Embed Size (px)

Citation preview

1

Gresham Mining Services Quarterly

Chris Branston

We are pleased to present Edition 16 of the Gresham Mining Services Quarterly (GMSQ), a snapshot of the performance, news and trends across the resources (including oil & gas) services sector.

The Gresham Mining Services Index (GMSI) increased by 15.9% during the March 2016 quarter, the largest improvement since the September 2013 quarter. The positive start to 2016 was driven by the strong performance of the larger companies, particularly CIMIC, which recorded a 43% share price increase. Small companies generally continued to struggle, with 12 of the 18 sub-$50m market capitalisation businesses subject to share price falls during the period.

For companies that performed well, we believe there have been two main contributing factors:

1. A modest increase in commodity prices. Iron ore, oil and base metals have bounced from their lows in December/January, and the gold price continued to be strong with global uncertainty. There has also been some capital raising activity by gold juniors, providing hope for additional spending and new projects.

2. The first half reporting season showed that while mining services earnings were generally lower than 1H FY15, there are some signs that conditions are stabilising and the restructuring activities of 2014-2015 are starting to yield benefits. This was most evident for mining contractors, with results for Ausdrill, Macmahon, NRW, and Mineral Resources well received.

Earnings multiples ticked up on average, reflecting the share price increases. While equity values improved (off a low base), the consensus view is that the challenging environment will continue for some time, with fewer available construction contracts and fierce competition for production services.

Balance sheets are generally in reasonable shape, but a number of the more highly geared companies are pursuing strategies to reduce debt. For those companies with cash, the focus in 2016 has been more on capital management than M&A (7 companies are currently undertaking on-market buybacks). However, we expect to see some further consolidation as companies seek additional cost savings through merger synergies.

In this edition’s Quarterly Focus, we look at a few examples of what ASX-listed services companies are doing on the technology and innovation front. With the automation trend being driven by the major miners and their global equipment suppliers, developing themes amongst service providers include use of wireless technology, real time analytics and energy efficiency. This trend will continue as the industry’s focus starts to turn from cost and capex cutting to improving productivity.

Editorial Team

Gresham Advisory Partners Ltd is a leading Australian mergers and acquisitions/corporate advisory business and one of Australia’s largest and highest ranking independent corporate advisors.

Edition 16

April 2016

(1) The Gresham Mining Services Index is a market capitalisation weighted index comprising 50 mining services companies selected by Gresham at the date of this report. Brad Hancock

Tom Waddell

2

Share Price Movements

GRESHAM MINING SERVICES INDEX CONSTITUENTS (DEC15 – MAR 16)

LEADERS & LAGGERS (SHARE PRICE) (DEC15 – MAR 16)

PERFORMANCE OVER TIME

PERFORMANCE RELATIVE TO S&P 200 INDICES (DEC15 – MAR 16)

Source: FactSet, IRESS.

