Embed Size (px)

Citation preview

1

GOOD CORPORATE GOVERNANCE IMPLEMENTATION REPORT

PT BANK CENTRAL ASIA Tbk

YEAR OF 2013

Good Corporate Governance ("GCG") Implementation Report ofPT Bank Central Asia Tbk ("BCA") for 2013 was prepared inaccordance with Bank Indonesia Regulation Number: 8/4/PBI/2006 dated January 30, 2006 concerning Good CorporateGovernance Implementation for Commercial Banks, as alreadyamended by means of Bank Indonesia Regulation Number: 8/14/PBI/2006 dated October 5, 2006, and Circular Letter of BankIndonesia Number: 15/15/DPNP dated April 29, 2013 on GoodCorporate Governance Implementation for Commercial Banks.The GCG Implementation Report of BCA for 2013 consists of:I. GCG Implementation Transparency as referred to in point

IX of the Circular Letter of Bank Indonesia Number:15/15/DPNP dated April 29, 2013; and

II. Self Assessment Report on GCG Implementation in 2013.I. GCG Implementation Transparency

A. Disclosures of GCG Implementation includes:1. Implementation of the duties and responsibilities

of the Board of Commissioners and the Board ofDirectors, consisting of:a. Number, composition, criteria and independency

of the members of the Board of CommissionersAs of December 31, 2013, the total number ofmembers of the BCA’s Board of Commissionersis 5 (five) persons, consisting of 1 (one)President Commissioner, 1 (one) Commissioner,and 3 (three) Independent Commissioners. Thetotal number of members of the BCA’s Board ofCommissioners does not exceed the total numberof members of the BCA’s Board of Directors.Total number of the BCA’s Independent Commis-sioners is 60% of the total number of BCA’sBoard of Commissioners.Composition of the members of the BCA’s Boardof Commissioners as of December 31, 2013 underthe deed of Minutes of Annual General Meetingof Shareholders of BCA Number: 143 dated May12, 2011 and the deed of Minutes of Extra-ordinary General Meeting of Shareholders of BCANo. 206 dated May 16, 2012, is as follows:

Title Name

President Commissioner Djohan Emir Setijoso

Commissioner Tonny Kusnadi

Independent Commissioner Cyrillus Harinowo

2

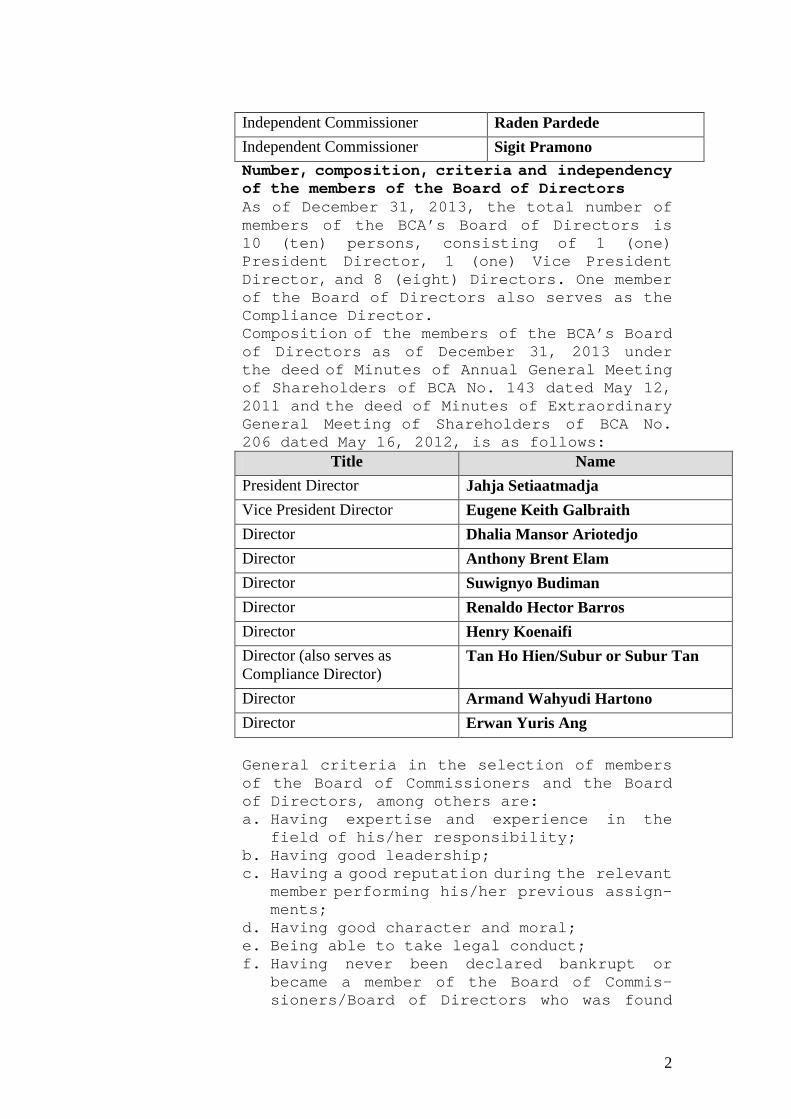

Independent Commissioner Raden Pardede

Independent Commissioner Sigit Pramono

Number, composition, criteria and independencyof the members of the Board of DirectorsAs of December 31, 2013, the total number ofmembers of the BCA’s Board of Directors is10 (ten) persons, consisting of 1 (one)President Director, 1 (one) Vice PresidentDirector, and 8 (eight) Directors. One memberof the Board of Directors also serves as theCompliance Director.Composition of the members of the BCA’s Boardof Directors as of December 31, 2013 underthe deed of Minutes of Annual General Meetingof Shareholders of BCA No. 143 dated May 12,2011 and the deed of Minutes of ExtraordinaryGeneral Meeting of Shareholders of BCA No.206 dated May 16, 2012, is as follows:

Title Name

President Director Jahja Setiaatmadja

Vice President Director Eugene Keith Galbraith

Director Dhalia Mansor Ariotedjo

Director Anthony Brent Elam

Director Suwignyo Budiman

Director Renaldo Hector Barros

Director Henry Koenaifi

Director (also serves asCompliance Director)

Tan Ho Hien/Subur or Subur Tan

Director Armand Wahyudi Hartono

Director Erwan Yuris Ang

General criteria in the selection of membersof the Board of Commissioners and the Boardof Directors, among others are:a. Having expertise and experience in the

field of his/her responsibility;b. Having good leadership;c. Having a good reputation during the relevant

member performing his/her previous assign-ments;

d. Having good character and moral;e. Being able to take legal conduct;f. Having never been declared bankrupt or

became a member of the Board of Commis-sioners/Board of Directors who was found

3

guilty of causing a company to be declaredbankrupt within a period of 5 (five) yearsprior to his/her appointment;

g. Having never been sentenced for committingany crime in the financial sector withina period of 5 (five) years prior to his/her appointment.

h. Meeting the requirements of integrity,competence, and financial reputation asreferred to in the Regulation of BankIndonesia and Circular Letter of BankIndonesian concerning Fit and Proper Test.

Independency of the Board of CommissionersAll members of the Board of Commissioners haveno financial relationship, management relation-ship, shareholding relationship and/or familyrelationship with fellow members of the Board ofCommissioners, members of the Board of Directorsand/or Controlling Shareholders or relation-ship with BCA, which may affect their abilityto act independently.Independency of the Board of DirectorsAll members of the Board of Directors have nofinancial relationship, management relation-ship, shareholding relationship and/or familyrelationship with the members of the Board ofCommissioners and fellow members of the Boardof Directors, which may affect their abilityto act independently.The majority of the members of the Board ofDirectors have no financial relationship, mana-gement relationship, shareholding relation-ship and family relationship with ControllingShareholders or relationship with BCA, whichmay affect their ability to act independently.The President Director is an independent partyto the controlling shareholders.

b. Duties and Responsibilities of the Board ofCommissioners, among others are:1. Supervising the management policies of BCA,

and the running of the management in general,and providing advices to the Board ofDirectors. The supervision performed by theBoard of Commissioners shall be in theinterest of BCA in accordance with thepurposes and objectives as well as theBCA’s Articles of Associations.

2. Ensuring the implementation of GCG prin-ciples in any business activities of BCAat all levels of BCA’s organization.

4

3. Directing, monitoring and evaluating theimplementation of BCA’s strategic policies.

4. Ensuring that the Board of Directors hastaken follow-up actions on audit findingsand recommendations from the Internal AuditDivision, External Auditors, monitoringreports of the authorities, including butnot limited to the Financial Services Autho-rity, Bank Indonesia, and/or the IndonesiaStock Exchange.

5. Informing Bank Indonesia/Financial ServicesAuthority no later than 7 (seven) businessdays as of discovering violations of thelaws and regulations in the field of financeand banking, and circumstances or anapproximation of circumstances which mayjeopardize the business continuity of BCA.

6. Establishing:a. Audit Committee;b. Risk Oversight Committee; andc. Remuneration and Nomination Committee.

7. Ensuring that the Committees established bythe Board of Commissioners perform theirduties effectively.

8. Providing adequate time to perform theirduties and responsibilities in an optimalmanner.

9. Organizing the Board of Commissionersmeetings regularly, no less than four (4)times a year. The Board of Commissionersmeeting shall be attended physically byall members of the Board of Commissionersat least twice (2) a year.

10. Preparing minutes of the Board of Commis-sioners meetings, and it shall be signedby all members of the Board of Commissionersattending the Board of Commissioners meeting.

