Embed Size (px)

Citation preview

GOODS & SERVICES TAX

SUMMARY NOTES

FOR CS EXECUTIVE &

CS PROFESSIONAL

Address:- 2/14, 3rd Floor, Patel Nagar (In front of Patel Nagar Metro Station)

Ph. 011-45139922, 45719209, 9899259817

Page | 1

GOODS & SERVICES TAX CONCEPT – 1 What is Tax

- It is an amount paid by people of India to government, which is used to provide public services.

For example, Defence, health services, provision of education, infrastructure facility like Roads/Dams etc.

- Taxes are basic source of Revenue for government.

CONCEPT – 2 There are generally two type of taxes in India DIFFERENCE BETWEEN DIRECT TAX & INDIRECT TAX

Aspect Direct Tax Indirect Tax

1. Nature Direct Taxes are the taxes directly incurred and paid by the same person.

Indirect Taxes are paid by one person (Assessee / Dealer), but the same is recovered from another person (Consumer).

2. Levied on Levied on the income of the Assessees.

Levied on Purchase / Sale / Manufacturer of goods and Provision of Services.

3. Shifting of Burden

There is no shifting of tax burden. Hence, it is directly borne by the taxpayer.

Tax burden is shifted to the subsequent user.

4. Time of Collection

Direct Taxes are collected after the income for a year is earned.

It is collected at the time of sale or purchase or rendering of services.

5. Examples Income Tax. Goods and Services Tax, Customs Duty

CONCEPT – 3

History of GST

- 19th December, 2014 The constitution 122nd Amendment bill, 2014 seeking to amend constitution to introduce the goods & services tax was introduced in lok sabha but congress object.

- Feb 2015: Sh. Arun Jaitly SET April 1st 2016 as dead line for GST Roll out.

Page | 2

- 6th May 2015:

Lok Sabha passes GST Constitutional amendment bill

- 12th May 2015: The Amendment bill presented in Rajya Sabha.

- 14th May 2015 GST Bill forwarded to joint committee of Rajya Sabha & Lok Sabha.

- 3rd Aug, 2016 Rajya sabha passes constitution amendment bill by 2/3rd majority

- 8th Aug, 2016 Changes made by Rajya Sabha were unanimously passed by Lok Sabha on 8th Aug, 2016.

- On 2nd September 2016 – bill was adopted by majority of state legislature where in approval of at

least 50% of sate Assemblies was required.

- On 8th September 2016 – the president of India sh. Pranab mukherjee gave assent to constitution amendment bill & it had become constitutional (101st ament) Act, 2016

- On September 12th, the union cabinet cleared formation of GST council.

- On September 22 and 23 – the council met for 1st time

- 16th January 2017- Finance Minister announced 1st july 2017 as GST roll out dead line.

- 20 march 2017 – cabinet approved CGST, IGST, UTGST, and compensation bill.

- 27th march 2017 – Finance Minister tabled CGST/IGST/UTGST compensation bill in parliament &

all 4 key bills were passes

- April 2017 – president assented all 4 key bills.

- 1 July 2017 – GST Applicable to whole of India except J&K.

- 8th July – GST law was made applicable state of J&K. CONCEPT – 4

GOODS & SERVICES TAX Article 366 (12A) – GST means any tax on supply of goods or services except tax on supply of Alcoholic Liquor for Human Consumption

Page | 3

CONCEPT – 5 Features of GST as given as below.

(i) It is a dual structure (ii) It is based on destination based concept (iii) It is levied on Goods & Services (iv) It based on value added by giving seamless credits to Recipient.

CONCEPT 6 CONSTITUTIONAL BACKGROUND 246A(1) 246A(2)

Parliament & Legislature of state have powers to make laws in respect to GST

Parliament has exclusive power to make laws IRT GST when Trade/Commerce inter-state

CONCEPT 7 Reason of GST (problems in existing law)

(i) Cenvat of central taxes against state levy (ii) Cascading effects VAT payable inclusive of excise paid at manufacturing stage (iii) Origin based tax (iv) No cross set off VAT dealers unable to set off any service tax

CONCEPT 8 Intentional scenario

France first country to levy GST 1954 Nearly 160 countries adopted GST in world Along with India Canada & Brazil also adopted Dual based GST

CONCEPT 9 Taxes sub-summed in GST

Central taxes State taxes

(i)Excise (ii) service tax (i) State VAT

(iii) Excise ( M & TP) (i) CST

(iv) Add GSI (iii) purchase tax

(v) Add T & TA (iv) Luxury Tax

(vi) CVD (v) Entry Tax

(vii) SAD (vi) Entertainment tax (except levied by local bodies)

(viii) Cess/ surcharge (vii) Tax on advertisement

(viii) Tax on lottery betting/ gambling

(ix) State Cess/ surcharge

Page | 4

CONCEPT 9

Goods out of GST

Alcoholic liquor

5 petro product at any time at later Date on recommendation of council petro crude/motor spirit (petrol)/ HSD aviation turbine fuel/ natural gas

CONCEPT 10

GST council Article 279 A

CONSTITUTION

(i) Chair person union finance minister (ii) Union minister of state in charge of revenue or Finance (Member) (iii) Minister in charge of finance nominated by SG. (iv) Vice – chair man to be selected out of members themselve (v) Quorum of meeting 50% of total number of members (vi) Vote of CG 1/3 of total votes cast

vote of SG 2/3 of total votes cast (vii) For taking any decision minimum 75% of weighted votes

votes in favour of decision (viii) Matter on which council can make recommendation to Centre & State

(i) (ii) (iii) (iv) (v)

Goods to be exempted

thresh-hold limit of turnover GST not leviable

Rates

Special provision IRT north Eastern states

any other matter

CONCEPT 11 DEFINITIONS

(i) Goods 2(52) meansEvery kind of movable property except money & securities include actionable claim/ growing crops/grass, things attached/ forming part of land Which are agreed to be severed before supply or under a Contract of supply

(ii) Types of Goods

2 (19) 2 (59)

capital goods Input

Capitalized in books Other than capital goods

Used/intended to used in course or in furtherance of business

Page | 5

(iii) Service section 2(102)

Means Anything other than Goods/Money/securities but include activities relating to use of money or its conversion by cash or any other mode from one form, currency, denomination to another form.

(iv) Taxable supply section 2 (108): Means supply of goods or services or both

which is leviable to tax under this Act.

(v) Outward supply IRT taxable person means supply by way of sale/trans/barter/ exchange/license rent/lease/disposal or any other mode by such person in course/furtherance of business

(vi) SECTION 2 (47): EXEMPT SUPPLY

“Exempt supply” means supply of any goods or services or both which attracts nil rate of tax or which may be wholly exempt from tax under section 11, or under section 6 of the Integrated Goods and Services Tax Act, and includes non-taxable supply;

CONCEPT 12

SCOPE OF SUPPLY (SECTION 7)

Supply includes (Section 7 (1)) 7 (i)(a) 7 (i)(b) 7 (i)(c) 7 (i)(d)

All form of supply such as sale, transfer barter, exchange disposal lease/license/rent

Made or agreed to be made for a consideration by a person in course or furtherance of business

Import of service in course or not in course of business for consideration

Activities in Schedule I without consideration

Schedule I

Activities to be treated as supply of goods/service as referred to in schedule II

(i) permanent disposal of asset on which ITC has been taken

(ii) branch transfer or related person

(iii) principal/agent

(iv) import from related/any of his establishment located outside India

Section 7 (2) Neither supply of Goods/nor supply of services

Activities/trans in Schedule III Undertaken by CG/SG/LA in which they are engaged as public authority as may be notified by Govt. on recommendation of council.

