Embed Size (px)

Citation preview

Hoda Vasi Chowdhury & CoChartered AccountantsBTMC Bhaban (7th Floor). 7-9 Karwan Bazar, Dhaka-1215Tele (88-2): 9120090.9140094Faxj880-2): _8j19298Website: www.hodavasi.com_______

Auditors' report and financial statementsfor the year ended 31 December 2016

Habib Bank Limited - Bangladesh Branches

Habib Bank Limited - Bangladesh BranchesCountry OfficeSouth Avenue Tower7 Gulshan AvenueGulshan 1. Dhaka 1212

National Office: BTMC Bhaban (7th & 8th Floor), 7-9 Karwan Bazar Commercial Area, Dhaka-1215, BangladeshMotijheel Office: Ispahan! Building (3rd Floor), 14-1S Motijheel Commercial Area, Dhaka-1000, BangladeshChhtagong Office: Del war Bhaban (4th Floor), 104 Agrabad Commercial Area, Chittagong-4100, Bangladesh

An audit involves performing procedures to obtain audit evidence about the amounts and

disclosures in the financial statements. The procedures selected depend on the auditors'judgment,including the assessment of the risks of material misstatement of the financial statements, whether

due to fraud and error. In making those risk assessments, the auditors consider internal controlrelevant to the entity's preparation and fair presentation of the financial statements that give a true

and fair view in order to design audit procedures that are appropriate in the circumstances, but not

for the purpose of expressing an opinion on the effectiveness of the entity's internal control. Anaudit also includes evaluating the appropriateness of accounting policies used and thereasonableness of accounting estimates made by management as well as evaluating the overall

presentation of the financial statements of the Bank.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basisfor our audit opinion.

Opinion

In our opinion, the financial statements of the Bank give a true and fair view of the financialposition of the Bank as at 31 December 2016, and of its financial performance and cash flows for

the year then ended in accordance with Bangladesh Financial Reporting Standards (BFRS) as

explained in Note2.1.

1

We have audited the accompanying financial statements of Habib Bank Limited - Bangladesh

Branches (the "Bank") which comprise the balance sheet as at 31 December 2016, profit and lossaccount, cash flow statement, statement of changes in equity for the year then ended, and a

summary of significant accounting policies and other explanatory notes and annexure thereto.

Management's responsibility for the financial statements and internal controls

Management is responsible for the preparation and fair presentation of financial statements that

give a true and fair view in accordance with Bangladesh Financial Reporting Standards (BFRS) asexplained in Note 2.1 and for such internal control as management determines is necessary to

enable the preparation of financial statements that are free from material misstatement, whether dueto fraud or enor. The Bank Company Act 1991 and the local central bank (Bangladesh Bank)

regulations require the management to ensure effective internal audit, internal control and riskmanagement functions of the Bank. The management is also required to make a self-assessment on

the effectiveness of anti-fraud internal controls and report to Bangladesh Bank on instances of

fraud and forgeries.

Auditors' responsibility

Our responsibility is to express an opinion on these financial statements based on our audit. We

conducted our audit in accordance with Bangladesh Standards on Auditing. Those standardsrequire that we comply with ethical requirements and plan and perform the audit to obtain a

table assurance about whether the financial statements of the Bank are free from material

Independent Auditors' Report to the Management of

Habib Bank Limited - Bangladesh Branches

Hoda Vasi Chowdhury & CoChartered Accountants

Dhaka, 27 February 2017

Report on other legal and regulatory requirements

In accordance with the Companies Act 1994, the Bank Company Act 1991 and the rules andregulations issued by Bangladesh Bank, we also report that:

(a)we have obtained all the information and explanations which to the best of our knowledge

and belief were necessary for the purposes of our audit and made due verification thereof;

(b)to the extent noted during the course of our audit work performed on the basis stated under

the auditors' responsibility section in forming the above opinion on the financial statementsof the Bank and considering the reports of the management to Bangladesh Bank on anti-

fraud internal controls and instances of fraud and forgeries as stated under the management'sresponsibility for the financial statements and internal control:

(i) internal audit, internal control and risk management arrangements of the Bank appeared

to be materially adequate;

(ii) nothing has come to our attention regarding material instances of forgery or irregularity

or administrative error and exception or anything detrimental committed by employees

of the Bank during the year ended 31 December 2016;

(c)in our opinion, proper books of account as required by law have been kept by the Bank sofar as it appeared from our examination of those books and proper returns adequate for the

purpose of our audit have been received from branches not visited by us;

(e)the balance sheet and profit and loss statement of the Bank dealt with by the report are in

agreement with the books of account and returns;

(d)the expenditures incurred during the year were for the purposes of the Bank's business;

(f)the financial statements of the Bank have been drawn up in conformity with prevailing rules,

regulations and accounting standards as well as with related guidance issued by Bangladesh

Bank;

(g)adequate provisions have been made for classified loans and advances;

(h) the records and statements submitted by the branches have been properly maintained and

consolidated in the financial statements;

(i) the information and explanations required by us have been received and found to be

(j) we have reviewed over 80% of risk-weighted assets of the Bank and spending over 1,500

person hours; and

Capital Adequacy B

adequately during the year.

HodaVasiChowdhury&Co

12,563,836,212

4,086,887,815

155,473,068138,024,859

4,380,385,742

8,183,450,4701,472,514,031

1,800,163,1414,297,563,044

367,097,83316,112,421

230,000,000

6,480,936,439

12,563,836,212

43,386,6211,059,214,182

4,916,977,196

4,550,921

441,318,000

1,710,334,217

4,921,528,117

22,68773,945,868

73,968,555

41,463,151

4,272,623,369

2015BDT

4,314,086,520

12,881,976,950

4,096,673,37559,254,59789,418,411

4,245,346,382

8,636,630,5681,567,899,857

1,886,504,9204,346,252,569

449,302,31336,670,909

350,000,000

6,718,730,711

12,881,976,950

47,233,6991,029,555,152

4,783,688,2749,051,077

908,740,000

1,758,079,495

4,792,739,351

35,28256,112,499

86,147,781

49,094,855

4,240,386,617

2016BDT

4,289,481,472

13

14

12

3

11

910

6

78

5

Notes

4

Total liabilities and shareholders' equity

Capital fundRevaluation reserve

Retained earnings

Capital/shareholders' eguityTotal shareholders' equity

Total liabilitiesOther liabilities

Current deposit and other accounts

Fixed depositsSavings bank depositsBills payable

LIABILITIES AND CAPITALLiabilities:Borrowings from other banks, financial institutions and ageni

Deposits and other accounts :

Total assets :

Fixed assets including premises, furniture and fixtures

Other assetsNon - banking assets

Loans, cash credits, overdrafts, etc

Bills purchased and discounted

Money at call and on short noticeInvestments:Government securities

Loans and advances:

In BangladeshOutside Bangladesh

Balance with other banks and financial institutions

In hand (including foreign currencies)Balance with Bangladesh Bank and its agent bank(including foreign currencies)

PROPERTY AND ASSETSCash

Balance SheetAs at 31 December 2016

Hablb Bank Limited - Bangladesh Branches

Hoda Vasi Chowdhury & CoChartered Accountants

Dhaka, 27 February 2017

As per our report of same date

j YousufRegional General Manager

Mohammad Nazmul Huq BhuiyanHead - Finance

for Habib Bank Limited — Bangladesh Branches

These financial statements should be read in conjunction with annexed notes

1,826,687,981-

-

2,277,190,817

1,826,687,981

447,292,938418,295,200431,714,176

21,593,147507,792,520

2015BDT

2,277,190,817

835,589,514312,217,191349,344,617106,669,887673,369.608

2016BDT

OFF-BALANCE SHEET ITEMSContingent liabilities:15Acceptances and endorsementsLetters of guaranteeIrrevocable letters of creditBills for collectionOther contingent liabilitiesTotal

Other commitments:Documentary credits and short term trade-related transactionsForward assets purchased and forward deposits placedUndrawn note issuance and revolving underwriting facilities

Undrawn formal standby facilities, credit lines and other commitmentsTotalTotal Off-Balance Sheet Items Including Contingent Liabilities

Balance SheetAs at 31 December 2016

Habib Bank Limited - Bangladesh Branches

Hoda Vasi Chowdhury & CoChartered Accountants

Dhaka, 27 February 2017

As per our report of same date

b YousufRegiona^eneral Manager

Mohammad Nazmul Huq BhuiyanHead - Finance

These financial statements should be read in conjunction with annexed notes

for Habib Bank Limited — Bangladesh Branches

26,746,66735,000,00035,000,000

61,746,6671,332,326

(48,606,449)3,500,0003,500,000

(45,106,448)

5,200,000652,326

(4,520,000)

(2,850,000)16,057.158

650,000

General provisionSpecific provisionProvision for off-balance sheet itemsProvision for diminution in value of investmentsOther provisions

