Embed Size (px)

Citation preview

In p

art

ners

hip

wit

h:

Sponso

red b

y:

Pub

lishe

d M

ay 2

015

Wri

tte

n B

y:

Eric

Joh

nson

Res

earc

h D

irect

or

Am

eric

an S

hipp

er

Glob

al T

rans

port

atio

n M

anag

emen

t Be

nchm

ark

Stud

yGo

od D

esig

n is

Goo

d Bu

sine

ss

Pa

rt o

f Am

eric

an S

hipp

er’s

Tra

nsp

ort

ati

on

Pro

cu

re-t

o-P

ay

Ben

ch

ma

rk S

eri

es

Executive Summary

Glo

ba

l T

ran

sp

ort

ati

on

Ma

na

ge

me

nt

| B

ench

mar

k S

tudy

: 201

5

ii

Wel

com

e to

Am

eric

an S

hipp

er’s

sev

enth

ann

ual b

ench

mar

k st

udy

of g

loba

l

tran

spor

tatio

n m

anag

emen

t, pr

oduc

ed in

con

junc

tion

with

the

Nat

iona

l Ret

ail

Fede

ratio

n (N

RF)

, Ret

ail I

ndus

try

Lead

ers

Ass

ocia

tion

(RIL

A) a

nd th

e C

ounc

il

of S

uppl

y C

hain

Man

agem

ent P

rofe

ssio

nals

(CS

CM

P).

This

rep

ort a

nnua

lly

exam

ines

the

tren

ds th

at im

pact

how

shi

pper

s an

d lo

gist

ics

serv

ice

prov

ider

s

man

age

thei

r int

erna

tiona

l fre

ight

tran

spor

tatio

n pr

oces

ses,

and

the

tech

nolo

gy

that

hel

ps s

uppo

rt th

ose

proc

esse

s.

Tran

spor

tatio

n m

anag

emen

t has

sta

rted

to m

ove

beyo

nd a

nut

s-an

d-bo

lts

func

tion

for

man

y sh

ipp

ers

and

LS

Ps—

it is

the

hub

aro

und

whi

ch t

hese

com

pani

es o

rient

oth

er k

ey s

uppl

y ch

ain

proc

esse

s. A

gain

st th

at b

ackd

rop,

this

yea

r’s

stud

y ke

enly

exa

min

es th

e el

emen

ts o

f tra

nspo

rtat

ion

man

agem

ent

com

pani

es a

re la

yerin

g ar

ound

sim

ple

plan

ning

and

exe

cutio

n.

Kee

p in

min

d, t

he v

ast

pro

po

rtio

n o

f re

spo

nden

ts t

o A

mer

ican

Shi

pp

er

rese

arch

initi

ativ

es m

anag

e g

lob

al, o

ften

hig

hly

com

ple

x su

pp

ly c

hain

s.

Run

ning

dai

ly la

ne o

ptim

izat

ions

and

bui

ldin

g lo

ad p

lans

are

nic

e, b

ut

mos

tly e

xpec

ted

func

tions

of a

tra

nsp

orta

tion

man

agem

ent

syst

em. G

lob

al

ship

per

s ne

ed v

isib

ility

and

net

wor

k d

esig

n p

latf

orm

s th

at w

ork

on a

cont

inuo

us b

asis

, allo

win

g th

em t

o p

lan

furt

her

upst

ream

and

rea

ct t

o

dis

rup

tions

up

stre

am o

r d

owns

trea

m.

The

stud

y in

clud

es th

e re

spon

ses

of 1

91 q

ualifi

ed g

loba

l log

istic

s pr

actit

ione

rs

surv

eyed

from

mid

-Mar

ch th

roug

h la

te A

pril.

For

the

purp

oses

of t

his

stud

y,

the

focu

s is

pla

ced

spec

ifica

lly o

n th

e st

ages

invo

lvin

g pl

anni

ng th

roug

h ev

ent

man

agem

ent a

nd th

e vi

sibi

lity

into

eac

h le

g of

thos

e pr

oces

ses.

Abo

ut tw

o-th

irds

of re

spon

dent

s in

this

yea

r’s s

tudy

are

task

ed w

ith m

anag

ing

both

dom

estic

and

inte

rnat

iona

l mod

es o

f tra

nspo

rtat

ion,

and

mor

e th

an h

alf

of t

hose

usi

ng s

yste

ms

to m

anag

e tr

ansp

orta

tion

do

so f

or fi

ve o

r m

ore

mod

es. G

iven

the

dive

rsity

of t

he re

spon

dent

poo

l—fr

om c

ompa

nies

man

agin

g

hund

reds

of m

illio

ns o

f dol

lars

in fr

eigh

t spe

nd to

thos

e m

anag

ing

less

than

$10

mill

ion

annu

ally

—th

e ne

eds

of th

ese

vario

us s

hipp

ers

and

LSP

s va

ry g

reat

ly.

And

whi

le T

MS

had

larg

ely

been

see

n as

a d

omes

tic to

ol th

at h

as b

een

shoe

horn

ed in

to in

tern

atio

nal e

nviro

nmen

ts in

the

past

, the

per

cept

ion

has

stea

dily

cha

nged

sin

ce w

e be

gan

benc

hmar

king

shi

pper

s si

x ye

ars

ago.

Shi

pper

s an

d LS

Ps

see

TMS

as

a to

ol th

at s

houl

d be

use

d to

pla

n gl

obal

tran

spor

tatio

n m

oves

and

exe

cute

thos

e pl

ans.

Exec

utiv

e Su

mm

ary

Transp

ort

ati

on

Managem

ent

Trends

Executive Summary

Glo

ba

l T

ran

sp

ort

ati

on

Ma

na

ge

me

nt

| B

ench

mar

k S

tudy

: 201

5

iii

The R

ole

of

Vis

ibilit

y in

G

lobal Tr

ansp

ort

ati

on

Managem

ent

One

unu

sual

dyn

amic

this

rep

ort e

xplo

red

this

yea

r w

as th

e ef

fect

Wes

t Coa

st

port

con

gest

ion

had

on tr

ansp

orta

tion

man

agem

ent c

osts

. Whi

le n

early

90

perc

ent s

aid

they

wer

e im

pact

ed c

ost-

wis

e by

the

cong

estio

n, a

roun

d a

third

said

the

impa

ct w

as le

ss th

an 5

per

cent

ove

r th

eir

expe

cted

tran

spor

tatio

n

spen

d. H

owev

er, n

early

a th

ird o

f res

pond

ents

sai

d th

e co

nges

tion

caus

ed

cost

impa

cts

of 1

0 pe

rcen

t or

mor

e.

