Embed Size (px)

Citation preview

Government Fraud Investigations: Case Study,

Auditing Tips and Navigating the Political Minefields

June 9, 2011

������������ ����������������� ��������� ����

Presented by

Richard Fechterand

L.T. Lafferty

Economic Damages: Case Law Update

A. Government Fraud Detection Investigations –Monroe County School Board – A Case Study

1. The Tipping Point – the Decision to Investigate

2. Retention of Counsel & Forensic Accountant

3. The Scope of Representation / Investigation

4. The Investigation

5. Reporting to the Governing Body

6. Remedies

AGENDA

Government Fraud Investigations

B. Auditing Tips

1. Audit Requirements a. SAS No. 99b. SAS No. 112

2. Procurement Fraud

3. Fraud Red Flags

Government Fraud Investigations

C. Political Minefields

1. Benefits of Legal Counsel2. Who is Your Client?

3. Florida Sunshine Law4. Up for Reelection?5. Political Agendas

6. Potential Litigation7. Law Enforcement / Prosecution

Government Fraud Investigations

ACFE Survey

�Government and public administration agencies were among the most defrauded organizations in 2008 and 2009, according to a new survey from the Association of Certified Fraud Examiners.

�The median reported loss of a government fraud was $91,000, a number that puts it on the low end of reported loss.

�When it comes to detecting fraud, government agencies had the highest rate of detection by tips and had a proportionately high rate of frauds caught through external audit, the survey finds.

