Embed Size (px)

Citation preview

GOVERNMENT SECURITIES

MANAGEMENT January 8, 2016

Directorate of Government Debt Securities

Directorate General of Budget Financing and Risk Management

Ministry of Finance of The Republic of Indonesia

OUTLINE

1. Government Securities Management and

Financing Strategy 2016

2. Government Securities Performance

3. Crisis Management Protocol & Bond Stabilization

Framework

4. Debt Outstanding & Risk Profile

DISCLAIMER: This presentation does not constitute or form part of and should not be construed as an offer to sell or issue or the solicitation of an offer to buy or acquire securities of the Republic in any jurisdiction or as an inducement to enter into investment activity. No part of this presentation, nor the fact of its distribution, should form the basis of, or be relied on in connection with, any contract or commitment or investment decision whatsoever. This presentation is not and should not be construed as financial, legal, tax, investment or other product advice.

2

Divider title GOVERNMENT SECURITIES FINANCING

STRATEGY 2016

FINANCING TREND, 2004 – 2015

(trillion IDR)

Notes: * Revised Budget 2015 4

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015*

Govt Securities - net 6.9 22.6 36.0 57.2 85.9 99.5 91.1 119.9 159.7 224.7 226.7 297.7

Domestic Loan - - - - - 0.4 0.6 0.8 0.5 1.0 1.7

External Loan - net (28.1) (10.3) (26.6) (26.6) (18.4) (12.4) (4.6) (17.8) (23.5) (5.8) (12.4) (20.0)

Others/Non-Debt - net 42.0 (1.2) 20.0 9.1 16.6 25.5 4.6 28.3 38.1 18.1 (4.3) (56.9)

Budget Defisit, % to GDP 1.1 0.5 0.9 1.3 0.1 1.6 0.7 1.1 1.8 2.3 2.3 1.9

1.1

0.5

0.9

1.3

0.1

1.6

0.7

1.1

1.8

2.3 2.3

1.9

(0.5)

-

0.5

1.0

1.5

2.0

2.5

-50

0

50

100

150

200

250

GENERAL DEBT FINANCING STRATEGY 2016

DEBT POLICY IN 2016 BUDGET

1. Manageable Debt-to-GDP

ratio 2. Financial inclusion &

market deepening

3. Debt issuance for productive

activity 4. Selective external loan

(infrastructure and energy

sector)

5. Loan as an alternative

instrument for financing

6. Active debt management

and ALM

5

Description 2016 BudgetA. Total Revenue 1,822.5

I. Domestic Revenue 1,820.5

1. Taxation 1,546.7

2. Non-Taxation 273.8

II. Grant 2.0

B. Government Spending 2,095.7

I. Central Government Spending 1,325.6

1. Ministerial Spending 784.1

2. Non-Ministerial Spending 541.4

II. Fund Transfer and Village Fund 770.2

C. Primary Balance (88.2)

D. Deficit (273.2)

Deficit to GDP (2.1%)

E. Financing 273.2

I. Domestic 272.8

a. Domestic Banks 5.5

b. Domestic Non-Banks 267.3

1. Government Securities (net) 327.2

2. Capital Injection (48.4)

II. Foreign 0.4

Surplus (Deficit) Funding

GOVERNMENT BUDGET FOR 2016

In IDR Trillion, where applicable

6

GOVERNMENT SECURITIES – INDICATIVE FINANCING

PLAN FOR 2016

Domestic Bonds

International Bonds Issuance (USD, EUR, JPY-denominated)

Weekly Auction:

Conventional securities:

23 x

Islamic securities: 23 x

Non-Auction:

Retail bonds: SR (Q1), SBR (Q2), Sukuk Tabungan

(Q3), and ORI (Q4)

Private Placement Based on request

Issuance of International Bonds as complement to avoid crowding out in domestic market and provide benchmark for corporate issuance, consists of USD, YEN or EURO global bonds

Maximum issuance international bond 30% from target gross

Issuance targets for GDS, Sukuk and ATM target

• Government Debt Securities (SUN): 76 %; • Sukuk: 24% • ATM for Goverrnment Securities (SBN) by auction: 10-12

years.

