Embed Size (px)

Citation preview

Global Payment Integration: Success Stories in Optimization

Rene Pelegero

President

Retail Payments Global Consulting Group LLC

Steve Bernstein

Executive Director

J.P. Morgan

Colleen Anderson Ramsay

Manager, Treasury

Amazon, Inc.

1

Agenda

Page

1 Day In The Life of a Treasurer 2

2 Global Treasury Evolution 3

3 Global Payment Types, Integration, and Adoption 20

4 Global Payments Progression and Integration with Blockchain 33

5 Key Takeaways 37

6:00PM

Leaving to go home, Sam is comfortable knowing the Treasury AI will be initiating

payments, executing hedges, making investments, moving intercompany- funds,

24/7/365 given the always-on nature of the banking system in 2025.

A POSSIBLE DAY IN THE LIFE OF SAM

4:30PM

Sam’s last meeting for the day is with Jordan, the Head of Treasury Operations.

Sam & Jordan discuss how the firm’s Treasury AI is performing, risk levels and

opportunities to tweak the algorithms to maximize efficiency & returns.

3:00PM

Risk management is a key part of Sam’s role. Being part of a treasury fraud

prevention community, Sam has access to a network of treasures and experts that

share emerging threats against their organizations plus a suite of advanced self-

service fraud tools.

2:00PM

Sam’s treasury team is globally dispersed, comprised of 5 FTE + 7 on-demand

experts, and the longest serving team member has only been at the firm for 4 years.

However, using their treasury collaboration cloud, they are able to seamlessly

operate as if working side-by-side.

1:30PM

Sam meets with the company’s innovation team to discuss how quantum

computing could be used in treasury, the two teams are planning to start a

pilot starting next week.

1:00PM

Throughout the day, jumping meeting to meeting, Sam is able to easily

approve large payments on a treasury mobile app via seamless biometric

authentication.

12:00PM

Sam meets with the CEO & CFO to discuss a new acquisition the firm is

considering. Sam brings recommendations on how to free up capital to fund the

acquisition as well as powerful insights into the cash flow, working capital, risk

and supply chain synergies of the acquisition target.

10:30AM

Sam meets with a LOB or Regional CEO to discuss expansion into a new

geography. Acore part of the expansion team, Sam is armed with powerful

insights leveraging the firm’s own data, bank partner data and third party data.

8:00AM

Taking an autonomous car to work, Sam accesses a treasury dashboard

on the in-car tablet. The customized dashboard gives Sam a dynamic,

real-time, multi-bank snapshot of all the key treasury KPIs as well as

curated newsfeed specific to Sam’s industry, firm and role.

6:30AM

Starting at home, an Alexa alerts Sam to any treasury anomalies

requiring immediate attention. Treasury AI has already conducted

complex scenario analysis to quantify the financial impact of these

outliers and developed a recommended ‘best action’ plan.

2

Agenda

Page

1 Day In The Life of a Treasurer 2

2 Global Treasury Evolution 3

3 Global Payment Types, Integration, and Adoption 20

4 Global Payments Progression and Integration with Blockchain 33

5 Key Takeaways 37

Colleen Anderson Ramsay

3

Payment Modalities

4

Payment Standards

Bank Transfers OBePs Cards Paper

ANSI X.12

Edifact

ISO 20022

Screen

Scraping

Mashups

ISO 8583

Standard?

What’s a

standard?

5

Many Payment Schemes Globally

Source: Adyen N.V6

Global Card Payment Issues

Approval/Decline Ratios– Increased decline rates for remote transactions

– Issuers in some countries issue cards branded as Visa and Mastercard for domestic use only

– Inconsistent implementation of Visa/Mastercard rules (i.e. $1 authorization vs. card

verification)

– Outages and Do Not Honor and Insufficient Funds

Money Movement– Funds repatriation can be difficult

– FX spread is not known

– Cost of payments

Regulatory and Compliance– Implementation of local or regional regulations (e.g. GDPR, SCA)

– Ongoing change introduced by card schemes (e.g. authorization prior to issuing a reffund)

7

Optimize Card Payments Globally

Global• Simpler, less expensive

• Low market penetration and approval rates

Regional• Expensive but increases market reach with

lower risk

• Approach might not be available in every Region

Local• Most expensive, FX

implications

• Highest penetration and approval rates

8

Card Optimization Strategic Trade Offs

Addressable

market

Payment

Instruments

Implementation

costs

Local Legal

Entities and

bank accounts

Local

Payment

Know-how

Payment

Processing

Costs

9

Cross Border Acquiring Regulations

Licenses– Acquirers can acquire transactions only in countries where Visa and Mastercard have granted them licenses

