Embed Size (px)

Citation preview

5

Global Retail Trends 2016

DEBORAH WEINSWIG, MANAGING DIRECTOR, FUNG GLOBAL RETAIL & TECHNOLOGY [email protected] US: 917.655.6790 HK: 852.6119.1779 CN: 86.186.1420.3016 Copyright © 2016 The Fung Group. All rights reserved.

GLOBAL RETAIL TRENDS UPDATE Smarter malls, online fashion resale, loyalty programs, off-‐price shopping and 12 other trends will influence the retail industry and play a larger role in everyday life in 2016. In this report, our analysts identify and outline these 16 trends and share their thinking on what to watch for this year and why.

SUSTAINABILITY AND ETHICS: YOU ARE WHAT YOU BUY Socially conscious retailers that sell sustainably produced, ethically sourced products will perform well, especially among millennials. Etsy, Reformation, TOMS and Warby Parker are leading the way in ethical retailing.

What It Is Consumers are increasingly looking for products and services that provide them with trustworthy information, reflect a mission to do good, and are produced using socially conscious and ethical practices. This trend is primarily driven by millennials, who are likely to choose brands that reflect their values and personalities. Demand for sustainable products will grow in importance as millennials mature in the marketplace and increase their spending power.

Why It Is a Trend Millennials weigh corporate responsibility and sustainability more heavily in their purchasing decisions than do other generations. Information on ethically sourced products used to be hard to come by, but technology now puts such information at consumers’ fingertips and democratizes access to niche products.

• Apps such as GoodGuide, Buycott and aVOID (billed as a “plug-‐in for fair online shopping”) allow users to scan barcodes in order to get detailed information about how a product is made and whether any ethical issues are related to the product or the seller.

More retailers will adopt sustainability practices as they strive to satisfy younger consumers’ demand for ethically sourced products and transparent business practices.

1

6

Global Retail Trends 2016

DEBORAH WEINSWIG, MANAGING DIRECTOR, FUNG GLOBAL RETAIL & TECHNOLOGY [email protected] US: 917.655.6790 HK: 852.6119.1779 CN: 86.186.1420.3016 Copyright © 2016 The Fung Group. All rights reserved.

• Etsy, the online marketplace and community for handcrafted goods, is also designated as a B Corporation, which means it has earned a certificate for adhering to “the highest standard for socially responsible businesses.” The company registered year-‐over-‐year growth in gross merchandise sales of 21.7% in the third quarter of 2015 and revenue growth of 37.9%.

• Fashion brand Reformation designs and manufactures sustainable apparel, sourcing sustainable fabrics and vintage garments. Meanwhile, TOMS and Warby Parker have both successfully employed a “one for one” business model in which they give away one pair of shoes (TOMS) or one pair of eyeglasses (Warby Parker) for every pair sold.

• Social innovation hubs, such as the Impact Hub and the Good Lab in Hong Kong, provide social entrepreneurs with resources, inspiration and collaboration opportunities to help them expand their impact.

• In the food and beverage segment, Shake Shack is winning over millennials with a local sourcing strategy, while Panera Bread announced that it would remove all artificial colors, flavors, sweeteners and preservatives from its menu by the end of 2016.

What to Expect More retailers will adopt sustainability initiatives in order to create a brand that satisfies the younger generation’s demand for socially conscious products and practices. Locally sourced products and handmade and crafted goods are the categories that stand to benefit most from the sustainability trend, and they will likely perform well.

“THE INSTAGRAM EFFECT” BOOSTS THE EXPERIENCE ECONOMY Consumers in the US and Europe are showing a willingness to grow their spending on leisure services more than on retail categories. We see two factors underpinning this: social media is increasing pressure on consumers to be perceived as leading “fun” lives, and mobile connectivity is making finding and booking leisure services easier than ever. Retailers will likely need to face up to a lower-‐growth future in light of this trend.

What It Is

Over the past several years, US consumers have been growing their spending on services such as dining out at the expense of retail categories such as apparel. A recent downturn in clothing sales and general retail weakness in the UK suggests this trend may be crossing the Atlantic.

Millennials lead this trend, preferring to attend live events, travel and dine at hip venues instead of spending on goods. We see social media fueling this trend, as people increasingly want to be seen doing “interesting stuff.” Many seek out fun experiences and enthusiastically record and share them on their social networks.

We see social media fueling the experience economy, as people increasingly want to be perceived as living lives that are “fun” and “interesting.”

2

7

Global Retail Trends 2016

DEBORAH WEINSWIG, MANAGING DIRECTOR, FUNG GLOBAL RETAIL & TECHNOLOGY [email protected] US: 917.655.6790 HK: 852.6119.1779 CN: 86.186.1420.3016 Copyright © 2016 The Fung Group. All rights reserved.

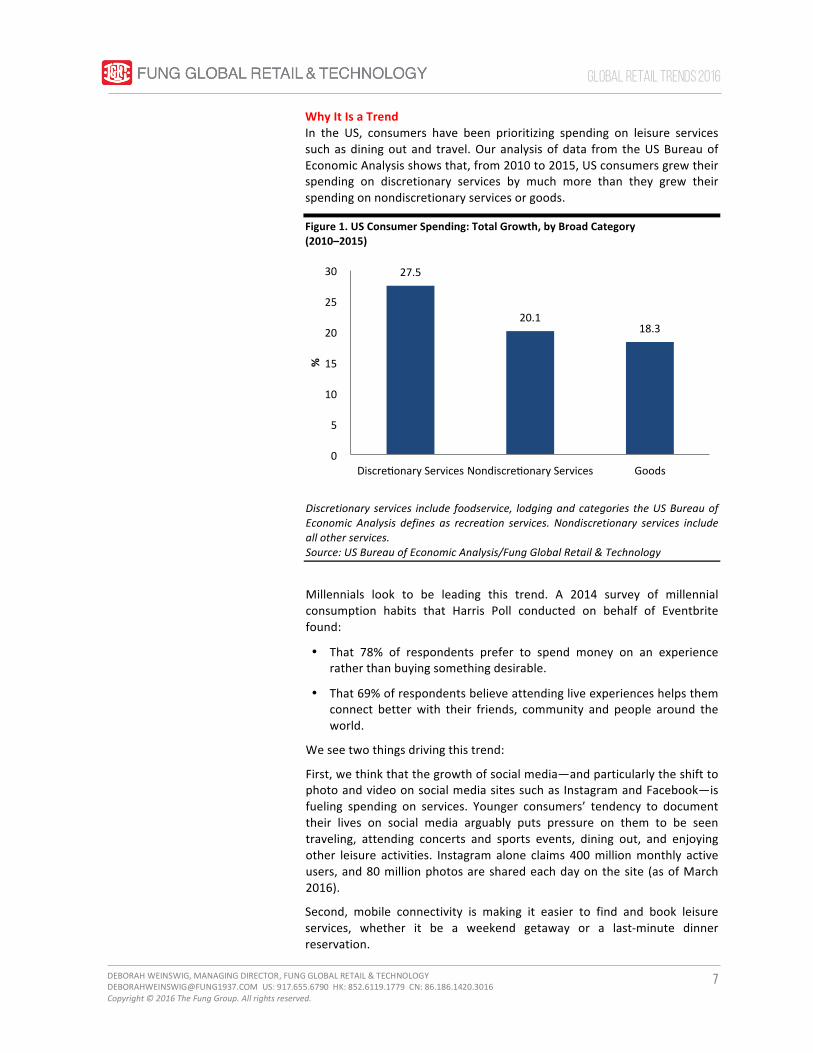

Why It Is a Trend In the US, consumers have been prioritizing spending on leisure services such as dining out and travel. Our analysis of data from the US Bureau of Economic Analysis shows that, from 2010 to 2015, US consumers grew their spending on discretionary services by much more than they grew their spending on nondiscretionary services or goods.

Figure 1. US Consumer Spending: Total Growth, by Broad Category (2010–2015)

Discretionary services include foodservice, lodging and categories the US Bureau of Economic Analysis defines as recreation services. Nondiscretionary services include all other services. Source: US Bureau of Economic Analysis/Fung Global Retail & Technology

Millennials look to be leading this trend. A 2014 survey of millennial consumption habits that Harris Poll conducted on behalf of Eventbrite found:

• That 78% of respondents prefer to spend money on an experience rather than buying something desirable.

• That 69% of respondents believe attending live experiences helps them connect better with their friends, community and people around the world.

We see two things driving this trend:

First, we think that the growth of social media—and particularly the shift to photo and video on social media sites such as Instagram and Facebook—is fueling spending on services. Younger consumers’ tendency to document their lives on social media arguably puts pressure on them to be seen traveling, attending concerts and sports events, dining out, and enjoying other leisure activities. Instagram alone claims 400 million monthly active users, and 80 million photos are shared each day on the site (as of March 2016).

Second, mobile connectivity is making it easier to find and book leisure services, whether it be a weekend getaway or a last-‐minute dinner reservation.

27.5

20.1 18.3

0

5

10

15

20

25

30

Discrekonary Services Nondiscrekonary Services Goods

%

8

Global Retail Trends 2016

DEBORAH WEINSWIG, MANAGING DIRECTOR, FUNG GLOBAL RETAIL & TECHNOLOGY [email protected] US: 917.655.6790 HK: 852.6119.1779 CN: 86.186.1420.3016 Copyright © 2016 The Fung Group. All rights reserved.

A number of startups are catering to and facilitating these changing consumption habits:

• Gigzolo is a curated network of musicians and DJs available for hire for events.

• Zaptravel is a digital travel agent that uses a semantic search engine to scroll through its database.

• IfOnly is an online marketplace for unique experiences that range in price from $50 to $5,000.

• Apps such as Fever and YPlan allow consumers to discover leisure events and activities in their city.