Res

pond

ents

to th

is s

tudy

the

past

two

year

s ha

ve g

ener

ally

take

n a

mor

e

soph

istic

ated

vie

w o

f vis

ibili

ty th

an th

ey d

id w

hen

we

first

ask

ed a

bout

thei

r

pers

pect

ive

on v

isib

ility

in 2

013.

Tha

t mea

ns th

ey s

ee v

isib

ility

as

mor

e th

an

trac

k an

d tr

ace,

and

eve

n m

ore

than

exc

eptio

n-ba

sed

man

agem

ent.

Shi

pper

s ha

ve m

any

mot

ivat

ions

for

seek

ing

visi

bilit

y, b

ut th

e on

e th

at tr

umps

them

all

is th

e ab

ility

to r

espo

nd to

dis

rupt

ions

in th

eir

supp

ly c

hain

. Thi

s is

whe

re s

hipp

ers

have

evo

lved

from

the

“whe

re’s

my

stuf

f” m

enta

lity.

Tha

t

old-

fash

ione

d vi

ew a

llow

ed s

hipp

ers

to k

now

whe

n sh

ipm

ents

wer

e hu

ng u

p,

but i

t did

n’t p

rovi

de th

em w

ith m

uch

abili

ty to

red

irect

the

flow

of t

heir

carg

o.

It le

ft th

em m

ore

know

ledg

eabl

e, b

ut n

o m

ore

agile

.

The

valu

e of

vis

ibili

ty is

impo

rtan

t eve

n w

hen

ther

e is

no

disr

uptio

n or

cris

is.

Hav

ing

a vi

ew o

f shi

pmen

ts in

tran

sit a

llow

s a

ship

per

or L

SP

to e

nsur

e th

eir

netw

ork

is r

unni

ng e

ffici

ently

and

pro

perly

aga

inst

tran

spor

tatio

n pl

ans.

Res

pond

ents

hav

e ov

erw

helm

ingl

y in

dica

ted

that

vis

ibili

ty is

not

prim

arily

abou

t red

uced

cos

ts o

f low

erin

g in

vent

ory.

The

gran

d m

ajor

ity o

f res

pond

ents

see

sup

ply

chai

n de

sign

as

an im

port

ant

part

of t

rans

port

atio

n m

anag

emen

t. H

owev

er, t

here

’s a

cle

ar d

icho

tom

y

betw

een

wha

t res

pond

ents

per

ceiv

e to

be

impo

rtan

t and

wha

t des

ign

capa

-

bilit

y th

ey a

ctua

lly h

ave.

Nea

rly tw

o-th

irds

of r

espo

nden

ts d

on’t

have

the

abili

ty

to d

esig

n th

eir

supp

ly c

hain

out

side

of t

he d

ay-t

o-da

y pl

anni

ng a

nd e

xecu

ting

of th

at s

uppl

y ch

ain.

Few

er th

an o

ne in

five

res

pond

ents

use

a th

ird p

arty

serv

ice

or to

ol to

hel

p m

anag

e th

is in

crea

sing

ly im

port

ant f

unct

ion.

Jux

tapo

se

that

with

mor

e th

an fo

ur in

five

say

ing

supp

ly c

hain

des

ign

is im

port

ant.

In y

ears

pas

t we’

ve a

sked

res

pond

ents

to c

hara

cter

ize

the

qual

ity o

f dat

a th

ey

rece

ive

from

car

riers

in d

iffer

ent m

odes

. In

this

yea

r’s

repo

rt, t

he to

pic

was

fram

ed in

a s

uppl

y ch

ain

desi

gn c

onte

xt—

mos

t res

pond

ents

see

thei

r ca

rrie

r

data

as

good

or

aver

age.

Airf

reig

ht c

arrie

rs r

ate

the

high

est i

n te

rms

of d

ata

qual

ity, w

ith r

ail a

nd in

term

odal

pro

vide

rs a

mon

g th

e lo

wes

t. B

ut a

dam

ning

indi

ctm

ent o

f car

riers

acr

oss

all m

odes

is th

e pa

ucity

of r

espo

nden

ts w

ho s

aid

the

data

they

rec

eive

from

car

riers

is v

ery

good

.

The R

ole

of

Supply

C

hain

Desi

gn in

Transp

ort

ati

on

Managem

ent

Executive Summary

Glo

ba

l T

ran

sp

ort

ati

on

Ma

na

ge

me

nt

| B

ench

mar

k S

tudy

: 201

5

iv

Few

er th

an o

ne in

six

res

pond

ents

use

a p

redo

min

antly

man

ual p

roce

ss fo

r

tran

spor

tatio

n m

anag

emen

t—it

seem

s lik

e an

ant

iqua

ted

notio

n fo

r a

glob

al

ship

per

to p

ersi

st w

ithou

t a T

MS

of a

ny k

ind

thes

e da

ys. T

hat s

aid,

the

high

est

perc

enta

ge o

f res

pond

ents

(as

in p

ast y

ears

) ind

icat

ed th

ey u

se a

hyb

rid a

ppro

ach

to tr

ansp

orta

tion

man

agem

ent,

and

that

like

ly m

eans

som

e m

odes

for

thes

e

ship

pers

are

stil

l bei

ng m

anag

ed in

a m

anua

l way

. Glo

bal t

rans

port

atio

n m

anag

e-

men

t is

still

larg

ely

driv

en b

y 3P

Ls, b

y in

tern

al s

yste

ms,

or

by s

prea

dshe

ets.

A c

lue

as to

why

mor

e sh

ippe

rs a

nd L

SP

s do

n’t h

ave

a TM

S a

re th

eir

conc

erns

over

cos

t (bo

th u

pfro

nt im

plem

enta

tion

and

long

-ter

m s

ubsc

riptio

n or

mai

nte-

nanc

e co

sts)

, int

egra

tion

to in

tern

al s

yste

ms

and

conn

ectiv

ity to

out

side

par

tner

s.

Des

pite

big

pus

hes

from

TM

S v

endo

rs to

mak

e po

tent

ial u

sers

feel

thes

e as

pect

s

are

easy

to o

verc

ome,

ther

e re

mai

ns a

fear

that

a T

MS

will

take

tim

e to

impl

emen

t,

will

be

com

plex

to r

un, a

nd th

at th

e R

OI w

ill b

e de

pend

ent o

n in

tegr

atio

ns w

ith

syst

ems

and

part

ners

.

