Embed Size (px)

Citation preview

Guide

Emigration Process

A simple how to guide to

understand the documentation

required when taking up residence

in any country outside the CMA

1

Standard Bank Moving Forward™ Emigration Process Guide

Contents

Background .......................................................................................................................................... 2

Emigration Procedure........................................................................................................................ 2

Checklist................................................................................................................................................ 3

COMPLETION OF FORM MP336(b) ................................................................................................ 3

Page 1................................................................................................................................................... 3

Section 1 – Details of applicant/family unit emigrating .................................................................. 3

Section 2 – If the spouse is not emigrating provide the reason for this. ........................................ 3

Section 3 – The reply to question (d) must be yes or the person will not be emigrating. Details of

permission must be quoted in this section. .................................................................................... 4

Section 4 – This section can be completed once the form and the net asset value has been

ascertained. ..................................................................................................................................... 4

Section 5 – Self explanatory ............................................................................................................ 4

Page 2................................................................................................................................................... 5

Section 7 – Complete declaration of all assets held in the Common Monetary Area (South

Africa, Lesotho, Swaziland and Namibia). ....................................................................................... 5

Page 3................................................................................................................................................... 6

Page 4................................................................................................................................................... 9

Section 8 - Less: South African liabilities (including those in Lesotho, Swaziland and Namibia) .... 9

Section 9 - Value of items to be exported .....................................................................................10

Section 10 - Declaration .................................................................................................................11

Page 5.................................................................................................................................................11

Section 11. For completion by the Authorised Dealer ..................................................................12

Extract from Currency and Exchanges Manual ........................................................................13

Opening a Non-Resident account ................................................................................................17

Converting your existing account (if applicable) .....................................................................18

Conclusion..........................................................................................................................................18

2

Standard Bank Moving Forward™ Emigration Process Guide

Background The Financial Surveillance Department of the South African Reserve Bank (SARB) states that when

individuals leave South Africa to take up permanent residence in any county outside the Common

Monetary Area, i.e. Lesotho, Namibia, South Africa and Swaziland (CMA), they may apply to an

Authorised Dealer to be accorded emigration facilities. Applications must be accompanied by a duly

completed Form MP336(b) together with a Tax Clearance Certificate (emigration) obtained via the

South African Revenue Service (SARS) Tax Compliance Status System.

Emigration Procedure In order to place your emigration on record with the SARB, you are required to complete the application

for emigration {Form MP336 (b)}, and return the original to us together with the following documents:

• Tax Clearance Certificate - Emigration

• Certificate of Citizenship/ Naturalisation or Permanent Residence permit in the Foreign Country

(Please include spouse & children if they are South African residents as well)

• Certified copy of passport and Identity documents/Birth Certificates of all individuals listed on

the Form MP336(b)

• If there is any item of value listed of the Form MP336(b) we would require a copy of the

document of title in support thereof. The original of title e.g. property title deeds etc. will need

to be dispatched to the Non- Resident Centre to form part of the your South African blocked

assets.

• The letter of confirmation needs to be signed by you and your spouse.

All the documents must be couriered back to us via courier to the following address:

Standard Bank

Non-Resident Centre

Exchange Control Department

6 Simmonds Street

Fourth Floor

Entrance 1, Blue Pillar 8,

Johannesburg 2001

Our cost for submitting the application to the SARB is currently R 1 450 (subject to change) for the initial

process and R410 per hour thereafter. This can be paid prior to the application or it can be recovered

from the proceeds of assets received before the funds are remitted abroad.

We also attach herewith an extract from the Exchange Control Manual with respect to Emigrations. This

is merely for information purposes. Alternatively, you may visit the SARB website

https://www.resbank.co.za/RegulationAndSupervision/FinancialSurveillanceAndExchangeControl/FA

Qs/Pages/Emigrants.aspx for more information relating to the emigration process.

A reply is expected within 6-8 weeks from submission of the application and only once your application

has been approved may Standard Bank remit funds abroad.

3

Standard Bank Moving Forward™ Emigration Process Guide

Checklist Below is a checklist for ease of reference for all the required documentation;

Emigration Documents Checklist

1. Emigration: Application for foreign capital allowance (Form MP336(b)

2. Tax Clearance Certificate – Emigration

3. Certified copy of valid passport

4. Certified copy of South African Identity Documents

5. Letter of Confirmation

6. Certificate of citizenship/Naturalisation/ Permanent Residence

7. Documents of title pertaining to all assets in Lesotho, Namibia, South Africa and

Swaziland.