• More established online and app-‐based booking intermediaries—such as GrubHub, Seamless, Just Eat and Deliveroo in foodservice—are making it easier to spend on services in what are often still-‐fragmented markets.

What to Expect If social media is indeed helping drive spending on services, the continued growth in these sites’ member numbers suggests this will be a sustained trend. So, retailers may need to adjust to a world where consumers continue to prioritize services over goods.

We are not the only ones expecting spending on services to grow substantially. Mintel, in its American Lifestyles 2015 report, forecasts that US spending on vacations and tourism will outpace spending on all other categories in the five years to 2019, increasing by 27%, and that spending on dining out will grow by just under 27%. In contrast, total US consumer spending will grow by just under 22% across the forecast period, Mintel predicts.

Finally, while millennials currently look to be leading this trend, we think it will soon trickle down to other demographic groups as older generations continue to adopt smartphone technology and social media.

9

Global Retail Trends 2016

DEBORAH WEINSWIG, MANAGING DIRECTOR, FUNG GLOBAL RETAIL & TECHNOLOGY [email protected] US: 917.655.6790 HK: 852.6119.1779 CN: 86.186.1420.3016 Copyright © 2016 The Fung Group. All rights reserved.

THE SILVER ECONOMY: AN AGING, CONNECTED POPULATION WILL BOOST HEALTH TECH AND SERVICES Retailers will focus more heavily on the fast-‐growing “silver” demographic, developing technologies, goods and services that specifically target consumers aged 65 or older. Investment in telehealth, wearable devices and other health technologies will increase.

What It Is Silvers are consumers aged 65 and over, and they constitute nearly 23% of the world’s population, or 1.7 billion people. Data from the United Nations suggest that the cohort will grow 2.5 times as fast as the total global population from 2016 to 2050. In developed countries, this group accounts for a disproportionate percentage of spending relative to its share of the population, which presents an attractive opportunity for retailers and brands that can market products and services that meet the aging population’s needs. Data from the US Federal Reserve’s 2013 Survey of Consumer Finances indicate that people aged 55 and older control more than three-‐fourths of America’s household wealth of $81.5 trillion.

The graph below shows United Nations growth forecasts for the 60+ population.

Figure 2. Global Population Projections

Source: UN Department of Economic and Social Affairs, Population Division: World Population Prospects: The 2015 Revision/International Labour Organization, World Social Protection Report 2014–15

901 1,402

6,448

7,099

12.3

16.5

0

2

4

6

8

10

12

14

16

18

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

2026

2027

2028

2029

2030

%

Mil.

60+ Populakon (Lep Axis)

Under 60 Populakon (Lep Axis)

60+ as % of Total Populakon (Right Axis)

Silvers face unique challenges in using new digital devices, and they are an underserved market when it comes to fashion and apparel.

3

10

Global Retail Trends 2016

DEBORAH WEINSWIG, MANAGING DIRECTOR, FUNG GLOBAL RETAIL & TECHNOLOGY [email protected] US: 917.655.6790 HK: 852.6119.1779 CN: 86.186.1420.3016 Copyright © 2016 The Fung Group. All rights reserved.

Why It Is a Trend

The older population is growing and becoming more connected:

• According to data from the United Nations, the number of people aged 50 or older has reached 1.64 billion globally, while the number of people aged 65 or older has reached 608 million globally. The latter group has doubled in size over the last three decades, and it continues to grow rapidly.

• Fung Global Retail & Technology estimates that, in 2015, consumers aged 65 and older spent around $7 trillion globally on goods and services, representing a little over 17% of total worldwide consumer spending. Seniors will account for around $10 trillion in consumer spending in 2020, or approximately 19% of the worldwide total, we estimate, based on population projections from the United Nations and total spending data from Euromonitor International.

• Our estimates suggest that seniors accounted for around 16.1%, or $1.3 trillion, of healthcare spending globally in 2015. Our figures are approximate, and based on from data for the US, the UK and Japan and total healthcare spending figures from the World Bank.

• A growing proportion of seniors are using the Internet. In the US, 58% of seniors aged 65 or older are online; in Europe, 41% of seniors aged 65 to 74 are online. Smartphone usage is growing among seniors, too. According to UK communications regulator Ofcom, smartphone ownership among those aged 65 or older in the UK increased from 5% in 2012 to 18% in 2015.

The health tech market is also being driven by advances in technology, including the Internet of Things (IoT), and by the rising cost of seniors’ healthcare, with businesses and governments motivated to limit costs through new technologies.

Notable health tech products include smart inhalers from Novartis; the MocaHeart cardiovascular tracker from MocaCare; the VitalSnap health data recorder from Validic; and BodyGuardian, a wearable health monitor. Adjacent products and services include Honor, an online marketplace that brings seniors and caregivers together, and GrandCare’s remote monitoring systems.

11

Global Retail Trends 2016

DEBORAH WEINSWIG, MANAGING DIRECTOR, FUNG GLOBAL RETAIL & TECHNOLOGY [email protected] US: 917.655.6790 HK: 852.6119.1779 CN: 86.186.1420.3016 Copyright © 2016 The Fung Group. All rights reserved.

And in telehealth services (i.e., remote healthcare that is provided through video calls), we have seen new firms such as Doctor On Demand and Pager join more established firms such as Teladoc in what is a growing market.

Figure 3. Global Revenue: Telehealth Devices and Services (USD Bil.)

Source: IHS

What to Expect

The silver economy is a growth area for numerous categories, but the demand for healthcare will drive health tech and telehealth in particular. There will also likely be a crossover at some point between connected homes and senior care, as smart home devices will enable better remote monitoring of seniors and their health. In fact, health tech’s role in administering healthcare could be key to driving down overall costs. As the senior population continues to grow, cost will become a matter of growing concern to those who pay for seniors’ healthcare: private companies and their paying customers, and governments and their taxpayers.

We expect more firms, both established and new, to innovate and so tackle the challenges and costs associated with an aging population.

0.44 0.70

1.12

1.78

2.83

4.50

$0

$1

$2

$3

$4

$5

2013 2014 2015 2016F 2017F 2018F

12

Global Retail Trends 2016

DEBORAH WEINSWIG, MANAGING DIRECTOR, FUNG GLOBAL RETAIL & TECHNOLOGY [email protected] US: 917.655.6790 HK: 852.6119.1779 CN: 86.186.1420.3016 Copyright © 2016 The Fung Group. All rights reserved.

BUYING FOR BABY: CHINA’S SECOND-CHILD BOOM IS COMING Purchases for expectant moms and new little siblings will likely increase in China as the country’s one-‐child policy is lifted this year.

What It Is The one-‐child policy imposed in 1979 by the Chinese government is in the process of being lifted. This means that couples in China can have two children without being fined. In the long run, this will likely help relieve China’s aging population problem; in the short run, it is expected to boost the economy.

Figure 4. Projected Population Growth in China

Source: The New York Times/United Nations Population Division/Kristin Bietsch, Population Reference Bureau

The baby boom in China will initially impact the sales of maternity clothes and mother care goods.

4

13

Global Retail Trends 2016

DEBORAH WEINSWIG, MANAGING DIRECTOR, FUNG GLOBAL RETAIL & TECHNOLOGY [email protected] US: 917.655.6790 HK: 852.6119.1779 CN: 86.186.1420.3016 Copyright © 2016 The Fung Group. All rights reserved.

Why It Is a Trend Lifting the one-‐child policy makes 90 million couples in China eligible to have a second child. Experts predict a second-‐child boom, with the number of newborns increasing by 3 million to 8 million each year.

Even under the one-‐child policy, the childcare market was a huge business in China. According to BaoBei360, the 0–12-‐year-‐old childcare market was worth about $178 billion in 2013. In terms of industries, the second-‐child boom will benefit a wide range of categories, including food and dairy (over 75% of Chinese mothers use infant formula to feed their babies); healthcare (mother and baby care products); garments (baby and maternity clothes); automotive (families purchasing their first car or switching to a larger SUV or MPV); and education (private education starts with play groups for children as young as six months in China).

Figure 5. China: Child-‐Related Consumption of Total Family Daily Expenditure, December 2014

Figure 6. China: Breakdown of Child-‐Related Consumption, by Category, December 2014

Source: Insite/Fung Global Retail & Technology

What to Expect The first wave of the second-‐child boom is expected in 2017, but the impact on consumption could hit this year, driven mainly by expectant parents purchasing mother care products and maternity clothes. Given the surging cost of living in China, the second-‐child boom might be limited to the emerging middle class. This demographic is mostly located in top-‐tier cities such as Beijing, Shanghai and Guangzhou and in rapidly developing second-‐tier cities in the coastal areas. Families in this group tend to have higher incomes and more spending power, which will enable many of them to raise a second child. Their above-‐average purchasing power also means that they will look for higher-‐quality products, especially given recent product safety scandals, such as the 2009 Chinese milk scandal.

33%

8.8%

10.4%

18.8%

24.4%

37.6%

0% 5% 10% 15% 20% 25% 30% 35% 40%

Toys

Entertainment

Apparel

Food and Beverage

Educakon

14

Global Retail Trends 2016

DEBORAH WEINSWIG, MANAGING DIRECTOR, FUNG GLOBAL RETAIL & TECHNOLOGY [email protected] US: 917.655.6790 HK: 852.6119.1779 CN: 86.186.1420.3016 Copyright © 2016 The Fung Group. All rights reserved.

IMPROVEMENT: FROM DIY TO DIFM The housing market in the US looks set for a strong run. Annual household formation is forecast to be well above 1 million, and comfortably above the long-‐term average, in both 2016 and 2017.

What It Is

In theory, do-‐it-‐yourself (DIY) stores should be enjoying boom times, not just in the US, but also in robust European property markets. In reality, however, structural changes mean consumer-‐focused DIY retailers are likely to underperform versus the housing markets over the medium term. Shoppers in mature markets are shifting more toward “do it for me” (DIFM), where they pay tradespeople to do home maintenance for them instead of doing it themselves.

