Embed Size (px)

Citation preview

GMR INFRASTRUCTURE LTD. BUSINESS OVERVIEW

Nov 2010

1

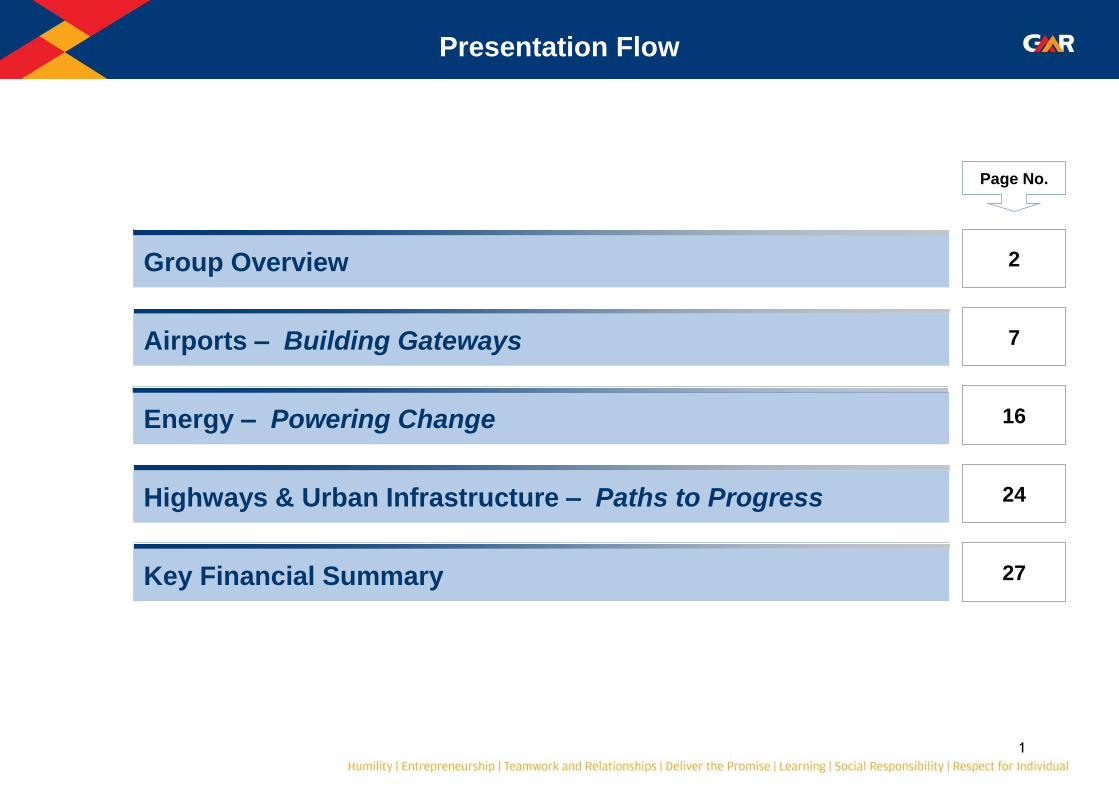

Presentation Flow

Page No.

2 Group Overview

16 Energy – Powering Change

27 Key Financial Summary

24 Highways & Urban Infrastructure – Paths to Progress

7 Airports – Building Gateways

Group Overview

3

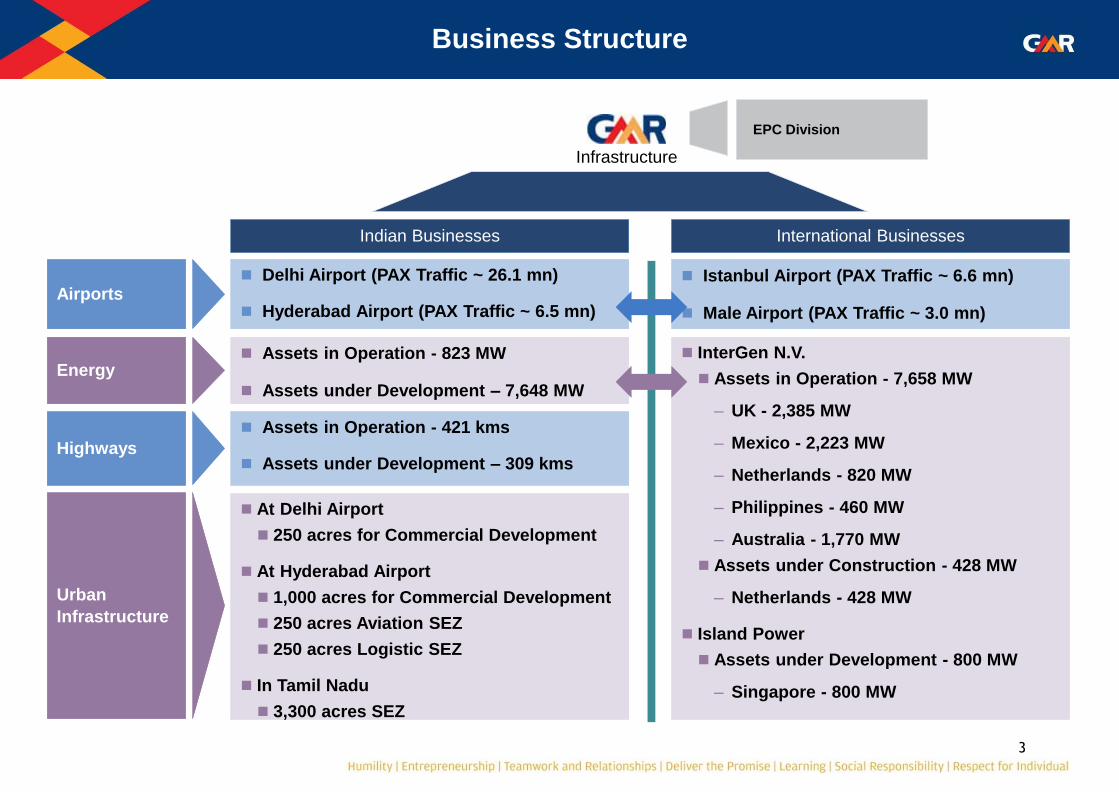

Business Structure

Infrastructure

Indian Businesses International Businesses

InterGen N.V.

Assets in Operation - 7,658 MW

– UK - 2,385 MW

– Mexico - 2,223 MW

– Netherlands - 820 MW

– Philippines - 460 MW

– Australia - 1,770 MW

Assets under Construction - 428 MW

– Netherlands - 428 MW

Island Power

Assets under Development - 800 MW

– Singapore - 800 MW

Airports Istanbul Airport (PAX Traffic ~ 6.6 mn)

Male Airport (PAX Traffic ~ 3.0 mn)

Delhi Airport (PAX Traffic ~ 26.1 mn)

Hyderabad Airport (PAX Traffic ~ 6.5 mn)

Energy Assets in Operation - 823 MW

Assets under Development – 7,648 MW

Highways

Assets in Operation - 421 kms

Assets under Development – 309 kms

Urban

Infrastructure

At Delhi Airport

250 acres for Commercial Development

At Hyderabad Airport

1,000 acres for Commercial Development

250 acres Aviation SEZ

250 acres Logistic SEZ

In Tamil Nadu

3,300 acres SEZ

EPC Division

4

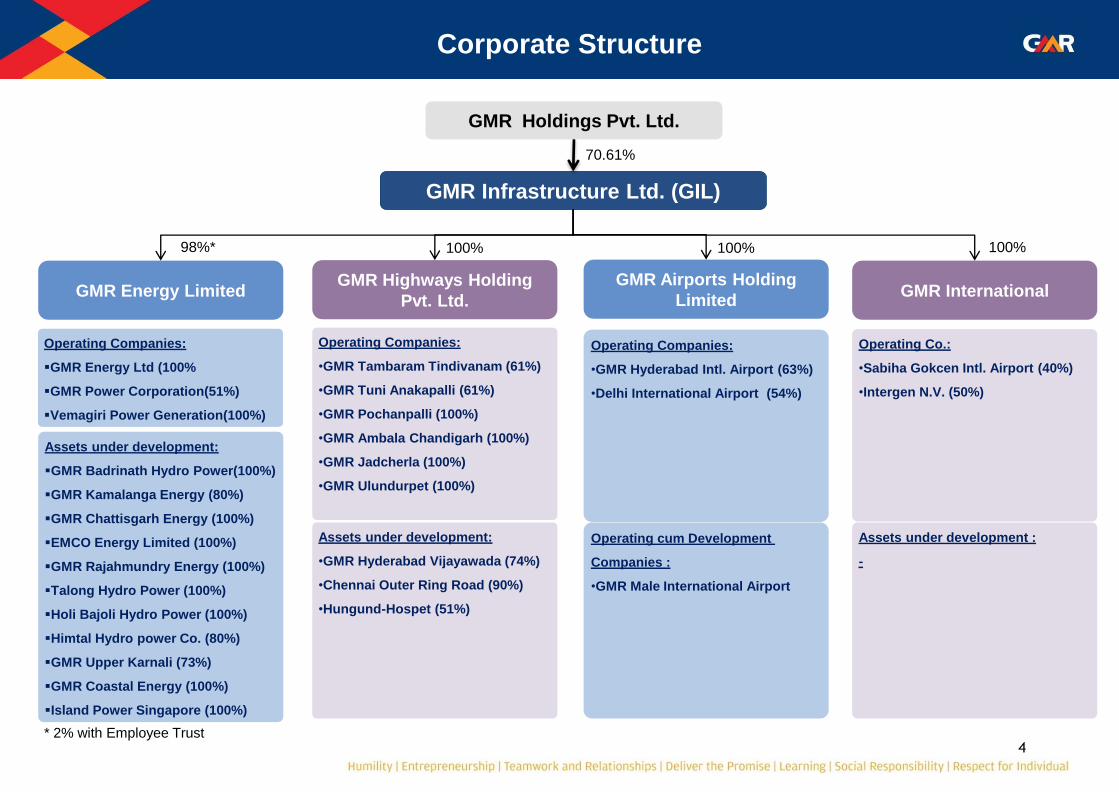

GMR International GMR Airports Holding

Limited

GMR Highways Holding

Pvt. Ltd. GMR Energy Limited

Operating Co.:

•Sabiha Gokcen Intl. Airport (40%)

•Intergen N.V. (50%)

Operating Companies:

•GMR Hyderabad Intl. Airport (63%)

•Delhi International Airport (54%)

Operating Companies:

•GMR Tambaram Tindivanam (61%)

•GMR Tuni Anakapalli (61%)

•GMR Pochanpalli (100%)

•GMR Ambala Chandigarh (100%)

•GMR Jadcherla (100%)

•GMR Ulundurpet (100%)

Corporate Structure

GMR Infrastructure Ltd. (GIL)

GMR Holdings Pvt. Ltd.

