Embed Size (px)

Citation preview

ACCOUNTING GUIDELINE

GRAP 23

Revenue From Non-

exchange

Transactions

All rights reserved. No part of this publication may be reproduced, stored in retrieval system, or transmitted, in any form or by any means, electronic,

mechanical, photocopying, recording, or otherwise, without the prior permission of the National Treasury of South Africa.

Permission to reproduce limited extracts from the publication will not usually be withheld.

Though National Treasury (NT) believes reasonable efforts have been made to ensure the accuracy of the information contained in the guideline,

it may include inaccuracies or typographical errors and may be changed or updated without notice. NT may amend these guidelines at any time by

posting the amended terms on NT's Web site.

Note that this document is not part of the GRAP standard. The GRAP takes precedence while this guideline is used mainly to provide further

explanations on the concepts already in the GRAP.

GRAP 23 on Revenue from Non-Exchange Transactions

Issued February 2020 Page 3 of 33

Contents

1. Introduction .................................................................................................................. 4

2. Scope .......................................................................................................................... 5

3. Definition and identification .......................................................................................... 6

3.1 Transactions including exchange and non-exchange components...................... 7

3.2 Licenses, subscriptions and similar fees ............................................................. 8

3.3 Stipulations ......................................................................................................... 9

3.4 Conditions on transferred assets ....................................................................... 10

3.5 Restrictions on transferred assets ..................................................................... 10

3.6 Substance over form ......................................................................................... 11

4. Initial Recognition....................................................................................................... 12

4.1 Recognition of assets ........................................................................................ 12

4.2 Recognition of liabilities .................................................................................... 13

4.3 Recognition of revenue ..................................................................................... 14

5. Initial Measurement .................................................................................................... 15

5.1 Measurement of assets ..................................................................................... 15

5.2 Measurement of revenue and liabilities ............................................................. 15

6. Transfers ................................................................................................................... 16

6.1 Debt forgiveness ............................................................................................... 16

6.2 Grants, gifts, donations, including goods in-kind ............................................... 17

6.3 Services in-kind ................................................................................................ 21

6.4 Pledges ............................................................................................................. 22

6.5 Bequests ........................................................................................................... 23

6.6 Advanced receipts ............................................................................................ 23

6.7 Concessionary loan .......................................................................................... 25

7. Taxes ......................................................................................................................... 28

7.1 Advance receipts of taxes ................................................................................. 30

7.2 Measurement of assets arising from taxation .................................................... 30

8. Entity Specific Guidance ............................................................................................ 32

9. Useful links and references ........................................................................................ 33

GRAP 23 on Revenue from Non-Exchange Transactions

Issued February 2020 Page 4 of 33

1. Introduction

This document provides guidance on the accounting treatment of revenue from non-exchange

transactions.

The contents should be read in conjunction with GRAP 23.

For purposes of this guide, “entities” refer to the following bodies to which the standard of

GRAP relate to, unless specifically stated otherwise:

Public entities

Constitutional institutions

Municipalities and all other entities under their control

Trading entities and government components applying the standards of GRAP

Parliament and the provincial legislatures

TVET and CET colleges

Explanation of images used in manual:

Definition

Take note

Management process and decision making

Example

GRAP 23 on Revenue from Non-Exchange Transactions

Issued February 2020 Page 5 of 33

2. Scope

GRAP 23 is applicable to all entities preparing their financial statements on the accrual basis

of accounting and includes revenue arising from non-exchange transactions.

Reorganisation of departments or shifting of functions between departments (i.e. transfer of

functions), are therefore not addressed by the standard and this guide.

To confirm, this guide will not provide guidance on a transfer of functions between entities

under common control or a merger that is a non-exchange transaction as well as revenue

received by entities as a result of non-exchange transactions in construction contract.

Non-exchange transactions are transactions that are not exchange transactions. In a non-exchange transaction, an entity either receives value from another entity without directly giving approximately equal value in exchange, or gives value to another entity without directly receiving approximately equal value in exchange. For example:

X provides a grant to Entity P Entity P provides a service to the public

Public receives services

Transfer of functions is a reallocation of government activities and responsibilities between entities or functions into one reporting entity or by transferring functions between entities.

GRAP 23 on Revenue from Non-Exchange Transactions

Issued February 2020 Page 6 of 33

3. Definition and identification

Contributions from owners are accounted for in accordance with GRAP 1 on Presentation of

Financial Statements. In essence, contributions from owners are transactions that directly

affect the net assets of the recipient, for example an entity is given a grant/loan with no

repayment terms. In determining whether a transaction satisfies the definition of a contribution

from owners, the substance rather than the form of the transaction is considered. If, despite

the form of the transaction, the substance is clearly that of a loan or another kind of liability, or

revenue, the entity recognises it as such. For example, if a transaction has the form of a

contribution from owners, but specifies that the entity will pay fixed distributions to the

transferor, with a return of the transferor’s investment at a specified future time, the transaction

is more characteristic of a loan.

In some transactions it is clear that there is an exchange of approximately equal value, these

transactions are exchange transactions. Refer to the accounting guideline on GRAP 9 for the

recognition, measurement and disclosure of revenue from exchange transactions.

In other transactions an entity will receive revenue and provide no or a nominal consideration

directly in return, these transactions are non-exchange transactions and are dealt with in this

guide.

Revenue arising from non-exchange transactions include, for example:

Transfers, including debt forgiveness, fines, grants, gifts, donations, goods and services

in-kind, bequests and concessionary loans; and

Taxes.

Revenue is the gross inflow of economic benefits or service potential during the reporting period when those inflows result in an increase in net assets, other than increases relating to contributions from owners.

Example: Exchange and non-exchange transactions

Entity EN provides water and electricity to a customer to the value of R5,000. This is an exchange transaction as the entity will receive R5, 000 from the customer in return.

Entity EN received R5,000 from a customer for property taxes. This is a non-exchange transaction as the entity does not provide any services directly to the customer.

GRAP 23 on Revenue from Non-Exchange Transactions

Issued February 2020 Page 7 of 33

3.1 Transactions including exchange and non-exchange components

There are instances where a transaction can be a combination of exchange and non-exchange

transactions. In these instances the entity needs to determine what portion of the transaction

is an exchange transaction and what portion is a non-exchange transaction and then

recognise it separately.