Page | 6

Section 7 (3) Govt. may on recommendations of council, Specify by notifications transactions to be treated as supply of Goods not services & supply of service not as Goods

Schedule III (i) (ii) (iii) (iv) (v) (vi)

Service by employee to Employer in course of Employment

Service by court/tribunal Established under any law for time being in force

(a) functions performed by MP/MLA/MO Panchayat member of municipal or other LA

Services of funeral, burial crematorium or mortuary including transportation of deceased

Sale of land building

Actionable claim except lottery betting gambling

(b) duties performed by any person who hold post under constitution

(c) Duties by chair person/member director in body established by CG/SG/LA

CONCEPT 13

COMPOSITE /MIXED SUPPLY Section 2 (30) Composite supply Section 2 (74) mixed supply

Supply made by taxable person to recipient consisting of 2 or more taxable supplies of goods/Services or both or combination thereof which are naturally bundled

Means Two or more individual supplies/or any combination by a taxable person for a single price where such supply do not constitute a composite supply

one of which is principal Taxability : Section 8 (a) Taxability : Section 8 (b)

Shall be treated as a supply of such principal supply Shall be treated as a supply of that particular supply which attract highest rate of tax

CONCEPT 14

Import of service

With consideration [Section 7 (1) (b)] Without consideration [Section 7 (1) (c) Schedule I]

In course or furtherance of business

Not in course or furtherance of Business

in course of furtherance of business + from related person any of his establishment located outside India

Supply Supply Supply

Section 7 (4) IGST Act import of service shall always be treated as inter-state Supply hence subject to IGST

Page | 7

CONCEPT 15

OIDAR Services Section 14 IGST Act

SUPPLIER RECIPIENT

any person located in Non- taxable territory

Non-Taxable online recipient

Taxable Online recipient

Liability to pay Supplier recipient under

FCM RCM

For place of supply of OIDAR Supplies Section 13 (12), GST Act. Location of Recipient of services

CONCEPT 16 Import of Goods Subject to GST via Section 3 of custom tariff Act & on value as determine under section 14 of Custom Act. As per section 7 (2) of IGST shall be treated as inter-State unless it crosses

custom frontier.

CONCEPT 17

SUPPLY FROM PRINCIPAL TO AGENT. & VICE VERSA

Even if without

Consideration 7 (1) (c)+ Schedule I for value refer to

rule 29 Covers in scope of supply

Rule 29

Optional OMV or 90% of price charged for supply of Goods of like kind & Quality by recipient

to his customer where Goods intended for further supply, by said recipient

Otherwise Apply Rule 30 or Rule 31 in that order

CONCEPT 18 Supply of Goods or Service or both between distinct or Related person

Distinct person Related person

25 (4)

25 (5)

Explanation to Section 15

A person who has obtained or is required to obtain more than one registration, whether in one State or Union territory or more than one State or Union territory shall, in respect of each such registration, be treated as distinct persons for the purposes of this Act

Where a person who has obtained or is required to obtain registration in a State or Union territory in respect of an establishment, has an establishment in another State or Union territory, then such establishments shall be treated as establishments of distinct persons for the purposes of this Act

(i) Such persons are officers or directors of

one another’s businesses

Page | 8

(ii) Such persons are legally recognised partners in business;

(iii) Such persons are employer and employee;

(iv) Any person directly or indirectly owns, controls or holds twenty-five per cent. Or more of the outstanding voting stock or shares of both of them

(v) One of them directly or indirectly controls the other;

(vi) Both of them are directly or indirectly controlled by a third person

(vii) Together they directly or indirectly control a third person; or

(viii)they are members of the same family;

Section 10 Composition Levy

Section 10(1) Section 10(2)

Section 10(3)

Section 10(4)

Section 10(5)

Notwith standing anything contained in this act but subject to the Provision of Sub. Section (3) and (4) of section 9, A registered Person whose aggregate Turnover in preceding financial year

Did not exceed Rs. 1 Crore May opt. scheme and pay tax at rate given under Rule 7. On turnover in a state

Person shall not be eligible to opt. scheme

Lapse of option

No credit of Input Tax

Demand and recovery

↓

option availed by Registered person U/s 10(1) shall lapse with effect from the day on which his aggregate turnover during a financial year exceed Rs 1 Crore

Composition person shall not collect any tax from Receipient in supplies made by him nor shall be entitle to any credit of input tax

If the proper officer has reasons to believe that a taxable person has paid tax under sub-section (1) despite not being eligible, such person shall, in addition to any tax that may be payable by him under any other provisions of this Act, be liable to a penalty and the provisions of section 73 or section 74 shall,

Note: Reduce limit of Rs 75 Lakh have been kept for special category states. (Except J&K & Utrakhand)

Page | 9

Section 10(2) Composition Levy

(a) (b) (c) (d) (e) (f) (g)

Engaged in supply of service other than - Restaurant - Mandap keeper Outdoor catering

Engaged in making any supply of goods which is not leviable to tax - Alcoholic liquor - Petroleum crude - high speed diesel - motor spirit - Natural gas - aviation turbine fuel

Engaged in making any Interstate outward supply of goods

Engaged in making any supply of goods through an ECO who is required to collect tax at source u/s 52

Manufacturer of - Tobacco - Ice-Cream - Pan Masala - Manufactured tobacco substitute

Casual taxable person or Non- Resident taxable person

Supplier who has purchased any goods or service from unregistered supplier unless he has paid GST on such goods or service on RCM Basis

Provided: - More than one registered person having SAME PAN, the registered person shall not be eligible to opt. for the scheme unless all registered person opt to pay tax under that sub-section

AGGREGATE TURNOVER

Taxable Supplies (excluding the value of inward supplies on which tax is payable by a person on reverse charge basis)

Exempt Supplies Exports of goods or service or both

inter-State supplies of persons having the same Permanent Account Number

Page | 10

RULE 3 COMPOSITION LEVY

Rule 3 (1) of CGST Rules 2017

Migrated Taxpayer

Migrated to GST law through provisional Registration Separate intimation

Form GST CMP-01 Time Limit

Prior to appointed day, but not later than 30 days after the appointed day, or such further period as may be extended by Commissioner

Rule3(2) Of CGST Rules 2017

Fresh GST Registration

Intimate through registration application itself, which shall be considered as an intimation to pay tax under the said section

Part B of Form GST REG-01

Rule 3 (3) of CGST Rules 2017

Fresh GST Registration taken (normal scheme) & subsequently, switching over to composition

Separate intimation required (before Start of FY for which option to pay Tax is exercised)

Form GST CMP-02 Regular supplier now becoming Composition supplier : Reversals of ITC availed on stock He shall also furnish statement he shall also furnish the statement in Form GST ITC-03 (as required by Rule 44 (4)) within 60 days from the commencement of relevant FY,

RULE 4 EFFECTION DATE OF COMPOSITION LEVY Rule 4 (1) of CGST Rules, 2017

Option shall be effective from appointed day.

Rule 4 (2) of CGST Rules, 2017

Intimation shall be considered only after grant of registration. Option shall be effective fromdate of registration

Rule 4 (1) of CGST Rules, 2017

Beginning of the FY

Rule 3(5) Any intimation under sub-rule (1) or sub-rule (3) in respect of any place of business in any State or Union territory shall be deemed to be an intimation in respect of all other places of business registered on the same Permanent Account Number.

RULE 5 (1) CONDITIONS AND RESTRICTIONS FOR COMPOSITION LEVY.- The person exercising the option to pay tax under section 10 shall comply with the following conditions, namely:-

Page | 11

a) he is neither a casual taxable person nor a non-resident taxable person;

b) the goods held in stock by him on the appointed day have not been purchased in the course of inter- State trade or commerce or imported from a place outside India or received from his branch situated outside the State or from his agent or principal outside the State, where the option is exercised under sub-rule (1) of rule 3;

c) the goods held in stock by him have not been purchased from an unregistered supplier and where

purchased, he pays the tax under sub-section (4) of section 9;

d) he shall pay tax under sub-section (3) or sub-section (4) of section 9 on inward supply of goods or services or both;

e) he was not engaged in the manufacture of goods as notified under clause (e) of sub-section (2) of

section 10, during the preceding financial year;

f) he shall mention the words “composition taxable person, not eligible to collect tax on supplies” at the top of the bill of supply issued by him; and

g) he shall mention the words “composition taxable person” on every notice or signboard displayed at a

prominent place at his principal place of business and at every additional place or places of business.

