Embed Size (px)

Citation preview

© Copyright 2018. Strictly Private & Confidential. Not For Circulation.

GST UPDATES – REAL ESTATE SECTOR

34th GST Council Mee�ng19 March 2019

2© Copyright 2018. Strictly Private & Confidential. Not For Circulation.

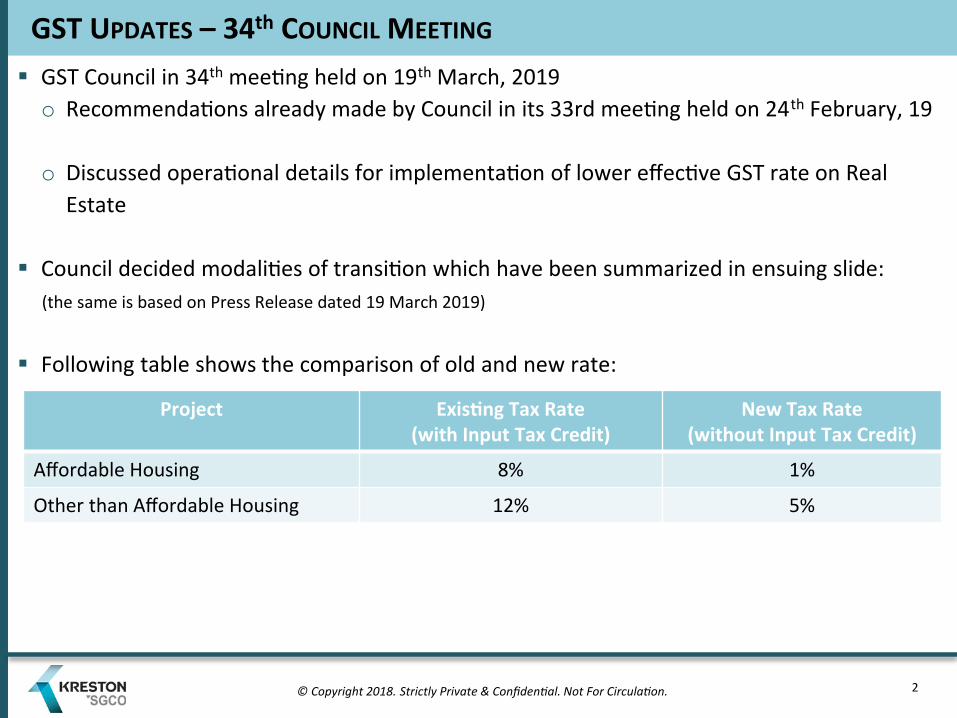

GST Council in 34th mee�ng held on 19th March, 2019 o Recommenda�ons already made by Council in its 33rd mee�ng held on 24th February, 19

o Discussed opera�onal details for implementa�on of lower effec�ve GST rate on Real Estate

Council decided modali�es of transi�on which have been summarized in ensuing slide:(the same is based on Press Release dated 19 March 2019)

Following table shows the comparison of old and new rate:

GST UPDATES – 34th COUNCIL MEETING

Project Exis�ng Tax Rate (with Input Tax Credit)

New Tax Rate (without Input Tax Credit)

Affordable Housing 8% 1%

Other than Affordable Housing 12% 5%

3© Copyright 2018. Strictly Private & Confidential. Not For Circulation.

Affordable and non-affordable means:

Metros Ci�es - Bengaluru, Chennai, Delhi NCR (limited to Delhi, Noida, Greater Noida, Ghaziabad, Gurgaon, Faridabad), Hyderabad,Kolkata and Mumbai (whole of MMR) (as explained in press release dated 24 Feb, 2019)

Ongoing Projects means were construc�on and actual booking both have commenced before 1st April, 2019 and have not beencompleted by 31 March 2019.

New Projects means project were:o Construc�on has commenced prior to 1 April 2019 but Actual Booking has not happened upto to 1 April 2019;o Construc�on has not commenced up to 1 April 2019 but Actual Booking has happened prior to 1 April 2019; oro Both Construc�on and Actual Booking has commenced a�er 31 March, 2019.

AFFORDABLE AND NON – AFFORDABLE HOUSES

Affordable Housing Non Affordable Housing

• Houses as decided by GST Councilo Carpet area of 60 square meter (sqm.) in non-

metros/ 90 sqm in metros; and

o Value of property is upto Rs 45 lakhs

• Houses being constructed in ongoing projectso Exis�ng Central and State housing scheme eligible

for old concessional rate of 8%

• All houses other than affordable houses in ongoing project / New project

• Commercial apartment such shops, offices carpet area of which should not be more than 15% of total carpet area

4© Copyright 2018. Strictly Private & Confidential. Not For Circulation.