Example: Transaction containing both exchange and non-exchange components

Entity C received R100,000 from Entity M. In return, Entity C provides Entity M with a motor vehicle. The motor vehicle is valued at R300,000.

In this example, Entity C gave more than equal in value to Entity M, i.e. R200,000 in value more.

According to GRAP 23, an asset received for no or nominal consideration should be recognised at its fair value, the difference, i.e. credit entry will be revenue from non-exchange transactions.

In this example, Entity M did give some compensation to Entity C for the motor vehicle, and therefore the difference should be treated as a donation and recognised as revenue from non-exchange transactions.

The transaction should be split and accounted for as follows by Entity M:

1. Debit Credit

R R

Property, Plant and Equipment – Motor vehicle 300,000

Bank 100,000

Revenue from non-exchange transaction – donation 200,000

Recording the receipt of the asset

It is not always immediately clear whether or not a transaction is exchange or non-exchange.

In determining the classification the entity needs to look at the substance of the transaction

and in doing so the entity exercises professional judgement.

Example: Substance of a transaction

Entity L sells goods at R10 per item and if a client buys 100 or more the client will pay only R8.50 per item. Sale of goods at R10 per item is normally classified as an exchange transaction, however if the transaction is conducted at a subsidised price of R8.50, thus a price that is not approximately equal to the fair value of the goods, then the transaction falls within the definition of a non-exchange transaction.

It is in situations like these that the entity should exercise professional judgement and look at the substance of the transaction. The substance of the transaction is that of a sale transaction where bulk discount is given thus the transaction is an exchange transaction.

GRAP 23 on Revenue from Non-Exchange Transactions

Issued February 2020 Page 8 of 33

Where entities receive trade discounts, quantity discounts or other reductions in the quoted

price, it does not necessarily mean that the transaction is a non-exchange transaction and

therefore the transaction should be treated in accordance with the Standard of GRAP on

Revenue from Exchange Transactions. If it is not possible to distinguish between the

exchange and non-exchange components, the transaction should be treated as a non-

exchange transaction.

3.2 Licenses, subscriptions and similar fees

Entities often issue licences such as motor vehicle, fishing, gambling and similar licences as

part of their mandate and/or issue subscription fees to be paid by other entities or the public

in order for the entities to provide a service to them as part of their mandate. These fees can

be either revenue from exchange or non-exchange transactions, depending on the nature and

circumstances of the transaction.

To assist in deciding the correct accounting treatment, the following steps should be

considered:

Step 1:

Apply the principles as in GRAP 109 on Accounting by Principals and Agents, to assess

whether the entity acts as an agent or a principal. If the entity concludes that it acts as the

agent, then no revenue is recognised as the entity is only collecting the fees on behalf of

another party (i.e. the revenue it actually earned). If the entity concluded that it acts as the

principal, and is the issuer of the licence, subscription or similar fees, then consider step 2.

Step 2:

Consider the definitions of exchange and non-exchange transactions.

Interest levied on transactions arising from exchange or non-exchange transactions is classified based on the nature of the underlying transaction, i.e. if the underlying transaction is a non-exchange transaction then any interest levied is also classified as non-exchange, while interest levied on an exchange transaction is classified as exchange.

GRAP 23 on Revenue from Non-Exchange Transactions

Issued February 2020 Page 9 of 33

The following is important in determining whether the revenue is exchange or non-exchange:

Whether the entity provides goods and services directly to the licence or subscription

holder in return for the consideration received; and

The value of the goods or services provided in relation to the consideration received.

In determining whether the substance of a transaction is that of a non-exchange or an

exchange transaction, professional judgement is exercised.

3.3 Stipulations

Stipulations cannot be imposed by an entity on itself, whether or not it was done directly or

through an entity that controls it. Stipulations are enforceable through legal or administrative

processes. If a term in laws or regulations or other binding arrangements is unenforceable

then it is not a stipulation.

Stipulations can either be in the form of conditions or in the form of restrictions. For both

conditions and restrictions a recipient may be required to use the transferred asset for a

particular purpose.

However the difference between a restriction and a condition is that a condition has an

additional requirement which states that the asset or its future economic benefits or service

potential should be returned to the transferor should the recipient not use the asset for the

particular purpose stipulated.

An exchange transaction is one in which the entity receives assets or services, or has liabilities extinguished, and directly gives approximately equal value (primarily in the form of goods, services or use of assets) to the other party in exchange.

A non-exchange transaction is any transaction other than an exchange transaction. In a non-exchange transaction, the entity received value from another entity without directly giving approximately equal value in exchange, or gives value to another entity without directly receiving approximately equal value in exchange.

Stipulations on transferred assets are terms in laws or regulations, or a binding arrangement, imposed upon the use of a transferred asset by entities external to the reporting entity.

GRAP 23 on Revenue from Non-Exchange Transactions

Issued February 2020 Page 10 of 33

3.4 Conditions on transferred assets

Conditions on transferred assets require that the entity either:

Consume the future economic benefits or service potential of the asset as specified; or

Return future economic benefits or service potential to the transferor in the event that the

conditions are breached.

When conditions are attached to a transferred asset, the entity incurs a liability. The entity

has a present obligation to comply with the conditions of the asset or to return the economic

benefits or service potential of the asset to the transferor when the conditions are not met.

Therefore, when a recipient initially recognises an asset that is subject to a condition, the

recipient also incurs a liability.

3.5 Restrictions on transferred assets

Restrictions on transferred assets arise when there is an expectation and/or understanding

about the particular way that the assets will be used. However, there is no requirement that

the transferred asset, or future economic benefits or service potential are to be returned to the

transferor if the assets are not used as per the expectation or understanding. Thus, initially

gaining control of an asset with restrictions does not impose a present obligation on the

recipient and consequently no liability is recognised.

Conditions on transferred assets are stipulations that specify that the future economic benefits or service potential embodied in the asset are required to be consumed by the recipient as specified or future economic benefits or service potential must be returned to the transferor.

Example: Conditions on transferred assets

A museum receives a grant from an overseas funder, requiring the museum to utilise the funds to host a fossil exhibition within the current calendar year, or return the funds within 2 months of the end of the year. The museum will recognise the asset (cash) upon receipt of the grant and will recognise a corresponding liability to the extent that the museum has not yet met the conditions attached to the grant.

