Embed Size (px)

Citation preview

Kristin Gorski, Director, The Nielsen CompanySeptember 20, 2015

HEALTH CARE AND INDUSTRY TRENDS

2

Co

pyr

igh

t ©

2015

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

AGENDA

U.S. Retail Hot Buttons: December 19, 2014

1. Retail/CPG Industry Overview

2. Private Label Overview

3. Population & Demographic Trends

4. Health Care Category Performance

5. Digital Shopping & Digital Retailing

6. Health & Wellness Trending

7. Key Takeaways & Closing Thoughts

INDUSTRY OVERVIEW

Co

pyr

igh

t ©

2015

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

4

RETAIL HOT BUTTONS

Price & Value

Winning with Non-Edibles

Food Fight

Health & Wellness

Private Brands

Sustainability

Right-Sized Box

Experiential Retailing

Connecting with Shoppers That Matter

Digital Shopping

Co

pyr

igh

t ©

2015

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

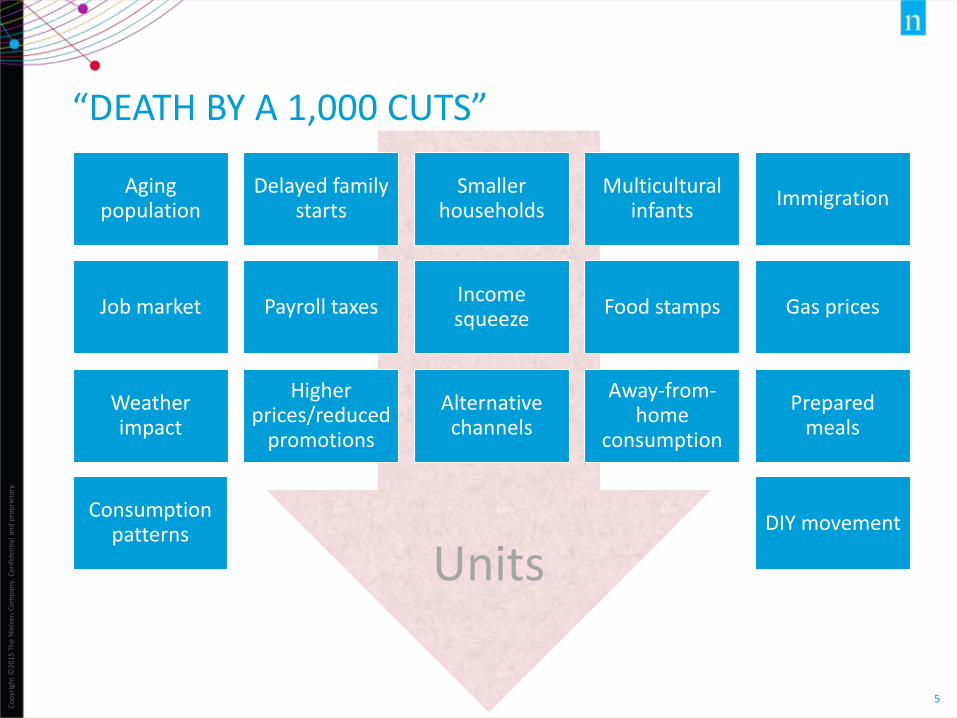

5

Units

“DEATH BY A 1,000 CUTS”

Aging population

Delayed family starts

Smaller households

Multicultural infants

Immigration

Job market Payroll taxesIncome squeeze

Food stamps Gas prices

Weather impact

Higher prices/reduced

promotions

Alternative channels

Away-from-home

consumption

Prepared meals

Consumption patterns

DIY movement

Co

pyr

igh

t ©

2015

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

6

CONVENIENCE & VALUE WINNING, BUT NOT MUCH GROWTH GAP BETWEEN VALUE & SUPERMARKETSAll Departments – Dollar Sales & Trend

Source: Nielsen Answers, Total U.S., 52 weeks ending 06/27/2015 (vs. year ago); *Club Stores, Dollar Stores, Mass-Merchandisers, Supercenters, & Military

1.9%

0.1%

4.2%

2.8%

$0

$50

$100

$150

$200

$250

$300

$350

$400

Bill

ion

s Supermarkets

C-Stores

Drug Stores

Value*

Low Growth High Growth

Total measured channels: $811 Billion & up 2.5%

UPC-coded items

Co

pyr

igh

t ©

2015

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

7

CONVENIENCE & VALUE DRIVE STORE EXPANSION

Source: Nielsen TDLinx

152,794

41,799

33,566

26,572

3,886

4,150

1,320

Convenience

Drug

Supermarkets $2MM+

Dollar Stores

Mass Merch

Supercenters

Warehouse Clubs2014

Expansion from all formats but Mass Merchandisers in 2014 vs. previous year

U.S. Store Counts

72% + of growth from niche formats

Value & Convenience

vs. 2005

8

Co

pyr

igh

t ©

2015

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

Household Income

% of Households 30 34 36

RETAIL PERFORMANCE LINKED TO SPENDING POWER OF SHOPPERS

Source: Nielsen Homescan, Total U.S., excludes gas only or Rx only trips, 52-weeks ending 12/27/2014

24%

12%

17%

18%

24%

24%

29%

28%

46%

33%

28%

30%

31%

31%

33%

33%

36%

33%

44%

60%

53%

50%

46%

43%

38%

36%

21%

Total Outlets

Club

Pet

HHI

Online

Grocery

Drug

Mass

Dollar

$29k or less $30 - $69.9k $70k +

Share of Basket Ring Dollar Sales by Household Income

Co

pyr

igh

t ©

2015

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

9

INFLATION & DEMAND DRIVING GROWTH

Source: Nielsen Answers, Total U.S. – All Outlets Combined (plus Convenience), 52 weeks ending 06/27/2015 (vs. year ago), UPC-coded

2%-2%

1%1%

1%2%

2%2%

2%3%

3%4%

5%5%

6%7%

Total All DepartmentsGeneral Merchandise

Frozen FoodsPet Care

Tobacco & AlternativesHousehold Care

GroceryBakery

Beauty CarePersonal Care

DairyAlcohol

DeliProduce

Health CareMeat

All departments except General Merchandise growing

All Outlets Combined (plus Convenience) – Dollar Trend

UPC-coded items

10

Co

pyr

igh

t ©

2015

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

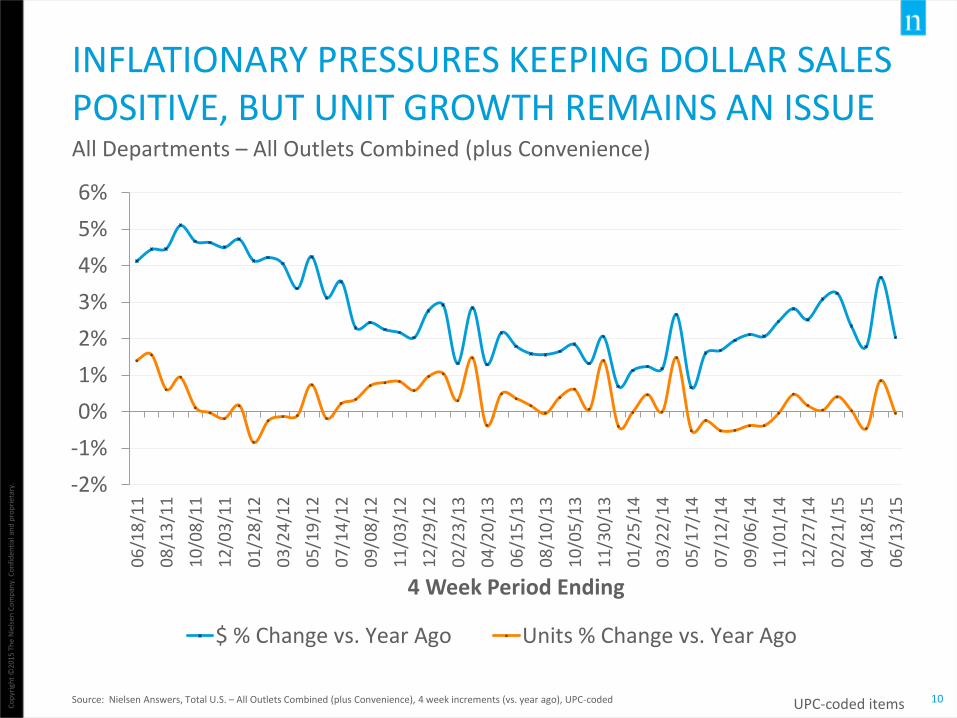

INFLATIONARY PRESSURES KEEPING DOLLAR SALES POSITIVE, BUT UNIT GROWTH REMAINS AN ISSUE

Source: Nielsen Answers, Total U.S. – All Outlets Combined (plus Convenience), 4 week increments (vs. year ago), UPC-coded

-2%

-1%

0%

1%

2%

3%

4%

5%

6%

06

/18

/11

08

/13

/11

10

/08

/11

12

/03

/11

01

/28

/12

03

/24

/12

05

/19

/12

07

/14

/12

09

/08

/12

11

/03

/12

12

/29

/12

02

/23

/13

04

/20

/13

06

/15

/13

08

/10

/13

10

/05

/13

11

/30

/13

01

/25

/14

03

/22

/14

05

/17

/14

07

/12

/14

09

/06

/14

11

/01

/14

12

/27

/14

02

/21

/15

04

/18

/15

06

/13

/15

4 Week Period Ending

$ % Change vs. Year Ago Units % Change vs. Year Ago

All Departments – All Outlets Combined (plus Convenience)

UPC-coded items

11

Co

pyr

igh

t ©

2015

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

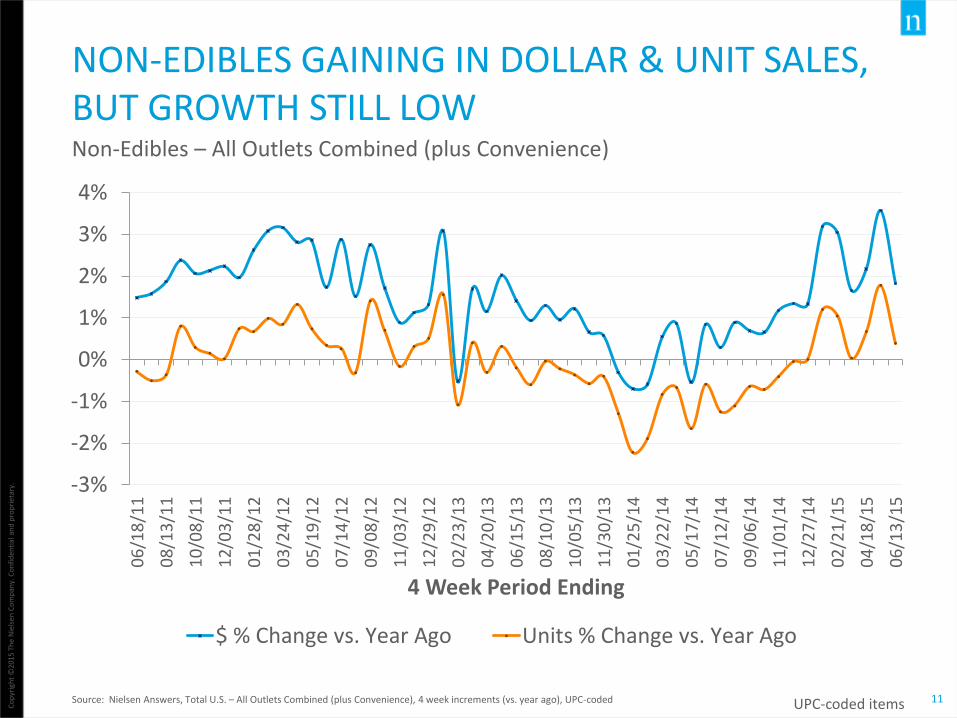

NON-EDIBLES GAINING IN DOLLAR & UNIT SALES, BUT GROWTH STILL LOW

Source: Nielsen Answers, Total U.S. – All Outlets Combined (plus Convenience), 4 week increments (vs. year ago), UPC-coded

