Embed Size (px)

Citation preview

1

Goods & Service Tax (GST)Impact on Dairy Industry

Discussion DraftBy Bharat Kedia

2

Agenda1 • Present Indirect Tax structure

2 • Changes due to GST

3 • GST Framework

4 • Key impact summary

5 • Next steps

3

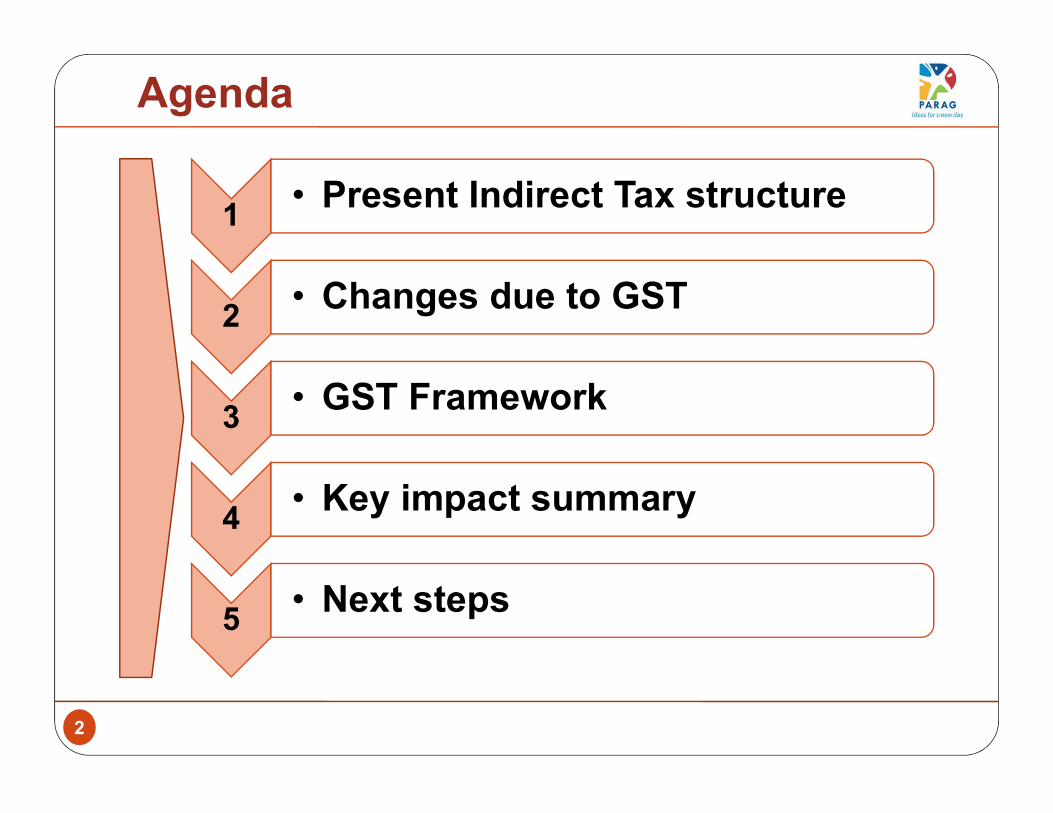

Present Indirect Tax StructureCentral Taxes Parameters Rates

Custom DutyAdditional Duty of CustomsSpecial Additional DutyCentral ExciseService TaxKrishi Kalyan Cess (KKC)Swachh Bharat Cess (SBC)CST

State / Local TaxesVAT

Import / Export of GoodsImport of goods levied in lieu of excise dutyImport of goods levied in lieu of VATManufacturing of goodsProvision of ServicesProvision of ServicesProvision of ServicesInter-state sale of goods

ParametersSale of goods within a state

Entry Tax / Octroi Movement of goods into local territories

10%12.5%4%12.5%14%0.5%0.5%2%Rate5/15%xx%

CostPass Through

4

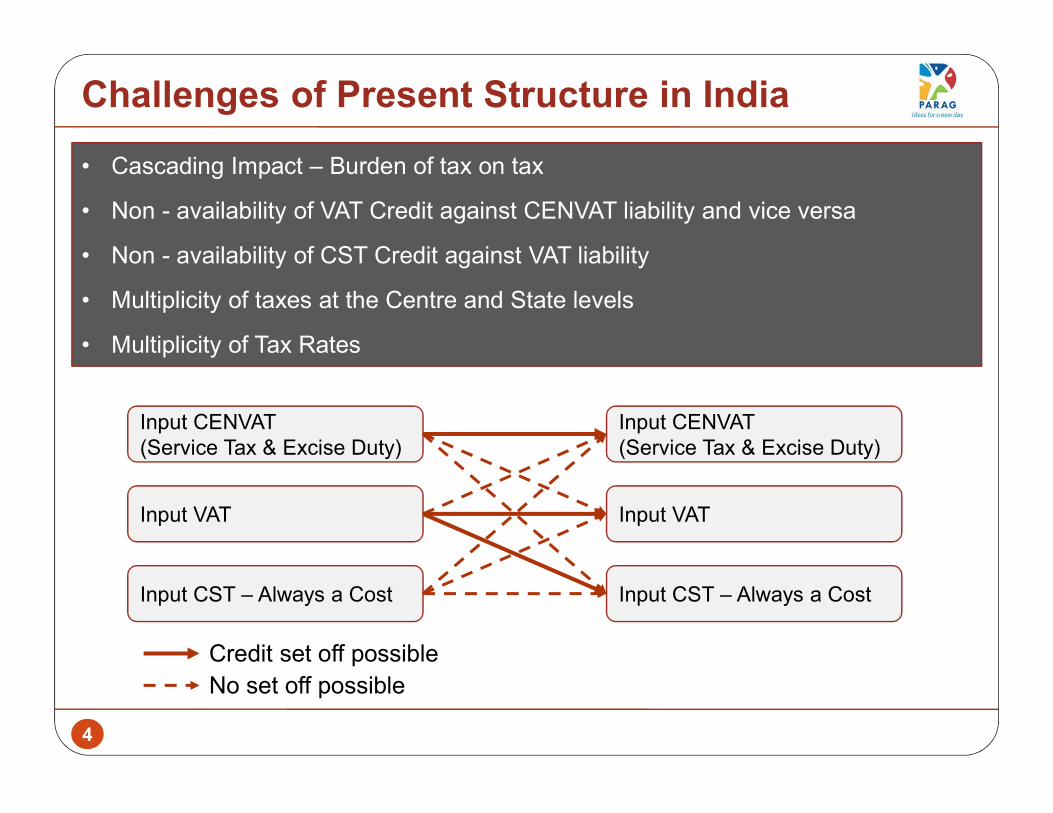

Challenges of Present Structure in India• Cascading Impact – Burden of tax on tax • Non - availability of VAT Credit against CENVAT liability and vice versa• Non - availability of CST Credit against VAT liability• Multiplicity of taxes at the Centre and State levels• Multiplicity of Tax Rates

Input CENVAT(Service Tax & Excise Duty)

Input VAT

Input CST – Always a Cost

Input CENVAT(Service Tax & Excise Duty)

Input VAT

Input CST – Always a CostCredit set off possibleNo set off possible

5

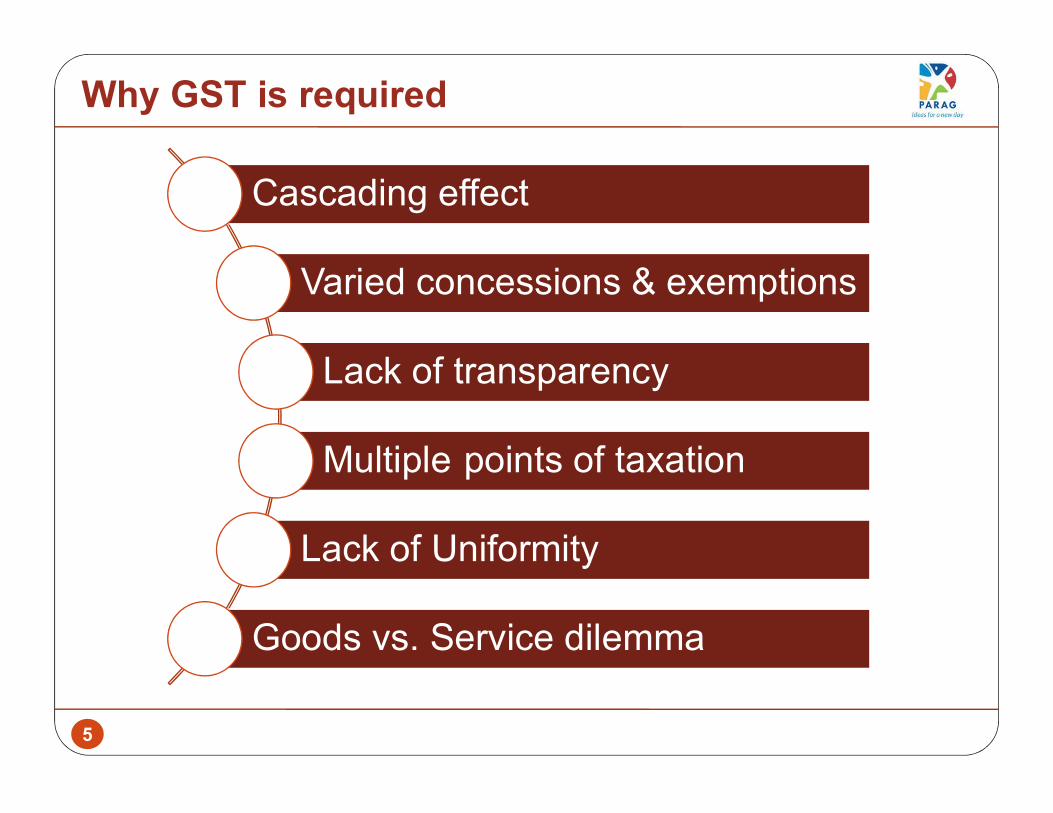

Why GST is requiredCascading effect

Varied concessions & exemptionsLack of transparencyMultiple points of taxation

Lack of UniformityGoods vs. Service dilemma

6

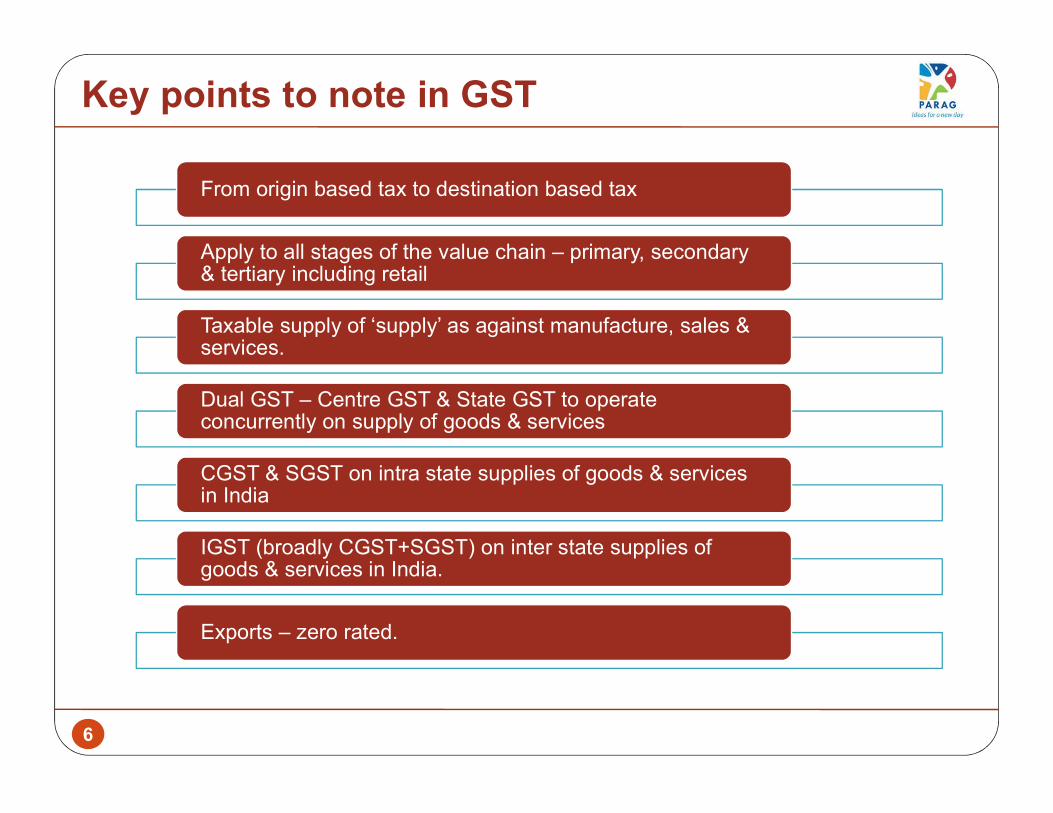

Key points to note in GSTFrom origin based tax to destination based tax

Apply to all stages of the value chain – primary, secondary & tertiary including retailTaxable supply of ‘supply’ as against manufacture, sales & services.Dual GST – Centre GST & State GST to operate concurrently on supply of goods & servicesCGST & SGST on intra state supplies of goods & services in IndiaIGST (broadly CGST+SGST) on inter state supplies of goods & services in India.

Exports – zero rated.

