Embed Size (px)

Citation preview

Growing Asian Demand In Physical Gold And Its Impact

On Gold Prices

Minerals Council of AustraliaGold Forum

2 June 2015

Market Maker of the year

2014

COMMODITY RISK

SURVEY

COMMODITY RISK

SURVEY

Market Maker of the year

2013

Market Maker of the year

2012

Precious metals house of the year

2014

No 1. ranking in precious metals

2013

No 1. ranking in precious metals

2012

•Sydney, Singapore, London and New York

Trading Desks

•Largest lender to the Natural Resources Industry in Australia

Lending

•Active in Precious Metals derivatives

Derivatives

•Active in trading over 10% of global supply

Physical Gold

•Significant supplier to Asia: 20% of China’s imports

Asia

•Largest foreign trader on the Shanghai Gold Exchange

Shanghai Gold Exchange

•First foreign bank to be awarded the license

Import License in China

Awards At a Glance

ANZ Precious Metals at a Glance

10

The LBMA Bullion Market Forum 2015 25 June 2015

Session 5 - John Levin 1

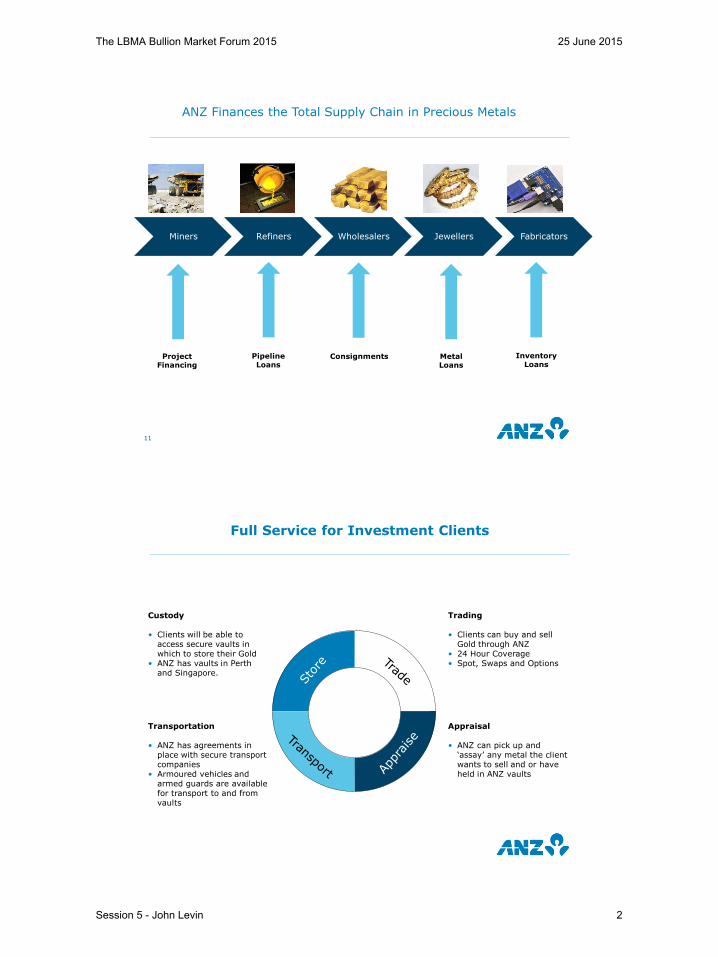

Miners Refiners Wholesalers Jewellers Fabricators

Project Financing

Pipeline Loans

Consignments Metal Loans

Inventory Loans

ANZ Finances the Total Supply Chain in Precious Metals

11

Full Service for Investment Clients

Custody

• Clients will be able to access secure vaults in which to store their Gold

• ANZ has vaults in Perth and Singapore.