TMS

use

rs w

ant

to b

e ab

le t

o re

spon

d t

o a

tran

spor

tatio

n d

isru

ptio

n or

an

unex

pec

ted

up

tick

in d

eman

d in

rea

l tim

e, b

ut o

nly

36 p

erce

nt o

f res

pon

den

ts

say

thei

r TM

S a

llow

s th

em t

o re

spon

d t

o su

pp

ly c

hain

dis

rup

tions

, whi

le 4

4

per

cent

can

use

the

ir TM

S t

o re

spon

d t

o ch

ange

s in

dem

and

acr

oss

thei

r

rout

es a

nd m

odes

.

With

out t

his

capa

bilit

y, a

TM

S is

an

expe

rt p

lann

ing

tool

whe

n th

ings

are

run

ning

smoo

thly

, but

not

so

usef

ul w

hen

thin

gs g

o w

rong

, as

they

oft

en d

o in

rea

l wor

ld

supp

ly c

hain

s. H

avin

g a

TMS

that

allo

ws

you

to re

spon

d on

a g

loba

l bas

is, a

cros

s

all m

odes

, has

bec

ome

a ne

cess

ary

feat

ure

for

the

mos

t sop

hist

icat

ed s

hipp

ers.

Transp

ort

ati

on

Managem

ent

Technolo

gy

Trends

Table of Contents

Glo

ba

l T

ran

sp

ort

ati

on

Ma

na

ge

me

nt

| B

ench

mar

k S

tudy

: 201

5

5

Tabl

e of

Con

tent

sExe

cuti

ve S

um

mary

.................................................................................................................................................................................i

i

Sec

tion

I: In

trod

uct

ion

..............................................................................................................................................................................

7

Sec

tion

II:

Dem

og

rap

hic

s .........................................................................................................................................................................9

Sec

tion

III

: Tr

an

sport

ati

on

Man

ag

emen

t Tr

end

s ...................................................................................................................................1

1

Sec

tion

IV

: Th

e R

ole

of

Vis

ibilit

y in

Glo

bal Tr

an

sport

ati

on

Man

ag

emen

t ............................................................................................

15

Sec

tion

V: Th

e R

ole

of

Su

pp

ly C

hain

Des

ign

in

Tra

nsp

ort

ati

on

Man

ag

emen

t .....................................................................................

21

Sec

tion

VI:

Tra

nsp

ort

ati

on

Man

ag

emen

t Te

chn

olo

gy

Tren

ds

...............................................................................................................2

4

Sec

tion

VII

: B

est

Pra

ctic

es ..

...................................................................................................................................................................2

7

Ap

pen

dix

A: A

bou

t O

ur

Sp

on

sors

..........................................................................................................................................................

28

> A

mbe

r R

oad

.....

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

...28

> G

T N

exus

.....

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

..28

Ap

pen

dix

B: A

bou

t O

ur

Part

ner

s ...........................................................................................................................................................2

9

> C

ounc

il of

Sup

ply

Cha

in M

anag

emen

t Pro

fess

iona

ls ..

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

...29

> N

atio

nal R

etai

l Fed

erat

ion .

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

.....

29

> R

etai

l Ind

ustr

y Le

ader

s A

ssoc

iatio

n ...

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

.....

29

Ap

pen

dix

C: A

bou

t Am

eric

an S

hipp

er R

esea

rch

...................................................................................................................................3

0

Section I: Introduction

Glo

ba

l T

ran

sp

ort

ati

on

Ma

na

ge

me

nt

| B

ench

mar

k S

tudy

: 201

5

6

Figu

res

Fig

ure

1:

Indu

stry

Seg

men

ts ...

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

9

Fig

ure

2:

Com

pany

Size

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

..10

Fig

ure

3:

Job

Title

s Su

rvey

ed ...

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

...10

Fig

ure

4:

Tran

spor

tatio

n M

anag

emen

t Res

pons

ibili

ty ..

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

...11

Fig

ure

5:

Tran

spor

tatio

n M

odes

Man

aged

by

TMS

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

....1

2

Fig

ure

6:

Tran

spor

tatio

n Sp

end .

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

..13

Fig

ure

7:

Tran

spor

tatio

n Pr

oduc

tivity

Tabl

e—M

anuf

actu

rers

vs.

Ret

aile

rs ..

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

...14

Fig

ure

8:

Addi

tiona

l Tra

nspo

rtatio

n Co

sts

Incu

rred

Due

to W

est C

oast

Por

t Con

gest

ion.

......

......

......

......

......

......

......

......

......

......

......

......

...15

Fig

ure

9:

Ship

pers

’ Defi

nitio

n of

Vis

ibili

ty 2

013-

2015

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

16

Fig

ure

10

: M

ost I

mpo

rtant

Ben

efit o

f Vis

ibili

ty ...

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

..17

Fig

ure

11

: Ha

rdes

t Mod

e to

Atta

in V

isib

ility

—M

anua

l vs.

Sys

tem

s-ba

sed

Ship

pers

.....

......

......

......

......

......

......

......

......

......

......

......

......

...17

Fig

ure

12

: Do

es V

isib

ility

Pro

vide

Qua

ntifi

able

ROI

? ..

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

.....

18

Fig

ure

13

: W

hat S

yste

ms

Prov

ide

Visi

bilit

y In

put ..

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

.....

19

Fig

ure

14

: Vi

sibi

lity—

Days

Prio

r to

Ship

men

t ....

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

.20

Fig

ure

15

: Su

pply

Cha

in D

esig

n is

Crit

ical

to Tr

ansp

orta

tion

Man

agem

ent .

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

...21

Fig

ure

16

: Cu

rrent

Sup

ply

Chai

n De

sign

Tool

.....

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

.22

Fig

ure

17

: Ca

rrier

Dat

a Qu

ality

By

Mod

e ....

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

...23

Fig

ure

18

: Gl

obal

Tran

spor

tatio

n M

anag

emen

t Pla

tform

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

..24

Fig

ure

19

: Bi

gges

t Ben

efits

of G

loba

l TM

S ...

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

.25

Fig

ure

20

: Bi

gges

t Cha

lleng

es o

f Glo

bal T

MS .

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

.....

25

Fig

ure

21

: TM

S En

able

s Ea

sy M

ode

and

Rout

e Op

timiza

tion .

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

......

