Embed Size (px)

Citation preview

GOVERNMENTAL ACCOUNTINGOVERVIEW

ALABAMA ASSOCIATION OF SCHOOL

BUSINESS OFFICIALS

September 16 – 17, 2014

Tuscaloosa, Alabama

Governmental Accounting Overview

“Keren”Dr. Keren H. Deal, CPA, CGFMProfessor of AccountingCollege of BusinessAuburn University MontgomeryP.O. Box 244023Montgomery, Alabama 36124-3792334-244-3971

Disclaimer: Some of the materials in this presentation came from the GASB website, presenter research of topics or presentations at past educational events including GFOAA Summer Conference, AGA PDT, GAAF, etc. Materials presented todayare for educational purposes only.

Governmental Accounting Overview

Today’s Agenda

• Introduction

• Financial Reporting Under Current GASB Standards

• Fund Accounting

• Budgeting

• Activity Funds in Local Schools

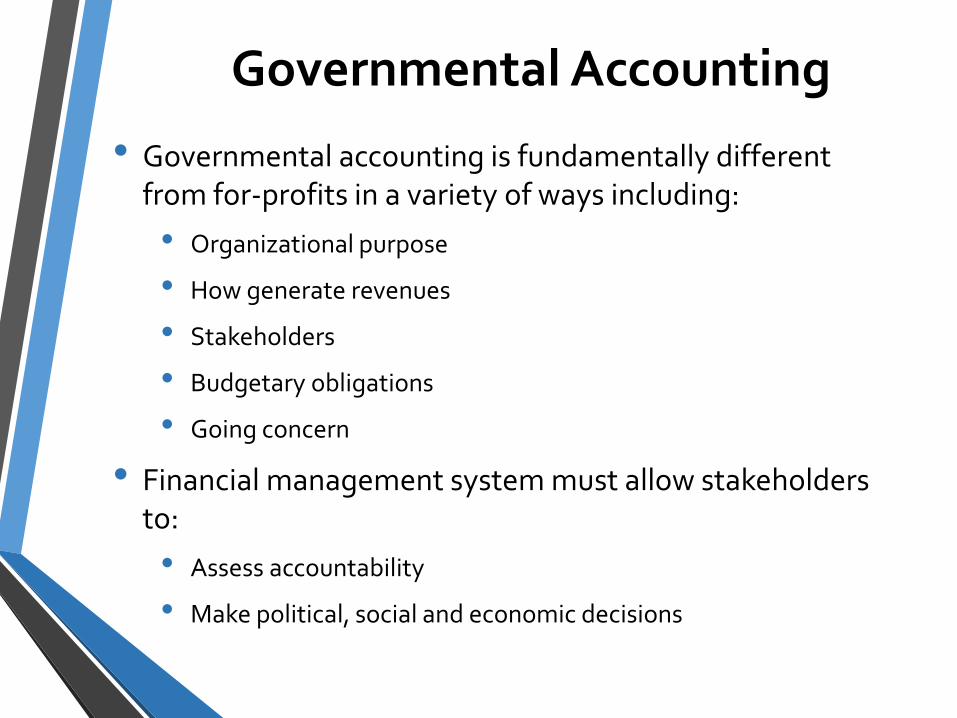

Governmental Accounting

• Governmental accounting is fundamentally different from for-profits in a variety of ways including:

• Organizational purpose

• How generate revenues

• Stakeholders

• Budgetary obligations

• Going concern

• Financial management system must allow stakeholders to:

• Assess accountability

• Make political, social and economic decisions

Governmental Accounting Systems

A governmental accounting system must make it possible to do both:

• To present fairly and with full disclosure the financial position and results of financial operations of the funds and activities of the government in conformity with generally accepted accounting principles (GAAP); and

• To determine and demonstrate compliance with finance-related legal and contractual provisions.

Primary Sources of GAAP for Governments and Not-for-Profits

Governmental

Accounting

Standards Board

State and Local

Government

Organizations

Governmental

Not-for-Profit

Organizations

Governmental Accounting Standards Board (GASB)

• Rule 203 of the Code of Professional Conduct for the American Institute of Certified Public Accountants (AICPA) has given GASB the “authority to establish accounting principles” for SLG.

• GASB’s due process activities are designed to encourage broad public participation in the standards setting process (www.gasb.org).

• GASB has issued 71 Statements to date with 19 Statements issued in past 5 years

GASB’s Financial Reporting –Accountability Emphasis

• Should assist users in evaluating the operating results of the governmental entity for the year.

• Did financial position improve or deteriorate?

• Did entity meet its cash requirements?

• Should assist users in assessing the level of services that can be provided and its ability to meet its obligations as they become due.

• Legal or contractual restrictions on resources?

• Risks of potential loss of resources?

Governmental GAAP Hierarchy

CategoryGASB (STATEMENT 55)

State and Local Governments

A. GASB Statements and Interpretations

B.

GASB Technical Bulletins and,

if cleared by the GASB, AICPA Industry Audit and Accounting Guides and Statements of Position

C. AICPA Practice Bulletins that have been cleared by the GASB

D.

Implementation guides (Q&As) published by the GASB staff, and Practices that are widely recognized and prevalent in state and

local governments.

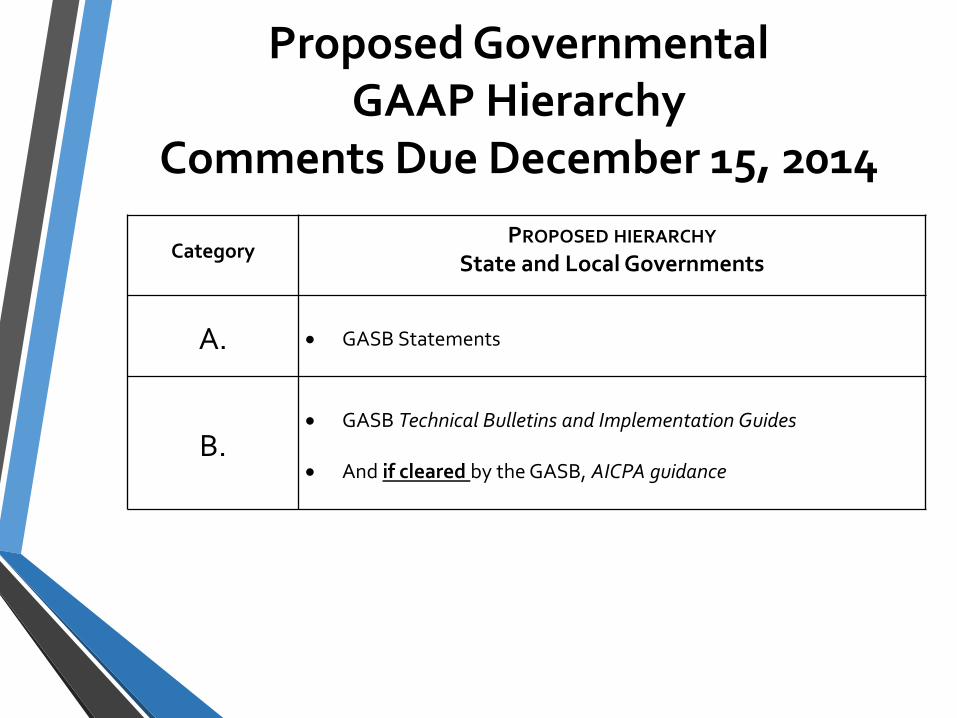

Proposed Governmental GAAP Hierarchy

Comments Due December 15, 2014

CategoryPROPOSED HIERARCHY

State and Local Governments

A. GASB Statements

B. GASB Technical Bulletins and Implementation Guides

And if cleared by the GASB, AICPA guidance

Under the current proposal, what would be non-authoritative?

