY15, the actual

O&M expenditure is as follows:

TABLE – 4.10

O&M Expenses of HESCOM as per Annual Audited Accounts for FY15

Amount in Rs.Crores

Repairs & Maintenance 48.86

Employee Expenses 455.46

A&G expenses 76.64

O&M expenses 580.96

The Commission in its preliminary observations, had sought the details

of the items of expenditure incurred by HESCOM during FY15 under A &

G expenses. HESCOM in its replies has stated that it has incurred

expenses of Rs.26.24 Crores towards professional charges, Rs.21.90

Crores towards conveyance, travel and vehicle hire expenses besides

other A&G expenses. On a detailed review of the expenses, it is

observed that HESCOM is incurring substantial expenses on vehicle hire

charges and professional charges.

Also, the R&M expenses are increasing year on year, without proper

justification. One of the major items incurred under R & M is expenses

are on repairs of distribution transformers. The HESCOM needs to

institutionalize a mechanism for minimizing such expenses. These

expenses are abnormally increasing as compared to the previous

years. Since the O & M expenses are controllable, HESCOM has to

initiate necessary measures to ensure prudence in incurring these

expenses. The Commission is of the view that HESCOM should control

its O & M expenses as per the approved O & M expenses so that the

xxxviii

actual O & M expenses does not exceed the approved levels.

However, for the present based on the provisions of the MYT

Regulations, the Commission has proceeded with determining the

normative O & M expenses.

Considering the Wholesale Price Index (WPI) as per the data available

from the Ministry of Commerce & Industry, Government of India and

Consumer Price Index (CPI) as per the data available from the Labour

Bureau, Government of India and adopting the methodology followed

by the CERC with CPI and WPI in a ratio of 80: 20, the allowable

inflation for FY15 is computed as follows:

Year WPI CPI Composite

Series Yt/Y1=Rt Ln Rt

Year

(t-1)

Product [(t-

1)* (LnRt)]

2003 92.6 107 104.12

2004 98.72 111.1 108.624 1.04 0.04 1 0.04

2005 103.37 115.8 113.314 1.09 0.08 2 0.17

2006 109.59 122.9 120.238 1.15 0.14 3 0.43

2007 114.94 130.8 127.628 1.23 0.20 4 0.81

2008 124.92 141.7 138.344 1.33 0.28 5 1.42

2009 127.86 157.1 151.252 1.45 0.37 6 2.24

2010 140.08 175.9 168.736 1.62 0.48 7 3.38

2011 153.35 191.5 183.87 1.77 0.57 8 4.55

2012 164.93 209.3 200.426 1.92 0.65 9 5.89

2013 175.35 232.2 220.83 2.12 0.75 10 7.52

2014 182 246.9 233.92 2.25 0.81 11 8.90

A= Sum of the product column 35.36

B= 6 Times of A 212.19

C= (n-1)*n*(2n-1) where n= No of years of data=12 3036.00

D=B/C 0.07

g(Exponential factor)= Exponential (D)-1 0.0724

e=Annual Escalation Rate (%)=g*100

7.24

For the purpose of determining the normative O & M expenses for FY15,

the Commission has considered the following:

a) The actual O & M expenses allowed for FY13 excluding contribution

to Pension and Gratuity Trust.

b) The three year compounded annual growth rate (CAGR) of the

number of installations considering the actual number of

installations as per audited accounts up to FY15.

c) The weighted inflation index (WII) at 7.24% as computed above.

xxxix

d) Efficiency factor at 2% as considered in the earlier two control

periods.

Thus, the normative O & M expenses for FY15 will be as follows:

Particulars FY15

No. of Installations as per actuals as per Audited Accts 4090052

Weighted Inflation Index 7.24%

Consumer Growth Index (CGI) based on 3 Year CAGR 3.52%

O & M expenses for FY13 excluding P&G contribution - Rs.

Crs. 400.19

Normative O&M Expenses - Rs.Crs. 470.61

The above normative O & M expenses have been computed without

considering the contribution to Pension and Gratuity Trust.

The Commission has treated certain employee costs on account of

contribution to P&G Trust as uncontrollable O&M expenses as these

expenditure are incurred on the basis of actuarial valuation. This

component has been allowed beyond the normative O&M expenses

to enable ESCOMs to meet their actual employee costs.