-3%

-2%

-1%

0%

1%

2%

3%

4%

06

/18

/11

08

/13

/11

10

/08

/11

12

/03

/11

01

/28

/12

03

/24

/12

05

/19

/12

07

/14

/12

09

/08

/12

11

/03

/12

12

/29

/12

02

/23

/13

04

/20

/13

06

/15

/13

08

/10

/13

10

/05

/13

11

/30

/13

01

/25

/14

03

/22

/14

05

/17

/14

07

/12

/14

09

/06

/14

11

/01

/14

12

/27

/14

02

/21

/15

04

/18

/15

06

/13

/15

4 Week Period Ending

$ % Change vs. Year Ago Units % Change vs. Year Ago

Non-Edibles – All Outlets Combined (plus Convenience)

UPC-coded items

12

Co

pyr

igh

t ©

2015

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

HEALTH CARE CATEGORIES ON RIGHT TREND

Source: Nielsen Answers, Total U.S. – All Outlets Combined (plus Convenience), 4 week increments (vs. year ago), UPC-coded

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

06

/18

/11

08

/13

/11

10

/08

/11

12

/03

/11

01

/28

/12

03

/24

/12

05

/19

/12

07

/14

/12

09

/08

/12

11

/03

/12

12

/29

/12

02

/23

/13

04

/20

/13

06

/15

/13

08

/10

/13

10

/05

/13

11

/30

/13

01

/25

/14

03

/22

/14

05

/17

/14

07

/12

/14

09

/06

/14

11

/01

/14

12

/27

/14

02

/21

/15

04

/18

/15

06

/13

/15

4 Week Period Ending

$ % Change vs. Year Ago Units % Change vs. Year Ago

Health Care – All Outlets Combined (plus Convenience)

UPC-coded items

Co

pyr

igh

t ©

2015

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

13

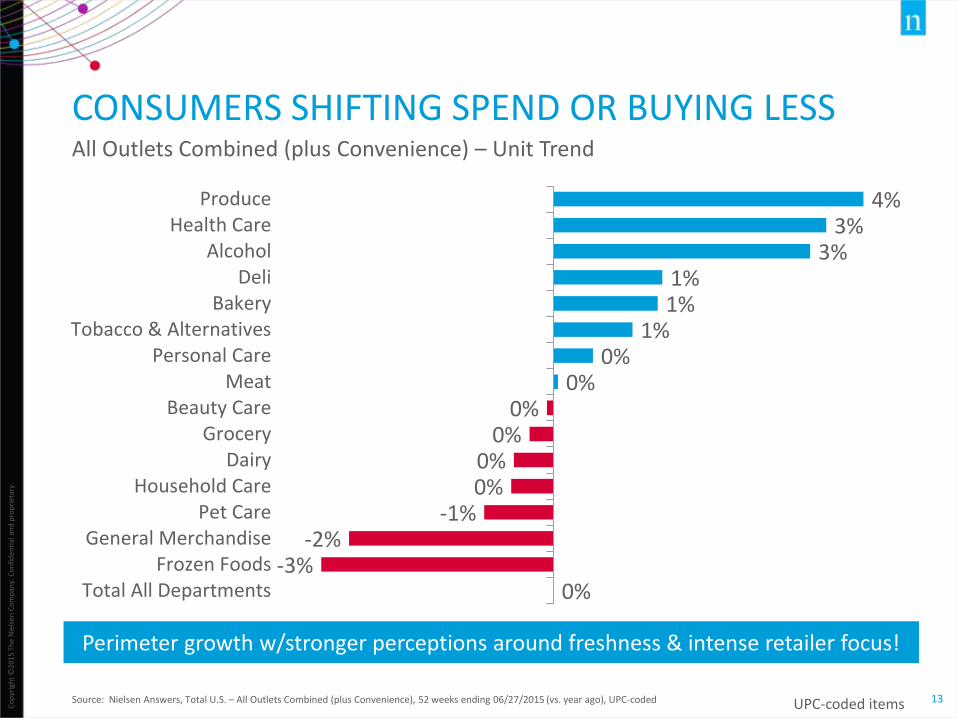

CONSUMERS SHIFTING SPEND OR BUYING LESS

Source: Nielsen Answers, Total U.S. – All Outlets Combined (plus Convenience), 52 weeks ending 06/27/2015 (vs. year ago), UPC-coded

0%-3%

-2%-1%

0%0%

0%0%

0%0%

1%1%1%

3%3%

4%

Total All DepartmentsFrozen Foods

General MerchandisePet Care

Household CareDairy

GroceryBeauty Care

MeatPersonal Care

Tobacco & AlternativesBakery

DeliAlcohol

Health CareProduce

Perimeter growth w/stronger perceptions around freshness & intense retailer focus!

All Outlets Combined (plus Convenience) – Unit Trend

UPC-coded items

Co

pyr

igh

t ©

2015

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

14

TOTAL STORE GAINS LESS THAN SPECTACULAR

Source: Nielsen Answers, Total U.S. All Outlets Combined (plus Convenience), All Departments, All Brands, % Change, 52 week periods vs. year ago

$731 $762 $780 $791 $811

250 250 252 253 253

52 weeks ending07/02/2011

52 weeks ending06/30/2012

52 weeks ending06/29/2013

52 weeks ending06/28/2014

52 weeks ending06/27/2015

Bill

ion

s

Dollar Sales Unit Volume

Shouldn’t an economic recovery be delivering more growth?

All Departments

Dollar Trend +4 +2 +1 +2

Unit Trend +0 +1 +0 +0

Average U Price Trend +4 +2 +1 +2

Any Promo U Trend +1 +8 -6 -4

UPC-coded items

Co

pyr

igh

t ©

2015

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

15

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

Perc

ent

Ch

ange

vs.

Yea

r A

go

Frozen Foods

Deli

Grocery

Beauty Care

Total All Departments

Health Care

Household Care

Alcohol

Personal Care

Meat

Pet Care

Bakery

Produce

Tobacco & Alternatives

General Merchandise

Dairy

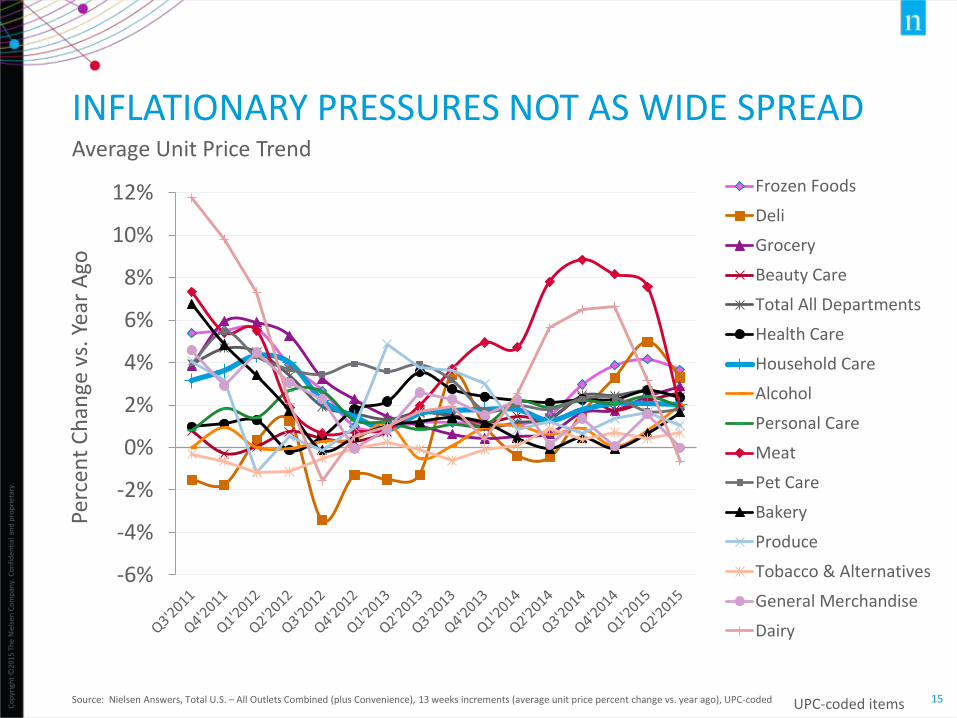

INFLATIONARY PRESSURES NOT AS WIDE SPREAD

Source: Nielsen Answers, Total U.S. – All Outlets Combined (plus Convenience), 13 weeks increments (average unit price percent change vs. year ago), UPC-coded

Average Unit Price Trend

UPC-coded items

Co

pyr

igh

t ©

2015

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

16

$1

$2

$3

$4

$5

$6

$7

$8

U.S

. Do

llars

Alcohol

General Merchandise

Health Care

Tobacco & Alternatives

Beauty Care

Personal Care

Household Care

Meat

Pet Care

Frozen Foods

Total All Departments

Deli

Produce

Dairy

Bakery

Grocery

PRICES HAVE NEVER RETREATED

Source: Nielsen Answers, Total U.S. – All Outlets Combined (plus Convenience), 13 weeks increments, UPC-coded

Average Unit Price

UPC-coded items

17

Co

pyr

igh

t ©

2015

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

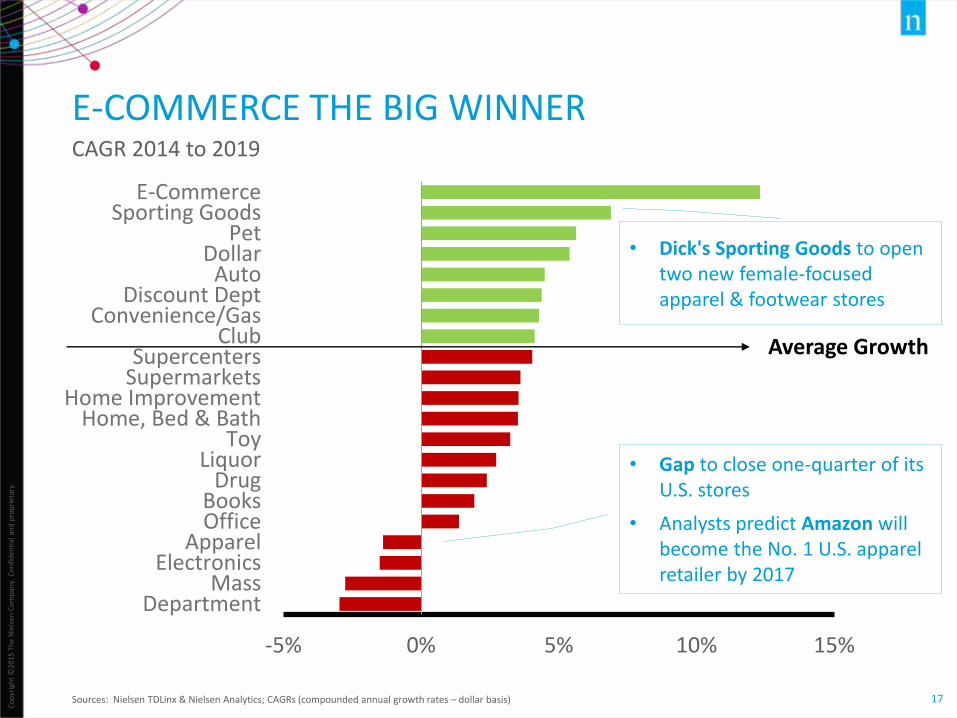

E-COMMERCE THE BIG WINNER

Sources: Nielsen TDLinx & Nielsen Analytics; CAGRs (compounded annual growth rates – dollar basis)