Restrictions on transferred assets are stipulations that limit or direct the purposes for which a transferred asset may be used, but do not specify that future economic benefits or service potential is required to be returned to the transferor if not deployed as specified.

GRAP 23 on Revenue from Non-Exchange Transactions

Issued February 2020 Page 11 of 33

When recipients breach a restriction, a third party or the transferor can seek a penalty against

the recipient. Such actions may direct the recipient to fulfil the restrictions or face a civil or

criminal penalty; however such a penalty is not incurred as a result of acquiring the asset, but

as a result of breaching the restriction.

3.6 Substance over form

It could be difficult to decide whether the stipulation represents a condition or restriction. When

determining if a stipulation is a condition or a restriction the recipient has to look at the

substance of the transaction and not just the form.

The fact that the agreement states that the transferred asset should be used for a particular

purpose or be returned to the transferor is not sufficient to classify the stipulation as a

condition. The recipient has to determine if the stipulations are enforceable and if the transferor

will enforce them.

If the recipient’s past experience with the transferor shows that the transferor never enforces

the requirement to return the asset when a breach occurs then the recipient classifies the

stipulations as restrictions although the form of the agreement stipulates conditions.

On the other hand, if the recipient has no experience with the transferor, and the recipient has

no evidence to the contrary, it would assume that the transferor would enforce the stipulations

and therefore the stipulations meet the definition of conditions.

The definition of a condition imposes on the recipient a performance obligation; this

performance obligation should be a consequence of the condition itself.

Example: Restrictions on transferred assets

A museum enters into a funding agreement with an overseas funder whereby overseas funder will transfer R500,000 to the museum specifically to host a fossil exhibition within the current calendar year. Although the overseas funder can turn to the courts to enforce the stipulations in the contract, there is no requirement in the contract that the R500,000 is to be returned to the funder if not used per the agreement. Consequently no liability is recognised.

Performance obligations requires the recipient to consume the future economic benefits or service potential embedded in the transferred asset as specified, or return the asset or other future economic benefits or service potential to the transferor.

GRAP 23 on Revenue from Non-Exchange Transactions

Issued February 2020 Page 12 of 33

A term in a transfer agreement, for example, that requires the entity to perform an action that

it has no alternative but to perform, may lead the entity to conclude that the term is in

substance neither a condition nor a restriction. This is because in these cases, the terms of

the transfer itself do not impose on the recipient entity a performance obligation. This is

especially relevant if the mandate of the entity is the same as the stipulations in the transfer

agreement.

A liability will only be recognised to the extent that an outflow of resources is probable and

performance against the condition is required and can be assessed.

4. Initial Recognition

4.1 Recognition of assets

In order to recognise an asset (inflow of resources), the key recognition criteria that have to be met are:

Entity needs to gain control of the asset as a result of a past event(s);

It is probable that future economic benefits or service potential associated with the asset will flow to the entity; and

The fair value of the asset can be measured reliably.

GRAP 23 on Revenue from Non-Exchange Transactions

Issued February 2020 Page 13 of 33

4.2 Recognition of liabilities

Where an entity receives resources prior to, for example a taxable event occurring or the

existence of a binding arrangement, a liability for ‘revenue received in advance’ should be

recognised and not the relevant liability, e.g. unspent conditional grants (deferred revenue) in

the latter case, until the taxable event occurs or the arrangement becomes binding.

In order to recognise a liability (outflow of resources), the key recognition criteria that have to be met are:

There is a present obligation;

It is probable that an outflow of resources embodying future economic benefits or service potential will be required to settle the obligation; and

A reliable estimate can be made.

Present obligations can arise from stipulations in binding arrangements which state the manner in which the transferred asset(s) should be used for particular purposes.

For example, transfers (through binding arrangements that includes conditions) from national to provincial or local governments or from provincial to local governments, etc.

GRAP 23 on Revenue from Non-Exchange Transactions

Issued February 2020 Page 14 of 33

4.3 Recognition of revenue

Conditions on transferred assets

Only conditions can give rise to present obligations, on initial recognition, of transactions relating to government grants, subsidies, donated assets and other similar transactions.

Therefore stipulations included in agreements related to the inflow of resources should be assessed to determine if they are conditions or restrictions. Refer to the section on Definition and Identification for detail on these three terms.

Conditions on transferred assets

As an entity satisfies the present obligation recognised as a liability, i.e. conditions are attached to the related asset transferred, the carrying amount of the liability is reduced and revenue is recognised to an amount equal to the reduction in the liability.

GRAP 23 on Revenue from Non-Exchange Transactions

Issued February 2020 Page 15 of 33

5. Initial Measurement

5.1 Measurement of assets

Non-monetary assets such as property, plant and equipment, investment property, intangible

assets and heritage assets and inventory, acquired through a non-exchange transaction, are

initially measured at its fair value on acquisition date. This is consistent with the requirement

under the respective standards of GRAP.

Monetary assets can arise from both contractual and statutory (non-contractual)

arrangements. Monetary assets arising out of a contractual agreement, such as cash and

receivables, are initially measured at fair value on acquisition date. Receivables that arise

from statutory (non-contractual) arrangements are also initially measured at fair value on

acquisition date

These assets are subsequently measured, derecognised and disclosed in accordance with

GRAP104 on Financial Instruments on GRAP 108 on Statutory Receivables.

5.2 Measurement of revenue and liabilities

Revenue is measured at the amount equal to the increase in net assets (i.e. the net effect). If

a liability is recognised, revenue will only be recognised to the extent that the liability is not

recognised.

The amount recognised as a liability is the best estimate of the amount required to settle the

present obligation at the reporting date. Refer to the section on Recognition of liabilities for

detail on what will give rise to a present obligation.

Example: Recognition and measurement of assets, revenue and liabilities

Municipality A receives a conditional grant of R20million from the national government to purchase busses for general transport. The grant has to be repaid if not utilised for the specific purpose before the end of the financial year and therefore, the municipality recognises a receivable of R20 million and a corresponding liability of R20 million.

If the municipality spends R15million on busses during the financial year, the condition attached to the grant will be partially satisfied and consequently the liability will be reduced to R5million (R20m – R5m), as that is the remaining amount of the obligation that may have to be repaid.

As the liability is reduced by R15 million, this will result in a corresponding R15 million increase in revenue as the present obligation is satisfied.