7

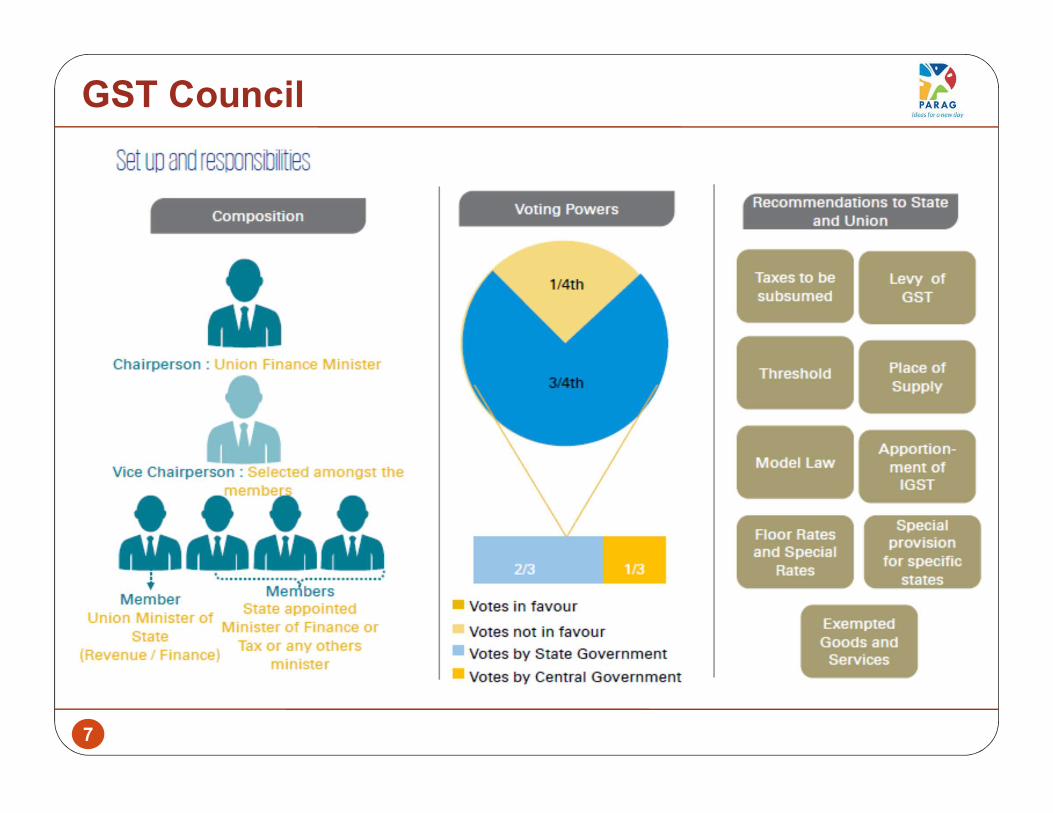

GST Council

8

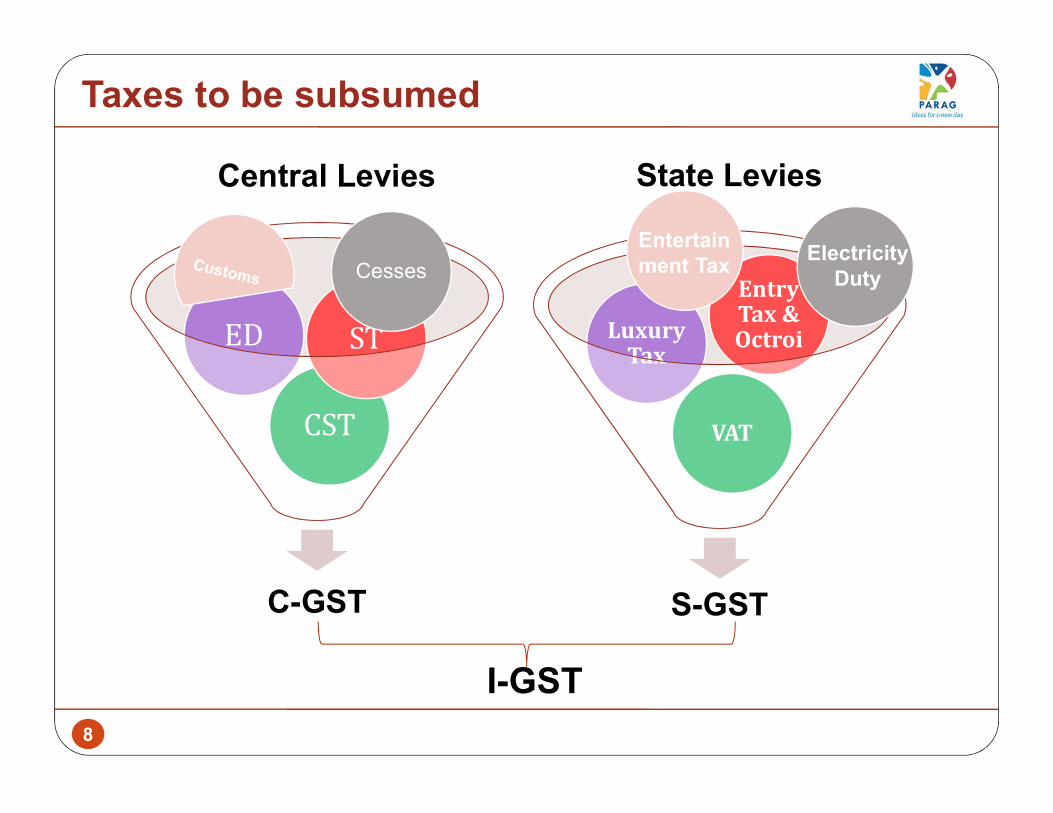

Taxes to be subsumed

C-GST

CSTED ST

Central Levies

S-GST

VAT

Luxury TaxEntry Tax & Octroi

Entertainment Tax Electricity

Duty

State Levies

I-GST

Cesses

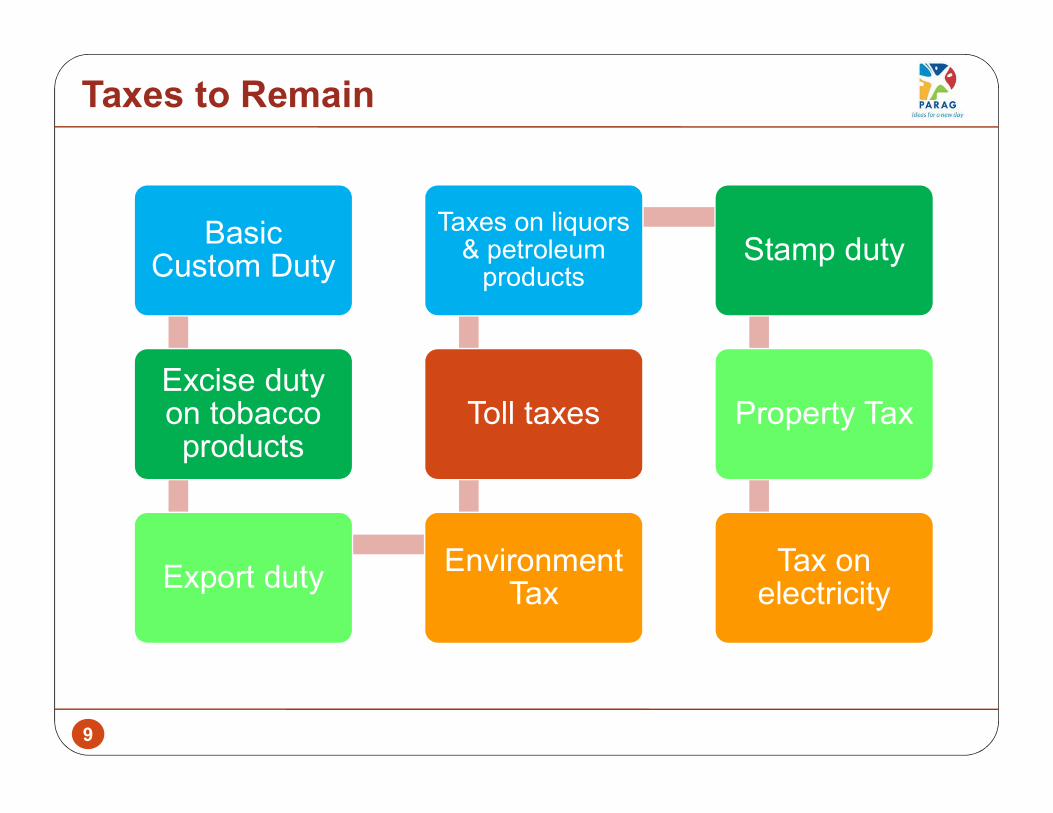

9

Taxes to Remain

Basic Custom Duty

Excise duty on tobacco products

Export duty Environment Tax

Toll taxes

Taxes on liquors & petroleum products Stamp duty

Property Tax

Tax on electricity

10

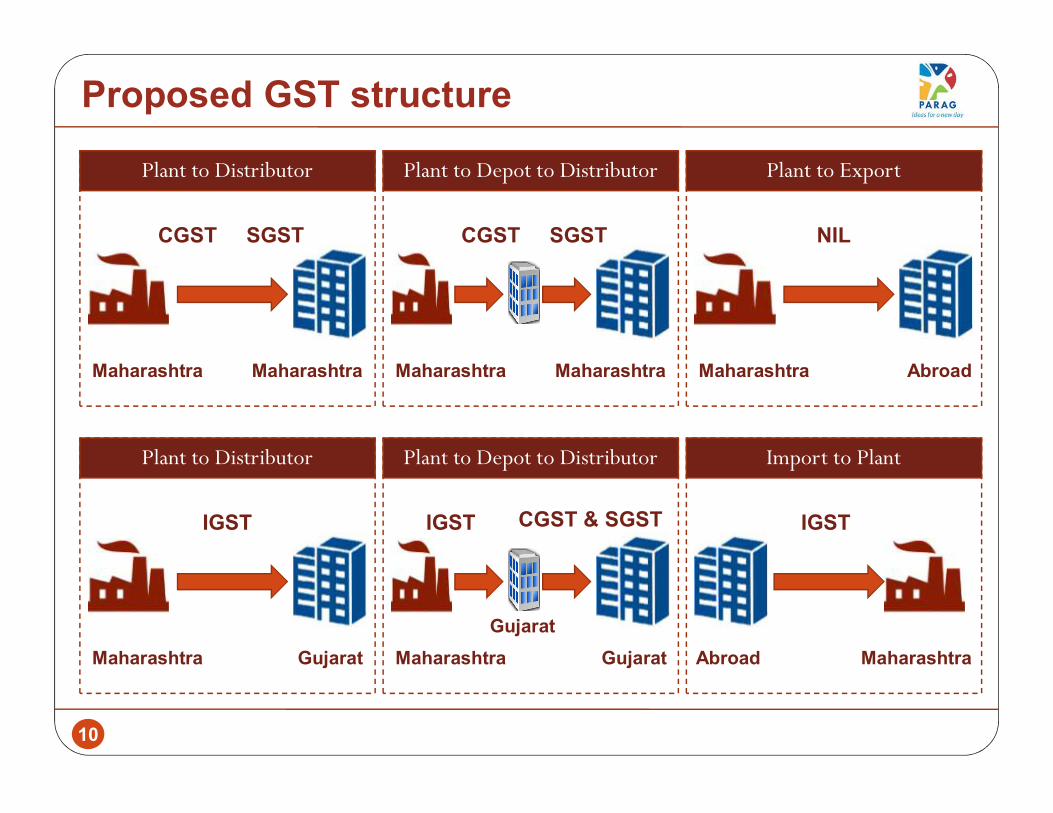

Proposed GST structurePlant to Distributor Plant to Depot to Distributor Plant to Export

