Embed Size (px)

DESCRIPTION

GST

Citation preview

Case StudyROI for a Customer Relationship ManagementInitiative at GST

Professor Robert J. Sweeney, Wright State University

Professor Mark Jeffery, Kellogg School of Management

Professor Robert J.

Sweeney of Wright

State University and

Robert J. Davis of

Teradata prepared

this case study in

collaboration with

Professor Mark Jeffery

from Northwestern

University’s

Kellogg School of

Management as

the basis for class

discussion rather

than to illustrate

effectiveness of

management. Some

facts within the case

have been altered

for reasons of

confidentiality.

OverviewRobert Davis of Teradata entered the manage-

ment conference room at GST Inc. and was

greeted by Mark Johnson, GST CFO. Johnson

had a big smile and gave an enthusiastic:

‘Hi Bob, good to see you.’

It was three years since the original data mart

consolidation pilot program was initiated. The

results of the pilot study originally proposed by

Davis exceeded even the most optimistic fore-

cast. The documented ROI prompted GST to

consolidate the remaining 45 data marts into

an enterprise data warehouse (EDW). The now

complete EDW had a documented return on

investment of 65%, and had saved GST $27

million in just one year. Johnson was eager to

learn from Davis how GST might further lever-

age the $32 million infrastructure investment

to help grow top-line revenue.

Erica Kolks, Vice President of Marketing,

arrived at the meeting a few minutes later.

Kolks came to GST ten years ago shortly after

obtaining her MBA from the Kellogg School of

Management. She joined the GST management

team with an impressive background in mar-

keting and over 15 years of experience in the

telecommunications industry. Through the

years, Kolks had made several recommenda-

tions that helped GST better compete, especial-

ly in the growing wireless market.

Johnson remarked that Davis had some ideas

on how GST might maximize marketing

investments and improve sales revenues. Davis

explained that the natural next step for GST

was to leverage their new enterprise data ware-

house for top-line growth with Customer

Relationship Management (CRM) solutions.

Johnson suddenly looked perplexed. It was not

exactly what he had anticipated hearing,“We

already have CRM—the sales team sold me on

funding CRM some time ago, but I have no

idea what return we are getting on the $3 mil-

lion I dump into it every year.”

Kolks explained that four years ago, Jill

Newberg, Vice President of Sales Region #2 and

Dominique Arnold, Vice President of Sales,

Region #3 convinced Johnson that GST needed

CRM. That resulted in an updated call center

and a new sales force automation tool.

Kolks added that although the CRM

investments seemed to be worthwhile, it was

not what marketing needed. She needed to

identify which customers to best target for new

service offerings, cross sell/up sell the most

profitable mix of product offerings, and to

maximize return from their marketing invest-

ments. Kolks clearly wanted to analyze cus-

tomer behavior over time and more quickly act

on detailed customer information for

enhanced decision making.

Johnson did not want to acknowledge the CRM

investments had any payback, in spite of the

fact that Newberg and Arnold were convinced

Case StudyROI for a Customer Relationship ManagementInitiative at GST

EB-3104 PAGE 2 OF 13

“Your new enterprise data warehouse combined withanalytical CRM solutions could significantly contributeto top line growth.”

that they recognized return. He declared,“Since

performance metrics to determine the ROI

were not established during the adoption

phase and have not been monitored through-

out the implementation, the calculation of ROI

at this point is pure speculation.”

Davis could sense the tension. It was obvious

that this was not the first time that the ROI of

GST CRM initiative was discussed. It was also

apparent that CRM was a topic of confusion.

Johnson looked at Davis. He wanted to focus

on discussing new possibilities.

“Actually,” said Davis,“I was thinking about

analytical CRM. Your new enterprise data

warehouse combined with analytical CRM

solutions could improve the take rate of your

important marketing programs and the reten-

tion of your most profitable customers, signifi-

cantly contributing to top-line growth.”

Johnson was skeptical, but he knew that Davis

had not disappointed him with the data mart

consolidation program. Kolks liked what she

heard and wanted to learn more. Johnson and

Kolks concurred that if Davis could demonstrate

a believable ROI, GST would be very interested.

Davis was excited with this response and start-

ed to map out the next steps. He believed that

the first step was to propose a detailed busi-

ness discovery. Once the business discovery

was complete, the ultimate question was “what

was the ROI and payback for the Teradata CRM

solution?” Davis knew his team had a lot of

work to do, but he felt confident that this new

project would be a success, provided that he

could convince Johnson and Kolks it was worth

the investment.

TELECOMMUNICATIONSINDUSTRY

The explosion in the demand for wireless serv-

ices, deregulation, the elimination of barriers

in the European markets, and an ever-growing

Internet market characterized the telecommu-

nications industry as the millennium came to

a close. However, once attractive profit margins

were shrinking or disappearing altogether,

consolidation had replaced expansion as the

industry practice, and the trend of almost

unlimited spending for new infrastructure had

been reversed. In 2001, many viewed the tele-

com industry as ‘melting down’.

Bankruptcies have been filed and many more

were expected. Experts believed the U.S. and

European telecom companies, burdened with

about $700 billion in debt, would either default

on, or force lenders to restructure, over $100

billion of this debt.1 The telecommunications

industry crisis was reminiscent of the real

estate debacle that befell the savings and loan

industry in the 1980s.

The promise of heightened competition

following deregulation was proving illusory.

Consolidation within the industry, coupled

with a dampened enthusiasm by Wall Street

limiting available capital for new entrants, was

negatively affecting everything from customer

service to spending on new technologies.

Although the number of telephone calls and

the amount of data transmitted were both ris-

ing, companies had found customers demand-

ing lower prices. This combination results in

modest revenue growth and a declining return

on equity. According to Lehman Brothers, Inc.,

the 5.9% return on equity in 2000 was down

from the 13.8% figure achieved in 1996.1

Analysts were not expecting the industry to

return to the earlier level of profitability for

several years.

However, there were bright spots in an otherwise

bleak picture. Wireless continued to be a high

demand item and revenue growth was expect-

ed in metropolitan markets. According to

industry analysts:

“The up-tick in wireless will also come in spite

of rapidly slowing spending on next-generation

(also known as 3G) designed to dramatically

increase the speed of moving wireless data.

Rather, wireless carriers will be spending on

hybrid wireless local area networks, a more eco-

nomical way to offer high-bandwidth wireless

data coverage in key areas. They’ll also spend to

expand current-generation wireless infrastruc-

ture and upgrade their networks to accommo-

date increased customer demand, ...” 2

With technologies coming and going,

mergers and acquisitions that blurred the

boundaries between service providers, and

fickle customers that had a countless array of

choices (both wireless and long distance), the

communications environment had never been

more challenging. The industry found itself in

the unenviable position of scrambling to keep

up with a technological explosion while mar-

gins evaporated and the regulatory landscape

changed. In addition, Telco’s faced these condi-

tions in the midst of the worst economic reces-

sion in a decade that had lessened Wall Street’s

willingness to pump funding into the industry.

Case StudyROI for a Customer Relationship ManagementInitiative at GST

EB-3104 PAGE 3 OF 131 Telecom Meltdown, Peter Elstrom and Heather Timmons, BusinessWeek, April 23, 2001. 2 Tailwinds in the Telecom Tempest, Olga Kharif, BusinessWeek, June 20, 2001.

As the telecommunications challenges had

evolved, so had their strategies for survival.

Fred Harris, vice-president for research, archi-

tecture, and design at Sprint succinctly

described the situation for the entire industry

when he said:

“We are in the business to make money, so

our investments follow where our customer

demand is.”2

SURVIVING THE STORM

To win in these new conditions businesses must

understand what their customers’ demand is

today and what that demand will become

tomorrow. It is not enough to understand what

has happened. A successful communications

service provider must analyze detailed customer

data to better understand ‘why’ it happened and

proactively manage to better forecast ‘what will’

happen—and then ensure that it takes place.