– Acquirers can only enter into acquiring agreements with legal entities that reside in the same country as the

acquirer is licensed

Physical Presence– Merchants must have a physical presence with “employees or agents conduct[ing] business activity directly

related to providing the cardholder with the goods or services purchased in the specific transaction”.* In other

words, having an attorney’s office as the legal presence in a country is not sufficient

Settlement– Although many large trans-national acquirers can accept and process transactions in many currencies, they are

generally limited to the number of currencies in which they can settle

– Acquirers will only deposit funds from payment transactions into bank accounts that belong to the legal entity

with whom they have an agreement

– Unless otherwise agreed with acquirer, acquirer will automatically convert from transaction currency (Ct) to

settlement currency (Cs) at a FX rate and uplift only known to the acquire

10

Other Cross Border Regulations

–GDPR and California Privacy Law

–PSD2 and Strong Customer

Authentication

11

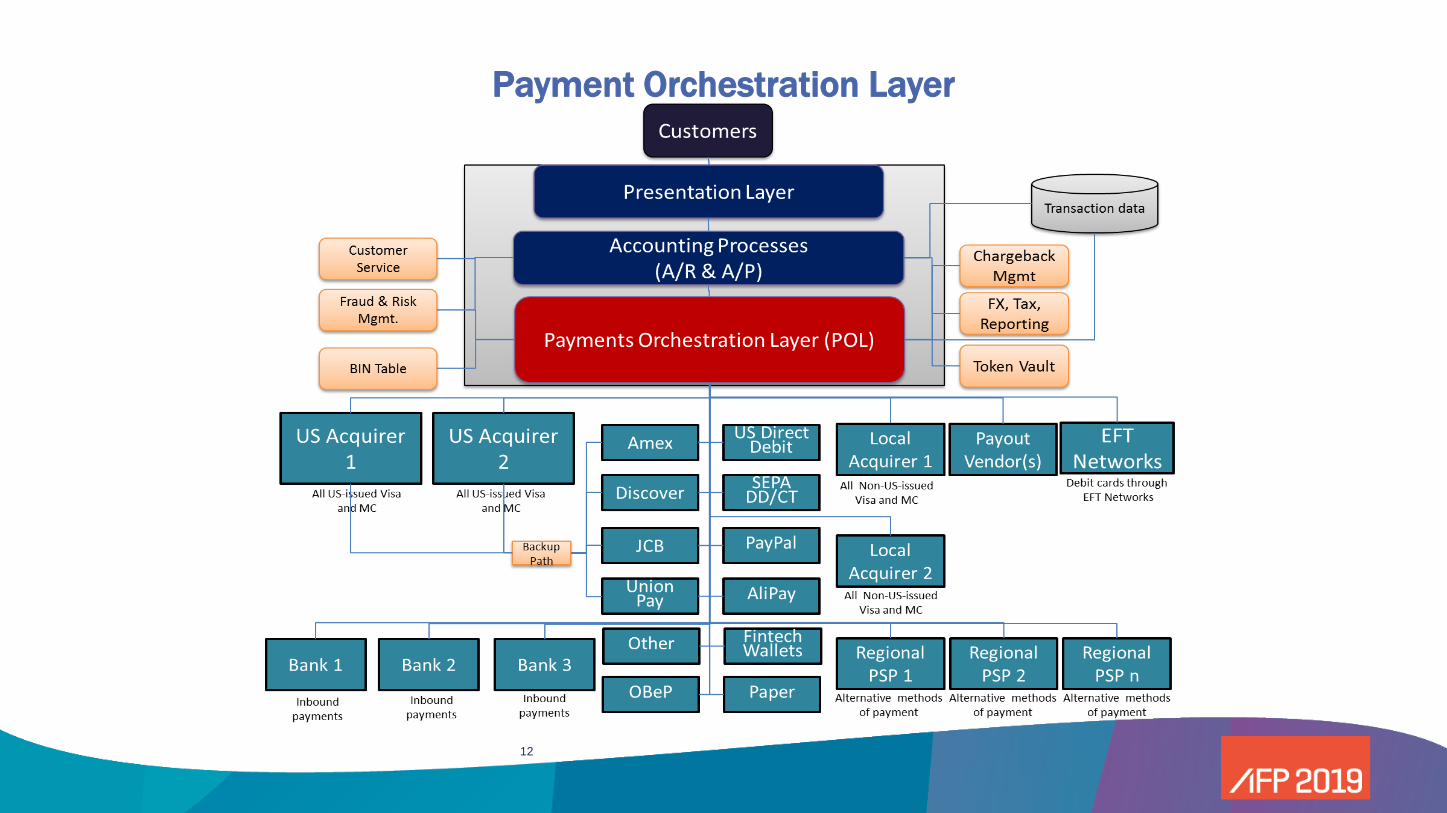

Payment Orchestration Layer

12

Payment Orchestration Layer

13

Global Card Payments – Best Practices

Approval/Decline Ratios– Multiple acquirer strategies for key markets

– Retry declined transaction logic

– Smart authorization and orchestration panels

– Machine learning and artificial intelligence

– Engage with issuers

Money Movement– Establish local legal entities if economically feasible

– Accept local currency and manage own FX

– Net expenses from payment proceeds to avoid double FX

Regulatory and Compliance– Global implementation of selected regulations (even if not required to do so)

