Embed Size (px)

DESCRIPTION

Health Care Reform Presented by Barb Gerken, Regional Sales Manager. Definitions. PPACA – Patient Protection and Affordable Care Act ACA – Affordable Care Act - PowerPoint PPT Presentation

Citation preview

Health Care Reform

Presented by Barb Gerken, Regional Sales Manager

Definitions

PPACA – Patient Protection and Affordable Care Act

ACA – Affordable Care Act

Grandfathered – those plans that existed on March 23, 2010, when the Patient Protection and Affordable Care Act (PPACA) was enacted with no “substantial changes”

HHS – Department of Health & Human Services

General Overview

Federal law enacted on March 23, 2010

Expected Benefits Expansion of access to health care coverage Reduce premium costs and make coverage affordable Prevent denials of care and coverage State or federal based mechanism for purchasing insurance Create standards in coverage

Grandfathering

Grandfathered – those plans (group and individual) that existed on March 23, 2010, when the Patient Protection and Affordable Care Act (PPACA) was enacted with no “substantial changes”

Grandfathered plans are permitted to make “routine” changes and still remain exempt from some of the provisions in PPACA.

“Routine” changes include adding new benefits; or making modest adjustments to employer contributions, premiums, co-payments and deductibles.

Grandfathering

A health plan can lose its grandfathered status if it:

Eliminates all or substantially all benefits to diagnose or treat a particular condition.

Increases deductibles or out-of-pocket limits by more than the rate of medical inflation plus 15 percentage points.

Example: Current deductible of $500, 15% change would be $575

Increases fixed copayment by more than the greater of medical inflation plus 15 percentage points or $5.

Grandfathering

A health plan can lose its grandfathered status if it:

Reduces the employer’s contribution rate so that the employer’s share of the total cost of coverage declines by more than 5% points below the contribution rate on March 23, 2010

Increases a percentage cost-sharing requirement above the level at which it was on March 23, 2010

Reduces the overall annual limit on the dollar value of benefits paid for covered services

Grandfathering

Grandfathered Plan MUST comply with the following reforms:

Summary of Benefits and Coverage

Reporting of Medical Loss Ratio and premium rebates if minimum loss ratio has not been met.

Prohibition on lifetime limits on essential benefits

Prohibition on health plan rescissions

Grandfathering

Grandfathered Plan MUST comply with the following reforms:

Dependent coverage offering to child until age 26

Prohibition on waiting periods greater than 90 days

Prohibition on coverage exclusions for pre-existing conditions

Grandfathering

Grandfathered Plan WILL NOT be required to comply with the following reforms:

Preventive care and immunization coverage at 100%

Cover emergency services without pre-authorization or increased cost-sharing out of network

Eliminate discrimination in favor of highly compensated employees

Grandfathering

Grandfathered Plan WILL NOT be required to comply with the following reforms:

Apply federal rating limitations (community rating)

Provide essential benefits in small group market

Cost Sharing and deductible limits

Grandfathering

Special Notes

New employees and members may add on to a plan without loss of grandfathering.

Union contracts in place as of March 23, 2010 will be considered grandfathered until the contract is renewed.

Groups changing insurance carriers between March 23, 2010 and November 15, 2010 lost grandfathered status.

Grandfathering

Special Notes

As of November 15, 2010 a change in carriers would not result in loss of grandfathering as long as all other criteria is met.

A change from self-insured to fully-insured will result in the loss of grandfathering.

Additions/Changes to Benefits

Effective with Plan Year on or afterSeptember 23, 2010

No lifetime dollar limits on benefits

Restricted annual dollar limits on essential health benefits

No pre-existing condition exclusions for children under 19

100% coverage for preventive services covered in network (not required for grandfathered group health plans)

Effective with new business and renewals after 8/1/2012

Includes expanded coverage for FDA-approved contraception methods

Initial guidance allowed a narrowly defined group of religious employers to choose not to cover contraceptives/sterilizations

Updates in 2012 allowed religiously affiliated groups allowed a one-year safe harbor for non-profit groups currently excluding contraceptive coverage

Effective August 1, 2012Expanded Coverage for Women’s Services

February, 2013 – HHS released additional guidance broadening definition of “religious” employers to include houses of worship, dioceses and affiliated organizations to be completely exempt using IRS tax code definition

Also allowed other “faith-based” employers to transfer the cost and administrative tasks of the birth control policies to insurance companies

Costs incurred by carriers and third party administrators would be offset by reduction in exchange fees

Effective August 1, 2012Expanded Coverage for Women’s Services

Effective August 1, 2012Expanded Coverage for Women’s Services

Following services covered at no-cost share when in-network:

Well woman visits (including prenatal visits)

Screening for gestational diabetes

Human papillomavirus (HPV) DNA testing

Counseling for sexually transmitted infections

Counseling for sexually transmitted diseases

Counseling for human immunodeficiency virus (HIV)

