Embed Size (px)

Citation preview

GOVERNING A LARGE, COMPLEX AND

GLOBAL PENSION-BASED ENTERPRISE

S U B M I S S I O N BY

T H E

B OA R D O F D I R E C TO RS

O F

O M E RS A D M I N I ST RAT I O N

C O R P O RAT I O N

TO

TO N Y D E A N

O M E RS 2012

G OV E R N A N C E R E V I E W E R

AU G U ST 29 , 2012

T A B L E O F C O N T E N T S

Letter from the OAC Board Chair 3 Key Points 6 A Brief Contextual History 7 What Needs to Be Governed? 12 The OAC Today and Tomorrow 15 Enhancing OAC Governance 33 Clarifying Roles and Authorities 39 Conclusion 41

3

August29,2012Mr.TonyDeanOMERS2012GovernanceReviewerOMERSGovernanceReviewc/oMunicipalFinancePolicyBranchMinistryofMunicipalAffairsandHousing777BayStreet,13thFloorTorontoONM5G2E5DearMr.Dean:OMERSAdministrationCorporation(theOAC)welcomestheopportunitytomakeaformalsubmissionasyoureviewtheeffectiveness,efficiencyandfairnessofOMERSgovernancestructure,asrequiredundertheOntarioMunicipalEmployeesRetirementSystemReviewAct,2006.TheOACBoardacceptsthatithasafiduciarydutytomakeasubmissiononbehalfoftheOACandalltheplanmembersitserves.Thegovernanceofapension‐basedinstitutionthatisimportanttosomanyOntariansdeservesbroad‐basedandtransparentconsultation.HowOMERSisgovernedandbywhomisalsocriticaltorelationshipbuildingwithawidearrayofstakeholdersandinvestmentpartnersinOntario,acrossCanadaandincreasinglyworldwide.TheOACBoardhascarefullyconsideredyourmandateandtermsofreference.Weconvenedfourfull‐dayspecialgovernancereviewmeetingswithafacilitator,developedaseriesofgovernancediscussionpapersandsharedourinitialthoughtsonwaystoimprovetheefficiency,effectivenessandfairnessofOMERSgovernancewiththeSponsorsCorporationBoard(theSCBoard).FollowingthesesessionsandourexchangewiththeSCBoard,wedecidedthat,insteadofmakingspecificrecommendations,wewouldadoptthefollowingprinciplestoshapeoursubmission:

1. TheOACandSCBoardsshouldmutuallyagreeonrecommendingchangestotheOMERSAct,2006,wheneverpossible.

2. TheOACBoardiscommittedtotheexistingbi‐cameralpartnershipmodel.

3. ThesponsorsoftheOMERSPrimaryPensionPlanhavetheultimateauthoritytonominatecandidatesdirectlytotheOACBoard.

4. EmployeeandemployersponsorshaveequalrightstonominatecandidatestotheOACBoard.

4

5. TheOACBoardiscommittedtogovernanceexcellenceandbestpracticesadaptedtotheneedsofajointlysponsoredmulti‐employerpensionplan.

6. OACBoardeffectivenessincarryingoutitsfiduciaryandoversightrolesrequiresdirectorswiththerightmixofcompetenciesrelevanttoplanadministrationandfundinvesting.

7. TheOACBoardrequiresarobustnominatingprocessthatacknowledgesthecompetencyneedsoftheBoardasawhole.

8. TheOACBoardisbestpositionedtoidentifythegovernanceneedsoftheOACBoardandprovideguidancetosponsorsonnominatingcandidatesthatcanfillcompetencygaps.

9. Therobustnominatingprocessmaybesupportedbyasearchfirmtoassistsponsorsinsourcingandevaluatingpotentialdirectorcandidates.

10. OMERSgovernancestructureshouldbesufficientlyflexibletoaccommodatefutureplanmembershipgrowth,includingplanconsolidation,whichisessentialtothePrimaryPensionPlan’slong‐termfinancialsustainability.

11. TherolesanddutiesoftheSCandOACrequirecleardelineation,reducingoverlapwhereverpossible,toensureefficientandeffectivegovernance.

12. ThesuccessofOMERSdependsoncooperationandpartnershipbetweentheOACandSC.

Astheresultofourconsiderationoftheseprinciples,theOACBoarddecidedtofocusitssubmissiononthemandateoftheOACandtheroleofitsboardbyasking:

• Whatneedstobegoverned?• WhatistheOACtodayandtomorrow?• HowshouldOACgovernancebeenhanced?• Whereandhowshouldrolesandauthoritiesbeclarified?

OnAugust23,2012,theOACBoardunanimouslyapprovedthissubmission,directedmetosubmitittoyouandagreedtopostitatthattimeontheOMERSwebsite.ThesubmissionbeginswithabriefcontextualhistorytodefinetheOAC’sroleastheplanadministratorandfundtrusteeforOMERSPensionPlans.Wethendescribeinsomedetailthelarge,complexandglobalpension‐basedenterprisethatneedstobegoverned.TheOACisoneofthelargestcorporationsinOntario.Itemploysapproximately1,000professionalsinplanadministrationandfundinvestingandhasanorganizationstructure,policies,procedures,protocols,legalandethicalobligationsandspecifieddutiesmuchlikeanypublicorprivatesectorcorporation.TheOACisalsosubjecttocommonlawfiduciaryobligationsandOntario’sPensionBenefitsActinitsadministrationandinvestmentofthePensionPlans.Thegovernanceofsuchavitalprovince‐widecorporationshouldbeanexemplarofbestpracticesinOntario’spublicsector.

5

Wethenexplorewhatcanbedoneundertheexistingbi‐cameralmodeltoimprovethegovernanceoftheOACandprovideexamplesofoverlappingauthoritiesthatarecausinginefficiencies.Amajorissuethataffectsgovernanceefficiency,effectivenessandfairnessismatchingthecompetenciesoftheOACBoardwiththecomplexitiesandscopeoftheOACitself.OurBoardhasaddressedthischallengewithinthelimitsofourstatutoryauthoritiesfornearlyfiveyears,andwewelcomeyourindependentviewsonhowwecanmakesubstantiveprogressaswellasimprovetheOACBoardnominatingprocess.OnapersonalnoteasChair,IbecameanOMERSmemberin1984andjoinedtheOMERSBoardin1997.Ihavehadafront‐rowseatfor15yearstothesurprisesthatcanchallengegovernance.OMERSwentfromahugefundingsurplusin1998intodeficitby2003,gotbacktobreakevenforabriefmomentin2007andthenfellsteeplyintodeficitwhenthe2008globalcreditcrisisshookcapitalmarkets.In2003and2004,theOACBoardandManagementbegantoaddresstheneedtotransformOMERSinreadinessfortroublingtimesahead.OMERShastransitionedfromatraditionalandpassivepensionplanintoadynamicandprogressivepension‐basedcorporation,ajourneythathasinvolved40directorsandthreeconsecutiveCEOs.Likeotherlargebusinesses,theOACfacesmanyinvestment,operationalandstrategicrisks,anditdoesn’ttakemuchtotarnishourTripleAreputation.Thegovernancechallengedoesnotgeteasier.Wehaveafundingdeficittocorrectandtherightinvestmentstrategytogetbacktosurplusataffordablecontributionratesforemployersandplanmembers.OurjobasdirectorsistomakesurethatManagementdeliversonthepensionpromise.Withthepublicmarketshighlyvolatile,thereismuchforustobeconcernedabout.TheOACBoardiscurrentlyreviewingtheappropriatenessofitsassetmixpolicyandwhetherweshouldacceleratethealreadysubstantialmoveintoprivatemarketinvestmentstodelivermorestableandpredictableinvestmentreturnstounderwritethepensionpledge.

WelookforwardtodiscussingourrecommendationssothatOMERScanmoveforwardwithconfidenceunderanefficient,effectiveandfairgovernancestructurethatservicesthebestinterestsofallplanmembersandemployerswithinthecontextofpublicpoliciesandtheinterestsoftheprovince’staxpayers.SubmittedonbehalfoftheOACBoard,RickMillerOACBoardChair

• The OMERS Administration Corporation is one of Ontario’s largest

and most important corporations providing vital fi nancial security and

pension services to more than 420,000 pension plan members.

