Embed Size (px)

Citation preview

Goldman Sachs Global Economics, Commodities and Strategy Research 2010 1

Goldman Sachs Global Economics, Commodities and Strategy Research 2010 2

The Credit Crisis and the Euro

Ben BroadbentManaging Director & Senior European Economist

September 2010

Goldman Sachs Global Economics, Commodities and Strategy Research 2010 3

Summary

Europe recovering but sharp divergence within the Euro-zone.

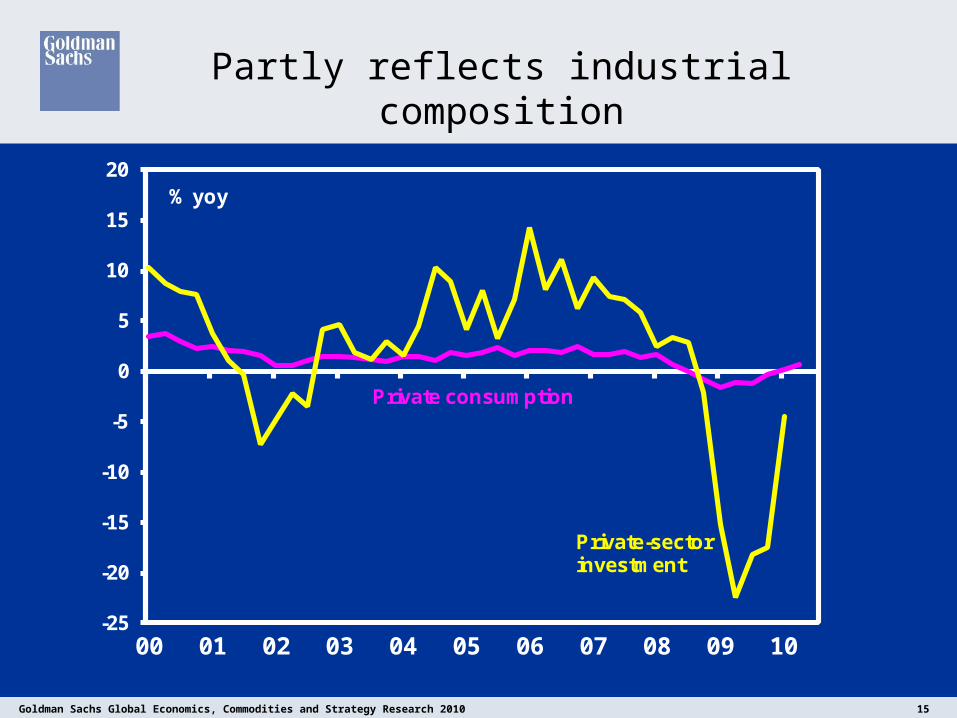

Partly industrial composition: investment-driven cycle so sharpest “V”s in capital-goods-producing countries.

Credit crunch has also blown away a decade of interest-rate convergence between “core” and “periphery”.

Eurozone needs (i) more fiscal discipline ahead in good times &/or (ii) more support in bad times. Will politics allow this?

Goldman Sachs Global Economics, Commodities and Strategy Research 2010 4

Estimated banks’ losses, March 2009

Eurozone banks: EUR 920bn (10.1% of GDP)

UK banks: GBP 210bn (14.6%)

Total: USD 1.4tn (15.1%)