Instruments Indicative Target (IDR tn)

Preliminary Budget

Government Securities (Net) 327,224

Redemption 187,202

Cash Management 15,000

Buyback 3,000

Government Securities (Gross) 532,426

Composition

Domestic 76%

Auction 66%

Non-Auction 10%

International Bond 24%

7

*(Million IDR)

Budget 2016Realization

(a.o. Jan. 8, 2016)

% Realization to

Revised Budget

2016

Government Securities Net 327,224,357 66,735,500 20.39%

Government Securities Maturing in 2016 and Buyback 215,351,999 8,750,000 4.06%

Issuance Need for 2016 542,576,356 75,485,500 13.91%

Government Debt Securities (GDS) 74,485,500

Domestic GDS 26,000,000

-Coupon GDS 9,250,000

-Conventional T-Bills 2,750,000

-Private Placement 14,000,000

-Retail Bonds -

International Bonds 48,485,500

-USD GMTN 48,485,500

-Euro GMTN -

-Samurai Bonds -

-Domestic GDS -

Government Islamic Debt Securities 1,000,000

Domestic Government Islamic Debt Securities 1,000,000

- IFR/PBS/T-Bills Sukuk (Islamic Fixed Rated Bond/Project Based

Sukuk)

- Retail Sukuk

- Private Placement 1,000,000

Global Sukuk

2016 SECURITIES FINANCING REALIZATION

8

Divider title GOVERNMENT SECURITIES

PERFORMANCE

-10%

0%

10%

20%

30%

40%

50%

60%

-

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

Jan-15 Feb-15 Mar-15 Apr-15 May-15 Jun-15 Jul-15 Aug-15 Sep-15 Oct-15 Nov-15 Dec-15 5-Jan-16

Incoming Bids Awarded Bids Foreign Incoming Bids

Foreign Awarded Bids % Foreign Incoming Bids (RHS)

10

• In the first auction in 2016, foreign incoming bids is Rp6.01T. While during 2015, the average foreign incoming bids

reached 6.87T.

• In the first auction in 2016, total incoming bid = Rp26.20T. During 2015, average incoming bid = Rp20.84T

• In the first auction in 2016, total bid awarded = Rp12.00T. During 2015 average awarded bid = Rp10.59T.

Average incoming bid

2015 = Rp20.84T/auction

Average awarded bid

2015 = Rp10.59T/auction

GDS PRIMARY MARKET PERFORMANCE

as of Jan 5, 2016

10

0%

10%

20%

30%

40%

50%

60%

-

20,000

40,000

60,000

80,000

100,000

120,000

Jan-15 Feb-15 Mar-15 Apr-15 May-15 Jun-15 Jul-15 Aug-15 Sep-15 Oct-15 Nov-15 Dec-15 5-Jan-16

Incoming Bids Awarded Bids Foreign Incoming Bids Foreign Awarded Bids % Foreign Incoming Bids (RHS)

11

• Average bid to cover ratio 2015 = 2.08

• In the first auction in 2016, total incoming bid = Rp26.20T. During 2015, average incoming bid = Rp14.05T

• In the first auction in 2016, total bid awarded = Rp12.00T. During 2015 average awarded bid = Rp6.75T.

Average Awarded Bid

2015 = Rp6.75T

Average Incoming Bid

2015= Rp14.05T

Average Foreign Incoming

Bid 2015= Rp4.65T

GS PRIMARY MARKET PERFORMANCE

as of Jan 5, 2016

11

PRIMARY MARKET PERFORMANCE

GLOBAL BONDS 2016

12

RI0126 RI0146

Issuer

Issuer Ratings BB+ positive (S&P), Baa3 stable (Moody's), BBB- stable (Fitch) BB+ positive (S&P), Baa3 stable (Moody's), BBB- stable (Fitch)

Issue Ratings BB+ (S&P), Baa3 (Moody's), BBB- (Fitch) BB+ (S&P), Baa3 (Moody's), BBB- (Fitch)