Screening and counseling for interpersonal and domestic violence

Breastfeeding support, supplies and counseling

Contraceptives

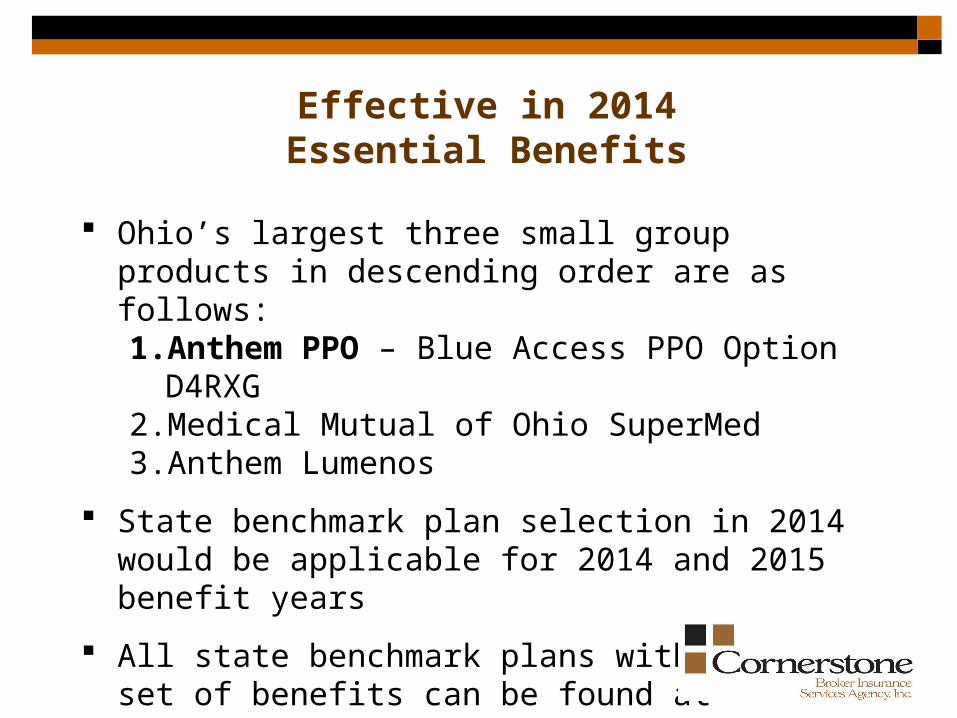

Effective in 2014Essential Benefits

Essential Benefits: A set of health care service categories that must be covered by certain plans beginning in 2014

Will apply to all non-grandfathered plans in the individual and small group market

Effective with plans year starting on or after January 1, 2014

Effective in 2014Essential Benefits

Recommendations based on a report released by the Institute of Medicine in October of 2011

Cited affordability and value as core concerns

Recommended that coverage be limited/excluded if following tests were not met:

Safe Medically effective Shows meaningful improvement Medical service Cost effective

Effective in 2014Essential Benefits

States had the option of choosing one of the following benchmark plans

one of three largest small group plans in the state

one of three largest state employee health plans

one of the three largest federal employee health plan options

largest HMO plan offered in the state’s commercial market

Effective in 2014Essential Benefits

Ohio’s largest three small group products in descending order are as follows:1. Anthem PPO – Blue Access PPO Option D4RXG2. Medical Mutual of Ohio SuperMed 3. Anthem Lumenos

State benchmark plan selection in 2014 would be applicable for 2014 and 2015 benefit years

All state benchmark plans with full set of benefits can be found at www.cciio.cms.gov

Effective in 2014Essential Benefits

PPACA requires that Essential Health Benefits include items and services in the following 10 categories

Ambulatory patient services Prescription Drugs

Emergency Services Rehabilitative and habilitative services and devices

Hospitalization Laboratory services

Maternity and newborn care Preventive and wellness services and chronic disease management

Mental Health and Substance Use Disorder Services, including behavioral health treatment

Pediatric services, including oral and vision care

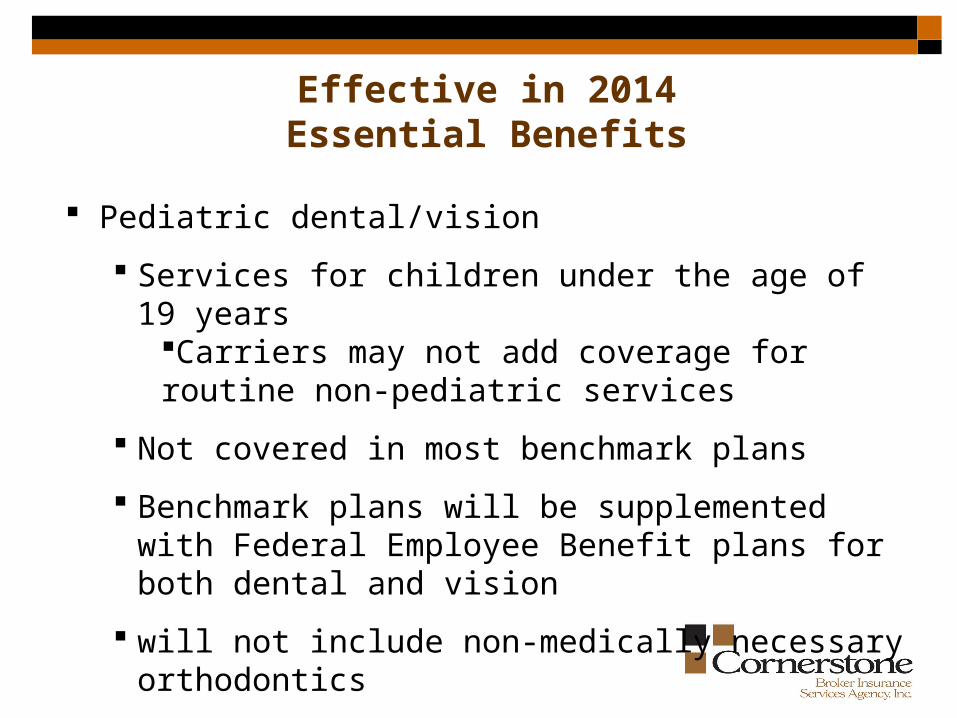

Effective in 2014Essential Benefits

Pediatric dental/vision

Services for children under the age of 19 yearsCarriers may not add coverage for routine non-pediatric services

Not covered in most benchmark plans

Benchmark plans will be supplemented with Federal Employee Benefit plans for both dental and vision

will not include non-medically necessary orthodontics

Effective in 2014Essential Benefits

Mental Health

Benchmark plans must comply with mental health and substance abuse parity standards outlined in 45 CFR 146.136

States will not be required to defray cost of this parity

Effective in 2014Essential Benefits

Prescription Drug Benefits

Will require at least one drug in every United States Pharmacopeia’s (USP) category and class or

The same number of prescription drugs in each category and class as the benchmark plan

Does not require that drugs be covered in a particular tier

Will require a procedure for enrollees to request clinically appropriate drugs not covered by the health plan