Government Fraud Investigations

Government Fraud Investigations

Government Fraud Investigations

Government Fraud Investigations

Government Fraud Investigations

Government Fraud Investigations

Government Fraud Investigations

Government Fraud Investigations

Government Fraud Investigations

Government Fraud Investigations

Government Fraud Investigations

Government Fraud Investigations

Government Fraud Investigations

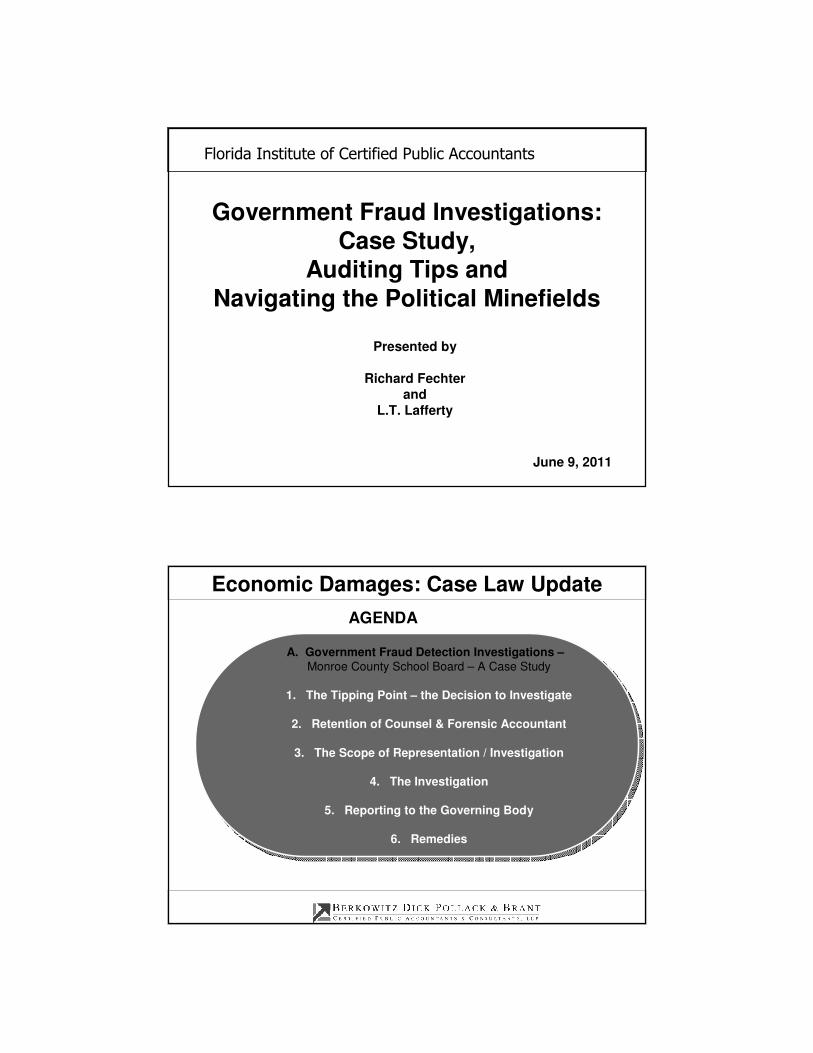

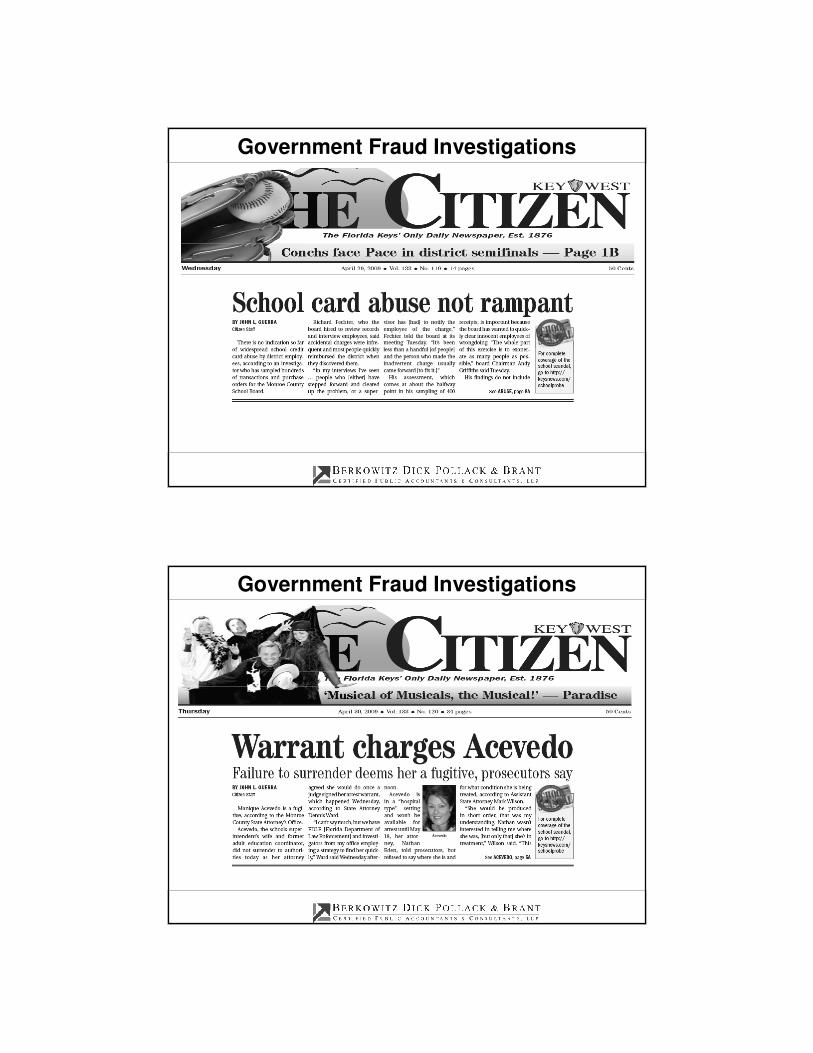

Saturday, August 29, 2009

ACEVEDO GUILTY BY JOHN L. GUERRA Citizen Staff

Prosecutors will ask a judge to sentence suspended Schools Superintendent Randy Acevedo to three or four years in state prison, Monroe County State Attorney Dennis Ward said Friday.

Acevedo faces a maximum of 15 years and a $15,000 fine when Circuit Judge Mark Jones sentences him on Sept. 17. "He is guilty of three felonies," Ward said. "He put his wife in front of taxpayers and the school district, and stood by while his wife broke the law."

Government Fraud Investigations

Wednesday, September 1, 2010

EIGHT YEARS IN PRISONMonique Acevedo on Tuesday pleaded guilty and was sentenced to eight years in state prison, followed by 22 years on probation, during which time she must make monthly payments to repay the $413,000 she was accused of stealing -- a punishment she cannot appeal, prosecutors said.