– Outsource orchestration and compliance to third parties

14

Conclusions

Global Payments Integration can be challenging

– Regulations, customary practices, economics

– Transaction flows, technologies, multiple vendors

– Global payments cannot be ignored

Take a long term view

– Develop road map (i.e. countries and methods of payment)

– Stay abreast of market developments (e.g. new methods of payment, new vendors)

Manage Payments as a Business

– Actively manage payment vendors

– Monitor, measure, analyze, test, implement

15

Global trade growth

EM capital flows

FX & interest rate volatility

Cybersecurity threats

Treasury Objectives

The treasury eco-system is experiencing significant change brought about by new emerging technologies, regulatory

developments, economic events and market changes yet the key objectives of the Treasurer remain the same

And more is expected from

treasurers with limited

resources…

Yet the treasurer’s objectives

remain the same.

The Treasury universe is

constantly changing…

Blockchain

Analytics

Machine learning

Robotics

Real-time payments

ERP Adapters

Brexit

U.S. tax reform

North Korea

SEPA

KYC

BEPS

FX regulations

Basel III

Window guidance

Tre

asu

ry F

un

cti

on

Time

Increasing

demands

on treasury

Treasury

Resourcing

Optimize

Capital

Mitigate

Risks Sh

are

ho

lder

Valu

e

Operational

Efficiency

16

THE CORPORATE TREASURY

OF 2025 WILL LOOK

NOTABLY DIFFERENT

‘MORNING TREASURY’

TASKS AUTOMATED

STRATEGIC ADVISOR

TO BUSINESSES

LEVERAGING DATA

BROADER RISK

MANAGEMENT

PERSPECTIVE

NEW INTERNAL &

EXTERNAL PARTNERS

PRO-ACTIVE,

INNOVATIVE MINDSET

INCREASED COMPLEXITY

& SCALABILITY

CONVERSATIONAL

EXPERIENCES

REAL-TIME 24/7/365

OPERATIONS

NEW TEAM

DYNAMICNEW WORKING CAPITAL

PARADIGM

SOURCE: 1. McKinsey; 2. BCG

~80% of treasury tasks can be

automated to some extent1

The number of critical business risks

that treasurers manage has more

than doubled since 20162

Corporate Treasury in 2025

17

CHANGING WORKFORCEMillennials will make up 75% of the workforce by 2030

BANKING DIGITIZATION

& DISRUPTION80% of traditional financial services firms will go out of

business by 20305

MACRO GLOBAL

SHIFTS“Vast majority of CEOs believe that economic and financial

volatility will increase over the next 12 months”6

OPPORTUNITIES OF

EMERGING TECHNOLOGY>130Bn connected devices by 20307

AI will increase labor productivity by 40% through 20358

INCREASING PACE

OF CHANGELandline telephone took 75yrs to hit 50M users, electricity took

46yrs, Twitter took less than 2yrs, Angry Birds took 35 days1

INDUSTRY DIGITIZATION

& DISRUPTIONDigitization will have a $100Tr impact through 2025

2

CHANGING TREASURY

EXPECTATIONS80% of treasurers agree treasury will be playing a more

strategic role 3yrs from now3

01 05

02 06

03 07

SOURCE 1. Wall Street Journal; 2. World Economic Forum; 3. Marsh & McLennan; 4. Forbes; 5. Gartner ; 6. A.T. Kearney Global Business Policy Council; 7. HIS Markit ; 8. Accenture

404

KEY FORCES THAT MAY DRIVE A SIZABLE SHIFT IN

CORPORATE TREASURY OVER THE NEXT 7 YEARS

18

Payments analytics

of thefuture

Personalized Customer Engagement: Contactless

mobile wallets and data partnerships with merchants

lead to contextualized offers based on “asking the

right question”

Real-Time Transaction Flow:

Real-time transaction graph analysis provides

insights for merchants to manage cashflow,

inventory, and service levels

Digital Onboarding:

Use digital onboarding to collect KYC data,

automate account opening forms, and

identify customer needs promptly

Leverage Compliance Investments:

Consumer Financial Protection

Bureau(CFPB) compliance and

KYC/AML investments lead to better

“voice of customer” measurement and

customer experience

Robotics & Process Automation:

Automate transactional testing,

fulfillment, and dispute management to

reduce manual work

Preferred Payments:

A single card becomes “top of wallet,” so

include this in behavioral segmentation to

target the “moments that matter ’”