Effective in 2014Essential Benefits

Carriers will be require to submit drug lists to:

Exchange – plans sold in the public exchange

State – plans sold in the private market

Office of Personnel Management – multi-state plans

Effective in 2014Essential Benefits

No annual dollar limits applies to all plans except grandfathered individual plans

Stand-alone dental plans would have separate annual limitations on cost sharing from qualified health plans covering the remaining Essential Health Benefits

plan must demonstrate that separate limit is reasonable for coverage of the pediatric dental plan

Effective in 2014Essential Benefits

Maximum deductible of $2,000/$4,000 - small group only does not apply to individual, large group or self-insured markets cannot use FSA, HRA or HSA dollars to offset this maximum carriers may exceed the annual deductible limit if they cannot reasonably reach a given level of coverage without doing so

Effective in 2014Essential Benefits

Maximum out-of-pocket (cost-sharing) tied to the annual limitation on cost sharing for high deductible plans ($6,250/$12,500 – 2013)

does not apply to grandfathered health plans will apply to large groups and self-insured plans

Carriers would be prohibited for any plan design that would discriminate based on age, life expectancy, disability, medical dependency, quality of life or other health condition

Effective in 2014Essential Benefits

States may require a qualified health plan to cover additional benefits

States will be required to defray the cost of these additional benefits if enacted after December 31, 2011

Will allow states to base payment on either statewide average or each issuer’s actual cost

Payments will be made to either the enrollee or to the carrier

Effective in 2014Essential Benefits

Network adequacy requirements are not in the scope of this regulation

Carriers may use prior authorization and other medical management techniques as long as they are not used to discriminate

Effective in 2014

Actuarial Value (AV)

Refers to value of coverage in the SMALL group market

Measure of % of expected health care costs a health plan will cover

Will use national calculator with a single standardized dataset for 2014. Will revert to state data in 2015

Effective in 2014

Actuarial Value (AV)

Will use value of in-network services only

Deductible, co-insurance, out-of-pockets to have large impact on actuarial value

Cost-sharing for emergency rooms, inpatient admissions and diagnostic imaging to have smaller impact on actuarial value

Benefits not compatible with the calculator will provide documentation of actuarial certification

Effective in 2014

Actuarial Value (AV)

Annual employer contributions to HSA account will be included in the AV calculation

Amounts newly made available under an HRA for the current year will be included in the AV calculation

Value will be based on in-network utilization only

Effective in 2014

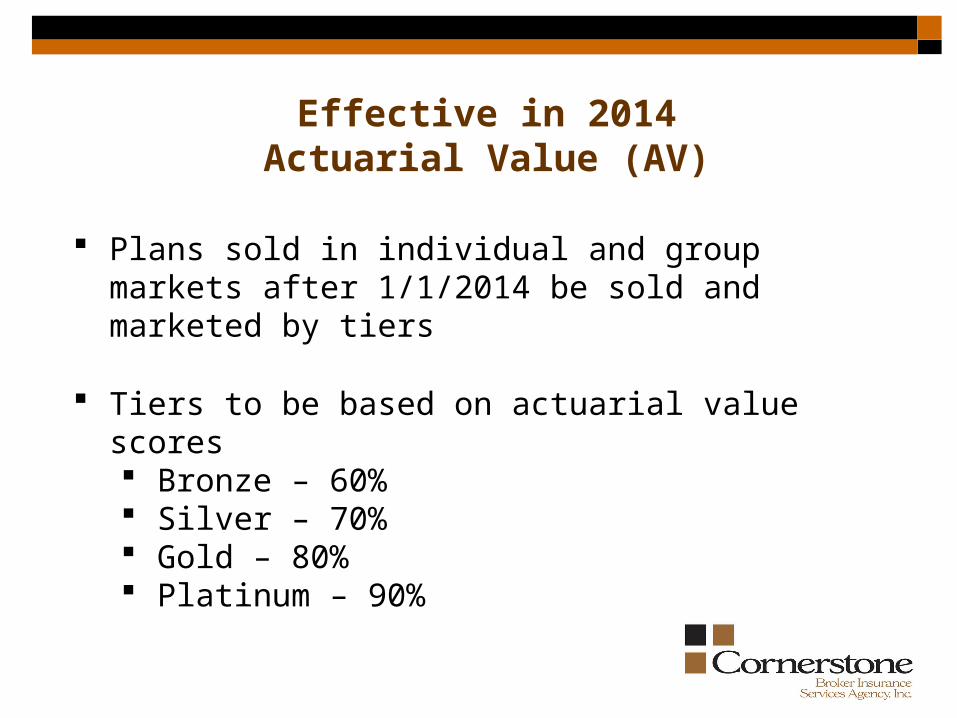

Actuarial Value (AV)

Plans sold in individual and group markets after 1/1/2014 be sold and marketed by tiers

Tiers to be based on actuarial value scores Bronze – 60% Silver – 70% Gold – 80% Platinum – 90%

Effective in 2014Actuarial Value (AV)

Will allow for variations of +/- 2 percentage points i.e. Silver plan may have actuarial value of 68-72%

Effective January 1, 2014

Guarantee Issue

Considering “Mandate Plus” language to encourage enrollment at time of first eligibility

No Pre-Existing Conditions Clause for Adults

Removal of annual and lifetime dollar limits on ALL plans (including grandfathered)

Administrative Changes

Effective with Plan Year on or afterSeptember 23, 2010

Dependent Age

Adult children coverage to age 26, end of birth month.

Dependent:

May be eligible for their own employer sponsored plan

May be eligible for Medicare/Medicaid

May be married

Many carriers allowed early adoption of provisions

Effective with Plan Year on or afterSeptember 23, 2010

Dependent Age

Not required for grandfathered groups before 2014 if the dependent is eligible for employer-sponsored coverage

Employer may not charge more or have different benefit structure for dependents based on age

Effective with Plan Year on or afterSeptember 23, 2010

Dependent Age – Ohio Law

Adult children coverage to age 28, end of birth month.