• OMERS should be an exemplar of best governance practices adapted

to the needs of a jointly sponsored multi-employer pension plan.

• All employer and employee sponsors groups should be actively

and directly engaged in appointing those who govern the OMERS

Administration Corporation through a robust and transparent

nominating process.

• The OMERS Administration Corporation requires a board of directors

that has competencies aligned with the scope and complexity of an

increasingly global pension-based enterprise under professional

management.

• OMERS existing governance structure requires clarifi cation of

the roles and authorities between the fi duciary board and the

non-fi duciary board.

• OMERS governance structure must be fl exible to accommodate future

employers and plan members, recognizing that plan membership

growth is essential to the continued long-term sustainability of the

OMERS Primary Pension Plan.

KEY POINTS

6

PG 6 – Key Points with bleedsOAC bleed pgs Aug25.indd 1OAC bleed pgs Aug25.indd 1 8/27/12 3:13:30 PM8/27/12 3:13:30 PM

7

A BRIEF CONTEXTUAL HISTORY

The Ontario Municipal Employees Retirement System Review Act, 2006 requires a

review of the efficiency, effectiveness and fairness of the actual governance and

administration of OMERS since 2006. The scope of the review also includes an

evaluation of the efficiency and effectiveness of the decision-making by the Sponsors

Corporation (the SC) and its impact on the governance of the Pension Plan. This

submission focuses primarily on governance of OMERS Administration Corporation (the

OAC) and its relationship with the SC.

Governance History

OMERS governance has evolved since the first municipal members joined the Pension

Plan on January 1, 1963. Until 1967, direct taxpayer representatives dominated the

OMERS Board with three provincial officials, two municipal councilors and two

municipal treasurers, and only two plan members on the board.

Over time, provincial representation diminished. By 1980, one provincial official served

on the OMERS Board, a situation that continued until 2006. The presence of provincial

officials on the OMERS Board reflected Ontario’s funding obligation until plan changes

in 1992 required members and employers to share funding shortfalls or surpluses

equally, i.e. joint sponsorship.

Throughout most of OMERS history (1963 until 2006), two municipal councilors (or

local board members) served as directors, representing taxpayers. The requirement

that two board members be municipal treasurers changed in 1967 to any municipal

official and by 1980 expanded to four municipal officials.

On the employee side, plan member representation increased from two to five

directors by 1991, plus a retiree. By this time, the OMERS Board consisted of one

provincial official, two municipal councilors (or local board members), four employer

officials, five plan members and a retiree. The composition of the 13-member board

remained until the dual-corporation structure was introduced in the OMERS Act 2006.

Under the bi-cameral model introduced in 2006, the SC identified 13 designated

sponsors with the right to appoint members of the SC Board and the OAC Board. On

the SC employer side, the designated sponsors are associations with the exception of

the City of Toronto. On the SC employee side, three are employee or retiree

associations and four are unions.

8

Today, the OAC Board has 14 directors1 with equal voting rights, and board decisions

are made by a simple majority vote. Seven directors are appointed by employer

sponsors, six directors by organized plan members and one director by retirees.

Critical Definitions

A good place to begin in examining the efficiency, effectiveness and fairness of OMERS

bi-cameral model is by defining two critical pieces:

i. OMERS defined benefits pension plans (collectively, the Pension Plan) that is a

financial arrangement or agreement to deliver the pension promise to plan

members; and

ii. the large and complex corporation, the OAC, that is the plan administrator and

the pension fund trustee.

Prior to 2006, a single corporation and fiduciary board governed OMERS. Among its

responsibilities, the single corporation and board recommended changes in

contribution rates and benefit levels, consistent with the requirements of OMERS

funding policy, to the Ontario government. The OMERS Board also notified the

government of pending board vacancies and the Ministry of Municipal Affairs and

Housing contacted sponsor groups directly to solicit their nominees, who were

subsequently appointed by the Ontario government.

The 2006 devolution of Ontario government powers to the OAC and the SC has added

a layer of governance complexity, largely due to the overlap of certain responsibilities

between the boards.

The Pension Plan as a Financial Agreement

The assets of the Pension Plan are held in trust for the benefit of plan members and

the Pension Plan is obligated to make benefit payments to retired members every

month. Payments may be required earlier than assumed due to early retirements, or

for a longer duration than assumed if retirees (and their survivors) live longer than

projected by mortality tables. The obligation to the youngest plan members today

could easily span 70 years.

1 13 designated sponsors appointing 14 directors is not symmetric because two sponsors have multiple appointments, one employee sponsors group alternates appointments between two unions, and two employer groups alternate an appointment

9

Since the OMERS Act and its Regulations were introduced on January 1, 1963, this

financial arrangement or agreement (that is, the Pension Plan) has been a living

document that has required periodic amendments to OMERS enabling legislation. Prior

to the OMERS Act 2006, the legislation was amended 19 times and since 2006 three

times, and the Regulations were amended 76 times. Opening the legislation from time

to time has kept pace with the evolution of OMERS investment and plan administration

policies.

The OAC as Pension Plan Administrator

Under the OMERS Act 2006, the OAC is the plan administrator. It has the primary

responsibility for delivering the pension promise because it has the fiduciary

responsibility to the entire plan membership as required by the Pension Benefits Act.

The OAC as Pension Fund Trustee

Under the OMERS Act 2006, the OAC is the pension fund trustee. It invests the plan’s

funds to ensure that net assets (that is, investments and projected contributions by

employers and plan members) are sufficient over the long term to make benefit

payments when plan members retire.

10

The management of the Pension Plan’s assets and liabilities over the long term must

be seen in the context of membership demographics and plan maturity on the liability

side, and employer and employee contributions, the investment strategy and future

expected investment returns on the asset side. The OAC is (and through its

predecessor corporation has been historically) responsible for the Pension Plan’s

funding policy because it has the sole statutory authorities for establishing the

actuarial methodology and assumptions, appointing the external actuary and

developing and implementing the investment strategy.

In the event there is a funding surplus or deficit, the OAC informs the SC (as it did the

Ontario government between 1963-2006) so that the SC can make decisions on

adjusting contribution rates and benefit levels within the parameters (such as

regulatory requirements) set by the OAC funding policy.

Common Law Fiduciary Duty

To fully understand the role of the OAC as plan administrator and pension fund

trustee, it is important to appreciate the meaning of common law fiduciary duty in the

pension plan context. A widely accepted definition by a distinguished Canadian

regulator (now a Court of Appeal judge) is as follows:

“The result of one person being held to be a fiduciary in respect of another is

that the first person owes a duty of loyalty to the other. In the pension plan

context, the duty of loyalty translates into an obligation on behalf of those

administering the plan to act honestly, prudently, diligently, even-handedly,

with strict candor and confidentiality and strictly in the best interests of the plan

members. The duty of loyalty precludes those administering the plan from

making unauthorized profits, from delegating their responsibilities and from

placing themselves in a position of conflict of interest”.2

2 Eileen E. Gillese, “Fiduciary Responsibility – A Regulator’s Viewpoint” (1995), PCOP Bulletin, Vol. 6, Issue 2

11

Section 22 of the Pension Benefits Act imposes a similar fiduciary obligation on the

OAC and the OAC Board.

Fiduciary duty, also described as one of “utmost good faith”, results in the actions of the fiduciary being “viewed with a strictness unknown to most other areas of law”.3

Moreover, the trust relationship is the most exacting of fiduciary relationships in terms

of accountability and associated liability.

In the case of OMERS, this means that the OAC must always: (i) act strictly in the

best interests of all plan members in its administration and oversight of the pension

plan assets and liabilities; and (ii) act in an evenhanded manner with respect to all

classes or categories of members and participating employers.

OAC/SC Relationship

How does the SC relate to the Pension Plan and its administrator and pension fund

trustee (the OAC)?

The SC is a special entity created in 2006 by the Province of Ontario to assume its

pre-2006 responsibilities for making plan design decisions, plan amendments, setting

contribution rates and appointing directors to the OAC. The intent of the legislation is

to separate the entity that sets the terms of the pension plan text (impacting only the

employer/employee relationship) and the fiduciary body that acts as the plan

administrator and pension fund trustee.