Transportation

• ANZ has agreements in place with secure transport companies

• Armoured vehicles and armed guards are available for transport to and from vaults

Trading

• Clients can buy and sell Gold through ANZ

• 24 Hour Coverage• Spot, Swaps and Options

Appraisal

• ANZ can pick up and ‘assay’ any metal the client wants to sell and or have held in ANZ vaults

The LBMA Bullion Market Forum 2015 25 June 2015

Session 5 - John Levin 2

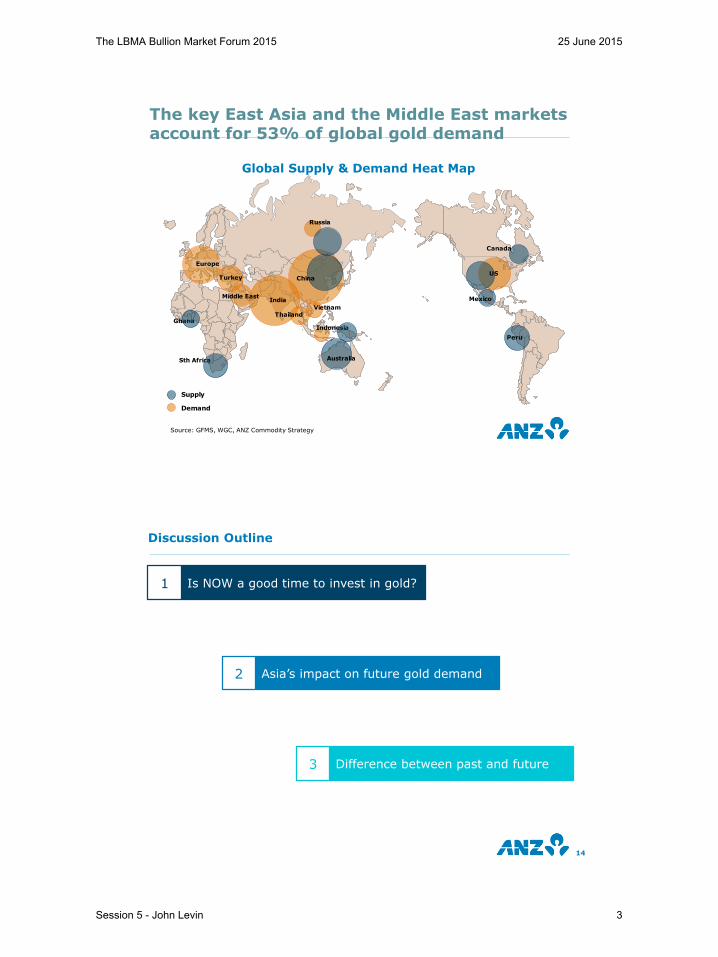

Sth Africa

Europe

Indonesia

Russia

Ghana

India

Peru

Australia

Canada

Mexico

US

ThailandVietnam

ChinaTurkey

Middle East

Source: GFMS, WGC, ANZ Commodity Strategy

Global Supply & Demand Heat Map

The key East Asia and the Middle East markets account for 53% of global gold demand

Supply

Demand

Discussion Outline

14

Is NOW a good time to invest in gold?1

Difference between past and future3

Asia’s impact on future gold demand2

The LBMA Bullion Market Forum 2015 25 June 2015

Session 5 - John Levin 3

Discussion Outline

15

Is NOW a good time to invest in gold?1

Precious metals the outperformer of the commodity complex

16Source: Bloomberg, ANZ Research

• The ANZ-China Commodity Index is down

30% over the past 18 months

• Precious metals are the shining beacon in the

commodity world

Precious metals don’t look so bad, do they?

• In some currencies, gold is still in a bull

market

• In Euro terms, gold is up nearly 25% in the

past 18 months

• Australian, Canadian and Japanese

consumers/producers have seen prices rise by

10-15%

Gold looks even better in local currency terms

40

50

60

70

80

90

100

110

120

Jan 14 Apr 14 Jul 14 Oct 14 Jan 15 Apr 15

PM

Agri

Industrials

ANZ CCI

Energy

Bulks

90

95

100

105

110

115

120

125

130

Jan 14 Apr 14 Jul 14 Oct 14 Jan 15 Apr 15

Index,

Jan 2

014 =

100

EUR

JPY

CAD

AUD

GBP

CHF

INR

Gold

The LBMA Bullion Market Forum 2015 25 June 2015

Session 5 - John Levin 4

What does the big dollar mean for gold?