98%* 100% 100% 100%

Assets under development:

GMR Badrinath Hydro Power(100%)

GMR Kamalanga Energy (80%)

GMR Chattisgarh Energy (100%)

EMCO Energy Limited (100%)

GMR Rajahmundry Energy (100%)

Talong Hydro Power (100%)

Holi Bajoli Hydro Power (100%)

Himtal Hydro power Co. (80%)

GMR Upper Karnali (73%)

GMR Coastal Energy (100%)

Island Power Singapore (100%)

Assets under development:

•GMR Hyderabad Vijayawada (74%)

•Chennai Outer Ring Road (90%)

•Hungund-Hospet (51%)

Operating cum Development

Companies :

•GMR Male International Airport

Assets under development :

-

70.61%

* 2% with Employee Trust

Operating Companies:

GMR Energy Ltd (100%

GMR Power Corporation(51%)

Vemagiri Power Generation(100%)

5

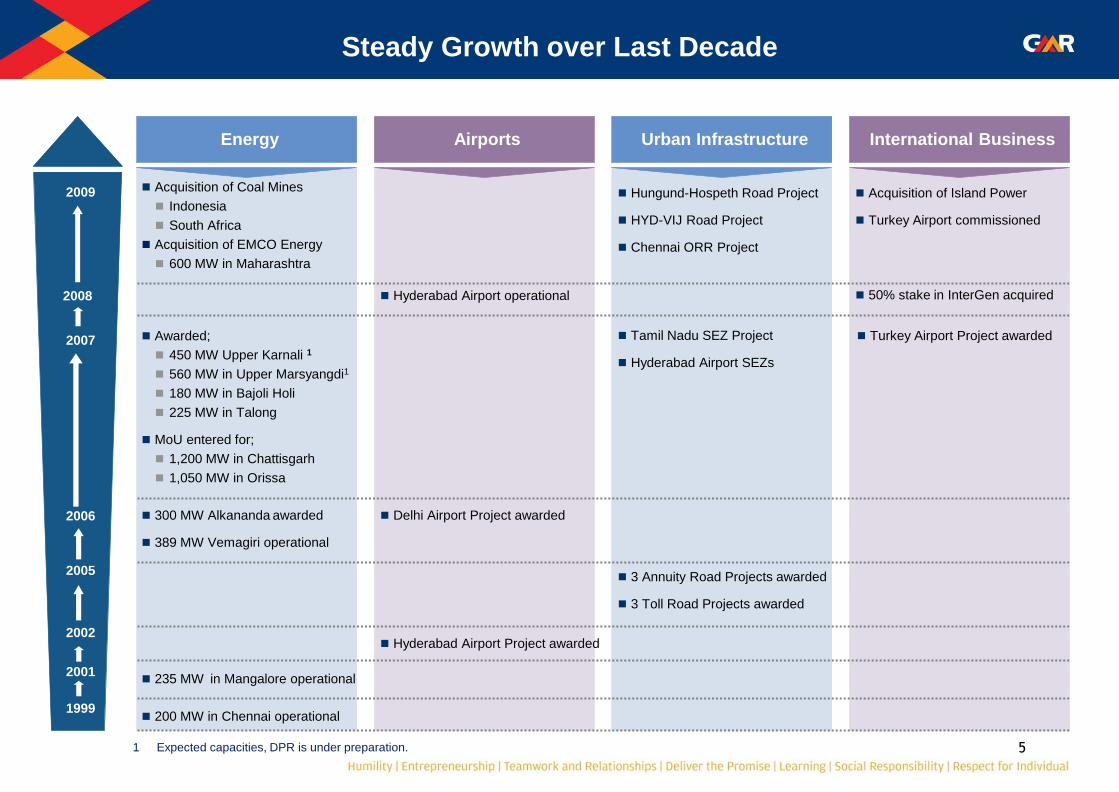

Steady Growth over Last Decade

1 Expected capacities, DPR is under preparation.

Airports

Hyderabad Airport Project awarded

Energy

200 MW in Chennai operational

235 MW in Mangalore operational

Delhi Airport Project awarded 300 MW Alkananda awarded

389 MW Vemagiri operational

Acquisition of Coal Mines

Indonesia

South Africa

Acquisition of EMCO Energy

600 MW in Maharashtra

Urban Infrastructure

3 Annuity Road Projects awarded

3 Toll Road Projects awarded

Hungund-Hospeth Road Project

HYD-VIJ Road Project

Chennai ORR Project

International Business

Awarded;

450 MW Upper Karnali 1

560 MW in Upper Marsyangdi1

180 MW in Bajoli Holi

225 MW in Talong

MoU entered for;