26

Section I: Introduction

Glo

ba

l T

ran

sp

ort

ati

on

Ma

na

ge

me

nt

| B

ench

mar

k S

tudy

: 201

5

7

Sec

tion

I: In

trod

uctio

n

Wel

com

e to

Am

eric

an S

hipp

er’s

sev

enth

ann

ual b

ench

mar

k st

udy

of g

loba

l

tran

spor

tatio

n m

anag

emen

t, pr

oduc

ed in

con

junc

tion

with

the

Nat

iona

l Ret

ail

Fede

ratio

n (N

RF)

, Ret

ail I

ndus

try

Lead

ers

Ass

ocia

tion

(RIL

A) a

nd th

e C

ounc

il of

Sup

ply

Cha

in M

anag

emen

t Pro

fess

iona

ls (C

SC

MP

). Th

is re

port

ann

ually

exa

min

es

the

tren

ds th

at im

pact

how

shi

pper

s an

d lo

gist

ics

serv

ice

prov

ider

s m

anag

e th

eir

inte

rnat

iona

l fre

ight

tran

spor

tatio

n pr

oces

ses,

and

the

tech

nolo

gy th

at h

elps

supp

ort t

hose

pro

cess

es.

Tran

spor

tatio

n m

anag

emen

t ha

s st

arte

d t

o m

ove

bey

ond

a n

uts-

and

-bol

ts

func

tion

for m

any

ship

pers

and

LS

Ps—

it is

the

hub

arou

nd w

hich

thes

e co

mpa

nies

orie

nt o

ther

key

sup

ply

chai

n pr

oces

ses.

Aga

inst

that

bac

kdro

p, th

is y

ear’

s st

udy

keen

ly e

xam

ines

the

elem

ents

of t

rans

port

atio

n m

anag

emen

t com

pani

es a

re

laye

ring

arou

nd s

impl

e pl

anni

ng a

nd e

xecu

tion.

Kee

p in

min

d, th

e va

st p

ropo

rtio

n of

res

pond

ents

to A

mer

ican

Shi

pper

res

earc

h

initi

ativ

es m

anag

e gl

obal

, oft

en h

ighl

y co

mpl

ex s

uppl

y ch

ains

. Run

ning

dai

ly la

ne

optim

izat

ions

and

bui

ldin

g lo

ad p

lans

are

nic

e, b

ut m

ostly

exp

ecte

d fu

nctio

ns o

f

a tr

ansp

orta

tion

man

agem

ent s

yste

m. G

loba

l shi

pper

s ne

ed v

isib

ility

and

net

wor

k

desi

gn p

latf

orm

s th

at w

ork

on a

con

tinuo

us b

asis

, allo

win

g th

em to

pla

n fu

rthe

r

upst

ream

and

rea

ct to

dis

rupt

ions

ups

trea

m o

r do

wns

trea

m.

The

stud

y in

clud

es th

e re

spon

ses

of 1

91 q

ualifi

ed g

loba

l log

istic

s pr

actit

ione

rs

who

par

ticip

ated

in th

e su

rvey

from

mid

-Mar

ch th

roug

h la

te A

pril.

It’s

impo

rtan

t

to r

ecog

nize

that

glo

bal t

rans

port

atio

n m

anag

emen

t is

a br

oad

term

that

cov

ers

the

full

cycl

e of

tran

spor

tatio

n ac

tivity

, inc

ludi

ng p

rocu

rem

ent,

plan

ning

, ord

er

man

agem

ent,

tend

erin

g, e

vent

man

agem

ent,

and

finan

cial

set

tlem

ent.

For

the

purp

oses

of t

his

stud

y, th

e fo

cus

is p

lace

d sp

ecifi

cally

on

the

stag

es in

volv

ing

plan

ning

thro

ugh

even

t man

agem

ent a

nd th

e vi

sibi

lity

into

eac

h le

g of

thos

e

proc

esse

s. P

rocu

rem

ent a

nd s

ettle

men

t are

pur

pose

ly s

et a

side

to fo

cus

on th

e

“blo

ckin

g an

d ta

cklin

g” o

f glo

bal l

ogis

tics

man

agem

ent.

Glo

bal s

hipp

ers

need

vis

ibili

ty a

nd n

etw

ork

de

sign

pla

tfor

ms

that

wor

k on

a c

ontin

uous

ba

sis,

allo

win

g th

em to

pla

n fu

rthe

r up

stre

am a

nd

reac

t to

disr

uptio

ns u

pstr

eam

or

dow

nstr

eam

.

Section I: Introduction

Glo

ba

l T

ran

sp

ort

ati

on

Ma

na

ge

me

nt

| B

ench

mar

k S

tudy

: 201

5

8

Rea

ders

of t

his

repo

rt s

houl

d al

so u

nder

stan

d th

at th

is b

ench

mar

king

initi

ativ

e

stric

tly p

erta

ins

to g

loba

l and

cro

ss-b

orde

r tr

ansp

orta

tion

man

agem

ent.

Qua

lified

resp

onde

nts

repr

esen

t a v

arie

ty o

f ind

ustr

y se

gmen

ts, i

nclu

ding

ret

ail,

man

ufac

-

turin

g, m

ater

ials

, and

third

-par

ty lo

gist

ics.

Res

pons

es fr

om c

arrie

rs, c

onsu

ltant

s,

tech

nolo

gy v

endo

rs, a

nd o

ther

unq

ualifi

ed r

espo

nden

ts a

re n

ot in

clud

ed in

the

aggr

egat

e da

ta p

rese

nted

of t

his

repo

rt.

Dis

trib

utio

n ch

anne

ls f

or

the

20-q

uest

ion

ben

chm

arki

ng s

urve

y in

clud

ed

Am

eric

an S

hipp

er’s

web

site

, e-m

ail l

ists

, and

new

slet

ters

. In

addi

tion,

NR

F, R

ILA

and

CS

CM

P m

embe

rs w

ere

invi

ted

to p

artic

ipat

e vi

a e-

mai

l pro

mot

ions

dire

ctly

from

thos

e as

soci

atio

ns. A

s a

polic

y, A

mer

ican

Shi

pper

doe

s no

t sha

re a

ny

indi

vidu

al s

urve

y re

spon

ses.

All

data

is d

ispl

ayed

in a

ggre

gate

onl

y.