-5% 0% 5% 10% 15%

DepartmentMass

ElectronicsApparel

OfficeBooks

DrugLiquor

ToyHome, Bed & Bath

Home ImprovementSupermarketsSupercenters

ClubConvenience/Gas

Discount DeptAuto

DollarPet

Sporting GoodsE-Commerce

CAGR 2014 to 2019

Average Growth

• Gap to close one-quarter of its U.S. stores

• Analysts predict Amazon will become the No. 1 U.S. apparel retailer by 2017

• Dick's Sporting Goods to open two new female-focused apparel & footwear stores

Co

pyr

igh

t ©

2015

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

18

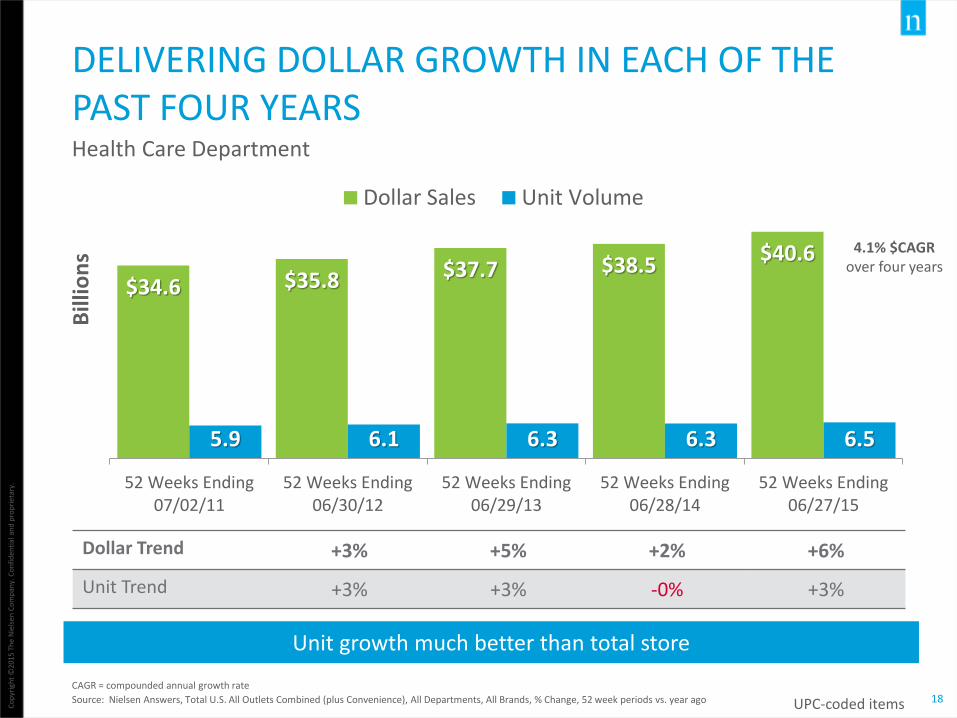

DELIVERING DOLLAR GROWTH IN EACH OF THE PAST FOUR YEARSHealth Care Department

CAGR = compounded annual growth rate

Source: Nielsen Answers, Total U.S. All Outlets Combined (plus Convenience), All Departments, All Brands, % Change, 52 week periods vs. year ago

$34.6 $35.8 $37.7 $38.5$40.6

5.9 6.1 6.3 6.3 6.5

52 Weeks Ending07/02/11

52 Weeks Ending06/30/12

52 Weeks Ending06/29/13

52 Weeks Ending06/28/14

52 Weeks Ending06/27/15

Bill

ion

s

Dollar Sales Unit Volume

Unit growth much better than total store

Dollar Trend +3% +5% +2% +6%

Unit Trend +3% +3% -0% +3%

UPC-coded items

4.1% $CAGR over four years

PRIVATE BRANDS OVERVIEW

Co

pyr

igh

t ©

2015

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

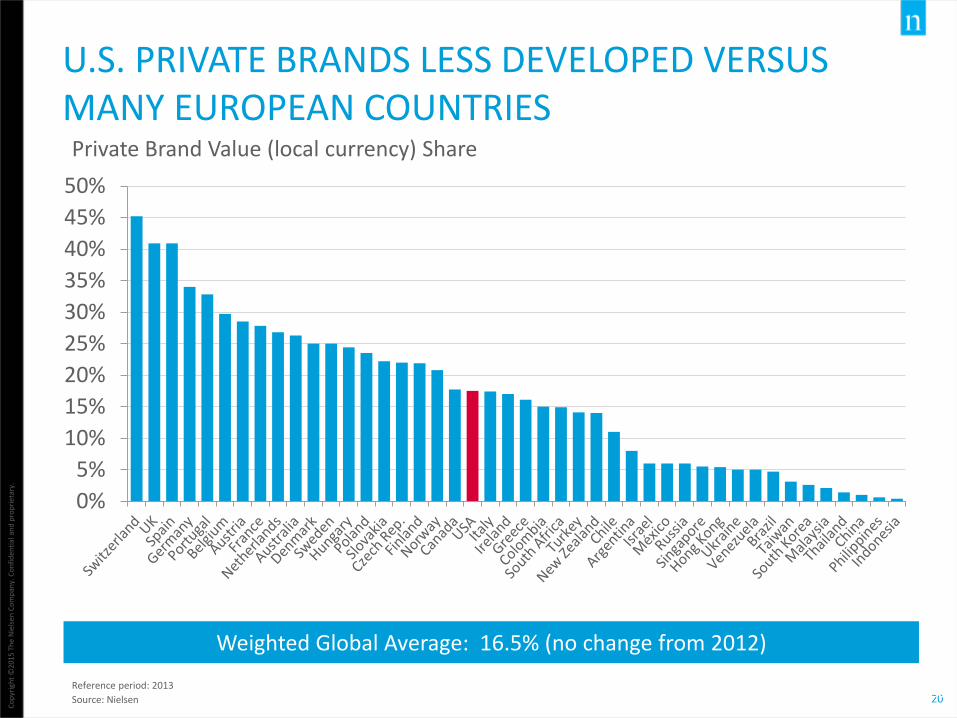

20

U.S. PRIVATE BRANDS LESS DEVELOPED VERSUS MANY EUROPEAN COUNTRIES Private Brand Value (local currency) Share

Reference period: 2013

Source: Nielsen

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

Weighted Global Average: 16.5% (no change from 2012)

Page 20

21

Co

pyr

igh

t ©

2015

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

BIGGER SHARE IN EDIBLE DEPARTMENTS; SHARE GROWTH NOT ALWAYS A FUNCTION OF SHARE

Source: Nielsen Answers, Total U.S. – All Outlets Combined (xAOC), 52 weeks ending 06/27/2015, UPC-coded

0

1

5

11

11

14

14

17

20

20

22

29

30

30

35

Tobacco & Alternatives

Alcohol

Beauty Care

General Merchandise

Personal Care

Grocery

Pet Care

Meat

Frozen Foods

Produce

Household Care

Health Care

Bakery

Deli

Dairy

Private Brands: Dollar Share & Point Change versus Year Ago

-0.7

-0.2

-0.1

-0.1

-0.1

-0.1

0.0

0.1

0.2

0.2

0.3

0.3

0.9

1.1

1.5

Health Care

Grocery

Dairy

Bakery

Personal Care

Alcohol

Tobacco & Alternatives

Produce

Pet Care

Frozen Foods

Deli

Beauty Care

Household Care

Meat

General Merchandise

All Departments Private Brands $ Share: 17.8%; up 0.2 points from year ago

UPC-coded items

Edibles Non-Edibles Share Loss Share Gain

22

Co

pyr

igh

t ©

2015

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

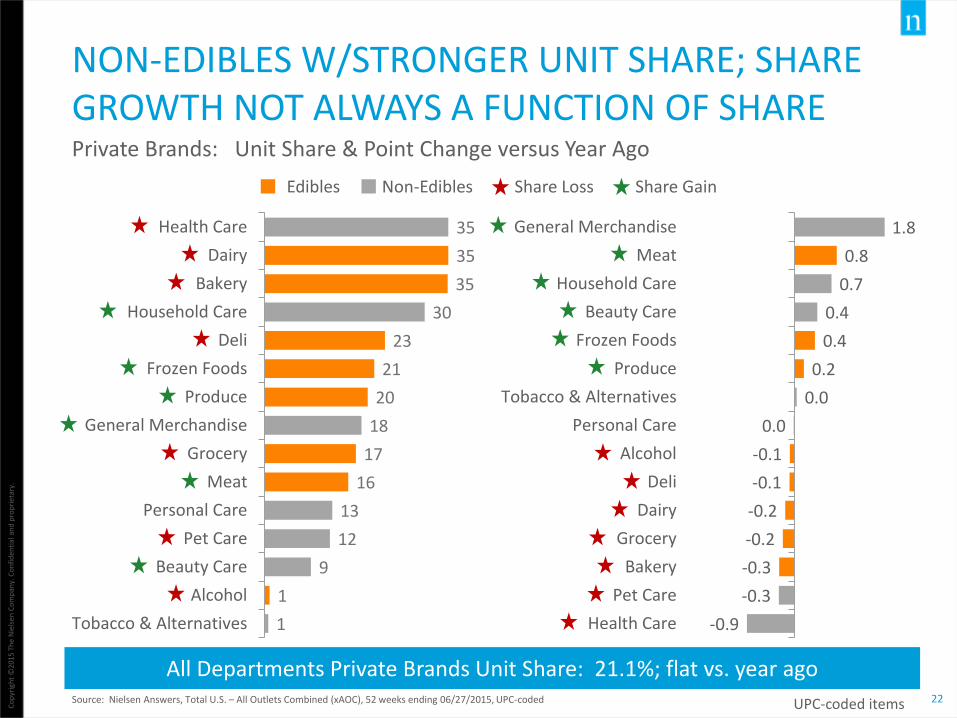

NON-EDIBLES W/STRONGER UNIT SHARE; SHARE GROWTH NOT ALWAYS A FUNCTION OF SHARE

Source: Nielsen Answers, Total U.S. – All Outlets Combined (xAOC), 52 weeks ending 06/27/2015, UPC-coded

1

1

9

12

13

16

17

18

20

21

23

30

35

35

35

Tobacco & Alternatives

Alcohol

Beauty Care

Pet Care

Personal Care

Meat

Grocery

General Merchandise

Produce

Frozen Foods

Deli

Household Care

Bakery

Dairy

Health Care

Private Brands: Unit Share & Point Change versus Year Ago

-0.9

-0.3

-0.3

-0.2

-0.2

-0.1

-0.1

0.0

0.0

0.2

0.4

0.4

0.7

0.8

1.8

Health Care

Pet Care

Bakery

Grocery

Dairy

Deli

Alcohol

Personal Care

Tobacco & Alternatives

Produce

Frozen Foods

Beauty Care

Household Care

Meat

General Merchandise

All Departments Private Brands Unit Share: 21.1%; flat vs. year ago

UPC-coded items

Edibles Non-Edibles Share Loss Share Gain

Co

pyr

igh

t ©

2015

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

23

SUPERMARKETS GARNER HIGHEST PRIVATE BRAND SHARE; > SHARE GROWTH IN OTHER CHANNELS

Source: Nielsen Answers, Total U.S., UPC-coded;*Club Stores, Dollar Stores, Mass-Merchandisers, Supercenters, & Military