Builders of Ongoing projects have One �me op�ons to choose either of the following twoalterna�ves:

o Alterna�ve 1:– Op�on to charge and pay GST at the rate of 12% (8% in case of affordable housing);– Benefit of Input Tax Credit (ITC) is available and can be passed on to the buyer.

o Alterna�ve 2:– Op�on to collect and pay GST at the rate of 5% (1% in case of affordable housing);– Benefit of ITC will not be available to builder for procurements during the project.

Op�on will be available once to be exercised within a prescribed �me frame.o Time frame to be no�fied by GST Councilo If not opted, Alterna�ve 2 i.e. New rates would be applicable

OPTIONS IN RESPECT OF ONGOING PROJECTS

5© Copyright 2018. Strictly Private & Confidential. Not For Circulation.

ITC - TRANSITIONS FOR ONGOING PROJECTS OPTING FOR NEW RATES

Builders / developers of Ongoing Projects op�ng for New Rates of 1 percent for affordablehousing / 5 percent in cases other than affordable housing

o Will have Transi�on to ITC as per method to be prescribed

o Transi�on of ITC based on pro-rata basis based on a formula

– Extrapolate ITC taken basis percentage comple�on of construc�on as on 1 April 2019 – to arrive atITC for en�re project

– ITC eligible to be determined based on percentage of booking of flats and invoicing done �ll 31March 2019

o For mixed project ( Commercial plus residen�al ) ITC would be transited on pro-rata basisof carpet area of commercial por�on to total carpet area of project

6© Copyright 2018. Strictly Private & Confidential. Not For Circulation.

CONDITIONS FOR NEW TAX RATES – NO ITC / REGISTERED DEALERS PURCHASES

New rates of 1 percent on affordable housing / 5 percent in case other than affordablehousing shall be subject to following condi�ons:

1. Input Tax Credit will not be available

2. 80% procurement should be from the registered dealer

– Procurements to include Input, Input Services and Capital Goods but not include TDR /JDA / FSI / long term lease premiums

– On shor�all, tax shall be paid by builder under Reverse Charge Mechanism (RCM)

– RCM payable @ 18 percent (Except Cement - 28 percent and Capital goods - applicablerates)

7© Copyright 2018. Strictly Private & Confidential. Not For Circulation.

EXEMPTION OF TDR/FSI AND LONG TERM LEASE

Supply of TDR / FSI / Long Term Lease premium is exempt

o Provided flats are sold before issuance of Comple�on Cer�ficate and GST is paid on them

Above exemp�on shall be withdrawn if flats sold a�er issues of Comple�on Cer�ficate

o Exemp�on withdrawal limited to 1% (value of affordable houses) and 5% (other thanaffordable houses ) and liability shi�ed to builder on reverse charge mechanism ( RCM)

Date on which such RCM to be paid is been shi�ed to date of issue of comple�on cer�ficate

JDA Cases - Liability of builder to pay tax on construc�on of houses given to land owner isshi�ed to date of comple�on

8© Copyright 2018. Strictly Private & Confidential. Not For Circulation.

OPEN ISSUES…Open Issues that would require more clarity from GST Council are summarized as below:

Meaning – “Comple�on of Project” – needs more clarityo Whether Complex with mul�ple building - Whole Complex to be considered as one / phase wise

Construc�on to be allowed

Meaning – “Construc�on of Started” – needs more clarityo Whether Construc�on started – would also mean and include site clearance, site excava�on and

other ac�vi�es prior to start of actual construc�on

Meaning - “Actual Booking” – needs more clarityo Whether Agreements signed between the par�es / Payment received/ Allotment for the purchase of

the house – which needs to be considered as Actual Booking?

Clarity whether New Rate of 1% for affordable housing is applicable for ongoing projects?

9© Copyright 2018. Strictly Private & Confidential. Not For Circulation.