Goldman Sachs Global Economics, Commodities and Strategy Research 2010 5

Domestic Demand and Growth Contributions, Last Decade

Source: GS Global ECS Research

0

5

10

15

20

25

30

35

40

45

China Russia India Brazil BRICs US Euroland

%

Demand Contribution

Growth Contribution

2000-2009 average contribution in USD terms

Goldman Sachs Global Economics, Commodities and Strategy Research 2010 6

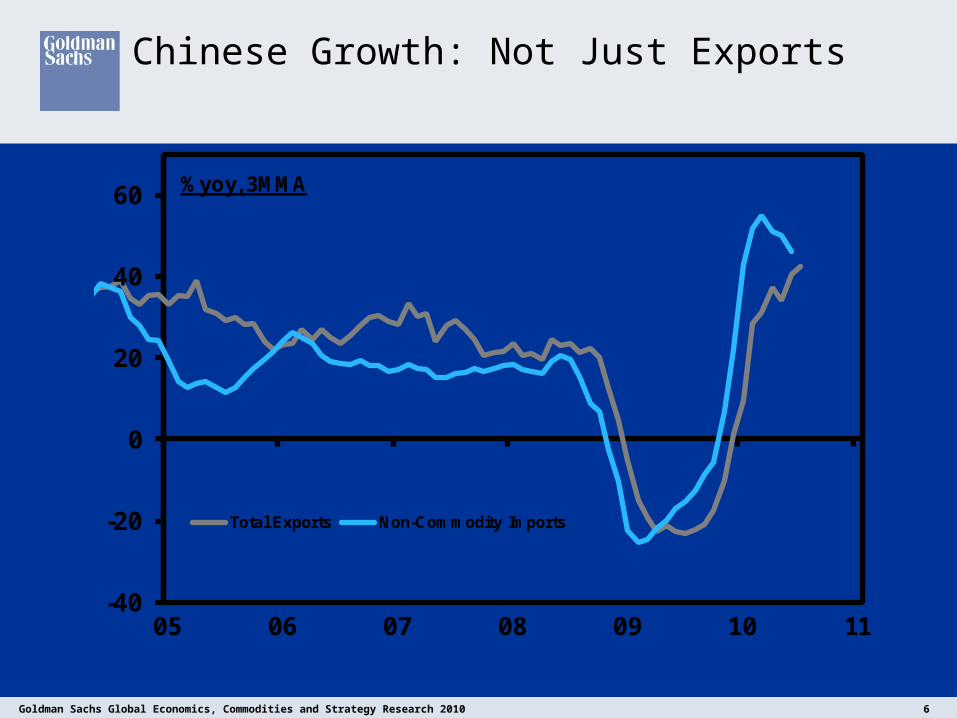

Chinese Growth: Not Just Exports

-40

-20

0

20

40

60

05 06 07 08 09 10 11

%yoy, 3MMA

Total Exports Non-Commodity Imports

Goldman Sachs Global Economics, Commodities and Strategy Research 2010 7

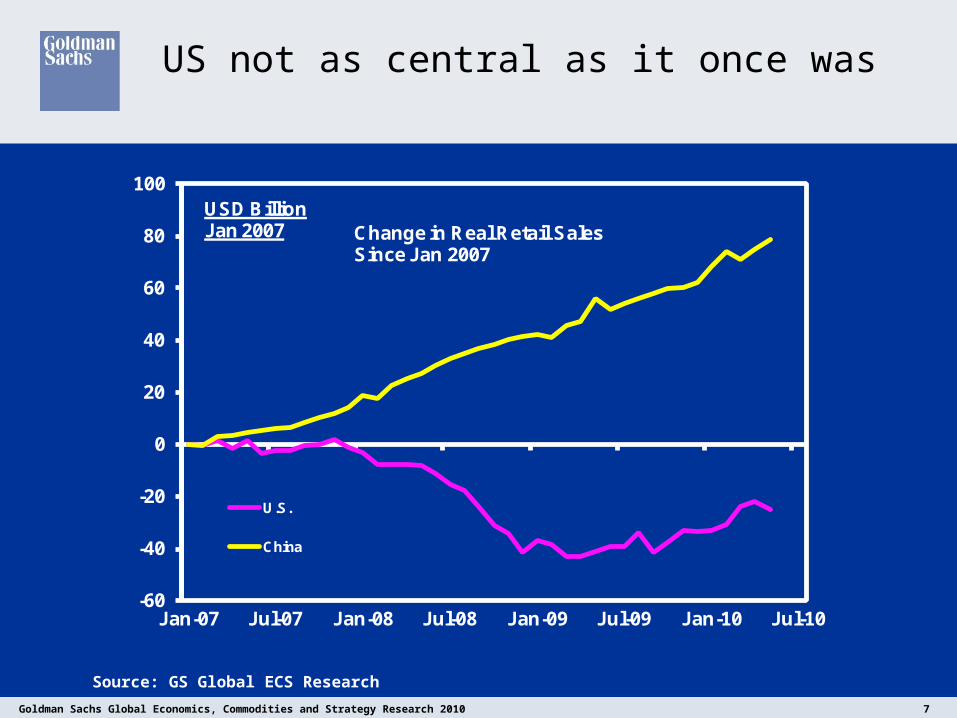

US not as central as it once was

Source: GS Global ECS Research

-60

-40

-20

0

20

40

60

80

100

Jan-07 Jul-07 Jan-08 Jul-08 Jan-09 Jul-09 Jan-10 Jul-10

USD Billion Jan 2007

U.S.