RULE 6 RULE 6 (1) OF CGST RULE 2017 Once opted for, its valid for life time so long as he satisfies all the conditions mentioned in the said section and under these rules.

WITHDRAWAL OF OPTION

AUTO WITHDRAWAL (may take place at any time in the CY)

When supplier ceases to satisfy any of condition mentioned in section-10

Intimation of withdrawal shall be given of occurrence of event Form GST CMP-04

DISCRETIONARY WITHDRAWAL OF SUPPLIER (may take place at any time in the CY)

Intimation of withdrawal shall be given by supplier (before withdrawal) Form GST CMP-04

DENIAL BY PROPER OFFICER( AC/DC) (as he has reason to believe That supplier was ineligible or has contravened condition)

SCN proposing denial – FORM GST CMP-05 Reply of SCN by supplier (within 15 days-) FORM GST CMP-06 Order (within 30 days)- FORM GST CMP-07

COMPOSITION SUPPLIER NOW BECOMING REGULAR SUPPLIER : ENTITLED TO TAKE ITC ON STOCK Such person shall also furnish a statement in FORM GST ITC-01 containing details of stock in hand on the date on which composition option is withdrawn or denied.

FORM GST ITC-01

It shall be filed (within 30 days (or extended period) from the date from which the option is withdrawn or from the date of the order passed in FORM GST CMP-07,as the case may be.

CHAPTER - 2 CHARGING SECTION

1. Extent & Commencement of CGST Act/ SGST Act/ UTGST Act/ IGST Act

Applicability CGST SGST UTGST IGST

Intra-State supply Inter-State

supply

States of India

Union Territories with

State Legislature

Union Territories

without State

Legislature

2. Levy and collection of CGST/IGST

Particulars CGST IGST

Levied on Intra-State supplies of

goods/services/both

Inter-State supplies of

goods/services/both

Collected and

paid by

Taxable person

Supply

outside

purview of tax

Alcoholic liquor for human consumption

Value for levy Transaction value under section 15 of the CGST Act

Rates Rates as notified by IGST rate= CGST rate + SGST

Page 12

Government.

Maximum rate of CGST

will be 20%.

rate (more or less)

Maximum rate of IGST will

be 40%.

Supplies on

which tax to

be levied

w.e.f. a

notified date

Section 9(2)

petroleum crude

high speed diesel

motor spirit (commonly known as petrol)

natural gas and

aviation turbine fuel

Tax payable

under reverse

charge

Section

9(3)/9(4)

Supply of goods or services or both, notified by the

Government on the recommendations of the GST

Council.

Supply of taxable goods or services or both by an

unregistered supplier to a registered person

Tax payable

by the

electronic

commerce

operator

The Government may notify specific categories of services

the tax on supplies of which shall be paid by electronic

commerce operator (ECO) as if such services are supplied

through it.

Section 9(5) If the ECO is located in

taxable territory

Person liable to pay tax is the

ECO

If the ECO does not have

physical presence in the

taxable territory

Person liable to pay tax is the

person representing the ECO

If the ECO has neither the

physical presence nor any

representative in the

taxable territory

Person liable to pay tax is the

person appointed by the ECO

for the purpose of paying the

tax

Goods

imported into

India

No CGST and

SGST/UTGST payable.

IGST shall be levied and

collected on import of goods

as per the section 3 of the

Page 13

Custom Tariff Act, 1975.

NotificationNo.–17/2017

- Service by Transportation of passengers by a Radio-Taxi, Motor-Cab,

Maxi- Cab, Motorcycle.

- Service by providing accommodation in Hotel except person supplying

though Eco liable to be registered U/s 22.

- Service by house-keeping, except person supplying though Eco liable to

be registered U/s 22.

Page 14

CHAPTER - 3 PLACE OF SUPPLY (POS)

A. Place of supply of goods other than import and export [Section 10]

S.

No.

Nature of Supply Place of Supply

1. Where the supply involves the

movement of goods, whether by the

supplier or the recipient or by any

other person

Location of the goods at the time

at which, the movement of goods

terminates for delivery to the

recipient

2. Where the goods are delivered to

the recipient, or any person on the

direction of the third person by way

of transfer of title or otherwise, it

shall be deemed that the third

person has received the goods

The principal place of business of

such third person

3. Where there is no movement of

goods either by supplier or recipient

Location of such goods at the

time of delivery to the recipient

4. Where goods are assembled or

installed at site

The place where the goods are

assembled or installed

5. Where the goods are supplied on-

board a conveyance like a vessel,

aircraft, train or motor vehicle

The place where such goods are

taken on-board the conveyance

6. Where the place of supply of goods

cannot be determined in terms of

the above provisions

It shall be determined in such

manner as may be prescribed

Page 15

B. Place of supply of goods imported into, or exported from India

[Section 11]

S. No. Nature of Supply of Goods Place of Supply

1. Import Location of importer

2. Export Location outside India

Page 16

C. Place of supply of services where location of supplier and recipient is in India [Section 12]

(i) In respect of the following 12 categories of services, the place of supply is

determined with reference to a proxy; rest of the services are governed by the default provision.

1 Immovable property related-services

including accommodation in

hotel/boat/vessel

Location at which the immovable

property or boat or vessel is located or

intended to be located

If located outside India: Location

of the recipient

2 Restaurant and catering services,

personal grooming, fitness, beauty

treatment and health service

Location where the

services are actually performed

3 Training and performance Appraisal

B2B: Location of such registered Person

B2C: Location where the services are actually performed

4 Admission to an event or amusement park

Place where the event is actually held or where the park or the other place is located

5 Organisation of an event B2B: Location of such registered person

B2C: Location where the event is actually held

• If the event is held outside India: Location of the recipient

6 Transportation of goods, including mails

B2B: Location of such registered Person

B2C: Location at which such goods are handed over for their Transportation

Page 17

7 Passenger transportation B2B: Location of such registered Person

B2C: Place where the passenger embarks on the conveyance for a continuous journey

8 Services on board a Conveyance

Location of the first scheduled point of departure of that conveyance for the journey

9 Banking and other financial services

Location of the recipient of services on the records of the supplier

Location of the supplier of services if the location of the recipient of services is not available

10 Insurance services B2B: Location of such registered Person

B2C: Location of the recipient of services on the records of the supplier

11 Advertisement services to the Government

Each of States/Union Territory where the advertisement is broadcasted/displayed/run

Proportionate value in case of multiple States

Telecommunication services Services involving fixed line, circuits, dish etc: Location of such fixed equipment

Mobile/ Internet post-paid services: Location of billing address of the recipient

Sale of pre-paid voucher: Place of sale of such vouchers

Other cases: Address of the recipient in records

(ii) For the rest of the services other than those specified above, the default provision has been prescribed as under:

Page 18

Default rule for the services other than the 12 specified services S. No. Description of Supply Place of Supply

1 B2B Location of such registered person 2 B2C Where the address on record

exists: Location of the recipient Other cases: Location of the supplier of services

D. Place of supply of services where location of supplier OR location of recipient is outside India [Section 13]

(i) In respect of the following categories of services, the place of supply is

determined with reference to a proxy; rest of the services are governed by the default provision.

