Embed Size (px)

Citation preview

Healthcare Seminar

Medical Malpractice and Its Complementary Coverages: What Are

They?

March 7, 2007

Today’s Speakers

KIMBER LANTRY – Hudson Healthcare

BILL DYER – HCP National Insurance Services

ALICE JOHANSSON – OneBeacon Professional Partners

DREW BARTKIEWICZ – Darwin Professional Underwriters

Malpractice Loss Trends 2007 Malpractice Loss Trends 2007 UpdateUpdate

Kimber J. Lantry, Executive Vice PresidentHudson Insurance Group851 Napa Valley Corporate Way, Suite NNapa, CA 94558(707) 225-3301(707) 224-6936 [email protected]

Medical Malpractice IndustryMedical Malpractice IndustryCombined RatioCombined Ratio

106.6% 107.9%

129.7%

154.2%

141.6%136.9%

112.0%

95.5%

115.7%

99.8%

133.8%

85%

95%

105%

115%

125%

135%

145%

155%

165%

175%

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

Medical Malpractice

Source: Bests Aggregates & Averages, 2005 Property & Casualty edition

Selected Company ResultsSelected Company Results20052005

Source: A. M. Best Statistical Study, August 28, 2006Source: A. M. Best Statistical Study, August 28, 2006

Companies Direct Premiums Written* *$thousands

Loss Ratio

MLMIC $871,089 97%

AIG $856,834 30%

Berkshire Hathaway (Med Pro, GenStar) $710,021 57%

ProAssurance Group $612,242 28%

CNA Insurance Companies $516,517 60%

Doctors Co Ins Group $492,153 41%

ISMIE $405,420 56%

Mag Mutual Group $355,949 43%

ProMutual Group $344,706 57%

Health Care Indemnity $331,020 56%

Norcal Group $297,648 56%

Physicians’ Reciprocal Insurers $290,698 77%

FPIC Ins Group $279,540 46%

Fairfax Financial Group $148,701 41%

SEVERITYSEVERITY

Sources of Medical Malpractice DataSources of Medical Malpractice Data

State by state filings- Little hospital data available as hospitals are written surplus lines- Quality varies by size, state requirements and quality of filing

St. Paul data – no longer available Aon Study – largest available database

- 84 hospitals; 63,000 bed equivalents; $250M premium in first $1M layer

Jury Verdicts Research - Countrywide, accurate, but only about 5% of all medical malpractice,

skewed towards high severity

National Practitioners Data Base - Physician data only; no hospital data- Only closed claims = 5 year lag- No expense costs included