The HESCOM in its audited accounts for FY15 has indicated an amount

of Rs.83.22 Crores towards contribution to Pension and Gratuity Trust.

Considering the contribution to terminal benefits to the Pension and

Gratuity Trust as uncontrollable O & M expenses, the Commission has

computed the allowable O & M expenses for FY15, as follows:

TABLE – 4.11

Allowable O & M Expenses for FY15

Amount in Rs. Crores

Sl.

No. Particulars FY15

1 Normative O & M expenses 470.61

2 Additional employee cost (uncontrollable

O & M expenses)

83.22

3 Allowable O & M expenses for FY15 553.83

Thus, the Commission decides to allow an amount of Rs.553.83 Crores

as O&M expenses for FY15.

xl

4.2.6 Depreciation:

HESCOM’s Submission:

The HESCOM has claimed an amount of Rs.99.05 Crores as

depreciation, worked out after deducting depreciation on assets

created out of consumers’ contributions / grants as per Accounting

Standards (AS) – 12

Commission’s analysis and decisions:

As per the Audited accounts of the HESCOM for FY15, it is noted that,

Rs.99.05 Crores has been accounted as depreciation. The

depreciation is determined by the Commission in accordance with the

provisions of the KERC (Terms and Conditions for Determination of

Tariff) Regulations, 2006 as amended on 1st February, 2012.

Considering the opening and closing amount of gross blocks of fixed

assets for FY15 and the depreciation as per the annual accounts, the

weighted average rate of depreciation works out to 4.30%. The

amount of depreciation claimed by the HESCOM as per its audited

accounts is rightly without considering the cost of assets created out of

consumer contribution / grants.

Based on the above, the Commission decides to allow the net

depreciation of Rs.99.05 Crores for FY15.

4.2.7 Capital Expenditure for FY15

The HESCOM has reported a capital expenditure of Rs.527.21Crores

(Format D17) against the approved capex of Rs.797.5 Crores for FY15.

But, it has furnished the capital expenditure against each category of

works for a total of Rs.458.78 Crores as shown below:

xli

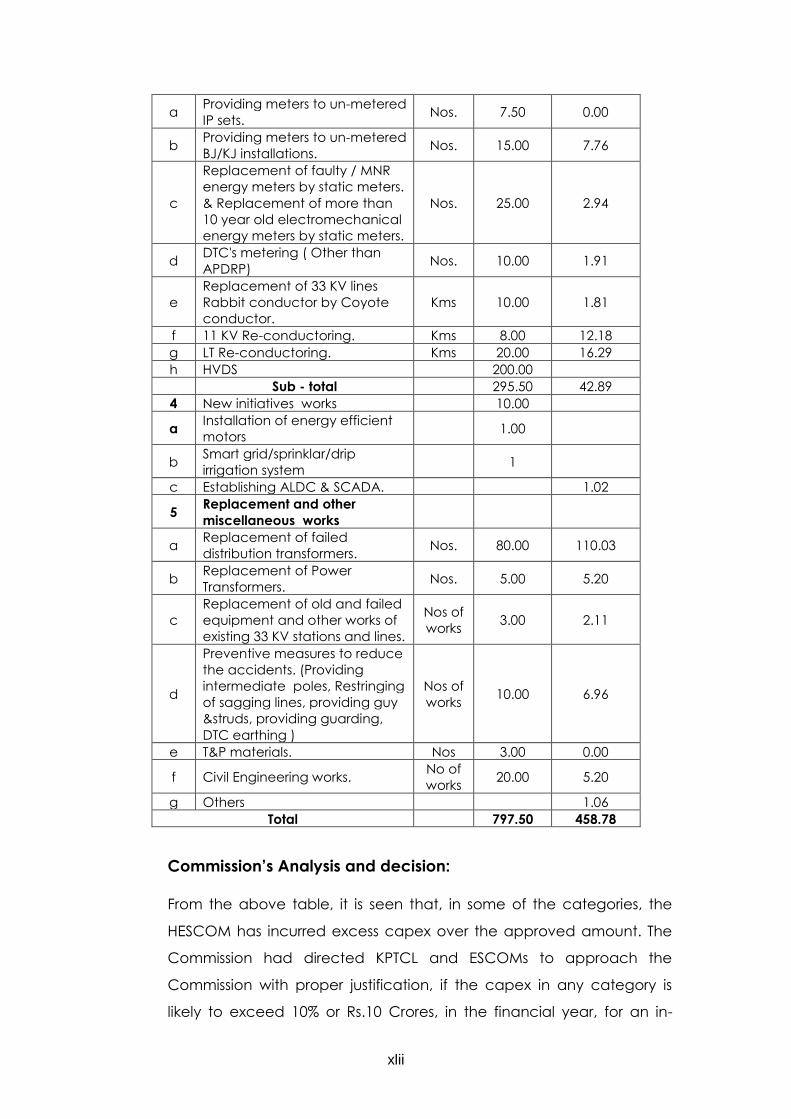

TABLE – 4.12

Capital expenditure for FY15

Amount in Rs. Crores

Sl

No Particulars Units

Approve

d Capex

Actual

Expenditur

e

1 Mandatory works, Social

obligation and other works

a Gangakalyan 50.00 35.85

b

Special Development Plan for

backward talukas under

Nanjundappa scheme(SDP)

village

s 1.98

c Electrification of Hamlets(Not

covered under RGGVY) Nos. 1.00 1.32

d

Electrification of HB/DB/JC/AC

(Habitations) including IP Sets

under SCSP

Nos. 0.50 0.83

e

Electrification of

TC(Habitations) including IP

Sets under TSP

Nos. 0.50 0.32

f

Electrification of BPL

Households (Not covered

under RGGVY)

1.00

g RGGVY

No of

House

hold

3.04

H Rehabilitation of flood affected

villages (special Programme).

Nos. of

Village

s

10.00 0.53

I Water works Nos. 30.00

2 Expansion of network and

system improvement works.

a E & I works. 50.00 19.52

b Energization of IP sets under

general. Nos. 40.00 1.87

c Service connections other than

IP/BJ/KJ/Water works. Nos. 35.00 21.83

d

Construction of new 33 KV

stations Nos

8.00 4.68 Construction of new 33 KV

lines. Kms

e Augmentation of 33 KV

stations. Nos. 8.00 0.05

f Construction of 11 KV lines for

33 KV / 110 KV sub-stations. Feeders 40.00 12.43

g Nirantar Jyoti Yojana.

No of

feeder

/Kms

50.00 72.77

h R- APDRP. PART

A&B 15.49

i Creating infrastructure to UAIP

Sets Nos 45.00 91.80

3 Reduction of T & D and ATC loss

xlii

a Providing meters to un-metered

IP sets. Nos. 7.50 0.00

b Providing meters to un-metered

BJ/KJ installations. Nos. 15.00 7.76

c

Replacement of faulty / MNR

energy meters by static meters.

& Replacement of more than

10 year old electromechanical

energy meters by static meters.

Nos. 25.00 2.94

d DTC's metering ( Other than

APDRP) Nos. 10.00 1.91

e

Replacement of 33 KV lines

Rabbit conductor by Coyote

conductor.

Kms 10.00 1.81

f 11 KV Re-conductoring. Kms 8.00 12.18

g LT Re-conductoring. Kms 20.00 16.29

h HVDS 200.00

Sub - total 295.50 42.89

4 New initiatives works 10.00

a Installation of energy efficient

motors 1.00

b Smart grid/sprinklar/drip

irrigation system 1

c Establishing ALDC & SCADA. 1.02

5 Replacement and other

miscellaneous works

a Replacement of failed

distribution transformers. Nos. 80.00 110.03

b Replacement of Power

Transformers. Nos. 5.00 5.20

c

Replacement of old and failed

equipment and other works of

existing 33 KV stations and lines.

