Embed Size (px)

DESCRIPTION

Key market indicators from Greater Toronto Area's office real estate market including vacancies, rents and absorption.

Citation preview

www.colliers.com/toronto

FALL 2011 | OFFICE

Canadian Market Overview The Canadian economy is once again outperforming many of its peers. While this is an enviable position, the question remains: will Canada be able to navigate the global economic headwinds and sidestep either a noticeable slowdown or recession?

Commercial real estate has weathered the recent storm and is well positioned for any softening of the economy. Office markets have largely digested the new inventory that was delivered in the past 24 months and are moving towards healthy levels of occupancy. One area that appears somewhat exposed should the global economy enter a protracted downturn is the industrial property class, which in many markets is tied closely to import and export activity. There are mixed signals on both import and export activity levels. Exports have recently reported gains, however the slowing United States economy points to a pullback from our largest customer. The most recent jobs report from the U.S. has further demonstrated the fragility of their economy and will likely hurt U.S. consumer confidence, and hence retail activity. Imports are also in positive territory in the most recent releases, but some caution is warranted as the Canadian Consumer Confidence Index has retreated slightly in July, which may point to a future softening of retail sales and, of greater concern, housing activity. Retail activity is a driver of warehouse and distribution facility demand in many markets, pointing to a reduction in demand for that property type if retail spending is reduced. On a positive note, Canadian businesses appear bullish on future prospects and have started to make capital investments in machinery and equipment, boosting imports in those areas. The outlook appears to call for slow and steady performance in the near term, with a return to moderate growth as external economic variables are stabilized.

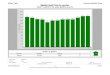

Greater Toronto Area Overview The last six months were no exception to the strong performance of the Greater Toronto Area (GTA) office market in 2011. Year-to-date demand for office space has exceeded annual levels dating back to 2001 and with over 5.2 million square feet of office space absorbed this year, available space has fallen by almost two percent to pre-recession levels. With 9 percent of GTA office space available—defined as available for lease and may be vacant or occupied—and 5.6 percent physically vacant, the availability rate is now below the ten year average of 10 percent. The strongest performing markets in 2011 thus far include Class A space in Midtown Toronto, Downtown Toronto, and GTA North, which contains Markham, Richmond Hill and Vaughan. The only market where the inventory of Class A availability has increased is in the Central East.

Notwithstanding the overall strong performance, a number of office nodes remain challenged with available space exceeding 12 percent, including the Class AAA towers in the Financial

toronto ontario

COLLIERS INTERNATIONAL | MARKET REPORT

MARKET INDICATORS

2011 Q2 2011 Q3

INVENTORY NET ABSORPTION VACANCY RATE

ASKING NET RENT

ADDITIONAL RENT

FORECAST

Net Absorption Asking Net Rent Vacancy Rate

Source: Colliers International, September 2011

Net A

bsor

ptio

n (1

00,0

00 S

F)

Aski

ng N

et R

ent (

$)/V

acan

cy R

ate

(%)

6

(10)

10

0

(12)

0

12

2001

3 4

(6)

1820

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4

2012

1 2 3

GTA Historical Performance & ForecastQ3 2001 - Q3 2012f

Net Absorption Asking Net Rent Vacancy Rate

GTA | HISTORICAL PERFORMANCE & FORECAST | Q3 2001 - Q3 2012F

GTA East

GTA North

GTA West

Central East

DowntownMidtown

Central West

Core, Class A space at Woodbine Avenue-Steeles Avenue East, Highway 404-Highway 7, Markham Town Centre, Scarborough Town Centre, Brampton, Burlington, Mississauga City Centre, the older inventory of buildings in Downtown South, Yonge Street-Eglinton Avenue, and the entire Consumers Road, Airport Corporate Centre and Oakville markets.

