Embed Size (px)

Citation preview

Handbook Cover Photos:1. Lancaster Lincoln - HCMC

2. Spirit of Saigon - HCMC

3. Lancaster Legacy - HCMC

4. Vietcapital Tower - HCMC

5. Empire City - HCMC

14

2

3 5

AR

CA

DIS

VIE

TNA

M C

O.,

LTD

2

3

Copyright Statement and information ca-veat

Tenth Edition 2017

© Arcadis Vietnam Co., Ltd

All rights reserved. No part of this publication may be produced, copied, stored or transmitted in any form without prior written permission from Arcadis Vietnam Co., Ltd.

handbook are current as at 4th Quarter 2016.

The information contained herein should be regarded as indicative and for general guidance only. Arcadis Vietnam Co., Ltd. makes no representation, expressed or implied, with regard to the accuracy of the information herein and cannot accept any responsibility or liability for any errors or omissions that may be made.

AR

CA

DIS

VIE

TNA

M C

O.,

LTD

4

TABLE OF CONTENTS

Table of ContentsCalendarsIntroduction

1. CONSTRUCTION COST DATA

Construction Market 2017 OutlookMajor Rates for Selected Asian CitiesConstruction Cost SpecificationConstruction Costs for Selected Asian CitiesM&E Costs for Selected Asian CitiesUtility Costs for Selected Asian Cities

2. GENERAL CONSTRUCTION DATA

Material Price IndicesImport DutiesProgress PaymentsEstimating Rules of Thumb

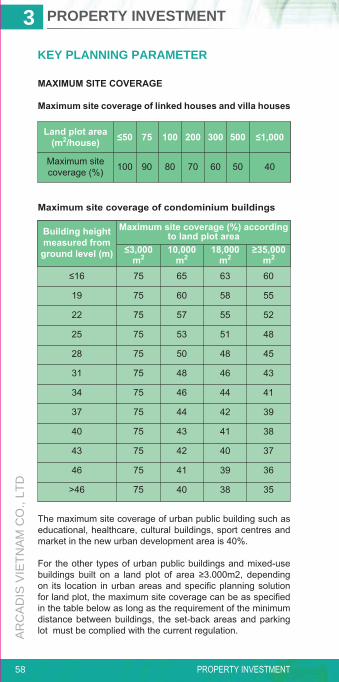

3. PROPERTY INVESTMENT

Building Control and ProceduresProject Closed Out ProceduresTypical Submission FlowchartKey Planning ParameterBuilding Areas DefinitionsProcurement StrategiesContractor Selection StrategiesProperty Overview

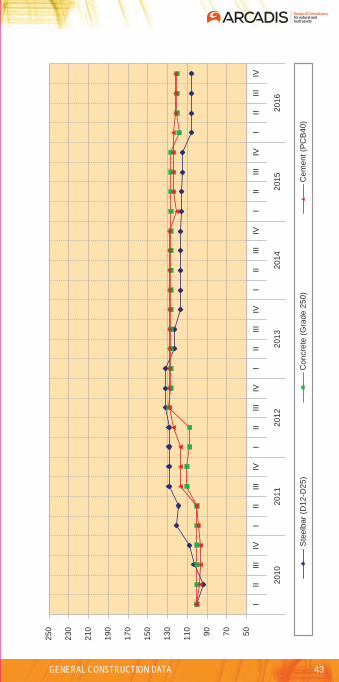

Page No.

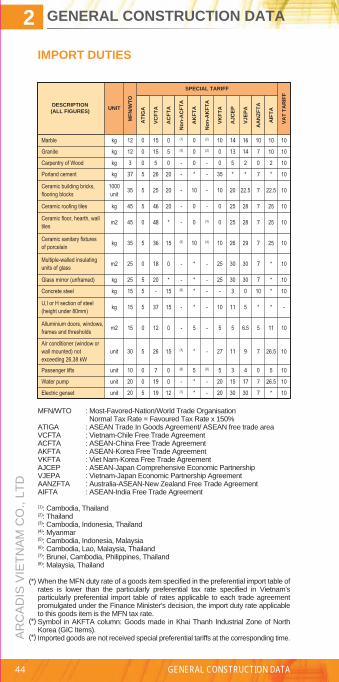

467

101622243036

42444546

5256575861667176

5

4. VIETNAM BUSINESS ENVIRONMENT

LanguageAccounting SystemBanksGovernment AdministrationTaxationInsuranceWorkforce

5. OTHER INFORMATION

Vietnam MapDomestic RoutesVietnam Key DataSome Interesting FactsRelevant WebsitesPublic HolidaysPrime RatesFinancial FormulaeIDD Codes and Time DifferencesConversion FactorsArcadis Asia Leadership TeamArcadis Asia SectorsArcadis Asia ServicesDirectory of officesAcknowledgement

Page No.

909091939499

105

108109110114116118128129130132134136140142158

AR

CA

DIS

VIE

TNA

M C

O.,

LTD

6 CALENDARS

CALENDARS

7INTRODUCTION

INTRODUCTION

This version of Arcadis Handbook - Vietnam 2017, as other future annually published handbooks, focuses on the construction cost profile of Vietnam and those of the major cities in Asia.

The handbook is structured to serve as a general reference guide on construction cost indicators in Asia.

The information contained in this handbook has been compiled by Arcadis Vietnam Co., Ltd. Any further information and/or if advice relating to particular projects in specific region is required, please contact any of the regional offices listed under the Directory of Arcadis Offices at the end of this handbook.

Arcadis Vietnam Co., Ltd.

Construction Market 2017 Outlook

Major Rates for Selected Asian Cities

Construction Costs for Selected Asian Cities

M&E Costs for Selected Asian Cities

Utility Costs for Selected Asian Cities

CONSTRUCTION COST DATA1

AR

CA

DIS

VIE

TNA

M C

O.,

LTD

1 CONSTRUCTION COST DATA

CONSTRUCTION COST DATA10

CONSTRUCTION MARKET 2017 OUTLOOK

In 2016 we at ARCADIS have seen our business expand significantly in: Project & Construction Management, Water Management and Environmental Management. Also and happily our sister company Callison RTKL have made great inroads into the Architectural market.

Our rapid expansion in 2016 is a function of renewed optimism within the Vietnam market. Foreign interest has increased and consequently we have seen growth in Foreign Investment and also the domestic market is picking up. The banking sectors non-performing loans issues are being rectified and as consequence we do expect an improvement in money supply into the domestic economy.

We think Vietnam will still expand as a manufacturing export growth economy in 2017 however the US withdrawal from the Trans Pacific Partnership will have some effects on manufacturing output.

Vietnams GDP growth in 2017 will remain quite strong at circa 6.5% and thus it will remain one of the Asia regions best performers.

11CONSTRUCTION COST DATA

ANNUAL FOREIGN INVESTMENT

0500

1000

1500

2000

2500

3000

'00

'01

'02

'03

'04

'05

'06

'07

'08

'09

'10

'11

'12

'13

'14

'15

'16

(Nos

. of p

roje

cts)

0

100 80 60 40 20(bn

US$

)

‘00

2.84

1.31

391

‘01

3.14

1.71

555

‘02

3.00

1.27

808

‘03

3.19

1.14

791

‘04

4.55

1.22

811

‘05

6.84

1.97

970

‘06

12.0

0

4.67

987

‘07

21.3

0

6.04

1544

‘08

71.7

3

11.5

0

1557

‘09

22.6

3

10.0

0

1155

‘10

18.6

0

11.0

0

969

‘11

12.7

0

10.0

5

919

‘12

12.1

8

10.0

0

980

‘13

20.8

2

10.5

5

1175

‘14

20.2

3

12.3

5

1588

‘15

22.7

6

14.5

0

2013

‘16

24.3

7

15.8

0

2556

Year

R

egis

tere

d C

apita

l (bn

US

$)

Le

gal C

apita

l (bn

US

$)

N

o. o

f Pro

ject

s

AR

CA

DIS

VIE

TNA

M C

O.,

LTD

1 CONSTRUCTION COST DATA

CONSTRUCTION COST DATA12

Taiw

an

1,86

0.16

122.

00

Mal

aysi

a

914.

03

40.0

0

Japa

n

2,58

9.86

341.

00

S.Ko

rea

7,03

6.30

828.

00

Sing

apor

e

2,41

9.09

210.

00

B.V.

Isla

nds

858.

24

48.0

0

Hon

g Ko

ng

1,64

0.15

166.

00

Thai

land

706.

50

35.0

0

Unite

d St

ates

400.

40

64.0

0

Chi

na

1,87

5.22

278.