Dependent: Unmarried Resident of Ohio or full-time student Not eligible for employer-sponsored coverage Not eligible for government-sponsored coverage

Additional costs may be charged to the employee

Effective with Plan Year on or afterSeptember 23, 2010

Dependent Age – Ohio Law

State law does NOT apply to self-insured plans governed by ERISA

Will apply to non-ERISA self-funded groups (public employers, government entities, etc.)

Most carriers will require an affidavit

Effective with Plan Year on or afterSeptember 23, 2010

No discrimination in favor of highly compensated employees Delayed until further notice

Effective in 2014

Small group redefined as 1-100

State have option of leaving as 2-50 for 2014 & 2015

Mandated as 1-100 as of 2016

New Taxes / Rating Changes

Effective October 1, 2012

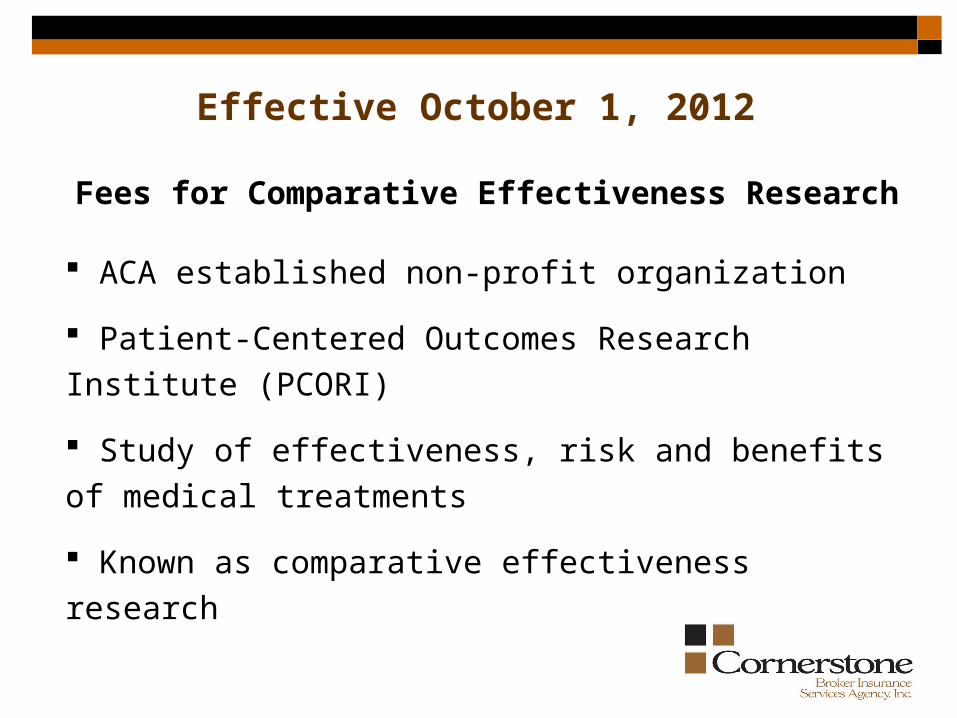

Fees for Comparative Effectiveness Research

ACA established non-profit organization

Patient-Centered Outcomes Research Institute (PCORI)

Study of effectiveness, risk and benefits of medical treatments

Known as comparative effectiveness research

Effective October 1, 2012

Fees for Comparative Effectiveness Research

Supported by a trust fund

Financed in part from fees from health issuers and plan

sponsors

Fees to be collected for plan and policy years that end after

September 30, 2012 and before October 1, 2019

Calculation of fees based on average # of lives covered by

accident and illness insurance during year

Effective October 1, 2012

Fees for Comparative Effectiveness Research

Does not apply to dental and vision plans

Applies to individual and group plans regardless of funding

Carriers will pay fee for fully insured customers included as part of medical premium

Effective October 1, 2012

Fees for Comparative Effectiveness Research

The fee is considered an excise tax and will be filed on IRS Form 720

Carriers will pay fee for fully insured customersincluded as part of medical premium

Self-insured (ASO) groups will file the Form 720 and pay the appropriate fee

Fee is due by July 31 of calendar year immediately following last day of plan year

Effective October 1, 2012

Fees for Comparative Effectiveness Research

Plan/Policy years ending

October 1, 2012 -9/30/2013

Plan/Policy years ending

10/1/2013 -9/30/2014

Plan/Policy years ending

10/1/2014 -9/30/2019

$1 multiplied by average # of covered lives ($1 per year)

$2 multiplied by average # of covered lives ($2 per year)

$2 (adjusted for medical inflation) multiplied by average # of covered lives ($2 adjusted per year)

Effective in 2014

Insurer Fee

Annual fee on health insurance providers based on their market share of net premiums written, or the sum of premiums earned for all policies during previous years

To offset a portion of the expenses related to premium subsidies and tax credits for individuals purchasing coverage through the exchanges

Fee is due by September 30 of following calendar year

Impact to be approximately 2.46% of premium

Effective in 2014

Insurer Fee

Total fee amount to be collected from all carriers is set at $8 billion in 2014, $11.3 billion in 2015 and 2016, $13.9 billion in 2017 and $14.38 billion in 2018.

After 2018, fee will increase based on premium growth

Fee applies to medical, dental and vision plans

Applies to fully insured customers – not self-insured

Fee is not tax deductible

Effective in 2014

Transitional Reinsurance Fee

To help stabilize premiums for coverage in the individual market during the years 2014 through 2016

All health insurers and TPAs, on behalf of their self-insured group health plans, will submit contributions to support reinsurance payments to issuers covering high-cost individuals in non-grandfathered individual market plans

Aggregate fee of $25 billion over the next three-year period

Effective in 2014

Transitional Reinsurance Fee

Applies to both fully insured and self-insured plans

Current fee is estimated at $6.35 per participant per month

Rating Changes

Effective with new business and renewals after January 1, 2014

Applies to individual and small group market segments

Based on community rating Age (highest age band no more than 3x lowest) Tobacco use (rate for users no more than 1.5x non-

users) Geography Family tier

Effective in 2018

40% excise tax on high cost Cadillac plans

• Insurers to pay tax on any amount over $10,200 – Single and $27,500 – Family annual premium

• 50% of business are anticipated to be affected

• Will not index with inflation

• Current premiums will be affected by several factors (community rating, minimum deductible, 4 years of increases, etc.)