S. No.

Nature of Service Place of Supply

1. Services supplied in respect of goods which are required to be made physically available

Location where the services are actually performed

Services supplied in respect of goods but from a remote location by way of electronic means

Location where the goods are situated at the time of supply of services

Above provisions are not applicable in case of goods that are temporarily imported into India for repairs and exported after repairs

2. Services which require the physical presence of the recipient or the person acting on his behalf with the supplier of services

Location where the services are actually performed

3. Service supplied directly in relation to an immovable property

Place where the immovable property is located or intended to be located

4. Admission to or organisation of an event Place where the event is actually held If the above services are supplied at more than one locations. i.e., (i) Goods & individual related (ii) Immovable property-related (iii) Event related

At more than one location, including a location in the taxable territory

Location in the taxable territory

Page 19

In more than one State Each such State in proportion to the value of services provided in each State

5. Services supplied by a banking company, or a financial institution, or a NBFC to account holders

Location of the supplier of services

Intermediary services

Services consisting of hiring of means of transport, including yachts but excluding aircrafts and vessels, up to a period of one month

6. Transportation of goods, other than by way of mail or courier

Place of destination of such goods

7. Passenger transportation Place where the passenger embarks on the conveyance for a continuous journey

8. Services provided on-board a conveyance

First scheduled point of departure of that conveyance for the journey

9. Online information and database access or retrieval services

Location of recipient of service

(ii) For the rest of the services other than those specified above, a default provision has been prescribed as under:

Default rule for the cross-border supply of services other than nine specified services S. No. Description of Supply Place of Supply 1. Any Location of the recipient of

service Location of the supplier of service, if location of recipient is not available in the ordinary course of business

Page 20

Place of Supply of Goods

Other than Goods Imported into or

Exported from India

Goods Imported into or Exported from India

Goods Imported into India

Goods Exported from India

Place of supply of Goods shall

be the location of the Importer Place of supply of Goods shall be the location outside India

Supply Involves

Movement of Goods

Location of Goods where

movement terminates for

delivery

Goods are supplied by transfer of

document during Movement of Goods

Principal Place of Business of Third person on whose direction Goods

where supplied to Another person

Supply does not Involve

Movement Of Goods

Location of Goods at

the time of delivery

Goods are Assembled or Installed

at Site

Place of such installation or delivery

Goods are supplied

on Board a Conveyance

Location at which such Goods are taken on Board

Place of supply of Goods cannot be

Determined

Place of supply shall be determined in such manner

as may be prescribed

Page 21

Where the passenger

embarks on the conveyance for continuous

journey

Where the event is

actually held

Place of Supply of Services

Location of supplier of service and

recipient of service is in India

General rule

Specific situations

Supply to a registered person - Location of such person. Supply to non-registered person - Location of recipient, if address exists in records. In other cases, location of supplier

Specific Services such as Health services,

Restaurant services

Services

relating to Training &

Performance Appraisal

Organization of event and

ancillary services relation to such event or assigning of Sponsorship

Admission

to a cultural,

artistic, sporting

etc., events,

amusement

park & ancillary

services thereto

Goods transportation

services

Passenger transportation

services

Services

on Board a Conveyance

such as Aircraft,

Vessel etc.

Services directly

related to Immovable Property

Telecommunication services including

data transfer, Broadcasting, cable

and DTH

Place of Actual

Performance

Services to Registered

person

Services to Unregistered

person

Place where the event is actually held or

where the park or such other place is located

Services to

Registered person

Location of such person

Services to unregistered

person

Location

of the first scheduled point of

departure of that

conveyance

Location of such person

Services to registered

person

Place of

actual performance

Services to Unregistered

person

Services to Registered

person

Location of

recipient

Services to Unregistered

person

Place where goods are handed over for their transportation

Immovable property located in India

Immovable property located outside India

Location of such person

Event is held in India

Event is held outside

India

Location of the recipient

Fixed line / Leased circuit, Internet based

circuit

Place of Installation of such circuit

Mobile connection & Internet

services (post paid services)

Billing address of the recipient

Mobile connection & Internet

services (pre paid services)

In any other case

If provided through selling agent then place of supply is address of

such selling agent

If provided by any person to final subscriber then

location where such payment is received

Address of the recipient as per records of the

supplier

Page 22

Place of Supply of Services

Location of supplier of service and recipient of services outside India

Services provided in relation to

Goods

Specific Services

Admission

to a cultural, artistic, sporting,

educational or entertainment or

similar events

Transportation

of Goods other than by way of Mail or Courier

services

Passenger Transportation

Services

Services

on Board a Conveyance

such as Aircraft,

Vessel etc.

Services in relation to Immovable

Property , hotel accommodation, inn guest house

or grant to u se immovable

property

Online information services and

database access or retrieval services

Goods required to

be made available for providing services to

the supplier of services

Services provided

from remote location

Place

where the event is actually

held

Place of

Destination

Where the passenger embarks on the

conveyance for continuous

journey

Location of the first scheduled point of

departure of that

conveyance

Location of Immovable property

Location of Recipient of

services

Location where the

services are performed

Location where the Goods are situated

Banking services or services by

non- banking financial

companies

Intermediary Services

Services consisting of hiring of means of transport

Location of Supplier of Services

Page 23

Special order

CHAPTER-4 EXEMPTION

1. Power to exempt from tax [Section 11 of the CGST Act/ section 6 of IGST

Act]

Power to exempt from tax

by way of issuance of

Notification

• exempt generally

• either absolutely or subject to such

conditions as may be specified,

• goods and/or services of any specified

description.

exempt from payment of tax under

circumstances of an exceptional

nature to be stated in such order, in

public interest.

Special Points:-

(1) The Government may, if it considers necessary or expedient so to do for the

purpose of clarifying the scope or applicability of any notification issued under sub-

section (1) or order issued under sub-section (2), insert an explanation in such

notification or order, as the case may be, by notification at any time within one year of

issue of the notification under sub-section (1) or order under sub-section (2), and every

such explanation shall have effect as if it had always been the part of the first such

notification or order, as the case may be.

Explanation.––For the purposes of this section, where an exemption in respect of any

goods or services or both from the whole or part of the tax leviable thereon has been

granted absolutely, the registered person supplying such goods or services or both

shall not collect the tax, in excess of the effective rate, on such supply of goods or

services or both.

Page 24

CHAPTER-5 TIME OF SUPPLY

TIME OF SUPPLY WHERE TAX IS PAYABLE UNDER FORWARD CHARGE

Time of supply of goods [Section

12(2)]

Time of supply of services [Section

13(2)]

Earliest of the following:

(a) Date of issue of invoice by the

supplier or

(b) the last date on which he is

required, to issue the invoice

under section 31(1) with respect to

the supply or

(c) Date on which the supplier

receives the payment (entering

the payment in books of account or

crediting of payment in bank

account, whichever is earlier) with

respect to the supply

(a) Invoice issued within the time

period prescribed under section

31(2)

Earliest of the following:

Date of issue of invoice by the

supplier

Date of receipt of payment

(entering the payment in books

of account or crediting of

payment in bank account,

whichever is earlier)

(b) Invoice not issued within the time

period prescribed under section

31(2)

Earliest of the following:

Date of provision of service

Date of receipt of payment

(entering the payment in books

of account or crediting of

payment in bank account,

whichever is earlier)

(c) When the above events are

unascertainable

Date on which the recipient

shows the receipt of services in

his books of account

Page 25

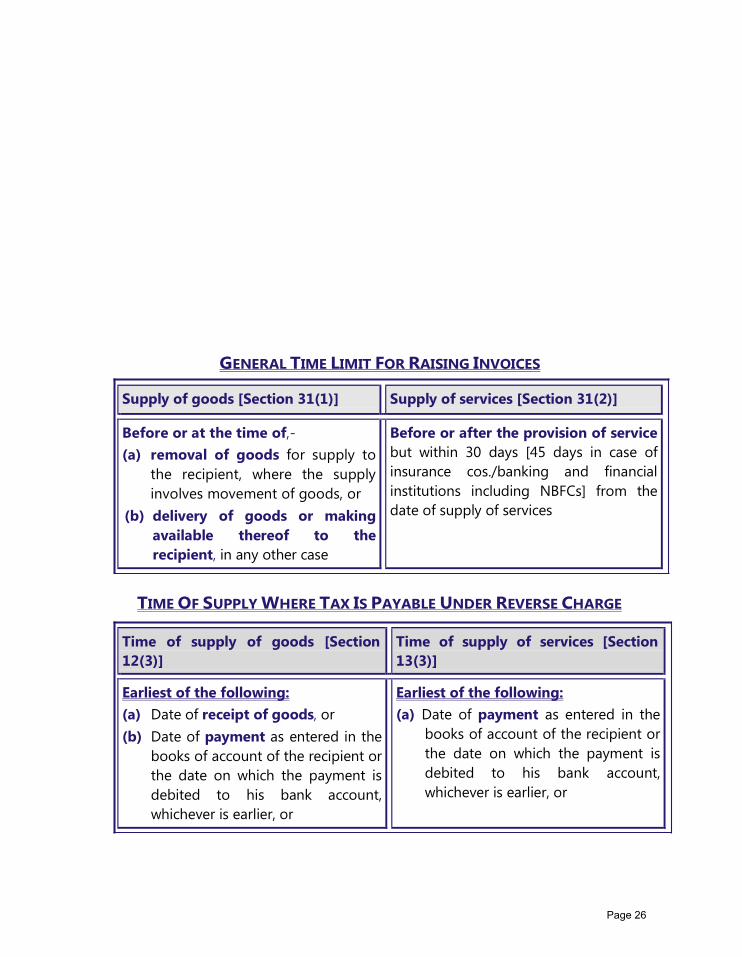

GENERAL TIME LIMIT FOR RAISING INVOICES

Supply of goods [Section 31(1)] Supply of services [Section 31(2)]