Total provision (D)Total profit before tax (C-D)Less: Provision for taxation

Current tax

Net profit after taxation

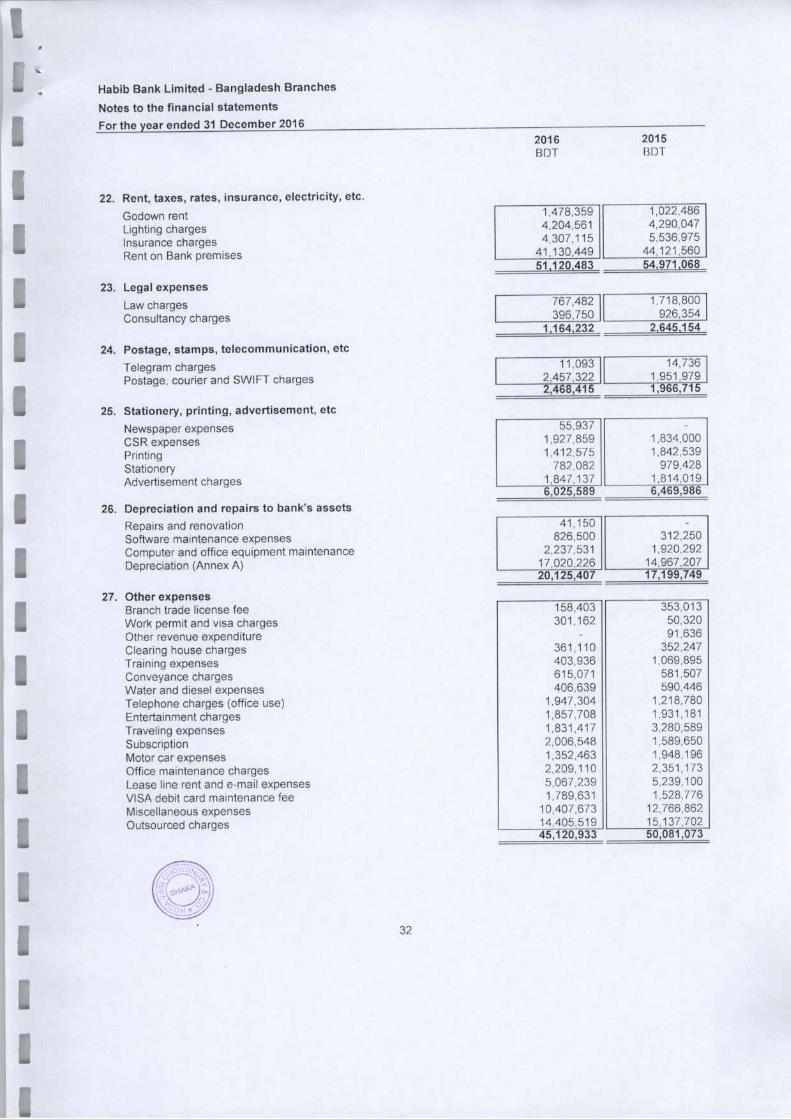

50,081,07317,199,749

173,00022,597,1676,469,9861,966,7152,645,154

54.971,068144.218,420

45.120,93320,125,407

173,00021,583,2596,025,5892,468,4151,164,232

51,120,483167,252,678

134,743,495106,346,335

12,447,693

486,905,957377,042,155

2015BDT

76,472,183 I77,265,063 I10,185,461 fl

408.498.734R286.636.735|

2016BDT

Operating incomeInterest income16Less: Interest paid on deposit and borrowing, etc17Net interest incomeInvestment income18Commission, exchange and brokerage19Other operating income20Total operating income (A)

LESS: OPERATING EXPENSESSalaries and allowances21Rent, taxes, insurance, electricity, etc22Legal & Professional charges23Postage, stamp, telecommunication, etc24Stationery, printing, advertisements, etc25Chief executive salary and feesAuditors' feesDepreciation and repairs of bank's assets26Other expenses27Total operating expenses (B)Profit before provision (C=A-B)

Profit and Loss StatementFor the year ended 31 December 2016

Kabita Bank Limited - Bangladesh Branches

b YousufRegional General Manager

Mohammad Nazmul Huq BhuiyanHead Finance

4,829,491,975118,900

441,318,00073,968,555

4,272623,36941,463,151

5.254.595.753226,500

908,740,00056,147,781

4,240,386,61749,094,855

4,829,491,9755,083,449,663

23,932,077(277,889.765)

-

230,000,000

88,903,165107,515,911

(18,632,744)

5.254.595.7534,829,491,975

9,785,560415.318,217

120,000.000

151.592.356)(47,745,278)

(3,847,078)

(596,792,930)(584,019630)

(86,380,920)(158,037,215)

44,613 52428,406.776

(412,621,795)

(12,773,300)(42,610,920)12,447694

(62,800,662)52,200 000

(83,547.421)(155,916,467)

137,392 735106,346,335

(464,067,393)487,782,799

BDT2015

346,910,574306,389,942(32,068,582)208,902,500(28,891,772)29659,030

128.788,766

40,620,631(46,376,600)

8,516,778(25,703,599)37,435,000

(113,899,652)(183,886,265)107,575,43477 265,063

(471,101,196)650,695,670

BDT2016

These financial statements should be read in conjunction with annexed notes

for Habib Bank Limited — Bangladesh Branches

Notes

Cash flows from operating activities (A)Interest receipts in cashInterest paymentsFee and commission receipts in cashIncome from investments

Cash payments to employeesCash payments to suppliersRecoveries on loans

Income tax paidReceipts from other operating activitiesPayments for other operating activitiesOperating profit before changes in operating assets and liabilities

Increase/decrease in operating assets and liabilitiesLoans and advances to customers

Other assetsDeposits from other banksDeposits from customers

Other liabilities

Net cash from operating activities (A)Cash flows from investing activities (B)Purchase/sale of property, plant and equipmentSale proceeds of property, plant and equipmentPayments for purchase of securities

Net cash used in investing activities

Cash flows from financing activities (C)Borrowings from other banksRemittance received from Head OfficeNet cash from/fused) in financing activities

Net increase in cash and cash equivalents (A+B+C)Effects of exchange rate changes on cash and cash equivalents

Cash and cash equivalents at the beginning of the yearCash and cash equivalents at end of the year

Cash and cash equivalents:CashBalance with Bangladesh Bank and its agent bank(s)Balance with other banks and financial institutionsMoney at call and on short noticePrize bonds

Habib Bank Limited • Bangladesh Branches

Cash Flow StatementFor the year ended 31 December 2016

Mohammad Nazmul Huq BhuiyanHead Finance

for Habib Bank Limited — Bangladesh Branches

4.096.673,37559.254.5S889.418,410 4.245.346.383

(96,218.471)

4,086,887,815155,473.068138,024,859 4,380.385,7424,086,887,815155,473,068138,024.859 4,380,385,742

9,785,560-9,785,560

(96,218,471)

(48,606,448) (48,606,448)

111,278.192 4,242,240,967

23,932,07687,466,031

26,746,66726,746,6'

Balance at 01 Jan 2015Capital fund received from Head Office

Currency translation differencesRevaluation of treasury bills and BondsNet profit for the yearBalance at 31 Dec 2015Balance at 01 Jan 2016Capital fund received from Head OfficeCurrency translation differencesRevaluation/ amortisation of treasury bills and

BondsNet profit for the yearBalance at 31 Dec 2016

TotalBDT

Retainedearnings

BDT

Revaluation

reserveBDT

Capital fundBDT

Hablb Bank Limited - Bangladesh Branches

Statement of Changes in EquityFor the year ended 31 December 2016

^ ^ ^ ^i *^;

I!

8 S'8 ^n

8

o" r--" 10 m" t-"o co Oi c^ oa cm eg r^ to

^S'S

1The Bank and its activities

1.1Habib Bank Limited, Bangladesh Branches/ Legal Form of the Bank

Habib Bank Limited (HBL) - Bangladesh Branches (the "Bank") is the Branch of Habib BankLimited, a banking company incorporated in Pakistan having its Head Office at Habib Bank Plaza,Karachi, Pakistan, The Bank is carrying on banking business in Bangladesh since 1976 withbranches in Dhaka (Gulshan, Uttara, Motijheel, Karwanbazar and Nayabazar), Chittagong andSylhet after obtaining necessary permissions from the regulatory authorities.

1.2Principal activities

The principal activities of the Bank are to provide conventional banking services to its customers

through deposits, loans and advances, trade financing, remittances facilities through its branches,alternate distribution channels namely, ATM booths, VISA debit cards and Internet Banking inBangladesh.

2Basis of preparation

2.1 Statement of compliance

The financial statements of the Bank as at and for the year ended December 31, 2016 have beenprepared on accrual basis under the historical cost convention, except investments and definedbenefit schemes, and in accordance with the "First Schedule" (section 38) of the Bank Companies

Act 1991, as amended by Bangladesh Bank (the Central Bank of Bangladesh) through BRPDCircular No. 14 dated 25 June 2003, other Bangladesh Bank Circulars and International

Accounting Standards (IAS) and International Financial Reporting Standards (IFRS) as adopted bythe Institution of Chartered Accountants of Bangladesh (ICAB) into Bangladesh Accounting

Standards (BAS) and Bangladesh Financial Reporting Standards (BFRS) where relevant to theBank to the extent that these does not contradict the applicable statutory provisions of BangladeshBank.

In case any requirement of provisions and circulars issued by Bangladesh Bank differs with thoseof other regulatory authorities, the provisions and circulars issued by Bangladesh Bank shallprevail. Accordingly the Bank has departed from such requirements of BFRSs in order to comply

with the rules and regulations of Bangladesh Bank which are disclosed below:

i) Investment in shares and securities

BFRS: As per requirements of BAS 39 investment in shares and securities generally fails eitherunder "at fair value through profit and loss account" or under "available for sale" where any changein the fair value (as measured in accordance with BFRS 13) at the year-end is taken to profit andloss account or revaluation reserve respectively.

Bangladesh Bank: As per BRPD circular no. 14 dated 25 June 2003 investments in quotedshares and unquoted shares are revalued at the year end at market price and as per book value oflast audited balance sheet respectively. Provision should be made for any loss arising fromdiminution in value of investment; otherwise investments are recognized at cost.