17Source: Bloomberg, ANZ Research

40

50

60

70

80

90

100100

110

120

130

140

150

160

Oct 80 Oct 81 Oct 82 Oct 83 Oct 84

USD Gold (RHS)

Higher USD, Lower Gold

100

110

120

130

140

150

160

170

18050

60

70

80

90

100

Mar 85 Mar 86 Mar 87 Mar 88

USD Gold (RHS)

Lower USD, Higher Gold

USD bull markets = gold bear markets… but the reverse is also true

60

70

80

90

100

11090

100

110

120

130

140

Oct 11 Oct 12 Oct 13 Oct 14 Oct 15

USD Gold (RHS)

Higher USD, Lower Gold

60

70

80

90

100

11090

100

110

120

130

140

Aug 95 Aug 96 Aug 97 Aug 98 Aug 99 Aug 00 Aug 01

USD Gold (RHS)

Higher USD, Lower Gold

100

120

140

160

180

20065

70

75

80

85

90

95

100

Feb 02 Feb 03 Feb 04 Feb 05 Feb 06

USD Gold (RHS)

Lower USD, Higher Gold

USD Gold (RHS)

Lower USD, Higher Gold

1980to

1988

1995to

2006

2011to

----

Market Trend #1 - China

18Source: ANZ Research

-300

-250

-200

-150

-100

-50

0

50

100

150

200

250

300

-500

-400

-300

-200

-100

0

100

200

300

400

500

09 10 11 12 13 14 15

Metr

ic t

onnes

Metr

ic t

onnes

Supply Demand Physical Stock Change (RHS)

Eyes too big for stomach…

… imports are still too high

• Onshore stocks have increased by over 500

tonnes over the past 12 months

• This is likely to create problems with

oversupply of physical metal

• Gold jewellery demand down 10% y/y in the

first quarter of 2015

• Our Physical Demand barometer showed a

sharp pickup in Q2 imports

• This will continue to exacerbate the physical

oversupply issues onshore

• Physical premiums and spreads will remain

soft this year-0.1

0.0

0.1

0.2

0.3

0.4

0.5

0

20

40

60

80

100

120

140

Jun 13 Sep 13 Dec 13 Mar 14 Jun 14 Sep 14 Dec 14 Mar 15

Valu

e

Metr

ic t

onnes

Imports (CH) Imports (HK) Demand Barometer (2m fwd) (RHS)(RHS)

The LBMA Bullion Market Forum 2015 25 June 2015

Session 5 - John Levin 5

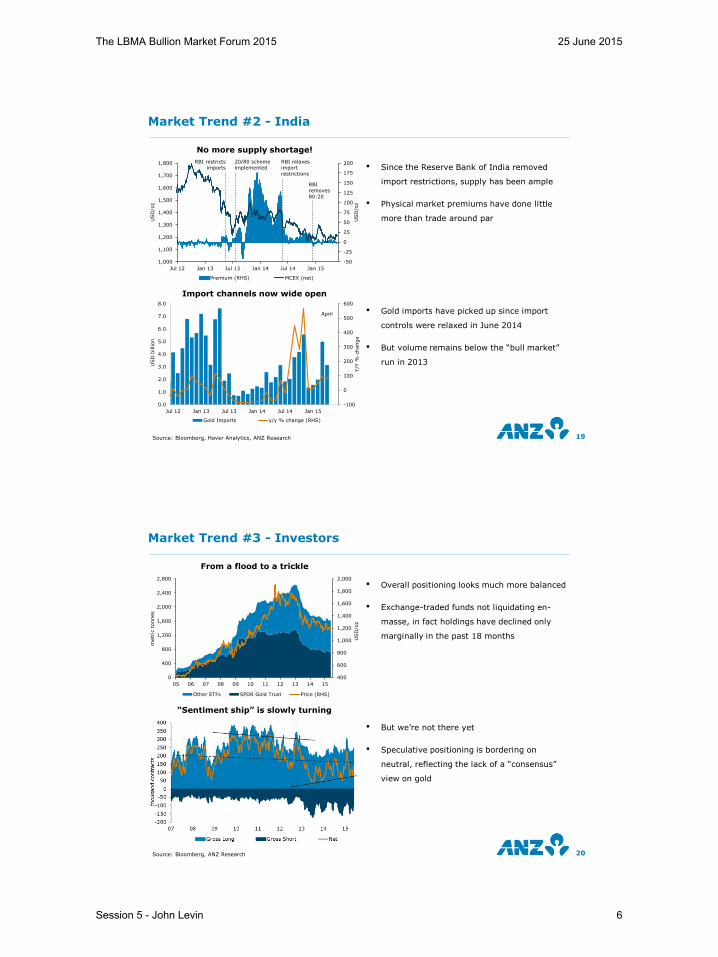

Market Trend #2 - India

19Source: Bloomberg, Haver Analytics, ANZ Research

No more supply shortage!