• GASB Concepts Statements

• Pronouncements of FASB, FASAB, IPSASB, IASB

• AICPA Issue Papers

• Technical Information Service Inquiries and Replies Included in AICPA Technical Practice Aids

• Practices that are widely recognized and prevalent in SLG

• Pronouncements of other professional associations or regulatory agencies

• Accounting textbooks, handbooks and articles

Financial Reporting Under Current GASB Standards

and GuidanceGovernmental Accounting Overview

September 2014

Financial Reporting

• Financial Reporting Overview

• Management Discussion and Analysis (MD&A)

• Basic Financial Statements – Government-Wide

• Fund Financial Statements

• Notes to Financial Statements

• Required Supplementary Information Other Than MD&A

• Alabama State Department of Education Financial Statements

Financial Reporting Overview

• For external reporting purposes, a government may wish to issue general-purpose financial reports

• GASB’s minimum requirements for these reports:

• Management Discussion and Analysis

• Basic Financial Statements

• Required Supplementary Financial Information other than MD&A

Minimum External Financial Reporting Requirements

MD&A

• Introduces Basic Financial Statements

• Objective analysis that is easily readable to help the reader understand the government’s financial position

Basic Financial Statements

• Government-wide statements

• Fund financial statements

• Notes to the financial statements

Required Supplementary

Information

• Budgetary comparison schedules

• Pension and OPEB information, if applicable

• Infrastructure asset information, if applicable

Management Discussion and Analysis (MD&A)

• GASB 37 (issued June 2001)

• Precedes the financial statements.

• Typically prepared by the officials of the school district knowledgeable about financial management and is intended to be readable, objective analysis of financial activity during the fiscal year.

• Serves several purposes:

• Introduces readers to financial statements and provides a framework and context for understanding financial information found in financial reports.

• Should enhance accessibility of financial statements to general public, however, prepared with a knowledgeable user in mind

• Gives officials opportunity to highlight issues they believe are important to financial statement users and what a citizen might miss if they examined statements without that information

MD&A Topics

• Conceptual information about school district’s financial statements

• Function of statements and type of information found in them

• Analysis of information in the financial statements

• Overall financial position AND changes in financial position

• Activities during the fiscal year regarding capital assets and long-term debt

• Currently known facts bearing on the future finances of the school district

• Discernable, verifiable facts known at time of financial statement preparation and audit that might affect future –NOT predictions

Financial Section Pyramid

At a minimum, must present information necessary to support analysis of financial position and results of information including:

• Total assets – distinguish between capital and other• Total liabilities – distinguish between long term and other• Total net assets – distinguish between amounts invested in capital

assets (net of related debt), restricted amounts, and unrestricted amounts

• Program revenues – by major source• General revenues – by major source• Total revenues• Program expenses – at a minimum by function• Total expenses• Contributions and transfers• Special items and extraordinary items• Change in net assets• Beginning and ending net assets

Analysis of Financial Information

MD&A must include an analysis of the overall financial position and results of operations

• Should include both governmental activities and business-type activities (if any) and include reasons for significant changes from the prior year

• Important economic factors – such as changes in tax or employment bases – that significantly affect the year’s operating results

• Should include comments about the significant changes in the fund balance or fund equity of individual funds

Analysis of balances and transactions of individual funds• Should address significant changes in fund balances or fund net

assets and whether restrictions, commitments or other limitations significantly affect the availability of fund resources for future use

Analysis of Financial Information (continued)

• Analysis of significant variations between original and final budget amounts AND final budget amounts and actual budget RESULTS for the General Fund

• Any known reasons for variations that are expected to have significant effect on future services or liquidity

• Description of capital asset and long-term debt activity during the year ◦ Material commitments for capital expenditures◦ Any changes in credit ratings◦ Whether debt limitations affect the financing of planned facilities or

services

• Description of currently known facts, decisions, or conditions that are expected to have material effect on financial position (net assets) OR results of operations (revenues, expenses, and other changes in net assets)

MD&A Breakdown (continued)

• GASB 54 (2010) – Fund balance classifications based on hierarchy of constraints on government’s resources

• Users need to know extent and nature of restraints so they can make determination of availability for future general-purpose spending

• MD&A should include an analysis of balances and transactions of individual funds.

• The analysis should address the reasons for significant changes in TOTAL fund balances or fund net assets and whether restrictions, commitments, or other limitations significantly affect the availability of fund resources for future use.

How did GASB 54 affect MD&A?

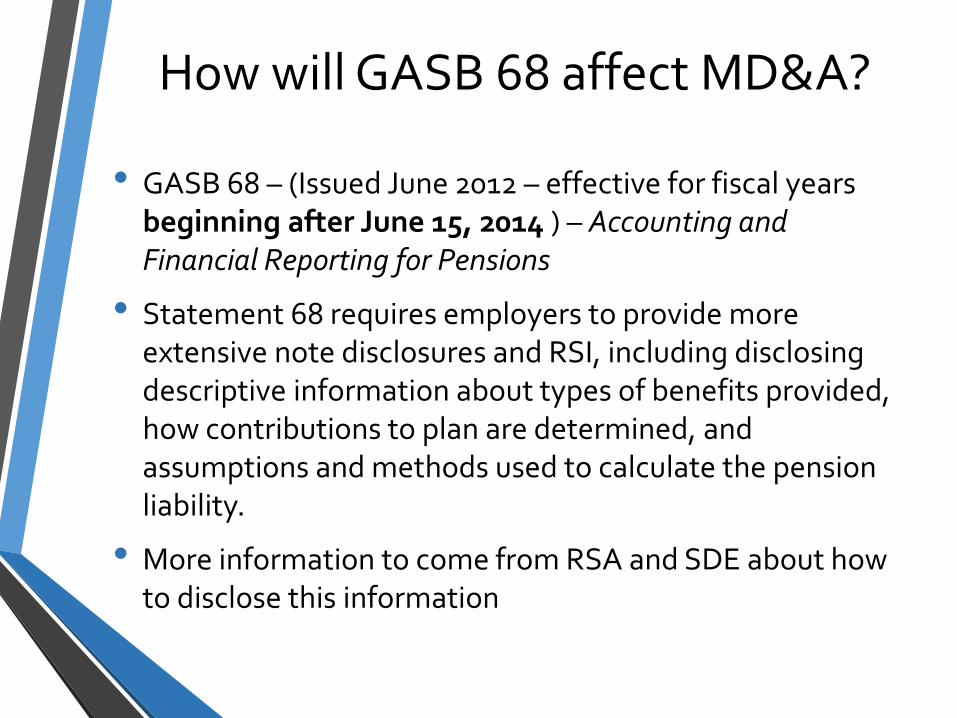

• GASB 68 – (Issued June 2012 – effective for fiscal years beginning after June 15, 2014 ) – Accounting and Financial Reporting for Pensions

• Statement 68 requires employers to provide more extensive note disclosures and RSI, including disclosing descriptive information about types of benefits provided, how contributions to plan are determined, and assumptions and methods used to calculate the pension liability.

• More information to come from RSA and SDE about how to disclose this information

How will GASB 68 affect MD&A?

From RSA Presentation March 2014

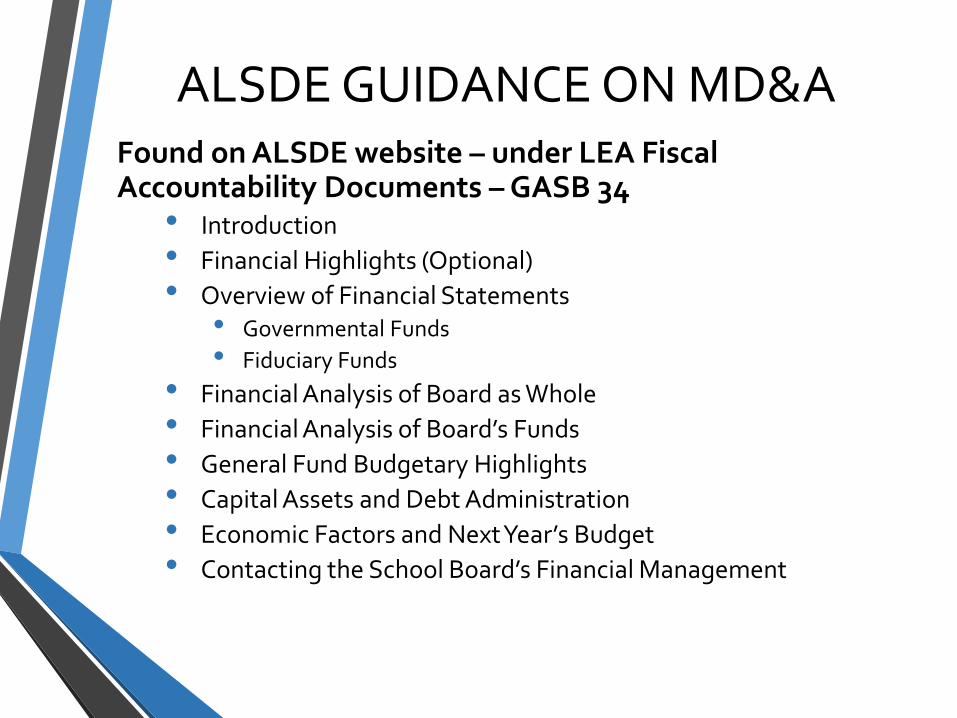

Found on ALSDE website – under LEA Fiscal Accountability Documents – GASB 34

• Introduction

• Financial Highlights (Optional)