11. Distributing a copy of the minutes of theBoard of Commissioners meeting to allmembers of the Board of Commissioners andrelated parties.

12. Submitting the report on the supervisoryduties which were carried out during theprevious financial year to the Annual GMS.

In carrying out its duties and responsibili-ties, the Board of Commissioners shall observethe provisions of the BCA’s Articles ofAssociation, Guidelines and Code of Conduct ofthe Board of Commissioners, as well as theprevailing laws and regulations.

5

The Board of Commissioners carries out itsduties and responsibilities independently.Duties and Responsibilities of the Board ofDirectors, among others are:1. Directing and managing BCA in accordance

with the BCA’s purposes and objectives;2. Controlling, maintaining and managing BCA’s

assets in the interest of BCA;3. Creating an internal control structure,

ensuring the implementation of internalaudit function at each management level andfollowing up Internal Audit findings inaccordance with the policies or directivesprovided by the Board of Commissioners.

4. Submitting Annual Work Plan, which alsoincludes Annual Budget to the Board ofCommissioners for approval of the Board ofCommissioners prior to the commencementof the forthcoming financial year, with dueobservance of the applicable provisions.

5. Implementing the GCG principles in eachbusiness activity of BCA at all organi-zational levels of BCA.

6. Preparing and maintaining the Register ofShareholders, Special Register, Minutes ofGeneral Meetings of Shareholders and Minutesof the Board of Directors Meetings.

7. Preparing Annual Report and other corporatedocuments as referred to in the prevailinglaws and regulations.

8. Following up the audit findings and recom-mendations of the External Auditors, thesupervisory reports of Bank Indonesia,Financial Services Authority and/or otherauthorities, including but not limited tothe Indonesia Stock Exchange.

9. Being accountable for the performance ofits duties and responsibilities to theshareholders through a General Meeting ofShareholders.

In carrying out its duties and responsibili-ties, the Board of Directors shall observe theprovisions of the BCA’s Articles of Associa-tion, Guidelines and Code of Conduct of theBoard of Directors, as well as the prevailinglaws and regulations.The Board of Directors carries out its dutiesand responsibilities independently.

c. Recommendations of the Board of CommissionersOne of the duties and responsibilities of the

6

Board of Commissioners is to provide advicesto the Board of Directors in the interest ofthe company in accordance with the purposes andobjectives of the company.In 2013, the advices and recommendations pro-vided by the Board of Commissioners to theBoard of Directors, among others are:1. Relating to business management in general:

In consideration of the rapid develop-ment of BCA’s business and the increasein the number of BCA’s subsidiaries, itis necessary to develop a consolidatedand integrated risk control.

Business programs/targets contained inthe Bank’s Business Plan and Annual WorkPlan and Budget need to be socializedto the branches and in its implementa-tion must consider prudential and com-pliance aspects.

2. Relating to credit risk:In lending, the risk of high concentrationon one group/specific industry needs to beavoided.

3. Relating to liquidity risk:Taking into account the increasingly tightliquidity conditions, competition in gettingDeposits, and high demand for credit, theavailability of adequate liquidity of BCAshall become a priority.

4. Relating to operational risk:From the aspect of operational risk, thesecurity of information technology in orderto maintain BCA’s excellence in transactio-nal banking requires special attention.

5. Relating to reputation risk:In the implementation of the wealth mana-gement business development, the aspects ofreputation risk should always be controlledand mitigated.

6. Relating to strategic risk:In the future, availability of reliable andcompetent human resources will be crucial,so it is necessary to develop a lean organi-zation concept and planning for the avail-ability of human resources in accordancewith the requirements of BCA.

7. Relating to compliance risk:The Board of Commissioners is of the opinionthat regulatory compliance needs specialattention from all ranks, especially from

7

the aspect of internal control and InternalAudit in order to mitigate regulatory risk.

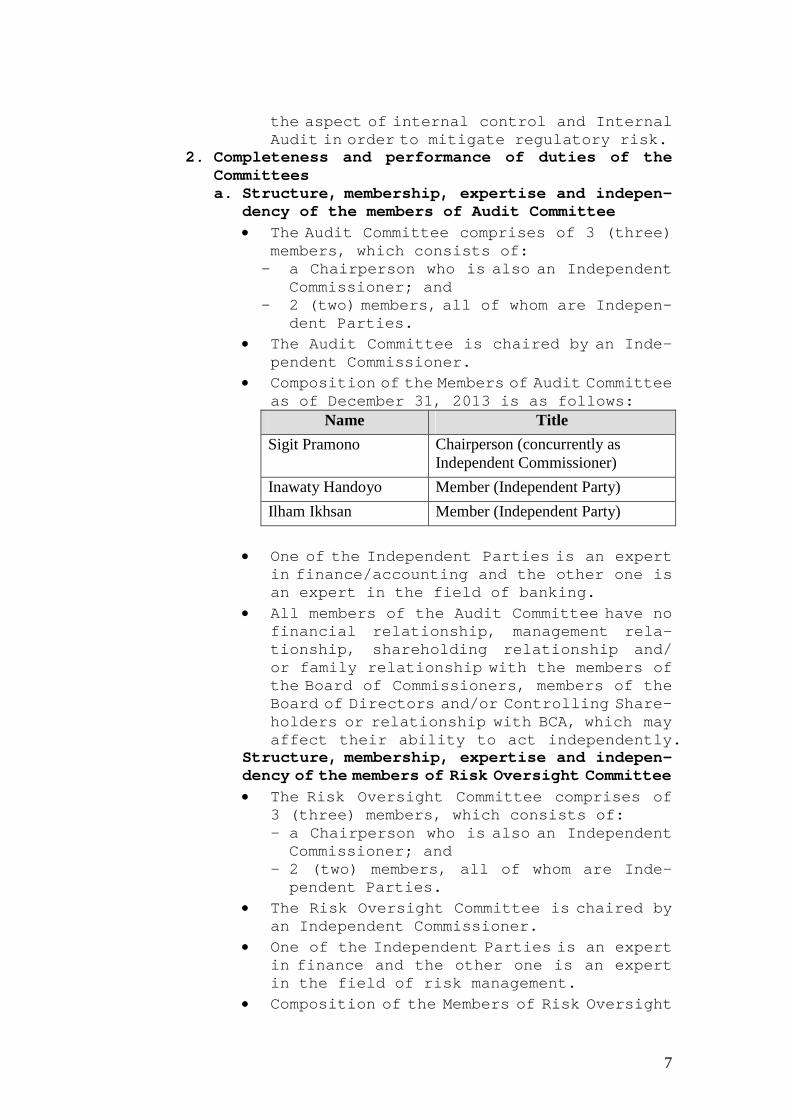

2. Completeness and performance of duties of theCommitteesa. Structure, membership, expertise and indepen-

dency of the members of Audit Committee

The Audit Committee comprises of 3 (three)members, which consists of:- a Chairperson who is also an Independent

Commissioner; and- 2 (two) members, all of whom are Indepen-

dent Parties.

The Audit Committee is chaired by an Inde-pendent Commissioner.

Composition of the Members of Audit Committeeas of December 31, 2013 is as follows:

Name Title

Sigit Pramono Chairperson (concurrently asIndependent Commissioner)

Inawaty Handoyo Member (Independent Party)

Ilham Ikhsan Member (Independent Party)

One of the Independent Parties is an expertin finance/accounting and the other one isan expert in the field of banking.

All members of the Audit Committee have nofinancial relationship, management rela-tionship, shareholding relationship and/or family relationship with the members ofthe Board of Commissioners, members of theBoard of Directors and/or Controlling Share-holders or relationship with BCA, which mayaffect their ability to act independently.

Structure, membership, expertise and indepen-dency of the members of Risk Oversight Committee

The Risk Oversight Committee comprises of3 (three) members, which consists of:- a Chairperson who is also an IndependentCommissioner; and

- 2 (two) members, all of whom are Inde-pendent Parties.

The Risk Oversight Committee is chaired byan Independent Commissioner.

One of the Independent Parties is an expertin finance and the other one is an expertin the field of risk management.

Composition of the Members of Risk Oversight

8

Committee as of December 31, 2013 is asfollows:

Name Title

Cyrillus Harinowo Chairperson (concurrently asIndependent Commissioner)

Endang SwasthikaWibowo

Member (Independent Party)

Andreas E. Susetyo Member (Independent Party)

One of the Independent Parties is an expertin finance and the other one is an expertin the field of risk management.

All members of the Risk Oversight Committeehave no financial relationship, managementrelationship, shareholding relationshipand/or family relationship with the membersof the Board of Commissioners, members ofthe Board of Directors and/or ControllingShareholders or relationship with BCA, whichmay affect their ability to act indepen-dently.

Structure, membership, expertise and inde-pendency of the members of Remuneration andNomination Committee

The Remuneration and Nomination Committeecomprises of 3 (three) members, whichconsists of:- a Chairperson who is also an IndependentCommissioner; and

- 2 (two) members, i.e. the PresidentCommissioner and an Executive Officer incharge of the Division of Human CapitalManagement (Human Resources).

The Remuneration and Nomination Committeeis chaired by an Independent Commissioner.

Composition of the Members of Remunerationand Nomination Committee as of December 31,2013 is as follows:

Name Title

Raden Pardede Chairperson (concurrently asIndependent Commissioner)

Djohan Emir Setijoso Member (concurrently as thePresident Commissioner)

Lianawaty Suwono Member (concurrently as theHead of the Division of HumanCapital Management)

9

The Executive Officer serving as a memberof the Remuneration and Nomination Committeeshall have the knowledge of remunerationsystem and/or nomination as well as succes-sion plan.