Habib Bank Limited - Bangladesh Branches

Notes to the financial statements

For the year ended 31 December 2016

ii) Revaluation gains/losses on Government securities

BFRS: As per requirement of BAS 39 where securities will fall under the category of "Held for

Trading" (HFT), any change in the fair value (as measured in accordance with BFRS 13) of Heldfor Trading assets is recognized through profit and loss account. Securities designated as "Held toMaturity" (HTM) are measured at amortized cost method and interest income is recognized

through the profit and loss account.

Bangladesh Bank: HFT securities are revalued on the basis of mark to market and at year endany gains on revaluation of securities which have not matured as at the balance sheet date arerecognized in other reserves as a part of equity and any losses on revaluation of securities whichhave not matured as at the balance sheet date are charged in the profit and loss account. Intereston HFT securities including amortization of discount are recognized in the profit and loss account.HTM securities which have not matured as at the balance sheet date are amortized at the yearend and gains or losses on amortization are recognized in other reserve as a part of equity.

Ill) Provision on loans and advances

BFRS: As per BAS 39 an entity should start the impairment assessment by considering whetherobjective evidence of impairment exists for financial assets that are individually significant. Forfinancial assets that are not individually significant, the assessment can be performed on anindividual or collective (portfolio) basis.

Bangladesh Bank: As per BRPD circular No.16 dated 18 November 2014, BRPD circular no: 14dated 23 September 2012, BRPD circular No. 19 dated 27 December 2012 and BRPD circular No.

05 dated 29 May 2013 a general provision at 0.25% to 5% under different categories ofunclassified loans (good/standard loans) has to be maintained regardless of objective evidence ofimpairment. Also specific provision for substandard loans, doubtful loans and bad losses has to beprovided at 20%, 50% and 100% respectively for loans and advances depending on the durationof overdue. Furthermore a general provision at 1% is required to be provided for all off-balance

sheet exposures.

iv) Other comprehensive income

BFRS: As per BAS 1 Other Comprehensive Income (OCI) is a component of financial statementsor the elements of other comprehensive income are to be included in a single ComprehensiveIncome statement.

Bangladesh Bank: Bangladesh Bank has issued templates for financial statements throughBRPD circular no. 14 dated 25 June 2003 which will strictly be followed by all banks. Thetemplates of financial statements issued by Bangladesh Bank do not include OtherComprehensive Income nor are the elements of Other Comprehensive Income allowed to beincluded in a single (OCI) statement. As such the Bank does not prepare an OCI statement.However elements of OCI, if any, are shown in the statements of changes in equity.

v) Financial instruments - presentation and disclosureIn several cases, Bangladesh Bank guidelines categories, recognize, measure and presentfinancial instruments differently from those prescribed in BAS 39. As such, some disclosure andpresentation requirements of BFRS 7 and BAS 32 cannot be made in the financial statements.

Habib Bank Limited -Bangladesh Branches

Notes to the financial statementsFor the year ended 31 December 2016

viii) Recognition of interest in suspense

BFRS: Loans and advances to customers are generally classified as 'loans and advances' as per

BAS 39 and interest income is recognized through effective interest rate method over the life ofthe loan. Once a loan is impaired, interest income is recognized in profit and loss account on the

same basis based on revised carrying amount.

Bangladesh Bank: As per BRPD circular no. 14 dated 23 September 2012, once a loan isclassified other than Bad and Loss, interest on such loans are not allowed to be recognized asincome, rather the corresponding amount needs to be credited to an interest suspense account,which is presented as liability in the balance sheet.

fx) Cash and cash equivalent

BFRS: Cash and cash equivalent items should be reported as cash Item as per BAS 7.

Bangladesh Bank: As per BRPD circular no. 14 dated 25 June 2003, balance with BangladeshBank is part of cash and cash equivalent regardless of any restriction. Some cash and cashequivalent items such as 'money at call and on short notice', treasury bills, prize bond are notshown as cash and cash equivalent. Money at call and on short notice is shown as face item in thebalance sheet, and treasury bills, prize bonds are shown under investments in the balance sheet.

11

vi) Repo and Reverse Repo transactions

BFRS: When an entity sells a financial asset and simultaneously enters into an agreement to

repurchase the asset (or a similar asset) at a fixed price on a future date (repo or stock lending),the arrangement is treated as a loan and the underlying asset continues to be recognized in theentity's financial statements. The difference between selling price and repurchase price will betreated as interest expense. Same rule applies to the opposite side of the transaction (reverserepo).

Bangladesh Bank: As per DOS Circular letter no. 6 dated 15 July 2010 and subsequentclarification in DOS circular no. 02 dated 23 January 2013, when a bank sells a financial asset and

simultaneously enters into an agreement to repurchase the asset (or a similar asset) at a fixedprice on a future date (repo or stock lending), the arrangement is accounted for as a normal sales

transaction and the financial asset is derecognized in the seller's book and recognized in thebuyer's book,

vii) Financial guarantees

BFRS: As per BAS 39, financial guarantees are contracts that require an entity to make specified

payments to reimburse the holder for a loss it incurs because a specified debtor fails to makepayment when due in accordance with the terms of a debt instrument. Financial guaranteeliabilities are recognized initially at their fair value, and the initial fair value is amortized over the lifeof the financial guarantee. The financial guarantee liability is subsequently carried at the higher of

this amortized amount and the present value of any expected payment when a payment under theguarantee has become probable. Financial guarantees are included within other liabilities.

Bangladesh Bank: As per BRPD 14, dated 25 June 2003 financial guarantees such as letter ofcredit, letter of guarantee, etc. will be treated as off-balance sheet items. No liability is recognizedfor the guarantee except the cash margin.

Habib Bank Limited -Bangladesh Branches

Notes to the financial statementsFor the year ended 31 December 2016

x) Non-banking asset

BFRS: No indication of Non-banking asset is found in any BFRS.

Bangladesh Bank: As per BRPD 14, there is a separate balance sheet item named Non-BankingAsset existed in the standard format

xi) Cash flow statement

BFRS: The Cash flow statement can be prepared using either the direct method or the indirectmethod. The presentation is selected to present these cash flows in a manner that is mostappropriate for the business or industry. The method selected is applied consistently.

Bangladesh Bank: As per BRPD 14, dated 23 June 2003 cash flow is the mixture of direct andindirect methods.

xii) Balance with Bangladesh Banks: ^Cash Reserve Requirement)

BFRS: Balance with Bangladesh Bank should be treated as other asset as it is not available foruse in day to day operations as per BAS 7.

Bangladesh Bank: As per BRPD 14, dated 23 June 2003 balance with Bangladesh Bank istreated as cash and cash equivalents.

xiii) Presentation of intangible asset

BFRS: Intangible assets must be identified and recognized, presented in the face of the balancesheet and the disclosure must be given as per BAS 38.

Bangladesh Bank: As per BRPD 14, dated 23 June 2003 no intangible asset is presented in theface of the balance sheet.

xiv) Off-balance sheet items

BFRS: There is no concept of off-balance sheet items in any BFRS; hence there is no requirementfor disclosure of off-balance sheet items.

Bangladesh Bank: As per BRPD 14, dated 23 June 2003 off balance sheet items (e.g. Letter ofcredit, Letter of guarantee etc.) must be disclosed separately on the face of the balance sheet,

xv) Loans and advances/Investments net of provision

BFRS: Loans and advances/Investments should be presented net of provision.

Bangladesh Bank: As per BRPD 14, dated 23 June 2003 provision on loans andadvances/investments are presented separately as liability and cannot be netted off against loansand advances.

xvi) Disclosure of appropriation of profitBFRS: There is no requirement to show appropriation of profit in the face of statement ofcomprehensive income.

Bangladesh Bank: As per BRPD circular no. 14 dated 25 June 2003, an appropriation of profitshould be disclosed in the face of profit and loss account.

Habib Bank Limited -Bangladesh Branches

Notes to the financial statementsFor the year ended 31 December 2016

xvli) Recognition of derivativesBFRS: As per BAS 39, all derivatives including forward contracts are initially recognized at fairvalue {as measured in accordance with BFRS 13) which is generally the transaction price.Subsequent to initial recognition, derivatives are classified as "fair value through profit & loss" andchanges in Fair value are recognized in profit and loss accounts.

Bangladesh Bank: As per BRPD circular no. 14 dated 25 June 2003, derivative contracts aredisclosed outside of balance sheet exposures.

2.2Basis of measurement

The financial statements of the Bank have been prepared on accrual basis under historical costconvention except for the following:

-Government treasury bills and bonds designated as 'Held for Trading (HFT)' which are measured

at present value using mark to market. Revaluation gains if any are credited to revaluation reserve

account as per DOS circular 05 dated 26 May 2008 and DOS circular 05 dated 28 January 2009

• Government treasury bills and bonds designated as 'Held to Maturity (HTM)' are remeasured at

present value using amortisation concept as per DOS circular 05 dated 26 May 2008 and DOScircular 05 dated 28 January 2009.-Investment in shares of listed companies are valued at market price and unlisted companies atcost or book value of last audited balance sheet whichever is lower.-Net asset/Liability of the defined benefit scheme which is net of present value of the definedbenefit obligations, total plan assets and other related items required by BAS 19

2.3Use of estimates and judgments

The preparation of the financial statements in conformity with BASs/BFRSs requires management

to make judgments, estimates and assumptions that affect the application of accounting policiesand the reported amounts of assets, liabilities, income and expenses. Actual results may differfrom these estimates. Estimates and underlying assumptions are reviewed on an ongoing basis.Revisions to accounting estimates are recognised in the period in which the estimate is revised

and in any future periods, if affected. Information about significant areas of estimation, uncertainty

and critical judgments in applying accounting policies that have the most significant effect on theamounts recognized in the financial statements are described below:

a.Provisions for loans and advances

The Bank assesses its loans and advances for objective evidence of impairment on a regular

basis and particularly at year end. While the primary criteria set out in BRPD circular no. 14 dated23 September 2012, for determining whether a loan is impaired is objective, being based onborrower's ability to make timely repayments, loans and advances may also be classified based onqualitative judgment. This involves making assessments regarding the economic environment inwhich borrowers operate in addition to making judgments about a borrower's financial situation andnet realizable value of any underlying collateral.

b.Taxation

The estimation of current tax provision involves making judgments regarding admissibility ofcertain expenses as well as estimating the amount of other expenses for tax purposes. In addition,the recognition of deferred tax assets and liabilities requires the Bank to estimate to which it is

probable that future taxable profits or loss will be available against which the deferred tax may beutilized.

