Embed Size (px)

Citation preview

Group 5

Brad Maryman

Cristina Matthews

Todd Duncan

Tom Tran

Sean Rose

Agenda

Chapter 2 Overview Case 2-3

– SWOT analysis

Reading 2-1– Value chain analysis

Reading 2-3, Case 2-1– Value chain analysis– The balanced scorecard

Chapter 2 Overview

Important management tools for implementing strategy:

SWOT analysis Value chain analysis The balanced scorecard

SWOT Analysis

SWOT analysis is a procedure for identifying a firm’s critical success factors: its internal strengths and weaknesses and its external opportunities and threats.

Critical Success Factors (CSFs) are measures of those aspects of the firm’s performance that are essential to its competitive advantage.

Value-Chain Analysis

Firms use this tool to identify the specific steps required to provide a competitive product or service. It is specifically used to:

Better understand a firm’s competitive advantage Identify where to add value or reduce costs Better understand external connections to the

firm (suppliers, customers, competitors)

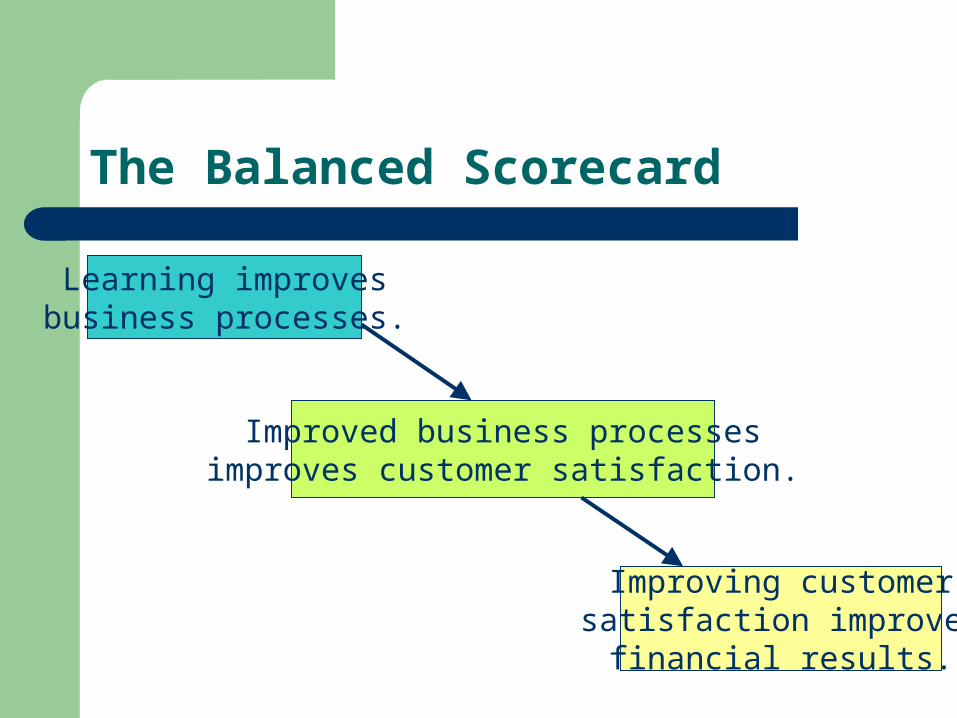

The Balanced Scorecard

Learning improvesbusiness processes.

Improved business processesimproves customer satisfaction.

Improving customersatisfaction improves

financial results.

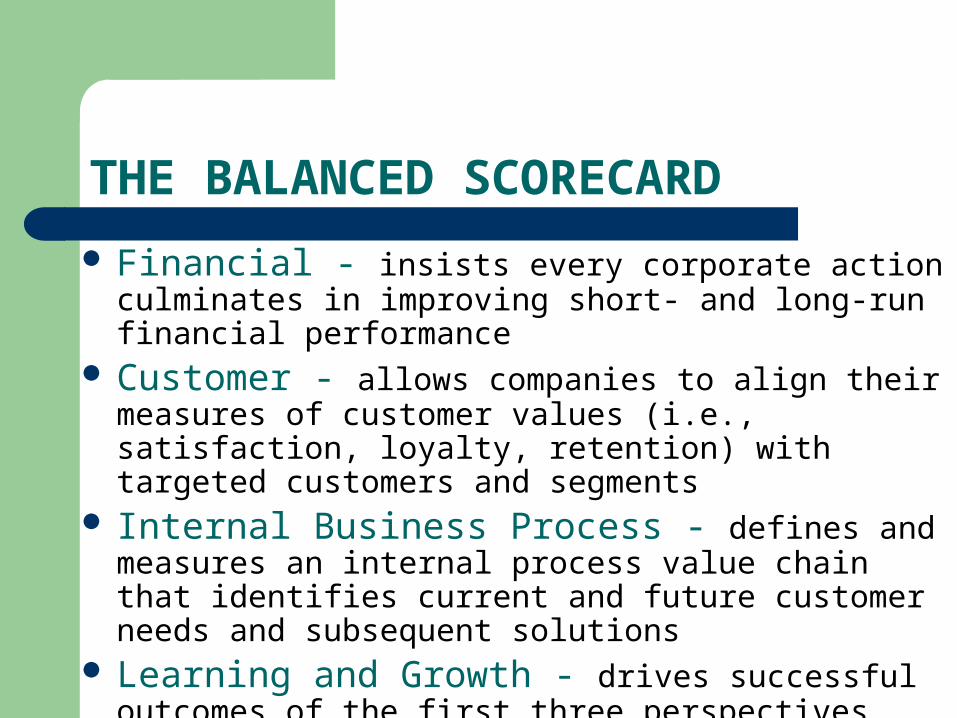

THE BALANCED SCORECARD

Financial - insists every corporate action culminates in improving short- and long-run financial performance