All members of the Remuneration and Nomi-nation Committee have no financial rela-tionship, management relationship, share-holding relationship and/or family rela-tionship with the members of the Board ofCommissioners, members of the Board ofDirectors and/or Controlling Shareholdersor relationship with BCA, which may affecttheir ability to act independently.

b. Duties and responsibilities of the AuditCommittee:1. Monitoring and evaluating the planning

and implementation of audit as well asmonitoring the follow up to audit findingsin order to assess the adequacy of internalcontrol, including the adequacy of financialreporting process.

2. In order to carry out the duties as referredto in point 1 above and to provide recom-mendations to the Board of Commissioners,the Audit Committee shall monitor andevaluate:a. The implementation of duties by the

Internal Audit Division (IAD).b. The compliance of audit implementation

by a Public Accounting Firm to the appli-cable Auditing Standards.

c. The compliance of Financial Statementsto the applicable Accounting Standards.

d. Provide independent opinion in the eventof disagreements between the managementand the Public Accounting Firm for theservices rendered.

e. The follow-up implementation by the Boardof Directors on the findings of IAD,Public Accountants and Bank Indonesia(BI) supervisory report.

3. Reviewing other financial information tobe released by BCA to the public and/orthe authorities, such as projections, andother reports relating to the BCA’s finan-cial information.

4. Reviewing the compliance of BCA with thelaws and regulations in the field of banking,

10

Capital Market and other laws and regula-tions as well as provisions relating tothe business activities of BCA.

5. Providing recommendations to the Board ofCommissioners on the appointment of PublicAccounting Firm based on the independency,the scope of assignment, and the fee tobe submitted to a General Meeting of Share-holders.

6. Reviewing and reporting to the Board ofCommissioners regarding any complaintsrelating to accounting and financial report-ing processes of BCA.

7. Reviewing and providing advices to theBoard of Commissioners related with anypotential conflict of interest in BCA.

8. Reviewing and monitoring the implementa-tion of effective and sustainable goodcorporate governance (GCG).

9. Performing other duties relevant to thefunctions of the Audit Committee at therequest of the Board of Commissioners.

Duties and responsibilities of the RiskOversight Committee:1. Assisting and providing recommendations to

the Board of Commissioners within the frame-work of improving the effective implementa-tion of duties and responsibilities in thefield of risk management and ensuring thatthe risk management policies are implementedproperly.

2. With respect to the process of provision ofthe recommendation, the Risk OversightCommittee shall:a. Evaluate consistency between the risk

management policy and the implementa-tion of the policy.

b. Monitor and evaluate the implementationof duties of the Risk Management Com-mittee and Risk Management Working Unit.

Duties and responsibilities of the Remunera-tion and Nomination Committee:1. Evaluating the remuneration and nomination

policies of BCA.2. Providing recommendation to the Board of

Commissioners concerning:a. Policy on Remuneration for the Board of

Commissioners and the Board of Directorsto be submitted to a General Meeting ofShareholders of BCA.

11

b. Policy on Remuneration for the ExecutiveOfficers and employees in general to besubmitted by the Board of Commissionersto the Board of Directors.

3. Developing and providing recommendation tothe Board of Commissioners concerningsystems and procedures for election and/orreplacement of the members of the Board ofCommissioners and the Board of Directorsto be submitted to the GMS.

4. Ensuring that the remuneration policy ofBCA is in compliance with the prevailinglaws and regulations.

5. Providing recommendation to the Board ofCommissioners regarding would-be member(s)of the Board of Commissioners and/or would-be member(s) of the Board of Directors tobe submitted to the GMS.

6. Recommending independent parties to bewould-be member(s) of the Audit Committeeand the Risk Oversight Committee to theBoard of Commissioners.

7. Assessing the feasibility of the policy forthe provision of facilities for the Boardof Commissioners and Board of Directors aswell as providing recommendation on therequired revision/additional explanation.

8. Performing other duties assigned by theBoard of Commissioners relating to the remu-neration and nomination in accordance withapplicable provisions.

9. Reporting the results of assessments andrecommendations with respect to the dutiesof the Remuneration and Nomination Com-mittee to the Board of Commissioners, ifrequired.

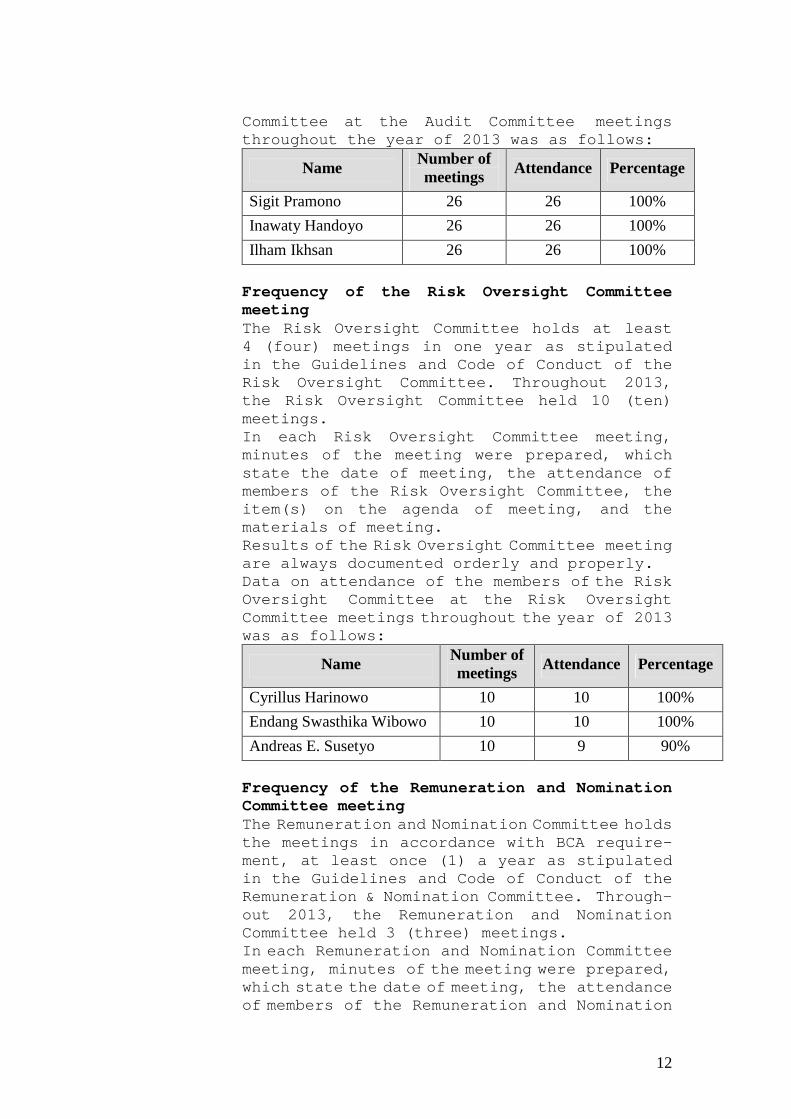

c. Frequency of the Audit Committee meetingThe Audit Committee holds at least 4 (four)meetings in one year as stipulated in theGuidelines and Code of Conduct of the AuditCommittee. Throughout 2013, the Audit Committeeheld 26 (twenty six) meetings.In each Audit Committee meeting, minutes ofthe meeting were prepared, which state thedate of meeting, the attendance of members ofthe Audit Committee, the item(s) on the agendaof meeting, and the materials of meeting.Results of the Audit Committee meeting arealways documented orderly and properly.Data on attendance of the members of the Audit

12

Committee at the Audit Committee meetingsthroughout the year of 2013 was as follows:

NameNumber ofmeetings

Attendance Percentage

Sigit Pramono 26 26 100%

Inawaty Handoyo 26 26 100%

Ilham Ikhsan 26 26 100%

Frequency of the Risk Oversight CommitteemeetingThe Risk Oversight Committee holds at least4 (four) meetings in one year as stipulatedin the Guidelines and Code of Conduct of theRisk Oversight Committee. Throughout 2013,the Risk Oversight Committee held 10 (ten)meetings.In each Risk Oversight Committee meeting,minutes of the meeting were prepared, whichstate the date of meeting, the attendance ofmembers of the Risk Oversight Committee, theitem(s) on the agenda of meeting, and thematerials of meeting.Results of the Risk Oversight Committee meetingare always documented orderly and properly.Data on attendance of the members of the RiskOversight Committee at the Risk OversightCommittee meetings throughout the year of 2013was as follows:

NameNumber ofmeetings

Attendance Percentage

Cyrillus Harinowo 10 10 100%

Endang Swasthika Wibowo 10 10 100%

Andreas E. Susetyo 10 9 90%

Frequency of the Remuneration and NominationCommittee meetingThe Remuneration and Nomination Committee holdsthe meetings in accordance with BCA require-ment, at least once (1) a year as stipulatedin the Guidelines and Code of Conduct of theRemuneration & Nomination Committee. Through-out 2013, the Remuneration and NominationCommittee held 3 (three) meetings.In each Remuneration and Nomination Committeemeeting, minutes of the meeting were prepared,which state the date of meeting, the attendanceof members of the Remuneration and Nomination

13

Committee, the item(s) on the agenda of meeting,and the materials of meeting.Results of the Remuneration and NominationCommittee meeting are always documented orderlyand properly.Data on attendance of the members of theRemuneration and Nomination Committee at theRemuneration and Nomination Committee meetingsduring the year of 2013 is as follows:

NameNumber ofmeetings

Attendance Percentage

Raden Pardede 3 3 100%

Djohan Emir Setijoso 3 3 100%

Lianawaty Suwono 3 3 100%

d. Work Program of the Audit Committee and therealization thereof1. Held a meeting with the Public Accounting

Firm of Siddharta & Widjaja to discuss thefinal audit outcomes of the BCA’s FinancialStatement for the 2012 financial yearalong with its Management Letter.