COMPLETION OF FORM MP336(b)

Page 1

Section 1 – Details of applicant/family unit emigrating

The full names, marital status and Identity numbers of all parties in the family unit who will be emigrating

must be inserted. Date of Birth is required if ID number is unknown.

Section 2 – If the spouse is not emigrating provide the reason for this.

4

Standard Bank Moving Forward™ Emigration Process Guide

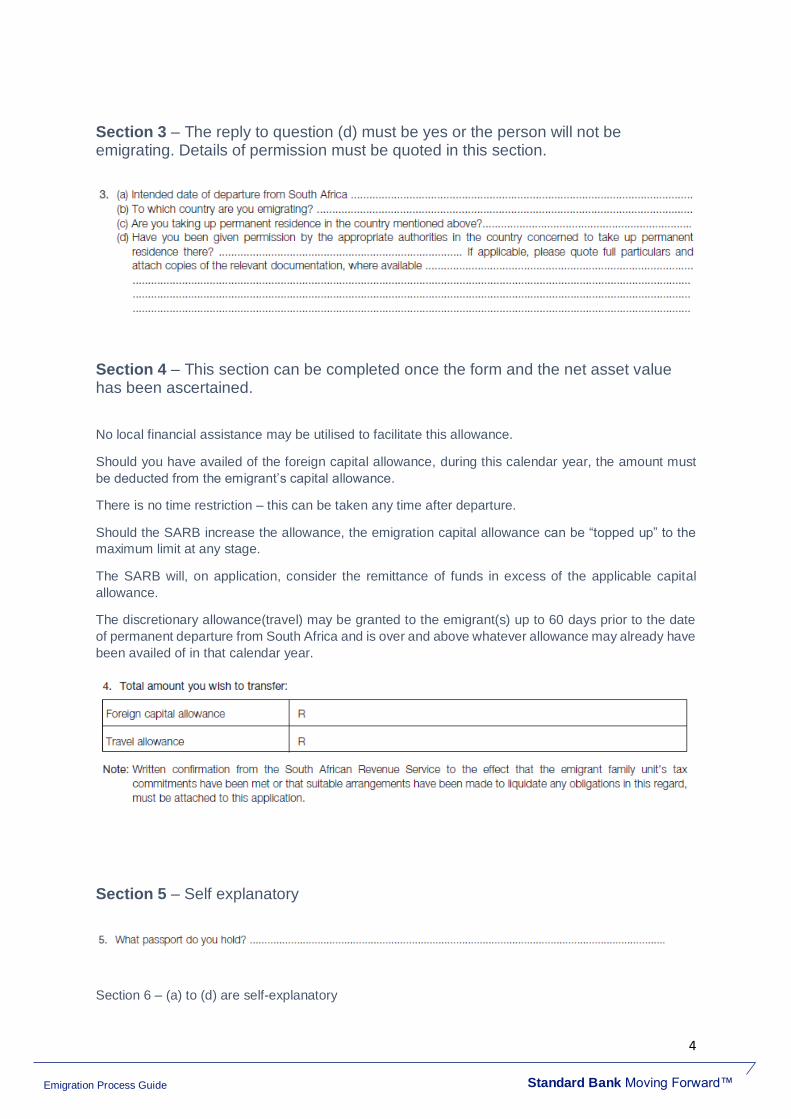

Section 3 – The reply to question (d) must be yes or the person will not be emigrating. Details of permission must be quoted in this section.

Section 4 – This section can be completed once the form and the net asset value has been ascertained.

No local financial assistance may be utilised to facilitate this allowance.

Should you have availed of the foreign capital allowance, during this calendar year, the amount must

be deducted from the emigrant’s capital allowance.

There is no time restriction – this can be taken any time after departure.

Should the SARB increase the allowance, the emigration capital allowance can be “topped up” to the

maximum limit at any stage.

The SARB will, on application, consider the remittance of funds in excess of the applicable capital

allowance.

The discretionary allowance(travel) may be granted to the emigrant(s) up to 60 days prior to the date

of permanent departure from South Africa and is over and above whatever allowance may already have

been availed of in that calendar year.

Section 5 – Self explanatory

Section 6 – (a) to (d) are self-explanatory

5

Standard Bank Moving Forward™ Emigration Process Guide

Should you have been granted permanent residence in South Africa less than five years prior to

emigrating, this will be dealt with as an Immigration that failed to materialise and must be placed on

record with SARB by a Bureau de Change.