The SC is not an administrator or a trustee. It does not hold plan assets and does not

have fiduciary duties to plan members. Under the OMERS Act 2006, its key

responsibilities are to make plan design changes and set contribution rates (both

within the context of the OAC funding policy) and to file an actuarial valuation report

more frequently than required under the PBA.

The OMERS Act 2006 also gave the SC Board exclusive authority to appoint OAC

Board members and set their compensation and expense reimbursement policy.

The Governance Challenge

Given its responsibility and obligation to act as the pension plan administrator and

pension fund trustee, the OAC requires professional management which, in turn,

requires informed governance oversight by a board of directors that has the requisite

level of expertise and the ability to always act in the best interests of the entire plan

membership. The OAC Board’s directors are required to be independently minded and

to be at arm’s length from the influence of those that appointed them.

Reinforcing this point of law for all stakeholders will go a long way to clarifying the

roles and responsibilities of the OAC and SC – and thus improve the efficiency,

effectiveness and fairness of the governance model.

3 Regal Hastings Ltd. V Gulliver (1942) 1 All E.R. 378 at 381

12

WHAT NEEDS TO BE GOVERNED?

In addition to examining the governance of the SC as specified in the Review Act, a

central issue for the Reviewer to consider is the kind of governance appropriate for a

large and complex global pension-based corporation like the OAC.

The OAC is one of Ontario’s largest corporations and touches the social and economic

health of every community in the province. One in 20 Ontario employees is an OMERS

member. Together these members contribute more than $1 billion annually to the

Pension Plan. Every municipality and other participating public sector employers in

Ontario communities also contribute tax dollars exceeding $1 billion annually.

Approximately 420,000 members (and their surviving dependents) rely on OMERS for

retirement income and most of it will be paid from investment income.

As an economic force, OMERS has approximately $54 billion invested in Canadian

businesses that employ well in excess of 10,000 people (with $26 billion invested

outside Canada).

OMERS is a major investor in Bruce Power’s six operating nuclear units and the

refurbishment of two nuclear units which have been laid up for 17 years, which (in

aggregate) provides 25% of Ontario’s electricity supply; Teranet that manages

Ontario’s electronic land registry; LifeLabs that processes more than one-third of

Ontario’s medical testing for patients and physicians; the Detroit River Tunnel that

handles up to $20 billion of annual goods traded between Canada and the United

States; Enwave that provides green technology cooling to Toronto’s commercial and

institutional buildings; and Husky International Ltd. – headquartered in Bolton,

Ontario – with global sales exceeding $1 billion.

OMERS owns and manages 20% of Toronto’s Class A office space, three super-

regional shopping malls in the Greater Toronto Area, 2,300 long-term care facilities in

12 Ontario communities, hospitals in three Ontario cities, 5,000 residential units in 10

Ontario cities and the Metro Toronto Convention Centre. New properties are being

developed to meet Toronto’s future commercial growth.

Photos: 1. 5,000 residential units 2. Teranet: Ontario electronic land registry 3. Husky Injection Molding Systems 4. LifeLabs 5. Metro Toronto Convention Centre 6. Office towers in downtown Toronto 7. Bruce Power nuclear plant 8. Toronto super-regional malls 9. Porter Airlines 10. Detroit River Tunnel

14

The OAC employs more than 1,000 professionals in plan administration, fund

investing, asset management and corporate functions. This corporation has an

enormous wealth of talent in employees as diverse as corporate executives, actuaries,

accountants, lawyers, engineers, customer service specialists, stock pickers, portfolio

managers, securities and foreign currency traders, risk managers, IT specialists and

teams in asset classes like private equity, real estate, infrastructure and oil and gas

properties.

Keeping such a diverse professional management team accountable for proper

management of the Pension Plan is the primary role of the OAC Board, which asserts

its authority by controlling OMERS strategic direction, demanding regular and detailed

reporting, setting pre-determined results in exchange for performance-based

incentives and monitoring compliance with behavioral policies and procedures. The

role the OAC Board plays matters to the province and its local communities, to active

plan members, retirees and employers, and to the OAC’s investment partners.

A corporation of such vital importance to Ontario should be an exemplar of best

governance practices in its public sector and among Canada’s largest pension plans.

15

THE OAC TODAY AND TOMORROW

OMERS is a well-structured organization with three cornerstones: Pension Services,

Investment Entities and the Corporate Office. The nature and scope of the core

businesses highlight why the governance of such a large and diverse organization

requires directors with specialized knowledge and expertise.

Pension Services

Pension Services deals with regulatory, actuarial, funding policy, plan administration

and plan member services and is an innovator in developing savings products for plan

members. It has its fingers on the pulse and concerns of employers, active members

and retirees through more than one million electronic and face-to-face contacts per

year with stakeholders in Ontario. The customer service organization is watched over

by the OAC Board’s Member Services Committee, which oversees the Pension Plan’s

liabilities and regulatory framework; ensures Management accountability for funding

and actuarial matters; recommends the appointment of the external actuary, actuarial

methods, assumptions and valuations; reviews strategic initiatives for new products

and services; and oversees plan administration.

16

Plan administration and pension services expanded following the Pension Plan’s

inauguration for municipal employees on January 1, 1963 as the government decreed

new employers and employees eligible to join – utility commissions and children’s aid

societies in 1966, all new municipal employees in 1968, municipal councilors in 1972

and any organization providing local government services (known as associated

employers) since 1998. A diversified multi-employer plan emerged, bringing together

tax-funded employers and unionized and non-unionized employees throughout

Ontario.

Today, the Pension Plan has 950 employers, although only 25 employers have more

than 1,000 plan members. On the employee side, the Pension Plan has 420,000

members (including retirees). Active members are represented by 36 unions and

associations, of which six unions/associations have more than 7,500 plan members

each.

A Professionally Managed Customer Service Organization

In the past five years, Pension Services has evolved from a traditional transaction-

based plan administrator into a full-fledged and professionally managed customer

service organization. It employs about 170 professionals with diverse talents,

including benefits processors, customer service representatives, project managers,

information technology specialists, operations managers, actuaries, lawyers and

policy, government and stakeholder relations and communications specialists.

17

Stakeholders and plan members are engaged through an extensive outreach program

including 340,000 inbound and outbound calls per year; 1,000 education sessions for

20,000 stakeholders and plan members annually; two annual stakeholder information

meetings; presentations to stakeholder organizations; and relations with Canadian

governments and non-government organizations in the financial, pension, public

policy, educational and union sectors. The OAC web site has 770,000 visits annually

and fully discloses OMERS financial information through an electronic annual report

that combines information for the OAC and SC. All members also receive a simplified

annual report.

On the regulatory front, tenacious effort over many years culminated in the

elimination or reduction of regulatory barriers to growth contained in the Federal

Investment Regulations that are incorporated in Ontario’s Pension Benefits Act. In

2011, after three years of effort, the OAC gained exemption from solvency funding as

a jointly sponsored pension plan, to the benefit of all stakeholders as well as giving

OMERS a competitive advantage for pension plans lacking solvency relief.

Technological Sophistication

Pension Services installed most of its current pension systems 15 years ago to

improve productivity, service standards and data integrity, positioning the OAC as an

industry leader in customer service. Today, it is preparing for a new era of potential

growth with a pension system incorporating advanced technologies, such as cloud

storage of pension data and data mining and analytics, to design better products and

outreach strategies.

18

The new Pension Services IT system, scheduled for completion in 2014, is flexible,

sustainable and scalable. It will provide increased functionality and flexibility to handle

growth in new services and products and accommodate new employers and their

pension plans.

An Innovative Customer-Focused Business

For many years, plan members asked OMERS to provide savings products. OAC

responded with the Additional Voluntary Contributions (“AVCs”) program. The program

allows plan members to make additional contributions to the Pension Plan and transfer

RRSP funds into an AVC account. AVCs were first offered in 2011 and in two years

7,000 plan members have contributed $152 million. In the next five years, AVCs could

raise as much as $1 billion. The AVC program has sparked member interest in buying

back past service to enhance pension benefits and transfers into the Pension Plan.

Buybacks also have raised about $150 million of capital in the last two years.