For example, managers should ask:

how do you analyze a customer’s

propensity to buy new or addition-

al bundles of services? How do you

predict and respond to events that

may lure away current customers

to the competition? How do you

satisfy the customer and maintain

double-digit growth while control-

ling costs? How do you communi-

cate with your most valuable cus-

tomers to increase the depth of the

relationship and important wallet

share of that customer? In order to

answer these questions, a corpo-

rate commitment must be taken to

shift the entire organization from a

product centric focus to a cus-

tomer centric focus.

In addition, all resources of the firm must be

managed optimally to maximize value. These

resources include the operational aspects of

the firm—product supply chain management,

enterprise resource management, services sup-

ply chain management — as well as the man-

agement of the financial aspects of the opera-

tions. Decision-makers need a single view of

the enterprise in order to get the most out of

the resources of the firm. This integrated view

is made possible with enterprise data

warehousing (EDW) technology, and is

enhanced with Customer Relationship

Management (CRM) solutions.

CUSTOMER RELATIONSHIPMANAGEMENT

Confusion in the marketplace seems to abound

about CRM, not only from the need to clearly

understand the potential return on investment

but also with basic definitions and the compet-

itive landscape of technology vendors that sell

in this market space. CRM should be viewed

first and foremost as an organizational strategy

to understand and influence customer behavior

through continuous communication to

improve customer acquisition, customer reten-

tion, and customer profitability.

Another commonly used definition places the

focus of the strategy on identifying the right

customer with the right offer, at the right time,

using the right channel. Armed with this per-

spective, CRM should therefore not be consid-

ered “product point solutions” but rather, tech-

nology-enabled solutions and associated skills

that support the organizational strategy of

being customer centric.

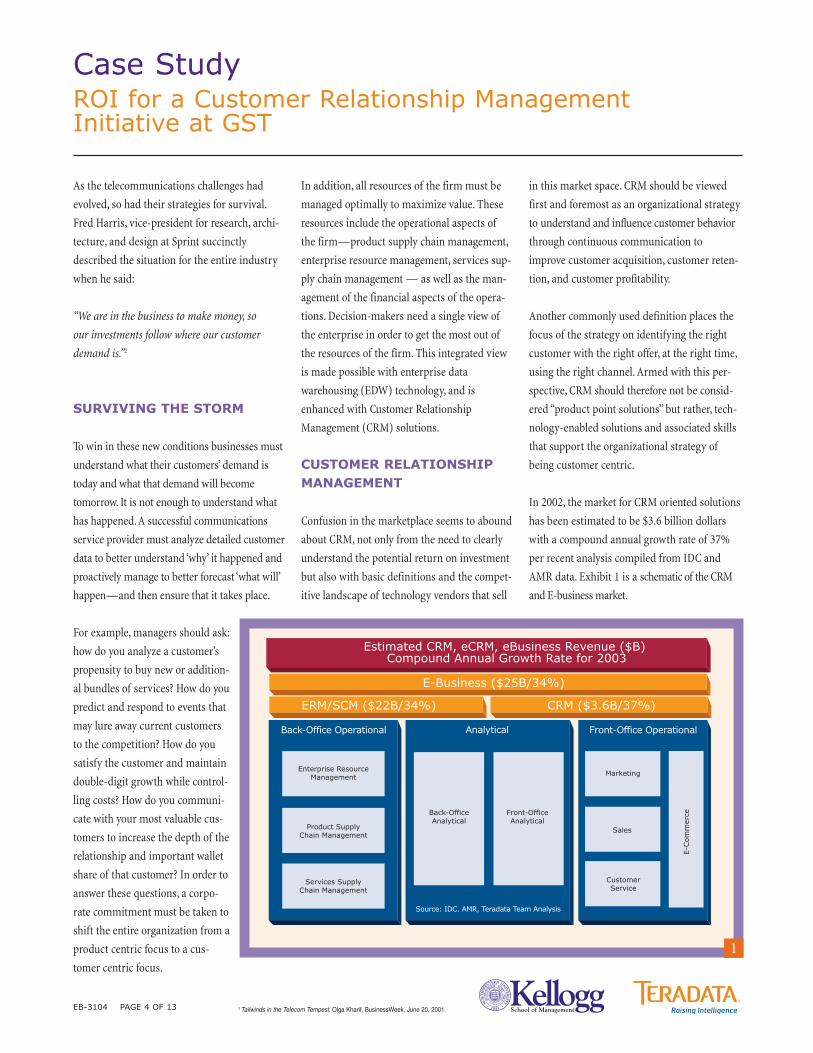

In 2002, the market for CRM oriented solutions

has been estimated to be $3.6 billion dollars

with a compound annual growth rate of 37%

per recent analysis compiled from IDC and

AMR data. Exhibit 1 is a schematic of the CRM

and E-business market.

Case StudyROI for a Customer Relationship ManagementInitiative at GST

EB-3104 PAGE 4 OF 13 2 Tailwinds in the Telecom Tempest, Olga Kharif, BusinessWeek, June 20, 2001.

ERM/SCM ($22B/34%)

E-Business ($25B/34%)

CRM ($3.6B/37%)

AnalyticalBack-Office Operational

Enterprise ResourceManagement

Product SupplyChain Management

Services SupplyChain Management

Front-Office Operational

Marketing

Sales

CustomerService

E-C

om

mer

ceBack-OfficeAnalytical

Front-OfficeAnalytical

Source: IDC. AMR, Teradata Team Analysis

Estimated CRM, eCRM, eBusiness Revenue ($B) Compound Annual Growth Rate for 2003

1

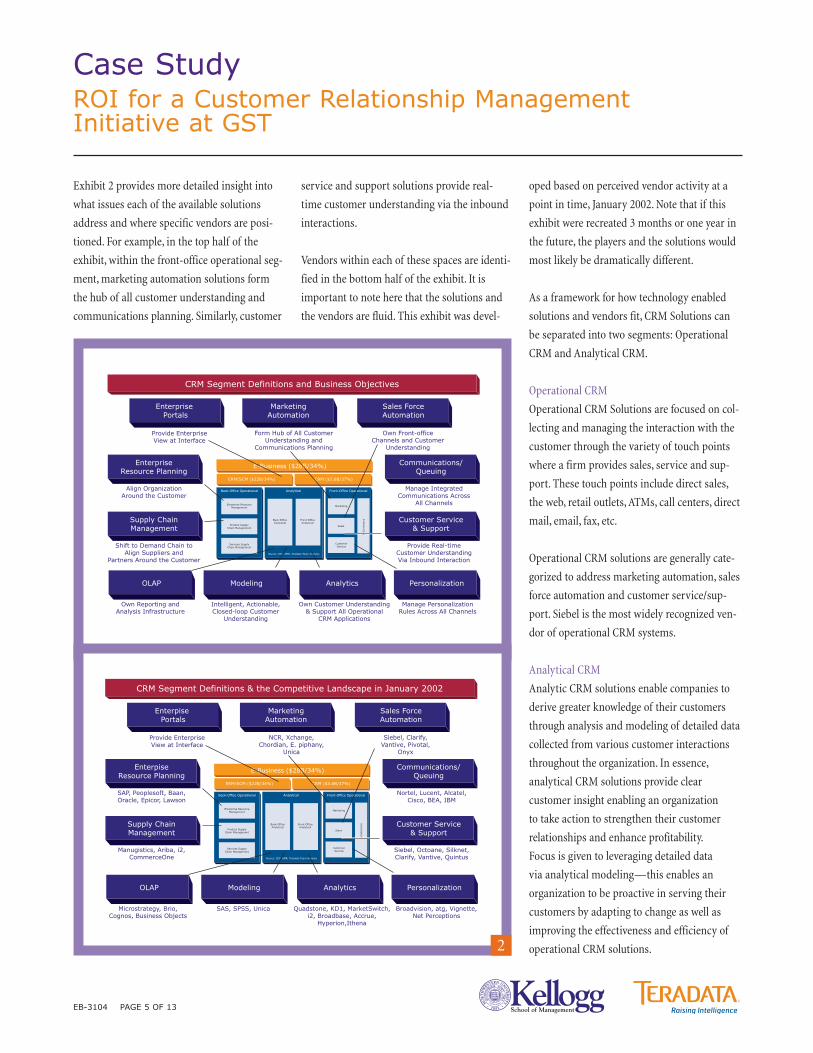

Exhibit 2 provides more detailed insight into

what issues each of the available solutions

address and where specific vendors are posi-

tioned. For example, in the top half of the

exhibit, within the front-office operational seg-

ment, marketing automation solutions form

the hub of all customer understanding and

communications planning. Similarly, customer

service and support solutions provide real-

time customer understanding via the inbound

interactions.