Page 2

Section 7 – Complete declaration of all assets held in the Common Monetary Area (South Africa, Lesotho, Swaziland and Namibia).

7.1 Fixed Property

Only property(ies) which have not been sold will form part of the blocked assets and must be listed.

Should you receive rental income, a copy of the rental agreement is required. Should there be any

amendments to the agreement, a revised copy must be obtained. The title deeds of these properties

must be taken in and be housed in safe custody. Should there be a bond over the property, this must

be declared on page 3 under liabilities and the bondholder advised of the fact that the applicant has

emigrated and that the property forms part of the capital assets. An application will need to be submitted

in respect of Exemption from Exchange Control Regulation 3.1(f)

7.2 Stocks, shares, unit trust etc.

7.2.1 Listed investments

6

Standard Bank Moving Forward™ Emigration Process Guide

This relates to shares quoted on the JSE (Johannesburg Securities Exchange), RSA Bonds and Eskom

Stock. The shares may be in certificate (paper) form or electronic form (dematerialised). If in paper form

you must hand in all the original certificates for housing in safe custody. If dematerialised, provide the

latest scrip account statement detailing the holdings and current market value. We will need to advise

the scrip company that the holdings form part of the emigrant’s remaining capital assets and no dealings

are permitted without our prior approval, quoting the capital and income account numbers for the

purchases/sales and income.

7.2.2 Unlisted Investments

This refers to shares in companies/close corporations not listed on the JSE. Request the following

documentation: -

• Original share certificate/certificate of member’s interest

• Latest available financial statements of each entity.

Page 3

7.3 Insurance policies

7

Standard Bank Moving Forward™ Emigration Process Guide

Copy of policy schedules must be held by the Non Resident Centre as they form part of the emigrant’s

blocked assets.

Endowment and Life policies – quote the current surrender value

Retirement annuities – list the current death value

Matured retirement annuity policies that are paying out

- Obtain a copy of the policy schedule of the original annuity and the resultant annuity schedule that

was purchased with the matured funds (paid out 1/3 capital and 2/3 annuity) i.e. letter/schedule

from insurance company detailing the amount to be paid.

- If the original policy was purchased with a single premium, the source of funding will be required.

All policies falling outside of the abovementioned sections of the Currency and Exchanges Manual must

be referred to the Financial Surveillance Department for approval.

7.4 Cash balances

Only credit balances held in accounts must appear in this section.

Should you hold accounts with other financial institutions, the accounts must be closed and the funds

transferred to the accounts held at Standard Bank. Should the funds only mature after departure from

South Africa, the financial institution must be informed of the client’s emigration status and be requested

to transfer the funds held to the credit of the emigrant’s capital account. A letter of undertaking from the

respective financial institution must be furnished.

7.5 Debtors

These are loan accounts in companies/trusts and any funds owing to you.

8

Standard Bank Moving Forward™ Emigration Process Guide

Loan account in an unlisted entity not having any directly or indirectly relationship with the emigrant –

confirmation is required of the loan amount and terms on an entity’s letterhead stating that the interest

rate applicable will not exceed the South African prime lending rate plus five percent at any given time

and that all capital repayments will be credited to the emigrant’s capital account.

Loan account in a trust – a letter signed by the Trustees of the trust is required confirming the loan

amount, terms and that interest payable will not exceed South African prime lending rate at any given

time and that all capital repayments will be credited to the emigrant’s capital account.

Loan account due to the emigrant by an individual – a letter must be signed by the borrower confirming

the loan amount, terms and that interest payable will not exceed the South African prime lending rate

plus five percent at any given time and that all capital repayments will be credited to the emigrant’s

capital account.

7.6 Interest in trusts

(a) Inter Vivos Trust – trust formed by living persons where the beneficiary/(ies) receive(s) benefit while

the donor/funder is still alive.

(b) Will Trust – trust created in terms of the last will and testament of a deceased person.

Should the beneficiaries have no fixed capital or income interest in the trust, it is termed a ‘discretionary’

trust. In this instance, it is at the full discretion of the trustees which beneficiary will receive

income/capital and the amount to be distributed. From an Exchange Control point of view such a trust

is deemed to be an ‘affected entity’, i.e. 100% non-resident owned. Therefore, the full capital value of

the trust as at date of completion must be inserted on the Form MP336(b).