2

Ranks

Mar Dec 31 Mar 16 31 Dec 15

1 1 CIMIC Group Ltd. (ASX:CIM) 11,460 8,226 43%

2 2 Orica Ltd. (ASX:ORI) 5,740 5,788 -1%

3 3 ALS Ltd. (ASX:ALQ) 2,012 1,901 6%

4 4 Downer EDI Ltd. (ASX:DOW) 1,637 1,551 7%

5 5 WorleyParsons Ltd. (ASX:WOR) 1,319 1,135 16%

6 6 Mineral Resources Ltd. (ASX:MIN) 1,123 753 50%

7 9 Monadelphous Group Ltd. (ASX:MND) 666 614 8%

8 7 Broadspectrum Ltd. (ASX:BRS) 607 717 -15%

9 10 UGL Ltd. (ASX:UGL) 518 405 28%

10 11 Tox Free Solutions Ltd. (ASX:TOX) 434 376 9%

11 8 Programmed Maintenance Services Ltd. (ASX:PRG) 369 616 -40%

12 13 Cardno Ltd. (ASX:CDD) 277 287 -3%

13 15 MACA Ltd. (ASX:MLD) 211 170 24%

14 12 RCR Tomlinson Ltd. (ASX:RCR) 193 307 -37%

15 16 Pacific Energy Ltd. (ASX:PEA) 155 146 6%

16 24 Ausdrill Ltd. (ASX:ASL) 151 80 90%

17 20 MMA Offshore Ltd. (ASX:MRM) 145 95 53%

18 17 GR Engineering Services Ltd. (ASX:GNG) 140 119 17%

19 18 Macmahon Holdings Ltd. (ASX:MAH) 135 109 26%

20 14 Decmil Group Ltd. (ASX:DCG) 131 178 -26%

21 23 Bradken Ltd. (ASX:BKN) 103 83 25%

22 19 Global Construction Services Ltd. (ASX:GCS) 94 99 -5%

23 25 Neptune Marine Services Ltd. (ASX:NMS) 84 77 10%

24 28 Boart Longyear Ltd. (ASX:BLY) 83 57 46%

25 21 AJ Lucas Group Ltd. (ASX:AJL) 81 94 -34%

26 26 Fleetwood Corp. Ltd. (ASX:FWD) 77 76 1%

27 29 Southern Cross Electrical Engineering Ltd. (ASX:SXE) 72 57 26%

28 22 RungePincockMinarco Ltd. (ASX:RUL) 69 83 -14%

29 47 NRW Holdings Ltd. (ASX:NWH) 60 24 150%

30 27 Alliance Aviation Services Ltd. (ASX:AQZ) 54 60 -10%

31 31 Lycopodium Ltd. (ASX:LYL) 54 48 11%

32 30 Imdex Ltd. (ASX:IMD) 53 50 8%

33 32 SRG Ltd. (ASX:STS) 47 48 -2%

34 34 OTOC Ltd. (ASX:OTC) 45 46 -3%

35 38 Ausenco Ltd. (ASX:AAX) 45 41 9%

36 33 Saunders International Ltd. (ASX:SND) 43 46 -9%

37 36 Boom Logistics Ltd. (ASX:BOL) 37 44 -16%

38 48 Tempo Australia Ltd. (ASX:TPP) 36 23 54%

39 43 Swick Mining Services Ltd. (ASX:SWK) 36 27 32%

40 37 Matrix Composites & Engineering Ltd. (ASX:MCE) 31 42 -26%

41 35 LogiCamms Ltd. (ASX:LCM) 30 44 -33%

42 40 Mitchell Services Ltd. (ASX:MSV) 26 28 -10%

43 44 Austin Engineering Ltd. (ASX:ANG) 25 27 -9%

44 51 Hughes Drilling Ltd. (ASX:HDX) 23 19 22%

45 45 Brierty Ltd. (ASX:BYL) 23 25 -10%

46 49 VDM Group Ltd. (ASX:VMG) 22 19 -

47 41 XRF Scientific Ltd. (ASX:XRF) 21 27 -22%

48 39 Onterran Ltd. (ASX:OTR) 18 30 -40%

49 46 Emeco Holdings Ltd. (ASX:EHL) 17 25 -29%

50 52 McAleese Ltd. (ASX:MCS) 16 14 16%

Market Cap (A$m) Share

price chg

%

Company

-4%-4%

16%

5%5%5%3%2%

0%-2%-3%-3%-4%

-6%-11%

All

Ord

inar

ies

S&P

/ASX

20

0

GM

SI

A-R

EIT

Indu

stri

als

Uti

litie

s

Mat

eria

ls

Res

ou

rces

Con

s. D

isc.

Hea

lth

Car

e

Ener

gy

Telc

o S

ervi

ces

Con

s. S

tapl

esIT

Fina

ncia

l-x-A

-RE

IT

20

40

60

80

100

120

Mar13 Sep13 Mar14 Sep14 Mar15 Sep15 Mar16

Gresham Mining Services Index (GMSI)

S&P/ASX 200

S&P/ASX 200 Resources

GMSI (excl. top 5)

150%

90%

54% 53% 50%

-33% -33% -37% -40% -40%

NR

W

Au

sdri

ll

Tem

po

MM

A O

ffsh

ore

Min

eral

Res

ou

rces

Logi

Cam

ms

AJ

Luca

s

RC

R T

om

linso

n

Pro

gram

me

d

On

terr

an

Leaders Laggers

3

Large Cap (>$1bn) Mid Cap (between $200m and $1bn) Small Cap (<$200m)

Notes: (1) Share price reaction based on closing price on the first full trade day post results announcement and closing price on the last trade day prior to announcement. Source: FactSet, Company announcements.

1H FY16 Results Wrap

Median sector revenue fell during 1H FY16, with only 15 companies recording revenue growth over the prior corresponding period. The trend for EBITDA was similar, with median margins falling slightly relative to 1H FY15. Share price reactions to the first half results were mixed. The results of a number of mining contractors (eg NRW, Ausdrill, Mineral Resources and Macmahon) were well received.