Issue USD fixed rate USD fixed rate

Size USD 2,250,000,000.00 USD 1,250,000,000.00

Pricing / Settlement Date December 1 / December 8, 2015 December 1 / December 8, 2015

Maturity January 8, 2026 January 8, 2026

Coupon 4.75% payable semi annually 5.95% payable semi annually

Reoffer Yield / Price 4.800% / 99.599% 6.000% / 99.299%

Format Rule 144A/Reg S Rule 144A/Reg S

Listing SGX-ST SGX-ST

Total Book Order USD 5,500,000,000 USD 2,600,000,000

Distribution Indonesia 14%, Asia 10%, Europe 14%, USA 62% Indonesia 2%, Asia 22%, Europe 26%, USA 50%

Investor TypeFund/Asset Managers 75%, Banks 18%, Private Banks 1%,

Insurance/Pension Funds 4%, Central Banks/Sovereigen Funds 2%

Fund/Asset Managers 71%, Banks 6%, Private Banks 1%,

Insurance/Pension Funds 21%, Central Banks/Sovereigen Funds 1%

Republic of Indonesia

Summary Terms of Offering

2468

10121416182022

Jan'0

9

Apr'0

9

Jul'0

9

Oct'0

9

Jan'1

0

Apr'1

0

Jul'1

0

Oct'1

0

Jan'1

1

Apr'1

1

Jul'1

1

Oct'1

1

Jan'1

2

Apr'1

2

Jul'1

2

Oct'1

2

Jan'1

3

Apr'1

3

Jul'1

3

Oct'1

3

Jan'1

4

Apr'1

4

Jul'1

4

Oct'1

4

Jan'1

5

Apr'1

5

Jul'1

5

Oct'1

5

Jan'1

6

5Y 10Y 15Y 20Y

8.80 (5Y), 8.75 (10Y), 8.90 (15Y), 8.94 (20Y)

4.39 5.88 5.73 5.31

7.91 9.38

5.58

0.22

0.16 0.38 0.41

0.76 0.72

0.63

0.34

1.54 3.07

6.30

8.80

10.15

20.98

-

10.00

20.00

30.00

40.00

2010 2011 2012 2013 2014 2015 7-Jan-16

OUTRIGHT REPO BANK REPO BI

0

5

10

15

20

25

30

35

40

Spread (bid-ask)

As of January 8, 2016 [In Percentage]

Activities of the domestic bonds are growing Yields of Benchmark Series steadily decrease

Bid Ask Spread 10 Y Government Bond Turn Over 10 Y Government Bond

As of January 8, 2016

As of January 7, 2016

SECONDARY MARKET PERFORMANCE

Spread 8.752 bps (ask 8.707 bid

8.797)

13

5.12

7.04

5.15

14.12 12.88

10.75 10.53

3.29

-

3.00

6.00

9.00

12.00

15.00

2008 2009 2010 2011 2012 2013 2014 2015

-

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

20.0

22.0

1Y 2Y 3Y 4Y 5Y 6Y 7Y 8Y 9Y 10Y 15Y 20Y 30Y

11 Jan '16 4 Jan '16

8 Dec '15 9 Feb '12

23 Sep '11 27 Oct '08

13 Sep'05

[in percentage]