Import channels now wide open

• Since the Reserve Bank of India removed

import restrictions, supply has been ample

• Physical market premiums have done little

more than trade around par

• Gold imports have picked up since import

controls were relaxed in June 2014

• But volume remains below the “bull market”

run in 2013

-50

-25

0

25

50

75

100

125

150

175

200

1,000

1,100

1,200

1,300

1,400

1,500

1,600

1,700

1,800

Jul 12 Jan 13 Jul 13 Jan 14 Jul 14 Jan 15

USD

/oz

USD

/oz

Premium (RHS) MCEX (net)

RBI restricts

imports

20/80 scheme

implemented

RBI relaxes

import

restrictions

RBI

removes 80:20

-100

0

100

200

300

400

500

600

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

Jul 12 Jan 13 Jul 13 Jan 14 Jul 14 Jan 15

Y/Y

% c

hange

USD

billion

Gold Imports y/y % change (RHS)

April

Market Trend #3 - Investors

20Source: Bloomberg, ANZ Research

From a flood to a trickle

“Sentiment ship” is slowly turning

• Overall positioning looks much more balanced

• Exchange-traded funds not liquidating en-

masse, in fact holdings have declined only

marginally in the past 18 months

• But we’re not there yet

• Speculative positioning is bordering on

neutral, reflecting the lack of a “consensus”

view on gold

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

0

400

800

1,200

1,600

2,000

2,400

2,800

05 06 07 08 09 10 11 12 13 14 15

USD

/oz

metr

ic t

onnes

Other ETFs SPDR Gold Trust Price (RHS)

The LBMA Bullion Market Forum 2015 25 June 2015

Session 5 - John Levin 6

• Gold will rise once the USD has had its run

• China/India physical demand is soft, “rush to buy” is not there

• Investors are sidelined by low conviction

Discussion Outline

21

Is NOW a good time to invest in gold?1

Asia’s impact on future gold demand2

Accumulate!

• Asia’s ascension will be led by 10 economies – China, India, Indonesia, Japan, South Korea, Malaysia, Philippines, Singapore, Thailand and Vietnam