China

Change in Real Retail Sales Since Jan 2007

Goldman Sachs Global Economics, Commodities and Strategy Research 2010 8

Very aggressive policy response

-5

-4

-3

-2

-1

0

1

2

3

-4 -2 0 2 4 6 8 10 12 14 16 18 20 22 24 26 28 30 32 34 36

Base Rate (%)

Source: GS Global ECS Calculations

Euroland (Current Cycle)

UK (Current Cycle)

Max

Min

Mean

Months from start of crisis

Goldman Sachs Global Economics, Commodities and Strategy Research 2010 9

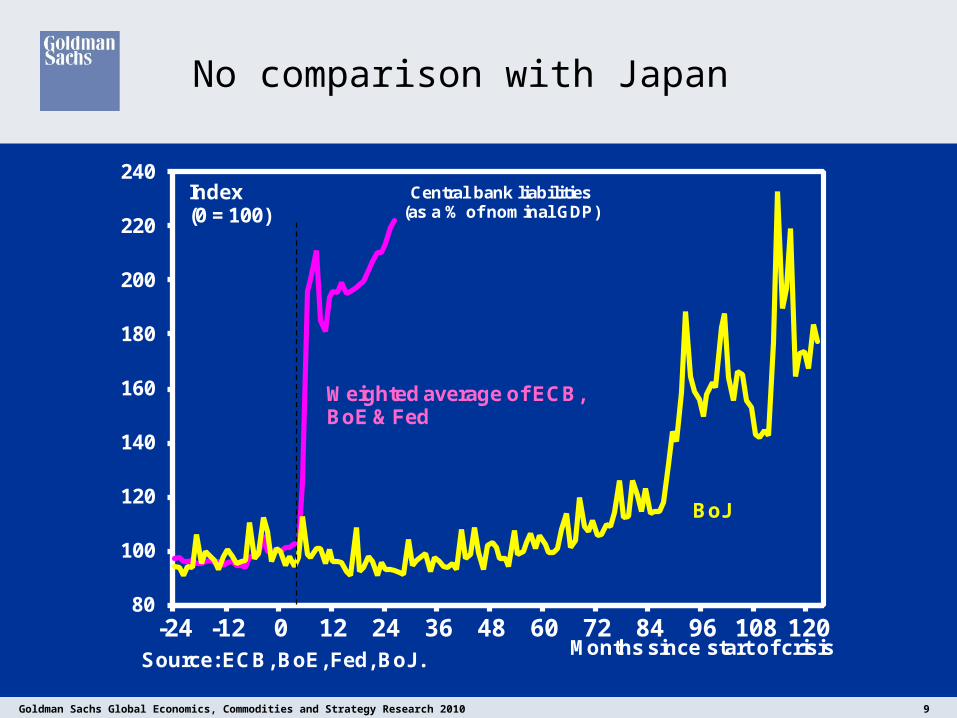

No comparison with Japan

80

100

120

140

160

180

200

220

240

-24 -12 0 12 24 36 48 60 72 84 96 108 120

Index(0 = 100)

Source: ECB, BoE, Fed, BoJ.