This

rep

ort

mak

es fr

eque

nt c

omp

aris

ons

bet

wee

n sy

stem

s-b

ased

shi

pp

ers

and

man

ual s

hip

per

s. F

or t

he p

urp

oses

of r

ead

ing

this

rep

ort,

sys

tem

s-b

ased

ship

per

s ar

e th

ose

who

se t

rans

por

tatio

n m

anag

emen

t p

roce

sses

are

han

dle

d

pre

dom

inan

tly (b

ut n

ot n

eces

saril

y w

holly

) via

a T

MS

, whi

le m

anua

l shi

pp

ers

are

thos

e w

ho p

red

omin

antly

use

sp

read

shee

ts t

o m

anag

e th

e ex

ecut

ion

of

thei

r sh

ipm

ents

. It’

s im

por

tant

to

und

erst

and

tha

t sy

stem

s-b

ased

shi

pp

ers

are

not

com

ple

tely

aut

omat

ed, a

nd m

anua

l shi

pp

ers

use

bas

ic t

echn

olog

ies

in

thei

r b

usin

esse

s.

Qualif

ied

resp

ond

ents

rep

resent a v

ariety

of

ind

ustr

y s

egm

ents

,

inclu

din

g r

eta

il, m

anu -

factu

ring, m

ate

rials

, and

third

-part

y lo

gis

tics.

Section II: Demographics

Glo

ba

l T

ran

sp

ort

ati

on

Ma

na

ge

me

nt

| B

ench

mar

k S

tudy

: 201

5

9

Sec

tion

II: D

emog

raph

ics

The

typi

cal r

espo

nden

t poo

l for

Am

eric

an S

hipp

er r

esea

rch

initi

ativ

es is

eve

nly

com

pose

d of

man

ufac

ture

rs, r

etai

lers

, and

3P

Ls, a

nd th

is y

ear

is n

o di

ffere

nt, w

ith

an a

lmos

t eve

n br

eaku

p be

twee

n th

ose

thre

e gr

oups

. The

re is

, how

ever

, lar

ger

repr

esen

tatio

n fr

om g

roup

s ou

tsid

e of

thos

e th

ree

grou

ps, w

ith n

early

20

perc

ent

of r

esp

ond

ents

iden

tifyi

ng t

hem

selv

es a

s sh

ipp

ers

in t

he g

over

nmen

t, r

aw

mat

eria

ls, a

nd c

omm

oditi

es s

ecto

rs.

191

tota

l res

pond

ents

30%

13%

3PL/

Forw

ard

er/N

VO

CC

/Int

erm

edia

ry

Ret

ail/W

hole

sale

Dis

cret

e m

anuf

actu

ring

Pro

cess

man

ufac

turin

g

Raw

mat

eria

ls/C

omm

oditi

es

Gov

ernm

ent/

Pub

lic S

ecto

r

Eng

inee

ring/

Con

stru

ctio

n/E

nerg

y

9%

15%

4%5%

24%

Fig

ure

1:

Ind

ustr

y S

eg

me

nts

Section II: Demographics

Glo

ba

l T

ran

sp

ort

ati

on

Ma

na

ge

me

nt

| B

ench

mar

k S

tudy

: 201

5

10

Alm

ost t

ypic

al fo

r an

Am

eric

an S

hipp

er b

ench

mar

k re

port

is th

e br

eaku

p by

com

pany

siz

e, w

ith n

early

40

perc

ent o

f com

pani

es p

artic

ipat

ing

havi

ng $

1 bi

llion

or m

ore

in r

even

ue. T

his

stud

y m

akes

com

paris

ons

betw

een

the

way

$1

billi

on-

plus

com

pani

es h

andl

e tr

ansp

orta

tion

man

agem

ent v

ersu

s th

e w

ay c

ompa

nies

with

rev

enue

of l

ess

than

$1

billi

on d

o. O

ur r

esea

rch

has

foun

d th

at th

is is

a k

ey

line

of d

emar

catio

n in

term

s of

shi

pper

and

LS

P b

ehav

ior

and

tech

nolo

gy u

sage

.

Nea

rly h

alf o

f res

pond

ents

sur

veye

d fo

r th

is r

epor

t are

in m

anag

eria

l rol

es, w

hile

a qu

arte

r ar

e in

the

exec

utiv

e- o

r C

-lev

el, a

nd a

noth

er n

early

20

perc

ent a

re a

t

the

dire

ctor

leve

l. Th

is le

vel o

f upp

er m

anag

emen

t par

ticip

atio

n is

in li

ne w

ith

mos

t Am

eric

an S

hipp

er r

esea

rch

initi

ativ

es.

189

tota

l res

pond

ents

13%

10%

C-L

evel

(CE

O,C

IO,C

FO, e

tc)

Exe

cutiv

e (S

VP,

VP,

GM

, etc

.)

Dire

ctor

Man

ager

Sta

ff

12%

48%

18%

Fig

ure

3:

Jo

b T

itle

s S

urv

eye

d

189

tota

l res

pond

ents

38%

Gre

ater

tha

n $1

bill

ion

$100

mill

ion

to $

1 b

illio

n

Less

tha

n $1

00 m

illio

n

31%

31%

Fig

ure

2:

Co

mp

an

y S

ize

Section III: Transportation Management Trends

Glo

ba

l T

ran

sp

ort

ati

on

Ma

na

ge

me

nt

| B

ench

mar

k S

tudy

: 201

5

11

Sec

tion

III

: Tr

ansp

orta

tion

M

anag

emen

t Tre

nds

Aro

und

tw

o-th

irds

of r

esp

ond

ents

for

this

rep

ort

have

res

pon

sib

ility

for

dom

estic

and

inte

rnat

iona

l tra

nsp

orta

tion.

Tha

t spe

aks

to th

e co

mpl

exity

that

man

y di

rect

ors

and

VP

s of

tran

spor

tatio

n fa

ce in

thei

r ro

les,

ove

rsee

ing

a ra

nge

of m

odes

and

geo

grap

hies

and

oft

en ju

gglin

g m

ultip

le s

yste

ms

to m

anag

e

thos

e m

odes

. Our

ane

cdot

al r

esea

rch

into

the

man

agem

ent

of g

lob

al a

nd

dom

estic

tra

nsp

orta

tion

ind

icat

es t

hat

even

whe

n co

mp

anie

s ta

ke a

n in

te-

grat

ed a

pp

roac

h to

end

-to-

end

frei

ght

tran

spor

tatio

n, t

he t

wo

pro

cess

es a

re

ofte

n ke

pt

apar

t an

d h

and

led

by

sep

arat

e te

ams,

usi

ng d

iffer

ent

syst

ems

that

rare

ly in

tera

ct in

a w

ay d

esig

ned

to

func

tiona

lly im

pro

ve t

he w

hole

.