Why It Is a Trend

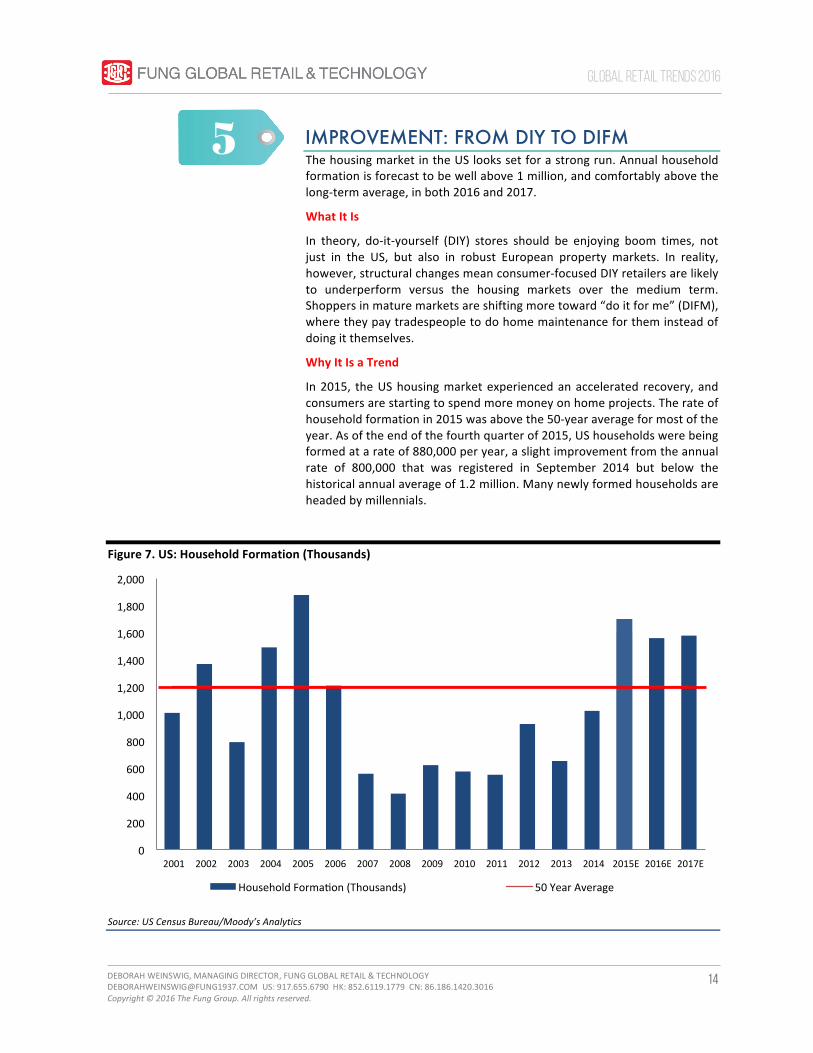

In 2015, the US housing market experienced an accelerated recovery, and consumers are starting to spend more money on home projects. The rate of household formation in 2015 was above the 50-‐year average for most of the year. As of the end of the fourth quarter of 2015, US households were being formed at a rate of 880,000 per year, a slight improvement from the annual rate of 800,000 that was registered in September 2014 but below the historical annual average of 1.2 million. Many newly formed households are headed by millennials.

Figure 7. US: Household Formation (Thousands)

Source: US Census Bureau/Moody’s Analytics

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015E 2016E 2017E

Household Formakon (Thousands) 50 Year Average

5

15

Global Retail Trends 2016

DEBORAH WEINSWIG, MANAGING DIRECTOR, FUNG GLOBAL RETAIL & TECHNOLOGY [email protected] US: 917.655.6790 HK: 852.6119.1779 CN: 86.186.1420.3016 Copyright © 2016 The Fung Group. All rights reserved.

Demographic and consumer shifts mean the buoyant property markets of the US and some major European economies will not translate to strong growth for DIY stores. The DIFM trend is being driven largely by the aging of populations in Western Europe and North America, where affluent older consumers are looking more to professionals to do work for them. At the same time, many younger shoppers appear to be less familiar with DIY techniques than previous generations were, and so are likely to need professional help with home projects.

And specific markets are facing particular changes. In the UK, home ownership is becoming much more skewed toward older generations, with millennials—“generation rent”—less likely than previous generations to own their own home. In the US, growth in multifamily households is helping drive demand for home improvement services.

The most obvious result of the DIFM trend for DIY retailers is a loss of share of total home-‐improvement spending: professionals tend to turn to specialist business-‐to-‐business suppliers rather than to consumer-‐positioned DIY stores for their needs.

What to Expect

We see two trends playing out among major DIY retail groups. First, these groups are chasing the professional customer. When we attended Home Depot’s analyst day in December, the pursuit of this customer was a recurring theme. The company noted a number of initiatives it had undertaken in pursuit of the business: it had reorganized in order to have one team dedicated to the needs of professionals; it had acquired Interline, a seller of products to trade customers, which should bolster its penetration among professionals; and it had worked on developing delivery and credit options, sales reps, and a loyalty program focused on trade customers.

Second, big consumer-‐focused DIY chains are not limited to serving professional customers; they can compete with them, too. We expect to see more home maintenance services being offered by big, trusted DIY retail names. These companies can attempt to grab share of the home maintenance services market, which offers the prospect of fatter margins and which tends to be dominated by small traders.

The home maintenance market is a growth market, but its nature is changing. Mature DIY retailers can find opportunities to tap, if their product offerings are convincing enough to win professional customers and their services appeal sufficiently to consumers.

16

Global Retail Trends 2016

DEBORAH WEINSWIG, MANAGING DIRECTOR, FUNG GLOBAL RETAIL & TECHNOLOGY [email protected] US: 917.655.6790 HK: 852.6119.1779 CN: 86.186.1420.3016 Copyright © 2016 The Fung Group. All rights reserved.

PREMIUM LIFESTYLE BRANDS SET TO OUTPERFORM Premium brands that connote a certain type of lifestyle should remain strong in 2016.

What It Is “Lifestyle brands” are those characterized by premium, aspirational positioning and distinct designs, among other things. The most successful, such as Lululemon and Ted Baker, have performed strongly, and we expect this to continue in 2016. We see opportunities for premium lifestyle brands to further diversify, including into services, in order to create 360-‐degree brands that truly deliver lifestyle experiences.

Why It Is a Trend Although more consumers than ever will buy into the budget segment, we expect lifestyle brands, which are more premium-‐positioned, to gain in 2016. We define lifestyle brands as those combining several characteristics:

• A premium, aspirational brand identity that suggests a certain quality of lifestyle. These are not luxury brands; they are more moderately priced and so more attainable, and they are also often younger than heritage luxury brands.

• A product offering with distinct design characteristics. These brands can often be recognized by their design, which many customers like to be seen wearing, using or carrying.

• Many of the most successful lifestyle brands have expanded beyond their core, original category. For instance, Ted Baker has moved into electronics and Cath Kidston has diversified into homewares.

• A further feature of the biggest, most successful lifestyle brands is vertical integration: they operate their own monobrand stores as well as wholesaling through third-‐party retailers. By controlling the retail experience more tightly, this vertical integration provides a further means through which to build the brand.

Figure 8. Features of Successful Lifestyle Brands

Source: Fung Global Retail & Technology

Verkcal Integrakon

Category Diversificakon

Disknct Designs

Premium Posikoning

We see opportunities for premium brands to further diversify, including into services, in order to create 360-‐degree brands that truly deliver lifestyle experiences.

6

17

Global Retail Trends 2016

DEBORAH WEINSWIG, MANAGING DIRECTOR, FUNG GLOBAL RETAIL & TECHNOLOGY [email protected] US: 917.655.6790 HK: 852.6119.1779 CN: 86.186.1420.3016 Copyright © 2016 The Fung Group. All rights reserved.

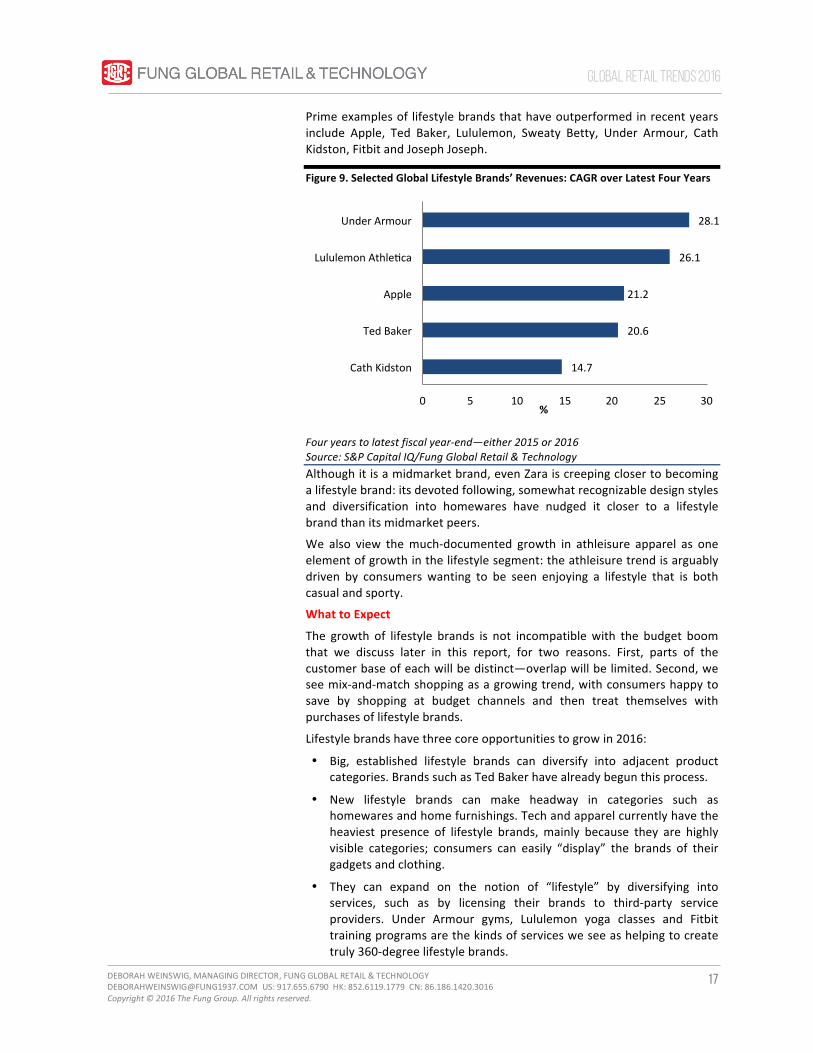

Prime examples of lifestyle brands that have outperformed in recent years include Apple, Ted Baker, Lululemon, Sweaty Betty, Under Armour, Cath Kidston, Fitbit and Joseph Joseph.