REPORTED REVENUE GROWTH (1H16 VS 1H15)

REPORTED EBITDA GROWTH (1H16 VS 1H15)

3

SHARE PRICE REACTION (1 DAY PRIOR)

CHANGE IN EBITDA MARGINS (1H16 VS 1H15)

(30%)

(20%)

(10%)

0%

10%

20%

30%

NW

H

ASL

VM

G

MIN

MSV

UG

L

OTC

CIM

DO

W

BR

S

MA

H

TOX

SWK

BO

L

MN

D

LYL

TPP

OR

I

AJL

CD

D

ALQ

GC

S

NM

S

SXE

RU

L

AQ

Z

IMD

HD

X

OTR

EHL

MC

S

STS

PEA

FWD

SND

AN

G

MR

M

BYL

PR

G

MC

E

GN

G

BLY

XR

F

BK

N

WO

R

AA

X

DC

G

MLD

RC

R

LCM

v

(100%)

(80%)

(60%)

(40%)

(20%)

0%

20%

40%

60%

OTR TP

P

OTC

MSV

MIN

GN

G

GC

S

ASL

PEA

IMD

FWD

SWK

LYL

ALQ

CD

D

PR

G

OR

I

TOX

EHL

BR

S

DO

W

UG

L

SXE

NM

S

WO

R

AN

G

BYL

BLY ST

S

XR

F

AQ

Z

RU

L

RC

R

LCM

SND

HD

X

BK

N

MC

E

MC

S

CIM

AA

X

AJL

BO

L

MN

D

MR

M

MLD

MA

H

DC

G

NW

H

VM

G

v

Median: -6%

(100%)

(80%)

(60%)

(40%)

(20%)

0%

20%

40%

60%

OTC

NW

H

AN

G

EHL

AJL

PEA BR

S

TOX

GN

G

ASL

SWK

GC

S

ALQ

UG

L

MIN

CIM

NM

S

PR

G

DO

W

BYL ST

S

LYL

OR

I

HD

X

BK

N

AQ

Z

SXE

MN

D

RC

R

XR

F

BO

L

WO

R

SND

MC

E

MLD

MR

M

IMD

CD

D

FWD

MA

H

DC

G

BLY

RU

L

AA

X

v

Median: -13%

(10%)

(8%)

(6%)

(4%)

(2%)

0%

2%

4%

6%

8%

10%

NW

H

OTC AJL

EHL

AN

G

PEA

TOX

CIM

HD

X

BR

S

UG

L

NM

S

ALQ

SWK

BK

N

PR

G

ASL

STS

BYL

DO

W

MN

D

LYL

MA

H

SXE

GN

G

RC

R

BO

L

WO

R

AQ

Z

OR

I

GC

S

BLY

RU

L

MLD

DC

G

MIN

MC

E

SND

MR

M

CD

D

XR

F

FWD

IMD

v

Median: -0.6%

4

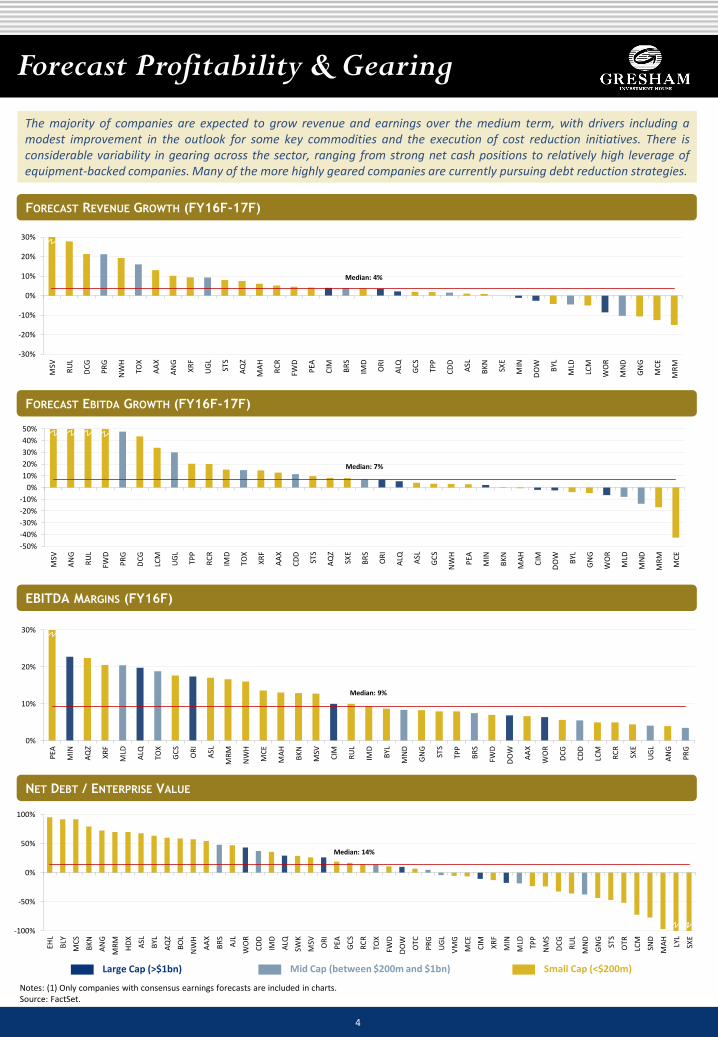

Forecast Profitability & Gearing

The majority of companies are expected to grow revenue and earnings over the medium term, with drivers including a modest improvement in the outlook for some key commodities and the execution of cost reduction initiatives. There is considerable variability in gearing across the sector, ranging from strong net cash positions to relatively high leverage of equipment-backed companies. Many of the more highly geared companies are currently pursuing debt reduction strategies.