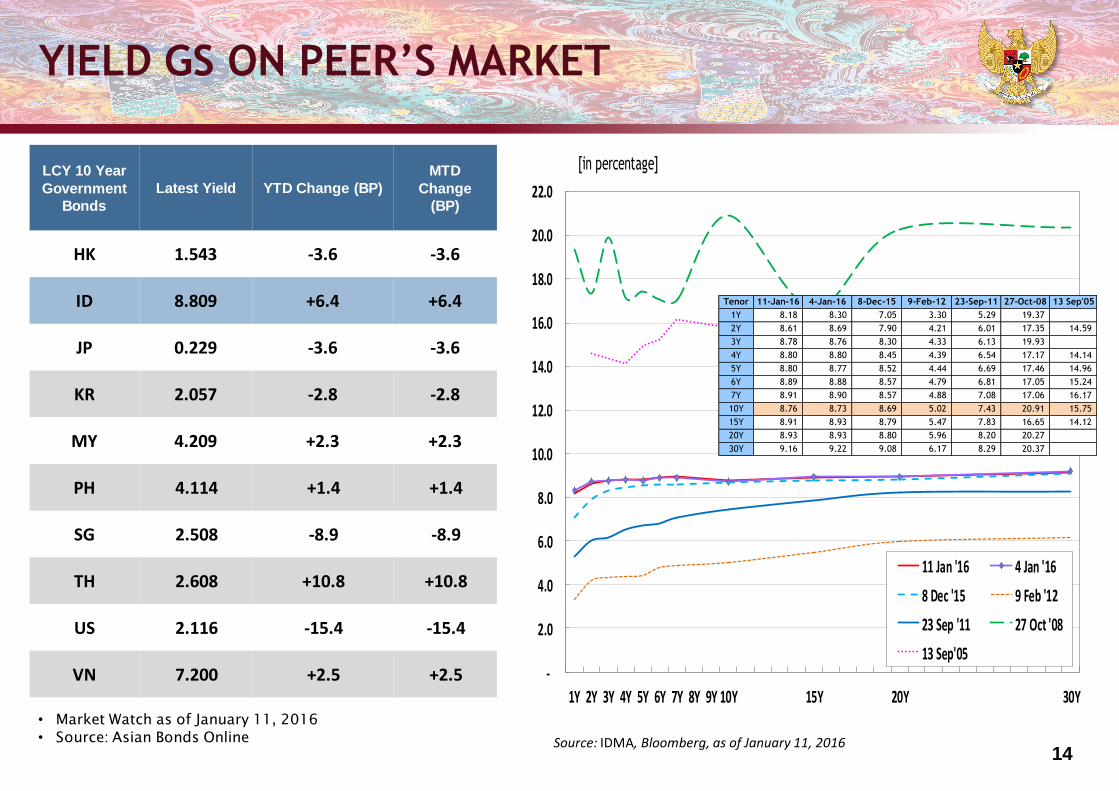

• Market Watch as of January 11, 2016

• Source: Asian Bonds Online

YIELD GS ON PEER’S MARKET

Source: IDMA, Bloomberg, as of January 11, 2016

LCY 10 Year

Government

Bonds

Latest Yield YTD Change (BP)

MTD

Change

(BP)

HK 1.543 -3.6 -3.6

ID 8.809 +6.4 +6.4

JP 0.229 -3.6 -3.6

KR 2.057 -2.8 -2.8

MY 4.209 +2.3 +2.3

PH 4.114 +1.4 +1.4

SG 2.508 -8.9 -8.9

TH 2.608 +10.8 +10.8

US 2.116 -15.4 -15.4

VN 7.200 +2.5 +2.5

Tenor 11-Jan-16 4-Jan-16 8-Dec-15 9-Feb-12 23-Sep-11 27-Oct-08 13 Sep'05

1Y 8.18 8.30 7.05 3.30 5.29 19.37

2Y 8.61 8.69 7.90 4.21 6.01 17.35 14.59

3Y 8.78 8.76 8.30 4.33 6.13 19.93

4Y 8.80 8.80 8.45 4.39 6.54 17.17 14.14

5Y 8.80 8.77 8.52 4.44 6.69 17.46 14.96

6Y 8.89 8.88 8.57 4.79 6.81 17.05 15.24

7Y 8.91 8.90 8.57 4.88 7.08 17.06 16.17

10Y 8.76 8.73 8.69 5.02 7.43 20.91 15.75

15Y 8.91 8.93 8.79 5.47 7.83 16.65 14.12

20Y 8.93 8.93 8.80 5.96 8.20 20.27

30Y 9.16 9.22 9.08 6.17 8.29 20.37

14

OWNERSHIP OF TRADABLE DOMESTIC

GOVERNMENT SECURITIES (in trillion Rp)