Customer - allows companies to align their measures of customer values (i.e., satisfaction, loyalty, retention) with targeted customers and segments

Internal Business Process - defines and measures an internal process value chain that identifies current and future customer needs and subsequent solutions

Learning and Growth - drives successful outcomes of the first three perspectives

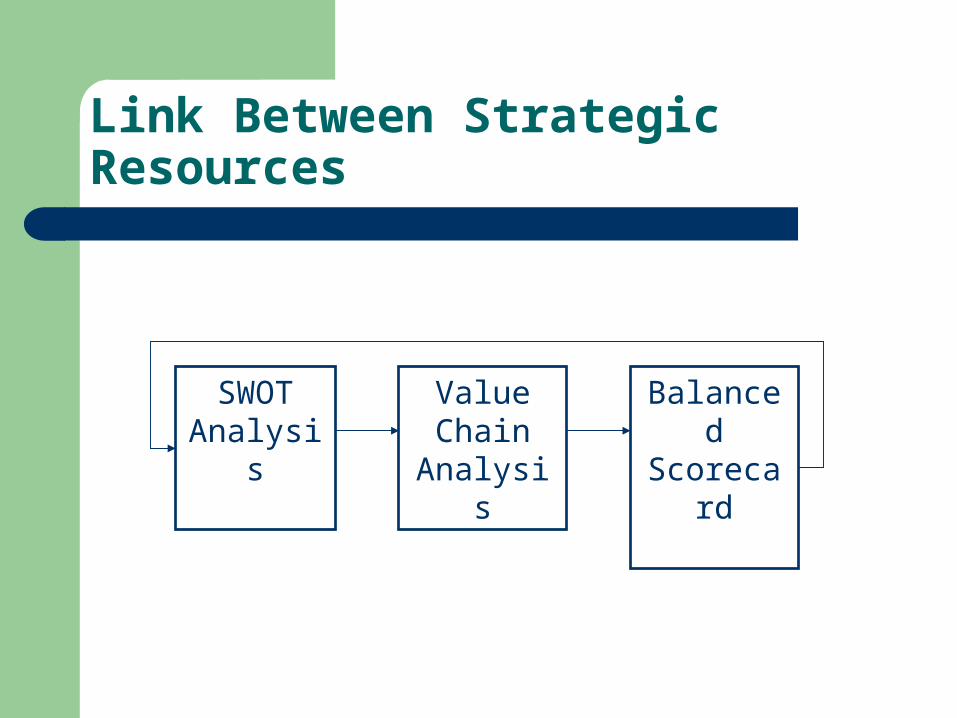

Link Between Strategic Resources

SWOTAnalysis

ValueChain

Analysis

BalancedScorecard

Case 2-3: Accounting & Tax Practice

Background on Terry Merton– CPA, controller for small manufacturing firm– Dreams of owning her own business

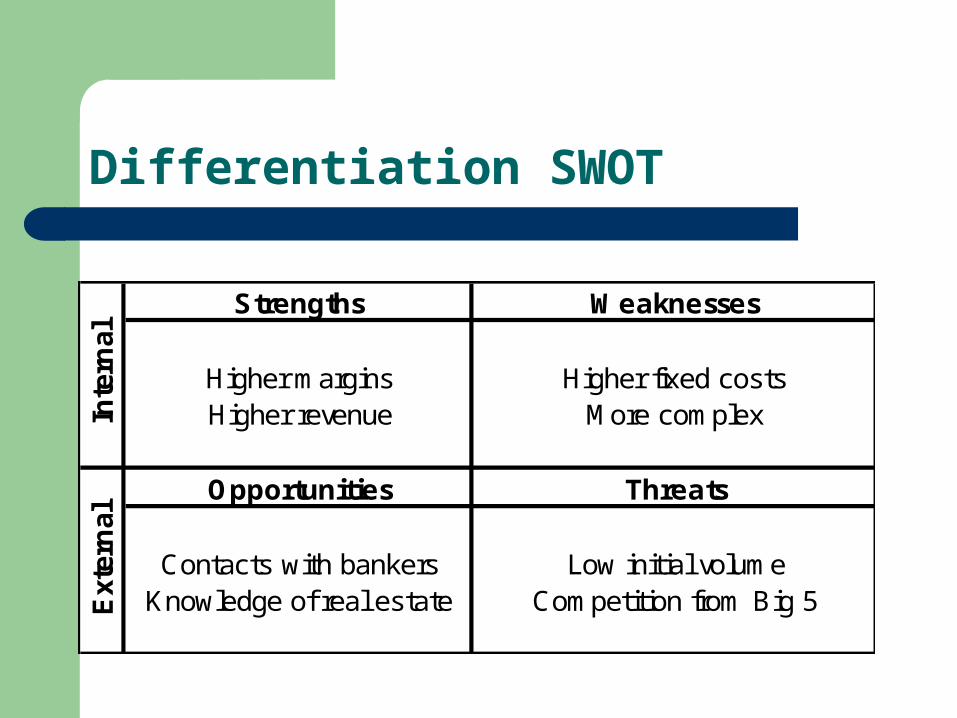

Who should be her target market?– Tax practice = cost leadership– Tax and accounting practice = differentiation

Bill Anderson, the loan officer– Maximum loan of $8,000– Annual payments of $2,110