4

FORECAST REVENUE GROWTH (FY16F-17F)

FORECAST EBITDA GROWTH (FY16F-17F)

Large Cap (>$1bn) Mid Cap (between $200m and $1bn) Small Cap (<$200m)

Notes: (1) Only companies with consensus earnings forecasts are included in charts. Source: FactSet.

EBITDA MARGINS (FY16F)

NET DEBT / ENTERPRISE VALUE

0%

10%

20%

30%

PEA

MIN

AQ

Z

XR

F

MLD

ALQ

TOX

GC

S

OR

I

ASL

MR

M

NW

H

MC

E

MA

H

BK

N

MSV

CIM

RU

L

IMD

BYL

MN

D

GN

G

STS

TPP

BR

S

FWD

DO

W

AA

X

WO

R

DC

G

CD

D

LCM

RC

R

SXE

UG

L

AN

G

PR

GMedian: 9%

-100%

-50%

0%

50%

100%

EHL

BLY

MC

S

BK

N

AN

G

MR

M

HD

X

ASL

BYL

AQ

Z

BO

L

NW

H

AA

X

BR

S

AJL

WO

R

CD

D

IMD

ALQ

SWK

MSV OR

I

PEA

GC

S

RC

R

TOX

FWD

DO

W

OTC

PR

G

UG

L

VM

G

MC

E

CIM XR

F

MIN

MLD

TPP

NM

S

DC

G

RU

L

MN

D

GN

G

STS

OTR

LCM

SND

MA

H

LYL

SXE

Median: 14%

-30%

-20%

-10%

0%

10%

20%

30%

MSV

RU

L

DC

G

PR

G

NW

H

TOX

AA

X

AN

G

XR

F

UG

L

STS

AQ

Z

MA

H

RC

R

FWD

PEA

CIM BR

S

IMD

OR

I

ALQ

GC

S

TPP

CD

D

ASL

BK

N

SXE

MIN

DO

W

BYL

MLD

LCM

WO

R

MN

D

GN

G

MC

E

MR

M

Median: 4%

-50%

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

MSV

AN

G

RU

L

FWD

PR

G

DC

G

LCM

UG

L

TPP

RC

R

IMD

TOX

XR

F

AA

X

CD

D

STS

AQ

Z

SXE

BR

S

OR

I

ALQ ASL

GC

S

NW

H

PEA

MIN

BK

N

MA

H

CIM

DO

W

BYL

GN

G

WO

R

MLD

MN

D

MR

M

MC

E

Median: 7%

5 Notes: (1) Only companies with consensus earnings forecasts are included in charts; (2) Share prices are as at 31 Mar 2016; (3) Earnings multiples are not calendarised; (4) Companies exhibiting negative multiples have been excluded from the above analysis. Source: FactSet.

Valuation Multiples

PE multiples are currently sitting slightly above the long term median, and have generally trended up since the September 2015 quarter. This has been driven by a combination of recent share price improvements and continued resetting of analyst earnings expectations.

1 YEAR FORWARD PRICE EARNINGS RATIO OVER TIME

PRICE EARNINGS RATIO (FY16F)

5

Large Cap (>$1bn) Mid Cap (between $200m and $1bn) Small Cap (<$200m)

DIVIDEND YIELD (FY16F)

2x

4x

6x

8x

10x

12x

14x

16x

18x

Mar 08 Sep 08 Mar 09 Sep 09 Mar 10 Sep 10 Mar 11 Sep 11 Mar 12 Sep 12 Mar 13 Sep 13 Mar 14 Sep 14 Mar 15 Sep 15 Mar 16

Gresham Mining Services PER

All Ordinaries Index PER

Gresham Mining Services Median

Gresham Mining Services Median: 9.3x

-

5x

10x

15x

20x

25x

AA

X

MSV

CIM

ALQ

TOX

CD

D

SXE

DC

G

MC

E

OR

I

UG

L

MIN

PEA

RU

L

DO

W

PR

G

LCM

MN

D

RC

R

STS

WO

R

GN

G

ASL

XR

F

NW

H

BR

S

GC

S

MLD

TPP

BK

N

AQ

Z

BYL

Median: 9.9x

0%

2%

4%

6%

8%

10%

12%

14%

HD

X

GC

S

GN

G

MLD

MN

D

PR

G

SXE

DO

W

PEA OR

I

AQ

Z

STS

DC

G

MIN

ALQ

TOX

BR

S

CIM

FWD

XR

F

RC

R

ASL

Median: 5.5%

1-yr fwd median as at: Mar 15: 9.1x (FY15) Jun 15: 9.5x (FY16) Sep 15: 9.2x (FY16) Dec 15: 9.5x (FY16)