Government Fraud Investigations

Government Fraud Investigations

Yellow Book – Audit Requirements

SAS No. 99

�Expands the auditor’s responsibility for detecting fraud

�Maintain professional skepticism - Auditors must always consider that fraud could be present

�Consider the fraud triangle

Government Fraud Investigations

Yellow Book – Audit Requirements

SAS No. 99 – Cont’d

�Staff must discuss fraud during the audit

�Obtain information to identify and assess the risks of fraud

�Do not accept less-than-persuasive evidence because you consider management to be honest

Government Fraud Investigations

Yellow Book – Audit Requirements

SAS No. 99 – Cont’dPerformance Audits

�Determine which laws and regulations are significant to audit objectives and design tests to have reasonable assurance of detecting violations, including fraud

�Be alert to indications of fraud. If so, determine whether it likely occurred and its effect on results

�Use judgment to avoid interfering with investigations or legal proceedings

Government Fraud InvestigationsYellow Book – Audit Requirements

SAS No. 99 – Cont’dPerformance Audits

�Consider the Fraud Triangle –

� Incentives or Pressures / Reasons to Commit Fraud

� Opportunity - Poor internal controls or management’s ability to override them

� Rationalizations - Individuals ability to rationalize fraud (Frequently tied to lack of ethical framework)

Government Fraud Investigations

Yellow Book – Audit Requirements

SAS No. 99 – Cont’dPerformance Audits

�Increase communication about fraud among the audit staff

� Auditors should communicate with each other throughout the engagement

� Audit signer must determine that there was appropriate communication

� The auditor must document the brainstorming session and other activities related to fraud detection

Government Fraud Investigations

Yellow Book – Audit Requirements

SAS No. 99 – Cont’dReporting Requirements

�Report all instances of fraud, unless inconsequential (place findings in perspective)

�May need to report directly to outside parties (e.g., Law Enforcement, State Attorney)

�May need to report if management does not act promptly and appropriately

Government Fraud Investigations

Yellow Book – Audit Requirements

SAS No. 112Communicating Internal Control Related Matters Identified in an Audit

�SAS No. 112 instructs independent auditors that inadequate “anti-fraud programs and controls” constitute, at a minimum, a significant deficiency that would need to be reported.

Government Fraud Investigations

Yellow Book – Audit Requirements

SAS No. 112Communicating Internal Control Related Matters Identified in an Audit

�The Government Finance Officers Association recommends at a minimum, a government should do all of the following:

� Formally approve, and widely distribute and publicize an ethics policy that can serve as a practical basis for identifying potential instances of fraud or abuse and questionable accounting or auditing practices.

Government Fraud Investigations

Yellow Book – Audit Requirements

SAS No. 112 – Cont’dCommunicating Internal Control Related Matters Identified in an Audit

� Establish practical mechanisms (e.g., hot line) to permit the confidential, anonymous reporting of concerns about fraud or abuse and questionable accounting or auditing practices to the appropriate responsible parties.

� A government should regularly publicize the availability of these mechanisms and encourage individuals who may have relevant information to provide it to the government.

Government Fraud Investigations

Yellow Book – Audit Requirements

SAS No. 112 – Cont’dCommunicating Internal Control Related Matters Identified in an Audit

� Government may wish to explore the possibility of engaging the services of an outside vendor to receive complaints from employees. The use of an outside vendor offers a number of potential advantages, including the following:

� Employees may be more readily persuaded of the confidentiality of their calls if they are made directly to a party outside the government.

� Vendors may be able to provide extended hours of service, thus avoiding the need to place a call during regular working hours (i.e., while the employee is still at work).