Nos of

works 3.00 2.11

d

Preventive measures to reduce

the accidents. (Providing

intermediate poles, Restringing

of sagging lines, providing guy

&struds, providing guarding,

DTC earthing )

Nos of

works 10.00 6.96

e T&P materials. Nos 3.00 0.00

f Civil Engineering works. No of

works 20.00 5.20

g Others 1.06

Total 797.50 458.78

Commission’s Analysis and decision:

From the above table, it is seen that, in some of the categories, the

HESCOM has incurred excess capex over the approved amount. The

Commission had directed KPTCL and ESCOMs to approach the

Commission with proper justification, if the capex in any category is

likely to exceed 10% or Rs.10 Crores, in the financial year, for an in-

xliii

principle approval, but the HESCOM has not sought any approval of

this kind. Some of the categories in which the capex has been

exceeded above the approved limit are:

i. In the case of Electrification of Hamlets (Not covered under

RGGVY) & Electrification of HB/DB/JC/AC (Habitations) including IP

Sets under SCSP programs, HESCOM has achieved 32% and 66%

above the approved capex of Rs.1.0 Crore and Rs.0.5 Crore.

ii. In the case of NJY and creating infrastructure to Un-Authorized IP

Sets, the HESCOM has exceeded its own projections by 46% and

104% over the approved capex of Rs.50 Crores and Rs.45 Crores.

iii. In the case of 11kV Re-conductoring work, the capex is exceeded

by 52% over the approved capex of Rs.8 Crores.

iv. In case of Replacement of failed distribution transformers, the

capex incurred is indicated at an alarmingly high value of Rs.110.03

Crores which is 38% above the approved limit of Rs.80 Crores.

v. With regard to the Replacement of failed distribution transformers,

the Commission had sought the details of failed distribution

transformers, repaired and replacement and also, the procurement

of new transformers for replacement of failed transformers for FY15.

In its reply the HESCOM has stated that, 22064 Transformers had

failed, 662 nos were scrapped as they could not be repaired, 17944

Nos were repaired and 1356 new transformers were procured for

replacement of failed transformers which has cost Rs.9.34 Crores.

The HESCOM should note that, the failed transformers should be

replaced by repaired good transformers only and it should be

charged to revenue expenditure. In case, the failed transformer is

scrapped, only then, it can be replaced by a new transformer, to be

accounted under capex. Hence, the amount spent for procurement

of new transformers for replacement of failed transformers at Rs.9.34

Crores shall have to be considered as capex instead of Rs.110.03

Crores and the total capex indicated at Rs.458.78 Crores will

become Rs.358.09 Crores (after deducting the excess capex of

xliv

Rs.100.69 Crores indicated as capex of new transformers for

replacement of failed ones).

vi. In many other categories of works, HESCOM has not achieved more

than 20% of the approved capex, which shows that, the planning

and implementation coordination is not properly monitored by while

taking up the capex program.

The year-wise capital expenditure incurred by HESCOM against the

approved Capex during the last four years is shown in the following

Table:

TABLE – 4.13

Approved Vs Actual capital investment Amount in Rs.Crores

Particulars FY12 FY13 FY14 FY15

Capital Investment Proposed &

Approved 1495.17 1189.22* 1178* 797.5*

Capital Investment actually

incurred (Figures as per Annual

Report)

224.48 251.27 343.05

358.09

Short fall 1270.69 937.95 834.95 431.41

% Achievement 15.01% 21.13% 29.12% 44.90%

* Rs.500 Crores was considered for the purpose of computing ARR for FY13, FY14 & FY15

From the above table, it can be noted that, the HESCOM was not able

to achieve more than 44.90% of the approved capex in any of the

year from FY12. Further, looking at the capital expenditure for FY15, it is

noted that, even though it has exceeded the capex in certain

categories of works, it has not exceeded the overall capex approved

by the Commission.

Taking into consideration the above facts, the Commission decides to

allow the actual capital expenditure of Rs.358.09 Crores for FY15, after

deducting the capex not meeting the prudence norms as per the

following para.

4.2.8 Prudence check of FY15:

The prudence check of capex of HESCOM was taken in two parts:

a) Prudence check of execution of the capital works of FY15:

b) Prudence check of material Procurement process of FY15:

xlv

a) Prudence check of execution of the capital works of FY15:

The Commission had taken up prudence check of the capital

expenditure incurred by for the period FY15 by engaging the services

of M/s. Deloitte Touche Tohmatsu India Private Limited, (M/s. Deloitte)

as consultant to evaluate the capital expenditure of FY15 pertaining to

completed and categorized works.