IRS Tax Changes / Miscellaneous Changes

Effective January 1, 2011Medical Loss Ratio - MLR

Applies to individual and fully insured group coverages

(including grandfathered groups)

Does not apply to self-insurance plans

Requires health plans to report the proportion of premium dollars spent on clinical services, quality service and other costs

Effective January 1, 2011Medical Loss Ratio - MLR

Medical Loss ratio standards 80% for small group and individual 85% for large group

Must provide rebates if the share of premium spent is less than set percentages

Effective January 1, 2011Medical Loss Ratio - MLR

Began with coverages purchased in 2011 with rebates issued to enrollees by August of the following year

1st round of payments began in August, 2012

Average rebate of $157 for 2011 reporting year

Rebates to Enrollees in Group Markets

Rebates to be provided to group policyholder for

distribution

Carriers must provide rebates to policyholder covered

during the MLR reporting year on which the rebate is based

Effective January 1, 2011Medical Loss Ratio - MLR

Rebates to Enrollees in Group Markets

Carrier must provide notice of rebate to both policyholder and

subscribers

Notice must contain explanation that the policyholder must

agree to use portion of rebate attributable to subscriber

contribution to premium for the benefit of current subscribers

Effective January 1, 2011Medical Loss Ratio - MLR

Rebates to Enrollees in Group Markets

Initial rule only required notification from issuers who did owe rebates

Guidance released in August 2012 required notice from carriers whether or not MLR has been met

Notice from carriers who meet or exceed standards only required to provide notice for 2011 reporting period

Effective January 1, 2011Medical Loss Ratio - MLR

Rebates to Enrollees in Group Markets

Carriers who meet or exceed standards not required to include current or prior year MLR

Notices must direct enrolled to HHS website for specific information on carrier MLRs

Effective January 1, 2011Medical Loss Ratio - MLR

Rebates to Enrollees in Group Markets

Groups subject to ERISA - rebates to policyholder may have

plan asset, fiduciary responsibility and prohibited transaction

implications under Title 1 of ERISA

Decisions regarding the handling and allocation of the rebates

should be made by plan fiduciary consistent with ERISA

Effective January 1, 2011Medical Loss Ratio - MLR

Rebates to Enrollees in Group Markets

Rebates must be sent to policyholder and must provide appropriate % of subscriber premium contribution

i.e. rebate of $20,000 due to group and employee pays 40% of premium…$8,000 must be used for benefit of subscriber

Effective January 1, 2011Medical Loss Ratio - MLR

Rebates to Enrollees in Group Markets

Rebate can be used in several ways:

refund to subscriber covered by group health policy in form of cash, reimbursement to enrollee credit card or direct payment to enrollee bank account

this option should be used if the rebate is larger than 90 days worth of premium this rebate option will result in a taxable income amount to the employee

Effective January 1, 2011Medical Loss Ratio - MLR

Rebates to Enrollees in Group Markets

Rebate can be used in several ways:

reduce subscriber portion of annual premium for subsequent policy year (“premium holiday”)

enhancement of benefits

programs to improve member health

Effective January 1, 2011Medical Loss Ratio - MLR

Rebates to Enrollees in Group Markets

Private plans also need to understand that the DOL has interpreted ERISA to require that participant monies in private employer plans be put into a trust within 90 days after they arereceived. Very few insured plans operate through a trust, so it would be a burden to create a trust due to delays in dispensing the rebates. To avoid the 90-day rule, private plans should take steps to use or pay out the rebate within 90 days after it is received.

Effective January 1, 2011Medical Loss Ratio - MLR

2011 MLR Reporting Period Results

HHS indicates $1.1 billion in rebates distributed in July to 12.8 million consumers

Less than 10% of the private health insurance consumers

Average rebate to be $151.

Aetna – Met in all division, UHC – Ohio – met all but River Valley products in individual and large group, Anthem – met in small and large group markets, but not individual

Effective January 1, 2011Medical Loss Ratio - MLR

Effective January 1, 2011

Prescription required for over-the-counter medications under health care reimbursements

20% tax for non-qualified HSA withdrawals

Effective in 2013Employer Notification Guidelines

Medicare Tax Increase New 3.8% Medicare contribution on certain unearned

income from high-income individuals

Itemized deductions for Medical Expenses –

Increases from 7.5% - 10% of adjust gross income

Waives increase for individuals 65 and older for tax years 2013 through 2016

Shared Responsibility Payment for Not Maintaining Minimum Essential Coverage

Proposed Regulations released February 2013

90 day comment period

Comments need to be received by May 2, 2013

Public hearing scheduled for May 29, 2013

Individual Mandate

Requires individuals requires a non-exempt individual to maintain minimum essential coverage or make a shared responsibility payment

Payment would be included with Federal income tax return

Effective January 1, 2014

Payments will be assessed on a monthly basis

Taxpayer is responsible for the payment for any claimed dependents

Individual Mandate

Member of a recognized religious sect or a division thereof and is adherent to the tenets or teachings of the sect

1. Has established tenets or teachings for which members/adherents are conscientiously opposed to acceptance of benefits of any private or public insurance

2. Maintains, and has maintained for a substantial period of time, practice whereby its members make provision for its dependent members that is reasonable in view of their general level of living

3. Has been in existence since December 31, 1950

Individual Mandate - Exemptions

Member of a health care sharing ministry

1. Described in Section 501(c)(3) and exempt from tax under Section 501(a)

2. Members of which share a common set of ethical or religious beliefs and share medical expenses amongst themselves regardless of the State in which member resides or is employed

3. Members retain membership even after the develop a condition

Individual Mandate - Exemptions

Member of a health care sharing ministry (cont.)