Should the beneficiary(ies) only have a specified percentage interest in the trust, the value of their

percentage must be inserted.

Documents required to be submitted to the SARB: -

- Copy of original Trust Deed and all subsequent amendments. In the case of a Will/ Testamentary

Trusts, the last will and testament.

- Full names of all the beneficiaries of the trust, their domiciles and percentage interest and the date

of their emigration

- Audited financial statements of the trust for the past three years

- Audited financial statements for the past three years for all the unlisted companies in which the

trust has an interest as well as all the names, domiciles and percentage shareholding of all the

shareholders. If emigrants from the Republic, the Bank and Branch who attended to their

emigration formalities.

- Full details of funding (loans/donations) made to the trust from date of inception.

9

Standard Bank Moving Forward™ Emigration Process Guide

- Full details of financing made available to the unlisted companies mentioned above, in which the

Trust has an interest.

- Full names of the Trustees and their domiciles.

- Full details of any distributions to the emigrant client within 3 years prior to date of emigration.

7.7 Other assets – assets not listed above and funds still to be received

This section will include, inter alia, properties that have been sold, lump sum pension payments, sale

proceeds of vehicles, household furniture, timeshare etc. as well as other assets in the emigrant’s

possession at the time of completion of the MP336(b).

Assets remaining in the emigrant’s name must have documents of title to be housed in safe custody,

e.g. timeshare certificate, motor vehicle registration, valuation certificate for coin/stamp collections and

artworks.

Page 4

Section 8 - Less: South African liabilities (including those in Lesotho, Swaziland and Namibia)

10

Standard Bank Moving Forward™ Emigration Process Guide

This section will include, inter alia, taxes still to be paid, mortgage bonds, credit cards,

shipment/relocation costs and estimated living costs prior to departure.

In terms of Exchange Control policy, emigrants/non-residents may not avail of any local borrowings in

excess of the value equivalent to their remaining assets at any specific point in time. In the event that

there is an outstanding liability in excess of the value of the emigrant’s remaining assets, full details

thereof must be submitted to the SARB, requesting exemption from Exchange Control Regulation 3(1)(f)

which could be granted for a period of one year when the matter must again be reviewed.

Section 9 - Value of items to be exported

Any household and personal effects, motor vehicles, caravans, trailers, motorcycles, stamp/coin

collections (excluding coins that are legal tender in the Republic) per family unit or single person within

the overall insured value of R2million.

Prior approval must be obtained from the SARB for the export of the emigrant’s household and personal

effects in excess of R2million. Permission will, in general, be given, but where the value is unduly high

or the goods have been recently purchased, some deduction from the capital allowance may be

imposed.