1-yr fwd median as at: Mar 15: 5.8% (FY15) Jun 15: 6.0% (FY16) Sep 15: 6.7% (FY16) Dec 15: 6.8% (FY16)

6

Notes: (1) Only companies with consensus earnings forecasts are included in charts; (2) Share prices are as at 31 Mar 2016; (3) Earnings multiples are not calendarised; (4) Enterprise Value is based on market capitalisation plus minority interests and last reported net debt adjusted for capital raisings and acquisitions. (5) Companies exhibiting negative multiples have been excluded from the above analysis. Source: FactSet.

Valuation Multiples

Forecast EBIT and EBITDA multiples have also edged upwards, currently sitting at 7.3x and 4.6x respectively. A significant number of companies continue to trade below reported NTA.

EV/EBIT (FY16F)

EV/EBITDA (FY16F)

6

Large Cap (>$1bn) Mid Cap (between $200m and $1bn) Small Cap (<$200m)

PRICE/NTA

-

5x

10x

15x

20x

MA

H

MSV

ALQ

IMD

CD

D

AA

X

CIM

TOX

OR

I

RU

L

ASL

BK

N

DC

G

PEA

WO

R

MC

E

MIN

RC

R

UG

L

DO

W

NW

H

AQ

Z

BR

S

PR

G

XR

F

LCM

MN

D

GC

S

SXE

GN

G

STS

TPP

BYL

MLD

Median: 7.3x

v

-

2x

4x

6x

8x

10x

ALQ

AN

G

MSV OR

I

CIM

CD

D

TOX

RU

L

WO

R

MR

M

AA

X

PEA

UG

L

DC

G

IMD

BK

N

PR

G

GN

G

XR

F

RC

R

TPP

MN

D

BR

S

FWD

MIN

DO

W

ASL

GC

S

AQ

Z

LCM

NW

H

SXE

BYL ST

S

MA

H

MC

E

MLD

Median: 4.6x

v

0%

100%

200%

300%

400%

AA

X

VM

G

UG

L

OR

I

TOX

CD

D

TPP

CIM

GN

G

OTR

OTC

PR

G

SND

RU

L

BR

S

MN

D

DO

W

RC

R

LCM

PEA XR

F

MSV AJL

NM

S

MIN LY

L

SXE

MLD ST

S

DC

G

MA

H

GC

S

FWD

IMD

BK

N

AQ

Z

NW

H

SWK

MC

S

BYL

AN

G

HD

X

ASL

MC

E

BO

L

MR

M

EHL

Median: 112% Companies trading at a discount to NTA

1-yr fwd median as at: Mar 15: 6.7x (FY15) Jun 15: 7.5x (FY16) Sep 15: 6.8x (FY16) Dec 15: 6.2x (FY16)

1-yr fwd median as at: Mar 15: 4.4x (FY15) Jun 15: 4.2x (FY16) Sep 15: 3.9x (FY16) Dec 15: 4.0x (FY16)

7

Contract Awards

7

MAJOR CONTRACT AWARDS

Very few major contracts were awarded in the first quarter. One of the most significant domestic jobs awarded was Maca’s $115m contract to provide open pit mining services at Regis Resources’ Moolart Well Project.

Ausdrill and Ausenco secured offshore work during the period, with the latter awarded preferred contractor status for a $89m EPC contract at Atlantic Gold’s Moose River gold project in Nova Scotia, Canada.

Notes: (1) Contract awarded to African Underground Mining Services, in which Ausdrill holds a 50% interest Source: Company announcements.

Date

Announced Company Client Project/Facility Location Services Value (A$m) Commodity