Plant to Distributor Plant to Depot to Distributor Import to Plant

Maharashtra Maharashtra

CGST SGST

Maharashtra Gujarat

IGST

Maharashtra Maharashtra

CGST SGST

Maharashtra Gujarat

IGST CGST & SGST

Gujarat

Maharashtra Abroad

NIL

Abroad Maharashtra

IGST

11

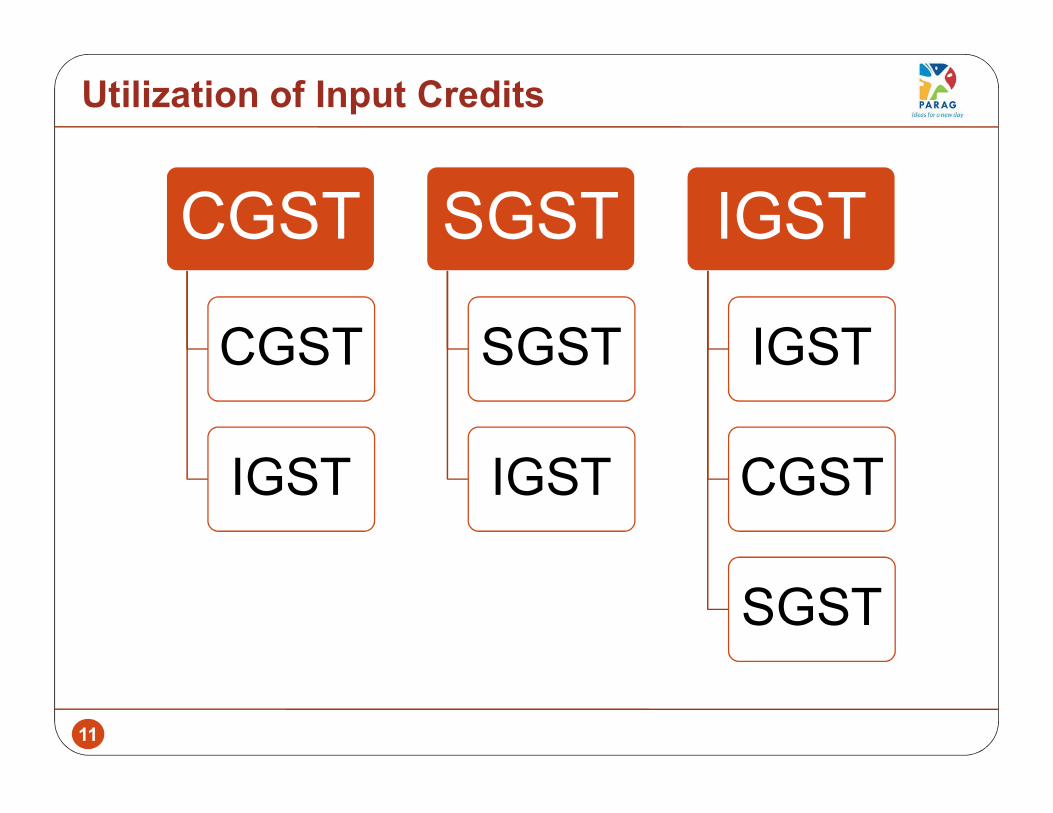

Utilization of Input Credits

CGSTCGSTIGST

SGSTSGSTIGST

IGSTIGSTCGSTSGST

12

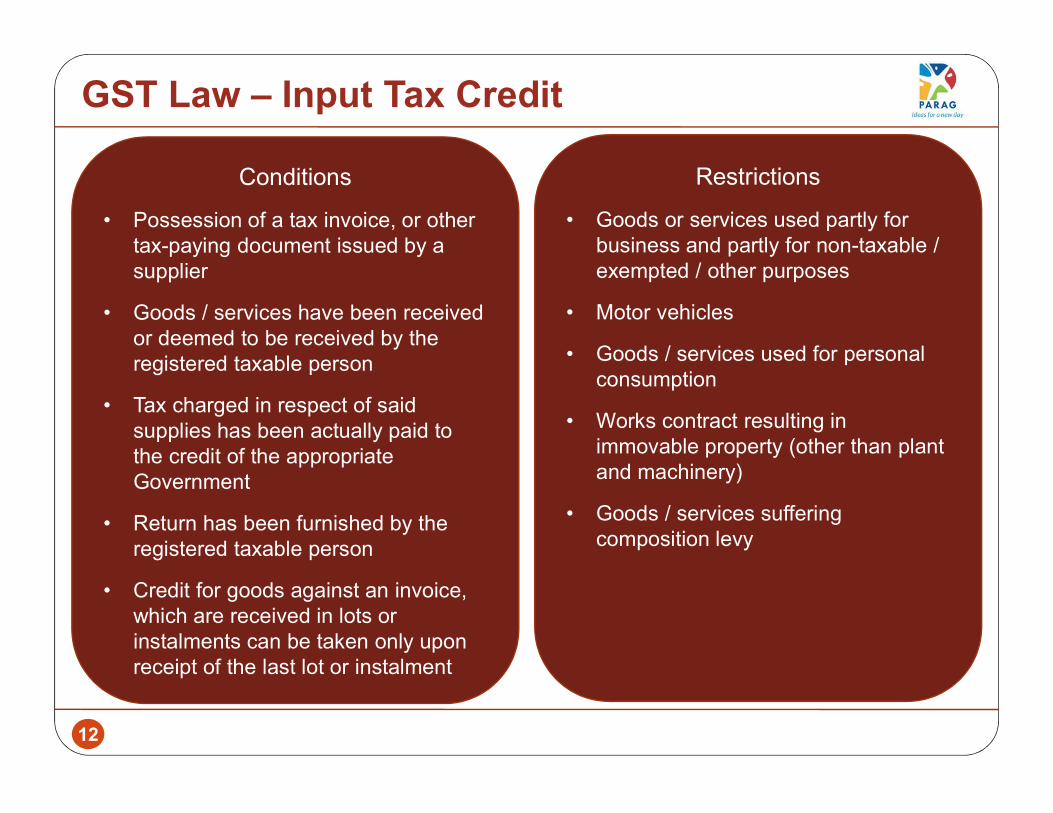

GST Law – Input Tax CreditConditions

• Possession of a tax invoice, or other tax-paying document issued by a supplier

• Goods / services have been received or deemed to be received by the registered taxable person

• Tax charged in respect of said supplies has been actually paid to the credit of the appropriate Government

• Return has been furnished by the registered taxable person

• Credit for goods against an invoice, which are received in lots or instalments can be taken only upon receipt of the last lot or instalment

Restrictions• Goods or services used partly for

business and partly for non-taxable / exempted / other purposes

• Motor vehicles• Goods / services used for personal

consumption• Works contract resulting in

immovable property (other than plant and machinery)

• Goods / services suffering composition levy

13

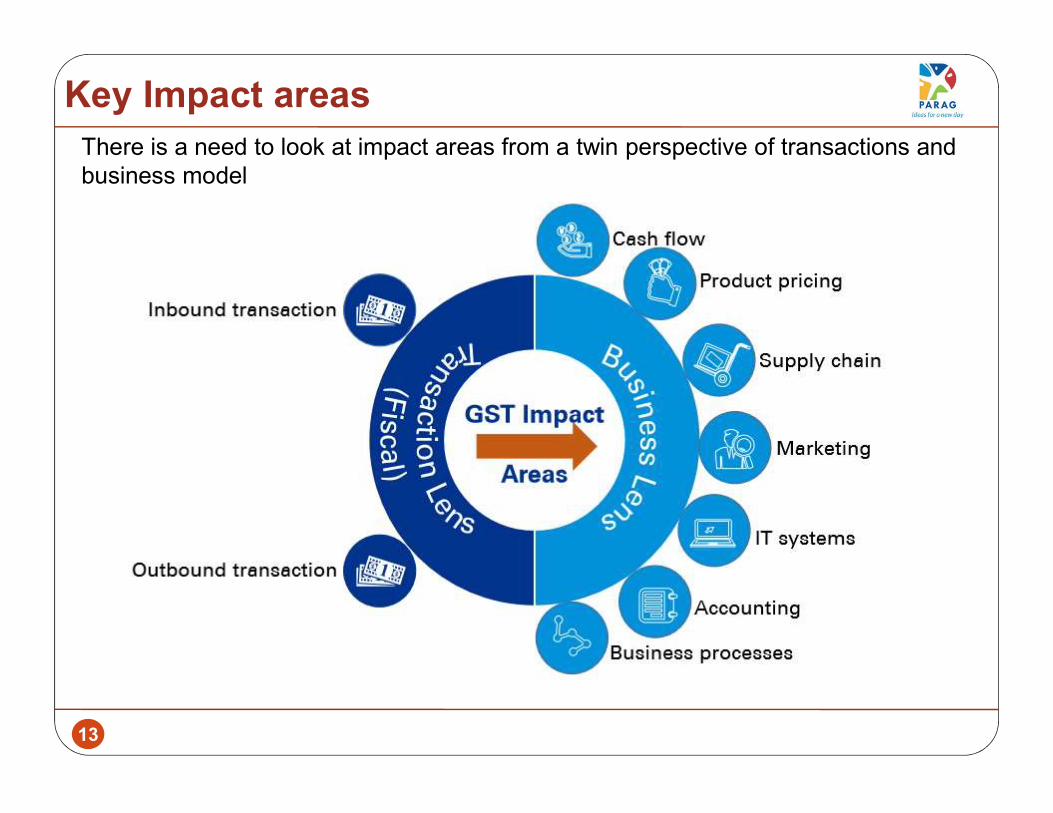

Key Impact areasThere is a need to look at impact areas from a twin perspective of transactions and business model

14

Impact of GST on Industry

IT Applications

Cash Transactions

15

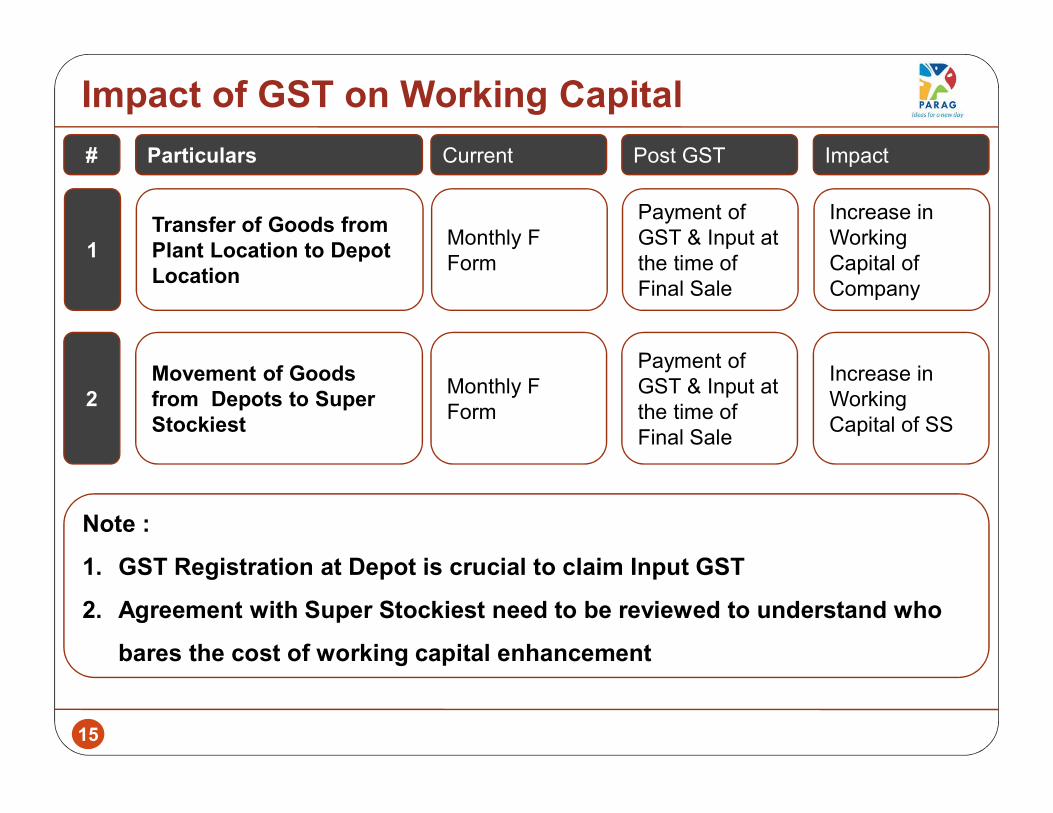

Impact of GST on Working Capital

Transfer of Goods from Plant Location to Depot Location

Monthly F Form

Movement of Goods from Depots to Super Stockiest

Payment of GST & Input at the time of Final Sale

Increase in Working Capital of Company

Monthly F Form

Payment of GST & Input at the time of Final Sale

Increase in Working Capital of SS

Particulars Current Post GST Impact

1

2

#

Note :1. GST Registration at Depot is crucial to claim Input GST2. Agreement with Super Stockiest need to be reviewed to understand who

bares the cost of working capital enhancement

16

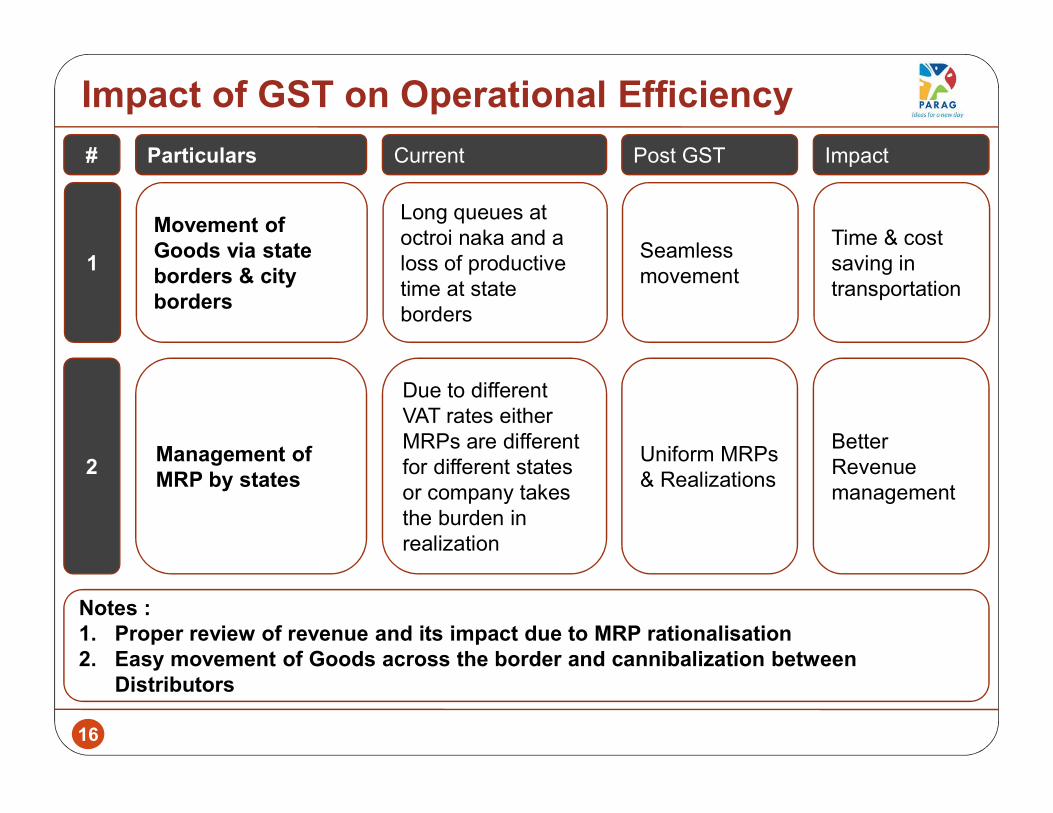

Impact of GST on Operational Efficiency

Movement of Goods via state borders & city borders

Long queues at octroi naka and a loss of productive time at state borders

Management of MRP by states

Seamless movement

Time & cost saving in transportation

Due to different VAT rates either MRPs are different for different states or company takes the burden in realization

Uniform MRPs & Realizations

Better Revenue management

Particulars Current Post GST Impact

1

2

#

Notes :1. Proper review of revenue and its impact due to MRP rationalisation2. Easy movement of Goods across the border and cannibalization between