Figure 9. Selected Global Lifestyle Brands’ Revenues: CAGR over Latest Four Years

Four years to latest fiscal year-‐end—either 2015 or 2016 Source: S&P Capital IQ/Fung Global Retail & Technology Although it is a midmarket brand, even Zara is creeping closer to becoming a lifestyle brand: its devoted following, somewhat recognizable design styles and diversification into homewares have nudged it closer to a lifestyle brand than its midmarket peers.

We also view the much-‐documented growth in athleisure apparel as one element of growth in the lifestyle segment: the athleisure trend is arguably driven by consumers wanting to be seen enjoying a lifestyle that is both casual and sporty.

What to Expect

The growth of lifestyle brands is not incompatible with the budget boom that we discuss later in this report, for two reasons. First, parts of the customer base of each will be distinct—overlap will be limited. Second, we see mix-‐and-‐match shopping as a growing trend, with consumers happy to save by shopping at budget channels and then treat themselves with purchases of lifestyle brands.

Lifestyle brands have three core opportunities to grow in 2016:

• Big, established lifestyle brands can diversify into adjacent product categories. Brands such as Ted Baker have already begun this process.

• New lifestyle brands can make headway in categories such as homewares and home furnishings. Tech and apparel currently have the heaviest presence of lifestyle brands, mainly because they are highly visible categories; consumers can easily “display” the brands of their gadgets and clothing.

• They can expand on the notion of “lifestyle” by diversifying into services, such as by licensing their brands to third-‐party service providers. Under Armour gyms, Lululemon yoga classes and Fitbit training programs are the kinds of services we see as helping to create truly 360-‐degree lifestyle brands.

14.7

20.6

21.2

26.1

28.1

0 5 10 15 20 25 30

Cath Kidston

Ted Baker

Apple

Lululemon Athlekca

Under Armour

%

18

Global Retail Trends 2016

DEBORAH WEINSWIG, MANAGING DIRECTOR, FUNG GLOBAL RETAIL & TECHNOLOGY [email protected] US: 917.655.6790 HK: 852.6119.1779 CN: 86.186.1420.3016 Copyright © 2016 The Fung Group. All rights reserved.

REFOCUSING LUXURY: CHINESE STILL BUY, BUT OVERSEAS Luxury brands have been hit by softening demand inside China. However, Chinese consumers have continued to buy abroad, and we expect this to continue through 2016.

What It Is The luxury market took a hit in China and Hong Kong in 2015, but growth in overseas luxury purchases by Chinese travelers remained strong. This bifurcation will continue in 2016, not least because outbound traveler numbers are expected to continue to grow significantly. Within China, major luxury brands may respond by shutting stores, cutting prices and focusing more heavily on digital channels.

Why It Is a Trend Chinese customers led eight years of consecutive growth in luxury spending in Asia, but the tide turned in 2014, and 2015 was another tough year. In Mainland China, luxury spending fell by 2% in 2015, according to Bain & Company’s annual report on global luxury retailing, while in Hong Kong and Macau, it fell by fully 25% during the year.

Yet demand from Chinese consumers traveling internationally remained buoyant, with overseas sales up 10% year over year. Surging luxury sales to Chinese tourists in Japan were underpinned by beneficial currency effects, but even in the US and Europe, Chinese travelers continued to spend big on high-‐end products, according to Bain. Global Blue, a tax-‐refund company, found that Chinese tax-‐free purchases (including nonluxury purchases) increased by 64% in Europe.

Chinese demand for luxury goods will remain bifurcated in 2016: overseas growth will likely remain substantially stronger than domestic demand, even if domestic demand turns positive. The simple reason for this is that outbound traveler numbers are expected to continue to grow significantly. So, even if per-‐traveler retail spending stays level or declines slightly, total overseas spending on luxury goods will increase in 2016.

Figure 10. Outbound Chinese Traveler Numbers and YoY % Change

Source: China Statistical Yearbook/Fung Global Retail & Technology

57 70

83 98

107 115 123

0.0

5.0

10.0

15.0

20.0

25.0

0

50

100

150

200

2010 2011 2012 2013 2014 2015E 2016E

YoY % Change

Million

Traveler Numbers (Lep Axis) YoY % Change (Right Axis)

7

19

Global Retail Trends 2016

DEBORAH WEINSWIG, MANAGING DIRECTOR, FUNG GLOBAL RETAIL & TECHNOLOGY [email protected] US: 917.655.6790 HK: 852.6119.1779 CN: 86.186.1420.3016 Copyright © 2016 The Fung Group. All rights reserved.

Overseas spending will be underpinned by the relaxation of visa requirements in some countries, such as the UK, and by Chinese shoppers buying in Japan in order to beat a planned sales tax hike that Japan will implement in April 2017.

What to Expect

The latest results from major luxury brands suggest that the Chinese slump may have already reached its nadir: Burberry and Tod’s have both recently noted an improvement in Mainland Chinese demand, while the latest figures from Richemont suggest its declines are easing. But, even if this easing continues in 2016, the Chinese domestic market will likely remain a long way from its heyday of strong growth.

And after years of tapping growth in Mainland China through aggressive store-‐opening plans, some major luxury brands are now reconsidering their space needs. According to Bloomberg, luxury giant LVMH said in late 2015 that it would review eight stores in second-‐tier cities in China, equivalent to around one-‐fifth of its total network in the country.

Luxury brands could follow one of three scenarios as they adapt to this changing demand:

1. Follow LVMH’s lead and reshape their Mainland China store portfolios, particularly in smaller cities.

2. Follow Chanel and Gucci in cutting prices in China to reduce the disparity with other regions (a 2015 cut in import taxes makes it easier for brands to do this).

3. Focus more heavily on e-‐commerce to serve Chinese consumers. Bain noted that online shopping contributed to falling sales of luxury goods in Chinese stores in 2015, and Burberry recently noted the outperformance of its digital channels. Meanwhile, Tod’s stated that it was paying increasing attention to e-‐commerce.

If the robust demand for luxury goods in China does not return, big luxury brands may have a smaller presence in the country, and work to become more digitally adept by the end of the year.

And although strong outbound traveler numbers will sustain total international luxury spending by Chinese consumers, retailers in the US will likely continue to be negatively impacted by the strength of the dollar.

20

Global Retail Trends 2016

DEBORAH WEINSWIG, MANAGING DIRECTOR, FUNG GLOBAL RETAIL & TECHNOLOGY [email protected] US: 917.655.6790 HK: 852.6119.1779 CN: 86.186.1420.3016 Copyright © 2016 The Fung Group. All rights reserved.

GLOBAL WAVE OF BUDGET FORMAT EXPORTS UNDERPINS THE DISCOUNT BOOM Budget retailing will continue to grow as a “new wave” of globalized discount retailers drives higher standards in the sector.

What It Is The biggest budget retailers, including grocery, apparel and general merchandise sellers, are flourishing—and expanding into new markets. The key to their success is not simply low prices; they are raising standards in discount retailing and thus drawing in more shoppers.

Why It Is a Trend The budget boom was a major theme of 2015, and the trend is not likely to abate. In apparel, Primark launched in the US in September, announcing that it will eventually open eight stores. Other value-‐positioned apparel players, such as H&M and boohoo.com, continue to grow strongly. These retailers unite low prices and fashionable offerings, catering to younger shoppers’ appetite for short-‐lived but stylish clothing.

In the US, off-‐price has been another element in the discount apparel boom, bringing more brands to the discount segment. In 2015, Macy’s launched its off-‐price Backstage concept, with plans for around 50 stores; Kohl’s unveiled its Off-‐Aisle concept; Hudson’s Bay Company announced its Find @ Lord & Taylor format; and Nordstrom opened 27 new off-‐price Nordstrom Rack stores across its first three quarters.

Now, Hudson’s Bay Company is set to bring its off-‐price concept, Saks Off 5th, to Germany. This will create the first major rival for TK Maxx in the underdeveloped European off-‐price segment.

In grocery, Aldi and Lidl continue their global expansion. Lidl stated it will join Aldi in the US market in 2018, and some speculate that it could be even sooner. Aldi and Lidl have built recent success by adding stores and flexing their hard-‐discount proposition. New store formats that are tailored to specific markets and improved food offerings have made these retailers’ discount grocery stores appeal to more consumers. Schwarz Group, which owns Lidl, and Aldi have both grown their total revenue solidly in recent years; if this trend continues, they will collectively be turning over more than €200 billion (US$225 billion) annually by 2020.

As discount retailers continue to shake off their down-‐market image, they will become not only a respectable alternative to midmarket rivals, but also destination stores in and of themselves.

8

21

Global Retail Trends 2016

DEBORAH WEINSWIG, MANAGING DIRECTOR, FUNG GLOBAL RETAIL & TECHNOLOGY [email protected] US: 917.655.6790 HK: 852.6119.1779 CN: 86.186.1420.3016 Copyright © 2016 The Fung Group. All rights reserved.

