Embed Size (px)

Citation preview

Graphite market report and forecast for Nouveau Monde Graphite October 2018

Prepared by Benchmark Mineral Intelligence

Introduction

• Nouveau Monde Graphite is developing the Matawinie Graphite production area in Quebec, Canada, for which it is preparing 43-101 report in order to support further financing.

• This report has been prepared for Nouveau Monde Graphite in order to assist with its financing efforts and presents Benchmarks independent forecasts for graphite demand, supply and pricing.

• The report will cover the following:

1. Introduction and Forecast Assumptions 2. Long Term Supply Forecasts for Natural Flake and Synthetic Graphite to 2040 3. Natural Flake Graphite Price Forecasts 4. Premium Graphite Markets Outlook and Prices

BENCHMARK MINERAL INTELLIGENCE – NOUVEAU MONDE GRAPHITE – OCTOBER 2018 Page 2

1. Introduction and Forecast Assumptions

1. Introduction and Forecast Assumptions

• This section will look at the current and future supply chain for graphite, with a focus on the burgeoning li-ion battery market. We will also highlight the current announcements and investments being made in the supply chain, including government policy, investment in battery manufacturing plants and announced investments from the automotive sector.

• We will also show our demand forecast methodology, flowing from government policy to EV penetration to battery demand and graphite consumption in Li-ion batteries and the outlook of other end-use markets.

• Graphite plays a critical role in the lithium-ion battery supply chain, as the main input for the anode material. At present roughly half of anode material is sourced from natural graphite, the other 50% comes from synthetic graphite, demand from this sector in 2018 is estimated at 161,000 tonnes.

• In terms of total graphite demand, our current base case shows graphite consumption increasing from 723,000 tonnes in 2018 to 1.9m tonnes in 2025, excluding inventory build, and shows a structural supply gap opening in natural flake graphite markets.

BENCHMARK MINERAL INTELLIGENCE – NOUVEAU MONDE GRAPHITE – OCTOBER 2018 Page 4

1. Introduction and Forecast Assumptions

• The chart below outlines the key drivers of demand for lithium-ion batteries over the forecast period. As can be seen the major growth area is for EVs, followed by stationary (grid) applications. In our base case scenario we expect that demand will be approximately 134,000 MWH in 2018, reaching 760,000 MWH by 2025 and 4M MWH by 2035.

1,000

3,500

2,500

5,000

4,500

0

3,000

1,500

4,000

2,000

500

2,155

2027

1,959

‘000 MWH

1,567

20162015 2017 2018 2019

949

2020 2021

1,175

72

2022 2023 2024 2025 20292026

3,135

2028 2030

760

2031

444

2032 2033 2034 2035

92 105 134 153 191 254 339

585

2,351

2,743

3,526

3,918

Upside

Electric Vehicles

Other

Downside

Stationary

Base Case MWH Compound Annual Growth Rate by sector, 2018-2035

Electric vehicles 24%

Stationary 33%

Other – includes electronics, portable batteries

4%

Total Li-ion battery demand 22%

BENCHMARK MINERAL INTELLIGENCE – NOUVEAU MONDE GRAPHITE – OCTOBER 2018 Page 5

1. Introduction and Forecast Assumptions

• The chart below outlines the development of demand for graphite over the forecast period to 2035, broken down by broad end-use sector. As can be seen batterydemand broadly reaches parity with other industrial demand by 2025-2026 given the level of growth forecast for both sectors. By the end of the forecast period we expect that graphite demand will reach 5.9 million tonnes, growing at a CAGR of 13% over the forecast period.