2. Evaluated and approved the proposal forrenewal of the contract with the PublicAccounting Firm of Siddharta & Widjaja,which is affiliated to KPMG International("KPMG International") and recommendedthe accounting firm to the Board ofCommissioners to perform the audit forthe BCA’s Financial Statement for the2013 financial year.

3. Held a meeting with the Public AccountingFirm of Siddharta & Widjaja to discuss theplan and scope of the audit of BCA’sFinancial Statement for the 2013 financialyear.

4. Held a meeting with the Finance and PlanningDivision to review the BCA’s FinancialStatement which will be published everyquarter.

5. Assessed the analysis of financial reali-zation with its budget.

6. Held 7 (seven) meetings with the InternalAudit Division to:a) Evaluate the annual planning.b) Evaluate the implementation of internal

audit each semester.c) Conduct discussions on audit findings

which are considered quite significant.

14

7. Conducted 6 (six) visits to the workingunits at the Head Office and Branch Officeto attend internal audit exit meeting.

8. Reviewed reports of internal audit findings(more than 167 reports) and monitored thefollow-up actions.

9. Assessed the compliance of BCA with theprevailing provisions of the laws andregulations in the field of banking througha review of the compliance report to theprudential provisions which is reportedevery month.

10. Assessed credit portfolio report issuedevery semester.

11. Monitored risk management implementationthrough quarterly report of BCA’s RiskProfile and monthly report of OperationRisk Management Information System (ORMIS).

12. Conducted discussions with the relatedworking unit to evaluate operational riskand internal control in the process andactivities of strategic working units: ITOperations, Housing Credit (KPR) Business,Credit Card Business, Logistics and HumanCapital Management, in order to provideopinion to the Board of Commissionersregarding the adequacy of mitigation effortsfor various existing risks.

13. Conducted evaluation with the relevantworking unit regarding the implementationof GCG in accordance with the ASEAN GCGScore Card criteria.

14. Prepared the Audit Committee Charter andCode of Ethics as regulated in the Regu-lation of the Capital Market and FinancialInstitutions Supervisory Agency (Bapepam-LK) No. IX.I.5 concerning Establishmentand Work Guidelines of Audit Committee –Attachment to the Decree of the Chairpersonof Bapepam-LK No. Kep-643/BL/2012 datedDecember 7, 2012.

15. Conducted discussion with External Consul-tant (Grant Thornton International Ltd)regarding the effectiveness of DAI’s per-formance.

16. Conducted a review on:a) The findings of Bank Indonesia’s audit

and the follow-up actions.b) Follow-up on the management letter from

the Public Accounting Firm of Siddharta

15

& Widjaja.17. Reported the results of routine studies

and evaluations to the Board of Commis-sioners in every quarter.

18. Attended the GMS, Analyst Meeting, and theNational Work Meeting of BCA in 2014 withinthe framework of GCG implementation.

Work Program of the Risk Oversight Committeeand the realization thereof1. Conducted:

a. Monitoring of risk by reviewing andevaluating various risk reports. TheRisk Oversight Committee providesopinions and recommendations in writing,but if further clarification is neededan explanation will be provided and/ora special meeting will be held to discussthe topic.

b. Monitoring of stress test results,which is reported every quarter.

c. Monitoring of all risks in the form ofrisk dashboard.

d. Reporting of the progress of monitoringto the Board of Commissioners.

2. Conducted special monitoring on:a. Operational risk, especially the Infor-

mation Technology (IT) risks to ensurethat the risks of internet banking andmobile banking are controlled.

b. Analysis of the stress test results,specifically on the following aspects:- Liquidity risk (general market stress

test scenario).- Market risk, especially interest

rate risk and foreign exchange risk.- Capital Allocation and Reverse.- Rupiah Secondary Reserve Limit.

3. Evaluated treasury activities, includingforeign exchange transactions.

4. Evaluated the implementation of GCG byevaluating the work documents of Riskmanagement Working Unit (SKMR) and theRisk Management Committee.

5. Provided input to the Board of Commis-sioners on the implementation and deve-lopment of the risk management processwith respect to:a. Information Technology Architecture and

Planning;b. Security aspects, potential vulnera-

16

bilities of IT system and the riskmitigation measures.

c. Testing of Data Recovery Center function,development of Disaster Recovery Plan(DRP), and Business Impact Analysis(BIA).

6. Ensured that BCA has a good infrastructurefor controlling the risks, and for thatpurpose, evaluated the provisions and thework guidelines by:a. Reviewing the provisions and guidelines

of risk management.b. Evaluating the methods, indicators and

measurement of risk.7. Attended:

a. The General Meeting of Shareholders,Analyst Meeting and the 2014 NationalWorking Meeting within the framework ofGCG implementation.

b. Workshop which discusses the improve-ment of quality in the implementationof risk management.

Work Program of the Remuneration and NominationCommittee and the realization thereof1. Recommended the re-adjustment of ranks

level in BCA in connection with the mostrecent changes in employment policy.

2. Formulated the principles of remunerationand nomination policy as follows:a. Basic principle in stipulating remu-

neration policy:• Complying with the applicable provi-sions of employment (compliance).

• The position is competitive in itsindustry (positioning and competiti-veness).

• Based on the classification/type andweight of the job (job weight).

• It is linked with individual performance(performance driven) in order that anemployee is always encouraged toperform, but still pays attention tothe potential risk.

• In accordance with the BCA performanceand capabilities.

• Observing an increase in the cost ofliving (Decent Living Needs/KHL), themovement of inflation, etc.)

b. Basic principles for selecting nomineesof the executive officers and members

17

of the Board of Commissioners and theBoard of Directors:• Complying with the provisions of Arti-cles of Association, GCG, and BankIndonesia Regulation (PBI).

• Existence of the Company’s requirement.• Qualification of candidates (compe-tence, experience and achievements,personality which shall be inaccordance with the corporate values,clean track record.)

• Prioritizing internal development,but also considering external recruit-ment in a planned way to enrichpoints of views in the management anddecision making for the company.

• Observing the alignment with thecandidate’s career development plan.

3. Recommended further studies of the remu-neration policy to anticipate an aggressivedecision making so that the risk factorsbecome less noticed.

4. Recommended to the Board of Commissionersthe distribution of bonus for the 2012financial year to all members of theBoard of Commissioners and the Board ofDirectors holding office during the 2012financial year in order that it ispresented by the Board of Commissionersto the Annual General Meeting of Share-holders (AGMS) held on May 6, 2013 forapproval.

5. Recommended to the Board of Commissionersnecessary adjustments to several compo-nents of remuneration in connection withthe resolutions of Annual General Meetingof Shareholders (AGMS) and ExtraordinaryGeneral Meeting of Shareholders (EGMS)held on May 16, 2012 regarding changes interm of office of the Board of Commis-sioners and the Board of Directors from 3(three) years to 5 (five) years.

3. Implementation of compliance, internal auditand external audit functionsImplementation of compliance functionIn running its business, BCA has a strong commit-ment to comply with the regulations of Bank Indo-nesia and the prevailing laws and regulations.Within the framework of implementing these commit-ments, the establishment of a permanent compliance

18

function is an important element in minimizing thecompliance risks and establishing a complianceculture.BCA has established a Compliance Working Unitthat is independent and free from the influenceof other working units. The Compliance WorkingUnit was established to assist the implementationof duties of the Compliance Director. The Com-pliance Working Unit is positioned at the samelevel as a Division and directly responsible tothe Compliance Director.In order that the compliance function worksproperly, the Board of Commissioners and the Boardof Directors of BCA perform active supervision.The active supervision is conducted in the formof, among others, approval upon the policies andprocedures, periodic reporting, and request forexplanations.The Compliance Working Unit has establishedpolicies and procedures in order to minimize thecompliance risk. In addition, the ComplianceWorking Unit also conducts socialization andtraining, is involved in the approval upon newproducts and activities, approval for the issuanceof internal regulations, conducts reviews of thereleases of large exposures, carries out com-pliance tests of internal control related to thecompliance with the working unit, monitors theadherence of the Company to the commitments madeto regulators.The Compliance Working Unit, in addition to beingresponsible for the implementation of the com-pliance function, is also responsible for theimplementation of the provisions of Anti-MoneyLaundering and Prevention of Terrorism Financing(AML and PTF). The AML and PTF is an interna-tional standard that must be implemented in orderto prevent the Bank being used as an instrumentor a target of crime.Compliance Activities during 2013

Performed gap analysis and its impact on newprovisions against the BCA operations and madenecessary adjustments of the internal policies.

Performed compliance risk assessment andprepared compliance risk profile report everyquarter, within the framework of managingthe compliance risks.

Conducted socialization and training to theemployees as an effort to realize a complianceculture. Socialization and training are not

19

only addressed to the existing employees,but also to new employees.