The Plan’s Funding Policy

Pension Services is responsible for the Pension Plan’s funding policy, including the

actuarial methods and assumptions, based on recommendations by the external

actuary appointed by the OAC. Senior management, with the assistance of the

actuarial and legal teams, provides extensive technical support to the SC. This support

was critical in assisting the SC Board in making knowledgeable decisions about

contribution rates and benefit changes to address the Pension Plan’s funding

deficiency; played a critical role in the development of the SC’s Statement of Plan

Design Objectives and Strategy setting out protocols for future contribution rate or

benefit changes; and clarified the methodology for contribution rate allocations

between different membership classes (NRA 60 and NRA 65) within the Pension Plan.

Plan Membership Growth

19

Pension Services discusses consolidation opportunities with Ontario public pension

plans lacking scale and sufficient internal resources in plan administration and

investing. Current discussions include three major municipalities regarding their closed

plans and other municipally related plans that fall within Section 5 of the OMERS Act.

The OAC’s Strategic Plan emphasizes plan membership growth beyond Sections 5 and

6 employers. To facilitate this membership growth, at the direction of the OAC Board,

Management has undertaken extensive research to develop potential new benefit

classes within the Pension Plan that should appeal to plans seeking more flexible

terms than the current plan text allows. This growth would support OMERS

sustainability by allowing for the most efficient risk pooling (for assets and liabilities)

across broad groups that over time would reduce contribution rate volatility and

reduce administration costs and enhance investment returns.

While there are risks in plan membership growth, they are overshadowed by the risks

to OMERS staying with the status quo and the public perception that defined benefit

plans are financially unsustainable. Public policy discussions at both the federal and

provincial government levels are leap-frogging other public policy issues as

governments come to terms with an aging population and a pension system with little

flexibility for needed and important change.

20

The Investment Enterprise

With $80 billion of capital under management, including $55 billion of Pension Plan net

assets, the OAC invests in a wide diversity of assets around the world. It has

specialized investment platforms that originate and actively manage investments.

Many transactions are complex and individually very large, often deploying advanced

investment techniques.

The OAC Board is committed to protecting OMERS Triple A credit rating by complying

with legislation that requires pension funds to invest prudently and avoid excessive

use of debt. On June 27, 2012, Standard & Poor’s affirmed OAC’s ‘AAA’ long-term

issuer credit and ‘A-1+’ short-term ratings and stated:

”The affirmation reflects our view of OMERS very strong net asset base;

continued participation of Ontario municipalities, local boards, including school

boards (non-teaching staff only) and their employees; and solid long-term

investment performance. The stable outlook reflects our expectations that in

the next two years, the fund will continue increasing its strong net asset

position and maintain its very strong liquidity levels, pension contribution

inflows will continue to be stable, and investment performances meet or

exceed their benchmarks.”

OAC is one of a handful of Canadian institutions with a Triple “A” credit rating – fewer

than 10 institutions. Besides the Federal Government, no Provincial Government has a

Triple “A” credit rating other than Alberta. No Canadian chartered bank has a Triple

“A” credit rating.

OMERS Triple “A” credit rating is the result in part of the OAC Board’s decisions to

expand the OAC’s direct professional management of the Pension Plan’s assets and

diversify the asset base by entering new asset classes.

21

It is the breadth, depth and complexity of this professional management that requires

informed governance. This directly led to the OAC Board passing a resolution in 2008

to move toward a board on which sponsor directors would be augmented by external

directors with investment, financial experience and other required board skill sets.

This composition has been recommended to the SC Board which controls the

appointment process.

Liabilities Drive the Investment Strategy

The investment strategy is liabilities driven, based on the financial agreement to

deliver $64.5 billion of pension benefits to all current plan members over their

retirement years. The present value of liabilities is expected to grow by 35% to exceed

$87 billion by 2016.

Many organic factors drive liability costs, such as enhanced permanent benefits

approved more than a decade ago when the Pension Plan was in surplus and the

persistence in recent years of historically low interest rates. The plan is aging. As

members get closer to retirement, benefit costs increase due to the time value of

entitlements and new benefits earned since the last actuarial valuation (required every

three years). The baby boom generation will retire over the next 20 years and the

average age of the membership base will not return to today’s level (46 years old)

until 2034. Retirees are living longer and since 1995 the average lifespan of a retired

member has increased by almost two years. For every additional year of life

expectancy for the current membership, expected liabilities could increase by

approximately 2%.

Aging and life expectancy demographics are included in actuarial assumptions in

estimating liability costs, though there is a risk that continuous aging could result in

more stringent actuarial valuation standards with respect to mortality assumptions,

which would increase liabilities further. Another risk is fiscal decisions by municipal

governments and other local employers to downsize their workforce and privatize

services to new employers who do not join the Pension Plan. Forced early retirements

22

will increase benefit costs. If younger workers are laid off, the Pension Plan will age

faster. Currently, the Pension Plan has 2.3 active members for each retiree, compared

with a 3.8:1 ratio 20 years ago.

The growing cost of liabilities puts increased pressure on investment performance to

finance the pension promise at a time when traditional assets like stocks and bonds

are an unreliable source of sufficient investment income. The Pension Plan’s funding

shortfall will remain around $10 billion in the short term. Under the SC policy of

temporary contribution rate increases and benefit adjustments, and based on the

actuarial requirement of a 6.5% annual investment return, the Pension Plan should

return to surplus by approximately 2028.

The investment strategy, approved by the OAC Board (which is embedded in the OAC

Strategic Plan) and being implemented by OAC investment professionals, is designed

to return the Primary Pension Plan to surplus 10 years sooner.

The Search for Consistent Investment Returns

The current liability-driven investment strategy has been in place since 2004 in

response to the Pension Plan’s funding position going from a $6 billion surplus in 1998

to a $3 billion deficit in 2003. This dramatic reversal in just six years followed a

mandatory contribution holiday under the Income Tax Act for a pension plan with what

was then deemed to be “excessive” surplus, decisions by the sponsors to make

permanent benefit enrichments that continue today, and the steep 2000-2002 decline

in the stock market when the dot.com bubble burst. In 2004, the OMERS Board

decided to allocate a substantial portion of future capital to private market

investments so that the Pension Plan would be less vulnerable to another stock market

catastrophe. (Unfortunately, the Pension Plan had barely regained break-even in 2007

when the 2008 global credit crisis and stock market meltdown drove it back into

funding deficit.)

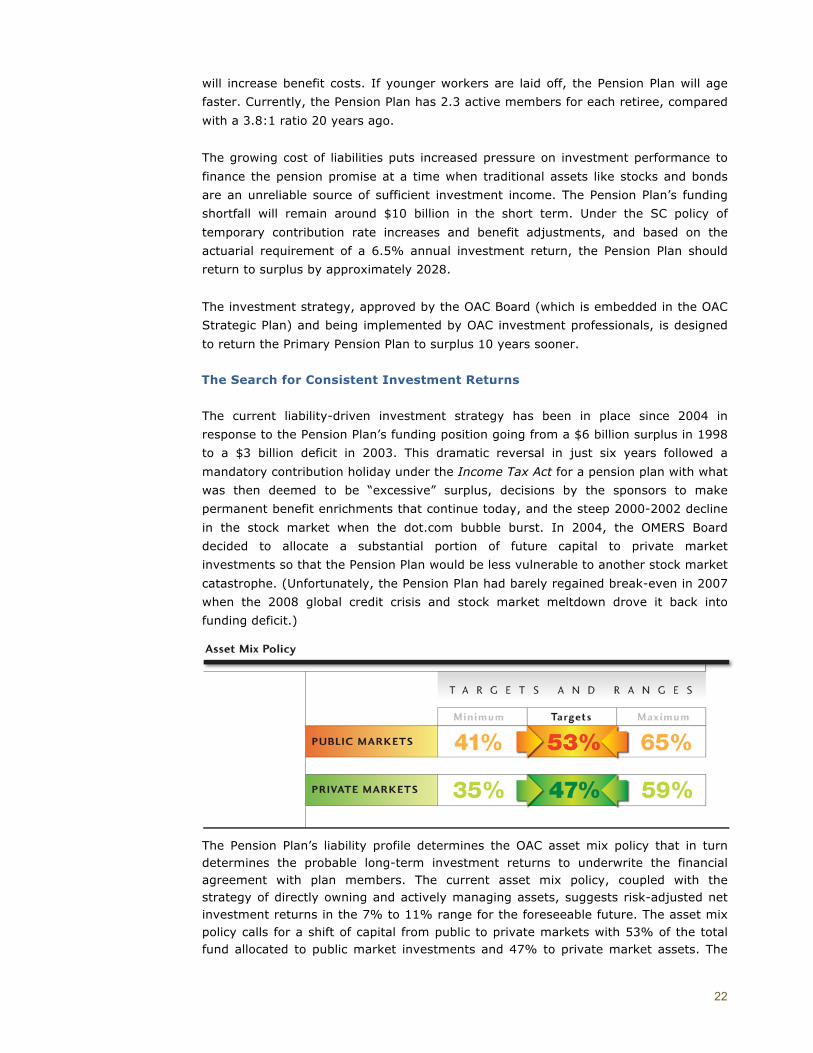

The Pension Plan’s liability profile determines the OAC asset mix policy that in turn determines the probable long-term investment returns to underwrite the financial agreement with plan members. The current asset mix policy, coupled with the strategy of directly owning and actively managing assets, suggests risk-adjusted net investment returns in the 7% to 11% range for the foreseeable future. The asset mix policy calls for a shift of capital from public to private markets with 53% of the total fund allocated to public market investments and 47% to private market assets. The