PIAA Data- Fear of competitors’ use = limited utility

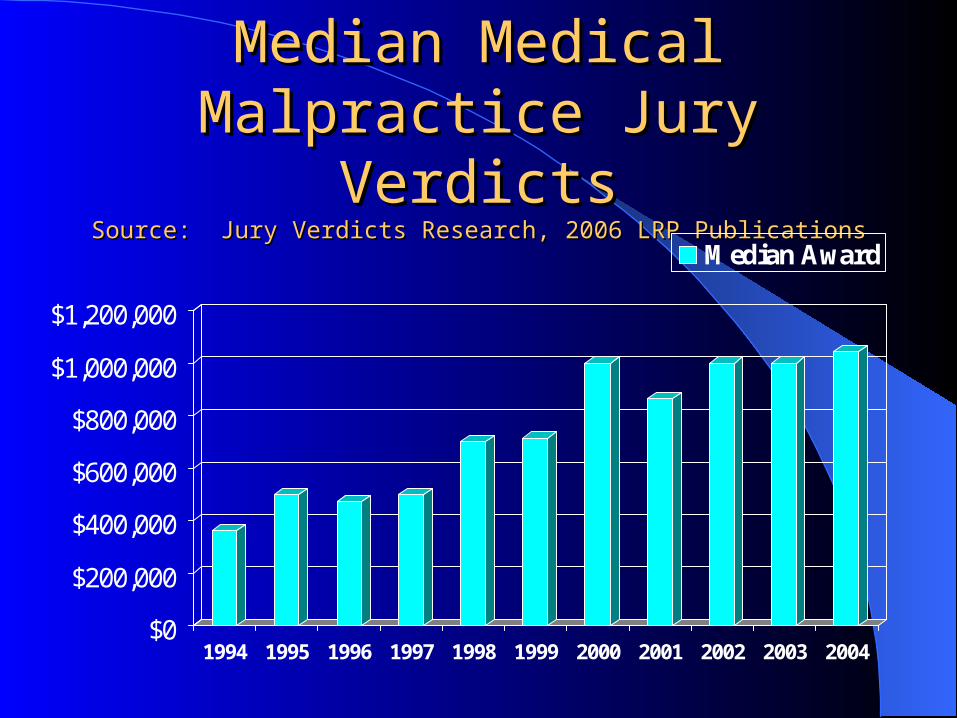

Median Medical Malpractice Median Medical Malpractice Jury VerdictsJury Verdicts

Source: Jury Verdicts Research, 2006 LRP PublicationsSource: Jury Verdicts Research, 2006 LRP Publications

$0

$200,000

$400,000

$600,000

$800,000

$1,000,000

$1,200,000

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

Median Award

Mean Medical Malpractice Mean Medical Malpractice Jury VerdictsJury Verdicts

Source: Jury Verdicts Research, 2005 LRP PublicationsSource: Jury Verdicts Research, 2005 LRP Publications

$0

$1,000,000

$2,000,000

$3,000,000

$4,000,000

$5,000,000

$6,000,000

1997 1998 1999 2000 2001 2002 2003

Mean Award

National Practitioners Data BaseNational Practitioners Data BaseSeverity AnalysisSeverity Analysis

Source: National Practitioner Data Bank Public Use File, June 30, 2006Source: National Practitioner Data Bank Public Use File, June 30, 2006

0

50,000

100,000

150,000

200,000

250,000

300,000

1990 1992 1994 1996 1998 2000 2002 2004 2006

Ave

rage

Clo

sed

Cla

im

Average Indemnity Payment

PIAA Data BasePIAA Data BaseSeverity AnalysisSeverity Analysis

Source: PIAA, 2004Source: PIAA, 2004

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

1996 1997 1998 1999 2000 2001 2002 2003

Ave

rage

Clo

sed

Cla

im

Average Indemnity Payment Median Indemnity Payment

Aon Risk Consultants, Inc., Aon Risk Consultants, Inc., Medical Professional LiabilityMedical Professional LiabilityPhysician Professional Liability BenchmarkPhysician Professional Liability Benchmark

HISTORICAL SEVERITY *HISTORICAL SEVERITY *

120,000 130,000

140,000 135,000 140,000

155,000 161,000

170,000

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

180,000

1996 1997 1998 1999 2000 2001 2002 2003

* Based on non-zero claims only; Individual losses limited to $2M

FREQUENCYFREQUENCY

FrequencyFrequencyPer Earned Unit of ExposurePer Earned Unit of Exposure

Source: PIAA DataSource: PIAA Data

0.081

0.09

0.095

0.115

0.07

0.081

0.089

0.073

0.08

0.075 0.075 0.075

0.063

0.076

0.0590.063

0.067 0.069

0.063

0.02

0.04

0.06

0.08

0.1

0.12

1983 1985 1987 1989 1991 1993 1995 1997 1999 2001

National Practitioners Data BaseNational Practitioners Data BaseFrequency AnalysisFrequency Analysis

Source: National Practitioners Data Bank public use file, June 30, 2006Source: National Practitioners Data Bank public use file, June 30, 2006

2.93.1 3 2.9

2.6 2.62.4 2.3 2.4 2.4 2.5

2.2 2.22 1.91.8

0

0.5

1

1.5

2

2.5

3

3.5

Cla

ims

Per

100

Phy

sici

ans

Aon Risk Consultants, Inc., Aon Risk Consultants, Inc., Medical Professional LiabilityMedical Professional LiabilityPhysician Professional Liability BenchmarkPhysician Professional Liability Benchmark

HISTORICAL FREQUENCY PER CLASS 1 EQUIVALENT *HISTORICAL FREQUENCY PER CLASS 1 EQUIVALENT *

6.00%

7.00%

6.50%

7.50%

8.00%

7.00%7.00% 7.00%

0%

1%

2%

3%

4%

5%

6%

7%

8%

1996 1997 1998 1999 2000 2001 2002 2003

* Number of claims per physician; for example, the 2003 year indicates 7 claims per 100 class 1 physicians.