0%10%

20%

30%

40%

50%

60%

70%

80%

I am

res

pon

sib

lefo

r d

omes

ticm

anag

emen

t on

ly

I am

res

pon

sib

lefo

r in

tern

atio

nal

man

agem

ent

only

I am

res

pon

sib

le fo

rin

tern

atio

nal a

ndd

omes

tic m

anag

emen

t

62%

69%

8%

36%

Larg

e S

hip

per

s

Sm

all/M

ediu

m S

hip

per

s

22%

2%

Fig

ure

4:

Tra

nsp

ort

ati

on

Ma

na

ge

me

nt

Re

sp

on

sib

ilit

y

191

tota

l res

pond

ents

0%10%

20%

30%

40%

50%

60%

70%

80%

I am

res

pon

sib

lefo

r d

omes

ticm

anag

emen

t on

ly

I am

res

pon

sib

lefo

r in

tern

atio

nal

man

agem

ent

only

I am

res

pon

sib

le fo

rin

tern

atio

nal a

ndd

omes

tic m

anag

emen

t

54%

72%

68%

7%9%

26%

37%

Man

ufac

ture

rs

Ret

aile

rs

3PLs

25%

2%

Section III: Transportation Management Trends

Glo

ba

l T

ran

sp

ort

ati

on

Ma

na

ge

me

nt

| B

ench

mar

k S

tudy

: 201

5

12

This

is p

artly

due

to

the

inna

te d

iffer

ence

s in

the

way

glo

bal

and

dom

estic

mod

es a

re p

rocu

red

and

man

aged

. Som

e en

terp

risin

g co

mp

anie

s ha

ve k

ey

per

sonn

el s

witc

h ro

les

to g

et a

bet

ter

und

erst

and

ing

of t

he is

sues

face

d b

y th

e

othe

r. F

ig. 4

, how

ever

, ind

icat

es t

hat

com

pan

ies

do

have

a p

erso

n or

tea

m

resp

onsi

ble

for

over

all t

rans

por

tatio

n m

anag

emen

t m

ore

ofte

n th

an w

e ex

per

i-

ence

in o

ur d

iscu

ssio

ns w

ith s

hip

per

s. T

he d

ivid

e is

see

n m

ost

keen

ly b

etw

een

reta

ilers

and

man

ufac

ture

rs/3

PLs

, with

bar

ely

half

of r

etai

lers

man

agin

g b

oth

sets

of m

odes

.

Ab

out

half

of t

he r

esp

ond

ents

to

this

sur

vey

ind

icat

e th

ey u

se a

tra

nsp

orta

tion

man

agem

ent

syst

em, a

nd o

f tho

se, F

ig. 5

sho

ws

whi

ch m

odes

the

y m

anag

e.

A m

ajor

ity o

f TM

S u

sers

em

plo

y th

e sy

stem

to

man

age

at le

ast

five

mod

es,

and

give

n th

e in

tern

atio

nal f

ocus

of m

ost c

ompa

nies

sur

veye

d, it

’s li

ttle

sur

pris

e to

see

ocea

n, a

irfre

ight

and

LC

L am

ong

thos

e m

ost w

idel

y m

anag

ed b

y a

syst

em.

As

we’

ve r

epor

ted

in t

he p

ast,

TM

S h

ad la

rgel

y b

een

seen

as

a d

omes

tic t

ool

that

has

bee

n sh

oeho

rned

into

inte

rnat

iona

l env

ironm

ents

but

tha

t p

erce

ptio

n

has

stea

dily

cha

nged

sin

ce w

e b

egan

ben

chm

arki

ng s

hip

per

s si

x ye

ars

ago.

Shi

pp

ers

and

LS

Ps

see

a TM

S a

s a

tool

tha

t sh

ould

be

used

to

pla

n gl

obal

tran

spor

tatio

n m

oves

and

exe

cute

tho

se p

lans

.

0%10

%20

%30

%40

%50

%60

%70

%80

%

Oth

er (p

leas

e sp

ecify

)

Oce

an T

rans

por

t (o

ther

, non

-con

tain

eriz

ed)

Par

cel/S

mal

l Pac

kage

Rai

l/Int

erm

odal

LCL

Oce

an

Airf

reig

ht

Truc

kloa

d

Less

tha

n Tr

uckl

oad

(LTL

)

FCL

Oce

an

56%

46%

56%

57

%

75%

43%

62%

39%

11%

Fig

ure

5:

Tra

nsp

ort

ati

on

Mo

de

s M

an

ag

ed

by T

MS

91 to

tal r

espo

nden

ts

Section III: Transportation Management Trends

Glo

ba

l T

ran

sp

ort

ati

on

Ma

na

ge

me

nt

| B

ench

mar

k S

tudy

: 201

5

13

Litt

le s

urp

rise

in F

ig. 6

: lar

ge s

hip

per

s m

anag

e a

lot

of fr

eigh

t sp

end

. Mor

e

surp

risin

g: th

at s

o m

any

smal

l shi

pper

s sp

end

less

than

$10

mill

ion

on fr

eigh

t. It

spea

ks to

the

dive

rsity

of o

pera

tions

that

LS

Ps

and

carr

iers

acr

oss

all m

odes

mus

t

cate

r to

. In

the

TMS

wor

ld, i

t als

o m

eans

tech

nolo

gy p

rovi

ders

—be

it 3

PLs

or

outr

ight

sof

twar

e ve

ndor

s—ha

ve t

o d

ecid

e w

hich

mar

ket

thei

r p

rod

ucts

are

bes

t su

ited

to,

or

whe

ther

the

y ca

n re

alis

tical

ly t

arge

t sh

ipp

ers

of m

ultip

le s

izes

and

com

ple

xitie

s. A

shi

pp

er w

ith m

ore

than

$10

0 m

illio

n in

frei

ght s

pend

doe

sn’t

just

hav

e 10

tim

es th

e sp

end

of o

ne w

ith $

10 m

illio

n. It

s ne

twor

k is

like

ly e

xpo-

nent

ially

mor

e co

mp

lex,

its

tran

spor

tatio

n d

epar

tmen

t lik

ely

muc

h la

rger

and

pot

entia

lly m

ore

silo

ed. S

mar

t ve

ndor

s an

d L

SP

s kn

ow t

he m

arke

ts w

here

the

ir

offe

rings

are

mos

t re

leva

nt, a

nd d

on’t

ove

rrea

ch in

mar

kets

whe

re t

here

’s li

kely

to b

e lit

tle a

ccep

tanc

e of

the

ir p

rod

ucts

.