`

Banks 217,27 33,88% 265,03 36,63% 299,66 36,73% 335,43 33,70% 375,55 31,04% 372,66 29,95% 369,11 27,21% 413,99 28,79% 350,07 23,95% 435,84 29,75%

Govt Institutions (Bank Indonesia*) 17,42 2,72% 7,84 1,08% 3,07 0,37% 44,44 4,47% 41,63 3,44% 38,37 3,08% 80,58 5,94% 67,09 4,67% 148,91 10,19% 64,81 4,42%

Non-Banks 406,53 63,40% 450,75 62,29% 517,53 63,09% 615,38 61,83% 792,78 65,52% 833,42 66,97% 906,74 66,85% 956,85 66,54% 962,86 65,87% 964,44 65,83%

Mutual Funds 51,16 7,98% 47,22 6,53% 43,19 5,27% 42,50 4,27% 45,79 3,78% 47,16 3,79% 56,28 4,15% 59,47 4,14% 61,60 4,21% 61,82 4,22%

Insurance Company 79,30 12,37% 93,09 12,86% 83,42 10,17% 129,55 13,02% 150,60 12,45% 149,95 12,05% 161,81 11,93% 170,86 11,88% 171,62 11,74% 172,80 11,79%

Foreign Holders 195,76 30,53% 222,86 30,80% 270,52 32,98% 323,83 32,54% 461,35 38,13% 500,83 40,25% 537,53 39,63% 548,52 38,15% 558,52 38,21% 558,49 38,12%

Foreign Govt's&Central Banks** 50,06 6,10% 78,39 7,88% 103,42 8,55% 104,66 8,41% 102,34 7,54% 109,49 7,61% 110,32 7,55% 109,58 7,48%

Pension Fund 36,75 5,73% 34,39 4,75% 56,46 6,88% 39,47 3,97% 43,30 3,58% 43,00 3,46% 46,32 3,42% 48,69 3,39% 49,83 3,41% 50,27 3,43%

Securities Company 0,13 0,02% 0,14 0,02% 0,30 0,04% 0,88 0,09% 0,81 0,07% 0,65 0,05% 0,74 0,05% 0,15 0,01% 0,26 0,02% 0,19 0,01%

Individual 32,48 3,26% 30,41 2,51% 28,35 2,28% 32,23 2,38% 52,40 3,64% 42,53 2,91% 42,46 2,90%

Others 43,43 6,77% 53,05 7,33% 63,64 7,76% 46,68 4,69% 60,51 5,00% 63,49 5,10% 71,82 5,29% 76,76 5,34% 78,50 5,37% 78,42 5,35%

Total 641,21 100% 723,61 100% 820,27 100% 995,25 100% 1.209,96 100% 1.244,45 100% 1.356,43 100% 1.437,93 100% 1.461,85 100% 1.465,10 100%

1) Including ownership of SBSN (government sukuk).

2) Foreign are consisted of Private Banking, Fund/Asset Management, Securities, Insurance, Pension Fund.

3) Others are consisted of Corporation, Individual, Foundation.

*) Since February 8th, 2008, repo transaction of Government Securities to Bank Indonesia was included.

**) Since November 21, 2014, foreign government(s) was included to the same category as foreign central bank(s).

Dec-13Dec-12Dec-11Dec-10 Dec-14 Jan-15 Jun-15 Nov-15 Dec-15 Jan-7-2016

15

FOREIGN INVESTOR ACTIVITY (YEARLY)

Foreign Net Buy/Sell up to September (YTD) & yearly total (IDR) trillion)

Investors Net Buy/Sell (IDR trillion)

Source: Bank Indonesia

• Foreign investors (Asing) recorded a net buy of IDR0.13 trillion (year to date).