M/s. Deloitte has collected the list of works carried out in HESCOM for

FY15.The works were divided into three categories based on their cost

(a) works costing above Rs.6 Lakh, (b) works costing Rs.3 to 6 Lakh and

(c) works below Rs.3 Lakhs. The works were taken up under various

schemes like RAPDRP, UNIP and Niranthara Jyothi Schemes apart from

General capital works like service connection, Extension &

Improvement works, Civil engineering works, metering, etc. A

representative sample in each category was selected covering the

geographical area of the Company as per the Scope of work and

submitted the report of the prudence check.

The consultant has considered sample works of 120 Nos. with a cost of

Rs.4,463 Lakh in Rs.6 Lakh and above category, 40 No. of works with a

cost of Rs.217 Lakh in Rs.6 Lakh to Rs.3 Lakhs category and 33 Nos. of

works from 11 divisions with a total cost of Rs.91 Lakh in below Rs.3 Lakh

category.

As per the report of the consultant, the following are the salient

features:

TABLE – 4.14

Gist of Prudence check findings for FY15

Particulars Numbers Amount

in Rs. Lakhs

Works costing Rs.6 Lakhs and above considered as

samples for validation 120 4,463

Works costing between than Rs.6 Lakhs and Rs.3

Lakhs considered as samples 40 217

Works costing below Rs.3 Lakhs considered as

samples 33 91

Works not meeting the

norms of prudence

Rs.6 Lakhs and above 01 68.68

Rs.6 Lakhs and Rs.3 Lakhs Nil

below Rs.3 Lakhs Nil

Total works not meeting the norms of prudence 01 68.68

Some of the other findings of the prudence check are summarized in

the following Table:

xlvi

TABLE – 4.15

Summary of Works having cost overrun

Particulars Within 10% 10-25% Above 25%

Rs.6 Lakhs and above 66 13 41

Rs.6 Lakhs and Rs.3 Lakhs 20 03 17

below Rs.3 Lakhs 23 03 07

TABLE – 4.16

Summary of Works having Time overrun

Particulars Within Year Between one

and two Years

Above 2

Years

Rs.6 Lakhs and above 106 09 05

Rs.6 Lakhs and Rs.3 Lakhs 40 - -

below Rs.3 Lakhs 33 - -

The Commission had forwarded the copy of the Report on the

Prudence check seeking HESCOM’s comments thereon. The reply

forwarded by HESCOM is summarized below:

HESCOM has stated that, it has categorised assets of the pertaining to

work of establishment 5 MVA transformers other than the transformer

on 28.01.2015. Subsequently, it has installed 5 MVA transformer on

12.08.2015 for which pre commissioning test has been carried out after

four months on 01.12.2015 and the load on the transformer has been

taken. The categorization of works before commissioning of the

project is not proper. The Commission views this matter seriously and

directs the HESCOM to monitor and avoid such things in future. The

Commission noting the above points has taken a view that, one work

amounting to Rs.68.68 Lakhs in the samples selected by the consultant

during FY15, does not qualify for being treated as prudent and

consequently the corresponding depreciation and interest on loans

allowed by the Commission in the tariff have to be disallowed in APR of

FY15 as detailed below:

xlvii

TABLE – 4.17

Details of Amounts disallowed in APR FY15

Particulars Amount in Rs.

Lakhs

Total cost of categorized works eligible for prudence check 10,313

Total cost of the sample works 4,771

Cost of sample works not meeting prudence norms (01 work

with cost of Rs.68.68 lakh against a sample basket of 61 works

with Rs.954 Lakhs)

68.68

Percentage of cost not meeting prudence norms with respect

to the total samples considered in the category (Rs.68.68 lakh

against a sample basket with Rs.954 Lakhs)

7.20

Overall cost of capex not meeting prudence norms compared

with the cost of that category of samples (Rs.68.68 lakh forming

7.2% of sample basket escalated to total capex under the

respective category of works of Rs.1964 Lakhs)

141.39

Amount to be disallowed towards works not meeting prudence

norms calculated on the basis of weighted average interest &

weighted average depreciation on the capex to be disallowed. 17.43

b) Prudence check of Material Procurement process of FY15:

The HESCOM has been executing capital works both on turnkey as well

as partial turnkey contracts. In the process, the HESCOM procures

major materials like, distribution transformers, poles and conductor etc.

and issues them to the partial turnkey contractor for carrying out the

labour contract work as per award. The contractor would also invest

on some of the smaller materials associated with the works viz., cross

arm, bolt & nuts, earthing materials etc.