Provided approval for new products and activi-ties plans, to ensure that the new productsand activities to be launched have been incompliance with the applicable provisions.

Provided approval for draft of internal regu-lations to be issued.

Conducted a review of the compliance of corpo-rate credit release.

Performed consultative function with otherworking unit associated with the implementa-tion of the applicable regulations.

Monitored fulfillment of reporting obligationsto external parties.

Ensured the Company’s compliance to the commit-ments made by the Company to Bank Indonesiaand/ or other supervisory authorities.

Performed coordination within the framework ofconducting assessment on the Risk-based BankSoundness level.

Activities related to the Implementation of AntiMoney Laundering and Preventing Terrorism Finan-cing (AML and PTF) during 2013:

Adjusted policies and procedures of AML andPTF to be in compliance with the BankIndonesia Regulation Number: 14/27/PBI/2012dated December 28, 2012, and the CircularLetter of Bank Indonesia Number: 15/21/DPNPdated June 14, 2013 concerning theImplementation of Anti-Money Laundering andPrevention of Terrorism Financing Programfor Commercial Banks.

Conducted training and socialization of AMLand PTF continuously.

Ensuring new products and activities havecomplied with the AML and PTF regulations.

Monitoring suspicious financial transactionsby using application Suspicious TransactionIdenti-fication Model (STIM).

Reporting suspicious financial transactionsand cash transactions to the Financial Tran-saction Reporting and Analysis Center (INTRAC).

Improving STIM application parameters foridentifying suspicious financial transactions.

Coordinating the implementation of customerdata updating through target preparation andmonitoring of the realization of the targets.

20

Increasing the STIM applications capacity to becompleted in 2014.

Compliance indicators at year end 2013 are reportedas follows:

Capital Adequacy Ratio (CAR) including creditrisk, market risk and operational risk was15.66%, above the prevailing Bank Indonesiaregulations which is 9% to less than 10% (CARbased on BCA risk profile was ranked second).

NPL ratio (net) was 0.19%, well within themaximum allowed by Bank Indonesia regulationof 5% (net).

There was no exceedances or violations of theLegal Lending Limit (LLL), either to therelated parties or to the business groups.

Primary Rupiah Currency Statutory ReserveRequirements (GWM) of 8.30% and Secondary –Rupiah GWM of 20.45%, was in conformity withthe provisions of the Bank Indonesia regula-tions concerning Rupiah Currency StatutoryReserve Requirements (GWM).

Foreign Currency Statutory Reserves Require-ments (GWM) of 8.54%, was in conformity withBank Indonesia regulations concerning ForeignCurrency Statutory Reserves Requirements (GWM).

Net Open Position (NOP) at 0.24%, far withinthe limited allowed by the Bank Indonesiaregulations for a maximum of 20% of the capital.

Commitments to Bank Indonesia and other super-vising authorities were fulfilled well.

Implementation of internal audit functionIn performing its functions, the Internal AuditDivision assesses the adequacy and effectivenessof the processes of risk management, internalcontrol, governance and providing consultationfor the internal party of BCA as required.Duties and Responsibilities of the Internal AuditDivision:1. Preparing and implementing a risk based annual

internal audit plan and reporting the reali-zation thereof.

2. Examining and evaluating the processes of riskmanagement, internal control, and governance toassess the adequacy and effectiveness thereof.

3. Carrying out credit quality review.4. Providing recommendations for improvements and

objective information on the activitiesexamined.

5. Conducting investigations/special inspection

21

upon the request of the Board of Commissioners/the Board of Directors/Audit Committee, theworking unit or the existence of certain indi-cations.

6. Monitoring, analyzing and reporting the imple-mentation of the follow-up that has been doneby the auditee over the audit finding recom-mendations.

7. Acting as a consultant for internal BCA asrequired, especially concerning the InternalAudit scope of duties.

8. Compiling a program to evaluate the qualityof internal audit activities.

Audit Implementation StandardsActivities of the Internal Audit Division areguided by the Work Manual and Charter of InternalAudit as set forth in the Resolutions of theBoard of Directors Number 074A/SK/DIR/ 2012 datedApril 30, 2012 prepared in accordance with theStandard of Implementation of Internal AuditFunction of Banks issued by Bank Indonesia andthe regulation on the Establishment and Guidelinefor Preparation of Internal Audit Charter issuedby the Bapepam-LK. As a reference towards globalbest practices, the Internal Audit Division alsouses standards and codes of ethics issued by TheInstitute of Internal Auditors (IIA) and theInformation Systems Audit & Control Association(ISACA).The effectiveness of the implementation ofInternal Audit Division function and the com-pliance with the Standard of Implementation ofInternal Audit Function of Banks (SIIAFB) isreviewed by an independent external party atleast once in 3 (three) years. The most recentreview was undertaken at the end of 2013.Audit Implementation in 2013The Internal Audit Division activities in 2013were as follows:1. Implemented auditing processes related the

activities of: e-channel development, procure-ment of IT goods and services, social media,development of Customized branch format andbranch offices network, system development lifecycle, cash and cash Office and cash Car.

2. Implemented auditing on outsourced activities,records/files management and cash replenish-ment services of ATMs.

3. Implemented 26 continuous auditing programswithin the scope of branch operations and

22

lending, operations centers, IT security.4. Enhanced electronic working papers applica-

tions to improve the utilization of informationtechnology in the audits (completed the useracceptance test phase)

5. Made adjustments (alignment) to the RiskManagement Working Unit regarding the use ofthe risk scale and risk grading in branchoperations.

6. Implemented audit quality development projectsin the implementation of risk-based audits forthe audit execution and audit reporting phasesthrough training programs as well as inter-active meetings with the help of a consultant.

Focus of Audit Plan in 20141. Focusing 2014 audit on the business strategies

of BCA related to maintaining BCA's positionin the DPK particularly CASA, fee-based incomeimprovement and efficiency as well as overalloptimization of payment settlement costs.

2. Implementing end-to-end process audit approachto the application of the AML/PTF provisions,implementation of corporate social responsi-bility, the process of foreign exchange tran-sactions, development of partnership creditschemes, the function of Branch InternalControl activities, branch cash managementand ATM management by branches.

3. Implementing audit on outsourced activitiesparticularly activities which support tran-saction banking, such as: management of ATMsand EDCs machines.

4. Implementing audit on the activities of thesubsidiaries: BCA Sekuritas, BCA FinanceLimited Hongkong, BCA Syariah.

5. Improving the audit finding report and imple-menting the enhanced RBA approach to each newrating audit assignment and implementation.

6. Implementing new applications of enhancedelectronic working papers at each assignment.

7. Following up the external reviewer’s recom-mendations on the quality assurance reviewactivities in 2013 to the Internal AuditDivision.

Implementation of external audit functionIn order to fulfill the implementation of ExternalAudit functions in accordance with Bank IndonesiaRegulation Number: 14/14/PBI/2012 concerning BankTransparency Reports and Publications, and BankIndonesia Circular Letter Number: 3/32/DPNP

23

concerning the relationship between the Bank, thePublic Accounting Firms and the Bank Indonesia:1. The BCA Financial Statements have been audited

by a Certified Public Accountants which isindependent, competent, professional, andobjective using due professional care.

2. The Certified Public Accountants designatedby BCA to conduct an audit in accordance withprofessional standards, employment agreements,and the scope of the audit.

3. According to the resolutions of Annual GeneralMeeting of Shareholders, the designation ofPublic Accounting Firm and the determinationof its fees shall be made by the Board ofCommissioners with due observance of therecommendation of the Audit Committee.

4. The designation of Public Accounting Firm shallbe made in accordance with applicable regu-lations, among others:

Such Public Accounting Firms and CertifiedPublic Accountants (partner in charge) areregistered with Bank Indonesia. BCA onlyconsiders 4 (four) largest Public Account-ing Firms that are registered with BankIndonesia.

The relevant Public Accounting Firm willnot provide other services to BCA for theyear to avoid a possible conflict ofinterest.

The relevant Public Accounting Firm onlyprovides audit services for no more thanaudit period of 5 (five) financial yearscontinuously.

The Public Accounting Firm Siddharta & Widjajaaffiliated with KPMG International, wasdesignated as BCA auditor to audit the BCA’sfinancial statements for the financial yearended December 31, 2013.

5. BCA authorizes the Public Accounting Firm tosubmit audited financial statements (auditreport) accompanied by a Management Letter toBank Indonesia no later than 4 (four) monthsafter the financial year.

The Registered Public Accounting Firm and thePublic Accountants who have audited the FinancialStatements of BCA with the past 3 (three) years:

2013 2012 2011Registered PublicAccounting Firm

Siddharta &Widjaja

Siddharta &Widjaja

Purwantono,Suherman &

24

SurjaAccountant Publics Elisabeth Imelda Elisabeth

ImeldaPeter Surja

4. Implementation of risk management includinginternal control systemThe implementation of BCA risk managementinclude:

Active supervision by the Board of Commis-sioners and the Board of Directors.

Adequacy of risk management policies, proce-dures and determination of limit.

Adequacy of the process of identification,measurement, monitoring and control of riskand the risk management information system.

Internal control system.BCA implement risk management and internal controlsystems which are effectively tailored to the goalsand policies of the business lines, the size andcomplexity of the business activities of theBank based on the requirements and procedures asset down in the Bank Indonesia Regulations, andwith reference to best practice through thefollowing actions:1. Identifying and controlling all risks including

those arising from new products and newactivities.