Figure 11. Schwarz Group (Lidl and Kaufland) and Aldi: Estimated Revenue Growth

Source: Euromonitor International/company reports/Fung Global Retail & Technology

A key feature of the discount boom is the internationalization of the most successful formats, led by European and US retailers expanding into new markets. In some markets, these retailers are providing strong competition for more established, and often less exceptional, discount retailers.

What to Expect Budget retailers have been successful where they have innovated and raised standards, and this will likely continue through 2016. More brands will pursue growth through grocery discounters, mixed-‐goods discount shops and off-‐price stores, and stores across these sectors—from flagships at Primark to concept stores at Lidl to online ventures by Aldi—will continue to improve the customer experience.

We also continue to see “white space” opportunities, such as the off-‐price segment in Europe, where TK Maxx has been the only major player.

As a result of the raising of standards, we expect more shoppers than ever to turn to discount stores in 2016. As discount retailers continue to shake off their down-‐market image, they will become not only a respectable alternative to midmarket rivals, but also destination stores in and of themselves. This year, we will get closer to the point where every shopper is a budget shopper.

59.8 63.3 67.6

74.0 79.3 85.2

91.5 98.3

105.7 113.5

122.0

49.4 51.5 55.3 58.2 60.8 63.7 66.8 70.0 73.4 76.9 80.6

0

30

60

90

120

150

2010

2011

2012

2013

2014

2015E

2016E

2017E

2018E

2019E

2020E

€ Bil.

Schwarz Group

Aldi

Figure 12. Selected Exported Budget Retail Formats

Primark: UK to Europe and US

Off-‐Price: US to Europe

Grocery Discounters:

Germany to UK and US

Source: Fung Global Retail & Technology

22

Global Retail Trends 2016

DEBORAH WEINSWIG, MANAGING DIRECTOR, FUNG GLOBAL RETAIL & TECHNOLOGY [email protected] US: 917.655.6790 HK: 852.6119.1779 CN: 86.186.1420.3016 Copyright © 2016 The Fung Group. All rights reserved.

ONLINE FASHION RESALE: GUILT-FREE BUYING Online marketplaces for secondhand apparel will continue to thrive, offering a consistent mix of branded goods in verified “like new” condition at large discounts to retail prices.

What It Is Online marketplaces for secondhand apparel were a big story in 2015, and they will continue to thrive. Driven by the growth of the sharing economy and facilitated by advances in technology and logistics, the online consignment model is capitalizing on consumers who historically had reservations about purchasing secondhand fashion. Upfront Ventures, one of the investors in online consignment platform ThredUP, highlights the following findings from its research, which underlie the rationale behind online consignment:

• In the US, 70% of the items in the average woman’s closet go unworn each year.

• The average American generates 60 pounds of apparel to be recycled annually.

• Parents will recycle more than 1,800 items on average by the time their child turns 18.

There is a big imbalance in the way people consume clothing, and online fashion resellers are looking to fix the equation. These retailers offer a consistent mix of branded products in verified like-‐new condition at large discounts to retail prices.

Why It Is a Trend In the US, the online consignment market includes startups such as ThredUP, The RealReal, Tradesy, Twice and Swap.com. The size of the online resale industry is estimated to be $34 billion, according to ThredUP, and SnobSwap estimates that the market is growing at a compound annual growth rate of 10%. Patagonia, Eileen Fisher and H&M are also running their own resale programs.

Driven by the growth of the sharing economy, the online consignment model is attracting consumers who historically had reservations about purchasing secondhand fashion.

9

23

Global Retail Trends 2016

DEBORAH WEINSWIG, MANAGING DIRECTOR, FUNG GLOBAL RETAIL & TECHNOLOGY [email protected] US: 917.655.6790 HK: 852.6119.1779 CN: 86.186.1420.3016 Copyright © 2016 The Fung Group. All rights reserved.

• ThredUP raised $81 million in series E funding in September 2015, led by Goldman Sachs Investment Partners, bringing the company’s total capital raised to over $131 million. ThredUP saw significant user growth before its latest investment round, reporting that its site visitor numbers had grown from 700,000 in 2014 to 1.8 million in the first eight months of 2015.

• In April 2015, luxury consignment site The RealReal raised $40 million in funding. Tradesy secured $30 million in funding in January 2015.

• In December 2014, e-‐commerce company Rent the Runway raised $60 million, bringing its total funding to $114.4 million.

• Smaller consignment players Threadflip and Bib + Tuck were acquired by Le Tote and Crossroads Trading, respectively, showing that consolidation in the space has already started.

What to Expect The online consignment business model is clearly favored by venture capital investors, and 2016 will likely be a key year for this business sector. We see rapid growth for the leading marketplaces and will not be surprised if some of it comes through acquisitions as the industry consolidates.

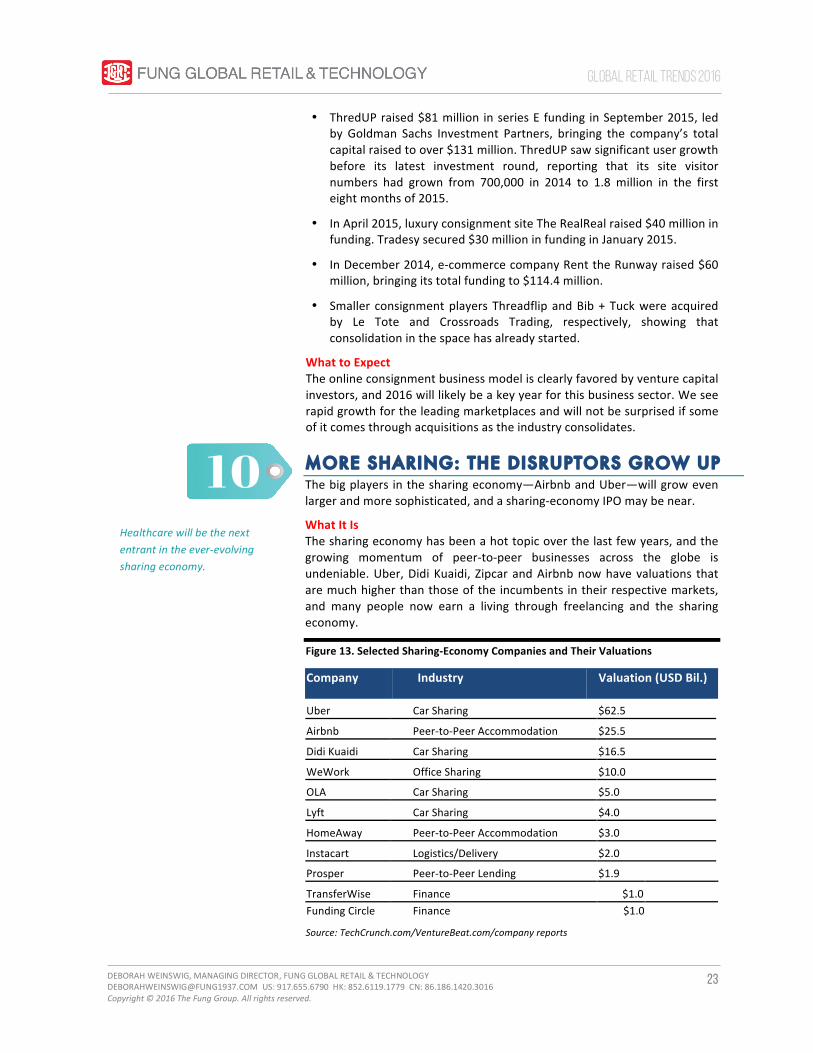

MORE SHARING: THE DISRUPTORS GROW UP The big players in the sharing economy—Airbnb and Uber—will grow even larger and more sophisticated, and a sharing-‐economy IPO may be near.

What It Is The sharing economy has been a hot topic over the last few years, and the growing momentum of peer-‐to-‐peer businesses across the globe is undeniable. Uber, Didi Kuaidi, Zipcar and Airbnb now have valuations that are much higher than those of the incumbents in their respective markets, and many people now earn a living through freelancing and the sharing economy.

Figure 13. Selected Sharing-‐Economy Companies and Their Valuations

Company Industry Valuation (USD Bil.) Uber Car Sharing $62.5 Airbnb Peer-‐to-‐Peer Accommodation $25.5 Didi Kuaidi Car Sharing $16.5 WeWork Office Sharing $10.0 OLA Car Sharing $5.0 Lyft Car Sharing $4.0 HomeAway Peer-‐to-‐Peer Accommodation $3.0

Instacart Logistics/Delivery $2.0 Prosper Peer-‐to-‐Peer Lending $1.9 TransferWise Finance $1.0

Funding Circle Finance $1.0

Source: TechCrunch.com/VentureBeat.com/company reports

Healthcare will be the next entrant in the ever-‐evolving sharing economy.

10

24

Global Retail Trends 2016

DEBORAH WEINSWIG, MANAGING DIRECTOR, FUNG GLOBAL RETAIL & TECHNOLOGY [email protected] US: 917.655.6790 HK: 852.6119.1779 CN: 86.186.1420.3016 Copyright © 2016 The Fung Group. All rights reserved.

Why It Is a Trend • The sharing-‐economy model has continued to make its way across

industries, and healthcare is likely to be the next big industry it disrupts. In the US, startups such as Doctor On Demand, Pager, Studio Dental and MedZed are betting that consumers will eventually be receptive to “uberifying” their doctor visits.

• Leading sharing companies have become more sophisticated in how they service their markets, showing that the sector has started to mature. Airbnb and Uber, for example, have launched separate apps for business and personal customers.