1,200 MW in Chattisgarh

1,050 MW in Orissa

Tamil Nadu SEZ Project

Hyderabad Airport SEZs

Turkey Airport Project awarded

Hyderabad Airport operational 50% stake in InterGen acquired

Acquisition of Island Power

Turkey Airport commissioned

2007

2006

2002

1999

2001

2005

2008

2009

6

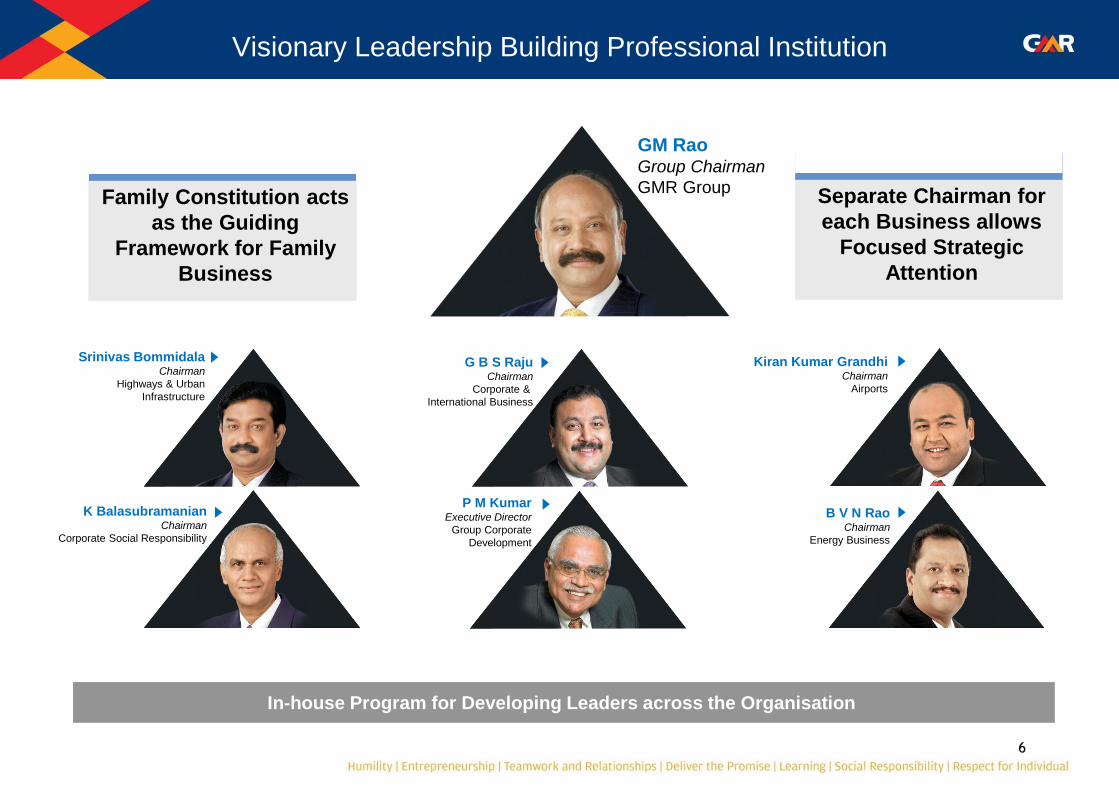

Visionary Leadership Building Professional Institution

GM Rao Group Chairman

GMR Group

Srinivas Bommidala Chairman

Highways & Urban

Infrastructure

K Balasubramanian Chairman

Corporate Social Responsibility

B V N Rao Chairman

Energy Business

Kiran Kumar Grandhi Chairman

Airports

P M Kumar Executive Director

Group Corporate

Development

G B S Raju Chairman

Corporate &

International Business

In-house Program for Developing Leaders across the Organisation

Family Constitution acts

as the Guiding

Framework for Family

Business

Separate Chairman for

each Business allows

Focused Strategic

Attention

Airports – Building Gateways

8

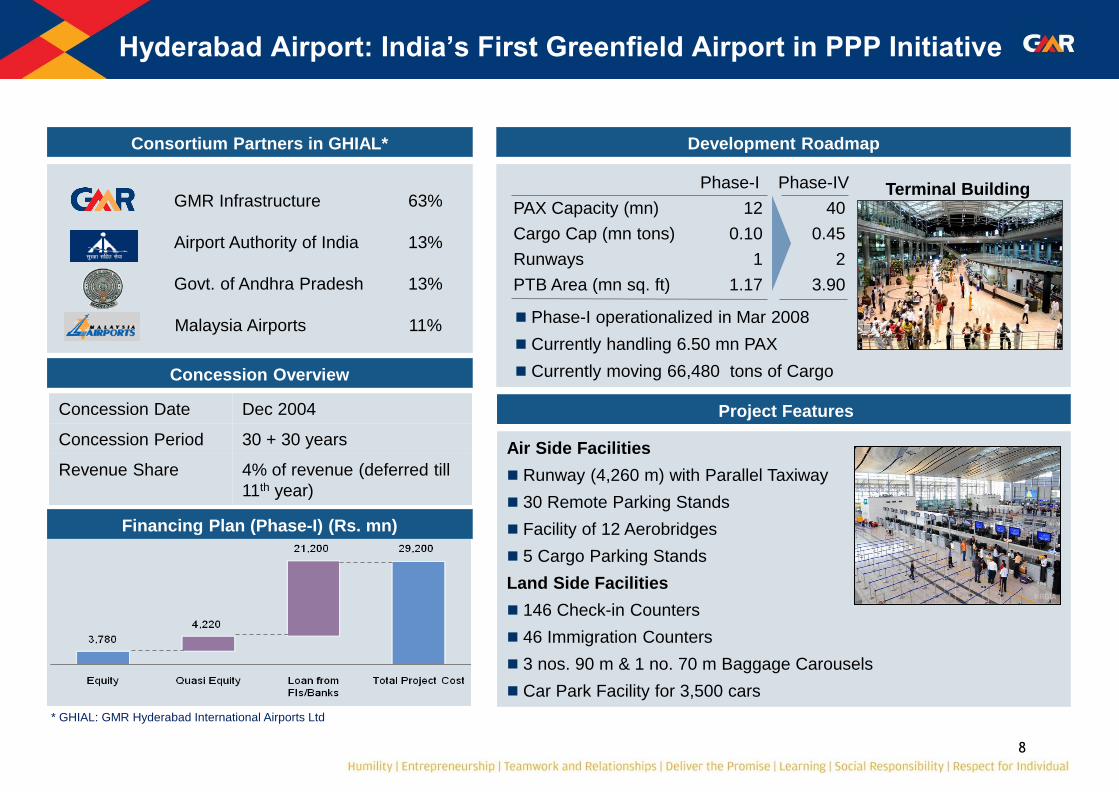

Concession Date Dec 2004

Concession Period 30 + 30 years

Revenue Share 4% of revenue (deferred till

11th year)

Hyderabad Airport: India’s First Greenfield Airport in PPP Initiative

Consortium Partners in GHIAL*

Project Features

Air Side Facilities

Runway (4,260 m) with Parallel Taxiway

30 Remote Parking Stands

Facility of 12 Aerobridges

5 Cargo Parking Stands

Land Side Facilities

146 Check-in Counters

46 Immigration Counters

3 nos. 90 m & 1 no. 70 m Baggage Carousels

Car Park Facility for 3,500 cars

Financing Plan (Phase-I) (Rs. mn)

Development Roadmap

Terminal Building

Phase-I operationalized in Mar 2008

Currently handling 6.50 mn PAX

Currently moving 66,480 tons of Cargo

Concession Overview

Phase-I Phase-IV

PAX Capacity (mn) 12 40

Cargo Cap (mn tons) 0.10 0.45

Runways 1 2

PTB Area (mn sq. ft) 1.17 3.90

GMR Infrastructure 63%

Airport Authority of India 13%

Govt. of Andhra Pradesh 13%

Malaysia Airports 11%

* GHIAL: GMR Hyderabad International Airports Ltd

9

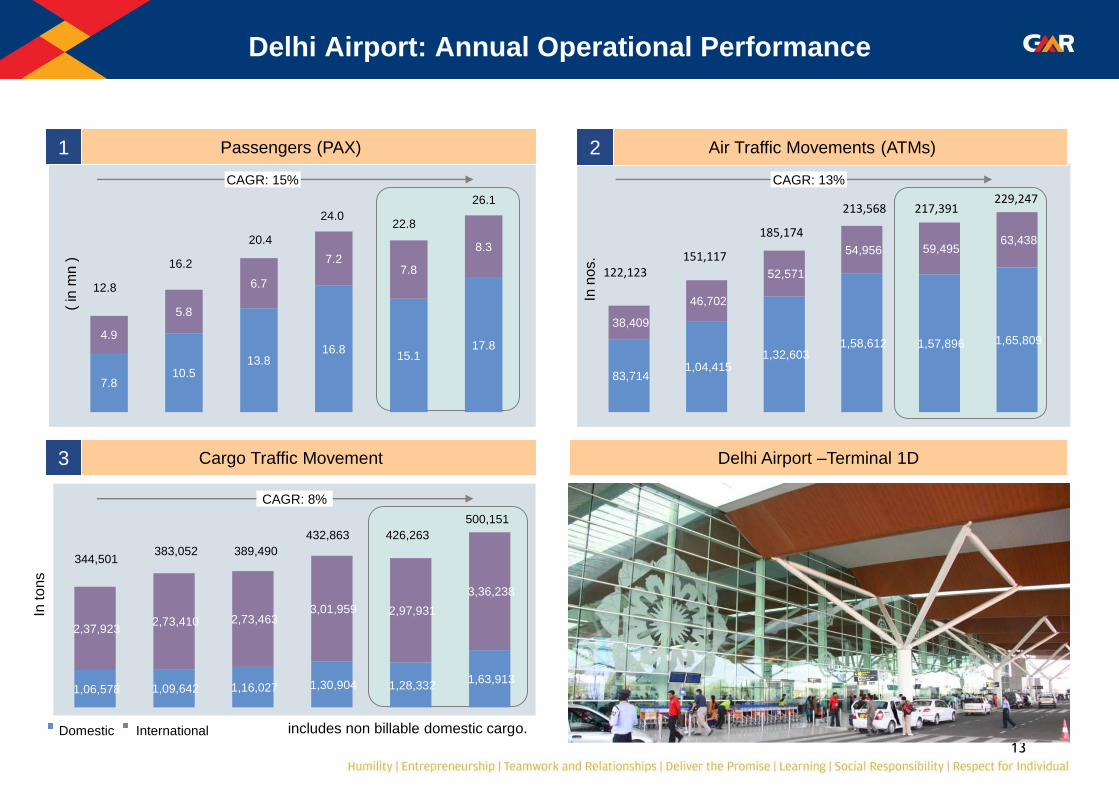

19835 18812 22973 27119 23923 29361

13952 17459

23438 24059 33314

37119

30139 43016

59894 70980 68762 66899 7352

9155

9719

10992 12077 13557

2.1 3.04

4.57 5.52

4.65 4.8 0.75

1.00

1.21

1.43 1.57 1.69

Hyderabad Airport: Annual Operational Performance

CAGR: 19.7%

(in m

n)

CAGR: 18.1%

(in n

os.)

CAGR: 14.3%

Cargo Traffic Movement

Air Traffic Movements (ATMs) Passengers (PAX)

3

2 1

Hyderabad Airport

(in

tons)

2.85

4.04

5.78

6.95 6.22

37,491

52,171

69,613

81,972 80,456

33787 36271

46411 51178

66480

6.49

80,839

57237

FY05 FY06 FY07 FY08 FY09 FY10 FY05 FY06 FY07 FY08 FY09 FY10

FY05 FY06 FY07 FY08 FY09 FY10

Domestic International

10

Hyderabad Airport: 1,500 Acres of Property Development

Superior connectivity of Airport with City to further enhance the value of land

11.4 km 4 lane Elevated Expressway operational from Oct 2009 – reducing time taken to reach the city centre to 45min

Outer Ring Road Phase-I operational - reducing time taken to reach IT District (HiTech City) to 30min

Enhanced connectivity with completion of Metro Lines planned in future

Healthport

(~25 Acres)

Multi-Specialty Hospital focused on medical tourism as the anchor

Research & Clinical Trial Facilities

Medical education and training facilities

Funport

(~145 Acres)

Amusement Park with Destination Retail and Multi Purpose Arena as the

anchor

Discussion with leading global and Indian players in entertainment and sporting

events and content provision

Commercial

District

(~ 75 Acres)

Convention Centre cum Exhibition Facility as the anchor

Office Space, Hotels, Restaurants & supporting Retail facilities

Discussions with leading international convention and exhibition organization

Eduport

(~40 Acres)

International Business Institution and an International School as anchors

Supporting Retail and Sports Facility

Discussions currently in progress with leading global and Indian business

schools

Creating a theme-based, anchor-led mixed-use Airport City with Phase-I being 275 acres

11

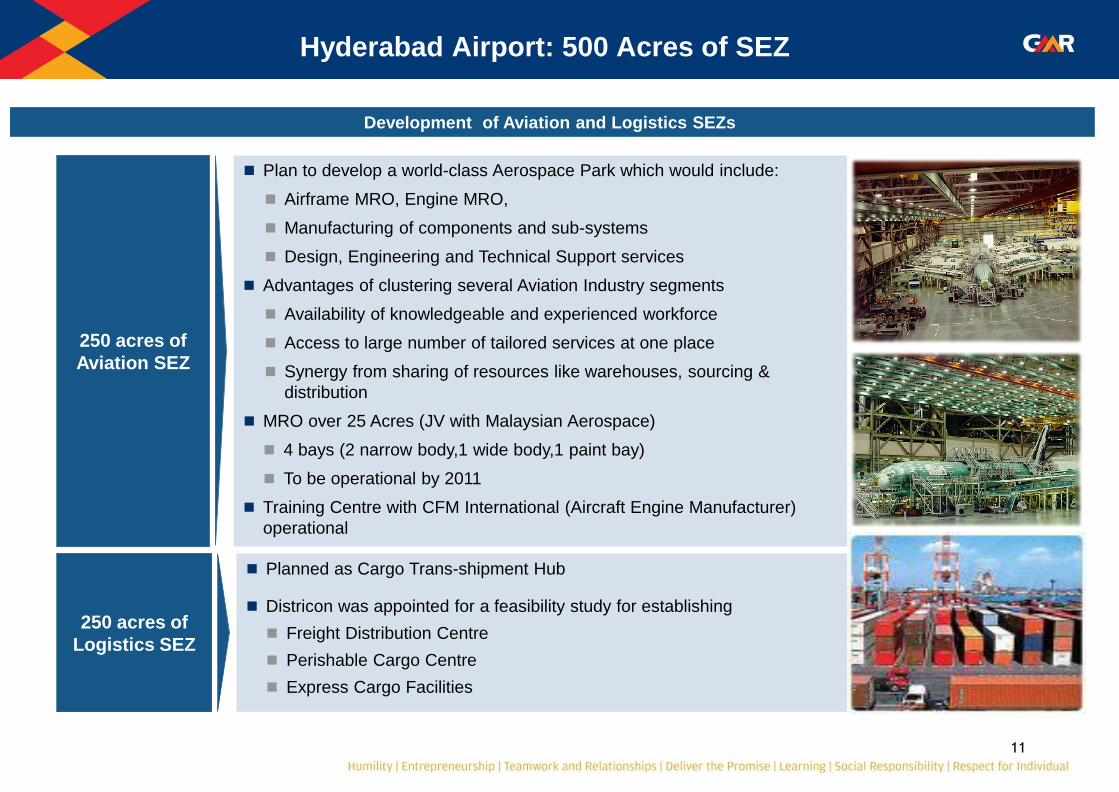

Hyderabad Airport: 500 Acres of SEZ

250 acres of

Aviation SEZ

Plan to develop a world-class Aerospace Park which would include:

Airframe MRO, Engine MRO,

Manufacturing of components and sub-systems

Design, Engineering and Technical Support services

Advantages of clustering several Aviation Industry segments

Availability of knowledgeable and experienced workforce

Access to large number of tailored services at one place

Synergy from sharing of resources like warehouses, sourcing &

distribution

MRO over 25 Acres (JV with Malaysian Aerospace)

4 bays (2 narrow body,1 wide body,1 paint bay)

To be operational by 2011

Training Centre with CFM International (Aircraft Engine Manufacturer)

operational

250 acres of

Logistics SEZ

Planned as Cargo Trans-shipment Hub

Districon was appointed for a feasibility study for establishing

Freight Distribution Centre

Perishable Cargo Centre

Express Cargo Facilities

Development of Aviation and Logistics SEZs

12

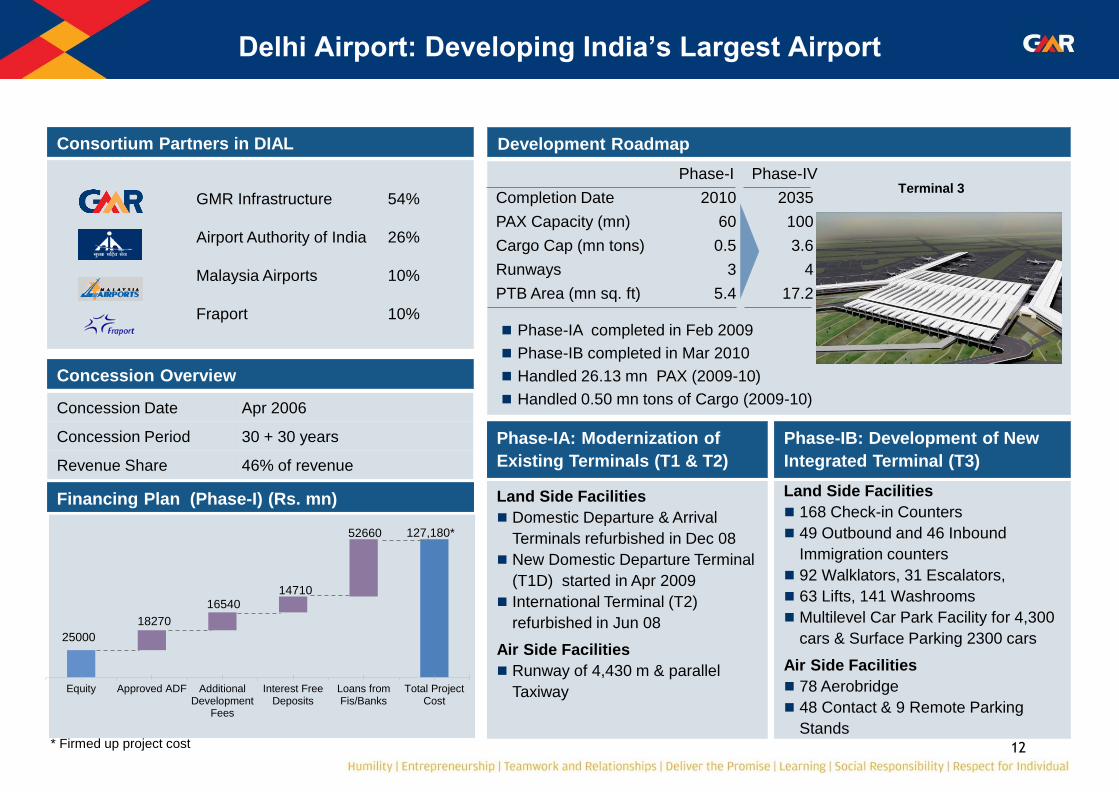

Phase-I Phase-IV

Completion Date 2010 2035

PAX Capacity (mn) 60 100

Cargo Cap (mn tons) 0.5 3.6

Runways 3 4

PTB Area (mn sq. ft) 5.4 17.2

GMR Infrastructure 54%

Airport Authority of India 26%

Malaysia Airports 10%

Fraport 10%

Delhi Airport: Developing India’s Largest Airport

Consortium Partners in DIAL

Financing Plan (Phase-I) (Rs. mn)

Development Roadmap

Concession Overview

Phase-IB: Development of New

Integrated Terminal (T3)

Phase-IA: Modernization of

Existing Terminals (T1 & T2)

Land Side Facilities

168 Check-in Counters

49 Outbound and 46 Inbound

Immigration counters

92 Walklators, 31 Escalators,

63 Lifts, 141 Washrooms

Multilevel Car Park Facility for 4,300

cars & Surface Parking 2300 cars

Air Side Facilities

78 Aerobridge

48 Contact & 9 Remote Parking

Stands

Land Side Facilities

Domestic Departure & Arrival

Terminals refurbished in Dec 08

New Domestic Departure Terminal

(T1D) started in Apr 2009

International Terminal (T2)

refurbished in Jun 08

Air Side Facilities

Runway of 4,430 m & parallel

Taxiway

Terminal 3

Phase-IA completed in Feb 2009

Phase-IB completed in Mar 2010

Handled 26.13 mn PAX (2009-10)

Handled 0.50 mn tons of Cargo (2009-10) Concession Date Apr 2006

Concession Period 30 + 30 years

Revenue Share 46% of revenue

25000

18270

16540 14710

52660 127,180*

Equity Approved ADF AdditionalDevelopment

Fees

Interest FreeDeposits

Loans fromFis/Banks

Total ProjectCost

* Firmed up project cost

13

Delhi Airport: Annual Operational Performance

Cargo Traffic Movement

Air Traffic Movements (ATMs) Passengers (PAX)

3

2 1

Delhi Airport –Terminal 1D

7.8 10.5

13.8 16.8

15.1 17.8

4.9

5.8

6.7

7.2 7.8

8.3

12.8

16.2

20.4

24.0 22.8

26.1

CAGR: 15%

83,714 1,04,415

1,32,603 1,58,612 1,57,896 1,65,809

38,409

46,702

52,571

54,956 59,495 63,438

122,123 151,117

185,174

213,568 217,391 229,247

CAGR: 13%

( in

mn )

In n

os.

In to

ns

CAGR: 8%

includes non billable domestic cargo.

1,06,578 1,09,642 1,16,027 1,30,904 1,28,332 1,63,913

2,37,923 2,73,410 2,73,463

3,01,959 2,97,931

3,36,238

344,501 383,052 389,490

432,863 426,263

500,151

Domestic International

14

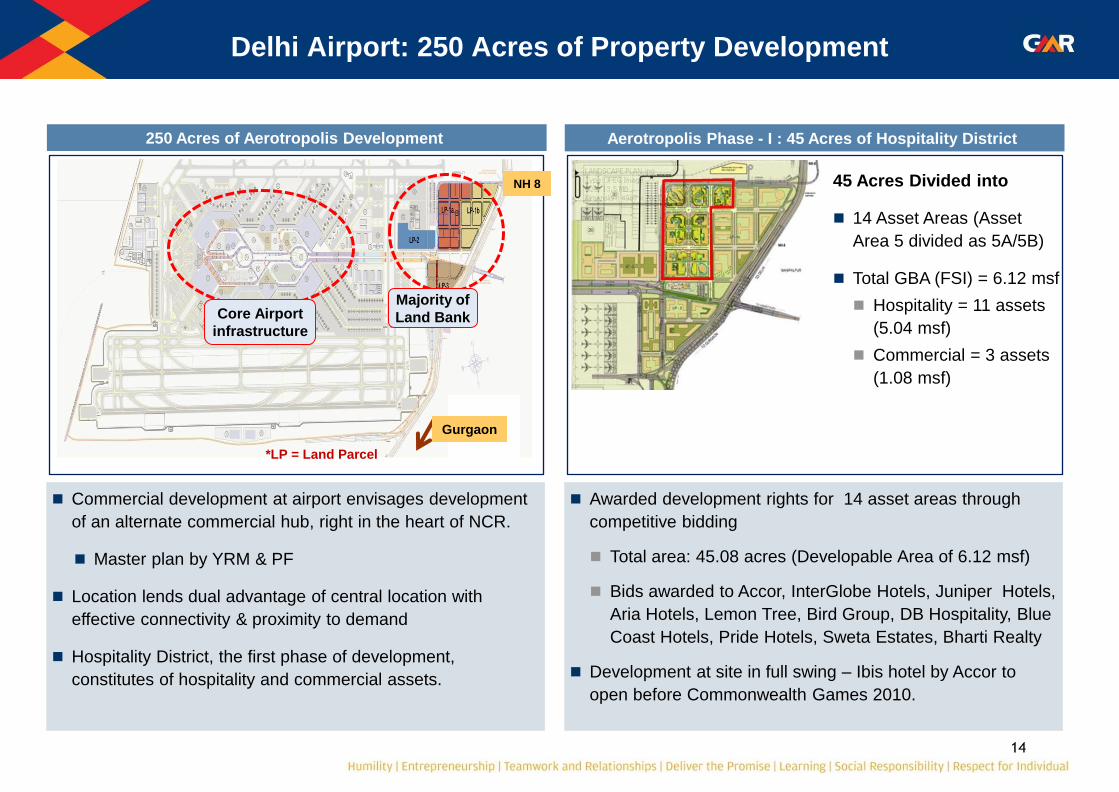

Delhi Airport: 250 Acres of Property Development

250 Acres of Aerotropolis Development Aerotropolis Phase - I : 45 Acres of Hospitality District

45 Acres Divided into

14 Asset Areas (Asset

Area 5 divided as 5A/5B)

Total GBA (FSI) = 6.12 msf

Hospitality = 11 assets

(5.04 msf)

Commercial = 3 assets

(1.08 msf)

Commercial development at airport envisages development

of an alternate commercial hub, right in the heart of NCR.