00

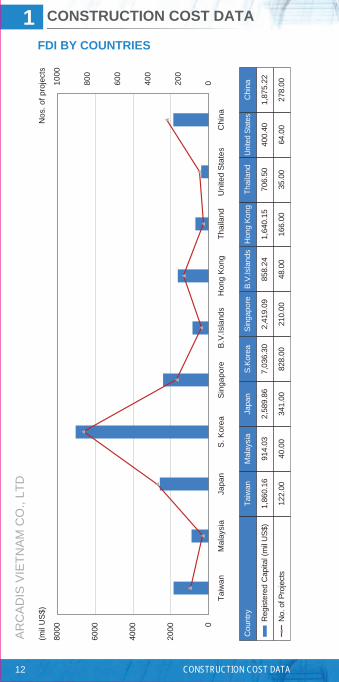

FDI BY COUNTRIES

Taiw

anM

alay

sia

Japa

nS

. Kor

eaS

inga

pore

B.V

.Isla

nds

Hon

g K

ong

Thai

land

Uni

ted

Sta

tes

Chi

na020

0

400

600

800

1000

Nos

. of p

roje

cts

0

2000

4000

6000

8000

(mil

US

$)

Cou

ntry

R

egis

tere

d C

apita

l (m

il U

S$)

N

o. o

f Pro

ject

s

13CONSTRUCTION COST DATA

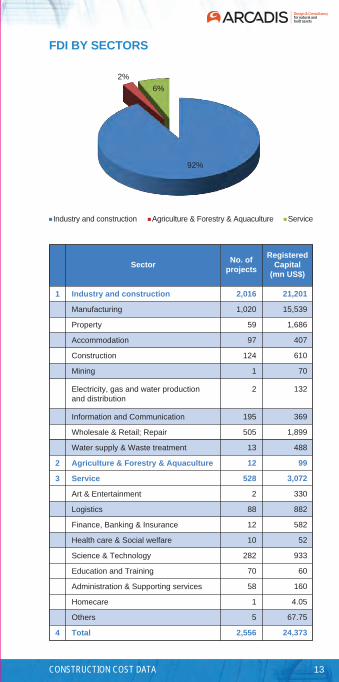

FDI BY SECTORS

92%

2%6%

Industry and construction Agriculture & Forestry & Aquaculture Service

Sector No. ofprojects

RegisteredCapital

(mn US$)

1

2

3

4

Industry and construction

Manufacturing

Property

Accommodation

Construction

Mining

Electricity, gas and water productionand distribution

Information and Communication

Wholesale & Retail; Repair

Water supply & Waste treatment

Agriculture & Forestry & Aquaculture

Service

Art & Entertainment

Logistics

Finance, Banking & Insurance

Health care & Social welfare

Science & Technology

Education and Training

Administration & Supporting services

Homecare

Others

Total

2,016

1,020

59

97

124

1

2

195

505

13

12

528

2

88

12

10

282

70

58

1

5

2,556

21,201

15,539

1,686

407

610

70

132

369

1,899

488

99

3,072

330

882

582

52

933

60

160

4.05

67.75

24,373

Billio

n U

S$

AR

CA

DIS

VIE

TNA

M C

O.,

LTD

1 CONSTRUCTION COST DATA

CONSTRUCTION COST DATA14

‘00

1.77

1.65

‘01

2.41

1.50

‘02

1.81

1.53

‘03

1.76

1.42

‘04

5.57

1.65

‘05

2.52

1.79

‘06

2.82

1.79

‘07

3.80

2.18

‘08

3.46

2.14

‘09

5.40

4.10

‘10

3.40

3.54

‘11

6.80

3.65

‘12

5.87

4.18

‘13

6.60

5.13

‘14

4.38

5.66

‘15

3.50

5.00

‘16

5.38

3.70

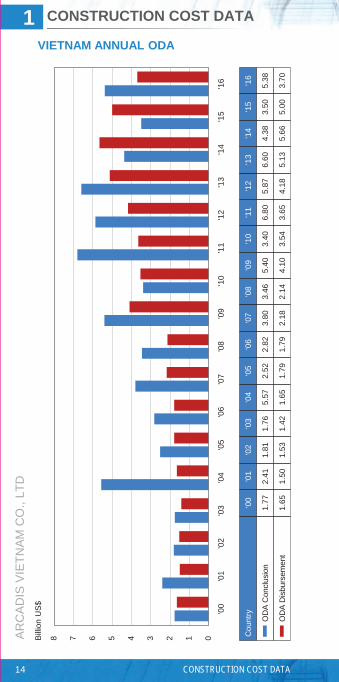

VIETNAM ANNUAL ODA

012345678

'00

'01

'02

'03

'04

'05

'06

'07

'08

'09

'10

'11

'12

'13

'14

'15

'16

Cou

ntry

O

DA

Con

clus

ion

O

DA

Dis

burs

emen

t

15CONSTRUCTION COST DATA

CONSTRUCTION VALUE

‘00

7.51

1.63

‘01

12.7

8

1.94

‘02

10.5

7

2.07

‘03

10.5

9

2.39

‘04

9.03

2.82

‘05

10.8

0

3.36

‘06

11.0

5

4.03

‘07

12.1

0

4.95

‘08

0.02

5.83

‘09

11.3

6

6.19

‘10

10.0

6

7.26

‘11

(0.9

7)

7.86

‘12

2.09

8.59

‘13

5.83

9.14

‘14

7.07

9.80

‘15

10.8

2

10.3

9

‘16

9.10

7.01-24681012%

(2)-2468101214Billio

n U

S$

Cou

ntry

C

onst

ruct

ion,

Rea

l Gro

wth

C

onst

ruct

ion

Valu

e

'00

'01

'02

'03

'04

'05

'06

'07

'08

'09

'10

'11

'12

'13

'14

'15

'16

DES

CR

IPTI

ON

MAN

ILA

INDI

A₲

JAK

AR

TA#

HO

CH

I MIN

H#

SEO

UL

$UN

ITPH

PIN

RID

RVN

DK

RW

1. Ex

cava

ting b

asem

ent ≤

2.00

m de

ep

2. Ex

cava

ting f

or fo

oting

s ≤ 1.

50m

deep

3. Re

move

exca

vated

mate

rials

off si

te

4. Ha

rdco

re be

d blin

ded w

ith fin

e mate

rials

5. Ma

ss co

ncre

te gr

ade 1

5

6. Re

infor

ced c

oncre

te gr

ade 3

0

7. Mi

ld ste

el ro

d rein

force

ment

8. Hi

gh te

nsile

rod r

einfor

ceme

nt

9. Sa

wn fo

rmwo

rk to

soffit

s of s

uspe

nded

slab

s

10. S

awn f

ormw

ork t

o colu

mns a

nd w

alls

11. 1

12.5m

m thi

ck br

ick w

alls

m3 m3 m3 m3 m3 m3 kg kg m2 m2 m2

250

280

145

850

2,800

3,600 41 42 1,000

950

N/A

185

210

N/A

4,350

5,850

7,150 66 68 650

700

1,050

35,00

0

60,00

0

25,00

0

400,0

00

1,000

,000

980,0

00

8,500

8,500

190,0

00

170,0

00

200,0

00

92,40

0

92,40

0

84,70

0

280,9

00

1,696

,400

1,955

,800

16,80

0

16,00

0

201,8

00

198,9

00

312,7

80

1,990

1,990

10,10

0

30,00

0

66,00

0

80,00

0

1,280

1,310

30,00

0

30,00

0

46,00

0

AR

CA

DIS

VIE

TNA

M C

O.,

LTD

1 CONSTRUCTION COST DATA

CONSTRUCTION COST DATA16

MAJOR RATES FOR SELECTED ASIAN CITIES

The

abov

e co

sts

are

at 4

th Q

uart

er 2

016

leve

ls a

nd a

re b

ased

on

lum

p su

m fi

xed

pric

e co

ntra

ct ra

tes

excl

usiv

e of

pre

limin

arie

s an

d co

ntin

genc

ies.

Ω R

ate

for a

lum

iniu

m w

ith a

nodi

zed

finis

h; 6

mm

thic

k.

₲

All

rate

s ab

ove

are

Sup

ply

and

Fix,

bas

ed o

n pr

ojec

ts in

Ban

galo

re a

nd

ar

e ne

tt of

VA

T an

d S

ervi

ce T

ax. M

umba

i cos

ts a

re g

ener

ally

8%

hig

her.

# R

ates

are

net

t of V

AT.

æ

Rat

e fo

r 9m

m g

ypsu

m b

oard

.

$ R

ates

incl

ude

labo

ur c

osts

and

are

net

t of V

AT.