Vendors within each of these spaces are identi-

fied in the bottom half of the exhibit. It is

important to note here that the solutions and

the vendors are fluid. This exhibit was devel-

oped based on perceived vendor activity at a

point in time, January 2002. Note that if this

exhibit were recreated 3 months or one year in

the future, the players and the solutions would

most likely be dramatically different.

As a framework for how technology enabled

solutions and vendors fit, CRM Solutions can

be separated into two segments: Operational

CRM and Analytical CRM.

Operational CRM

Operational CRM Solutions are focused on col-

lecting and managing the interaction with the

customer through the variety of touch points

where a firm provides sales, service and sup-

port. These touch points include direct sales,

the web, retail outlets, ATMs, call centers, direct

mail, email, fax, etc.

Operational CRM solutions are generally cate-

gorized to address marketing automation, sales

force automation and customer service/sup-

port. Siebel is the most widely recognized ven-

dor of operational CRM systems.

Analytical CRM

Analytic CRM solutions enable companies to

derive greater knowledge of their customers

through analysis and modeling of detailed data

collected from various customer interactions

throughout the organization. In essence,

analytical CRM solutions provide clear

customer insight enabling an organization

to take action to strengthen their customer

relationships and enhance profitability.

Focus is given to leveraging detailed data

via analytical modeling—this enables an

organization to be proactive in serving their

customers by adapting to change as well as

improving the effectiveness and efficiency of

operational CRM solutions.

Case StudyROI for a Customer Relationship ManagementInitiative at GST

EB-3104 PAGE 5 OF 13

CRM Segment Definitions and Business Objectives

E-Business ($28B/34%)

ERM/SCM ($22B/34%) CRM ($3.6B/37%)

Back-Office Operational Front-Office OperationalAnalytical

Enterprise ResourceManagement Marketing

Sales

CustomerService

Product SupplyChain Management

Services SupplyChain Management

E-C

om

mer

ceBack-OfficeAnalytical

Front-OfficeAnalytical

Source: IDC. AMR, Teradata Team Analysis

MarketingAutomation

Enterprise Portals

Sales ForceAutomation

Communications/Queuing

Customer Service& Support

EnterpriseResource Planning

Supply ChainManagement

PersonalizationAnalyticsModelingOLAP

Provide EnterpriseView at Interface

Form Hub of All Customer Understanding and

Communications Planning

Own Front-officeChannels and Customer

Understanding

Manage Integrated Communications Across

All Channels

Provide Real-timeCustomer UnderstandingVia Inbound Interaction

Manage PersonalizationRules Across All Channels

Own Customer Understanding & Support All Operational

CRM Applications

Intelligent, Actionable, Closed-loop Customer

Understanding

Own Reporting andAnalysis Infrastructure

Shift to Demand Chain toAlign Suppliers and

Partners Around the Customer

Align OrganizationAround the Customer

CRM Segment Definitions & the Competitive Landscape in January 2002

E-Business ($28B/34%)

ERM/SCM ($22B/34%) CRM ($3.6B/37%)

Back-Office Operational Front-Office OperationalAnalytical

Enterprise ResourceManagement Marketing

Sales

CustomerService

Product SupplyChain Management

Services SupplyChain Management

E-C

om

mer

ceBack-OfficeAnalytical

Front-OfficeAnalytical

Source: IDC. AMR, Teradata Team Analysis

MarketingAutomation

Enterpise Portals

Sales ForceAutomation

Communications/Queuing

Customer Service& Support

EnterpiseResource Planning

Supply ChainManagement

PersonalizationAnalyticsModelingOLAP

Provide EnterpriseView at Interface

NCR, Xchange,Chordian, E. piphany,

Unica

Siebel, Clarify,Vantive, Pivotal,

Onyx

Nortel, Lucent, Alcatel,Cisco, BEA, IBM

Siebel, Octoane, Silknet,Clarify, Vantive, Quintus

Broadvision, atg, Vignette,Net Perceptions

Quadstone, KD1, MarketSwitch, i2, Broadbase, Accrue,

Hyperion,Ithena

SAS, SPSS, UnicaMicrostrategy, Brio,Cognos, Business Objects

Manugistics, Ariba, i2,CommerceOne

SAP, Peoplesoft, Baan,Oracle, Epicor, Lawson

2

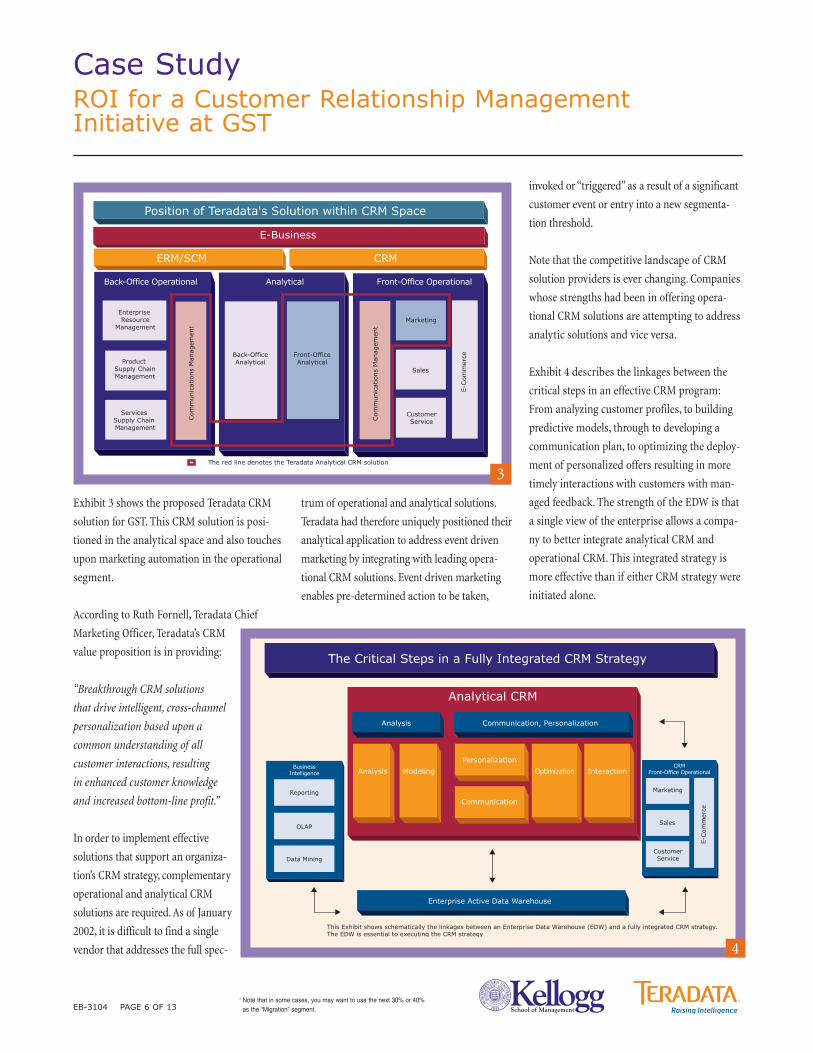

Exhibit 3 shows the proposed Teradata CRM

solution for GST. This CRM solution is posi-

tioned in the analytical space and also touches

upon marketing automation in the operational

segment.