FREQUENCY AND FREQUENCY AND SEVERITY SEVERITY

TREND ANALYSISTREND ANALYSIS

Aon Risk Consultants, Inc., Aon Risk Consultants, Inc., Medical Professional LiabilityMedical Professional LiabilityPhysician Professional Liability BenchmarkPhysician Professional Liability Benchmark

HISTORICAL LOSS COSTS PER CLASS 1 EQUIVALENT *HISTORICAL LOSS COSTS PER CLASS 1 EQUIVALENT *

7,500

9,50010,000

10,500

12,250 12,000 12,250 12,500

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

1996 1997 1998 1999 2000 2001 2002 2003

* Individual losses limited to $2M

Frequency and SeverityFrequency and Severity

Frequency = number of claims reported

Severity = average cost per claim

Frequency & severity trend factor– General Consensus: 6% - 7%, higher in jurisdictions

without tort reform

PHYSICIAN ISSUESPHYSICIAN ISSUES

Hospital vs. Physician Loss Hospital vs. Physician Loss CostsCosts

Source: 2006 Update on U.S. Tort Cost Trends, Towers Source: 2006 Update on U.S. Tort Cost Trends, Towers Perrin Tillinghast Perrin Tillinghast

0

5,000,000

10,000,000

15,000,000

20,000,000

1975 1979 1983 1987 1991 1995 1999 2003

HospitalPhysicianOther

MEDICAL MALPRACTICE MEDICAL MALPRACTICE INSURANCE COMPANY INSURANCE COMPANY

RESULTSRESULTS

Medical Malpractice Premium Medical Malpractice Premium VolumeVolume

2005: $9,124,374

Source: 2006 Best’s Aggregates & Averages – Property/Casualty

This doesn’t count:

– Self insurance– Captives– Patient compensation funds– Risk retention and risk purchase groups– JUAs– Trusts

Accident Year vs. Calendar Accident Year vs. Calendar YearYear

Accident Year = Results from all policies written during that year

Calendar Year = Results from all polices written during that year plus any reserve changes made to prior years

Virtually all published data is on a calendar year basis

Loss Ratios for Medical Loss Ratios for Medical Malpractice IndustryMalpractice Industry

Source: 2006 Bests Aggregates & Averages – Property/CasualtySource: 2006 Bests Aggregates & Averages – Property/Casualty

53.3% 57.7%68.5%

74.1%

98.3%

85.9% 82.8%

49.1%62.5%

0%

20%

40%

60%

80%

100%

120%

1997 1998 1999 2000 2001 2002 2003 2004 2005

1

Loss Adjusting Expense Loss Adjusting Expense Ratios for Medical Malpractice Ratios for Medical Malpractice

IndustryIndustrySource: 2006 Bests Aggregates & Averages – Property/CasualtySource: 2006 Bests Aggregates & Averages – Property/Casualty

29.9%

33.7%

36.1% 36.0%

33.7%

37.2%38.1%

34.0%

28.9%

20%22%24%26%28%

30%32%34%36%38%40%

1997 1998 1999 2000 2001 2002 2003 2004 2005

1

Incurred Loss Ratios for Incurred Loss Ratios for Medical Malpractice IndustryMedical Malpractice Industry

Pure Loss + Allocated Loss Adjusting Expenses (ALAE) = Incurred LossesPure Loss + Allocated Loss Adjusting Expenses (ALAE) = Incurred Losses Source: 2006 Bests Aggregates & Averages – Property/Casualty Source: 2006 Bests Aggregates & Averages – Property/Casualty

83.2%91.4%

104.5%110.1%

132.0%123.1%120.9%

96.5%

78.0%

0%

20%

40%

60%

80%

100%

120%

140%

1997 1998 1999 2000 2001 2002 2003 2004 2005

1

Loss Triangles Loss Triangles Source: Schedule P – Part 3F – Section 2 – Medical Malpractice Claims MadeSource: Schedule P – Part 3F – Section 2 – Medical Malpractice Claims Made

1996 136,406 760,973 1,560,219 2,154,219 2,645,481 2,929,605 3,105,875 3,119,273 3,176,262 3,211,716