1,500

3,500

4,500

6,000

3,000

5,500

4,000

0

500

2,000

5,000

2,500

1,000

1,073

20272017 203420332031

‘000 tonnes

2016

2,912

1,164

161

561

2018

3,659

20232019 2020 2021

2,129

2022 2024

2,586

911

991

2030

1,361

2025 2026

635

2028

588

2029 2032

4,702

1,184

2015

664 723

4,407

775 873997

2035

1,902

2,421

3,402

3,915

4,900

5,393

5,886

1,608

+13%

Other industrial demand

Battery demand

Base Case Compound Annual Growth Rate by sector, 2018-2035

Battery demand 22%

Other industrial demand 4%

BENCHMARK MINERAL INTELLIGENCE – NOUVEAU MONDE GRAPHITE – OCTOBER 2018 Page 6

1. Introduction and Forecast Assumptions

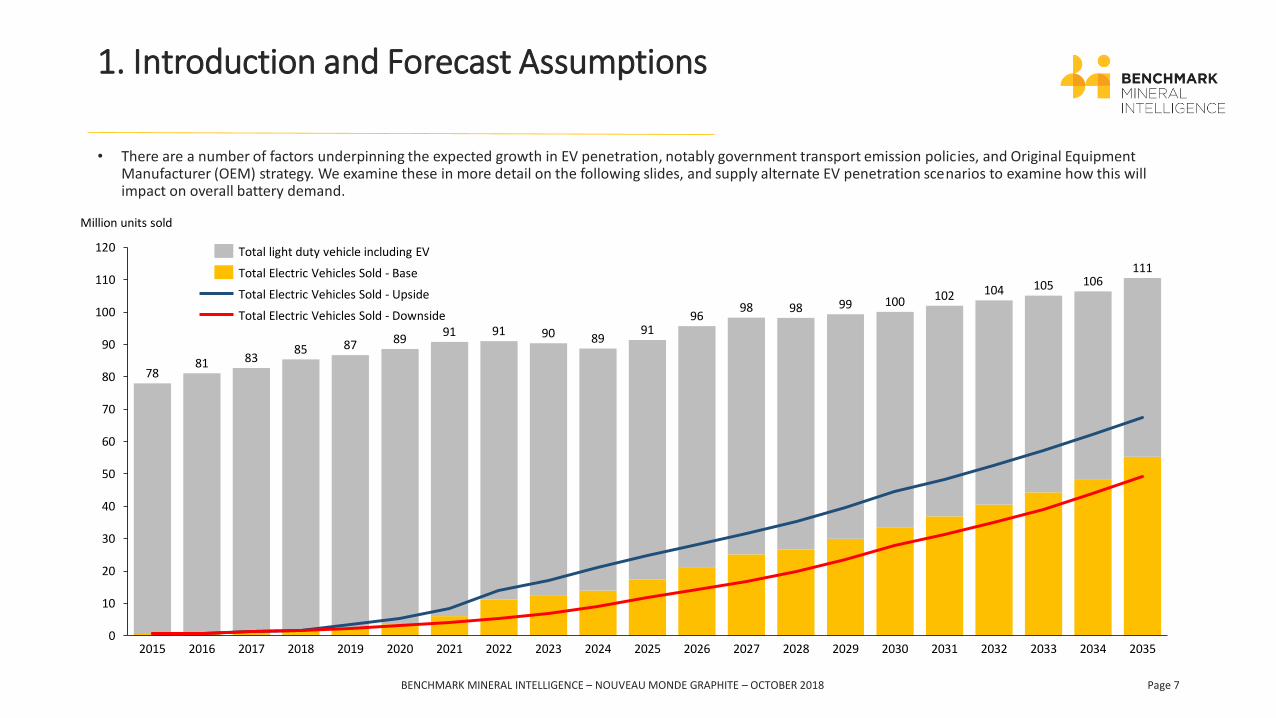

• There are a number of factors underpinning the expected growth in EV penetration, notably government transport emission policies, and Original Equipment Manufacturer (OEM) strategy. We examine these in more detail on the following slides, and supply alternate EV penetration scenarios to examine how this will impact on overall battery demand.

0

10

20

30

40

50

60

70

80

90

100

110

120

2021

Million units sold

202020162015 2017

98

20272018

98

2022 2023 2024 2025

96

89

2026

102

83

2028 2029 2030 2031 2032 2033

85

2034

111

2035

7881

87

2019

91 91 90 9189

99 100105 106

104

Total light duty vehicle including EV

Total Electric Vehicles Sold - Base

Total Electric Vehicles Sold - Downside

Total Electric Vehicles Sold - Upside

BENCHMARK MINERAL INTELLIGENCE – NOUVEAU MONDE GRAPHITE – OCTOBER 2018 Page 7

1. Introduction and Forecast Assumptions

Brazil: Target of 30% penetration of electric vehicle sales by 2030

Mexico: Target of 30% penetration of electric vehicle sales by 2030

USA: No Federal target set, California has set nominal state level targets for size of EV fleet

Canada: Target of 30% penetration of electric vehicle sales by 2030

China: Target of 5% penetration of electric vehicle sales by 2020, 20% by 2025

Japan and South Korea: Target of 30% penetration of electric vehicle sales by 2030

India: Proposal to end ICE sales by 2030

Italy: Target of 30% penetration of electric vehicle sales by 2030

Norway and Netherlands: Proposal to end ICE sales by 2025, Germany by 2030

UK and France: Proposal to end ICE sales by 2040

05

1015202530

Ch

ina

USA

Jap

an

Ger

man

y

Ind

ia UK

Fran

ce

Bra

zil

Ital

y

Can

ada

Sou

th K

ore

a

Mex

ico

Net

her

lan

ds

No

rway

Oth

er

Passenger Car and LDV sales, 2017, M units

Global policy statements by governments supporting EV adoption

BENCHMARK MINERAL INTELLIGENCE – NOUVEAU MONDE GRAPHITE – OCTOBER 2018 Page 8

1. Introduction and Forecast Assumptions

2022 2025 2030

Total annual vehicle production

10-12M

5-9m

1-4M

EV strategy timeline

VW group plans to invest more than $24bn in zero-

emission vehicles by 2030. Will develop 80 EV models by 2025, wants to offer an

electric version of each of its 300 models by 2030

Chinese OEMs expected to comply with

20% EV penetration rate

ruling by 2025

PSA aims to develop at least 40 electric vehicles by 2025

Aiming to develop 8 EV models by 2025, with 30 panned by

2030 Has set a target of two thirds of vehicle

sales EV by 2030

GM planning to introduce at least 20

EVs by 2023

Launching 12 EV models by 2022

Ford is planning to invest $11Bn in EVs by 2022, and will have 40 hybrid and full

EV models

Toyota has set a sales target of around 1m EVs

and fuel-cell vehicles (FCVs) by 2030,

investment $13 billion to develop and make

batteries

BMW plans to deliver 12 pure EVs by 2025Daimler will bring

10 pure EVs to the market by 2022

Major passenger car and light duty vehicle OEM EV strategy announcements

BENCHMARK MINERAL INTELLIGENCE – NOUVEAU MONDE GRAPHITE – OCTOBER 2018 Page 9

1. Introduction and Forecast Assumptions

For our base case scenario, in 2018 we expect battery demand, expressed in Mega Watt Hours, will be in the region of 82,000 MWH. By 2025, we expect this to grow to 405,000 MWH, by 2030 to 1.9M MWH.

4,200

2,000

1,400

3,000

0

2,800

2,200

200

600

2,400

400

1,000

800

3,600

2,600

4,000

1,200

3,200

3,800

1,600

1,800

3,400

82

2019

3,372

2029

29

2026

57

356

46

2034

‘000 MWH

20322015 2016 20282017 2018 2020

95

2021 2022

1,846

2023 2024

2,707

2025

263

2030 20332031 2035

126 185

478

2027

787

2,012

986

1,375

1,708

2,374

3,039

619

Base case

Upside

Downside

BENCHMARK MINERAL INTELLIGENCE – NOUVEAU MONDE GRAPHITE – OCTOBER 2018 Page 10

1. Introduction and Forecast Assumptions

0

50

100

150

200

250

300

350

400

450

500

550

600

650

700

750 726

Annual Cap 2016 (GWh)

GWH

Gwh by 2028Gwh by 2023

64

401

Japan

Europe

Australia

North America

South Korea

China

• In order to meet higher battery demand new Giga-factory capacity will need to be added. In this slide we summarise by country where new mega-factory supply is likely to be added, as we can see the majority of capacity will be added in China and North America.