11

Standard Bank Moving Forward™ Emigration Process Guide

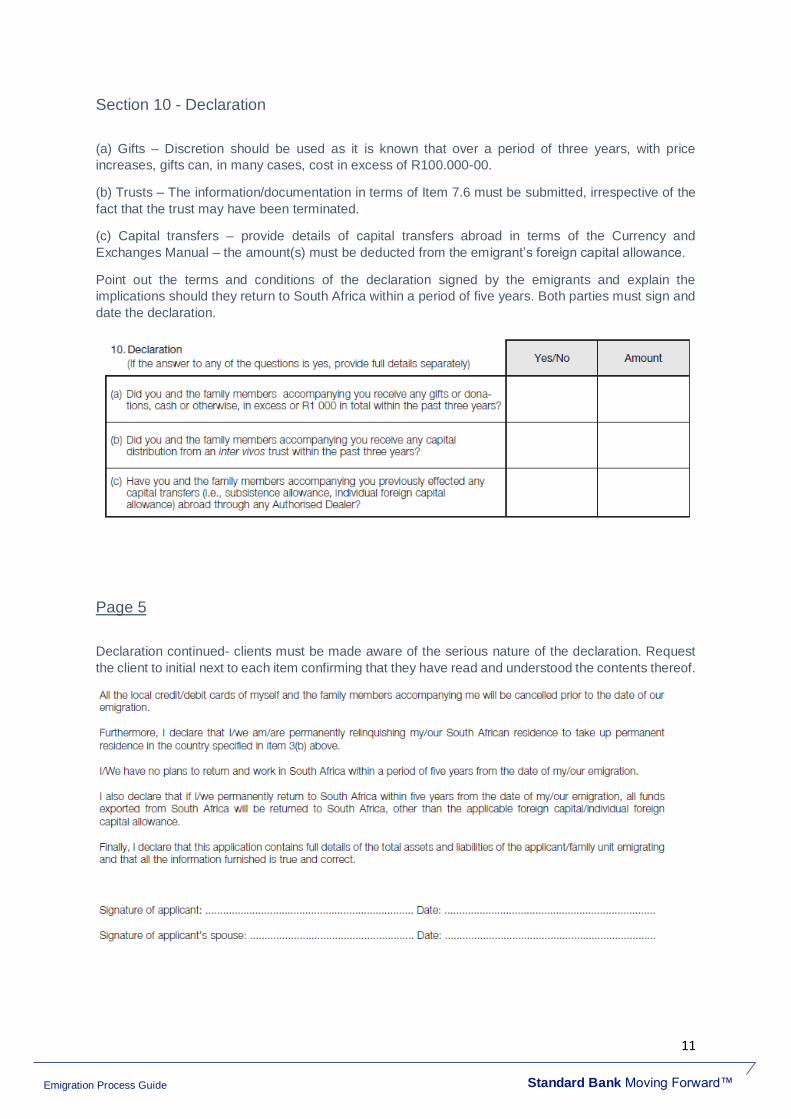

Section 10 - Declaration

(a) Gifts – Discretion should be used as it is known that over a period of three years, with price

increases, gifts can, in many cases, cost in excess of R100.000-00.

(b) Trusts – The information/documentation in terms of Item 7.6 must be submitted, irrespective of the

fact that the trust may have been terminated.

(c) Capital transfers – provide details of capital transfers abroad in terms of the Currency and

Exchanges Manual – the amount(s) must be deducted from the emigrant’s foreign capital allowance.

Point out the terms and conditions of the declaration signed by the emigrants and explain the

implications should they return to South Africa within a period of five years. Both parties must sign and

date the declaration.

Page 5

Declaration continued- clients must be made aware of the serious nature of the declaration. Request

the client to initial next to each item confirming that they have read and understood the contents thereof.