Before or at the time of,-

(a) removal of goods for supply to

the recipient, where the supply

involves movement of goods, or

(b) delivery of goods or making

available thereof to the

recipient, in any other case

Before or after the provision of service

but within 30 days [45 days in case of

insurance cos./banking and financial

institutions including NBFCs] from the

date of supply of services

TIME OF SUPPLY WHERE TAX IS PAYABLE UNDER REVERSE CHARGE

Time of supply of goods [Section

12(3)]

Time of supply of services [Section

13(3)]

Earliest of the following:

(a) Date of receipt of goods, or

(b) Date of payment as entered in the

books of account of the recipient or

the date on which the payment is

debited to his bank account,

whichever is earlier, or

Earliest of the following:

(a) Date of payment as entered in the

books of account of the recipient or

the date on which the payment is

debited to his bank account,

whichever is earlier, or

Page 26

(c) 31st day from the date of issue of

invoice

(b) 61st day from the date of issue of

invoice

Where the above events are not ascertainable, the time of supply shall be the

date of entry in the books of account of the recipient of supply

- Import of service from associated

enterprise Date of entry in the books of

account of the recipient or the date of

payment, whichever is earlier

TIME OF SUPPLY OF VOUCHERS EXCHANGEABLE FOR GOODS AND SERVICES

Supply of vouchers exchangeable for goods and services [Sections 12(4) and 13(4)]

(a) Supply of goods or services is identifiable at the time of issue of voucher

Date of issue of the voucher

(b) Other cases

Date of redemption of the voucher

TIME OF SUPPLY OF GOODS AND SERVICES IN RESIDUAL CASES

Supply of goods and services in residual cases [Sections 12(5) and 13(5)]

(a) Where a periodical return is required to be filed

Due date of filing such return

(b) Other cases

Date of payment of tax

Page 27

TIME OF SUPPLY FOR ADDITION IN VALUE BY WAY OF INTEREST/ LATE

FEE/PENALTY FOR DELAYED PAYMENT OF CONSIDERATION

Addition in value by way of interest, late fee/penalty for delayed payment of

consideration

Time of Supply Date on which the supplier receives such addition in value

CHANGE IN RATE OF TAX

In case of change in rate of tax, determination of rate of tax depends upon three

events namely,-

Date of supply of goods or services,

Date of invoice; and

Date of receipt of payment

If any two of the above events occur before the change of rate, the time of supply

is before the change of rate. If any two of them occur after the change of rate,

the time of supply is after the change of rate and the new rate becomes

applicable to the supply. Using this principle, time of supply, in case of change

in rate of tax, can be determined as under:

Supply Issue of

invoice

Receipt of

payment

Time of supply

BEFORE BEFORE AFTER Date of issue of invoice

BEFORE AFTER BEFORE Date of receipt of payment

BEFORE AFTER AFTER Date of issue of invoice or

date of receipt of

payment, whichever is

earlier

Page 28

AFTER AFTER

BEFORE

Date of issue of invoice

AFTER

BEFORE

AFTER

Date of receipt of payment

AFTER

BEFORE

BEFORE

Date of issue of invoice or

date of receipt of

payment, whichever is

earlier

Page 29

Supply made to

unrelated person

where price is the

sole consideration

Assessable Value

= Transaction value u/s 15

+

CHAPTER-6 VALUATION

VALUE OF SUPPLY

Supply made to

related person

Supply where price

is not the sole

consideration

Supply is a

notified supply u/s

15(4)

Value to be determined under Chapter IV:

Determination of Value of Supply of CGST Rules

⇒ Taxes other than GST

⇒ Third party payments made by customer in relation to supply, which supplier was

liable to pay and were not included in the price

⇒ Incidental expenses till delivery of goods/ for supply of services, if charged to

recipient

⇒ Subsidies linked to price of supply other than the ones given by Central/State

Governments

⇒ Interest/late fee/penalty for delay in payment of consideration

⇒ Post supply discount/incentive, if not known in advance & invoice-wise

Page 30

VALUATION RULES

RULE 27: Consideration

not wholly in money

Value shall be either of the

following in the given

order:

• open market value

• total of consideration in

money + amount equal

to the consideration not

in money

• value of supplies of like

kind and quality

• consideration in money

+ money value of

consideration as per rule

30 or 31 in that order.

RULE 28: Supply

between distinct/

related persons, other

than agent

Value shall be either of the

following in the given

order:

• open market value

• value of supplies of like

kind and quality

• value as per rule 30 or

31 in that order.

♦Option to supplier to

value goods sold as such

by recipient⇒Value= 90%

of price charged by

recipient to its unrelated

customer

♦Recipient eligible for ITC

⇒ invoice value = open

market value (taxable

value)

RULE 29: Supply

made/received

through an agent

Value shall be either of

the following in the

given order:

• open market value or

90% of price charged

by recipient to his

unrelated customer

for supplies of like

kind and quality;

• value as per rule 30 or

31 in that order.

RULE 31: Residual

method (Best

Judgement Method)

Value shall be determined

using reasonable means

consistent with the

principles and general

provisions of section 15 &

valuation rules. For

services, rule 31 can be

adopted before rule 30.

RULE 34: Rate of

exchange for

determination of value

Goods = Rate notified by

CBEC under Customs Act

on the date of time of

supply of such goods;

Services = Rate as per

GAAP on the date of time

of supply of such services

RULE 30: Value based

on cost

Value shall be 110% of

cost of

production/acquisition/

provision of goods or

services

RULE 33: Supply as a

pure agent

Costs incurred by the

supplier as a pure agent of

recipient shall be excluded

from value

Rule 35: Value inclusive of taxes

Where value of supply is inclusive of CGST, SGST/UTGST or IGST, the tax amount is calculated by making back

calculations. Tax amount = (Value inclusive of GST x GST rate in % of IGST or CGST, SGST/UTGST)/100 + sum

of applicable GST rates in %)

RULE 32: Value of in respect of certain specific supplies

⇒ Purchase/sale of foreign currency: 1st method-Value = [Buying/Selling rate - RBI reference rate at that

time] x total units of currency. If no RBI reference rate, value = 1% of INR received/provided. If the currencies

exchanged are not in INR, value = lesser of the 2 amounts that would have been received by converting any

of currencies into INR at RBI reference rate OR 2nd method

Currency Value

Upto ` 1,00,000 1% or ` 250 whichever is higher

From `1,0001 to ` 10,00,000 ` 1,000 + 0.5%

From ` 10,00,001 ` 5,500 + 0.1% subject to maximum of ` 60,000

⇒ Booking of tickets by air travel agent: Value = 5% of basic fare for domestic bookings and 10% of the

basic fare for international bookings.