Real-Time Fraud Analytics:

Issuers use scalable machine learning

platforms to generate fraud alerts and

mitigate cyber risk

Treasury focusing on and responding to the payments trends

Analytics allow the payments ecosystem to respond to change

Source: Deloitte December 2018 – The Financial Brand

Faster Payments:

Innovation produces faster rails, international

transfer, and B2B solutions to enable cheaper

payments and reduce reliance on cash

19

Agenda

Page

1 Day In The Life of a Treasurer 2

2 Global Treasury Evolution 3

3 Global Payment Types, Integration, and Adoption 20

4 Global Payments Progression and Integration with Blockchain 33

5 Key Takeaways 37

Improve cross-border payment efficiency by leveraging new technologies

Leveraging new technologies will help Treasury achieve its operational and strategic objectives as well as be able to successfully

operate the Treasury department of tomorrow

63%are leveraging robotics process

automation to drive the shift

from transactional to value

adding activities

2018 / 2019 Industry Survey

69%highlighted leveraging smart

technology to drive further

efficiencies as a key objective

over the next 5 years

82%already have or setting up a data

analytics function and / or

upskilling staff in data analytics

Finance and Treasury

Cloud based ERP and Treasury Management Systems

Use Cases of New Technologies within Finance and Treasury

Front Office

Middle Office

Back Office/SSCE

XA

MP

LE

S O

F U

SE

C

AS

ES

Machine Learning RPA APIs Data Analytics

Cash forecasting FX exposures

RPAAPIs Block-chain

Machine Learning RPA Data Analytics

FX execution

Interco netting

Treasury accountingSWIFT GPI

FX confirmation

KYC, trade finance,

payments

Fraud / error detection Payment, collection

trends

Reconciliations, data

retrieval, reporting

Source: PwC 2018 Global State of Information Security Survey

20

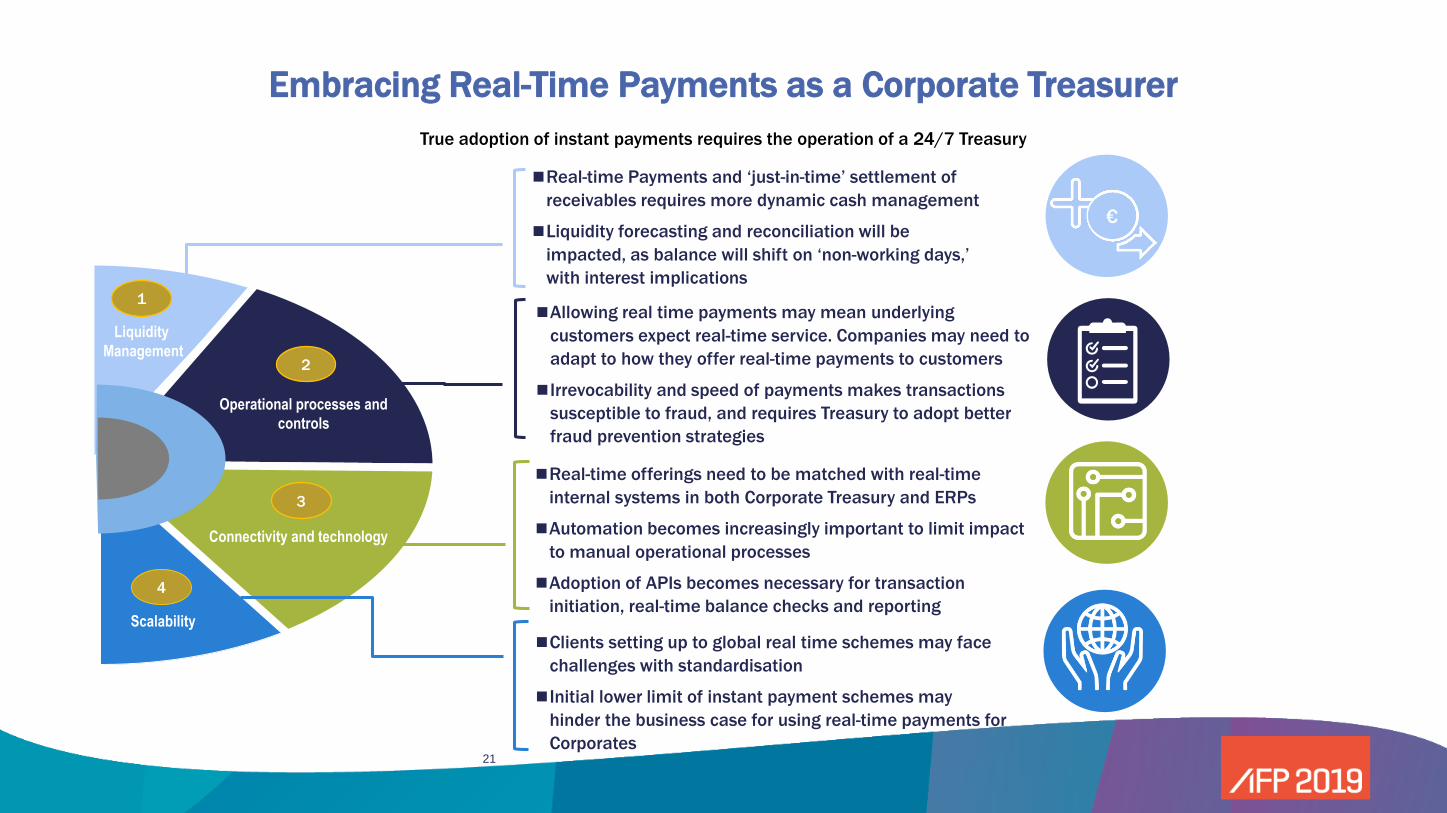

Liquidity

Management

Operational processes and

controls

Connectivity and technology

Scalability

1

2

3

4

Embracing Real-Time Payments as a Corporate Treasurer

True adoption of instant payments requires the operation of a 24/7 Treasury

◼Real-time Payments and ‘just-in-time’ settlement of

receivables requires more dynamic cash management

◼Liquidity forecasting and reconciliation will be

impacted, as balance will shift on ‘non-working days,’

with interest implications

◼Real-time offerings need to be matched with real-time

internal systems in both Corporate Treasury and ERPs

◼Automation becomes increasingly important to limit impact

to manual operational processes

◼Adoption of APIs becomes necessary for transaction

initiation, real-time balance checks and reporting

◼Allowing real time payments may mean underlying

customers expect real-time service. Companies may need to

adapt to how they offer real-time payments to customers

◼Irrevocability and speed of payments makes transactions

susceptible to fraud, and requires Treasury to adopt better

fraud prevention strategies

◼Clients setting up to global real time schemes may face

challenges with standardisation

◼Initial lower limit of instant payment schemes may

hinder the business case for using real-time payments for

Corporates

€

21

What is ISO 20022 and why is it used as a global standard?

Global and open financial messaging standard, ISO 20022 has evolved into the industry’s preferred standard for global payments.

The ISO 200222 adoption is increasing globally, allowing for ubiquity and optimized real time cross-border payments.

ISO 20022 is a Universal

Financial Industry

Message Scheme based

on XML (eXtensible Mark-

up Language)

ISO 20022 with Common

Global Implementation

(CGI) has become the

format of choice for

consistent messaging

across multiple banks and

countries

27

Format Extended Field

length

Transaction

Batching

Interoperable

Messaging

Global

applicability

Language / Multi-

byte Characters

Simple Bank

Integration

ANSI X12 ✓

SWIFT FIN ✓

EDIFACT ✓ ✓

Global Flat File ✓ ✓

ISO20022 ✓ ✓ ✓ ✓ ✓ ✓

Flexible in structure and

language to operate with

the latest and emerging

technologies

22

Real Time Payments landscape and expansion of the ISO20022 standard.