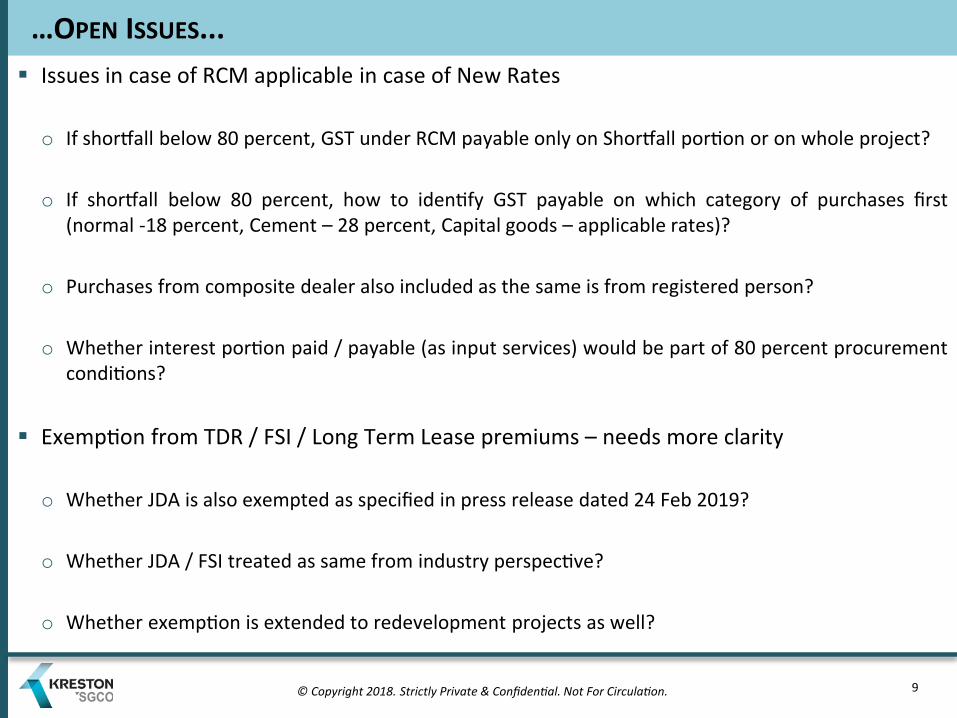

…OPEN ISSUES... Issues in case of RCM applicable in case of New Rates

o If shor�all below 80 percent, GST under RCM payable only on Shor�all por�on or on whole project?

o If shor�all below 80 percent, how to iden�fy GST payable on which category of purchases first(normal -18 percent, Cement – 28 percent, Capital goods – applicable rates)?

o Purchases from composite dealer also included as the same is from registered person?

o Whether interest por�on paid / payable (as input services) would be part of 80 percent procurementcondi�ons?

Exemp�on from TDR / FSI / Long Term Lease premiums – needs more clarity

o Whether JDA is also exempted as specified in press release dated 24 Feb 2019?

o Whether JDA / FSI treated as same from industry perspec�ve?

o Whether exemp�on is extended to redevelopment projects as well?

10© Copyright 2018. Strictly Private & Confidential. Not For Circulation.

…OPEN ISSUES

GST Payable under RCM in case of TDR / FSI / Long Term Lease Premiums

o In case of unsold inventory on date of issue of comple�on cer�ficate - Whether GST is payable on TDR/ FSI / Long Term Lease Premiums value or GST is payable on unsold inventory?

– If GST is payable on TDR / FSI / Long Term Lease Premium – on which value – Full value / propor�onate value ofTDR / FSI / Long Term Lease premium related to such unsold inventory

– If GST is payable on Unsold Inventory – On which Value – Ready Reckoner Rate / Nearest Sale Value / MarketValue?

11© Copyright 2018. Strictly Private & Confidential. Not For Circulation.

Strictly Private & Confidential. Not For Circulation

4-A, 2nd Floor, HDIL Kaledonia Building, Sahar Road, Andheri (East), Mumbai – 400069.

Board No: +91 - 22 – 6625 6363 | Fax: +91 - 22 – 6625 6364 | website: www.sgco.co.in | email: [email protected]

Corporate Office

Note:A reference to CGST Act also provides reference to provision mentioned in SGST Act, IGST Act and UTGST Act. Further, above proposed amendments in act / rules/ rates / clarifications etc. is approved by GST council in its Meeting. However, same would be effective only after issuance of notification in public gazette by the government.

Disclaimer:GST Presentation is based on our understanding of the GST law and regulations prevailing as of the date of this Presentation and is prepared based on information available in public domain. The GST Law is under discussion / evolution and may be subject to changes. Accordingly, i t is important to consult a qualified professional consultant before taking any decision / advice or relying on the presentation. The conclusions reached and views expressed in this presentation are matters of opinion. However, there can be no assurance that the GST Authorities may have a position contrary to our views.

![Untitled-2 [img.staticmb.com]2. Noida Extension is located close to Delhi & Noida is emerging one of the destination for investment in real estate in delhi ncr region. 3. Over the](https://img.dokumen.tips/doc/110x75/5f2164a4e3a28f58e141add3/untitled-2-img-2-noida-extension-is-located-close-to-delhi-noida-is-emerging.jpg)