• Overview of Financial Statements• Governmental Funds

• Fiduciary Funds

• Financial Analysis of Board as Whole

• Financial Analysis of Board’s Funds

• General Fund Budgetary Highlights

• Capital Assets and Debt Administration

• Economic Factors and Next Year’s Budget

• Contacting the School Board’s Financial Management

ALSDE GUIDANCE ON MD&A

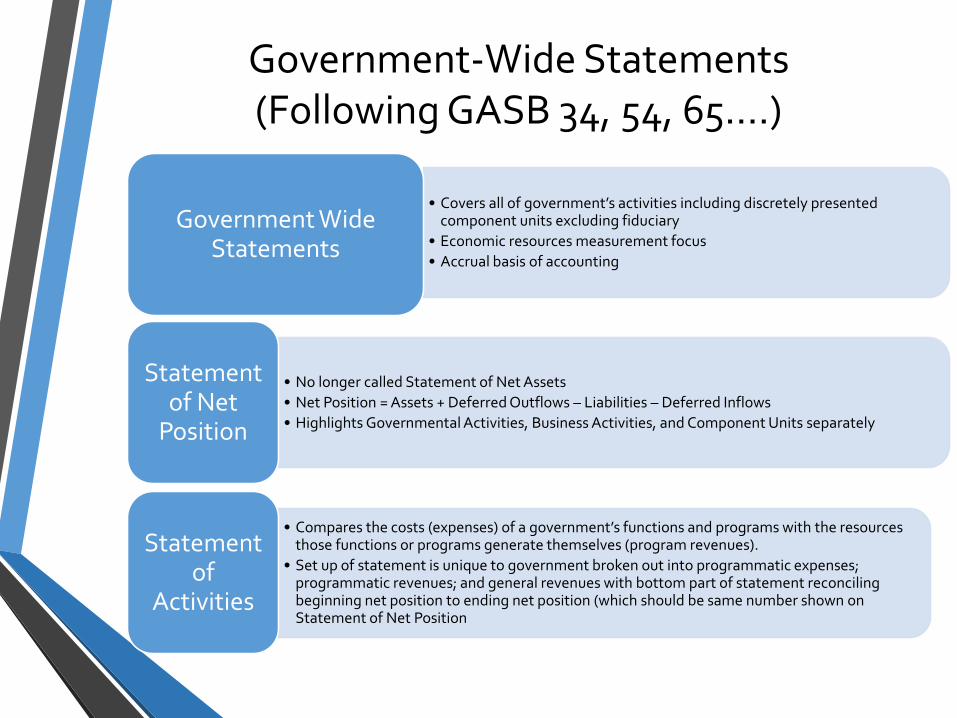

Government-Wide Statements (Following GASB 34, 54, 65….)

• Covers all of government’s activities including discretely presented component units excluding fiduciary

• Economic resources measurement focus

• Accrual basis of accounting

Government Wide Statements

• No longer called Statement of Net Assets

• Net Position = Assets + Deferred Outflows – Liabilities – Deferred Inflows

• Highlights Governmental Activities, Business Activities, and Component Units separately

Statement of Net

Position

• Compares the costs (expenses) of a government’s functions and programs with the resources those functions or programs generate themselves (program revenues).

• Set up of statement is unique to government broken out into programmatic expenses; programmatic revenues; and general revenues with bottom part of statement reconciling beginning net position to ending net position (which should be same number shown on Statement of Net Position

Statement of

Activities

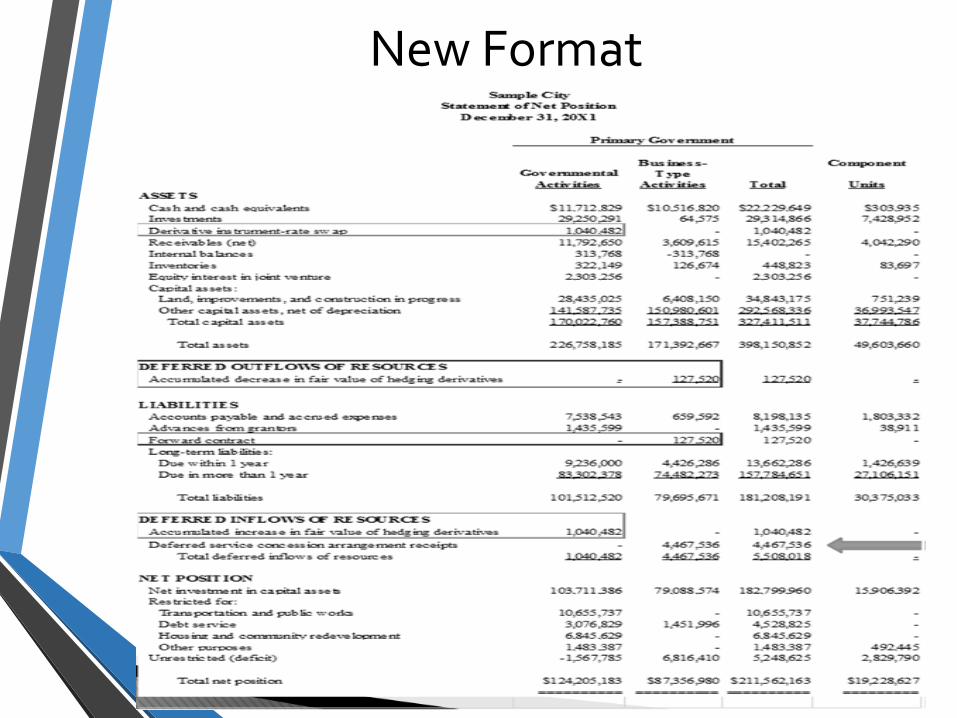

Statement of Net Position

• Presents information in order:

• Assets – listed in order of liquidity with classified format optional

• Deferred Outflows – use of net assets by government applicable to future reporting periods

• Liabilities – listed in order of maturity with classified format optional

• Deferred Inflows – acquisition of net assets by government applicable to future reporting periods

• Net Position – broken out into Net Investment in Capital Assets, Restricted and Unrestricted categories

• Allows for analysis of the governmental entity’s liquidity and financial flexibility

Definitions based on GASB Concepts Statement No. 4

• Assets – resources with present service capacity that the government presently controls.

• Deferred Outflows – consumption of net assets by the government that is applicable to a future reporting period – prepaid items and deferred charges.