According to Ruth Fornell, Teradata Chief

Marketing Officer, Teradata’s CRM

value proposition is in providing:

“Breakthrough CRM solutions

that drive intelligent, cross-channel

personalization based upon a

common understanding of all

customer interactions, resulting

in enhanced customer knowledge

and increased bottom-line profit.”

In order to implement effective

solutions that support an organiza-

tion’s CRM strategy, complementary

operational and analytical CRM

solutions are required. As of January

2002, it is difficult to find a single

vendor that addresses the full spec-

trum of operational and analytical solutions.

Teradata had therefore uniquely positioned their

analytical application to address event driven

marketing by integrating with leading opera-

tional CRM solutions. Event driven marketing

enables pre-determined action to be taken,

invoked or “triggered” as a result of a significant

customer event or entry into a new segmenta-

tion threshold.

Note that the competitive landscape of CRM

solution providers is ever changing. Companies

whose strengths had been in offering opera-

tional CRM solutions are attempting to address

analytic solutions and vice versa.

Exhibit 4 describes the linkages between the

critical steps in an effective CRM program:

From analyzing customer profiles, to building

predictive models, through to developing a

communication plan, to optimizing the deploy-

ment of personalized offers resulting in more

timely interactions with customers with man-

aged feedback. The strength of the EDW is that

a single view of the enterprise allows a compa-

ny to better integrate analytical CRM and

operational CRM. This integrated strategy is

more effective than if either CRM strategy were

initiated alone.

Case StudyROI for a Customer Relationship ManagementInitiative at GST

EB-3104 PAGE 6 OF 13

E-Business

ERM/SCM CRM

Back-Office Operational Analytical Front-Office Operational

Enterprise Resource

ManagementMarketing

Sales

CustomerService

Product Supply ChainManagement

Services Supply Chain Management

E-C

om

mer

ceBack-OfficeAnalytical

Front-OfficeAnalytical

Com

munic

atio

ns

Man

agem

ent

Com

munic

atio

ns

Man

agem

ent

Position of Teradata's Solution within CRM Space

The red line denotes the Teradata Analytical CRM solution

3

Analytical CRM

CRMFront-Office Operational

Marketing

Sales

CustomerService

E-C

om

mer

ce

BusinessIntelligence

Reporting

OLAP

Data Mining

Analysis Communication, Personalization

Personalization

Communication

Analysis Modeling Optimization Interaction

Enterprise Active Data Warehouse

The Critical Steps in a Fully Integrated CRM Strategy

This Exhibit shows schematically the linkages between an Enterprise Data Warehouse (EDW) and a fully integrated CRM strategy. The EDW is essential to executing the CRM strategy

4

1 Note that in some cases, you may want to use the next 30% or 40%as the “Migration” segment.

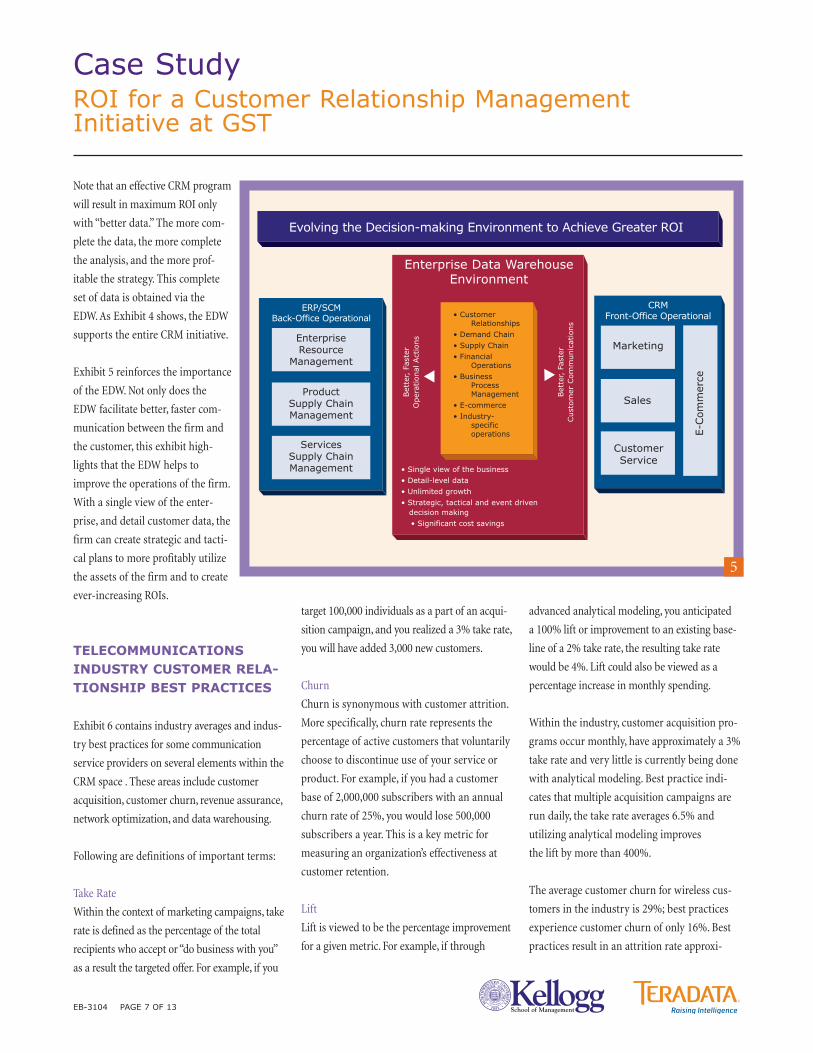

Note that an effective CRM program

will result in maximum ROI only

with “better data.” The more com-

plete the data, the more complete

the analysis, and the more prof-

itable the strategy. This complete

set of data is obtained via the

EDW. As Exhibit 4 shows, the EDW

supports the entire CRM initiative.

Exhibit 5 reinforces the importance

of the EDW. Not only does the

EDW facilitate better, faster com-

munication between the firm and

the customer, this exhibit high-

lights that the EDW helps to

improve the operations of the firm.

With a single view of the enter-

prise, and detail customer data, the

firm can create strategic and tacti-

cal plans to more profitably utilize

the assets of the firm and to create

ever-increasing ROIs.

TELECOMMUNICATIONSINDUSTRY CUSTOMER RELA-TIONSHIP BEST PRACTICES

Exhibit 6 contains industry averages and indus-

try best practices for some communication

service providers on several elements within the

CRM space . These areas include customer

acquisition, customer churn, revenue assurance,

network optimization, and data warehousing.

Following are definitions of important terms:

Take Rate

Within the context of marketing campaigns, take

rate is defined as the percentage of the total

recipients who accept or “do business with you”

as a result the targeted offer. For example, if you

target 100,000 individuals as a part of an acqui-

sition campaign, and you realized a 3% take rate,

you will have added 3,000 new customers.

Churn

Churn is synonymous with customer attrition.

More specifically, churn rate represents the

percentage of active customers that voluntarily

choose to discontinue use of your service or

product. For example, if you had a customer

base of 2,000,000 subscribers with an annual

churn rate of 25%, you would lose 500,000

subscribers a year. This is a key metric for

measuring an organization’s effectiveness at

customer retention.