4. Been in existence since December 31, 1999

5. Members have continuously, and without interruption, shared medical expenses since December 31, 1999

6. Conducts an annual audit performed by an independent certified public accounting firm with reports made available to members

Individual Mandate - Exemptions

An individual who is not a citizen or who is an illegal alien

Incarcerated individuals (except those pending disposition of charges)

Individual Mandate - Exemptions

Individual lacking access to affordable minimum essential coverage

Required contribution exceeds a percentage (8% for 2014) of the individual’s household income

Household income = sum of taxpayer’s and claimed dependents’ modified adjusted gross incomes

Modified AGI = calculated by adding back certain items to your Adjusted Gross Income.

Individual - Exemptions

An individual who’s household income is less than required to file taxes

Member of an Indian tribe Includes Federally recognized Indian tribes as listed

in the Indian Entities Recognized and Eligible to Receive Services from the United States Bureau of Indian Affairs

An individual suffering a hardship (rules to be developed)

Individual Mandate - Exemptions

All exemptions based on affordability are based on the household income for the year for which an exemption is being claimed

A certificate of exemption issued by an Exchange is required in order for the exemption to be recognized

Individual MandatesNotes on Exemptions

Assessed on a monthly basis. Penalty of 1/12 of the greater of the following amounts:

1. Flat dollar amount

2. Percentage of income

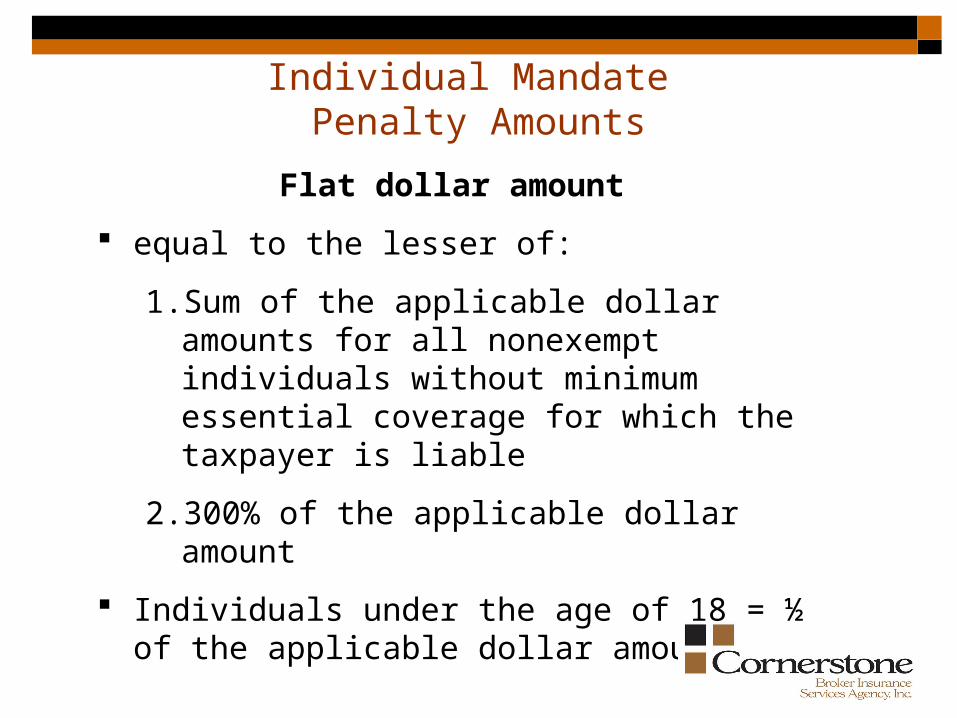

Individual MandatePenalty Amounts

Flat dollar amount

equal to the lesser of:

1. Sum of the applicable dollar amounts for all nonexempt individuals without minimum essential coverage for which the taxpayer is liable

2. 300% of the applicable dollar amount

Individuals under the age of 18 = ½ of the applicable dollar amount

Individual Mandate Penalty Amounts

Flat dollar amount

$95 for 2014

$325 for 2015

$695 for 2016

Will increase by cost-of-living adjustments after 2016

Individual Mandate Penalty Amounts

Exchanges – Marketplaces

An exchange is a marketplace for consumers to compare apples to apples plan designs and elect coverages

Exchanges can be public or private

Private exchanges have been in existence for many years

The exchanges proposed under the Affordable Care Act have many eligibility requirements and regulations

Exchanges – Marketplaces

Exchanges will be available to certain individuals and also to groups (under the SHOP) program

All U.S. citizens are eligible to purchase coverage in the public exchanges

Subsidies will be available for both premiums and for out-of-pocket costs based on income levels

Exchanges – Marketplaces

States had option to elect to run their own exchange, partner with the federal government or turn it over to the federal government (Federal Fallback Exchange (FFE))

Ohio has elected the FFE Ohio will retain the oversight function with regards to carriers and brokers – certifications, licensing, rate reviews