Master plan by YRM & PF

Location lends dual advantage of central location with

effective connectivity & proximity to demand

Hospitality District, the first phase of development,

constitutes of hospitality and commercial assets.

Awarded development rights for 14 asset areas through

competitive bidding

Total area: 45.08 acres (Developable Area of 6.12 msf)

Bids awarded to Accor, InterGlobe Hotels, Juniper Hotels,

Aria Hotels, Lemon Tree, Bird Group, DB Hospitality, Blue

Coast Hotels, Pride Hotels, Sweta Estates, Bharti Realty

Development at site in full swing – Ibis hotel by Accor to

open before Commonwealth Games 2010.

Majority of

Land Bank Core Airport

infrastructure

NH 8

Gurgaon

*LP = Land Parcel

15

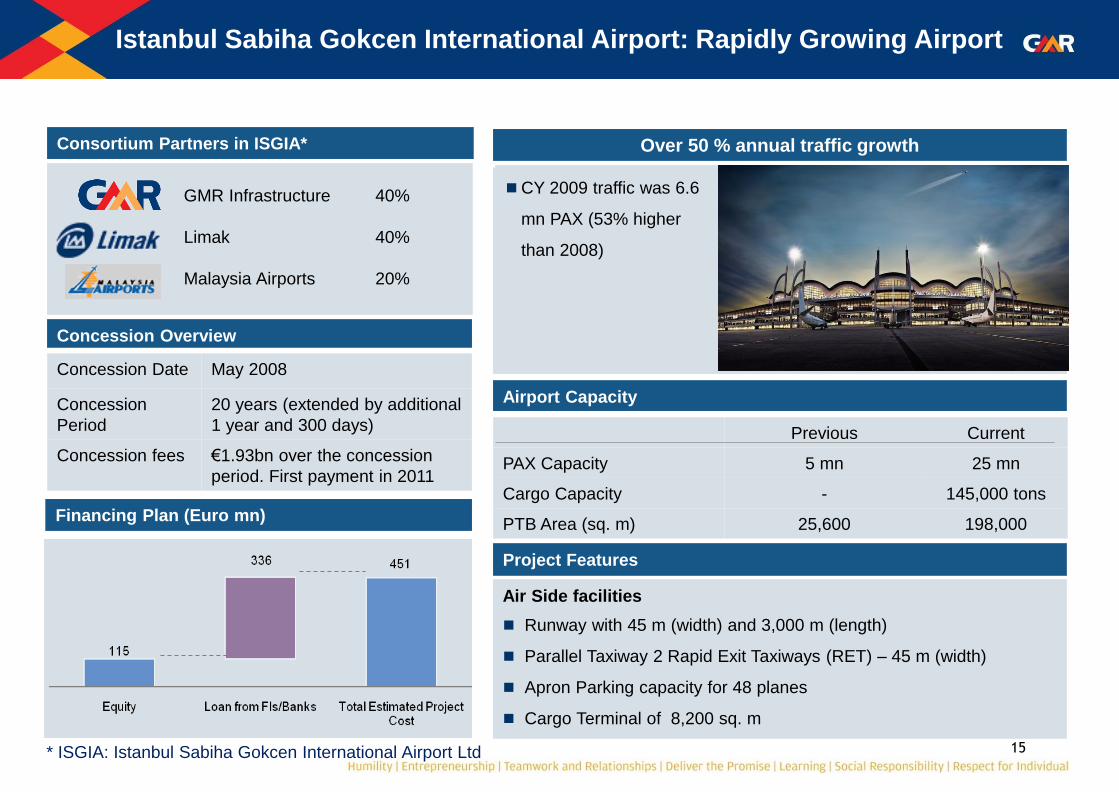

Airport Capacity

Project Features

Air Side facilities

Runway with 45 m (width) and 3,000 m (length)

Parallel Taxiway 2 Rapid Exit Taxiways (RET) – 45 m (width)

Apron Parking capacity for 48 planes

Cargo Terminal of 8,200 sq. m

Istanbul Sabiha Gokcen International Airport: Rapidly Growing Airport

Financing Plan (Euro mn)

Over 50 % annual traffic growth

CY 2009 traffic was 6.6

mn PAX (53% higher

than 2008)

Consortium Partners in ISGIA*

Concession Overview

GMR Infrastructure 40%

Limak 40%

Malaysia Airports 20%

* ISGIA: Istanbul Sabiha Gokcen International Airport Ltd

Concession Date May 2008

Concession

Period

20 years (extended by additional

1 year and 300 days)

Concession fees €1.93bn over the concession

period. First payment in 2011

Previous Current

PAX Capacity 5 mn 25 mn

Cargo Capacity - 145,000 tons

PTB Area (sq. m) 25,600 198,000

16

Airport Capacity

Project Features

Air Side facilities

Runway of 3,200 m with intermediate turnpad at 1,800m from runway

3 connecting taxiways

Apron – 16 Code C stands and 7 Code E stands

Seaplane water runway, jetties and boat pathways

Male International Airport

Financing Plan

High end premium tourist destination

Pax : 3 mn (Est for yr

2010). Achieved 20%+

growth over year 2009

for the first half of the

year

Consortium Partners

Concession Overview

GMR Infrastructure 77%

Malaysia Airports 23%

Concession Date Jan 2011

Concession

Period

25 years (extended by additional

10 years on mutual consent)

Concession fees Upfront : USD 78 mn

Fixed annual : USD 1.5 mn

Previous Current

PAX Capacity 2.6 mn 5.2 mn

Cargo terminal 10000 sq mts

Total est. Project Cost USD 511 mn

ADC of $25 per departing international passenger

from 1st Jan 2012.

17

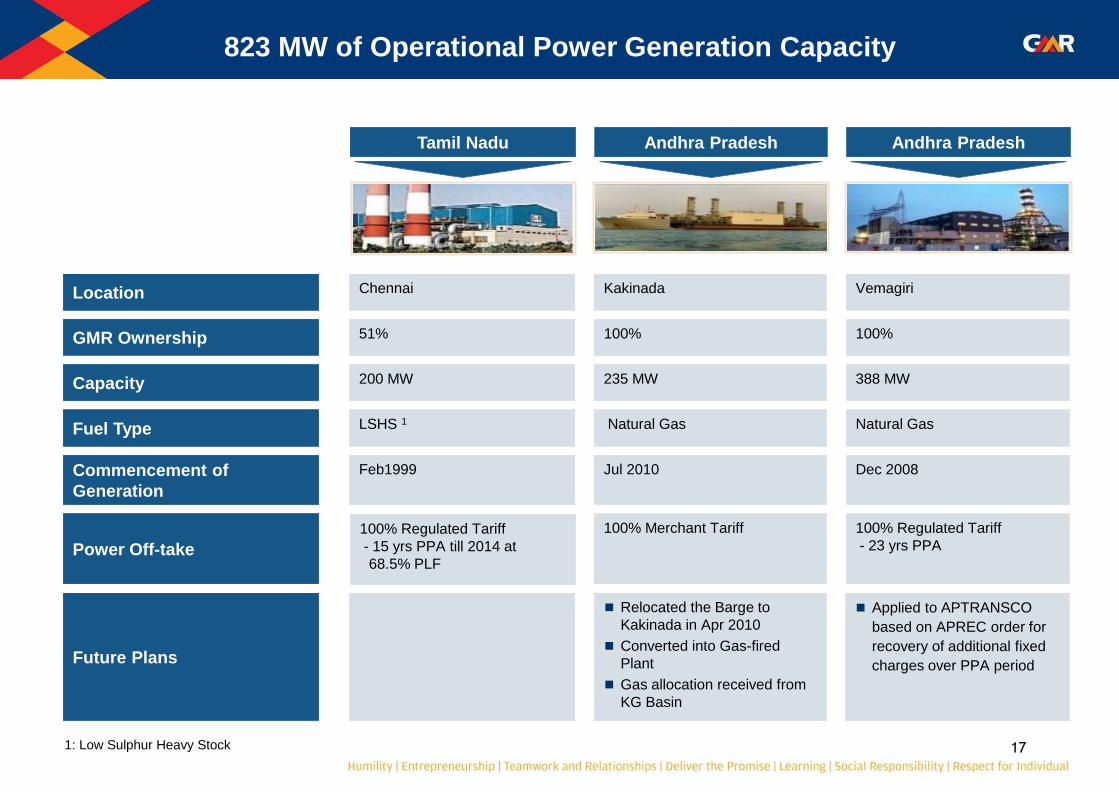

823 MW of Operational Power Generation Capacity

Location

Capacity

Fuel Type

Commencement of

Generation

GMR Ownership

Future Plans

Power Off-take

Andhra Pradesh

Vemagiri

388 MW

Natural Gas

Dec 2008

100%

Applied to APTRANSCO

based on APREC order for

recovery of additional fixed

charges over PPA period

100% Regulated Tariff

- 23 yrs PPA

Tamil Nadu

Chennai

200 MW

LSHS 1

Feb1999

51%

100% Regulated Tariff

- 15 yrs PPA till 2014 at

68.5% PLF

Andhra Pradesh

Kakinada

235 MW

Natural Gas

Jul 2010

100%

Relocated the Barge to

Kakinada in Apr 2010

Converted into Gas-fired

Plant

Gas allocation received from

KG Basin

100% Merchant Tariff

1: Low Sulphur Heavy Stock

Energy – Powering Change

19

823

768

2,000

1,370

1,670

1,840 8,471

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

2009 2012 2013 2014 2015 2016 UltimateCapacity

Well Diversified Power Project Portfolio in India

Project Pipeline (MW)

Balanced

fuel mix

Good portfolio of coal, gas & liquid

fuel and hydro projects

Portfolio approach

to revenue mix

Healthy mix of Merchant and PPA

based projects

Ensuring fuel

security

Acquisition of Coal Mines

(Indonesia and South Africa)