GRAP 23 on Revenue from Non-Exchange Transactions

Issued February 2020 Page 16 of 33

6. Transfers

Transfers satisfy the definition of a non-exchange transaction due to the transferor providing

resources (grants, donations, etc.) to the recipient entity without the recipient entity providing

approximately equal value directly in exchange. If a transfer agreement stipulates that the

recipient entity should provide approximately equal value in exchange, then it is an exchange

transaction and will be accounted for under GRAP 9 on Revenue from Exchange

Transactions.

Transfers can be cash or non-cash (i.e. non-monetary item) and include:

Debt forgiveness;

Fines;

Grants;

Gifts and donations;

Goods and services in-kind;

Bequests; and

Concessionary loans.

These will be discussed in more detail in the sections below.

As indicated under the section on Recognition of assets, an asset received from transfers will

be recognised when the transferred resource meets the definition of an asset and satisfy the

recognition criteria.

For the measurement of transferred assets, refer to the section on Measurement of assets for

detail.

6.1 Debt forgiveness

Debt forgiveness is when a lender waives their right to collect a debt owed by an entity,

effectively cancelling the debt.

An entity analyses all stipulations contained in transfer agreements to determine if it incurs a liability when it accepts transferred resources, i.e. it will only incur a liability if the stipulations amount to conditions. Refer to the sections on Identification and Recognition of liabilities for more detail.

GRAP 23 on Revenue from Non-Exchange Transactions

Issued February 2020 Page 17 of 33

In such cases, the receiving entity recognises revenue and a corresponding decrease in the

liability as there is no longer a present obligation to repay the debt.

An increase in net assets and not revenue will be recognised if the debt forgiveness satisfies

the definition of a contribution from owners. Refer to the section on Contributions from owners

for more detail.

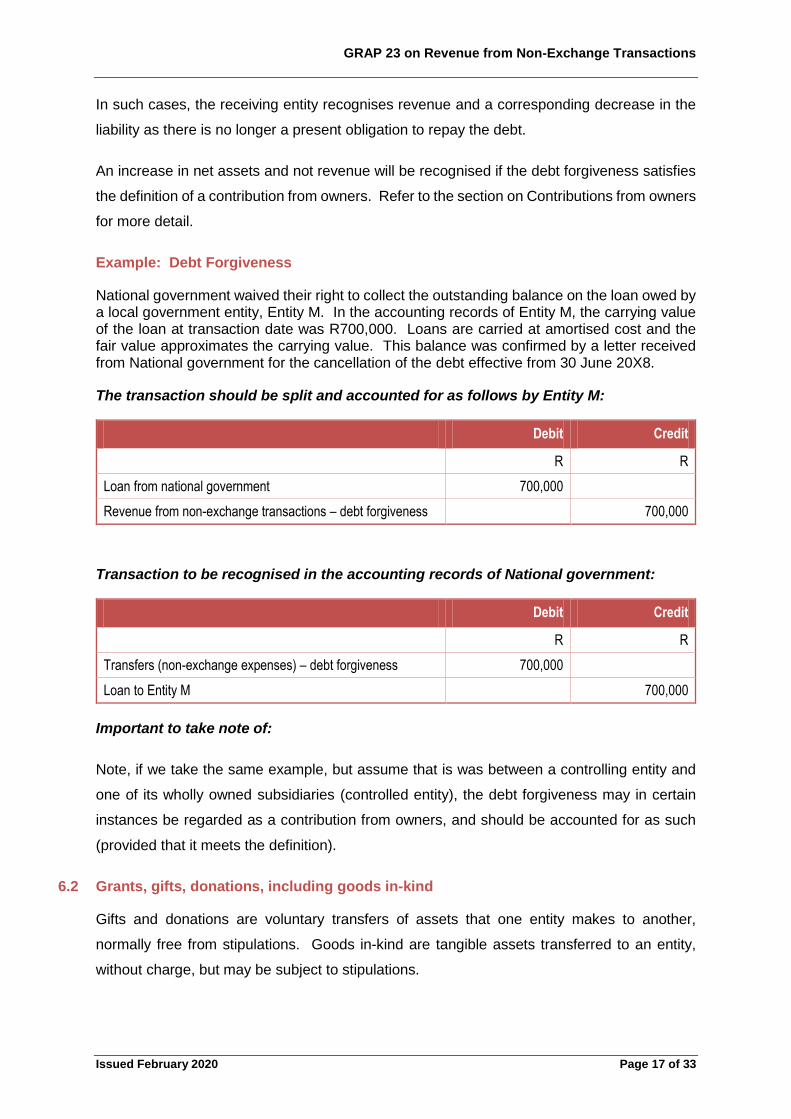

Example: Debt Forgiveness

National government waived their right to collect the outstanding balance on the loan owed by a local government entity, Entity M. In the accounting records of Entity M, the carrying value of the loan at transaction date was R700,000. Loans are carried at amortised cost and the fair value approximates the carrying value. This balance was confirmed by a letter received from National government for the cancellation of the debt effective from 30 June 20X8.

The transaction should be split and accounted for as follows by Entity M:

2. Debit Credit

R R

Loan from national government 700,000

Revenue from non-exchange transactions – debt forgiveness 700,000

Transaction to be recognised in the accounting records of National government:

3. Debit Credit

R R

Transfers (non-exchange expenses) – debt forgiveness 700,000

Loan to Entity M 700,000

Important to take note of:

Note, if we take the same example, but assume that is was between a controlling entity and

one of its wholly owned subsidiaries (controlled entity), the debt forgiveness may in certain

instances be regarded as a contribution from owners, and should be accounted for as such

(provided that it meets the definition).

6.2 Grants, gifts, donations, including goods in-kind

Gifts and donations are voluntary transfers of assets that one entity makes to another,

normally free from stipulations. Goods in-kind are tangible assets transferred to an entity,

without charge, but may be subject to stipulations.

GRAP 23 on Revenue from Non-Exchange Transactions

Issued February 2020 Page 18 of 33

Grants are the actions of government to provide subsidies to entities that benefit the public.

Grants can be in the form of:

Grants to acquire or construct fixed assets (capital grants);

Grants for the furtherance of national and provincial government policy objectives; and

General grants to subsidise the cost incurred by entities in rendering services (operational

grants).