1997 XXX 179,905 901,259 1,758,117 2,453,131 2,959,947 3,294,766 3,439,669 3,534,482 3,597,670

1998 XXX XXX 186,512 954,799 1,984,009 2,720,659 3,310,598 3,655,174 3,823,325 3,942,837

1999 XXX XXX XXX 162,422 993,215 2,048,387 2,890,342 3,326,553 3,622,793 3,794,908

2000 XXX XXX XXX XXX 192,852 1,026,414 2,216,381 3,091,845 3,409,977 3,661,659

2001 XXX XXX XXX XXX XXX 206,232 1,256,625 2,487,802 3,387,676 3,911,623

2002 XXX XXX XXX XXX XXX XXX 204,059 1,145,453 2,322,222 3,189,346

2003 XXX XXX XXX XXX XXX XXX XXX 164,104 1,007,225 1,961,633

2004 XXX XXX XXX XXX XXX XXX XXX XXX 162,393 852,692

2005 XXX XXX XXX XXX XXX XXX XXX XXX XXX 154,901

Expense RatioExpense RatioSource: 2006 Bests Aggregates & Averages – Property/CasualtySource: 2006 Bests Aggregates & Averages – Property/Casualty

15.2%16.8%

16.8%18.0%19.7%19.8%21.1%20.5%20.3%

0%

5%

10%

15%

20%

25%

1997 1998 1999 2000 2001 2002 2003 2004 2005

1

Consists of:– Costs to run company– Commissions to agents & brokers– Premium taxes

Combined Ratio Combined Ratio Source: 2006 Bests Aggregates & Averages – Property/CasualtySource: 2006 Bests Aggregates & Averages – Property/Casualty

112.3%95.5%107.9%

142.3%154.8%133.8%

129.7%115.7% 138.1%

0%

20%

40%

60%

80%

100%

120%

140%

160%

180%

1997 1998 1999 2000 2001 2002 2003 2004 2005

1

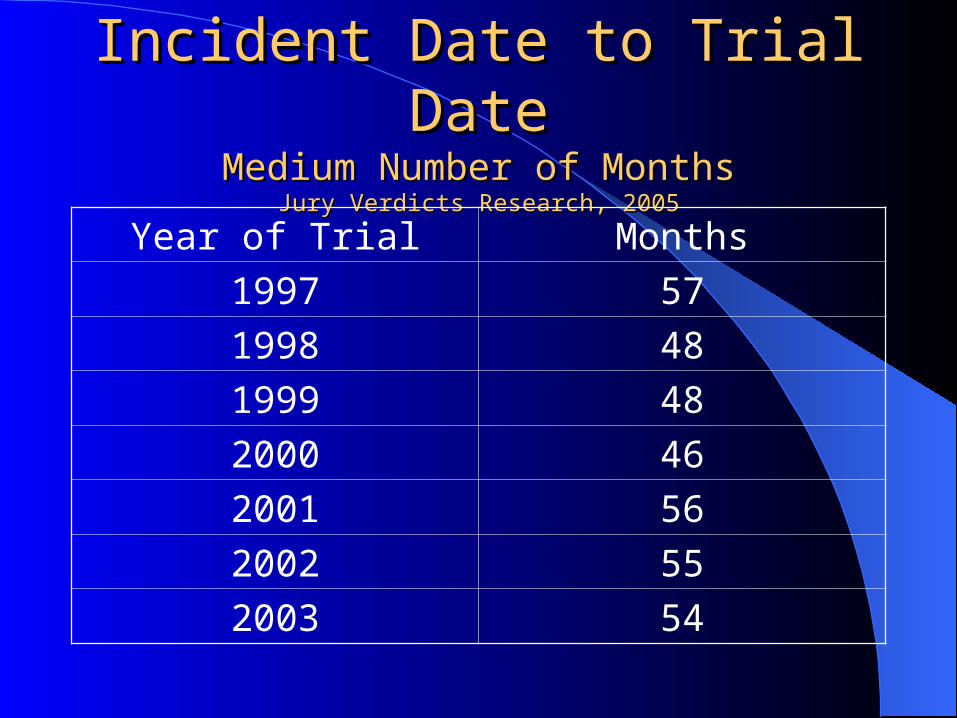

Incident Date to Trial DateIncident Date to Trial DateMedium Number of MonthsMedium Number of Months