Diversification into

related areas

Power Trading and Transmission

Operational Assets

3 Projects

(823 MW)

Projects under Construction/Development

10 Projects

(7,648 MW)

8,471 MW of power projects spread across the country

Bajoli Holi

Alaknanda

Orissa

Vemagiri

Chennai

Mangalore

Upper Karnali

Upper Marsyangdi

Vemagiri

Expansion

Talong

Emco Energy

Chattisgarh

Financial Year

Madhya

Pradesh

20

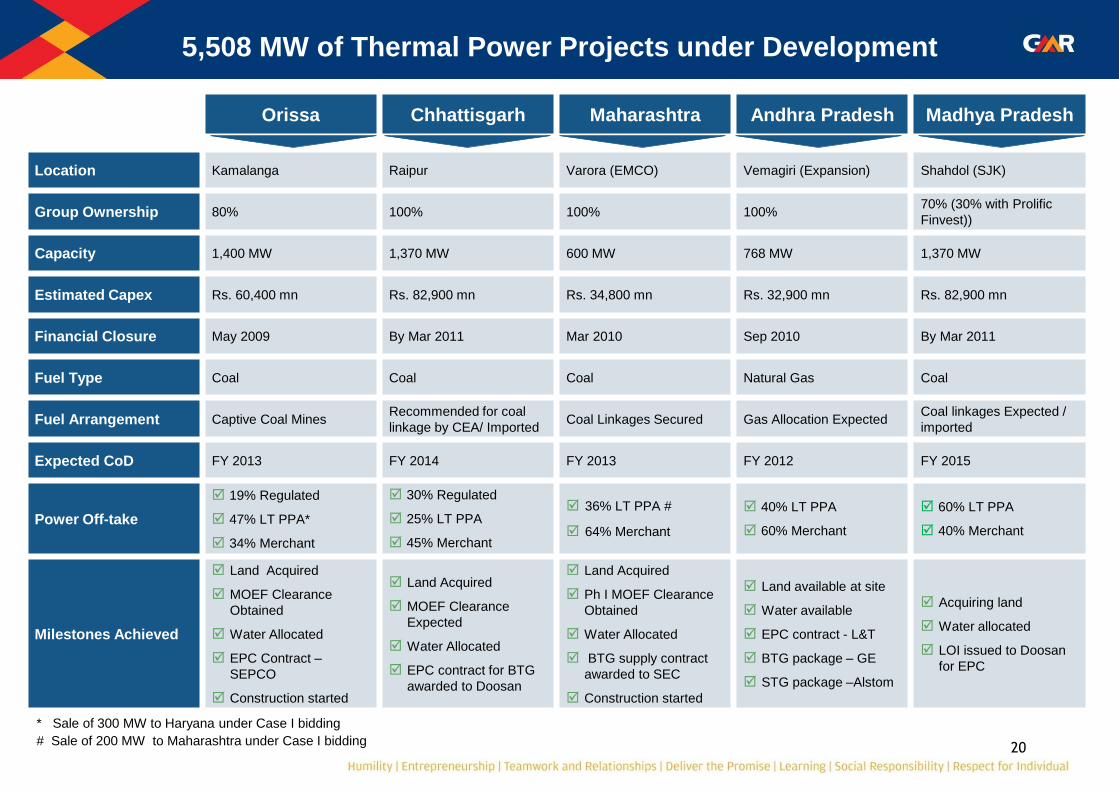

5,508 MW of Thermal Power Projects under Development

* Sale of 300 MW to Haryana under Case I bidding

# Sale of 200 MW to Maharashtra under Case I bidding

Orissa Chhattisgarh Maharashtra Andhra Pradesh Madhya Pradesh

Location Kamalanga Raipur Varora (EMCO) Vemagiri (Expansion) Shahdol (SJK)

Group Ownership 80% 100% 100% 100% 70% (30% with Prolific

Finvest))

Capacity 1,400 MW 1,370 MW 600 MW 768 MW 1,370 MW

Estimated Capex Rs. 60,400 mn Rs. 82,900 mn Rs. 34,800 mn Rs. 32,900 mn Rs. 82,900 mn

Financial Closure May 2009 By Mar 2011 Mar 2010 Sep 2010 By Mar 2011

Fuel Type Coal Coal Coal Natural Gas Coal

Fuel Arrangement Captive Coal Mines Recommended for coal

linkage by CEA/ Imported Coal Linkages Secured Gas Allocation Expected

Coal linkages Expected /

imported

Expected CoD FY 2013 FY 2014 FY 2013 FY 2012 FY 2015

Power Off-take

19% Regulated

47% LT PPA*

34% Merchant

30% Regulated

25% LT PPA

45% Merchant

36% LT PPA #

64% Merchant

40% LT PPA

60% Merchant

60% LT PPA

40% Merchant

Milestones Achieved

Land Acquired

MOEF Clearance

Obtained

Water Allocated

EPC Contract –

SEPCO

Construction started

Land Acquired

MOEF Clearance

Expected

Water Allocated

EPC contract for BTG

awarded to Doosan

Land Acquired

Ph I MOEF Clearance

Obtained

Water Allocated

BTG supply contract

awarded to SEC

Construction started

Land available at site

Water available

EPC contract - L&T

BTG package – GE

STG package –Alstom

Acquiring land

Water allocated

LOI issued to Doosan

for EPC

21

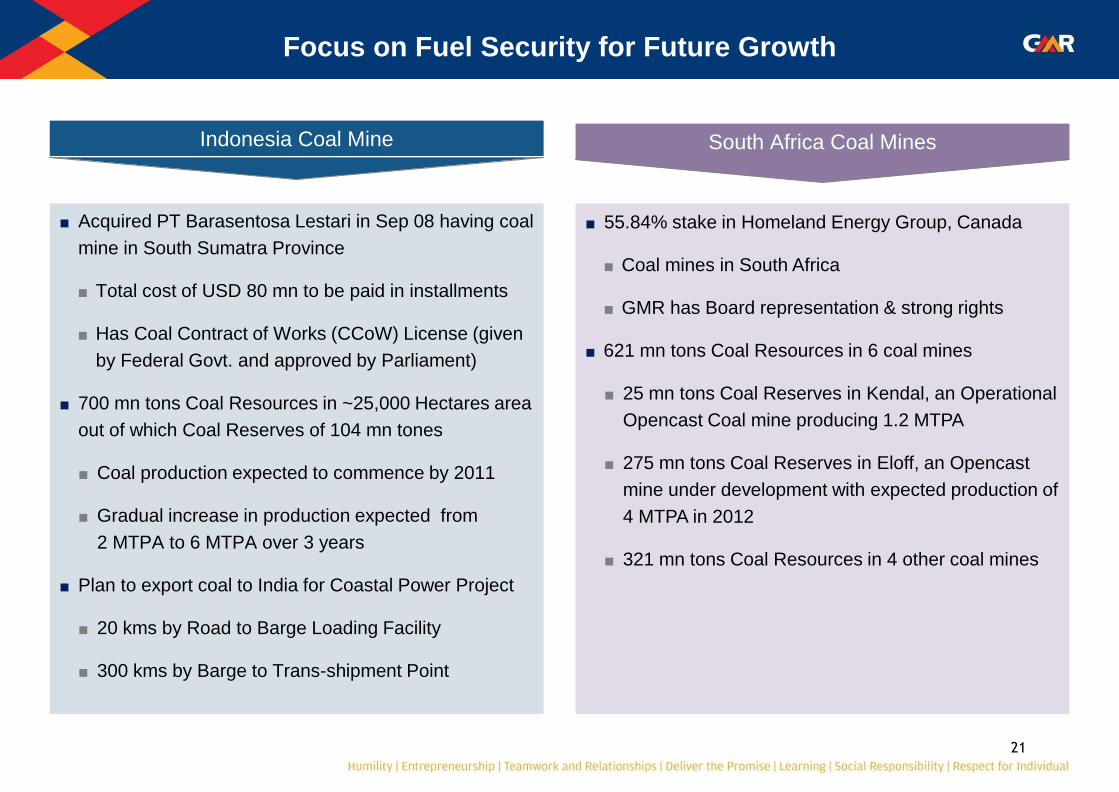

Focus on Fuel Security for Future Growth

■ Acquired PT Barasentosa Lestari in Sep 08 having coal

mine in South Sumatra Province

■ Total cost of USD 80 mn to be paid in installments

■ Has Coal Contract of Works (CCoW) License (given

by Federal Govt. and approved by Parliament)