Differentiation SWOT

Strengths Weaknesses

Higher margins Higher fixed costsHigher revenue More complex

Opportunities Threats

Contacts with bankers Low initial volumeKnowledge of real estate Competition from Big 5E

xter

nal

Inte

rnal

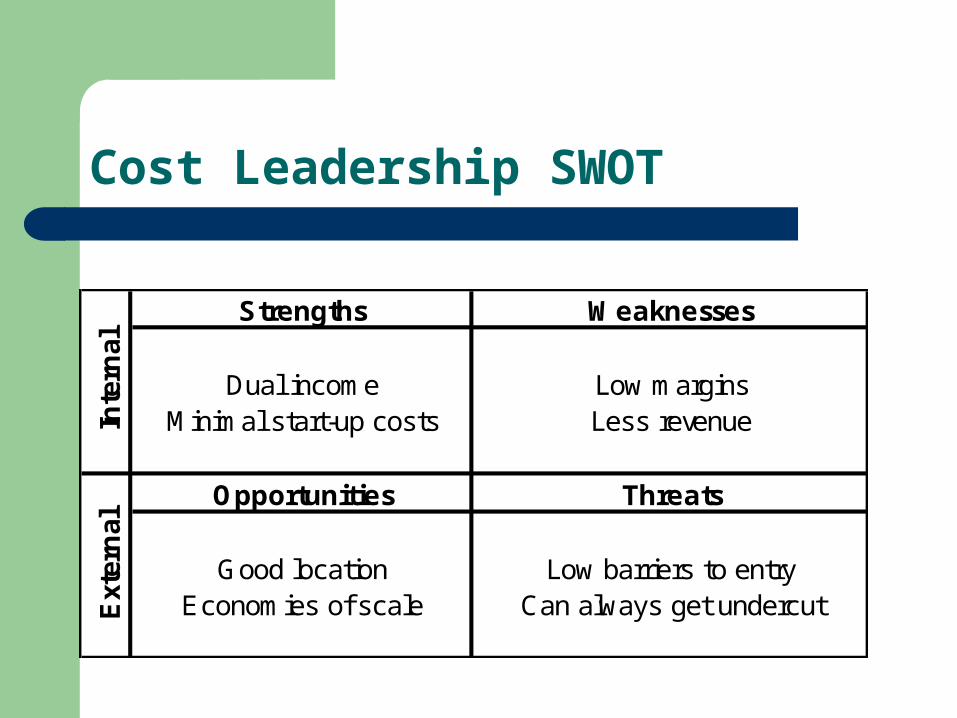

Cost Leadership SWOT

Strengths Weaknesses

Dual income Low marginsMinimal start-up costs Less revenue

Opportunities Threats

Good location Low barriers to entryEconomies of scale Can always get undercut

Inte

rnal

Ext

ern

al

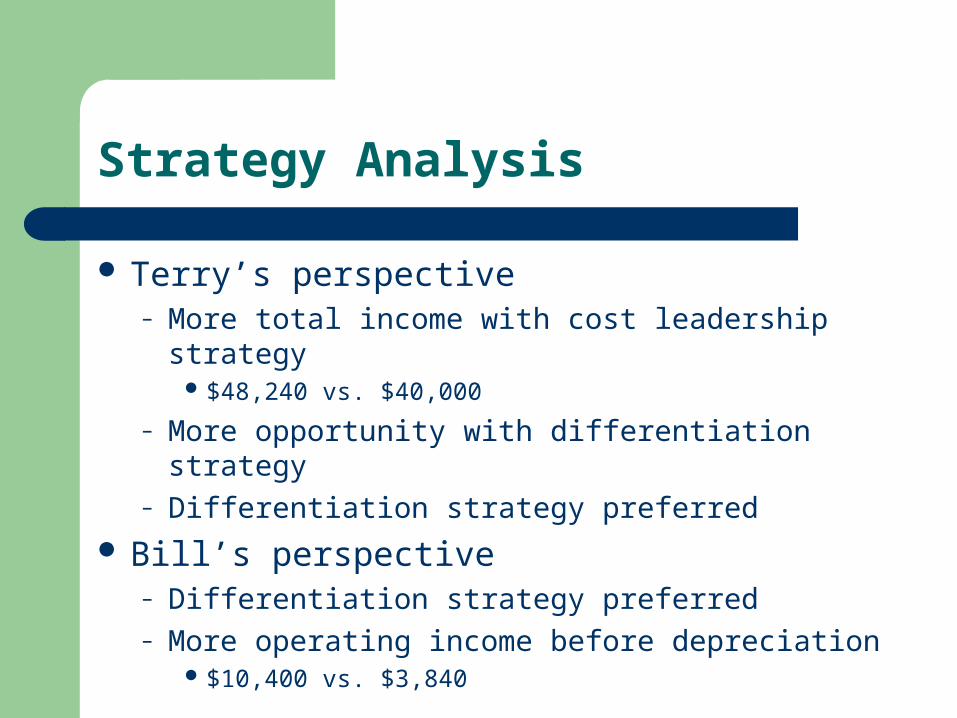

Strategy Analysis

Terry’s perspective– More total income with cost leadership strategy

$48,240 vs. $40,000

– More opportunity with differentiation strategy– Differentiation strategy preferred

Bill’s perspective– Differentiation strategy preferred– More operating income before depreciation