Distributors

17

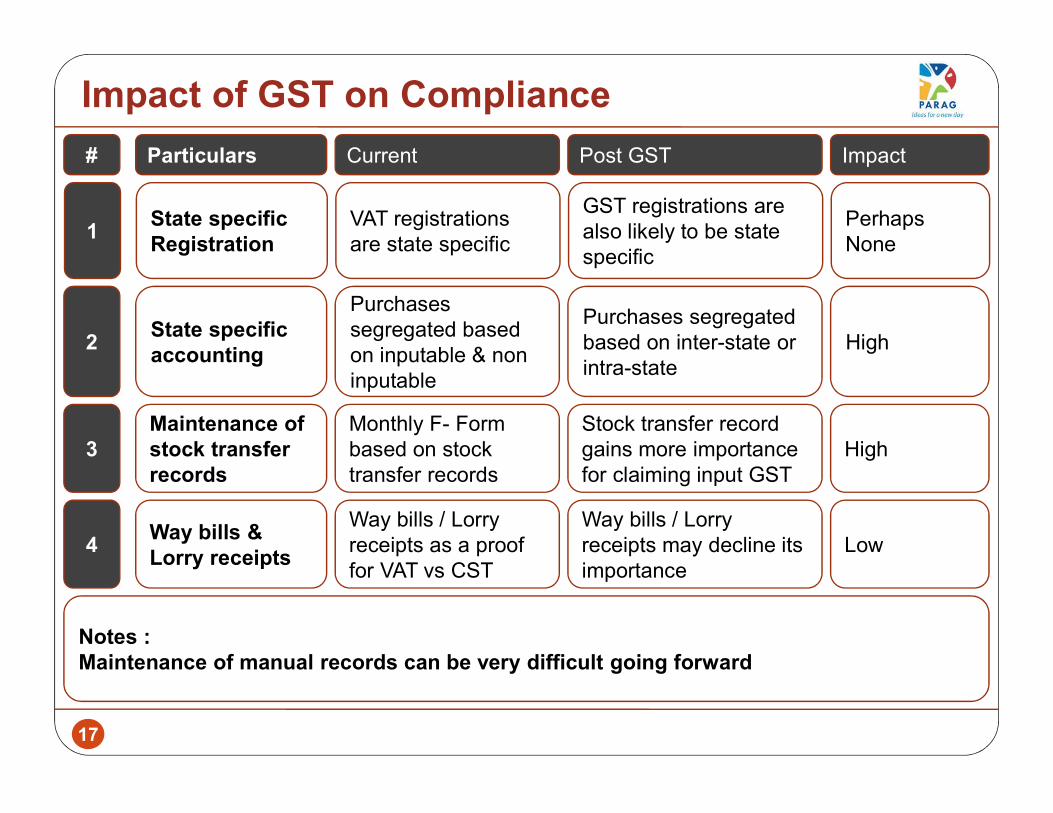

Impact of GST on Compliance

State specific Registration

VAT registrations are state specific

State specific accounting

GST registrations are also likely to be state specific

Perhaps None

Purchases segregated based on inputable & non inputable

Purchases segregated based on inter-state or intra-state

High

Particulars Current Post GST Impact

1

2

#

Notes :Maintenance of manual records can be very difficult going forward

Maintenance of stock transfer records

Monthly F- Form based on stock transfer records

Stock transfer record gains more importance for claiming input GST

High3

Way bills & Lorry receipts

Way bills / Lorry receipts as a proof for VAT vs CST

Way bills / Lorry receipts may decline its importance

Low4

18

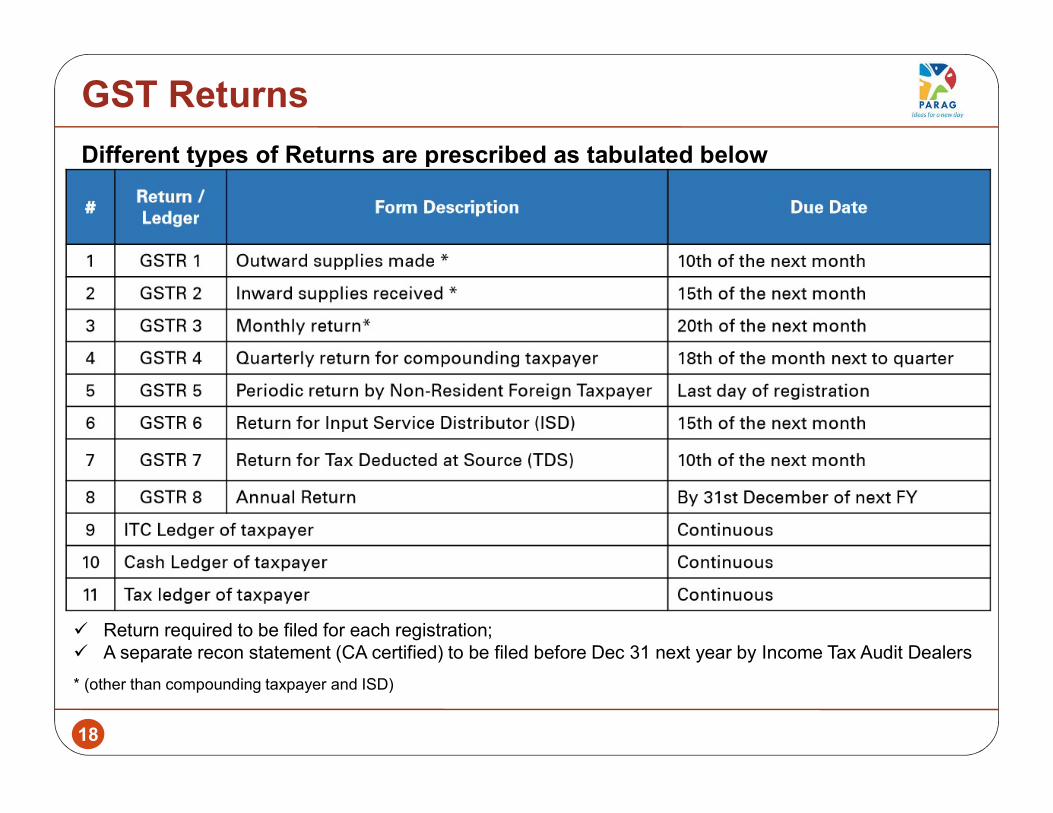

GST ReturnsDifferent types of Returns are prescribed as tabulated below

Return required to be filed for each registration; A separate recon statement (CA certified) to be filed before Dec 31 next year by Income Tax Audit Dealers* (other than compounding taxpayer and ISD)

19

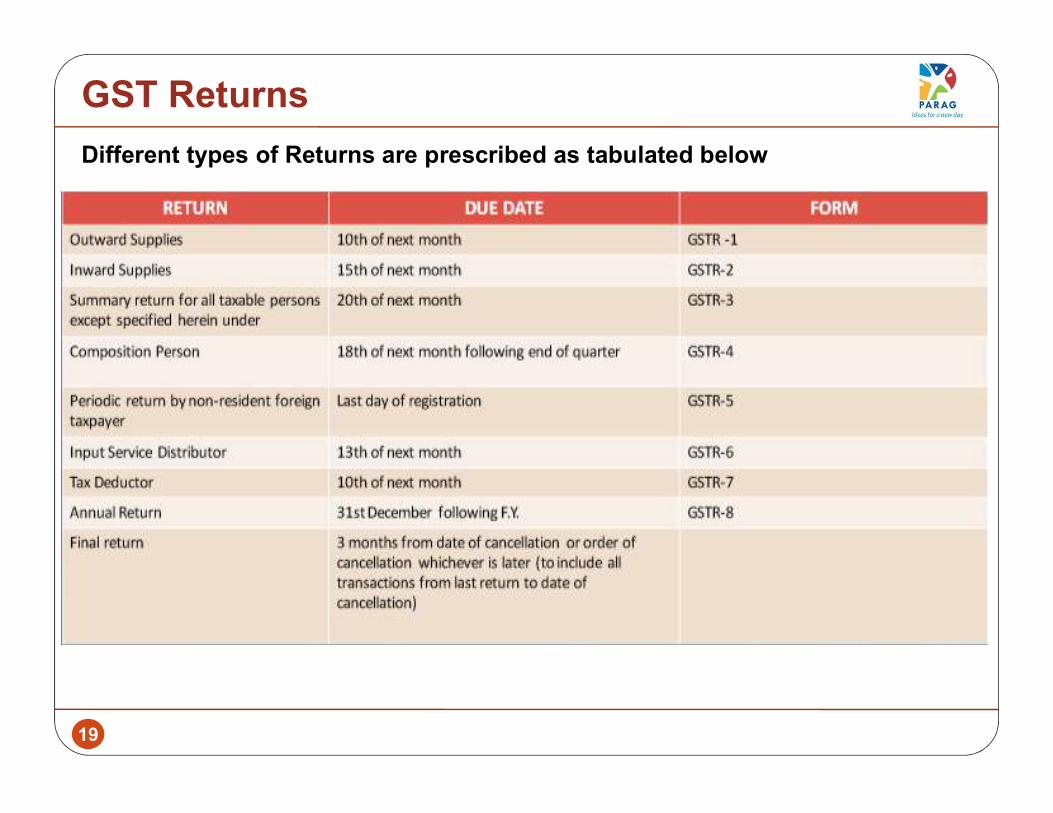

GST ReturnsDifferent types of Returns are prescribed as tabulated below

20

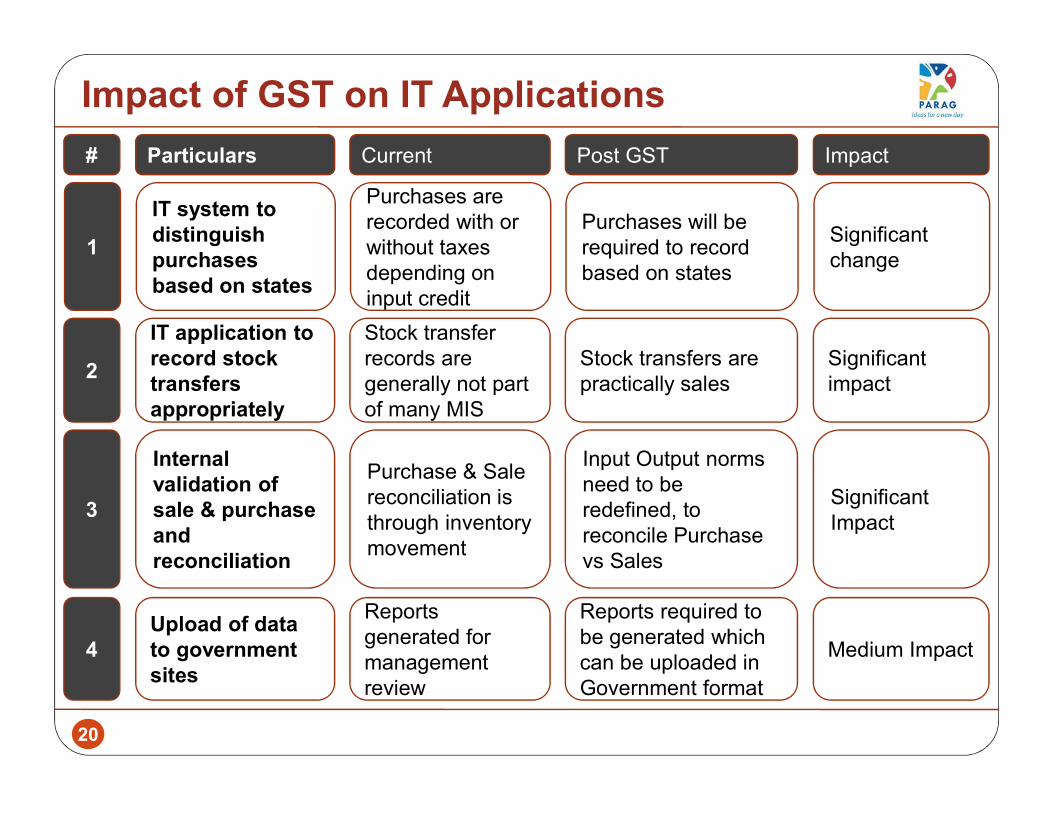

Impact of GST on IT Applications

IT system to distinguish purchases based on states

Purchases are recorded with or without taxes depending on input credit

IT application to record stock transfers appropriately

Purchases will be required to record based on states

Significant change

Stock transfer records are generally not part of many MIS

Stock transfers are practically sales

Significant impact

Particulars Current Post GST Impact

1

2

#

Internal validation of sale & purchase and reconciliation

Purchase & Sale reconciliation is through inventory movement

Input Output norms need to be redefined, to reconcile Purchase vs Sales

Significant Impact3

Upload of data to government sites

Reports generated for management review

Reports required to be generated which can be uploaded in Government format

Medium Impact4

21

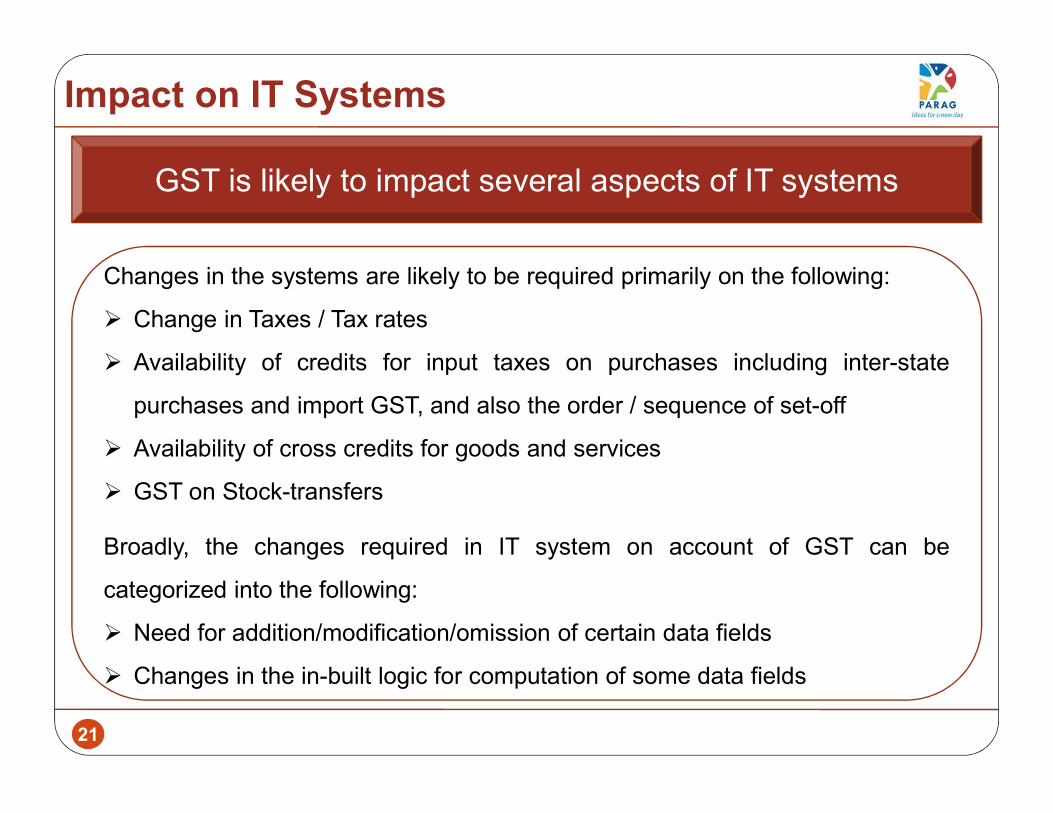

Impact on IT Systems

Changes in the systems are likely to be required primarily on the following: Change in Taxes / Tax rates Availability of credits for input taxes on purchases including inter-state

purchases and import GST, and also the order / sequence of set-off Availability of cross credits for goods and services GST on Stock-transfersBroadly, the changes required in IT system on account of GST can becategorized into the following: Need for addition/modification/omission of certain data fields Changes in the in-built logic for computation of some data fields