• These 10 economies could account for 50% of global GDP by 2050

0%

10%

20%

30%

40%

50%

60%

1980 1985 1990 1995 2000 2005 2010 2015 2020 2025 2030 2035 2040 2045 2050

Percen

tag

e o

f W

orld

GD

P C

urren

t P

ric

es

Asia 10

Euro Zone

USA

Source: CEIC, ANZ Research projections

The ‘Asian Century’ – an economic perspective of the A10

The LBMA Bullion Market Forum 2015 25 June 2015

Session 5 - John Levin 7

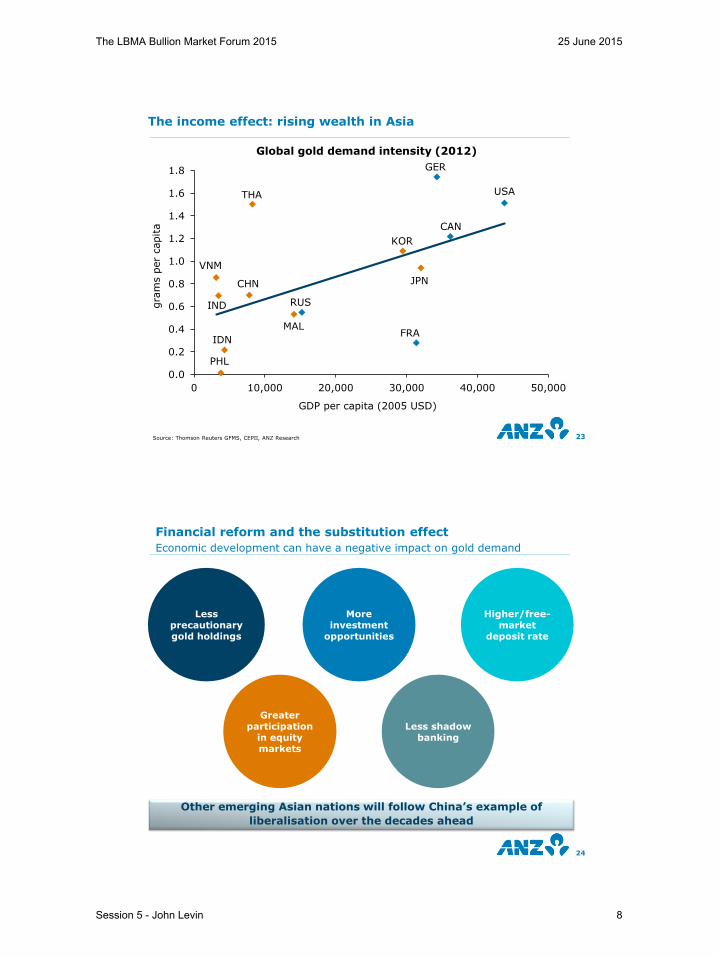

23

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

0 10,000 20,000 30,000 40,000 50,000

gra

ms p

er

capita

GDP per capita (2005 USD)

USA

GER

CAN

FRA

JPN

KOR

THA

CHN

RUS

MAL

VNM

IND

IDN

PHL

Global gold demand intensity (2012)

Source: Thomson Reuters GFMS, CEPII, ANZ Research

The income effect: rising wealth in Asia

Financial reform and the substitution effect

Economic development can have a negative impact on gold demand

24

Other emerging Asian nations will follow China’s example of

liberalisation over the decades ahead

Less precautionary gold holdings

More investment

opportunities

Higher/free-market

deposit rate

Greater participation

in equity markets

Less shadow banking

The LBMA Bullion Market Forum 2015 25 June 2015

Session 5 - John Levin 8

Financial reform and Asia’s new fund managersInstitutional asset base of Asia 10 countries to continue growing

25

Projected size of institutional assets (% of GDP)

0

50

100

150

200

250

300

350

400

Chin

a

India

Indonesia

Japan

South

Kore

a

Mala

ysia

Philip

pin

es

Sin

gapore

Thailand

Vie

tnam

Asia

10

% o

f G

DP

2009 2030 2050

Source: World Bank, ANZ Research

Total retail and institutional gold demand to double by 2050An increase to 5,000 annually, from 2,500 tonnes currently

26

Asia 10 projected annual gold investment demand

RETAIL

CONSUMPTION

(gm/capita)

0.0% 0.5% 1.0% 1.5% 2.0% 2.5% 3.0% 3.5% 4.0% 4.5%

0.5 1,841 2,024 2,208 2,391 2,575 2,758 2,941 3,125 3,308 3,492

0.6 2,209 2,392 2,576 2,759 2,943 3,126 3,310 3,493 3,677 3,860

0.7 2,577 2,760 2,944 3,127 3,311 3,494 3,678 3,861 4,045 4,228

0.8 2,945 3,129 3,312 3,495 3,679 3,862 4,046 4,229 4,413 4,596

0.9 3,313 3,497 3,680 3,864 4,047 4,231 4,414 4,598 4,781 4,964

1.0 3,681 3,865 4,048 4,232 4,415 4,599 4,782 4,966 5,149 5,333

1.1 4,049 4,233 4,416 4,600 4,783 4,967 5,150 5,334 5,517 5,701

1.2 4,418 4,601 4,785 4,968 5,152 5,335 5,518 5,702 5,885 6,069

1.3 4,786 4,969 5,153 5,336 5,520 5,703 5,887 6,070 6,254 6,437

1.4 5,154 5,337 5,521 5,704 5,888 6,071 6,255 6,438 6,622 6,805

1.5 5,522 5,706 5,889 6,072 6,256 6,439 6,623 6,806 6,990 7,173

1.6 5,890 6,074 6,257 6,441 6,624 6,808 6,991 7,174 7,358 7,541

1.7 6,258 6,442 6,625 6,809 6,992 7,176 7,359 7,543 7,726 7,910

1.8 6,626 6,810 6,993 7,177 7,360 7,544 7,727 7,911 8,094 8,278

1.9 6,995 7,178 7,362 7,545 7,728 7,912 8,095 8,279 8,462 8,646

2.0 7,363 7,546 7,730 7,913 8,097 8,280 8,464 8,647 8,830 9,014

% OF INSTITUTIONAL HOLDINGS BY 2050

Source: Thomson Reuters GFMS, World Bank, ANZ Research

The LBMA Bullion Market Forum 2015 25 June 2015

Session 5 - John Levin 9

Discussion Outline

27

Is NOW a good time to invest in gold?1

Difference between past and future3

Asia’s impact on future gold demand2

• Gold will rise once the USD has had its run

• China/India physical demand is soft, “rush to buy” is not there

• Investors are sidelined by low conviction

• Annual gold demand in Asia to double to 5,000 tonnes by 2050

• Higher incomes boosting consumption - “Income” effect

• “Substitution” effect initially negative, ultimately positive for demand

Accumulate!