Hablb Bank Limited -Bangladesh Branches

Notes to the financial statementsFor the year ended 31 December 2016

c. Depreciation

Depreciation is provided on a straight line basis over the estimated useful lives of each item ofproperty, plant and equipment. The determination of useful life involves the use of estimates

regarding expected use of the assets, expected physical wear and tear, technical or commercialobsolescence and legal or similar limits on the use of the asset.

2.4Foreign currency transactions

Functional and presentation currency

These financial statements have been presented in Bangladesh Taka (BDT), which is the Bank'sfunctional currency. Except otherwise indicated, financial information presented in Taka has beenrounded to the nearest integer.

Foreign currency translation

Foreign currency transactions have been converted into equivalent Taka (BDT) currency at theruling exchange rates on the respective date of such transactions as per BAS 21 "The Effects ofChanges in Foreign Exchange Rates".

Assets and liabilities in foreign currencies as at 31 December 2016 have been converted intoBangladesh Taka (BDT) currency at the spot rate for the day taken from Bangladesh Bank.

Differences arising through buying and selling transactions of foreign currencies on different datesof the year have been adjusted by debiting /crediting exchange gain or loss account.

Translation gain and losses

Gains or losses arising out of translation of foreign exchange have been included in the Profit and

Loss Statement except for the exchange rate differences on funds deposited with BB as capital

which is recognized directly in equity.

2.5Cash flow statement

Cash Flow Statement is prepared principally in accordance with BAS 7 "Cash Flow Statement"under direct method as per the guidelines of BRPD circular no. 14 dated 25 June 2003. The CashFlow Statement shows the structure of and changes in cash and cash equivalents during the year.Cash flows during the period have been classified as operating activities, investing activities andfinancing activities.

2.6Statement of changes In equity

Statement of Changes in Equity has been prepared in accordance with BAS 1 "Presentation ofFinancial Statements" and following the guidelines of Bangladesh Bank BRPD circular no.14 dated25 June 2O03.This statement reflects information about the increase or decrease in net assets orwealth.

2.7Reporting period

These financial statements cover one calendar year from 1 January to 31 December 2016.

Habib Bank Limited -Bangladesh Branches

Notes to the financial statementsFor the year ended 31 December 2016

Significant accounting policies

The accounting policy set out below have applied consistently to all the periods presented in thesefinancial statements and have been applied consistently by the Bank.

3.1 Assets and basis of their valuation

3.1.1Cash and cash equivalents

Cash and cash equivalents include cash in hand and balances with Bangladesh Bank and itsagent bank, balances with other banks and financial institutions, money at call and on short

notice, reverse repo and prize bonds,

3.1.2Investments

Investment in securities

All investments in securities (bills and bonds) are initially recognised at purchase priceexcluding commission and accrued coupon interest. Investments are segregated in two broad

categories. These are Held to maturity (HTM) and Held for trading (HFT).

Held to MaturityInvestment which have "determinable Payment" and are intended to be held to maturity are

classified as HTM.

Held for TradingInvestment classified in the category are acquired principally for the purpose of selling orrepurchasing in short trading in order to generate profits.

RevaluationAs per Bangladesh Bank DOS circular letter no. 5 dated 28 January 2009, HFT securities arerevalued each week using Marked to Market concept and HTM securities are amortised once ayear according to Bangladesh Bank guidelines. The HTM securities are also revalued if theseare reclassified to HFT category with the ALCO approval. Value of investment has been shown

as under:

Government treasury bills and bonds (HFT) ; At present value (using marked to marketconcept)

Government treasury bills and bonds (HTM) : At present value (using amortisation concept)Prize bonds and other bonds: At costDebentures: At cost

Habib Bank Limited ^ Bangladesh Branches

Notes to the financial statementsFor the year ended 31 December 2016

Loans and advances/investments are written off as per guidelines of Bangladesh Bank.

Such write off however will not undermine/affect the claim amount against the borrower.Detailed memorandum records for all such written off accounts are meticulously maintained

and followed up.

100%

100%

100%

100%,

100%

100%BL

50%

50%

5%

50%

50%

50%DF

20%

20%

5%

20%,

20%

20%SS

1%

0.25%

0%

2%

5%

2%SMA

1%

0.25%

5%

2%

5%

2%UC

Provision

Others

Small and medium enterprisefinance

Short-term agri-credit and micro

credit

Provision for loan to broker house,

merchant banks, stock dealers, etc

Other than housingfinance &professionals toset,in business

House building andprofessional

Consumer

Types of loans and advances

3.1.3 Loans and advances

a)Loans and advances are stated in the balance sheet on gross basis.

b)Interest/profit is calculated on daily product basis, but charged and accounted for quarterlyon accrual basis. Interest/profit on classified loans and advances/investments is kept in

interest suspense account as per BRPD circular no. 14 dated 23 September 2012 onMaster Circular: Loan Classification and Provisioning, and BRPD circular no 19 dated 27December 2012. Interest is not charged on bad and loss loans and advances/ investments

as per guidelines of Bangladesh Bank. Records of such interest amounts are kept in

separate memorandum accounts.

c)Commission and discounts on bills purchased and discounted are recognised at the time of

realisation.d)Provision for loans and advances/investments is made based on the arrear in equivalent

month and reviewed by the management following instructions contained in BangladeshBank BRPD circulars no. 14 dated September 23, 2012, 16 of dated December 06, 1998, 9of May 14, 2001, 9 and 10 of August 20, 2005, 5 of June 05, 2006, 8 of August 07, 2007, 10of September 18, 2007, 5 of April 29, 2008 and 32 of October 27. 2010.

Rates of provision on loans and advances/investments are given below:

Habib Bank Limited - Bangladesh Branches

Notes to the financial statementsFor the year ended 31 December 2016

3.1.4Property, plant and equipment

Recognition and measurementAll property, plant and equipments are stated at cost less accumulated depreciation as per BAS16 "Property, Plant and Equipment". Land is measured at cost.

The cost is the amount of cash or cash equivalents paid or the fair value of the other considerationgiven to acquire an asset at the time of its acquisition or construction or, where applicable, the

amount attributed to that asset when initially recognised in accordance with the specific

requirements of the BFRS.The cost of an item of property, plant and equipment is recognised as an asset if-

it is probable that future economic benefits associated with the item will flow to the entity; and

the cost of the item can be measured reliably.

The cost of an items of property, plant and equipment comprises:(a)its purchase price, including import duties and non- refundable purchase taxes, after

deducting trade discounts and rebates.(b)any costs directly attributable to bringing the asset to the location and condition necessary for

it to be capable of operating in the manner intended by management.

(c)the initial estimate of the costs of dismantling and removing the item and restoring the site onwhich it is located, the obligation for which an entity incurs either when the item is acquired oras a consequence of having used the item during a particular period for the purpose otherthan to produce inventories during that period.

Subsequent costsThe cost of replacing part of an item of property, plant and equipment is recognised in the carryingamount of the item if it is probable that the future economic benefits embodied within the part willflow to the entity and its cost can be measured reliably. The carrying amount of the replaced partis derecognised. The costs of the day-to-day servicing of property, plant and equipment arerecognised in profit or loss as incurred.

DepreciationDepreciation on addition shall be charged from the month of acquisition whereas no depreciationshall be charged in the month of deletion.

Category of asset

Furniture and fixtures

Major Repairs and RenovationOffice equipment and electrical appliancesComputerMotor vehiclesSoftwareGain or loss on sale of property, plant and equipment is recognised in profit and loss statement asper provision of BAS 16 "Property, Plant and Equipment".

3.1.5Other assets

Other assets include all other financial assets and include fees and other unrealised incomereceivable, advance for operating and capital expenditure and stocks of stationery and stamps.

3.2 Liabilities and provisions3.2.1 Deposits and borrowings from other banks, financial institutions and agents

Deposits by customers and borrowings from other banks, financial institutions and agents include

interest-bearing borrowings redeemable at call and Bangladesh Bank refinance. These items are

brought to financial statements at the gross value of the outstanding balance.

Habib Bank Limited - Bangladesh Branches

Notes to the financial statementsFor the year ended 31 December 2016

3.2.2 other liabilitiesAs per BAS 37 "Provisions, Contingent Liabilities and Contingent Assets" the Bank recognisesprovisions only when it has a present obligation as a result of a past event and it is probable thatan outflow of resources embodying economic benefits will be required to settle the obligation andwhen a reliable estimate of the amount of the obligation can be made.

Other liabilities comprise items such as provision for loans and advances/investments, provisionfor taxes, interest payable, interest suspense, accrued expenses etc. Other liabilities are

recognised in the balance sheet according to the guidelines of Bangladesh Bank, income tax laws

and internal policy of the Bank.

3.3Reserve

Statutory reserve

As per Section 24(1) of the Banking Companies Act 1991, Banks which are incorporated outsideBangladesh do not require to set aside any reserve out of their profits.