Jury Verdicts Research, 2005Jury Verdicts Research, 2005

Year of Trial Months

1997 57

1998 48

1999 48

2000 46

2001 56

2002 55

2003 54

Occurrence to Settlement LagOccurrence to Settlement Lag(in number of years)(in number of years)

Source: National Practitioners Data Bank public use file, June 30, 2006Source: National Practitioners Data Bank public use file, June 30, 2006

4.14.24.34.44.54.64.74.84.9

5

Filing Date to Trial DateFiling Date to Trial DateMedium Number of MonthsMedium Number of Months

Jury Verdicts Research, 2005Jury Verdicts Research, 2005

Year of Trial Months

1997 33

1998 25

1999 26

2000 25

2001 30

2002 30

2003 30

Investment IncomeInvestment IncomeSource: 2006 Bests Aggregates & Averages – Property/CasualtySource: 2006 Bests Aggregates & Averages – Property/Casualty

Med Mal companies hold on to each premium dollar for an average of 3 years

12.6%

16.1%15.7%

12.8%

19.0%

27.9%

23.7%

28.0%30.0%

0%

5%

10%

15%

20%

25%

30%

35%

1997 1998 1999 2000 2001 2002 2003 2004 2005

1

Overall Operating RatioOverall Operating Ratio“The Bottom Line”“The Bottom Line”

Source: 2006 Bests Aggregates & Averages – Property/CasualtySource: 2006 Bests Aggregates & Averages – Property/Casualty

96.3%82.9%

122.4%

129.5%

135.8%105.9%

106.0%87.7%

77.9%

0%

20%

40%

60%

80%

100%

120%

140%

160%

1997 1998 1999 2000 2001 2002 2003 2004 2005

1

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

11,00019

7619

7719

7819

7919

8019

8119

8219

8319

8419

8519

8619

8719

8819

8919

9019

9119

9219

9319

9419

9519

9619

9719

9819

9920

0020

0120

0220

0320

0420

05

Premiums Latest AY Losses

Malpractice Industry Premium and Losses 1976-2005

Medical Malpractice Accident-Year Results ($ in millions)

TORT REFORMTORT REFORM

Average Loss per Physician in States Average Loss per Physician in States With and Without CapsWith and Without Caps

Loss ($) per PhysicianLoss ($) per PhysicianSource: Richard S. Biondi & Arthur Gurevitch Source: Richard S. Biondi & Arthur Gurevitch ContingenciesContingencies November/December November/December

20032003

0

2,000

4,000

6,000

8,000

10,000

1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002

Year Closed

States without caps

States with caps

Malpractice Claims per Physician in States With Malpractice Claims per Physician in States With & Without Caps - Claims per 100 Physicians& Without Caps - Claims per 100 Physicians

Source: Richard S. Biondi & Arthur Gurevitch Source: Richard S. Biondi & Arthur Gurevitch ContingenciesContingencies November/December November/December 20032003

1.50

2.00

2.50

3.00

3.50

1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002

Year Closed

States without caps

States with caps

Differential in Loss per Physician in States Differential in Loss per Physician in States With & Without CapsWith & Without Caps

Capped States % of Uncapped StatesCapped States % of Uncapped States

Source: Richard S. Biondi & Arthur Gurevitch Source: Richard S. Biondi & Arthur Gurevitch ContingenciesContingencies November/December November/December 20032003

40%

45%

50%

55%

60%

1998 1999 2000 2001 2002

Year Closed

Malpractice Premium per Physician Malpractice Premium per Physician in States With & Without Capsin States With & Without Caps

Premium ($) per PhysicianPremium ($) per PhysicianSource: Richard S. Biondi & Arthur Gurevitch Source: Richard S. Biondi & Arthur Gurevitch ContingenciesContingencies November/December November/December

20032003

0

4,000

8,000

12,000

16,000

20,000

1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002

Year Closed

States without caps

States with caps

National Practitioners Data BaseNational Practitioners Data BaseFrequency Analysis – MichiganFrequency Analysis – Michigan

NOTE: Michigan enacted caps on non-economic NOTE: Michigan enacted caps on non-economic damages in 1994damages in 1994

Source: National Practitioners Data Bank public use June 30, 2006Source: National Practitioners Data Bank public use June 30, 2006