23

objective is to acquire quality investments in public markets to generate dividends, interest and capital gains from a diversified portfolio and strong cash-yielding investments in infrastructure, real estate and private equity assets.

Progress in earning acceptable investment returns is best measured since the OAC

Board approved shifting capital to private market investments in 2004:

• exposure to public markets has decreased from 82% in 2004 to 58% in 2011,

with private market assets growing from 18% to 42%;

• the value of public market assets grew by 9% from $29.5 billion in 2004 to

$32.1 billion in 2011, while private market assets almost quadrupled from

$6.7 billion to $23.6 billion; and

• the Pension Plan has earned an eight-year annualized return of 7.5% – above

the 6.5% actuarial investment return requirement to achieve full funding.

The goal is to earn consistent returns above the actuarial requirement by investing

prudently as required by the OAC Board in compliance with the PBA.

Growth in Capital Under Management

Capital under management is projected to more than double in the next few years

from $80 billion in 2011 and will consist mostly of equity and related debt on the

Pension Plan’s balance sheet, supplemented by third-party capital not included in the

Pension Plan or its funding position. A strategic goal is to attract third-party capital so

that OAC can increase investment income from large-scale assets that it would

otherwise be unable to acquire because of the current capital size of the pension fund

and the risk management associated with a large financial exposure to a single

investment. Managing third-party capital will also generate fees to reduce investment

expenses.

24

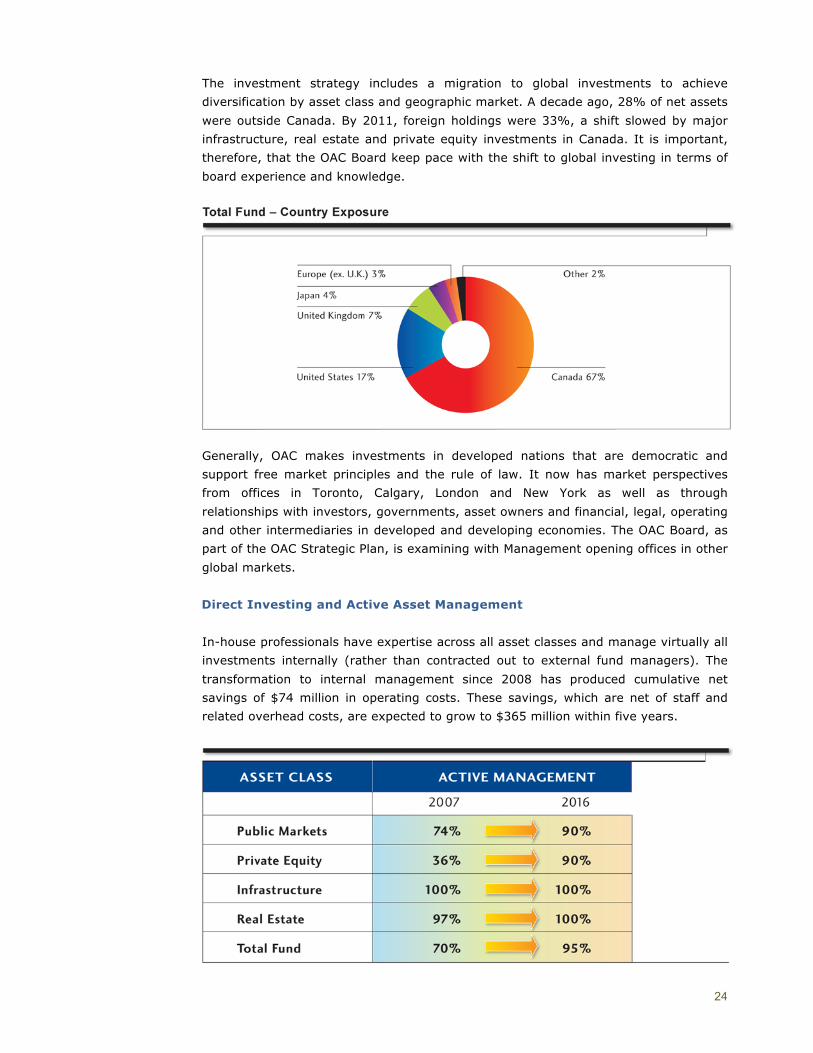

The investment strategy includes a migration to global investments to achieve

diversification by asset class and geographic market. A decade ago, 28% of net assets

were outside Canada. By 2011, foreign holdings were 33%, a shift slowed by major

infrastructure, real estate and private equity investments in Canada. It is important,

therefore, that the OAC Board keep pace with the shift to global investing in terms of

board experience and knowledge.

Generally, OAC makes investments in developed nations that are democratic and

support free market principles and the rule of law. It now has market perspectives

from offices in Toronto, Calgary, London and New York as well as through

relationships with investors, governments, asset owners and financial, legal, operating

and other intermediaries in developed and developing economies. The OAC Board, as

part of the OAC Strategic Plan, is examining with Management opening offices in other

global markets.

Direct Investing and Active Asset Management

In-house professionals have expertise across all asset classes and manage virtually all

investments internally (rather than contracted out to external fund managers). The

transformation to internal management since 2008 has produced cumulative net

savings of $74 million in operating costs. These savings, which are net of staff and

related overhead costs, are expected to grow to $365 million within five years.

25

PUBLIC MARKETS INVESTMENT STRATEGY

The global economic outlook, with its prospect of subdued investment returns for the

foreseeable future, is changing OMERS traditional approach to investing in public

markets. Historically, asset/liability studies established relative return objectives for

the asset classes managed by OMERS Capital Markets (“OCM”). Relative returns

measure performance against market index benchmarks. Earning minus 5%, for

example, when the benchmark return is minus 10% is interpreted as “value add” –

but beating a negative benchmark return does not pay pensions. Only positive

absolute returns pay pensions – and absolute returns are OCM’s focus.

Between 2008 and 2011, OCM established five investment teams, each with specific

capital allocations. Most teams manage portfolios incorporating beta (earning market

index returns) and alpha (earning positive absolute returns under all market

conditions). The Multi-Strategy team invests in equities, sovereign bonds, inflation-

linked bonds, corporate bonds, gold and other commodities and currencies (beta and

alpha investing). The Quantitative team invests in Canadian, U.S. and foreign equity

market indexes (beta investing). The Global Equities team is primarily focused on

picking stocks (alpha investing). The Hedge Fund team, based in New York, does pure

alpha investing. The Fixed Income and Foreign Exchange team has beta and alpha

components in federal, provincial and municipal government bonds, corporate bonds,

real return bonds, Canadian commercial mortgages and foreign currency trading.

Under the new strategy, OCM is pooling all beta investments in a single portfolio and

all alpha components in a separate portfolio, each with dedicated investment teams.

The beta portfolio uses risk parity and economic leverage. Risk parity adjusts the risk

exposure of different asset classes so that their return profile is approximately equal.

Once asset class returns and risk profiles are equalized, the more diversified beta

portfolio is better able to weather sharp declines in equity markets. Achieving risk

parity across asset classes involves economic leverage. For example, buying futures

contracts on margin, rather than for cash, frees up capital to create more risk

exposure in fixed income and produce a return profile that is similar to equities. With

the return streams and risk profiles of different asset classes equalized, a portfolio can

26

be constructed that performs better across different economic environments, reduces

overall portfolio risk and improves the consistency of investment returns.