• At the same time, Airbnb and Uber have faced some challenges resulting from their scale, mostly related to ensuring the safety of their customers. In addition, both companies have hit regulation battles in some of their markets, as legislators have been slow to come up with policies governing the peer-‐to-‐peer model and as incumbent competitors have looked for ways to stem their loss of market share.

• PwC estimates that the sharing economy will grow at a compound annual growth rate of 32.6% until 2025, to reach $335 billion.

What to Expect The big players in the sharing economy will become even bigger, and we expect to see strong growth from the leading companies in the sector. This might even be the year of the first big sharing-‐economy IPO, which would set the tone for the rest of the sector; Airbnb is the most likely sharing-‐economy company to go public this year. The most interesting developments will be in the healthcare industry, which is ripe for disruption by an Uber-‐type business.

SMARTER MALLS: USING TECH TO BATTLE COMPETITORS Shopping malls in the US are facing difficulties. As their numbers of visitors continue to decrease, malls will need to become “smarter” in order to attract shoppers.

What It Is In the US, shopping malls face fierce competition in attracting tenants, and the double-‐digit growth of e-‐commerce has worsened the situation. To help differentiate their properties, some developers are upgrading their malls, leveraging technology to make them smarter. China and the US have been at the forefront of technological innovation inside the mall, but shopping center operators in Europe have been experimenting, too, even though they appear not to have been as hit as hard by consumers’ move to online shopping as malls in the US have been.

In the past decade, real estate developers in China have poured billions of dollars into building shopping malls, and mall retail space has grown almost fivefold in the country. In 2014, 44% of all new shopping malls opened globally were in China, which is also home to the world’s largest shopping mall. However, as economic growth in China slows, retailers are becoming more conservative about opening outlets.

Malls will increasingly turn to technology to track consumer behavior, enhance marketing and engage customers.

11

25

Global Retail Trends 2016

DEBORAH WEINSWIG, MANAGING DIRECTOR, FUNG GLOBAL RETAIL & TECHNOLOGY [email protected] US: 917.655.6790 HK: 852.6119.1779 CN: 86.186.1420.3016 Copyright © 2016 The Fung Group. All rights reserved.

In the US, the overall number of malls is declining, but high-‐end malls are striving to succeed. Premium mall operators have been experimenting with technologies that allow them to better understand consumer behavior and traffic flow inside their properties. Some have also deployed location-‐based marketing technologies to improve the shopping experience.

Why It Is a Trend Many companies are actively experimenting with consumer behavior analytics and consumer engagement in China and the US:

• Westfield operates Westfield Labs, a Silicon Valley–based unit that designs and experiments with innovations to improve the retail experience. Many Westfield malls now include touchscreen displays, electronic parking assistance and free wi-‐fi.

• HGTV partnered with Macerich to launch virtual and hands-‐on technology-‐based experiences. Traffic at trial malls was up 45%.

• Simon Venture Group is exploring and investing in retail technology such as data analytics, localized and personalized commerce, and experiential retail.

• RetailNext, a US in-‐store data analytics company, provides real-‐time analysis of shoppers’ movements, behavior and preferences, which mall operators can use to make better business decisions regarding leasing and marketing. The company also formed a strategic alliance with StepsAway, which provides in-‐mall mobile retail solutions, to offer relevant promotions to shoppers and measure their conversion rates.

Many malls are attempting to interact with shoppers digitally via their smartphones or other screens.

• Shanghai’s Cloud Nine and Shenzhen’s SEG Plaza use the social-‐messaging app WeChat for their news and loyalty programs. This helps to create stronger bonds with customers and increase repeat visits to the malls. Such platforms allow malls to engage with customers and extend their relationships with them, even when those customers are not at the mall. In some Macerich and Westfield properties in the US, shoppers can text questions to the mall’s information desk and get answers in real time.

• Mall operator Scentre recently rolled out a customer engagement platform at 27 locations that uses a SmartScreen network of 1,200 interconnected digital screens to show advertisements. The network also utilizes QR codes, near-‐field communication and beacon technology.

Elsewhere, the Westfield San Francisco Centre offers charging stations and free wi-‐fi throughout the mall as well as an experimental co-‐working office that features a space for retail pop-‐up stores. The space is outfitted with wall-‐mounted and mobile touchscreens that brands can use to test products and showcase new technology. Westfield Century City in Los Angeles was the first mall in North America to offer Park Assist, an electronic parking management system that uses a series of lights and signs to reduce the time shoppers spend looking for a parking spot, so they can spend more time shopping.

26

Global Retail Trends 2016

DEBORAH WEINSWIG, MANAGING DIRECTOR, FUNG GLOBAL RETAIL & TECHNOLOGY [email protected] US: 917.655.6790 HK: 852.6119.1779 CN: 86.186.1420.3016 Copyright © 2016 The Fung Group. All rights reserved.

Other malls are taking their customer engagement programs to the next level. Shenzhen Rainbow owns over 30 department stores and shopping malls across China. It recently launched a proprietary app that delivers promotional messages to its members, and it is collaborating with tech giant Baidu to run big data analysis. The company aims to use retail, shopping mall and Baidu search engine data to deliver promotions that match customers’ needs precisely, in order to increase sales conversion for its retailers. Baidu has also announced tie-‐ins with real estate developer China Vanke to work together on 20 new digitally smart malls and with Dalian Wanda to launch one-‐stop-‐shopping app Feifan for in-‐mall use.

US premium malls are also introducing location-‐based marketing. Some US malls have incorporated touchscreen displays, augmented-‐reality selfie videos and other fun digital experiences to better engage shoppers.

What to Expect More shopping malls will apply smart technologies in 2016, as they will be key to maintaining competitiveness and attracting both consumers and retail tenants. Mall operators will also work more closely with their retail partners to enhance the customer experience. We believe there is an opportunity for operators and tenants to share data in order to target the customer on a more personal level.

Beacon technology also continues to offer promise, even though adoption remains persistently low.

Chinese shopping centers are likely to be some of the fastest adopters of smart technologies. More developed markets, such as the US, will pick up the trend, and premium malls will continue to lead innovation in both in-‐store analytics and shopper engagement.

27

Global Retail Trends 2016

DEBORAH WEINSWIG, MANAGING DIRECTOR, FUNG GLOBAL RETAIL & TECHNOLOGY [email protected] US: 917.655.6790 HK: 852.6119.1779 CN: 86.186.1420.3016 Copyright © 2016 The Fung Group. All rights reserved.

RETAILTAINMENT: DRINK, DINE AND DISCOVER Brick-‐and-‐mortar retailers will grow into entertainment destinations in a bid to differentiate themselves from the online shopping experience.

What It Is To help drive in-‐store traffic and provide a more meaningful customer experience, many brick-‐and-‐mortar retailers are adding an element of “retailtainment” to their stores. They are incorporating in-‐store events, more interesting and decorative store interiors, and interactive elements that fully involve customers in a way that is unique to the brand. This allows brands to provide a personal, tangible experience and engage with customers, and gives customers a reason to come back to the physical store even when they can choose to make their purchase online.

Why It Is a Trend RetailNext reported that traffic during the 2015 Thanksgiving weekend decreased by 5.1% in the US, and more and more customers are shopping for and researching products online.

Figure 14. US Thanksgiving Weekend Foot Traffic: YoY % Change

Source: RetailNext In December 2015, traffic continued to decline, decreasing by 5.8% on a year-‐over-‐year basis, even though the average transaction value (ATV) at stores increased by 3.6%.

(1.1)%

(12.4)%

(5.1)%

2013 2014 2015

Brands hope to give customers a reason to come back to the physical store, even though most purchases can now be made online.

12

28

Global Retail Trends 2016

DEBORAH WEINSWIG, MANAGING DIRECTOR, FUNG GLOBAL RETAIL & TECHNOLOGY [email protected] US: 917.655.6790 HK: 852.6119.1779 CN: 86.186.1420.3016 Copyright © 2016 The Fung Group. All rights reserved.