GST is likely to impact several aspects of IT systems

22

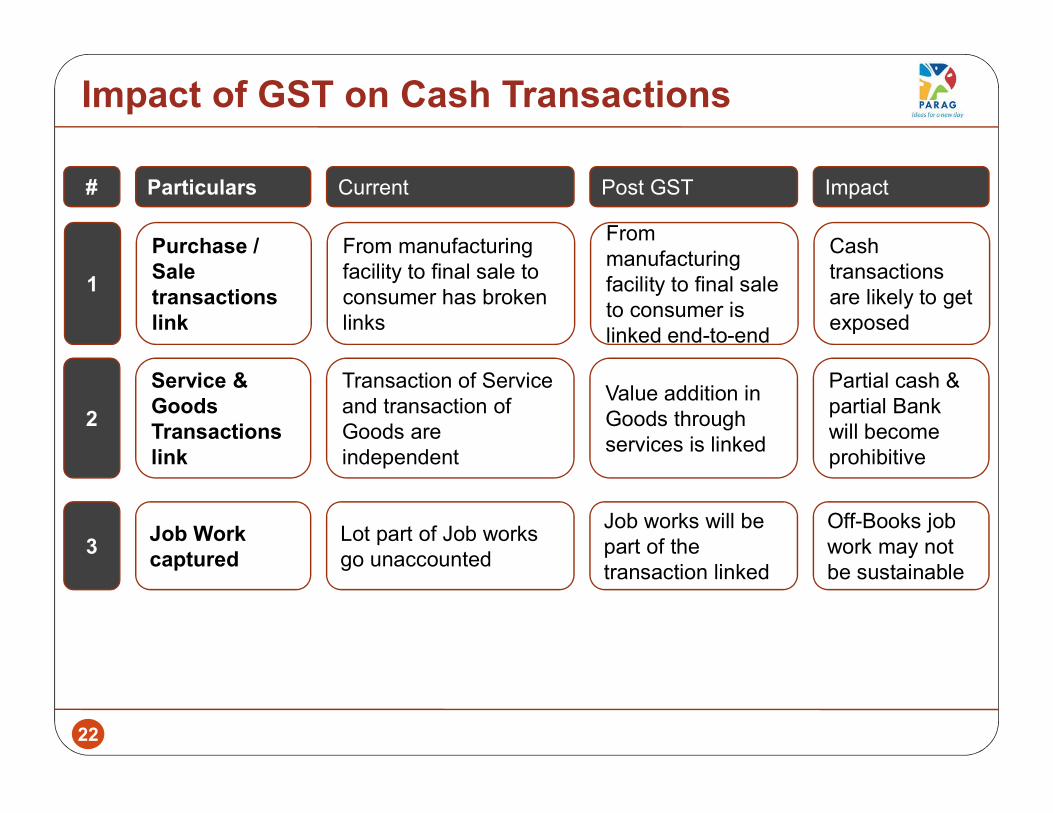

Impact of GST on Cash Transactions

Purchase / Sale transactions link

From manufacturing facility to final sale to consumer has broken links

Service & Goods Transactions link

From manufacturing facility to final sale to consumer is linked end-to-end

Cash transactions are likely to get exposed

Transaction of Service and transaction of Goods are independent

Value addition in Goods through services is linked

Partial cash & partial Bank will become prohibitive

Particulars Current Post GST Impact

1

2

#

Job Work captured

Lot part of Job works go unaccounted

Job works will be part of the transaction linked

Off-Books job work may not be sustainable

3

23

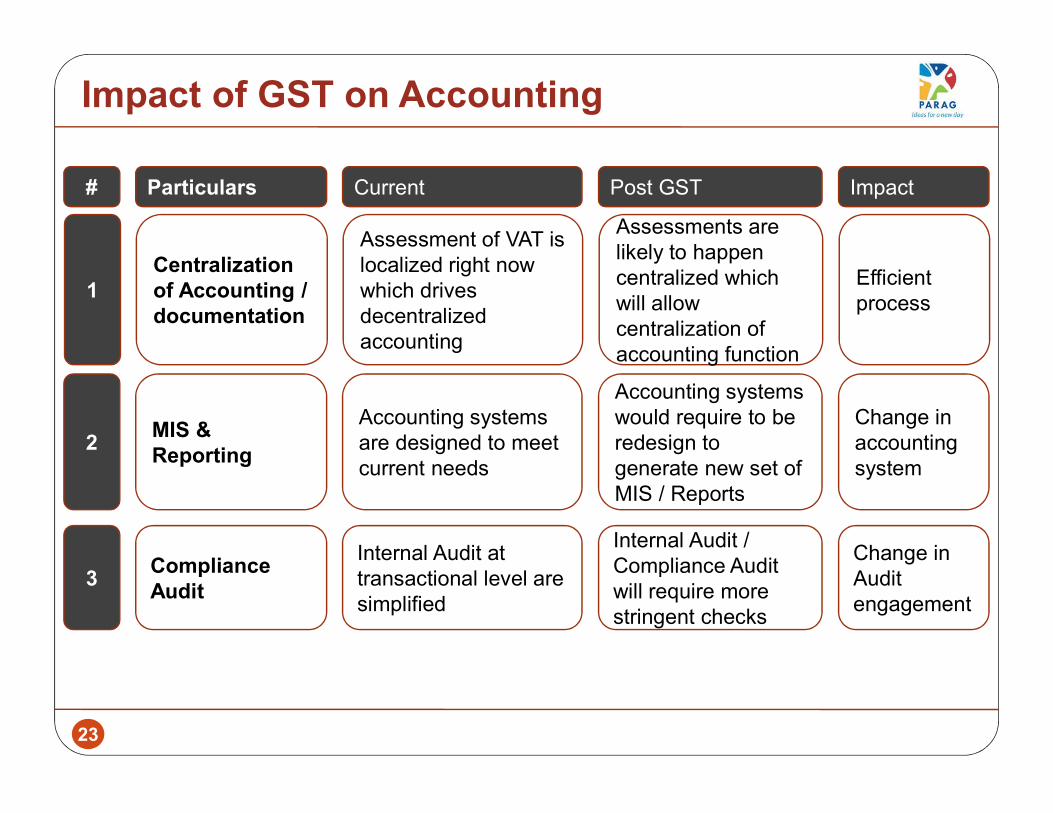

Impact of GST on Accounting

Centralization of Accounting / documentation

Assessment of VAT is localized right now which drives decentralized accounting

MIS & Reporting

Assessments are likely to happen centralized which will allow centralization of accounting function

Efficient process

Accounting systems are designed to meet current needs

Accounting systems would require to be redesign to generate new set of MIS / Reports

Change in accounting system

Particulars Current Post GST Impact

1

2

#

Compliance Audit

Internal Audit at transactional level are simplified

Internal Audit / Compliance Audit will require more stringent checks

Change in Audit engagement

3

24

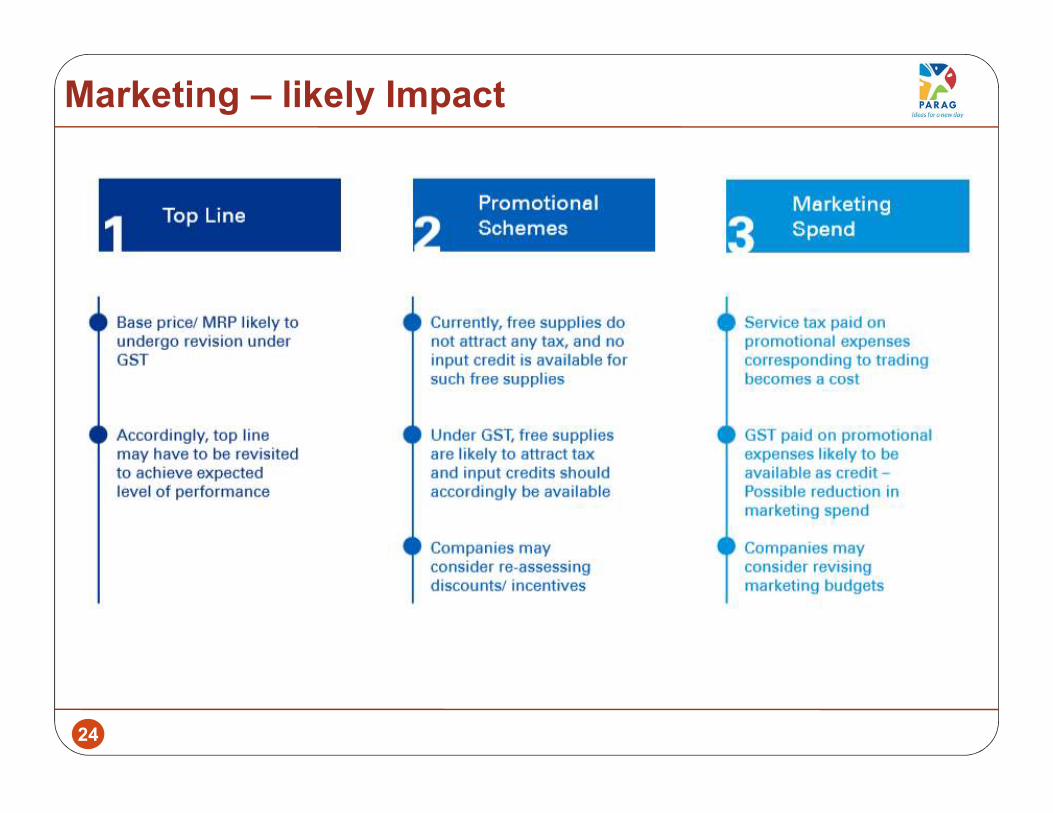

Marketing – likely Impact

25

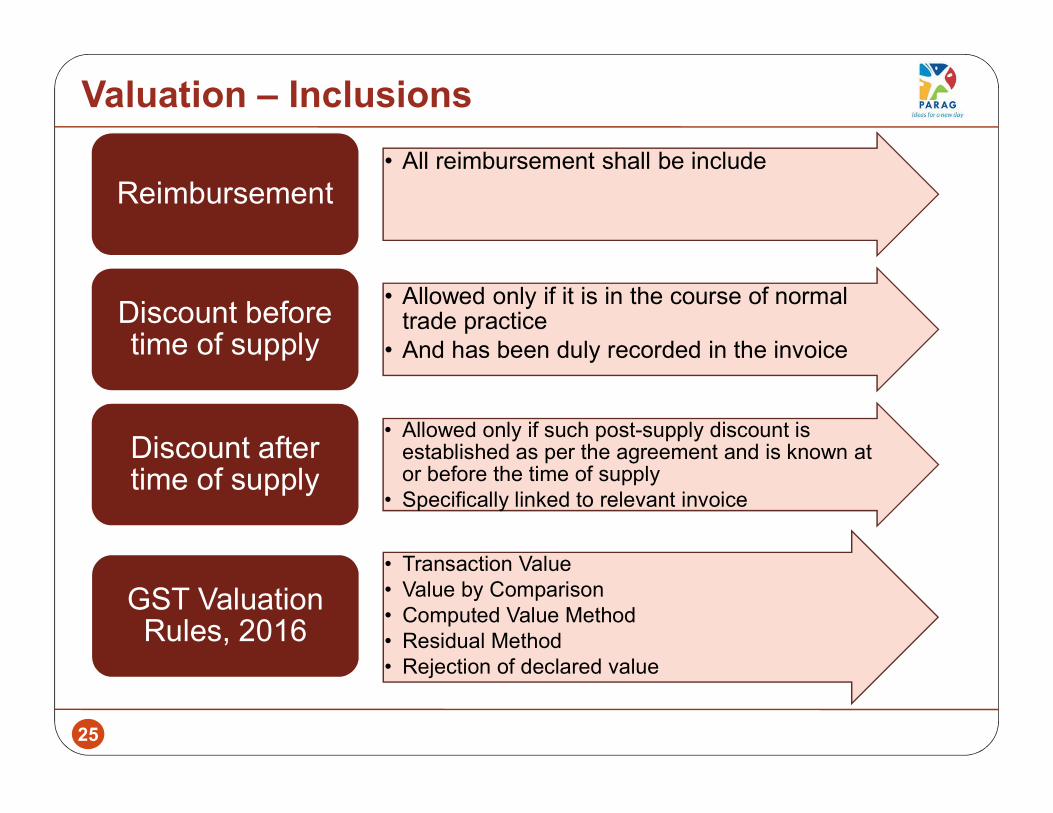

Valuation – Inclusions• All reimbursement shall be includeReimbursement

• Allowed only if it is in the course of normal trade practice• And has been duly recorded in the invoice