Lift

Lift is viewed to be the percentage improvement

for a given metric. For example, if through

advanced analytical modeling, you anticipated

a 100% lift or improvement to an existing base-

line of a 2% take rate, the resulting take rate

would be 4%. Lift could also be viewed as a

percentage increase in monthly spending.

Within the industry, customer acquisition pro-

grams occur monthly, have approximately a 3%

take rate and very little is currently being done

with analytical modeling. Best practice indi-

cates that multiple acquisition campaigns are

run daily, the take rate averages 6.5% and

utilizing analytical modeling improves

the lift by more than 400%.

The average customer churn for wireless cus-

tomers in the industry is 29%; best practices

experience customer churn of only 16%. Best

practices result in an attrition rate approxi-

Case StudyROI for a Customer Relationship ManagementInitiative at GST

EB-3104 PAGE 7 OF 13

Enterprise Data WarehouseEnvironment

CRMFront-Office Operational

Marketing

Sales

CustomerService

E-C

omm

erce

ERP/SCMBack-Office Operational

EnterpriseResource

Management

ProductSupply ChainManagement

ServicesSupply ChainManagement

• CustomerRelationships

• Demand Chain• Supply Chain• Financial

Operations• Business

ProcessManagement

• E-commerce• Industry-

specificoperations

Evolving the Decision-making Environment to Achieve Greater ROI

• Single view of the business• Detail-level data• Unlimited growth• Strategic, tactical and event driven

decision making• Significant cost savings

Bet

ter, F

aste

rO

per

atio

nal

Act

ions

Bet

ter, F

aste

rCust

om

er C

om

munic

atio

ns5

mately one-half the industry average. For long

distance, the industry average is 25% annually

while best practice only loses 20% per year.

Customer churn for cable, on average, is 28%;

for firms demonstrating best practice, they

only lose 7.3% to attrition.

Revenue assurance statistics contained in Exhibit

6 refers to fraud management. On average, the

industry loses over 5% of revenue to fraud, takes

90-120 days to detect and remove fraud, and

fraud constitutes about 15% of bad debts. Best

practice, on the other hand, detects and removes

fraud in fewer than 3 days—this reduces the per-

cent of bad debts associated with fraud to 2%

and the percent of revenue lost to fraud to 1%.

The management of operational assets is also

compared for the industry and best practice.

The industry examines monthly data trends,

generates engineering reports monthly and

receives 50–100 customer complaints per day.

Best practice in the same industry produces

daily data trends, daily engineering reports,

and receives fewer than 2 customer complaints

per day for a comparable company.

Finally, considering the industry’s use of data

warehouses, on average, 1–2 operations are sup-

ported, fewer than 20 end users, and fewer than

10 applications. Firms that fully exploit their

warehouse typically handle more than 10,000

end users and run more than 100 applications.

A CRM STRATEGY FOR GST INC.

A Single Integrated View of the Customer

As a result of the data mart consolidation proj-

ect, GST had made significant progress in

bringing together a wide variety of processes

and systems to achieve an integrated view of

their customers. End users and decision-mak-

ers no longer had to search for information

about its business, customers and competitors

in multiple data silos. One marketing manager

commented:

“With the new enterprise data warehouse I no

longer have to wait weeks before getting important

information on my largest corporate accounts.”

Several marketing mangers wanted to under-

stand how to take more complete advantage of

the customer information in the Teradata data

warehouse. With the EDW they could access

customer information quickly, but they lacked

the right analytical tools to improve take rates.

Davis knew that the Teradata CRM solution

could assist in this and other areas.

The Power of Analytics

Davis wanted to clearly position the Teradata

CRM solution. Operational CRM is typically

only effective when combined with robust

analysis and planning tools. These tools enable

managers to understand who the

customers are, patterns and trends in their

behavior, and to craft communications tailored

to individual customer needs.

Davis also wanted to position the value of

GST’s existing Teradata data warehouse

as the foundation to store all customer

information (transactional, external and/or

purchased data). The data warehouse would

therefore enable the development of new

creative approaches to better understand and

predict customer behavior. He knew that

GST’s EDW combined with Teradata CRM

solutions would enhance decision-making,

especially given the dynamic environment

that GST was forced to compete in.

Exhibit 1 and Exhibit 3 illustrate the CRM

landscape and an enterprise view of CRM

using the Teradata data warehouse. The EDW

would act as a bridge between operational

CRM (such as sales force automation tools)

and analytical CRM (predictive capabilities)

for improved business insights.

Case StudyROI for a Customer Relationship ManagementInitiative at GST

EB-3104 PAGE 8 OF 13

Customer Acquisition Campaignsa. Quantity of Campaigns a. Monthly (12/year) a. 20–50 per dayb. Take rates b. _ – 5% b. 5 – 8%c. Lift with analytical modeling c. n/a c. 442%Customer Churna. Wireless a. 29% a. 16%b. Long Distance b. 25% b. 20%c. Cable c. 28% c. 7.3%Revenue Assurancea. Lost revenue to fraud a. 5–6% a. 1%b. Days: fraud detect-to-remove b. 90–120 days b. 2–3 daysc. Fraud % of bad debt c. 15% c. 2%Network Optimizationa. Data trending a. Every 30 days a. dailyb. Engineering reports b. Every 30 days b. dailyc. Customer complaints c. 50-100 per day c. 1–2 per dayData Warehousinga. Organizations supported a. 1–2 a. Entire enterpriseb. Average number of end users b. 5–20 b > 10,000

Average number of applications c. 1–10 c. > 100

Business Driver Industry Averages Industry Best Practices

Industry Averages and Industry Best PracticesTelecommunications Industry

Adapted from: “Communications Strategies and Best Practices” by Jack Knapp, Director of Marketing, Teradata, and Carol Martin, Marketing Specialist, Teradata

66

Davis planned to focus his recommendation

on the business benefits of CRM. With

appreciation for the internal battles

that Kolks might face, Davis prepared a

business discovery proposal (see Exhibit 7).

The business discovery was an important

starting point for GST’s analytic CRM initiative.

The proposal defined a business discovery as a

statement of work between Teradata and GST to

identify the “pain points” most critical to senior

management and to suggest a specific solution

based on the findings. During the

business discovery, Teradata professional

services would also collect current

financial and operational information

and develop a projection of the return

on investment (ROI) associated with the

proposed Teradata CRM solution.

BUSINESS DISCOVERY

Statement of Work

The Statement of Work (SOW) between

Teradata and GST, is included in

Exhibit 7. The SOW details, step by

step the process Teradata would follow

when developing a specific solution.

The exhibit describes the business

impact assessment as well as the

development and delivery of the

business impact model. In addition,

the project’s duration and the responsi-

bilities of the parties to the agreement

are detailed.

Kolks was successful in selling the

business discovery to her peers. Kolks

liked that the business discovery would

help enable buy-in across multiple

business units on the most critical

business issues. She also knew that

she would need assistance in defining metrics

for the ROI. Teradata’s business discovery was

appealing to GST senior management, since it

would assess GST’s standing within the indus-

try and propose a solution to help GST move

towards best practices.

Findings

The business discovery process uncovered

many facts, summarized in Exhibit 8,

which Davis would present to Kolks and

Johnson in his final recommendation.

The main finding, described below, was

that GST needed to embark on a targeted

acquisition campaign.

A review of GST’s 5-year strategic plan by the

Teradata team discovered a growth target for

a portion of their customer base. Specifically,

GST management believed the 13,000,000

wireless accounts should grow by 5% per year.

Furthermore, GST currently ran monthly

campaigns to acquire new customers.

Case StudyROI for a Customer Relationship ManagementInitiative at GST

EB-3104 PAGE 9 OF 13

Statement of Work Between Teradata and GST Inc.

This Statement of Work (“SOW”) between Teradata, a division of NCR Corporation (“TERADATA”) and GST Inc. (“GST”) isfor services to be provided to GST by TERADATA in connection with Business Impact Consulting.