23

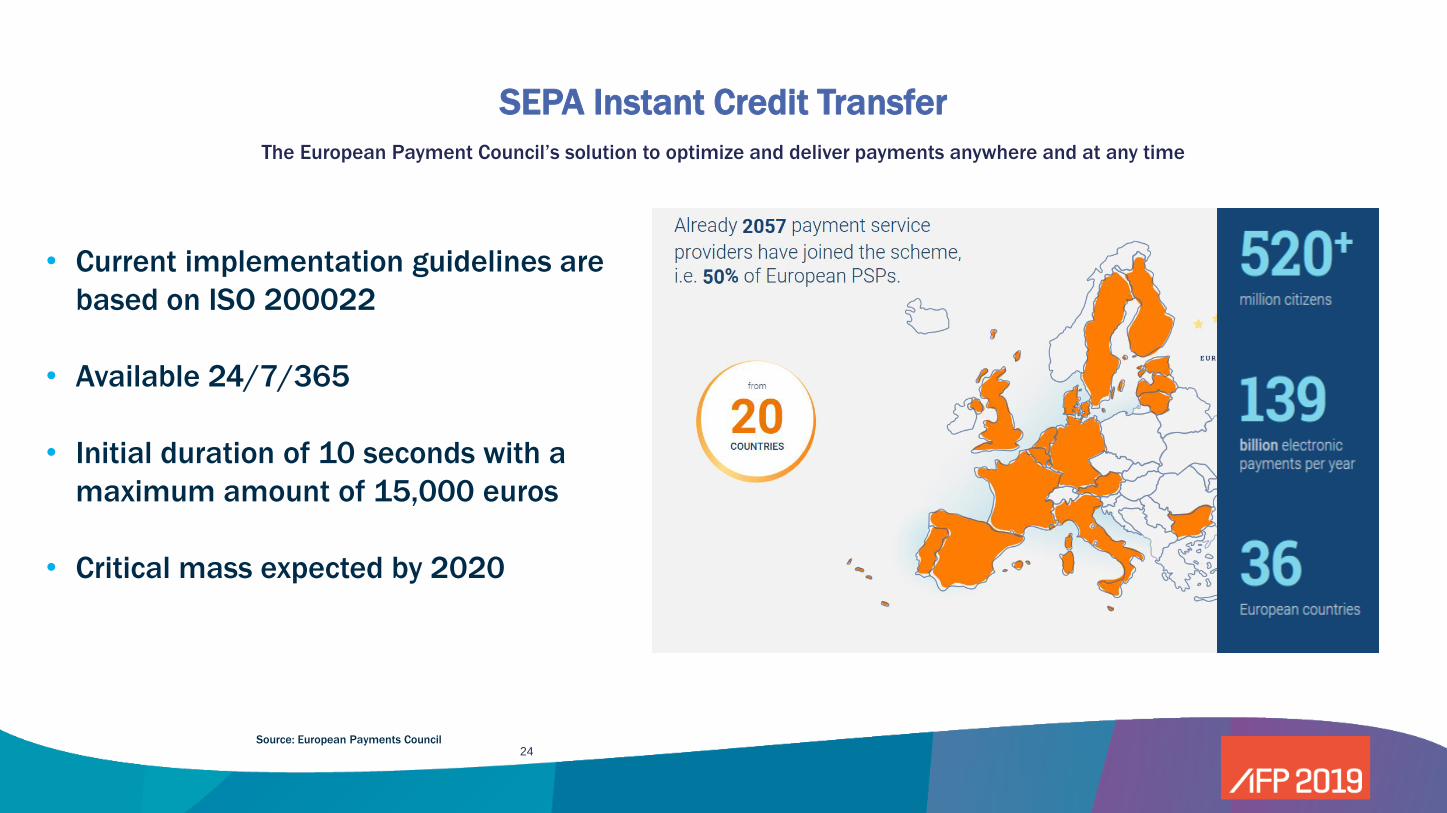

SEPA Instant Credit Transfer

The European Payment Council’s solution to optimize and deliver payments anywhere and at any time

• Current implementation guidelines are

based on ISO 200022

• Available 24/7/365

• Initial duration of 10 seconds with a

maximum amount of 15,000 euros

• Critical mass expected by 2020

Source: European Payments Council24

APAC Real Time Payments Real time payment capabilities progressively expand across APAC

25

Real-Time cross border payments in APAC

• NPP API framework is aligned to ISO 20022 standards

• This will allow faster P2P remittances and trade settlement

• Working with banks in Australia, China, Thailand, and Singapore, the

Swift GPI pilot successfully executed cross-border payments in 2018.

• NPP launched PayID to link financial accounts to mobile numbers, email

addresses, and ABN for businesses.

• Launched Payment Control Service (PCS) to block payments with

irregularities during the transaction.

• Adoption of SWIFT GPI in India increased to 11 banks including India’s

largest lender, State Bank of India.

• India- The unified Payment Interface (UPI) is a real time payments and

tokenization scheme that enables collections from 60 banks. Volumes

and values are growing exponentially and a number of fintech players are

building new services on top of the platform.

• Source: https://www.moneycontrol.com/news/business/companies/11-indian-banks-to-go-live-on-swift-gpi-for-cross-

border-payments-3621701.html

• Source: https://www.computerworld.com.au/mediareleases/33118/instant-cross-border-swift-gpi-payments-test-a/

• https://www.citibank.com/tts/sa/flippingbook/2017/The-Request-to-Pay-

Revolution/files/assets/common/downloads/The20Request20to20Pay20Revolution.pdf

26

SWIFT Global Payments Innovation (GPI)

Dramatically improves cross-border payments across the correspondent banking network and is built on the ISO20022 standard

• SWIFT gpi is an initiative meant to dramatically

improve the customer experience by increasing the

speed, transparency and end-to-end tracking of

cross-border payments.

• In parallel, SWIFT gpi is exploring the use of open

APIs and blockchain technologies to build additional

value into the cross-border payment process

gpi Bank

sending

institution

Payment

originator

Unique

Transaction

Identifier

gpi Bank

receiving

institution

Payment

beneficiary

Payment flowPayment status and

confirmations

What is SWIFT global payment innovation (gpi)

Source: https://www.treasury-management.com/news/1176/swift-gpi-reaches-2440-trillion-milestone-at-two-year-anniversary.html

2018-2019 Swift Updates

• More than $40 trillion transferred in 2018

• YOY increase of 270%

• More than 3,500 banks committed to adopting gpi.