Revaluation reserve

Revaluation reserve arises from the revaluation of treasury bills and bonds (HFT & HTM) inaccordance with the Bangladesh Bank DOS circular no. 5 dated 26 May 2008. The tax effects onrevaluation gain are measured and recognised in the financial statements as per BAS 12: Income

Taxes.

3.4Revenue recognition

Interest incomeInterest on loans and advances is calculated on daily product basis, but charged and accounted

for on quarterly basis. Interest on loans and advances ceases to be taken into income when such

advances fall under classification. It is then kept in interest suspense account. Interest on

classified loans and advances is accounted for on a cash receipt basis.

As per BRPD circular no; 6, dated 19 March 2015 and dated 16 February 2016, the Bank isrequired to identify its good borrowers and to pay 10% rebate on the interest earned from themduring the year. This amount is netted off with interest income.

Investment income

Income on investments is recognised on accrual basis. Investment income includes discount on

treasury bills , interest on treasury bonds, debentures and fixed deposits with other banks.

Fees and commission Income

The Bank earns fees and commissions from diverse range of services provided to its customers.

This includes fees and commission income arising on financial and other services provided by theBank including trade finance, credit cards, debit cards, passport endorsement, loan processing,loan syndication and locker facilities, etc. Fees and commission income is recognised on the basis

of realisation.

3.5Employee benefits

There is a Recognised Provident Fund (RPF) in which each employee contributes @10% of theirbasic salary which is matched by an equal amount of contribution by the Bank. The accumulatedProvident Fund balance including interest thereon are paid to the members at the time of theirseparation from the employment of the Bank in accordance with Bank's service rules. Contribution

to the fund is recognised as and when it accrues.

The Bank operates a funded gratuity scheme which has been approved by the National Board ofRevenue as a recognised gratuity fund with effect from January 2001. Employees are entitled to

gratuity benefit after completion of minimum 10 (ten) years of service with the Bank. The gratuityis calculated on the basis of last basic pay and is payable at the rate of one month's basic pay forevery completed year of service. The Bank's expense related to Gratuity is estimated on a yearly

basis and the amount is transferred to the fund and charged to expenses of the Bank.

18

Habib Bank Limited - Bangladesh Branches

Notes to the financial statementsFor the year ended 31 December 2016

3.11 Pledge of bank assets against any loan or guarantee

The Bank has not pledged any of its assets as security against any kind of loans taken from any

individual or institutions or against any guarantee given to a third party.

3.6 Interest paid on borrowing and other deposits

Interest paid on deposits and other accounts except fixed deposit is accrued on a monthly basis,but credited to customer account on half yearly basis. Interest on fixed deposit is accrued on adaily basis and credited to customer account on maturity of fixed deposit. Interest on borrowing

from other banks is accrued on a daily basis and paid through Bangladesh Bank account onmaturity.

3.7Provision for off-balance sheet exposures

In compliance with Bangladesh Bank guidelines off-balance sheet items have been disclosedunder contingent liabilities. As per BRPD circular no. 14 dated 23 September 2012, the Bank isrequired to maintain provision @ 1 % against off-balance sheet exposures.

3.8Provision for nostro accounts

According to Foreign Exchange Policy Department of Bangladesh Bank (FEPD), BangladeshBank circular no 677 dated 13 September 2005, Bank is required to make provision regarding theun-reconciled debit balance as at balance sheet date and these are certified by External Auditor.

3.9TaxationIncome tax expense comprises only current taxes. Current tax are recognised in profit or loss

except to the extent that it relates to items recognised directly in equity.

Current tax is the expected tax payable or receivable on the taxable income or loss for the year,using tax rates enacted or substantively enacted at the reporting date, and any adjustment to taxpayable in respect of previous years.

Provision for income tax has been made @ 42.5% ( 2015: 42.5%) as prescribed in Finance Act2016 of the profit made by the Bank by considering taxable add-backs of income anddisallowances of expenditures.

3.10Off-settingFinancial assets and liabilities are offset and the net amount presented in the balance sheet when,and only when, the Bank has a legal right to set off the recognised amounts and it intends either tosettle on a net basis or to realise the asset and settle the liability simultaneously.

Income and expenses are presented on a net basis only when permitted under BFRSs, or for

gains and losses arising from a group of similar transactions such as in the Bank's trading activity.

Habib Bank Limited -Bangladesh Branches

Notes to the financial statementsFor the year ended 31 December 2016

3.12 Risk Management at Habib Bank Limited, Bangladesh Branches

The possibility of losses, financial or otherwise, is defined as risk. The assets and liabilities of HBLBangladesh are managed so as to minimise, to the degree prudently possible, the Bank's exposureto risk, while at the same time attempting to provide a stable and steadily increasing flow of netInterest income, an attractive rate of return on an appropriate level of capital and a level of liquidityadequate to respond to the needs of depositors and borrowers and earning enhancement

opportunities.

The risk management of the Bank covers all core risk areas of banking i.e. i) Credit Risk, ii) ForeignExchange Risk, iii) Assets and Liability Management Risk, iv) Money Laundering Risk, v) InternalControl and Compliance Risk, and vi) Information and Communication Technology Risk.

i. Credit risk management

Credit risk is the risk of loss due to the failure of a borrower to meet its credit obligations inaccordance with agreed contract terms. Credit risk makes up the largest part of bank's riskexposures. The bank's credit process is guided by centrally established credit policies, rules andguidelines continuing a close-to-the market approach with an aim to maintain a well-diversified creditportfolio which produces a reliable and consistent return.

The Global Credit Policy of the bank is approved by the Board of Directors which ensures the systemof checks and balances are in place while taking credit decisions. Salient features of the riskapproval process are delineated below:

-Every extension of credit to any counterparty requires approval by the pre-defined level of

authority.

-All business groups must apply consistent standards in arriving at their credit decisions.

-Every material change to a credit facility requires approval at the appropriate^pre-defined level.

-Credit approval authority is assigned to individuals according to their qualifications andexperience.

II. Foreign exchange risk

Foreign exchange risk refers to the risk that a Bank may suffer losses as a result of adverseexchange rate movements during a period in which it has an open position, either in the form of abalance sheet asset or liability account, or an off-balance sheet item. Foreign exchange risk arises inthe Bank due to (i) structural imbalance between foreign exchange assets and liabilities, (ii)transactions with customers in foreign currencies and (iii) foreign exchange denominated revenuesand costs.

Business line managers are concerned with the consequences of potential exchange ratemovements on the domestic currency equivalent value for all foreign currency positions. The goal offoreign exchange risk management is to minimize the losses that the Bank may incur due to adverseexchange rate movements of currencies in which the Bank has an open position.

Foreign Exchange risk is primarily managed by Treasury Front office through strict compliance withthe set limits in different areas such as (i) Foreign Exchange Exposure Limit, (ii) Net open positionlimit, (ii) Intraday limit, (iv) Settlement limit, (v) Dealers trading limit, (vi) Dealers stop loss limit and(vii) Counter party limits.

Treasury Mid office (TMO) is a specialized unit formed with a view to implement robust market andliquidity risk Management practices as prescribed by internal policies and Bangladesh Bankguidelines. To minimize foreign exchange risk. Treasury Mid office analyzes the Market trend andmonitors treasury dealings and exposures and reports to local and global Risk Management. TMOalso monitors all limits set by the Bank and Bangladesh Bank.

Treasury Back office is responsible for settlement of all deals done by front office, its transactionsand reporting to Treasury Mid Office (TMO) and Bangladesh Bank in line with the policies andguidelines.

Hablb Bank Limited- Bangladesh Branches

Notes to the financial statementsFor the year ended 31 December 2016

•v. Prevention of money laundering

To ensure implementation of Anti-Money Laundering Policies and regulatory directives, Habib Bankhas restructured the Central Compliance Committee (CCC) ensuring member from General Banking,IT, HR as instructed by BFIU. The purpose of the Central Compliance Committee is to provide aguide line within which to comply with laws and regulations to safeguard the bank from potentialAML/CFT CDD risk. AML/CFT/CDD policy and procedure has been set up with detailed guidelines forconducting due diligence on customers end transactions have been established for sanctionscreening prior to account opening and the periodical review of existing customer portfolio.Transaction monitoring is conducted through automated system SSW and Manias. Processes forcustomer Risk rating have also been implemented. Training has been taken as a continuousprocess for creating/developing awareness among the officers through centralization of accountopening , account deactivation and activation etc. HBL Bangladesh has ensured further control on itsAML/CFT program. CCC also meet BAMLCOs on quarterly basis to provide guidance and resolutions

on issues branches are facing.

v. Internal control and Compliance Risk

HBL Bangladesh ICU prepares its annual monitoring plan as per the approved ICU policy for HBLBangladesh. The unit carries out reviews of risk management procedures, internal control systems,and governance processes. This also involves periodic review of transactions, testing of controlsystems, special investigations, and assessments of regulatory compliance. Any identifiedgaps/discrepancies/weaknesses are followed up till their rectification. All functions/ departments /

units of HBL Bangladesh, fall within scope of ICU reviews,

vl. Information and communication technology Risk

The Bank maintains its in-house IT department for the support and services of IT systems where thecore system is centralized in Head Office, Karachi, Pakistan. IT department maintains performancelevel agreement and service level agreement with business lines for service quality assurance whichdescribes all the IT services with target service up time and response time for troubleshooting or anyIT related requests. For more tracking on service issue HBL Bangladesh IT has already beenintroduced incident Management system to all HBL Bangladesh Users to log the Incident and ITPersonnel will generate report in order to submit seniors for performance tracking by IT. ITdepartment reviews and ensures appropriate controls and security standards are in place and are incompliant with group IT and regulatory requirements. It also performs Risk Assessment on various ITsystems through Head Office, Karachi, Pakistan and processes to mitigate operational risks. HBLBangladesh has been recently introduce another Risk based approach which is known as 2 FA (TwoFactor Authentication) authentications for Fund Transfer between HBL to HBL. The bank has abusiness recovery Plan (BRP) in place to ensure business continuity in case of any major disaster.To overcome Risk on SMS, HBL BD IT has been setup local SMS Server to generate transaction

SMS alert for their client.