1. Project SCOPE/Services1.1 Scope. TERADATA will have its consultant(s) review and analyse GST’s current financial and operational results and will

facilitate a meeting to discuss TERADATA’s findings and make recommendations. TERADATA will interface with a person appointed by GST to sponsor the work (“Business Impact Assessment Sponsor”).TERADATA will provide the following:• Business Impact Assessment • Development and Delivery of Business Impact Model

1.2 Business Impact Assessment. TERADATA will interview a number of GST employees to collect current financial and operational information and develop a projection of the return on investment (ROI) associated with the proposedsolution. TERADATA will provide a presentation of business impact assessment findings to GST.

1.3 Development and Delivery of Business Impact Model. TERADATA will leverage the knowledge gained from the BusinessImpact Assessment task to develop and deliver a detailed Business Impact Report and a GST specific Business ImpactModel for further analysis and use. TERADATA will provide a presentation of the anticipated financial results andoverview of the business impact model.

2. Project DeliverablesTERADATA will provide a written report covering its findings and recommendations from the assessment services. The

report may cover areas such as:Business Impact Assessment • An Executive Summary • Recap of Business/Operational Impact Findings• Financial Impact ReportBusiness Impact Model • Development of a GST specific business impact model based on TERADATA’s impact model(s)• Restricted access to customer specific Business Impact Model (Microsoft Excel Version with access to formulas

locked)

3. Project DURATION3.1 The parties anticipate that TERADATA service delivery will begin on 7th January 2002 (“Start Date”) and be

completed within approximately 4 weeks from the Start Date (“End Date”). Should the Start Date be postponed due toa delay in the execution of this SOW, or non-availability of GST personnel, the End Date may be extended. GST will grantthis extension with no penalty to TERADATA.

3.2 GST recognises that any delay that GST may incur in providing to TERADATA the technological and human resources,data, and necessary information for the execution of the objectives of this Service may, in turn, generate a delay inTERADATA’s provision of services. GST also recognizes that the provision of information that is inexact, incomplete,and/or different from specified requirements may generate similar delays. When these delays result in an increase inService cost, TERADATA will inform GST of any impact to cost, schedule, services, or Deliverables.

Continued next page

7

2 Note that marketing research studies may provide additional insights into what constitutes a reasonable percentage increase in value.

3 This is where some thought will have to be given as to what marketing actions will be taken.

As an example, one targeted acquisition

campaign started with GST’s analysis

of their customer base and prospect

list (augmented by external information

on the household) for children

between the ages of 15 – 17 who were

celebrating a birthday. The offer was

made through direct mail to the par-

ent(s) with a special package on a pre-

paid wireless phone. For $99, the par-

ent could buy the phone and the initial

1,000 minutes of use. The customer

would then have the option of prepay-

ing ongoing required increments of

time with options available for $30, $50

or $100 with cost per minute being

lower as you buy larger “blocks” of air-

time. The value of the offer stressed a

“manageable plan” from a cost stand-

point that provides the added security

of being in touch with your ever more

mobile children.

The process for designing and execut-

ing other campaigns was the same,

independent of the details of the offer.

The process began with analysis and

segmentation of targeted prospects for

increased probability of acceptance.

A personalized offer was then extended

through single or multi channels

(direct mail, telemarketers, and

email) — the results were tracked

for continued knowledge of customers

and prospects.

GST’s latest experience shows that the

cost to contact a single potential new

customer is $5. Approximately 3% of

the potential customers contacted

recently became new customers (3%

take rate). In addition, the average

monthly spending by a customer in the

Case StudyROI for a Customer Relationship ManagementInitiative at GST

EB-3104 PAGE 10 OF 13

4. RESPONSIBILITIES4.1 TERADATA will provide the resource described in this SOW. GST will work with the TERADATA to provide the services

called for in this SOW and, as reasonably requested, will provide the required personnel to complete the services.4.2 GST will provide TERADATA personnel and third-party vendors with safe and reasonable access, working space and

facilities (including heat, light, ventilation, electric current, and outlets), convenient fax access, local telephone extensions(including outgoing analogue telephone lines for modems), computer space, and other necessary physical facilities for TERADATA and third-party personnel.

4.3 GST is responsible for the identification and interpretation of any applicable laws, regulations, and statutes that affect theexisting GST application system or programs that TERADATA will have access to under this SOW. It is the responsibility ofGST to assure that the systems and processes meet the requirements of those laws.

4.4 GST is responsible for the articulation and approval of the business requirements driving the definition of this phase of theservice. Additionally, GST is responsible to provide all the necessary data elements (customer specific responses) requiredto adequately assess the impact of the solution on their business. Any information provided regarding the return on invest-ment of the Project is a non-binding estimate only.

4.5 The services to be provided by TERADATA include only what is expressly described in the SOW. The services and deliver-ables excluded from the present contract include, but are not limited to, the solution of any problem originating from thequality of the data used to develop the Business Impact Model.

5. Personnel5.1 TERADATA and GST will assign personnel to execute the roles required for this Project. Such personnel will constitute the

Project Team. Actual individuals assigned to the Project may fill different combinations of roles. TERADATA and GST willmake available additional personnel as needed.

5.2 Roles required for this SOW are as follows:TERADATA Roles:• Business Impact Modelling Analyst • Professional Services Consultant GST Roles• Business Impact Assessment Sponsor• Departmental Level Executives• Business Users

5.2 During the performance of this SOW, and for a period of one year thereafter, GST agrees to not employ, make an offer of employment to, or enter into a consulting relationship with any employee of, or subcontractor of, TERADATA who isdirectly involved with the delivery of services under this SOW, except upon the prior written consent of TERADATA, as stated in the Addendum.

6. Payment6.1 TERADATA will perform the services specified in this SOW for $30,000, made up of 15 days professional services at $2,000

per day. GST will be billed on a monthly basis.6.2 This price does not include travel and living expenses or the price for products, software, Third-Party Deliverables, or

maintenance.6.3 Travel and living expenses, including travel time to and from GST locations for TERADATA and its subcontractors, will be

invoiced on a monthly basis. GST will pay all invoices in accordance with the Master Agreement.6.4 All taxes incurred and all duties assessed on the products and services, except for income taxes levied against TERADATA,

are GST’s responsibility.6.5 The total amount billed to GST against this SOW, for both services and expenses will not exceed $50,000.

7. Change Control ProcessAny changes to this SOW, including scope, services, fees, etc., will be made in a written document signed by both parties.

8. DELIVERABLE COMPLETION SIGN-OFF 8.1 Deliverables will be considered accepted upon delivery. GST Program Sponsor will complete a “Deliverable Completion

Sign-Off Form” for each Deliverable or billing milestone.8.2 If GST requires rework or modifications beyond the scope of the Deliverable as provided in this SOW, TERADATA will

be entitled to an adjustment in price equal to TERADATA’s standard price for the additional work and a correspondingadjustment in the Project schedule. The Change Control Process will be followed to determine the impact of additional workrequired and both TERADATA and GST will agree to this work before it begins. Such rework or modifications may not belimited to the affected Deliverable and may include items such as regression testing or integrating the affected Deliverableinto the overall solution.