12

Standard Bank Moving Forward™ Emigration Process Guide

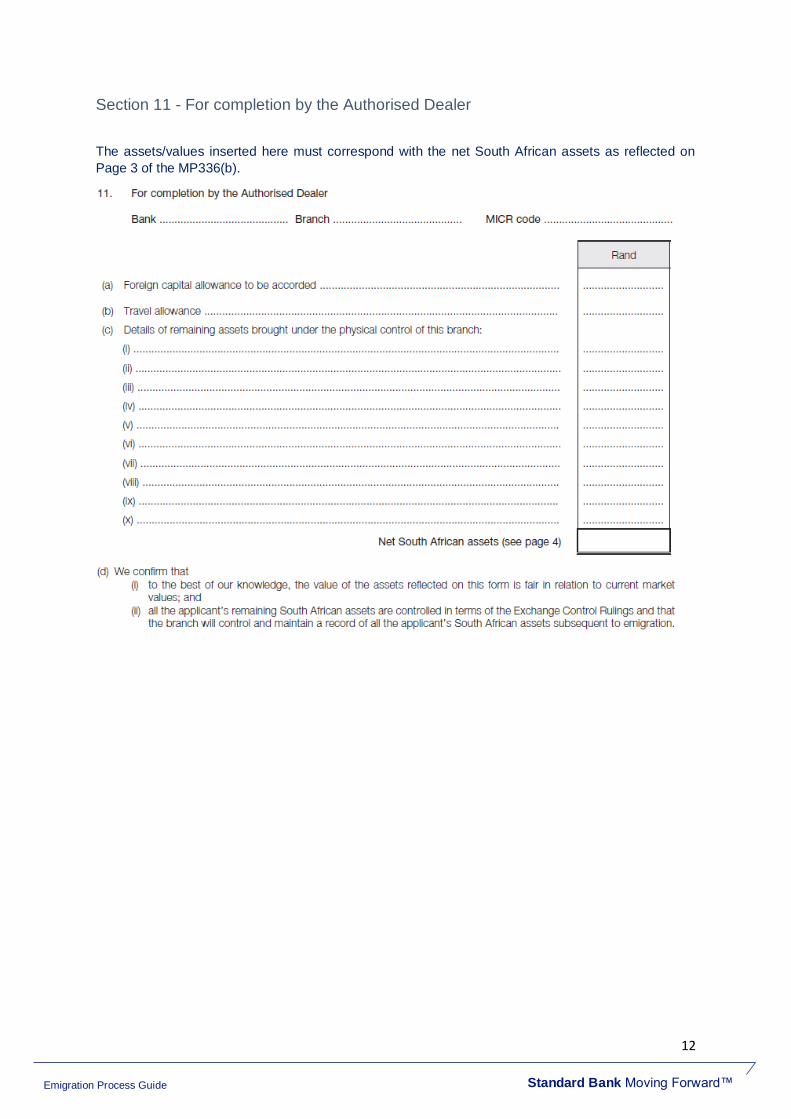

Section 11 - For completion by the Authorised Dealer

The assets/values inserted here must correspond with the net South African assets as reflected on

Page 3 of the MP336(b).

13

Standard Bank Moving Forward™ Emigration Process Guide

Extract from Currency and Exchanges Manual

Individuals regarded as residents by the Financial Surveillance Department who are leaving South Africa to take up permanent residence in any country outside the CMA may apply to an Authorised Dealer before departure to be accorded the facilities set out below. Applications must be accompanied by a duly completed Form MP336(b) signed by the applicant, together with a duly electronically completed ‘Tax Clearance Certificate - Emigration’ obtained via the SARS Tax Compliance Status System. 4.2 Family units emigrating to any country outside the CMA will qualify, at the time of emigration and after all their assets have been brought under the administration of an Authorised Dealer, to be accorded the following facilities: (a) a foreign capital allowance of up to R20 million per calendar year after all liabilities including the cost of the relative passenger tickets and the applicable travel allowances in (b) below have been provided for; (b) in addition, a travel allowances applicable to each member of the family unit on the basis and subject to the prescribed limits; and (c) a widow or widower or a single parent with accompanying dependant(s) may also be regarded as a family unit. 4.3 Single persons may be accorded a foreign capital allowance of up to R10 million per calendar year after all liabilities including the cost of the relative passenger ticket and the applicable travel allowance, have been provided for. 4.4 Quoted and/or unquoted securities may be exported as part of or in lieu of the applicable foreign capital allowance based on the market value thereof at the time of availing of the applicable allowance. The relevant securities must, of course, be endorsed ‘non-resident’ by the Authorised Dealer concerned. 4.5 Donations or gifts in excess of R100 000 received within three years or capital distributions from inter vivos trusts within three years, prior to the date of emigration, will be deducted by your Authorised Dealer prior to according the remaining foreign capital allowance. 4.6 Provided that the prescribed SARS Customs Declaration is completed any household and personal effects, motor vehicles, caravans, trailers, motorcycles, stamps, coins and minted gold bars (excluding coins that are legal tender in South Africa) per family unit or single person, within the overall insured value of R2 million, may be exported. 4.7 Emigrants may transfer the proceeds of claims lodged by them for the loss of or damage to household and personal effects, motor vehicles, caravans, trailers, motorcycles, stamps and coins (excluding coins that are legal tender in South Africa). 4.8 Persons who have already emigrated but who have not fully utilised the current authorised foreign capital allowance may be accorded additional capital transfers provided that the total amount availed of does not exceed the current limits.

4.9 South African insurance companies may be requested to transfer life policies (excluding single-premium policies) from a register in South Africa to a register in any country outside the CMA, provided that: (a) they are satisfied that the insured has formally emigrated and has placed their emigration on record with the Authorised Dealer;