Discount before time of supply• Allowed only if such post-supply discount is established as per the agreement and is known at or before the time of supply• Specifically linked to relevant invoice

Discount after time of supply• Transaction Value• Value by Comparison• Computed Value Method• Residual Method• Rejection of declared value

GST Valuation Rules, 2016

26

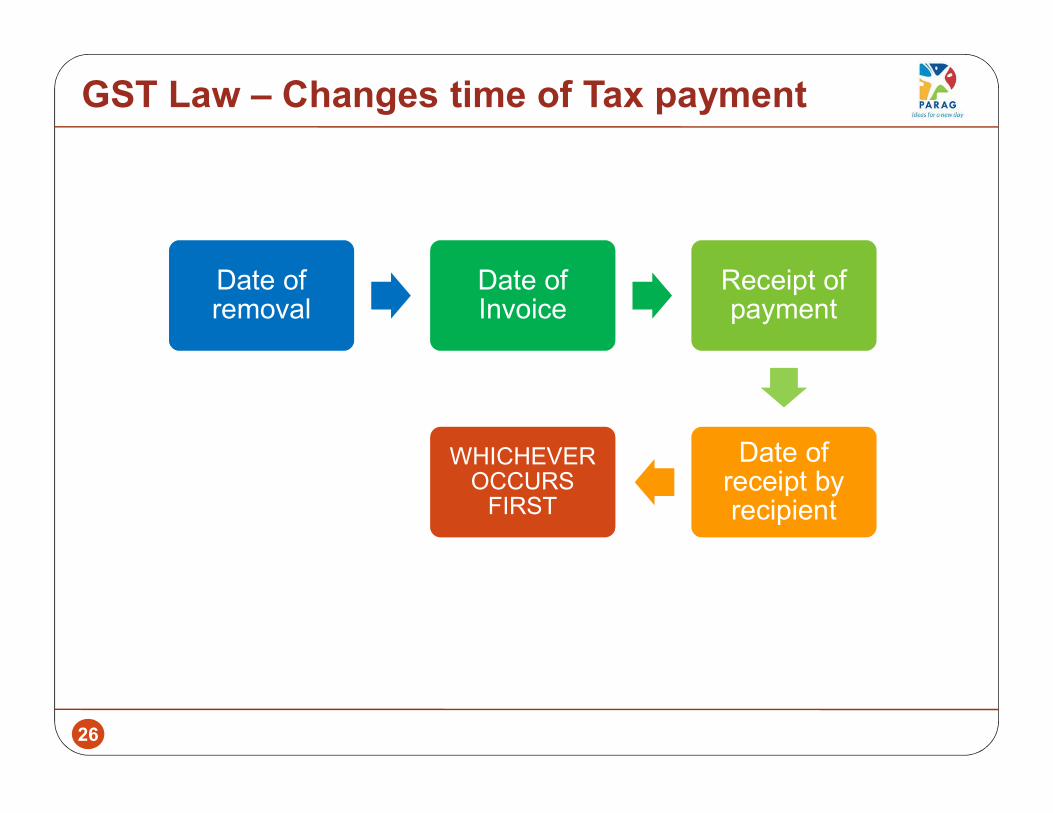

GST Law – Changes time of Tax payment

Date of removal Date of Invoice Receipt of payment

Date of receipt by recipientWHICHEVER OCCURS FIRST

27

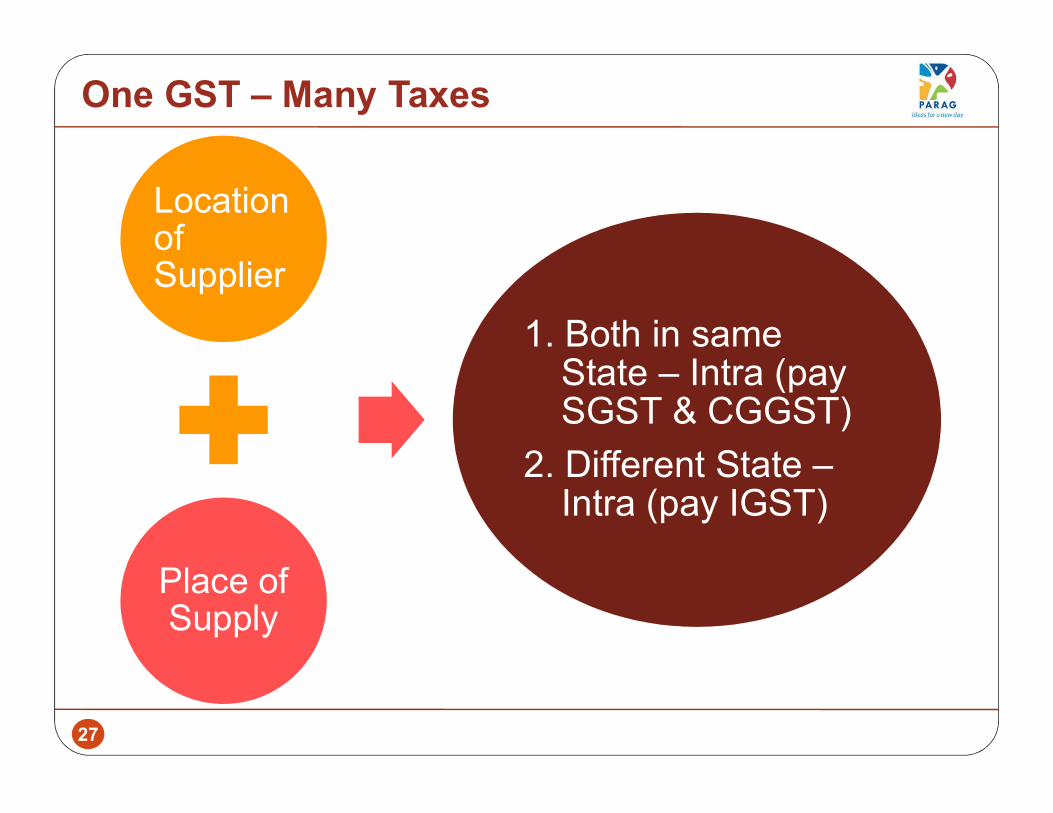

One GST – Many TaxesLocation of Supplier

Place of Supply

1. Both in same State – Intra (pay SGST & CGGST) 2. Different State –Intra (pay IGST)

28

Transitional AspectsOption to forego exemption immediately prior to transition to be evaluated so that credit of stocks lying on transition could be carried forward

Foregoing optional exemptions under excise/VAT

Purchases from manufacturers for higher credits Purchases should be made based on excise documents so that the credit lying on transition date could be claimed.Capturing of service taxinbuilt in stock Service Tax component could be planned to carry forward equivalent to portion in stock.Inventory/Production/Distribution Planning Procurement patterns of customers could see a change during transition period. This needs to be forecasted depending upon the tax incidence current vs GST, the nature of products and B2B/B2C sale.Vendor analysis Procurement cost in case of many products is likely to come down. Impact need to be analysed for price negotiation.Credit on capital goods-representation Representation to be made to government to allow credit on capital goods.Opting 6% ED to be evaluated to claim credit on CG purchased recently.

Credit on stock/capital goods lying with agents to be declared, captured and availed. Stock of input/capital goods lying with agents

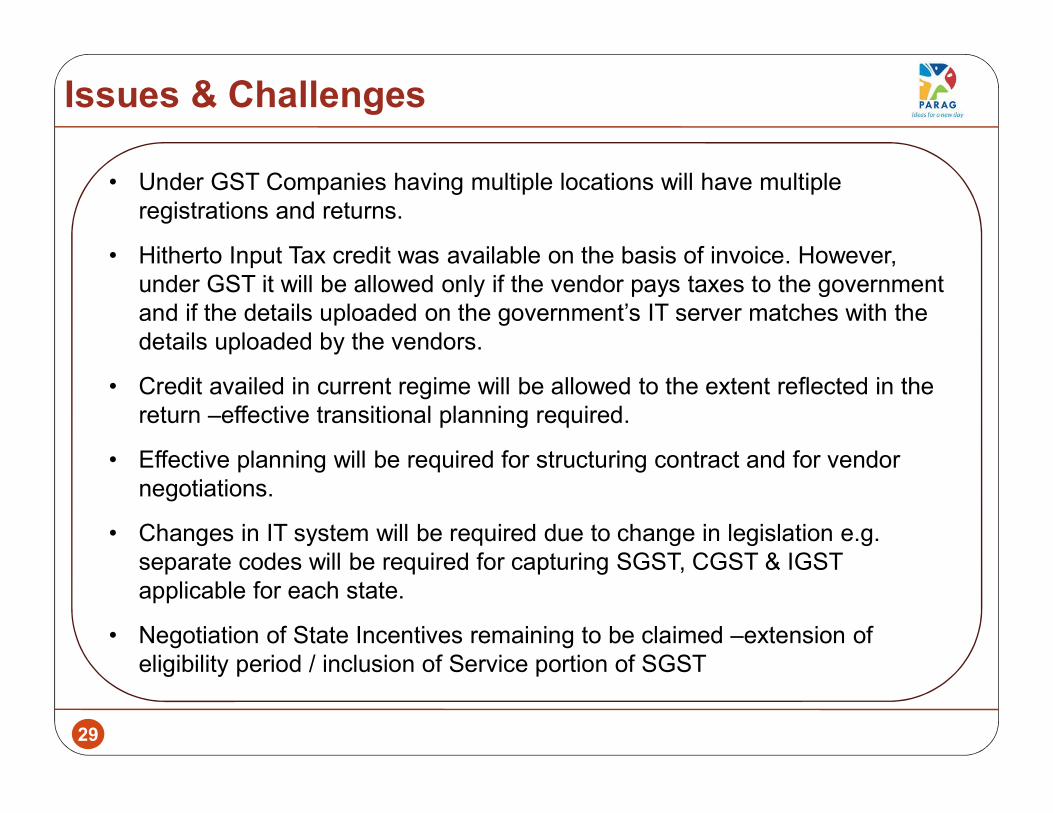

29

Issues & Challenges• Under GST Companies having multiple locations will have multiple

registrations and returns.• Hitherto Input Tax credit was available on the basis of invoice. However,

under GST it will be allowed only if the vendor pays taxes to the government and if the details uploaded on the government’s IT server matches with the details uploaded by the vendors.

• Credit availed in current regime will be allowed to the extent reflected in the return –effective transitional planning required.

• Effective planning will be required for structuring contract and for vendor negotiations.

• Changes in IT system will be required due to change in legislation e.g. separate codes will be required for capturing SGST, CGST & IGST applicable for each state.

• Negotiation of State Incentives remaining to be claimed –extension of eligibility period / inclusion of Service portion of SGST

30

GST Changes provide Challenges & opportunities

How to be Future ready? Opportunities for Employment Opportunities for Practicing CA Ethical Practices - International Trends

31

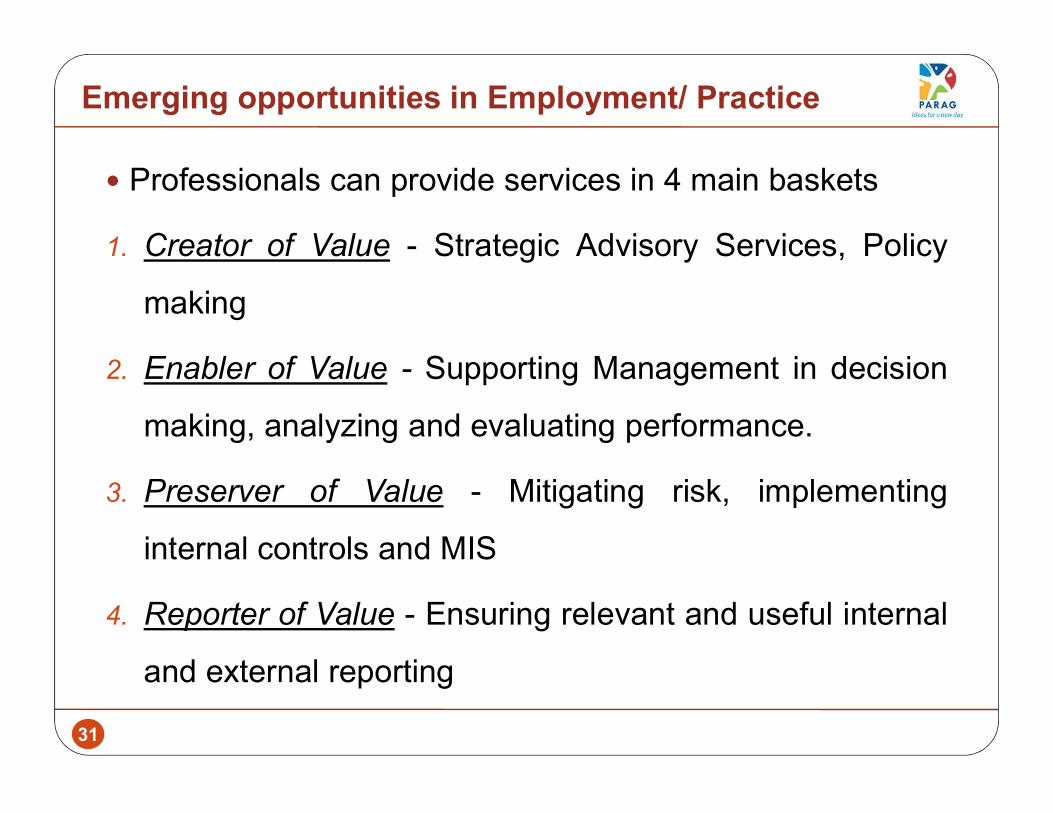

Emerging opportunities in Employment/ Practice Professionals can provide services in 4 main baskets1. Creator of Value - Strategic Advisory Services, Policy