Exchanges – Marketplaces

As of May, 2013

Exchanges – Marketplaces

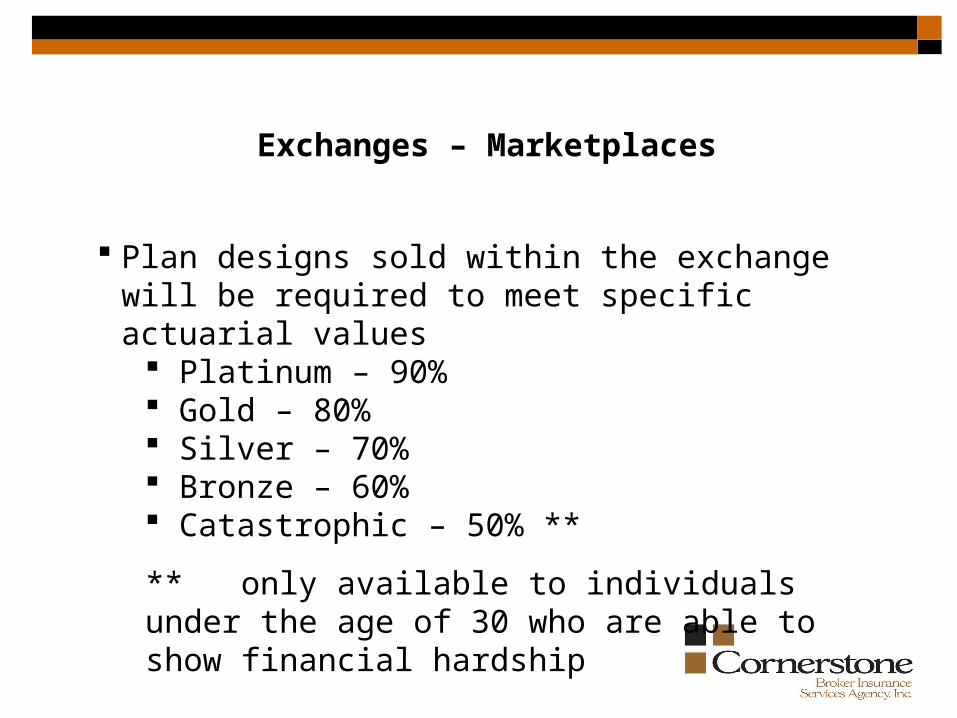

Plan designs sold within the exchange will be required to meet specific actuarial values

Platinum – 90% Gold – 80% Silver – 70% Bronze – 60% Catastrophic – 50% **

** only available to individuals under the age of 30 who are able to show financial hardship

Exchanges – Marketplaces

Plans sold in the exchange will also be required to:

include the essential health benefits

provide minimum of 60% actuarial value

be certified by the exchange

allow for subsidies based on income levels

Exchanges – Marketplaces

Plans sold in the exchange will also be required to:

include the essential health benefits

provide minimum of 60% actuarial value

be certified by the exchange

allow for subsidies based on income levels available only on the Silver level plans

Exchanges – MarketplacesFederal Poverty Levels

48 Contiguous States and DCNote: The 100% column shows the federal poverty level for each family size, and the percentage columns

that follow represent income levels that are commonly used as guidelines for health programs.

Household Size 100% 133% 150% 200% 300% 400%

1 $11,490 $15,282 $17,235 $22,980 $34,470 $45,960

2 15,510 20,628 23,265 31,020 46,530 62,040

3 19,530 25,975 29,295 39,060 58,590 78,120

4 23,550 31,322 35,325 47,100 70,650 94,200

5 27,570 36,668 41,355 55,140 82,710 110,280

6 31,590 42,015 47,385 63,180 94,770 126,360

7 35,610 47,361 53,415 71,220 106,830 142,440

8 39,630 52,708 59,445 79,260 118,890 158,520

For each additional person, add

$4,020 $5,347 $6,030 $8,040 $12,060 $16,080

Exchanges – Marketplaces

Individual Premium Contribution Based on Income

Income (individual) Minimum Premium Contribution

FPL (2013 guidelines)

Annual dollar amount Annual percent of income

Annual dollar amount

100-150% $11,490-$17,235 2-4% $229.80-$689.40

150-200% $17,235-$22,980 4-6.3% $689.40-$1,447.74

200-250% $22,980-$28,725 6.3-8.05% $1,447.74-$2,312.36

250-300% $28,725-$34,470 8.05-9.5% $2,312.36-$3,274.65

300-400% $34,470-$45,960 9.5% $3,274.65-$4,366.20

Actuarial Value (Generosity of Plan) Based on Income

Income (individual) Actuarial Value of Coverage

FPL Annual dollar amount Percent

100-150% $11,490-$17,235 94%

150-200% $17,235-$22,980 87%

200-250% $22,980-$28,725 73%

250-300% $28,725-$34,470 70%

300-400% $34,470-$45,960 70%

Exchanges – Marketplaces

Exchanges – Marketplaces

Exchange responsibilities include: Consumer assistance Enrollment Eligibility Financial Management Plan Management QHP selections

Exchanges – Marketplaces

Consumer assistance will be provided by: Navigators In-Person Assisters Enrollers Brokers/Agents

Exchanges – Marketplaces

Navigators

Conduct public education activities to raise awareness of availability of coverage through the exchange

Distribute information concerning enrollment in QHPs and the availability of tax credits and cost-sharing reductions

Facilitate enrollment

CANNOT recommend plan designs or discuss details of the benefits

Exchanges – Marketplaces

Navigators

Will be required to complete training programs related to the duties outlined

Cannot accept payment in any form from an insurance company or stop loss carrier

Will not be required to carry E&O coverage

To Do List

Effective January 1, 2010Small Group Tax Credit

Available to employers with no more than 25 full-time equivalent employees

Average annual wages less than $50,000

Employer sponsored coverage offered with minimum of 50% employer contribution

Effective January 1, 2010Small Group Tax Credit

For-profit groups: tax credit up to 35% of employer cost in years 2010-2013

Increases to 50% in 2014

Non-profit groups: tax credit up to 25% of employer cost in years 2010-2013

Increases to 35% in 2014

Effective January 1, 2010Small Group Tax Credit

Designed to encourage small businesses to offer heath care coverage for the first time or to help them maintain coverage

Available to for-profit and non-profit organizations

Will only be available 2014-2016 if group coverage is purchased through the public exchange (SHOP)