• As can be seen, based on current mega-factory capacity expansion announcements and our outlook for battery demand we are projecting a shortage by 2028 of 649 GWH. We do expect that further capacity projects will be announced in order to fill this gap, especially given the level of pledged investment from automotive manufacturers.

Mega-factory capacity by region, 2016-2028

BENCHMARK MINERAL INTELLIGENCE – NOUVEAU MONDE GRAPHITE – OCTOBER 2018 Page 11

1. Introduction and Forecast Assumptions

LG C

hem

Mic

hig

an I

nc.

Pan

aso

nic

Him

eji

Pan

aso

nic

Su

min

oe

Lith

ium

En

ergy

Jap

an (

GS

Yuas

a te

chn

olo

gy)

AES

C Z

ama

32

Pan

aso

nic

Kas

ai

You

lion

Bat

tery

Inc

30

BYD

Ch

ina

LFP

SK In

no

vati

on

128

SK In

no

vati

on

Eu

rop

e

LG C

hem

Wro

claw

En

ergy

Sp

. z o

.o.

1

Dyn

avo

lt, F

ujia

n

BA

K

CA

LB

Nan

jing

LG C

hem

New

En

ergy

Bat

tery

Co

., Lt

d.

10

GSR

Cap

ital

, Sw

ede

n

BYD

Ch

ina

NC

M

Gu

anzh

ou

Gre

at P

ow

er E

ner

gy &

Tec

hn

olo

gy

GX

GK

BEI

/Mag

nis

, To

wn

svill

e, A

ust

ralia

4

Imp

eriu

m3

(B

EI/M

agn

is)

Sam

sun

g SD

I Xia

n

84

LG C

hem

Ko

rea

Sam

sun

g SD

I Ko

rea

AES

C, Z

hen

jian

g, J

ian

gsu

AES

C J

ian

gsu

Pan

aso

nic

Dal

ian

23

Gre

at W

all

Lish

en

No

rth

volt

Terr

a E

Ho

ldin

g

CA

TL

Tesl

a /

Pan

aso

nic

En

ergy

of

No

rth

Am

eric

a

5

25

5

1814

89 816

10 10

2015 15

20 18 20 20

3034

100

150

25

2028

2016

Mega-factory capacity by company, 2016-2028Gigawatt Hours

BENCHMARK MINERAL INTELLIGENCE – NOUVEAU MONDE GRAPHITE – OCTOBER 2018 Page 12

1. Introduction and Forecast Assumptions

BENCHMARK MINERAL INTELLIGENCE – NOUVEAU MONDE GRAPHITE – OCTOBER 2018 Page 13

1. Introduction and Forecast Assumptions

The chart below outlines our forecast for graphite material for use as an input to anodes in the lithium-ion battery supply chain, we expect that graphite by battery type will remain stable throughout the forecast period

1.5

4.5

4.0

0.0

0.5

3.5

2.0

2.5

1.0

3.0

5.0

2027 203520242021

2.4

0.2

2028

Million tonnes

2015

0.5

0.1

2016 20202017 2018

1.9

2019 2022 2023 2025 2026 20322029 2030

2.6

2031 2033

3.8

1.4

2034

0.1 0.1 0.2

0.7

0.2 0.3 0.4

0.91.1

2.8

3.3

4.2

4.7LMO

LMNO

LTO

Other

LCO

LFP

NCA

NCM

BENCHMARK MINERAL INTELLIGENCE – NOUVEAU MONDE GRAPHITE – OCTOBER 2018 Page 14

2. Long Term Supply Forecasts for Natural Flake and Synthetic Graphite to 2040

2. Long Term Supply Forecasts for Natural Flake and Synthetic Graphite to 2040

• This analysis will examine the outlook for supply, identifying key capacity changes among existing market players and new entrants. We will review existing capacity and provide an outlook for both likely mine expansion projects, as well closures over the forecast period, also provided in an Excel database format.

• Graphite is mined in several countries around the world, the main sources of flake graphite for batteries are Brazil, Mozambique and China. Nearly all of this material is currently processed to uncoated spherical (anode precursor) and coated spherical (anode) in China. Battery cell manufacture also takes place in China, as well as Japan, Korea, Poland and the US.

• At present roughly 60% of total graphite supply comes from synthetic production, based in China, India, Europe and the US, we expect this share to fall over time owing to the relatively high cost of production, and an expansion in natural graphite capacity

Imerys, Lac-des-îles, QC mine closing Q4 2018

Nouveau Monde Graphite, Matawinie, QC mine

BENCHMARK MINERAL INTELLIGENCE – NOUVEAU MONDE GRAPHITE – OCTOBER 2018 Page 16

2. Long Term Supply Forecasts for Natural Flake and Synthetic Graphite to 2040

Overview and outlook for synthetic graphite

• Synthetic graphite is produced using high temperature treatment of amorphous carbon materials, notably petroleum coke, also know as needle or green coke, a by-product of crude oil production. The production process is described in the flow diagram below.

• Synthetic graphite production has the advantage of producing consistently high quality graphite (90%+ C) suitable for battery applications, however owing to the energy intensity of production it is a very high cost source of supply. In addition the principal feedstock, needle coke, has increased in price dramatically in recent years, from a long-term average of roughly $800 per tonne to $8,000 per tonne. Further, given that needle coke is a by-product of crude oil production supply is subject to movements in oil output, affecting both price and availability.

• At present synthetic graphite is manufactured in China, India, Europe and the US. In China the main producers are Fangda Carbon New Material Technology Co Ltd, Jilin Carbon Co Ltd, Sunstone Development Co Ltd, Hongte Group and Jinzhou Petrochemical Co Ltd. Outside of China the main producers are SGL, Graftech, Imerys and Showa Denko.