According to the Conference Board of Canada, the GTA will

experience positive, but slower economic growth in the next 12 to 24 months. Considering this, Colliers expects demand for office space to further slow down and delay anticipated office developments out into the future. By Q3 2012, vacancy is projected to decline from 5.6 percent to 5.0 percent, with rental rates increasing marginally from $15.77 per square foot to $16.27 per square foot.

P. 2 | COLLIERS INTERNATIONAL

MARKET REPORT | FALL 2011 | OFFICE | TORONTO

THE MARKET The largest and most prestigious office market in the GTA continues to be home to many global and national companies, primarily in the Finance, Insurance, Real Estate (FIRE) and business services sectors.

The commercial market has benefited from consistent growth in downtown condominium development as an expanding number of office workers are choosing to live downtown. Additionally, the increased service and popularity of Billy Bishop Toronto City Airport has contributed to the attractiveness of this market for business travelers given the location convenience and time savings.

TRENDSSince Q2 2011, available office space has decreased in the Downtown market from 9.1 percent to 8.2 percent, well below the 10 year average of 9.2 percent. Over the same time period, vacant unoccupied space declined

from 5.7 percent to 4.5 percent, down to less than four million square feet. While this indicated solid demand for office space, the rate of decline actually slowed compared to the period from Q4 2010 through to the beginning of 2011. All building classes experienced a decrease in available space, but the most in-demand were buildings of Class A quality and particularly new development in the submarkets of Downtown South, Financial Core and Downtown East.

In contradiction with supply and demand dynamics, weighted average asking net rents have trended downwards as a result of the successful lease up of higher cost new buildings in the market. The Downtown office market continues to expand to the east, west and south through conversion of existing stock and new development, demonstrating the continued demand for business proximity and access to services and transportation.

DowntownFORECAST Downtown Toronto is a vibrant area with an increasing resident population and retail service base. Colliers expects continued movement of firms from suburban markets to areas on the fringe of the Downtown Core, where new development opportunities exist that can cater to the needs of the “new generation” of employees. A recent example of this trend includes the announcement from Coca-Cola regarding their relocation to a new office development on the site formerly occupied by the Toronto Sun in Downtown East.

FORECAST

Net Absorption Asking Net Rent Vacancy Rate

Source: Colliers International, September 2011

Net A

bsor

ptio

n (1

00,0

00 S

F)

Aski

ng N

et R

ent (

$)/V

acan

cy R

ate

(%)

10

(8)

(4)

4

0

(20)

0

20

2001

3 4

(10)

30

8

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4

2012

1 2 3

Downtown Historical Performance & ForecastQ3 2001 - Q3 2012f

Net Absorption Asking Net Rent Vacancy Rate

GTA DOWNTOWN | HISTORICAL PERFORMANCE & FORECAST | Q3 2001 - Q3 2012F

COLLIERS INTERNATIONAL | P. 3

MARKET REPORT | FALL 2011 | OFFICE | TORONTOMARKET REPORT | FALL 2011 | OFFICE | TORONTO

Midtown THE MARKET Public space improvements such as the Bloor Street Transformation Project between Church Avenue and University Avenue, as well as RioCan’s proposed Yonge-Eglinton Centre revitalization adopting innovative urban design, will enhance location value in this market for both landlords and occupiers seeking an urban work environment. This market houses companies of all major office space utilizing industries: business services, FIRE and public administration.

TRENDSWith vacancy and availability fairly stable for more than two years, the Midtown market is now outperforming historic averages. Over the past two quarters, the overall availability rate remained at 7.1 percent of total inventory, or 1.3 million square feet. However, Class A vacancy has decreased by 2.0 percent from

year end 2010 to its current level of 4.6 percent, well below the 8.1 percent recorded in Q2 2010 . The decline was seen almost exclusively in Class A buildings, as there has been more vacant space marketed in Class B and C buildings compared to Q2 of this year. Older stock in the Bloor Street and Eglinton Avenue markets are showing signs of weakness with available space in Class C buildings in the mid teens.