12. “

Kliplo

k Colo

rbond

” 0.64

mm pr

ofiled

stee

l she

eting

13. A

lumini

um ca

seme

nt wi

ndow

s, sin

gle gl

azed

14. S

tructu

ral st

eelw

ork - b

eams

, stan

chion

s and

the l

ike

15. S

teelw

ork - a

ngles

, cha

nnels

, flats

and t

he lik

e

16. 2

5mm

ceme

nt an

d san

d (1:3

) pav

ing

17. 2

0mm

ceme

nt an

d san

d (1:4

) plas

ter to

wall

s

18. C

erami

c tile

s bed

ded t

o floo

r scre

ed (m

/s)

19. 1

2mm

fibrou

s plas

terbo

ard ce

iling l

ining

20. T

wo co

ats of

emuls

ion pa

int to

plas

tered

surfa

ces

Avera

ge ex

pecte

d prel

imina

ries

m2 m2 kg kg m2 m2 m2 m2 m2 %

401,1

10 - 5

97,60

0

6,315

,000

52,65

0

52,65

0

73,20

0

144,0

00

674,1

80

205,9

20

88,90

0

8 - 12

1,100

10,50

0

125

125

400

360

1,600

1,090

370

12 -

18

1,650

5,750

110

110

450

380

1,650

1,300

230

8 - 12

250,0

00

1,500

,000

21,00

0

21,00

0

80,00

0

90,00

0

160,0

00

180,0

00

25,00

0

8 - 10

40,00

0

330,0

00

1,710

1,710

3,200

9,500

66,00

0

27,00

0

8,100

6 - 11

æ

Ω

17CONSTRUCTION COST DATA

(Cont'd)

DES

CR

IPTI

ON

SHA

NG

HA

IB

EIJI

NG

GU

AN

GZH

OU

/SH

ENZH

ENH

ON

G K

ON

GC

HO

NG

QIN

G/

CH

ENG

DU

UNIT

RM

BR

MB

RM

BH

K$

RM

B

1. Ex

cava

ting b

asem

ent ≤

2.00

m de

ep

2. Ex

cava

ting f

or fo

oting

s ≤ 1.

50m

deep

3. Re

move

exca

vated

mate

rials

off si

te

4. Ha

rdco

re be

d blin

ded w

ith fin

e mate

rials

5. Ma

ss co

ncre

te gr

ade 1

5

6. Re

infor

ced c

oncre

te gr

ade 3

0

7. Mi

ld ste

el ro

d rein

force

ment

8. Hi

gh te

nsile

rod r

einfor

ceme

nt

9. Sa

wn fo

rmwo

rk to

soffit

s of s

uspe

nded

slab

s

10. S

awn f

ormw

ork t

o colu

mns a

nd w

alls

11. 1

12.5m

m thi

ck br

ick w

alls

m3 m3 m3 m3 m3 m3 kg kg m2 m2 m2

30 30

100 -

180

165

320

420

3.8 3.8 85 85 85

26 31 37 170

433

430

4.1 4.1 85 73 72

30 25 65 180

460

498

5.3 5.3 80 80 60

225

205

280

950

1,150

1,350 9.2 9.2 420

420

420

18 25 58 160

300

320

3.7 3.7 50 50 65

δ

@

AR

CA

DIS

VIE

TNA

M C

O.,

LTD

1 CONSTRUCTION COST DATA

CONSTRUCTION COST DATA18

MAJOR RATES FOR SELECTED ASIAN CITIES

The

abov

e co

sts

are

at 4

th Q

uart

er 2

016

leve

ls a

nd a

re b

ased

on

lum

p su

m fi

xed

pric

e co

ntra

ct ra

tes

excl

usiv

e of

pre

limin

arie

s an

d co

ntin

genc

ies.

δ R

ates

incl

udin

g du

mpi

ng c

harg

es.

@ R

ates

for 1

20m

m th

ick

conc

rete

blo

ck w

alls

.

* R

ates

for d

oubl

e gl

azed

win

dow

.

12. “

Kliplo

k Colo

rbond

” 0.64

mm pr

ofiled

stee

l she

eting

13. A

lumini

um ca

seme

nt wi

ndow

s, sin

gle gl

azed

14. S

tructu

ral st

eelw

ork - b

eams

, stan

chion

s and

the l

ike

15. S

teelw

ork - a

ngles

, cha

nnels

, flats

and t

he lik

e

16. 2

5mm

ceme

nt an

d san

d (1:3

) pav

ing

17. 2

0mm

ceme

nt an

d san

d (1:4

) plas

ter to

wall

s

18. C

erami

c tile

s bed

ded t

o floo

r scre

ed (m

/s)

19. 1

2mm

fibrou

s plas

terbo

ard ce

iling l

ining

20. T

wo co

ats of

emuls

ion pa

int to

plas

tered

surfa

ces

Avera

ge ex

pecte

d prel

imina

ries

m2 m2 kg kg m2 m2 m2 m2 m2 %

880

3,500 34 38 140

150

380

570 65

10 -

15

N/A

700

8.5 7.5 30 30 155

150 40 5 -

10

N/A

815

9.35

8.5 27 28 140

162 32 7 -

10

N/A

525

12.2 8.4 30 25 150

180 30 5 -

10

N/A

600

8.3 8.3 22 32 120

120 35 5 -

10

**

19CONSTRUCTION COST DATA

(Cont'd)

DES

CR

IPTI

ON

SIN

GA

POR

E ♣

KU

ALA

LUM

PUR

BR

UN

EIM

AC

AU

BA

NG

KO

K ⱷ

UNIT

S$R

MB

$M

OP

THB

1. Ex

cava

ting b

asem

ent ≤

2.00

m de

ep

2. Ex

cava

ting f

or fo

oting

s ≤ 1.

50m

deep

3. Re

move

exca

vated

mate

rials

off si

te

4. Ha

rdco

re be

d blin

ded w

ith fin

e mate

rials

5. Ma

ss co

ncre

te gr

ade 1

5

6. Re

infor

ced c

oncre

te gr

ade 3

0

7. Mi

ld ste

el ro

d rein

force

ment

8. Hi

gh te

nsile

rod r

einfor

ceme

nt

9. Sa

wn fo

rmwo

rk to

soffit

s of s

uspe

nded

slab

s

10. S

awn f

ormw

ork t

o colu

mns a

nd w

alls

11. 1

12.5m

m thi

ck br

ick w

alls

m3 m3 m3 m3 m3 m3 kg kg m2 m2 m2

20 20

15 -

20

50

190 -

200

125 -

130

1 - 1.

2

1 - 1.

2

42 42

35 -

40

15 -

22

15 -

22

20 -

25

60 -

70

240 -

280

260 -

320

2.9 -

3

2.9 -

3

38 -

45

38 -

45

45 -

52

3.5 3 3 43 115

130

0.9 0.9 15 15 16

130

150

100

1,200

1,350

1,250 7 7 250

250

450

140

160

120

650

2,200

2,400 23 22 420

420

450

♣♣

AR

CA

DIS

VIE

TNA

M C

O.,

LTD

1 CONSTRUCTION COST DATA

CONSTRUCTION COST DATA20

MAJOR RATES FOR SELECTED ASIAN CITIES

The

abov

e co

sts

are

at 4

th Q

uart

er 2

016

leve

ls a

nd a

re b

ased

on

lum

p su

m fi

xed

pric

e co

ntra

ct ra

tes

excl

usiv

e of

pre

limin

arie

s an

d co

ntin

genc

ies.

♣ R

ates

are

net

t of G

ST.

♣♣ R

ate

for l

ean

conc

rete

blin

ding

.

ⱷ

Rat

es a

re n

ett o

f VA

T.

12. “

Kliplo

k Colo

rbond

” 0.64

mm pr

ofiled

stee

l she

eting

13. A

lumini

um ca

seme

nt wi

ndow

s, sin

gle gl

azed

14. S

tructu

ral st

eelw

ork - b

eams

, stan

chion

s and

the l

ike

15. S

teelw

ork - a

ngles

, cha

nnels

, flats

and t

he lik

e

16. 2

5mm

ceme

nt an

d san

d (1:3

) pav

ing

17. 2

0mm

ceme

nt an

d san

d (1:4

) plas

ter to

wall

s

18. C

erami

c tile

s bed

ded t

o floo

r scre

ed (m

/s)