• Given the higher cost of production of synthetic graphite and the relative availability of cheaper natural flake graphite, we do not expect that new synthetic graphite capacity will be added in the coming years. That, coupled with the expansion of natural graphite supply will see the market share for synthetic graphite contract markedly in the forecast period

BENCHMARK MINERAL INTELLIGENCE – NOUVEAU MONDE GRAPHITE – OCTOBER 2018 Page 17

2. Long Term Supply Forecasts for Natural Flake and Synthetic Graphite to 2040

1,606

900

706

Total Supply Mined - Existing producers

Synthetic

2,758

900

1,061

797

SyntheticTotal Supply Mined - Existing producers

Mined - New Entrants

Natural Flake and Synthetic graphite supply-balance 2018(‘000 tonnes)

Natural Flake and Synthetic graphite supply-balance 2025(‘000 tonnes)

Synthetic graphite market share -

60%

Synthetic graphite market share - 33%

• The charts below illustrate our forecasts for the breakdown of graphite supply for all end-uses in both 2018 and 2025. As can be seen, we expect that significant new capacity will come online from both incumbent natural graphite miners and new entrants

• In the following slides we detail how we expect this to happen, beginning with brownfield capacity expansions at existing operations and then looking at mining projects.

BENCHMARK MINERAL INTELLIGENCE – NOUVEAU MONDE GRAPHITE – OCTOBER 2018 Page 18

2. Long Term Supply Forecasts for Natural Flake and Synthetic Graphite to 2040

• At any time there are a number of brownfield and greenfield graphite capacity projects announced and undergoing development, however there are a number that will either never come to fruition and some that proceed at a faster or slower pace than projected.

• The factors that determine how likely a project is to come online are often related, below we group individual issues by type and show linkages between them:

Resource geography factors Resource geology factors Financial factors

Political risk – resources located in territories with an unstable political

situation are less likely to secure financing or necessary human resources to proceed

Access to key markets – transportation costs and lead times often feature heavily

in a projects ability to be competitive

Resource costs – Capex factors such as land values and opex factors such as

labour, transport and energy costs will largely be determined by resource

geography

Resource size – Resource size will determine the likely capex for the project as well as the mine life and

capacity

Resource quality – the distribution of flake sizes and quality, and suitability for processing to battery grades are crucial

for securing buyers and premium pricing

Resource costs – the resource type and quality will largely determine the capex

and operating mining costs for the project and likelihood of securing

financing

Access to financing – securing financing is a crucial stage in project development, and linked to several

factors as shown

Price forecasts – consensus price forecasts determine a projects forecast

revenue and are therefore vital in securing financing

Off-take agreements and strategic partnerships – the likelihood a project coming online is massively boosted by securing off-take agreements and/or

involvement of an end-user

Natural flake capacity expansions, 2018-2040

BENCHMARK MINERAL INTELLIGENCE – NOUVEAU MONDE GRAPHITE – OCTOBER 2018 Page 19

2. Long Term Supply Forecasts for Natural Flake and Synthetic Graphite to 2040

Brownfield natural flake capacity expansions, 2018-2040• In this slide we outline expected capacity expansions at existing graphite producers over the forecast period. Over the period to 2040 we

expect that there will be nearly 900,000 tonnes of brownfield capacity expansions by existing producers, notably in China, the Ukraine and Mozambique

90,000

20302018 20352025 2040

100,000

157,000

209,000 209,000

468,000477,500 453,600

2018 20402025 2030 2035

472,400472,400

Grafite do Brasil - Extractiva

Nacional do Grafite

2030 20352018 2040

81,500

2025

42,000

73,00081,500 81,500

2030 20352018 2025 2040

436,000

102,000

779,000871,000 871,000

40,000

20302018 2025 2035

46,000

32,000

2040

55,000 55,000

Russia - Ural Graphite

Norway - Skaland Graphite AS - LNS Group

Ukraine - Zavalivskiy GraphiteImerys, Lac-des-îles, QC mine closing Q4 2018

Heilon Jiang

Inner Mongolia, Shanxi

Other provinces Hubei, Hebei, Henan, Sichuan

Shandong

Madagascar - Bass Metals

Zimbabwe - AMG Mining - Government JV

Namibia - Imerys Graphite and Carbon/Gecko Jv

Mozambique - Syrah Resources

Jharkhand

Tamil Nadu

Odisha

BENCHMARK MINERAL INTELLIGENCE – NOUVEAU MONDE GRAPHITE – OCTOBER 2018 Page 20

2. Long Term Supply Forecasts for Natural Flake and Synthetic Graphite to 2040

Typical project development milestones

• Scoping: initial financing to undertake preliminary exploration of a deposit

• Resource estimation: scoping results used to raise further finance for sufficient drilling to publish NI 43-101 and/or JORC compliant resource estimates1

• Pre-feasibility study: preliminary engineering plans and economic viability to determine whether to proceed to a full feasibility study

• Feasibility study: presentation of plans for extraction and processing and full assessment of a project’s geological profile and economic viability

• Financing: subsequent to feasibility study financing is secured for project construction

• Construction: final development of project to completion

1. NI 43-101 is the mineral project disclosure standard for companies listed on Canadian Stock Exchanges, JORC is the equivalent for Australian-listed companies

Mineral lease

Exploration

Environmental

Infrastructure

Head Frame/Shaft Sinking

Mine development/ Ramp up

Engineering and design

Construct mill

Year

1

Year

2

Year

3

Year

4

Year

5

Year

6

Year

7

Year

8

Greenfield development timeline

Route to development for a greenfield mining project

Greenfield natural flake capacity expansions, 2018-2040• In the flow chart below we outline the main development stages for the development of a greenfield graphite mining project. • At present we are tracking numerous projects that we classify as ‘Highly probable, ‘Probable’ and ‘Possible’ based on their current stage of

development and likely progress to production. In the following slide we outline the current stage of development for a number of major greenfield projects