The overall average asking net rent has increased slightly by less than $0.20 per square foot to $15.75 per square foot, and occupied space has expanded by 230,000 square feet over the course of the last two quarters. The combination of lower additional rent charges compared to the Downtown market, while still being able to offer direct subway access, makes Midtown an affordable and convenient office market.

FORECAST

Net Absorption Asking Net Rent Vacancy Rate

Source: Colliers International, September 2011

Net A

bsor

ptio

n (1

00,0

00 S

F)

Aski

ng N

et R

ent (

$)/V

acan

cy R

ate

(%)

(4)

(2)

0

(20)

0

10

2001

3 4

(10)

20

2

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4

2012

1 2 3

Midtown Historical Performance & ForecastQ3 2001 - Q3 2012f

Net Absorption Asking Net Rent Vacancy rate

MIDTOWN | HISTORICAL PERFORMANCE & FORECAST | Q3 2001 - Q3 2012F

FORECASTSlower growth of the GTA economy due to a stalled global recovery may dampen demand for office space in this market. However, there are a limited number of large, contiguous office space options of 20,000 square feet and above available in Midtown and as a result, Colliers expects vacancy and rent levels to remain fairly stable over the next twelve months.

P. 4 | COLLIERS INTERNATIONAL

MARKET REPORT | FALL 2011 | OFFICE | TORONTO

THE MARKET Characterized by office clusters along the Don Valley Parkway and the southern portion of Highway 404, the Central East market serves businesses seeking highway access with proximity to downtown. There is a lack of new office development in this market, particularly in the Don Mills Road-Eglinton Avenue East, Consumers Road and Duncan Mill Road office nodes as rental rates remain well below replacement cost.

TRENDSBoth overall vacancy at 6.0 percent and the availability rate at 9.7 percent have been at 10 year lows in this market due to strong absorption and sustained demand since the beginning of 2011.

Average asking net rent is at $11.89 per square foot, close to the $12.00 per square

foot level it has been hovering at for some time. Within Class A product, availability has increased over the past year to 11.4 percent; however this is still well below the 10 year average of 17.3 percent.

FORECASTThe Central East market may be gaining some momentum as congestion and higher costs in markets along the northern stretch of Highway 404 force tenants to consider other options. Bentall’s SteelesTechnology Campus Phase 3 will add a minimum of 250,000 square feet of newly occupied office space to the Central East market once a lead tenant for this design build opportunity has been identified.

Colliers is projecting stable vacancy rates in the Central East over the next twelve months, remaining above the 5.5 percent mark. Rent

GTA Central East

FORECAST

Net Absorption Asking Net Rent Vacancy Rate

Source: Colliers International, September 2011

Aski

ng N

et R

ent (

$)/V

acan

cy R

ate

(%)

Net A

bsor

ptio

n (1

00,0

00 S

F)

(4)

(2)

00

16

8

2001

3 4

(8)

(16)

2

4

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4

2012

1 2 3

Central East Historical Performance & ForecastQ3 2001 - Q3 2012f

Net Absorption Asking Net Rent Vacancy Rate

GTA CENTRAL EAST | HISTORICAL PERFORMANCE & FORECAST | Q3 2001 - Q3 2012F

levels are expected to marginally increase to levels last observed earlier in 2011 of $12.25 per square foot by Q3 2012.

COLLIERS INTERNATIONAL | P. 5

MARKET REPORT | FALL 2011 | OFFICE | TORONTOMARKET REPORT | FALL 2011 | OFFICE | TORONTO

GTA Central NorthTHE MARKET As one of the GTA’s smaller office markets, the Central North experiences less activity, most of which is centered in the largest submarket of the North Yonge Corridor.

The majority of companies in this market are part of the FIRE and public administration sector as they occupy more than 70 percent of office space combined.

TRENDSThe availability rate has decreased since Q2 2011 by 760,000 square feet, from 6.8 percent to 6.3 percent of the total inventory. This was caused by strong leasing in Class A buildings in the North Yonge Corridor which offset an increase in availability of Class B buildings in the Dufferin Street-Finch Avenue West submarket. Vacancy followed suit, decreasing from 4.9 percent to 4.4 percent.