• Liabilities – present obligations to sacrifice resources that the government has little or no discretion to avoid

• Deferred Inflows – acquisition of net assets by government applicable to future reporting periods –deferred revenue and advance collections

• Net Position – residual of all other elements presented in Statement of Net Position

Old Format

New Format

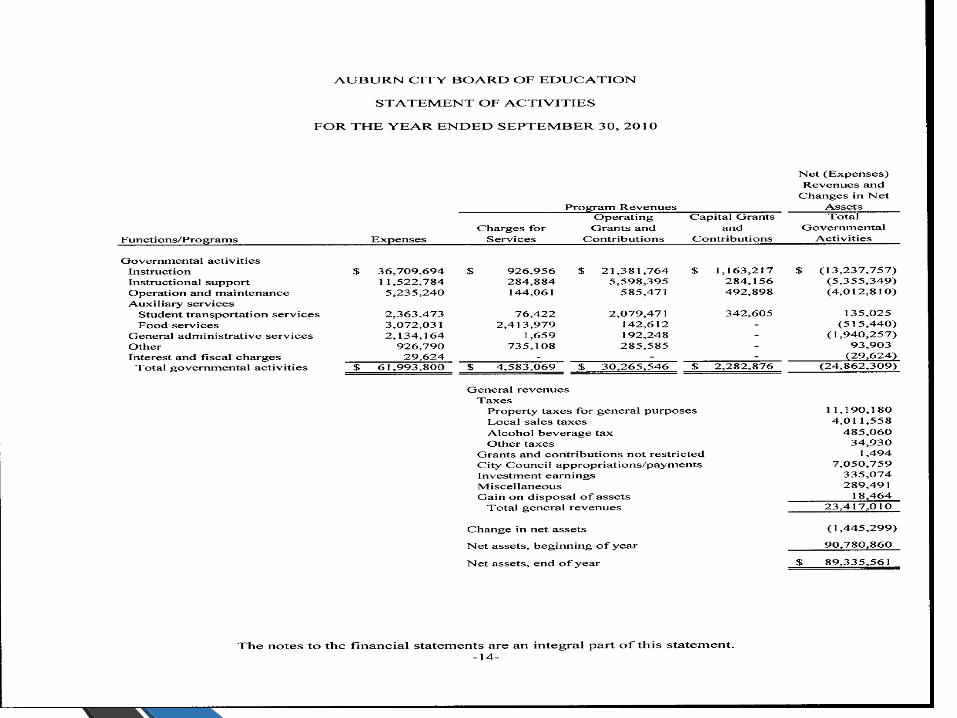

• Expenses – represent the full costs of providing education-related services. Shown by function which is similar activities grouped together.

• Program Revenues – revenues directly related to the functional expenses. Two types:

• Charges for Services – fees to the users or recipients of services

• Grants and Contributions – operating or capital

• Net (Expenses) Revenues and Changes in Net Assets – this part of statement tells the user what the taxpayers will cover with general revenues. NORMAL balance is negative.

• General Revenues – normally property taxes, unrestricted revenues or grants, income from investments.

• Transfers, Gains, Extraordinary Items, Special Items, and Miscellaneous Revenues – if any, shown after General Revenues.

• Reconciliation of Net Position - Beginning to Ending Net Position.

Statement of Activities

• Balance Sheet and Statement of Revenues, Expenditures and Changes in Fund Balance

• A school district typically has governmental and fiduciary funds only.

• Financial statements for governmental funds should be presented using the current financial resourcesmeasurement focus and the modified accrual basis of accounting.

• Revenues should be recognized in the accounting period in which they become available and measurable.

• Expenditures should be recognized in the accounting period in which the fund liability is incurred, if measurable, except for un-matured interest on general long-term liabilities, which should be recognized when due.

Fund Financial Statements

• Assets, resources it controls that enables it to provide services, are generally current in nature—cash, short-term investments, and short-term receivables - most notably absent are capital assets.

• Liabilities are amounts owed (more precisely, virtually unavoidable obligations to sacrifice resources). The liabilities generally are expected to be satisfied within a year. Deferred revenue is shown here, as well.

• After GASB 54 (2012), Fund balance is reported as:

• Nonspendable

• Restricted

• Committed

• Assigned

• Unassigned

• Reserved and Unreserved no longer used

Balance Sheet

• Shown in separate column on governmental fund financial statements

• General Fund is ALWAYS a major fund

• Any fund the SLG considers of significance to users can be reported as major (with note disclosure)

• Governmental fund OR enterprise fund (rare for school districts) has assets, liabilities, revenues, or expenditures/expenses that are at least:

• 10% of total for all governmental and enterprise funds respectively AND

• 5% of total for all governmental and enterprise funds combined

Major Funds

• Nonspendable – resources that cannot be spent, either because they are not in spendable form (inventory) or because they are contractually required to be intact

• Restricted - amounts that can be spent only for the specific purposes stipulated by constitution, external resource providers, or through enabling legislation.

• Committed - amounts that can be used only for the specific purposes determined by a formal action of the government’s highest level of decision-making authority.

• Assigned - intended to be used by the government for specific purposes but do not meet the criteria to be classified as restricted or committed.

• In governmental funds other than the general fund, assigned fund balance represents the remaining amount that is not restricted or committed.

• Unassigned - includes all spendable amounts not contained in the other classifications.

• In other funds, the unassigned classification should be used only to report a deficit balance resulting from overspending for specific purposes for which amounts had been restricted, committed, or assigned.

• Governments are required to disclose information about the processes through which constraints are imposed on amounts in the committed and assigned classifications.

Fund Balance Categories

What about encumbrances?

• There is no separate reporting of encumbrances within the fund balance section of the governmental funds’ balance sheet.

• At the very least, the existence of an encumbrance suggests that the government has an expressed intent to use resources for a particular purpose and therefore these resources should not be classified as unassigned.

• Encumbrance accounting may also be used in the case of contractual obligations, such as construction contracts. Statement 54 requires that resources obligated to contractual obligations be classified as committed.

• Significant encumbrances should be disclosed in the notes along with required disclosures about other commitments.

• Recap - encumbered resources should be reported within the restricted, committed or assigned categories in a manner consistent with the criteria for those classifications.

• Revenues are shown by source or type and there is not a set list of revenue categories that must be shown, nor a required level of detail, which results in some variation from government to government.

• Expenditures generally are shown by function and object with the current operating expenditures presented apart from debt service and capital expenditures.

• Other financing sources and uses include the cash received when bonds are issued, as well as transfers between funds.

• Extraordinary and Special Items presented apart from revenues and expenditures.

Statement of Revenues, Expenditures, and Changes in Fund Balance

Definitions of Elements on Statement of Revenues, Expenditures and Changes in Fund Balance

• Revenues are additions to fund financial sources other than from interfund transfers and debt issue proceeds

• Expenditures are recorded when liabilities are incurred pursuant to authority given in an appropriation. Designates the cost of goods delivered or services rendered, whether paid or unpaid, including current items, provision for interest and debt retirement, and capital outlays.

• Other financing sources are financial inflows other than revenues such as proceeds of general obligation bonds and transfers in.

• Other financing uses are financial outflows other than expenditures such as operating transfers out.

Expenditures Explored Further

• Expenditures are decreases in net financial resources.

• In governmental funds, expenditures are usually recognized in the accounting period in which the goods or services are received and the liability for payment is incurred.

• However, in instances when current financial resources are not reduced as a result of the incurrence of a liability, an expenditure is not recorded.

• Example is liability for compensated absences.

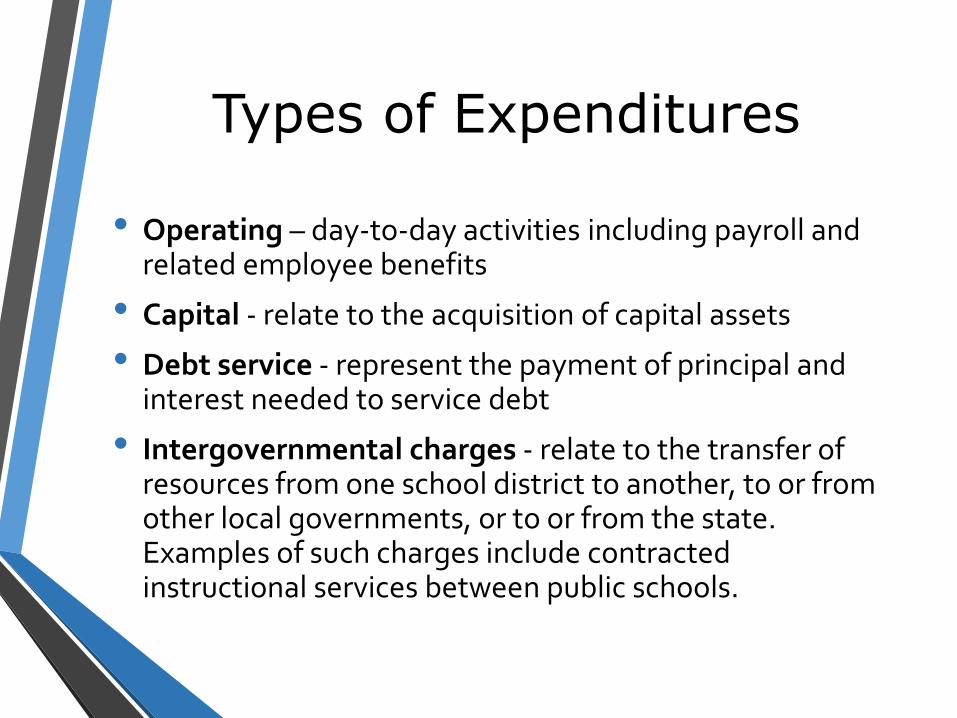

Types of Expenditures

• Operating – day-to-day activities including payroll and related employee benefits

• Capital - relate to the acquisition of capital assets

• Debt service - represent the payment of principal and interest needed to service debt

• Intergovernmental charges - relate to the transfer of resources from one school district to another, to or from other local governments, or to or from the state. Examples of such charges include contracted instructional services between public schools.