BoJ

Central bank liabilities(as a % of nominal GDP)

Months since start of crisis

Weighted average of ECB, BoE & Fed

Goldman Sachs Global Economics, Commodities and Strategy Research 2010 10

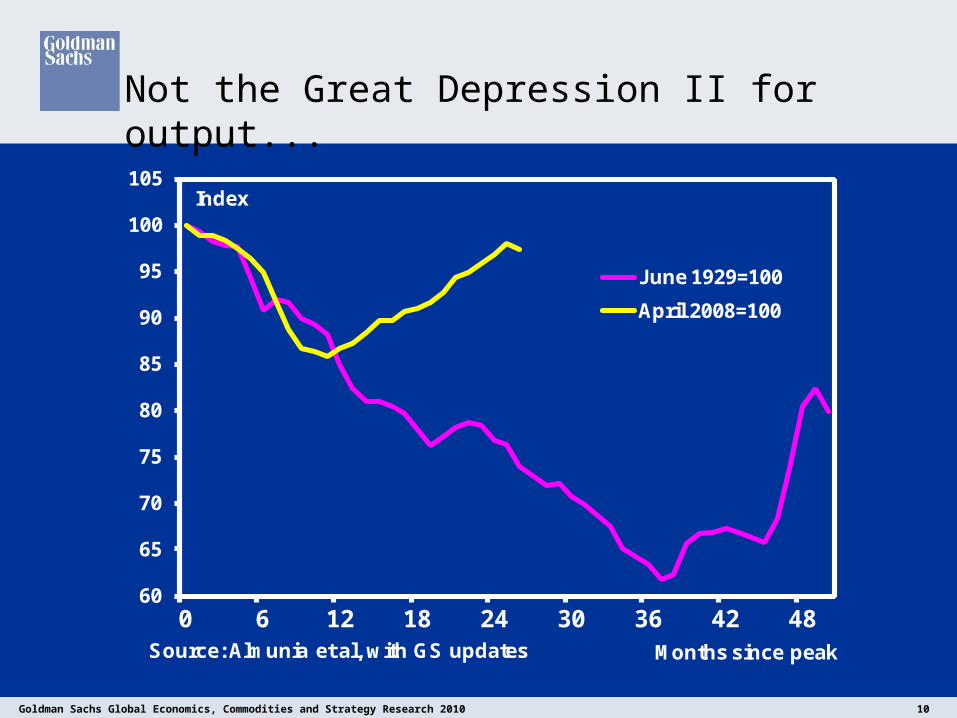

Not the Great Depression II for output...

60

65

70

75

80

85

90

95

100

105

0 6 12 18 24 30 36 42 48

Index

June 1929=100

April 2008=100

Source: Almunia et al, with GS updates Months since peak

Goldman Sachs Global Economics, Commodities and Strategy Research 2010 11

...or for asset prices

30

40

50

60

70

80

90

100

110

120

0 6 12 18 24 30 36 42 48

Index

June 1929=100

April 2008=100

Source: Almunia et al, with GS updates Months since peak

Goldman Sachs Global Economics, Commodities and Strategy Research 2010 12

Bounce in asset prices has helped banks’ balance sheets

0

2

4

6

8

10

12

14

Italy Spain France Germany UK

Tier I Capital, % RWA

Average 2005-07

2008

2009

Source: Bank of England FSR

Goldman Sachs Global Economics, Commodities and Strategy Research 2010 13

More like other post-war financial crises

78

83

88

93

98

103

108

-5 -4 -3 -2 -1 0 1 2 3 4 5 6

GDPIndex

Source: OECD, GS Global ECS research

FIN

SWEESPJAPNOR

Years from start of crisis

Current cycle includesGS Forecast

UK(current cycle)

Euro-zone(current cycle)