In view of the fact that, a large quantity of major materials are being

procured by the ESCOMs, the Commission decided to review material

procurement process of major materials as a part of prudence check

with a view ensure that procurement is carried out in a cost-effective

manner without compromising on the operational needs.

The Analysis of procurements in FY15 revealed that a considerable

level of inventory vis-à-vis the actual requirement, seems to have been

maintained in the case of,

xlviii

a. Special three pin cross arms,

b. 1.1 KV GI pins,

c. LT wiring Kit for 100KVA TC,

d. D.P Set.

Hence, the HESCOM has to take measures to utilize the procured

materials in a systematic way and reduce the inventory by planning

the delivery schedule of the material in synchronisation with the work

execution and the inventory level should be around 25% only of annual

requirement.

Further, the HESCOM is going for open tendering under e-procurement

mode for all the purchases, except in case of the orders placed with

Govt. owned firms, for which exemption is given under KTPP Act.

The Commission noting the above points directs HESCOM to maintain

its inventory judiciously.

c) Prudence Check of Capital Investment for the period FY13 to FY14:

The Commission has treated a capex of Rs.13.46 Crores along with

Rs.7.21 Crores for the asset created by KPTCL in the HESCOM area for

which the downstream lines not completed are attributable to the

HESCOM as not meeting the prudence norms. The Commission had

given an opportunity to the HESCOM to justify the project to meet the

norms of prudence by submitting sufficient data.

The HESCOM has submitted its reply with adequate data to claim that

the works meet the norms of prudence and after verifying all the data,

the Commission has decided that, the works could be considered as

meeting the norms of prudence and that no further disallowance, in

respect of these works, is necessary.

d) Prudence Check of Capital Investment for the period FY10 to FY12:

xlix

The Commission had disallowed a capex of Rs.2.64 Crores incurred for

one work pertaining to the period FY10 - FY12 as not meeting the

prudence norms and disallowed the weighted average interest and

depreciation on the corresponding capex in the Tariff order dated

02.03.2016. HESCOM has submitted the required data to justify the work

as meeting the prudence norms and after verifying the data submitted

by HESCOM, the Commission decides not to continue the

disallowance.