19. 1

2mm

fibrou

s plas

terbo

ard ce

iling l

ining

20. T

wo co

ats of

emuls

ion pa

int to

plas

tered

surfa

ces

Avera

ge ex

pecte

d prel

imina

ries

m2 m2 kg kg m2 m2 m2 m2 m2 %

N/A

4,000 35 40 120

150

450

650

200 10

43 290

4.5 -

5.5

4.5 -

5.5

21 22 74 30

3.5 -

4

13 -

17

55 -

60

350 -

500

6.5 -

8

6.5 -

8

15 -

22

15 -

22

50 -

70

35 -

45

3.5 -

4.5

6 - 12

58

160 -

210

3.1 3.1 8 8 33 28 5 5 - 8

1,200

7,000 55 55 200

220

1,200

550

120

12 -

18

21CONSTRUCTION COST DATA

AR

CA

DIS

VIE

TNA

M C

O.,

LTD

1 CONSTRUCTION COST DATA

CONSTRUCTION COST DATA22

CONSTRUCTION COST SPECIFICATIONO

UTL

INE

SPEC

IFIC

ATI

ON

BU

ILD

ING

DO

MES

TIC

OFF

ICE

/C

OM

MER

CIA

L

HO

TELS

IND

UST

RIA

L

Apa

rtmen

ts, h

igh

rise,

ave

rage

sta

ndar

d

Apa

rtmen

ts, h

igh

rise,

hig

h en

d

Terr

aced

hou

ses,

ave

rage

sta

ndar

d

Det

ache

d ho

uses

, hig

h en

d

Apar

tmen

t uni

ts w

ith fi

t-out

, inc

ludi

ng a

ir-co

nditi

onin

g, k

itche

n ca

bine

ts a

nd h

ome

appl

ianc

es,

but e

xclu

ding

dec

orat

ive

light

fitti

ngs

and

loos

e fu

rnitu

reAp

artm

ent u

nits

with

goo

d qu

ality

fit-o

ut, i

nclu

ding

air-

cond

ition

ing,

kitc

hen

cabi

nets

and

hom

e ap

plia

nces

, but

exc

ludi

ng d

ecor

ativ

e lig

ht fi

tting

s an

d lo

ose

furn

iture

Hou

ses

with

fit-o

ut, i

nclu

ding

air-

cond

ition

ing,

kitc

hen

cabi

nets

and

hom

e ap

plia

nces

, but

ex

clud

ing

deco

rativ

e lig

ht fi

tting

s, lo

ose

furn

iture

, gar

den

and

park

ing

Hou

ses

with

goo

d qu

ality

fit-o

ut, i

nclu

ding

air-

cond

ition

ing,

kitc

hen

cabi

nets

and

hom

e ap

plia

nces

, but

exc

ludi

ng d

ecor

ativ

e lig

ht fi

tting

s, lo

ose

furn

iture

, gar

den

and

park

ing

Med

ium

/hig

h ris

e of

fices

, ave

rage

sta

ndar

dH

igh

rise

offic

es, p

rest

ige

qual

ityO

ut-o

f-tow

n sh

oppi

ng c

entre

, ave

rage

sta

ndar

dR

etai

l mal

ls, h

igh

end

RC

stru

ctur

e, c

urta

in w

all,

incl

udin

g pu

blic

are

a fit

-out

, ten

ant a

rea

with

rais

ed fl

oor/c

arpe

t,pa

inte

d w

all a

nd fa

lse

ceili

ng

Incl

udin

g pu

blic

are

a fit

-out

and

M&

E, b

ut e

xclu

ding

sho

p fit

-out

Indu

stria

l uni

ts, s

hell

only

(Con

vent

iona

l sin

gle

stor

ey fr

amed

uni

ts)

Ow

ner o

pera

ted

fact

orie

s, lo

w ri

se, li

ght w

eigh

t indu

stry

RC

stru

ctur

e w

ith s

teel

roof

and

M&E

to m

ain

dist

ribut

ion,

but

exc

ludi

ng a

/c, h

eatin

g an

d lig

htin

g

RC

stru

ctur

e, in

clud

ing

smal

l offi

ce w

ith s

impl

e fit

-out

and

M&

E, b

ut e

xclu

ding

a/c

and

hea

ting

Bud

get h

otel

s - 3

-sta

r, m

id m

arke

t

Bus

ines

s ho

tels

- 4/

5-st

ar

Luxu

ry h

otel

s - 5

-sta

r

1) In

terio

r dec

orat

ion

2) F

urni

ture

(fix

ed a

nd m

ovab

le)

3) S

peci

al li

ght f

ittin

gs (c

hand

elie

rs, e

tc.)

4) O

pera

ting

Sup

plie

s an

d E

quip

men

t (O

S&

E) e

xclu

ded

23CONSTRUCTION COST DATA

OTH

ERS

RC

stru

ctur

e

RC

stru

ctur

e, n

atur

al v

entil

aion

, no

faca

de e

nclo

sure

Incl

udin

g fit

-out

and

a/c

, but

exc

ludi

ng e

duca

tiona

l equ

ipm

ent

Incl

udin

g fit

-out

, loo

se fu

rnitu

re a

nd a

/c

Dry

spo

rts (

no s

wim

min

g po

ol)

and

are

for

'leis

ure

cent

re' t

ype

sche

mes

inc

ludi

ng m

ain

spor

ts h

all,

anci

llary

spo

rts fa

cilit

ies,

cha

ngin

g an

d sh

ower

s, re

stau

rant

/ ca

fe, b

ar, e

tc. C

osts

in

clud

e a/

c, F

urni

ture

, Fitt

ings

and

Equ

ipm

ent (

FF&

E).

Exc

ludi

ng m

edic

al a

nd o

pera

ting

equi

pmen

t

Und

ergr

ound

/bas

emen

t car

par

ks (<

3 le

vels

)

Mul

ti st

orey

car

par

ks, a

bove

gro

und

(<4

leve

ls)

Sch

ools

(prim

ary

and

seco

ndar

y)

Stu

dent

s' re

side

nces

Spo

rts c

lubs

, mul

ti pu

rpos

e sp

orts

/leis

ure

cent

res

(dry

spo

rts)

Gen

eral

hos

pita

ls -

publ

ic s

ecto

r

Not

es:

1. T

he c

osts

for

the

resp

ectiv

e ca

tego

ries

give

n ab

ove

are

aver

ages

bas

ed o

n fix

ed p

rice

com

petit

ive

tend

ers.

It m

ust b

e un

ders

tood

that

the

actu

al c

ost o

f a

build

ing

will

dep

end

upon

the

desi

gn a

nd m

any

othe

r fac

tors

and

may

var

y fro

m th

e fig

ures

sho

wn.

2. T

he c

osts

per

squ

are

met

re a

re b

ased

on

Con

stru

ctio

n Fl

oor A

reas

(CFA

) mea

sure

d to

the

outs

ide

face

of t

he e

xter

nal w

alls

/ ex

tern

al p

erim

eter

incl

udin

glif

t sha

fts, s

tairw

ells

, bal

coni

es, p

lant

room

s, w

ater

tank

s an

d th

e lik

e.3.

All

bulid

ings

are

ass

umed

to h

ave

no b

asem

ents

(exc

ept o

ther

wis

e st

ated

) and

are

bui

lt on

flat

gro

und,

with

nor

mal

soi

l and

site

con

ditio

n.

The

cost

exc

lude

s si

te fo

rmat

ion

wor

ks, e

xter

nal w

orks

, lan

d co

st, p

rofe

ssio

nal f

ees,

fina

nce

and

lega

l exp

ense

s.4.

The

sta

ndar

d fo

r eac

h ca

tego

ry o

f bui

ldin

g va

ries

from

regi

on to

regi

on a

nd d

o no

t nec

essa

ry fo

llow

that

of e

ach

othe

r.5.

All

cost

s ar

e in

US

$/m

2 C

FA. F

luct

uatio

n in

exc

hang

e ra

tes

may

lead

to c

hang

es in

con

stru

ctio

n co

sts

expr

esse

d in

U.S

. dol

lars

.