• GPI carries over $300 billion a day in 148

currencies, and 1,100 country corridors on average.

• 40% of SWIFT gpi payments are credited within 24

hours.

27

SWIFT Global Payments Innovation (GPI)

28

PSD2 Open Banking – XS2A (Access to account in EMEA)

◼ XS2A concept provides the ability for regulated Third Party

Providers (TPPs) to offer services to account holders for

accessing account information and initiating payments

from their bank account

◼ AISP – Account Information Service Provider

◼ PISP – Payment Initiation Service Provider

◼ Regulatory Technical Standards (RTS) are being developed

by the EBA, which will cover the communication standards

for AISP and PISP to interact with banks and PSPs

◼ The connection between AISP/PISP and banks is likely to

be enabled using Application Programming Interface

(APIs) which enable companies to connect directly to

financial institutions

Bank

(TPP)PSU Bank

Access Data

PISP

PSD2 allows regulated third-party PISPs to initiate

payments directly from customer payment accounts so

long as they have the customer’s consent.

AISP

Regulated third-party AISPs can access customer data (with

the customer’s consent) to provide an overview of a

customer’s payment accounts (balances and transactions)

with different banks in one place Bank

(TPP)

PSU Banks

Access Data

Overview: Access to Account (XS2A) Bank acting as a PISP

Bank acting as a AISP

Bank

Client

Bank

Client

29

Global Digital Payment Adoption

Digital payments via eWallets and Cards continue to grow globally while cash payment declines.

Source: https://www.paymentscardsandmobile.com/wp-content/uploads/2018/11/Global-Payments-Report_Digital-2018.pdf