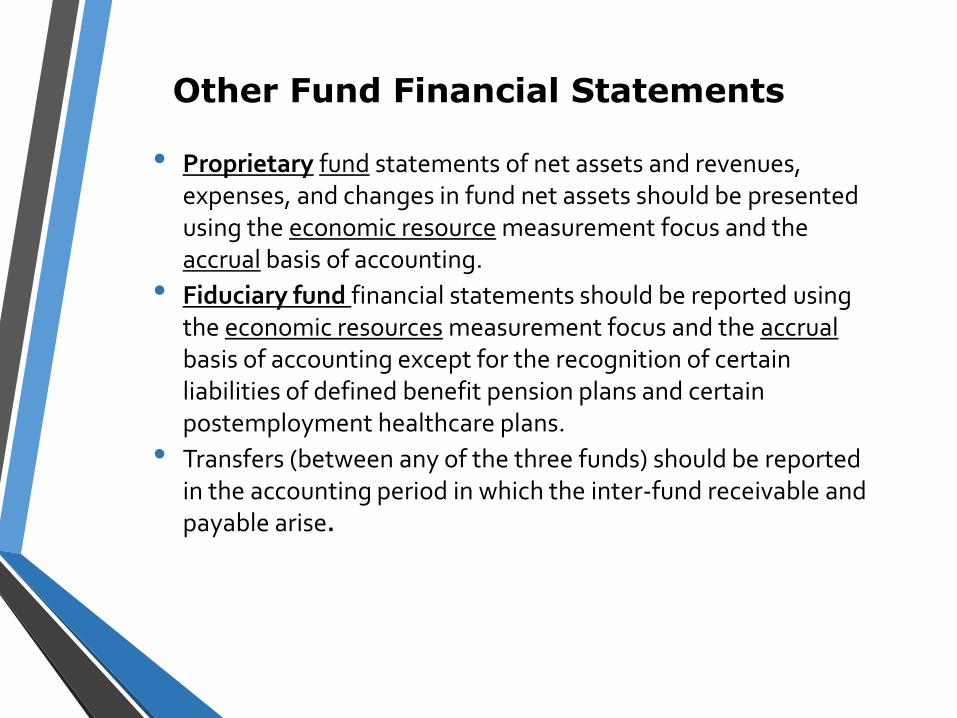

• Proprietary fund statements of net assets and revenues, expenses, and changes in fund net assets should be presented using the economic resource measurement focus and the accrual basis of accounting.

• Fiduciary fund financial statements should be reported using the economic resources measurement focus and the accrualbasis of accounting except for the recognition of certain liabilities of defined benefit pension plans and certain postemployment healthcare plans.

• Transfers (between any of the three funds) should be reported in the accounting period in which the inter-fund receivable and payable arise.

Other Fund Financial Statements

Common Terminology and Classification

• A common terminology and classification should be used consistently throughout the budget, the accounts, and the financial reports.

• Showing budgetary compliance as well as financial position is an important component of government's accountability.

• Readers of financials should be able to assess financial position, ability to provide services, debt load, etc.

Note Disclosures

• Integral part of the basic financial statements

• Summary of significant accounting policies should include:• Brief description of component units and relationships

• Descriptions of activities of major funds, internal service funds, and fiduciary fund types

• Discussion of financial statements and the measurement focus and basis of accounting used in the government-wide statements

• Definition of cash and cash equivalents

• Policy for capitalizing assets and for estimating the useful life of assets

• Policies and procedures for classifying fund balance

• Description of the type of transactions included in program revenues and the policy for allocating indirect expenses to functions in statement of activities

Other Note Disclosures to Include

• Investments

• Receivables

• Capital Assets

• Long-Term Liabilities

• Pensions and Retiree Benefits

• Contingent Liabilities

• Interfund Balances and Transfers

• Reconciliation of Governmental Activities and Governmental Funds

• Additional detail regarding the purposes of restrictions, commitments, and assignments, if the required level of detail is not met through display on the face of the balance sheet

• The decision-making authority and formal action, if any, that results in commitments of fund balance

• The bodies or persons with the authority to express intended uses of resources that result in assigned fund balance

• The order in which a government assumes restricted, committed, assigned, and unassigned amounts are spent when amounts in more than one classification are available for a particular purpose

• Information about minimum fund balance policies

• The purpose for each major special revenue fund, identifying which revenues and other resources are reported in each of those funds.

Note Disclosures Needed under 54

• Risk management activities• Property Taxes• Short-term debt instruments and liquidity• Related party transactions• Capital leases• Joint ventures and jointly governed organizations• Non-exchange transactions not recognized because they are

not measurable• Fund balance designations• Interfund eliminations in fund financials NOT apparent from

headings• Impairment losses when not apparent from headings• Amount of primary government’s net assets at the end of the

reporting period that are RESTRICTED by enabling legislation

Additional Note Disclosures

• NOTE 1: SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES:

• NOTE 2: RECONCILIATION OF FINANCIAL STATEMENTS:

• NOTE 3: STEWARDSHIP, COMPLIANCE, AND ACCOUNTABILITY

• NOTE 4: DEPOSITS AND INVESTMENTS

• NOTE 5: RECEIVABLES AND PAYABLES

• NOTE 6: CAPITAL ASSETS

• NOTE 7: DEFINED BENEFIT PENSION PLAN

• NOTE 8: LONG-TERM OBLIGATIONS

• NOTE 9: SHORT-TERM DEBT

• NOTE 11: RISK MANAGEMENT

• NOTE 12: CONTINGENT LIABILITIES

• NOTE 13: SUBSEQUENT EVENTS

Sample Notes on ALSDE Website

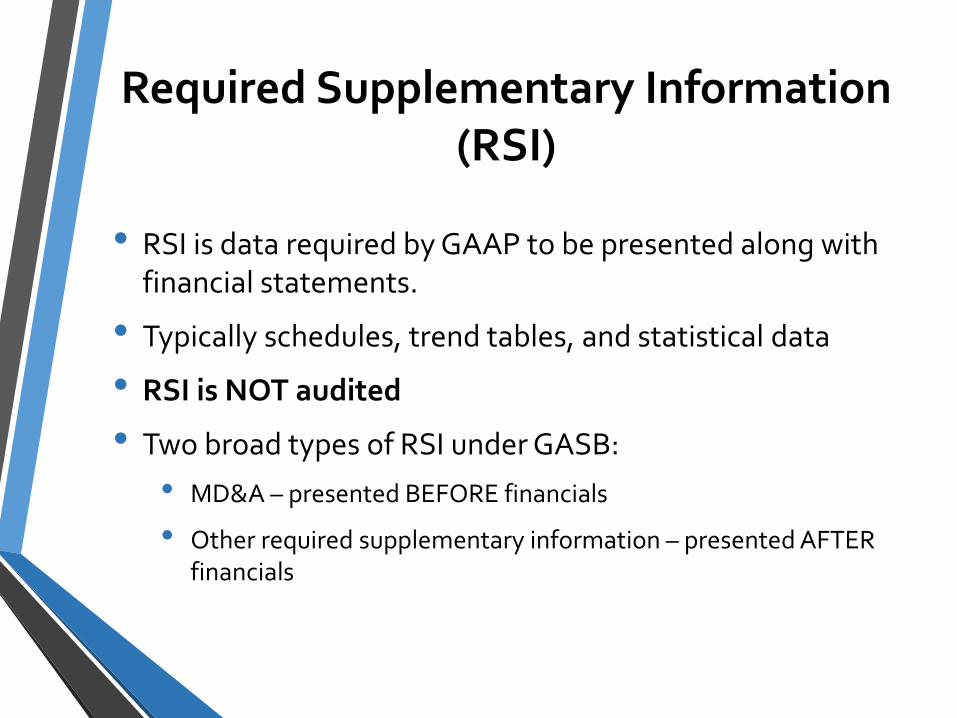

• RSI is data required by GAAP to be presented along with financial statements.