19.1

15.3

15.0

2.9

19.6

16.6

16.0

3.9

Supermarkets

Drug Stores

Value*

C-Stores

Private Brands Dollar Share

23.0

16.5

18.8

4.5

23.1

17.4

19.0

5.4

Supermarkets

Drug Stores

Value*

C-Stores

Private Brands Unit Share

52 Weeks Ending: 07/02/2011 06/30/2012 06/29/2013 06/28/2014 06/27/2015

UPC-coded items

Co

pyr

igh

t ©

2015

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

24

Dollar Sales Percent Change vs. Year Ago

Private Brand +5% +8% +3% +3% +3% +3%

Branded +1% +3% +3% +2% +1% +2%

ON PAR WITH BRAND GROWTH SINCE 2012 WITH MODEST SHARE GROWTH IN 2013 & 2014All Departments

Sources: Nielsen Strategic Planner (2009 data) & Nielsen Answers (2010-2015 data), Total U.S. – All Outlets Combined (xAOC), Total All Departments,

16.2%

16.8%

17.4% 17.4% 17.6%17.8% 17.8%

2009 2010 2011 2012 2013 2014 52 W/E06/27/2015

Private Brand $ Share

UPC-coded items

Co

pyr

igh

t ©

2015

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

25

NON-LEAD BRANDS WINNING SHAREUnit Share

Source: Nielsen Answers, Total U.S. – All Outlets Combined (xAOC) – based on approximately 50,000 top-selling brands

47.5% 47.9% 48.0%

21.2% 21.1% 21.1%

31.3% 31.0% 30.9%

52 weeks ending06/29/2013

52 weeks ending06/28/2014

52 weeks ending06/27/2015

Lead Brands*

Private Brands

Other Brands

*Lead brand could be #1 or 2 depending on private brand unit share

Unit SharePoint Change

versus two years ago

- 0.4

- 0.1

+ 0.5

UPC-coded items

Co

pyr

igh

t ©

2015

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

26

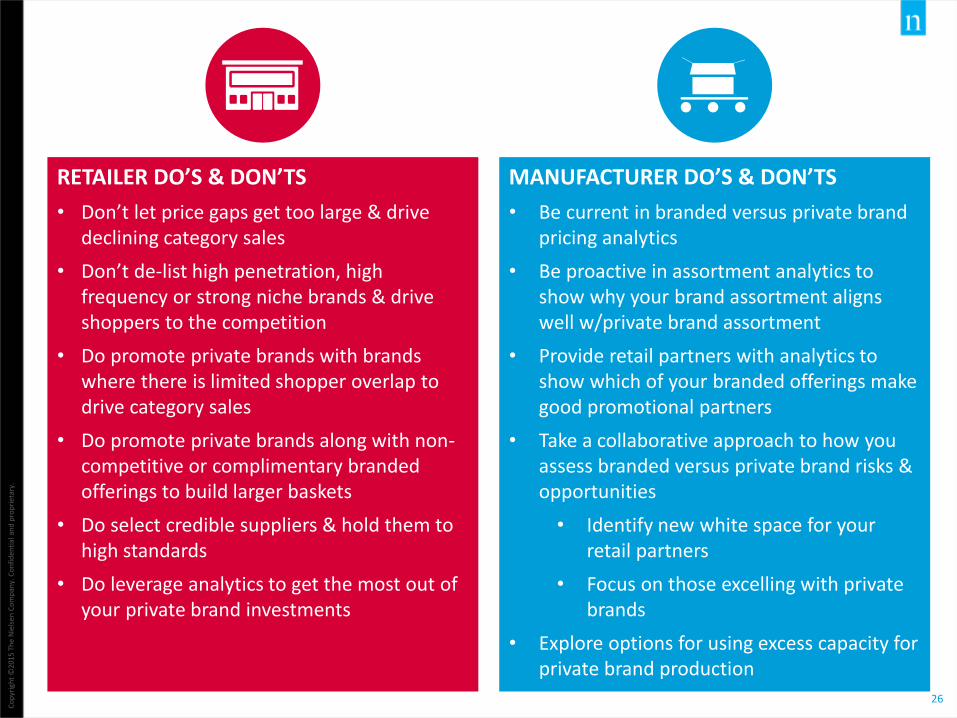

MANUFACTURER DO’S & DON’TS

• Be current in branded versus private brand pricing analytics

• Be proactive in assortment analytics to show why your brand assortment aligns well w/private brand assortment

• Provide retail partners with analytics to show which of your branded offerings make good promotional partners

• Take a collaborative approach to how you assess branded versus private brand risks & opportunities

• Identify new white space for your retail partners

• Focus on those excelling with private brands

• Explore options for using excess capacity for private brand production

RETAILER DO’S & DON’TS

• Don’t let price gaps get too large & drive declining category sales

• Don’t de-list high penetration, high frequency or strong niche brands & drive shoppers to the competition

• Do promote private brands with brands where there is limited shopper overlap to drive category sales

• Do promote private brands along with non-competitive or complimentary branded offerings to build larger baskets

• Do select credible suppliers & hold them to high standards

• Do leverage analytics to get the most out of your private brand investments

POPULATION AND DEMOGRAPHIC TRENDS

28

Co

pyr

igh

t ©

2015

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

BY 2020, 57% OF U.S. POPULATION WILL BE MILLENNIALS OR YOUNGER

Source: U.S. Census Bureau (2014 National Population Projections); MM = million

02,500,000

Males (165 MM)

U.S. Population Projections – 2020: All Races/Ethnicities

0 2,500,000

05

101520253035404550556065707580859095

100

Females (169 MM)

Population

Millennials

Gen X

Boomers 38MM

25MM

40MM

34MM

24MM

41MM

Age

10MM 14MM

53MM56MMGen Z

Greatest Generation

In 2020,

57%of the U.S.

population will be

Millennials or younger, up from 50% in

2014

Co

pyr

igh

t ©

2015

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

29

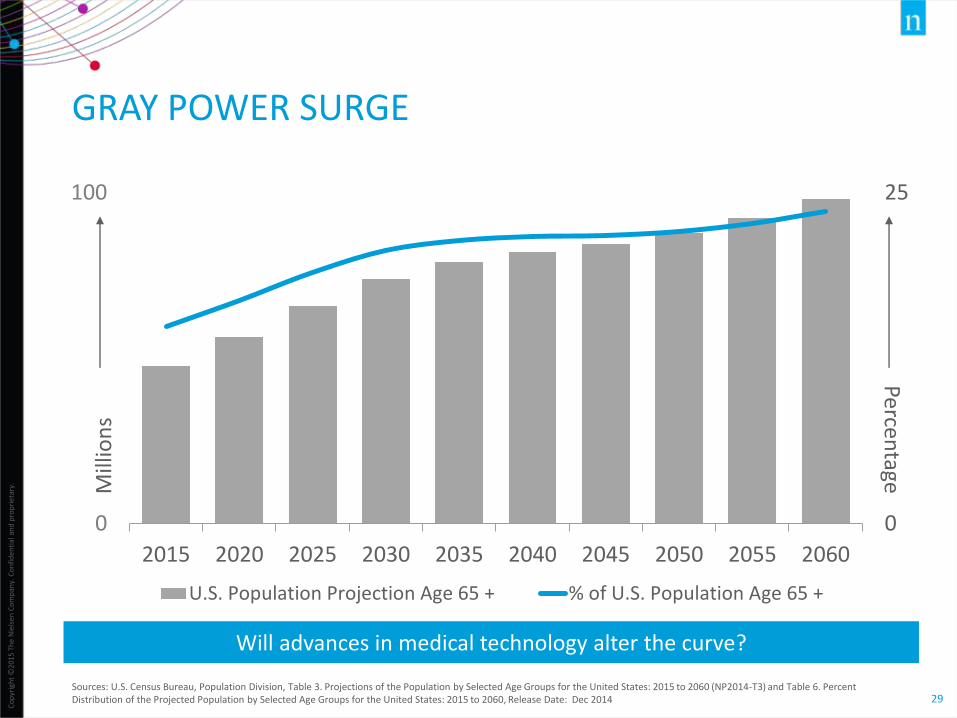

GRAY POWER SURGE

Sources: U.S. Census Bureau, Population Division, Table 3. Projections of the Population by Selected Age Groups for the United States: 2015 to 2060 (NP2014-T3) and Table 6. Percent Distribution of the Projected Population by Selected Age Groups for the United States: 2015 to 2060, Release Date: Dec 2014

0

25

0

100

2015 2020 2025 2030 2035 2040 2045 2050 2055 2060

U.S. Population Projection Age 65 + % of U.S. Population Age 65 +

Will advances in medical technology alter the curve?

Percentage

Mill

ion

s

Co

pyr

igh

t ©

2015

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

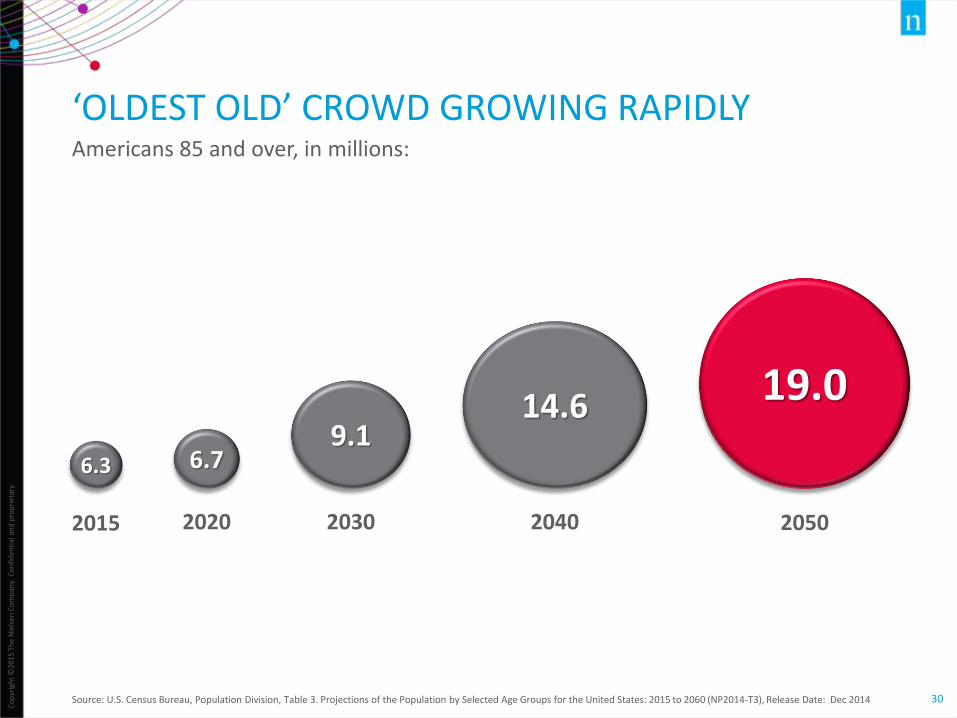

30Source: U.S. Census Bureau, Population Division, Table 3. Projections of the Population by Selected Age Groups for the United States: 2015 to 2060 (NP2014-T3), Release Date: Dec 2014

‘OLDEST OLD’ CROWD GROWING RAPIDLYAmericans 85 and over, in millions:

2015 2020 2030 20502040

6.3 6.79.1

14.6 19.0

Co

pyr

igh

t ©

2015

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

31

OLDER MORE TRIPS; YOUNGER BIGGER BASKETS

Source: Nielsen Homescan, Total U.S. 52 weeks ending 12/27/2014, excludes gas only or Rx only trips; *UPC-coded products

Total Retail Channels

160

151

127

101

Greatest Gen

Boomers

Gen X

Millennials

Shopping Trips per Household

Deals matter to all!