For

inst

ance

, sof

twar

e-as

-a-s

ervi

ce v

end

ors

are

muc

h m

ore

likel

y to

tar

get

smal

l to

mid

dle

-mar

ket

ship

per

s an

d L

SP

s w

ith a

TM

S s

ince

the

up

fron

t co

sts

are

low

er, t

he im

ple

men

tatio

n te

nds

to b

e q

uick

er, a

nd r

obus

tnes

s of

the

syst

em is

not

as

imp

orta

nt a

s th

e ab

ility

to

qui

ckly

cre

ate

a ne

twor

k ef

fect

amon

g its

sup

ply

cha

in p

artn

ers.

Larg

er s

hip

per

s ar

e m

ore

likel

y to

eye

a s

yste

m t

hat

can

crun

ch h

uge

amou

nts

of d

ata,

run

nea

rly c

ontin

uous

wha

t-if

scen

ario

s, a

nd c

reat

e st

ocha

stic

mod

els

for

thei

r tr

ansp

orta

tion

netw

orks

. The

ir ne

eds

are

so c

ompl

ex th

at th

e po

tent

ially

long

er a

nd c

ostli

er im

ple

men

tatio

n is

mor

e th

an o

ffse

t b

y th

e p

ower

of t

he

optim

izat

ion

engi

nes.

49%

5%

46%

Mor

e th

an $

100

mill

ion

per

yea

r

Bet

wee

n $1

0 an

d

$100

mill

ion

per

yea

r

Less

tha

n $1

0 m

illio

n p

er y

ear

42%

58%

Fig

ure

6:

Tra

nsp

ort

ati

on

Sp

en

d

134

tota

l res

pond

ents

La

rge S

hip

pers

Sm

all/M

ed

ium

Sh

ipp

ers

Section III: Transportation Management Trends

Glo

ba

l T

ran

sp

ort

ati

on

Ma

na

ge

me

nt

| B

ench

mar

k S

tudy

: 201

5

14

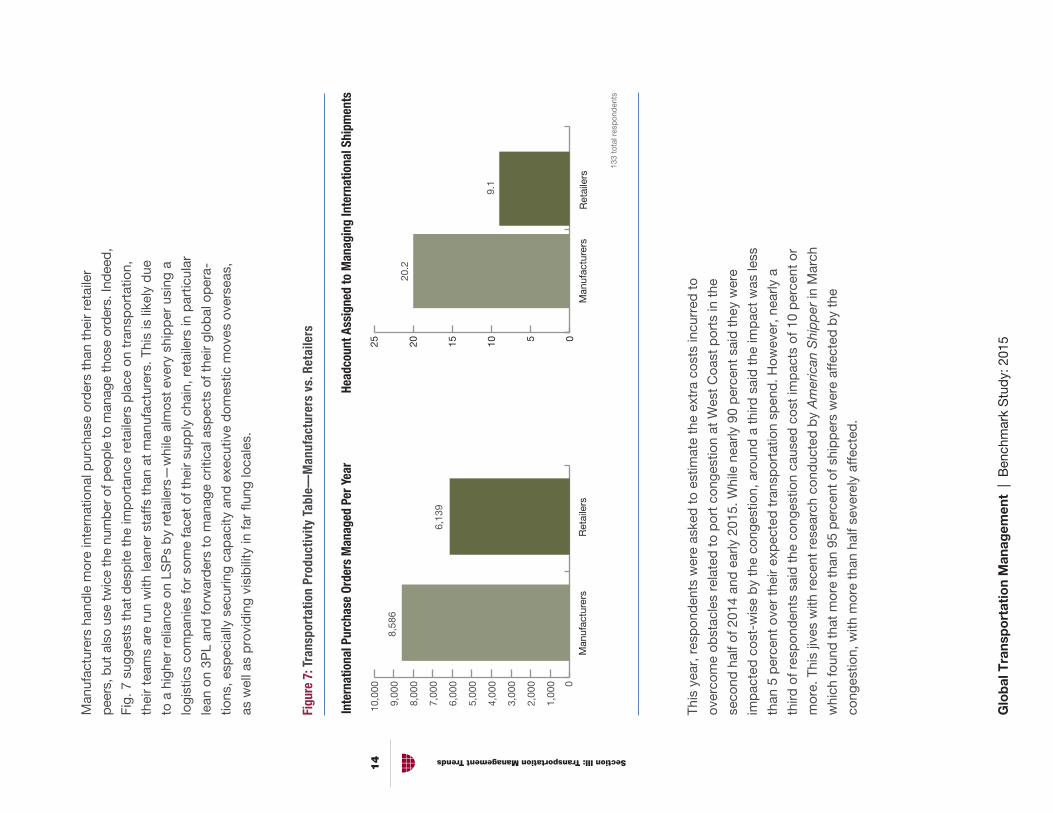

Man

ufac

ture

rs h

and

le m

ore

inte

rnat

iona

l pur

chas

e or

der

s th

an t

heir

reta

iler

peer

s, b

ut a

lso

use

twic

e th

e nu

mb

er o

f peo

ple

to m

anag

e th

ose

orde

rs. I

ndee

d,

Fig.

7 s

ugge

sts

that

des

pite

the

imp

orta

nce

reta

ilers

pla

ce o

n tr

ansp

orta

tion,

thei

r te

ams

are

run

with

lean

er s

taff

s th

an a

t m

anuf

actu

rers

. Thi

s is

like

ly d

ue

to a

hig

her

relia

nce

on L

SP

s b

y re

taile

rs—

whi

le a

lmos

t ev

ery

ship

per

usi

ng a

logi

stic

s co

mp

anie

s fo

r so

me

face

t of

the

ir su

pp

ly c

hain

, ret

aile

rs in

par

ticul

ar

lean

on

3PL

and

forw

ard

ers

to m

anag

e cr

itica

l asp

ects

of t

heir

glob

al o

per

a-

tions

, esp

ecia

lly s

ecur

ing

cap

acity

and

exe

cutiv

e d

omes

tic m

oves

ove

rsea

s,

as w

ell a

s p

rovi

din

g vi

sib

ility

in fa

r flu

ng lo

cale

s.

133

tota

l res

pond

ents

0

1,00

0

2,00

0

3,00

0

4,00

0

5,00

0

6,00

0

7,00

0

8,00

0

9,00

0

10,0

00

Ret

aile

rsM

anuf

actu

rers

8,58

6

6,13

9

0510152025

20.2

Man

ufac

ture

rs

9.1

Ret

aile

rs

Fig

ure

7:

Tra

nsp

ort

ati

on

Pro

du

cti

vit

y T

ab

le—

Ma

nu

fac

ture

rs v

s.