5.4 5.7

4.8

5.85.1

3.3 3 3.2 3.32.9

3.43

2.42.1 1.9 1.7

0

1

2

3

4

5

6

7

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

Cla

ims

Per

100

Phy

sici

ans

National Practitioners Data BaseNational Practitioners Data BaseSeverity Analysis - MichiganSeverity Analysis - Michigan

Source: National Practitioner Data Bank Public Use File, June 30, 2006Source: National Practitioner Data Bank Public Use File, June 30, 2006

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

1990 1992 1994 1996 1998 2000 2002 2004 2006

Ave

rage

Clo

sed

Cla

im

Average Indemnity Payment

Tort ReformTort Reform

In 1975-77, in 1985-87 and in 2001-2003 numerous states enacted medical malpractice tort reform.

Five to seven years later (1980-82 and 1990-92), after court challenges to virtually every element of tort reform, approximately 50% was struck down by the states’ high courts. By that standard, we should start seeing the 2001-2003 tort reform start being struck down in 2007.

MT$250k

ID$250k

WA

OR

CA

$250k

AK$400k*

HI$375k

NV$350k

WY

UT$400k

AZNM

$200k*1

CO$300k

ND$500k

SD$500k

MN

NE$500k1

KS$250k

OK$300k

TX$250k

IA

MO$350k

AR

LA $500k1*

WI$350k1

MI$500k*

IL IN$250k1

OH$350k

KYT

NMS

$350kAL GA

$350k

FL$500k*

SC

VA*

WV$250k

PA

NY

ME$400k*

VT

NH

MA - $500k

RI

CT

NJDE

MD - $650k+*

DC

State by State Tort Reform InitiativesLimits on Noneconomic/Pain and Suffering Damage Awards

(as of March 15, 2005)

Source – National Conference of State Legislatures (January 13, 2005)

None

< $250k

$300 - 375k

$400- 500k

$500k and up *See notes for additional details 1 Cap is limit of liability for Providers; remainder to PCF

NC

THE FUTURETHE FUTURE

Medical Malpractice Crisis – Medical Malpractice Crisis – What Crisis?What Crisis?

HOSPITALSSoft market has returned. Hospital excess insurance is the most competitive, but insurance bidding wars are increasingly common for primary as well.

PHYSICIANSRate filing are commonly for modest declines. Large physician groups are enjoying insurance company bidding wars. Numerous carriers are aggressively attempting to expand market share.

Factors Affecting The MarketFactors Affecting The Market

“Class of 2001” is mostly doing wellArch CapitalAceGen StarEndurance SpecialtyBerkeley Medical Excess UnderwritersOneBeaconDarwin Underwriters

Availability of reinsurance support for new entrants A plethora of risk retention groups and admitted

physician company startups Rush to self-insurance and captives is over

The FutureThe Future

Steadily softening market for the next 5 years or more

Continued new market entrants as industry profitability becomes clearer

Higher limits, broader policies Likely to be followed by:

– Unwinding of captives as commercial insurance market becomes cheaper

Followed by…inexorable rising of severity…and the next malpractice crisis

Assessing An Insured ‘s Risk Covering All The Healthcare

Angles – Groups and Solo Doctors

Bill Dyer, President

If you have the opportunity to go to the provider’s office or offices, look at what they have for handouts in their lobby: • Non plastic surgeons or dermatologists offering

• Weight loss programs

• Telemedicine

• Doctor’s names on the door or in brochures that are not on the policy

cosmetic procedures

Ask How They Make Their Money, Meaning:

• Do they rent space to any other doctors?

• Do they have any PAs on salary or working

• Do they have an urgent care or lab?

in their practices that are not covered under their malpractice policy?

Other Insurance

• Do they have entity and individual protection? Many physicians do not know the difference.

• If it’s a group with multiple owners, do they have

• Check out their web sites. See what services they

Directors and Officers and Errors and Omissions insurance - do they have the right kind?

offer. Is there a tech medical E&O exposure not currently covered? (Telemedicine, askadoc.com)

Trends

• Non standard and standard markets are crossing over

• Non standard can be cheaper than standard.