As indicated under the section on Recognition of assets, grants, gifts and donations (other

than services in-kind) are recognised when the definition of an asset is met and the recognition

criteria of an asset are satisfied. The making of a gift or donation and the transfer of legal title

is often simultaneous and in these circumstances there is no doubt as to the future economic

benefits flowing to the entity, however the transfer of legal title does not necessarily have to

happen before the entity will have control over the asset.

For grants, gifts and donations received without conditions attached, revenue is recognised

when the asset is recognised. For grants, gifts and donations received that have conditions

attached to it, a liability will be recognised to the extent that the conditions have not been met,

and will be reduced as the conditions are satisfied with a corresponding increase in revenue.

Example: Grants with conditions

The national government grants R10 million on 1 April 20X7 to Entity G, to be used to improve and maintain the roads system. Specifically, the money is required to be used as follows: 60% for upgrading current roads and 40% to build new roads.

Under the terms of the grant, the money can only be used as stipulated in the current year or to be returned to the national government if not used for its intended purposes.

Past experience with the national government has indicated they are likely to enforce the requirement to return unspent funds. The reporting date is 31 March 20X8.

Accounting treatment of grant received on initial recognition:

The grant money is recognised as an asset when Entity G gains control of the resource due to a past event (the granting of R10 million), Entity G can measure reliably the fair value (R10 million) and it is probable that future service potential associated with the transferred asset will flow to Entity G (in the form of service delivery). Entity G recognises a liability for the conditions attached to the grant.

GRAP 23 on Revenue from Non-Exchange Transactions

Issued February 2020 Page 19 of 33

Initially the grant money will be recognised as follows:

4. 1 April 20X7 Debit Credit

R R

Bank 10,000,000

Unspent conditional grants (under payables in the statement of financial position)

10,000,000

Additional information:

In May 20X7, Entity G builds new roads to the value of R500,000. As the entity satisfies the conditions as it incurs the authorised expenditure, it reduces the liability and recognises revenue in the statement of financial performance in the reporting period during which the liability is discharged.

The R500,000 expenditure incurred (thus the conditions that were met) will be recognised as follows:

5. May 20x7 Debit Credit

R R

Unspent conditional grants (under payables in the statement of financial position)

500,000

Revenue from non-exchange transactions - grants 500,000

The remaining R9.5 million remains as a liability until the conditions are satisfied as stipulated in the agreement.

Goods in-kind are recognised as assets when the goods are received or there is a binding

agreement to receive the goods. If the goods in-kind have conditions attached to it, a liability

will be recognised to the extent that the conditions have not been met, and will be reduced as

the conditions are satisfied with a corresponding increase in revenue.

At initial recognition, gifts and donations including goods in-kind are measured at their fair

value. Due to the nature of these transactions, the fair values might not be readily available

and consequently it may be obtained with reference to market prices or appraisals by a

member of the valuation profession that holds a recognised and relevant professional

qualification. For example, current market prices can usually be obtained for land, vehicles,

and other regularly traded assets.

GRAP 23 on Revenue from Non-Exchange Transactions

Issued February 2020 Page 20 of 33

Example: Donation with no stipulations

Entity D donated a second hand delivery vehicle to Entity R on 15 March 20X8. Entity R started to use the vehicle on 1April 20X8 and the registration into the name of Entity R was finalised on 15 April 20X8.

Entity R concluded that fair value of the vehicle would be the trade-in value rather than the selling value as they are more inclined to trade-in the vehicle for a newer model than to sell it. Entity R phoned three reputable car dealers in town and obtained the trade-in value of the second hand vehicle. The prices obtained did not vary significantly and the average price of R70,000 was used as the fair value.

The asset and revenue is recognised when Entity R gains control of the vehicle due to a past event (the donation) which is 15 March 20X8 (remember that title need not necessarily be transferred in order for Entity R to gain control over the vehicle, unless information available indicates differently).

The transaction should be recorded by Entity R as follows:

6. 15 March 20X8 Debit Credit

R R

Property, plant and equipment – motor vehicles 70,000

Non-exchange revenue - donations 70,000

Example: Donation with stipulations

Land with a fair value of R5 million was donated to Entity P during the reporting period, subject to the stipulations that it be used for public health purposes and not sold for 50 years. The land was acquired by the transferor at a public auction immediately prior to its transfer and the auction price is the fair value.

The stipulations are a restriction thus no liability is recognised. The asset and revenue is recognised when Entity P gains control of the land due to a past event (the donation), Entity P can measure the fair value reliably (R5 million) and it is probable that future service potential associated with the land will flow to Entity P (in the form of service delivery).

The transaction should be recorded by Entity P as follows:

7. Transaction date Debit Credit

R R

Property, plant and equipment – land 5,000,000

Non-exchange revenue - donations 5,000,000

This example’s stipulations amount to restrictions and not conditions as there is no obligation to return the donated asset; therefore no liability will be recognised.

GRAP 23 on Revenue from Non-Exchange Transactions

Issued February 2020 Page 21 of 33

6.3 Services in-kind

Standard states that an entity shall recognise services in-kind that are significant to its

operations and/or service delivery objectives. For example, when an entity that receives

services in kind that are integral to its operations, such as office accommodation paid on its

behalf it should recognise those services in-kind when they meet the definition of an asset and

satisfy the criteria for recognition as assets and shall recognise the related revenue.

It therefore becomes important to determine whether the service in-kind is significant in

relation to its operations (i.e. is an integral part of its operations and/or service delivery

objectives).

Where service in-kind is/are not significant to the entity’s operations and/or service delivery

objectives and/or do not satisfy the criteria for recognition, the entity shall disclose the nature

and type of service in-kind received during the period.

Services in-kind includes services provided by individuals but also includes right of to use of

an asset, without charge, but may be subject to stipulations

Entities may, but are not required to, recognise services in-kind as revenue and as an asset.

Due to the uncertainties surrounding services in-kind, including the ability to exercise control

over the service, and measuring the fair value of the services, entities are not required to

recognise services in-kind. However entities are required to disclose the nature and type of

services in-kind that are material, during the reporting period.

For the recognition criteria of the services in-kind to be recognised, refer to the section on

assets. These assets are, however, immediately consumed and a transaction of equal value

is also recognised to reflect the consumption of the service. In many cases the entity will

recognise an expense for the consumption of the service; however the service may also be

used to construct an asset, in which case the amount recognised is included in the cost of the

asset being constructed.