GS F'cast

Goldman Sachs Global Economics, Commodities and Strategy Research 2010 14

Divergence

-6

-4

-2

0

2

4

05 06 07 08 09 10

GDP growth,% yoy

Periphery

Other EMU

Source: National sources, Eurostat

Goldman Sachs Global Economics, Commodities and Strategy Research 2010 15

Partly reflects industrial composition

-25

-20

-15

-10

-5

0

5

10

15

20

00 01 02 03 04 05 06 07 08 09 10

% yoy

Private-sector investment

Private consumption

Goldman Sachs Global Economics, Commodities and Strategy Research 2010 16

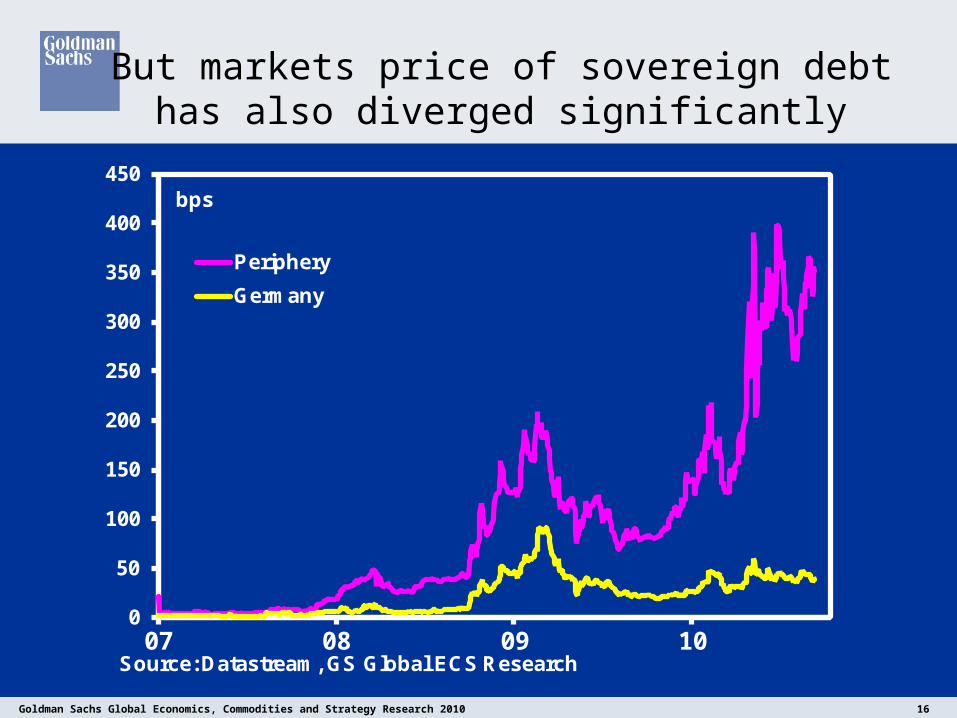

But markets price of sovereign debt has also diverged significantly

0

50

100

150

200

250

300

350

400

450

07 08 09 10

bps

Periphery

Germany

Source: Datastream, GS Global ECS Research

Goldman Sachs Global Economics, Commodities and Strategy Research 2010 17

Spill-over impact on banks’ funding costs

0

50

100

150

200

250

Nov-07 May-08 Nov-08 May-09 Nov-09 May-10

5-yr CDS Spread,bps

Weighted ave. of European SovereignsiTraxx Senior European Financials

Source: GS Global ECS Research, Datastream

Goldman Sachs Global Economics, Commodities and Strategy Research 2010 18

Divergence follows years of convergence

7

8

9

10

11

12

13

14

15

13

15

17

19

21

23

25

27

80 83 86 89 92 95 98 01 04 07 10

Other EMU

Periphery

Source: National sources, Eurostat

Real GDP Level ('000 EUR per capita)

Goldman Sachs Global Economics, Commodities and Strategy Research 2010 19

No evidence EMU deepened trade integration

13

14

15

16

17

18

19

20

21

22

23

18

20

22

24

26

28

30

32

34

91 93 95 97 99 01 03 05 07 09

%, GDP

World Exports (lhs)

Intra Euroland (rhs)

Source: Eurostat, IMF, GS Calculations.

(Trade shares)

Goldman Sachs Global Economics, Commodities and Strategy Research 2010 20

But it did help compress bond yields

2

4

6

8

10

12

14

16

18

80 82 84 86 88 90 92 94 96 98 00 02 04 06 08 10

%German 10-yr yields

Weighted ave. 10-yr yield (Periphery)

Source: National sources, Eurostat

Goldman Sachs Global Economics, Commodities and Strategy Research 2010 21

And as income converged, current accounts diverged

-15

-10

-5

0

5

10

95 96 97 98 99 00 01 02 03 04 05 06 07 08

% of GDP

Germany France Italy Spain

Greece Ireland Portugal

Source: Haver Analytics and GS Global ECS Research

Current Account

Goldman Sachs Global Economics, Commodities and Strategy Research 2010 22

Low rates encourage domestic demand

0

10

20

30

40

50

60

-4

-3

-2

-1

0

1

2

3

4

5

6

7

Germany France Spain Italy Greece Ireland Portugal

pp of GDP

Change in gov. expenditure (lhs)