21

ill. Asset liability management riskALM risk arises in absence of proper mechanism to address the risk of mismatch between assetsand liabilities either due to liquidity or change in interest rate. HBL Bangladesh to ensure bettermanagement of Balance Sheet Risk has formulated policies for Market Risk and Liquidity RiskManagement. Besides, Asset Liability Committee (ALCO) of the Bank meets once in a month toanalyze the economic indicators, review the liquidity position, pricing/interest rate structure and

suggests action plan strategies to manage Balance sheet Risk.

Habib Bank Limited- Bangladesh Branches

Notes to the financial statementsFor the year ended 31 December 2016

Habib Bank Limited- Bangladesh Branches

Notes to the financial statements

For the year ended 31 December 2016

3.13Related party transaction

The Bank, not being incorporated in Bangladesh, operates in Bangladesh under the banking licenseissued by Bangladesh Bank and therefore the key management personnel of the Bank for thepurposes of BAS 24 are defined as those persons having authority and responsibility for planning,directing and coordinating the bank, being members of the board of directors of the parent company,its senior management and close members of their families and companies they control or havesignificant influence. There were no transactions between the Bank and the key management

Dersonnel (2015: Nil)3.14Audit committee

The Bank being a branch of a foreign bank does not have a local Board of Directors from whom toselect an Audit Committee. HBL Bangladesh has obtained a dispensation from Bangladesh Bankthat the Bank does not need an Audit committee as it is incorporated outside Bangladesh vide letterno: BRPD (R-2) 651/9(47) Kha/2015-1682 dated March 02, 2015. Nevertheless in Bangladesh thereare seven operating branches which are reviewed by the Head Office based Internal Audit Teamperiodically and submit comprehensive report which are regularly reviewed and actioned.

3.15Credit rating of the Bank

Pursuant to the Bangladesh Bank's BRPD Circular No. 06 dated July 05, 2006 and in order tosafeguard the interest of investors, depositors, creditors the bank has completed the credit rating by

Credit Rating Information and Services Limited (CRISL).

Credit Rating Information and Services Limited assigned "A+" (Pronounced A plus) rating to HBLBangladesh in the Long term and "ST-2" rating in short term for the year 2015. Commercial banksrated in this category is adjudged to be very good financia^, healthy and sustainable franchises anda first rate operating environment. Rating in this category is characterized with commendable positionin terms of liquidity, internal fund generation and access to alternative sources of fund. The rating for

2016 is yet to be completed.

3.16Events after reporting period

All material events after the reporting period are considered and where necessary, adjusted for ordisclosed in accordance with BAS 10: Events after the reporting period.

3.17Changes in accounting policies

The Bank has consistently applied the accounting policies as set out in note 3: significant accountingpolicies. During the year ended 31 December 2016, the Bank has not adopted any new standardsand amendments to existing standards, having any material impact on preparing these financial

statements.A number of new standards and amendments to standards are effective for annual periods beginningafter 1 January 2018 and optional earlier adoption is permissible. However, the Bank has not earlyadopted these new or amended standards in preparing these financial statements. Some of these

new or amended standards relevant to the Bank are disclosed below:

(a)8FRS 9 Financial Instruments

BFRS 9, published in July 2014, replaces the existing guidance in BAS 39 Financial Instruments:Recognition and Measurement. BFRS 9 includes revised guidance on the classification andmeasurement of financial instruments, a new expected credit loss model for calculatingimpairment on financial assets, and new general hedge accounting requirements. It also carriesforward the guidance on recognition and derecognition of financial instruments from BAS 39.BFRS 9 is effective for annual reporting periods beginning on or after 1 January 2018, with early

adoption permitted.

The Bank is assessing the potential impact on its financial statements resulting from the

application of BFRS 9.

(b)BFRS 15 Revenue from Contracts with Customers

BFRS 15 establishes a comprehensive framework for determining whether, how much and whenrevenue is recognised. It replaces existing revenue recognition guidance, including BAS 18Revenue, BAS 11 Construction Contracts and BFRI 13 Customer Loyalty Programmes. BFRS15 is effective for annual reporting periods beginning on or after 1 January 2018, with early

adoption permitted.The Bank is assessing the potential impact on its financial statements resulting from the

application of BFRS 15.

22

22,68722,687

?3>68,555

22,68773 945 868

35,26235,282

56,147,781

35,282 II56,112,499 N

119,259,596710,216,66841,463,151

1214,766,126 ||758 079 498

49,094,855 II•

Local currencyForeign currenciesCash in ATM

4.2Balance with Bangladesh Bank and its agent bank

Balance with Bangladesh BankLocal currencyForeign currencies

4.3Cash Reserve Requirement (CRR) and Statutory Liquidity Ratio (SLR)

Cash reserve requirement (CRR) and statutory liquidity ratio (SLR) have been calculated and maintainedin accordance with Section 33 of the Banking Companies Act 1991 and subsequent BCD circular no. 13dated 24 May 1992; BRPD circular no. 12 dated 20 September 1999 and BRPD circular no. 22 dated 6November 2003; Bangladesh Bank DOS circular no. 03 dated 23 March 2005; DOS circular no. 06 dated05 October 2005 and MPD circular no. 04 dated 01 December 2010 and MPD circular no 04 dated 24

June 2014.4.3.1Cash reserve requirement (CRR)

Conventional bankingAs per Bangladesh Bank MPD circular no. 04 dated 24 June 2014, Bank has to maintain CRR @ 6,5% onfortnightly cumulative average basis and minimum @ 6% on daily basis.

Fortnightly Bank's CRR maintenance:Required reserve (6.5% of demand and time liabilit ies)I 400,671,880 || 417,223,910 [Actual reserve maintained (average)| 615,438,010 II 536,364,606 |

Surplus214.766,130119,140,696

4.3.2Statutory liquidity ratio (SLR)

As per the MPD circular nos. 5 dated 01 December 2010, Bank's has maintained 19% Statutory LiquidityReserve (SLR). On a new MPD circular nos. 2 Issued on 1 dated 23 June 2014, 13% SLR has beenmaintained on the Bank's time & demand liabilities in the form of treasury bills, bonds and debenturesincluding foreign currency balance with Bangladesh Bank. Statutory Liquidity Reserve maintained by the

Bank, Is shown below:

13% of average demand and time liabilities:

Required reserveActual reserve maintained (note 4.3.3)Surplus1,220,596,720 1^0

4.3.3Composition of actual reserve held (as per statement submitted to Bangladesh Bank)

Cash in handUnencumbered approved securitiesOthers

5. Balance with other banks and financial Institutions

In Bangladesh (note 5.1)Outside Bangladesh (note 5.2)

S.1 In BangladeshCurrent Account withDutch Bangla Bank Ltd

In hand (note 4.1)Balance with Bangladesh Bank (note 4.2)

4,272,623,369

539.217,1223,733,406,247

41,463,151

36,843,0472,991,1041,629 000

4.314.086.520

41,463,1514,272,623,369

BDT

4,240,386,617

597,388,036 ||3,642,998,58 ij|__

49,094,855

44,026,189 II2,372,6662 696 000 ||

4,2B9,481,472

49,094,855 II4,240 386 617 II

2016BDT

Habib Bank Limited - Bangladesh Branches

Notes to the financial statementsFor the year ended 31 December 2016

1,758,079,4951,710,334,217

placed under lien with Bangladesh Bank innaintenance.