The alpha portfolio is being structured on a standalone basis with investment teams

assigned risk budgets in specific asset classes (such as commodities, foreign currency

and sovereign debt) or global economic sectors (such as healthcare, consumer

products and energy) to meet pre-determined absolute return targets.

OCM’s risk managers make allocation adjustments to the beta and alpha portfolios to

take on more risk under certain economic conditions and reduce risk under other

economic conditions to find the best absolute return opportunities.

INFRASTRUCTURE INVESTMENT STRATEGY

OMERS created Borealis Infrastructure in 1997 to pioneer pension fund investing in

what was then a new asset class. Few organizations in the world have the built-in

proprietary expertise of Borealis to pursue, finance and acquire large-scale

infrastructure assets on a sustainable basis against increasing market participation.

OMERS is a co-owner of Associated British Ports, which has 21 marine ports in the U.K.

To learn the business, Borealis began by making small investments of $10 million to

$25 million in hospitals, schools and utilities. Today, as one of the world’s largest

infrastructure asset management firms, it writes equity cheques of $1 billion and

more. Borealis has $19 billion of capital under management, all of which is on the

Pension Plan’s balance sheet. These investments have an enterprise value exceeding

$50 billion when the capital of co-investors is included. Today, it employs 68

investment professionals, including 14 in London and New York.

27

Borealis’ strategy is to build platform businesses that are non-GDP dependent, have

regulated or semi-regulated revenue and other income protections, and have strong

management teams that participate in performance results. It is focused on high-

quality large-scale infrastructure assets with stable and predictable returns and cash

yields, often under 30 to 50-year concessionary contracts. In evaluating acquisitions,

Borealis conducts in-depth operational, financial and legal due diligence that includes

determining the optimal leverage assumptions in line with the underlying economics of

the business. Although it may pursue deals on its own, Borealis often partners with

investors that share OMERS long-term commitment to managing assets.

Borealis illustrates the benefits of owning and actively managing equity positions in

large-scale assets. In 2011, the $9 billion of net operating assets owned by OMERS

generated $722 million of gross investment income. By 2016, this income is expected

to exceed $1.5 billion. Borealis is a reliable and consistent contributor in delivering the

pension promise.

OMERS and Ontario Teachers’ own HS1 Limited, Britain’s high-speed rail line between London and the Eurotunnel

Borealis invests in developed markets where governments and corporations are

looking to sell off assets as they deleverage their balance sheets. Preferred markets

are Canada, the United States and Europe. Borealis is exploring and beginning to

pursue assets outside its traditional markets in, for example, South America. It has

historically avoided emerging markets where assets and regulatory environments have

not matured sufficiently. This has begun to change as political and regulatory systems

have entered an unprecedented period of stability.

28

REAL ESTATE INVESTMENT STRATEGY

Few pension plans in the world own a full-service real estate company. In 2001, the

OMERS Board approved the acquisition of Oxford Properties, one of Canada’s most

successful real estate companies. Founded in Calgary in 1960, Oxford absorbed

OMERS previous real estate interests and today is an international company with $20

billion of capital under management and employs 41 investment professionals,

including 21 in London and New York. It also employs 1,300 people in corporate and

property management across Canada. Oxford is a reliable and consistent contributor

to the Pension Plan.

Through Oxford, OMERS owns a large portfolio of Class A office properties, with

dominant positions in downtown Toronto and downtown Calgary, and three large

properties in London; mega shopping malls in the Greater Toronto Area; seven five-

star resort hotels in Ontario, Quebec, Alberta and British Columbia; multi-residential

apartment buildings; and thriving business parks.

Through Oxford, OMERS owns Class A Office towers in downtown Toronto (and other Canadian cities)

Oxford’s strategy is to own and manage high quality and diversified commercial real

estate and undertake select development and redevelopment projects to strengthen

the portfolio and enhance long-term returns. Its primary markets are Canada, the

United States and United Kingdom. Oxford’s properties have high occupancy by

creditworthy tenants on long-term leases in large part due to exceptional property

29

management, attentive tenant services and the unrelenting commitment to energy

conservation, reduced carbon emissions and operational efficiencies.

Oxford is generating growth with major development projects underway in Toronto,

Calgary, Vancouver, London and New York in the industrial, office, retail and multi-

residential property classes. The largest development project is Hudson Yards in New

York. This strategic investment has put Oxford “on the map” in the U.S. and a major

office lease has already been signed. When this undeveloped property in Manhattan is

completed, Hudson Yards will include six million square feet of office, retail and

hospitality, and an additional six million square feet of residential density. Another

major project is in London, where Oxford is a co-investor with British Land to build a

52-storey office and related retail project at a key intersection in the City of London,

with more than 30% of the space pre-leased.

Oxford is a partner in Manhattan’s Hudson Yards development project

Canada remains the primary market and Oxford recently acquired a multi-residential

complex in Toronto, an industrial property in Brampton, co-ownership of a shopping

centre in Richmond Hill, 64 acres for industrial development in Burnaby and the Metro

Toronto Convention Centre Complex, including the InterContinental Hotel.

In addition, the London team recently acquired a 190-acre master planned business

park with 1.3 million square feet of Grade A office space near London. Oxford is

monitoring high-quality core opportunities in France and Germany that will likely

become available at attractive prices.

30

PRIVATE EQUITY INVESTMENT STRATEGY

OMERS owns its own self-built private equity firm that is emerging as a successful

international player. For most of its history, OMERS invested in private equity through

externally managed funds. In 2008, the OAC Board approved a change in strategic

direction – to directly own private companies and actively engage in strategic planning

with the management of these companies.

Today, the private equity company, OMERS Private Equity (“OPE”), is focused solely

on direct active investing in North America and Europe. The strategy is to acquire for a

minimum equity investment of $100 million majority control of companies with an

enterprise value of $200 million to $1.5 billion. OPE also considers joint control

investments with like-minded partners for companies of a greater size. The direct

investment program represents 57% ($3.6 billion) of the OPE total portfolio. The

remaining assets are investments in and commitments to externally managed funds

that are gradually being wound down or divested.

OPE has built a strong team to originate and manage the expanding portfolio of direct

investments, as well as legacy fund investments. It employs 26 investment

professionals, including 16 in London and New York. The switch to direct investing has

generated substantial savings for the Pension Plan that more than offset the costs of

internal investment management. By investing directly, OPE avoids paying carried

interest to external managers, typically 20% of investment income when assets are

sold, as well as annual management fees.

OPE owns more than 30 private companies in Canada, the U.S. and the U.K. Unlike

typical private equity firms that seek to cash in their value gains within 7 to 12 years,

OPE is a patient investor with no set exit deadlines so that it can help its investee

companies attain sustainable long-term growth and profitability.

OPE has had very strong returns over the last eight years and expects to continue this

performance as it withdraws from externally managed funds and their associated fees

and delivers the full amount of investment returns to OMERS through active

management.

31

The Corporate Office

The corporate office provides enterprise-wide executive leadership including risk

management, policy compliance, financial disclosure and strategic planning and

deploys advanced human resources leadership training and customized IT systems to

administer the plan and monitor and value investments on a daily basis.

Cross-enterprise teams bring executives together from different work environments to

find improvements in enterprise-wide management. A committee led by the CFO with

Investment and Pension Services members has enhanced IT infrastructure, security

and overall connectivity across the enterprise. An Investment Tax Committee, chaired

by the CEO, examines the tax risks of investing in foreign jurisdictions. An Emerging

Markets Committee, chaired by the CIO, is studying the legal, political, economic and

ownership risks of investing in emerging markets.

The Corporate Office manages strategic and operational risks. The CFO chairs the 11-

member Cross-Enterprise Risk Management Committee and the CIO chairs the 12-

member Investment Risk Management Committee. Each business unit also has a risk

management committee. These resources are backed by technologies and systems

that track, quantify, analyze and measure 54 specific risks with detailed quarterly and

annual reports to the OAC Board.