BU

ILD

ING

TYP

EHO

CHI

MIN

H &

IND

IA ₲

JAK

AR

TA $

SEO

UL

$M

AN

ILA

Ω

US$

/m2 C

FA

DO

MES

TIC

Apar

tmen

ts, hi

gh ris

e, av

erag

e stan

dard

Apar

tmen

ts, hi

gh ris

e, hig

h end

Terra

ced h

ouse

s, av

erag

e stan

dard

Detac

hed h

ouse

s, hig

h end

610 -

760

775 -

895

410 -

480

470 -

570

880 -

990

1,200

- 1,4

9078

0 - 92

51,5

00 -

1,950

525 -

600

795 -

955

360 -

385

475 -

500

692 -

784

954 -

1,07

736

7 - 47

799

8 - 1,

116

1,316

- 1.5

981,5

81 -

1,966

N/A

2,145

- 3,2

82

OFF

ICE/

CO

MM

ERC

IAL

Mediu

m/hig

h rise

offic

es, a

vera

ge st

anda

rdHi

gh ris

e offic

es, p

resti

ge qu

ality

Out-o

f-tow

n sho

pping

centr

e, av

erag

e stan

dard

Retai

l mall

s, hig

h end

710 -

825

820 -

1,12

0N/

A66

5 - 87

0

840 -

890

1,280

- 1,3

9075

0 - 88

01,1

00 -

1,250

395 -

430

495 -

525

385 -

420

540 -

585

683 -

756

1,007

- 1,1

2458

7 - 65

064

8 - 70

0

1,171

- 1,3

681,3

50 -

1.709

1,103

- 1,7

521,2

82 -

2,137

HO

TELS

Budg

et ho

tels -

3-sta

r, mi

d mar

ket

Busin

ess h

otels

- 4/5-

star

Luxu

ry ho

tels -

5-sta

r

1,330

- 1,6

20N/

A1,7

25 -

2,000

1,200

- 1,3

701,3

50 -

1,685

1,600

- 2,0

20

745 -

825

1,160

- 1,3

751,4

65 -

1,605

1,186

- 1,4

021,6

20 -

1,750

1,723

- 1,9

43

1,598

- 2,0

262,2

39 -

3,868

2,487

- 3,9

74

AR

CA

DIS

VIE

TNA

M C

O.,

LTD

1 CONSTRUCTION COST DATA

CONSTRUCTION COST DATA24

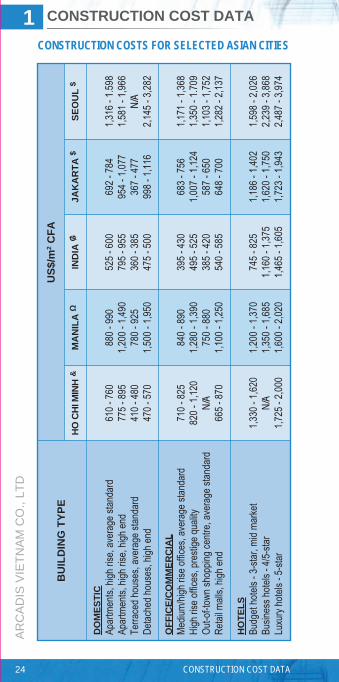

CONSTRUCTION COSTS FOR SELECTED ASIAN CITIES

IND

UST

RIA

LInd

ustria

l unit

s, sh

ell on

ly (C

onve

ntion

al sin

glesto

rey f

rame

d unit

s)Ow

ner o

pera

ted fa

ctorie

s, low

rise,

light

weigh

t ind

ustry

OTH

ERS

Unde

rgro

und/b

asem

ent c

ar pa

rks (<

3 lev

els)

Multi

store

y car

parks

, abo

ve gr

ound

(<4 l

evels

)Sc

hools

(prim

ary a

nd se

cond

ary)

Stud

ents'

resid

ence

sSp

orts

clubs

, mult

i pur

pose

spor

ts/lei

sure

centr

es(d

ry sp

orts)

Gene

ral h

ospit

als -

publi

c sec

tor

Exch

ange

Rate

Use

d : U

S$1 =

305 -

380

360 -

475

605 -

725

385 -

425

505 -

555

505 -

655

755 -

805

N/A

VND

22,60

0

450 -

460

560 -

650

510 -

560

460 -

600

690 -

760

700 -

800

1,200

- 1,4

50

1,350

- 1,5

00

PHP

48.60

310 -

365

330 -

385

260 -

280

200 -

220

250 -

280

280 -

310

550 -

575

600 -

660

INR

66

316 -

343

342 -

377

486 -

597

316 -

343

N/A

N/A

1,064

- 1,5

95

N/A

IDR

13,05

5

641 -

821

N/A

915 -

1,09

456

4 - 77

41,2

82 -

1,538

1,342

- 1,4

62N/

A

N/A

KRW

1,17

0

25CONSTRUCTION COST DATA

(Cont'd)

The

abov

e co

sts

are

at 4

th Q

uart

er 2

016

leve

ls, i

nclu

sive

of p

relim

inar

ies

but e

xclu

sive

of c

ontin

genc

ies.

Ω R

ates

incl

ude

12%

VA

T.

₲

Rat

es a

re b

ased

on

proj

ects

in B

anga

lore

and

are

net

t of V

AT

and

S

ervi

ce T

ax. M

umba

i cos

ts a

re g

ener

ally

8%

hig

her.

$ R

ates

are

net

t of V

AT.

&

Rat

es a

re n

ett o

f VA

T an

d co

ntig

enci

es.

AR

CA

DIS

VIE

TNA

M C

O.,

LTD

1 CONSTRUCTION COST DATA

CONSTRUCTION COST DATA26

CONSTRUCTION COSTS FOR SELECTED ASIAN CITIESB

UIL

DIN

G T

YPE

HONG

KO

NG £

BEI

JIN

G +

GU

AN

GZH

OU

/SH

ENZH

EN +

CH

ON

GQ

ING

/C

HEN

GD

U +

SHA

NG

HA

I +

US$

/m2 C

FA

DO

MES

TIC

Apar

tmen

ts, hi

gh ris

e, av

erag

e stan

dard

Apar

tmen

ts, hi

gh ris

e, hig

h end

Terra

ced h

ouse

s, av

erag

e stan

dard

Detac

hed h

ouse

s, hig

h end

3,140

- 3,6

904,2

40 -

4,940

4,310

- 5,0

305,5

80 -

6,350

634 -

704

1,550

- 1,6

9342

5 - 45

463

7 - 70

8

593 -

652

1,482

- 1,6

9043

2 - 50

665

5 - 73

0

491 -

541

816 -

898

370 -

410

507 -

559

445 -

593

786 -

1,02

237

3 - 52

250

6 - 59

6

OFF

ICE/

CO

MM

ERC

IAL

Mediu

m/hig

h rise

offic

es, a

vera

ge st

anda

rdHi

gh ris

e offic

es, p

resti

ge qu

ality

Out-o

f-tow

n sho

pping

centr

e, av

erag

e stan

dard

Retai

l mall

s, hig

h end

3,080

- 3,6

503,8

20 -

4,710

3,140

- 3,6

904,1

80 -

4,960

845 -

1,12

71,1

27 -

1,409

N/A

1,198

- 1,5

49

845 -

1,14

21,1

42 -

1,882

655 -

879

1,171

- 1,6

15

712 -

789

982 -

1,08

668

3 - 75

21,0

03 -

1,108

742 -

889

963 -

1,33

559

6 - 78

996

3 - 1,

364

HO

TELS

Budg

et ho

tels -

3-sta

r, mi

d mar

ket

Busin

ess h

otels

- 4/5-

star

Luxu

ry ho

tels -

5-sta

r

4,010

- 4,3

304,2

10 -

4,970

4,920

- 5,7

10

916 -

1,12

71,5

49 -

2,112

2,112

- 2,5

35

948 -

1,17

11,6

15 -

2,060

2,060

- 2,6

53

923 -

1,01

91,4

91 -

1,647

2,034

- 2,2

46

885 -

1,10

61,5

49 -

1,991

N/A

27CONSTRUCTION COST DATA

(Cont'd)

IND

UST

RIA

LInd

ustria

l unit

s, sh

ell on

ly (C

onve

ntion

al sin

glesto

rey f

rame

d unit

s)Ow

ner o

pera

ted fa

ctorie

s, low

rise,

light

weigh

t ind

ustry

OTH

ERS

Unde

rgro

und/b

asem

ent c

ar pa

rks (<

3 lev

els)

Multi

store

y car

parks

, abo

ve gr

ound

(<4 l

evels

)Sc

hools

(prim

ary a

nd se

cond

ary)

Stud

ents'

resid

ence

sSp

orts

clubs

, mult

i pur

pose

spor

ts/lei

sure

centr

es(d

ry sp

orts)

Gene

ral h

ospit

als -

publi

c sec

tor

Exch

ange

Rate

Use

d : U

S$1 =

N/A

2,410

- 3,0

60

2,370

- 2,9

501,4

70 -

1,730

2,590

- 2,8

102,5

40 -

2,950

3,970

- 4,4

90

5,130

- 5,8

30

HK$ 7

.80

491 -

560

N/A

708 -

993

353 -

496

496 -

637

353 -

496

916 -

1,12

7

1,409

- 1,8

30

RMB

6.78

506 -

581

N/A

730 -

804

432 -

506

506 -

655

357 -

506

875 -

1,17

1

1,171

- 1,4

68

RMB

6.78

466 -

513

N/A

471 -

754

336 -

370

373 -

413

239 -

264

695 -

768

N/A

RMB

6.78

417 -

522

N/A

N/A

268 -

342

N/A

N/A

N/A

N/A

RMB

6.78

The

abov

e co

sts

are

at 4

th Q

uart

er 2

016

leve

ls, i

nclu

sive

of p

relim

inar

ies

but e

xclu

sive

of c

ontin

genc

ies.

£ O

ffice

s of

ave

rage

sta

ndar

d ar

e bu

ilt to

the

follo

win

g pr

ovis

ions

:

(i

) C

urta

in w

all/w

indo

w w

all f

acad

e

(i

i) Te

nant

are

as in

clud

e sc

reed

ed fl

oor,

pain

ted

wal

l and

cei

ling

S

choo

ls (p

rimar

y an

d se

cond

ary)

are

of p

ublic

aut

horit

y st

anda

rd,

no

a/c

and

com

plet

e w

ith b

asic

ext

erna

l wor

ks.

+ H

ouse

s ar

e bu

ilt to

she

ll an

d co

re s

tand

ard

ON

LY, w

here

all

te

nant

or o

ccup

ant a

reas

are

unf

urni

shed

.

Sch

ools

(prim

ary

and

seco

ndar

y) a

re o

f pub

lic a

utho

rity

stan

dard

,

no a

/c a

nd c

ompl

ete

with

bas

ic e

xter

nal w

orks

.