Re

tail

ers

Inte

rna

tio

na

l P

urc

ha

se O

rders

Ma

na

ged

Per

Yea

rH

ea

dco

un

t A

ssig

ned

to

Ma

na

gin

g I

nte

rna

tio

na

l S

hip

men

ts

This

yea

r, r

esp

ond

ents

wer

e as

ked

to

estim

ate

the

extr

a co

sts

incu

rred

to

over

com

e ob

stac

les

rela

ted

to

por

t co

nges

tion

at W

est

Coa

st p

orts

in t

he

seco

nd h

alf o

f 201

4 an

d e

arly

201

5. W

hile

nea

rly 9

0 p

erce

nt s

aid

the

y w

ere

imp

acte

d c

ost-

wis

e b

y th

e co

nges

tion,

aro

und

a t

hird

sai

d t

he im

pac

t w

as le

ss

than

5 p

erce

nt o

ver

thei

r ex

pec

ted

tra

nsp

orta

tion

spen

d. H

owev

er, n

early

a

third

of r

esp

ond

ents

sai

d t

he c

onge

stio

n ca

used

cos

t im

pac

ts o

f 10

per

cent

or

mor

e. T

his

jives

with

rec

ent

rese

arch

con

duc

ted

by

Am

eric

an S

hip

per

in M

arch

whi

ch fo

und

tha

t m

ore

than

95

per

cent

of s

hip

per

s w

ere

affe

cted

by

the

cong

estio

n, w

ith m

ore

than

hal

f sev

erel

y af

fect

ed.

Section IV: The Role of Visibility in Global Transportation Management

Glo

ba

l T

ran

sp

ort

ati

on

Ma

na

ge

me

nt

| B

ench

mar

k S

tudy

: 201

5

15

Sec

tion

IV

: The

Rol

e of

Vis

ibili

ty in

Glo

bal

Tran

spor

tatio

n M

anag

emen

t

Tran

spor

tatio

n vi

sibi

lity

has

mov

ed fr

om a

nic

e-to

-hav

e fe

atur

e to

nee

d-to

-hav

e

elem

ent f

or m

ost s

hipp

ers

and

LSP

s. It

’s r

are

for

Am

eric

an S

hipp

er to

talk

to a

ship

per

that

doe

sn’t

have

or

wan

t som

e fo

rm o

f vis

ibili

ty. G

ener

ally

, tha

t boi

ls

dow

n to

kno

wle

dge

abou

t cer

tain

key

mile

ston

es fo

r in

-tra

nsit

carg

o.

The

divi

ding

poi

nt o

n vi

sibi

lity

is w

hat c

omes

nex

t. La

st y

ear,

the

them

e of

this

repo

rt c

ente

red

on th

e id

ea th

at s

hipp

ers

and

LSP

s ou

ght t

o be

str

ivin

g fo

r m

ore

usef

ul v

isib

ility

—no

t “w

here

’s m

y st

uff,”

but

“w

hat d

o I d

o if

ther

e’s

a pr

oble

m

with

my

stuf

f.”

141

tota

l res

pond

ents

0%5%10%

15%

20%

25%

30%

35%

40%

We

did

n't

incu

r an

yex

tra

cost

Mor

e th

an25

per

cent

20-2

5p

erce

nt16

-20

per

cent

11-1

5p

erce

nt5-

10p

erce

ntLe

ss t

han

5 p

erce

nt

25%

33%

14%

9%12

%

4%4%

Fig

ure

8:

Ad

dit

ion

al

Tra

nsp

ort

ati

on

Co

sts

In

cu

rre

d D

ue

to

We

st

Co

ast

Po

rt C

on

ge

sti

on

Fig.

8 s

how

s th

at r

espo

nden

ts h

ave

gene

rally

take

n a

mor

e so

phis

ticat

ed v

iew

of v

isib

ility

the

past

two

year

s. T

hat m

eans

they

see

vis

ibili

ty a

s m

ore

than

trac

k

and

tra

ce, a

nd e

ven

mor

e th

an e

xcep

tion-

bas

ed m

anag

emen

t. A

nced

otal

ly,

we

are

hear

ing

mor

e th

an e

ver

that

shi

pper

s w

ant a

con

trol

tow

er (t

he e

volu

tion

of th

e 4P

L co

ncep

t) to

ove

rsee

thei

r gl

obal

tran

spor

tatio

n ne

twor

k. A

nd im

por-

tant

ly, v

isib

ility

for

mor

e th

an h

alf

of s

hip

per

s en

com

pas

ses

mor

e th

an ju

st

tran

spor

tatio

n—it

stre

tche

s fr

om t

he m

omen

t a

pur

chas

e or

der

is c

ut t

o

dis

trib

utio

n or

eve

n st

ore

del

iver

y.

Section IV: The Role of Visibility in Global Transportation Management

Glo

ba

l T

ran

sp

ort

ati

on

Ma

na

ge

me

nt

| B

ench

mar

k S

tudy

: 201

5

16

Shi

pper

s ha

ve m

any

mot

ivat

ions

for

seek

ing

visi

bilit

y, b

ut th

e on

e th

at tr

umps

them

all

is th

e ab

ility

to r

espo

nd to

dis

rupt

ions

in th

eir

supp

ly c

hain

. Thi

s is

whe

re

ship

pers

hav

e ev

olve

d fr

om th

e “w

here

’s m

y st

uff”

men

talit

y. T

hat o

ld-f

ashi

oned

view

allo

wed

shi

pp

ers

to k

now

whe

n sh

ipm

ents

wer

e hu

ng u

p, b

ut it

did

n’t

pro

vid

e th

em w

ith m

uch

abili

ty t

o re

dire

ct t

he fl

ow o

f the

ir ca

rgo.

It le

ft t

hem

mor

e kn

owle

dge

able

, but

no

mor

e ag

ile.

Usi

ng v

isib

ility

to r

eact

to d

isru

ptio

ns in

volv

es in

tegr

atin

g vi

sibi

lity

with

pla

nnin

g

and

exe

cutio

n, s

o th

at p

ort

cong

estio

n in

Sou

ther

n C

alifo

rnia

aff

ectin

g a

ship

men

t cat

alyz

es a

pro

cess

whe

re a

noth

er m

ode

or g

eogr

aphy

is s

ough

t,

optim

ized

, and

exe

cute

d.

Fig.

10

also

sho

ws

that

the

valu

e of

vis

ibili

ty is

impo

rtan

t eve