$10,400 vs. $3,840

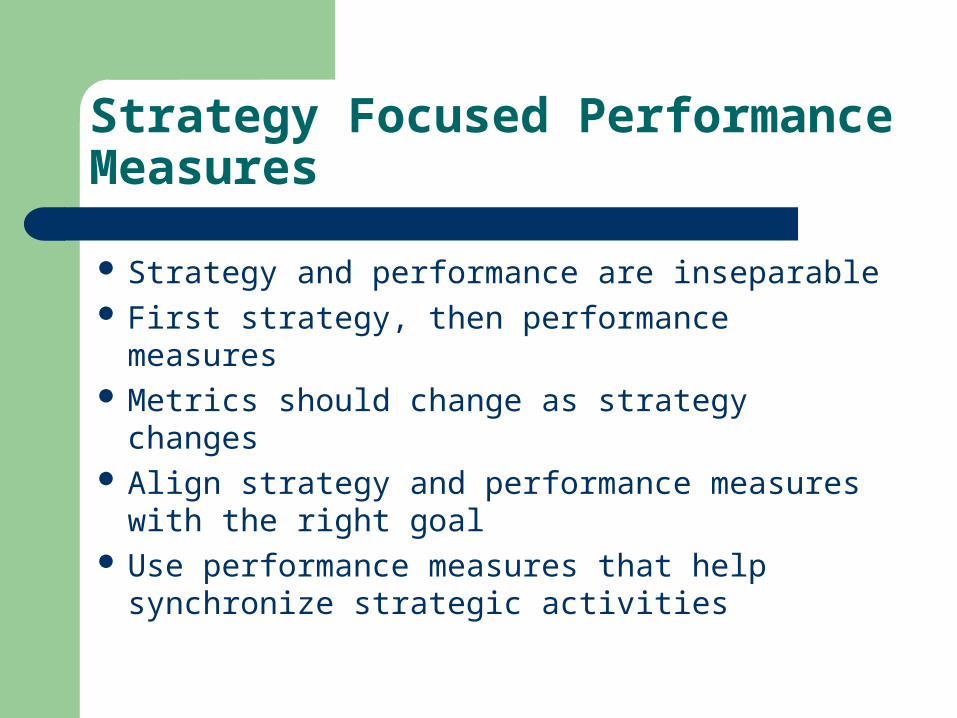

Strategy Focused Performance Measures

Strategy and performance are inseparable First strategy, then performance measures Metrics should change as strategy changes Align strategy and performance measures

with the right goal Use performance measures that help

synchronize strategic activities

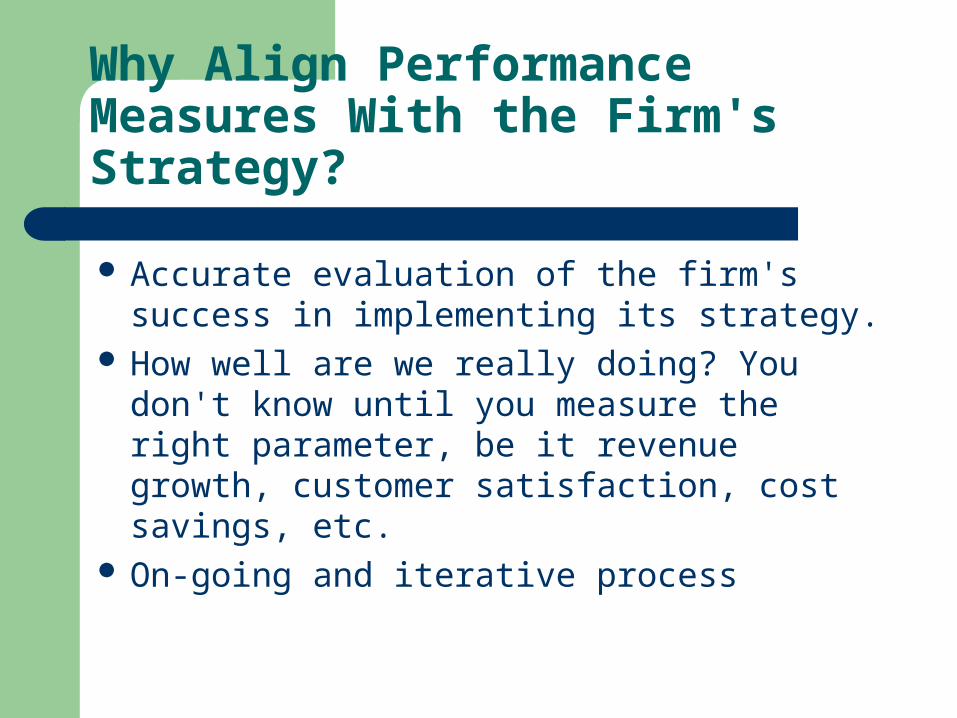

Why Align Performance Measures With the Firm's Strategy?

Accurate evaluation of the firm's success in implementing its strategy.

How well are we really doing? You don't know until you measure the right parameter, be it revenue growth, customer satisfaction, cost savings, etc.