Note: as of November 25, 2015

2011 2012 2013 2014 2015 2016

Domestic 55.29 49.00 121.68 77.19 154.71 (0.13)

Foreign 27.10 47.67 53.31 137.52 97.17 0.13

Total 82.39 96.66 174.99 214.71 251.88 0.00

27.10

47.67

53.31

137.52

97.17

0.13

13.11

2.68

4.82

39.48

0.13

0 20 40 60 80 100 120 140 160

2011

2012

2013

2014

2015

2016

Januari YTD

16

90.1

108.4

141.5 136.5

156.4 169.5

180.4 185.1 190.6 191.3

27.9%

27.4%

21.9%22.6% 19.7% 18.4% 16.9%

16.7% 16.5% 17.9%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

0

20

40

60

80

100

120

140

160

180

200

2008 2009 2010 2011 2012 2013 Dec-14 Feb-15 Jun-15 Oct-15

Govt. Securities (GS) Bond Deposit Stock Mutual Funds Others Total Investment (in Trillion) % GS to Total Investment (RHS)

241.7

326.2356.5 361.4

497.0 505.5

552.3

610.1650.2 647.2

27.09%

24.01%

21.77%

24.11%

19.74%20.71%

12.79%

22.79% 22.86% 23.57%

0.00%

10.00%

20.00%

30.00%

0

100

200

300

400

500

600

700

2008 2009 2010 2011 2012 2013 Mar-14 Dec-14 May-15 Oct-15

Govt. Securities (GS) Bond Deposit Stock Mutual Funds Others Total Investment (in Trillion) % GS to Total Investment (RHS)

DOMESTIC INSTITUTIONAL INVESTORS

Insurance Company

Source: Financial Service Authority (OJK), data processsed

Pension Fund

17

FOREIGN INVESTOR ACTIVITY

Net Buyer (Seller) - Non Resident Foreign Ownership - Proportion by Tenor [In IDR Trillion]

Foreign investors mostly dominated by high quality long term investors

As of January 8, 2015

5,20% 4,65% 5,38% 4,45% 3,33% 3,31% 3,85% 3,23% 2,66%

5,41%3,73% 2,89%

2,34%1,54% 1,51% 1,54% 1,28% 1,25%

12,88% 15,23% 12,92%12,46%

11,43% 11,02% 12,30% 11,82% 12,00%

32,04% 33,58%34,88%

36,18%39,69% 39,50%

36,98%38,98% 39,16%

44,46% 42,81% 43,94% 44,56% 44,00% 44,67% 45,33% 44,68% 44,93%

32,54%

38,13% 38,61% 39,63%37,59% 37,10% 38,15% 38,21% 38,17%

0%

20%

40%

60%

80%

100%

Dec 13 Dec 14 Mar-15 Jun-15 Sep-15 Oct-15 Nov-15 Dec-15 Jan-8'15

0-1 ≥1-2 ≥2-5 ≥5-10 ≥10 %Foreign Ownership of Total

2,68

8,44

(0,88)

17,97

4,22

(19,98)

2,81

(1,76)

10,13

23,98

6,08

(0,37)

4,82

16,49 15,77 16,10

20,15

6,43

14,67 15,95

13,17 12,49

21,34

(19,84)

39,48

6,84

(3,59)

4,10 6,31

23,04

(3,90)

(7,96)

(2,30)

5,39

8,38

21,37

-0,08

-0,06

-0,04

-0,02

0

0,02

0,04

0,06

0,08

0,1

(30,00)

(20,00)

(10,00)

0,00

10,00

20,00

30,00

40,00

50,00

Jan

-13

Ma

r-1

3

Ma

y-1

3

Jul-

13

Se

p-1

3

No

v-1

3

Jan

-14

Ma

r-1

4

Ma

y-1

4

Jul-

14

Se

p-1

4

No

v-1

4

Jan

-15

Ma

r-1

5

Ma

y-1

5

Jul-

15

Se

p-1

5

No

v-1

5

Jan

-16

Capital Inflows [LHS] capital inflows over foreign [RHS]

18

Divider title CRISIS MANAGEMENT PROTOCOL&

BOND STABILIZATION FRAMEWORK

Pre-emptive Measures

Implementing Crisis Management Protocol

(CMP)

Implementing Bond Stabilization Framework

(BSF)

Enhancing coordination between government

institutions and continuous dialogue with market

participants

Specific policies in place to address crises

enacted in 2016 budget law

Swap facility arrangements based on international cooperation

Crisis Management Protocol

Indicators to determine crisis level of

Government Securities Market condition (normal,

aware, alert, crisis)