2. Having a Risk Oversight Committee (ROC) whichaims to ensure that the existing risk manage-ment framework has provided adequate protectionagainst all risks faced by BCA and the ROChas main duty to provide recommendation and anindependent opinion professionally regardingthe appropriateness of policy and implementa-tion of risk management policies to the Boardof Commissioners, as well as to monitor andevaluate the performance of duties of the RiskManagement Committee (RMC) and the Risk Manage-ment Unit (RMU).

3. Having a Risk Management Committee (RMC) whichhas the main duties to develop policies, stra-tegies and guidelines for implementation ofrisk management, to enhance the implementa-tion of risk management based on the resultsof the evaluation of the implementation processand effective risk management system, andstipulate the matters related to businessdecisions that deviate from normal procedures(irregularities).

4. Having a Risk Management Unit (RMU) which aims

25

to ensure that the risks faced by BCA can beidentified, measured, monitored, controlled,and properly reported through the appropriateimplementation of a risk management framework.

5. Managing the risk and ensuring the availabi-lity of policies and risk limits which aresupported by procedures, reports, and infor-mation systems providing accurate and timelyinformation and analysis to the managementincluding development of measures to face thechange market conditions.

6. Ensuring that the development of the existingworking systems and procedures with due obser-vance of operations and business activitiesas well as level of risk that may occur in aworking unit.

7. Ensuring that there is clearly defined repor-ting lines segregation of functions betweenoperational working unit and the working unitcarrying out control functions. The controlfunctions shall be carried out by the RiskManagement Unit (RMU), Legal Group (LG), Com-pliance Unit (CU), and Internal Audit Division(IAD).

8. Ensuring that Internal Audit Division (IAD) hasregularly performed independent and objectivereview of the procedures and operational acti-vities of BCA. The results of review performedby the IAD shall be presented in the form ofthe Audit Report and Audit Follow-up Reportto the Board of Directors.

9. Monitoring the BCA compliance with the soundbanking management principles in accordancewith applicable regulations through ComplianceUnit (CU).

10. Ensuring that the Branch Internal Control(BIC), Regional Office Internal Control (ROIC)and Internal Audit Division (IAD) have per-formed their evaluation functions of theexisting systems and procedures at BCA. Thevaluation results by the BIC, ROIC, and IADserve as benchmark to measure the compliancelevel of working unit against the systemsand procedures which have been developed.

11. Preparing BCA Risk Profile Reports andConsolidated Risk Profile Reports quarterlyand submitting the same to the Bank Indonesiain a timely manner.

Based on the results of an assessment of riskprofile, BCA has Low to Moderate composite risk

26

level. These results can be achieved due to thequality of risk management implementation thatsupports the effectiveness of BCA-wide-risk-based supervision framework.The risk profile assessment includes 8 (eight)major risks faced by BCA, such as credit risk,market risk, liquidity risk, operational risk,legal risk, reputation risk, strategic risk andcompliance risk. BCA also has set out its policiesand procedures for managing the risks inherentin new products and new activities of BCA.++Risk Management SystemIn order to control the risk, BCA has implementedan integrated Risk Management Framework set forthin the Risk Management Basic Policy (RMBP). Theframework is used as an instrument for the deter-mination of strategy, organization, policies andguidelines, as well as infrastructure of BCA toensure that all risks faced by BCA can be properlyidentified, measured, controlled and reported.In order for the application of risk managementto be carried out effectively and optimally, BCAhas a Risk Management Committee that works toaddress issues of risk faced by BCA as a wholeand recommend risk management policies to theBoard of Directors.In addition to the above Committee, BCA has formedseveral other Committees assigned to handle morespecific risks faced by the Bank among others theCredit Policy Committee, the Credit Committee andthe Asset and Liability Committee (ALCO).BCA continues to do a thorough risk assessment ofthe plan for issuance of new products and activi-ties according to the type of risk as set forth inBank Indonesia Regulation Number: 5/8/PBI/2003dated May 19, 2003 and its amendments, amongothers: Bank Indonesia Regulation Number: 11/25/PBI/2009 dated July 1, 2009 and Circular Letter ofBank Indonesia Number: 15/6/DPNP dated March 8,2013.8 (eight) types of risk managed by the Bank:1. Credit Risk

Organization of credit continues to berefined based on the application of the "foureyes principle" whereby credit decisions aretaken based on the consideration of both thebusiness development side and credit riskanalysis side.

BCA has a Bank Basic Credit Policy (BBCP)that is continually refined and developed

27

in line with the BCA’s growth, Bank Indo-nesia Regulations and in accordance with"International Best Practice".

Refinement or improvement in proceduresand systems of the credit risk managementis made through the development of the "LoanOrigination System" over workflow of lendingprocess (from start to finish) so that theloan processing can be achieved effectivelyand efficiently. Development of debtor riskprofile measurement systems continues to bedeveloped and improved so that it can beapplied as a whole, as well as the develop-ment process of lending database continuesto be done and enhanced.

To properly maintain credit quality, themonitoring of credit quality continues tobe done on a regular basis, either by creditcategory (Corporate, Commercial, Small &Medium Enterprise (SME), Consumer and CreditCard) and on an overall loan portfolio basis.

BCA has developed a credit risk managementby analyzing the loan portfolio stresstesting and monitoring of the results ofthe stress testing. In response to changesin market conditions and economic turmoil,BCA conducts stress-testing analysis on aregular basis. Stress testing is beneficialto the Bank as a tool for estimating theimpact of risk in "stressful condition" sothat the Bank can devise appropriate stra-tegies to mitigate these risks as part ofthe implementation of "contingency plans".

In order to monitor and control creditrisk that occurs in subsidiaries, BCA hasconducted monitoring of subsidiary creditrisk on a regular basis, while ensuringthat the Subsidiaries have sound and effect-tive Credit Risk Management Policy.

2. Market Risk

In managing its foreign exchange risk,BCA centralizes the net open position atthe Treasury Division, which combines dailyreports of net open position from allbranches. In general, each branch isrequired to cover its total foreign exchangerisk at the end of each working day, althoughthere was a tolerance limit of net openposition for each branch depending on the

28

amount of foreign exchange transactionactivity in the branch. BCA creates a dailynet open position that combines the netopen position in the consolidated statementof financial position (balance sheet) andoff-balance sheet accounts.

To measure foreign exchange risk, BCA usesthe Value at Risk (VaR) methodology withHistorical Simulation approach for internalreporting purposes, while reporting of theBCA’s compliance with Minimum CapitalRequirement using Bank Indonesia standardmethodology.

The main components of BCA sensitive liabi-lity against the interest rate movementsare customer deposits, while the BCA sensi-tive assets are Government Bonds, Securities,and extended loans. ALCO regularly monitorthe development of markets and adjust theinterest rates on the deposits and loansextended.

BCA determines the interest rates on depo-sits based on market conditions and compe-tition by monitoring the movement of thebenchmark interest rate and the interestrates offered by Bank competitors.

3. Liquidity Risk

BCA is very concerned with maintenance ofadequate liquidity to meet its commitmentsto its customers and other parties, eitherwithin the framework of the provision ofcredit, repayment of customer deposits andto meet operational liquidity needs. Thefunction of managing the overall bankliquidity needs is undertaken by ALCO andoperationally implemented by the TreasuryDivision.

Measurement and control of liquidity riskis done by monitoring the liquidity reservesand the loan to deposit ratio (LDR), maturityprofile analysis, cash flow projections,as well as periodic stress tests to measurethe impact on the Bank liquidity in the faceof extreme conditions. BCA also has acontingency funding plan to deal with theextreme conditions.

BCA has complied with the provisions rela-ting to liquidity as stipulated in BankIndonesia Regulation which requires the

29

Bank to maintain Rupiah liquidity (StatutoryReserve) on a daily basis, which consistsof Primary GWM and GWM LDR in Rupiahdeposits with Bank Indonesia, a SecondaryGWM consisting of SBI, SDBI, SUN, and excessreserves, as well as reserve currency inthe foreign exchange currency currentaccounts with Bank Indonesia.

4. Operational Risk

Basel II Accord requires the Bank to includeoperational risk as a component in thecalculation of capital adequacy of a Bank.In connection with this, the Bank imple-mented preliminary Risk Control Self Assess-ment (RCSA) for all the branches/regionaloffices and all divisions in the Head-quarters. One goal of this implementationis to embed a RCSA risk culture and increaserisk awareness which is the main require-ment for risk management.

BCA also has a database of cases/operationalrisk losses that occur throughout theworking unit known as the Loss Event Database(LED). LED aims to assist BCA in recordingand analyzing cases or problems, so thatcorrective and preventive actions can betaken for the similar cases. The ultimatepurpose of the LED is that the risk ofoperational losses that may occur can beminimized. In addition, the LED is also amethod of collecting data of operationallosses risk to be used by BCA to calculatethe capital charge and continuously moni-toring cases that might lead to operationallosses such as those that have taken placein BCA.

BCA has implemented Key Risk Indicator(KRI) is an application used to provide anearly warning sign on the possibility ofan increased operational risk in a workingunit.

BCA has calculated the Bank’s capitaladequacy for operational risk based on theBank Basic Indicator Approach. CurrentlyBCA has implemented the relevant Bank Indo-nesia Regulation related to the inclusionof operational risk in the calculation ofrisk capital adequacy ratio (CAR) inaddition to credit risk and market risk.

