Embed Size (px)

Citation preview

Governance issues in the central bank investment function: the case of Banca d’Italia

Sovereign Investment PartnershipsExecutive Forum on Central Bank Reserves

and Official Sector Asset Management

Washington, April 27-29, 2009

Franco Passacantando, Managing DirectorCentral Banking, Markets and Payment System Area

2

USD 27,3%*

GOLD 60,2%

GBP 5,2%

YEN 5,8%

CHF 0,3%

Source: Annual Report

*The figure includes temporary operations in USD, carried out within the USD Term Auction Facility programme, for an amount of USD 6.141 mln.

Official reserves(forex EUR 32,4 bln; gold EUR 48,9 bln)

Investment portfolio(EUR 91,0 bln)

Funds & ETFs 1%Equities 5,2%

Other bonds 0,3%

Govt. Bonds 93,6%

Others 1,2%

Banca d’Italia’s financial portfolios(as of Dec 31st 2008)

3

The main drivers of change

Changing environment

Weakening of the links between reserve management and foreign exchange policy, after the introduction of the euro as a single currency

Growing importance of the return generated by the Bank’s foreign reserves and investment portfolio

Pressure to increase efficiency , effectiveness

Enhance specialization

Avoid duplications and exploit synergies

Enhancing horizontal and vertical governance

Enhance independence of risk management and control

Protect governing bodies from reputational risk

4

The recent reform (Dec. 2008)

NOW BEFORE

Risk Management Department

Middle Office

(RM e asset allocation, Op. Risk)

Financial Investment Department

Front Office Back Office

Central Banking Department

Mon. Pol. ELA

Mon. Policy and Exch.Rate Dept.

Mon. Pol. Reserves(F.O., B.O., M.O.)

Asset Management Dept.

Own Fund(F..O., B.O., M.O.)

ELA

5

Departments involved and respective functions

Central Banking Department: monetary policy operations, foreign exchange interventions, financial stability-related functions (ELA).

Financial Investment Department: investment of the Bank's own funds, foreign currencies, gold reserves and reserves held on behalf of the ECB.

Risk Management Department: assessment and control of financial and operational risk on all assets of the Bank; proposals for strategic and tactical asset allocation.

6

The present structure

7

1. The merger between reserve management and own funds management activities

Why?

Integrated approach towards asset management

Efficiency reasons

Increasing similarities between fx reserve portfolio and investment portfolio

Exploit the synergies arising from the concentration of investment activities within a single team

Avoid duplications and costs related to the ‘twin’ dealing rooms (we merged 3 dealing rooms into a single one!)

Moving towards an integrated risk management approach at enterprise-wide level

8

The merger between reserve management and own funds management activities (ctd.)

The institutional reasons why a central bank holds foreignreserves and own funds are different.

Foreign reserves must be characterised by a particularly low risk return profile and high liquidity.

The merger between operational and decision making structures does not prevent the definition of different profiles for different components of the portfolio.

However, risks of using ‘inside information’ can be mitigated.

Issues

9

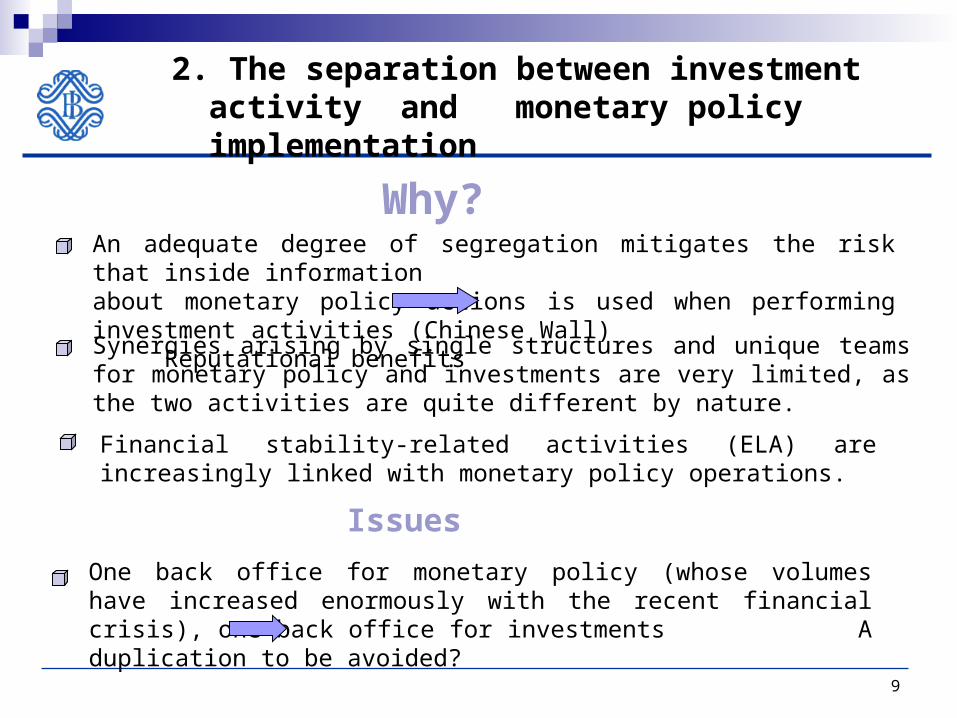

2. The separation between investment activity and monetary policy implementation

An adequate degree of segregation mitigates the risk that inside information about monetary policy actions is used when performing investment activities (Chinese Wall) Reputational benefits

Synergies arising by single structures and unique teams for monetary policy and investments are very limited, as the two activities are quite different by nature.

Why?

Issues

One back office for monetary policy (whose volumes have increased enormously with the recent financial crisis), one back office for investments A duplication to be avoided?

Financial stability-related activities (ELA) are increasingly linked with monetary policy operations.

10

3. The separation of the risk management function from operational activities

Why?

Achieve a higher degree of independence of the risk manager/controller

Stimulate a constructive ‘debate’ between risk managers and portfolio managers

Issues

Excessive distance between risk managers and portfolio managers may exacerbate tensions and develop diverging professionalities

Single reporting line at the level of Managing Director

High-level coordination achieved through Risk and Investment Committees

11

The decision making process for the investment offoreign reserves and own funds – The Committees

Strategic and Financial Risk Committee

Members

Main Activities

One Board Member (Chairman)Managing Directors for: Central Banking, Markets and Payment Systems, Economic Research, Accounting and Control AreasHeads of: Risk Dept., Investment Dept., Central Banking Dept.

Supports the Governor’s decisions on investments. Assesses the Bank’s strategic asset allocation and risk budgeting. Evaluates investment results. Strenghtens the consistency between the Bank’s financial decisions and its balance-sheet developments.

Frequency Semi-annual

12

The Committees (ctd.)

Investment Committee

Members Managing Director for Central Banking, Markets and Payment Systems Area (Chairman) Heads of: Risk Dept., Investment Dept., Central Banking Dept. Two members of the Research Department.

Main activities Assesses the tactical allocation of investments in foreign reserves and

own funds. Evaluates results for each investment portfolio.

Frequency Bi-monthly

13

The decision making process - Interactions

GOVERNORStrategic and Financial Risks Committee (SFRC)

Investment Committee

INVESTMENT PORTFOLIOS

Strategic asset alloc.Risk budget/limits

Tactical bmks (within the limits set by

SFRC)

PROPOSAL

APPROVAL

Risk Management Dep. Strategic Benchmark

ProposalsRisk Management

Dep.

Tactical Benchmark Proposals

Active management by Investment Dep.