AR

CA

DIS

VIE

TNA

M C

O.,

LTD

1 CONSTRUCTION COST DATA

CONSTRUCTION COST DATA28

CONSTRUCTION COSTS FOR SELECTED ASIAN CITIESB

UIL

DIN

G T

YPE

MAC

AU Ђ

BRUN

EIBA

NGKO

K œ

KUAL

ALU

MPU

R S

ING

APO

RE ♣

US$

/m2 C

FA

DO

MES

TIC

Apar

tmen

ts, hi

gh ris

e, av

erag

e stan

dard

Apar

tmen

ts, hi

gh ris

e, hig

h end

Terra

ced h

ouse

s, av

erag

e stan

dard

Detac

hed h

ouse

s, hig

h end

2,143

- 2,6

323,0

08 -

4,586

3,672

- 4,3

734,4

61 -

5,802

1,320

- 1,5

002,0

35 -

3,035

1,715

- 1,9

302,1

80 -

2,895

340 -

475

715 -

855

205 -

295

695 -

860

805 -

1,10

599

4 - 1,

294

520 -

821

792 -

1,09

2

614 -

742

913 -

1,08

542

8 - 51

474

2 - 89

9

OFF

ICE/

CO

MM

ERC

IAL

Mediu

m/hig

h rise

offic

es, a

vera

ge st

anda

rdHi

gh ris

e offic

es, p

resti

ge qu

ality

Out-o

f-tow

n sho

pping

centr

e, av

erag

e stan

dard

Retai

l mall

s, hig

h end

2,481

- 3,1

953,1

95 -

3,496

2,331

- 3,4

963,6

72 -

4,398

1,715

- 1,9

301,9

30 -

2,110

1,930

- 2,0

352,0

35 -

2,250

560 -

650

805 -

1,10

049

5 - 59

562

5 - 79

5

805 -

1,10

51,1

38 -

1,438

781 -

1,08

11,0

30 -

1,330

599 -

742

785 -

999

585 -

756

785 -

813

HO

TELS

Budg

et ho

tels -

3-sta

r, mi

d mar

ket

Busin

ess h

otels

- 4/5-

star

Luxu

ry ho

tels -

5-sta

r

3,258

- 3,6

844,4

24 -

5,288

5,288

- 6,2

53

2,145

- 2,3

602,7

50 -

3,110

2,750

- 3,1

10

935 -

1,30

51,6

15 -

1,890

1,800

- 2,0

95

1,521

- 1,8

212,1

46 -

2,446

2,203

- 2,5

03

1,071

- 1,1

841,3

70 -

1,570

1,598

- 1,7

12

♠ ♠

29CONSTRUCTION COST DATA

The

abov

e co

sts

are

at 4

th Q

uart

er 2

016

leve

ls, i

nclu

sive

of p

relim

inar

ies

but e

xclu

sive

of c

ontin

genc

ies.

Ђ R

ates

are

exc

lusi

ve o

f any

man

agem

ent c

ontra

ct fe

e.♣

Rat

es a

re n

ett o

f GS

T.♠

Incl

udes

rais

ed fl

oor a

nd c

eilin

g to

tena

nted

are

as b

ut

excl

udes

offi

ce c

arpe

ts (n

orm

ally

und

er te

nant

’s fi

t-out

).♥

Ope

n on

all

side

s w

ith p

arap

et.

6 - 1

2 un

its p

er fl

oor,

46m

2 - 8

3m2 p

er u

nit,

excl

ude

air-

cond

ition

ing

equi

pmen

t.

Te

rrac

ed h

ouse

s ex

clud

e ai

r-co

nditi

onin

g.

O

ffice

s ar

e av

erag

e st

anda

rd a

nd e

xclu

de te

nant

fito

ut.

Sch

ools

(prim

ary

and

seco

ndar

y) a

re s

tand

ard

gove

rnem

ent p

rovi

sion

s.♦

Stu

dent

host

els

to u

nive

rsity

sta

ndar

d.œ

Rat

es e

xclu

de V

AT.

IND

UST

RIA

LInd

ustria

l unit

s, sh

ell on

ly (C

onve

ntion

al sin

glesto

rey f

rame

d unit

s)Ow

ner o

pera

ted fa

ctorie

s, low

rise,

light

weigh

t ind

ustry

OTH

ERS

Unde

rgro

und/b

asem

ent c

ar pa

rks (<

3 lev

els)

Multi

store

y car

parks

, abo

ve gr

ound

(<4 l

evels

)Sc

hools

(prim

ary a

nd se

cond

ary)

Stud

ents'

resid

ence

sSp

orts

clubs

, mult

i pur

pose

spor

ts/lei

sure

centr

es(d

ry sp

orts)

Gene

ral h

ospit

als -

publi

c sec

tor

Exch

ange

Rate

Use

d : U

S$1 =

N/A

N/A

1,930

- 2,8

451,0

65 -

1,404

2,130

- 2,4

811,7

04 -

1,967

N/A

N/A

MOP

7.98

715 -

930

N/A

930 -

1,25

064

5 - 93

0N/

A1,5

70 -

1,715

1,965

- 2,1

10

2,750

- 2,8

95

S$ 1.

40

300 -

375

400 -

455

335 -

460

210 -

255

235 -

270

275 -

305

540 -

625

805 -

1,00

0

RM 4.

41

371 -

672

505 -

806

N/A

412 -

713

603 -

904

706 -

1,00

61,6

23 -

1,924

1,824

- 2,1

25

B$ 1.

36

457 -

571

N/A

514 -

671

171 -

274

N/A

N/A

N/A

N/A

THB

35.04

♥ ♦

AR

CA

DIS

VIE

TNA

M C

O.,

LTD

1 CONSTRUCTION COST DATA

CONSTRUCTION COST DATA30

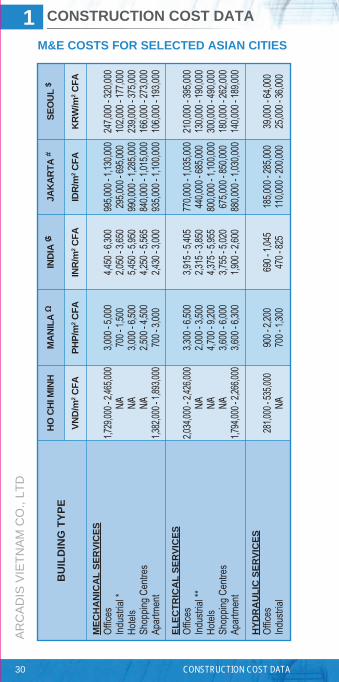

M&E COSTS FOR SELECTED ASIAN CITIESB

UIL

DIN

G T

YPE

VND/

m2 C

FAPH

P/m

2 CFA

INR/

m2 C

FAID

R/m

2 CFA

KRW

/m2 C

FA

HO C

HI M

INH

MAN

ILA

ΩIN

DIA

₲JA

KART

A #

SEO

UL $

MEC

HA

NIC

AL

SER

VIC

ESOf

fices

Indus

trial *

Hotel

sSh

oppin

g Cen

tres

Apar

tmen

t

1,729

,000 -

2,46

5,000

N/A N/A N/A1,3

82,00

0 - 1,

893,0

00

4,450

- 6,30

02,0

50 - 3

,650

5,450

- 5,95

04,2

50 - 5

,565

2,430

- 3,00

0

3,000

- 5,00

070

0 - 1,

500

3,000

- 6,50

02,5

00 - 4

,500

700 -

3,00

0

995,0

00 - 1

,130,0

0029

5,000

- 695

,000

990,0

00 - 1

,285,0

0084

0,000

- 1,01

5,000

935,0

00 - 1

,100,0

00

247,0

00 - 3

20,00

010

2,000

- 177

,000

239,0

00 - 3

75,00

016

6,000

- 273

,000

106,0

00 - 1

93,00

0

ELEC

TRIC

AL

SER

VIC

ESOf

fices

Indus

trial *

*Ho

tels

Shop

ping C

entre

sAp

artm

ent

2,034

,000 -

2,42

6,000

N/A N/A N/A1,7

94,00

0 - 2,

266,0

00

3,915

- 5,40

52,3

15 - 3

,850

4,375

- 5,95

53,7

55 - 5

,020

1,900

- 2,60

0

3,300

- 6,50

02,0

00 - 3

,500

4,700

- 9,20

03,6

00 - 6

,000

3,600

- 6,30

0

770,0

00 - 1

,035,0

0044

0,000

- 685

,000

800,0

00 - 1

,100,0

0067

5,000

- 850

,000

880,0

00 - 1

,030,0

00

210,0

00 - 3

95,00

013

0,000

- 190

,000

300,0

00 - 4

90,00

018

0,000

- 262

,000

140,0

00 - 1

89,00

0

HYD

RA

ULI

C S

ERVI

CES

Offic

esInd

ustria

l28

1,000

- 535

,000

N/A69

0 - 1,

045

470 -

825

900 -

2,20

070

0 - 1,

300

185,0

00 - 2

85,00

011

0,000

- 200

,000

39,00

0 - 64

,000

25,00

0 - 36

,000

31CONSTRUCTION COST DATA

(Cont'd)