• Non standard policies offer true group policies

Big advantage

• Some doctors are not accepted by the non standard market and then

• Standard insurers are getting more flexible about non standard physicians

• Pricing is softer as is underwriting requirements.

each other.

that offer Departed Physician Roster versus having to tail off doctors when they leave.

taken by the standard market…who knew?

and often are not requiring them to buy tail, but accepting them with full

prior acts.

• We find many physicians who are put in the non standard market for all the wrong reasons.

Questions/concerns insured’s have and how to address them

• Upfront - price, price, price.

Most clients are not concerned with: AM Best rating

Loss control

How many cases the insurer has settled

Financial ratings of most kinds

Questions/concerns insured’s have and how to address them

• Most doctors buy malpractice in denial - they don’t think they’ll

ever be sued so they want the cheapest deal no matter what.

• We need to educate the market as much as possible to go beyond just price, but unfortunately most learn the hard way by their mistakes or those of their colleagues.

• When a physician is sued, the only thing they want to hear fromtheir broker is, “The attorney for your malpractice insurer willbe contacting you shortly.” Remember, this is a very significantevent in a physician’s life. Your job is to make sure everythinggoes the way the policy and the insurer’s procedure’s dictate.

Medical Spas and Clinics

• Non MDs running and owning clinics?

• Where does the Medical Director begin and end? The non MD owner needs to be very careful about

patient care when it comes to his Medical Director.

• How will claims be effected when consumers findthere is no MD onsite?

• Vicarious liability issues for Medical Spas where an MD owns a spa and is also a partner in a medical

Group.

Healthcare D&O Risk Exposures

Presented by

Alice JohanssonMarch 7, 2007

It’s not your grandmother’s community hospital any more

Shift in exposures created by spiral of competitive and environmental issues

in the industry

Issues:• Mergers and acquisitions

• Growth in for-profits

• Budgets– Increased reliance on government funding– Increased costs related to technology– Increased cost of employees– High costs to maintain and improve facilities and

programs

• Increased regulatory scrutiny

• Changes in public perception

Increase in claim activity• Antitrust

– Competitors– Providers– FTC

• Regulatory– Fraud and abuse– Charity care– Executive compensation

• EPL

What does all of this mean to an underwriter?

• Areas of underwriting focus

• Declinations

Managed Care Risk Exposures

Presented by

Alice JohanssonMarch 7, 2007

All Managed Care OrganizationsHave Risk Exposures

• HMO

• PPO

• IPA

• PHO

• MSO

• TPA

• URO

• CVO

• Etc…

Six Primary MCO Liability Risk Exposures

1. Vicarious Liability

2. Credentialing– Negligent Credentialing– Practitioner Exclusion

3. Provider Contracting

Six Primary MCO Liability Risk Exposures

4. Utilization Management

– Financial incentives

– Practice of medicine

– Breach of contract/bad faith claim denial

Six Primary MCO Liability Risk Exposures

5. Misrepresentation– Of the coverage itself– Of the quality of care– Of the quality of the providers– By non-disclosure of financial arrangements– Through promotional materials– Through statements by employees

Six Primary MCO Liability Risk Exposures

6. Business Disputes– Customers– Providers– Vendors

MCO Exposure Shift

• Bodily injury claims on the decrease

• Business practices claims on the increase

• Increase in class action claims

• High cost of antitrust claims

• Shift in defense vs indemnity dollars spent

Contact me at [email protected]

• MCO organization descriptions

• Article on historical managed care claim trends

• Managed Care claim scenarios

Technology and Information Risk Summary

Drew Bartkiewicz

Darwin Professional Underwriters

Darwin Professional Copyright 2007

Two markets related to technology

SoftwareHi Tech Services Consulting and ImplementationE-Business models$5M - $1B

Health CareFinancial ServicesRetailLarger clients but we limit coverage to

Internet and Cyber Liability

“Provider” / Tech E&O

“Users” in highly regulated IT environments

$800M market

$350M market growing fast

Darwin Professional Copyright 2007

In high compliance industries, there is a clear technology landscape for Insurance.

Builders Software product for others as primary business model (product liabilities)

Software product as an enabler or secondary business model (for their customers or partners).

Providers On site tech services for others as primary business model (integration, installation, professional liabilities)

Information-based services for others as added service (sending newsletters, reports, analysis). Have content and professional liabilities.