On-going and iterative process

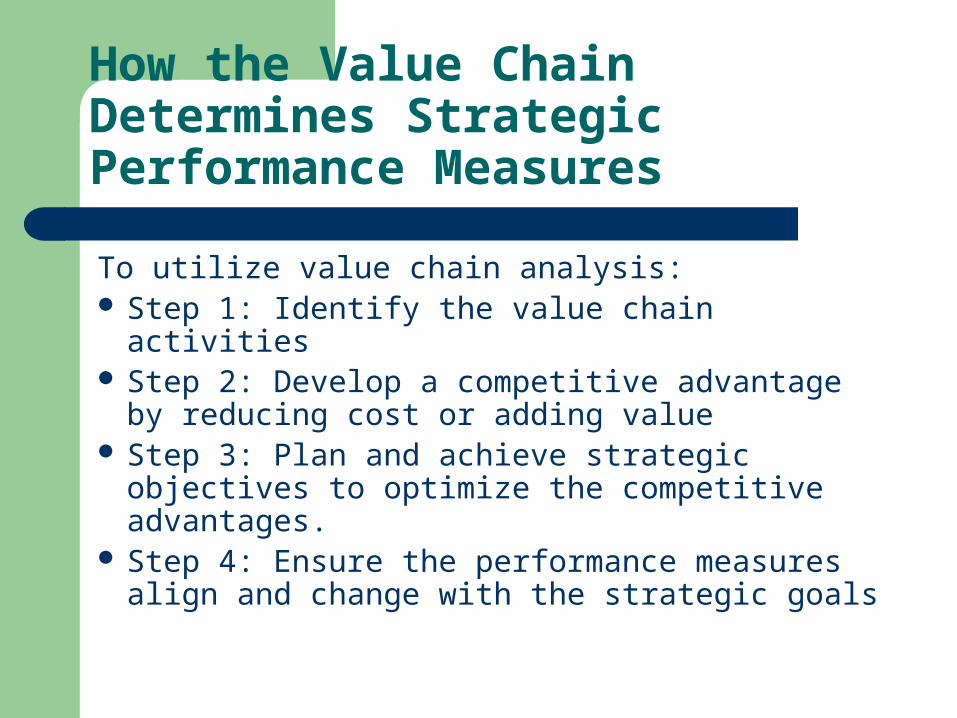

How the Value Chain Determines Strategic Performance Measures

To utilize value chain analysis: Step 1: Identify the value chain activities Step 2: Develop a competitive advantage by

reducing cost or adding value Step 3: Plan and achieve strategic objectives

to optimize the competitive advantages. Step 4: Ensure the performance measures

align and change with the strategic goals

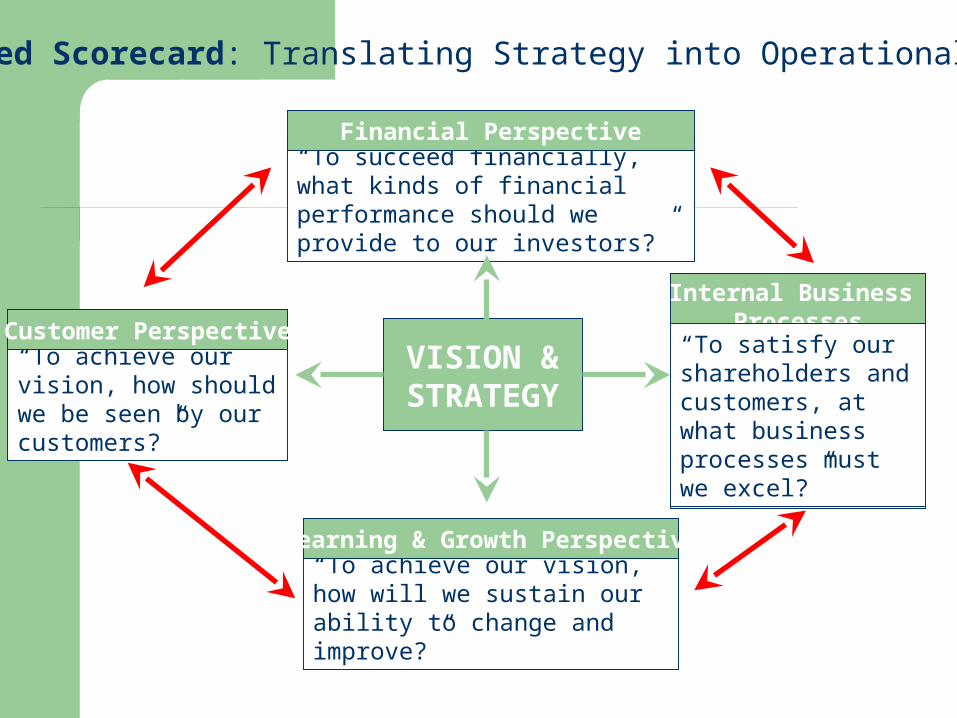

Balanced Scorecard: Translating Strategy into Operational Terms

VISION &STRATEGY

“To achieve our vision, how should we be seen by our customers?”

Customer Perspective

“To achieve our vision, how will we sustain our ability to change and improve?”

Learning & Growth Perspective

“To succeed financially, what kinds of financial performance should we provide to our investors?”

Financial Perspective

“To satisfy our shareholders and customers, at what business processes must we excel?”

Internal Business Processes

“To satisfy our shareholders and customers, at what business processes must we excel?”