Continued from previous page

7

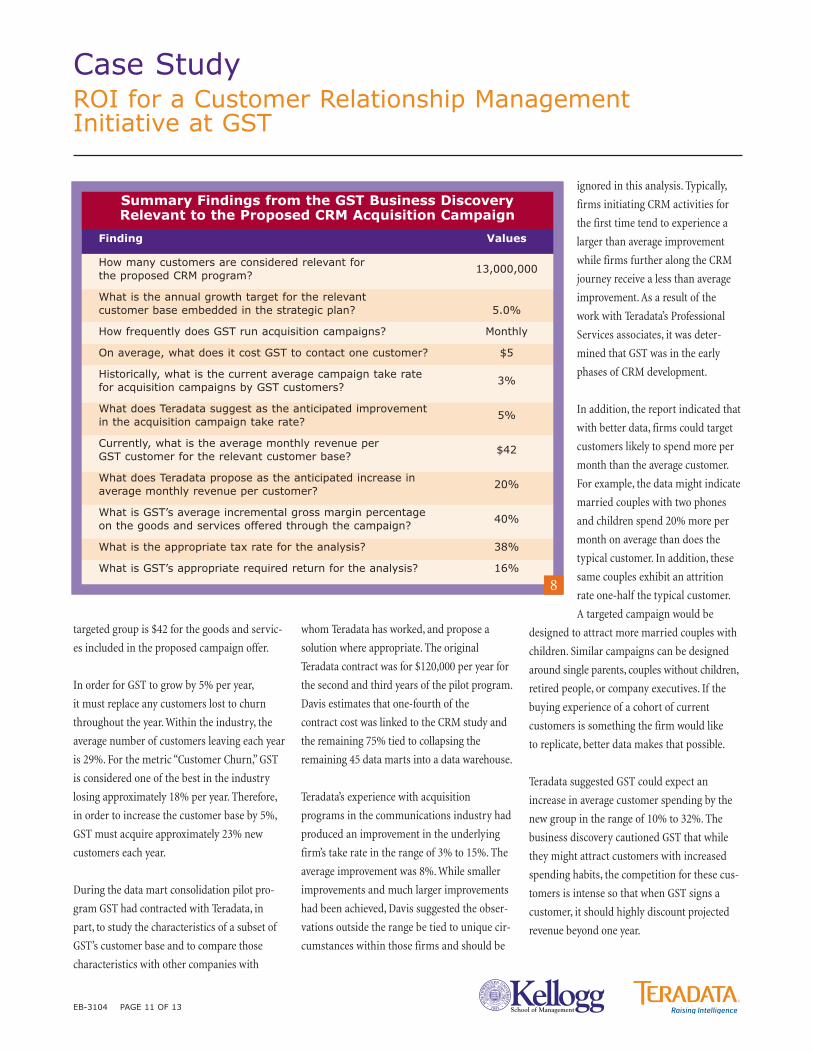

targeted group is $42 for the goods and servic-

es included in the proposed campaign offer.

In order for GST to grow by 5% per year,

it must replace any customers lost to churn

throughout the year. Within the industry, the

average number of customers leaving each year

is 29%. For the metric “Customer Churn,” GST

is considered one of the best in the industry

losing approximately 18% per year. Therefore,

in order to increase the customer base by 5%,

GST must acquire approximately 23% new

customers each year.

During the data mart consolidation pilot pro-

gram GST had contracted with Teradata, in

part, to study the characteristics of a subset of

GST’s customer base and to compare those

characteristics with other companies with

whom Teradata has worked, and propose a

solution where appropriate. The original

Teradata contract was for $120,000 per year for

the second and third years of the pilot program.

Davis estimates that one-fourth of the

contract cost was linked to the CRM study and

the remaining 75% tied to collapsing the

remaining 45 data marts into a data warehouse.

Teradata’s experience with acquisition

programs in the communications industry had

produced an improvement in the underlying

firm’s take rate in the range of 3% to 15%. The

average improvement was 8%. While smaller

improvements and much larger improvements

had been achieved, Davis suggested the obser-

vations outside the range be tied to unique cir-

cumstances within those firms and should be

ignored in this analysis. Typically,

firms initiating CRM activities for

the first time tend to experience a

larger than average improvement

while firms further along the CRM

journey receive a less than average

improvement. As a result of the

work with Teradata’s Professional

Services associates, it was deter-

mined that GST was in the early

phases of CRM development.

In addition, the report indicated that

with better data, firms could target

customers likely to spend more per

month than the average customer.

For example, the data might indicate

married couples with two phones

and children spend 20% more per

month on average than does the

typical customer. In addition, these

same couples exhibit an attrition

rate one-half the typical customer.

A targeted campaign would be

designed to attract more married couples with

children. Similar campaigns can be designed

around single parents, couples without children,

retired people, or company executives. If the

buying experience of a cohort of current

customers is something the firm would like

to replicate, better data makes that possible.

Teradata suggested GST could expect an

increase in average customer spending by the

new group in the range of 10% to 32%. The

business discovery cautioned GST that while

they might attract customers with increased

spending habits, the competition for these cus-

tomers is intense so that when GST signs a

customer, it should highly discount projected

revenue beyond one year.

Case StudyROI for a Customer Relationship ManagementInitiative at GST

EB-3104 PAGE 11 OF 13

Finding Values

How many customers are considered relevant for the proposed CRM program?

13,000,000

What is the annual growth target for the relevant customer base embedded in the strategic plan? 5.0%

How frequently does GST run acquisition campaigns? Monthly

On average, what does it cost GST to contact one customer? $5

Historically, what is the current average campaign take rate for acquisition campaigns by GST customers?

3%

What does Teradata suggest as the anticipated improvement in the acquisition campaign take rate?

5%

Currently, what is the average monthly revenue per GST customer for the relevant customer base?

$42

What does Teradata propose as the anticipated increase in average monthly revenue per customer?

20%

What is GST’s average incremental gross margin percentage on the goods and services offered through the campaign?

40%

What is the appropriate tax rate for the analysis? 38%

What is GST’s appropriate required return for the analysis? 16%

Summary Findings from the GST Business DiscoveryRelevant to the Proposed CRM Acquisition Campaign

8

Given the nature of the products and services

being offered (telecommunications) GST

should expect to begin receiving revenue from

any new customers in the month following the

campaign. In addition, from past experience

GST could assume the initial contract between

GST and the new customer would be for one

year. For example, a campaign run in January

would produce a new customer in February

and this new customer could be expected to

maintain his/her level of spending through the

following January. The first acquisition cam-

paign would be initiated one month after the

Teradata proposal was adopted.

GST FINANCIAL DATA & THE CRM PROJECT IMPLEMENTATIONCOSTS

The Teradata Professional Services

team suggested which items to

include in the product service offer.

These items included: 500 monthly

minutes of from anywhere to any-

where, 24/7, worldwide calling and

1000 peak-time monthly minutes

of Internet access through the

handset, laptop or television.

Standard with any offer were call

forwarding, call waiting, instant

paging/instant messaging, and

voice mail. Dan Wymer, CAO, deter-

mined the gross margin on those

items would be 40%.