BENCHMARK MINERAL INTELLIGENCE – NOUVEAU MONDE GRAPHITE – OCTOBER 2018 Page 21

2. Long Term Supply Forecasts for Natural Flake and Synthetic Graphite to 2040

Development phases for key greenfield graphite mining projects

Key: DR. – Drilling, Expl. – Exploration, Feas. – Feasibility, Cons. – Construction, Prop. St. Up – Proposed started Up, Ph. – Phase

BENCHMARK MINERAL INTELLIGENCE – NOUVEAU MONDE GRAPHITE – OCTOBER 2018 Page 22

2. Long Term Supply Forecasts for Natural Flake and Synthetic Graphite to 2040

• In the chart below we outline our forecast for the development of natural flake capacity over time. As can be seen there is a significant pipeline of new capacity coming online for graphite over the next decade. There will need to be further greenfield and brownfield capacity expansions in the period beyond 2028 in order to meet rising demand, even in our downside demand scenario

2.4

0.4

1.4

0.6

1.2

2.0

0.0

1.0

0.2

1.6

0.8

1.8

2.2

1.96

2030 2032

1.44

0.59

1.43

2033

0.84

Million tonnes

2015 2016

0.65

2017

1.75

0.67

2018 203720222019 2020 2021 2023 2024 2025

2.332.27

2026

1.971.92

2027 2028 2029

0.71

0.91

2035

1.15

2036

1.77

2.072.17

2031 2034 2038 2040

2.342.32 2.33 2.34 2.34 2.34 2.34 2.34

2039

Operational supply

Highly Probable additonal tonnes

Probable additonal tonnes

Possible additonal tonnes

• Factors in a 5% supply disruption allowance from stated capacity• Does not include synthetic supply

BENCHMARK MINERAL INTELLIGENCE – NOUVEAU MONDE GRAPHITE – OCTOBER 2018 Page 23

2. Long Term Supply Forecasts for Natural Flake and Synthetic Graphite to 2040

There is a significant pipeline of new capacity coming online for graphite over the next decade. There will need to be further greenfield and brownfield capacity expansions in the period beyond 2028 in order to meet rising demand, even in our downside demand scenario

Potential supply deficit once planned capacity and projects come online

• Includes non-battery demand• Factors in a 5% supply disruption allowance from stated capacity• Does not include synthetic supply

0.6

1.4

2.4

0.0

1.6

0.2

3.8

0.8

0.4

3.6

1.2

2.6

2.8

3.0

1.0

3.4

2.2

1.8

2.0

3.2

2017

1.43

2023

0.84

20292015

Million tonnes

2016 2018

0.59

2019

1.96

2020 2021 20272022 2024 2025 2026 2028

1.77

0.65

1.15

0.67 0.71

0.91

2030

1.75

1.92 1.972.07

2.17

1.44

Demand - Base Case

Possible additonal tonnes

Probable additonal tonnes

Operational supply

Highly Probable additonal tonnes

BENCHMARK MINERAL INTELLIGENCE – NOUVEAU MONDE GRAPHITE – OCTOBER 2018 Page 24

3. Natural Flake Graphite Price Forecasts

3. Natural Flake Graphite Price Forecasts

• In this section we provide a price forecast for each grade that Matawinie project will produce, on a delivered North America basis and also a weighted basket price forecast including all grades.

• The Matawinie project has high carbon contents, 97-98%, with the following flake size distribution for natural flake graphite:

Natural flake graphite (97-98% C) flake size Product weighting

+100 mesh 17%

+50 mesh 31%

+80 mesh 12%

-100 mesh 40%

• In order to arrive at a final forecast for each grade that Matawinie project will produce, on a delivered North America basis we look first at the drivers of graphite pricing, including price differences between grades, and we use the benchmark China Fob reference price as the basis for the forecast. We then add a location premium for a delivered North America price for the grades Matawinie will produce.