Hotel

sSh

oppin

g Cen

tres

Apar

tmen

t

FIR

E SE

RVI

CES

Offic

es

Indus

trial

Hotel

sSh

oppin

g Cen

tres

Apar

tmen

t

LIFT

S/ES

CA

LATO

RS

Offic

es

Indus

trial

Hotel

sSh

oppin

g Cen

tres

Apar

tmen

t

N/A N/A54

7,000

- 648

,000

632,0

00 - 1

,049,0

00N/A N/A N/A

434,0

00 - 5

45,00

0

605,0

00 - 1

,154,0

00N/A N/A

1,231

,000 -

1,74

3,000

687,0

00 - 9

94,00

0

1,950

- 4,00

070

0 - 1,

600

1,400

- 2,70

0

700 -

1,30

065

0 - 90

070

0 - 1,

200

700 -

1,30

065

0 - 1,

300

1,600

- 3,50

0N/

A1,8

00 - 3

,300

700 -

2,00

080

0 - 2,

100

3,585

- 5,40

01,0

20 - 1

,845

1,615

- 2,23

5

1,095

- 1,43

052

5 - 69

01,2

75 - 1

,630

1,050

- 1,21

058

0 - 69

5

910 -

1,16

059

0 - 76

01,3

25 - 1

,925

1,545

- 1,99

082

5 - 1,

050

935,0

00 - 1

,100,0

0018

5,000

- 285

,000

935,0

00 - 1

,100,0

00

255,0

00 - 3

85,00

011

0,000

- 200

,000

310,0

00 - 3

85,00

026

0,000

- 305

,000

285,0

00 - 3

10,00

0

410,0

00 - 1

,110,0

00N/

A66

0,000

- 1,03

0,000

305,0

00 - 8

20,00

066

0,000

- 825

,000

80,00

0 - 12

3,000

32,00

0 - 64

,000

55,00

0 - 84

,000

36,00

0 - 70

,000

27,00

0 - 42

,000

41,00

0 - 91

,000

28,00

0 - 76

,000

39,00

0 - 74

,000

42,00

0 - 67

,000

16,00

0 - 26

,000

100,0

00 - 1

75,00

048

,000 -

84,00

029

,000 -

41,00

0

The

abov

e co

sts

are

at 4

th Q

uart

er 2

016

leve

ls, e

xclu

sive

of c

ontin

genc

ies.

* G

ener

ally

with

out A

/C.

** E

xclu

des

spec

ial p

ower

sup

ply.

₲ R

ates

are

bas

ed o

n pr

ojec

ts in

Ban

galo

re a

nd

are

nett

of V

AT

and

Ser

vice

Tax

. Mum

bai c

osts

ar

e ge

nera

lly 8

% h

ighe

r.

Ω T

rans

form

er, i

nclu

ded

in E

lect

rical

Ser

vice

s.#

All

rate

s ar

e ne

tt of

VA

T. R

ates

for E

lect

rical

Ser

vice

s ar

e ex

clud

ing

gens

et.

R

ates

for H

ydra

ulic

Ser

vice

s ar

e ex

clud

ing

STP

.

Rat

es fo

r Mec

hani

cal S

ervi

ces

refe

rs to

AC

MV

Rat

es o

nly.

$ R

ates

are

net

t of V

AT.

AR

CA

DIS

VIE

TNA

M C

O.,

LTD

1 CONSTRUCTION COST DATA

CONSTRUCTION COST DATA32

M&E COSTS FOR SELECTED ASIAN CITIESB

UIL

DIN

G T

YPE

HK$/

m2 C

FARM

B/m

2 CFA

RMB/

m2 C

FARM

B/m

2 CFA

RMB/

m2 C

FA

HONG

KO

NGSH

ANG

HAI

BEIJ

ING

GUA

NGZH

OU/

SHEN

ZHEN

CHO

NGQ

ING

/CH

ENG

DU

MEC

HA

NIC

AL

SER

VIC

ESOf

fices

Indus

trial *

Hotel

sSh

oppin

g Cen

tres

Apar

tmen

t

2,000

- 2,8

0020

0 - 30

02,2

00 -

2,750

2,300

- 2,8

5085

0 - 1,

750

760 -

1,05

017

0 - 28

091

0 - 1,

150

790 -

950

140 -

410

761 -

966

173 -

289

971 -

1,26

51,0

50 -

1,103

310 -

410

765 -

1,04

015

0 - 26

81,0

71 -

1,339

707 -

954

122 -

380

680 -

980

130 -

220

720 -

1,15

058

0 - 98

090

- 28

0

ELEC

TRIC

AL

SER

VIC

ESOf

fices

Indus

trial *

*Ho

tels

Shop

ping C

entre

sAp

artm

ent

1,750

- 2,5

0065

0 - 90

01,9

00 -

2,600

1,900

- 2,5

001,1

00 -

1,750

460 -

703

320 -

450

705 -

943

481 -

676

253 -

398

593 -

651

305 -

431

651 -

830

520 -

651

252 -

368

530 -

765

306 -

445

680 -

916

483 -

653

278 -

445

420 -

650

250 -

350

500 -

750

400 -

650

220 -

330

HYD

RA

ULI

C S

ERVI

CES

Offic

esInd

ustria

l70

0 - 90

050

0 - 70

095

- 14

095

- 14

011

0 - 16

389

- 13

112

2 - 16

686

- 11

260

- 12

060

- 12

0

33CONSTRUCTION COST DATA

(Cont'd)

Hotel

sSh

oppin

g Cen

tres

Apar

tmen

t

FIR

E SE

RVI

CES

Offic

es

Indus

trial

Hotel

sSh

oppin

g Cen

tres

Apar

tmen

t

LIFT

S/ES

CA

LATO

RS

Offic

es

Indus

trial

Hotel

sSh

oppin

g Cen

tres

Apar

tmen

t

2,000

- 3,0

0070

0 - 90

01,5

00 -

2,400

550 -

700

400 -

500

600 -

850

550 -

700

200 -

450

700 -

1,20

055

0 - 75

055

0 - 85

085

0 - 1,

000

450 -

850

368 -

488

137 -

184

168 -

226

220 -

300

150 -

250

280 -

380

250 -

380

50 -

100

280 -

550

135 -

390

220 -

495

325 -

495

165 -

325

370 -

480

140 -

200

170 -

230

180 -

265

150 -

225

220 -

375

220 -

375

70 -

135

294 -

577

145 -

400

232 -

520

327 -

520

175 -

289

391 -

493

112 -

150

145 -

257

224 -

348

139 -

267

278 -

413

247 -

370

64 -

122

294 -

481

150 -

434

241 -

465

326 -

460

122 -

268

280 -

350

60 -

120

100 -

180

160 -

230

130 -

230

180 -

300

200 -

300

45 -

90

330 -

580

140 -

340

280 -

480

280 -

430

130 -

230

The

abov

e co

sts

are

at 4

th Q

uart

er 2

016

leve

ls, e

xclu

sive

of c

ontin

genc

ies.

* G

ener

ally

with

out A

/C.

** E

xclu

des

spec

ial p

ower

sup

ply.