• Typically schedules, trend tables, and statistical data

• RSI is NOT audited

• Two broad types of RSI under GASB:

• MD&A – presented BEFORE financials

• Other required supplementary information – presented AFTER financials

Required Supplementary Information (RSI)

• Budgetary comparison schedules NOT included in basic financial statements

• Pension plan schedule of funding progress and schedule of employer contribution

• OPEB plan schedule of funding progress and schedule of employer contributions

• Certain presentations required for public entity risk pools

• Disclosures required by governments that use modified approach to infrastructure accounting and reporting

Common RSI

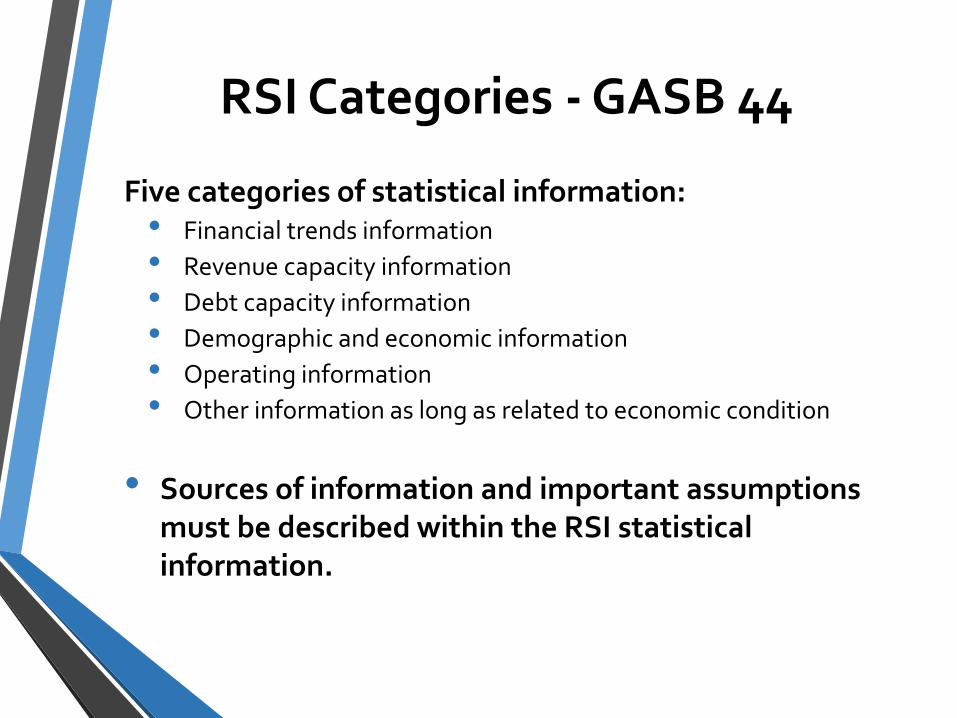

Five categories of statistical information:• Financial trends information

• Revenue capacity information

• Debt capacity information

• Demographic and economic information

• Operating information

• Other information as long as related to economic condition

• Sources of information and important assumptions must be described within the RSI statistical information.

RSI Categories - GASB 44

• Not part of financial section and not audited

• Typically present 10 years of information

• Purpose is to provide historical (trend) information and additional detail to help the financial statement user better understand and assess government’s economic condition

• GASB 44 – Economic Condition Reporting (2004) provides guidance on the content of statistical section

Statistical Section

Fund AccountingGovernmental Accounting Overview

September 2014

Measurement Focus

Economic Resources

• Measures both current and long-term assets and liabilities

• Measurement focus used by “business”

Current Financial Resources

• Measures current financial resources

• No fixed assets or long-term debt

• Unique to state and local governments (SLG)

All About Accountability

• Operational Accountability – flow of economic resources

• Government-Wide Statements

• Proprietary and Fiduciary Fund Level Statements

• Fiscal Accountability – flow of current financial resources

• Governmental Fund Level Statements

Accounting Basis

• Accrual Accounting - revenues are recorded when earned and expenditures/expenses are recorded as soon as they result in liabilities for benefits received.

• Cash payment/receipt does not have an impact on accrual.

• Modified Accrual Accounting – revenues are recorded only if they are measurable and available for paying current period obligations.

Modified Accrual vs. Accrual Basis of Accounting• Accrual

• Recognize revenues when earned

• Match expenses against the revenues when resources or services are used.

• Modified Accrual

• Recognize revenues when measurable and available

• (available to pay this year’s bills— for example, property taxes received within 60 days of year end)

• Recognize expenditures when the liability is incurred — no attempt to match to revenues, match to period of occurrence only

• Exception — recognize interest and principal payments as expenditures when DUE

Comparison

ACCRUAL MODIFIED ACCRUAL

REVENUE earned earned & available

EXPENSE incurred ------

EXPENDITURE ------ incurred

TRANSFERS interfund interfund

rec./pay. arise rec./pay. arise

Fund Accounting

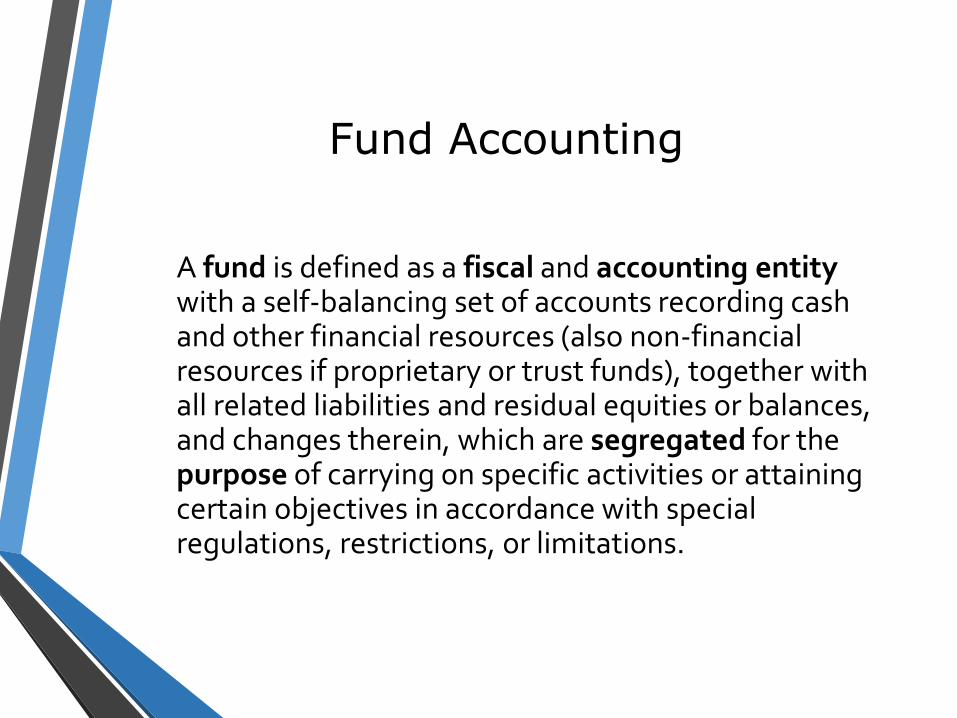

A fund is defined as a fiscal and accounting entitywith a self-balancing set of accounts recording cash and other financial resources (also non-financial resources if proprietary or trust funds), together with all related liabilities and residual equities or balances, and changes therein, which are segregated for the purpose of carrying on specific activities or attaining certain objectives in accordance with special regulations, restrictions, or limitations.

Fund Accounting Systems

Governmental accounting systems should be organized andoperated on a fund basis.

• GASB recommends that governments establish only the minimum number of funds needed to comply with legal requirements and to provide sound fiscal management.

• Minimum Fund Available to Governments – General Fund

Funds have many purposes

• Each fund has its own accounting equation.