838,463,065871,752,252

118,900

13,399,01212,858,478

3,300.85169.969,208

13,621,24613,189,387

351,370,58567,828,668

1,542,937,967

99,433,382277,042,342

1,166,462,2431,244,594,572

249,287,87849,935,753

945,370,942

1,542,937,967167,277,350

118,900

.710.334.217

710,334,217

•

1

1,758,079,495

1,758,079,495 II

62,808,000300,000,000

78,510,000

300.000.000

78,740,000190,000,000150,000,000190,000,000

53,583.192

1,617,395102.420

51,863,377

20,362,676

588,1193.470,0253,010,7788.463,5564,830,198

nstitutionsnclal

48,188,524

1,143,920234,826

46,809.778

7.923,975

745,671158,125492,912705,931

5 821,336

275,121,8011,482,731,194

226,500

1,244,594,572]513,258,423

226,500 ||

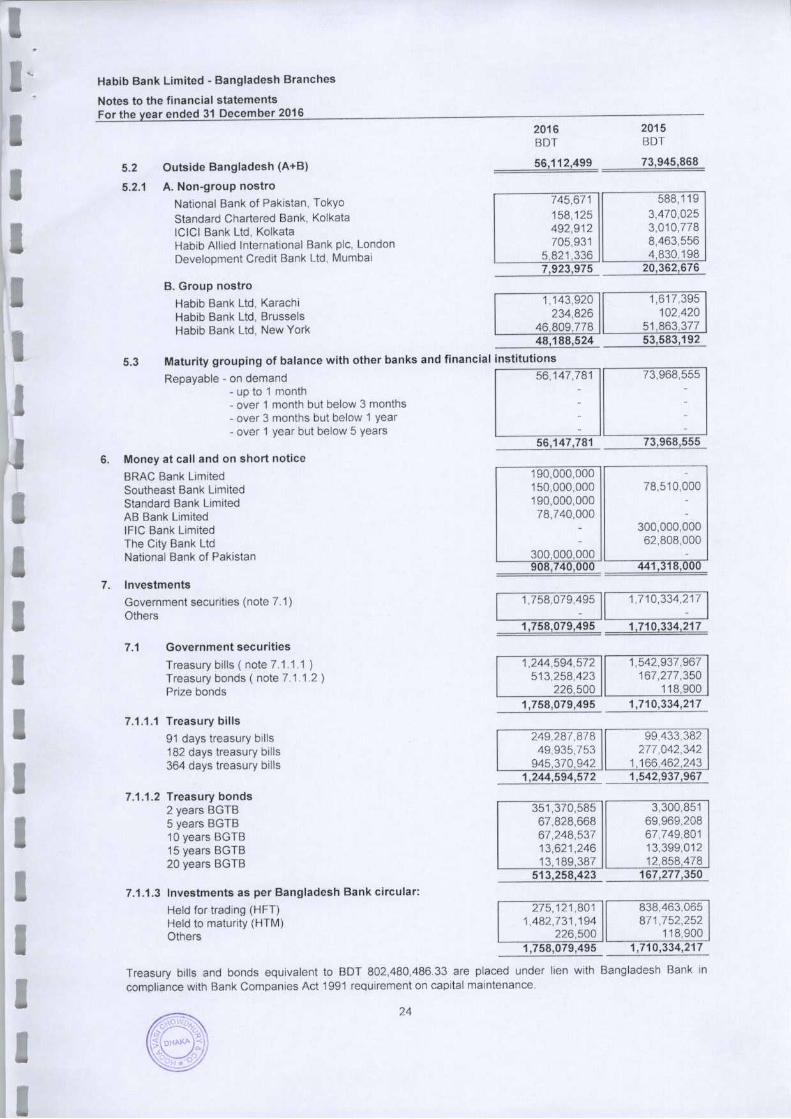

Treasury bills and bonds equivalent to BDT 802,480,486.33 arecompliance with Bank Companies Act 1991 requirement on capital

5.2Outside Bangladesh (A+B)

5.2.1 A. Non-group nostro

National Bank of Pakistan, TokyoStandard Chartered Bank, KolkataICICi Bank Ltd, KolkataHabib Allied International Bank pic, LondonDevelopment Credit Bank Ltd, Mumbai

B. Group nostro

Habib Bank Ltd, KarachiHabib Bank Ltd, BrusselsHabib Bank Ltd. New York

5.3Maturity grouping of balance with other banks and fl

Repayable - on demand-up to 1 month-over 1 month but below 3 months-over 3 months but below 1 year-over 1 year but below 5 years

6.Money at call and on short notice

BRAC Bank LimitedSoutheast Bank LimitedStandard Bank LimitedAB Bank LimitedIFIC Bank LimitedThe City Bank LtdNational Bank of Pakistan

7.InvestmentsGovernment securities (note 7.1)Others

7.1 Government securities

Treasury bills (note 7.1,1,1 )Treasury bonds ( note 7.1.1.2 )Prize bonds

7.1.1.1Treasury bills

91 days treasury bills182 days treasury bills364 days treasury bills

7.1.1.2Treasury bonds2 years BGTB5 years BGTB10 years BGTB15 years BGTB20 years BGTB

7.1.1.3Investments as per Bangladesh Bank circular:

Held for trading (HFT)Held to maturity (HTM)Others

2016BDT

Habib Bank Limited - Bangladesh Branches

Notes to the financial statementsFor the year ended 31 December 2016

4.921.528.1171,881,396,8001,082,006,611

676.912,425325.619,032308,420,430442,027,171201,579,763

3.565,885

4.921,528,1173,222,313,2311,673.419.071

25.795.815

4,921,528,11716,425,743

1,098,628,4911,574,484,4751,608,614,005

297,189.536326,185.867

4.550,9214,550,921

-

4,916,977,196

4,916,977,1961,760,056,5871,752,258,641

14,309,78340,807,35725,795,815

399,710,63986,843,186

4,671.146832,524,042

4.921.528.1174,550,921

1 4,916,977,196

1.710.333.317943,143,09159,666,342

209,565,88899,433,382

398,524,614

BDT2015

4.792.739.3511,939,802,189

860,702,129673,860,017226,459,988299,579,155442,480,436346,289,552

3,565,885

4,792,739,3512,878,515,2301,879,740,380

34,483,741

4,792,739,35129,076,078

837,971,7681,854,920,3651,505,295,058

214,973,526350,502,555

9.051.077-

9,051,077

4,783,688,274

4,783,688,2741,663,091,7992,025,381.891

10,751,63940,807.35734,483,741

224,533,377289.637,769

4,671,146490,329,557

4.792.739.3519.051,077

4,783,688,274

1.758.079.49594,059,170

419,199,253995,306,695249.514,378

BDT2016

OthersGeneral tradersFoods, tobacco and beverages, sugarTextileShoes and leather garmentsChemicals and PharmaceuticalsMetals and alliedAutomobile and transportation equipment

8.8 Industry-wise concentration

Industrial AdvancesAdvances to Customers GroupAdvances to Officers and Staff of the Bank

8.4 Significant concentration

More than 5 yearsOver 1 year but below 5 yearOver 3 month but below 1 yearOver 1 month but below 3 monthsUp to 1 monthRepayable on demand

8.3 Maturity-wise grouping

Foreign bills purchased (FBP)Outside BangladeshInland bills purchasedIn Bangladesh

8.2 Bills purchased and discounted

Including short term loanOutside Bangladesh

OverdraftsShort Term LoanPayment against documentsCash creditStaff loansTrust receiptsSME loanLoans against imported merchandise (LIM)Term loanIn Bangladesh

8.1 Loans, cash credits, overdrafts, etc/investments

Bills purchased and discounted (note 8.2)Loans, cash credits, overdrafts, etc/investments (note 8.1)

8. Loans and advances/investments

More than 5 yearsMore than 1 year but not more than 5 yearsMore than 3 months but not more than 1 yearUp to 3 monthsOn demand

7.1.1.4 Maturity-wise grouping

Hablb Bank Limited • Bangladesh Branches

Notes to the financial statementsFor the year ended 31 December 2016

viii. Maximum amount of advances including temporaryadvances made at any time during the year to thecompanies or firms in which the directors of the bank areinterested as directors, partners, managing agents or incase of private companies as members.

ix. Due from other banking companies.

x. Amount of classified loans on which interest has not beencharged:

26

4.319.741.4514.446.181.971

2,031,043,727

2,415,138,244

1,845,579,068

2,474,162,383

Particulars of loans and advances

i. Debts considered good in respect of which the Bank is fullysecured

ii. Debts considered good for which the bank hold!security other than the debtors personal guarantee,

iii. Debts considered good secured by the personalundertakings of one or more parlies in additionpersonal guarantee of the debtor.

iv. Debts adversely classified; provision not maintained thereagainst.

v. Debts due by directors or Officers/Executive of the Bank orany of them taken either separately or jointly with any other

persons.

vi. Debts due by companies or firms in which the directors ofthe bank are interested as directors, partners or managingagents or in the case of private companies, as members.

vii. Maximum total amount of advances including temporaryadvance made at any time during the year to directors orexecutives or manager or officers of the bank or any ofthem taken severally or jointly with any other persons.

1,538,341,997167.082.488

4,921,528.117475,346,146

46.448,309428,897,837

4,446.181.97141,810,761

4,792,739,351472,997,899

472,997.899 ][_

4,319,741,45236,535,037 ||

90,059,0151,298,212,8633,533,256,239

2015BDT

8.6Geographical location-wise distribution

Sylhet DivisionChittagong DivisionDhaka Division

8.7Grouping as per classification rules

Unclassified

StandardSpecial mention accountTotal unclassified loans and advances

ClassifiedDoubtfulBad/LossTotal classified loans and advancesTotal

8.8Large Loan disclosureTotal no of customers having facility of the 10% of the capital of the BankNo of Parties3Total amount outstanding1,587,232,129

FundedI 1,244,480,0061|Non funded|342,752,124 ||

84,004,701 I1,308,989,2943,399^45,356 ||

2016BDT

Hablb Bank Limited - Bangladesh Branches

Notes to the financial statementsFor the year ended 31 December 2016

6.7H.730.7116.480.936.43916,112,421

367,097,8334,297,563,0441,800,163,141

36 670 909 ||449,302,313

4,346,252,5691,886,504,920 [I

. Deposits and other accounts

Current deposit and other accounts (note 11.1)Fixed deposit (note 11.2)Savings bank deposits (note 11.3)Bills payable

62,800,662

929.831,662'

48,000,00014,.