29 Mar 16 Hughes Drilling Ramelius Resources Mt Magnet WA Grade control drilling n/a Gold

29 Mar 16 Hughes Drilling South32 Boddington WA Blast hole drilling n/a Bauxite

24 Mar 16 Swick Independence Group Jaguar / Nova WA Underground diamond

drilling n/a Nickel

11 Mar 16 Macmahon Moreton Resources South Burnett QLD Mining services n/a Coal

3 Mar 16 GR Engineering Vimy Resources Mulga Rock WA Feasibility Study n/a Uranium

24 Feb 16 Ausenco Atlantic Gold Moose River Canada EPC 89 Gold

24 Feb 16 Pacific Energy Doray Minerals Deflector WA BOO of power station n/a Gold

23 Feb 16 Toxfree BHP Olympic Dam SA Industrial services & total

waste management n/a Copper

17 Feb 16 SCEE SCJV Jimblebar WA E&I services 10 Iron Ore

12 Feb 16 Alliance Aviation Santos Cooper Basin SA Jet transport services n/a O&G

11 Feb 16 GR Engineering Gold Road Gruyere WA Feasibility Study n/a Gold

8 Feb 16 NRW Golding Contractors Isaac Plains QLD Drill and Blast services 40 Coal

4 Feb 16 Mitchell Services South32 Cannington WA Surface / Underground

mining 14 Silver / Lead

28 Jan 16 Ausdrill1 AngloGold Ashanti Geita Gold Mine Tanzania Underground mining US$70 Gold

19 Jan 16 GR Engineering Dacian Gold Mt Magnet WA Feasibility Study n/a Gold

12 Jan 16 Decmil QGC Pty Ltd Various QLD Wellsite installation 35 CSG

7 Jan 16 Ausenco Golding Contractors Isaac Plains QLD Plant operations and

maintenance 15 Coal

7 Jan 16 Ausenco Unknown NSW coal facility NSW Plant upgrade 17 Coal

4 Jan 16 Maca Regis Resources Moolart Well WA Open pit mining 115 Gold

8

Corporate Activity

8

Despite a quiet start to the year for corporate activity, foreign interest in the sector continued. German underground mining and construction company DYWIDAG-Systems acquired Jenmar Australia, whilst French electrical engineering group VINCI Energies acquired J&P Richardson, a Brisbane-based E&I contractor.

A number of companies continue share repurchases, with likely motivators perceived share price weakness and caution around allocating capital to acquisitions.

Date Announced

Status Target Business Target

HQ Seller Acquirer

Value (A$m) Forum

Interest (%)

Cons.

24 Mar 16 Completed Scope Australia EPC (Res / Infra) WA n/a Decmil 1.7 Private 100% Cash

17 Mar 16 Completed DT HiLoad Truck tray manufacturing WA Ausdrill Schlam

Engineering 2.6 Private 100% Cash

11 Feb 16 Completed Sedgman Minerals processing QLD n/a CIMIC 119 Public 100% Cash

8 Feb 16 Completed J&P Richardson Electrical engineering QLD Founders VINCI Energies n/a Private 100% Cash

2 Feb 16 Completed Jenmar Australia Ground control products NSW Jenmar Corp DYWIDAG-

Systems n/a Private 100% Cash

7 Jan 16 Completed Broadsword

Marine Offshore support services WA Programmed

Bhagwan Marine

25 Private 100% Cash

MERGERS & ACQUISITIONS

CAPITAL RAISINGS

Date Announced

Status Company Type Amount Raised

(A$m)

(Discount) / Premium to

Last Price (%) Purpose Underwritten

21 Mar 16 Completed Toxfree Placement / SPP 24 1.9% Acquisition funding Yes

17 Mar 16 Completed AJ Lucas Entitlement Offer 21.1 16% Debt repayment & working

capital Yes

Source: Mergermarket, company announcements.