30

5. Legal Risk

Inherent legal risk can be assessed aspotential losses based on the cases occur-ring against BCA and Subsidiaries of BCAwhich are currently under the court processdivided by BCA capital and consolidatedcapital. The parameters used to calculatethe potential losses of court cases are thebasis of a lawsuit (position case), thevalue of the case, and legal documentation.

To identify, measure, monitor and controllegal risks, BCA has established a LegalGroup at Headquarters and legal units inmost of the Regional Office.

In order to mitigate legal risks, the LegalGroup has taken the following actions:-Establishing Legal Risk Management Policy,having internal regulations which governthe organizational structure and the jobdescription of the Legal Group as wellas establishing legal document standardi-zation.

- Organizing legal communication forum toimprove the competence of legal staff.

- Doing socialization on the impact ofprevailing regulations on the bankingactivities of BCA and various modusoperandi of banking felony as well as thelegal handling guidelines for the relatedbranch and unit officers.

- Conducting legal defense on civil andcriminal cases that involve BCA whichare in the court process, as well asmonitoring the progress of the cases.

- Developing a loan security strategy plan(in collaboration with other working units,among others the Credit Settlement Bureau)in relations to issues of non performingloan.

- Registering the assets belonging to BCAincluding intellectual property rights(IPR) on banking products and services aswell as land and building rights belongingto BCA to the (relevant) authorities.

- Monitoring and taking legal actions forviolations of BCA’s assets, includingviolations of BCA’s intellectual propertyrights (IPR).

- Monitoring and analyzing the court casesfaced by BCA and Subsidiary Entities.

31

- Conducting an inventory, monitoring,analyzing and calculating the potentiallosses that may arise related to pendinglegal cases.

6. Reputation Risk

Assessment of reputational risk is performedusing parameters such as frequency ofcomplaints and negative publicity as well asthe achievement complaint resolution. Anassessment report is compiled in a quarterlyreputational risk profile.

To manage and control the reputational risk,BCA is supported by Halo BCA facility (a 24-hour telephone hot line service, e-mail andsocial media, as well as walk-in customersfor information, suggestions and complaints).

Reputational risk management is carried outbased on:- Bank Indonesia Regulation Number: 7/7/PBI/2005 dated January 20, 2005 concerningSettlement of Customer Complaints.

- Bank Indonesia Circular Letter Number:10/13/DPNP dated March 6, 2008 concerningAmendments to Bank Indonesia CircularLetter Number: 7/24/DPNP dated July 18,2005 concerning Settlement of CustomerComplaints.

- Bank Indonesia Circular Letter Number:7/24/DPNP dated July 18, 2005 concerningSettlement of Customer Complaints.

7. Strategic Risk

Assessment of inherent strategic risks isperformed using parameters such as theconformance of the strategy with thebusiness environment, low-risk strategyand high-risk strategy, positioning of BCAbusiness and achievement of Bank BusinessPlan.

Assessment of the quality of strategic riskmanagement is done by using parameterssuch as risk governance, the risk managementframework, risk management processes, MISand human resources, as well as the adequacyof the risk control system.

8. Compliance Risks

In accordance with the applicable BankIndonesia provisions, BCA has appointed amember of the Board of Directors as aDirector in charge of compliance function.

32

In the performance of duties, the ComplianceDirector is supported by the ComplianceUnit is responsible for managing the BCAcompliance risk.

BCA has developed compliance applies andprocedures containing, among others, theprocess to constantly adjust the rules andinternal systems with the applicable regula-tions and to communicate such provisions tothe related employees, to make review ofnew products/activities, to conduct periodiccompliance testing, to organize training forthe employees and to make monthly compliancereports to the Board of Directors and theBoard of Commissioners.

BCA already has and apply the Programs ofAnti-Money Laundering and Preventing theFinancing of Terrorism. BCA has also deve-loped applications to identify suspiciousfinancial transactions in accordance withapplicable regulations.

BCA’s composite risk in the fourth quarter of2013 was "Low to Moderate", this arises from anassessment of inherent risk as "Low to Moderate"with an assessment of quality of risk mana-gement as "Satisfactory". The quality of riskmanagement implementation is a reflection ofthe scope of risk management set down in theRisk Management Basic Policy (RMBP) of BCA.The risk of the composite of 8 (eight) types ofrisk assessed are as follows:- Risks that have a composite risk "low" areMarket Risk, Liquidity Risk and Legal Risk.

- Risks that have a composite risk "low tomoderate" are Credit Risk, Operational Risk,Reputation Risk, and Strategic Risk.

- Risks that have a composite risk "Moderate"are Compliance risk.

The trend of the bank inherent risks in thefourth quarter of 2013 was stable since basedon projection results, it was estimated therewould be no significant changes in inherentrisks. The trend of the quality of consoli-dated risk management implementation for thefourth quarter of 2013 was stable since BCAwas continuously improving adjustment of riskmanagement in all of its activities so that BCAwas able to identify, measure, monitor, andcontrol any existing risks.Implementation of internal control system

33

BCA has a policy of internal control systemwhich includes 5 (five) components:

Supervision by management and a riskcontrol culture

Identification and assessment of risk

Control activities and segregation of duties

Accounting, information, and communicationsystems

Monitoring and corrective action againstdeviations

In addition, BCA has also a business conti-nuity plan and disaster recovery plan toaccelerate the recovery process in the eventof a disaster has a system backup to preventthe high risk of business failure.All management and employees of BCA have a roleand responsibility in improving the qualityand implementation of BCA’s internal controlsystem.The parties involved and responsible for theimplementation of BCA’s internal control systeminclude the Board of Commissioners, the AuditCommittee, the Board of Directors, the InternalAudit Division, officers and employees of BCA,the Internal Control of Branch, the InternalControl of Regional Office and the InternalControl of Specified Working Unit at theHeadquarters.1. Internal controls are implemented among

others through:a. Financial Control:

BCA has prepared a Bank Business Planthat details BCA overall strategyincluding the business developmentdirection.

Development of the strategy that takesinto account the impacts on the BCA’scapital, among others projectedcapital and CAR (Capital AdequacyRatio).

The Board of Directors are activelyengaged in discussions/provide inputand monitor internal conditions andexternal factors development thatdirectly or indirectly affect theBCA’s business strategy.

BCA has procedures to monitor andmeasure the company performance on amonthly, quarterly, semi-annual, and

34

annual basis.

BCA has implemented financial controlprocesses through realization moni-toring efforts compared with finan-cial budget in a report which isperiodically generated and used forfollow-up remedial action by the Boardof Directors.

b. Operational Control:

BCA has completed standard operatingprocedures/operating manuals detail-ing the working procedures of eachbanking operating transaction appliedin BCA related to new products andactivities, including mitigation ofthe related operational risks. Prepa-ration of the working proceduresperformed by the Division of Opera-tions and Services Development (DOSD)and have been reviewed by variousrelated working units to ensure thatany operational risk that may existin such activities has been properlymitigated.

BCA applies the restriction onauthority to the officers by settingthe limit in conducting transactionsas well as restriction on access tothe officers to IT & computer networksthrough the use of user ID and passwordas well as fingerscan installation.

BCA has established an organizationalstructure, a well-equipped internalcontrol unit to support the opera-tional control:- Separation of functions that cangive rise to conflict of interest.

- Supervisor oversees the day-to-dayoperation of internal controls atBranches.

- Branch Internal Control (BIC) over-sees the periodic operation ofinternal controls at Branches.

- Regional Office Internal Control(ROIC) oversees the operation ofinternal controls in the RegionalOffices.

- Internal Control of SpecifiedWorking Unit at the Headquarters

35

oversees the operation of internalcontrol in a specified working unitat the Headquarters.

- Risk Management Working Unit(RMWU), Legal Group, ComplianceWorking Unit (CWU)

- Internal Audit Division (IAD):

Independent of the risk-taking unit.

Checking and assessing the adequacy/effectiveness of the internal controlsystem, risk management and corporategovernance by implementing the annualaudit plan.

c. Compliance with other laws and regula-tions:

BCA has a strong commitment to complywith the prevailing laws and regula-tions and take steps to improve theshort-comings, if any.

BCA has a Compliance Working Unit(CWU) that is independent of opera-tional working unit in carrying outcompliance functions.

The existence of Monthly Report ofMonitoring of Compliance with BCA’sPrecautionary Provisions submitted tothe Board of Commissioners and theBoard of Directors.

BCA’s Compliance Risk Management Stra-tegy has the policy to always complywith applicable regulations and takeproactive preventive action (ex-ante)in order to minimize the occurrenceof violations and curative actions(ex-post) in order to improve theshort-comings.

2. BCA has implemented an effective internalcontrol system which is adjusted to thepurpose, business policy, the size andcomplexity of BCA business activities basedon the requirements and procedures as setdown in the Bank Indonesia Regulation aswell as with reference to best practicethrough the following actions:

There is a determination of reportinglines and a clear separation of functionsbetween the operating working unit andthe working unit which carry out controlfunctions.

36

Control functions carried out by the RiskManagement Working Unit (RMWU), LegalGroup (LG), Compliance Working Unit (CWU)and the Internal Audit Division (IAD).

Internal Audit Division (IAD) has carriedout independently & objectively a reviewof BCA the procedures and operationalactivities periodically. IAD reviewresults are presented in the form of theAudit Reports and Audit Findings Follow-up Reports to the Board of Directors.