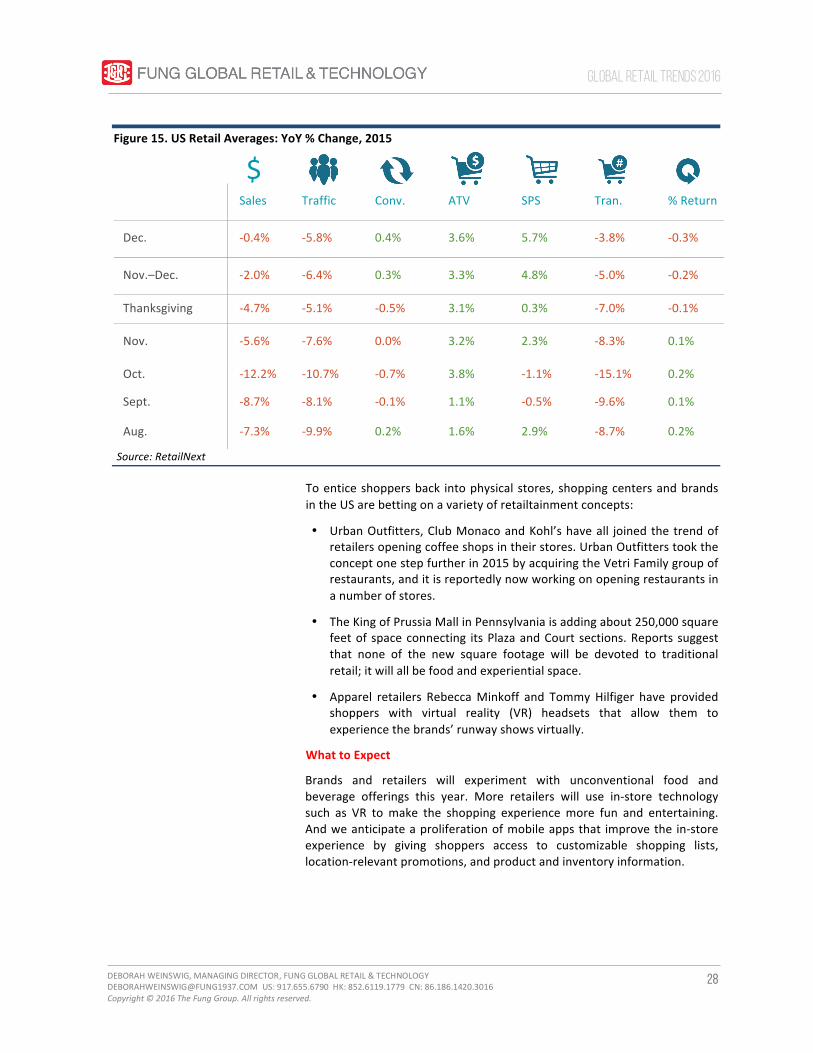

Figure 15. US Retail Averages: YoY % Change, 2015

Sales Traffic Conv. ATV SPS Tran. % Return

Dec. -‐0.4% -‐5.8% 0.4% 3.6% 5.7% -‐3.8% -‐0.3%

Nov.–Dec. -‐2.0% -‐6.4% 0.3% 3.3% 4.8% -‐5.0% -‐0.2%

Thanksgiving -‐4.7% -‐5.1% -‐0.5% 3.1% 0.3% -‐7.0% -‐0.1%

Nov. -‐5.6% -‐7.6% 0.0% 3.2% 2.3% -‐8.3% 0.1%

Oct. -‐12.2% -‐10.7% -‐0.7% 3.8% -‐1.1% -‐15.1% 0.2%

Sept. -‐8.7% -‐8.1% -‐0.1% 1.1% -‐0.5% -‐9.6% 0.1%

Aug. -‐7.3% -‐9.9% 0.2% 1.6% 2.9% -‐8.7% 0.2%

Source: RetailNext

To entice shoppers back into physical stores, shopping centers and brands in the US are betting on a variety of retailtainment concepts:

• Urban Outfitters, Club Monaco and Kohl’s have all joined the trend of retailers opening coffee shops in their stores. Urban Outfitters took the concept one step further in 2015 by acquiring the Vetri Family group of restaurants, and it is reportedly now working on opening restaurants in a number of stores.

• The King of Prussia Mall in Pennsylvania is adding about 250,000 square feet of space connecting its Plaza and Court sections. Reports suggest that none of the new square footage will be devoted to traditional retail; it will all be food and experiential space.

• Apparel retailers Rebecca Minkoff and Tommy Hilfiger have provided shoppers with virtual reality (VR) headsets that allow them to experience the brands’ runway shows virtually.

What to Expect

Brands and retailers will experiment with unconventional food and beverage offerings this year. More retailers will use in-‐store technology such as VR to make the shopping experience more fun and entertaining. And we anticipate a proliferation of mobile apps that improve the in-‐store experience by giving shoppers access to customizable shopping lists, location-‐relevant promotions, and product and inventory information.

$

29

Global Retail Trends 2016

DEBORAH WEINSWIG, MANAGING DIRECTOR, FUNG GLOBAL RETAIL & TECHNOLOGY [email protected] US: 917.655.6790 HK: 852.6119.1779 CN: 86.186.1420.3016 Copyright © 2016 The Fung Group. All rights reserved.

OMNI-CHANNEL RETAIL: CHASING GROWTH TO GIVE WAY TO FINANCIAL SUSTAINABILITY Following the race to roll out omni-‐channel services, including convenient, low-‐price delivery and collection options, we expect to see more retailers address the costs of these offerings in 2016.

What It Is

As more consumers browse, compare and shop via mobile devices, the demand for omni-‐channel propositions is only increasing. At the same time, smartphones are bringing connectivity and e-‐commerce into stores and so blurring the division between offline and online even further. Retailers continue to respond to these trends with cross-‐channel propositions that include offering services at low prices or free of charge—which can threaten margins. This year, we expect to see more retailers refocus on the profitability of their omni-‐channel operations instead of chasing double-‐digit channel growth.

Why It Is a Trend

Subsidized shipping, subsidized returns and subsidized buy online, pick up in store are great for customers who are looking for convenience on the cheap. They are decidedly less positive for retailers that are trying to make money while delivering the omni-‐channel experience that customers now expect.

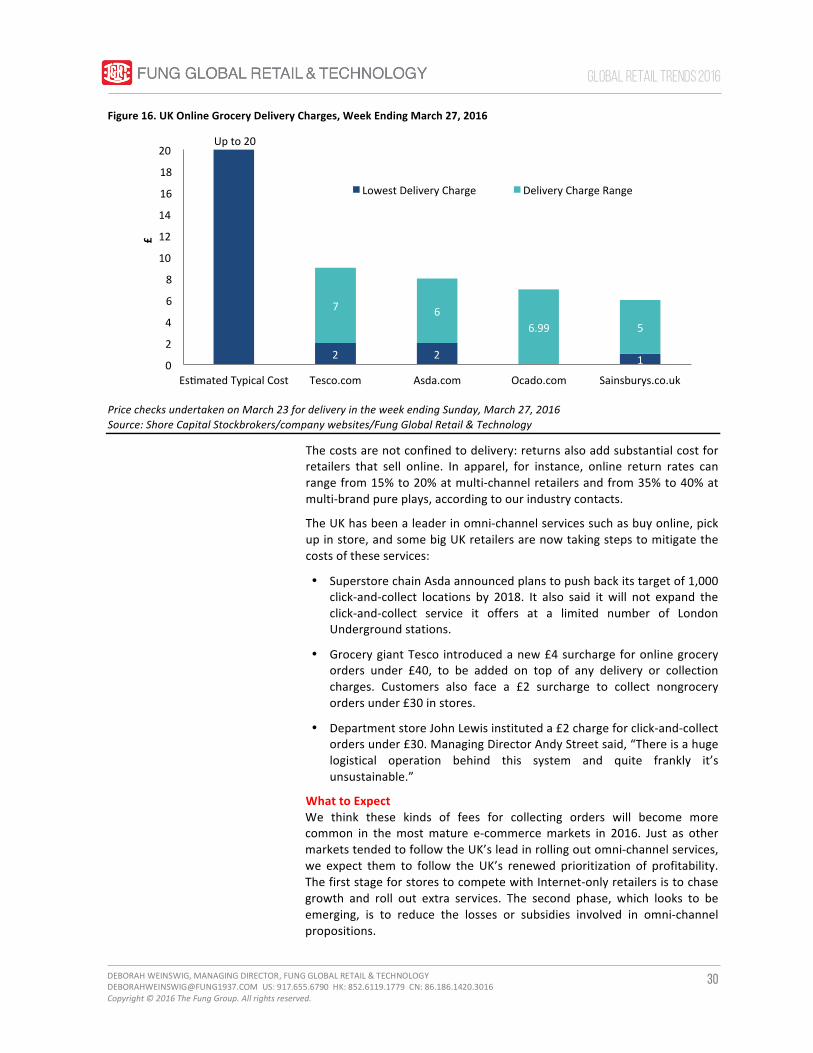

In March 2016, OC&C Strategy Consultants forecast that average retail margins in the UK could fall from their current 2.5% to just 1% due to the economics of online fulfillment. And the firm said multi-‐channel retailers will be hit the hardest, due to the costs of operating both physical stores and online fulfillment channels. OC&C said click-‐and-‐collect costs retailers, on average, four times more than in-‐store purchases, while home delivery costs retailers five to 23 times more.

In the UK online grocery sector, it costs retailers up to £20 to pick, pack and deliver an order to a customer, according to an analysis by Shore Capital Stockbrokers. Yet when we did spot checks on charges for a delivery in late March 2016, the fees levied by the major UK online grocers ranged from £0 (for selected delivery slots at Ocado.com) to a maximum of £7 (for selected slots at Tesco.com). Apart from Ocado, the lowest delivery charges we found were £1 or £2.

We expect more retailers to refocus on the profitability of their omni-‐channel operations instead of continuing to chase double-‐digit channel growth.

13

30

Global Retail Trends 2016

DEBORAH WEINSWIG, MANAGING DIRECTOR, FUNG GLOBAL RETAIL & TECHNOLOGY [email protected] US: 917.655.6790 HK: 852.6119.1779 CN: 86.186.1420.3016 Copyright © 2016 The Fung Group. All rights reserved.

Figure 16. UK Online Grocery Delivery Charges, Week Ending March 27, 2016

Price checks undertaken on March 23 for delivery in the week ending Sunday, March 27, 2016 Source: Shore Capital Stockbrokers/company websites/Fung Global Retail & Technology

The costs are not confined to delivery: returns also add substantial cost for retailers that sell online. In apparel, for instance, online return rates can range from 15% to 20% at multi-‐channel retailers and from 35% to 40% at multi-‐brand pure plays, according to our industry contacts.

The UK has been a leader in omni-‐channel services such as buy online, pick up in store, and some big UK retailers are now taking steps to mitigate the costs of these services:

• Superstore chain Asda announced plans to push back its target of 1,000 click-‐and-‐collect locations by 2018. It also said it will not expand the click-‐and-‐collect service it offers at a limited number of London Underground stations.

• Grocery giant Tesco introduced a new £4 surcharge for online grocery orders under £40, to be added on top of any delivery or collection charges. Customers also face a £2 surcharge to collect nongrocery orders under £30 in stores.

• Department store John Lewis instituted a £2 charge for click-‐and-‐collect orders under £30. Managing Director Andy Street said, “There is a huge logistical operation behind this system and quite frankly it’s unsustainable.”

What to Expect We think these kinds of fees for collecting orders will become more common in the most mature e-‐commerce markets in 2016. Just as other markets tended to follow the UK’s lead in rolling out omni-‐channel services, we expect them to follow the UK’s renewed prioritization of profitability. The first stage for stores to compete with Internet-‐only retailers is to chase growth and roll out extra services. The second phase, which looks to be emerging, is to reduce the losses or subsidies involved in omni-‐channel propositions.