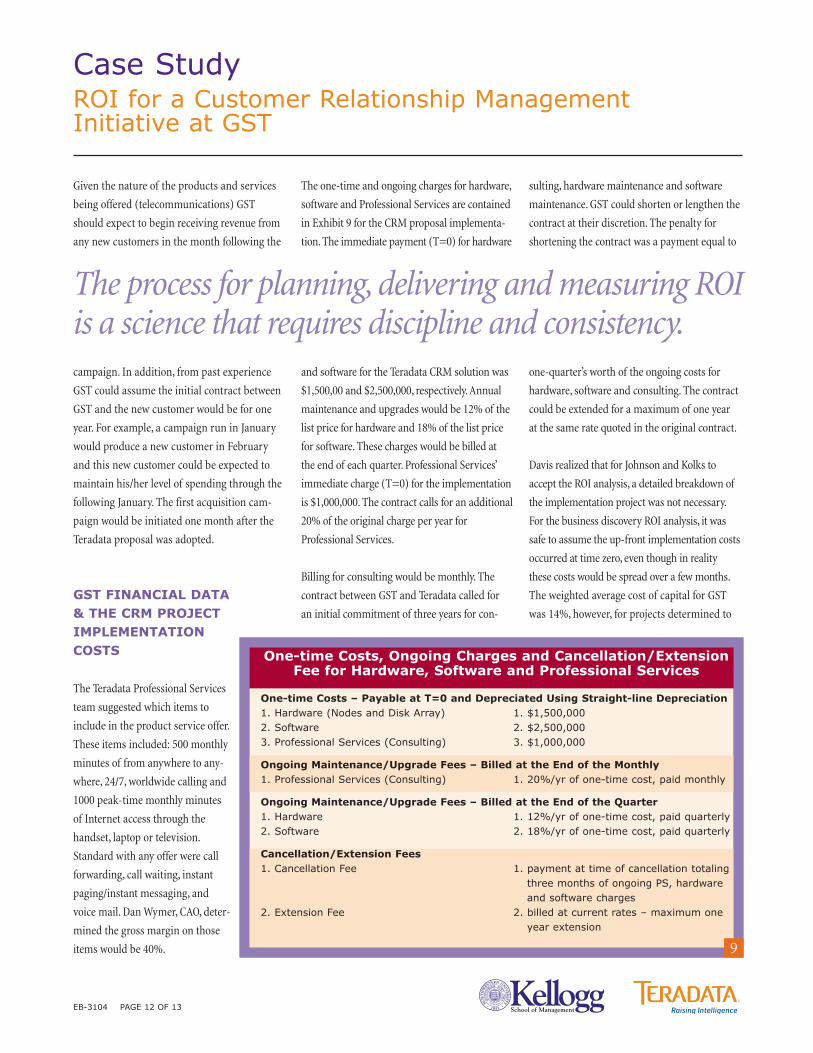

The one-time and ongoing charges for hardware,

software and Professional Services are contained

in Exhibit 9 for the CRM proposal implementa-

tion. The immediate payment (T=0) for hardware

and software for the Teradata CRM solution was

$1,500,00 and $2,500,000, respectively.Annual

maintenance and upgrades would be 12% of the

list price for hardware and 18% of the list price

for software. These charges would be billed at

the end of each quarter. Professional Services’

immediate charge (T=0) for the implementation

is $1,000,000. The contract calls for an additional

20% of the original charge per year for

Professional Services.

Billing for consulting would be monthly. The

contract between GST and Teradata called for

an initial commitment of three years for con-

sulting, hardware maintenance and software

maintenance. GST could shorten or lengthen the

contract at their discretion. The penalty for

shortening the contract was a payment equal to

one-quarter’s worth of the ongoing costs for

hardware, software and consulting. The contract

could be extended for a maximum of one year

at the same rate quoted in the original contract.

Davis realized that for Johnson and Kolks to

accept the ROI analysis, a detailed breakdown of

the implementation project was not necessary.

For the business discovery ROI analysis, it was

safe to assume the up-front implementation costs

occurred at time zero, even though in reality

these costs would be spread over a few months.

The weighted average cost of capital for GST

was 14%, however, for projects determined to

Case StudyROI for a Customer Relationship ManagementInitiative at GST

EB-3104 PAGE 12 OF 13

One-time Costs, Ongoing Charges and Cancellation/ExtensionFee for Hardware, Software and Professional Services

One-time Costs – Payable at T=0 and Depreciated Using Straight-line Depreciation1. Hardware (Nodes and Disk Array) 1. $1,500,0002. Software 2. $2,500,0003. Professional Services (Consulting) 3. $1,000,000

Ongoing Maintenance/Upgrade Fees – Billed at the End of the Monthly1. Professional Services (Consulting) 1. 20%/yr of one-time cost, paid monthly

Ongoing Maintenance/Upgrade Fees – Billed at the End of the Quarter1. Hardware 1. 12%/yr of one-time cost, paid quarterly2. Software 2. 18%/yr of one-time cost, paid quarterly

Cancellation/Extension Fees1. Cancellation Fee 1. payment at time of cancellation totaling

three months of ongoing PS, hardware and software charges

2. Extension Fee 2. billed at current rates – maximum one year extension

9

The process for planning, delivering and measuring ROIis a science that requires discipline and consistency.

© 2003 by Mark Jeffery. No part of this publication may be reproduced, stored in a retrieval system, used in a spreadsheet, or transmitted by any means - electronic, mechanical, photocopying, or otherwise - without the permission of Mark Jeffery. WorldMark is a trademark and Teradata is a registered trademark of Teradata Corporation. Teradata continually improves products as new technologies and components become available. Teradata therefore, reserves the right to change specifications without prior notice. All features, functions and operations described herein may not be marketed in all parts of the world. Consult yourTeradata representative for more information.

© 2002 – 2008 Teradata Corporation Dayton, OH U.S.A. Produced in U.S.A. All rights reserved.

www.teradata.com www.kellogg.nwu.edu

be riskier than average, a 16% required return

was used. For projects determined to be less

risky than average, a 12% return was required.

The appropriate tax rate was 38%.

THE PROFESSIONAL SERVICES TEAM MEETING

Davis convened the Professional Services team

meeting on Thursday morning with a rather

startling announcement:

“Well folks, we have a week. I have committed our

team to present the Business Impact Assessment

to Mark Johnson and Erica Kolks next Thursday

at 11AM ... I know we will be ready. We’ll be

ready or we’ll lose the opportunity!”

After a brief pause to make eye contact with

the team, he continued:

“And by ready, I mean I expect our analysis to

be thorough. We should be answering Mark

Johnson’s questions long before he has

had a chance to even think them up.

The business discovery process has been

completed. You have the results in front of you.

Now all that is left is to resolve the remaining

issues, calculate the ROI, and write the report.”

Davis went on to explain that he would like to

position the proposed acquisition campaign

within the context of an overall CRM solution

strategy that would include other key business

benefits. He wondered aloud to the team:

“Should the financial analysis account for

valuable cross sell/up sell opportunities facilitated

by the investment in the infrastructure for the

proposed acquisition program?”

Davis recognized that this was only one of many

additional benefits that the analytical CRM

investment could enable. Additional benefits

could include better evaluation of GST’s net-

work capacity, fraud detection, improved reten-

tion programs, etc. Davis asked the Teradata

Business Impact Modeling team for their sug-

gestions when evaluating these real options.

A second issue Davis highlighted for the team’s

discussion concerned the leads for the acquisi-

tion campaigns. Developing the profile of an

ideal new customer utilizing current customer

data was fraught with risk. GST would have

access to the demographic data of its existing

customers. Ideally, the data had been screened,

cleaned, and the appropriate information

obtained. This information provided a sense of

the kinds of new customers the firm would

like to attract. However, a big question was:

“Where does GST find the names and addresses

of potential new customers?”

At this point, GST was most likely relying on

the data reliability of a third party supplier of

mailing lists—sophisticated analytics are

worth nothing if the database employed is

incorrect. Davis wanted to know:

“What safe guards should be in place prior to

initiating a targeted campaign? How should this

knowledge of ‘data reliability’ affect GST’s

required return?”

The final issue that needed to be resolved by

the team was the appropriate time period for

the analysis. The team agreed that it would

take several months for the hardware and soft-

ware to be in place so clearly a one-year time

horizon from today was unreasonably short.

They could never expect such a quick payback.

On the other hand, the team also knew that if

the analysis continued far enough into the

future, the mathematics alone would

probably produce an acceptable ROI. Davis

needed his team to make a decision and be

prepared to defend their position in the

meeting on Thursday.

Case StudyROI for a Customer Relationship ManagementInitiative at GST

EB-3104 PAGE 13 OF 13

Davis needed his team to make a decision and be preparedto defend their position in the meeting on Thursday.

![Penalties Proposed under GST - GST panaceagstpanacea.com/.../Penalties-Proposed-under-GST-Regime.pdfOffences & Penalties [Section 66] According to GST law Penalty means under section](https://img.dokumen.tips/doc/110x75/5f0beedd7e708231d432ef1d/penalties-proposed-under-gst-gst-offences-penalties-section-66-according.jpg)