32

The Corporate Office leads the development of all strategic initiatives, including

initiatives to raise third-party capital. A potential strategic opportunity is the federal

proposal, supported by several provinces, to allow financial institutions, notably banks

and insurance companies, to offer Pooled Registered Pension Plans (“PRPPs”) to

Canadian workers lacking workplace pension plans. The OAC Board has approved in

principle securing a designation for public sector plans to be eligible administrators for

PRPPs to keep OAC’s options open and to allow OMERS to decide at a later date

whether to proceed. This initiative would raise capital outside the Pension Plan.

The Corporate Office has been working for several years on offering investment

contracts to Canadian pension plans choosing to invest with OMERS. The OMERS Act

gives the OAC powers to offer plan administration and pension fund investment

services to other pension plans/pension funds, federal and provincial governments and

their agencies and crown corporations, as well as colleges, university endowments,

corporations and charitable organizations.

The Corporate Office is also responsible for a pioneering initiative in the pension

industry to form an alliance with global investors to invest with OMERS in multi-billion-

dollar infrastructure assets that generate large and sustainable annuity-like cash flows

to pay pensions. To date, two Japanese institutional investors have committed to the

alliance.

Finally, the Corporate Office is responsible for OAC enterprise strategic planning with

the OAC Board.

Like the board of any public or private sector corporation, the OAC Board holds

Management accountable for performance and strategic progress and through board

committees monitors its compliance with a wide array of governance policies.

33

ENHANCING OAC GOVERNANCE

The best way for the OAC to deliver on its mandate under the OMERS Act is to follow

best corporate governance practices within a jointly sponsored multi-employer pension

plan context. With this in mind, the OAC Board has worked hard to improve its own

governance within the limits of its statutory authorities.

A governance reform project in 2008 updated how the OAC Board conducts its affairs

and its relationships with board committees and Management. Early in 2012, the OAC

Board took actions to reduce the governance burden that has arisen under the bi-

cameral structure, culminating in 2011 in 85 board and committee meetings by the

OAC and SC Boards, including joint meetings. Starting in July 2012, the OAC Board

will hold board and committee meetings every other month over a two-day period.

There is, however, unfinished business on the governance front. A priority is to

configure the composition and competencies of the OAC Board to higher standards

aligned with the scope and complexity of the OAC. The OAC Board has been working

on this mission since 2008.

The SC Board alone has legal authority over the appointments to the OAC Board under

the OMERS Act 2006. That a single entity, the SC, has the sole statutory authority to

appoint all directors is unusual among large Canadian pension plans. The OAC Board is

of the view that the sponsors should have a clear, direct and legal appointment

authority.

The OAC requires governance competencies quite different from those at the SC

because it is a different enterprise with a different purpose and different

34

accountability. The primary fiduciary duty of the OAC Board is informed oversight of

the OAC and its Management and ultimately oversight of the assets and liabilities of

the Pension Plan.

Accountabilities

The sufficiency of accountabilities under the bi-cameral governance model is identified

as a topic for examination under the Review Act. Active plan members, retirees and

employers are specifically mentioned. Sponsors representing employers and

employees are almost invisible under the Review Act and OMERS Act. A missing

ingredient is a roadmap for accountabilities among sponsors, the OAC and the SC and

their respective boards. For example, the OMERS Act provides little direction on the

accountability of the OAC and OAC Board, or the SC and its board, to sponsors.

An effective governance structure should clarify these accountabilities, leading to a

clearer understanding of the responsibilities of the OAC Board.

OAC Board Competencies

In 2007 and 2008, the OAC Board spent considerable effort studying the composition

and competency requirements of the OAC Board with an eye to matching composite

competencies with the requirements of overseeing a large and complex corporation.

As spelled out in a resolution it passed on June 19, 2008, the OAC Board’s Governance

Committee considered:

1. A representational model, under which identified parties have the power to

appoint a person to the OAC Board and there is no formal consultation process

for evaluating the overall needs of the OAC Board.

2. A competency-based model requiring a regular review of the needs of the

OAC Board in light of the priorities of the OAC to ensure the OAC Board has

the skills and expertise required.

3. A hybrid model responsive to both the representational model and the

competency model with some of the OAC Board appointed on a

representational basis and the rest based on a competency model approach.

The Governance Committee also considered several key factors:

• the range of competencies identified as important for the OAC Board and the

competency model;

• the increasingly complex and global nature of investments that require board

stewardship and strategic oversight in such an environment; and

• the fact that, while a representational model may be appropriate and

desirable at the sponsors’ level, requirements for the OAC are different.

35

The 2008 resolution states: “In today’s global investment environment, a competency-

based board would translate into an OAC Board with not only the pension, human

resources, compliance and other expertise that exists today, but also deep

competencies in areas such as international finance and global capital markets risks.”

The OAC Board endorsed a competency-based hybrid model as optimal for the

composition of the OAC Board and forwarded its recommendation to the SC for its

consideration in preparing a new by-law for the composition of the OAC Board, as

contemplated by Section 33 of the OMERS Act.

The same sentiments were set out in a detailed February 19, 2009 letter to the then

Minister of Municipal Affairs and Housing. In that letter, the OAC Board acknowledged

that its legacy would be elevating the OAC Board’s composition of skills, knowledge

and experience.

In a lengthy February 29, 2012 letter to the SC Board, the OAC Board elaborated on

its recommendations with the emphasis on a competency-based hybrid board and

robust appointment process. Under the OAC Board’s definition, the OAC Board would

consist of some representational and some expert appointments, with the latter filling

out investment, finance competency and global business requirements.

In support of the OAC Board recommendations, the OAC Board letter documented the

best governance practices researched and recommended by bodies as diverse as the

Treasury Board of Canada, the Conference Board of Canada, the Canadian Coalition

for Good Governance, the International Centre for Pension Management and the

Ontario Secondary Schools Teachers’ Federation. In addition, the OAC Board retained

Deloittes to provide an independent report on the required skills and competencies of

the OAC Board.

Impartial observers of public and private sector governance have expressed

knowledgeable opinions that are relevant to the future governance of OMERS. One

example is the Canadian Coalition for Good Governance (of which OMERS is a

founding member) that states in its governance guidelines:

“We believe the single most important corporate governance requirement is to

have directors of quality, both individually and as a whole … A number of directors

should have direct experience in the industry or industries that the company

operates in, to make sure the board asks for the right information from

management, asks knowledgeable and insightful questions and has the

background it needs to take appropriate positions.”

This submission is consistent with the OAC Board’s long-standing belief in the

importance of a hybrid board consisting of sponsors representatives and external

directors with competencies relevant to the scope and complexity of plan

administration, fund investing and the performance of the OAC under the OMERS Act.

In August, 2012 the Co-Chairs of the SC Board invited the OAC Board Chair and OAC

Governance Committee Chair to join the Co-Chairs and the SC Governance Committee

36

Chair to discuss for the first time the competency needs of the OAC Board. The

purpose of this SC nominating committee meeting was to share OAC Board

competency requirements with six sponsors whose current appointments were due to

expire at the end of 2012. This was a positive step in beginning a discussion on the

governance needs of the OAC Board as a whole.

OAC Board Compensation

Director compensation and expense policy are related to enhancing board

competencies.

The OAC Board believes that its directors should be fairly compensated for the work

they do at rates consistent with fiduciaries at public sector pension organizations in

Canada. Introducing a fair and market-based compensation policy for OAC directors

would make it easier to attract individuals with expertise relevant to OAC activities

who make all or a good part of their living from serving as professional directors.

Governing a large customer service and investment organization that competes in

public and private markets at home and abroad is not an act of benevolent public

service, especially in view of the risks and liabilities implicit in delivering a multi-

billion-dollar pension promise to 420,000 Ontarians.

OMERS policies of transparency and full disclosure will keep all stakeholders informed

annually on the remuneration and expenses of OAC Board members.

Introducing a Robust Nominating Process

Identifying the ongoing competency needs required by the OAC Board only matters if

they are supported by a robust nominating process. A robust nominating process does

not currently exist for the OAC Board.

To be robust, the nominating process should:

• actively and directly engage employer and employee sponsors;

• include an influential role for the OAC Board (through its Governance

Committee) because it knows the gaps in the OAC Board competencies;

• consider the competency needs of the OAC Board as a whole so that the OAC

Board’s Governance Committee can provide guidance to sponsors on the

quantitative attributes required when vacancies occur; and

• consider engaging a search firm to assist sponsors and the OAC Board in

identifying, evaluating and recruiting potential directors with requisite

competencies.