14

Standard Bank Moving Forward™ Emigration Process Guide

(b) in total the surrender values of the policies do not exceed R2 000 in respect of any one family unit; and (c) the relative transfer will not result in the beneficiaries receiving, on aggregate, assets with a value exceeding that of the applicable foreign capital allowance. 4.10 Upon receipt of confirmation of the emigrants’ departure from South Africa they will be re designated as resident in their new country, but the following procedures will apply in respect of assets held at the time of re designation: (a) any cash balances remaining after the appropriate facilities have been granted and all capital payments accruing thereafter to the emigrant, as well as the total proceeds of any asset subsequently sold, will require to be credited to an emigrant’s capital account, i.e. current, savings or interest bearing deposit account with an Authorised Dealer. Such funds may be utilised locally for any purpose, including locally managed investment products that have foreign exposures, such as collective investment schemes and long-term insurance policies, subject to the following: (aa) where such funds are utilised for investment purposes, e.g. investment in unit certificates issued by companies registered under the Collective Investment Schemes Control Act, 2002 (Act No. 45 of 2002), Authorised Dealers must at all times be able to demonstrate that such investments are being held to their order; (bb) the proceeds of mortgage bonds and/or mortgage bond participations forming part of the emigrants’ remaining assets, may be reinvested in further bonds and/or participations; and (cc) all quoted and/or unquoted securities owned by the emigrants at the time of their departure or accruing to them thereafter, must also be deposited with an Authorised Dealer and may be released for switching purposes, without the specific authority of the Financial Surveillance Department. Unquoted securities, however, may only be switched into quoted securities; (b) emigrants may not record a non-resident address in respect of any securities that form part of their remaining assets on emigration and such securities must be restrictively endorsed; (c) any other South African assets belonging to the emigrants at the time of their departure or accruing to them thereafter must be brought under the administration of an Authorised Dealer. The Financial Surveillance Department will, on application via an Authorised Dealer, consider requests to transfer the emigrants’ remaining liquid assets or the export of quoted and/or unquoted securities in lieu of cash, exceeding the foreign capital allowance limit of R20 million per family unit or R10 million per single person. Emigrants wishing to avail of the aforementioned dispensation must obtain a duly electronically completed ‘Tax Clearance Certificate – Foreign Investment Allowance’ in the prescribed format, issued by SARS bearing the SARS logo and specific background watermark obtained via the SARS Tax Compliance Status System which must accompany their application to the Financial Surveillance Department, for consideration; and (d) the proceeds from insurance policies may be transferred directly to the emigrant abroad where the emigrant has no bank account in South Africa, provided that the foreign capital allowance limit will not be exceeded. 4.11 Income due to emigrants defined hereunder is normally transferrable and all applications for the transfer of any other form of income must be referred to the Financial Surveillance Department via an Authorised Dealer: (a) interest and profit; (b) dividends: the declaration of a dividend in specie or a special dividend for any purpose requires the prior written approval of the Financial Surveillance Department; (c) income distributions from close corporations; (d) directors’ fees or members’ fees;

15

Standard Bank Moving Forward™ Emigration Process Guide

(e) pension payments paid by registered funds only; (f) cash bonuses on insurance policies; (g) income received from a trust created in terms of a last will and testament; (h) income received from an inter vivos trust (subject to the provisions outlined in subsection 4.17 hereunder); (i) rentals on fixed property including rental pool agreements, provided that rentals are substantiated by the production of a copy of the rental or rental pool agreement; (j) the difference between the purchase consideration and maturity value of quoted gilts; (k) annuity payments where the annuity has been in existence for a period of five years prior to the date of emigration; (l) annuity payments where the annuity has been funded from a pension pay out from a previous employer; and (m) refunds in respect of income tax paid by emigrants on income earned subsequent to the date of emigration. 4.12 Only the Authorised Dealer holding the emigrant’s remaining assets may allow the transfer of income earned in South Africa from the date of designation as an emigrant, provided that it can be established from the production of documentary evidence that: (a) the funds represent earned income from normal trading activities and do not include any element of a capital nature, e.g. the sale proceeds of assets or the revaluation of assets; (b) the funds do not represent future income; (c) where applicable the assets from which the income accrues are the sole property of the emigrant; (d) no third party has any interest therein; and (e) the emigrant has taken up permanent residence abroad. 4.13 Dividends, profit or income distributions received from non-quoted entities (excluding trusts) must be supported by an auditor’s report and representation letter. The format is specified in the Authorised Dealer Manual. Dividend distributions from quoted entities in favour of emigrant beneficiaries are transferable. 4.14 Requests for the transfer of income to the emigrant beneficiaries of a trust created in terms of a Last Will and Testament must be supported by an auditor’s report (Form MP1331 or Form MP1332) and representation letter (Form MP1330(a)). The wording and format may be accessed from the South African Reserve Bank’s website: www.reservebank.co.za, by following the links: Home>Regulation and supervision> Financial surveillance and exchange controls>Auditors reports and representation letters. 4.15 As an exception, however, where the total net income earned by a will trust does not exceed R500 000 per annum, it is not necessary to submit a Form MP1331 or a Form MP1332 in support of requests for the transfer of income abroad. In this regard a Form MP1330(a) must be submitted to an Authorised Dealer. 4.16 In the case of interim transfers of income from will trusts to emigrant beneficiaries, an interim representation letter must be submitted. The wording and format may be accessed from the South African Reserve Bank’s website: www.reservebank.co.za, by following the links: Home>Regulation and supervision> Financial surveillance and exchange controls>Auditors reports and representation letters.