25,703,599

955,534,651

15,700,000 |10,003,599 ||

1.029.555.152 1.059.214.182

22,652,0673.790,420

558,815929,831,052

12.007,6961,774,886

582,9031,907,300

9,547,1371,053,2091,384,258

955,534,651805.000791.098

1,551.4831,766,800

85,759,490349,550

- I

43,386,62189,840,402

3,099,690

3,459,625359,935

3,459,625 ||

47,233,69990,418.923

I

20,824,01819,199,04550,312,36342,891,597

11.558,968 II24,829,21550.863,17850,401,261 II

4,550.921

4,550,921

138,422,390138,619,914

138,619,914

30,625.993107,993,921

9,051,077

9,051,077 ||

138,422,390138,619,914

138,619,914

138,619,914 II

2015BDT

50,907,029 I6,214,487 ||

2,936,9636,114,114 ||

2016BDT

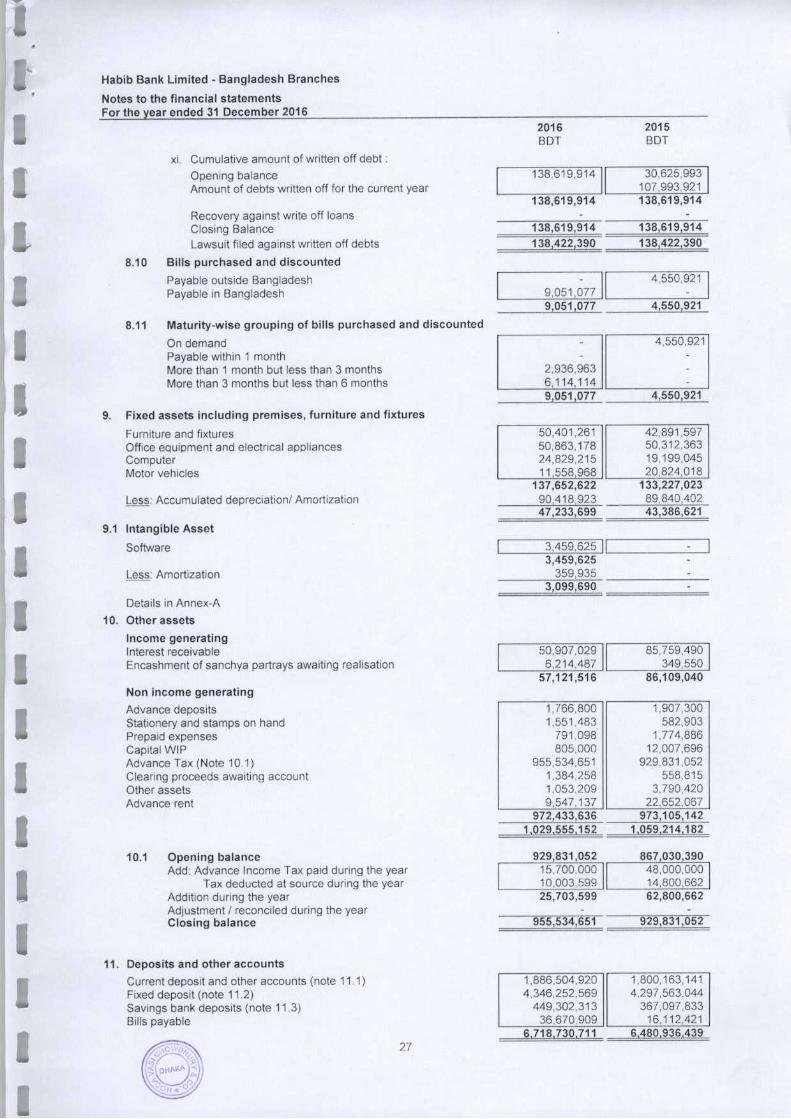

10.1 Opening balanceAdd: Advance Income Tax paid during the year

Tax deducted at source during the yearAddition during the yearAdjustment / reconciled during the yearClosing balance

xi. Cumulative amount of written off debt:

Opening balanceAmount of debts written off for the current year

Recovery against write off loansClosing BalanceLawsuit filed against written off debts

8.10Bills purchased and discounted

Payable outside BangladeshPayable in Bangladesh

8.11Maturity-wise grouping of bills purchased and disci

On demandPayable within 1 monthMore than 1 month but less than 3 monthsMore than 3 months but less than 6 months

9.Fixed assets Including premises, furniture and fixtures

Furniture and fixturesOffice equipment and electrical appliancesComputerMotor vehicles

Less: Accumulated depreciation/ Amortization

9.1 Intangible Asset

Software

Less: Amortization

Details in Annex-A

10.Other assets

Income generatingInterest receivableEncashment of sanchya partrays awaiting realisation

Non income generating

Advance depositsStationery and stamps on handPrepaid expensesCapital WIPAdvance Tax (Note 10.1)Clearing proceeds awaiting accountOther assetsAdvance rent

Habib Bank Limited - Bangladesh Branches

Notes to the financial statementsFor the year ended 31 December 2016

248,730,538

652,326

58,535 969157,883,643)

264,787,696

16,057,158

20,623,876 II(4,566,718)11

356,072,133(107,993,921)

1,567,899,8571,472,514,031179,103,737

2,091,675173,000

923.573,84358,141,23815,500,00045,200,000

248,730,538

255,524.9841,405.625

173.000927,073,843

60,434.70916,150,00042,350,000

264,787,696

1,347,480,5161,947.169,6091,904,825,8441,281,460,470

1,557,655.674 ||1^404,854,1511,227,672,4281,019,968,2041,508,580,254 II

69,217,032972,802291,683384.119

47,302

40,608,105394 708701,986131,883184,484

367.097,833

4,297,563,044

449,302,313

4,346,252,569

70.912,93814 033,064

140.631,925503,431,829239,229,472831,923,913

42,021,16612,283,912

112,147,179814,783,37391,819,981

813.449,309

2015BDT

2016BDT

11.1Current deposit and other accountsLocal currency current depositsForeign currency current depositsSpecial notice time depositsCurrent deposits from banksSundry depositsGroup vostro (note: 11.4)

11.2Fixed deposit

Deposit from customers

11.3Savings Deposits

11.4Group vostro

Habib Bank Ltd, Oman (BDT)Habib Bank Ltd, Dubai (BDT)Habib Bank Ltd, Mauritius (US $)Habib Bank Ltd, Colombo (USD)Habib Bank Ltd, Karachi (ACU $)

11.5Maturity-wise grouping

Repayable - on demand-up to 1 month-over 1 month but below 3 months-over 3 months but below 1 year-over 1 year but below 5 years

12. Other liabilities

Specific provision against classified loans and advances (note 12.1)General provision against unclassified loans and advances (note 12.2)General provision against off balance sheet items (note 12.3)Interest suspense account (note 12.4)Provision for taxation (note 12.5)Provision for audit feesProvision for professional feesOther liabilit ies (note 12.6)

12.1 Specific provision against classified loans and advances

Movement in specific provision:Provision held at the beginning of the yearLess: Fully provided debts written off during the yearAdd. Recoveries of amounts previously written offAdd: Specific provision for the yearLess. Recoveries and provisions no longer requiredAdd: Net charge to profit and loss account during the yearAdd: Transfer from general provisionProvision held at the end of the year

Habib Bank Limited - Bangladesh Branches

Notes to the financial statementsFor the year ended 31 December 2016

179,103,737139,075 691

47,8151 597 510

10,899,12218.184.3399,299,260

255.524,984159 315,356

97.31550.037,48618,964,24517 811 3239,299,260

927,073,843

888,573,84335,000,000

923,573,8433,500,000

12.3Provision for off-balance sheet items

Movement in general provision:Provision held at the beginning of the yearAdd : Amount provided during the yearLess: Recoveries and provisions no longer requiredAdd: Net charge to profit and loss account during the yearLess: Transfer to genera! provision on unclassified loansAdd: Transfer to off-balance sheet items from general provisionProvision held at the end of the year

Off-balance sheet items16,038,212

12.4Interest suspense account

Balance at the beginning of the yearAdd: Amount transferred to interest suspense during the year

Less: Amount recovered in interest suspense during the yearLess: Amount written off during the year

Balance at the end of the year

12.5Provision for taxation

Balance of provision at the beginning of the yearAdd: Provision made for the yearAdjustment/ reconciled during the yearBalance of the end of the year

Income tax assessments for few years are pending with different levels of assessing authority and/or atappeals stage The Bank's management is regularly monitoring all pending tax assessments andconfident that the existing level of provision for tax is adequate to offset any additional claims that mayarise from eventual settlement of these tax assessments.

12.6Other liabilitiesProvision against BCCI claim1'1

Other payableAccrued expensesRouting accountExcess cashInterest payable

(*) This includes the amount provided as provision against the decreed afiled by Eastern Bank Ltd. successor of BCCI Overseas Ltd.

58.141.23824 038,552

82,179,78924,038,552

62,570,01319,609,776

Excess/(Shortage)111,788

15.500.000

60.434,7001,348,506

61,783,2141,348.506

58,141,2383,641,976

16,150,000Maintained

16.150.000

1,848,000 |(6,368,000)1

6,820,000 |(6,170,000)11

6,363,269

1,357,1145,006,154

ess/(Shortaqe)

45.200,000

5,200,000

10,650.000(5,450,000)

307,137,696

42,350,000264,787,696

Maintained Exo

42.350.000

(2,850,000)

4,700,000 II(7.550,000)11

12.2 General provision against unclassified loans and advances

Movement in general provision:Provision held at the beginning of the yearAdd : Provision made during the yearLess: Recoveries and provisions no longer requiredAdd: Net charge to profit and loss account during the yearAdd/(Less): Transfer from general provision to off-balance sheet

Less: Transfer to specific provisionProvision held at the end of the year

Provision for

Un-classified loans and advance: 40,992,886Classified loans and advances 259,781,541

2015BDT

2016BDT

Habib Bank Limited - Bangladesh Branches

Notes to financial statementsFor the year ended 31 December 2016

360,466,000147,326,520

448.195,000 I225.174,608 ||673,369,608

Other contingent liabilities

Bangladesh Sanchay Patras (BSPs) and US Dollar Bonds

i in respect of guarantees given favoi

1.826.687.98115.1 Letter of guarantees

Money for which the Bank is contingently li i

GovernmentBank and other financial institutionsOthers

447,292,938418,295,200431,714,176

21,593,147507,792,520

2.277,190,817

835,589,514312,217.191349,344,617

138.024.859

111,278,192

26,746,667

89,418.411

138,024,859

(48,606,448)

306,506,2344.306.506,2344,000,000,000

1.64%84.96%

86.60%84.96%

14,226,978,057

4,306,506,234

81.593.560

1 54,405,52327,188,037

4,224,912,674