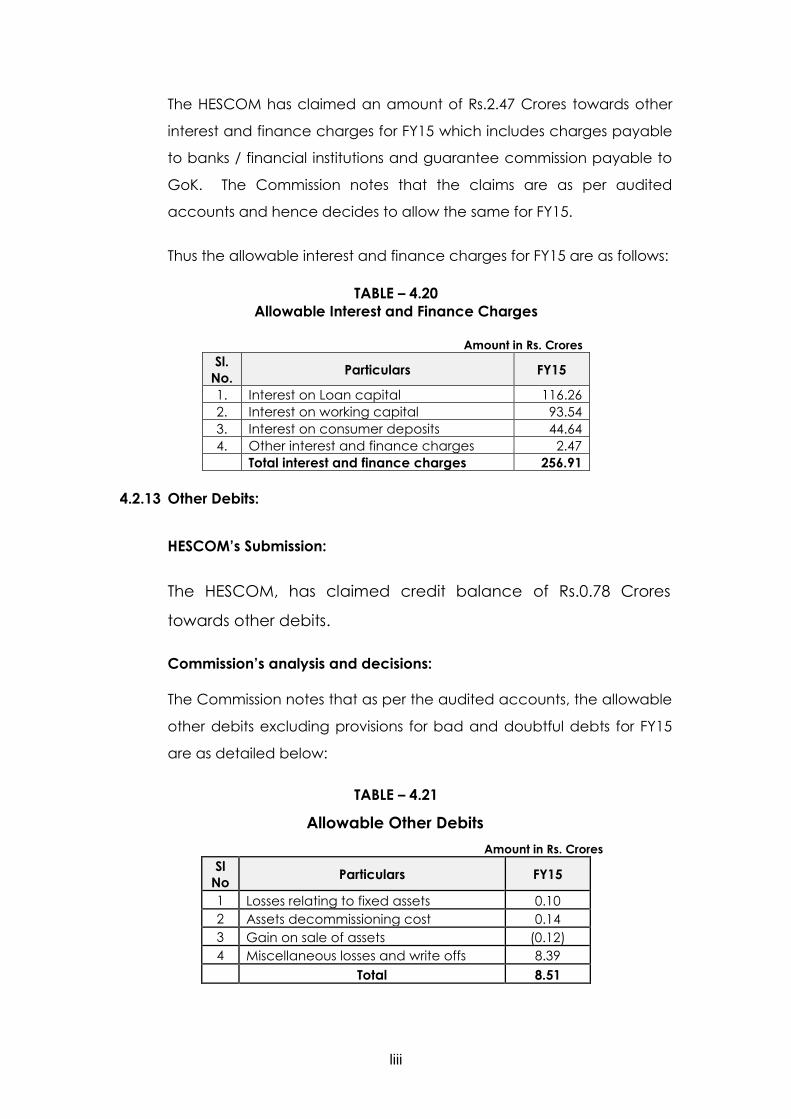

4.2.9 Interest and Finance Charges:

a) Interest on loan:

HESCOM’s Submission:

The HESCOM, in its application has claimed an amount of

Rs.180.75 Crores towards interest on long term loans drawn from

banks / financial institutions for FY15.

Commission’s analysis and decisions:

The Commission has noted the status of opening and closing balances

of long term loans as per the audited accounts for FY15, the details in

Format- D9 of the filings and replies to the preliminary observations as

shown below:

TABLE – 4.18

Allowable Interest on Loans – FY15

Amount in Rs.Crores

Particulars FY15

Total opening balance of loans 1003.47

Add new Loans 173.29

Less Repayments 153.63

Total loan at the end of the year 1023.13

Average Loan 1013.30

Interest on long term loans as per audited accounts for FY15 116.26

l

Considering the average loan amount of Rs.1013.30 Crores and an

amount of Rs.116.26 Crores incurred towards interest on long term

loans, the weighted average rate of interest works out to 11.47% which

is within the present interest rates charged by the bank/ financial

institutions.

Thus, the Commission decides to allow an amount of Rs.116.26 Crores

towards interest on long term loan for FY15.

4.2.10 Interest on Working Capital:

HESCOM’s Submission:

The HESCOM has stated that it has borrowed short term loans

and overdrafts during FY15 to meet its day to day expenditure

(working capital). As per the audited accounts and the replies

to preliminary observations, the HESCOM has incurred Rs.82.91

Crores towards interest on short term loans and overdraft for

FY15.

Commission’s analysis and decisions:

The Commission notes that, as per the audited accounts and the

replies to its preliminary observations, the HESCOM has incurred an

interest of Rs.82.91Crores on short term borrowings/ Overdrafts during

FY15.

The present interest rates by commercial banks and financial

institutions are charged mainly on the basis of base rate of interest

declared by RBI from time to time. The Commission has considered

interest on short term loan at base rate plus certain basis points

depending upon the tenure of the loan. As per the HESCOM’s

application, it is stated that short term loans for FY15 has been availed

at a weighted average rate of interest of 10.98%. However,

considering the base rate of interest with spread of 250 basis points

and noting the downward trend in the interest rate, the Commission

li

decides to allow short term loans at a normative interest of 11.75% for

FY15.

As per the KERC (Terms and Conditions for Determination of Tariff)

Regulations, 2006 as amended on 1st February, 2012, the Commission

computes the allowable interest on working capital for FY15 as follows:

lii

TABLE – 4.19

Allowable Interest on Working Capital for FY15

Amount in Rs.Crores

Particulars FY15

One-twelfth of the amount of O&M Expenses 46.15

Opening GFA 3174.87

Stores, materials and supplies 1% of Opening balance of GFA 31.75

One-sixth of the Revenue 808.60

Total Working Capital 886.50