To the extent that the service in-kind is significant to the operations and/or service delivery

objectives of the recipient of such a service in-kind and it meets the criteria for recognition,

although there maybe uncertainties surrounding services in-kind, including the ability to

exercise control over the services, and measuring the fair value of the services

Revenue is recognised when the asset is recognised.

GRAP 23 on Revenue from Non-Exchange Transactions

Issued February 2020 Page 22 of 33

The following may lead to the entity not being able to recognise the services in-kind as an

asset:

The entity has insufficient control over the services provided; or

The entity may have control over the service provided but may not be able to measure it

reliably.

Example: Services in-kind

Scenario 1

Entity Y’s operation’s include amongst others the provision of essential social service to impoverished squatter camp community it services, but for it to perform this function it needs to have a central accommodation. Since it does not have the necessary funds to hire out such accommodation to fulfil its mandate, Entity X which property has located in same community decided to that they would make available their unused central fully furnished building rent free to Entity Y so that it can perform its function.

Because accommodation is an important part of entity Y’s service delivery objective, the service in-kind will be considered to be a significant and integral part of entity y’s operations, therefore entity Y shall recognise and increase in revenue and a corresponding expensing in the statement of financial performance at the fair value of rent as determined by market in the property industry in the same neighbourhood.

Scenario 2

Hospitals controlled by government received medical services in-kind from medical practitioners as part of the medical profession’s organised volunteer programme.

These services in-kind are recognised as revenue and expenses in the statement of financial performance at their fair value as determined by reference to the medical profession’s published schedule of fees.

Scenario 3

Hospitals, schools and art galleries controlled by the government also received support from volunteers as part of organised programmes for hospital visitor guides, teachers’ aides and art gallery greeters and guides. These volunteers provide valuable support to these entities in achieving their objectives; however, the service provided cannot be measured reliably, as there are no equivalent paid positions available in the local markets and, in absence of volunteers, the services would not be performed.

These services are not recognised in either the statement of financial performance or statement of financial position, but disclosure can be provided about the nature and type of the services received.

6.4 Pledges

Pledges are unenforceable undertakings to transfer assets to the recipient entity. Pledges are

not recognised as assets or revenue because the recipient entity is unable to control the

access of the transferor to the future economic benefits or service potential.

GRAP 23 on Revenue from Non-Exchange Transactions

Issued February 2020 Page 23 of 33

If the pledge item is subsequently transferred to the recipient entity, it is recognised as a gift

or donation. Pledges may warrant disclosure in terms of contingent assets, i.e. the inflow of

future economic benefits or service potential is probable, but not certain. Refer to the

accounting guideline on GRAP 19 for the disclosure requirements of a contingent asset.

6.5 Bequests

A bequest is a transfer made according to the provisions of a deceased person’s will. Revenue

is recognised when the asset is recognised. Bequests are measured at the fair value of the

resources received or receivable.

The fair value of bequeathed assets is determined in the same manner as for gifts and

donations. Refer to the section on Grants, gifts and donations, including goods in-kind for

more detail.

6.6 Advanced receipts

As mentioned in the section on Recognition of liabilities, resources received before a transfer

arrangement becomes binding are recognised as a liability (income received in advance).

When the event that makes the transfer agreement binding occurs and all other conditions

under the agreement are fulfilled, the liability is discharged and revenue is recognised.

Example: Advance receipt with restrictions

National government grants R50 million to Entity B for the increase in stock of social housing by an additional 1,000 units over and above any other planned increase. The grant is for the period 1 July 20X8 to 30 June 20X9. On 1 June 20X8 the National government transfers the R50 million to Entity B. The reporting date is 30 June.

The funding received from National government on 1 June 20X8 is received in advance as the agreement between National government and Entity B is for the period 1 July 20X8 to 30 June 20X9. Thus, a liability is recognised until the agreed date that makes the agreement binding. The stipulation is a restriction, thus no liability was incurred for the stipulation.

Initially the grant money received in advance will be recognised as follows:

8. 1 June 20X8 Debit Credit

R R

Bank 50,000,000

Payables – payments received in advance 50,000,000

The agreement is binding from 1 July 20X8 at which date Entity B will discharge the liability and recognise the revenue (as stated above, there are only restrictions attached to the grant and no conditions).

GRAP 23 on Revenue from Non-Exchange Transactions

Issued February 2020 Page 24 of 33

The recognition of revenue will be recognised as follows:

9. 1 July 20X8 Debit Credit

R R

Payables – payments received in advance 50,000,000

Non-exchange revenue – grants and subsidies 50,000,000

Example: Advance receipt with conditions

National government grants R50 million to Entity B for the increase in stock of social housing by an additional 1,000 units over and above any other planned increase, should the entity not satisfy the restriction, Entity B must return the cash. The grant is for the period 1 July 20X8 to 30 June 20X9. On 1 June 20X8 National government transfers the R50million to Entity B. The reporting date is 30 June.

The funding received in advance will be treated the same way as in the example above.

However, the stipulation is a condition and therefore a liability should be recognised, but this will only occur once the agreement is binding, i.e. when Entity B has a present obligation to satisfy the conditions attached to the grant.

Initially the grant money received in advance will be recognised as follows:

10. 1 June 20X8 Debit Credit

R R

Bank 50,000,000

Payables – payments received in advance 50,000,000

The agreement is binding from 1 July 20X8 at which date Entity B will recognise a liability for the conditions to the agreement not yet met.

The recognition of the liability will be recognised as follows:

11. 1 July 20X8 Debit Credit

R R

Payables – payments received in advance 50,000,000

Unspent conditional grants (under payables in the statement of financial position)

50,000,000

The liability will be discharged and revenue recognised as the conditions of the agreement is satisfied.

GRAP 23 on Revenue from Non-Exchange Transactions

Issued February 2020 Page 25 of 33

6.7 Concessionary loan

The intention of entering into a concessionary loan is to provide or receive resources below

market terms, e.g. loan provided at a below-market interest rate, the repayment terms may be

more flexible or it may not be requirement to repay all or part of the capital provided. This is

referred to as the off-market portion of the loan provided.

The off-market portion of the loan is a non-exchange transaction and is accounted for in

accordance with GRAP 23. The portion of the loan that is repayable, along with any interest

payments, is an exchange transaction and is accounted for in accordance with GRAP 104 on

Financial Instruments.