Government Fraud Investigations

Yellow Book – Audit Requirements

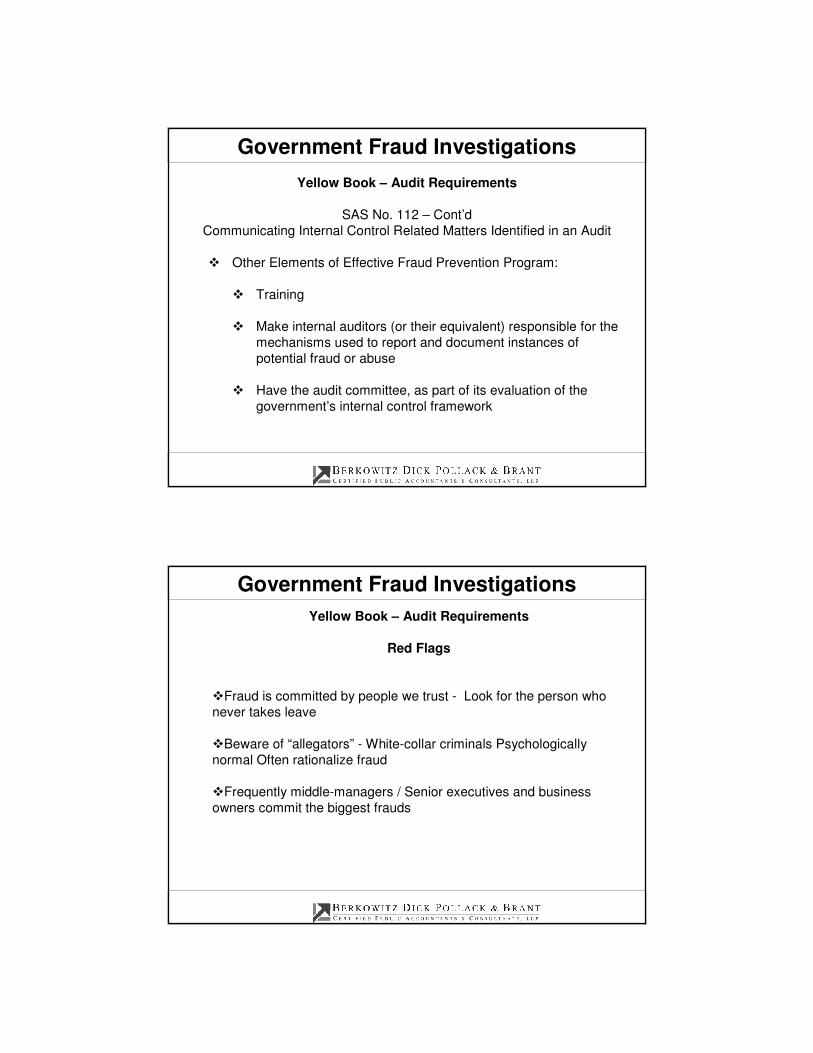

SAS No. 112 – Cont’dCommunicating Internal Control Related Matters Identified in an Audit

� Other Elements of Effective Fraud Prevention Program:

� Training

� Make internal auditors (or their equivalent) responsible for themechanisms used to report and document instances of potential fraud or abuse

� Have the audit committee, as part of its evaluation of the government’s internal control framework

Government Fraud InvestigationsYellow Book – Audit Requirements

Red Flags

�Fraud is committed by people we trust - Look for the person who never takes leave

�Beware of “allegators” - White-collar criminals Psychologically normal Often rationalize fraud

�Frequently middle-managers / Senior executives and business owners commit the biggest frauds

Government Fraud Investigations

Yellow Book – Audit Requirements

Red Flags

�Possible characteristics of people who commit fraud:

� Intelligent� Egotistical� Inquisitive� Rule breaker� Hard worker� Under stress� Greedy or needy� Disgruntled

Government Fraud Investigations

Yellow Book – Audit Requirements

Red Flags

�Reason Why People Commit Fraud:

� Need for money� Job frustration� “Everybody does it”� Low expectation of detection� Low expectation of prosecution

Government Fraud Investigations

Yellow Book – Audit Requirements

Red Flags

�Fraud Warning Signs - Organization:

� Poor internal controls, particularly segregation of duties

� Unethical leadership

� Lack of conflict-of-interest rules

� Poor management/employee relations

� Complicated, unclear accounting

Government Fraud Investigations

Yellow Book – Audit Requirements

Red Flags

�Fraud Warning Signs – Individuals� Behavioral changes� Personal problems or debts� Adversarial attitude to auditors� Resents questions about decisions, actions� Job dissatisfaction� Wants complete control over operation� Unusual allegiance to one vendor

Government Fraud InvestigationsYellow Book – Audit Requirements

Materiality

�Materiality may not be important

� Amounts are rarely enough for a major finding, but public interest is often greater than it is for big issues

� Public has different expectations of:� Governmental agencies� Governmental auditors

Government Fraud InvestigationsYellow Book – Types of Public Sector Fraud

�Procurement Frauds� Kickbacks� Bid rigging� Duplicate checks� Nonexistent vendors� Collusion to overprice products

� More specific items to look for:� Excessive write-offs� Duplicate vendor addresses� Vendor has same address as employee� Many payments to same vendor or address

Government Fraud InvestigationsYellow Book – Types of Public Sector Fraud – Cont’d

�Payroll� Ghost employees� Checks for former employees� Duplicate checks� Excess hours� Unauthorized advances

�Inventory� Stealing� Improperly reporting shipments as short� Altering bills of lading� Overstated outgoing shipments

Government Fraud InvestigationsYellow Book – Types of Public Sector Fraud – Cont’d