• Each fund has its own accounting records.

• Each fund can have its own financial statements.

• Each fund carries on specific activities or attains certain objectives in accordance with special regulations, restrictions or limitations.

Governmental Funds

General Fund Accounts for all financial resources except those

required to be accounted for in another fund.

Special Revenue

Fund***

Account for and report the proceeds of specific revenue

sources that are restricted or committed to expenditure for

specified purpose other than debt service or capital projects.

Capital Projects

Fund

Accounts for and reports those financial resources

restricted, committed or assigned to expenditure for capital

outlays (other than those financed by proprietary and trust

funds)

Debt Service Fund Accounts for and reports those financial resources that are

restricted, committed, or assigned to expenditure for principal

and interest.

Permanent Fund Accounts for legally restricted resources provided by trust in

which the earnings but not the principal may be used for

purposes that support the primary government’s programs.

Proprietary Funds

Enterprise Fund Accounts for operations that are financed and

operated in a manner similar to private enterprises –

where the intent of the governing body is that the

costs (including depreciation) of providing goods or

services to the general public on a continuing basis

be financed or recovered primarily through user

charges; or where the governing body has decided

that periodic determination of revenues earned,

expenses incurred, and/or net income is appropriate

for capital maintenance, public policy, management

control, or other purposes.

Internal Service

Fund

Accounts for financing of good or services

provided by one department or agency to other

departments or agencies of the governmental

unit, or to other governmental units, on a cost

reimbursement basis.

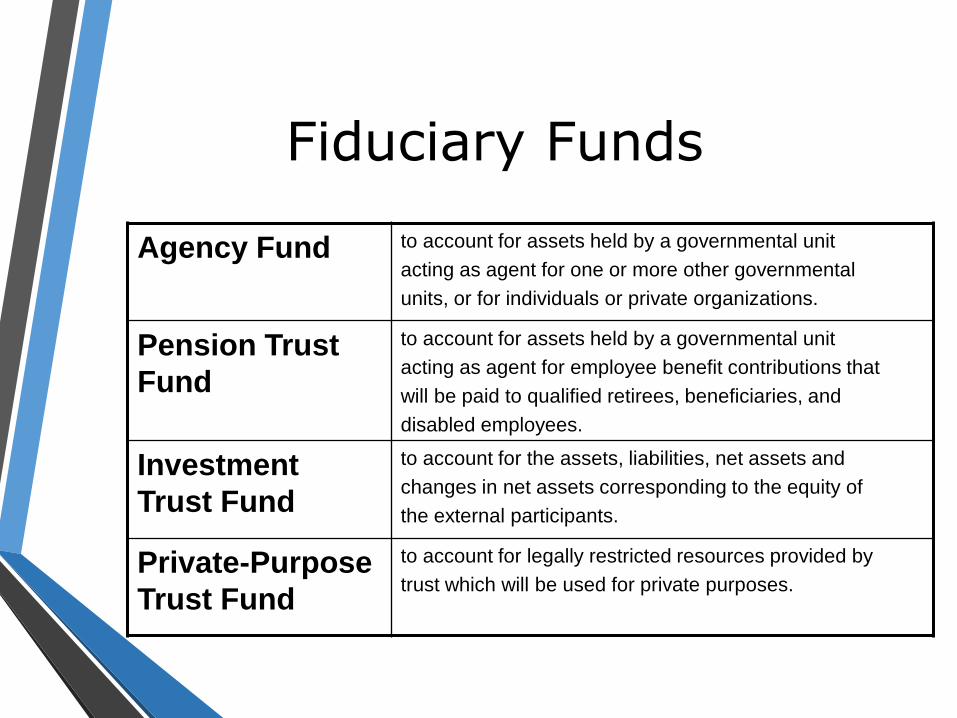

Fiduciary Funds

Agency Fund to account for assets held by a governmental unit

acting as agent for one or more other governmental

units, or for individuals or private organizations.

Pension Trust

Fund

to account for assets held by a governmental unit

acting as agent for employee benefit contributions that

will be paid to qualified retirees, beneficiaries, and

disabled employees.

Investment

Trust Fund

to account for the assets, liabilities, net assets and

changes in net assets corresponding to the equity of

the external participants.

Private-Purpose

Trust Fund

to account for legally restricted resources provided by

trust which will be used for private purposes.

Budgeting Governmental Accounting Overview

September 2014

Budgeting

• A budget is a plan of financial operations embodying an estimate of proposed expenditures for a given period and the proposed means of financing those expenditures for the government.

• Plan to finance public policy expenditures for coming fiscal year.

• Management Control Device

• Legislative Monitoring Device

Code of Alabama - Title 16: Education -Section 16-13A-6 - Required reports

(a) The State Board of Education shall by regulation provide for various financial and other information which local superintendents of education shall have prepared for the local boards of education, including, but not limited to, the following:◦ (1) A monthly financial statement showing the financial status of the local

board of education accounts with itemized categories specified by the State Board of Education.

◦ (2) A monthly report showing all receipts and the sources thereof.◦ (3) A monthly report showing all expenditures with itemized categories

specified by the State Board of Education.◦ (4) An annual projected budget.◦ (5) Monthly and/or quarterly reports showing expenditures relative to

such projected budget.◦ (6) A yearly report of the fixed assets inventory of the local board of

education with itemized categories specified by the State Board of Education.

◦ (7) Financial and other information necessary to participate in national statistical studies on education.

Budgetary Accounting

• GASB standards require governments to present a comparison of budgeted and actual results for the General Fund and special revenue funds with legally adopted budgets.

• While GASB standards guide the format of this comparison, the GASB does not prescribe budgetary accounting practices and does not require governments to maintain budgetary accounts.

• Although budgetary accounts do not appear in the general purpose financial statements, governments typically record budgets and governmental accounting systems are designed to assure compliance with budgets.

Local Education Agency Budgets

• A school budget is an instrument that provides a definite financial policy for direction of the business operations of a school district.

• The budget is one of the most important legal documents of an Alabama school district.

• It is not a static document but rather a working document that changes throughout the year, through board approved budget amendments, as actual financial data change.

• The budgeting cycle (preparation, adoption, implementation, operation, control, and evaluation) is a continuous process.

• Preparation for the next fiscal year must be carried on while implementation, operation, control, and evaluation of the budget for the current year are proceeding to completion.

Definitions of Budgetary Accounts

• Estimated Revenues are expected resource inflows from activities that constitute the normal, operating activities of the entity.

• Unallotted Appropriations are the legal spending limits set by legislative authority which specify planned resource outflows (expenditures) and obligations to be incurred from activities that constitute the normal, operating activities of the entity.

• Allotted Appropriations are the portion of the planned spending amount that are available for commitment by the agency or program.

• Estimated Other Financing Sources are expected resource inflows from events other than estimated revenues.

Definitions of Budgetary Accounts

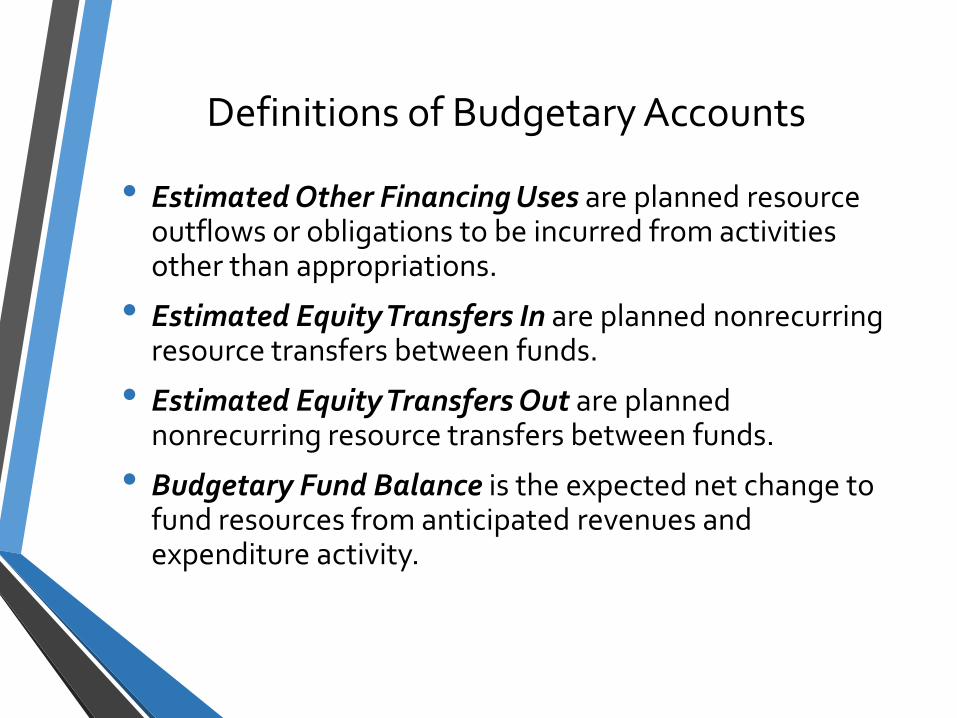

• Estimated Other Financing Uses are planned resource outflows or obligations to be incurred from activities other than appropriations.