Several market indicators that are monitored

daily:

- Yield of benchmark series;

- Exchange rate;

- Jakarta Composite Index;

- Foreign ownership in government securities

Policies to address the crisis at every level :

- Repurchase the government securities at

secondary market

- Postpone or stop the issuance

First Line of Defense

State’s Budget

Buyback fund at DG of Budget Financing

and Risk Management

Investment fund at Public Service Agency

(BLU) (min. level Aware)

State Owned Enterprises

(BUMN)’s Budget Related BUMNs (min. level Aware)

Social Security Organizing

Agency (BPJS)’s Budget BPJS (min. level Aware)

Second Line of Defense

State’s Budget

State General Treasury Account

(Rekening KUN) (min. level Alert)

Accumulated cash surplus (SAL) (min.

Level Crisis)

State Owned Enterprises

(BUMN)’s Budget Related BUMNs (min. level Alert)

Social Security Organizing

Agency (BPJS)’s Budget BPJS (min. level Alert)

Bond Stabilization Framework

Implement Measures to Manage External Volatility …to mitigate sudden reversals

20

Divider title DEBT OUTSTANDING &

RISK PROFILE

- 20 40 60 80

100 120 140 160 180 200 220 240

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

2026

2027

2028

2029

2030

2031

2032

2033

2034

2035

2036

2037

2038

2039

2040

2041

2042

2043

2044

2045

2046

-206

0

Loan Gov't Sec

020406080

100120140160180200220240

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

2026

2027

2028

2029

2030

2031

2032

2033

2034

2035

2036

2037

2038

2039

2040

2041

2042

2043

2044

2045

2046

-206

0

Domestic Foreign

TOTAL DEBT MATURITY PROFILE AS OF

END OF NOVEMBER, 2015

Maturity Profile of Central Government by Instruments (in trillion IDR)

Maturity Profile of Central Government by Currencies (in trillion IDR)

44%56%

Foreign Domestic

76%

24%

Gov't Sec Loan

22

Notes: • * Preliminary Figures

OUTSTANDING CENTRAL GOVERNMENT DEBT

BY INSTRUMENT

Nominal %

a. Foreign Loan (in billion USD) 68,6 68,4 63,6 58,4 53,9 53,6 24,1%

Bilateral 42,3 42,1 37,2 31,5 26,7 24,6 11,1%

Multilateral 23,2 23,5 23,8 23,7 23,5 25,5 11,5%

Commercial 3,0 2,8 2,5 3,3 3,7 3,5 1,6%

Suppliers 0,1 0,1 0,0 0,0 0,0 0,0 0,0%

b Domestic Loan (in billion USD) 0,0 0,1 0,19 0,2 0,2 0,3 0,1%

c. Government Securities (in billion USD) 118,4 131,0 140,8 136,3 155,2 168,3 75,7%