Average asking net rent declined significantly to levels that had not been reported for more

than two years. Similar to the downtown market, this was not a function of landlords lowering their rental expectations, but rather a result of more expensive, higher quality space being leased up and therefore no longer included in this equation.

FORECASTWith no new supply scheduled and overall minimal demand for office space, Colliers anticipates that vacancy and rent levels will remain stable over the next twelve months in the Central North market.

FORECAST

Net Absorption Asking Net Rent Vacancy Rate

Source: Colliers International, September 2011

Net A

bsor

ptio

n (1

00,0

00 S

F)

Aski

ng N

et R

ent (

$)/V

acan

cy R

ate

(%)

(2)

0 0

16

2001

3 4

(16)

2

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4

2012

1 2 3

Central North Historical Performance & ForecastQ3 2001 - Q3 2012f

Net Absorption Asking Net Rent Vacancy Rate

GTA CENTRAL NORTH | HISTORICAL PERFORMANCE & FORECAST | Q3 2001 - Q3 2012F

P. 6 | COLLIERS INTERNATIONAL

MARKET REPORT | FALL 2011 | OFFICE | TORONTO

THE MARKET The GTA West market originated in the airport area around growing distribution and warehousing businesses. Today, office nodes are located across five different municipalities and clustered along highway corridors that provide exposure for tenants. Public transportation options are expanding, but available parking remains a precursor to the success of any development. Nevertheless, lower real estate costs, larger floor plates, and easy access to transportation infrastructure make this market an attractive option for many companies. As a testament to that, the growth of this market in the last 10 years has been led by new office developments in the Airport Corporate Centre, Meadowvale, the Hurontario Street Corridor, and Burlington submarkets.

TRENDSSince Q2 2011, availability has decreased from 12.2 percent to 11.5 percent or approximately 5.4 million square feet of office

space, compared to pre-recession lows of 7.7 percent recorded in 2007 and 2008. The most significant decreases in availability have been observed in the Airport Corporate Centre, Airport East and Highway 427-Bloor Street West-Islington Avenue submarkets. Less significant but notable decreases were seen Meadowvale and Brampton of 200,000 and 100,000 square feet respecitively.

A similar trend has been seen in vacancy, which has decreased from 8.4 percent to 7.5 percent or 3.6 million square feet, due to the absorption of almost 900,000 square feet over the last six months, primarily in the Airport Corporate Centre and Meadowvale. Despite decreases in availability and vacancy, some of the GTA West submarkets continue to post the highest availability and vacancy rates compared to all other GTA submarkets, specifically in Airport East, Airport Corporate Centre, Oakville and Meadowvale.

GTA West

FORECAST

Net Absorption Asking Net Rent Vacancy Rate

Source: Colliers International, September 2011

Net A

bsor

ptio

n (1

00,0

00 S

F)

Aski

ng N

et R

ent (

$)/V

acan

cy R

ate

(%)

(4)

0

4

0

12

2001

3 4 (12)

8

12

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4

2012

1 2 3

GTA West Historical Performance & ForecastQ3 2001 - Q3 2012f

Net Absorption Asking Net Rent Vacancy Rate

GTA WEST | HISTORICAL PERFORMANCE & FORECAST | Q3 2001 - Q3 2012F

The GTA West market’s average asking net rent has trended down marginally from $14.60 to $14.24 per square foot. Aside from the downtown market, the GTA West offers the most sublease options to companies looking for improved space, often at cost-effective rates.

FORECASTA minimal amount of planned new development should not noticeably influence the supply of available office space. With recent increased uncertainty in economic confidence, it may take longer than anticipated to pre-lease the proposed developments. The GTA West is most exposed to changes in economic conditions, particularly from the United States, due to the concentration of manufacturing, warehousing and distribution facilities. As a result, vacancy rates are likely to remain flat or increase during the next year given a continued period of slow or stagnant growth in the U.S.