• Estimated Equity Transfers In are planned nonrecurring resource transfers between funds.

• Estimated Equity Transfers Out are planned nonrecurring resource transfers between funds.

• Budgetary Fund Balance is the expected net change to fund resources from anticipated revenues and expenditure activity.

Budgeting and Accountability

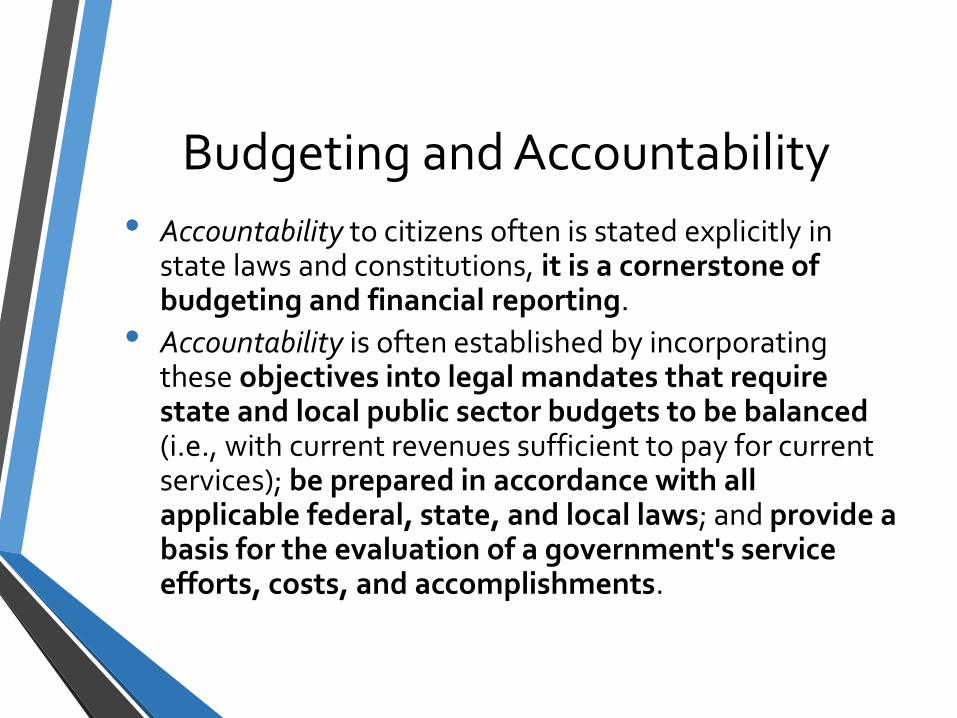

• Accountability to citizens often is stated explicitly in state laws and constitutions, it is a cornerstone of budgeting and financial reporting.

• Accountability is often established by incorporating these objectives into legal mandates that require state and local public sector budgets to be balanced (i.e., with current revenues sufficient to pay for current services); be prepared in accordance with all applicable federal, state, and local laws; and provide a basis for the evaluation of a government's service efforts, costs, and accomplishments.

Budgetary Approaches

• Line-Item Budgeting

• Performance Budgeting

• Zero-Based Budgeting

• Site-Based Budgeting

• Outcome-Focused Budgeting

• Line-Item is still the most popular despite the ‘drive’ to tie budget allocations with performance/outcomes.

Activity Funds in Local Schools Governmental Accounting Overview

September 2014

Activity Funds – Local Schools

• Activity funds are established to direct and account for monies used to support co-curricular and extracurricular student activities.

• Co-curricular activities are any kinds of school-related activities outside the regular classroom that directly add value to the formal or stated curriculum. Co-curricular activities involve a wide range of student clubs and organizations.

• Extracurricular activities encompass a wide variety of other district-directed activities, typified by organized sports and other nonacademic interscholastic competitions.

• Each state may have their own classifications for co-curricular and extracurricular activities.

Activity Fund Classification

• District Activity Funds

• Student Activity Funds

• Parent Support or School Related Organization Funds

District Activity Funds

• District activity funds are those funds that belong to the district which are used to support its co-curricular andextra-curricular activities and are administered by the school district.

• Disbursement of this type of funds rests only with the school board (designee).

• The local education agency determines how district activity fund monies are spent and the district programs that receive support.

Student Activity Funds

• Student activity funds are those funds that support activities that are based in student organizations.

• Students not only participate in the activities of the organization, but also are involved in managing and directing the organization's activities.

• An important distinction is that disbursing monies from the student activity fund may be subject to approval by the student organization and its sponsor, rather than by the board of education or principal.

Parent Support or School Related Organization Funds

• Parent Support or School Related Organizations Funds- support curricular, co-curricular, and extracurricular activities.

• Affiliated organizations include groups such as Parent-Teacher Associations (PTAs), Parent-Teacher Organizations (PTOs), school foundations, and athletic booster clubs.

• Contributions by these groups often include supplies, materials, equipment, and even school facilities, such as weight training rooms.

• Financial records may be included in the school books and classified as non-public funds or may be maintained outside the school records depending on the board’s policy.

• Additional procedures should be in place for those records maintained outside the school financial reporting system.

Funds Maintained Within Local Schools under ALSDE

• Public - Fund 12

• Special Revenue Fund

• Non-public – Fund 32

• Fiduciary Trust Fund

• Various factors must be considered in determining the proper classification, which affects the degree of expenditure restriction.

Public Funds

• Funds are generally classified as public funds when the following criteria are met:

• Money generated school-wide

• Money that can be used for all students

• Money controlled by the Principal or any school employee

• These funds are restricted to the same legal requirements as the Local Education Agency (Board of Education) funds.

Examples of Public Funds

• General

• Library

• Athletic

• Concession and Student Vending

• Fees

• Locker Fees

• Faculty Vending

• Donations

Allowable from Public Funds• Include:

• Professional development training.

• Refreshments expended for an open house at a school where the public would attend.

• Pregame meals for student athletes and coaches.

• Academic incentives for students.

• Athletic and band uniforms for students to participate in school activities.

• Memberships in professional organizations.

• School landscaping, maintenance, furnishings, and decorations.

• Note: Funds received from public (tax) sources or used for public purposes are public funds subject to the control of the school principal.

Non-Public Funds

• Restricted for expenditures subject to the intent and authorization of the organization’s sponsors and officers.

• Not used for general operations of the school.

• The principal does not direct the use of these funds but does have the authority to prohibit inappropriateexpenditures.

Non-Public Funds

• Funds are generally classified as non-public funds when the following criteria are met:

• Money generated for a particular group

• Money used for that particular group

• Money controlled by the students and/or a parental organization

Examples of Non-Public Funds

• Clubs and Classes

• Courtesy or Flower Fund

• Athletic Fundraisers

• Other School Related Organizations

Allowable Expenditures for Nonpublic Funds

• Food for social gatherings.

• Class prom entertainment.

• T-shirts for club members or faculty.

• Donations to various organizations.

• Transfers to other non-public accounts.

• Travel expenses to club events.

• Championship rings.

• Faculty appreciation gifts.

• Scholarships.

• Flowers for funerals.

Important to Note About Non-Public Funds

Non-public funds can become subject to the same expenditure restrictions as public funds if the accounting records do not maintain a separate account for each of the non-public funds.

Questions? Comments?

THANK YOU FOR YOUR ATTENTION!