⇒ Life insurance business: If amount allocated for investment is intimated - Value = Gross premium less

amount allocated for investment; Single premium annuity policies where amount allocated for investment is

not intimated - Value = 10% of single premium; Other cases – Value = 25% of premium in 1st year and 12.5%

of premium in subsequent years; Policy only towards risk cover – Value = Entire premium

⇒ Buying & selling of second hand goods: Value = Selling price – Buying price (ignore if value is negative);

Purchase value of goods repossessed from unregistered borrower = Purchase price- 5% per quarter or part

thereof from date of purchase till the date of disposal by the person making repossession

⇒ Coupon/voucher: Value = money value of supplies redeemable against such voucher/ coupon

⇒ Notified services between distinct persons without consideration: Value = Nil, if ITC is available

Page 31

Services

INPUT SERVICES

INPUTS

goods other than

capital goods

CHAPTER-7 INPUT TAX CREDIT

Goods

CAPITAL GOODS

means

means means

goods value of which is

capitalized in the books of

account of person claiming ITC

services

used/intended to be

used in the course/

furtherance of business

EXEMPT SUPPLY

means includes

Supply attracting NIL rate of

tax

Supply wholly exempt

from

Non-

taxable

supply

CGST IGST

Page 32

any person supplying goods and/or

services occasionally

INPUT TAX

Means Includes Excludes

Tax payable

under forward

charge

Tax payable

under reverse

charge

IGST

leviable on

import of

goods

Composition

tax

CGST SGST UTGST IGST

NON-RESIDENT TAXABLE PERSON

means

Principal

Agent

as

In any other

capacity

having NO fixed place of

business/residence in India

Page 33

acquisition

INWARD SUPPLY

means

receipt of goods and/or services by

purchase any other means

with/without consideration

ZERO-RATED SUPPLY

Export of goods and/or services

Supply of goods and /or services to SEZ developer/ SEZ unit

Page 34

II. Provisions of section 16 relating to eligibility and

conditions for taking ITC read with relevant rules are

summarized below:

Sec-16(1) Registered

person to take credit of

tax paid on inward supplies

of goods and/or services

used/ intended to be used in

the course or furtherance of

business

Sec-16(2) if the

following four

conditions are fulfilled:

He has furnished

GSTR 3

Tax on such supply

has been paid either

in

He has received

goods and/or

services

He has valid tax

invoice/debit

note/prescribed

tax paying

document

Proviso to Sec 16(2)

Goods received

in lots – ITC

allowed upon

receipt of last lot

Proviso to Sec 16(2)

Cash Utilisation of

ITC

Sec 16(3)

If depreciation

claimed on tax

component, ITC not

allowed

Goods delivered to

third person on the

direction of the

registered person

deemed to be

received by the

registered person

⇒ ITC available to

registered person

[Bill to Ship to

Model]

Sec 16(4)

Time limit for

availing ITC - ITC

pertaining to a

particular FY can

be availed by 20th

October of next FY

or filing of annual

return, whichever

is earlier.

Exception: Re-

availment of ITC

reversed earlier

ITC to be reversed with interest @ 18% if

value + tax of goods and /or services is not

paid within 180 days of the issuance of

invoice.

Such supplies will be specified in GSTR -2 of

the month immediately following 180 days

and ITC added in the output tax liability of

the said month.

On payment, the ITC could be re-availed

without any time limit.

EXCEPTIONS

Rule 37

• Supplies under

reverse charge

• Deemed supplies

without

consideration

Page 35

Goods and/or

services

III. The provisions of section 17 relating to apportionment

of credit and blocked credits read with relevant rules

are summarized as under:

A. Apportionment of credit

Sec 17(1)

Used partly for business

and partly for non-

business purposes

Sec 17(2)

Used partly for making

taxable (including zero

rated supplies) supplies

& partly for exempt

supplies

ITC available

only as

Attributable to

business purposes

Attributable to taxable

supplies including zero

rated supplies

Sec 17(3)

Exempt supplies include supplies charged to tax under reverse charge, transactions in

securities, sale of land and sale of building when entire consideration is received post

completion certificate.

B. Special provisions for banking companies and NBFCs

Sec 17(4)

Option 1: Avail

proportionate

ITC

Option 2: Avail

50% of eligible

ITC

• Remaining 50% ITC

will lapse.

• Restriction of 50%

shall not apply to the

tax paid on supplies

made to another

registration within

the same entity.

• Option once

exercised cannot be

withdrawn during

remaining part of the

year.

Page 36

T

Total IT on I + IS

IT on I+IS used

exclusively for

non-business

purposes

IT on I+IS used

exclusively for

exempt supplies

Blocked credits u/s

17(5)

Credit attributable to I + IS

used exclusively in taxable

supplies including ZRS

Credit attributable to non-

business purpose if common I +

IS used partly for business + non

-business purposes

D2 = 5% x C2

Ineligible credits

C. Apportionment of common credit in case of inputs and input

services

Rule: 42

T1 T2 T3 C1

Remaining ITC

credited to ECrL

= T- (T1 + T2 + T3)

(i) Exempt supplies include reverse

charge supplies, transactions in T4

securities, sale of land and sale of

building when entire consideration is

received after CC.

C2

Common credit (ii) Aggregate value of exempt

supplies and total turnover exclude

the CED, SED & VAT.

= C1 – T4

D1 D2 C3

Credit attributable to exempt supplies-

D1 = x C2

E = Value of ES during tax period

F = Total turnover during tax period

If no turnover during the tax period/values

not available, values for last period may be

used.

Remaining

common credit

= C2 – (D1 + D2)

Eligible ITC

attributable to

business & taxable

supplies including

ZRS

To be added to output

tax liability

Page 37

• C3 will be computed separately for ITC of CGST, SGST/ UTGST and IGST.

• ∑ (D1 + D2) will be computed for the whole financial year, by taking

exempted turnover and aggregate turnover for the whole financial year.

If this amount is more than the amount already added to output tax

liability every month, the differential amount will be added to the output

tax liability in any of the month till September of succeeding year along

with interest @ 18% from 1st April of succeeding year till the date of

payment.

• If this amount is less than the amount added to output tax liability every

month, the additional amount paid has to be claimed back as credit in

GSTR 3 of any month till September of the succeeding year.

IT = Input tax

I = Inputs

IS = Input services

ECrl = Electronic Credit Ledger

CC = Completion Certificate

CED = Central Excise Duty

SED = State Excise Duty

ZRS = Zero rated supply

ES = Exempt supplies

Page 38

Credited to EcrL

Common credit towards exempted supplies

Te = x Tr

E → Aggregate value of exempt supplies during the

tax period; F → Total turnover during the tax period.

If no turnover during the tax period/values not

available, values for last tax period may be used.

D. Apportionment of common credit on capital goods

Rule: 43

Total input tax (IT) on capital goods (CG)

(a) (b) ‘A’

IT on CG used exclusively for non-

business/exempt supplies

IT on CG used exclusively

for taxable supplies

including zero rated

supply (ZRS)

IT on CG not covered under (a) & (b).

Useful life of CG → 5 years from date of

invoice

Not to be credited to

Electronic Credit Ledger

(ECrL) Credited to ECrL

Tc

Tm

Common credit of CG for a tax

period during their useful life

Tm = Tc/60

Common credit on CG ⇒ Tc = ∑ (A)

If CG under (a)/(b) subsequently get covered

under ‘A’, then ‘A’ = (a)/(b) – 5% of IT for a

quarter or part thereof

Tr

Common credit at the beginning of a tax period

for all CG having useful life in that tax period

Tr = Tm of such CG

Te

Added to output tax liability

along with interest

• Te will be computed separately for ITC of CGST, SGST/ UTGST and IGST.

• Exempt supplies include reverse charge supplies, transactions in securities, sale of land and sale

of building when entire consideration is received after completion certificate.

• Aggregate value of exempt supplies and total turnover excludes the central excise duty, State

excise duty & VAT.