ACTIVE SHARE BUYBACKS

Date Announced Company Type Size Purpose

14 Dec 15 CIMIC On-market Up to 10% Improve shareholder returns and enhance

capital efficiency

4 Dec 15 RCR Tomlinson On-market Up to 2m shares Capital management

30 Nov 15 Swick On-market Up to 10% Capital management

20 Nov 15 RungePincockMinarco On-market Up to 10% Capital management

19 Nov 15 Mineral Resources On-market Up to 10% Capital management

6 Oct 15 Macmahon On-market Up to 10% Capital management

20 Aug 15 Downer EDI On-market Up to 43m shares Capital management

9 Note: (1) Excludes alternate appointments; (2) Internal appointment. Source: Company announcements.

Executive Movements

EXECUTIVE & DIRECTOR APPOINTMENTS1

Date Announced Company Name Role Date Effective

11 Mar 16 Cardno Robert Prieto NED Not Stated

11 Mar 16 Cardno Gary Jandegian NED Not Stated

9 Mar 16 NRW Michael Arnett2 Chairman 9 Mar 16

29 Feb 16 Onterran Lachlan McIntosh2 Executive Chairman 1 Mar 16

17 Feb 16 Austin Engineering Peter Pursey2 Executive Chairman Not Stated

15 Feb 16 Bradken Paul Zuckerman CEO 1 Mar 16

3 Feb 16 Programmed Lisa Paul NED 3 Feb 16

1 Feb 16 VDM Sam Diep CEO & MD 29 Feb 16

29 Jan 16 Boart Longyear Philip Mackey2 Company Secretary Not Stated

28 Jan 16 Cardno Steven Sherman NED 27 Jan 16

28 Jan 16 Cardno Jeffrey Forbes NED 27 Jan 16

22 Jan 16 CIMIC Louise Griffiths2 Company Secretary Not Stated

13 Jan 16 Lycopodium Steven Chadwick NED Not Stated

9

EXECUTIVE & DIRECTOR RESIGNATIONS / RETIREMENTS

Date Announced Company Name Role Date Effective

31 Mar 16 ALS Nerolie Withnall NED & Chairman 26 July 16

29 Feb 16 Onterran Heather Gardner CEO 29 Feb 16

24 Feb 16 Brierty Alan Brierty NED Not Stated

17 Feb 16 Austin Engineering Michael Buckland CEO & MD 30 Jun 16

1 Feb 16 VDM Dongyi Hua CEO & MD 28 Feb 16

29 Jan 16 Boart Longyear Paul Blewett Company Secretary Not Stated

22 Jan 16 CIMIC John Easy Company Secretary Not Stated

10

Quarterly Focus: Technology & Innovation

10

The world has seen significant technological advancements that have transformed many industries over the last 50 years. However, the hard-rock mining sector has long been regarded as lagging in major innovation. This has been attributed to a number of factors, including:

1. Inherent existing risks in developing new mines (orebody uncertainty, commodity price) making the further risks of new and unproven technologies intolerable;

2. The profits generated during good periods making it hard to justify downtime required to implement new technology; and

3. The information challenges associated with moving and metering non-homogenous solids (as opposed to liquids and gases in the oil and gas sector).(1)

It has been estimated that the mining and metals sector spends 90% less on technology and innovation than the petroleum sector as a ratio of revenue.(2)

But this trend is changing, with the large mining companies and their equipment suppliers investing heavily in research and development, clearly illustrated in remote control centres and autonomous trucks and trains at major projects. Mining services companies are also increasingly playing their part, adopting current technology and new processes to improve safety and productivity. This is likely to become more evident as we enter the next phase of the commodity cycle. Having been through the early stages of the downturn involving cost cutting and capital restrictions, we are now reaching the stage where companies will invest in making tasks and processes more efficient.

Below are a few examples of new technologies currently being marketed by ASX-listed services companies.

Company Current Innovation Initiatives

Orica Orica has developed the world’s first commercial wireless electronic blasting system.

The company notes that the requirement to manage wires and connections in current initiation systems is the last remaining barrier to remotely managing all of the drill and blast cycle. Wireless blasting presents opportunities for “non-entry mining methods, automating the blasting process, improving cycle times, and recovering ore locked in pillars or blocks that would otherwise be stranded”.

Mineral Resources

Mineral Resources is investing in a range of technologies, including:

its Bulk Ore Transportation System (BOTSTM) encompassing an elevated below rail structure, which reduces required earthworks and involves less disturbance to natural landscapes;

carbon fibre structural components which have significant weight saving advantages over steel products; and

LNG and solar power at remote mine sites.

Imdex Imdex has developed cloud-based data collection and analysis software (Reflex Hub). The platform transfers data from the company’s instruments and mobile devices and runs analytics that can be accessed anywhere. This enhances data accuracy and provides real-time or near-real time information to assist in decision making.

Emeco Emeco has developed a fleet management platform called Emeco Operating System (EOS). EOS provides insight down to individual assets, operators or materials and allows clients to measure fleet payload performance, dig rates, operational efficiency and time utilisation detail.

EOS is designed to be a cost effective tool to provide smaller miners with access to information and analysis that helps drive productivity improvements. The system’s first client, junior miner Alkane Resources, has achieved unit cost reductions for the load and haul system of c.20%.

Note: (1) For further discussion, see Andrew Shook, “Innovation in mining”, AUSIMM Bulletin, April 2015; (2) Ernst & Young, “Mining uncovered: The role of innovation in mining”, September 2015.

11

Gresham’s Credentials

LANDMARK MERGERS & ACQUISITIONS

TAKEOVER DEFENCE

STRATEGIC ADVISORY, JOINT VENTURES AND CAPITAL MARKETS

Advised Little World Beverages on its acquisition

by Lion

Advised Magma

Metals in relation to the

unsolicited takeover offer

from Panoramic Resources

Advised David

Jones in relation to acquisition by

Woolworths

Advised LinQ Capital on its acquisition by IMC Resources

Holdings

Advised BHP Billiton on its proposed iron ore production joint venture with Rio Tinto