$39

$47

$55

$57

Greatest Gen

Boomers

Gen X

Millennials

Basket Ring $ per Trip

$6,172

$7,081

$7,020

$5,710

Greatest Gen

Boomers

Gen X

Millennials

Basket Ring $ Per Household

25%

25%

25%

25%

Greatest Gen

Boomers

Gen X

Millennials

% Dollars on Deal*

Co

pyr

igh

t ©

2015

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

32

DIVERSE CATEGORY NEEDS ACROSSGENERATIONAL SEGMENTS Where is your category or brand driving sales?

Source: Nielsen Homescan, Total U.S. 52 weeks ending 12/27/2014, UPC-coded products

GREATEST GEN BOOMERS GEN X MILLENNIALS

BABY FOOD 45 44 94 163

CEREAL 83 91 115 113

HAIR CARE 69 98 123 97

CARBONATED BEVERAGES

76 107 108 89

DETERGENTS 88 102 110 92

PET FOOD 111 122 90 55

VITAMINS 139 110 88 63

WINE 117 120 85 60

ICE CREAM 114 109 96 75

How can manufacturers & retailers collaborate on generational store sets?

$ Buying Rate Index

Co

pyr

igh

t ©

2015

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

33

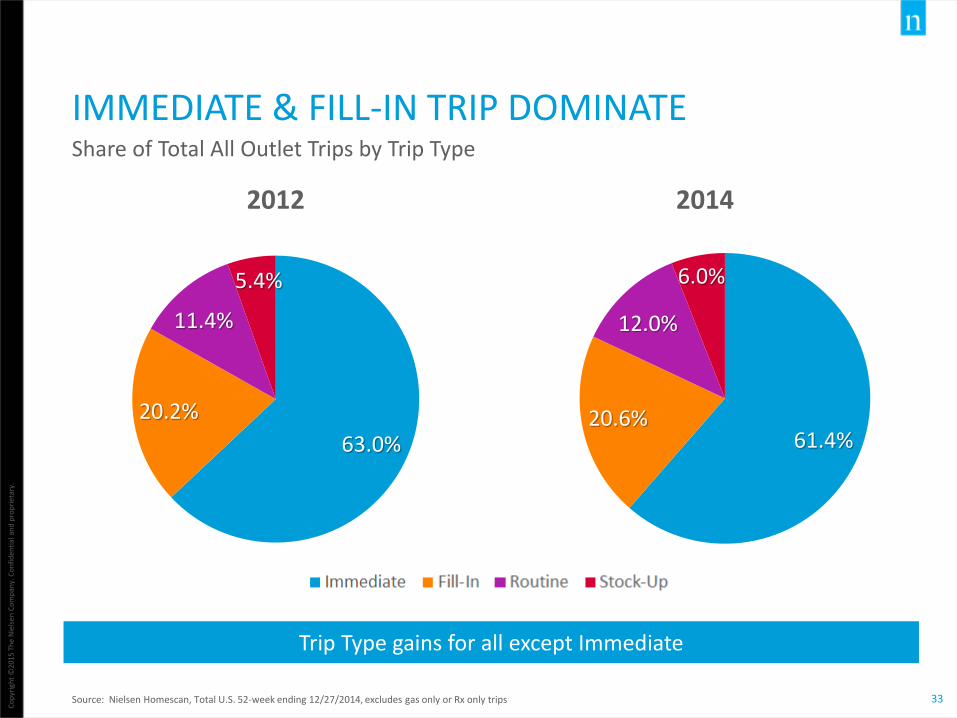

IMMEDIATE & FILL-IN TRIP DOMINATE

Source: Nielsen Homescan, Total U.S. 52-week ending 12/27/2014, excludes gas only or Rx only trips

63.0%

20.2%

11.4%

5.4%

2012

Immediate Fill-In Routine Stock-Up

Trip Type gains for all except Immediate

Share of Total All Outlet Trips by Trip Type

61.4%20.6%

12.0%

6.0%

2014

Immediate Fill-In

Co

pyr

igh

t ©

2015

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

34

LARGER TRIPS GAINED IMPORTANCE IN OVERALL SALES TOO

Source: Nielsen Homescan, Total U.S. 52-week ending 12/27/2014, excludes gas only or Rx only trips

22.0%

23.7%

25.3%

29.0%

2012

Immediate Fill-In Routine Stock-Up

Larger trips the real drivers of retail sales

Share of Total All Outlet Dollars by Trip Type

20.8%

23.2%

25.7%

30.3%

2014

Immediate Fill-In Routine Stock-Up

Co

pyr

igh

t ©

2015

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

35

FEMALES DRIVE TRIPS, BUT MALES GAININGShare of Retail Channel Shopping Trips

54

46

39

61

38

62

33

67

32

68

29

71

29

71

Mal

esFe

mal

es

54

46

37

63

37

63

34

66

30

70

25

75

26

74

Mal

esFe

mal

es

Mass

Dollar

Supers

Drug

Grocery

Club

C-Store

2004 2014

Source: Nielsen Homescan, Total U.S., excludes gas-only or Rx-only trips

Co

pyr

igh

t ©

2015

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

36

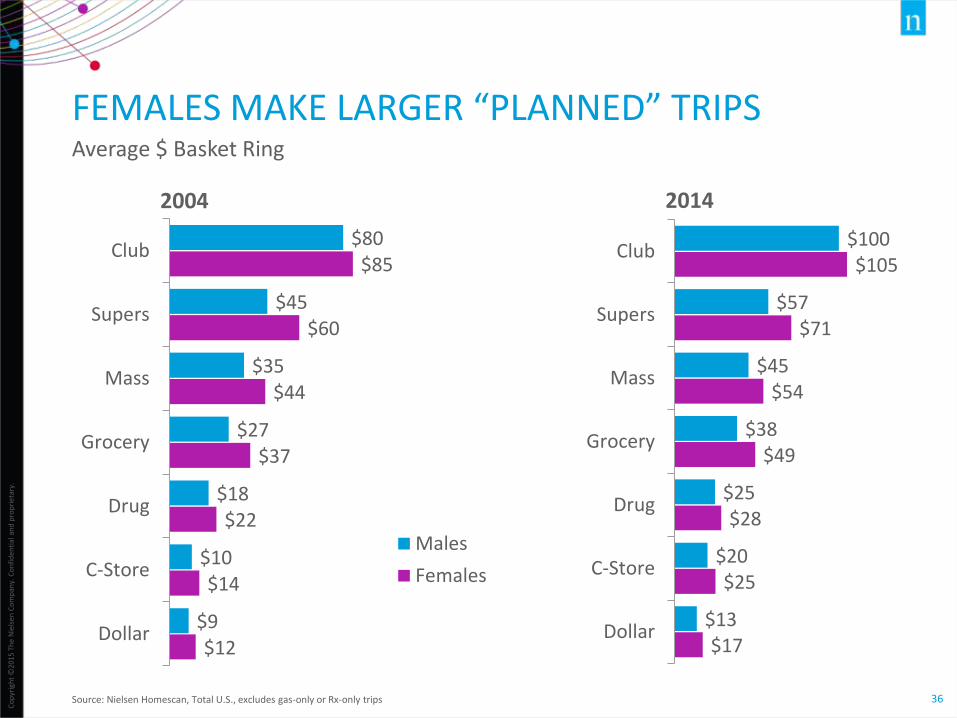

FEMALES MAKE LARGER “PLANNED” TRIPSAverage $ Basket Ring

$12

$14

$22

$37

$44

$60

$85

$9

$10

$18

$27

$35

$45

$80

Dollar

C-Store

Drug

Grocery

Mass

Supers

Club

Males

Females

$17

$25

$28

$49

$54

$71

$105

$13

$20

$25

$38

$45

$57

$100

Dollar

C-Store

Drug

Grocery

Mass

Supers

Club

Source: Nielsen Homescan, Total U.S., excludes gas-only or Rx-only trips

2004 2014

Co

pyr

igh

t ©

2015

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

37

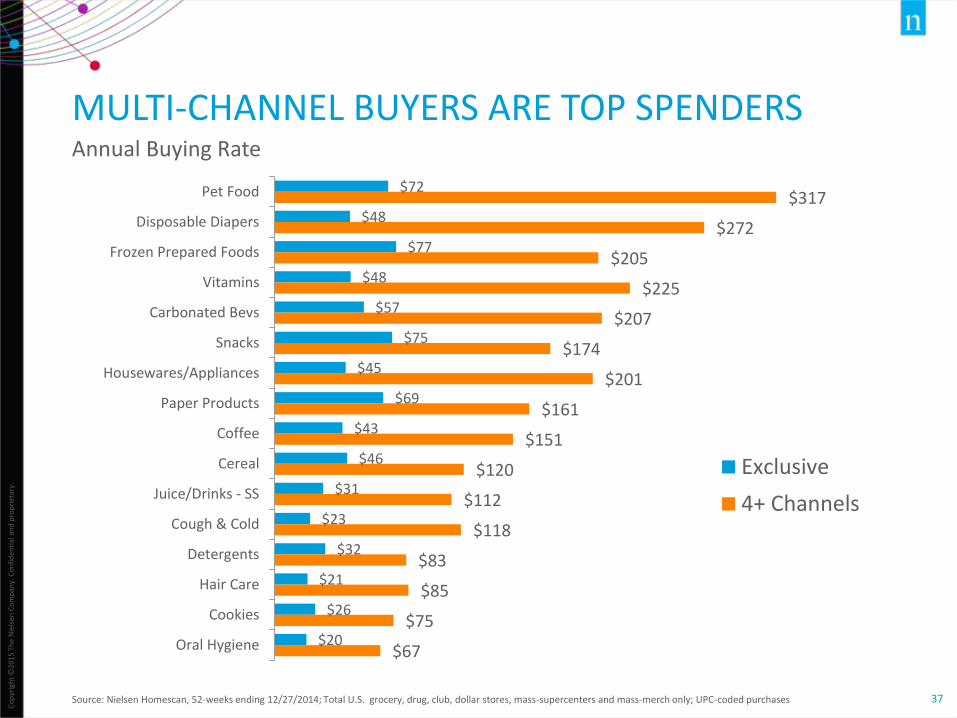

MULTI-CHANNEL BUYERS ARE TOP SPENDERS

Source: Nielsen Homescan, 52-weeks ending 12/27/2014; Total U.S. grocery, drug, club, dollar stores, mass-supercenters and mass-merch only; UPC-coded purchases

$72

$48

$77

$48

$57

$75

$45

$69

$43

$46

$31

$23

$32

$21

$26

$20

$317

$272

$205

$225

$207

$174

$201

$161

$151

$120

$112

$118

$83

$85

$75

$67

Pet Food

Disposable Diapers

Frozen Prepared Foods

Vitamins

Carbonated Bevs

Snacks

Housewares/Appliances

Paper Products

Coffee

Cereal

Juice/Drinks - SS

Cough & Cold

Detergents

Hair Care

Cookies

Oral Hygiene

Exclusive

4+ Channels

Annual Buying Rate

HEALTH CARE SEGMENT PERFORMANCE

Co

pyr

igh

t ©

2015

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

39

CONSUMERS INCREASINGLY UNDERSTAND HEALTH IS WEALTH

• Yet face many hurdles in their pursuit of good health including: Busier lifestyles Rising costs of healthcare Affordable, healthful food options Access to reliable health education and information Increased lifespan