BENCHMARK MINERAL INTELLIGENCE – NOUVEAU MONDE GRAPHITE – OCTOBER 2018 Page 26

3. Natural Flake Graphite Price Forecasts

0

500

1,000

1,500

2,000

2,500

Flake Graphite Pricing, 2015-2018

+50 mesh 96-97% C -100 mesh 96-97% C -100 mesh 90-93% C

USD per tonne, China FOB

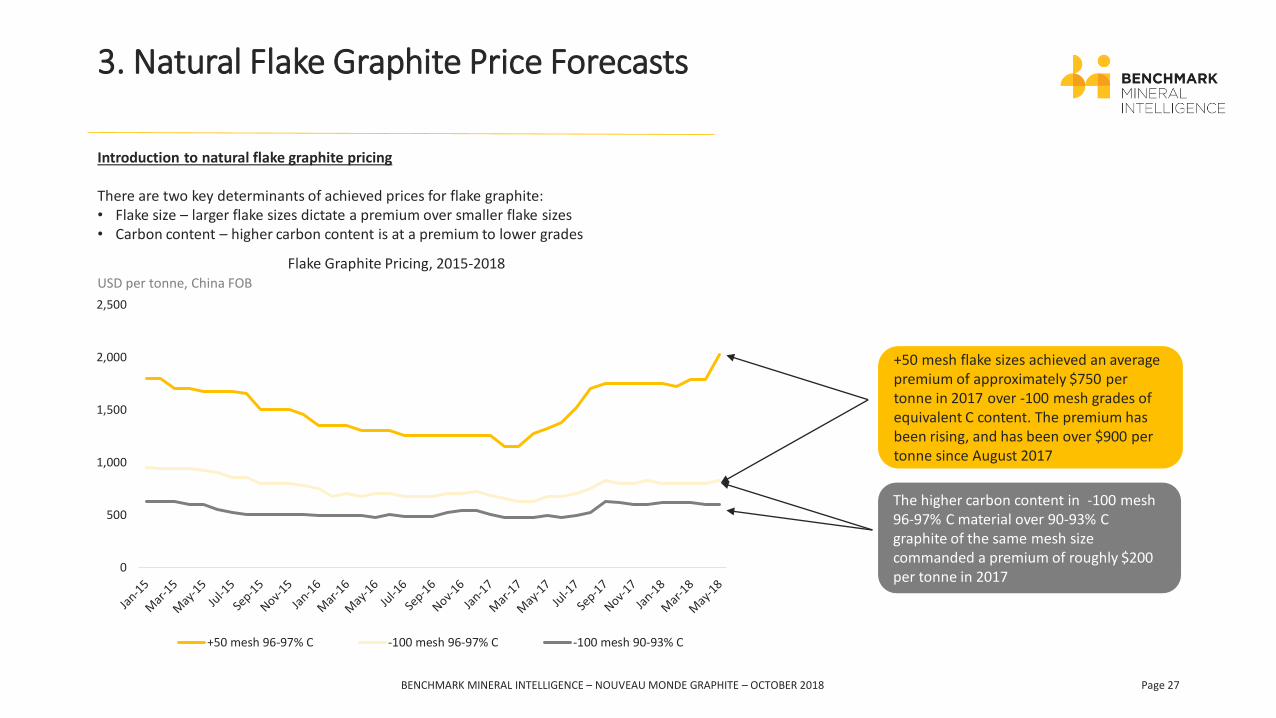

+50 mesh flake sizes achieved an average premium of approximately $750 per tonne in 2017 over -100 mesh grades of equivalent C content. The premium has been rising, and has been over $900 per tonne since August 2017

The higher carbon content in -100 mesh 96-97% C material over 90-93% C graphite of the same mesh size commanded a premium of roughly $200 per tonne in 2017

Introduction to natural flake graphite pricing

There are two key determinants of achieved prices for flake graphite:• Flake size – larger flake sizes dictate a premium over smaller flake sizes• Carbon content – higher carbon content is at a premium to lower grades

BENCHMARK MINERAL INTELLIGENCE – NOUVEAU MONDE GRAPHITE – OCTOBER 2018 Page 27

3. Natural Flake Graphite Price Forecasts

IRR assumptions for a ‘Typical’ greenfield graphite project

Output at full capacity (tonnes per annum) 40,000

Mine Life (years) 30

Capital Expenditure (USD Million) 200

Operating Cost (USD per tonne) 450

IRR at different graphite long run pricing

Graphite long run pricing long run price assumption

Indicative IRR

USD1,500 per tonne 22%

USD2,000 per tonne 27%

USD1,000 per tonne 15%

Benchmark Graphite price forecast methodology

• Our medium and long-term price forecast methodology for lithium considers the following factors:

• Balance of supply and demand – Based on our analysis of the development of demand over time, and our understanding of the pipeline of new greenfield and brownfield capacity, we are able to make an assessment of the extent of over and under supply in the market over time, and how this is likely to impact prices

• Production costs for the marginal cost producer – Long run pricing in commodity markets is often determined by the level at which the highest cost producer needed to supply the market can continue to operate; for graphite this would be at a cash cost level of around USD900 per tonne. For the forecast we expect this will be less of a factor, due to the ongoing need to incentivise new projects prices will be well above this level

• Incentive pricing for new greenfield and brownfield capacity investment – There will be an ongoing requirement for new greenfield capacity over the course of the forecast period. We have conducted an Initial Rate of Return (IRR) analysis for a ‘Typical’ greenfield natural flake graphite project, which suggests that at a price level of USD2,000 per tonne for a basket of graphite grades the IRR would be 27%. This is approximately the level that junior miners are using for their assessment of project economics, and reflects the fact that as the lower cost new supply comes online there will be a need for the development of higher capex projects over time.

BENCHMARK MINERAL INTELLIGENCE – NOUVEAU MONDE GRAPHITE – OCTOBER 2018 Page 28

3. Natural Flake Graphite Price Forecasts

900

800

700

600

500

400

300

100

200

0Heilon Jiang (Low Cost) Mahenge

Maiquinique

Shandong

Lynx, Nr KaroiHeilon Jiang (High Cost)

Montepuez

Epanko Tamil NaduOtjiwarongo

Ancuabe

Salto Da DivisaItapecerica

Inner Mongolia, ShanxiOther provinces Hubei, Hebei, Henan, Sichuan

Lac Guéret, QC

Odisha

Skaland

Molo

Coosa

Lac KnifeTaiginka

Graphmada Large Flake Graphite Mine

Lindi Jumbo Graphite

BunyuPedro Azul

Zavalivskiy

Balama

Jharkhand

Russia

China Norway

Namibia

Zimbabwe

Mozambique

Tanzania Madagascar

Canada

Brazil

Ukraine

India

United States of America

USD per tonne (Real 2018)

Graphite industry cash cost* curve 2035

*Excludes capital repayments and royalties

The marginal producer operates USD875 per tonne

BENCHMARK MINERAL INTELLIGENCE – NOUVEAU MONDE GRAPHITE – OCTOBER 2018 Page 29

3. Natural Flake Graphite Price Forecasts

300

0

500

700

200

400

600

900

800

100

Salto Da Divisa 2018

Pedro Azul 2018

Inner Mongolia, Shanxi

Bunyu

Graphmada Large Flake Graphite Mine

Itapecerica 2018

Lac Guéret, QC

MaiquiniqueHeilon Jiang (High Cost)

MoloItapecerica

Pedro AzulMontepuez

Lynx, Nr KaroiSalto Da DivisaLynx, Nr Karoi

Heilon Jiang (Low Cost) 2018 Mahenge

Otjiwarongo Tamil Nadu 2018

Maiquinique 2018

Graphmada Large Flake Graphite Mine 2018

Taiginka

Odisha 2018

Jharkhand 2018

Zavalivskiy 2018

CoosaSkaland

Jharkhand

Odisha

Shandong

Taiginka 2018

Balama

Lindi Jumbo GraphiteLac Knife

AncuabeEpanko

Heilon Jiang (Low Cost)

Otjiwarongo 2018

Tamil Nadu

Other provinces Hubei, Hebei, Henan, Sichuan

Balama 2018

Zavalivskiy

USD per tonne (Real 2018)

Graphite industry cash cost* curve 2035

*Excludes capital repayments and royalties

Possible

Operating

Highly Probable

Probable Brownfield expansion

The vast majority of new brownfield and greenfield capacity will operate at or below $450 per tonne

BENCHMARK MINERAL INTELLIGENCE – NOUVEAU MONDE GRAPHITE – OCTOBER 2018 Page 30

3. Natural Flake Graphite Price Forecasts

Natural flake graphite historical pricing 2015-2018

• In the charts below we illustrate the price history for high carbon graphite grades since 2015, and the industry supply and demand balance over the same period.