30

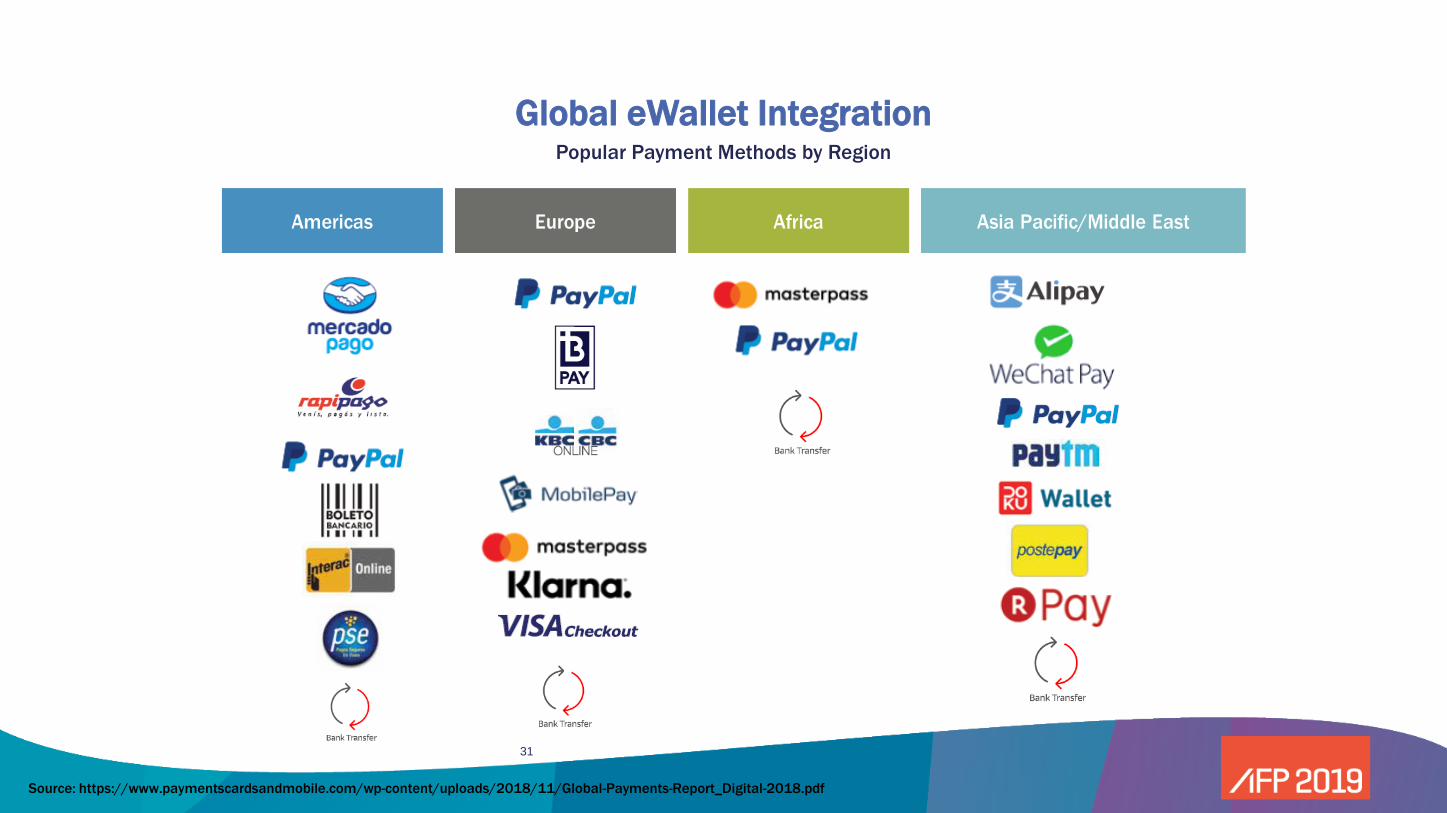

Global eWallet IntegrationPopular Payment Methods by Region

Source: https://www.paymentscardsandmobile.com/wp-content/uploads/2018/11/Global-Payments-Report_Digital-2018.pdf

31

Global FX Payments

Global cross-border cross currency mass payments capabilities

are being built out using local low-value clearing systems,

providing the ability to convert funding currency into payment

currencies. This reduces the need to hold local currency accounts.

How it Works?

◼ You would send one consolidated payment file via banking channels for

all of your payments from a centralized account

◼ For cross-border payments that require conversion to another currency,

FX rate and spread could be applied and converted payments would be

routed to payees around the world through local ACH (low-value) clearing

systems

◼ Payees receive payment in full (i.e. principal protection)

Global FX Payments Allow for:

◼Payroll/pension payments

◼Relocation payments

◼ Intercompany payments

◼ Interest/dividend payments

◼Consumer rebates

◼Vendor payments

◼E-Commerce merchant payments

◼ Tax payments

Current capability Q1 2019 capability

47 currencies 90+ countries 58 currencies 100+ countries

32

Agenda

Page

1 Day In The Life of a Treasurer 2

2 Global Treasury Evolution 3

3 Global Payment Types, Integration, and Adoption 20

4 Global Payments Progression and Integration with Blockchain 33

5 Key Takeaways 37

Size of Global Blockchain Market

Source: Statista.com34

How Blockchain can improve global payments

Source: https://gomedici.com/overview-of-the-payments-industry/

• Through smart contracts,

foreign exchange can be

sourced from participants

willing to facilitate the

conversion of fiat currencies

• Enable international

regulators to monitor

transactions in real-time and

enforce AML Policies.

• Allows transfer of funds with

minimal fees and efficient

delivery without need of

correspondent banks

35

Data remittance

◼ Beneficiary bank receives requests, accesses bank’s encrypted

data and responds to inquiry e.g., name, DOB, etc.

Interbank Information Network (IIN): Transforming cross-border payments