making2. Enabler of Value - Supporting Management in decision

making, analyzing and evaluating performance.3. Preserver of Value - Mitigating risk, implementing

internal controls and MIS4. Reporter of Value - Ensuring relevant and useful internal

and external reporting

32

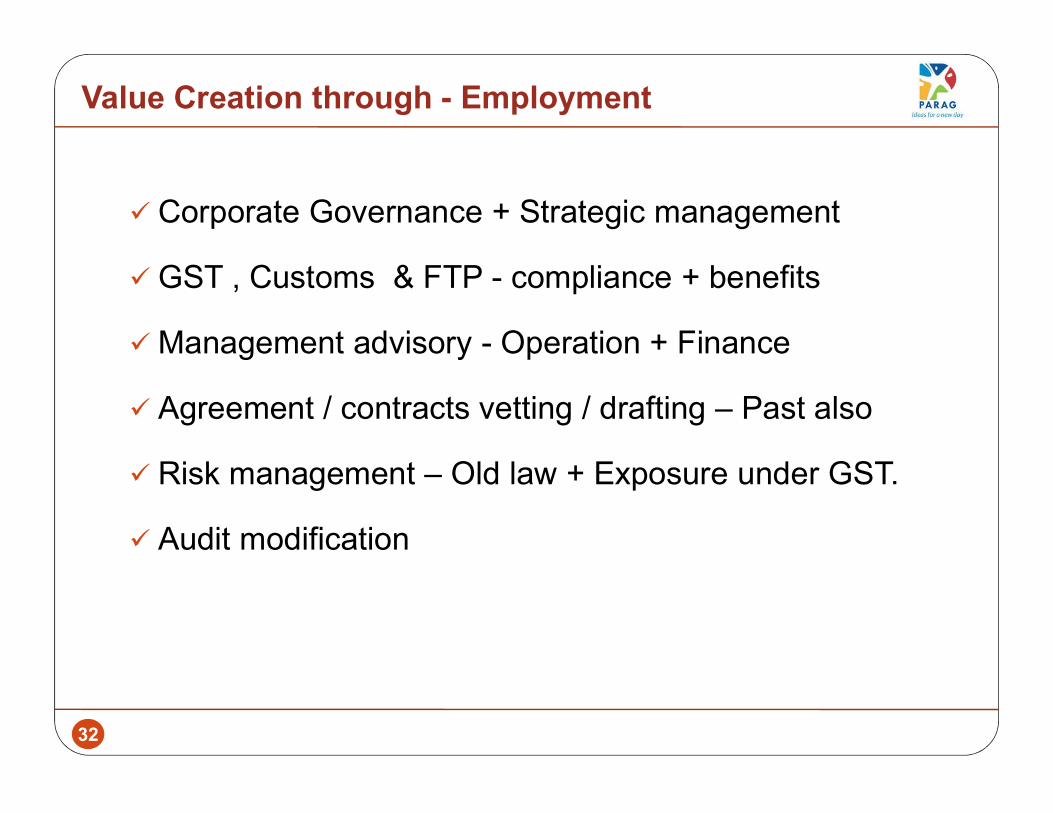

Value Creation through - Employment

Corporate Governance + Strategic managementGST , Customs & FTP - compliance + benefitsManagement advisory - Operation + Finance Agreement / contracts vetting / drafting – Past also Risk management – Old law + Exposure under GST. Audit modification

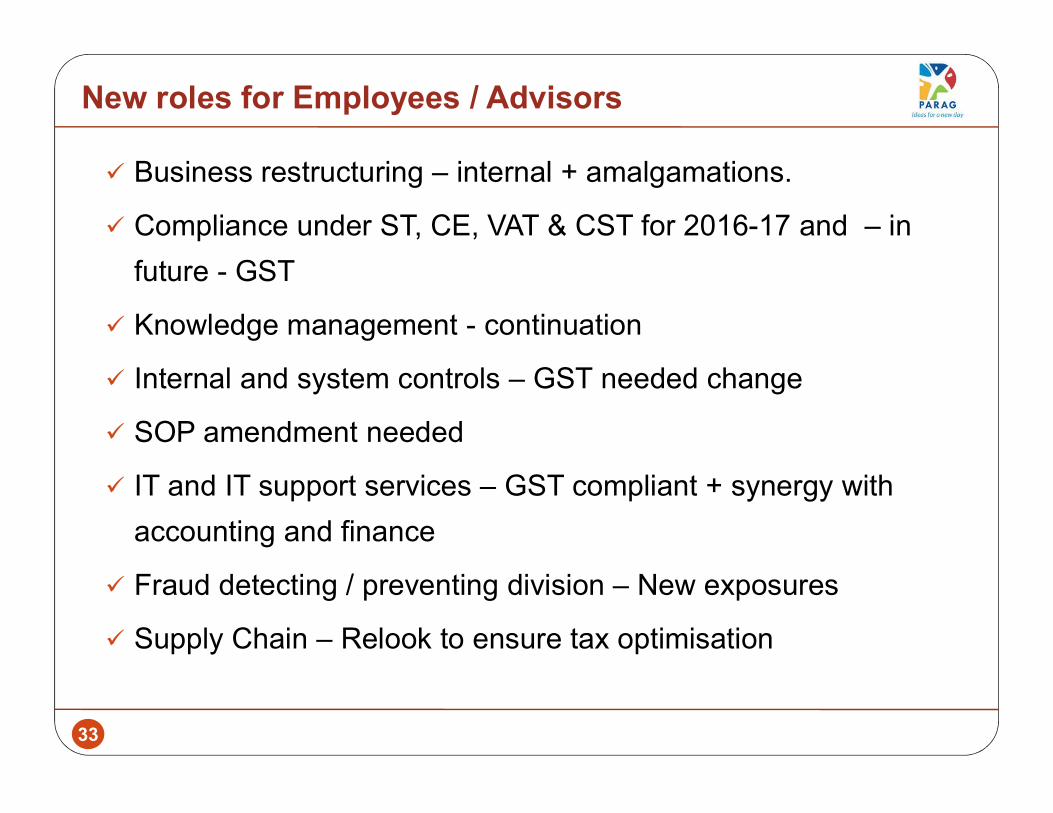

33

New roles for Employees / Advisors Business restructuring – internal + amalgamations. Compliance under ST, CE, VAT & CST for 2016-17 and – in

future - GST Knowledge management - continuation Internal and system controls – GST needed change SOP amendment needed IT and IT support services – GST compliant + synergy with

accounting and finance Fraud detecting / preventing division – New exposures Supply Chain – Relook to ensure tax optimisation

34

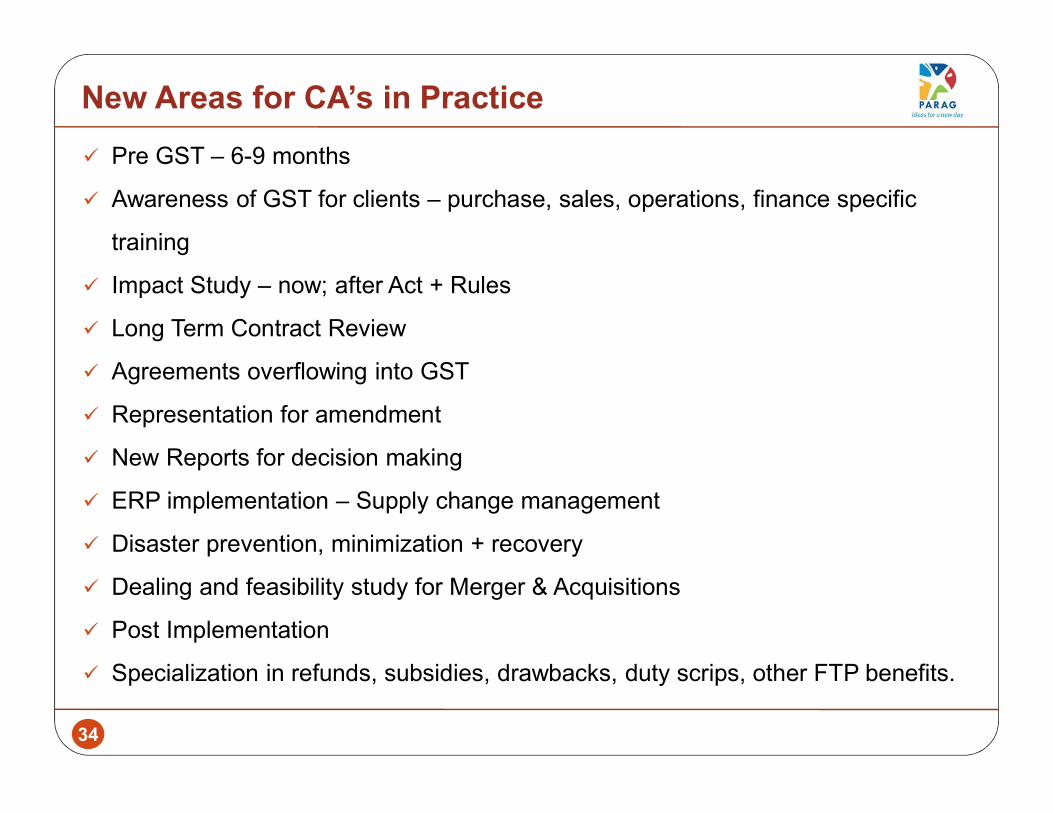

New Areas for CA’s in Practice Pre GST – 6-9 months Awareness of GST for clients – purchase, sales, operations, finance specific

training Impact Study – now; after Act + Rules Long Term Contract Review Agreements overflowing into GST Representation for amendment New Reports for decision making ERP implementation – Supply change management Disaster prevention, minimization + recovery Dealing and feasibility study for Merger & Acquisitions Post Implementation Specialization in refunds, subsidies, drawbacks, duty scrips, other FTP benefits.

35

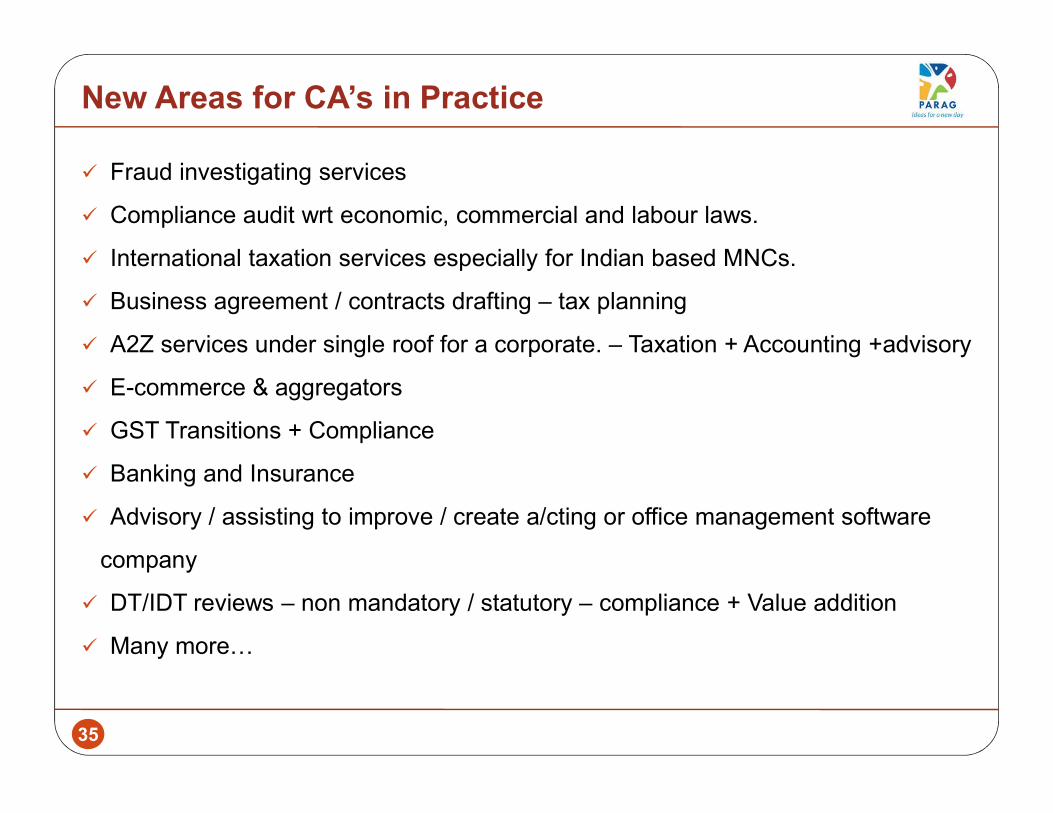

New Areas for CA’s in Practice Fraud investigating services Compliance audit wrt economic, commercial and labour laws. International taxation services especially for Indian based MNCs. Business agreement / contracts drafting – tax planning A2Z services under single roof for a corporate. – Taxation + Accounting +advisory E-commerce & aggregators GST Transitions + Compliance Banking and Insurance Advisory / assisting to improve / create a/cting or office management software

company DT/IDT reviews – non mandatory / statutory – compliance + Value addition Many more…