Foreign Currency Denominated 18,0 21,6 27,4 32,8 36,7 44,1 19,9%

Rupiah Denominated 100,4 109,4 113,4 103,5 118,5 124,1 55,9%

Total Central Government Debt

(in billion USD)187,0 199,5 194,9 209,4 222,2

Total Central Government Debt

(in trilion IDR)1.681,7 1.808,9 2.375,5 2.604,9 3.074,8

Exchange Rate Assumption (IDR/USD1) 8.991,0 9.068,0 12.189,0 12.440,0 13.840,0

GDP (in trillion IDR) 6.864,1 7.831,7 9.524,7 10.542,7

Debt to GDP Ratio 24,5% 23,1% 23,0% 24,9% 24,7%

8.615,7

9.670,0

1.977,7

Nov-15

204,5

2011 2012 2013 20142010Description

23

Notes: • * Preliminary Figures

OUTSTANDING CENTRAL GOVERNMENT DEBT

BY CURRENCY

2010 2011

Original Currency

IDR (in trillion) 902,6 993,0 1.098,0 1.263,9 1.477,5 1.722,1

Gov't Securities 902,4 992,0 1.096,2 1.261,7 1.474,6 1.718,2

Loan 0,2 1,0 1,8 2,2 2,9 3,9

USD (in billion) 39,6 43,9 49,8 56,8 61,0 69,1

Gov't Securities 16,9 20,4 25,6 31,3 34,2 39,7

Loan 22,8 23,5 24,2 25,4 26,8 29,4

JPY (in billion) 2.689,8 2.589,8 2.498,8 2.395,3 2.204,0 2.183,5

Gov't Securities 95,0 95,0 155,0 155,0 155,0 255,0

Loan 2.594,8 2.494,8 2.343,8 2.228,8 2.049,0 1.928,5

EUR (in billion) 5,4 5,0 4,5 4,2 5,1 6,1

Gov't Securities - - - - 1,0 2,3

Loan 5,4 5,0 4,5 4,2 4,1 3,9

Other currencies

Equivalent in Billion USD

IDR 100,4 109,5 113,5 103,7 118,8 124,4 56,0%

USD 39,8 43,9 49,8 56,8 61,0 69,1 31,1%

JPY 33,1 33,4 29,1 22,8 18,5 17,8 8,0%

EUR 7,2 6,4 6,0 5,8 6,2 6,5 2,9%

Other currencies 6,5 6,3 6,1 5,8 5,0 4,4 2,0%

Total Eq. in Billion USD 187,0 199,5 204,5 194,9 209,4 222,2

Equivalent in Trillion IDR

IDR 902,8 993,0 1.098,0 1.263,9 1.477,5 1.722,1

USD 357,6 397,9 481,9 692,0 758,3 955,9

JPY 297,6 302,5 281,2 278,3 229,8 246,2

EUR 65,0 58,5 57,5 71,1 76,9 89,9

Other currencies 58,6 57,1 59,1 70,2 62,4 60,7

Total Eq. in Trillion IDR 1.681,7 1.808,9 1.977,7 2.375,5 2.604,9 3.074,8

Foreign Currency Portion 46,3% 45,1% 44,5% 46,8% 43,3% 44,0%

Exchange Rate Assumption USD/IDR 8.991 9.068 9.670 12.189,0 12.440,0 13.840,0

----------------Multiple Currencies -----------------------

2014 Nov-152012 2013

24

CENTRAL GOVERNMENT DEBT RATIOS

Debt to GDP Ratio Interest Payment to Revenue and

Expenditure Ratio

Debt Service to GDP Ratio Interest Payment to Tax Revenue &

Central Government Expenditure Ratio

Notes: Using GDP at Current Market Prices [2010 Version] * Preliminary Figures 25

23.1% 23.0%24.9% 24.7% 24.7%

0%

5%

10%

15%

20%

25%

30%

2011 2012 2013 2014 2015*

7.7%

7.5%

7.9% 8.6%

8.8%

7.2%

6.7%

6.8% 7.5%

7.8%

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

2011 2012 2013 2014 2015*

Interest to Revenue Interest to Expenditure

2.9%3.2%

2.9%

3.5%3.2%

0%

1%

2%

3%

4%

2011 2012 2013 2014 2015*

10.7

%

10.8

%

10.5

%

11.6

%

10.5

%

10.6

%

9.9%

9.9%

11.1

% 11.8

%

9%

10%

10%

11%

11%

12%

12%

2011 2012 2013 2014 2015*

to Tax Revenue to Central Gov't Expenditure

RISK INDICATORS

Risk indicators are improving amidst pressure from rupiah depreciation Risk indicators show improvements in interest rate risk and stability in exchange and refinancing risks

26

Divider title

Directorate General of Budget Financing and Risk Management Ministry of Finance of Republic of Indonesia

Directorate of Government Debt Securities

Frans Seda building, 4th floor, Jl. Wahidin Raya No. 1, Jakarta Pusat – Postal Code: 10710

Phone: +6221 3810175 Fax. : +6221 3846516

Website: www.djppr.kemenkeu.go.id

END OF PRESENTATION