Gov. expenditure (2000)

Gov. expenditure (2008)

Source: OECD and GS Global ECS Research

% of GDP

Goldman Sachs Global Economics, Commodities and Strategy Research 2010 23

Strong demand raises domestic costs

60

70

80

90

100

110

120

14

15

16

17

18

19

20

21

22

85 87 90 92 95 97 00 02 05 07 10

Index (2005=100)% of GDP

Source: IMF, the Spanish Statistical Office and GS Global ECS Research

Real Effective Exchange Rate (ULC, rhs)

Government Consumption(lagged 4q)

Goldman Sachs Global Economics, Commodities and Strategy Research 2010 24

…causing declines in the periphery’s export market shares

70

75

80

85

90

95

100

105

110

00 01 02 03 04 05 06 07 08

Index (2000 =100)

GermanySpainPortugalFranceItalyGreece

Source: IMF

Export Market Shares (Volume Index)

Goldman Sachs Global Economics, Commodities and Strategy Research 2010 25

And sharp deteriorations in external positions

-120

-100

-80

-60

-40

-20

0

20

40

Portugal Spain Greece Ireland Italy France Germany

% of GDP

2000 2008

Source: Haver Analytics and GS Global ECS Research

Net International Investment Position

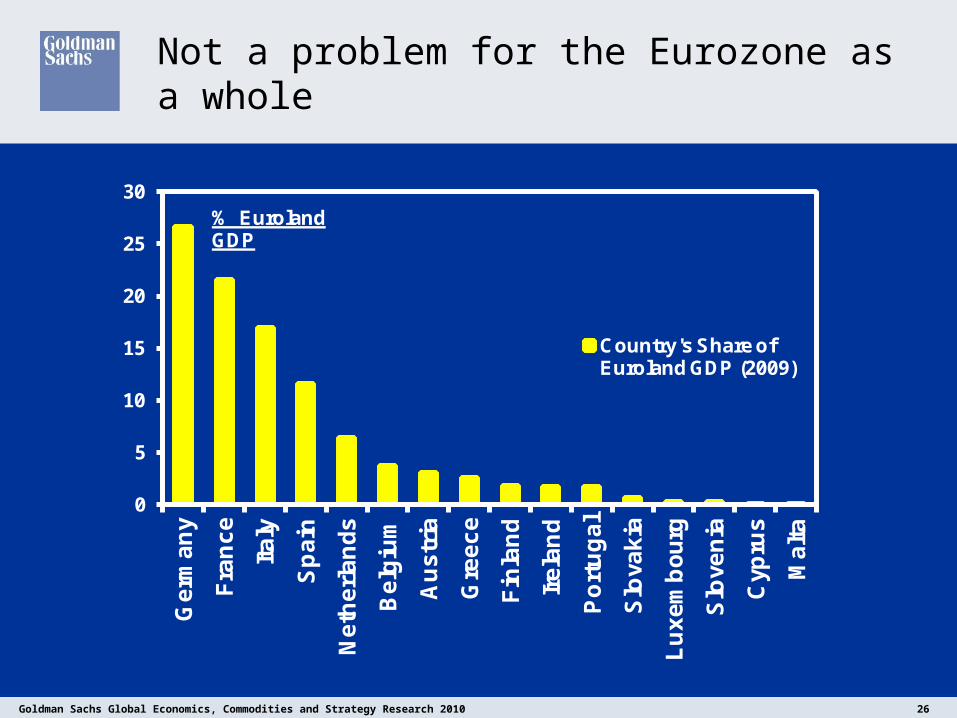

Goldman Sachs Global Economics, Commodities and Strategy Research 2010 26

Not a problem for the Eurozone as a whole

0

5

10

15

20

25

30G

erm

an

y

Fra

nc

e

Ita

ly

Sp

ain

Ne

the

rla

nd

s

Be

lgiu

m

Au

str

ia

Gre

ec

e

Fin

lan

d

Ire

lan

d

Po

rtu

ga

l

Slo

vak

ia

Lu

xe

mb

ou

rg

Slo

ven

ia

Cyp

rus

Ma

lta

% Euroland GDP

Country's Share of Euroland GDP (2009)