• Managing Chronic Conditions makes this even more difficult 7 out of 10 deaths are the result of a chronic illness in the U.S.* Aversion, treatment and maintenance all have implications when

comes to daily living, attitudes/preferences and purchase behaviors

*Quote source: http://www.cdc.gov/hrqol/pdfs/cdnrwinter03.pdf

Co

pyr

igh

t ©

2015

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

40

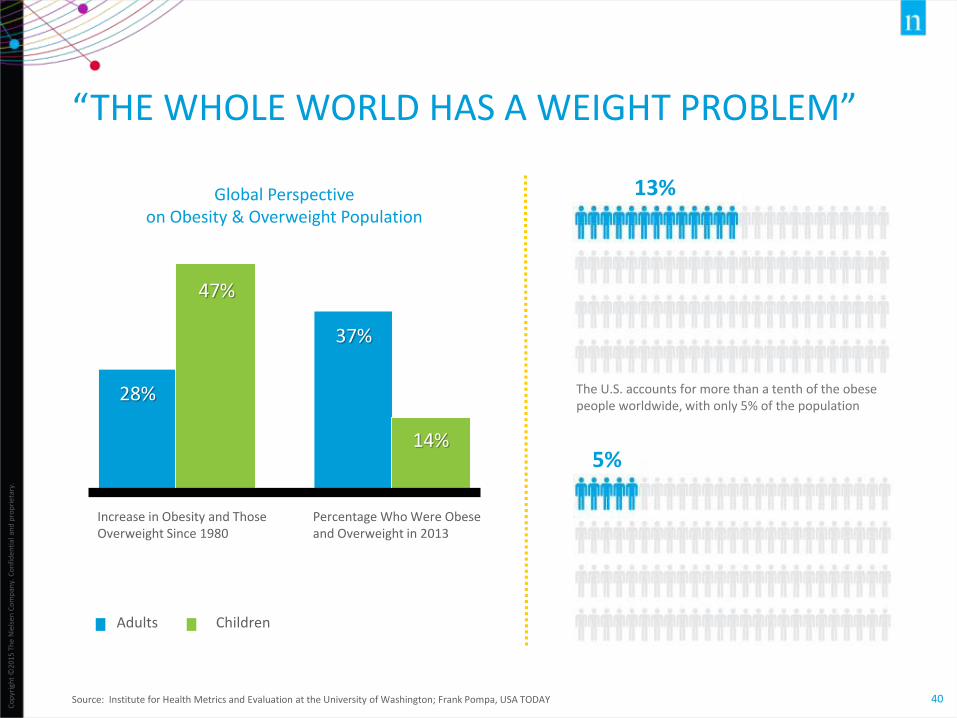

“THE WHOLE WORLD HAS A WEIGHT PROBLEM”

Source: Institute for Health Metrics and Evaluation at the University of Washington; Frank Pompa, USA TODAY

13%

5%

The U.S. accounts for more than a tenth of the obese people worldwide, with only 5% of the population

Increase in Obesity and Those Overweight Since 1980

Percentage Who Were Obese and Overweight in 2013

Global Perspective on Obesity & Overweight Population

28%

47%

37%

14%

Adults Children

Co

pyr

igh

t ©

2015

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

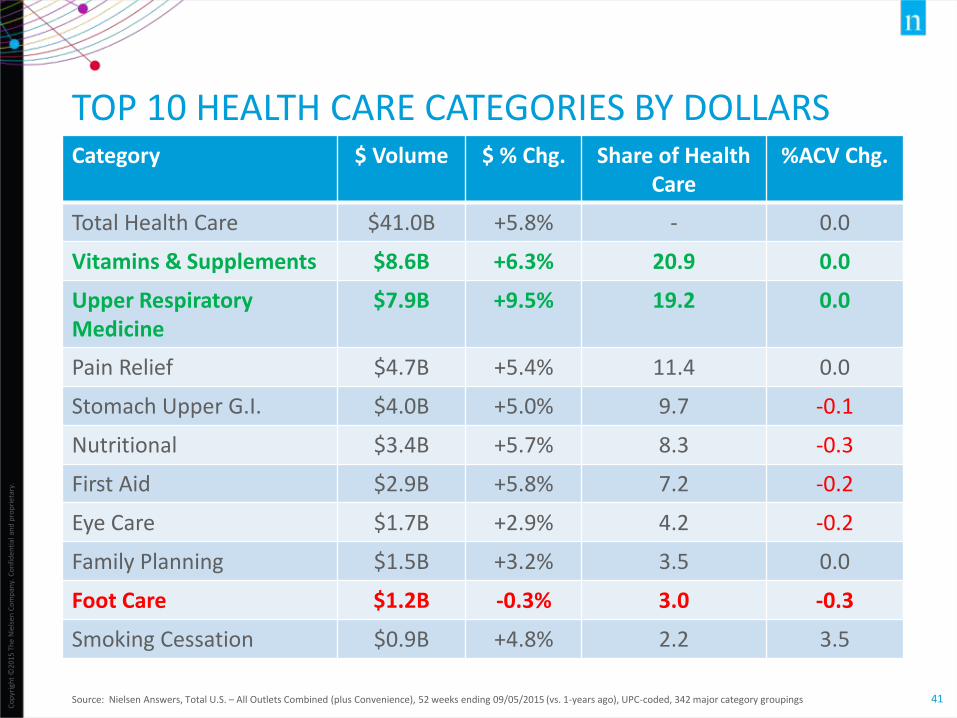

41Source: Nielsen Answers, Total U.S. – All Outlets Combined (plus Convenience), 52 weeks ending 09/05/2015 (vs. 1-years ago), UPC-coded, 342 major category groupings

TOP 10 HEALTH CARE CATEGORIES BY DOLLARSCategory $ Volume $ % Chg. Share of Health

Care%ACV Chg.

Total Health Care $41.0B +5.8% - 0.0

Vitamins & Supplements $8.6B +6.3% 20.9 0.0

Upper Respiratory Medicine

$7.9B +9.5% 19.2 0.0

Pain Relief $4.7B +5.4% 11.4 0.0

Stomach Upper G.I. $4.0B +5.0% 9.7 -0.1

Nutritional $3.4B +5.7% 8.3 -0.3

First Aid $2.9B +5.8% 7.2 -0.2

Eye Care $1.7B +2.9% 4.2 -0.2

Family Planning $1.5B +3.2% 3.5 0.0

Foot Care $1.2B -0.3% 3.0 -0.3

Smoking Cessation $0.9B +4.8% 2.2 3.5

Co

pyr

igh

t ©

2015

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

42

TAKING CHARGE OF AILMENT TREATMENTS

Source: Nielsen Answers, Total U.S. – All Outlets Combined (plus Convenience), 52 weeks ending 06/27/2015 (vs. year ago), UPC-coded

5%5%5%5%6%6%6%6%8%8%10%11%12%

18%110%

Jock Itch Product

Nutritional

Pain Relief

Stomach Upper G.I.

Vitamins & Supplements

Diabetic

Antiseptics & Disinfectants

First Aid

Motion Sickness

Medical Accessory

Upper Respiratory Medicine

Home Health Testing

Lice Treatment

First Aid Other

Pain Relieving Device

Avoiding a visit to the doctor?

Fastest Growing ($) Health Care Categories: All Outlets Combined (plus Convenience)

UPC-coded items

Are Medicare recipients or households with minimal or full

health coverage behind the growth?

Co

pyr

igh

t ©

2015

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

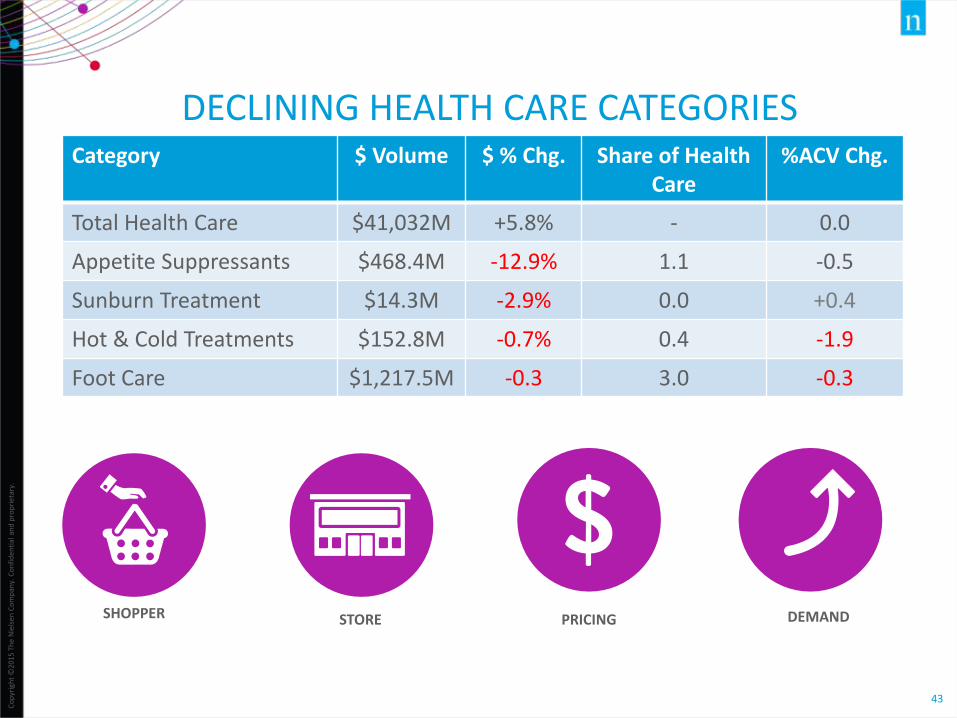

43

DECLINING HEALTH CARE CATEGORIESCategory $ Volume $ % Chg. Share of Health

Care%ACV Chg.

Total Health Care $41,032M +5.8% - 0.0

Appetite Suppressants $468.4M -12.9% 1.1 -0.5

Sunburn Treatment $14.3M -2.9% 0.0 +0.4

Hot & Cold Treatments $152.8M -0.7% 0.4 -1.9

Foot Care $1,217.5M -0.3 3.0 -0.3

SHOPPER STORE PRICING DEMAND

Co

pyr

igh

t ©

2015

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

44

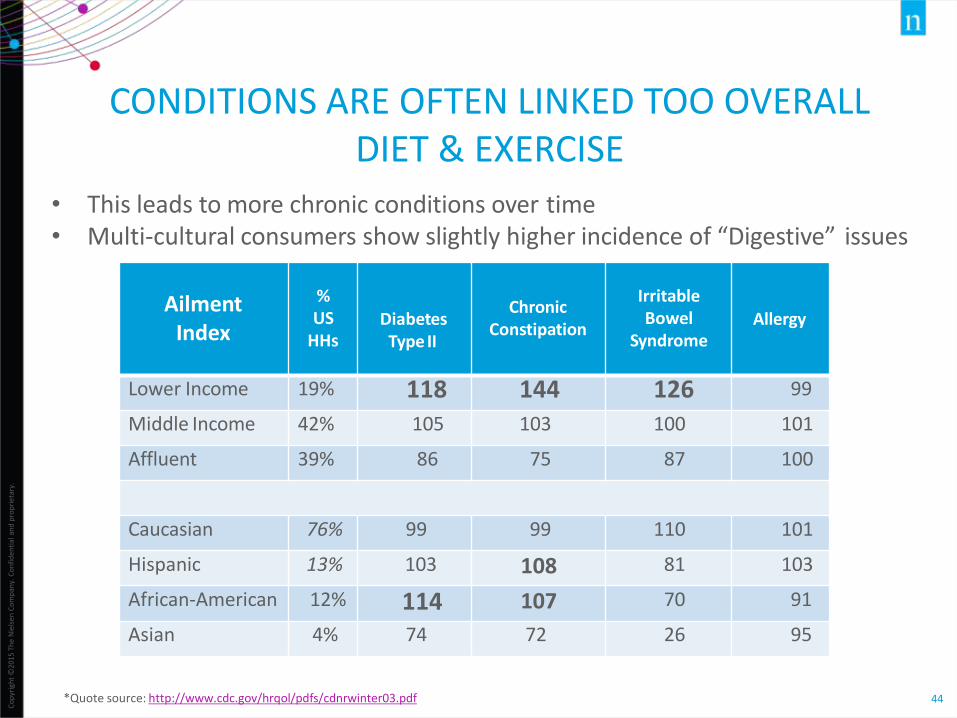

CONDITIONS ARE OFTEN LINKED TOO OVERALL DIET & EXERCISE

*Quote source: http://www.cdc.gov/hrqol/pdfs/cdnrwinter03.pdf

• This leads to more chronic conditions over time• Multi‐cultural consumers show slightly higher incidence of “Digestive” issues