Branch Internal Control (BIC), RegionalOffice Internal Control (ROIC) andInternal Audit Division (IAD) has con-ducted evaluation function of the systemand procedures the implementation inBCA. The evaluation results of the BIC,the ROIC and IAD shall serve as abenchmark for the level of compliance ofthe working unit with the systems andprocedures in place.

5. Lending to related parties and large exposuresBCA has a policy on lending to the relatedparties and large exposures, as stipulated inthe Credit Provisions Manual. The evaluation andupdating of the policies in the Credit ProvisionsManual shall be done periodically. The lending tothe related parties and large exposures are alwaysundertaken with due observance of the prudentprinciples and always in compliance with BankIndonesia regulations or other prevailing lawsand regulations, among others concerning theLegal Lending Limit (LLL).In addition, the Lending to the related partiesmust also be decided by the Board of Commis-sioners independently.Routine reporting of LLL to the Bank Indonesiashall be conducted in a timely manner. Throughoutthe year of 2013 there were no violations orexceedances of the LLL.The Lending to the Related Parties and to theIndividuals Core and Groups Debtors (largeexposure) in BCA during 2013.

No. LendingTotal

DebtorNominal

(Million Rupiah)1. To the Related Parties 195 2,963,4872. To the Core Debtors

a. Individual 50 66,081,139

37

b. Group 30 88,471,810

6. Strategic planIn anticipation of the dynamics of changes inthe external environment, BCA always reviews itsshort, medium and long-terms strategies asoutlined in the Bank Strategic Plan in the form ofBank Business Plan (BBP) and Annual Work Plan &Budget (AWPB). The formulation of Bank StrategicPlan is undertaken with reference to the BankIndonesia Regulation Number: 12/21/PBI/2010 datedOctober 19, 2010 concerning the Bank Business Planand the Circular Letter of Bank Indonesia Number:12/27/DPNP dated October 25, 2010 concerning theBank Business Plan.As part of BCA’s policies direction and strategicmeasures to achieve its vision and mission, BCAhas designed and developed a number of businessinitiatives oriented to meet the evolving custo-mers' needs.BCA Strategic Plan in 2014Overall, BCA sees the Indonesian economy andbanking sector has a solid footing to face anyeconomic slowdown in 2014. BCA supports BankIndonesia’s efforts to manage national loan growthat a sustainable level as well as to maintainthe sound banking capital and liquidity.In the long term, BCA is very optimistic aboutthe prospects for Indonesian economic and banking.The solid economic growth in Indonesia over thepast decade has produced a GDP per capita of morethan US$ 3,500 accompanied by an increase in themiddle class growth, which serve as a magnet forinvestment flows as well as supports an expandingdomestic economy.With the support of the good capital and liquiditypositions, BCA commits to keep making investmentsin 2014 in order to maintain and increase BCA’sfranchise value. BCA will continue to strive tosupport its customers who have established agood relationship, in meeting the credit needs,transaction needs and fund placement as well asother banking activities.Strategic priorities in 2014 will remain open tothe sustainable development of customer relation-ships through enhancing payment settlementservices, lending, especially for the existingcustomers and development of new businesses.Lending opportunities and development of newbusinesses will optimize the superiority of BCA

38

as a provider of banking transaction services.The following is a further elaboration of threemain business objectives:

Enhancing payment settlement servicesBCA will focus on funding, particularly streng-thening the transactional accounts (currentand savings accounts) by continuing to improvepayment settlement services and developingnew transaction related products and services.With regard to the network expansion, BCA willincrease the number of branches and bankingelectronic delivery channels, supported bythe increase in the capability and capacityof information technology infrastructure. BCAalso continues the process of improving itscapabilities in cash management.Amid tight liquidity and rising of interestrates, BCA will keep paying attention andmake adjustments to the deposit interest raterequired to maintain the position of the thirdparty funds and to achieve a strong and soundliquidity position.

LendingBCA will continue to provide lending to allsegments with a priority towards businesscustomers who have established good relation-ships with BCA and has a solid track record.BCA believes that fostering relationships withthe customers through consistent lending is akey to maintaining loyalty of the qualifieddebtors. In the consolidation phase of thecredit activity, BCA will continue to reviewand improve credit infrastructure to supportthe short-term and long-term interests.Furthermore, streamlining of the credit processwill be continued to be made.

Development of new businessesBCA also continue to develop new businessthrough its subsidiaries in the field of ShariaBanking, insurance, securities and consumerfinance designed to complement BCA’s mainbusiness. In 2014, BCA will explore the lifeinsurance business through the establishment ofa new subsidiary. Development of new businessesis expected to provide more comprehensivefinancial solutions to its customers.Faced with the challenges of the current macro-economic, BCA believes that the medium-termstrategy will support BCA in strengtheningthe long-term competitive advantages. BCA

39

believes that this consistent strategic measureis able to build a quality customers base evenwith increasing banking competition in Indo-nesia.

7. Transparency of financial and non-financial condi-tions that have not been disclosed in other reportsInformation on BCA’s financial condition has beenset forth clearly and transparently in severalreports, including as follows:1. Annual Report, among others, including:

a. Financial highlights including shares per-formance, the report of the Board of Com-missioners, the report of Board of Directors,company profiles, management analysis anddiscussion on business and financial per-formance, corporate governance and corporatesocial responsibility.

b. Annual Financial Statements that have beenaudited by the Public Accountants and thePublic Accounting Firm registered with theBank Indonesia. Annual Financial Statementscovers a period of 1 (one) Financial Yearand presented with a ratio of 1 (one)previous financial year.

c. Statement of responsibilities of the Boardof Commissioners and the Board of Directorsregarding the accuracy of the contents ofthe Annual Report. The statements are setforth in the statement letter which is signedby all members of the Board of Commissionersand all members of the Board of Directors.

2. Quarterly Published Financial StatementBCA has announced a Quarterly Published FinancialStatements in accordance with the prevailingregulations. The Published Financial Statementshall be signed by 2 (two) members of the Boardof Directors of BCA. The Published FinancialStatements shall be announced in 3 (three) dailynewspapers, 2 (two) daily newspapers publishedin Indonesian language and 1 (one) daily news-paper published in English-language, which havea wide circulation in the place of domicile ofthe BCA Headquarters.

3. Monthly Published Financial StatementBCA prepares and submits a Monthly FinancialStatement in the format of Commercial BankMonthly Report (CBMR) in accordance with theBank Indonesia regulations. Furthermore, thereport shall be used as a basis by the BankIndonesia to publish monthly financial state-

40

ments on the website of Bank Indonesia.Transparency of Non-Financial ConditionsBCA provides clear, accurate and up-to-date infor-mation on BCA products. Such information can beeasily obtained by the customers, among others inleaflets, brochures or other written forms at eachBCA branch offices in locations easily accessibleto customers, and/or in the form of electronicinformation that is provided through hotlineservice/call center or on the website.In addition, BCA provides and informs the proceduresfor customer complaints and the settlement ofdisputes to the customers in accordance with BankIndonesia regulations concerning customer complaintsand banking mediation.In connection with the above matters, BCA has takenthe following actions:a. Publicating transparently the financial and

non-financial conditions to the stakeholders,including Periodic Financial Statement, LLLRoutine Reporting to Bank Indonesia, QuarterlyPublished Financial Statements, and the sameare posted on the BCA’s website in accordancewith prevailing regulations.

b. Preparing and presenting a report in a manner,type and scope as stipulated in the Bank Indo-nesia regulations concerning Transparency ofBank Financial Conditions.

c. Publishing the BCA’s product information inaccordance with the Bank Indonesia regulationsconcerning Transparent Information of BankingProducts and Utilization of Customer’s PersonalData.

d. Providing procedures for customer complaints andthe settlement of disputes for the customers inaccordance with Bank Indonesia regulationsconcerning Customer Complaints and BankingMediation.

e. Submitting the Annual Report to Bank Indonesia,regulators and other agencies as required orother agencies deemed necessary to have them.

f. Disclosing the Ownership Structure in theAnnual Report and on the BCA’s website.

8. Other Information relating to Corporate GovernanceNo intervention from the owner in:

the composition of the members of the Boardof Commissioners and the Board of Directors;

implementation of the duties of the Board ofCommissioners and the Board of Directors;

which causes the BCA operations is disrupted that

41

result in the BCA;s profits being reduced and/orcausing harm to BCA.

the composition of the Committees under theBoard of Commissioners;

the implementation of duties of the Committeesunder the Board of Commissioners;

B. Share ownership of the members of the Board of Commis-sioners and the Board of Directors with an equityamount of 5% (five percent) or more than the amount ofpaid-up capital, including the type and number ofshares in:a. BCA;b. Other banks;c. Non-Bank Financial Institutions; andd. Other companies;domiciled in Indonesia or overseas.Share ownership of the members of the Board of Commis-sioners totaling 5% or more than the amount of paid-up capital

Name

Share ownership of the members of the Board ofCommissioners totaling 5% or more than the amount

of paid-up capital in

BCAOtherBanks

Non-BankFinancial

Institutions

Othercompanies

Djohan Emir Setijono - - - Tonny Kusnadi - - - Cyrillus Harinowo - - - -Raden Pardede - - - Sigit Pramono - - - -Remarks: = Possessing shares totaling 5% (five percent) or more than the amount of

paid up capital

42

Share ownership of the members of the Board of Directorstotaling 5% or more than the amount of paid-up capital

Name

Share ownership of the members of the Board ofDirectors totaling 5% or more than the amount of

paid-up capital in

BCAOtherBanks

Non-BankFinancial

Institutions

Othercompanies