Goldman Sachs Global Economics, Commodities and Strategy Research 2010 27

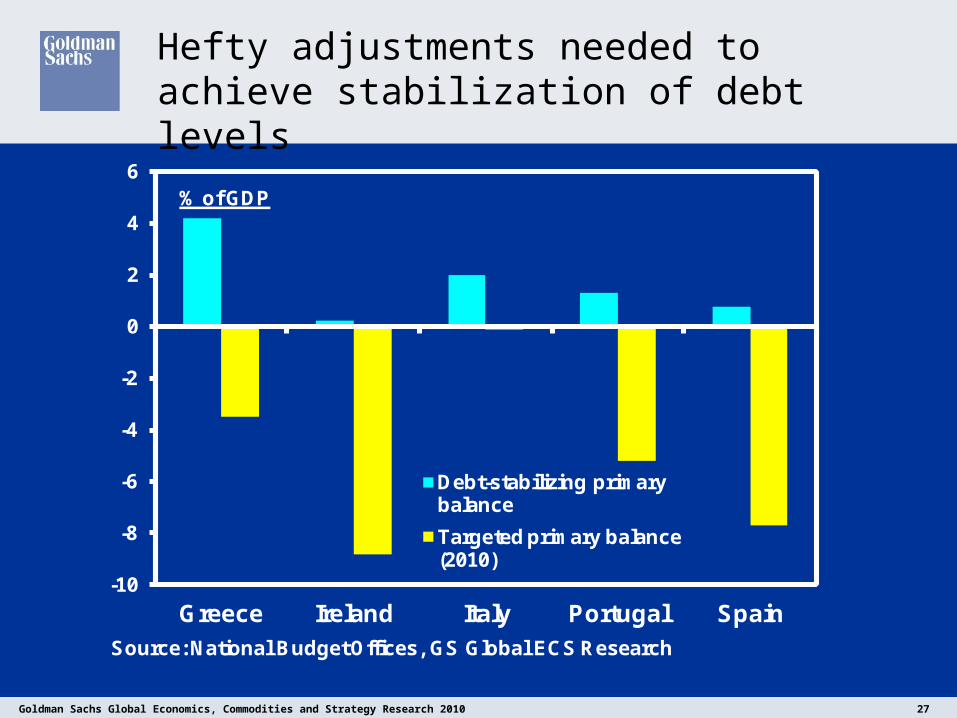

Hefty adjustments needed to achieve stabilization of debt levels

-10

-8

-6

-4

-2

0

2

4

6

Greece Ireland Italy Portugal Spain

% of GDP

Debt-stabilizing primary balance

Targeted primary balance (2010)

Source: National Budget Offices, GS Global ECS Research

Goldman Sachs Global Economics, Commodities and Strategy Research 2010 28

Decline in interest rates not restricted to the Eurozone

0

1

2

3

4

5

6

7

1750 1775 1800 1825 1850 1875 1900 1925 1950 1975 2000

Real ex ante consol rate, %

Source: BoE, GS calculations

Avg. since 1700

Goldman Sachs Global Economics, Commodities and Strategy Research 2010 29

Reform: The options

Nothing: let countries restructure (if they have to)

Piecemeal: More support/control ex post (EFSF plus EC intervention); tighter standards ex ante (Van Rompouy)

Wholesale: Full fiscal federalism (note US example: political union precedes monetary union).

Euro break-up

Goldman Sachs Global Economics, Commodities and Strategy Research 2010 30

Macro rebalancing

Keynes (Bretton Woods, 1946):

“the process of adjustment is compulsory for the debtor and voluntary for the creditor. If the creditor does not choose to make, or allow, his share of the adjustment, he suffers no inconvenience. For whilst a country’s reserve cannot fall below zero, there is no ceiling which sets an upper limit”.

Goldman Sachs Global Economics, Commodities and Strategy Research 2010 31

Disclaimer

I, Ben Broadbent, hereby certify that all of the views expressed in this report accurately reflect personal views, which have not been influenced by considerations of the firm’s business or client relationships.