The objective is to strengthen the overall composition of the OAC Board to ensure it

can provide independently minded oversight of the OAC trust assets and properly

37

represent the best interests of the entire plan membership. This is a particularly

sensitive subject as some employees have no sponsor affiliations.

Since 2006, a majority of sponsors groups have continued to appoint “one of their

own” to the SC and OAC Boards. This may continue to be appropriate for certain

sponsors. The reason for emphasizing OAC Board competency requirements and a

robust nominating process, however, is to broaden sponsors’ perspectives of

appropriate appointments while preserving their right to decide who governs OMERS.

For example, employers have a contingent interest in the Pension Plan’s funding

surplus or deficit. Their priorities are to ensure that the OAC Board has the right

balance of expertise to protect the taxpayer interest and to ensure the Pension Plan’s

financial viability. This perspective by employers recognizes that:

• municipalities and their agencies, including police service boards and utilities,

make approximately 65% of employer contributions to the Pension Plan. They

are all supported by municipal taxpayers; and

• provincially supported agencies, such as school boards and children’s aid

societies, and certain municipal programs, such as housing authorities and

health units, make about 35% of employer contributions. They are all

supported by provincial taxpayers.

Flexibility for Future Growth

The current governance structure does not provide sufficient flexibility to

accommodate plan membership growth, which is critical to the Pension Plan’s

continued sustainability.

It is impossible for a large pension plan to give everyone a seat at the boardroom

table. An efficient, effective and fair nominating and appointment process should,

however, engage as many employers and employee groups as possible. Under the bi-

cameral model, 13 designated sponsors have appointment rights. On the employer

side, all are associations with the exception of the City of Toronto. On the employee

side, three associations and four unions collectively represent 78% of the plan

membership.

For membership growth to occur, plans considering consolidation with OMERS Pension

Plan must see a clear path to participating in its governance, a situation that does not

exist today. For example, if a large employer/employee group were to join the Pension

Plan neither the employer nor the new plan members would have a seat on or

appointment rights to the OAC Board.

In its 2012 budget, the Ontario government addressed improving efficiencies in

pension fund management and noted the importance for pension funds to have access

to large-scale investment opportunities. The 2012 budget repeated the policy

objective of facilitating access by smaller Ontario defined benefits pension funds to the

investment expertise of the larger Ontario public sector pension funds. If the Ontario

38

government enables plan consolidations with large plans like OMERS, the restricted

access to governance under the bi-cameral model would have to be addressed.

Commitment to Governance Excellence

Governance standards in the corporate and public sectors increasingly emphasize the

competencies and independent mindedness of directors. Other best practices deal with

clear term limits, board self-evaluation and renewal practices, and public transparency

on management accountability to the board for performance, policy compliance and

compensation. The Ontario Pension Benefits Act does not really address the

governance expectations and standards for public sector pension plans, many of which

are among Canada’s most influential financial institutions.

Best practices include:

• set and staggered terms for directors, with a limit on eligibility for

reappointments to ensure board regeneration over time;

• a multi-year term for the OAC Board chair, instead of a one-year term;

• governance leadership training for representational directors;

• expanding the current annual process for evaluating the performance of the

OAC Board and its committees to include annual assessments through

confidential board member questionnaires summarized by an independent

consultant for review by the OAC Board to determine how governance should

be enhanced; and

• a confidential annual peer review to assist each director in identifying self-

development initiatives and provide guidance on reappointment

recommendations.

39

CLARIFYING ROLES AND AUTHORITIES

The OMERS Act 2006 has created inevitable tensions and inefficiencies between the

two boards by not clearly delineating and separating authorities in two key areas. As a

result, operational inefficiencies and extra costs occur through duplication of effort and

resources. It is imperative that the OAC and SC Boards work together to clarify

authorities in the best interests of all plan members and employers.

One area of inefficiency and overlap concerns investment capital outside the Pension

Plan. The OAC Board believes that the OAC should be responsible for decisions to raise

third-party capital for investment purposes where the capital raised does not affect

the Pension Plan’s contribution rates or funding. Examples of non-pension plan capital

growth initiatives include investment contracts offered by an OAC subsidiary, OMERS

Investment Management Inc., so that Canadian pension plans can invest their capital

alongside the Pension Plan in OMERS total asset mix or in contracts that earn the

returns of OMERS infrastructure, real estate and private equity portfolios.

An even more complex area relates to inter-corporate confusion over the Pension

Plan’s funding policy. The funding policy has resided with the fiduciary board since

1992 when the Ontario government made plan changes to shift responsibility for

sharing funding shortfalls or surpluses on plan members and employers.

The OAC’s sole responsibility for the Pension Plan’s funding policy is clearly enunciated

in the OMERS Act 2006. The purpose of a funding policy is to establish a framework

for funding a defined benefit pension plan taking into account factors relevant to the

plan, the contributing employers and the plan members. There is an inextricable

connection between development of the funding policy and pension fund investing.

The OAC has the historical and continuing responsibility for pension investments and

investment policy. As the fiduciary, it is always required to act in an evenhanded

manner with respect to all categories or classes of members and participating

employers. All told, the OAC must be responsible for the funding policy. This is

particularly important in a jointly sponsored pension plan where funding obligations

are pooled over a large and diverse group of employers and plan members.

40

Other specific authorities assigned to the OAC reinforce its responsibility for the

funding policy, such as:

• determining the actuarial methods and assumptions to be used for purposes

of administering the pension plans and pension funds, based on

recommendations from the actuary;

• appointing the OMERS external actuary;

• appointing the OMERS external auditor;

• filing actuarial valuations as required by the PBA;

• providing the SC with actuarial advice and cost estimates on the impact of

plan amendments or other changes on contribution rates; and

• providing the SC with advice on administrative or other issues arising from

proposed plan changes.

The OAC Board’s retention of these authorities is important to ensure that the growth

in benefit levels does not outpace reasonable contribution rates and the ability of the

OAC to generate reasonable risk-adjusted investment returns. This means ensuring

that contribution rates are set and benefits managed within the parameters of the

funding policy, which will mitigate potential conflicts of interest for sponsors.

41

CONCLUSION

The OAC Board has not made any specific recommendations in this submission for two

reasons. The first is that OMERS is a very large and complex organization and it is

important that all points of view be expressed before conclusions are reached. The

second reason is that the OAC Board has every confidence that the Reviewer will take

a dispassionate and objective view on behalf of Ontario and its provincial and

municipal taxpayers.

Turning to the OMERS Administration Corporation, this brief portrays a corporation

that is innovative in meeting the pension promise to plan members, clear on its

accountability to the entire membership and responsive to the social and fiscal needs

of public policy with respect to public sector pension plans. The OAC Board and

Management have demonstrated governance leadership in crafting the annual OAC

Strategic Plan since 2008 that anticipates the world in which the OAC must operate

and compete five years ahead and incorporates initiatives to sustain and grow plan

membership, generate stable and consistent cash returns, manage strategic risks and

optimize investment and capital growth opportunities.

The role and legal rights of the fiduciary board as the plan administrator and pension

fund trustee are clear and do not require amendment. While the OAC Board has

enhanced its own governance, it has reached the limits of its statutory authority in

elevating the competencies of the OAC Board as a whole, aligning those competencies

with the scale and complexity of the OAC and seeking a robust nominating process

that engages all employer and employee sponsors groups directly. In addition, the

submission draws the attention of the Reviewer to the need to clarify certain OAC and

SC authorities that have given rise to tensions and inefficiencies. Making progress on

these points alone will go a long way toward enhancing the efficiency, effectiveness

and fairness of OMERS governance.

The Reviewer has promised constructive and inclusive consultation after the

September 4, 2012 deadline for written submissions. The OAC Board, through its

Chair, looks forward to engaging the Reviewer in such discussions and to re-address

any of the issues raised in this submission.

42

N O T E S

![Property 452 Reviewer-[Vena Verga] Property Midterms Reviewer](https://img.dokumen.tips/doc/110x75/55cf8a9355034654898bef13/property-452-reviewer-vena-verga-property-midterms-reviewer.jpg)