Ailment Index

% US

HHsDiabetes

Type II

Chronic Constipation

Irritable Bowel

SyndromeAllergy

Lower Income 19% 118 144 126 99

Middle Income 42% 105 103 100 101

Affluent 39% 86 75 87 100

Caucasian 76% 99 99 110 101

Hispanic 13% 103 108 81 103

African‐American 12% 114 107 70 91

Asian 4% 74 72 26 95

Co

pyr

igh

t ©

2015

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

45

DEMAND FOR OTC VARIES BY CONDITION

OTC $% US HH’s WITH SUFFERER SPEND INDEX* % US HH’s WITH SUFFERER

OTC $ SPEND INDEX*

ALLERGY

HIGH BLOOD PRESSURE

IMPERFECT VISION

ACID REFLUX

OBESITY

CHOLESTEROL

HEADACHE

JOINT/NECK/BACK PAIN

ANXIETY & DEPRESSION

INSOMNIA

37%

32%

34%

31%

27%

24%

23%

22%

17%

21%

119

117

116

123

115

124

108

113

114

120

OSTEO ARTHRITIS

MUSCLE PAIN SPASMS

TYPE II DIABETES

ACNE

SKIN ‐ NON ACNE

ASTHMA

MENOPAUSE

DRY EYE

OVERACTIVE BLADDER

LACTOSE INTOLERANCE

7%

7%

8%

9%

11%

13%

13%

14%

14%

16% 129

117

135

109

115

122

129

136

148

123

Source: Nielsen Health Survey 2015

*OTC $ PER HH AMONG SUFFERER GROUP DIVIDED BY TOTAL OTC $ PERHH*100

Co

pyr

igh

t ©

2015

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

46

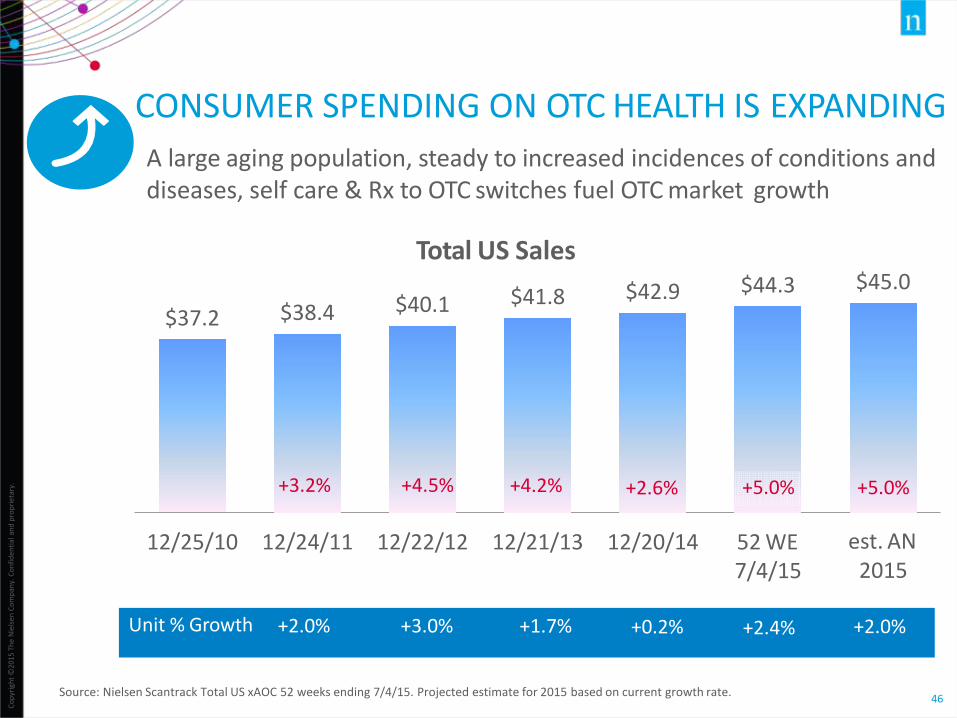

CONSUMER SPENDING ON OTC HEALTH IS EXPANDING

A large aging population, steady to increased incidences of conditions and diseases, self care & Rx to OTC switches fuel OTC market growth

Total US Sales

12/25/10 12/24/11 12/22/12 12/21/13 12/20/14 52 WE7/4/15

est. AN 2015

Unit % Growth +2.0% +3.0% +1.7% +0.2% +2.4% +2.0%

$37.2 $38.4 $40.1 $41.8 $42.9 $44.3 $45.0

+3.2% +4.5% +4.2% +2.6% +5.0% +5.0%

Source: Nielsen Scantrack Total US xAOC 52 weeks ending 7/4/15. Projected estimate for 2015 based on current growth rate.

Co

pyr

igh

t ©

2015

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

47

HEAVIEST OTC USERS DRIVING GROWTH

Total Consumer Health $44.3B

Gen X Boomers

Millennials

$7.1B+2%

Greatest Generation

*Source: Nielsen Boomer Segmentation Homescan U.S. Mid‐Year 2015 proportions adjusted to Nielsen Scantrack OTC Therapeutic & Preventative $ Sales, % Change Based on Dollars Per HH

Segment Definitions: Gen Y Born ‘77 to ‘94, Gen X ‘65 to ‘76, Boomers ‘46 to ‘64, Greatest Generation Pre‐1946

% of US HH’s – Boomers 43%, Gen X 22%, Gen Y 22%, Greatest Gen 13%

$6.6B+1%

$21.3B+3%

$9.3B+2%

Co

pyr

igh

t ©

2015

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

48

GROCERS AND DISCOUNT MAINTAIN A SIGNIFICANT PRICE ADVANTAGE

Total OTC% Change V Year Ago

0.6%

0%

‐0.4%

‐2%

Units

Dollars

10%

8%

6%

4%

2% 1.5%

4.7% 4.7%

2.3%

1.3%

4.6%

2.0%

4.7%

TOTAL MKT TOTAL DRUG INDEPENDENTS GROCERY DISCOUNT CHANNELS**

AvgUnitPrice

$6.45 $8.41 $7.46 $5.85 $5.56

Source: Nielsen Scantrack ‐ Total US 52 weeks ending 7/4/15 Total OTC Line includes Therapeutic MedicationsOnly **Includes Walmart, Target, Kmart, BJ’s, Sams, Dollar General Family Dollar andMilitary

DIGITAL SHOPPING & DIGITAL RETAILING

Co

pyr

igh

t ©

2015

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

50

COUNTER TO BRICK & MORTAR, GREATER INTENT TO BUY NON-EDIBLES% intending to buy ONLINE in next 6 months:

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

Bottom ten mostly edibles; intent to buy 10% or less for most categories

Source: Nielsen, E-Commerce, Digital Technology and Changing Shopper Preferences Around the World Report (April 2015)

Note: Category list is not exhaustive

Top 10

1. Shampoo /Conditioner2. Vitamins / Supplements3. Body Wash4. Deodorant5. Cosmetics6. Hand / Body Lotion7. Toothpaste8. Bar Soap9. Air freshener10.Cleaners

Bottom 10

1. Spirits2. Dog Food Wet3. Baby Formula / Food4. Pet Supplies / Litter5. Peanut Butter6. Frozen Appetizers7. Cat Food Wet8. Salad Dressing9. Packaged Bread10.Fresh Vegetables

HEALTH & WELLNESS TRENDING

Co

pyr

igh

t ©

2015

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

52

HEALTH & WELLNESS OUTPACING RETAIL GROWTH

1Dollar sales $10 billion or more, 2Dollar sales $5 billion to $10 billion, 3Dollar sales less than $5 billion; Note: Health & Wellness claims are not additive

Source: Nielsen Answers, Wellness Track, Total U.S. – All Outlets Combined, plus Convenience, 52-weeks ending 06/27/2015, UPC-coded products only, CAGR = compound annual growth rate

Dollar growth

14%

Total store(52 weeks ending 6/27/2015 versus

year ago)

2%

Organic Content Presence1 claims

(4-YR CAGR)

Top 5 CAGR ($) over four years:

1. Corn Free3 49%2. Grain Free3 43%3. Low Glycemic3 24%4. Ancient Grains3 21%5. GMO Free1 17%

Top 5 Dollar Growth vs. year ago:

1. Grain Free3 95%2. Corn Free3 45%3. Ancient Grains3 32%4. Low Glycemic3 21%5. Stevia3 18%

Wellness claims not just for humans; majority of grain & corn free sales in pet food

Co

pyr

igh

t ©

2015

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

53

HEALTH & WELLNESS CLAIMS: TOP RANKING

1Dollar sales $10 billion or more, 2Dollar sales $5 billion to $10 billion, 3Dollar sales less than $5 billion; Note: Health & Wellness claims are not additive

Source: Nielsen Answers, Wellness Track, Total U.S. – All Outlets Combined, plus Convenience, 52-weeks ending 06/27/2015, UPC-coded products only, CAGR = compound annual growth rate

$ % CHANGE VS. YEAR AGO

1. Grain Free3 94.9%2. Corn Free3 44.6%3. Ancient Grains3 31.9%4. Low Glycemic3 21.0%5. Stevia3 18.2%6. GMO Free1 17.0%7. Organic Content Presence1 16.0%8. Cough3 14.6%9. Gluten Free1 14.3%10. Hormone Antibiotic Free1 12.4%11. Sleeping Aid3 12.1%12. HFCS Free2 12.1%13. No MSG2 11.9%14. Natural11 11.9%15. Artificial Color Flavor1 11.2%16. Non Food Allergy3 9.9%17. Arthritis3 9.0%18. Fortified3 8.6%19. Heartburn Acid Reflux3 7.4%20. Preservative Presence1 6.7%21. Diabetes3 6.5%22. Lactose Presence2 6.1%23. Sweetener Presence2 5.2%24. Soy/Soy Free1 4.8%25. Flax or Hemp3 4.5%

DOLLAR SALES (billions)

1. Fat Presence $ 56.0 2. Soy/Soy Free 55.6 3. Vitamin/Mineral Presence 55.3 4. Gluten Free 46.4 5. Preservative Presence 41.3 6. Caffeine Presence 40.3 7. Calorie Presence 39.6 8. Natural 36.7 9. Salt or Sodium Presence 34.8 10. Artificial Color Flavor 33.5 11. Trans Fat Presence 23.5 12. Grain Type 20.9 13. Cholesterol Presence 19.4 14. Sugar Presence 18.9 15. Protein Presence 18.4 16. Calcium Presence 17.1 17. GMO Free 13.6 18. Organic Content Presence 13.2 19. Fiber Presence 10.6 20. Hormone Antibiotic Free 10.5 21. Omega 3 Type 9.3 22. Lactose Presence 8.5 23. Antioxidants 8.0 24. HFCS Free 7.8 25. Fruit & Veg Presence 7.4