The pattern of gold production has changed in recent decadesChina is both the world’s largest producer and consumer

28

135

Source: Thomson Reuters GFMS, ANZ Research

The LBMA Bullion Market Forum 2015 25 June 2015

Session 5 - John Levin 10

Ultimately, the producer cost-curve should underpin prices20% of world production is not profitable on a cash-cost basis

29

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

0 250 500 750 1,000 1,250 1,500 1,750 2,000

Cash C

ost

(USD

/oz)

Cumulative Production (tonnes)

2014 average price

Source: Wood Mackenzie, US Geological Survey, Bloomberg, ANZ Research

Gold mining is not cheap… Long-term, the cost-curve will underpin prices

• China may only have 5 years of domestic

supply left

• Australia and South Africa are some of the

highest-cost producers

• Historically, the 75th percentile has provided a

good guide to long-term price levels

92 94 96 98 00 02 04 06 08 10 12 14 16

USD

/oz (

log s

cale

)

Gold Price Weighted Average 75th Percentile 90th Percentile

200

400

600

1,200

1,600

2,000

800

10,000

9,000

8,000

7,000

6,000

5,000

4,000

3,000

2,000

1,000

0

1,000

2,000

Oth

er

Austr

alia

South

Afr

ica

Russia

Chile

United S

tate

s

Indonesia

Bra

zil

Peru

Chin

a

Uzbekis

tan

Ghana

Mexic

o

PN

G

Canada

tonnes

Annual Mine Production

Below Ground Reserves

But the years ahead could look different…

Producer hedging was common practice during the 1990’sBut the impact of this is now much smaller

30

Producer hedging activity in the gold market

Source: Thomson Reuters GFMS, Bloomberg, ANZ Research

(500)

(250)

0

250

500

90 92 94 96 98 00 02 04 06 08 10 12 14

tonnes

Hedging

De-hedging

0

250

500

750

1,000

1,250

1,500

1,750

0

500

1,000

1,500

2,000

2,500

3,000

90 92 94 96 98 00 02 04 06 08 10 12 14

USD

/oz

tonnes

Global Hedge Book Avg. gold price (RHS)

The LBMA Bullion Market Forum 2015 25 June 2015

Session 5 - John Levin 11

Central banks no longer net sellers of goldAfter liquidating holdings for most of the past 25 years

31

(800)

(600)

(400)

(200)

0

200

400

600

84 86 88 90 92 94 96 98 00 02 04 06 08 10 12 14

tonnes

Central bank activity in the gold market

Some should be holding more gold

0

10

20

30

40

50

60

70

80

90

Perc

ent

of to

tal FX r

eserv

es

Upper middle-

income

High-income Lower middle-

income

Low income

Source: World Gold Council, World Bank, Bloomberg, ANZ Research

• Central banks became net accumulators of

gold since the global financial crisis

• Most of the buying has been from emerging

market central banks, particularly Russia,

Turkey and Kazakhstan

• “High-income” countries hold an average 20%

of FX reserves in gold, though this is heavily

skewed by western European countries and

the U.S.

• Countries in the other income brackets hold

gold comprising less than 10% of reserves, on

average

CONCLUSIONS

32

Is NOW a good time to invest in gold?1

Difference between past and future3

Asia’s impact on future gold demand2

• Gold will rise once the USD has had its run

• China/India physical demand is soft, “rush to buy” is not there

• Investors are sidelined by low conviction

• Cost-curve is supportive of prices

• Producer hedging is minimal and central banks net buyers

• Gold prices forecast to reach USD2,400/oz by 2030

• Annual gold demand in Asia to double to 5,000 tonnes by 2050

• Higher incomes boosting consumption -“Income” effect

• “Substitution” effect initially negative, ultimately positive for demand

Accumulate!

The LBMA Bullion Market Forum 2015 25 June 2015

Session 5 - John Levin 12