Runs on Quorum, ®, a permissioned-variant of the Ethereum blockchain

Creating a secure, decentralized, permission-based network to securely

exchange information associated with cross-border payments may help

enable banks to address today’s key pain points, costs and risks by:

◼ Reducing payment delays and touch points

◼ Facilitating faster and comprehensive payment tracking

◼ Providing real-time sanctions, AML and fraud management tools

◼ Maintaining personal information (PI) within a secure network provisioned

for validated payments

Fraud

Fraudster Lists

Account

Validation

Anti-Money

Laundering

Inquiries

Risk Rating

Sanctions

Customer

Information

FATF

Account/Name/

Address

Enrichment

Tracking

Payment Status

Inquiry Status

Data request

◼ Remitter bank or correspondent bank is hit with a compliance

inquiry.

◼ Remitter bank or correspondent bank receives information and

makes determination to proceed, further investigate or hold.

Compliance process with a global network

Remitter BeneficiaryRemitter bankBeneficiary

bank

Compliance

Inquiry!

Global

Network

Avg time: <1 hour1

41

2 2

3

1

4

Data exchange

◼ Remitter bank requests data from beneficiary bank. Network

validates requests per agreed terms and maintains encrypted,

time stamped records for all permissioned parties.

2

3

36

Agenda

Page

1 Day In The Life of a Treasurer 2

2 Global Treasury Evolution 3

3 Global Payment Types, Integration, and Adoption 20

4 Global Payments Progression and Integration with Blockchain 33

5 Key Takeaways 37

Key Takeaways

•Gain insight as to what impact regulatory changes are having on

Treasury practices

•Understanding of how practitioners are leveraging Global Payment

types for integrated reconciliation

•Gain insight in best practices Treasury practitioners are adopting

based upon New Payment and format types for future consideration

37

Global Payment Integration: Success Stories in Optimization

Rene Pelegero

President

Retail Payments Global Consulting Group LLC

Steve Bernstein

Executive Director

J.P. Morgan

Colleen Anderson Ramsay

Manager, Treasury

Amazon, Inc.

38