COLLIERS INTERNATIONAL | P. 7

MARKET REPORT | FALL 2011 | OFFICE | TORONTOMARKET REPORT | FALL 2011 | OFFICE | TORONTO

Accelerating success.

GTA East

THE MARKET The GTA North market has been continuously quoting the lowest availability rate among all of the suburban markets and is the only suburban market to quote an availability rate below the GTA average of 9.0 percent.

TRENDSGTA North’s available office space decreased from 9.3 percent to 8.9 percent, amounting to 1.4 million square feet out of a total office inventory of 15 million square feet. The majority of the decreases occurred in the Highway 404-Highway 407 and Vaughan submarkets, which offset marginal increases in Richmond Hill and Markham Town Centre. Vacancy declined to 980,000 square feet, a marginal change from 6.4 percent to 6.3 percent.

www.colliers.com/toronto

Simultaneously, occupied space grew by almost 300,000 square feet, the same amount as in the GTA East market. On average, the GTA North market has had the highest suburban asking net rent, remaining stable at just below the $15.00 per square foot mark. Notably, on a percentage basis this market quoted one of the highest sublease availability rates at 27.6 percent of the available space. This amounted to approximately 400,000 square feet out of the 3.1 million square feet of available sublease space in the entire GTA.

FORECASTAbsorption is expected to remain positive over the next twelve months, although at a much slower pace of less than 50,000 square feet per quarter. As a result, vacancy is forecasted to decline further, causing rental rates to increase slightly.

GTA North

THE MARKET The GTA East is the smallest of all GTA office markets with about 5.6 million square feet of office space covering the Scarborough, Pickering and Oshawa submarkets. Most of the office space is occupied by companies in public administration, finance and data, publishing, and broadcasting services.

TRENDSConsistent with the trends of declining availability and vacancy in the rest of the GTA, this market has experienced some recent demand for office space and has seen occupied space expand by almost 300,000

square feet. Since Q2 2011, availability has decreased marginally to 550,000 square feet or 9.7 percent of total market inventory and vacancy has decreased to 5.5 percent or 310,000 square feet. Current available space has become more expensive than it was in Q2 2011 as average asking net rent increased by over $2.50 per square foot to $10.17 per square foot by the end of the third quarter..

FORECASTColliers expects the GTA East market vacancy to decline on a small scale but remain above the five percent mark in the coming year, while rental rates should increase marginally.

512 offices in 61 countries

• $1.5 billion* in revenue

• 12,000 employees

• 979 million square feet under management

• $59.6 billion* total transaction value

* USD based on 2010 results

This document has been prepared by Colliers International for advertising and general information only. Colliers International makes no guarantees, representations or warranties of any kind, expressed or implied, regarding the information including, but not limited to, warranties of content, accuracy and reliability. Any interested party should undertake their own inquiries as to the accuracy of the information. Colliers International excludes unequivocally all inferred or implied terms, conditions and warranties arising out of this document and excludes all liability for loss and damages arising there from. Colliers International is a worldwide affiliation of independently owned and operated companies. This publication is the copyrighted property of Colliers International and /or its licensor(s). © 2011. All rights reserved. Colliers Macaulay Nicolls (Ontario) Inc., Brokerage.

OUR SERVICES> Brokerage

• Landlord Representation • Tenant Representation

> Corporate Solutions

> Investment Services

> Project Management

> Real Estate Management Services

> Valuation & Advisory Services

> Residential Marketing & Sales Services

+1 416 777 2200

CONTACT INFORMATIONJohn Arnoldi Managing Director Toronto +1 416 643 3733 [email protected]

David Wood Managing Director, Sales Development & Research | Toronto+1 416 643 3419 [email protected]

For information on available properties, additional research reports, and our services please visit www.collierscanada.com/toronto

MARKET REPORT | FALL 2011 | OFFICE | TORONTO