■ 700 mn tons Coal Resources in ~25,000 Hectares area

out of which Coal Reserves of 104 mn tones

■ Coal production expected to commence by 2011

■ Gradual increase in production expected from

2 MTPA to 6 MTPA over 3 years

■ Plan to export coal to India for Coastal Power Project

■ 20 kms by Road to Barge Loading Facility

■ 300 kms by Barge to Trans-shipment Point

Indonesia Coal Mine South Africa Coal Mines

■ 55.84% stake in Homeland Energy Group, Canada

■ Coal mines in South Africa

■ GMR has Board representation & strong rights

■ 621 mn tons Coal Resources in 6 coal mines

■ 25 mn tons Coal Reserves in Kendal, an Operational

Opencast Coal mine producing 1.2 MTPA

■ 275 mn tons Coal Reserves in Eloff, an Opencast

mine under development with expected production of

4 MTPA in 2012

■ 321 mn tons Coal Resources in 4 other coal mines

22

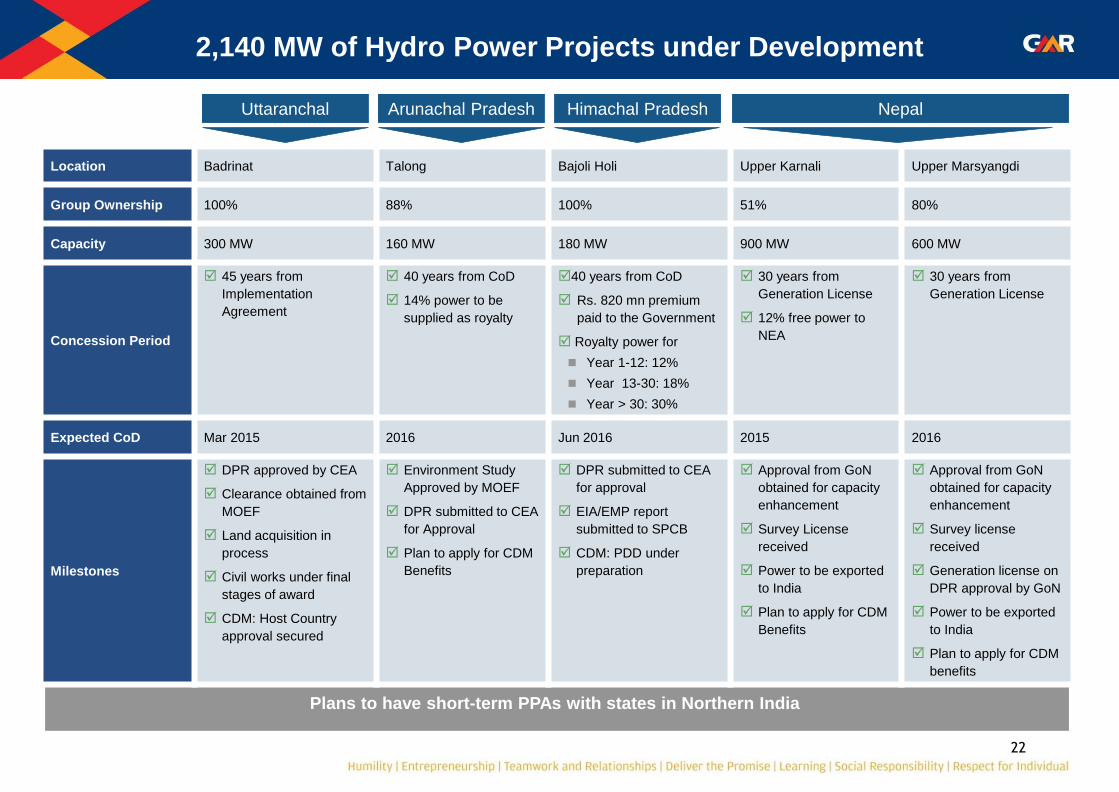

2,140 MW of Hydro Power Projects under Development

Plans to have short-term PPAs with states in Northern India

Uttaranchal Himachal Pradesh Nepal Arunachal Pradesh

Location Badrinat Talong Bajoli Holi Upper Karnali Upper Marsyangdi

Group Ownership 100% 88% 100% 51% 80%

Capacity 300 MW 160 MW 180 MW 900 MW 600 MW

Concession Period

45 years from

Implementation

Agreement

40 years from CoD

14% power to be

supplied as royalty

40 years from CoD

Rs. 820 mn premium

paid to the Government

Royalty power for

Year 1-12: 12%

Year 13-30: 18%

Year > 30: 30%

30 years from

Generation License

12% free power to

NEA

30 years from

Generation License

Expected CoD Mar 2015 2016 Jun 2016 2015 2016

Milestones

DPR approved by CEA

Clearance obtained from

MOEF

Land acquisition in

process

Civil works under final

stages of award

CDM: Host Country

approval secured

Environment Study

Approved by MOEF

DPR submitted to CEA

for Approval

Plan to apply for CDM

Benefits

DPR submitted to CEA

for approval

EIA/EMP report

submitted to SPCB

CDM: PDD under

preparation

Approval from GoN

obtained for capacity

enhancement

Survey License

received

Power to be exported

to India

Plan to apply for CDM

Benefits

Approval from GoN

obtained for capacity

enhancement

Survey license

received

Generation license on

DPR approval by GoN

Power to be exported

to India

Plan to apply for CDM

benefits

23

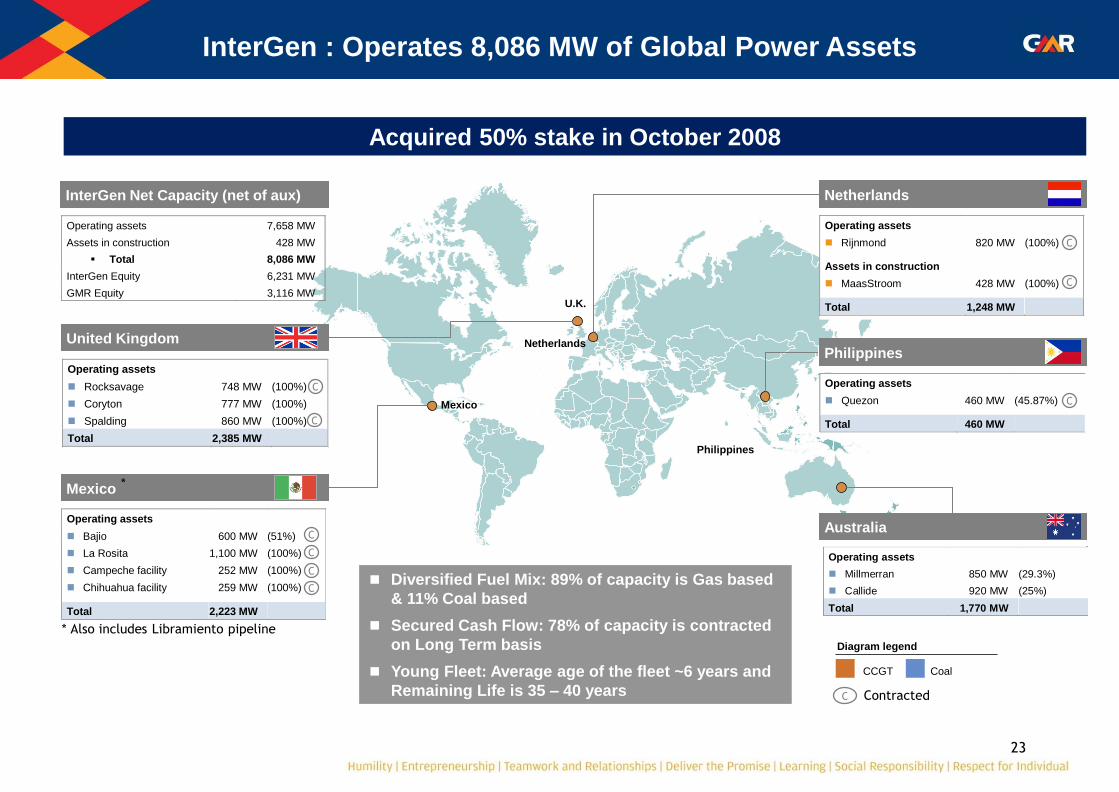

Operating assets

Millmerran 850 MW (29.3%)

Callide 920 MW (25%)

Total 1,770 MW

Operating assets

Rocksavage 748 MW (100%)

Coryton 777 MW (100%)

Spalding 860 MW (100%)

Total 2,385 MW

Operating assets

Bajio 600 MW (51%)

La Rosita 1,100 MW (100%)

Campeche facility 252 MW (100%)

Chihuahua facility 259 MW (100%)

Total 2,223 MW

Mexico

United Kingdom

Philippines

Mexico

U.K.

Netherlands

C

Diversified Fuel Mix: 89% of capacity is Gas based

& 11% Coal based

Secured Cash Flow: 78% of capacity is contracted

on Long Term basis

Young Fleet: Average age of the fleet ~6 years and

Remaining Life is 35 – 40 years

Netherlands

Operating assets

Rijnmond 820 MW (100%)

Assets in construction

MaasStroom 428 MW (100%)

Total 1,248 MW

Philippines

Operating assets

Quezon 460 MW (45.87%)

Total 460 MW

Australia

Operating assets 7,658 MW

Assets in construction 428 MW

Total 8,086 MW

InterGen Equity 6,231 MW

GMR Equity 3,116 MW

InterGen Net Capacity (net of aux)

* Also includes Libramiento pipeline

Acquired 50% stake in October 2008

InterGen : Operates 8,086 MW of Global Power Assets

Diagram legend

■ CCGT ■ Coal

C Contracted

*

C

C

C

C

C

C

C

C

Highways & Urban Infrastructure – Paths to Progress

25

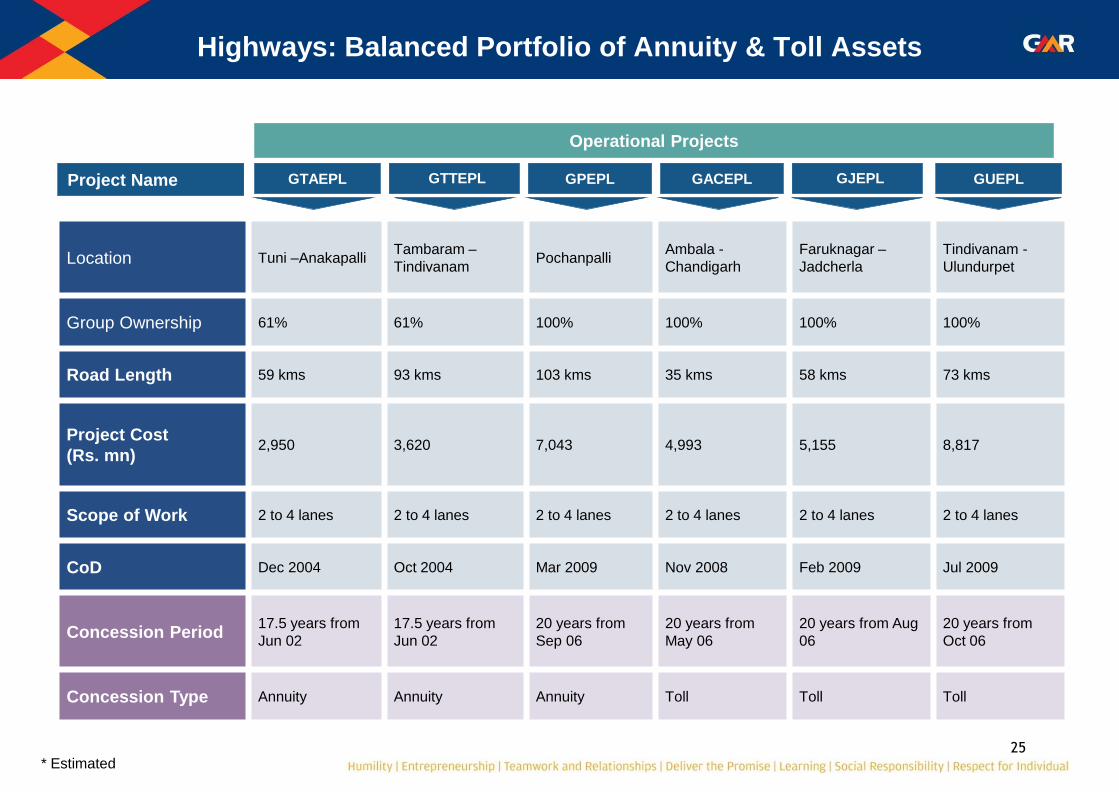

Highways: Balanced Portfolio of Annuity & Toll Assets

* Estimated

Operational Projects

GTAEPL GPEPL GTTEPL GACEPL GUEPL GJEPL Project Name

Location Tuni –Anakapalli Tambaram –

Tindivanam Pochanpalli

Ambala -

Chandigarh

Faruknagar –

Jadcherla

Tindivanam -

Ulundurpet

Group Ownership 61% 61% 100% 100% 100% 100%

Road Length 59 kms 93 kms 103 kms 35 kms 58 kms 73 kms

Project Cost

(Rs. mn) 2,950 3,620 7,043 4,993 5,155 8,817

Scope of Work 2 to 4 lanes 2 to 4 lanes 2 to 4 lanes 2 to 4 lanes 2 to 4 lanes 2 to 4 lanes