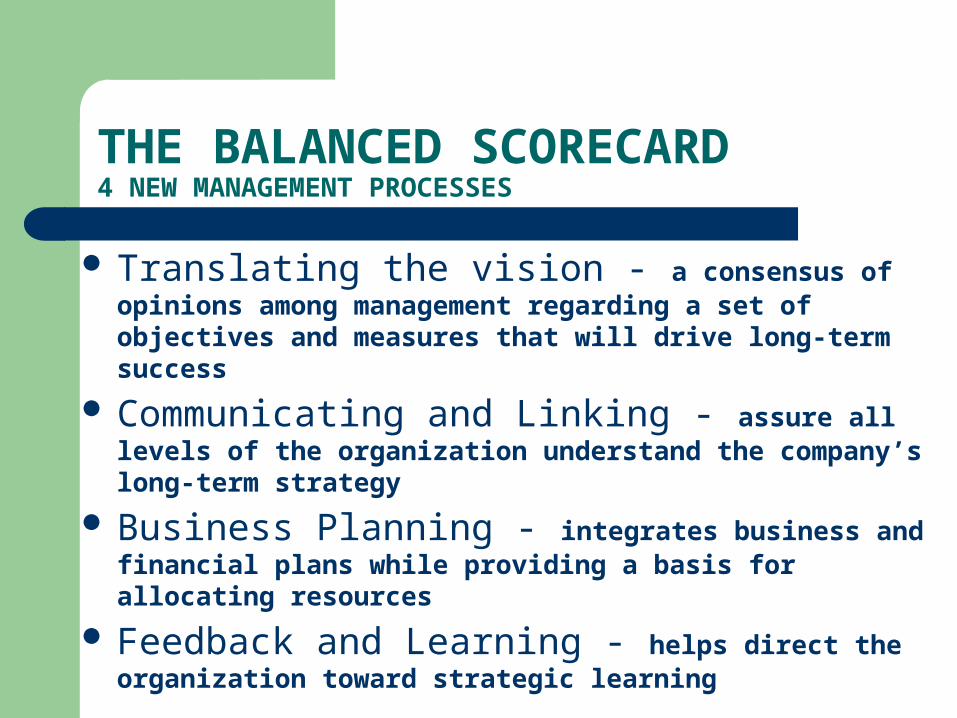

THE BALANCED SCORECARD 4 NEW MANAGEMENT PROCESSES

Translating the vision - a consensus of opinions among management regarding a set of objectives and measures that will drive long-term success

Communicating and Linking - assure all levels of the organization understand the company’s long-term strategy

Business Planning - integrates business and financial plans while providing a basis for allocating resources

Feedback and Learning - helps direct the organization toward strategic learning

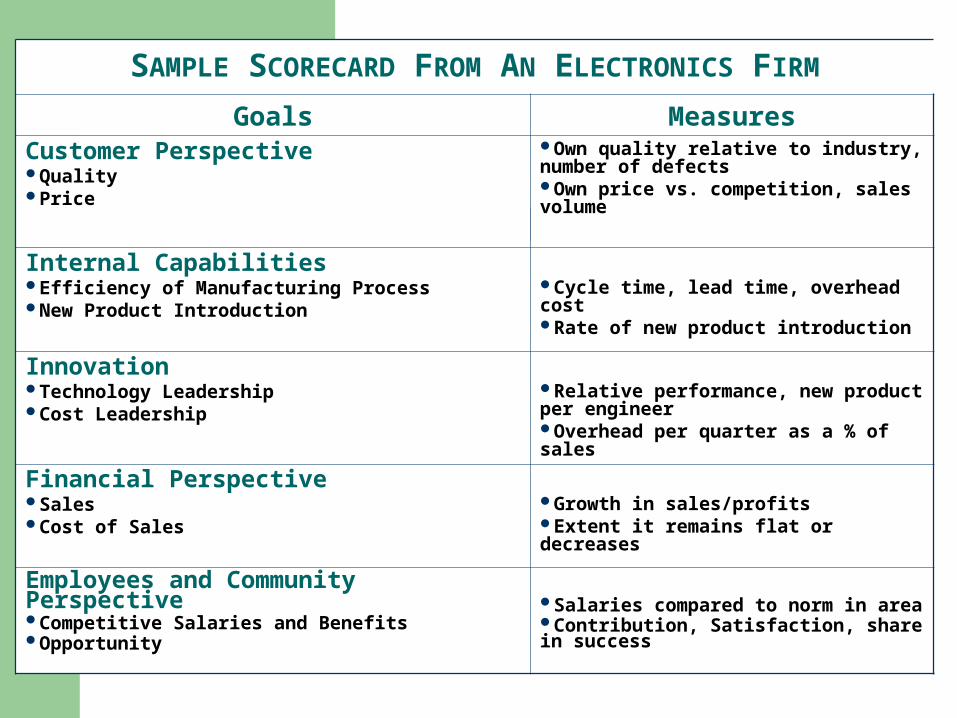

SAMPLE SCORECARD FROM AN ELECTRONICS FIRM

Goals MeasuresCustomer PerspectiveQualityPrice

Own quality relative to industry, number of defectsOwn price vs. competition, sales volume

Internal CapabilitiesEfficiency of Manufacturing ProcessNew Product Introduction

Cycle time, lead time, overhead costRate of new product introduction

InnovationTechnology LeadershipCost Leadership

Relative performance, new product per engineerOverhead per quarter as a % of sales