Page 39

F & B, Out cat, BT,

HS, C & PS

EXCEPTION

Rent a cab, life

insurance and health

insurance

EXCEPTIONS

Inward supplies

received by NRTP

EXCEPTION

Section 17(5)

BLOCKED CREDITS PART-A

MV & OC

EXCEPTIONS

(A) MV & OC used for

transportation of goods

(B) MV & OC used for

making taxable supplies

of-

(i) such MV & OC

(ii) transportation of

passengers

(iii) imparting training on

driving/ flying/ navigating

such MV & OC

Where a particular

category of such

inward supplies is

used for making an

outward taxable

supply of the same

category - [Sub-

contracting] or as an

element of a taxable

composite or mixed

supply

(A) Services notified by the

Government as being

obligatory for an employer

to provide to its employees

under any law

(B) Where a particular

category of such inward

supplies is used for making

an outward taxable supply

of the same category [Sub-

contracting] or as part of a

taxable composite or mixed

supply

Goods

imported

by him

Credit available on the above exceptions

Tax paid u/s 74 (Tax short / not paid or

erroneously refunded due to fraud etc.,)

129 (Amount paid for release of goods

and conveyances in transit which are

detained) and 130 (Fine paid in lieu of

confiscation)

Goods lost/ stolen/ destroyed/

written off or disposed of by way of

gift or free samples

Inward supplies used

for personal

consumption

Page 40

WCS for construction of

immovable property

EXCEPTIONS

Cre

dit

av

ail

ab

le o

n

such

ex

ce

pti

on

s

Section 17(5) BLOCKED CREDITS PART-B

Inward supplies received by taxable person for

construction of immovable property on his own account

including when such supplies are used in the course or

furtherance of business

EXCEPTIONS

(A) WCS for P & M

(B) Where WCS for immovable

property is input service for further

supply of WCS [Sub-contracting]

(A) Construction of P & M

(B) Construction of

immovable property for

others

Inward supplies charged to

composition levy

Travel benefits to

employees on vacation

[LTC/HT]

Membership of a club/

health & fitness centre

MV&OC-Motor vehicle & other conveyance;

F&B-Food & beverages; Out cat-Outdoor

catering; BT-Beauty treatment

HS-Health services; C&PS-Cosmetic &

plastic surgery; NRTP-Non-resident taxable

person; WCS-Works contract service; LTC-

Leave Travel Concession; HT-Home town

(A) Construction includes re-construction/

renovation/ addition/ alterations/ repairs to

the extent of capitalisation to said immovable

property.

(B) P & M means apparatus, equipment, &

machinery fixed to earth by foundation or

structural supports but excludes land,

building/ other civil structures,

telecommunication towers, and pipelines laid

outside the factory premises.

Page 41

Credit entitled on

• Inputs as such held in stock

• Inputs contained in semi-

finished goods held in stock

• Inputs contained in finished

goods held in stock

IV. The provisions of section 18 read with relevant rules have

been summarized as under:

A. Special circumstances enabling availing of credit

Section 18)

Special circumstances enabling availing of credit

Registered person

switching from

composition levy to

regular scheme of

payment of taxes

Registered person's

exempt supplies

becoming taxable

Person applying for

registration within 30

days of becoming liable

for registration

Person obtaining

voluntary

registration

Credit entitled on

• Inputs as such held in stock

• Inputs contained in semi-finished goods held in

stock

• Inputs contained in finished goods held in stock

• Capital goods [In case of exempt supply

becoming taxable Capital Goods used

exclusively for such exempt supply] reduced

by 5% per quarter or part thereof from the

date of invoice

Note: ITC claimed shall be verified with the

corresponding details furnished by the corresponding

supplier.

On the day

immediately

preceding the date

from which he

becomes liable to pay

tax under regular

On the day immediately

preceding the date

from which such

supply becomes

taxable

On the day

immediately

preceding the

date from which

he becomes

liable to pay tax

On the day

immediately

preceding the

date of

registration

Section 18(2)

ITC, in all the above cases, is to be availed within 1 year from the date of issue of invoice

by the supplier.

Page 42

Amount to be reversed is equivalent to ITC on :

• Inputs held in stock/ inputs contained in semi-finished or finished goods

held in stock

• Capital goods

on the day immediately preceding the date of switch over/ date of

exemption/date of cancellation of registration

Conditions for availing above credit:

(i) Filing of electronic declaration giving details of inputs held in stock/contained in

semi-finished goods and finished goods held in stock and capital goods on the days

immediately preceding the day on which credit becomes eligible.

(ii) Declaration has to be filed within 30 days from becoming eligible to avail credit.

(iii) Details in (i) above to be certified by a CA/ Cost Accountant if aggregate claim of

CGST, SGST/ IGST credit is more than ` 2,00,000.

B. Special circumstances leading to reversal of credit/payment of amount

Special circumstances leading to reversal

of credit /payment of amount

Section 18(4) Section 18(6)

Registered person (who has

availed ITC) switching from

regular scheme of payment

of tax to composition levy

Supplies of registered

person getting wholly

exempted from tax

Cancellation of

registration

Supply of capital goods

(CG)/ plant and machinery

(P& M) on which ITC has

been taken

Section 18(5)

Manner of reversal of credit on inputs and capital goods & other

conditions

(i) Inputs ⇒ Proportionate reversal based on corresponding invoices. If such

invoices not available, prevailing market price on the effective date of switch

over/ exemption/cancellation of registration should be used with due

certification by a practicing CA/ Cost Accountant

(ii) Capital goods ⇒ Reversal on pro rata basis pertaining to remaining useful

life (in months), taking useful life as 5 years.

(iii) ITC to be reversed will be calculated separately for ITC of CGST,

SGST/UTGST and IGST.

(iv) Reversal amount will be added to output tax liability of the registered

person.

(v) Electronic credit/cash ledger will be debited with such amount. Balance

ITC if any will lapse.

Amount to be paid is

equivalent to higher of

the following:

(i) ITC on CG or P&M

less 5% per quarter or

part thereof from the

date of invoice

(ii) Tax on transaction

value of such CG or P &

M

• If amount at (i)

exceeds (ii), then

reversal amount will

be added to output

tax liability.

• Separate ITC reversal

is to be done for

CGST, SGST/UTGST

and IGST

• Tax to be paid on

transaction value

when refractory

bricks, moulds, dies,

jigs & fixtures are

supplied as scrap.

Page 43

n

l

he

o

s

Tra

nsf

er

o

f u

nu

tili

sed

IT

C o

n a

cco

un

t o

f

ch

an

ge in

co

nst

itu

tio

n o

f re

gis

tere

d p

ers

on

Section 18 (3) , RULE - 41

In case of sale, merger, amalgamation, lease or transfer of business,

unutilised ITC can be transferred to the new entity if there is a specific

provision for transfer of liabilities to the new entity. The inputs and

capital goods so transferred shall be duly accounted for by the

transferee in his books of accounts.

In case of demerger, ITC will be apportioned in the ratio of value of

assets of new unit as per the demerger scheme.

Details of change in constitution will have to be furnished on

common portal along with request to transfer unutilised ITC.

CA/Cost Accountant certificate will have to be submitted certifying

that change in constitution has been done with specific provision for

transfer of liabilities.

Upon acceptance of such details by the transferee on the common

portal, the unutilized ITC will be credited to his Electronic Credit

Ledger.

V. The provisions of section 19 relating to ITC on goods sent for job work read

with relevant rules are summarized as under:

Rule: 45

Principal can take credit o

goods (inputs and capital

goods) sent for job work.

Credit can be taken even if t

said goods are sent directly t

job worker without being first

brought to the principal'

place of business

Time limit for return of goods sent

for job work/supply from job

worker's place of business

• Inputs - 1 year

• Capital goods - 3 years

from the date of sending the same for

job work or from the date of receipt

of the same by the job worker

On failing to comply with the timelines for return of goods, the goods

will be deemed to be supplied to the job worker on the day they were

sent out.

Principal is liable to pay tax along with applicable interest on such

supply.

Time-lines for return of goods do not apply to moulds and dies, jigs

and fixtures or tools sent out for job work.

Page 44

VI. The provisions of section 20 relating to ISD are

summarized as under:

ISD is basically an office meant to receive tax invoices towards

receipt of input services and distribute the credit of taxes paid on

such input services to supplier units (having the same PAN)

proportionately

An ISD is required to

obtain a separate

registration even

though it may be

separately registered.