AR

CA

DIS

VIE

TNA

M C

O.,

LTD

1 CONSTRUCTION COST DATA

CONSTRUCTION COST DATA34

M&E COSTS FOR SELECTED ASIAN CITIESB

UIL

DIN

G T

YPE

MO

P/m

2 CFA

S$/m

2 CFA

RM/m

2 CFA

B$/m

2 CFA

THB/

m2 C

FA

MA

CAU

SIN

GAP

ORE

♣BR

UNEI

BAN

GKO

K ⱷ

KUAL

ALU

MPU

R

MEC

HA

NIC

AL

SER

VIC

ESOf

fices

Indus

trial *

Hotel

sSh

oppin

g Cen

tres

Apar

tmen

t

N/A

N/A

2,600

- 3,0

002,2

00 -

2,800

900 -

1,10

0

360 -

520

85 -

190

300 -

585

320 -

510

195 -

285

160 -

262

35 -

123

135 -

292

154 -

258

94 -

178

179 -

224

23 -

3928

9 - 33

320

5 - 24

421

2 - 24

4

4,400

- 4,8

001,5

50 -

1,600

4,600

- 5,1

004,4

00 -

4,800

4,400

- 4,5

00

ELEC

TRIC

AL

SER

VIC

ESOf

fices

Indus

trial *

*Ho

tels

Shop

ping C

entre

sAp

artm

ent

N/A

N/A

2,600

- 3,1

002,6

00 -

2,800

1,000

- 1,3

00

310 -

515

144 -

190

285 -

600

310 -

500

105 -

220

166 -

269

55 -

142

190 -

372

167 -

319

102 -

238

231 -

289

192 -

231

289 -

377

377 -

314

249 -

314

3,400

- 3,8

001,9

50 -

2,200

3,800

- 4,5

002,8

00 -

3,200

2,800

- 3,3

50

HYD

RA

ULI

C S

ERVI

CES

Offic

esInd

ustria

lN/

AN/

A26

- 60

37 -

4628

- 57

19 -

3816

- 39

11 -

1979

0 - 91

075

0 - 79

0

35CONSTRUCTION COST DATA

Hotel

sSh

oppin

g Cen

tres

Apar

tmen

t

FIR

E SE

RVI

CES

Offic

es

Indus

trial

Hotel

sSh

oppin

g Cen

tres

Apar

tmen

t

LIFT

S/ES

CA

LATO

RS

Offic

es

Indus

trial

Hotel

sSh

oppin

g Cen

tres

Apar

tmen

t

1,800

- 2,2

0060

0 - 80

01,5

00 -

2,000

N/A

N/A

900 -

1,10

060

0 - 80

025

0 - 30

0

N/A

N/A

600 -

800

450 -

700

450 -

600

95 -

181

48 -

8576

- 14

8

34 -

5824

- 53

29 -

5838

- 58

25 -

52

66 -

171

43 -

109

52 -

114

58 -

9543

- 11

9

180 -

250

26 -

3520

- 50

60 -

8045

- 65

65 -

9565

- 85

20 -

30

95 -

400

55 -

190

85 -

370

85 -

110

63 -

105

60 -

8312

- 41

38 -

59

32 -

3912

- 19

26 -

4932

- 65

26 -

51

9 - 32

4 - 19

12 -

4512

- 36

11 -

26

1,400

- 1,6

5079

0 - 95

01,2

00 -

1,400

780 -

850

730 -

750

780 -

890

780 -

820

720 -

850

1,100

- 1,3

50N/

A1,1

00 -

1,400

250 -

450

500 -

580

The

abov

e co

sts

are

at 4

th Q

uart

er 2

016

leve

ls, e

xclu

sive

of c

ontin

genc

ies.

* G

ener

ally

with

out A

/C.

** E

xclu

des

spec

ial p

ower

sup

ply.

♣ R

ates

are

net

t of G

ST

and

excl

udin

g B

AS

.ⱷ

B

ased

upo

n ne

tt en

clos

ed a

rea

and

nett

of V

AT.

CITYEXCHANGE

RATEELECTRICITY

DOMESTIC COMMERCIAL/INDUSTRIAL

US$1= US$/kWh US$/kWh

VND 22,600 0.11Ho Chi Minh 0.10 - 0.17 /0.06 - 0.11

Bangalore INR 66.00 0.042 - 0.098 0.117 - 0.122

New Delhi INR 66.00 0.061 - 0.128 0.137 - 0.158

Seoul KRW 1,170 0.05 - 0.16 0.06 - 0.09

Singapore

Kuala Lumpur

Bangkok

Manila

Brunei

Jakarta

S$ 1.40

RM 4.41

THB 35.04

PHP 48.60

B$ 1.39

IDR 13,055

0.14

0.049 - 0.13

0.053 - 0.112

0.21 - 0.22

0.009 - 0.13

0.112

0.14

0.086 - 0.10

0.076 - 0.078

0.21

0.065 - 0.182

0.112

AR

CA

DIS

VIE

TNA

M C

O.,

LTD

1 CONSTRUCTION COST DATA

CONSTRUCTION COST DATA36

UTILITY COSTS FOR SELECTED ASIAN CITIES

The above costs are at 4th Quarter 2016 levels.

Basis of Charges in Singapore (All rates are nett of GST) Electricity tariff is based on low tension power supply. Domestic water rate includes water conservation tax and water-borne fee and is an average for the 1st 40m3, exclude sanitary appliance fee. Non-domestic water rate includes water conservation tax and water-borne fee, exclude sanitary appliance fee. Unleaded fuel rate is for 98 Unleaded petrol as at 7 November 2016. Diesel fuel rate as at 7 November 2016.

Basis of Charges in Kuala Lumpur, Malaysia Unleaded fuel rate is for Unleaded petrol Ron 95.

Basis of Charges in Bangkok, Thailand Electricity (Domestic) = For normal tariff with consumption not exceeding 150kWh per month Fuel (Unleaded) = Gasohol 95

Basis of Charges in Brunei Electricity (Domestic) : Tariff effective from 1st Jan 2012. 1-10 kWh 10c, 11-60 kWh 8c, 61-100kWh 12c, above 100kWh 15c

Basis of Charges in Ho Chi Minh, Vietnam (All rates are VAT inclusive) Electricity : Domestic electricity rates are applied to the 301 KW above wards Fuel : Diesel fuel D.O - 0.05% : 92 and 95 Unleaded petrol as at October 2012.

37CONSTRUCTION COST DATA

Basis of Charges in Manila, PhilippinesWater and Electricity actual billing includes miscellaneous charges such as Environmental Charge, Currency Exchange Rate Adjustment (CERA), VAT, etc. Electricity Domestic : 190kWh - 860kWh Commercial/Industrial : 150,000kWh Water Domestic : 29m3 - 41m3/month Commercial/Industrial : 4,030m3/month

Basis of Charges in Seoul, Korea Electricity (Plus electricity basic rates) Domestic = US$1.37/month (basic rate) + US$0.05/kWh ~ 0.16/kWh (300kWh below in use) Commercial = US$5.27/month (basic rate) + US$0.06/kWh ~ 0.09/kWh (300kWh below in use) Water (Plus water basic rates) Domestic = US$0.95/month (basic rate, the usage of 15mm caliber) + US$0.32/m3 + Tax (within 30m3 usage) Commercial = US$77.92/month (basic rate, the usage of 100mm caliber) + US$0.69/m3 + Tax (within 100m3 usage)

0.23 - 0.51

0.394 - 0.682

0.284 - 1.021

0.31 - 0.67

1.29

0.234 - 0.454

0.243 - 0.412

0.48 - 0.80

0.099 - 0.398

0.080 - 0.571

0.76 / 0.43

1.338

1.298 - 5.797

0.67 - 1.08

1.49

0.469 - 0.517

0.271- 0.451

1.47

0.552 - 0.596

0.522 - 1.122

0.56

0.915

0.856

1.04

0.86

0.431

0.685

0.60

0.343

0.517

N/A

N/A

N/A

N/A

N/A

N/A

N/A

N/A

0.461

N/A

0.73 - 0.77

1.101

1.026

1.22

1.60

0.442

0.721

0.90

0.479

0.563

WATER FUEL

DOMESTIC COMMERCIAL/INDUSTRIAL DIESEL LEADED UNLEADED

US$/m3 US$/m3 US$/litre US$/litre US$/litre

(Cont'd)

AR

CA

DIS

VIE

TNA

M C

O.,

LTD

1 CONSTRUCTION COST DATA

CONSTRUCTION COST DATA38

The above costs are at 4th Quarter 2016 levels.

Basis of Charges in Hong Kong, China Electricity (Based on tariff scheme of CLP Holdings Limited) Domestic (bi-monthly consumption) : 0 - 400kWh = US$ 0.11/kWh; 400 - 1,000kWh = US$ 0.12/kWh; 1,000 - 1,800kWh = US$ 0.14/kWh; 1,800 - 2,600kWh = US$ 0.18/kWh; 2,600 - 3,400kWh = US$ 0.21/kWh; 3,400 - 4,200kWh = US$ 0.23/kWh; Above 4,200kWh = US$ 0.23/kWh Water Domestic : 0 - 12m3 = Free of charge; 12 - 43m3 = US$ 0.53/m3; 43 - 62m3 = US$ 0.83/m3; Above 62m3 = US$ 1.16/m3

Basis of Charges in Macau, China Electricity Electricity tariffs are a composition of demand charges, consumption charges, fuel clause adjustment and government tax. Water Domestic : Consumption charge = US$ 0.56/m3 for 28m3 or below; US$0.65/m3

for 29m3 to 60m3; US$0.76/m3 for 61m3 to 79m3 and US$0.91/m3

for 80m3 or above. Other charges (Depending on meter size 15mm - 200mm) : Meter rental = US$0.34 - 58.00/month Commercial/ Industrial : Charges for ordinary users (e.g. Business, government buildings, schools, associations, hospitals and others) only. Special users (e.g. gaming industries, hotels, saunas, golf courses, construction, public infrastructure and other temporary consumption) are excluded.

CITYEXCHANGE

RATEELECTRICITY

DOMESTIC COMMERCIAL/INDUSTRIAL

US$1= US$/kWh US$/kWh

HK$ 7.80 0.11 0.13Hong Kong

Macau

Shanghai

Beijing

Guangzhou

Chongqing

MOP7.98

RMB 6.78

RMB 6.78

RMB 6.78

RMB 6.78

0.16

0.07

0.10

0.09

0.16

0.16 / 0.11

0.12

0.091(peak) /0.045(normal)

0.162(peak) /0.080(normal)

0.24(peak) /0.13(normal)

UTILITY COSTS FOR SELECTED ASIAN CITIES

39CONSTRUCTION COST DATA