Financial PerspectiveSalesCost of Sales

Growth in sales/profitsExtent it remains flat or decreases

Employees and Community PerspectiveCompetitive Salaries and BenefitsOpportunity

Salaries compared to norm in areaContribution, Satisfaction, share in success

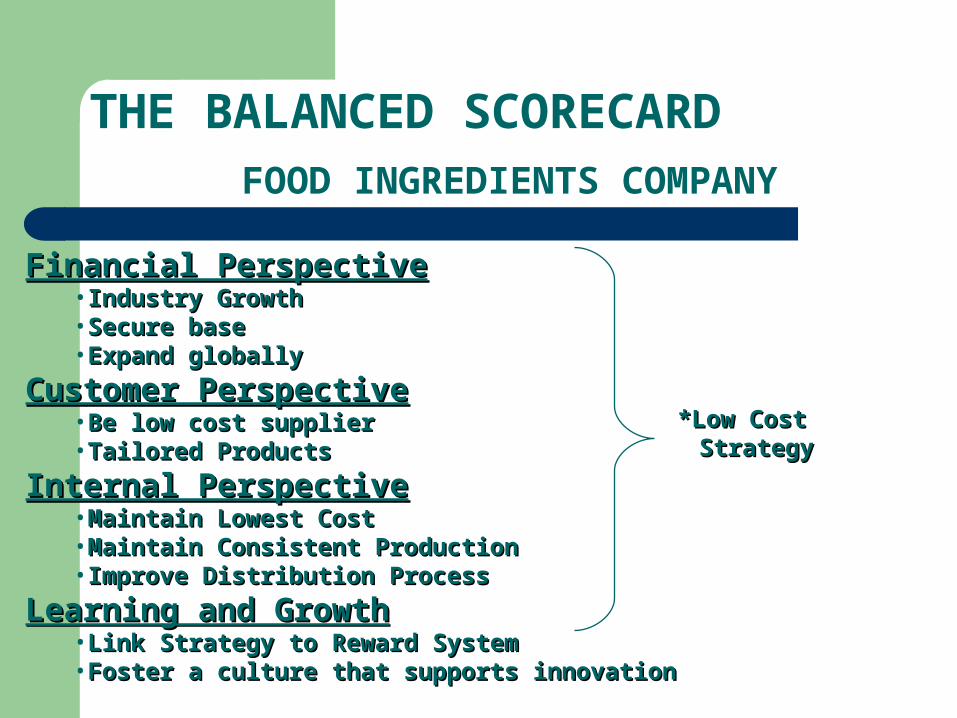

THE BALANCED SCORECARDFOOD INGREDIENTS COMPANY

Financial PerspectiveFinancial Perspective•Industry GrowthIndustry Growth•Secure baseSecure base•Expand globallyExpand globally

Customer PerspectiveCustomer Perspective•Be low cost supplierBe low cost supplier•Tailored ProductsTailored Products

Internal PerspectiveInternal Perspective•Maintain Lowest CostMaintain Lowest Cost•Maintain Consistent ProductionMaintain Consistent Production•Improve Distribution ProcessImprove Distribution Process

Learning and GrowthLearning and Growth•Link Strategy to Reward SystemLink Strategy to Reward System•Foster a culture that supports innovationFoster a culture that supports innovation

*Low Cost *Low Cost StrategyStrategy

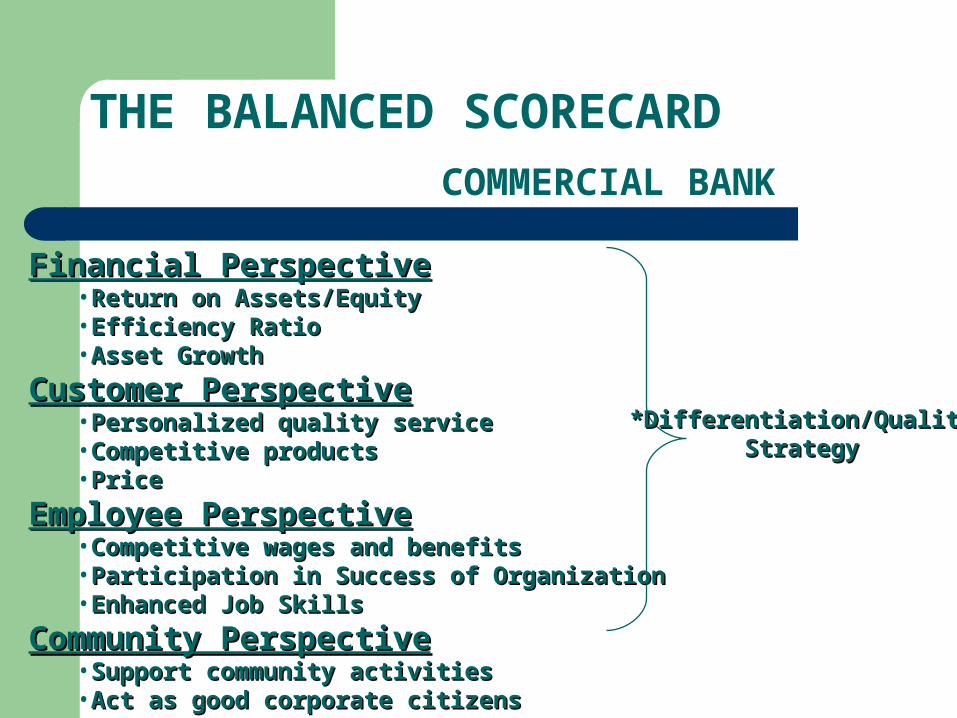

THE BALANCED SCORECARD

COMMERCIAL BANK

Financial PerspectiveFinancial Perspective•Return on Assets/EquityReturn on Assets/Equity•Efficiency RatioEfficiency Ratio•Asset GrowthAsset Growth

Customer PerspectiveCustomer Perspective•Personalized quality servicePersonalized quality service•Competitive productsCompetitive products•PricePrice

Employee PerspectiveEmployee Perspective•Competitive wages and benefitsCompetitive wages and benefits•Participation in Success of OrganizationParticipation in Success of Organization•Enhanced Job SkillsEnhanced Job Skills

Community PerspectiveCommunity Perspective•Support community activitiesSupport community activities•Act as good corporate citizensAct as good corporate citizens

*Differentiation/Quality*Differentiation/QualityStrategyStrategy

THE BALANCED SCORECARD

BIOTECHNOLOGY FIRM

Customer PerspectiveCustomer Perspective•New ProductsNew Products•Early purchase of seasonal productsEarly purchase of seasonal products•Accurate invoicesAccurate invoices

Internal Business PerspectiveInternal Business Perspective•Low Cost ProducerLow Cost Producer•Reduce InventoryReduce Inventory•New ProductsNew Products

Innovation PerspectiveInnovation Perspective•New Active IngredientsNew Active Ingredients•Proprietary positionsProprietary positions

Financial PerspectiveFinancial Perspective•GrowthGrowth•ProfitabilityProfitability•Industry leadershipIndustry leadership

*Differentiation/Quality*Differentiation/QualityStrategyStrategy

Case 2-1: Atlantic City Casino

Background– HCA purchased LV casino, constructed another– Casino is an independent operating unit – Low ROI (better return in CDs)– Casino located several blocks off of main strip– Proposal for new entertainment center at casino– Management is cautious