Global product; distributing entities

The Global Investment Research Division of Goldman Sachs produces and distributes research products for clients of Goldman Sachs, and pursuant to certain contractual arrangements, on a global basis. Analysts based inGoldman Sachs off ices around the w orld produce equity research on industries and companies, and research on macroeconomics, currencies, commodities and portfolio strategy. This research is disseminated in Australiaby Goldman Sachs JBWere Pty Ltd (ABN 21 006 797 897) on behalf of Goldman Sachs; in Canada by Goldman Sachs & Co. regarding Canadian equities and by Goldman Sachs & Co. (all other research); in Hong Kong byGoldman Sachs (Asia) L.L.C.; in India by Goldman Sachs (India) Securities Private Ltd.; in Japan by Goldman Sachs Japan Co., Ltd.; in the Republic of Korea by Goldman Sachs (Asia) L.L.C., Seoul Branch; in New Zealand byGoldman Sachs JBWere (NZ) Limited on behalf of Goldman Sachs; in Russia by OOO Goldman Sachs; in Singapore by Goldman Sachs (Singapore) Pte. (Company Number:1986021

European Union: Goldman Sachs International, authorised and regulated by the Financial Services Authority, has approved this research in connection w ith its distribution in the European Union and United Kingdom;Goldman, Sachs & Co. oHG, regulated by the Bundesanstalt für Finanzdienstleistungsaufsicht, may also distribute research in Germany.

General disclosuresThis research is for our clients only. Other than disclosures relating to Goldman Sachs, this research is based on current public information that w e consider reliable, but w e do not represent it is accurate or complete, and itshould not be relied on as such. We seek to update our research as appropriate, but various regulations may prevent us from doing so. Other than certain industry reports published on a periodic basis, the large majority ofreports are published at irregular intervals as appropriate in the analyst's judgment.

Goldman Sachs conducts a global full-service, integrated investment banking, investment management, and brokerage business. We have investment banking and other business relationships w ith a substantial percentage ofthe companies covered by our Global Investment Research Division. SIPC: Goldman, Sachs & Co., the United States broker dealer, is a member of SIPC (http://w w w .sipc.org).

Our salespeople, traders, and other professionals may provide oral or w ritten market commentary or trading strategies to our clients and our proprietary trading desks that reflect opinions that are contrary to the opinionsexpressed in this research. Our asset management area, our proprietary trading desks and investing businesses may make investment decisions that are inconsistent w ith the recommendations or view s expressed in thisresearch.

We and our aff iliates, off icers, directors, and employees, excluding equity and credit analysts, w ill from time to time have long or short positions in, act as principal in, and buy or sell, the securities or derivatives, if any,referred to in this research. This research is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction w here such an offer or solicitation w ould be illegal. It does not constitute a personal recommendation or take into accountthe particular investment objectives, f inancial situations, or needs of individual clients. Clients should consider w hether any advice or recommendation in this research is suitable for their particular circumstances and, ifappropriate, seek professional advice, including tax advice. The price and value of investments referred to in this research and the income from them may fluctuate. Past performance is not a guide to future performance,future returns are not guaranteed, and a loss of original capital may occur. Fluctuations in exchange rates could have adverse effects on the value or price of, or income derived from, certain investments.

Certain transactions, including those involving futures, options, and other derivatives, give rise to substantial risk and are not suitable for all investors. Investors should review current options disclosure documents w hich areavailable from Goldman Sachs sales representatives or at http://w w w .theocc.com/publications/risks/riskchap1.jsp. Transactions cost may be signif icant in option strategies calling for multiple purchase and sales of optionssuch as spreads. Supporting documentation w ill be supplied upon request.

All research reports are disseminated and available to all clients simultaneously through electronic publication to our internal client w ebsites. Not all research content is redistributed to our clients or available to third-partyaggregators, nor is Goldman Sachs responsible for the redistribution of our research by third party aggregators. For all research available on a particular stock, please contact your sales representative or go tow w w .360.gs.com

Disclosure information is also available at http://w w w .gs.com/research/hedge.html or from Research Compliance, 200 West Street, New York, NY 10282.

No part of this material may be (i) copied, photocopied or duplicated in any form by any means or (ii) redistributed w ithout the prior written consent of The Goldman Sachs Group, Inc.

© Copyright 2010, The Goldman Sachs Group, Inc. All Rights Reserved.