Introduced

Denham Capital to Trans Tasman

Resources resulting in NZ

iron sands investment

Advised BHP Billiton on the disposal of the Yabulu Nickel

refinery

Advised

Bannerman Resources on its

financing with Resource Capital

Funds

Advised Iluka on its institutional placement and

accelerated rights issue

Advised Boral on its joint venture

with USG Corporation

AWARDS & ACCOLADES

2011 M&A Deal of the Year

SABMiller’s

acquisition of Foster’s Group

2009 Most

Innovative Deal

Babcock & Brown

Infrastructure’s recapitalisation

Secondary Market Equity Raising of

the Year

Wesfarmers’ $2.6bn equity

raising

2007 Best M&A

Deal

Wesfarmers’ acquisition of

Coles

Best M&A Deal

in Australia

Wesfarmers’ acquisition of

Coles

Advised Foster’s on the demerger

of its wine business

2011

Joint lead adviser to Japan Post on the acquisition of

Toll Holdings

2015

2012

Advised Coffey in

relation to acquisition by

Tetra Tech

2014

Advised Clough

in relation to acquisition by

Murray & Roberts

2013 2012

2010 2010 2009 2008 2009/08 2013

2013

Advised Platinum Equity in relation to the acquisition of a 70% stake in

the Sensis directories

business from Telstra

2014

Advised Wesfarmers on the sale of its

underwriting and insurance broking

businesses

2014

Advised Bank of Queensland on

the acquisition of loan portfolio from Investec

2014

Excellence in Corporate

Advisory - 2012

Boutique / Independent

Lead

Independent financial adviser to the Board of BHP Billiton on

the demerger of South32

2015

2015

12

Contact Details

Gresham Advisory Partners Limited ABN 88 093 611 413

Level 17, 167 Macquarie Street

Sydney NSW 2000

Telephone: +61 2 9221 5133

Facsimile: +61 2 9221 6814

Level 39, 120 Collins Street

Melbourne VIC 2000

Telephone: +61 3 9664 0300

Facsimile: +61 3 9650 7722

Level 3, 28 The Esplanade

Perth WA 6000

Telephone: +61 8 9486 7077

Facsimile: +61 8 9486 7024

www.gresham.com.au

Michael Lishman Managing Director, Perth E: [email protected] T: +61 8 9213 0289

Terms and Conditions Information contained in this publication The opinions, advice, recommendations and other information contained in this publication, whether express or implied, are published or made by Gresham Advisory Partners Limited (ABN 88 093 611 413), Australian financial services license (247113), and by its officers and employees (collectively “Gresham Advisory Partners”) in good faith in relation to the facts known to it at the time of preparation. Gresham Advisory Partners has prepared this publication without consideration of the investment objectives, financial situation or particular needs of any individual investor, and you should not rely on the publication for the purpose of making a financial decision. To whom this information is provided This publication is only made available to persons who are wholesale clients within the meaning of section 761G of the Corporations Act 2001. This publication is supplied on the condition that it is not passed on to any person who is a retail client within the meaning of section 761G of the Corporations Act 2001. Disclaimer and limitation of liability To the maximum extent permitted by law, Gresham Advisory Partners will not be liable in any way for any loss or damage suffered by you through use or reliance on this information. Gresham Advisory Partners’ liability for negligence, breach of contract or contravention of any law, which cannot be lawfully excluded, is limited, at Gresham Advisory Partners’ option and to the maximum extent permitted by law, to resupplying this information or any part of it to you, or to paying for the resupply of this information or any part of it to you. No warranties made as to content Gresham Advisory Partners makes no warranty, express or implied, concerning this publication. The publication provided by us on an “AS IS” basis at your sole risk. Gresham Advisory Partners expressly disclaims, to the maximum extent permitted by law, any implied warranty of merchantability or fitness for a particular purpose, including any warranty for the use or the results of the use of the publication with respect to its correctness, quality, accuracy, completeness, or reliability. Copyright Copyright in this publication is owned by Gresham Advisory Partners. You may use the information in this publication for your own personal use, but you must not (without Gresham Advisory Partners’ consent) alter, reproduce or distribute any part of this publication, transmit it to any other person or incorporate the information into any other document. General matters These Terms and Conditions are governed by the law in force in the State of Victoria, and the parties irrevocably submit to the non-exclusive jurisdiction of the courts of Victoria and courts of appeal from them for determining any disputes concerning the Terms and Conditions. If the whole or any part of a provision of these Terms and Conditions are void, unenforceable or illegal in a jurisdiction it is severed for that jurisdiction. The remainder of the Terms and Conditions have full force and effect and the validity or enforceability of that provision in any other jurisdiction is not affected. This clause has no effect if the severance alters the basic nature of the Terms and Conditions or is contrary to public policy. If Gresham Advisory Partners do not act in relation to a breach by you of these Terms and Conditions, this does not waive Gresham Advisory Partners’ right to act with respect to subsequent or similar breaches.

Chris Branston Executive Director, Perth E: [email protected] T: +61 8 9213 0290

Matt Keenan Managing Director, Melbourne E: [email protected] T: +61 3 9664 0353

Charlie Graham Managing Director, Sydney E: [email protected] T: +61 2 9224 0247

Michail Lagogiannis Executive Director, Melbourne E: [email protected] T: +61 3 9664 0375

Neville Spry Managing Director, Sydney E: [email protected] T: +61 2 9224 0237