Up to 20

2 2 1

7 6 6.99 5

0

2

4

6

8

10

12

14

16

18

20

Eskmated Typical Cost Tesco.com Asda.com Ocado.com Sainsburys.co.uk

£

Lowest Delivery Charge Delivery Charge Range

31

Global Retail Trends 2016

DEBORAH WEINSWIG, MANAGING DIRECTOR, FUNG GLOBAL RETAIL & TECHNOLOGY [email protected] US: 917.655.6790 HK: 852.6119.1779 CN: 86.186.1420.3016 Copyright © 2016 The Fung Group. All rights reserved.

SOCIAL SELLING: SNAP, CHAT, BUY Social media and the power of its celebrities, or “influencers,” will become increasingly important. Facebook, Twitter and Pinterest will continue to play a part, but Instagram, Snapchat and WeChat will drive innovation.

What It Is Social media will become increasingly important for retailers in two major ways: as a selling channel and as an improved marketing channel that can amplify consumer engagement and sway shoppers’ buying decisions. Many social media companies are already including “Buy” buttons in posts, allowing customers to purchase directly through their platforms. In terms of marketing, social media influencers have become the celebrities of the digital world, and companies are looking to maximize the power of these trendsetters.

Why It Is a Trend • Major developments took place in US social media in 2015, including

Pinterest’s launch of a “Buy it” button and Instagram’s expanded ad program. Twitter, Facebook and YouTube also became more commerce-‐friendly by experimenting with “Buy” buttons.

• Pinterest users can already buy directly from Macy’s, Neiman Marcus and Nordstrom, and the platform is integrated with Shopify and Demandware. Pinterest users’ average order value is $123.50, which is about 126% higher than Facebook users’ average of $54.64, according to Javelin Strategy & Research.

• Chinese messaging platform WeChat leads the way in social selling. It successfully integrates brands’ commercial accounts and digital influencers, reaching shoppers directly through an app that many of them check constantly throughout the day.

• Before Singles’ Day 2015 in China, brands and retailers engaged shoppers actively on WeChat by offering mobile reward vouchers and coupons and by launching stickers, such as the one created by key opinion leader and artist Zhang Xiaobai for The Cambridge Satchel Company. Research by InSites Consulting indicates that influencers “are over 40% more likely than average to trigger others to look up information on products/brands [and] 90%...more likely to convince others to choose a certain brand.”

• Fashion bloggers gained prominence in 2015. Bloggers such as Man Repeller and Chiara Ferragni are more influential on Twitter than Taylor Swift is, according to SocialBro, a social-‐marketing company.

• In China, brands such as Burberry, Tommy Hilfiger, Gucci and Diane von Furstenberg greatly benefit from the influence of “verified” key opinion leaders who generate content for the microblogging platform Weibo. Many of these influencers have more than 1 million followers.

Many social media companies are already including “Buy” buttons in posts.

14

32

Global Retail Trends 2016

DEBORAH WEINSWIG, MANAGING DIRECTOR, FUNG GLOBAL RETAIL & TECHNOLOGY [email protected] US: 917.655.6790 HK: 852.6119.1779 CN: 86.186.1420.3016 Copyright © 2016 The Fung Group. All rights reserved.

What to Expect “Social selling” will reach a new level of importance in 2016. The combination of instant social media buying and the rise of influencers’ marketing power will make social media an even more important channel for brands and retailers. Adding to the complexity, most of the transactions will be done on mobile platforms, similar to what is already happening with WeChat in China.

TECH INVESTMENTS: FEED THE DIGITAL SHOPPING HABIT Retailers will boost investments in technology in order to feed consumers’ appetite for researching and buying products online.

What It Is Many US retailers will increase their spending on technology in order to expand their e-‐commerce and omni-‐channel capabilities, allowing them to better provide the seamless experience consumers expect.

Improved mobile apps, faster fulfillment capability, and more secure payment systems and data are on the menu.

15

33

Global Retail Trends 2016

DEBORAH WEINSWIG, MANAGING DIRECTOR, FUNG GLOBAL RETAIL & TECHNOLOGY [email protected] US: 917.655.6790 HK: 852.6119.1779 CN: 86.186.1420.3016 Copyright © 2016 The Fung Group. All rights reserved.

Why It Is a Trend In 2015, online sales surged during the holidays. Growth in the online channel handily outpaced growth in brick-‐and-‐mortar sales, spurring many retailers to increase their investment in digital capabilities.

Figure 17. Selected Major US Retailers’ Technology Capex

Source: Company reports

• In a few highly visible incidents during the 2015 holiday season, retailers’ websites were overwhelmed by traffic and orders.

• Walmart’s strong mobile growth was driven by recent efforts to improve its app and simplify the checkout process on Walmart.com. The retailer cut its checkout load time from 7.2 seconds to 2.9 seconds, reportedly increasing conversions by 2%. Walmart also opened two automated fulfillment centers in the third quarter to scale fast delivery to customers across the US.

• Home Depot increased its online presence with initiatives such as buy online, ship to store; buy online, pick up in store; and buy online, return in store. The company is also investing in its supply chain to support online growth by completing a fulfillment center in Ohio. The center will allow Home Depot to ship parcels to 90% of US customers within two days.

• Amazon launched Amazon Underground, a new app for Android phones that includes the same functionality as the Amazon iOS mobile shopping app, plus over $10,000 worth of apps, games and in-‐app items for free. The company added Prime Now service to eight metro areas in the third quarter of 2015. Prime members can now choose from tens of thousands of daily essentials with free two-‐hour and paid one-‐hour delivery in 17 locations around the world.

• Warby Parker’s move into the offline channel has been effective. The company has seen in-‐store sales of over $3,000 per square foot. These offline sales are feeding back into its e-‐commerce growth, as over 85% of shoppers who visit a physical store later visit the company’s website.

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

$0.0

$0.5

$1.0

$1.5

$2.0

$2.5

$3.0

$3.5

CVS

Home De

pot

JCPe

nney

Kohl's

Macy's

Nordstrom

Sears

Target

TJX Co

mpanies

Walmart

Capex/Sales

USD

Bil.

2014 Tech Capex 2015 Tech Capex 2014 Capex/Sales (Right Scale)

34

Global Retail Trends 2016

DEBORAH WEINSWIG, MANAGING DIRECTOR, FUNG GLOBAL RETAIL & TECHNOLOGY [email protected] US: 917.655.6790 HK: 852.6119.1779 CN: 86.186.1420.3016 Copyright © 2016 The Fung Group. All rights reserved.

What to Expect Consumers will continue to shop online and be influenced by e-‐commerce and mobile sites. Most e-‐commerce growth will come from mobile, and consumers will research products and prices on their mobile devices, even when they are shopping in stores. Retailers will have to boost their technology investment in order to compete successfully. Relevant spending areas will likely be mobile app improvement, fulfillment capability, and payment systems and data security.

LOYALTY PROGRAMS: KEEP THEM COMING BACK Retailers will refocus on loyalty, which has become increasingly difficult to generate and maintain in the omni-‐channel world.

What It Is Generating and maintaining customer loyalty has become a bigger challenge for retailers, and shoppers expect superior customer service these days. Operating a retail business has become much more complicated, but customers are not aware of that—and they do not care about what happens on the back end. JDA’s 2015 Consumer Survey found that:

• Of the shoppers surveyed, 35% said they had experienced a negative delivery issue with an online order and that they were not likely to shop with that retailer again.

• Of the shoppers who had experienced an issue with a retailer, 51% said they would not shop with that retailer during peak holiday shopping times such as Black Friday and Cyber Monday.

In light of the more complex relationships that retailers now have with customers across multiple channels, many are focusing on improving customer loyalty by making the shopping experience more personalized via membership and loyalty programs.

Smartphone apps are set to become more prominent in loyalty programs, and many members are likely to use their smartphones in place of plastic cards.

16

35

Global Retail Trends 2016

DEBORAH WEINSWIG, MANAGING DIRECTOR, FUNG GLOBAL RETAIL & TECHNOLOGY [email protected] US: 917.655.6790 HK: 852.6119.1779 CN: 86.186.1420.3016 Copyright © 2016 The Fung Group. All rights reserved.

Why It Is a Trend

Retailers frequently use clubs, memberships and elements of gamification to help increase customer loyalty. Many retailers also work to personalize their offerings in order to strengthen their bond with individual customers. Such efforts particularly resonate with millennials, who tend to view themselves as unique individuals and demand that the products and services they receive be customized to their wants and needs.

Currently, only 37% of retailers use internal and external data to gain insights on their customers, according to SAP. According to Accenture, nearly 60% of customers want real-‐time promotions and offers, yet only 20% want retailers to know their current location.

Major retailers are responding to these trends:

• During its Investor Day on December 17, CVS announced that one of its five strategic themes for 2016 was customer-‐driven personalization.

• In 2014, Walmart launched Savings Catcher and the Savings Catcher app. The loyalty program allows members to automatically receive the difference in price on a product if the member finds it cheaper elsewhere.

In Europe, grocery stores and drugstores have been among the leaders in loyalty programs. Now, major clothing retailers are also offering them:

• In October 2015, Marks & Spencer launched its members club, Sparks, with over 2 million cardholders in the UK.

• In February 2016, British pure play ASOS launched its A-‐List rewards program.

What to Expect More retailers will work toward providing personalized experiences for customers at all discovery, consideration and purchase touch points this year. Currently, however, the physical store is typically a black hole in terms of customer data: physical retailers have little or no data of the type they can garner online—such as shopper consideration, conversion and preference data.

Retailers will close the data gap between their in-‐store and online channels—and so achieve greater personalization—by investing in new or improved loyalty and membership programs and by implementing in-‐store and e-‐commerce data analytics technologies.