Operators Remote management of data, processes, applications as primary business model (privacy and security liabilities)

Aggregation of direct customer or patient data or hosted online application to support their primary business of medical or financial transactions (privacy and security liability)

Providers Users

Darwin Professional Copyright 2007

Every professional industry has changed

1. Improved professional efficiency2. Demand from customers for access and “self service”3. Compliance expectations4. Competitive mandate5. Financial requirements to drive better performance, aka

higher revenue / employee

Technology has become necessary to respond to:

A Business Imperative that every other industry has embraced.

Darwin Professional Copyright 2007

Professionals have their own IT networks

Professionals have centralized their data storage and servers

Professionals outsource certain IT intensive activities (storage, coding, hosting)

Professionals conduct business and processes via the Internet

Professionals are under required standards of care for information technology (HIPAA, state privacy laws, federal upcoming)

Professionals have placed IT security as a boardroom priority

A company’s balance sheet, liability, and reputation can be severely impacted by a technology wrongful act

The Risk Profile of professionals has shifted

Darwin Professional Copyright 2007

Example: risks of electronic customer or patient records

Improves documentation quality Facilitates better patient communication Provides built-in protocols and reminders Improves medication management

Increases concentration of risk for data privacy Increases the expense to notify and rectify Increases the expense to manage the PR fall outCreates new standards of care to process and protect dataCreates the next generation of class action suitsSpecific state and HIPAA standards exists to regulate how

hospitals operate electronically

Positive

Negative

Darwin Professional Copyright 2007

The Internet is also driving new liabilities

Email errorsWebsite incidents Improved communication and “patient

information”

Wrong online adviceWrong person accessing the data

(privacy)Wrong people sent the data (privacy) Infringement of other’s copyright and

trademarkLibel, slander, defamation via chat

rooms, blogs, advertising

Darwin Professional Copyright 2007

The typical costs associated with a technology incident

1. notification expense under regulatory requirements, state and federal - $$

2. crisis management expense- $

3. remediation expense / possible credit or ID monitoring expense - $$$

4. cyber investigation expense - $

5. fines, fees, or penalties - $$

6. defense against a regulatory or state investigation - $$$

7. defense against a class action / liability - $$$$

8. 3rd party damages (economic loss, mental anguish, damage to reputation, etc) - $$$$ ?

The average data privacy incident costs a traditional company $3M to $4M in direct and indirect expense.

Darwin Professional Copyright 2007

Difference between 1st party and 3rd party

1. 1st party loss of Income2. 1st party loss of Data3. Fines fees4. Notification Expense5. Compliance Expense6. Cyber Investigation7. Crisis Management8. Cyber Extortion

First Third

1. Class Action2. 3rd party3. ID Theft4. Media5. Transmission of

Virus6. 3rd party business

interruption7. Loss of Income to

third party

Contemplated by Tech//404

Darwin Professional Copyright 2007

Technology Wrongful Acts – Failure of a technology service or product (outsourcing, data processing, online scheduling, software) causes bodily harm or interrupts another organization’s business.

Data Privacy Wrongful Acts – Failure to protect patient data.

Network Security Wrongful Acts – Failure to prevent hospital interruption or hackers.

Internet / Content Wrongful Acts – Error in a hospitals online activities (libel, slander, privacy, defamation, advertising, intellectual property infringement).

This coverage is now available in Darwin’s TECH//404sm.

These changes have created new liabilities

Darwin Professional Copyright 2007

Summary

The diversity of accounts is a testament to the mass market appeal of this coverage

ID Theft and Data Privacy standards moving toward a national law

Hi-Tech represents 11% of the national GDP and is one of the fastest growing sectors. Insurance just now catching up

The Media is driving more awareness and concern through headlines of incidents

Darwin Professional Copyright 2007

Resources to help you sell…

www.tech-404.com for general education

Our Industry Specific sell sheets on www.darwinpro.com

Our articlesOur industry specific self-

assessmentsOur access on client visits

or client calls

Darwin Professional Copyright 2007

Drew Bartkiewicz

860-284-1456

Darwin Professional Underwriters

Questions

Contact:

Darwinism #8 regarding Information Currency

“Information thieves, black market buyers of data, and data brokers are definitive reference

points to suggest that information has surged as a

new resource, no longer protected by scarcity and

location, but unleashed with abundance and access.”

Questions and Answers

March 7, 2007