36

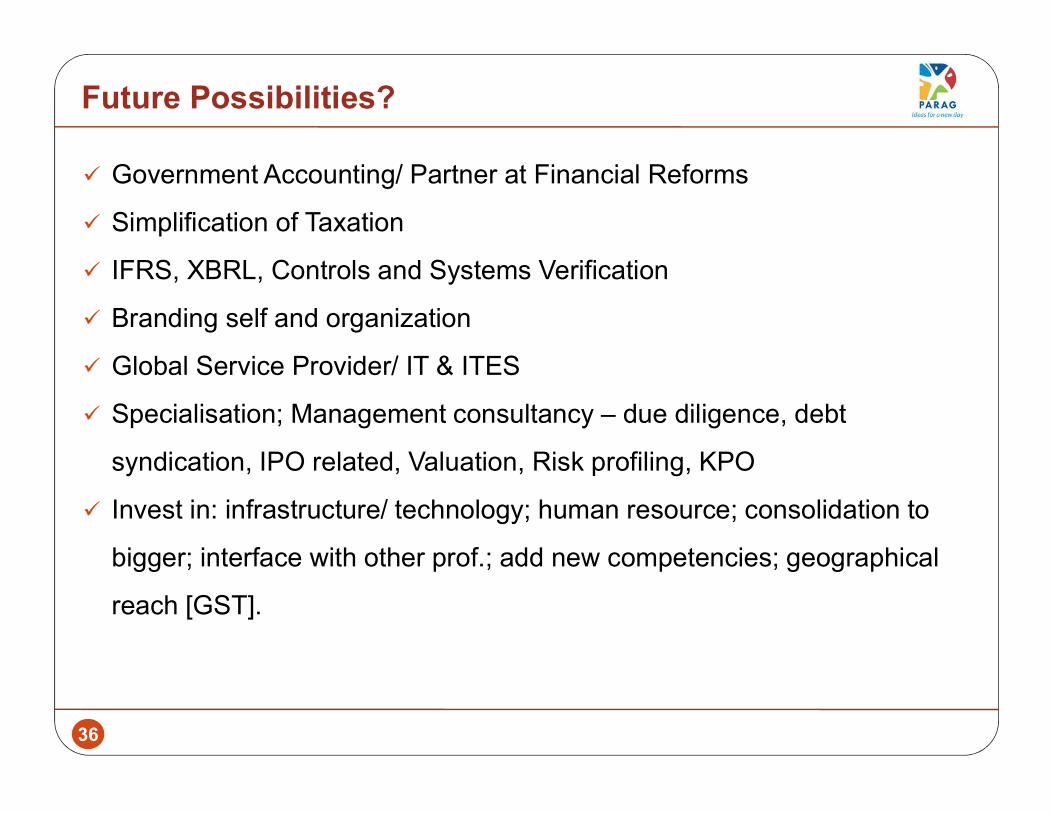

Future Possibilities? Government Accounting/ Partner at Financial Reforms Simplification of Taxation IFRS, XBRL, Controls and Systems Verification Branding self and organization Global Service Provider/ IT & ITES Specialisation; Management consultancy – due diligence, debt

syndication, IPO related, Valuation, Risk profiling, KPO Invest in: infrastructure/ technology; human resource; consolidation to

bigger; interface with other prof.; add new competencies; geographical reach [GST].

37

Am I ready? Where I stand in terms of subject knowledge - in respective field – whether updated -

frequency What is the uniqueness I have that could distinguish me from others? – expertise /

ambition / in depth knowledge in not so common areas Am I keen to learn new things – from experience / mistakes (own / others) / reading /

networking- being social. I may get many new ideas but whether I put sufficient effort to make it happen? –

feasibility study + Research + marketing analysis etc – competing Edge Do I Have goals – specific – 1 year/ 5 years / 10 years – plan + resources + path Self-monitoring – am I better than yesterday? Mile stone analysis – where am I supposed to stand Vs Where am I actually

standing? Benchmarking – Role models – Road map to reach / overtake the best. Life style – punctuality – small aspects make big difference – system / way of life

38

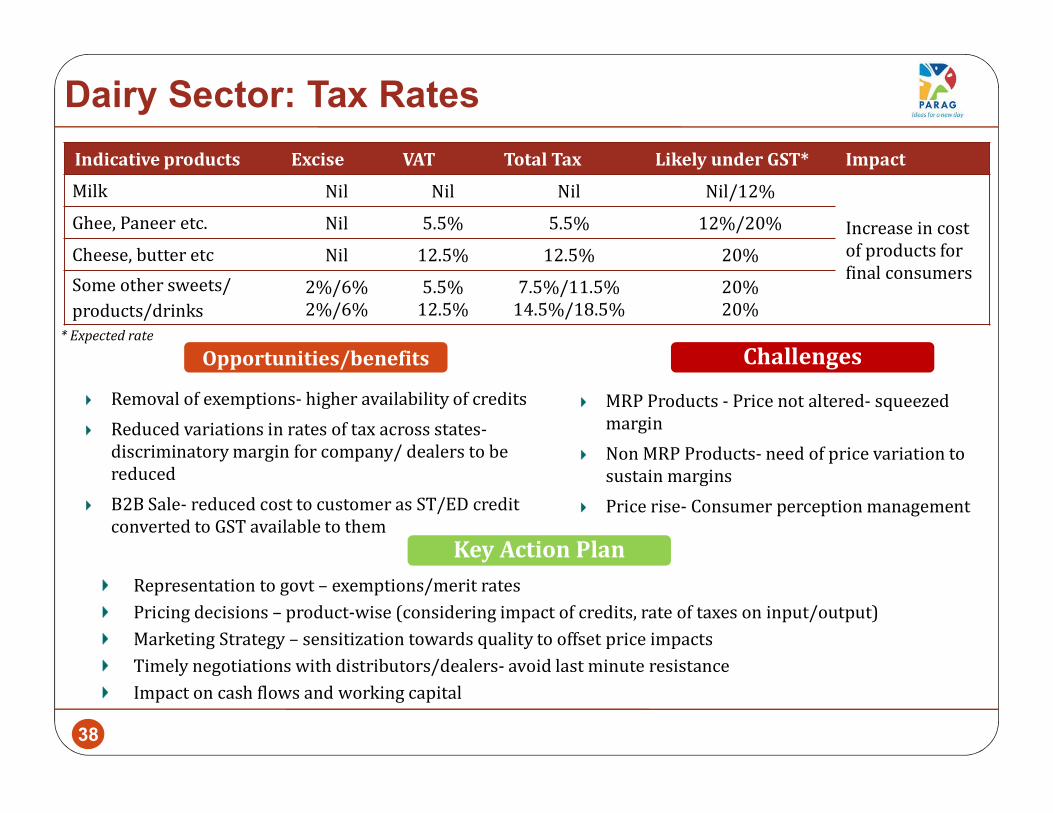

Dairy Sector: Tax RatesIndicative products Excise VAT Total Tax Likely under GST* ImpactMilk Nil Nil Nil Nil/12%

Increase in cost of products for final consumersGhee, Paneer etc. Nil 5.5% 5.5% 12%/20%Cheese, butter etc Nil 12.5% 12.5% 20%Some other sweets/ products/drinks

2%/6%2%/6% 5.5%12.5% 7.5%/11.5%14.5%/18.5% 20%20%

Removal of exemptions- higher availability of creditsReduced variations in rates of tax across states-discriminatory margin for company/ dealers to be reducedB2B Sale- reduced cost to customer as ST/ED credit converted to GST available to them

MRP Products - Price not altered- squeezed margin Non MRP Products- need of price variation to sustain marginsPrice rise- Consumer perception management

Opportunities/benefits

Representation to govt – exemptions/merit ratesPricing decisions – product-wise (considering impact of credits, rate of taxes on input/output)Marketing Strategy – sensitization towards quality to offset price impactsTimely negotiations with distributors/dealers- avoid last minute resistanceImpact on cash flows and working capital

Challenges

Key Action Plan

* Expected rate

39

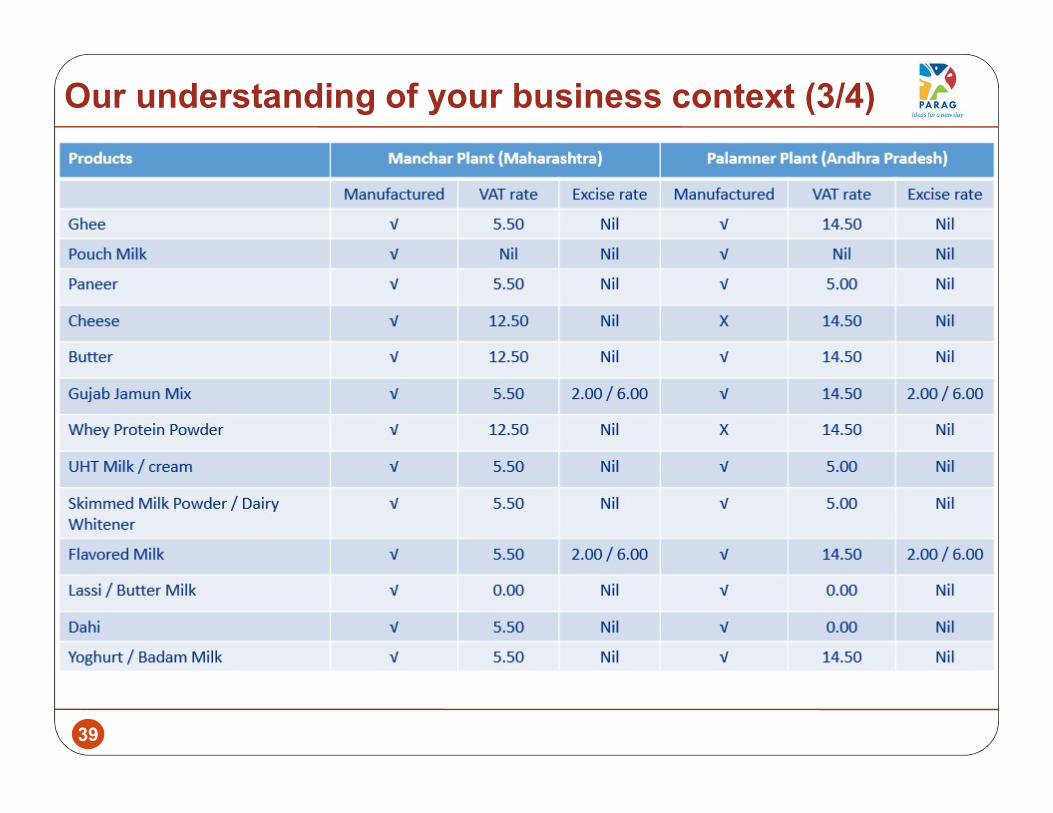

Our understanding of your business context (3/4)

40

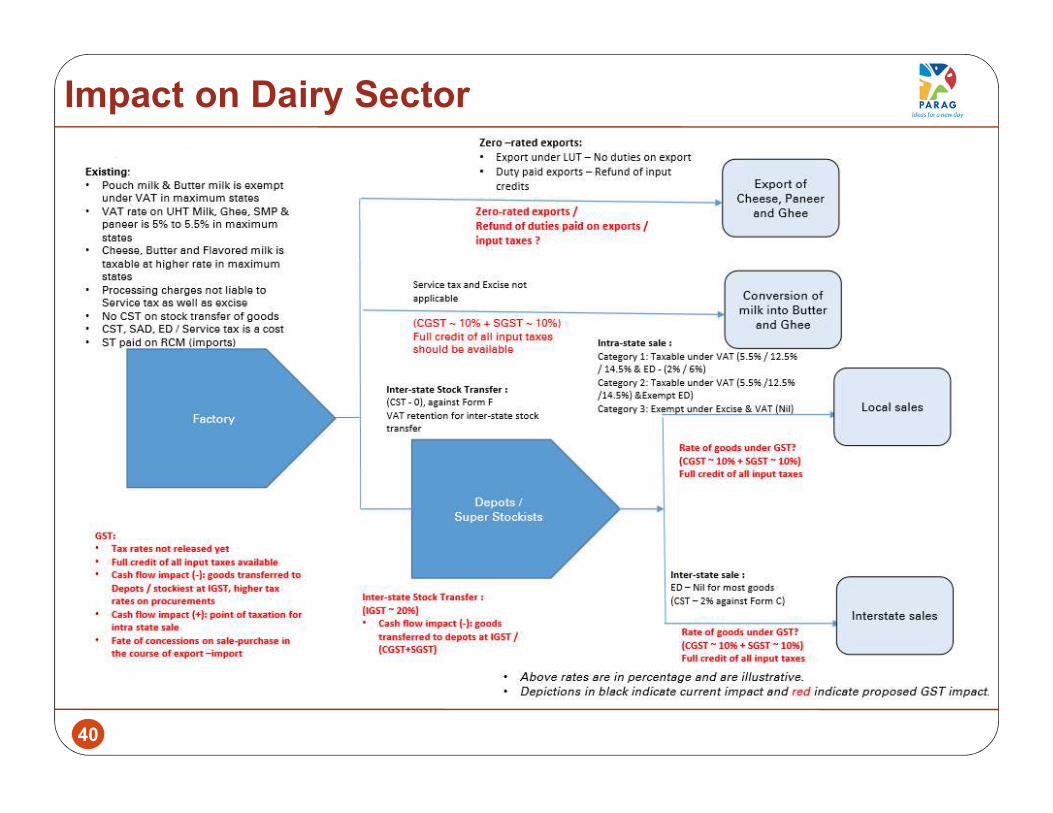

Impact on Dairy Sector

41

![The Institute of Chartered Accountants of India VASAI ...vasai-icai.org/Image/August 2011[1].pdf2 The Institute of Chartered Accountants of India VASAI BRANCH of WIRC NEWSLETTER Winner](https://img.dokumen.tips/doc/110x75/5e23f2112bef071a1501af82/the-institute-of-chartered-accountants-of-india-vasai-vasai-icaiorgimageaugust.jpg)