16

Standard Bank Moving Forward™ Emigration Process Guide

4.17 All initial requests for the transfer of income derived from an inter vivos trust to emigrant beneficiaries are subject to certain conditions and must be referred to the Financial Surveillance Department via an Authorised Dealer. 4.18 Emigrants may be granted local financial assistance facilities in respect of bona fide foreign direct investment into South Africa without restrictions. However, where the funds are required for financial transactions and/or the acquisition of residential or commercial property in South Africa, a 1:1 borrowing ratio applies, i.e. for every R1 in cash or assets that a non-resident introduces or owns, such non-resident may borrow an equivalent amount in the local market. Financial transactions, inter alia, include the purchase and sale of any securities (listed or unlisted), hedging, securities lending, repurchase agreements and any derivative transactions on securities. If facilities are granted for the acquisition of fixed property, such facilities may not be increased at any stage based on a revaluation of the property in question. Local financial assistance granted to emigrants that utilise their remaining local Rand balances or Rand assets as collateral must comply with the 1:1 ratio irrespective of the nature of the transaction. 4.19 Emigrants who have been permanently resident outside the CMA for a period in excess of five years will on completion of the necessary immigration declaration and undertaking via an Authorised Dealer, be regarded as new immigrants to South Africa by the Financial Surveillance Department.

17

Standard Bank Moving Forward™ Emigration Process Guide

Opening a Non-Resident account

Please refer to the terms and conditions and the pricing guides. There are exchange control

restrictions that apply to a Non-Resident account and all credits and debits has to comply with the

Currency and Exchanges Manual. We further advise that cash deposit may not be deposited into your

Non-Resident Account. The pricing guide are for reference purposes and not to be returned to us.

The minimum activation fee is R1000 for opening the account.

We also offer the option to send the ATM / Debit card directly to you with additional cost alternative

you can collect your card at any Standard Bank branch.

N.B. The issued ATM/ Card cannot be utilized for withdrawals as this is a contravention of exchange

control. We issue the cards as this is a requirement to setup internet banking. There are exchange

control restrictions that apply to Non Resident account, where no cash deposit is allowed.

The documents needed to apply for a non-resident account:

• Non-resident application form. Please take note that page 4 of the application form needs to

be certified.

• Original certified copy of passport (Three Copies)

• Latest proof of residential address

• Indemnity form for card (if required)

• Replacement card (if required)

• FATCA

Original Certificate of introduction from existing bank translated in English –

• full names,

• passport number/ date of birth,

• your foreign address,

• length of relationship &

• the conduct of your account.

• Letter must be signed by the bank manager with his particulars and stamp.

• 3 months’ bank statements – Only required if you are applying for an Elite Current Account.

18

Standard Bank Moving Forward™ Emigration Process Guide

Converting your existing account (if applicable)

Account conversion involves designating your existing Standard Bank account as “non-resident”. The

account will only be converted to “emigrant’s transferable/emigrant’s capital upon receipt of a

favourable response from the South African Reserve Bank.

Please be advised that we require the below documents in order to convert the account to a non-

resident account:

- A valid certified passport copy (stamped and signed).

- The fax and email indemnity certified

- Personal contact information form

Documents need to be witnessed and stamped by either one of the following individuals:

- Any foreign bank within a Financial Action Task Force (FATF) member country (FATF)

- A Standard Bank correspondent bank, if outside FATF territories.

- A Commissioner of Oaths

- Lawyer or Notary Public,

- Justice of the Peace,

- Embassy, consulate or High Commission Office

- A member of the judiciary or senior civil servant

- Excluding the S.A Police and post office

Conclusion

A designated professional within the Exchange Control Department will be allocated to manage your

emigration application from the beginning until your relationship ends with Standard Bank.

![From: STANDARD BANK Date ... Africa... · From: ibsupport@ [mailto:standardbank.co.za information@standardbank.co.za] Sent: 02 March 2015 11:48](https://img.dokumen.tips/doc/110x75/5eb7e7069e76e136bd6a0ef2/from-standard-bank-date-africa-from-ibsupport-mailtostandardbankcoza.jpg)