4-YEAR $ CAGR

1. Corn Free3 49.5%2. Grain Free3 42.9%3. Low Glycemic3 24.1%4. Ancient Grains3 21.3%5. GMO Free1 17.3%6. Gluten Free1 16.8%7. Probiotic/Prebiotic3 14.4%8. Hormone Antibiotic Free1 14.4%9. Organic Content Presence1 13.8%10. Natural1 12.4%11. Artificial Color Flavor1 11.3%12. No MSG2 11.2%13. Sleeping Aid3 11.0%14. HFCS Free2 10.6%15. Bone Health3 10.0%16. Lactose Presence2 9.1%17. Stevia3 8.6%18. Soy/Soy Free1 8.2%19. Protein Presence1 7.8%20. Non Food Allergy3 7.4%21. Preservative Presence1 7.0%22. Cough3 6.5%23. Flax or Hemp3 5.8%24. Arthritis33 5.7%25. Fruit & Veg Presence2 5.1%

Average of 31% growth

UPC-coded items

54

Co

pyr

igh

t ©

2015

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

HEALTH & WELLNESS CLAIMS: BOTTOM RANKING

1Dollar sales $10 billion or more, 2Dollar sales $5 billion to $10 billion, 3Dollar sales less than $5 billion; Note: Health & Wellness claims are not additive

Source: Nielsen Answers, Wellness Track, Total U.S. – All Outlets Combined, plus Convenience, 52-weeks ending 06/27/2015, UPC-coded products only, CAGR = compound annual growth rate

$ % CHANGE VS. YEAR AGO

26. Oil Presence3 4.2%27. Protein Presence1 3.6%28. Salt or Sodium Presence1 3.5%29. Sugar Presence1 1.9%30. Hypertension3 1.8%31. Caffeine Presence1 1.6%32. Antioxidants2 1.3%33. Fruit & Veg Presence2 0.9%34. Iron Presence2 0.6%35. Carb Conscious3 0.5%36. Fiber Presence1 0.5%37. Fat Presence1 0.3%38. Vitamin/Mineral Presence1 0.2%39. Omega 3 Type2 0.1%40. Cholesterol Presence1 -0.1%41. Omega Presence2 -0.4%42. Probiotic/Prebiotic3 -0.6%43. Bone Health3 -0.7%44. Calorie Presence1 -0.7%45. Grain Type11 -0.9%46. Saturated Fat Presence2 -1.0%47. Calcium Presence1 -1.5%48. Trans Fat Presence1 -1.5%49. Immune2 -3.5%50. Multigrain3 -4.4%51. Fish/Krill Oil3 -5.8%52. Plant Sterol3 -6.3%53. Calorie 1003 -7.4%

4-YEAR $ CAGR

26. Sweetener Presence2 5.0%27. Oil Presence3 4.5%28. Diabetes3 4.0%29. Omega Presence2 3.9%30. Fiber Presence1 3.8%31. Cholesterol Presence1 3.4%32. Carb Conscious3 3.0%33. Saturated Fat Presence2 2.8%34. Omega 3 Type2 2.6%35. Salt or Sodium Presence1 2.0%36. Heartburn Acid Reflux3 1.9%37. Caffeine Presence1 1.7%38. Iron Presence2 1.2%39. Sugar Presence1 1.1%40. Hypertension3 1.1%41. Fat Presence1 1.1%42. Grain Type1 0.7%43. Vitamin/Mineral Presence1 0.5%44. Calorie Presence1 0.4%45. Multigrain3 0.3%46. Antioxidants2 0.2%47. Fortified3 -0.5%48. Calcium Presence1 -0.7%49. Immune2 -1.1%50. Trans Fat Presence1 -4.1%51. Fish/Krill Oil3 -4.3%52. Plant Sterol3 -4.5%53. Calorie 1003 -5.4%

DOLLAR SALES (billions)

26. Omega Presence $ 7.0 27. Saturated Fat Presence 6.2 28. No MSG 6.0 29. Sweetener Presence 5.9 30. Iron Presence 5.9 31. Immune 5.2 32. Bone Health 4.8 33. Probiotic/Prebiotic 4.2 34. Multigrain 3.7 35. Carb Conscious 3.4 36. Non Food Allergy 3.3 37. Cough 3.2 38. Oil Presence 2.8 39. Heartburn Acid Reflux 2.3 40. Fortified 1.8 41. Stevia 1.4 42. Ancient Grains 1.4 43. Sleeping Aid 1.3 44. Calorie 100 1.2 45. Diabetes 1.0 46. Low Glycemic 0.9 47. Corn Free 0.8 48. Flax or Hemp 0.6 49. Fish/Krill Oil 0.5 50. Arthritis 0.4 51. Hypertension 0.4 52. Grain Free 0.3 53. Plant Sterol 0.1

UPC-coded items

KEY TAKEAWAYS AND CLOSING THOUGHTS

Co

pyr

igh

t ©

2015

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

56

DRIVING GROWTH IN DYNAMIC TIMES

Stay connected with winning

retailers & categories

Determine your role in digital retailing & digital shopping engagement & act

Win the trip through precision marketing & sales

focused against shoppers that

matter

Drive the health & wellness

growth wave

Win the occasion

Co

pyr

igh

t ©

2015

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

57

ACTIVATION

*Quote source: http://www.cdc.gov/hrqol/pdfs/cdnrwinter03.pdf

Retailers and manufacturers can drive topline growth with increased focus on the needs of chronic sufferers

- Who are they?- Where do they shop- What to the buy?- What are their needs (packaging, language, etc.)

Conditions are complex varying in size, age, socio‐economic status, level of Healthcare engagement and other factors

Co

pyr

igh

t ©

2015

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

58

HEALTH & BEAUTY CARE SENIOR FOCUS

Sources: MultiAd Kwikee & company websites

Co

pyr

igh

t ©

2015

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

59

SMALLER PORTION SIZES, BUT WHAT ELSE?

Source: MultiAd Kwikee

Co

pyr

igh

t ©

2015

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

60

INNOVATING FOR LOWER PRICE POINT

Source: MultiAd Kwikee

10 oz standup bag

5 oz

0.95 oz packets

10 oz

9 oz standup bag

61

Co

pyr

igh

t ©

2015

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

CONSUMERS WILL PAY MORE IF THE BENEFITS OUTWEIGH THE PRICE

Sources: MultiAd Kwikee

Co

pyr

igh

t ©

2015

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

62

ACTIVATION

Develop a marketing plan and retail activation plan- Set goals and objective- Collaborate with your retailer and manufacturer partners

Create measurable objectives and track and report- Sales and shares- Customers- Consumer basics and purchase habits

Co

pyr

igh

t ©

2015

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

63

KEY TAKEAWAYSThe Spending Environment

• Socio-economic factors profoundly influence health behavior of chronic sufferers. The totalburden of healthcare falls on Genx & Boomers; Younger households see food as medicine

• Pocketbook Pressures: fixed expenses force some families to reduce household, food & discretionary spend

• What is the Spending Power Risk or Opportunity for your shoppers or consumers?

Co

pyr

igh

t ©

2015

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

CLOSING THOUGHTS

• Win the Trip: through superior shopper or consumer connection, innovation &/or operating excellence

• Retailing @ the Extremes: drives store expansion & product innovation efforts. How can you capitalize with new store offerings and formats?

• Chronic sufferers vary in market size and OTC opportunity: Diabetes Type II, Overactive Bladder and Osteo-Arthritis are the most productive OTC conditions to build programs around

• Large Sufferer groups include allergy, high blood pressure, imperfect vision and acid reflux: All possess US HH penetrations greater than 36M, offering significant customer acquisition opportunity for retailers and manufacturers

64

Questions or requests for additional information:Kristin Gorski, Director, Business [email protected]

APPENDIX

67

Co

pyr

igh

t ©

2015

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

SUMMARY OF U.S. RETAIL HOT BUTTONS

U.S. Retail Hot Buttons: July 27, 2015

Retail Landscape & Performance

Growth Challenges: Over the past four years, the only meaningful dollar growth (+4%) experienced by the (Nielsen-measured) fast-moving consumer-packaged goods market, was in the 52-week period ending June 30, 2012 when inflationary pressures had retailers accepting manufacturer price increases as well as passing on increases on their own-brand products. Over the past three 52-week periods, dollar sales grew by about 2%. Low unit sales growth has been more problematic with no growth over the last two 52-week periods. In an economic recovery, shouldn’t we expect more growth or is flat or slow growth the best we can expect?

Dollar sales across all measured channels grew 2.49% to $810.8 billion during 52-weeks ending June 27, 2015. Convenience and value-focused (i.e., club, dollar and mass-merchandisers) retail channels continue to show the strongest growth in dollar sales, up 4.2% and 2.8% respectively. Supermarkets (up 1.9%) aren’t lagging too far behind, while drug store sales were flat (up 0.1%).

New store openings and closings are key drivers of retail channel and retailer sales levels and trends. Most leading retailers within the major retail channels of mass-merchandisers, drugstores, warehouse clubs, and dollar stores have been expanding their store count over the past several years. The supermarket channel is the exception as store expansion has come mostly from niche players as well as from regional mainstream supermarkets.

68

Co

pyr

igh

t ©

2015

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

SUMMARY OF U.S. RETAIL HOT BUTTONS

U.S. Retail Hot Buttons: July 27, 2015

Retail Landscape & Performance (con’t)

When we compare winning retailers with how the various retail channels are connected with households across the economic spectrum, retail performance is linked to the spending power of households who shop retail channels. That is, sales within club, pet, hardware/home improvement, and online retail channels are skewed to the more affluent shopper. Many retailers within those channels are driving stronger same-store-sales growth than retailers in channels where sales are driven by lower and middle income shoppers.

Retail 2019 – What’s In Store?

When we use historical data to project future retail channel growth, e-commerce will be the big winner, but sporting goods, pet, dollar, auto, discount department, convenience/gas, and club will also drive strong CAGRs (compounded annual growth rates – dollar basis) between 2014 and 2019 – between 12.3% and 4.1%, respectively and at or above the average for the industry (+4.1%).

As a retailer, do you know where your future competition is coming from? As a manufacturer, how are you managing your sales support with retail accounts where growth will either be an opportunity or a challenge?

69

Co

pyr

igh

t ©

2015

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

SUMMARY OF U.S. RETAIL HOT BUTTONS (CON’T)

U.S. Retail Hot Buttons: July 27, 2015

What’s Selling – Long-Term Trends

Over the past four years, salty snacks, candy, beer & malt beverages and new age beverages had the biggest gains in absolute dollar sales, and demand shifts are behind those gains. Salty snacks growing as U.S. consumers have increased snacking occasions at the expense of main meals. Growth in fresh produce as we look to lead healthier lifestyles, but inflationary pressures at work here as well. Candy an coffee have experienced a lot of price pressure from high commodity input costs, but they have also responded with innovation – particularly in premium segments.

In terms of categories with the biggest losses, rather than purchasing recorded movies on DVDs, consumer demand has shifted to downloading via the internet. Smartphones are being used to take pictures, so camera and film sales have suffered. We are reading more on-line, so a decline in magazine sales. The cereal category is still huge, but consumers are changing their breakfast eating habits and the category is losing sales.

70

Co

pyr

igh

t ©

2015

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

SUMMARY OF U.S. RETAIL HOT BUTTONS (CON’T)

U.S. Retail Hot Buttons: July 27, 2015

What’s Selling – Short-Term Trends

Inflationary pressures from rising commodity prices has driven growth in some major departments, but consumer demand and increased retailer focus are driving forces too, particularly in departments like alcoholic beverages and perimeter fresh departments including prepared snacks and meals. Elevated prices and increased demand in some segments are behind the growth in fresh meat, but an increase in fixed-weight/prepackaged fresh meat is a factor too. The net impact is that some retailers are winning away-from-home eating occasions, but at the expense of center store categories used to prepare meals and snacks. As one industry analyst claimed, the “power of now” is a driver of consumer spending.

In terms of unit trends, trends are generally softer versus dollar trend metrics as consumers continue to make trade-offs or buy less – particularly in center store categories.