The off-market portion is calculated as the difference between the proceeds received from the

loan, and the present value of the contractual cash flows of the loan, discounted using a market

related rate of interest (GRAP 104 on Financial Instruments provides guidance on determining

a market related interest rate).

Note that this guide mainly deals with the recognition of the off-market portion as non-

exchange revenue. The actual calculations and treatment of the loan portion are dealt with in

detail in the accounting guideline on GRAP 104.

The recognition of revenue will depend on the nature of any conditions that exist in the loan

agreement that may give rise to a liability. Where a liability exists an entity will recognise

revenue as and when it satisfies the conditions of the loan agreement. For more detail on

conditions and recognition of revenue or a liability, refer to the sections on identification and

initial recognition.

A concessionary loan is a loan received by an entity on terms that are not market related.

Entities may grant concessionary loans for, for example, student loans for tertiary education, housing loans received by low income families, loans to public or other entities to promote economic development.

Entities may receive concessionary loans from, for example, development agencies and other government entities

GRAP 23 on Revenue from Non-Exchange Transactions

Issued February 2020 Page 26 of 33

Example: Determining the non-exchange revenue component in a concessionary loan received

Entity BO received funding to the value of R10 million from the Independent Development Corporation (IDC), for the purposes of improving the infrastructure in the province, over a period of 4 years. The agreement stipulates that the loan should be repaid over 5 years as follows:

Year 1 No capital repayments

Year 2 10% of the capital

Year 3 15% of the capital

Year 4 25% of the capital

Year 5 50% of the capital

Interest is payable annually in arrears at a rate of 6% per annum on the outstanding balance of the loan.

Currently similar debt instruments in the market bear interest at 12% per annum.

Based on the information above, the present value of the cash flows (fair value of loan on initial recognition) amounted to R8,145,396. For details on how this amount was calculated, please refer to the accounting guideline GRAP 104.

Assume that no conditions were attached to the loan received, i.e. the entity was not required to repay the loan to the extent that the centres were not built.

Calculation of off-market portion to be recognised in accordance with GRAP 23:

Proceeds received R10,000,000

Less: Present value of cash flows (fair value of loan on initial recognition) R8,145,396

Off-market portion of loan to be recognised as non-exchange revenue R1,854,604

Journal entries:

12. Year 1 Debit Credit

R R

Bank 10,000,000

Loan 8,145,396

Revenue from non-exchange transactions - subsidy 1,854,604

Initial recognition of concessionary loan received

Note that non-exchange revenue and not a liability is credited as it was assumed that the off-market portion constituted revenue as the loan received had no conditions attached to it.

The journal entries for the repayment of interest and capital and accrual of interest have not been included in this example; refer to the accounting guideline on GRAP 104.

GRAP 23 on Revenue from Non-Exchange Transactions

Issued February 2020 Page 27 of 33

Additional information:

Assume the same information as above, but the loan stipulated that to the extent that infrastructure have not been improved, the funding provided should be returned to IDC (assume that IDC has effective monitoring systems in place and has a past history of requiring any unspent funds to be returned).

The entity spend the funding as follows over the period of four years:

Year 1 10 % of infrastructure approved

Year 2 40 % of infrastructure approved

Year 3 60 % of infrastructure approved

Year 4 100 % of infrastructure approved

Journal entries:

13. Year 1 Debit Credit

R R

Bank 10,000,000

Loan 8,145,396

Unspent conditional grants (under payables in the statement of financial position)

1,854,604

Initial recognition of loan received

Note that a liability is credited and not non-exchange revenue, as a liability exists due to the conditions attached to the loan received.

The following entries will be made at the end of each year for the off-market portion:

14. Year 1 Debit Credit

R R

Unspent conditional grants (under payables in the statement of financial position) (R1,854,604 x 10%)

185,460

Revenue from non-exchange transactions 185,460

Recognising revenue from the off-market portion as and when the conditions are met

15. Year 2 Debit Credit

R R

Unspent conditional grants (under payables in the statement of financial position) [(R1,854,604 x 40%) – R185,460]

556,382

Revenue from non-exchange transactions 556,382

Recognising revenue from the off-market portion as and when the conditions are met

GRAP 23 on Revenue from Non-Exchange Transactions

Issued February 2020 Page 28 of 33

16. Year 3 Debit Credit

R R

Unspent conditional grants (under payables in the statement of financial position) [(R1,854,604 x 60%) – R185,460 – R556,382]]

370,920

Revenue from non-exchange transactions 370,920

Recognising revenue from the off-market portion as and when the conditions are met

17. Year 4 Debit Credit

R R

Unspent conditional grants (under payables in the statement of financial position) [(R1,854,604 x 60%) – R185,460 – R556,382 – 370,920]]

741,842

Revenue from non-exchange transactions 741,842

Recognising revenue from the off-market portion as and when the conditions are met

7. Taxes

Taxes satisfy the definition of a non-exchange transaction due to the taxpayer transferring

resources (tax paid) to government without receiving approximately equal value directly in

exchange.

An entity will recognise an asset in respect of taxes when the taxable event occurs and the

assets recognition criteria are met.

The entity analyses the taxation laws to determine what the taxable events are for the various

taxes levied. Unless laws or regulations specify otherwise, it is likely that the taxable event for

the following is:

Income tax – the earning of assessable income during the taxation period;

Value added tax – the undertaking of vatable activity during the value added tax period by

the vendor;

Customs duty – movement of dutiable goods or service across the customs boundary;

Estate duty – the death of a person owning taxable property; and

Property tax – the passing of the date on which the tax is levied, or the period for which

the tax is levied, if the tax is levied on a periodic basis.

GRAP 23 on Revenue from Non-Exchange Transactions

Issued February 2020 Page 29 of 33

Example: Taxable event for property tax

A municipality levies a tax of 1 percent of the assessed value of all property. The municipality’s reporting period is 1 July 20X7 to 30 June 20X8. The tax is levied on 1 July with notices of assessment being sent to property owners in July, and payment due by 31 August. If taxes are unpaid on that date, property owners incur penalty interest on the late payments at a rate of three percent per month on the amount outstanding. The tax law permits the government to seize and sell a property to collect outstanding taxes.

The taxable event occurs on 31 July 2009 which is the passing of the date on which the tax was levied.

18. 31 July 20X7 Debit Credit

R R

Receivable XXX

Non-exchange revenue – property taxes XXX

Recognising revenue from property taxes

For the recognition criteria of the asset to be recognised, refer to the section on Recognition

of assets.