Value Chain Analysis For HCA

Value chain analysis– Casino operations (4th)– Hotel operations (5th)– Food/beverage operations (1st)

Casinos with similar revenues have greater net income Casino has been profitable from day one Cost reduction ideas

– Need more information Value-added ideas

– Improve access to the casino– Carry carnival theme into casino– Headline attractions to draw customers– Complimentary gaming chips for theme park customers

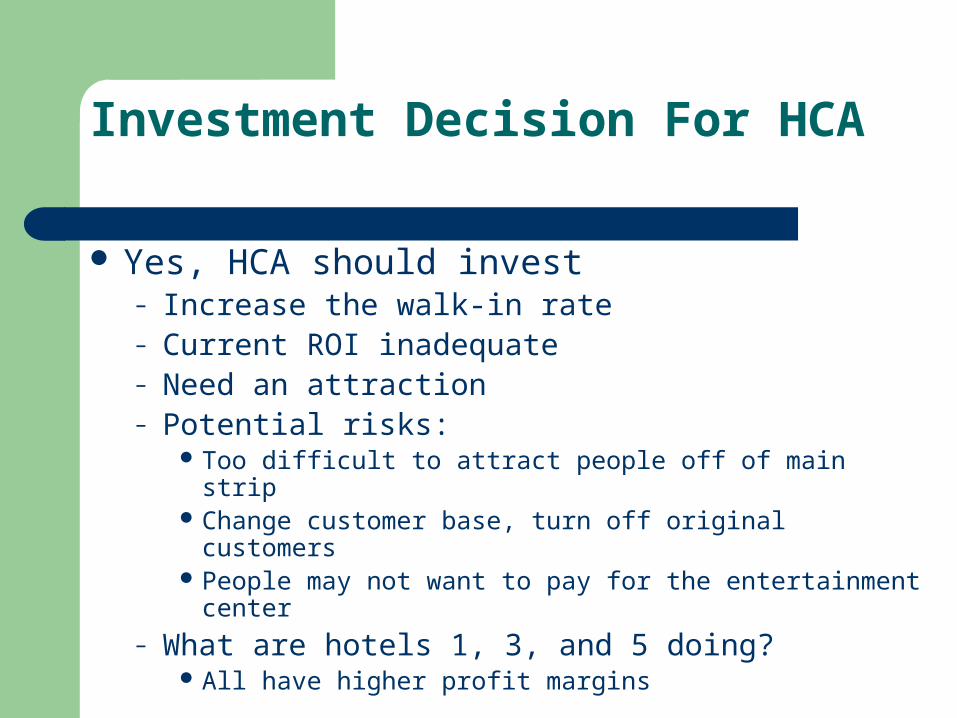

Investment Decision For HCA

Yes, HCA should invest – Increase the walk-in rate– Current ROI inadequate– Need an attraction – Potential risks:

Too difficult to attract people off of main strip Change customer base, turn off original customers People may not want to pay for the entertainment center

– What are hotels 1, 3, and 5 doing? All have higher profit margins

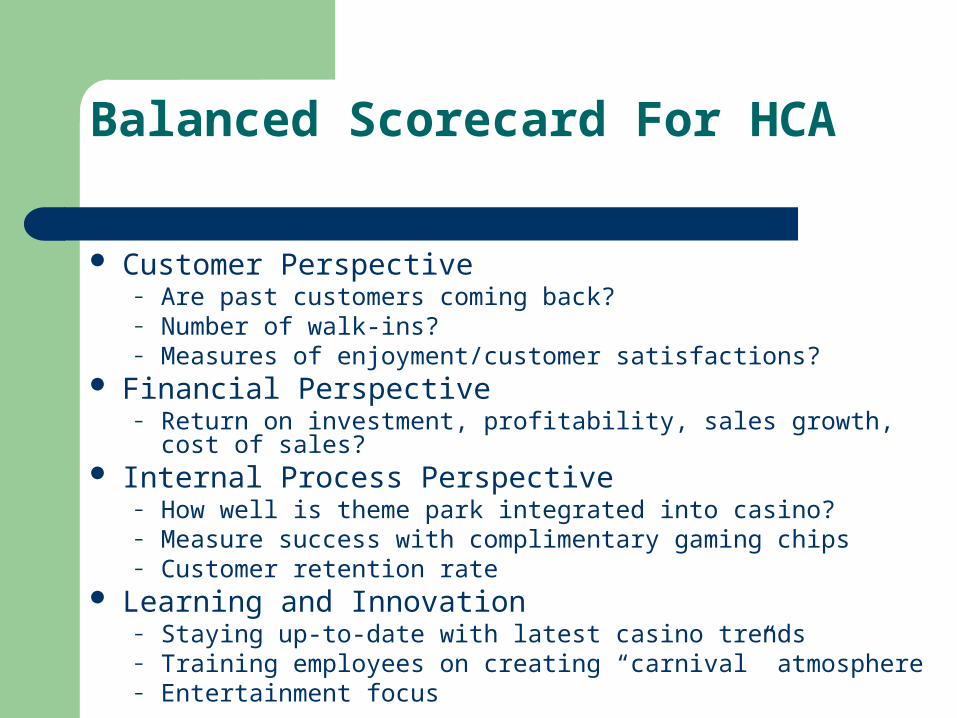

Balanced Scorecard For HCA

Customer Perspective– Are past customers coming back?– Number of walk-ins?– Measures of enjoyment/customer satisfactions?

Financial Perspective– Return on investment, profitability, sales growth, cost of sales?

Internal Process Perspective– How well is theme park integrated into casino?– Measure success with complimentary gaming chips– Customer retention rate

Learning and Innovation– Staying up-to-date with latest casino trends– Training employees on creating “carnival” atmosphere– Entertainment focus