CoD Dec 2004 Oct 2004 Mar 2009 Nov 2008 Feb 2009 Jul 2009

Concession Period 17.5 years from

Jun 02

17.5 years from

Jun 02

20 years from

Sep 06

20 years from

May 06

20 years from Aug

06

20 years from

Oct 06

Concession Type Annuity Annuity Annuity Toll Toll Toll

26

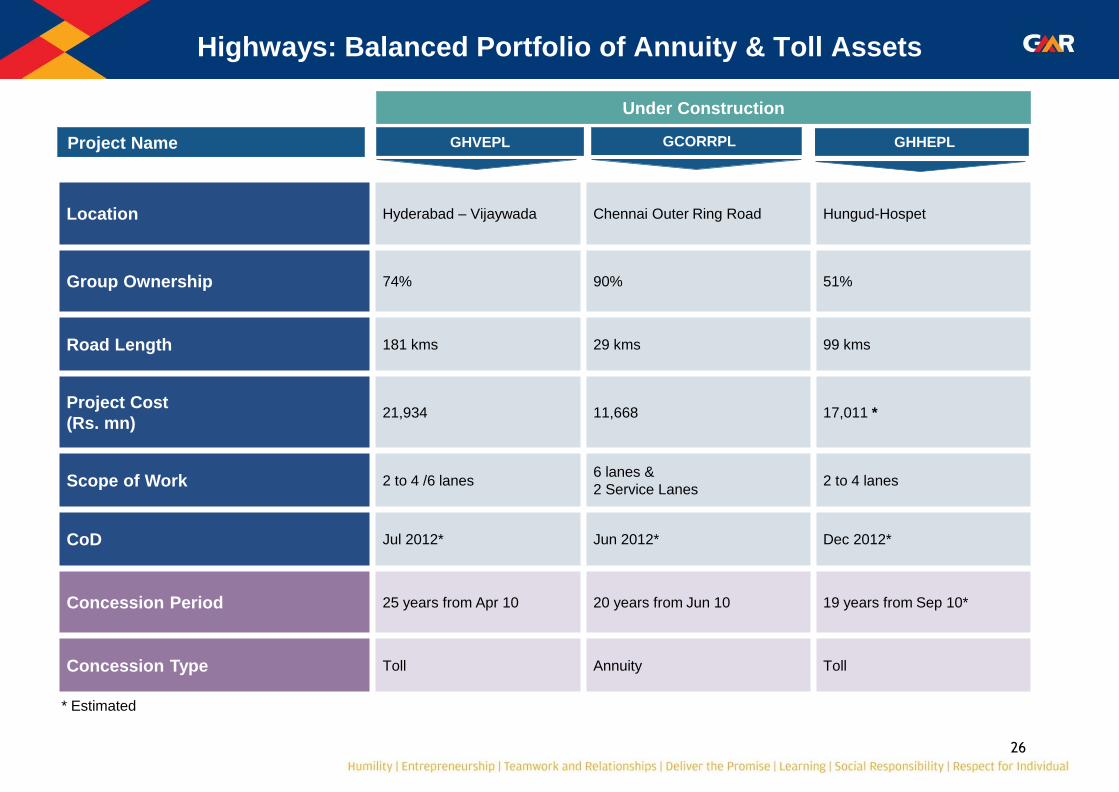

Location Hyderabad – Vijaywada Chennai Outer Ring Road Hungud-Hospet

Group Ownership 74% 90% 51%

Road Length 181 kms 29 kms 99 kms

Project Cost

(Rs. mn) 21,934 11,668 17,011 *

Scope of Work 2 to 4 /6 lanes 6 lanes &

2 Service Lanes 2 to 4 lanes

CoD Jul 2012* Jun 2012* Dec 2012*

Concession Period 25 years from Apr 10 20 years from Jun 10 19 years from Sep 10*

Concession Type Toll Annuity Toll

Highways: Balanced Portfolio of Annuity & Toll Assets

* Estimated

Under Construction

GHVEPL GCORRPL GHHEPL Project Name

27 27

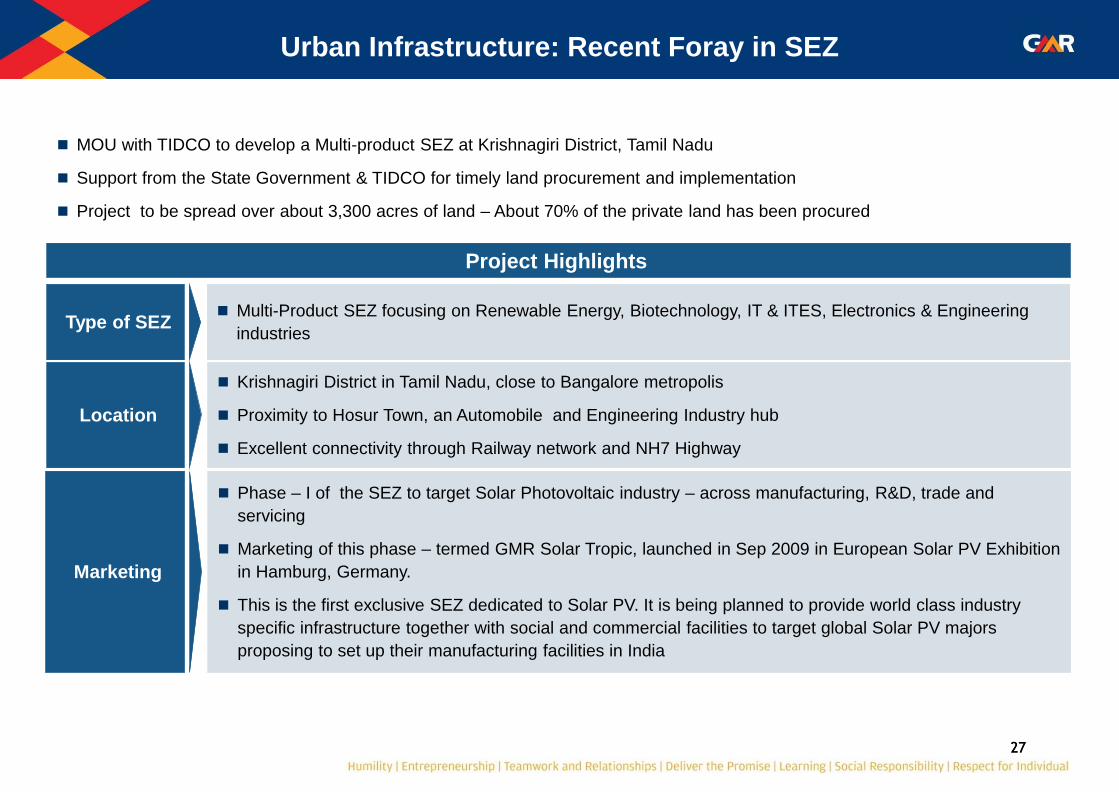

Urban Infrastructure: Recent Foray in SEZ

MOU with TIDCO to develop a Multi-product SEZ at Krishnagiri District, Tamil Nadu

Support from the State Government & TIDCO for timely land procurement and implementation

Project to be spread over about 3,300 acres of land – About 70% of the private land has been procured

Project Highlights

Type of SEZ Multi-Product SEZ focusing on Renewable Energy, Biotechnology, IT & ITES, Electronics & Engineering

industries

Location

Krishnagiri District in Tamil Nadu, close to Bangalore metropolis

Proximity to Hosur Town, an Automobile and Engineering Industry hub

Excellent connectivity through Railway network and NH7 Highway

Marketing

Phase – I of the SEZ to target Solar Photovoltaic industry – across manufacturing, R&D, trade and

servicing

Marketing of this phase – termed GMR Solar Tropic, launched in Sep 2009 in European Solar PV Exhibition

in Hamburg, Germany.

This is the first exclusive SEZ dedicated to Solar PV. It is being planned to provide world class industry

specific infrastructure together with social and commercial facilities to target global Solar PV majors

proposing to set up their manufacturing facilities in India

Key Financial Summary

29

23,332

43,181

1,06,840

1,35,101

1,89,760

3,136 3,764

4,412

6,669 7,346

4,564 5,436

5,985

10,670

13,643

10,617

19,967

26,979

44,762

51,234

29

Consolidated Financial Performance

¹ Cash Profit: PAT + Depreciation & Amortization+ Deferred Tax

27% 43% 32% 26% EBITDA

Margin

Capital Employed (2) Cash Profit (1)

EBITDA & Margins

4 3

2 Gross Revenues 1

CAGR: 48%

CAGR: 31%

CAGR: 23% CAGR: 68%

(Rs.m

n)

(Rs.m

n)

(Rs.m

n)

(Rs.m

n)

2 Capital employed: Total Assets – CWIP - EDCP

30%