• There has been a marked increase in graphite pricing over the last two years, especially for higher flake sizes, as a response to a tightening in the market over the same period, and this trend has accelerated in 2018 as the market has moved into a supply deficit despite brownfield expansions from existing producers.

0

500

1,000

1,500

2,000

2015 2016 2017 2018

0

100

200

300

400

500

600

700

800

2015 2016 2017 2018

Graphite supply and demand balance, 2015-2018

Operational supply Demand - Base Case

‘000 tonnes

+50 mesh+100 mesh -100 mesh+80 mesh

USD per tonne, FOB China

High carbon (96-97% C) natural flake graphite pricing history, 2015-2018

BENCHMARK MINERAL INTELLIGENCE – NOUVEAU MONDE GRAPHITE – OCTOBER 2018 Page 31

3. Natural Flake Graphite Price Forecasts

0

500

1,000

1,500

2,000

2,500

2019 2020 2021 2022 2023 2024 2025 2026

Tho

usa

nd

s

Graphite supply and demand forecasts, 2019-2026

Operational supplyHighly Probable additonal tonnesProbable additonal tonnesPossible additonal tonnesDemand - Base Case

Natural flake graphite price forecast 2019-2026

• In the ‘medium term’ to 2026 we will see continued brownfield expansions, and from 2021 new capacity coming online from greenfield projects.In the middle of this period it is likely that the market will move into slight oversupply for a number of years as new capacity ramps up faster than demand growth. The market quickly moves back into deficit towards the end of the period however, as the pipeline of new capacity projects is exhausted and demand continues to grow.

• As a result there will need to be incentivise new projects to come online from 2025 onwards, which would mean they begin development in 2019 or 2020, therefore we do not anticipate a significant price reduction in this period

‘000 Tonnes

Includes non-battery demand

0

500

1,000

1,500

2,000

2,500

2019 2020 2021 2022 2023 2024 2025 2026

-100 mesh

+100 mesh

+50 mesh

+80 mesh

High carbon (96-97% C) natural flake graphite price forecast, 2019-2026

USD per tonne, Real 2018, FOB China

BENCHMARK MINERAL INTELLIGENCE – NOUVEAU MONDE GRAPHITE – OCTOBER 2018 Page 32

3. Natural Flake Graphite Price Forecasts

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

2027 2028 2029 2030 2031 2032 2033 2034 2035 2036 2037 2038 2039 2040

Graphite supply and demand forecasts, 2027-2040

Operational supply

Highly Probable additonal tonnes

Probable additonal tonnes

Possible additonal tonnes

Demand - Base Case

’000 Tonnes

Includes non-battery demand

Natural flake graphite price forecast 2027-2040

• From 2027 until the end of the forecast period at 2040 the market remains in deficit and will continue to need new supply coming online in order to meet demand. Prices will therefore need to be high enough to incentivise demand.

• As we stated the main determinant of long term prices for graphite over the forecast period will be the need to incentivise new supply to make up this deficit. Based on our IRR calculations and our consideration of the typical cost of capital for greenfield mining projects of this type, we estimate that the average price for high carbon grades (96-97% C) will be USD2,000 based on the range of pricing in the chart on the left below.

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

2,200

2,400

2,600

2028 20342030 20402032 20382036

+100 mesh +80 mesh+50 mesh -100 mesh

High carbon (96-97% C) natural flake graphite price forecast, 2027-2040

USD per tonne, Real 2018, FOB China

BENCHMARK MINERAL INTELLIGENCE – NOUVEAU MONDE GRAPHITE – OCTOBER 2018 Page 33

3. Natural Flake Graphite Price Forecasts

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

2,200

2,400

2,600

2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030 2031 2032 2033 2034 2035 2036 2037 2038 2039 2040

+80 mesh+100 mesh

+50 mesh -100 mesh

High carbon (96-97% C) natural flake price history and forecast, 2015-2040

USD per tonne, Real 2018, FOB China

Forecast

BENCHMARK MINERAL INTELLIGENCE – NOUVEAU MONDE GRAPHITE – OCTOBER 2018 Page 34

3. Natural Flake Graphite Price Forecasts

• In order to arrive at a price forecasts for the Matawinie project on a delivered North America basis we add a location premium to the benchmark China Fob prices on the previous slides, as a well as adjustments for grades based on the expected output of the operation.

• The premium varies by grade, and there is some variance over time. For the purposes of this forecast we will use the following premiums by grade:

• We also provide a weighted average of the price forecast based on Matawinie’s planned product mix.