In many cases, taxes are levied in terms of laws or regulations that impose stipulations that

the taxes be used for a particular purpose. If these stipulations are conditions, the entity is

recognises a liability in respect of any conditions not yet met and it does not recognise revenue

until the conditions are satisfied and the liability is reduced. However, in most cases, taxes

levied for specific purposes are restrictions and not conditions and therefore no liability will

need to be recognised.

Taxation revenue arises only for the government that imposes the tax, and not for other entities. For example, where the national government imposes a tax that is collected by the South African Revenue Services (SARS), assets and revenue accrue to the government and not to SARS. SARS is acting as an agent of the national government.

GRAP 23 on Revenue from Non-Exchange Transactions

Issued February 2020 Page 30 of 33

7.1 Advance receipts of taxes

As mentioned in the section on Recognition of liabilities, taxes received prior to the occurrence

of a taxable event are recognised as a liability (income received in advance). When the

taxable event occurs, the liability is discharged and revenue is recognised.

Example: Advance receipts of taxes

Using the same information as in the example above.

On 25 June 20X8 an individual pays over an amount of R25,000 to the municipality in anticipation of the assessment to be issued on 1 July 20X8.

The R25,000 received from the individual in June 20x8 is an advance receipt of taxes due only on31 August 20X8. The taxable event is the passing of the period in respect of which the tax is levied.

The municipality has to recognise a liability for the advance receipt as follows:

19. 25 June 20X8 Debit Credit

R R

Bank 25,000

Revenue received in advance 25,000

Recognising revenue received in advance from property taxes

7.2 Measurement of assets arising from taxation

For the measurement criteria of an asset to be recognised, refer to the section on

Measurement of assets.

Assets arising from taxation transactions are measured at the best estimate of the inflow of

resources to the entity. In determining the best estimate, the entity may use statistical models

which will give consideration to the following:

The separation between the timing of the taxable event and the collection of taxes;

Declarations made by taxpayers; and

The relationship of taxation receivable to other events in the economy.

Example: Tax revenue likely to be measured reliably

It is likely that the related revenue can be reliably measured for:

Income tax with the submission of tax returns or declaration and/or receipt of payment by the taxpayer and/or employee;

Value added tax with the submission of a tax return or declaration and/or receipt of payment by the vendor;

GRAP 23 on Revenue from Non-Exchange Transactions

Issued February 2020 Page 31 of 33

Customs duty with the submission of a declaration and/or receipt of a payment by the importer or agent;

Estate duty with the submission of a tax return or declaration and/or payment by the executor; or

Rates and taxes with the submission of a declaration and/or payment by the ratepayer.

The actual assets and revenue recognised may differ from the estimates made. If this is the

case then revisions to the estimates are made in accordance with the GRAP 3 on Accounting

Policies, Changes in Accounting Estimates and Errors. Refer to the accounting guideline on

GRAP 3 for the recognition and disclosure of changes in accounting estimates.

GRAP 23 on Revenue from Non-Exchange Transactions

Issued February 2020 Page 32 of 33

8. Entity Specific Guidance

Entities converting from IFRS to GRAP in terms of the ASB Directive 12 on The Selection of

an Appropriate Reporting Framework by Public Entities should consider this comparison of

IAS 20 on Government Grants with GRAP 23.

In terms of IAS 20…..

Compensation for past

expenses or as

immediate financial

support?

Recognise as revenue

in the period in which

the grant becomes

receivable

YES

Recognise as revenue

over the period of the

grant (as expenditure is

incurred)

NO

Grant for future

expenses

An entity receives a

non-monetary asset or

cash towards the

purchase of a non-

monetary asset

Debit asset and credit

deferred revenue

(liability)

Entity received cash

Determine the fair value of the

non-monetary asset received

Entity received an

asset

Is the asset a

depreciable asset?

Recognise revenue

over the useful life of

the asset

YES

Recognise revenue as

and when the

conditions are met

IAS 20 would require deferral of revenue if there are restrictions on the use of the funds (and not only where there are conditions as specified in GRAP 23).

An entity must assess whether any “deferred revenue” recognised in terms of IAS 20 meets the requirements set out in paragraph .50 to .56 of GRAP 23. Any adjustments are as a result in a change in accounting policy as per GRAP 3.

In terms of GRAP 23, revenue is recognised when the conditions are met and not as and when the asset depreciates.

An entity must assess whether any “deferred revenue” recognised in terms of IAS 20 meets the requirements set out in paragraph .50 to .56 of GRAP 23. Any adjustments are as a result in a change in accounting policy as per GRAP 3.

GRAP 23 on Revenue from Non-Exchange Transactions

Issued February 2020 Page 33 of 33

9. Useful links and references

Reference Location of reference

Frequently Asked Questions (FAQs)

on the Standards of GRAP

ASB website:

http://www.asb.co.za/frequently-asked-questions/

IGRAP 1 on Applying The

Probability Test On Initial

Recognition Of Revenue

ASB website:

http://www.asb.co.za/interpretations-approved-

and-effective/

IGRAP 6 on Loyalty Programmes

IGRAP 10 on Assets Received from

Customers

IGRAP 11 on Consolidation –

Special Purpose Entities

IGRAP 18 on Recognition and

Derecogntion of Land

IGRAP 19 on Liabilities to Pay

Levies

IGRAP 20 on Accounting for

Adjustments to Revenue

ASB website:

http://www.asb.co.za/interpretations-approved-

and-not-yet-effective/

Directive 12 on The Selection of an

Appropriate Reporting Framework

by Public Entities

ASB website:

http://www.asb.co.za/directives/

Guideline on The Application of

Materiality to Financial Statements

ASB website:

http://www.asb.co.za/guidelines/

Standard Chart of Accounts for

Local Government (mSCOA)

National Treasury website:

http://mfma.treasury.gov.za

(mSCOA – Municipal Standard Chart of Accounts)

Illustrative Financial Statements for

local government

National Treasury website:

http://mfma.treasury.gov.za

(mSCOA – Municipal Standard Chart of Accounts)

![[Adrian bondy u.s.r. murty] Grap Theory](https://img.dokumen.tips/doc/110x75/55c3a8c8bb61eb210b8b46cd/adrian-bondy-usr-murty-grap-theory.jpg)