�Cash Disbursement Fraud� Checks and Deposits� Excessive voided checks or refunds� Missing blank checks� Old checks that have not been cashed� Unusual pattern of deposits

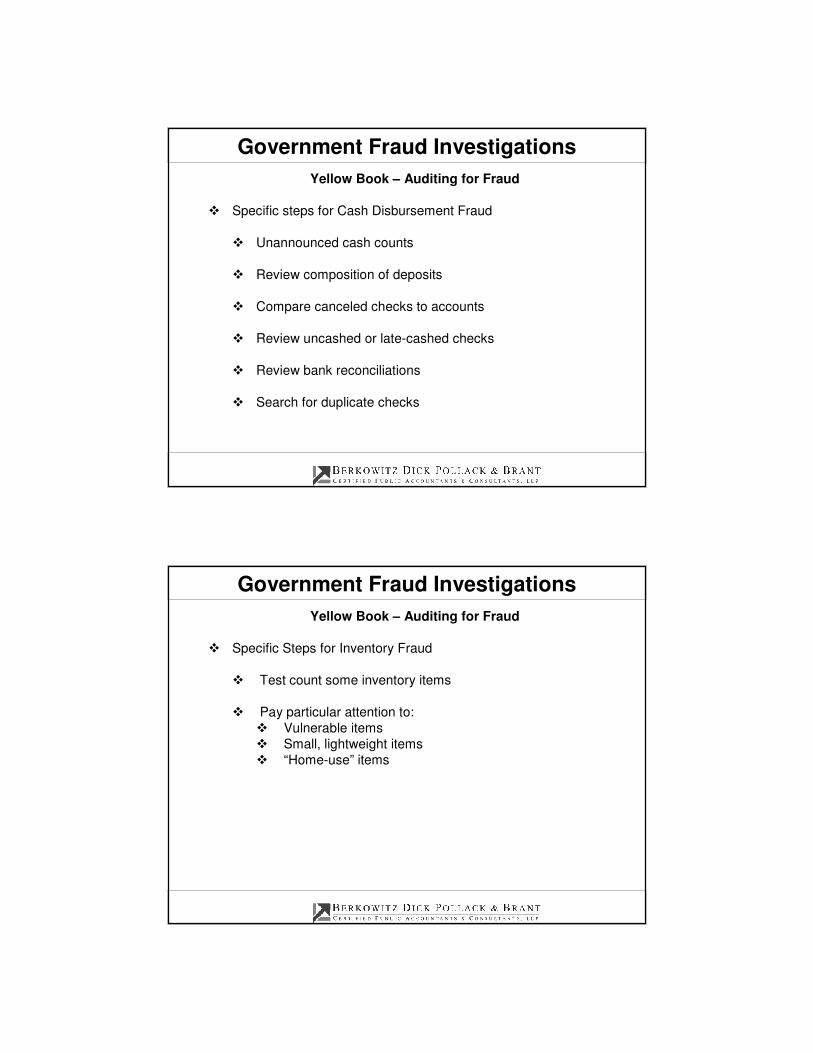

Government Fraud InvestigationsYellow Book – Auditing for Fraud

� Specific steps for Cash Disbursement Fraud

� Unannounced cash counts

� Review composition of deposits

� Compare canceled checks to accounts

� Review uncashed or late-cashed checks

� Review bank reconciliations

� Search for duplicate checks

Government Fraud InvestigationsYellow Book – Auditing for Fraud

� Specific Steps for Inventory Fraud

� Test count some inventory items

� Pay particular attention to:� Vulnerable items� Small, lightweight items� “Home-use” items

Government Fraud InvestigationsYellow Book – Auditing for Fraud

� Additional specific steps:

� Ratio analysis� Confirm accounts receivable� Evaluate reasonableness of payroll, particularly overtime� Review the dates on prenumbered documents� First-digit phenomenon

Government Fraud Investigations

C. Political Minefields

1. Benefits of Legal Counsel2. Who is Your Client?

3. Florida Sunshine Law4. Up for Reelection?5. Political Agendas

6. Potential Litigation7. Law Enforcement / Prosecution

Contact Information

Richard S. Fechter Latour “LT” [email protected] [email protected]

Berkowitz Dick Pollack and Brant, LLP Fowler White and Boggs200 South Biscayne Boulevard, 6th FL 501 East Kennedy Blvd.Miami, Florida 33131 Tampa, Florida 33602Phone: 305-960-1235 Phone: 813-222-1106Fax: 305-379-8200 Fax: 813-384-2830