Natural flake graphite (96-97% C) flake size Location premium, USD per tonne

+150 mesh 100

+50 mesh 150

+80 mesh 120

-100 mesh 110

Natural flake graphite (96-97% C) flake size Product weighting

+150 mesh 27.7%

+50 mesh 14.8%

+80 mesh 33.4%

-100 mesh 24.1%

BENCHMARK MINERAL INTELLIGENCE – NOUVEAU MONDE GRAPHITE – OCTOBER 2018 Page 35

3. Natural Flake Graphite Price Forecasts

0

500

1,000

1,500

2,000

2,500

3,000

3,500

2022 2023 2024 2025 2026 2027 2028 2029 2030 2031 2032 2033 2034 2035 2036 2037 2038 2039 2040 2041 2042 2043 2044 2045 2046 2047

Matawinie basket

+80 mesh

+50 mesh

+150 mesh

-150 mesh

High carbon (96-97% C) natural flake price history and forecast, 2022-2047

USD per tonne, Real 2018, North America CFR

BENCHMARK MINERAL INTELLIGENCE – NOUVEAU MONDE GRAPHITE – OCTOBER 2018 Page 36

4. Premium Graphite Markets Outlook and Prices

4. Premium Graphite Markets Outlook and Prices

• Nouveau Monde is currently developing second transformation processes in order to serve higher value-added markets. In this section we will provide an overview and market size breakdown for the following processed, premium graphite products, including:

• Spherical uncoated and coated graphite for anodes

• Expandable graphite

• Purified micronized graphite

BENCHMARK MINERAL INTELLIGENCE – NOUVEAU MONDE GRAPHITE – OCTOBER 2018 Page 38

4. Premium Graphite Markets Outlook and Prices

• Spherical graphite is formed by processing flake graphite through consecutive milling steps. This is an energy-intensive process, with a yield of 30 to 50%. In the case of Natural Graphite, the shaping must be preceded by purification, most commonly through chemical leaching.

• The current price for uncoated spherical (anode precursor) material is in the region of USD3,500 per tonne, while coated spherical (anode) currently sells for USD9,000 per tonne.

• Spherical shapes usually measure between 10 to 40 micron and generally have a carbon content of 99.95% C or above. This process increases the surface area and conductivity making it ideal for use as the anode material for battery technologies.

• As such demand growth is linked to the development of the battery market. On the following slide we detail our expectations for both coated and uncoated demand over the forecast period

Coated and uncoated spherical graphite overview Coated spherical graphite

BENCHMARK MINERAL INTELLIGENCE – NOUVEAU MONDE GRAPHITE – OCTOBER 2018 Page 39

4. Premium Graphite Markets Outlook and Prices

3.5

0.0

1.5

0.5

1.0

2.0

2.5

3.0

4.0

4.5

5.0

5.5

6.0

2020

Million tonnes

2016 2018 2022 2024 2026 2028 20382030 2032 2034 2036 2040

+19%

Coated spherical graphite (anode) demand forecast, 2015-2040

1.0

3.5

0.5

0.0

1.5

2.0

2.5

3.0

4.0

20302024 20342016 2018 2020 2022

Million tonnes

2026 2028 2032 2036 2038 2040

+19%

Uncoated spherical graphite (anode precursor) demand forecast, 2015-2040

BENCHMARK MINERAL INTELLIGENCE – NOUVEAU MONDE GRAPHITE – OCTOBER 2018 Page 40

4. Premium Graphite Markets Outlook and Prices

• Purified micronized graphite is subjected to the same chemical leaching process to achieve the required grades as is crushed and ground to achieve a size of less than 30 microns, with a carbon content of 99.9% C.

• It is used as a feedstock for spherical material and is suitable for a range of applications including traditional alkaline batteries, polymers, lubricants, powder metallurgy. As such we expect that demand for purified micronized graphite will grow at a similar pace to total graphite demand over the life of the forecast, at a compound annual growth rate (CAGR) of 12%, with the majority of this growth being driven by battery demand growth.

• Prices for Purified micronized graphite are reported at USD3,000 per tonne

Purified micronized graphite overview

BENCHMARK MINERAL INTELLIGENCE – NOUVEAU MONDE GRAPHITE – OCTOBER 2018 Page 41

4. Premium Graphite Markets Outlook and Prices

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

450,000

500,000

550,000

600,000

20282024 20302016 2018 20382020 203220262022

Tonnes

2034 2036 2040

+12%

Purified micronized graphite demand forecast, 2015-2040

BENCHMARK MINERAL INTELLIGENCE – NOUVEAU MONDE GRAPHITE – OCTOBER 2018 Page 42

4. Premium Graphite Markets Outlook and Prices

• Expandable graphite is produced by a process in which an intercalant material is inserted in between the graphene layers of flake graphite. Typically the feedstock for expandable graphite is flake graphite with particle size distribution of +80 mesh.

• A number of chemical compounds can be used to intercalate graphite materials. The most common process is the insertion of sulphate compounds to create ‘graphite bi-sulphate’

• This material is manufactured by treating highly crystalline natural flake graphite with a mixture of sulphuric acid and other oxidizing agents which aid the sulphate intercalation. The final carbon content of this material is very high at up to 99.9% C

• The resultant product is a highly intumescent form of graphite that useful in applications that include fire retardants, high performance gaskets, conductive fillers, electromagnetic pulse and radiation shielding, foundry products.

• Benchmark estimates that the market for expandable graphite at present stands at roughly 60,000 tonnes per annum, the bulk of which is for use in fire retardants.

• he markets for expanded graphite, in particular for fire retardants, are forecast to exceed industrial and GDP growth in the coming years as fire safety regulations are expected to become more stringent in all major economies. We anticipate a 6% CAGR for expandable graphite demand over the life of the forecast.

• At present the market price for expanded graphite is in the region of USD2,700-USD3,200 per tonne depending on the purity of material

Flak

e G

rap

hit

e

(un

exp

and

ed)

Exp

and

ed G

rap

hit

eBENCHMARK MINERAL INTELLIGENCE – NOUVEAU MONDE GRAPHITE – OCTOBER 2018 Page 43

4. Premium Graphite Markets Outlook and Prices

0

50,000

100,000

150,000

200,000

202220202016 2018 20382024 203020282026 2032 2034 2036 2040

Tonnes

+6%

Expandable graphite demand forecast, 2015-2040

BENCHMARK MINERAL INTELLIGENCE – NOUVEAU MONDE GRAPHITE – OCTOBER 2018 Page 44

BENCHMARK MINERAL INTELLIGENCE – NOUVEAU MONDE GRAPHITE – OCTOBER 2018 Page 45