Effective January 1, 2010Small Group Tax Credit

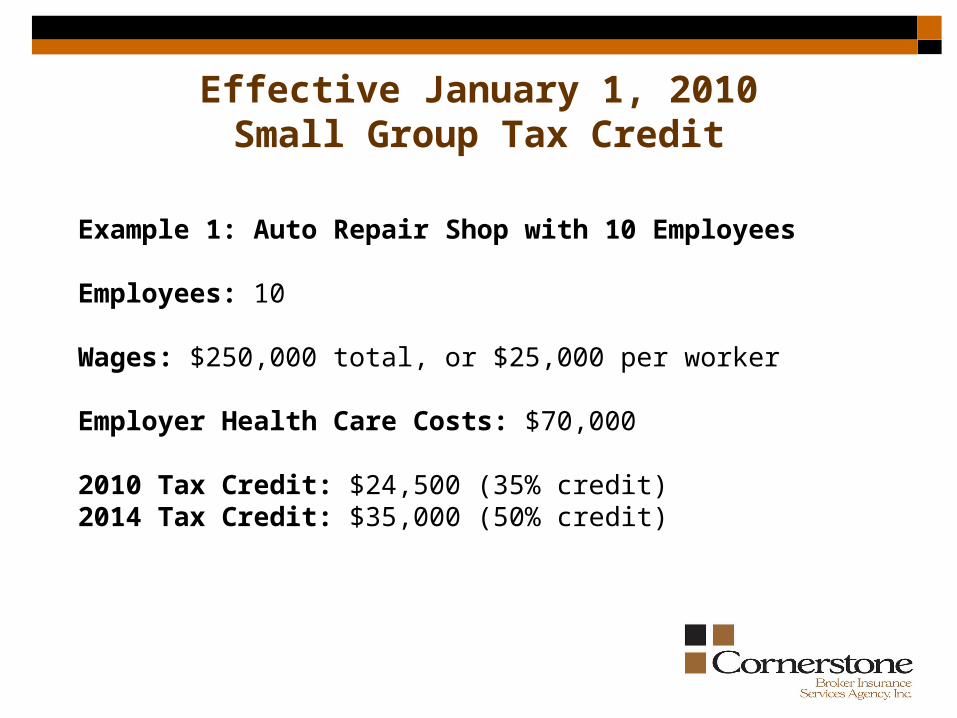

Example 1: Auto Repair Shop with 10 Employees

Employees: 10

Wages: $250,000 total, or $25,000 per worker

Employer Health Care Costs: $70,000

2010 Tax Credit: $24,500 (35% credit)2014 Tax Credit: $35,000 (50% credit)

Effective January 1, 2010Small Group Tax Credit

Example 2: Foster Care Non-Profit with 9 EmployeesFirst Street Family Services.org:

Employees: 9

Wages: $198,000 total, or $22,000 per worker

Employer Health Care Costs: $72,000

2010 Tax Credit: $18,000 (25% credit)2014 Tax Credit: $25,200 (35% credit)

Effective Date – plan year on or after September 23, 2012

General Requirements:

Health insurer is required to create and deliver summary of coverage and benefits to consumers shopping for coverage.

No one is exempt – individual and groups regardless of size and/or funding arrangement

Summary of Benefits and CoverageMaterial Modification Notice

General Requirements (cont.):

Summary can be up to four pages front and back

Electronic delivery is permitted. Different rules apply for individual, fully insured or ASO group

Can be included in SPD – must be intact and prominent

Summary of Benefits and CoverageMaterial Modification Notice

Delivery Requirements:

Group renewal – must be delivered no later than 30 days prior to renewal

Open enrollment period – must receive SBC with other open enrollment materials but no later than the first day of open enrollment

Benefit change – provide ASAP but no later than 7 days after renewal is issued or written confirmation of intent to renew is sent

New applications – with application/enrollment materials but no later than 7 days after application

Special enrollments – within 90 days of enrollment

Summary of Benefits and CoverageMaterial Modification Notice

Requires plan sponsors or issuers to provide 60 days advance notice to enrollees when making material modifications to the plan.

Does not apply to renewal changes

Duty can be satisfied by providing either a separate notice describing material modification or an updated coverage summary.

Plan issuers or sponsors who willfully fail to provide timely notice will be subject to a fine of $1,000 per enrollee

Summary of Benefits and CoverageMaterial Modification Notice

Must be provided in culturally and linguistically appropriate manner

If 10% or more of population in claimants county are literate in only the same non-English language

Determined by the American Community Survey data

Currently 255 U.S. Counties meet threshold78 in Puerto Rico

Summary of Benefits and CoverageMaterial Modification Notice

W2 Reporting

Section 6051(a) was added to the US Tax Code through PPACA

Required for 2012 W-2 Forms

Employer must report the aggregate cost of applicable employer-sponsored coverage

Applicable coverage = coverage under any group health plan made available to the employee by an employer which is excludable from the employee’s gross income

Additional interim guidance released by IRS on

January 3, 2012

Confirms that employers filing less than 250 W-2s are

not subject to requirement until further notice

does not impact employees’ taxable wages

W-2 Reporting

Doesn’t include coverage for:

On-site medical clinics Worker’s Compensation

Credit Only Insurance Long Term Care Insurance

Accident only/disability coverage Auto Medical Payment Insurance

General/Auto liability insurance Hospital Indemnity Insurance

Specified Disease or Illness Policy Fixed Indemnity Insurance

Dental/vision plans independent of the medical plan

W-2 Reporting

Does not apply to Archer MSA or health savings account contributions

Does not apply to the amount of any salary reduction contributions to a health flexible spending arrangement

W-2 Reporting

W-2 Reporting

Cost is reported on Form W-2 in Box 12, using code DD

Employer may apply any reasonable method of reporting cost of coverage for terminated employee

Should include costs for employee and any dependent covered under group plan

COBRA costs are included

Effective in 2013

Effective in 2013

Employer Notification Guidelines Employer to notify employee regarding health

insurance exchanges and availability of premium subsidies

Medicare Payroll Tax Increase Employers to withhold an additional 0.9% in Medicare

tax on employee wages in excess of $200,000

Effective in 2013

Flexible Spending Account Contribution Limits

New limits to health care spending account contributions

$2,500 per year

To be adjusted annually for cost of living

Questions