The threshold limit of

registration is not

applicable to ISD.

• ISD should issue an ISD invoice for

distributing ITC. It should be clearly

indicated in such invoice that it is

issued only for distribution of ITC.

• The ISD needs to issue a ISD credit

note, for reduction in credit if the

distributed credit gets reduced for

any reason.

• ITC available for distribution in a

month is to be distributed in the

same month.

• Details of distribution of credit and

all ISD invoices issued should be

furnished by ISD in monthly GSTR-6

within 13 days after the end of the

month.

• ITC of input services is distributed

only amongst those recipients to

whom the input services are

attributable.

• ITC is distributed amongst the

operational units only and in the

ratio of turnover in a State/UT of

the recipient during the relevant

period to the aggregate of

turnover of all recipients during

the relevant period to whom input

service being distributed is

attributable.

• Relevant period is previous FY or last

quarter prior to the month of

distribution for which turnover of all

recipients is available.

• Distributed ITC should not exceed the

credit available for distribution.

If the ISD has distributed excess

credit to any recipient, the excess

will be recovered from the

recipient with interest as if it was

tax not paid.

Page 45

VII. The provisions relating to availing and utilizing the ITC

are summarized as under:

A registered person is entitled to credits as under:

Transaction Credit

Intra-State supply CGST & SGST/UTGST

Inter-State-supply IGST

Imports of goods and services IGST

The protocol to avail and utilize the credit of CGST, SGST/UTGST and IGST is

as follows:

Credit of To be utilized first

for payment of

May be utilized further

for payment of

CGST CGST IGST

SGST/UTGST SGST/UTGST IGST

IGST IGST CGST, then SGST/UTGST

Credit of CGST cannot be used for payment of SGST/UTGST and credit of

SGST/UTGST cannot be utilised for payment of CGST.

Initially ITC will be credited to the

Electronic Credit Ledger (EcrL) of a

recipient provisionally for a period

of two months.

ITC matching of a month will be done

after filing of the GSTR 3 of that month

and discrepancy (claiming of excess

credit by the recipient), if any, will be

communicated to both the supplier and

the recipient.

If the supplier rectifies such discrepancy in his return

of the month in which discrepancy has been

communicated, credit will be confirmed for the

recipient else such excess credit will be added to the

recipient’s output tax liability along with interest @

18% in the return of the month succeeding the month

in which discrepancy has been communicated.

Page 46

CHAPTER-8 REGISTRATION

1. Nature of registration

The registration in GST is PAN based and State specific.

One registration per State/UT.

However, a business entity having separate business verticals in a State

may obtain separate registration for each of its business verticals.

GST identification number called “GSTIN” - a 15-digit number and a

certificate of registration incorporating therein this GSTIN is made

available to the applicant on the GSTN common portal.

Registration under GST is not tax specific, i.e. single registration for all

the taxes i.e. CGST, SGST/UTGST, IGST and cesses.

Page 47

2. Persons liable to registration (Section - 22(1)

Those who exceed threshold

limit

•Aggregate turnover > ` 20 lakh

•Aggregate turnover > `10 lakh in case of Special

Category States

Who are registered under

earlier law

In case of transfer of

business on account of

succession, etc.

•shall be liable to be registered under GST •transferee liable to be registered from the date of

succession of business

In case of amalgamation/

demerger by an order of

High Court etc.

•transferee liable to be registered from the date

on which Registrar of Companies issues

incorporation certificate giving effect to order of

High Court etc.

Taxable

Supplies

Exempt

supplies

Exports Inter State supplies

Aggregate

Turnover

Aggregate Turnover will be computed on All-India basis for same PAN

3. Compulsory registration in certain cases (Section - 24

(i) Persons making any inter-State taxable supply;

(ii) Casual taxable persons making taxable supply;

(iii) Persons who are required to pay tax under reverse charge;

(iv) Person who are required to pay tax under sub-section (5) of section 9;

(v) Non-resident taxable persons making taxable supply;

(vi) Persons who are required to deduct tax under section 51, whether or not separately registered under this Act;

(vii) Persons who make taxable supply of goods or services or both on behalf of other taxable persons whether as

an agent or otherwise;

(viii) Input Service Distributor, whether or not separately registered under this Act;

(ix) Persons who supply goods or services or both, other than supplies specified under sub-section (5) of section 9,

through such electronic commerce operator who is required to collect tax at source under section 52;

(x) Every electronic commerce operator;

(xi) Every person supplying online information and database access or retrieval services from a place outside India

to a person in India, other than a registered person; and

(xii) Such other person or class of persons as may be notified by the Government on the recommendations of the

Council.

Page 48

4. Persons not liable for registration (Section - 23)

- Person engaged exclusively in supplying

goods/services/both not liable to tax

- Person engaged exclusively in supplying

goods/services/both wholly exempt from tax

Agriculturist limited to supply of produce out of

cultivation of land

- Specified category of persons notified by the

Government

5. Where and by when to apply for registration? (Section - 25)

Person who is liable to be registered

under section 22 or section 24

•in every such State/UT in which he is

so liable

•within 30 days from the date on

which he becomes liable to

registration

A casual taxable person or a non-

resident taxable person

•in every such State/UT in which he is

so liable

•at least 5 days prior to the

commencement of business

6. Voluntary Registration and UIN (Section - 25)

Voluntary Registration

•Person not liable to be registered under

sections 22/24 may get himself registered

voluntarily.

Unique Identification

Number (UIN)

•In respect of supplies to some notified

agencies of United Nations organisation,

multinational financial institutions and

other organisations, a UIN is issued.

Page 49

Rule 10 7. Effective date of registration

Application submitted

within 30 days of the

applicant becoming liable

to registration

•Effective date is the date on which he

becomes liable to registration

Application submitted

after 30 days of the

applicant becoming liable

to registration

•Effective date is date of grant of

registration

8. Procedure for registration

Rule 8

How to apply for registration?

On common portal www.gst.gov.in

Part A: PAN + Mobile no. + E-mail ID

Part A

PAN Mobile No.

Email id

Temporary Reference

Number

CBDT database

OTP based verification

Complete and submit

Part B of application to

proper officer

Acknowledgment shall

be issued Electronically

in From GSTREG - 02

Page 50

Rule 9

Rule 9(1) Approval of Grant of registration - in 3 working day from date of

submission of application

Notice

GST Reg. - 03

If found in

deficient with

in 3 working

days

Rule 9(3)

Within 7 working

days

Deficient?

No

Response/

Clarification/

Documents?

Yes No

Yes

Rule 9(4)

Registration Certificate Within 7 working

days

Rejection of Registration

Application

10. Special procedure for registration of CTD and NRTD (Section - 27)

Casual Taxable Person Non-resident Taxable Person

A Casual taxable person is one

who has a registered business

in some State in India, but

wants to effect supplies from

some other State in which he is

not having any fixed place of

business.

Such person needs to register

in the State from where he

seeks to supply as a Casual

taxable person.

A Non-Resident taxable

person is one who is a

foreigner and occasionally

wants to effect taxable

supplies from any State in

India, and for that he needs

GST registration.

Page 51

Rule 9(2)

GST Reg - 06 GST Reg - 05

GST Reg - 04

Casual Taxable Person Non-resident taxable person

GST law prescribes special procedure for registration, as also for extension of the

operation period of such Casual or Non-Resident taxable persons.

They have to apply for registration at least 5 days in advance before making any

supply.

Registration is granted to them or period of operation is extended only after

they make advance deposit of the estimated tax liability.

Registration is granted to them for the period specified in the registration

application or 90 days from the effective date of registration.

11. Amendment of Registration (Sec - 28) (Rule - 19)

Except for the changes in some core information in the registration application,

a taxable person shall be able to make amendments without requiring any

specific approval from the tax authority.

In case the change is for legal name of the business, or the State of place of

business or additional place of business, the taxable person will apply for

amendment within 15 days of the event necessitating the change.

The Proper Officer, then, will approve the amendment within the next 15 days.

For other changes like the name of day-to-day functionaries, e-mail IDs,